Stochastic Choice and Optimal Sequential Sampling††thanks: We thank Stefano DellaVigna and Antonio Rangel for very stimulating conversations, Ian Krajbich, Carriel Armel and Antonio Rangel for sharing their experimental data with us, In Young Cho and Jonathan Libgober for expert research assistance, the Sloan Foundation and NSF grants SES-0954162, SES-1123729, and CAREER grant SES-1255062 for support, and seminar audiences at the ASSA annual meetings, Behavioral Game Theory conference at UCL; economics seminars at Chicago, Harvard/MIT, Northwestern, Queen’s, SITE, Stanford GSB, and Toronto; and a seminar at the Computational Cognitive Science Group at MIT for useful comments.

Abstract

We model the joint distribution of choice probabilities and decision times in binary choice tasks as the solution to a problem of optimal sequential sampling, where the agent is uncertain of the utility of each action and pays a constant cost per unit time for gathering information. In the resulting optimal policy, the agent’s choices are more likely to be correct when the agent chooses to decide quickly, provided that the agent’s prior beliefs are correct. For this reason it better matches the observed correlation between decision time and choice probability than does the classical drift-diffusion model, where the agent is uncertain which of two actions is best but knows the utility difference between them.

1 Introduction

In laboratory experiments where individuals are repeatedly faced with the same choice set, the observed choices are stochastic—individuals don’t always choose the same item from a given choice set, even when the choices are made only a few minutes apart.111See Hey (1995, 2001), Ballinger and Wilcox (1997), Cheremukhin, Popova, and Tutino (2011). In addition, individuals don’t always take the same amount of time to make a given decision—response times are stochastic as well. Our goal here is to model the joint distribution of choice probabilities and decision times in choice tasks, which we call a choice process.

We restrict attention to the binary choice tasks that have been used in most neuroscience choice experiments, and suppose that the agent is choosing between two items that we call left and right In this setting we can ask how the probability of the more frequent (i.e., modal) choice varies with the time taken to make the decision. If the agent is learning during the decision process, and is stopped by the experimenter at an exogenous time, we would expect the data to display a speed-accuracy tradeoff, in the sense that the agent makes more accurate decisions (chooses the modal object more often) when given more time to decide. However, in many choice experiments there is instead the opposite correlation: slower decisions are less likely to be modal (Swensson, 1972; Luce, 1986; Ratcliff and McKoon, 2008).

To explain this, we develop a new variant of the drift diffusion model (DDM); other versions of the DDM have been extensively applied to choice processes in the neuroscience and psychology literatures.222The DDM was first proposed as a model of choice processes in perception tasks, where the subjects are asked to correctly identify visual or auditory stimuli. (For recent reviews see Ratcliff and McKoon (2008) and Shadlen, Hanks, Churchland, Kiani, and Yang (2006).) More recently, DDM-style models have recently been applied to choice tasks, where subjects are choosing from a set of consumption goods presented to them. Clithero and Rangel (2013); Krajbich, Armel, and Rangel (2010); Krajbich and Rangel (2011); Krajbich, Lu, Camerer, and Rangel (2012); Milosavljevic, Malmaud, Huth, Koch, and Rangel (2010a); Reutskaja, Nagel, Camerer, and Rangel (2011) The specification of a DDM begins with a diffusion process that represents information the subjects is receiving over time, and two disjoint stopping regions and . The agent stops if at some point in time it happens that (in which case he chooses ) or (in which case he chooses ); otherwise the agent continues. Because the evolution of the diffusion depends on which choice is better, the model predicts a joint probability distribution on choices and response times conditional on the true state of the world, which is unknown to the agent.

The oldest and most commonly used version of the DDM (which we will refer to as simple DDM) specifies that the stopping regions are constant in time, i.e., and , and that is a Brownian motion with drift equal to the difference in utilities of the items. This specification corresponds to the optimal decision rule for a Bayesian agent who believes that there are only two states of the world corresponding to whether action or action is optimal, pays a constant flow cost per unit of time, and at each point in time decides whether to continue gathering the information or to stop and take an action.333Wald (1947) stated and solved this as a hypothesis testing problem; Arrow, Blackwell, and Girshick (1949) solved the corresponding Bayesian version. These models were brought to the psychology literature by Stone (1960) and Edwards (1965). The constant stopping regions of the simple DDM imply that the expected amount of time that an agent will gather information depends only on the current value of and not on how much time the agent has already spent observing the signal process, and that the probability of the modal choice is independent of the distribution of stopping times.444Stone (1960) proved this independence directly for the simple DDM in discrete time. Our Theorem 1 shows that the independence is a consequence of the stopping boundaries being constant. In contrast, in many psychological tasks (Churchland, Kiani, and Shadlen, 2008; Ditterich, 2006) reaction times tend to be higher in incorrect than correct trials. For this reason, when the simple DDM is applied to choice data, it predicts response times that are too long for choices in which the stimulus is weak, or the utility difference between them is small. Ad-hoc extensions of DDM have been developed to better match the data, by allowing more general processes or stopping regions , see e.g., Laming (1968); Link and Heath (1975); Ratcliff (1978). However, past work has left open the question of whether these generalizations correspond to any particular learning problem, and if so, what form those problems take.

Our main focus in this paper is to provide learning-theoretic foundations for an alternative form of DDM, where the agent’s behavior is the solution to a sequential sampling problem with a constant cost per unit time as in the simple DDM but with a prior that allows her to learn not only which alternative is better, but also by how much. In this uncertain-difference DDM, the state of the world is the vector of the utilities of the two choice. In this model an agent with a large sample and close to zero will decide the utility difference is small, and so be more eager to stop than an agent with the same but a small sample.

Our main insight is that the nature of the learning problem matters for the optimal stopping strategy and thus for the distribution of choices and response times. In particular, we show that in the uncertain-difference DDM it is optimal to have the range of for which the agent continues to sample collapse to as time goes to infinity, and moreover that is does so asymptotically at rate . The intuition for the fact that the boundary should converge to 0 is not itself new, and has been put forward both as a heuristic in various related models and as a way to better fit the data (see, e.g., Shadlen and Kiani, 2013) but we provide the first precise statement and solution of an optimization problem that generates decreasing boundaries, thus providing a foundation for their use in empirical work, such as the exogenous exponentially-declining boundaries in Milosavljevic, Malmaud, Huth, Koch, and Rangel (2010b).555Drugowitsch, Moreno-Bote, Churchland, Shadlen, and Pouget (2012) state a decision problem with two states (e.g. known payoff difference), a fixed terminal time, and time-dependent cost functions, and discuss how to use dynamic programming to numerically compute the solution. Note that even with constant costs the boundary is decreasing when the horizon is finite. We then use approximation results and numerical methods to determine the functional form of the boundary, thus providing guidance about what the rate of collapse might be expected to be.

Finally, we investigate the consequences of allowing the flow cost to vary arbitrarily with time. Intuitively, if the cost decreases quickly enough, this might outweigh the diminishing effectiveness of learning and lead to an increasing boundary. We show that this intuition is correct, and more strongly that any stopping region at all can be rationalized by a suitable choice of a cost function. Thus optimal stopping on its own imposes essentially no restrictions on the observed choice process, and so it is compatible with the boundaries assumed in Ratcliff and McKoon (2008) and Shadlen and Kiani (2013). However, the force of the model derives from its joint assumptions about the evolution of beliefs and the cost function, and the cost functions needed to rationalize various forms of boundary may or may not seem plausible in the relevant applications.

One motivation for modeling the joint distribution of decision times and choices is that the additional information provided by decision times can lead to models that are closer to the underlying neural mechanisms and may therefore be more robust.666See Shadlen and Kiani (2013) and Bogacz, Brown, Moehlis, Holmes, and Cohen (2006) for discussions of how DDM-type models help explain the correlation between decision times and neurophysiological data such as neuronal firing rates. In addition, as shown by Clithero and Rangel (2013), including decision times leads to better out-of-sample predictions of choice probabilities. In other settings than the simple choice tasks we study here, decision times can been used to classify decisions as “instinctive/heuristic” or “cognitive,” as in Rubinstein (2007) and Rand, Greene, and Nowak (2012).

In addition to the papers cited above, our theoretical approach is closely related to the recent work of Woodford (2014). In his model the agent can optimize the dependence of the process on subject to a Shannon capacity constraint, but the stopping rule is constrained to have time-invariant boundaries. In our model the process is exogenous but the stopping rule is optimal subject to a cost, so the two approaches are complementary: both models feature an optimization problem, but over different spaces.

Gabaix and Laibson (2005) and Ke, Shen, and Villas-Boas (2013) look at decisions derived from optimal stopping rules where the gains from sampling are exogenously specified as opposed to being derived from Bayesian updating, as they are here; neither paper examines the correlation between decision time and accuracy. Vul, Goodman, Griffiths, and Tenenbaum (2014) studies the optimal predetermined sample size for an agent whose cost of time arises from the opportunity to make future decisions; they find that for a range of parameters the optimal sample size is one.

Natenzon (2013) and Lu (2013) study models with an exogenous stopping rule. They treat time as a parameter of the choice function, and not as an observable in its own right. Similarly, decision field theory (Busemeyer and Johnson, 2004) specifies an exogenous stopping rule; while this literature does discuss the effect of time pressure it does not treat the observed choice times as data. Our model makes joint predictions about decisions and response times because the stopping time is chosen optimally. These additional predictions provide more structure on stochastic choice and can help us develop more accurate models.

2 Choice Processes and DDMs

2.1 Observables

Let be the set of alternatives, which we will call left and right Let be the set of decision times—the times at which the agent is observed to state a choice. The analyst observes a joint probability distribution ; we call this a choice process. We will decompose as

where is probability of choosing conditional on stopping at time and is the cdf of the marginal distribution of decision times.777Formally, we assume that is a Borel probability measure on . The conditional probabilities exist by Theorems 10.2.1 and 10.2.2 of Dudley (2002).

It will also be useful to decompose the other way

where is the overall probability of choosing at any time, and is the cdf of time conditional on choosing .

2.2 Speed and Accuracy

It is easy to define accuracy in perceptual decision tasks, since in such settings the analyst knows which option is ‘correct.’ However, in choice tasks the agents’ preferences are subjective and may be unknown to the researcher.888In some cases the analyst has a proxy of the preference in form of a separately elicited ranking, see, e.g., Krajbich, Armel, and Rangel (2010), Milosavljevic, Malmaud, Huth, Koch, and Rangel (2010b), Krajbich, Lu, Camerer, and Rangel (2012). One way of defining accuracy is with respect to the modal choice, as we expect that the objects the agent chooses more often are in some sense “better;” we denote the modal choice by , the other one by .

The simplest possible relationship between choices and times is no relationship at all, that is when the distribution of stopping times is independent of the distribution of choices. We will equivalently define this property as follows.

Definition 1.

displays a speed-accuracy independence iff is a constant function of

Speed-accuracy independence is a necessary implication of the simple DDM, which we introduce formally in the next section. The case of independence is by nature very knife-edge, and is natural to relax it. In this paper, we focus on qualitatively capturing a positive or a negative correlation between choices and time. To do this, we introduce the following definition.

Definition 2.

displays a speed-accuracy tradeoff iff is an increasing function of .

Note that this definition requires that the tradeoff holds for all times . We expect there to be a speed-accuracy tradeoff if the agent is learning about the options before her and is stopped by the experimenter at an exogenous stochastic time, as by waiting longer he obtains more information and can make more informed choices. But even if the agent is learning, the observed choice process need not display a choice-accuracy tradeoff if the stopping time is not exogenous but chosen by the agent as a function of what has been learned so far. In this case, the agent might stop sooner when she thinks his choice is likely to be accurate, so the choice of a stopping time may push towards the opposite side of the speed-accuracy tradeoff.

Definition 3.

displays a speed-accuracy complementarity iff is a decreasing function of .

A priori we could observe both kinds of , perhaps depending on the circumstances. This is indeed the case; for example, Swensson (1972) and Luce (1986) report that speed-accuracy complementarity is observed under normal conditions, but speed-accuracy tradeoff is observed when subjects are incentivized on speed; see also, Shadlen and Kiani (2013).999This could be explained if agents are stopping at random under time pressure, but are using some other rule under normal circumstances; for example they are following the uncertain-difference DDM, to be described in Section 3.3.

The speed-accuracy tradeoff can be equivalently expressed in terms of the monotone likelihood ratio property. Let be a choice process and let be the density of with respect to . Suppose that is absolutely continuous w.r.t. ; we say that and have the monotone likelihood ratio property, denoted , if the likelihood is an increasing function.

Though the above concepts will be useful for theoretical analysis, in empirical work time periods will need to be binned to get useful test statistics. For this reason we introduce two weaker concepts that are less sensitive to finite samples, as their oscillation is mitigated by conditioning on larger sets of the form . First, let be the probability of choosing conditional on stopping in the interval . Second, we say that first order stochastically dominates , denoted if for all . Below, we summarize the relationships between these concepts.

Fact 1.

-

1.

Let be a choice process and suppose that is absolutely continuous w.r.t. . Then displays the speed-accuracy tradeoff (complementarity/independence) if and only if ( / ).

-

2.

If displays a speed-accuracy tradeoff (complementarity, independence), then is an increasing (decreasing, constant) function

-

3.

If is an increasing (decreasing, constant) function, then (, ).

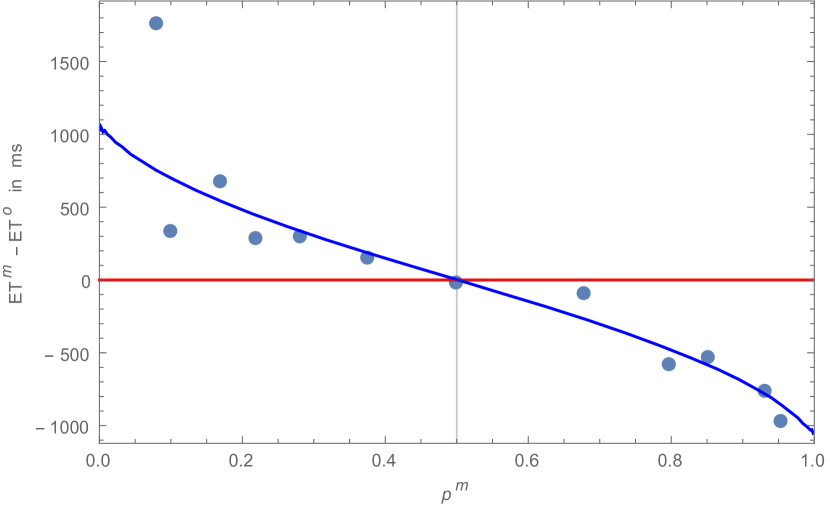

In particular, under speed-accuracy complementarity, the expected time to choose the modal alternative is smaller than the expected time to choose the other alternative, i.e., . Figure 1 shows that this fits the experimental data of Krajbich, Armel, and Rangel (2010).

The proof of Fact 1 and all other results is in the Appendix. In the next section of the paper we study a particular class of choice processes , called drift-diffusion models (DDM). Such models are defined by a signal process and a stopping boundary . We characterize the three subclasses of DDM: speed-accuracy tradeoff, complementarity, and independence in terms the function .

2.3 DDM representations

DDM representations have been widely used in the psychology and neuroscience literatures (Ratcliff and McKoon, 2008; Shadlen, Hanks, Churchland, Kiani, and Yang, 2006; Fehr and Rangel, 2011). The two main ingredients of a DDM are the stimulus process and a boundary .

The stimulus process is assumed to be a Brownian motion with drift and variance :

| (1) |

where is a standard Brownian motion. In early applications of DDM such as Ratcliff (1978) was is not observed by the experimenter. In some recent applications of DDM to neuroscience, the analyst may observe signals that are correlated with ; for example the neural firing rates of both single neurons (Hanes and Schall, 1996) and populations of them (e.g., Ratcliff, Cherian, and Segraves, 2003). In the later sections we interpret the process as a signal about the utility difference between the two alternatives.

Suppose that the agent stops at a fixed time and choose if and if (and flip a coin if there is a tie). Let be the frequency of the modal choice. It is easy to see that if then the modal choice is , and its probability is an increasing function of the exogenous stopping time : the process starts at , so if each choice is equally likely. At each subsequent point in time the distribution of is ; thus, the probability of increases. The same happens if the agent stops at a stochastic time that is independent of the process . Thus, an exogenously stopped process leads to a speed-accuracy tradeoff. We will now see that if the process is stopped endogenously, i.e., depending on its value, then this effect can be reversed.

The canonical example of a stopping time that depends on is the hitting time of a boundary. A boundary is a function . Define the hitting time

| (2) |

i.e., the first time the absolute value of the process hits the boundary. Let be the choice process induced by and a decision rule that chooses if and if .101010There are boundaries for which there is a positive probability that . This cannot happen for the primitive objects that we consider here, which are choice processes. Thus, we only focus on those boundaries that lead the agent to stop in finite tine with probability 1. This property will be satisfied in any model where the stopping time comes from a statistical decision problem in which never stopping incurs an infinite cost and the value of full information is finite.

Definition 4.

A choice process has a DDM representation () if . 111111Note that the parameter can be removed here by setting and . By a similar argument, can be assumed to be or . We nonetheless retain and here as we will use them in the next section to distinguish between utility and signal strength.

We note that the assumption that the process is Brownian is an important one, as without it the model is vacuous.

Fact 2.

Any choice process has a “DDM-like” representation where the stochastic process is arbitrary.

In particular an arbitrary may correspond to a process with jumps (or a filtration that is not right-continuous). However, the standard assumption in the literature is that is Brownian.121212For the Brownian motion Smith (2000) and Peskir et al. (2002) show that the distribution of hitting times satisfies a system of integral equations depending on the boundary. The inverse problem of finding a boundary such that the first hitting time has a given distribution was studied in Iscoe, Kreinin, and Rosen (1999) in the case Brownian Random walks and they propose a Monte Carlo algorithm for solving it numerically. The next result characterizes the relationship between speed and accuracy in the class of choice processes that admit a DDM representation.

Theorem 1.

Suppose that has a DDM representation . Then displays a speed-accuracy tradeoff (complementarity, independence) if and only if is increasing (decreasing, constant).

The intuition behind the proof of this theorem is as follows: Suppose that (so the modal action is ), that the barrier is decreasing, and that the process stopped at time . The odds that a modal decision is made in this situation are

where is the event that the process has not crossed the barrier before time . From Bayes rule and the formula for the density of the normal distribution

which is a decreasing function of whenever is. Moreover, a symmetry argument using the Brownian bridge shows that the conditioning event does not matter.

Theorem 1 says that the speed-accuracy tradeoff generated by exogenous stopping can be reversed if stopping is endogenous, i.e., the stopping time depends on the process .

The special case of the constant boundary DDM is well known to arise as the solution to an optimal sampling problem, for an agent who thinks there are only two possible states of the world. The next section presents that model in detail, and then focuses on a related model in which the agent is also learning about the intensity of her preference.

3 Optimal Stopping

3.1 Statement of the model

Both the simple DDM used to explain data from perception tasks and our uncertain-difference DDM are based on the idea of sequential learning and optimal stopping. As we will see, the models differ only in their prior, but this difference leads to substantially different predictions. In the learning model, the agent doesn’t know the true utilities, , but has a prior belief about them . The agent observes a signal which as in the DDM has the form of a drift plus a Brownian motion; in the learning model we assume that the drift of each is equal to the corresponding state, so that

| (3) |

where is the noisiness of the signal and the processes are independent.131313This process was also studied by Natenzon (2013) to study stochastic choice with exogenously forced stopping times; he allows utilities to be correlated, which can explain context effects. The signals and prior lie in a probability space where the information that the agent observed up to time is simply the paths We denote the agent’s posterior belief about given this information by . Let be the posterior mean for each . As long as the agent delays the decision she has to pay flow cost, which for now we assume to be constant . (Section 3.4 explores the implications of time varying cost.) The agent’s problem is to decide which option to take and at which time. Waiting longer will lead to more informed and thus better decisions, but also entails higher costs. What matters for this decision is the difference between the two utilities, so a sufficient statistic for the agent is

where is a Brownian Motion.

When the agent stops it is optimal to choose the option with the highest posterior expected value; thus, the value of stopping at time is . The agent decides optimally when to stop: he chooses a stopping time , i.e., a function such that for all ; let be the set of all stopping times. Hence, the problem of the agent at can be stated as

| (4) |

With the agent’s prior in hand, we can now define a subjective version of the relationship between speed and accuracy. Note that Definition 3 holds in a strong sense: For each possible value of the agent’s choices deteriorate over time. The following definition asks only that this is true on average, with respect to the subjective probability of the agent. Let be the probability of making the modal choice when the true state is and the agent stops at .

Definition 5.

displays a subjective speed-accuracy complementarity iff

is a decreasing function of .

Thus, under subjective speed-accuracy complementarity, the subjective probability of the agent of making a correct choice is a decreasing function of time.

3.2 Certain Difference

In the simple DDM the agent’s prior is concentrated on two points: and , where The agent receives payoff for choosing in state or in state and for choosing in state or in state , so she knows that the magnitude of the utility difference between the two choices is , but doesn’t know which action is better. We let denote the agent’s prior probability of

This model was first studied in discrete time by Wald (1947) (with a trade-off between type I and type II errors taking the place of utility maximization) and by Arrow, Blackwell, and Girshick (1949) in a standard dynamic programming setting. A version of the result for the continuous-time, Brownian-signal case can be found for example in Shiryaev (1969, 2007).

Theorem 2.

With a binomial prior, there is such that the minimal optimal stopping time is , where . Moreover, when , the optimal stopping time has a DDM representation with a constant boundary :

Theorems 1 and 2 imply that the simple DDM satisfies speed-accuracy independence and a fortiori subjective speed accuracy independence. From the point of view of most economic applications, the simple DDM misses an important feature, as the assumption that the agent knows the magnitude of the payoff difference rules out cases in which the agents is learning the intensity of his preference. At the technical level, the assumption that the utility difference is known, so there are only two states, implies that the current value of the process is a sufficient statistic, regardless of the elapsed time; this is why the stopping boundary in this model is constant. Intuitively, one might expect that if is close to zero and is large, the agent would infer that he is close to being indifferent between and and so stops, even though for the same value of the agent would choose to continue when is small. This inference is ruled out by the binomial prior, which says that the agent is sure that he is not indifferent. We now turn to a model with a Gaussian prior which makes such inferences possible.

3.3 Uncertain-difference DDM

In the uncertain-difference DDM, the agent’s prior is independent for each action and . Given the specification of the signal process (1), the posterior is , where

| (5) |

To gain intuition, consider the agent at time contemplating a strategy of waiting more seconds and stopping then. The agent’s utility of stopping now is . If the agent waits, he will have a more accurate belief and hence he will be able to make a more informed decision, but he will pay an additional cost, leading to an expected change in utility of . The main intuition for our results is that the value of the additional information gained per unit time is decreasing in , which leads to stopping regions being time-dependent.

The following theorem states this intuition formally.161616Time-dependent stopping thresholds also arise if the cost or utility functions are time-dependent or if there is a fixed terminal date, see e.g. Rapoport and Burkheimer (1971) and Drugowitsch, Moreno-Bote, Churchland, Shadlen, and Pouget (2012).

Theorem 3.

Let be the minimal optimal strategy in (4). Then

-

1.

There is a strictly decreasing, strictly positive such that

Moreover .

-

2.

If , there is a strictly positive such that

Part (1) of the theorem describes the optimal strategy in terms of stopping regions for posterior means : It is optimal for the agent to stop once the expected utility difference exceeds a decreasing threshold . This follows from the principle of optimality for continuous time processes and the shift invariance property of the value function, which is due to the normality of the posterior. Intuitively, if the expected utility difference is small for large , the agent concludes that the two items are most likely indifferent and since is small for large , the expected gain from learning more is low, so the agent stops. On the other hand, at even if the expected utility difference is small, is large so the expected value of learning is high and thus the agent continues.

Part (2) of the theorem describes the optimal strategy in terms of stopping regions for the signal process . This facilitates comparisons with the simple DDM, where the process of beliefs lives in a different space and is not directly comparable.

One way to understand the difference between this model and the one from the previous section is to consider the agent’s posterior beliefs when for large . In the certain difference model, the agent interprets the signal as noise, since according to his prior the utilities of the the two alternatives are a fixed distance apart, so the agent disregards the signal and essentially starts from anew. This is why the optimal boundaries are constant in this model. On the other hand, in the uncertain difference model the agent’s interpretation of for large is that the two alternatives are nearly indifferent, which prompts the agent to stop the costly information gathering process and make a decision right away. This is why the optimal boundaries are decreasing in this model.

We do not know of a closed-form solution for the functions and ; however, we can show that, as functions of the initial variance , , and noisiness , they have to satisfy the following conditions. The conditions provide useful information about the identification of the parameters of the model, and about how the predictions of the model change as the parameters are varied in experiments. They are also used to show that is Lipschitz continuous, which simplifies the analysis of the boundary value problem, and that it declines with time at rate at least , which is at the heart of the proof of Theorem 5 below.

Theorem 4.

The optimal solution to problem (4) is Lipschitz continuous in and satisfies:

| (6) | ||||

| (7) | ||||

| (8) | ||||

| (9) |

The first equality follows from the fact that an agent who starts at time 0 with prior , has the same beliefs at each time as an agent who started at time with prior This equality is used at various steps in the proofs, including showing that is Lipschitz continuous in , which is convenient for technical reasons; it allows us to ignore the complications of viscosity solutions and have an exact solution to the PDE that characterizes the optimal stopping rule. The proofs of equalities (7) and (8) use a space-time change. Inequality (9) follows from a space-time change argument and the fact that more information is always better for the agent.

Using the results of Bather (1962) we can characterize the functional form for that satisfies the above conditions with equality, and the that corresponds to it.

Fact 3.

Fact 3 implies that since declines to zero at rate , this implies that does too. Using numerical methods, we have found that and are good numerical approximations to the optimal boundaries and .171717The approximations obtained by Bather (1962) and Van Moerbeke (1974) show that ; however our simulations and the bounds from Fact 3 indicate that approximates the solution quite accurately, so it may be useful for estimation purposes.

Note that if is decreasing, like is, then by Theorem 1, any uncertain-difference DDM displays speed-accuracy complementarity. We have not been able to show this but we can show that the uncertain-difference DDM has the following weaker property:

Theorem 5.

The Gaussian DDM displays subjective speed-accuracy complementarity

This is true because the boundary is decreasing at the rate at least , which, as we show, follows from Theorem 4. This theorem implies that the analyst will observe a speed-accuracy complementarity in an experiment in which in the agent faces a series of decisions with states and the values of are drawn according to the agent’s prior. In particular, as long as the prior is correct, speed-accuracy complementarity will hold on average; i.e., it will hold for the average in a given experiment. In addition, we expect that the speed-accuracy complementarity should hold at least approximately if the agent’s beliefs are approximately correct but we have not shown this formally. Moreover, the complementarity can hold even across experiments as long as the distributions of the states (both objective and subjective) are close enough. That is, while we expect choice-accuracy complementarity to hold within a given class of decision problems, it need not hold across classes: if and are two apartments with a given utility difference , we expect the agent to spend on average more time here than on a problem where and are two lunch items with the same utility difference . This is because we expect the prior belief of the agent to be domain specific and in particular, the variance of the prior, , to be higher for houses than for lunch items. Similarly, the complementarity can hold across subjects (indeed, the data in Figure 1 is a cross-section of subjects), as long as their boundaries are not too different; in the extreme case when one subject has a cost much lower than another subject, the first one will make choices which are longer and more accurate than the choices of the second subject.

Finally, we note that the uncertain difference model is equivalent to the Chernoff (1961) ex post regret model, where for any stopping time the objective function is

that is, the agent gets zero for making the correct choice and is penalized the foregone utility for making the wrong choice.

Fact 4.

For any stopping time

where is a constant independent of ; therefore, these two objective functions induce the same choice process.

Chernoff and following authors have focused on the behavior of the optimal boundary for very small and very large values of . Lai and Lim (2005) say that Chernoff’s heuristic arguments can be adapted to provide a rigorous proof that the boundary converges to zero, but do not provide details. Moreover, we have not found any relevant monotonicity results in this literature.

3.4 Non-Linear Cost

In deriving the DDM representation from optimal stopping, we have so far have assumed that the cost of continuing per unit time is constant. We have seen that in the uncertain-difference model, the optimal boundary decreases due to the fact there is less to learn as time goes on. One would expect that the boundary could increase if costs decrease sufficiently quickly. This raises the question of which DDM representations can be derived as a solution to an optimal stopping problem when the cost is allowed to vary arbitrarily over time. The next result shows that for any boundary there exists a cost function such that the boundary is optimal in the learning problem with normal or binomial priors. Thus optimal stopping on its own imposes essentially no restrictions on the observed choice process; the force of the model derives from its joint assumptions about the evolution of beliefs and the cost function.

Theorem 6.

Consider either the Certain or the Uncertain-Difference DDM. For any finite boundary and any finite set there exists a cost function such that is optimal in the set of stopping times that stop in with probability one

In particular, there is a cost function such that the exponentially decreasing boundaries in Milosavljevic, Malmaud, Huth, Koch, and Rangel (2010b) are optimal, and a cost function such that there is speed-accuracy independence.

Intuitively, the reason this result obtains is that the optimal stopping rule always takes the form of a cut-off: If the agent stops at time when , she stops at time whenever This allows us to recursively construct a cost function that rationalizes the given boundary by setting the cost at time equal the expected future gains from learning. To avoid some technical issues having to do with the solutions to PDE’s, we consider a discrete-time finite-horizon formulation of the problem, where the agent is only allowed to stop at times in a finite set . This lets us construct the associated cost function period by period instead of using smoothness conditions and stochastic calculus.181818The proof of the theorem relies on a result on implementable stopping times from Kruse and Strack (2015). In another paper Kruse and Strack (2014) generalize this result to continuous time, but as the absolute value is not covered by their result we can not use it here. Nevertheless, we conjecture that the methods used in that paper can be extended to prove the result in continuous time directly.

4 Conclusion

The recent literature in economics and cognitive science uses drift-diffusion models with time-dependent boundaries. This is helpful in matching observed properties of reaction times, notably their correlation with chosen actions, and in particular a phenomenon that we call speed-accuracy complementarity, where earlier decisions are better than later ones. In Section 2 we showed that the monotonicity properties of the boundary characterize whether the observed choice process displays a speed-accuracy complementarity, or the opposite pattern of a speed-accuracy tradeoff. This ties an observable property of behavior (the correlation between reaction times and decisions) to an unobservable construct of the model (the boundary). This connection is helpful for understanding the qualitative properties of DDMs; it may also serve as a useful point of departure for future quantitative exploration of the connection between the rate of decline of the boundary and the strength of correlation between reaction times and actions.

In Section 3 we investigated the DDM as a solution to the optimal sequential sampling problem, where the agent is unsure about the utility of each action and is learning about it as the time passes, optimally deciding when to stop. We studied the dependence of the solution on the nature of the learning problem and also on the cost structure. In particular, we proposed a model in which the agent is learning not only about which option is better, but also by how much it is better. We showed that the boundary in this model declines to zero at the rate . We also showed that any boundary could be optimal if the agent is facing a nonlinear cost of time.

The analysis of our paper provides a precise foundation for DDMs with time-varying boundaries and establishes a set of useful connections between various parameters of the model and predicted behavior, thus enhancing the theoretical understanding of the model as well as making precise its empirical content. We expect the forces identified in this paper to be present in other decisions involving uncertainty: not just in tasks used in controlled laboratory experiments, but also in decisions involving longer time scales, such as choosing an apartment rental, or deciding which papers to publish (as a journal editor). We hope these results will be a helpful stepping stone for further work.

Appendix: Proofs

Appendix A General Results

A.1 Proof of Fact 1

Proof of Fact 1: To prove part (1) note that by the definition of a conditional distribution (property (c) p. 343 of Dudley, 2002) we have , so the density of is . Since is absolutely continuous w.r.t. , the ratio is well defined -almost everywhere and equals . This expression is increasing (decreasing, constant) if and only if is increasing (decreasing, constant).

To prove part (2), note that by the definition of a conditional distribution we have

| (12) |

Thus, for we have

which is true if is a decreasing function since the LHS is the average of on and the RHS is the average on . However, the opposite implication may not hold, for example, consider and for . Then is not decreasing, but is.

To prove part (3), note that by (12) we have

where we used the fact that and . Thus, if is a decreasing function, the RHS will hold. However, the opposite obviously doesn’t have to hold.∎

A.2 Proof of Fact 2

Let be a Borel probability measure on . Define the process as follows. For any let

Note that is Borel measurable for each , so is a stochastic process on the probability space . Set and observe that is a DDM-like representation of .

Note that a representation with continuous paths is possible, where

however, in this representation the filtration generated by is not right-continuous at zero. ∎

A.3 Proof of Theorem 1

Let be the density of the distribution of stopping times, and be the density of i.e

where is the density of the standard normal. By Bayes rule:

It follows from and the symmetry of the upper and the lower barrier that

| (13) |

because for any path of that ends at and crosses any boundary before , the reflection of this path ends at and crosses some boundary at the same time.

The induced probability measure over paths conditional on is the same as the probability of the Brownian Bridge.191919See, e.g., Proposition 12.3.2 of Dudley (2002) or Exercise 3.16, p. 41 of Revuz and Yor (1999). The Brownian Bridge is the solution to the SDE and notably does not depend on the drift , which implies that

| (14) |

Thus, by (13) and (14) we have that

Wlog and ; the above expression is decreasing over time if and only if is decreasing over time. ∎

Appendix B The Uncertain-Difference Model

B.1 The Value Function

Our results use on the following representation of the posterior process in the uncertain-difference model.

Lemma 1.

For any

where is a Brownian motion with respect to the filtration information of the agent.

Proof: This follows from Theorem 10.1 and equation 10.52 of Liptser and Shiryaev (2001) by setting and . ∎

Define the continuation value as the expected value an agent can achieve by using the optimal continuation strategy if he beliefs the posterior means to be at time and the variance of his prior equaled at time 0 and the noisiness of the signal is .

Lemma 2.

The continuation value has the following properties:

-

1.

-

2.

for every

-

3.

The option value is decreasing in for .

-

4.

is increasing in and

-

5.

The continuation value is Lipschitz continuous in and .

Proof of Lemma 2

In this proof we equivalently represent a continuation strategy by a pair of stopping times , one for each alternative.

Proof of 1: For the lower bound, the agent can always stop immediately and get or . For the upper bound, the agent can’t do better than receiving a fully informative signal right away and pick the better item immediately.

Proof of 2: Fix a continuation strategy ; the expected payoff equals

Intuitively, this comes from the translation invariance of the Brownian

motion, i.e., the distribution of conditional on is

the same as the distribution of conditional on . As

is defined as the supremum over all continuation strategies

the result follows.

Proof of 3: The expected difference between stopping at time with option and using the continuation strategy is

Note that the first part is independent of , and

is weakly decreasing in . As for every fixed strategy

the value of waiting is decreasing the supremum over all continuation

strategies is also weakly decreasing in Thus it follows that the

difference between continuation value

and value of stopping immediately on the first arm is decreasing in for every and every .

Proof of 4: The expected value of using the continuation strategy equals

which is weakly increasing in . Consequently, the supremum over all

continuation strategies is weakly increasing in . By

the same argument it follows that is

increasing in

Proof of 5: The following argument establishes that the value function is Lipschitz continuous with constant one. The initial belief about the mean of either option is additively separable from the change in belief caused by the information the agent observed after time zero. Thus changing the initial beliefs moves the posterior beliefs linearly. Hence, for any fixed stopping time the change in initial belief can at most linearly move the posterior beliefs about the mean. Furthermore, the expected cost are unaffected by a change in prior beliefs. Thus, the supremum over all stopping times can at most be linearly affected by a change in initial belief. To see this explicitly, observe that

B.2 Proof of Theorem 3

B.2.1 Characterization

Note that due to the symmetry of the problem Without loss of generality suppose otherwise swap and . As is a Markov process, the principle of optimality202020Our model does not satisfy condition (2.1.1) of Peskir and Shiryaev (2006) because for some stopping times the expected payoff is minus infinity, but as they indicate on p. 2 the proof can be extended to our case. implies that the agent’s problem admits a solution of the form . Thus, it is optimal to stop if and only if

An envelope argument yields that is continuous. Using the continuity and the monotonicity of we can define the function implicitly by

As , is monotone increasing in the second argument and by Lemma 2 we have

Hence the optimal strategy equals

B.2.2 Monotonicity

First, we show that is decreasing in . Note that by Doob’s optional sampling theorem for every fixed stopping strategy

Define the process , and note that

| (15) |

where is a Brownian motion. Define a time change as follows: Let solve This implies that . Define . By the Dambis, Dubins–Schwarz theorem (see, e.g., Theorem 1.6, chapter V of Revuz and Yor, 1999) is a Brownian motion and thus we can rewrite the problem as

Next, we remove the conditional expectation in the Brownian motion by adding the initial value

Define and let wlog , then

because the current state is a sufficient statistic for Brownian motion we have

Note that for every fixed strategy the cost term is increasing in and and thus is non-increasing.

B.2.3 Positivity

The payoff of the optimal decision rule is at least as high as the payoff from using the strategy that stops at time for sure. Because the information gained over a short time period is of order and the cost is linear, we expect that it is always worth buying some information when the expected utility of both options is the same. To see this formally, note that

As the first term goes to zero with the speed of square root while the second term shrinks linearly we get that for some small and thus the agent does not stop when his posterior mean is the same on both options.

B.2.4 Zero limit

Let for all . Consider the time history where . The probability that the agent never stops (and thus pays infinity costs) is bounded from below by the probability that the process stays in the interval ,

By the above time change argument this equals the probability that a Brownian motion leaves the interval in the time from to ,

This probability is non-zero. Thus, there is a positive probability the agent incurs infinite cost. Because the expected gain is bounded by the full information payoff, this is a contradiction. ∎

B.3 Proof of Theorem 4

Lemma 3.

Proof: We have that equals

For the step from the second to third line apply Proposition 1.4 of Chapter V of Revuz and Yor (1999) with and (pathwise to the integrals with limits and . In the next step we apply a time-change, where is a Brownian motion and is a stopping time measurable in the natural filtration generated by . ∎

B.3.1 Proof of (6)

Note that Lemma 1 implies that for any

where is a Brownian motion with respect to the filtration information of the agent. Thus, if the agent starts with a prior at time 0 equal to , then his belief at time is exactly the same as if he started with a prior at equal to where . Thus, so

B.3.2 Proof of (7)

B.3.3 Proof of (8)

First, observe that equals

Thus,

B.3.4 Proof of (9)

By Lemma 3, equals

As receiving more information is always better we have that for all

This implies that for all

B.3.5 Lipschitz continuity of

Let and note that by definition . We can thus use equations (6), (7) and (9) to get

As a consequence we can bound the difference between the value of the barrier at time zero and at time from below

Dividing by and taking the limit yields that the partial derivative of the boundary with respect to time satisfies

Since by equation (6) we have that

where the last equality follows from equation (6) and the last inequality follows since and are decreasing in . Thus, is bounded from below; since its upper bound is zero, is Lipschitz continuous in . ∎

B.4 Proof of Theorem 5

If the agent stops at time at the barrier his posterior belief is that the true states are normally distributed with . Thus,the probability that the agent assigns to picking when is optimal, conditional on stopping at , is

From the symmetry of the problem, there is the same probability of mistakenly picking instead of . To show that the probability of being wrong increases over time, it remains to show that is decreasing in . We have that

We will now show that this is equal to , which is nonnegative. To see that, we show that . Set

Inserting in equation. (7) gives

Dividing by and taking the limit yields

B.5 Proof of Fact 4

Let and fix a stopping time . To show that

the cost terms can be dropped. Let be the difference between the expected payoff from the optimal decision and the expected payoff from choosing the correct action, . By decomposing the expectation into two events,

| Plugging in the definition of and using the law of iterated expectations, | ||||

B.6 Proof of Fact 3

We rely on Bather’s (1962) analysis of the Chernoff model, which by Fact 4 applies to our model. Bather studies a model with zero prior precision. Since such an agent never stops instantaneously, all that matters is his beliefs at , which are well defined even in this case, and given by and . In Section 6, p. 619 Bather (1962) shows that

| which implies that | ||||

Fix . By equation (8) we have . Thus,

This implies that there exists such that for all we have

Fix and let . This way, the agent who starts with zero prior precision and waits seconds has the same posterior precision as the agent who starts with and waits seconds.212121To see this, observe that . Thus, by (6) we have , so

Finally, since , we have

B.7 Proof of Theorem 6

Let be a finite set of times at which the agent is allowed to stop and denote by all stopping times such that almost surely. As we restrict the agent to stopping times in , the stopping problem becomes a discrete time optimal stopping problem. By Doob’s optional sampling theorem we have that

so any optimal stopping time also solves . Define for all . Observe that is a one-dimensional discrete time Markov process. To prove that for every barrier there exists a cost function which generates by Theorem 1 in Kruse and Strack (2015) it suffices to prove that:

-

1.

there exists a constant such that .

-

2.

is increasing in in the sense of first order stochastic dominance

-

3.

is strictly decreasing in

Condition 1 keeps the value of continuing from exploding, which would be inconsistent with a finite boundary. Conditions 2 and 3 combined ensure that the optimal policy is a cut-off rule.

B.7.1 Certain-Difference DDM

Set . Then

Denote by the posterior probability that is the better choice. The expected absolute difference of the two choices satisfies

Let denote the change in the signal from to . We have that the log likelihood is given by . We thus have

| (16) |

(1): It is easily seen that , so for big enough, .

(2): To simplify notation we introduce . The process is Markov. More precisely, is folded

normal with mean of the underlying normal distribution equal to

| (17) |

and variance

As argued in part (2) of the uncertain difference case, a folded normal

random variable increases in the sense of first order stochastic dominance

in the mean of the underlying normal distribution. As (17) increases in it follows that

increases in in the sense of first order stochastic dominance. By (16) is increasing in

and is increasing in this completes the

argument.

(3): It remains to show that is decreasing in . As is a martingale, and moreover

conditioning on is equivalent to conditioning on we have that

As is a martingale we can replace by

The above term is strictly decreasing in as increases in the sense of first order stochastic dominance in and in the conditional expectation is increasing in .

B.7.2 Uncertain-Difference DDM

Let us further define . As is Normal distributed with variance and mean we have that is folded normal distributed with mean

where denotes the normal cdf. Thus, the expected change in delta is given by

(1): It is easily seen that .

(2): As is folded normal distributed we have that

Taking derivatives gives that

As it follows that and

hence, is increasing in in the sense of first

order stochastic dominance.

(3): The derivative of the expected change of the process equals

Hence, is strictly decreasing in .∎

References

- (1)

- Arrow, Blackwell, and Girshick (1949) Arrow, K., D. Blackwell, and M. Girshick (1949): “Bayes and minimax solutions of sequential decision problems,” Econometrica, 17, 213–244.

- Ballinger and Wilcox (1997) Ballinger, T. P., and N. T. Wilcox (1997): “Decisions, error and heterogeneity,” The Economic Journal, 107(443), 1090–1105.

- Bather (1962) Bather, J. A. (1962): “Bayes procedures for deciding the sign of a normal mean,” in Mathematical Proceedings of the Cambridge Philosophical Society, vol. 58, pp. 599–620. Cambridge Univ Press.

- Bogacz, Brown, Moehlis, Holmes, and Cohen (2006) Bogacz, R., E. Brown, J. Moehlis, P. Holmes, and J. D. Cohen (2006): “The physics of optimal decision making: a formal analysis of models of performance in two-alternative forced-choice tasks.,” Psychological review, 113(4), 700.

- Busemeyer and Johnson (2004) Busemeyer, J. R., and J. G. Johnson (2004): “Computational models of decision making,” Blackwell handbook of judgment and decision making, pp. 133–154.

- Cheremukhin, Popova, and Tutino (2011) Cheremukhin, A., A. Popova, and A. Tutino (2011): “Experimental evidence on rational inattention,” Federal Reserve Bank of Dallas Working Paper, 1112.

- Chernoff (1961) Chernoff, H. (1961): “Sequential tests for the mean of a normal distribution,” in Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability, vol. 1, pp. 79–91. Univ of California Press.

- Churchland, Kiani, and Shadlen (2008) Churchland, A. K., R. Kiani, and M. N. Shadlen (2008): “Decision-making with multiple alternatives,” Nature neuroscience, 11(6), 693–702.

- Clithero and Rangel (2013) Clithero, J. A., and A. Rangel (2013): “Combining Response Times and Choice Data Using A Neuroeconomic Model of the Decision Process Improves Out-of-Sample Predictions,” mimeo.

- Ditterich (2006) Ditterich, J. (2006): “Stochastic models of decisions about motion direction: behavior and physiology,” Neural Networks, 19(8), 981–1012.

- Drugowitsch, Moreno-Bote, Churchland, Shadlen, and Pouget (2012) Drugowitsch, J., R. Moreno-Bote, A. K. Churchland, M. N. Shadlen, and A. Pouget (2012): “The cost of accumulating evidence in perceptual decision making,” The Journal of Neuroscience, 32(11), 3612–3628.

- Dudley (2002) Dudley, R. M. (2002): Real analysis and probability, vol. 74. Cambridge University Press.

- Edwards (1965) Edwards, W. (1965): “Optimal strategies for seeking information: Models for statistics, choice reaction times, and human information processing,” Journal of Mathematical Psychology, 2(2), 312–329.

- Fehr and Rangel (2011) Fehr, E., and A. Rangel (2011): “Neuroeconomic foundations of economic choice—recent advances,” The Journal of Economic Perspectives, 25(4), 3–30.

- Gabaix and Laibson (2005) Gabaix, X., and D. Laibson (2005): “Bounded rationality and directed cognition,” Harvard University.

- Hanes and Schall (1996) Hanes, D. P., and J. D. Schall (1996): “Neural control of voluntary movement initiation,” Science, 274(5286), 427–430.

- Hey (1995) Hey, J. D. (1995): “Experimental investigations of errors in decision making under risk,” European Economic Review, 39(3), 633–640.

- Hey (2001) (2001): “Does repetition improve consistency?,” Experimental economics, 4(1), 5–54.

- Iscoe, Kreinin, and Rosen (1999) Iscoe, I., A. Kreinin, and D. Rosen (1999): “An integrated market and credit risk portfolio model,” Algo Research Quarterly, 2(3), 21–38.

- Ke, Shen, and Villas-Boas (2013) Ke, T., Z.-J. M. Shen, and J. M. Villas-Boas (2013): “Search for Information on Multiple Products,” Discussion paper, Working paper, University of California, Berkeley.

- Krajbich, Armel, and Rangel (2010) Krajbich, I., C. Armel, and A. Rangel (2010): “Visual fixations and the computation and comparison of value in simple choice,” Nature neuroscience, 13(10), 1292–1298.

- Krajbich, Lu, Camerer, and Rangel (2012) Krajbich, I., D. Lu, C. Camerer, and A. Rangel (2012): “The attentional drift-diffusion model extends to simple purchasing decisions,” Frontiers in psychology, 3, 193.

- Krajbich and Rangel (2011) Krajbich, I., and A. Rangel (2011): “Multialternative drift-diffusion model predicts the relationship between visual fixations and choice in value-based decisions,” Proceedings of the National Academy of Sciences, 108(33), 13852–13857.

- Kruse and Strack (2014) Kruse, T., and P. Strack (2014): “Inverse Optimal Stopping,” arXiv preprint arXiv:1406.0209.

- Kruse and Strack (2015) (2015): “Optimal stopping with private information,” forthcoming in Journal of Economic Theory.

- Lai and Lim (2005) Lai, T. L., and T. W. Lim (2005): “Optimal stopping for Brownian motion with applications to sequential analysis and option pricing,” Journal of statistical planning and inference, 130(1), 21–47.

- Laming (1968) Laming, D. R. J. (1968): Information theory of choice-reaction times. Academic Press.

- Link and Heath (1975) Link, S., and R. Heath (1975): “A sequential theory of psychological discrimination,” Psychometrika, 40(1), 77–105.

- Liptser and Shiryaev (2001) Liptser, R. S., and A. Shiryaev (2001): “Statistics of stochastic processes,” Springer-Verlag, 1.

- Lu (2013) Lu, J. (2013): “Random Choice and Private Information,” Working paper, Princeton University.

- Luce (1986) Luce, R. D. (1986): Response times. Oxford University Press.

- Milosavljevic, Malmaud, Huth, Koch, and Rangel (2010a) Milosavljevic, M., J. Malmaud, A. Huth, C. Koch, and A. Rangel (2010a): “The drift diffusion model can account for value-based choice response times under high and low time pressure,” Judgement & Decision Making, 5, 437–449.

- Milosavljevic, Malmaud, Huth, Koch, and Rangel (2010b) (2010b): “The drift diffusion model can account for value-based choice response times under high and low time pressure,” Judgement & Decision Making, 5, 437–449.

- Natenzon (2013) Natenzon, P. (2013): “Random choice and learning,” Working paper, University of Washington.

- Peskir et al. (2002) Peskir, G., et al. (2002): “On integral equation arising in the first-passage problem for Brownian motion,” Journal Integral Equations and Applications, 14, 397–423.

- Peskir and Shiryaev (2006) Peskir, G., and A. Shiryaev (2006): Optimal stopping and free-boundary problems. Springer.

- Rand, Greene, and Nowak (2012) Rand, D. G., J. D. Greene, and M. A. Nowak (2012): “Spontaneous giving and calculated greed,” Nature, 489(7416), 427–430.

- Rapoport and Burkheimer (1971) Rapoport, A., and G. J. Burkheimer (1971): “Models for deferred decision making,” Journal of Mathematical Psychology, 8(4), 508–538.

- Ratcliff (1978) Ratcliff, R. (1978): “A theory of memory retrieval.,” Psychological review, 85(2), 59.

- Ratcliff, Cherian, and Segraves (2003) Ratcliff, R., A. Cherian, and M. Segraves (2003): “A comparison of macaque behavior and superior colliculus neuronal activity to predictions from models of two-choice decisions,” Journal of neurophysiology, 90(3), 1392–1407.

- Ratcliff and McKoon (2008) Ratcliff, R., and G. McKoon (2008): “The diffusion decision model: Theory and data for two-choice decision tasks,” Neural computation, 20(4), 873–922.

- Reutskaja, Nagel, Camerer, and Rangel (2011) Reutskaja, E., R. Nagel, C. F. Camerer, and A. Rangel (2011): “Search dynamics in consumer choice under time pressure: An eye-tracking study,” The American Economic Review, 101(2), 900–926.

- Revuz and Yor (1999) Revuz, D., and M. Yor (1999): Continuous martingales and Brownian motion, vol. 293. Springer.

- Rubinstein (2007) Rubinstein, A. (2007): “Instinctive and cognitive reasoning: A study of response times,” The Economic Journal, 117(523), 1243–1259.

- Shadlen, Hanks, Churchland, Kiani, and Yang (2006) Shadlen, M. N., T. D. Hanks, A. K. Churchland, R. Kiani, and T. Yang (2006): “The speed and accuracy of a simple perceptual decision: a mathematical primer,” Bayesian brain: Probabilistic approaches to neural coding, pp. 209–37.

- Shadlen and Kiani (2013) Shadlen, M. N., and R. Kiani (2013): “Decision Making as a Window on Cognition,” Neuron, 80(3), 791–806.

- Shiryaev (1969) Shiryaev, A. N. (1969): Optimal stopping rules. Russian Edition published by Nauka.

- Shiryaev (2007) (2007): Optimal stopping rules. Springer.

- Smith (2000) Smith, P. L. (2000): “Stochastic dynamic models of response time and accuracy: A foundational primer,” Journal of mathematical psychology, 44(3), 408–463.

- Stone (1960) Stone, M. (1960): “Models for choice-reaction time,” Psychometrika, 25(3), 251–260.

- Swensson (1972) Swensson, R. G. (1972): “The elusive tradeoff: Speed vs accuracy in visual discrimination tasks,” Perception & Psychophysics, 12(1), 16–32.

- Van Moerbeke (1974) Van Moerbeke, P. (1974): “Optimal stopping and free boundary problems,” Rocky. Mountain. J. Math, 4(539-578).

- Vul, Goodman, Griffiths, and Tenenbaum (2014) Vul, E., N. Goodman, T. L. Griffiths, and J. B. Tenenbaum (2014): “One and done? Optimal decisions from very few samples,” Cognitive science, 38(4), 599–637.

- Wald (1947) Wald, A. (1947): Sequential analysis. John Wiley & Sons.

- Woodford (2014) Woodford, M. (2014): “An Optimizing Neuroeconomic Model of Discrete Choice,” Discussion paper, National Bureau of Economic Research.