Hedging of defaultable claims in a structural model using a locally risk-minimizing approach

Abstract

In the context of a locally risk-minimizing approach, the problem of hedging defaultable claims and their Föllmer-Schweizer decompositions are discussed in a structural model. This is done when the underlying process is a finite variation Lévy process and the claims pay a predetermined payout at maturity, contingent on no prior default. More precisely, in this particular framework, the locally risk-minimizing approach is carried out when the underlying process has jumps, the derivative is linked to a default event, and the probability measure is not necessarily risk-neutral.

Keywords Defaultable claims, Hedging strategy, Locally risk-minimizing,

Föllmer-Schweizer decomposition, Galtchouk-Kunita-Watanabe decomposition

1 Introduction

In its simple form, a defaultable claim pays a certain pre-defined amount at the maturity of the contract, if there has not been a prior default, and pays zero otherwise. In this work, an hedging analysis is carried out for these derivatives when the underlying risky asset is modeled by a finite variation Lévy process. It is of mathematical and practical interest to study the hedging of defaultable claims when the asset prices are affected by jumps. The extension to more complicated derivatives and underlying processes will be interesting for future work. First, we review the literature and related previous works.

We start by a definition of credit risk. Credit risk is the risk associated with the possible financial losses of a derivative caused by unexpected changes in the credit quality of the counterparty’s issuer to meet its obligations. The first paper that introduced credit risk for a path independent claim goes back to the work of Merton (1974).

When analyzing a credit derivative, normally there are two prominent issues, pricing and hedging of the derivative. The latter is a more challenging question, especially when the market is incomplete. In most financial models, even when working with simple stochastic processes, a complete hedge still may not be feasible for credit derivatives. There are different approaches to manage the risk in an incomplete market. Quadratic hedging is a well developed and applicable method to manage the risk.

Schweizer (2001) or Pham (1999) provide a good survey of quadratic hedging methods in incomplete markets. In Schweizer (2001) two quadratic hedging approaches are discussed for the case where the firm’s value process is a semimartingale. These are local risk-minimization and mean-variance hedging.

If we prefer a self-financing portfolio in order to hedge a contingent claim, we speak of mean-variance hedging. If we rather select a portfolio with the same terminal value as the contingent claim (but not necessarily self-financing), we are in the context of a (locally) risk-minimizing approach. Schweizer, Heath and Platen (2001) provide a comprehensive study and comparison of both approaches. In our paper a local risk-minimization approach is used to manage the risk associated with the defaultable claims.

Local risk-minimization hedging emerged in the development of the concept of risk minimization. Föllmer and Sondermann (1986) were among the first to deal with this problem. They solved the problem identifying the risk-minimization strategy when the underlying process is a martingale. The generalization to the local martingale case is done in Schweizer (2001). The solution of the risk-minimization problem is linked to the so called Galtchouk-Kunita-Watanabe (GKW) decomposition assuming that the underlying process is a local martingale.

For a non-martingale process, Schweizer (1988) provides an example of an attainable claim that does not admit a risk-minimization strategy. The extension is possible by putting more restrictive conditions on the underlying process as well as on the hedging strategies.

Literally saying, one has to pay more attention to the local properties of the problem. As for the role of the underlying process, it has to satisfy the structure condition***Assume that is a square integrable special semimartingale with the canonical decomposition . Then satisfies the structure condition, if there exists a predictable process such that for all , and the mean-variance tradeoff process, defined by , is -almost surely finite for all . (SC), see Schweizer (1991) or Schweizer (2001). Under certain conditions like SC, a locally risk-minimizing strategy is equivalent to a more tractable one, called pseudo-locally risk-minimizing strategy. Föllmer and Schweizer (1991) gives a necessary and sufficient condition for the existence of a pseudo-locally risk-minimizing strategy. It turns out that finding these strategies is equivalent to the existence of a generalized version of the GKW decomposition, known as the Föllmer-Schweizer (FS) decomposition. A sufficient condition for the existence of an FS decomposition is provided by Monat and Stricker (1995).

Although the existence of locally risk-minimizing strategies is proved under some conditions, it completely depends on the FS decomposition. In some special cases there are constructive ways of finding this decomposition explicitly. The case of continuous processes is more flexible, and the well known method of minimal equivalent local martingale measure (MELMM) is applicable. Biagini and Cretarola (2009) study general defaultable markets under a locally risk-minimizing approach. However the continuity of the underlying process is a crucial assumption in their work.

Most recently, Choulli, Vandaele and Vanmaele (2010) find an explicit form of the FS decomposition based on a representation theorem. They aimed to provide a general framework under which the FS decomposition is obtained. While this work could fit into theirs, our approach leads to a more explicit form of the FS decomposition. By using a slightly different method, we specifically focus on the hedging of the defaultable claims, based on the theory of local risk-minimization, assuming that the underlying process is a bounded variation Lévy process with positive drift.

Our paper studies a structural model, in the sense that a default event is defined, and we use the whole market information represented by the filtration generated by the underlying process. However, while the default event is structural (and so economically intuitive), we use an analysis like that of reduced form models and especially intensity based models. These models were pioneered by the works of Artzner and Delbaen (1995) or Jarrow and Turnbull (1995), and they do not use or determine a default model of the firm. They use an intensity process or hazard process instead.

Martingale techniques and the idea of intensity in reduced form models are applied to analyze the structure of the defaultable claims. In Section 2, under some conditions, a compensation formula is used to find a canonical decomposition of the defaultable process , where is a hitting time (defining the default time) and is a real valued function. This enables us to use compensator techniques for these types of processes.

The predictable finite variation part of this decomposition is absolutely continuous with respect to the Lebesgue measure. Hence, when is a constant function, this precisely determines the intensity of . This intensity is already obtained by Theorem 1.3 of Guo and Zeng (2008) for a Hunt process that has finitely many jumps on every bounded interval. However, a finite variation Lévy process could have infinitely many jumps on bounded intervals and so some modifications of their ideas would be essential.

Note that in our analysis the underlying process allows for jumps, the payoff is linked to a structural default event, and the probability measure is not necessarily a martingale measure. In addition we do not use any type of Girsanov’s theorem, but the results are based on solutions of partial integro-differential equations (PIDE). We also study the structure of the default indicator process and finite horizon ruin time. Apart from the theoretical concerns in this paper, the main effort is devoted to obtain answers to two interesting questions.

The first question is, given a defaultable claim, how a locally risk-minimizing hedging strategy can be carried out. As it is not possible to eliminate the credit risk completely, the second question is whether it is possible to design a customized defaultable security, to make the product completely hedgeable i.e., the claim can be written as the sum of a constant and a stochastic integral with respect to the underlying process. This will result in a risk-free defaultable claim. In our setup we find necessary and sufficient conditions for the existence of such a product.

The paper is structured as follows. The model, some preliminary assumptions, and results are provided in Section 2. A canonical decomposition of the stochastic process is discussed in Section 3. This is an essential tool in our analysis. Locally risk-minimizing hedging strategies for defaultable claims are obtained in Section 4. In Section 5, we take a look at the structure of the default time.

2 The Model and Preliminaries

We study a process , modeling a firm’s assets value, constructed on a probability space and we denote by its natural filtration, completed and regularized so that it satisfies the usual conditions.

We study defaultable claims with actual payoffs of the form

| (2.1) |

where , is a real valued function, and is the maturity or expiration time of the security, and

| (2.2) |

Note that the firm’s assets value is assumed to be observable. Therefore from a financial point of view, the definition in (2.2) for default makes sense if either the modeler is the firm’s management, the accounting data are publicly available or they can be well estimated in the market.

The security in (2.1) pays if there is no default in and zero otherwise, hence the recovery rate is considered to be zero. A defaultable zero-coupon bond is a special case of this security by letting , on for a constant . Later we will see that the function is the boundary condition of a PIDE.

For two semimartingales and , the notations and , respectively, stand for quadratic covariation and conditional quadratic covariation, see Section 6, Chapter \@slowromancapii@ and Section 5, Chapter \@slowromancapiii@ of Protter (2004) or Section 4, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987) for the definitions. For the sake of completeness, we recall some basic definitions.

The set of all uniformly integrable martingales is denoted by , and is the set of all square integrable martingales, i.e. the set of all martingales such that . If in addition , the notation is used. Also the set of integrable variation processes (starting at zero) is represented by . In what follows, if is a class of processes, its localized class is denoted by

One of the fundamental results in the theory of stochastic calculus is the following, see Proposition 4.50, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987) for the proof.

Proposition 2.1.

Assume that the process is a local martingale (i.e. ). Then almost surely if and only if

Definition 2.1.

The two processes and belonging to are called orthogonal to each other if belongs to .

If the processes and belong to , then it can be proved that is orthogonal to if and only if , for example see Theorem 4.2, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987). If and are two local martingales and belongs to , then by using the fact that is the compensator of , one can still show that is orthogonal to if and only if .

A similar result to Proposition 2.1 is still true for the conditional quadratic variations as well, and it is in fact a result that we use later.

Corollary 2.1.

Suppose that belongs to or then almost surely if and only if .

Proof.

Note that if is in then , see Proposition 4.50, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987). So it is enough to prove the result for . In this case, the result follows from Proposition 2.1 and the fact that is the compensator of . ∎

Now, we explain our model assumptions.

This work is motivated by the first basic question of how the riskiness of a corporate bond can be managed. Such bonds represent a special defaultable claim for the firm. Specifically we focus on finite variation Lévy processes modeling the firm’s assets value. See Geman (2002) for some motivations on how these processes model the dynamic of stock prices better than diffusion or jump-diffusion models. Besides, some technical reasons also motivate this choice.

The following hypothesis is used throughout the paper and especially in Section 3 to find the canonical decomposition of the process , where is a real-valued function.

Hypothesis 2.1.

It is assumed that the firm’s assets value process , starting at , is a bounded variation Lévy process with Lévy triplet , where the Lévy measure is concentrated on . The process has the following Lévy-Itô decomposition

| (2.3) |

where and is the jump measure of the process . It is supposed that and Also in the case of , we assume that the measure is continuous.

Note that the process in Hypothesis 2.1 has either finite activity†††In this case the process is nothing but a compound Poisson process plus drift starting at . () or infinite activity (). In the former case, by Remark 27.3 of Sato (1999), the compound Poisson process part of (2.3) has a continuous distribution on , and in the latter one by Theorem 27.4 of Sato (1999), has a continuous distribution for every . In particular, in either case we have . Hence, one can assume that the domain of the function in (2.1) is the positive real line. This is because of the fact that , almost surely, where is the restriction of to .

By Remark A.1, the default time given by (2.2) is a totally inaccessible stopping time. Total inaccessibility of guarantees the unpredictability of default.

Remark 2.1.

Regarding a financial risk process, for instance a stock price process, the process and a non-zero barrier level are preferred from a financial point of view. However, this case can be covered by our model. For example, suppose that default is defined by , for the constant barrier . This is equivalent to , and regarding (2.2), there is nothing special about crossing the level zero here, this is just for ease of notation.

The following hypothesis and definition are used in Sections 4 and 5 in order to find locally risk-minimizing hedging strategies and the distribution of the default time.

Hypothesis 2.2.

Given a function and a subinterval of , we say that it satisfies the integrability condition if the following holds for all in :

Definition 2.2.

A function belongs to class (*) if there is a function that is the solution of the following PIDE

and

where , , and the operator is given by

| (2.4) |

It is also assumed that the functions and satisfy the integrability condition of Hypothesis 2.2 on the interval .

Remark 2.2.

First note that given the integrability condition of Hypothesis (2.2), the expression (2.4) is well defined in the sense that the integrals are finite. The PIDE in Definition 2.2 will help to obtain strategies for the case when is not a martingale. This assumption can be thought of as a substitution for the change of probability measure.

In general, the existence of a classical solution for the PIDE in Definition 2.2 is not always guaranteed. However, if (i.e. when is a martingale), then under some regularity conditions a classical solution can be provided by Feynman-Kac’s representations. For a full discussion, examples, and many useful references, we refer the reader to Chapter 12 of Cont and Tankov (2004). In short, the main problem is that since we are in a pure jump model, there is no diffusion and hence the proposed Feynman-Kac representation is not necessarily . In cases where this smoothness holds then the Feynman-Kac representation is in fact a solution. Examples 1 and 2 of Cont, Tankov and Voltchkova (2004) show how the regularity can be easily violated. If the smoothness does not hold or when is non-zero, then some approximation techniques must be used; in practice, viscosity solutions can be applied. Extending the results to the non-smooth case is left for future work.

Finally, it is supposed that the market is frictionless and made of only two assets, a risky asset modeled by a process satisfying Hypothesis 2.1, and a risk-free one. For simplicity, it is supposed that the value of the risk-free asset is equal to 1 at all times, i.e. the interest rate is zero.

3 The Canonical Decomposition of

In this section we investigate the canonical decomposition of the process , where and is a function. More precisely, under some conditions we prove that it is a special semimartingale and we find a closed form for its finite variation predictable part. This result is used in Section 4.

Theorem 3.1.

Assume that satisfies Hypothesis 2.1. Let be a function that satisfies the integrability condition of Hypothesis 2.2 on . Then the process , where , is a special semimartingale and the process

| (3.5) |

is an - local martingale, where the stopping time is defined by

| (3.6) |

and the operator is given by (2.4).

Proof.

Because the function is a function, the process is a semimartingale and so by using the product formula of semimartingales, for we have

| (3.7) |

To get the canonical decomposition of , we prove that the processes defined by each of the three terms on the right-hand side of the above equation are special semimartingales and obtain their canonical decomposition. The rest of the proof is divided into four steps.

Step 1. Since is a function, by applying Itô’s formula, we have that

see Theorem 4.2 of Kyprianou (2006) for a proof. By the compensation formula, see Theorem 4.4 of Kyprianou (2006), we get that

for all bounded non-negative predictable processes , with the understanding that one of the expectations is well defined if and only if the other one is well defined as well and they are equal. Hence by the integrability condition of Hypothesis 2.2 and using Corollary 4.5 of Kyprianou (2006), one can show that for , where is an - local martingale and is a predictable finite variation process. The process is given by , where the operator is defined by

This proves that and hence are special semimartingales. Therefore

Since the first term on the right-hand side of the above is a local martingale, the first term of (3.7) is a special semimartingale and its predictable finite variation part is then given by

| (3.8) |

Step 2. Since is a special semimartingale, the second term of (3.7) is also a special semimartingale. To find its canonical decomposition, we consider two cases. First , in this case, the process is a compound Poisson process plus drift starting at , and there are finitely many jumps on every bounded interval. Furthermore, since , one can easily check that for every , . Also by Remark A.1, the stopping time is now totally inaccessible, hence Theorem 1.3 of Guo and Zeng (2008) is applicable, and so the process

is an - local martingale.

Now assume that , then by Theorem 21.3 of Sato (1999) there are infinitely many number of jumps on every bounded interval. Therefore the result of Guo and Zeng (2008) is not directly applicable this time. However, since , every is an irregular point for , which implies that , see Theorem 6.5 of Kyprianou (2006) and the discussions following it. So, using the compensation formula, their proof actually shows that

with the understanding that the left-hand side is well defined if and only if the right-hand side is well defined as well and they are equal. Also by Lemma A.2, for every , is almost surely finite, and so by Lemmas 3.10 and 3.11 of Chapter \@slowromancapi@ of Jacod and Shiryaev (1987), the process belongs to .

Therefore, by Lemma A.1, in either case, the predictable finite variation part of the second term in (3.7) is given by

| (3.9) |

Step 3. Finally we find the canonical decomposition of the third term in (3.7). The indicator process is of finite variation. Then by Proposition 4.49(a), Chapter \@slowromancapi@ of Jacod and Shiryaev (1987), we obtain

This is a special semimartingale, and one can show that it belongs to . Therefore, by Lemma A.1, to obtain the predictable finite variation part of the process, we need to calculate the following expectation

for an arbitrary bounded non-negative predictable process . Again, the calculations of this expectation follow almost the same lines as those of Theorem 1.3 in Guo and Zeng (2008) and similar to the second case of Step 2, where the compensation formula is used. From there we obtain that the expectation is equal to

with the understanding that one of the expectations is well defined if and only if the other one is well defined as well and they are equal. Because of the integrability condition of Hypothesis 2.2, the assumptions of Lemma A.1 are in force, and therefore the process

is an - local martingale. Hence the predictable finite variation part of the third term in (3.7) is given by

| (3.10) |

Step 4. From equations (3.8), (3.9), and (3.10), we conclude that the predictable finite variation part of the process

is equal to

Notice that in any of the above integrands, the strict inequality of the indicator process can be changed to include an equality, because the Lebesgue measure does not charge . From the above equation and since , after some manipulations, it concludes that the process (3.5) is an - local martingale. Hence the predictable finite variation part of the process is equal to

where is given by (2.4). ∎

Remark 3.1.

-

1.

Regarding Theorem 3.1, a few comments are worth of mentioning. In the proof of the theorem, the assumption of Hypothesis 2.1 was not used. The operator given by (2.4) is not the same as Dynkin’s or Itô’s operators. Theorem 3.1 still holds for a function satisfying the integrability condition of Hypothesis 2.2 on , . Finally, using Lemmas 3.10 and 3.11 of Chapter \@slowromancapi@ of Jacod and Shiryaev (1987), the canonical decomposition of the theorem shows that the process belongs to

-

2.

Note that if the derivative of is bounded, the integrability condition of Definition 2.2 is satisfied. In particular, this shows that admits a compensator that is absolutely continuous with respect to the Lebesgue measure; in other words, the following process is an - local martingale

Also, for a constant function , and a compound Poisson process plus drift, Theorem 3.1 is a result of Theorem 1.3 in Guo and Zeng (2008).

4 Hedging Strategies for Defaultable Claims

In this section our goal is to obtain locally risk-minimizing hedging strategies for the credit sensitive security with payoff in (2.1).

If the underlying process is a (local) martingale, local risk-minimization reduces to risk-minimization and the existence of the hedging strategies is guaranteed by a GKW decomposition. When the process is a semimartingale then risk-minimization is no longer valid. It must be improved to local risk-minimization and the hedging strategies are solved by the FS decomposition.

The FS decomposition was first introduced by Föllmer and Schweizer (1991). The existence of the FS decomposition of a square-integrable claim is proved even for a -dimensional semimartingale by Schweizer (1994), assuming that the process satisfies the SC condition and the mean-variance tradeoff (MVT) process is uniformly bounded in ( belongs to ), and and has jumps strictly bounded from above by 1. Monat and Stricker (1994) prove the existence of the FS decomposition just by assuming that the MVT process is uniformly bounded in and . Under this condition, further Monat and Stricker (1995) prove also the uniqueness.

Choulli, Krawczyk and Stricker (1998) find necessary and sufficient conditions for the existence and uniqueness of the FS decomposition by introducing a new notion for martingales. They prove that there is an FS decomposition for a square-integrable claim under the semimartingale , if first, the process satisfies an integrability condition and second if it is “regular” (we refer to the original paper for a definition). Here the process is the Doléans - Dade exponential process, see Section 8, Chapter \@slowromancapii@ of Protter (2004).

Choulli, Vandaele and Vanmaele (2010) discuss the relationship between the GKW and FS decompositions assuming that is strictly positive. Then in a general framework, under a weaker assumption that does not require the strict positivity of , they find a closed form of the FS decomposition based on a representation theorem, Theorem 2.1 of their paper.

Their general framework can cover our specific model. However in contrast to Theorem 2.1 of their paper, Theorem 3.1 of our work leads to more explicit solutions for hedging strategies. In addition, despite current methods that normally start from a payoff and then construct a value process, we somehow turn this around and present self-contained calculations for the components of the FS decomposition.

Assume that processes and belong to on . Then by the GKW decomposition there is a predictable process and a (local) martingale , orthogonal to , such that

and the process is given by

| (4.11) |

Also it is worth mentioning that this decomposition is still valid under milder conditions. For instance, it is enough to have , , a local martingale, and a locally bounded predictable process. In the space, all these conditions are satisfied.

The locally risk-minimizing strategy is linked to the FS decomposition. Hence, our aim is to find the FS decomposition of the payoff (2.1). To reach this goal, the next theorem first gives a decomposition that is close to the FS decomposition and in fact is more general. This theorem is also used in Section 5. Before stating the theorem, we explain the conditions on the underlying process .

Assuming Hypothesis 2.1 then , and therefore the process has the canonical decomposition , where is a martingale and is a continuous finite variation process (in fact a deterministic function) given by

We remind the reader that the process is represented by . Also let the process be given by

| (4.12) |

where , the functions and are defined in Definition 2.2, and . Notice that the process is predictable and implicitly depends on the function . Also, if is non-zero then can be equivalently represented by .

Theorem 4.1.

Assume that Hypothesis 2.1 holds and let the function belong to class (*). We further suppose that the process belongs to . Then for all , the following decomposition holds up to an evanescent set‡‡‡This means that up to an evanescent set we have

| (4.13) |

and specifically for , one obtains

| (4.14) |

where the function is introduced in Definition 2.2, and the process , , is a local martingale, orthogonal to the martingale part of , i.e. .

Proof.

First we find the GKW decomposition of versus . We show that

| (4.15) |

for a local martingale that is orthogonal to .

By Proposition 4.49, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987), . Therefore belongs to and its compensator exists which is given by , see Section 5, Chapter \@slowromancapiii@ of Protter (2004). By similar reasons or as we will see shortly, the process also exists. Because of these reasons, the GKW decomposition exists and formula (4.11) is applicable. So we need to obtain and .

Calculating is simple. Since is square integrable on , Proposition 4.50, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987) shows that . Also, we have that and therefore the conditional quadratic variation of , as the compensator of , exists and equals to . Hence the process is equal to

| (4.16) |

Since , the compensator is the same for the two processes and to get , it is enough to obtain . Integration by parts for semimartingales on gives

Let and , then , , and we also have Therefore the above integration by parts formula on becomes

The integrals on the right-hand side of the above equality are local martingales, the process

is a predictable finite variation process, and . Therefore the uniqueness of the conditional quadratic covariation (see Section 5, Chapter \@slowromancapiii@ of Protter (2004)) gives,

Hence after some manipulations is seen to be equal to

| (4.17) |

Then the GKW decomposition in (4.15) is a result of expressions (4.11), (4.16), and (4.17). By equation (1.1) of Lemma A.2, , almost surely, where is the Lebesgue measure. This implies that almost surely we have . On the other hand, satisfies the PIDE of Definition 2.2, therefore and the GKW decomposition (4.15) becomes

| (4.18) |

Because functions and satisfy the integrability condition of Hypothesis 2.2, both integrals and are almost surely finite for all . Therefore for all , and so the term are well defined and almost surely finite. Hence one can move the integral on the left-hand side to the other side of the equality. This gives the decomposition in (4.13). Finally the decomposition in (4.14) is obtained by letting in equation (4.13) and noticing that by Definition 2.2, , almost surely. ∎

Remark 4.1.

Remark 4.2.

Note that the calculations of Theorem 4.1, especially equation (4.17) along with Corollary 3.16 of Choulli, Krawczyk and Stricker (1998) show that is an - local martingale and is a local martingale where . Then in comparison to Proposition 4.2 of Choulli, Vandaele and Vanmaele (2010), this suggests that should be the value of the hedging portfolio. Proposition 4.1 confirms this.

In the special case when the process is a local martingale, we have the following corollary.

Corollary 4.1.

Assume that Hypothesis 2.1 holds. Let the function belongs to class (*) and the process belong to . Now further suppose that is a local martingale in the natural completed filtration generated by , i.e. . Then we have

| (4.19) |

where the operator is introduced in (2.4), the functions and are defined in Definition 2.2, and the process , is a local martingale orthogonal to .

Proof.

Our goal is to find the FS decomposition of the payoff in (2.1), but finding this decomposition leads to just a pseudo-local risk-minimization and not necessarily to local risk-minimization. To make a bridge between the two concepts, first we need to investigate the SC condition on the underlying process and also the existence of the FS decomposition, see Schweizer (2001) for more details. Since the process satisfies Hypothesis 2.1, it is square integrable and one can easily prove that the SC condition holds for .

Therefore, by Theorem 3.3 of Schweizer (2001), locally risk-minimizing strategies are the same as pseudo-locally risk-minimizing strategies. On the other hand by Proposition 3.4 of Schweizer (2001) the existence of the latter is equivalent and a result of the existence of the FS decomposition of the payoff. Since the MVT process in our model is uniformly bounded in both and , the FS decomposition exists.

So we conclude that in our framework the existence of the Föllmer-Schweizer decomposition, and so locally risk-minimizing strategies, are guaranteed.

From the above, to get a local risk-minimization strategy, all we need is to find the FS decomposition. Some integrability conditions turn the decomposition in (4.14) into the FS decomposition. The next proposition clarifies this. First we provide the definition of , - strategy, and that are used in the following proposition, see Schweizer (2001) for more explanations.

Definition 4.1.

Assume that is a local martingale. Then is the space of all predictable processes such that .

Definition 4.2.

Assume that is a square integrable special semimartingale with the canonical decomposition . Then is the space of all predictable processes such that .

Definition 4.3.

An -strategy is a pair , where and is a real valued adapted process such that the value process is right-continuous and square-integrable. That means for each .

Proposition 4.1.

Assume that Hypothesis 2.1 holds and let the function belongs to class (*). We further suppose that for all , belongs to and the process given by (4.12) is in . Then there exists a locally risk-minimizing - strategy as follows. The number of shares to be invested in the risky asset is given by . The hedging error belongs to . It is orthogonal to and given by

The value process of the portfolio associated with the strategy is equal to

the number of shares to be invested in the risk-free asset is

and finally the cost process is given by

Proof.

The process satisfies the SC condition. Therefore the existence of an - strategy is equivalent to the existence of the FS decomposition. Notice that for all , belongs to , and so by Proposition 4.50, Chapter \@slowromancapi@ of Jacod and Shiryaev (1987), the process is in . From equation (4.13) of Theorem 4.1, we have

where is a local martingale orthogonal to . Because is in and is square-integrable, the left-hand side and so the right-hand side of the above equation are square-integrable. Since belongs to , it is also in and so by Lemma 2.1 of Schweizer (2001) the process is in Hence the process is square-integrable on and belongs to . Now the result follows from Proposition 3.4 of Schweizer (2001). ∎

Remark 4.3.

A similar result to Proposition 4.1 can be obtained when is a local martingale, but with a simpler form for the strategy . Notice that although we did not use the MELMM method, we have paid the price by involving a PIDE. In the MELMM method when the underlying process is a martingale the problem of finding the hedging strategies is simpler. Here, the same happens, if the underlying process is a martingale, the PIDE to solve for the hedging strategy has a simpler form.

The next theorem investigates necessary and sufficient conditions under which the process in Theorem 4.1 vanishes.

Theorem 4.2.

Assume that Hypothesis 2.1 holds and the function belongs to class (*). Suppose that the integrability condition of Hypothesis 2.2 is met on by the function , defined as , where the function is defined in Definition 2.2. Now further suppose that the process and the process in the decompositions (4.13) and (4.14) belong to . Let the operator be defined as

| (4.20) |

where and the function is defined in Definition 2.2. Then the martingale is null on , if and only if for all and all . In this case, for all , we have the following, up to an evanescent set,

| (4.21) |

and specifically for , one obtains

| (4.22) |

Proof.

Since is in , by Corollary 2.1, is equivalent to . On the other hand, by Theorem 4.1 the following holds

From this decomposition, we have

| (4.23) |

In what follows, we show that this equation is valid, in the sense that all the terms on the right hand side exist and we compute them explicitly. First, let us obtain

We already know that and observe that . By Theorem 3.1, , where is an - local martingale and Using the integration by parts formula we get that

or

The right-hand side of the above equation is a local martingale. This shows that . Now the predictability of and uniqueness of conditional quadratic variation give

For the second term of (4.23), since and , computing the second term follows from

where was already computed in the proof of Theorem 4.1, see equations (4.12) and (4.17).

The process belongs to and the third term can be computed similarly

or

By combining Theorem 4.2 and Proposition 4.1, we get the following result that provides a necessary and sufficient condition for the existence of a risk-free product. In the context of jump-diffusion processes, Kunita (2010) answers a similar question for path independent payoffs.

Proposition 4.2.

Assume that Hypothesis 2.1 holds and the function satisfies Definition 2.2. Suppose that the integrability condition of Hypothesis 2.2 is met on by function defined as , where the function is defined in the hypothesis. Now further suppose that for all , belongs to and the process given by (4.12) is in . Let the operator be defined as (4.20). Then the process , defined in Proposition 4.1, is a locally risk-minimizing - strategy that makes the derivative completely hedgeable if and only if , for all , and all . It means that we have the following decomposition

Remark 4.4.

If the process is a martingale, then the operator simplifies to

Remark 4.5.

The next example shows an application of Proposition 4.1, and it was chosen simply because in this case there is a closed form solution for the PIDE of Definition 2.2 given by Theorem 5.6.3 of Rolski et al. (1999). Therefore, one can compare the simulated solution with the exact one. In general, simulation techniques must be used.

Example 4.1.

Assume that , where is an homogeneous Poisson process with intensity and the ’s are i.i.d. random variables with jump distribution . Let , , and suppose that the process is a martingale in the natural filtration generated by , which means that . We remind the reader that in this paper the interest rate is taken to be zero. Consider a defaultable zero-coupon bond that pays one unit of currency if there is no default, i.e. for all . One can check that belongs to class (*) and by Proposition 4.1, to implement the hedging strategy, the number of shares invested in the risky asset is given by

| (4.24) |

where satisfies the following PIDE

The Feynman-Kac formula or a renewal argument can be applied to prove that the solution has the following representation

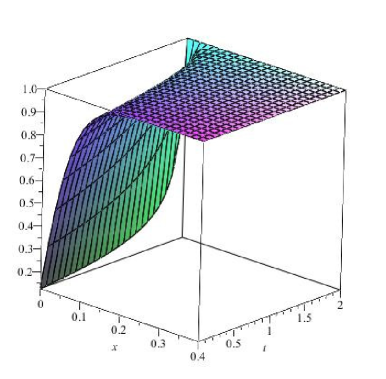

This representation holds regardless of the type of distribution of jumps. In the case of exponential jumps in this example, a closed form solution is available. This solution is provided by Theorem 5.6.3 or Theorem 5.6.4 in Rolski et al. (1999). It is a complicated function and its graph on is given in Figure 1 for , , , and .

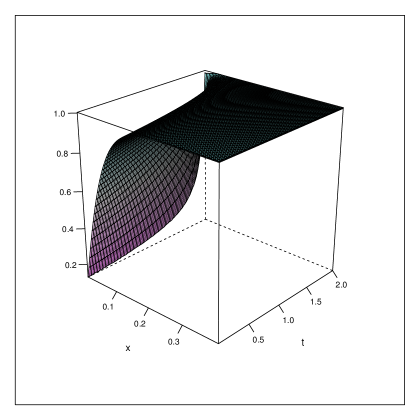

The function can also be estimated numerically by simulation. With the same parameters as above, Figure 2 gives the graph of an estimation of on . The number of shares invested in the risky asset is a closed form of this function given by equation (4.24). Therefore the function acts as an interface to solve the problem. However this function also has a nice interpretation. From Proposition 4.1, one can easily verify that the value process of the portfolio is provided through the function . More precisely we have that

Next we obtain the locally risk-minimizing strategy corresponding to a simulated sample path of the process . In practice, a dynamic portfolio is updated at some specific trading dates. In fact Proposition 4.1 and formula (4.24) cannot be applied directly. A discretization procedure is required to implement the theory.

Here we use a simple procedure. We divide the interval into 1000 equal subintervals. It is assumed that the trading dates are given by , for , where . Then the number of shares invested in the risky asset is given by

where each is a bounded -measurable random variable that is determined right after the transaction . This is due to the fact that a realistic strategy must be left continuous or predictable. The integral also must be discretized. This is essential to obtain the observed values of the process .

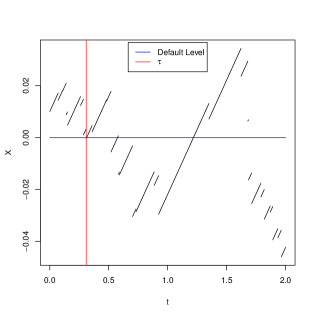

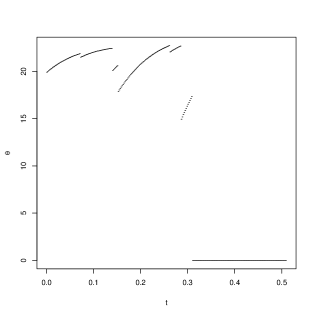

Figure 3 shows the simulated sample path of the process , for , together with the number of shares invested in the risky asset to be held in each trading period. As Figures 1 or 2 confirm, the probability of crossing the barrier is relatively high for this process, . For the sample path of the process shown in Figure 3, the default happens at . At this time, the number drops to zero and remains in this state until the maturity of the contract.

|

|

| A sample path of | The number of shares |

Similar graphs can be obtained for the number of shares of the risk-free asset, the value of the portfolio , the error term , and the cost process .

5 Structure and Distribution of the Default Time

In this section, we discuss the structure and the distribution of the default time. It is assumed that satisfies Hypothesis 2.1.

Some of the results of Section 4 can be helpful to understand the structure of the default time. Regarding Theorem 4.1, one can let be the constant function So without almost any effort, we have the following decomposition.

Proposition 5.1.

Assume that Hypothesis 2.1 holds.Then for all , we have the following decomposition up to an evanescent set

| (5.1) |

and specifically for , one obtains

| (5.2) |

where the function is introduced in Definition 2.2, the process is given by equation (4.12), and the process , , is a local martingale orthogonal to the martingale part of , i.e. .

Notice that since the process is square-integrable, the process belongs to . Although this decomposition reveals the structure of the default time, it does not tell us much about the distribution of the default time. This is the decomposition of the indicator process versus the process . Regarding the distribution of the default time, a more useful decomposition is the following.

Proposition 5.2.

Assume that Hypothesis 2.1 holds. Let the function be the solution of the following PIDE,

where the function is a real valued function and the function satisfies the integrability condition of Hypothesis 2.2. Let the process be the martingale part of the canonical decomposition of , i.e. . We further suppose that the process belongs to . Then for all , the following decomposition holds up to an evanescent set

and especially for , one obtains

| (5.3) |

where the process is given by

and the process , , is a local martingale orthogonal to the process .

Proof.

As a special case let , then by taking the expectation of both sides of (5.3), we obtain , and is the solution of the PIDE in Proposition 5.2. Finding the distribution of the default time using a PIDE is already known; for example, see Theorem 11.3.3 and its proof in Rolski et al. (1999) where this PIDE is obtained for a compound Poisson process plus drift.

Example 5.1.

Let be the same process as Example 4.1 and define the function by . Apply Proposition 5.2 for , then , and

Note that the above function is a special one that makes the operator zero and hence the process is a martingale. This martingale can also be obtained from Theorem 3.1. Therefore we have the following identity

Conclusion

In this paper, first a canonical decomposition of the processes was studied under some conditions. Then based on this result, the locally risk-minimizing approach was carried out to obtain hedging strategies for certain structural defaultable claims under finite variation Lévy processes.

The analysis is done simultaneously, when the underlying process has jumps, the security is linked to a default event, and the probability measure is a physical one. This approach does not use the MELMM method or any type of Girsanov’s theorem to obtain the strategies. However, the final answer is based on the solution of a PIDE. Besides, some theoretical results in finite horizon ruin time were obtained.

Acknowledgments

The authors are grateful to the Associate Editor and anonymous referees for their constructive comments. The first author is also very thankful to Friedrich Hubalek and Julia Eisenberg for many useful discussions.

References

- [1] Artzner, P. and Delbaen, F., 1995. Default risk insurance and incomplete markets. Mathematical Finance, 5, 187–195.

- [2] Biagini, F. and Cretarola, A., 2009. Local Risk Minimization for Defaultable Markets. Mathematical Finance, 19 (4), 669–689.

- [3] Choulli, T., Krawczyk, L. and Stricker, C., 1998. -martingales and their applications in mathematical finance. Annals of Probability, 26 (2), 853–876.

- [4] Choulli, T., Vandaele, N. and Vanmaele, M., 2010. The Föllmer-Schweizer decomposition: Comparison and description. Stochastic Processes and their Applications, 120 (6), 853–872.

- [5] Cont, R. and Tankov, P., 2004. Financial modelling with jump processes. Chapman & Hall / CRC Financial Mathematics Series: Boca Raton.

- [6] Cont, R., Tankov, P. and Voltchkova, E., 2004. Option pricing models with jumps: integro-differential equations and inverse problems, in European Congress on Computational Methods in Applied Sciences and Engineering, Eds. P. Neittaanmäki et al., 24–28.

- [7] Föllmer, H. and Schweizer, M., 1991. Hedging of contingent claims under incomplete information. Applied Stochastic Analysis, 5, 389–414.

- [8] Föllmer, H. and Sondermann, D., 1986. Hedging of non-redundant contingent claims, in Contributions to Mathematical Economics, Eds. W. Hilderbrand and A. Mas-Collel, 205–223.

- [9] Geman, H., 2002. Pure jump Lévy processes for asset price modelling. Journal of Banking and Finance, 26, 1297–1316.

- [10] Guo, X. and Zeng, Y. 2008. Intensity process and compensator: A new filtration expansion approach and the Jeulin–Yor formula. The Annals of Applied Probability, 18 (1), 120–142.

- [11] Jacod, J. and Shiryaev, A.N., 1987. Limit Theorems for Stochastic Processes. Springer: Berlin.

- [12] Jarrow, R.A. and Turnbull, S.M., 1995. Pricing derivatives on financial securities subject to credit risk. Journal of Finance, 50 (1), 53–86.

- [13] Kunita, H., 2010. Itô’s stochastic calculus: Its surprising power for applications. Stochastic Processes and their Applications, 120 (5), 622–652.

- [14] Kunita, H. and Watanabe, S., 1967. On square integrable martingales. Nagoya Mathematical Journal, 30, 209–245.

- [15] Kyprianou, A.E., 2006. Introductory Lectures on Fluctuations of Lévy Processes with Applications. Springer-Verlag: Berlin Heidelberg.

- [16] Merton, R.C., 1974. On the pricing of corporate debt: the risk structure of interest rates. Journal of Finance, 29, 449–470.

- [17] Monat, P. and Stricker, C. 1994. Fermeture de et de . In Séminaire de Probabilités XXVIII, Lecture Notes in Mathematics, 189–194.

- [18] Monat, P. and Stricker, C. 1995. Föllmer-Schweizer decomposition and mean-variance hedging of general claims. Annals of Probability, 23, 605–628.

- [19] Pham, H., 2000. On quadratic hedging in continuous time. Mathematical Methods of Operations Research, 51 (2), 315–339.

- [20] Protter, P., 2004. Stochastic Integration and Differential Equations. Springer-Verlag: Berlin.

- [21] Rolski, T., Schmidli, H., Schmidt, V. and Teugels, J., 1999. Stochastic Processes for Insurance and Finance. John Wiley & Sons: Chichester.

- [22] Sato, K. I., 1999. Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press: Cambridge.

- [23] Schweizer, M., 1988. Hedging of options in a general semimartingale model. Dissertation ETH Zürich 8615.

- [24] Schweizer, M., 1991. Option hedging for semimartingales. Stochastic Processes and their Applications, 37 (2), 339–363.

- [25] Schweizer, M., 1994. Approximating random variables by stochastic integrals. Annals of Probability, 22 (3), 1536–1575.

- [26] Schweizer, M., 2001. A guided tour through quadratic hedging approaches. in Option Pricing, Interest Rates and Risk Management, Cambridge University Press, Eds. E. Jouini, J. Cvitanic and M. Musiela, 538–574.

- [27] Schweizer, M., Heath, D. and Platen, E., 2001. A comparison of two quadratic approaches to hedging in incomplete markets. Mathematical Finance, 11 (4), 385–413.

Appendix A Technical Results

In what follows the concept of creeping and some technical results are discussed.

Definition A.1.

Assume that the process is a Lévy process such that (resp. ). Let the stopping time be defined as

Then creeps over (resp. creeps down) the level (resp. ), when

The following theorem is part (i) of Theorem 7.11 of Kyprianou (2006) that gives necessary and sufficient conditions for a process to creep upwards or creep downwards.

Theorem A.1.

Suppose that is a bounded variation Lévy process which is not a compound Poisson process with the characteristic exponent . Then creeps upwards (resp. downwards) if and only if the process has the following Lévy-Khintchine exponent

for (resp. ), and is the Lévy measure.

Remark A.1.

Since the process in Hypothesis 2.1 is not a compound Poisson process and its drift is positive, Theorem A.1 is in force and the process never creeps down. In simple words, this guarantees that the default happens only by a sudden jump of the process . Hence from Meyer’s previsibility theorem (see Theorem 4, Chapter \@slowromancapiii@ of Protter (2004)), the default time , given by (2.2), is a totally inaccessible stopping time.

Lemma A.1.

Let and belong to , the class of processes with locally integrable variation. Assume that for all predictable processes that are non-negative and bounded (in the sense that for each such predictable process , there is an upper bound free from and such that for all and ). Then is a local martingale.

Lemma A.2.

Proof.

Let be the Lebesgue measure. Since and are -finite measure, by Fubini-Tonelli Theorem, the integral (henceforth denoted by ) is well-defined and equal to . Now, we prove its finiteness in three steps.

Step 1. Since , we get

Let be the first integral in the second equality, then . However, from Fubini-Tonelli Theorem, we have

| (1.1) |

where the last equality is due to continuity of distribution of . Therefore, and so are almost surely Zero§§§Note that in the case of , the usual convention of measure theory is applied, i.e. ..

On the other hand, the process is quasi-left-continuous (see Lemma 3.2 of Kyprianou (2006)) which concludes that for every , , hence by a similar argument as above, the following equality holds almost surely

Step 2. Here we show that . Note that since is not predictable, quasi-left-continuity is not applicable. First, we have that , and , by Remark A.1. Hence

where is predictable, and so the compensation formula is applicable. By a similar argument to Step 1, we deduce that , almost surely. Therefore

Step 3. From Step 1, we almost surely have

Using Step 2 and the fact that the process is càdlàg, one can show that almost surely, hence

Because is a Radon measure this shows that , almost surely. ∎