Dynamic Bivariate Normal Copula

Abstract Normal copula with a correlation coefficient between and is tail independent and so it severely underestimates extreme probabilities. By letting the correlation coefficient in a normal copula depend on the sample size, Hüsler and Reiss (1989) showed that the tail can become asymptotically dependent. In this paper, we extend this result by deriving the limit of the normalized maximum of independent observations, where the -th observation follows from a normal copula with its correlation coefficient being either a parametric or a nonparametric function of . Furthermore, both parametric and nonparametric inference for this unknown function are studied, which can be employed to test the condition in Hüsler and Reiss (1989). A simulation study and real data analysis are presented too.

Key words Estimation; normal copula; tail dependence/independence.

AMS 2000 subject classification Primary 62F12, 62G30; Secondary 660G70, 62G32.

1 Introduction

Let be independent and identically distributed random vectors with distribution function , continuous marginals and . The copula of is defined as , where denotes the inverse function of . Assume the copula of follows from a normal copula , where is unknown. Hence the density of is

| (1.1) |

for , where is the standard normal distribution function.

Normal copulas are one of most commonly used elliptical copulas, and elliptical copulas are popular in risk management due to their ease of simulation (see McNeil, Frey and Embrechts (2005)). Recently Channouf and L’Ecuyer (2012) used normal copulas to model arrive processes in a call center, Fung and Seneta (2011) showed that a bivariate normal copula is regularly varying, Meyer (2013) studied the properties of a bivariate normal copula, efficient estimation for bivariate normal copula models was studied by Klaassen and Wellner (1997). Although normal copulas are easy to use and have some attractive properties, a serious drawback of using a normal copula is the so-called tail asymptotic independence (see Sibuya (1960)), which under-estimates extreme probabilities in risk management.

To overcome the shortcoming of the tail asymptotic independence of a normal copula, Frick and Reiss (2013) assumed that satisfies the so-called Hüsler-Reiss condition

| (1.2) |

(cf. Hüsler and Reiss (1989)) and proved that

| (1.3) |

for and as . This is the copula version of the limit in Hüsler and Reiss (1989) for the normalized maxima of independent random vectors with a bivariate normal distribution and its correlation coefficient satisfying (1.2). Obviously, a bivariate random vector with the above limiting distribution is dependent when . Extending the results in Hüsler and Reiss (1989) to elliptical triangular arrays is given in Hashorva (2005, 2006).

Since the above depends on the sample size , one may call it dynamic normal copula. Recently dynamic copulas are receiving some attention in modeling financial time series; see Benth and Kettler (2011), Mendes and de Melo (2010), Guégan and Zhang (2010), and Van den Goorbergh, Genest and Werker (2005).

In this paper, we further study the convergence in (1.3) by allowing to depend on both and . That is, we do not assume that are identically distributed. Motivated by (1.2), an obvious extension is to assume that is a function of and . As in nonparametric regression models, we assume that is a smoothing nonparametric or parametric function of so that we can employ well-developed local polynomial techniques to estimate this function and to test whether this function is a constant, which gives a way to verify the condition imposed by Hüsler and Reiss (1989) and Frick and Reiss (2013), and indicates the observations have the same distribution. More specifically we assume that is a sequence of independent random vectors and the copula of is a normal copula with correlation coefficient for an unknown smooth function . After deriving the convergence for the normalized maxima of the copulas of , we propose both parametric and nonparametric estimation for , which are based on either Kendall’s tau or correlation coefficient. We also derive the asymptotic limits of the proposed estimators, which turn out to be quite nonstandard with an unusual rate of convergence. The proposed estimators can be used to determine tail dependence, which is of importance in predicting co-movement in financial markets; see McNeil, Frey and Embrechts (2005).

We organize this paper as follows. Section 2 presents the main results and statistical inference procedures. A simulation study is given in Section 3. Section 4 reports some empirical data analyses. All the proofs are given in Section 5.

2 Methodology

Throughout, suppose are independent random vectors, have the same continuous distribution function and have the same continuous distribution function . Assume the copula of is the normal copula with density given by (1.1).

2.1 Convergence of maxima and tail coefficient

As motivated in the introduction, we extend the result (1.3) by assuming

| (2.1) |

which includes condition (1.2) as a special case.

Theorem 1.

Under condition (2.1),

-

i)

if , then for any and

-

ii)

if , then for any and

-

iii)

if is a continuous positive function on , then for any and

Furthermore the tail dependence function equals

for and , and the tail coefficient is

2.2 Parametric inference

Here we consider statistical inference for fitting a parametric form to the unknown function . First, we consider the family , where Note that when , can not be identified. Also when , and can not be distinguished.

It follows from Theorem 5.36 of McNeil, Frey and Embrechts (2005) that

| (2.2) |

where is an independent copy of , and

| (2.3) |

Also we have

| (2.4) |

Therefore, one can employ the standard least squares estimate based on one of the above equations.

Since are not identically distributed, we do not have an independent copy of , which prevents us from using (2.2). Hence we propose to use either (2.3) or (2.4) to construct the least squares estimator, which results in

or

where and . Alternatively we define to be the solution to the following score equations

| (2.5) |

and to be the solution to the following score equations

| (2.6) |

Note that we skip the term of in (2.5), which goes to a constant uniformly in since uniformly in .

The following theorems give the asymptotic normality of the proposed estimators.

Theorem 2.

Theorem 3.

Remark 1.

Since and , and have a smaller asymptotic variance than and , respectively, while the comparison for the asymptotic variances of and is unclear since both and converge in distribution to zero. On the other hand, if one is interested in estimating , then the estimator for the first element based on has a faster rate of convergence than the corresponding estimator based on , but the estimators for the second and third elements based on have a larger asymptotic variance than those based on . In spite of these theoretical comparisons, the simulation study below does prefer the estimation procedure based on equation (2.3) when the mean squared error is concerned. For testing , one should employ the well-known Hotelling test statistic based on either (2.7) or (2.9) because the limit in both (2.8) and (2.10) is degenerate.

Another interesting parametric form for is polynomial. Here we consider . In this case, when , becomes constant, which means that the observations are independent and identically distributed random vectors.

Theorem 4.

Theorem 5.

Remark 2.

When (2.1) holds with , we can show the rate of convergence for is faster than the rate of convergence for . That is, the estimator based on (2.4) is preferred to that based on (2.3). However, the simulation study below prefers the estimation procedure based on equation (2.3) when the mean squared error is used as a criterion.

2.3 Nonparametric inference

First we use (2.3) to estimate the smooth function nonparametrically. Especially we consider the local linear estimator defined as

where is a kernel function and is a bandwidth. That is,

where , . We refer to Fan and Gijbels [3] for details. Therefore we can estimate non parametrically by

Theorem 6.

Assume is symmetric with support . For a given , assume is continuous at , and as . Then as we have

Second we use (2.4) to estimate the smooth function nonparametrically by considering the local linear estimator

i.e.,

Theorem 7.

Assume is symmetric with support . For a given , assume is continuous at , and as . Then as we have

Remark 3.

Remark 4.

By minimizing the asymptotic mean squared error, the optimal choices of for and are

and

respectively, which are different from the standard optimal order in the bandwidth choice of nonparametric regression estimation and nonparametric density estimation. Data driven method for choosing the above and can be obtained via estimating . A future research is to investigate the possibility of using cross-validation method to choose the optimal bandwidth.

3 Simulation

In this section we examine the finite sample performance of the proposed estimators by drawing independent with following the normal copula with correlation coefficient . We consider or or , and repeat times.

First we consider with or , and calculate the average, sample variance and mean squared error for both and . Table 1 below shows that has a smaller variance than , which confirms the argument mentioned in Remark 2 that estimator has a faster rate of convergence than . We also observe from Table 1 that i) has a larger bias and a larger mean squared error than except the case of and ; ii) the variance and mean squared error of both and become larger when increases; iii) the accuracy for both estimators improves as becomes larger. In conclusion, has an overall better finite sample behavior in terms of mean squared error than although its asymptotic variance is larger theoretically and empirically.

| 1.0365 | 9.9660 | 1.0145 | 9.9836 | 1.0065 | 9.9976 | |

| 0.0144 | 0.0249 | 0.0045 | 0.0384 | 0.0016 | 0.0218 | |

| 0.0157 | 0.0203 | 0.0047 | 0.0387 | 0.0016 | 0.0218 | |

| 1.1690 | 9.8440 | 1.0788 | 9.9476 | 1.0368 | 9.9914 | |

| 0.0109 | 0.0191 | 0.0034 | 0.0322 | 0.0012 | 0.0193 | |

| 0.0395 | 0.0434 | 0.0096 | 0.0349 | 0.0026 | 0.0194 |

Next we consider the case of . In Table 2 we report the average, sample variance and mean squared error for estimators , , and . As we see, estimators have a smaller variance than , but has a smaller variance than , which is supported by Theorems 4 and 5 that has a faster rate of convergence than . As becomes larger, the accuracy of all estimators improves. Since and have a smaller mean squared error than and , respectively, we prefer the estimation procedure based on equation (2.3) to that based on equation (2.4).

| 1.0289 | 1.0270 | 1.0350 | 1.0266 | 1.0019 | 1.0000 | |

| 0.2901 | 0.3230 | 0.1245 | 0.1327 | 0.0453 | 0.0528 | |

| 0.2909 | 0.3237 | 0.1257 | 0.1334 | 0.0453 | 0.0528 | |

| 1.0345 | 0.0486 | 0.9612 | -0.0240 | 1.0022 | 0.0111 | |

| 1.1597 | 1.2678 | 0.5080 | 0.5095 | 0.1833 | 0.2082 | |

| 1.1609 | 1.2702 | 0.5095 | 0.5101 | 0.1833 | 0.2083 | |

| 1.5461 | 1.0513 | 1.5030 | 1.0146 | 1.5030 | 1.0055 | |

| 0.0270 | 0.0150 | 0.0097 | 0.0047 | 0.0032 | 0.0015 | |

| 0.0291 | 0.0176 | 0.0097 | 0.0049 | 0.0041 | 0.0015 | |

| 0.8593 | 0.5297 | 0.8379 | 0.5053 | 0.8350 | 0.5037 | |

| 0.0170 | 0.0131 | 0.0070 | 0.0047 | 0.0024 | 0.0019 | |

| 0.0177 | 0.0140 | 0.0070 | 0.0047 | 0.0024 | 0.0019 | |

| 1.1654 | 1.1557 | 1.1155 | 1.0880 | 1.0349 | 1.0292 | |

| 0.4281 | 0.4482 | 0.2303 | 0.2246 | 0.0934 | 0.1121 | |

| 0.4555 | 0.4724 | 0.2436 | 0.2323 | 0.0946 | 0.1130 | |

| 0.9802 | 0.0338 | 0.9188 | -0.0177 | 0.9931 | 0.0147 | |

| 1.6477 | 1.7563 | 0.9138 | 0.8838 | 0.3686 | 0.4504 | |

| 1.6481 | 1.7575 | 0.9204 | 0.8841 | 0.3686 | 0.4506 | |

| 1.6555 | 1.1726 | 1.5749 | 1.0792 | 1.5315 | 1.0365 | |

| 0.0221 | 0.0112 | 0.0076 | 0.0037 | 0.0025 | 0.0012 | |

| 0.0463 | 0.0410 | 0.0132 | 0.0100 | 0.0035 | 0.0025 | |

| 0.9094 | 0.5891 | 0.8640 | 0.5381 | 0.8485 | 0.5195 | |

| 0.0174 | 0.0152 | 0.0087 | 0.0071 | 0.0033 | 0.0036 | |

| 0.0232 | 0.0231 | 0.0096 | 0.0086 | 0.0035 | 0.0040 |

Finally we consider the case of . Given results in Tables 1 and 2, we only consider the estimators derived from equation (2.3) with the large sample size . Table 3 shows that all estimators have a rather large variance for , and the variance of is still quite big even when , which means estimating the shape parameter is very challenging as usually.

| 0.8631 | 0.2050 | 0.2237 | 1.2268 | 0.2840 | 0.3354 | 0.9787 | 8.0693 | 8.2985 | |

| 0.9964 | 15.8532 | 15.8532 | 1.1412 | 16.2379 | 16.2578 | 1.7859 | 11.1177 | 11.7353 |

4 Data Analysis

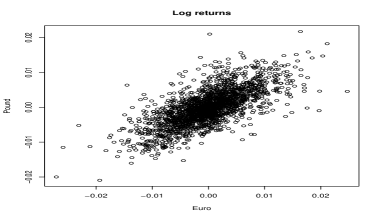

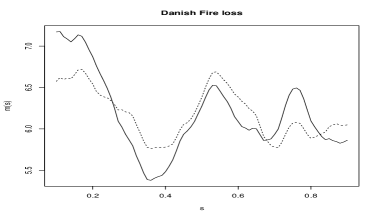

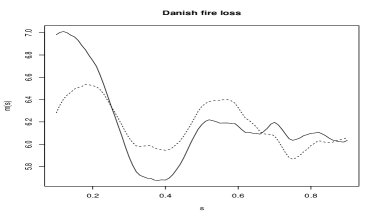

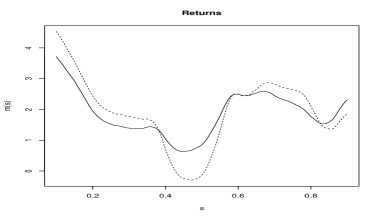

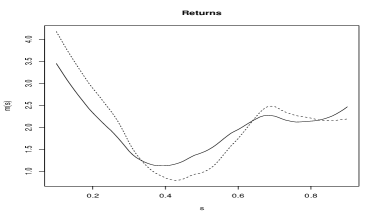

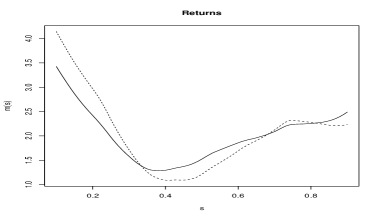

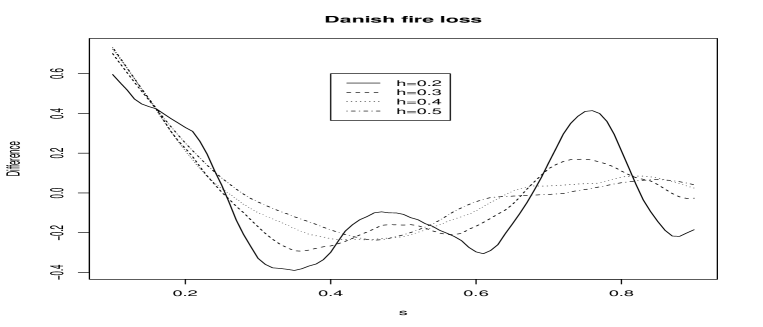

In this section we apply the proposed nonparametric estimators to two real data sets: Danish fire loss and log-returns of exchange rates; see Figure 1.

This first data set is the nonzero losses to building and content in the Danish fire insurance claims, which comprises 2167 fire losses over the period 1980 to 1990. The second data set is the log-returns of the exchange rates between Euro and US dollar and those between British pound and US dollar from January 3, 2000 till December 19, 2007.

We calculate both and for by using Epanechnikov kernel and the bandwidth with . From Figures 2 and 3, we observe that and have a quite similar pattern for the second data set, but seem having a different pattern for the first data set when a large bandwidth is employed. To further investigate this issue, we plot the difference of in Figure 4 for the above with , which indeed shows the differences for are quite similar to those for . Nevertheless, Remark 3 says that one should prefer to . The non-constant function indicates observations are not identically distributed.

5 Proofs

Proof of Theorem 1..

We focus on the proof of case iii) since the other two cases can be verified easily.

For any such that , write

| (5.1) |

For fixed and , we have

and

uniformly in , which implies that

| (5.2) |

uniformly for , where and are fixed and is any given constant.

Proof of Theorem 2..

Put , , and for . Then

| (5.4) |

It is also known that

| (5.5) |

see Inequality 1 in Page 134 of Shorack and Wellner [17](1986).

Put

and

Therefore

| (5.6) |

It follows from (5.5) that

| (5.7) |

Direct calculations show that and , which imply that

| (5.8) |

By (5.4), (5.6)–(5.8), we have

| (5.9) |

Using

we have

| (5.10) |

and

| (5.11) |

| (5.12) |

(see Plackett (1954)), we have

| (5.13) |

| (5.14) |

| (5.15) |

and

| (5.16) |

Hence, it follows from (5.13)–(5.16) that

| (5.17) |

It is easy to check that

which, combining with (5.17), implies that

| (5.18) |

Obviously we have

| (5.19) |

Hence, it follows from (5.9), (5.18), (5.19) and Theorem 3.2 of Hall and Heyde (1980) that

| (5.20) |

Note that the above limit has a nonstandard rate, which can be explained as follows. When for , we have

which becomes a constant. However, and are non-degenerate due to the involved factors and . That is, deriving the asymptotic limit of needs finer expansions than the other two quantities. Below we show the asymptotic limits for both and have the standard rate .

Define

and

Similar to the proof of (5.9), we can show that

| (5.21) |

Like the proofs of (5.13)–(5.16), we can show that

Proof of Theorem 3.

As in the proof of Theorem 2, we define

and

Since

we have

It is straightforward to check that

| (5.25) |

by noting that , and are odd functions,

| (5.26) |

By (5.12), we have

for any . Taking derivative with respect to at both sides, we have

for any . Therefore

which gives

| (5.27) |

Since

we have

| (5.28) |

Put . Then

| (5.29) |

It follows from (5.25)–(5.29) that

| (5.30) |

Similarly we can show that

| (5.31) |

| (5.32) |

| (5.33) |

and

| (5.34) |

Therefore, using (5.30)–(5.34) and the same arguments in proving (5.23), we can show that

| (5.35) |

It is straightforward to check that

| (5.36) |

Hence, the theorem follows from (5.35), (5.36) and Taylor expansions. ∎

Proof of Theorem 6..

Proof of Theorem 7.

It follows from standard arguments in local linear estimation. ∎

Acknowledgements We thank two reviewers for helpful comments. Liang Peng was partly supported by the Simons Foundation. Zuoxiang Peng was supported by the National Natural Science Foundation of China (Grant no. 11171275) and the Natural Science Foundation Project of CQ (Grant no. cstc2012jjA00029).

References

- [1] F.E. Benth and P.C. Kettler (2011). Dynamic copula models for the spark spread. Quant. Finance 11, 407–421.

- [2] N. Channouf and P. L’Ecuyer (2012). A normal copula model for the arrival process in a call center. Int. Trans. Oper. Res. 19, 771–787.

- [3] J. Fan and I. Gijbels (1996). Local Polynomial Modelling and Its Applications. Chapman & Hall.

- [4] M. Frick and R.D. Reiss (2013). Expansions and penultimate distributions of maxima of bivariate normal random vectors. Statist. Probab. Lett. 83, 2563–2568.

- [5] T. Fung and E. Seneta (2011). The bivariate normal copula function is regularly varying. Statist. probab. Lett. 81, 1670–1676.

- [6] D. Guégan and J. Zhang (2010). Change analysis of a dynamic copula for measuring dependence in multivariate financial data. Quant. Finance 10, 421–430.

- [7] P. Hall and C.C. Heyde (1980). Martingale Limit Theory and Its Application. Academic Press.

- [8] E. Hashorva (2005). Elliptical triangular arrays in the max-domain of attraction of Hüsler-Reiss distribution. Statist. Probab. Lett. 72, 125–135.

- [9] E. Hashorva (2006). On the multivariate Hüsler-Reiss distribution attracting the maxima of elliptical triangular arrays. Statist. Probab. Lett. 76, 2027–2035.

- [10] J. Hüsler and R.-D. Reiss (1989). Maxima of normal random vectors: between independence and complete dependence. Statist. Probab. Lett. 7, 283–286.

- [11] C.A.J. Klaassen and J.A. Wellner (1997). Efficient estimation in the bivariate normal copula model: normal margins are least favourable. Bernoulli 3, 55-77.

- [12] A.J. McNeil, R. Frey and P. Embrechts (2005). Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton University Press.

- [13] B.V.M. Mendes and E.F.L. de Melo (2010). Local estimation of dynamic copula models. Int. J. Theor. Appl. Finance 13, 241–258.

- [14] C. Meyer (2013). The bivariate normal copula. Communications in Statistics - Theory and Methods 42, 2402–2422.

- [15] R.L. Plackett (1954). A reduction formula for normal multivariate integrals. Biometrika 41, 351–360.

- [16] M. Sibuya (1960). Bivariate extreme statistics. Ann. Inst. Statist. Math. 11, 195–210.

- [17] G.R. Shorack and J.A. Wellner (1986). Empirical Processes With Applications To Statistics. John Wiley & Sons.

- [18] R.W.J. Van den Goorbergh, C. Genest and B.J.M. Werker (2005). Bivariate option pricing using dynamic copula models. Insurance Math. Econom. 37, 101-114.