Bayesian inference for Gaussian graphical models beyond decomposable graphs

Abstract

Bayesian inference for graphical models has received much attention in the literature in recent years. It is well known that when the graph is decomposable, Bayesian inference is significantly more tractable than in the general non-decomposable setting. Penalized likelihood inference on the other hand has made tremendous gains in the past few years in terms of scalability and tractability. Bayesian inference, however, has not had the same level of success, though a scalable Bayesian approach has its respective strengths, especially in terms of quantifying uncertainty. To address this gap, we propose a scalable and flexible novel Bayesian approach for estimation and model selection in Gaussian undirected graphical models. We first develop a class of generalized -Wishart distributions with multiple shape parameters for an arbitrary underlying graph. This class contains the -Wishart distribution as a special case. We then introduce the class of Generalized Bartlett (GB) graphs, and derive an efficient Gibbs sampling algorithm to obtain posterior draws from generalized -Wishart distributions corresponding to a GB graph. The class of Generalized Bartlett graphs contains the class of decomposable graphs as a special case, but is substantially larger than the class of decomposable graphs. We proceed to derive theoretical properties of the proposed Gibbs sampler. We then demonstrate that the proposed Gibbs sampler is scalable to significantly higher dimensional problems as compared to using an accept-reject or a Metropolis-Hasting algorithm. Finally, we show the efficacy of the proposed approach on simulated and real data.

Keywords: Gaussian graphical models, Gibbs sampler, Generalized Bartlett graph, Generalized G-Wishart distribution, Scalable Bayesian inference

1 Introduction

Gaussian graphical models have found widespread use in many application areas. Besides standard penalized likelihood based approaches (see Khare et al. (2015) and references therein), Bayesian methods have also been proposed in the literature for analyzing undirected Gaussian graphical models (see Asci and Piccioni, 2007; Dawid and Lauritzen, 1993; Letac and Massam, 2007; Mitsakakis et al., 2011; Rajaratnam et al., 2008; Roverato, 2000, 2002; Wang and Carvalho, 2010, to name just a few). Bayesian methods have the distinct and inherent advantage that they can incorporate prior information and yield a full posterior for the purposes of uncertainty quantification (and not just a point estimate), whereas standard frequentist approaches for uncertainty quantification (such as the bootstrap) may be computationally burdensome and/or break down in high dimensional settings. However, it is well known that Bayesian methods for graphical models in high dimensional settings lag severely behind their regularized likelihood based counterparts, in the sense that they are not scalable except under restrictive assumptions on the underlying sparsity pattern (such as for decomposable graphs). Hence a scalable and more general approach to graphical models, with theoretical and computational safeguards, is critical to leveraging the advantages of posterior inference.

To outline the issues with current Bayesian methods more clearly, consider i.i.d. vectors drawn from a -variate normal distribution with mean vector and a sparse inverse covariance matrix . The sparsity pattern in can be encoded in terms of a graph on the set of variables as follows. If the variables and do not share an edge in , then . Hence, an undirected (or concentration) graphical model corresponding to restricts the inverse covariance matrix to a submanifold of the cone of positive definite matrices (referred to as ). A Bayesian statistical analysis of these models requires specification of a prior distribution (supported on ) for . Dawid and Lauritzen (1993) introduced a class of prior distributions for called the Hyper Inverse Wishart (HIW) distributions. The induced class of prior distributions for (supported on ) is known as the class of -Wishart distributions (see Roverato (2000)). This class of prior distributions is quite useful and popular, and has several desirable properties, including the fact that it corresponds to the Diaconis-Ylvisaker class of conjugate priors for the concentration graph model corresponding to the graph .

Closed form computations of relevant quantities corresponding to the -Wishart distribution, such as expected value of the precision matrix and quantiles, are in general available only if the underlying graph is decomposable, i.e., does not have any induced cycle of length greater than or equal to 4. A variety of approaches have been developed in the literature to generate samples from the -Wishart distribution corresponding to a general non-decomposable graph. Asci and Piccioni (2007) have developed a maximal clique based Markov Chain Monte Carlo (MCMC) approach to sample from the -Wishart distribution corresponding to a general graph . Lenkoski (2013) develops a direct sampler for -Wishart distributions corresponding to a general graph . This approach uses an iterative algorithm to minimize an objective function over the space of positive definite matrices with appropriate sparsity constraints. Wang and Carvalho (2010) have developed an accept-reject algorithm to generate direct samples from the -Wishart distribution corresponding to a general graph . Mitsakakis et al. (2011) have developed a Metropolis-Hastings based MCMC approach for the same.

While the -Wishart prior is clearly very useful for Bayesian inference in graphical models, it has an important drawback. In particular, the -Wishart distribution has only one shape parameter, which makes it potentially inflexible and restrictive in terms of prior specification. Letac and Massam (2007) address this issue by constructing the so-called and families of distributions which are flexible in the sense that they have multiple shape parameters. These distributions include the -Wishart as a special case, and form a standard conjugate family of prior distributions for undirected decomposable graphical models. The construction of the Letac and Massam distributions uses the structure associated with decomposable graphs. It would thus be useful to develop a class of prior distributions which is flexible (multiple shape parameters) and leads to tractable Bayesian inference for non-decomposable graphs.

In this paper, we aim to develop a scalable and flexible Bayesian approach for estimation and model selection in Gaussian undirected graphical models for general graphs. Our approach preserves the attractive properties of previous approaches, while overcoming their drawbacks. We first develop a class of generalized -Wishart distributions (for an arbitrary underlying graph), which has multiple shape parameters and contains the -Wishart distributions as a special case. These distributions form a family of standard conjugate prior distributions for Gaussian concentration graph models. Developing methods for efficient posterior draws from generalized -Wishart distributions is crucial for scalable Bayesian inference. We proceed to introduce the class of Generalized Bartlett (GB) graphs, and derive an efficient Gibbs sampling algorithm (with Gaussian or GIG conditionals) to simulate from generalized -Wishart distributions corresponding to a GB graph. The class of Generalized Bartlett graphs contains decomposable graphs as a special case, but is substantially larger than the class of decomposable graphs. For example, any cycle of length greater than is Generalized Bartlett, but is not decomposable. Our approach has the flexibility of using multiple shape parameters (as opposed to the single parameter -Wishart), but goes beyond the class of decomposable graphs without losing tractability.

For the generalized -Wishart case, the conditional densities for any maximal clique of are intractable to sample from. Hence, the sampling approaches in (Asci and Piccioni, 2007; Lenkoski, 2013) for -Wisharts on a general graph do not extend to the generalized -Wishart. On the other hand, we show that the accept-reject and Metropolis-Hastings based methods in Wang and Carvalho (2010) and Mitsakakis et al. (2011) can be easily extended to the generalized -Wishart case. We compare the performance and scalability of these two approaches with our Gibbs sampler in Section 7.2.1 and Section 7.2.2.

The rest of the paper is organized as follows. Section 2 contains a brief overview of relevant concepts from graph theory and matrix theory. In Section 3 and Section 4, we define generalized -Wishart distributions and GB graphs respectively, and establish some basic properties. In Section 5, we derive a tractable Gibbs sampling algorithm to simulate from the generalized -Wishart distribution corresponding to a GB graph. Section 6 provides additional examples and properties of GB graphs. Section 7 contains a comprehensive simulation and real data analysis study for the Bayesian approach developed in the paper. The proofs of most of the technical results in the paper and additional numerical work are provided in the Supplemental Document.

2 Preliminaries

2.1 Graph theoretic preliminaries

For any positive integer , let . Let denote an undirected graph, where represents the finite vertex set and denotes the corresponding edge set. A function is defined to be an ordering of if is a bijection from to . An undirected graph and an ordering of can be used to construct an ordered graph , where if and only if .

Definition 1.

An undirected graph is called decomposable if it does not have a cycle of length greater than or equal to as an induced subgraph.

Such graphs are also called triangulated, or chordal graphs. A useful concept associated to decomposable graphs is that of a perfect elimination ordering (see Lauritzen (1996)).

Definition 2.

An ordering for an undirected graph is defined to be a perfect elimination ordering if for each , the set forms a clique.

In fact, an undirected graph is decomposable if and only if it has a perfect elimination ordering (see Paulsen et al. (1989)).

Definition 3.

For a given undirected graph , is called a decomposable cover of if is decomposable and .

Decomposable covers are also known as triangulations in graph theory literature (see Parraal and Schefflerb (1997)).

2.2 Matrix theoretic preliminaries

We denote the set of symmetric matrices by , and the space of positive definite symmetric matrices by . Given an ordered graph , we define

and

The space is a submanifold of the space of positive definite matrices, where the elements are restricted to be zero whenever the corresponding edge is missing from . Similarly the space is a subspace of lower triangular matrices with diagonal entries equal to , such that the elements in the lower triangle are restricted to be zero whenever the corresponding edge is missing from .

A positive definite matrix can be uniquely expressed as , where is a lower triangular matrix with diagonal entries equal to , and is a diagonal matrix with positive diagonal entries. Such a decomposition is known as the modified Cholesky decomposition of (see for example Daniels and Pourahmadi (2002)). Paulsen et al. (1989) showed that if , then if and only if is decomposable and is a perfect elimination ordering. If either of these two conditions is violated, then the sparsity pattern in is a strict subset of the sparsity pattern in . The entries (with ) such that is not (functionally) zero, are known as “fill-in” entries. The problem of finding an ordering which minimizes the number of fill-in entries is well-known and well-studied in numerical analysis and in computer science/discrete mathematics. Although this problem is NP-hard, several effective greedy algorithms for reducing the number of fill-in entries have been developed and implemented in standard software such as MATLAB and R (see Davis (2006) for instance).

In subsequent sections, we will consider a reparametrization from (the inverse covariance) matrix to its modified Cholesky decomposition. Such a reparametrization inherently assumes an ordering of the variables. In many applications (such as longitudinal data), a natural ordering is available. In the absence of a natural ordering, one can choose a fill-reducing ordering using one of the available fill-reducing algorithms mentioned previously. We will see that a fill-reducing ordering will help in reducing the computational complexity of proposed Markov chain Monte Carlo procedures.

2.3 Undirected graphical models and -Wishart distribution

Let be an undirected graph with , and be an ordering of . The undirected graphical model corresponding to the the ordered graph is the family of distributions

Let be i.i.d. observations from a distribution in . Note that the joint density of given is given by

The -Wishart distribution on is a natural choice of prior for (see Dawid and Lauritzen (1993) and Roverato (2000)). The density of the -Wishart distribution with parameters and is proportional to

Thus the posterior density of given is proportional to

and corresponds to a -Wishart distribution with parameters and , which implies that the family of -Wishart priors are conjugate for the family of distributions .

3 Generalized G-Wishart distributions

In this section we propose a generalization of the -Wishart distribution that is endowed with multiple shape parameters, and contains the -Wishart family as a special case. We shall show in later sections that the flexibility offered by the multiple shape parameters is very useful in high dimensional settings.

3.1 Definition

We now define a multiple shape parameter generalization of the -Wishart distribution for a general graph . To do this, we transform the matrix to its Cholesky decomposition. Consider the modified Cholesky decomposition , where is a lower triangular matrix with diagonal entries equal to , and is a diagonal matrix with positive diagonal entries. The (unnormalized) density of the generalized -Wishart distribution with parameters and is given by

| (3.1) |

We note that other generalizations of the Wishart have also been considered in Ben-David et al. (2015); Daniels and Pourahmadi (2002); Dawid and Lauritzen (1993); Khare and Rajaratnam (2011); Letac and Massam (2007). It is clear that the -Wishart density arises as a special case of the generalized -Wishart (by considering all the ’s to be equal and noting that ), and that the family of generalized -Wishart distributions defined above is a conjugate family of prior distributions for undirected graphical models. In fact, the posterior density of corresponds to a generalized -Wishart distribution with parameters and .

3.2 Some properties of the generalized G-Wishart distribution

We now proceed to derive properties of the generalized -Wishart distribution. To do so, we transform to its modified Cholesky decomposition as defined in Section 2.2.

We define to be the set of functionally independent elements of . Then the transformation is a bijection from to with Jacobian equal to , where for . Then the (unnormalized) generalized -Wishart density for is given by

| (3.2) |

We first establish sufficient conditions for the density to be proper.

Theorem 1.

If is positive definite and ,

Also under these conditions, , .

The proof of Theorem 1 is provided in Supplemental Section A.1. Under the conditions in Theorem 1, we will refer to the normalized version of as .

From Roverato (2000), if follows -Wishart with parameters then for or ,

We now provide an extension of this result for the case of generalized -Wishart distributions.

Theorem 2.

Let be generalized -Wishart with parameters for some . Denote as the principal submatrix of , and let denote the matrix with as its appropriate principal submatrix and rest of the elements equal to . Define the matrix as . If , then

The proof of Theorem 2 is quite detailed and technical and is thus provided in Supplemental Section A.2. Theorem 2 provides a useful tool to monitor convergence of any Markov chain Monte Carlo method for sampling from (and particularly the Gibbs sampler introduced in Section 5) .

We also undertake a comparison between generalized -Wishart distribution and the useful priors introduced by Letac and Massam (2007) for the case of decomposable graphs. A careful analysis demonstrates that the generalized -Wishart and Letac-Massam priors are quite different for decomposable graphs. The generalized -Wishart coincides with the Letac-Massam Type II Wishart in the special case when is homogeneous. See Supplemental Section B for details.

4 Generalized Bartlett graphs

As discussed earlier, the class of decomposable graphs is endowed with many properties helpful for closed form computation of posterior quantities. The assumption of decomposability can be rather restrictive in higher dimensions, as they constitute a very small fraction of all graphs see (Figure 2(a)). We develop in this section a class of graphs, which is substantially larger than the class of decomposable graphs. We will show in later sections that for this class of graphs, we can generate posterior samples from the generalized G-Wishart, using a tractable Gibbs sampling algorithm.

4.1 Preliminaries and Definitions

We now provide the definition of Generalized Bartlett graphs. First consider the following procedure to obtain a decomposable cover (see Section 2.1) of an arbitrary ordered graph .

We use the above algorithm to construct a decomposable cover for as follows. Let , and let denote the edge set of . It follows by construction that the ordering is a perfect vertex elimination scheme for . Hence, is a decomposable cover for . Note that, two different orderings may give rise to different decomposable covers. We now define Generalized Bartlett graphs.

Definition 4.

An undirected graph is said to be a Generalized Bartlett graph if there exists an ordering , with the property that there does not exist vertices satisfying and .

In such a case (i.e., when this property is satisfied), is called a Generalized Bartlett ordering of . When it exists, the Generalized Bartlett ordering may not be unique. The following lemma helps in proving an alternate characterization of Generalized Bartlett graphs, one that does not depend on any ordering of the vertices. The lemma shows that Algorithm 5 leads to a collection of minimal decomposable covers, in the sense that the edge set of any decomposable cover of has to contain for some ordering .

Lemma 1.

For any undirected graph and a decomposable cover of , an ordering of s.t., .

Proof.

Let be a decomposable cover of . Since is decomposable let be the perfect elimination ordering of it. We shall prove inductively that for in , . Since , that will prove this lemma. It is trivial to note that . Let us assume that the claim holds for . Consider any such that . Thus . Since is the perfect elimination ordering for , . Thus which completes the induction step and proves the lemma. ∎

We now provide a second definition of Generalized Bartlett graphs.

Lemma 2.

An undirected graph satisfies the Generalized Bartlett property if and only if has a decomposable cover such that every triangle in contains an edge from . That is for any such that , at least one of belongs to .

Proof.

If satisfies the Generalized Bartlett property then by definition an ordering of such that any triangle in contains an edge from . In that case we can simply take . On the other hand, let be a decomposable cover of such that every triangle in contains an edge from . By Lemma 1, an ordering of , such that . Thus any triangle in is also a triangle in and hence has an edge in . This makes the Generalized Bartlett ordering and an Generalized Bartlett graph.

∎

In the subsequent arguments we will also refer to Generalized Bartlett graphs as satisfying the Generalized Bartlett property. Some common Generalized Bartlett graphs are:

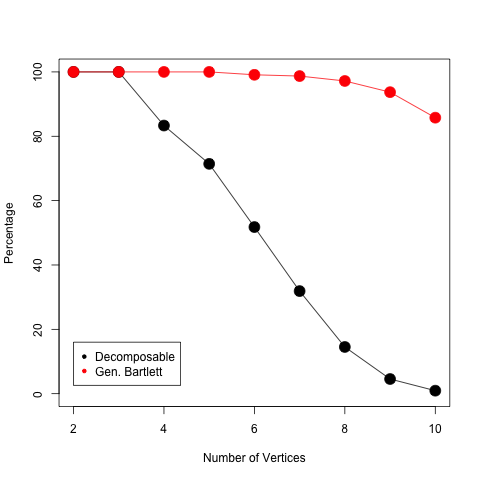

It is a natural question to ask how much larger the class of Generalized Bartlett graphs is compared to the class of decomposable graphs. It is quite difficult to obtain a closed form expression for the exact (or approximate) number of connected decomposable graphs (or Generalized Bartlett graphs) with a given number of vertices. However, a list of all possible connected non-isomorphic graphs having at most vertices is available at http://cs.anu.edu.au/~bdm/data/graphs.html. Using this list, we computed the number of decomposable and Generalized Bartlett graphs with at most vertices. Figure 2(a) provides a graphical comparison of these proportions, and Table 3(a) gives the actual values of these proportions. It is quite clear that the proportion of Generalized Bartlett graphs is much larger than the proportion of decomposable graphs. As expected, the proportions of both classes of graphs decreases as the total number of vertices increases. However, the rate of decrease in the proportions is much larger for decomposable graphs. For example, less than of connected isomorphic graphs with vertices is decomposable, but more than of connected isomorphic graphs with vertices is Generalized Bartlett. In this case the number of Generalized Bartlett graphs are approximately times larger.

of Generalized Bartlett graphs with

decomposable graphs

Generalized Bartlett graph.

| Order | No. of graphs | Percentage | Ratio | |

|---|---|---|---|---|

| Decom posable | Gen. Bart. | |||

| 2 | 1 | 100 | 100 | 100% |

| 3 | 2 | 100 | 100 | 100% |

| 4 | 6 | 83 | 100 | 83% |

| 5 | 21 | 71 | 100 | 71% |

| 6 | 112 | 52 | 99 | 53% |

| 7 | 853 | 32 | 98 | 32% |

| 8 | 11117 | 15 | 97 | 15% |

| 9 | 261080 | 4.5 | 94 | 5% |

| 10 | 11716571 | 0.9 | 86 | 1% |

4.2 Clique Sum Property of Generalized Bartlett graphs

An unordered graph is said to have a decomposition into components and if the vertex set can be decomposed as where such that the induced subgraph on is complete, and separates from (i.e., if and then ). If cannot be decomposed in the above manner it is called a prime graph. Hence any graph is either prime or can be broken down into several prime components by repeated application of the above procedure. It is well known that a graph is decomposable iff all of its prime components are complete. The following lemma provides a similar characterization for Generalized Bartlett graphs.

Lemma 3.

If all the prime components of a graph are Generalized Bartlett then the graph is also Generalized Bartlett.

Proof.

Note that, it is enough to prove the theorem, for a graph with two prime components. Let be an undirected graph with such that induced subgraph on is complete, and separates and . Let and be the corresponding induced subgraphs which are Generalized Bartlett. Then by Lemma 2, we can construct decomposable covers and of and respectively, such that every triangle in contains an edge in for . Define and . Note that is a cover for . We claim that is decomposable. Suppose to the contrary, that for for some there exists an induced cycle in on a set of vertices, say . Since and are both decomposable, all of cannot belong to exclusively in or in . Hence, there exist such that and . Since and are separated by , . Thus the subgraph induced by on the set of vertices contains two paths, both arising from and ending in and intersecting no where in between. Let be one of those paths. If , then there exists points in and connected to each other in , which is not possible. Thus s.t. . Similarly corresponding to the second path. Since is complete . Hence is a chord in the cycle giving us a contradiction. Hence, is a decomposable cover of .

To prove that is a Generalized Bartlett graph we shall prove that every triangle in the decomposable cover contains an edge in . Let us assume to the contrary that for , but . Since every triangle in has at least one edge from for , it follows that all cannot belong exclusively to or . Without loss of generality, let and . This implies giving us a contradiction. Thus is Generalized Bartlett. ∎

4.3 Constructing Generalized Bartlett covers

Given an ordered graph , Algorithm 2 below provides a Generalized Bartlett graph such that . Such a graph is referred to as a Generalized Bartlett cover of .

5 A tractable Gibbs sampler for generalized -Wisharts

In Section 4 we studied the graph theoretic properties of GB graphs. In this section we shall investigate the statistical/properties of GB graphs. In particular, we develop a tractable Gibbs sampling algorithm to sample from the generalized -Wishart distribution when the underlying graph is Generalized Bartlett. The first step in achieving this goal requires considering a further transformation of the Cholesky parameter from Section 3.2.

5.1 A reparametrization of the Cholesky parameter

Let be an undirected graph with , and an ordering for . Let be the modified Cholesky decomposition of . To facilitate our analysis, we consider a one-to-one transformation of defined as follows:

where and for . The following lemma shows that terms of the form can be expressed as a polynomial in the entries of and (with negative powers allowed for entries of ).

Lemma 4.

For , terms of the form , which appear in the modified Cholesky expansion of , are either functionally zero, or can be expressed as a sum of terms, where each term has the following form:

| (5.1) |

Proof: Note that

for all , and the Jacobian of this transformation is . Hence, the posterior density of is proportional to

| (5.2) |

where for . Note that if and , then , which implies

Making repeated substitutions in the RHS of the above equation, it follows that the entry is either functionally zero, or can be expressed as a sum of terms, where each term looks like

| (5.3) |

for suitable non-negative integers , and non-positive integers . It is easy to see that

Hence, can be expressed as a polynomial in entries of and . The results now follows from .

Note that for every with , the functionally dependent entry can be expressed in terms of and as in (5.3). The above analysis indicates that, in general, the posterior is a complicated function of . However, we will show that if is a Generalized Bartlett graph, and is a Generalized Bartlett ordering for , then the full conditional posterior distributions of all individual entries of are either Gaussian or Generalized Inverse Gaussian distributions (and therefore easy to sample from). This property will then be used to derive a Gibbs sampling algorithm to sample from the posterior density in (5.2).

5.2 The Gibbs sampler

We now derive a Gibbs sampling algorithm to sample from the posterior density in (5.2). We start by defining two properties which will be crucial to the development of the Gibbs sampler.

Definition 5.

Let be an ordered graph, and for , be the modified Cholesky decomposition.

-

1.

The ordered graph is defined to have Property-A if for every such that , the following holds: for every with , is a linear function of (keeping other entries of and fixed). In other words, in , can only be or for every with .

-

2.

The ordered graph is defined to have Property-B if for every such that , the following holds: for every , is a linear function of (keeping other entries of and fixed). In other words, in , can only be or for every .

We now state three lemmas which will be useful in our analysis. The first lemma provides an equivalent formulation of Property-B. The proofs of these lemmas are provided in Supplemental Section A.4, A.5 and A.6 respectively.

Lemma 5.

The following statements are equivalent.

-

(a)

The ordered graph satisfies Property-B.

-

(b)

For every , can be expressed as a polynomial in entries of and (with negative powers allowed for entries of ). Furthermore for every term in the expansion of , the power of any entry of is either or .

Let with . As noted above, for , both and can be expressed as polynomials in entries of and (with negative powers allowed for entries of ).

Lemma 6.

Both and are either functionally zero, or any term in the expansion of cannot be the exact negative (functionally) of any term in the expansion of .

The next lemma shows that Generalized Bartlett graphs satisfies Properties A and B.

Lemma 7.

Let be a Generalized Bartlett graph, and be a Generalized Bartlett ordering for . Then, the ordered graph satisfies both Property A and B.

We are now ready to state and prove the main result of this section, which provides a Gibbs sampler for the posterior density in (5.2).

Theorem 3.

Let be a Generalized Bartlett Graph, and be a Generalized Bartlett ordering for . Suppose follows a generalized -Wishart distribution with parameters and for some positive definite matrix and . If is the modified Cholesky decomposition of , and we define , , for , then

-

•

the conditional posterior density of the independent entry , given all other entries of and , is univariate normal,

-

•

the conditional posterior density of given and other entries of is either a Generalized Inverse Gaussian or Gamma.

Proof.

Note that for , can be expressed as a polynomial in the entries of and . Recall that is the decomposable cover obtained by the triangulation process described in Algorithm 5. We first establish that for , is functionally non-zero iff . We begin by noticing that at each step in the construction of we are adding some extra edges to to get , but never deducting anything. So if was an independent entry, i.e. , then .

Now lets assume to the contrary that is the first dependent but functionally non-zero entry s.t. . Since is dependent but non-zero s.t. appears in the expansion of . Now can be independent and hence . Otherwise is non-zero dependent. Since (the first non-zero dependent not in ) comes after , . We recall that, for any , while constructing , we only join vertices higher than . Thus must have been joined before construction of , i.e. . By a similar argument . Thus and we have a contradiction. Hence,

To prove the reverse implication we note that for , implies that is independent and hence . Now we use induction and assume that the claim holds upto . If for , then and hence appears in the expansion of . Since , and by assumption and which with the help of Lemma 6 implies . Thus the assumption holds for , which completes the induction step.

It follows by (5.2) and Property-A that for every , the conditional posterior density of given all other entries of and is proportional to

for appropriate constants and . Hence the conditional posterior density of is a Gaussian density. Similarly, it follows from (5.2) and Property-B that for every , the conditional posterior density of given all entries of and is proportional to

for appropriate constants and . Hence the conditional posterior density of is Gamma, and for , the conditional posterior density of is a Generalized Inverse Gaussian density. ∎

The results in Theorem 3 can be used to construct a Gibbs sampling algorithm, where the iterations involve sequentially sampling from the conditional densities of each element of . It is well known that the joint posterior density of is invariant for the Gibbs transition density. Since the Gaussian density is supported on the entire real line, and the Generalized Inverse Gaussian density is supported on the entire positive real line, it follows that the Markov transition density of the Gibbs sampler is strictly positive. Hence, the corresponding Markov chain is aperiodic and -irreducible where is the Lebesgue measure on (Meyn and Tweedie (1993), Pg 87). Also, the existence of an invariant probability density together with -irreducibility imply that the chain is positive Harris recurrent (see Asmussen and Glynn (2011) for instance). We formalize the convergence of our Gibbs sampler below. The following lemma on the convergence of the Gibbs sampling Markov chain facilitates computation of expected values for generalized -Wishart distributions.

Lemma 8.

Let be a Generalized Bartlett graph, and be a Generalized Bartlett ordering for . Then, the Markov chain corresponding to the Gibbs sampling algorithm in Theorem 3 is positive Harris recurrent.

5.3 Maximality of Generalized Bartlett graphs

Note that the Gibbs sampling algorithm described in Theorem 3 is feasible only if Property-A and Property-B hold. The following theorem shows that if a graph is not Generalized Bartlett, then at least one of Property-A and Property-B does not hold.

Theorem 4.

If an ordered graph satisfies Property-A and Property-B, then the graph is a Generalized Bartlett graph and is a Generalized Bartlett ordering for .

Proof.

Suppose there exists s.t. but i.e. . Hence is in the expansion of . The power of in the expansion of and is . . Also we know that, no term of can cancel with any term of . Hence in the expansion of the power of is . Thus Property-B is violated. The result now follows by Definition 7.

∎

Theorem 4 demonstrates that the class of Generalized Bartlett graphs is maximal, in the sense that the conditional distributions considered in Theorem 3 are Gaussian/Generalized-Inverse-Gaussian only if the underlying graph is Generalized Bartlett. In other words the above tractability is lost for graphs outside the Generalized Bartlett class.

5.4 Improving efficiency using decomposable subgraphs

It is generally expected that ‘blocking’ or ‘grouping’ improves the speed of convergence of Gibbs samplers (see Liu et al. (1994)). Suppose follows a generalized -Wishart distribution. In this section, we will show that under appropriate conditions, the conditional density of a block of variables in (given the other variables) is multivariate normal. Based on the discussion above, this result can be used to sample more efficiently from the joint density of .

Lemma 9.

Let be a Generalized Bartlett graph with vertices and follows generalized -Wishart with parameters . Suppose that for some , the induced subgraph of corresponding to the vertices is decomposable with a perfect elimination ordering. Then follows a multivariate normal distribution.

Proof.

We partition the matrix as

where has dimension and correspondingly,

Note that the density of is proportional to

A sample calculation gives:

| (5.4) |

Consider such that . Since the induced subgraph on is a decomposable graph with a perfect elimination ordering, there does not exist such that . It follows that is a function of entries in . Hence, all the dependent entries in are functions of . It follows by (5.4) that given , is a quadratic form in the independent entries of . Hence, the log of the conditional density of given the other entries in is a quadratic form. This proves the required result. ∎

5.5 Closed form expressions for decomposable graphs

A closed form expression for the mean of can be obtained if is assumed to be a decomposable graph. For and positive definite, the generalized -Wishart density on is,

Let us define,

Also let be the diagonal matrix with -th element as and is a matrix whose -th element is if , is if and otherwise. The following theorem provides closed form expectations of the elements of the matrix .

Theorem 5.

If is decomposable where the vertices have been ordered by an perfect elimination ordering, and is generalized -Wishart with parameters , then

| (5.5) |

where are the independent entries of the -th column of and . Also,

The proof is provided in the Supplemental Section A.3.

6 Classes of Generalized Bartlett Graphs

As mentioned earlier, the class of Generalized Bartlett graphs contains the class of decomposable graphs. In this section we will consider two naturally occurring examples of non-decomposable Generalized Bartlett graphs. We then provide schemes for combining a group of Generalized Bartlett graphs to produce a bigger Generalized Bartlett graph.

6.1 The -cycle

We show that the -cycle (with its standard ordering) satisfies Property-A and Property-B, and is hence a Generalized Bartlett graph. Let , where , is the identity permutation and

The independent entries of are . After some straightforward algebraic manipulations, the dependent entries of can be calculated as follows:

It is clear from the expressions in the above equation that Property-A and Property-B are satisfied and hence by Theorem 4, the -cycle is Generalized Bartlett.

6.2 Grids

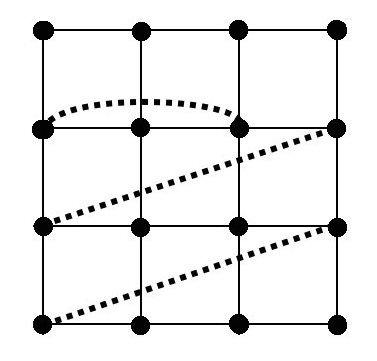

A grid is an undirected graph formed by the intersection of rows and columns where the vertices correspond to the intersection points and as a result edges are formed. In this section we shall prove that for some particular ordering all and grid are Generalized Bartlett. We order an grid row wise starting from the top as shown in Figure 2(b).

Let be an ordered graph, , and denote the modified Cholesky decomposition of . Note that Property-A and Property-B have been defined for ordered graphs, but we extend these notions to polynomials as follows. For any polynomial of , we say that satisfies Property-A if the power of any independent can be . Similarly we say satisfies Property-B if the power of any can be . We note that if and satisfies Property-B then also satisfies Property-B.

Lemma 10.

An grid when ordered as above is Generalized Bartlett.

6.3 Expansion property of Generalized Bartlett graphs

In this section we develop two methods, which combine an arbitrary number of Generalized Bartlett graphs in a suitable manner to produce a larger Generalized Bartlett graph.

6.3.1 Maximum vertex based expansion

We start by proving a lemma which will be useful for further analysis.

Lemma 11.

Let be a Generalized Bartlett graph. If is a subset of and is the corresponding subgraph then is also a Generalized Bartlett graph.

Proof.

Since is Generalized Bartlett, let be the decomposable cover of such that any triangle in has at least one edge in . Let be the induced subgraph of for . Then is decomposable since it is a induced subgraph of a decomposable graph. Also any triangle in is a triangle in and thus has atleast one edge in and hence in . Thus by Lemma 2, is Generalized Bartlett. Moreover from the proof of Lemma 2 we can observe that if is the Generalized Bartlett ordering for then the same ordering works for . ∎

Let be a Generalized Bartlett graph with, . Suppose we replace each vertex of , by a Generalized Bartlett graph , where for , . Here and are the sizes of the graphs. Note that the graphs being considered here are already ordered. For ease of exposition, we will suppress the ordered graph notation, and refer to the graphs as just .

Definition 6.

The expanded graph is constructed from using as follows,

-

•

-

•

iff either for some , or for some and .

Hence is constructed from by replacing the -th vertex of by . An edge between and in translates to an edge between the maximal vertices of and namely and . For any , if , the notation shall denote , and shall denote

Theorem 6.

The expanded graph defined as above is Generalized Bartlett.

The proof this theorem is given in the Supplemental Section A.7.

6.3.2 Tree based expansion

Consider a tree with vertices . For each consider an arbitrary number of GB graphs say . We add an edge from to each vertex in for every . Denote the resulting graph by . Next the vertices in are labeled in the following order.

The labeling is done in such a way that the induced ordering on each is a GB ordering and every parent vertex in gets a higher label than any of its children in . Again for ease of exposition we will suppress the ordering notation and refer to the resulting ordered graph as .

Theorem 7.

The graph defined and ordered as above is Generalized Bartlett.

The proof of this theorem is provided in the Supplemental Section A.8.

7 Illustrations and Applications

We now illustrate the advantages of our Generalized Bartlett approach on both simulated and real data and demonstrate that the proposed GB method is scalable to significantly higher dimensions. In Section 7.1, we illustrate the advantage of having multiple shape parameters in the generalized -Wishart distribution. In Section 7.2.1 and Section 7.2.2, we undertake a comparison of our algorithm with the accept-reject and Metropolis-Hastings approaches. Section 7.3 contains a real data analysis using data from a temperature study. Although the main focus of this paper is development of the flexible class of -Wishart distributions, and tractable methods to sample from these distributions, we also illustrate that the methods developed in this paper can be used for high-dimensional graphical model selection in conjunction with existing penalized likelihood methods (see Supplemental Sections C and D).

7.1 Comparing -Wishart with generalized -Wisharts

In this section, we present a simulation experiment to demonstrate that the multiple shape parameters in the generalized -Wishart distribution can yield differential shrinkage and improved estimation as compared to the single parameter -Wishart in higher dimensional setting.

For the purposes of this experiment we consider a Generalized Bartlett graph with vertices, defined as follows. Let,

A graph is constructed by forming the -cycle and then connecting with all elements of for . An inverse covariance matrix is then constructed by taking , where if . Here is a lower triangular matrix with independent entries equal to , and dependent entries chosen such that .

We then generate samples from a distribution. Let denote the corresponding sample covariance matrix. Let denote the mean of the diagonal entries of . We first consider a -Wishart prior for with and different choices of . Using the Gibbs sampler proposed in Section 5, the posterior mean for (and ) is then computed for each choice of . Figure 4 depicts the performance of these posterior mean estimators in terms of the Steins loss function (denote by ). It can be seen from Figure 4 that, and are minimized at and respectively.

We now illustrate the improved performance of the posterior mean estimators when using our generalized -Wishart priors endowed with multiple shape parameters. If follows a -Wishart distribution with parameters and , then for every and , see (see Roverato, 2002, Corollary 2). Borrowing intuition from this result, we first choose a generalized -Wishart empirical prior for with and . Here denotes the vector of diagonal entries of a given matrix. It can be seen from Table 1 that even with this empirical choice of we observe a decrease in Stein’s loss for and for compared to the best performance in the single shape parameter case. Next, we perform a restricted grid search to check if the performance can be further improved. In particular, a -dimensional grid search is performed on where for we assign for all . As shown in Table 1, the best posterior mean estimator obtained via this search improves the Stein’s loss for and by and respectively (compared to the best estimator in the single parameter case).

| 161.9 | 207.6 | |

| 222.4 | 158.3 | |

| 113.0 | 137.7 | |

| 105.2 | 114.4 |

7.2 Comparison with other Monte Carlo based approaches

We shall show in this section that two other approaches, namely the accept-reject algorithm and the Metropolis algorithm, can also be used to sample from the generalized -Wishart distribution. We demonstrate however that both these algorithms can have specific scalability issues, but the proposed Gibbs sampler can overcome these challenges.

7.2.1 Comparison with the accept-reject algorithm

A useful accept-reject algorithm to simulate from a -Wishart distribution for a general graph is provided in Wang and Carvalho (2010). This algorithm can be easily generalized to simulate from our generalized -Wishart distributions. Below, we present this generalized version of the accept-reject algorithm for a graph , where cannot be decomposed into any prime components. Many graphs, such as cycles, grids (with ) satisfy this property.

Let follow a generalized -Wishart distribution with parameters and for some positive definite matrix and . Let be the Cholesky decompositions of . Also for , define . The accept-reject algorithm can now be specified as follows.

- Step 1

-

Simulate as follows; For , and for , . For , we calculate as,

- Step 2

-

Simulate and check whether

If this holds, then accept this value of , else go to Step 1.

- Step 3

-

Set and .Then has the required generalized Wishart distribution.

A common problem with the vanilla application of accept-reject algorithm even in moderate dimensional settings is that the average acceptance probability can be extremely small. This issue can make the accept-reject algorithm computationally infeasible. We find that the same phenomenon happens with the accept-reject algorithm in the generalized -Wishart distribution setting. The algorithm works well for small dimensional examples, such as the simulation example in Wang and Carvalho (2010) for a -vertex graph (where the largest prime component has order ). We find however, that the low acceptance probability issue mentioned above, surfaces as we increase the size of the largest prime component. To illustrate this, let be a cycle (which cannot be decomposed into prime components) with an ordering as specified in Section 4. Consider a generalized -Wishart distribution with parameters and . Here and for and otherwise. The shape parameters, for , and for . The average time taken by the accept-reject algorithm to complete one iteration is more than hours on a 2.4 Ghz processor with 4 GB RAM. Clearly, this happens due to low acceptance probabilities. However, the Gibbs sampler does not suffer from these issues, since no acceptance/rejection step is involved. The results obtained by using iterations of the Gibbs sampler (which take approximately minutes) are provided in Table 2. In particular, this table demonstrates that the difference between mean of from the Gibbs sampler (for or ) and its theoretical expectation (as given by Theorem 2) is very small.

| i | j | Simulated mean | True Mean | i | j | Simulated mean | True Mean |

|---|---|---|---|---|---|---|---|

7.2.2 Comparison with the Metropolis-Hastings Algorithm

A useful Metropolis-Hastings algorithm to sample from the -Wishart distribution has been developed in Mitsakakis et al. (2011). This approach can also be conveniently adapted to the setting of our generalized -Wishart distribution. Suppose we want to simulate from a generalized -Wishart distribution with parameters and corresponding to an undirected graph , with a specified ordering . Let and be the Cholesky decompositions of and . Mitsakakis et al. (2011) propose the following algorithm to simulate , and thereby from the required distribution.

For and they call to be a ‘dependent’ entry, while are referred to as the independent entries of . Also for , they define . Given the independent entries, the dependent entries can be calculated exactly as in Section 7.2.1. Let denote the distribution on , where for , and for , are independent standard normal. For a given positive integer , the procedure to generate iterations of the Metropolis-Hastings algorithm is given as follows.

-

•

Initialize by sampling from and set .

-

•

For in do ::

-

1.

Sample from .

-

2.

Set .

-

3.

Sample from Bernoulli. If , set , else set .

-

1.

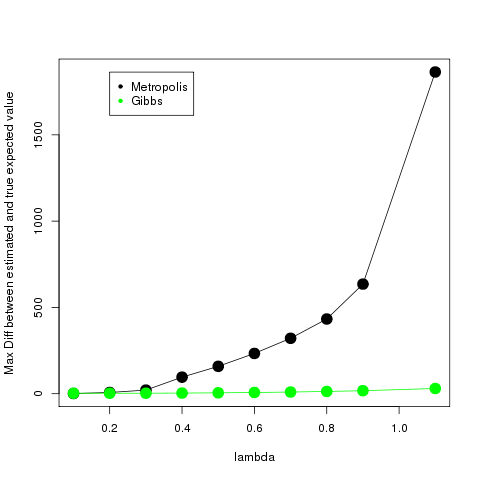

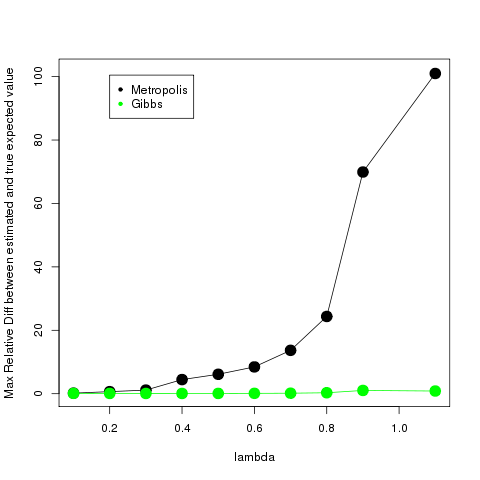

In the above algorithm at each stage the acceptance probability depends on , which then depends on the dependent entries of and . The dependent entries in turn depend on the matrix via terms of the form for . If the terms are large in magnitude then we expect the terms and to be large in magnitude as well. This typically makes either a large positive number or a large negative number which makes the acceptance probability close to or , thereby making the process potentially expensive in terms of timing. To illustrate this fact lets consider the grid (which satisfies the Generalized Bartlett property) and take all values of equal to for some and the diagonal entries of as . We illustrate below that as the value of increases, the performance of the Metropolis-Hastings algorithm can deteriorate. In comparison, this change in has negligible effect on the performance of the proposed Gibbs sampling algorithm. If is a generalized -Wishart with parameters and , then for or , the expected value of is (see Theorem 2). Thus, to compare the performance of the two algorithms, we check the difference between the estimated values of and (the independent parts only) using the sup norm and also the relative error. Figure 5 shows the comparison between the Gibbs algorithm and the MH algorithm (both of which are algorithms for the generalized Wishart class) for varying values of (choosing the entries of chosen uniformly on a grid from to for all cases). The running time for both algorithms for each is approximately 10 mins on an AMD-V 2.4 GHz processor.

7.3 Application to temperature data

In this section, we provide an illustration of our methods on the (Brohan et al. (2006)) dataset. HadCRUT3 dataset consists of monthly temperature data provided on a grid over the globe starting from 1850 till 2012. The spatial resolution is at a latitude and longitude. Here, we consider locations from the US map (out locations worldwide) as shown in Figure 6. Thus we have samples for variables. Our goal is to estimate the precision matrix of these temperature variables. Given the spatial nature of the data, it is natural to impose sparsity on the precision matrix, with the underlying graph as shown in Figure 6. We use an ordering of the variables specified as follows: label the vertex in the bottom of the leftmost column of the grid as , and then move up the columns from south to north, and the rows from east to west. We proceed to fit a concentration graph model, which assumes that , with and defined as above.

The graph is not decomposable, but can be shown to be a Generalized Bartlett graph (it is an induced subgraph of an grid). Hence, the Bayesian framework developed in this paper can be used to obtain an estimate of . We use two different empirical/objective priors for our analysis. In particular, our first choice is a generalized Wishart prior with scale parameter and shape parameter with for . As a second choice, we use a generalized Wishart prior with scale parameter and shape parameter with for . The Gibbs sampling procedure specified in Section 5.2 was used to generate samples from the two corresponding posterior distributions. The burn-in period was chosen to be iterations, and the subsequent iterations were used to compute the posterior means and credible intervals. Increasing the burn-in to more than iterations did not lead to significant changes in the estimates, thus indicating that the chosen burn-in period is appropriate. The posterior mean estimates for both the priors are provided in Table 3. The MLE for was also computed using the glasso function in , and is provided in Table 3 as well. As noted in the introduction, an inherent advantage of Bayesian methods is ability to easily provide uncertainty quantification using the posterior distribution. The estimated posterior credible intervals for both prior choices are provided in Table 4.

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

References

- Asci and Piccioni (2007) Asci, C. and Piccioni, M. (2007) Functionally compatible local characteristics for the local specification of priors in graphical models. Scand. J. Statist., 34, 829–840.

- Asmussen and Glynn (2011) Asmussen, S. and Glynn, P. W. (2011) A new proof of convergence of mcmc via the ergodic theorem. Statistics & Probability Letters, 81, 1482–1485.

- Banerjee et al. (2008) Banerjee, O., Ghaoui, L. E. and d’Aspremont, A. (2008) Model selection through sparse maximum likelihood estimation for multivariate gaussian or binary data. Journal of Machine Learning Research, 9, 485–516.

- Ben-David et al. (2015) Ben-David, E., Li, T., Massam, H. and Rajaratnam, B. (2015) High dimensional bayesian inference for gaussian directed acyclic graph models.

- Brohan et al. (2006) Brohan, P., Kennedy, J. J., Harris, I., Tett, S. F. B. and Jones, P. D. (2006) Uncertainty estimates in regional and global observed temperature changes: A new data set from 1850. Journal of Geophysical Research: Atmospheres, 111(D12), 1984–2012.

- Chang et al. (2005) Chang, H. Y., Nuyten, D. S. A., Sneddon, J. B., Hastie, T., T., R., Sorlie, T., Dai, H., He, Y. D., van’t Veer, L. J., Bartelink, H., van de Rijn, M., Brown, P. O. and van de Vijver, M. J. (2005) Robustness, scalability, and integration of a wound-response gene expression signature in predicting breast cancer survival. Proceedings of the National Academy of Sciences of the United States of America, 102(10), 3738–3743.

- Daniels and Pourahmadi (2002) Daniels, M. J. and Pourahmadi, M. (2002) Bayesian analysis of covariance matrices and dynamic models for longitudinal data. Biometrika, 89, 553–566.

- Davis (2006) Davis, T. (2006) Direct Methods for Sparse Linear Systems. SIAM.

- Dawid and Lauritzen (1993) Dawid, A. P. and Lauritzen, S. L. (1993) Hyper markov laws in the statistical analysis of decomposable graphical models. Ann. Statist., 21, 1272–1317.

- Friedman et al. (2007) Friedman, J., Hastie, T. and Tibshirani, R. (2007) Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9, 432–441.

- Friedman et al. (2010) Friedman, J. H., Hastie, T. and Tibshirani, R. (2010) Applications of the lasso and grouped lasso to the estimation of sparse graphical models. Tech. rep., Department of Statistics, Stanford University.

- Khare et al. (2015) Khare, K., Oh, S. Y. and Rajaratnam, B. (2015) A convex pseudo-likelihood framework for high dimensional partial correlation estimation with convergence guarantees. to appear in Journal of the Royal Statistical Society B.

- Khare and Rajaratnam (2011) Khare, K. and Rajaratnam, B. (2011) Wishart distributions for decomposable covariance graph models. Annals of Statistics, 39, 514–555.

- Lauritzen (1996) Lauritzen, S. L. (1996) Graphical Models. Oxford Univ. Press, New York.

- Lenkoski (2013) Lenkoski, A. (2013) A direct sampler for g-wishart variates. Stat, 2, 119–128.

- Letac and Massam (2007) Letac, G. and Massam, H. (2007) Wishart distributions for decomposable graphs. Ann.Statist., 35, 1278–1323.

- Liu et al. (1994) Liu, J. S., Wong, W. and Kong, A. (1994) Covariance structure of the gibbs sampler with applications to the comparisons of estimators and augmentation schemes. Biometrika, 81, 27–40.

- Meyn and Tweedie (1993) Meyn, S. P. and Tweedie, R. L. (1993) Markov Chains and Stochastic Stability. Springer-Verlag, London.

- Mitsakakis et al. (2011) Mitsakakis, N., Massam, H. and Escobar, M. D. (2011) A metropolis-hastings based method for sampling from the g-wishart distribution in gaussian graphical models. Electronic Journal of Statistics, 5, 18–30.

- Parraal and Schefflerb (1997) Parraal, A. and Schefflerb, P. (1997) Characterizations and algorithmic applications of chordal graph embedding. Discrete Applied Mathematics, 79, 171–188.

- Paulsen et al. (1989) Paulsen, V. I., Power, S. C. and Smith, R. R. (1989) Schur products and matrix completions. Journal of Functional Analysis, 85, 151–178.

- Peng et al. (2009) Peng, J., Wang, P., Zhou, N. and Zhu, J. (2009) Partial correlation estimation by joint sparse regression models. J. of Amer. Statist. Assoc., 104, 735–746.

- Rajaratnam et al. (2008) Rajaratnam, B., Massam, H. and Carvalho, C. (2008) Flexible covariance estimation in graphical models. Ann. Statist., 36, 2818–2849.

- Roverato (2000) Roverato, A. (2000) Cholesky decomposition of a hyper inverse wishart matrix. Biometrika, 87, 99–112.

- Roverato (2002) Roverato, A. (2002) Hyper inverse wishart distribution for non-decomposable graphs and its application to bayesian inference for gaussian graphical models. Scandinavian Journal of Statistics, 29, 391–411.

- Wang and Carvalho (2010) Wang, H. and Carvalho, C. M. (2010) Simulation of hyper-inverse wishart distributions for non-decomposable graphs. Electronic Journal of Statistics, 4, 1470–1475.

Supplemental Document

Appendix A Proofs

A.1 Proof of Theorem 1

Note that,

where is the -th column of . Since is positive definite, let be its minimum eigenvalue. Hence,

where denote the vector of independent entries of and the length of is . Hence, there exists such that,

Now,

and we know that

since . Hence can be normalized to a proper density . Next we prove that , has finite expectation under this density. Since , it is enough to show that , the expectation of exists. Let us consider the following cases,

- Case 1

-

- Case 2

-

- Case 3

-

- Case 4

-

It follows from equation 3.2, that

Note that both and are uniformly bounded above in . It follows by that in all the cases considered above, is uniformly bounded in . Since we have already established that

is integrable, it follows that has finite expectation under .

A.2 Proof of Theorem 2

Let

Let denote the principal submatrix corresponding to the first rows and columns of . Then . Thus

where . Hence,

Differentiating both sides w.r.t. and assuming that we can take the derivative inside the integral, we get

Since for and otherwise, we observe that

We now rigorously establish the validity of exchanging the derivative and the integral mentioned above. Define,

We see that is an open subset of and has a positive measure (with respect to induced Lebesgue measure on ). Thus can also be seen as a density on taking value on . We claim that is continuous on . Clearly, it is enough to prove this claim on the boundary between and . Since is open, . Thus for , .

Let and be a sequence in such that . We want to show . If, denote the submatrix of corresponding to the first rows and columns, then

and

Since is positive definite, the above ratio is postie and less than equal to . But , meaning that the sequence is positive and bounded above. Since is not positive definite, either , or there exists such that and .

The exponential term in is and in both cases mentioned above we have atleast one term outside the exponential converging to , while the rest are bounded above; which proves that .

Next for we find the partial derivatives and double derivatives of . For notational convenience we replace by for the rest of this proof. We have already seen that for ,

Note that for , . Differentiating the above equation again we get,

For a symmetric non-singular matrix ,

For in the interior of , above partial derivatives and double derivatives exists and equals . Now, fix and consider in . Let us define to be a matrix such that, if and . If then . We now show that for , such that

This will show that for , exist and equal . Since is positive definite . Hence such that and . Consider . Note that , and is a quadratic in , which equals at . Hence can be written as . If , then

Now note that the other terms in are either or ; which are all positive and bounded above. Thus if the partial derivatives exist and equal at . Before exploring the partial double derivatives we state the following fact, which is straightforward to establish.

Fact.

If is a polynomial in elements of and is p.d. then as a function of is uniformly bounded above.

If the existence of partial double derivatives on can proved with the the help of the above fact and similar arguments as in the case of single partial derivatives.

If is the marginal density of then,

Note that has support over whole real line. For arbitrary ,

If,

and then . If then by the fact above, is uniformly bounded above on by a constant . Thus,

The above integral is finite, which means we can take limit as , in to obtain,

Since the support of is the entire real line, . Thus which establishes .

A.3 Proof of Theorem 5

If are the independent entries in then the Jacobian of the transformation from , is . Thus the unnormalized density of is,

Since is decomposable, and the vertices have been ordered by a perfect elimination ordering,

Now,

where is the -th column of . Now for , and since is decomposable, for , if . Thus, if denotes the set of independent entries in the -th column of , then,

Thus,

which implies that are mutually independent. After straightforward calculations we find that,

Now for , we calculate the expectation of . Note that,

and for ,

Similarly for ,

Adding the expectations above gives us the required result, i.e.,

A.4 Proof of Lemma 5

(a) (b): It follows that for the power of any in and can be only. Hence the power of in can be only and hence the power of in can be only.

(b) (a): Suppose to the contrary that Property-B does not hold. Then there exist with and such that the maximal negative power of in the expansion of is at least . Let denote this power. Then the expansion of has at least one term where the power of is . Since , this contradicts (b).

A.5 Proof of Lemma 6

Firstly, note that if either of or is functionally zero, then by assumption is functionally non-zero, and we are done. Hence, without loss of generality, we consider a situation where both and are functionally non-zero.

- Case 1:

-

Suppose or . Then is functionally dependent on atleast one of or , whereas is functionally independent of and by (5.1).

- Case 2:

A.6 Proof of Lemma 7

Suppose to the contrary that either Property-A or Property-B is violated.

- Case 1::

-

Property-A does not hold.

Let be the first (dependent) entry where it is violated. Thus , s.t. has a square term. Now if any one of them is independent, say , then has the square term because can’t have in it’s expansion. But that violates the assumption that is the first term. Hence we have, such that,Thus we have violated Generalized Bartlett Property.

- Case 2::

-

Property-B does not hold.

Let be the first (dependent) entry where it is violated. Then , s.t. the power of in is . Now if any one (or both) of and is independent, we will get a contradiction since is the first term. Thus we get s.t.,contradicting Generalized Bartlett Property.

A.7 Proof of Theorem 6

We prove that satisfies Property-A and Property-B. In particular we will show that for every , satisfies Property A and Property B. Consider the following cases.

- Case 1

-

Suppose and .

Here , which implies that,

- Case 2

-

Suppose and .

If , then is an independent parameter. Otherwise using Case 1 we get that,

Since and is a Generalized Bartlett graph, it follows from Lemma 7 that has Property A and Property B.

- Case 3

-

Suppose and .

Since again using Case 1, we get

Now suppose . Since , it follows that

since by Case 1, . Now, we can show inductively for ;

.

- Case 4

-

Suppose and . If then is an independent parameter. Otherwise by Case 1,

Similar arguments as that in Case 2 can now be used to show that satisfies Property A and Property B.

- Case 5

-

Suppose .

If then is an independent parameter.If not,

Note that every belongs to . By Case 3, for , . Hence,

Since belongs to and is a Generalized Bartlett graph it follows from Lemma 7 has Property A and Property B.

A.8 Proof of Theorem 7

We will prove Property-A and Property-B by considering the following cases. In particular we will show that for every , satisfies Property A and Property B.

- Case 1

-

Suppose for and .Here is not a neighbor of any of . Thus .

- Case 2

-

Suppose . If , then is an independent parameter. Otherwise,

Since belong to the same Generalized Bartlett graph it follows from Lemma 7, satisfies Property A and Property B.

- Case 3

-

Suppose and . Then is independent.

- Case 4

-

Suppose and where . Note that , and hence by Case 1,

If is the smallest labeled element of , . From here by induction in can be proved that .

Cases 1 through 4 prove that for all , satisfies Property A and Property B.

A.9 Proof of Lemma 10

We shall prove the Generalized Bartlett property by induction on . Suppose . We will now express the dependent entries in terms of the independent entries and see whether any quadratic terms appear or not.

Thus for grid, Property-A and Property-B is satisfied. Now suppose it is satisfied for grid, we want to prove for a grid.

Again we will express the dependent entries in terms of the independent entries and see whether any quadratic terms appear or not. The induction hypothesis implies that Property A and Property B are satisfied for with . Note that,

| [ does not contain ] | ||||

Thus a grid satisfies Property-A. We now proceed to check Property-B. Since and satisfy Property-B, so does and . Hence by induction, and Theorem 4, for all , grid satisfies the Generalized Bartlett property.

Appendix B Comparison with Letac-Massam distributions

For a decomposable graph , Letac and Massam (2007) generalized the Wishart distribution, by defining two classes of distributions with multiple shape parameters on the cones and . They are called Type I and Type II Wishart distributions and have proved to be useful in high-dimensional Bayesian inference, as shown in Rajaratnam et al. (2008). Let denote the set of incomplete matrices , where is missing iff . Recall that is defined as

For , let be the unique matrix such that, for and , and . Also for a matrix , let be symmetric incomplete matrix such that -th entry is missing if , and otherwise.

It is natural to compare and contrast our generalized -Wishart distributions with the Letac-Massam distributions when is decomposable.

First, we consider the family of Type II Wishart distributions (defined on the space ) in Letac and Massam (2007). In particular, the density on is proportional to

Clearly, the exponential term in the above density is the same as the exponential term in the generalized -Wishart density in (3.1). Now let us compare terms outside the exponential. For the generalized -Wishart density in (3.1), the non-exponential term is

where is the modified Cholesky decomposition of . The corresponding term for is

To contrast these two terms, we consider the case when the graph is the -chain, , given by . Hence, and . It follows that

Thus even for this simple graph the non-exponential term for is very different than the corresponding non-exponential term for the generalized -Wishart. However, if the graph is homogeneous, then Letac and Massam (2007) shows that for any clique and separator ,

In the homogeneous setting we see that the term outside the exponential is similar to that of the generalized -Wishart. The family of generalized -Wishart distributions introduced in the paper are therefore in general structurally different than the family of Type I and Type II Wishart distributions introduced in Letac and Massam (2007). In the special case of homogeneous graphs, the family of generalized -Wishart distributions coincides with the family of Type II Wishart distributions in Letac and Massam (2007).

Next we consider the family of Type I Wishart distributions (defined on the space ), which is refereed to as in Letac and Massam (2007). The family of inverse Wishart distributions induced by on the space is referred to as . In particular, the density on is proportional to

where and , are real numbers, and is the multiplicity of the minimal separator which is positive and independent of the perfect order of the cliques considered (as proved by Lauritzen (1996)). Note that, as expected, the exponential term in the above density is , whereas the exponential term in the generalized -Wishart density in (3.1) is . Hence the difference between the two classes is fundamental.

Appendix C Model Selection Example

We now demonstrate through a simulation experiment that the methodology proposed in the paper is competitive with standard methods for high-dimensional graphical model selection.

For a given dimension , a “true” sparse graph with vertices is chosen by taking a simple random sample (without replacement) of size from the total number of possible edges. We consider five different values for the number of variables , ranging from to . The sample size is chosen to be , or . Then, a “true” precision matrix is generated by taking , where is the identity matrix and is a some constant (depending on ) if else . Then, i.i.d. samples from a distribution are generated. Let denote the sample covariance matrix of these samples.

The goal now is to estimate the original graph . Our approach is as follows. We first obtain a collection of “good” models (equivalently, graphs) by using the popular penalized graphical model selection method Friedman et al. (2007), and then use our Bayesian approach to select the best model out of this collection. The Glasso method takes a penalty parameter as an input, and for a given value of provides a sparse estimate of the inverse covariance matrix . The sparsity pattern in the estimate of in turn leads to an estimate of the underlying graph/model. Banerjee et al. (2008) propose a simple and popular method for choosing the penalty parameter for Glasso, and thereby choosing a graph.

Our model selection algorithm works in conjunction with Glasso, the penalized likelihood algorithm introduced in Friedman et al. (2007). We shall consider a grid of penalty parameters for Glasso and consider models with various levels of sparsity. Before applying the Glasso algorithm we standardize the covariance matrix . In this case, it is known that produces extremely sparse models and close to produces extremely dense models. Our penalty parameter grid starts with and ends at and decreases by steps of . For each value of in this grid, the Glasso algorithm is run to obtain a graph estimate with adjacency matrix . Graphs with edge density from to are considered.

For each thus obtained, we use the Deviance Information Criterion (DIC) as a measure of how well the estimated graph/model fits the data. Recall from Mitsakakis et al. (2011) that , where , is the posterior expectation of , and is the posterior expectation of . Ideally, for each value of , we would like to compute the DIC for the model corresponding to . Note however, that the graph corresponding to may not in general be Generalized Bartlett. Thus we generate a Generalized Bartlett cover for as described in Algorithm 2. If is large, and is quite dense, then for computational reasons, we choose a decomposable cover using the R package “igraph” . Once the appropriate cover has been computed, we compute the DIC score corresponding to this cover using hyperparameter values (where is the mean of the diagonal entries of ) and for . This DIC score is treated as a measure of goodness of fit for the model corresponding to . Finally, we choose the with the best goodness of fit score. For each value of , the whole process is repeated times, and the average sensitivity and specificity is reported in Table 5. For comparison purposes we also report the average sensitivity and specificity of the model obtained by using the penalized likelihood method proposed in Banerjee et al. (2008).

In order to make sure that we are searching for models in a range whose edge density includes the true density () we use the starting value of (edge density almost ) and the algorithm ends at value of with edge density around . Thus the true edge density of lies in the range.

We compare the model selection performance of Glasso (using the approach in Banerjee et al. (2008)) and the generalized -Wishart based Bayesian approach outlined above, in Table 5. Both approaches have very high specificity, with the Glasso based approach performing slightly better. On the contrary, the generalized -Wishart approach shows an immense improvement in terms of sensitivity as compared to the Glasso approach. This is particularly useful in high dimensional biological applications where discovery of an important gene is much more important than exclusion of a non-important one.

| Specificity | Sensitivity | ||||

|---|---|---|---|---|---|

| Glasso-Ban | gen. G-Wishart | Glasso-Ban | gen. G-Wishart | ||

| 50 | 100 | 1 | 0.9830 | 0.5833 | 1 |

| 100 | 100 | 1 | 0.9714 | 0 | 0.8663 |

| 200 | 100 | 1 | 0.9316 | 0.0007538 | 0.7781 |

| 500 | 200 | 0.9999 | 0.9166 | 0.0041 | 0.5570 |

| 1000 | 300 | 0.9899 | 0.9214 | 0.0023 | 0.2772 |

Appendix D Application to Breast cancer data

In this section, we use the methodology developed in this paper to analyze a dataset from a breast cancer study in Chang et al. (2005). This study is based on patients, whose expression level of genes are recorded. As in Khare et al. (2015), we focus on the reduced dataset of genes closely associated with breast cancer. The objective is to obtain a sparse partial correlation graph, i.e., a sparse estimate of the inverse covariance matrix for the genes, to identify the hub genes. As in Section C, we shall choose candidate partial correlation graphs by using penalized likelihood/pseudo-likelihood methods, and then choose the best graph by computing the DIC score using the Bayesian methodology developed in this paper. The idea is to reduce our search space to a handful of graphs and then use the generalized Bartlett methodology developed in this paper for Bayesian model selection. To obtain the candidate graphs, we shall use four standard penalized algorithms: SYMLASSO (Friedman et al. (2010)), CONCORD (Khare et al. (2015)), GLASSO (Friedman et al. (2007)) and SPACE (Peng et al. (2009)). For each of these algorithms, the respective penalty parameters are chosen so that the resulting partial correlation graph has 100 edges. All the four graphs thus obtained are not Generalized Bartlett, and we obtain Generalized Bartlett covers for each of them using Algorithm 2. All of these covers have at most extra edges as compared to the original graph.

Note that each of these four partial correlation (cover) graphs represents a concentration graph model. Let denote the sample covariance matrix. Note that, as in Khare et al. (2015), each of the data columns were centered and scaled (with respect to mean absolute deviation) prior to computing . For each of the four models, we choose a generalized Wishart prior with parameters and as

and

where denotes the -dimensional vector of all ones. Next, we run the Gibbs sampling algorithm for each of these four scenarios for steps. The resulting Markov chains are used to compute the DIC score for each of the four partial correlation graphs (using the procedure from Mitsakakis et al. (2011) outlined in Section C). The DIC scores are provided in the Table 6, and show that the graph chosen using the CONCORD algorithm performs the best. This example illustrates that the methodology developed in this paper can be used in conjunction with DIC for high-dimensional graphical model selection in applied settings.

| Algorithm | DIC |

|---|---|

| SYMLASSO | 298816.6 |

| CONCORD | 295766.6 |

| GLASSO | 299601.1 |

| SPACE | 299302.8 |