Thermodynamics of firms’ growth

Abstract

The distribution of firms’ growth and firms’ sizes is a topic under intense scrutiny. In this paper we show that a thermodynamic model based on the Maximum Entropy Principle, with dynamical prior information, can be constructed that adequately describes the dynamics and distribution of firms’ growth. Our theoretical framework is tested against a comprehensive data-base of Spanish firms, which covers to a very large extent Spain’s economic activity with a total of firms evolving along a full decade. We show that the empirical exponent of Pareto’s law, a rule often observed in the rank distribution of large-size firms, is explained by the capacity of the economic system for creating/destroying firms, and can be used to measure the health of a capitalist-based economy. Indeed, our model predicts that when the exponent is larger that 1, creation of firms is favored; when it is smaller that 1, destruction of firms is favored instead; and when it equals 1 (matching Zipf’s law), the system is in a full macroeconomic equilibrium, entailing “free” creation and/or destruction of firms. For medium and smaller firm-sizes, the dynamical regime changes; the whole distribution can no longer be fitted to a single simple analytic form and numerical prediction is required. Our model constitutes the basis of a full predictive framework for the economic evolution of an ensemble of firms that can be potentially used to develop simulations and test hypothetical scenarios, as economic crisis or the response to specific policy measures.

I Introduction

Many natural, social and economic phenomena follow power laws. It has been previously ascertained that the distribution of incomes Pareto (1896), size of cities Krugman (1995); Gabaix (1999); Bettencourt (2013); Hernando and Plastino (2012a); Hernando et al. (2013); Hernando and Plastino (2013); Hernando, Hernando, and Plastino (2014); Hernando et al. (2015), evolution of human language Cancho and Solvé (2003), internet and genetic networks Barabási and Albert (1999), and scientific publications and citations Katz (1999); van Raan (2013), all follow power laws. Finding a complete theory for describing these kind of systems seem an impractical task, given the huge amount of degrees of freedom involved these social systems. Notwithstanding, remarkable regularities were reported and studied, such as Zipf’s law Zipf (1949); Newman (2005); Hernando et al. (2009); Cristelli, Batty, and Pietronero (2012), or the celebrated Gibrat’s Law of proportional growth Gibrat (1931), which constitutes important milestones on the quest for a unified framework that mathematically describe predictable tendencies.

Firm size distributions (FSD) are the outcome of the complex interaction among several economic forces. Entry of new firms, growth rates, business environment, government regulations, etc., may shape different FSD. The underlying dynamics that drives the distribution of firms’ sizes is still an issue under intense scrutiny. According to Gaffeo et al. Gaffeo et al. (2012), there is an active debate going on among industrial organization’s scholars, in which log-normal, Pareto, Weibull, or a mixture of them, compete for the best-fitting distributions of FSD. One of the controversial issues is the very definition of “size”, which can be measured by different proxies such as annual sales, number of employees, total assets, etc.

The seminal contribution by Gibrat Gibrat (1931) initiated a research line concerning the formal model that governs firms’ sizes and industry structure. The introduction of a theoretical model that would underlie the industrial demography could be of great help for authorities interested in maintaining fair competence and/or antitrust policies.

Hart and Prais Hart and Prais (1956) find, using a database of large firms, that average growth rates and sizes are independent variables. Quandt Quandt (1966) states that Pareto’s distribution is often rejected when analyzing industries sub-sectors. Other independent empirical studies, carried out by Simon and Bonnini Simon and Bonnini (1958), Mansfield Mansfield (1962), and Bottazzi and Secchi Bottazzi and Secchi (2006), among others, confirm that firms’ growth rates are not related to firm size and that FSD follow a log-normal distribution. Jacquemin and Cardon de Lichtbuer Jacquemin and de Lichtbuer (1973) study the degree of firms and industry concentration in British firms using Fortune’s 200 largest industrial companies outside the United States, ranked according to sales. This study detects an increasing degree of concentration.

Kwasnicki Kwasnicki (1998) affirms that skewed size distributions could be found even in the absence of economies of scale, and that the shape of the distribution is the outcome of innovation in firms. In particular, according to his simulations, cost improving innovations generate Pareto-like skewed distributions. This work also reconciles the finding by Ijiri and Simon Ijiri and Simon (1977) about the concavity toward the origin of the log-log rank size plot. Such concavity could be produced by the evolutionary forces and innovation in the market. Jovanic Jovanic (1982) finds that rates of growth for smaller firms are larger and more variable than those of bigger firms. Similar results are found empirically for Dutch companies by Marsili Marsili (2005). On contrary, Vining Vining (1976) had argued that the origin of the concavity is the existence of decreasing returns to scale.

Segal and Spivak Segal and Spivak (1989) develop a theoretical model in which, under the presence of bankruptcy costs, the rate of growth of small firms is prone to be higher and more variable than that of larger firms. The same model also predicts that, for the largest firms, the sequence of growth rates is convergent satisfying Gibrat’s law, namely

| (1) |

where is the size of the th firm at time , its change in time, and a size-independent growth rate. This model is consistent with some previous empirical evidence, as that of Mansfield Mansfield (1962).

Sutton Sutton (1997) has published a review of the literature on markets’ structure, highlighting the current challenges concerning FSD modelling.

During the 1990s, the interest in FSD experienced a revamp, with the availability of new data-bases. A drawback of early studies was a biased selection of firms. Typically, data comprise only publicly traded firms, i.e., the largest ones. In recent years, new, more comprehensive data sources became available.

Stanley et al. Stanley et al. (1995), use the Zipf-plot technique in order to verify fittings of selected data for US manufacturing firms and find a non-lognormal right tail. Shortly afterwards, Stanley et al. Stanley et al. (1996) encounter that the distribution of growth rates has an exponential form. Kattuman Kattuman (1996) studies intra-enterprise business size distributions, finding also a skewed distribution. Axtell Axtell (2001), using Census data for all US firms, encounters that the FSD is right skewed, giving support for the workings of Pareto’s law. A similar finding is due to Cabral and Mata Cabral and Mata (2003) for Portuguese manufacturing firms, although a log-normal distribution underestimates the skewness of the distribution and is not suitable for its lower tail. In this line, Fu et al. Fu et al. (2005) find that, for pharmaceutical firms in 21 countries, and for US publicly traded firms, growth rates exhibit a central-portion distributed according to a Laplace distribution, with power law tails. Palestrini Palestini (2007) agrees with a power law distribution for firm sizes, although he models firm growth as a Laplace distribution, that could change over business cycles.

According to Riccaboni et al. Riccaboni et al. (2008), the simultaneous study of firm sizes and growth presents an intrinsic difficulty, arising from two facts: (i) the size distribution follows a Pareto Law and (ii) firms’ growth rate is independent of the firm’s size. This latter property is known as the “Law of Proportionate Effect”. Growiec et al. Growiec et al. (2008) study firms’ growth and size distributions using firms’ business units as units of measurements. This study reveals that the size of products follow a log-normal distribution, whereas firm-sizes decay as a power law.

Gaffeo et al. Gaffeo et al. (2012), using data from 38 European countries, find that log mean and log variance size are linearly related at sectoral levels, and that the strength of this relationship varies among countries. Di Giovanni et al. di Giovanni, Levchenko, and Ranciere (2011) find that the exponent of the power law for French exporting firms is lower than for non-exporting firms, raising the argument of the influence of firm heterogeneity in the industrial demography. Additionally, Gallegati and Palestrini Gallegati and Palestrini (2010) and Segarra and Teruel Segarra and Teruel (2012), show that sampling sizes influence the power-law distribution.

One can fairly assert that the concomitant literature has not yet reached a consensus regarding what model could best fit empirical data. An overview of several alternative models is detailed in Ref. de Wit (2005), and references therein. As shown in the above literature review, previous attempts to model growth and sizes of firms have not been entirely successful. In particular, there is a dispute concerning the underlying stochastic process that steers FSD. A possible solution in terms of agent-based model was proposed Farmer and Foley (2009); these models are remarkable as descriptive tools, but they do not furnish an overall panorama because are single-purpose models. Besides, they are sensitive to the initial conditions, and, in some cases, their outcome depends on the length of the simulation time.

The aim of this paper is twofold. First, to develop a thermodynamic-like theoretical model, able to capture typical features of firms’ distributions. We try to uncover the putative universal nature of FSD, which could be characterized by general laws, independent of “microscopic” details. Secondly, to validate our theoretical model using an extensive database of Spanish manufacturing firms during a long time-period.

This paper contributes to the literature in several aspects. First, it provides an explanation for the stochastic distribution of firms’ sizes. The understanding of FSD is relevant for economic policy because it deals with market concentration, and thus, with competition and antitrust policy measures —for example, Naldi Naldi (2003) exhibits a relationship between Zipf’s law and some concentration indices. Second, we apply our model to a large sample of Spanish firms. Third, this work expands the literature on industrial economics modelling.

The paper is organized as follows. First, we present the theoretical framework and perform numerical experiments to validate our analytic approach. Then, we show the empirical application to the Spanish firms. Finally, we draw some discussions and conclusions of our work.

II Theoretical framework

Our framework is based on two fundamental hypothesis:

-

1.

a micro-economic dynamical hypothesis for individual firm growth; and

-

2.

using the maximum entropy principle, with dynamical prior information, for describing macroeconomic equilibrium.

II.1 Microdynamics

For the micro-economical hypothesis, we assume Gibrat’s law of proportional growth (Eq. (1)) as the main mechanism underlying firms’ size evolution. A finite-size term, due to the central limit theorem Hernando et al. (2013), becomes dominant for medium and small sizes, being proportional to the square root of the size. In addition to these two terms, we also assume that non-proportional forces become eventually effective, being dominant for the smallest sizes. Thus, our full dynamical equation is written as

| (2) |

where (, and ) are independent growth rates. It is expected that the growth rates are of a stochastic nature. Thus, a temperature can be defined from their variance . Accordingly, assuming that the variation in the growth rates is much larger than the variation in the observable —as done in Refs. Hernando and Plastino (2012a); Hernando et al. (2015) — the variance of the growth for several realizations becomes

| (3) |

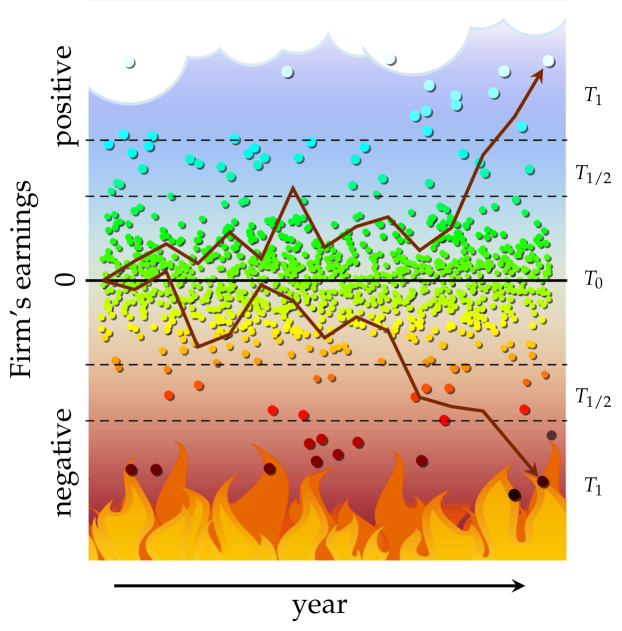

This equation defines three regimes, according to the size: small sizes ; medium sizes ; and large sizes . Because of the existence of the non-proportional term, is allowed to eventually take negative values. This defines an additional set of temperatures for the negative domain, which in principle can be independent of those at the positive one. Since all these temperatures can be measured from the raw data, their properties can be empirically determined. In Fig. 1 we show a conceptual sketch of the ensemble of firms evolving in time as random walkers along the different regimes, with the corresponding temperature and dynamics for each of them.

II.2 MaxEnt Principle

For an ensemble of firms following Eq. (1), we assume that dynamical equilibrium is asymptotically reached when some macroscopic constraints are obeyed. We cite the average total number of firms , the typical wealthiness of a given particular region, or any other objective observable. In view of the success of an entropic procedure for describing equilibrium distributions in other social systems (as, e.g., city population distributions), we take as our macroeconomic hypothesis the Principle of Maximum Entropy (MaxEnt) with dynamical prior information Hernando and Plastino (2012a); Hernando et al. (2013); Hernando and Plastino (2012b); Hernando, Plastino, and Plastino (2012), to predict the equilibrium density of the system. We focus our analytic derivation on that particular regime that has received most attention in the literature: the proportional growth-one: for the largest sizes. According to Ref. Hernando and Plastino (2012a), the entropy of a system following Gibrat’s law is measured in terms of the new dynamical variable (where is some reference value, in our case, the transition size ) which linearizes the dynamical equation as . Thus, we write the macroscopic entropy for the system’s density distribution for firms as

| (4) |

The equilibrium density is obtained by extremization of under the empirical constraints Hernando and Plastino (2012b); Hernando, Plastino, and Plastino (2012), such as the total number of firms, the minimum size of a firms, among others. Lacking them, as sometimes happens in physics, we will use a symmetry criterion Griffiths (1987): employ constraints that preserve a symmetry of scale of , i.e. translation symmetry in . For this, we define an energy function, , that depends on powers of the dynamical variable , namely

| (5) |

where are the central moments of and the coupling constants. The maximization problem is written as , where is a Lagrange multiplier ( become then the multipliers for each term), and the general solution is of the form

| (6) |

The values of the multipliers are obtained by solving the system of Lagrange equations, for the distribution of Eq. (6).

II.3 Connection with Thermodynamics

We consider, for simplicity, the linear regime with only the first two moments (a constraint on the average total number of firms ) and (a constraint on the mean value written as ). Since the equations are formally equivalent to those found in Thermodynamics, and traditionally the multipliers associated with these constraints are Reif (1965); Balian (2006) , , , we have a thermodynamic potential

| (7) |

where . The variational problem becomes . We obtain the distribution

| (8) |

The distribution is cast in terms of the observable as

| (9) |

where and . Accordingly, we obtain a power law density. Useful for analyzing the empirical data is the complementary of the cumulative distribution , that reads

| (10) |

The solutions of the Lagrange equations lead to

| (11) |

and to the equation of state:

| (12) |

This is the relevant equation for interpreting the empirical data, since can be measured from the data and can be interpreted thanks to the thermodynamic analogy.

Indeed, comparing our results with those of a physical system, one can identify with the chemical potential. We interpret as the “cost” for including/creating or excluding/extinguishing firms in the proportional large-size regime. Following MaxEnt Hernando and Plastino (2012a); Hernando et al. (2013); Hernando and Plastino (2012b), the system is in contact with a reservoir of firms, and tends to minimize . Since , for any new firm, in the proportional regime, decreases , making it more likely the emergence of a flow of firms entering into the system. However, for , any new firm will increase the value of , allowing for a flow of firms exiting the system. In the particular case there is no cost for the flow of firms, in what we expect to be an equilibrium, stable, and healthy situation for a capitalist economy.

The thermodynamic variable defines the exponent of the distribution, and can be interpreted as a measure of the typical wealth of a region. Specifically, it determines the scale of the size of firms, because it constraints the geometric mean of . Indeed, the use of the geometric mean instead of the mean is common for systems with scale invariance, where long-tailed distributions have undefined moments but well-defined log-moments IHD (2014); RPI (2013). This value will change from one economy to other one.

Thanks to the equation of state Eq. (12), we can provide an intuitive, physically-based interpretation of that exponent:

-

•

for () the system favors the extinction of firms;

-

•

for () the system favors the creation of firms;

-

•

for () the system freely creates and extinguishes firms.

This last particular case corresponds to the Zipf’s law distribution, namely

| (13) |

III Numerical experiments

In aim of testing our theoretical procedure we have performed numerical experiments in terms of random walkers via a Monte Carlo simulation (MC). At the initial time, the random walkers are randomly located using a uniform distribution. We assume independent stochastic Wiener coefficients for different firms, within each of the three regimes or, more explicitly,

| (14) |

where defines the specific dynamical regime, as in Eq. (2). In order to make explicit the mechanisms that govern the dynamics, we will use a reduced approach, in which each of the regimes, according to the size , evolves independently. Therefore, instead of simulating the whole dynamics, i.e. Eq. (2), we aim to understand the particular contribution of each term in that equation. Henceforth, we will focus in the interplay between the linear and proportional growth regimes, disregarding the intermediary regime. To achieve this goal, we use the following equation for the microscopic dynamics:

| (15) |

where defines the border between the linear and the proportional regimes. Since the number of walkers in the proportional regime is not constrained, we follow here the given recipe for a Grand canonical ensemble Reif (1965); Balian (2006) where is fixed and the fluctuation in the number of walkers is determined by the probabilities of including () or extracting () a walker as

| (16) |

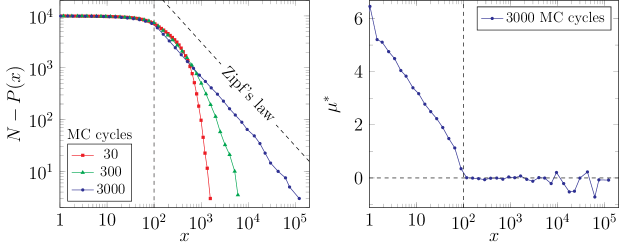

According to these probabilities, in an ensemble with any walker can leave or enter into the system without any restriction. Additionally, following Eq. (11) the constraint should be fulfilled. We have performed several realizations with different initial conditions, and let the system evolve until reaching equilibrium. In Fig. 2, we show the rank plot, Eq. (10), for different simulation times, measured in MC steps. Here we choose . We see that the equilibrium distribution (for MC cycles) follows the Zipf’s law. Moreover, we show in Fig. 2 the chemical potential for the equilibrium distribution. We see that, up to some fluctuations, the constraint is respected.

We find that the equilibrium distribution does not depend on the initial conditions, and follows Zipf’s law: for large values, the complementary of the cumulative distribution follows Eq. (13), as predicted by our thermodynamic framework. The distribution deviates from the analytic result, Eq. (13), as the size of reaches the transition critical valued . In view of these results, we numerically validate our analytic procedure.

IV Empirical application

In order to empirically verify our theoretical model, we consider the Spanish SABI database Dijk (2001); SAB , which is a comprehensive one for all firms that have the obligation to disclose balance sheets in the Spanish Mercantile Register. Our sample consists of firms along a decade, with more than firms per year. We select those firms which have been active at any time during the last 10 years and use as our observable for the th firm at year the so-called Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). This quantity is widely employed for assessing companies’ performances. It is homogeneous across companies and is not affected by different forms of financing. We believe that our proxy for size is a clear indicator of both corporate performance and size.

IV.1 Microdynamics

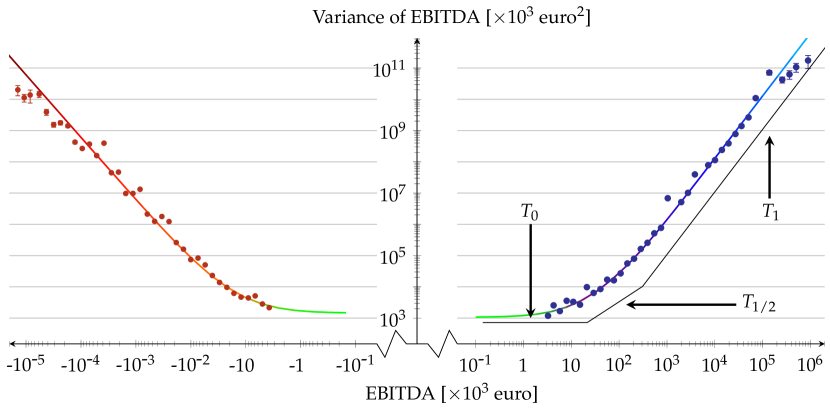

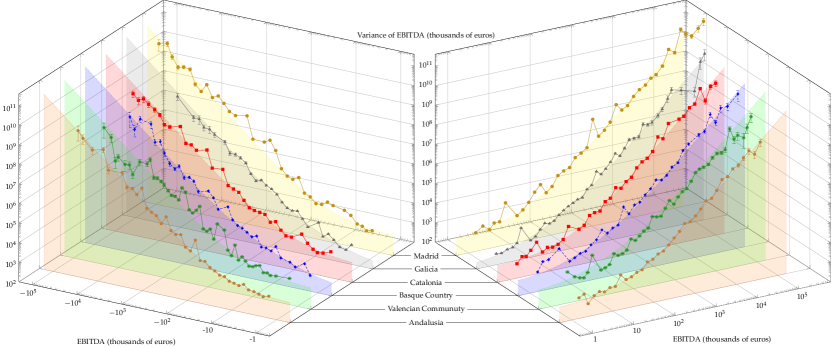

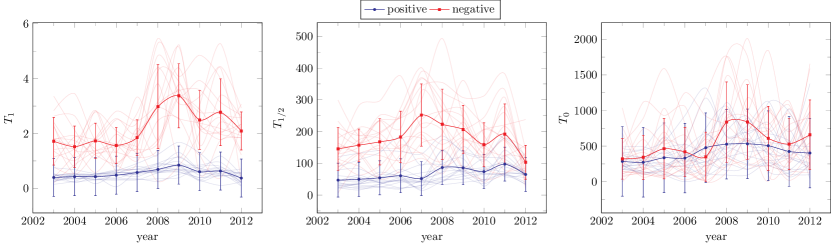

We first test our microscopic dynamical hypothesis by measuring the variance of the EBITDA growth for each year. Since the EBITDA values can be negative, we study separately positive and negative domains. We first analyze all the Spanish firms in the same set, displaying in Fig. 3 the dependence of the growth-variance on the EBITDA for the year 2009. We find a remarkable match to Eq. (2) for both positive and negative domains. The transition to proportional growth takes place, in this case, at euro. Additionally, in both domains, the linear regime temperature, , is of the same order of magnitude. As shown in the Supporting Information, all the available data for 10 years match Eq. (2), with slightly changing temperatures. A similar analysis, made per each Spanish autonomous community, shows that the dynamics is also obeyed individually by regions, as shown in Fig. 4. We do not find any exception for all the 15 Spanish autonomous communities during these 10 years. In view of these results, we empirically confirm the validity of the dynamical equation (2). Additionally, we find that the temperatures and for the negative domain are significantly higher than those for the positive one. Remarkable, as shown in Fig. 5, can be considered the same for positive and negative EBITDA, indicating that the same non-proportional regime is connecting both domains.

IV.2 Macroequilibrium

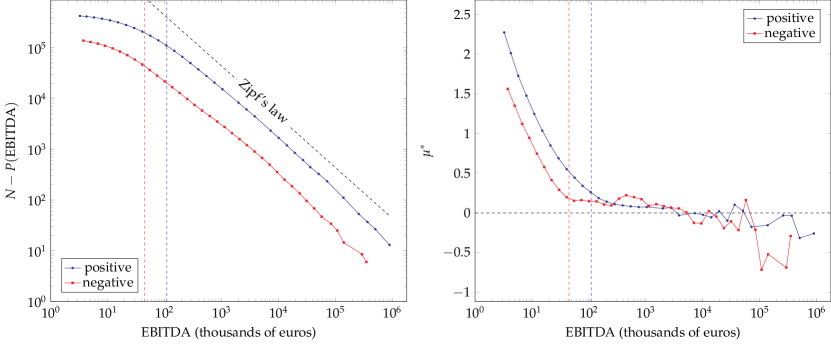

Once the dynamical equation has been validated, we pass to the rank-distributions. We plot in Fig. 6 the complementary cumulative function for all Spanish firms in 2009, including those with positive and negative EBITDA. We observe that for large values of this function the power law Eq. (13) is followed, as predicted by our thermodynamic equilibrium hypothesis, with an exponent very close to that of Zipf’s law . For smaller values, the distribution deviates from the power law. We have checked that this deviation takes place at about the same transition value , as predicted by our numerical experiments. This is a compelling evidence for the relation between the dynamics and the distribution given by our theoretical framework. We also measure the chemical potential , via the equation of state Eq. (12). This chemical potential is, in general, with some deviations, close to , value for which the creation/extinction of firms has no cost for the energy potential function . We find the same picture when studying the firms’ distribution per each community. In general, all distributions are very close to the Zipf’s regime. In view of these results, we consider that our theoretical framework properly describes the dynamics and equilibrium of the ensemble of Spanish firms.

V Discussion

Some interesting assertions can be made with regards to our theoretical framework. The most relevant, the thermodynamic interpretation of the exponent of the long-tail in size distribution. Thanks to the equation of state Eq. (12) we provide for the first time a clear explanation of this exponent, linking that adimensional number with a dynamical, intuitive mechanism as the cost to the system of creating or extinguish a firm, measured by the chemical potential . This interpretation can be used to measure the macroscopic effect of particular economical policies, and to measure how healthy is a capitalist-based economy. We find that, in general, the value of in Spanish regions is close to zero —as shown in Fig. 6— indicating the freedom of creating or extinguishing a firm.

Additionally, we settle here the form of the microscopic dynamics by Eq. (2), and its dependence with the size. Contrarily to other social systems following proportional growth Hernando and Plastino (2012a); Hernando et al. (2015); Eliazar (2015), here exists the possibility of negative values. This requires an additional dynamical mechanism for the evolution of firms, that is successfully included in our current approach as a linear term dominant for small sizes. Firms can be classified according to the dynamical regime, even if they are in the negative (losses) or positive (gain) domain. In a pictorial way, we can talk about heaven (positive proportional regime), hell (negative proportional regime), or purgatory (linear regime). The fact that the temperatures in the positive domain are systematically smaller than in the negative one, as illustrated in Fig. 5, can be summarized as hell is warmer than heaven. Thus, a firm in hell losses money in a faster fashion than it would equivalently earn it in heaven.

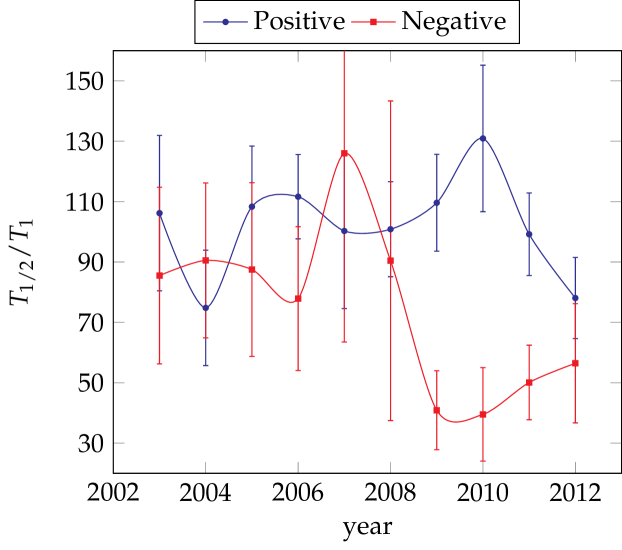

We also find useful as macroeconomic indicator the position of the transition zone between medium and proportional growth regime in the negative domain, that gives an estimate of the minimum losses a firm can afford before going bankrupt —or metaphorically, the hell’s gate. Similarly, the same transition but in the positive domain provides an estimation of the success region for firms —that we might wish to call heaven’s door. Fig. 7 shows both transition values from 2003 to 2012 as measured by the respective temperature ratios . We observe that, before the 2008 Global Financial Crisis, both transitions were approximately equivalent in size, exhibiting a symmetry between positive and negative regimes. Right before this crisis, the negative value reached its maximum, indicating some abnormal economic growth, potentially related with the speculative bubble. The confidence interval for this specific year is higher than the absolute value, indicating that this phenomenon did not happen with the same intensity among all the autonomous communities. Finally, in the succeeding years, the negative value was reduced to a half, augmenting the probability of firms to go bankrupt; whereas the positive transition also decreased, although not as rapidly as in the negative domain. After the burst of the crisis, both transitions tend to converge again to a similar value, but lower than before the crisis. Because the equation of state Eq. (12) and the constrained value of , this lower value reflects a general reduction of the wealth in the whole system, because it diminishes, on average, the scale of the successful firms at the proportional regime.

As a final remark, the numerical simulation provided here based on walkers under the Grand canonical ensemble opens the possibility of developing simulation tools where economical forces can be introduced in the same fashion as done for physical forces for gases and liquids. Indeed, we open a bridge between the mathematical tools used in statistical mechanics and firms’ dynamics. Our analytic and numerical procedures can be used to deeply analyze the empirical data measuring and parameterizing the economic forces in play, and develop a full quantitative theory about these dynamics. Work in this line is in progress.

VI Conclusions

We advanced in this paper a complete thermodynamic framework which accommodates the firm size distribution of a given region. We propose an empirically proof a microscopic dynamical hypothesis, and show how the firms obey the maximum entropy principle at the macroscopic level. We analytically proof the connection between microscopic dynamics and equilibrium firm’s size-distributions via MaxEnt, and formulate the equation of state that relates the exponent of the long tail in size distributions with a well-known thermodynamic observable as the chemical potential. This lead to a clear and intuitive interpretation of the exponents, showing that can be used to measure the health of a economy. Indeed, the emergence of Zipf’s law is associated with the free cost to the system of creating and extincting firms, as expected in a capitalist-based economy. All these theoretical considerations have been validated by comparison with empirical data concerning Spanish firms, in a window of a decade. We expect this work to be a first step towards the formalization of a theory of the evolution of firms that will yield underlying forces and laws of evolution.

References

- Pareto (1896) V. Pareto, Cours d’Economie Politique (Genève: Droz, 1896).

- Krugman (1995) P. R. Krugman, Japan and the World Economy 7, 371 (1995).

- Gabaix (1999) X. Gabaix, Q J Econ 114, 739 (1999).

- Bettencourt (2013) L. M. A. Bettencourt, Science 340, 1438 (2013).

- Hernando and Plastino (2012a) A. Hernando and A. Plastino, Phys Rev E - Stat, Nonlinear, Soft Matter Phys 86, 066105 (2012a).

- Hernando et al. (2013) A. Hernando, R. Hernando, A. Plastino, and A. R. Plastino, J. R. Soc. Interface 10, 20120758 (2013).

- Hernando and Plastino (2013) A. Hernando and A. Plastino, Phys Lett A 377, 176 (2013).

- Hernando, Hernando, and Plastino (2014) A. Hernando, R. Hernando, and A. Plastino, J. R. Soc. Interface 11, 20130935 (2014).

- Hernando et al. (2015) A. Hernando, R. Hernando, A. Plastino, and E. Zambrano, J. R. Soc. Interface 12, 20141185 (2015).

- Cancho and Solvé (2003) R. F. Cancho and R. V. Solvé, Proc Natl Acad Sci U S A 100, 788 (2003).

- Barabási and Albert (1999) A. L. Barabási and R. Albert, Science 286, 509 (1999).

- Katz (1999) S. Katz, Res Policy 28, 501 (1999).

- van Raan (2013) A. F. J. van Raan, PLoS ONE 8, e59384 (2013).

- Zipf (1949) G. K. Zipf, Human Behavior and the Principle of Least Effort (Addison-Wesley, 1949).

- Newman (2005) M. J. Newman, Contemporary physics 46, 323 (2005).

- Hernando et al. (2009) A. Hernando, D. Puigdomèech, D. Villuendas, C. Vesperinas, and A. Plastino, Phys Lett A 374, 18 (2009).

- Cristelli, Batty, and Pietronero (2012) M. Cristelli, M. Batty, and L. Pietronero, Scientific Reports 2, 812 (2012).

- Gibrat (1931) R. Gibrat, Les Inegalité, economiques: applications aux inéqualité, des richesses, à la concentration des entreprises, aux populations des villes, aux statistiques des familles, etc., d’une loi nouvelle: la loi de l’effect proportionnel (Paris, Librairie du Recueil Sirey, 1931).

- Gaffeo et al. (2012) E. Gaffeo, C. D. Guilmi, M. Gallegati, and A. Russo, Ecol Comp 11, 109 (2012).

- Hart and Prais (1956) P. E. Hart and S. J. Prais, J R Stat Soc 119, 150 (1956).

- Quandt (1966) R. E. Quandt, Am Econ Rev 56, 416 (1966).

- Simon and Bonnini (1958) H. A. Simon and C. P. Bonnini, Am Econ Rev 48, 607 (1958).

- Mansfield (1962) E. Mansfield, Am Econ Rev 52, 1023 (1962).

- Bottazzi and Secchi (2006) G. Bottazzi and A. Secchi, RAND Journal of Economics 37, 235 (2006).

- Jacquemin and de Lichtbuer (1973) A. P. Jacquemin and M. C. de Lichtbuer, Eur Econ Rev 4, 393 (1973).

- Kwasnicki (1998) W. Kwasnicki, Struc C Econ Dynam 9, 135 (1998).

- Ijiri and Simon (1977) Y. Ijiri and H. A. Simon, Skew distribution and the size of business firms (North-Holland, Amsterdam, 1977).

- Jovanic (1982) B. Jovanic, Econometrica 50, 649 (1982).

- Marsili (2005) O. Marsili, Rev Ind Org 27, 303 (2005).

- Vining (1976) D. R. Vining, J Pol Econ 84, 369 (1976).

- Segal and Spivak (1989) U. Segal and A. Spivak, Eur Econ Rev 33, 159 (1989).

- Sutton (1997) J. Sutton, J Econ Lit 35, 40 (1997).

- Stanley et al. (1995) M. H. R. Stanley, S. V. Buldyrev, S. Havlin, R. N. Mantegna, M. A. Salinger, and H. E. Stanley, Econ Lett 49, 453 (1995).

- Stanley et al. (1996) M. H. R. Stanley, L. A. N. Amaral, S. V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M. A. Salinger, and H. E. Stanley, Nature 379, 804 (1996).

- Kattuman (1996) P. A. Kattuman, Struc C Econ Dynam 7, 479 (1996).

- Axtell (2001) R. L. Axtell, Science 293, 818 (2001).

- Cabral and Mata (2003) L. M. B. Cabral and J. Mata, Am Econ Rev 93, 1075 (2003).

- Fu et al. (2005) D. Fu, F. Pammolli, S. V. Buldyrev, M. Riccaboni, K. Matia, K. Yamasaki, and H. E. Stanley, Proc Natl Acad Sci U S A 102, 18801 (2005).

- Palestini (2007) A. Palestini, Econ Lett 94, 367 (2007).

- Riccaboni et al. (2008) M. Riccaboni, F. Pammolli, S. V. Buldyrev, L. Ponta, and H. E. Stanley, Proc Natl Acad Sci U S A 105, 19595 (2008).

- Growiec et al. (2008) J. Growiec, F. Pammolli, M. Riccaboni, and H. E. Stanley, Econ Lett 98, 207 (2008).

- di Giovanni, Levchenko, and Ranciere (2011) J. di Giovanni, A. A. Levchenko, and R. Ranciere, J Int Econ 85, 42 (2011).

- Gallegati and Palestrini (2010) M. Gallegati and A. Palestrini, Transdiscipl Perspect Econ Complex 75, 69 (2010).

- Segarra and Teruel (2012) A. Segarra and M. Teruel, J Econ Behav Org 82, 314 (2012).

- de Wit (2005) G. de Wit, Int J Ind Organ 23, 423 (2005).

- Farmer and Foley (2009) J. D. Farmer and D. Foley, Nature 460, 685 (2009).

- Naldi (2003) M. Naldi, Econ Lett 78, 329 (2003).

- Hernando and Plastino (2012b) A. Hernando and A. Plastino, Eur Phys J B 85, 293 (2012b).

- Hernando, Plastino, and Plastino (2012) A. Hernando, A. Plastino, and A. R. Plastino, Eur Phys J B 85, 147 (2012).

- Griffiths (1987) D. J. Griffiths, Introduction to Elementary Particles (Wiley, John & Sons, 1987).

- Reif (1965) F. Reif, Fundamentals of Statistical and Thermal Physics (McGraw–Hill, 1965).

- Balian (2006) R. Balian, From microphysics to macrophysics. Vol I and II (Springer Science & Business Media, 2006).

- IHD (2014) “Human development report,” United Nations (2014).

- RPI (2013) “News release,” Office for National Statistics – UK (10 January, 2013).

- Dijk (2001) B. V. Dijk, SABI (Bureau van Dijk, Paris, 2001).

- (56) “SABI Sistema de Análisis de balances ibéricos,” Bureau van Dijk Electronic Pub, Brussels [online database] http://www.bvdinfo.com/en-gb/products/company-information/national/sabi.

- Eliazar (2015) I. Eliazar, Annals of Physics , (in press) (2015).