capbtabboxtable[][\FBwidth]

Regularization-free estimation in trace regression with symmetric positive semidefinite matrices

Abstract

Over the past few years, trace regression models have received considerable attention in the context of matrix completion, quantum state tomography, and compressed sensing. Estimation of the underlying matrix from regularization-based approaches promoting low-rankedness, notably nuclear norm regularization, have enjoyed great popularity. In the present paper, we argue that such regularization may no longer be necessary if the underlying matrix is symmetric positive semidefinite (spd) and the design satisfies certain conditions. In this situation, simple least squares estimation subject to an spd constraint may perform as well as regularization-based approaches with a proper choice of the regularization parameter, which entails knowledge of the noise level and/or tuning. By contrast, constrained least squares estimation comes without any tuning parameter and may hence be preferred due to its simplicity.

1 Introduction

Trace regression models of the form

| (1) |

where is the parameter of interest to be estimated given measurement matrices and observations contaminated by errors , , have attracted considerable interest in high-dimensional statistical inference, machine learning and signal processing over the past few years. Research in these areas has focused on a setting with few measurements and being (at least approximately) of low rank . Such setting is relevant, among others, to problems such as matrix completion [8, 26], compressed sensing [7, 21], quantum state tomography [14] and phase retrieval [9]. A common thread in these works is the use of the nuclear norm of a matrix as a convex surrogate for its rank [22] in regularized estimation amenable to modern optimization techniques. This approach can be seen as natural generalization of -norm (aka lasso) regularization for the standard linear regression model [28] that arises as a special case of model (1) in which both and the measurement matrices are diagonal. It is inarguable that in general regularization is essential if . However, the situation is less clear if is known to satisfy additional constraints that can be incorporated in estimation. Specifically, in the present paper we consider the case in which and is known to be symmetric positive semidefinite (spd), written as with denoting the positive semidefinite cone in the space of symmetric real-valued matrices . The set deserves specific interest as it includes covariance matrices and Gram matrices in kernel-based learning methods [24]. It is rather common for these matrices to be of low rank (at least approximately), given the widespread use of principal components analysis and low-rank kernel approximations [33]. In the present paper, we focus on the usefulness of the spd constraint for estimation. We argue that if is spd and the measurement matrices obey certain conditions, constrained least squares estimation

| (2) |

may perform similarly well in prediction and parameter estimation as approaches employing nuclear norm regularization with proper choice of the regularization parameter, including the interesting regime , where . Note that the objective in (2) only consists of a data fitting term and is hence convenient to work with in practice since one does not need to choose any parameter. Our findings can be seen as a non-commutative extension of recent results on non-negative least squares estimation for high-dimensional linear regression with non-negative parameters [20, 25]. In these papers it is shown that for certain design matrices, non-negative least squares can achieve comparable performance to -norm regularized estimation with regard to prediction, estimation and support recovery, thereby generalizing prior work [4, 13, 31] on sparse recovery of a non-negative vector in a noiseless setting.

Related work. Model (1) with has been studied in several recent papers. A good deal of these papers consider the setup of compressed sensing according to which the matrices can be chosen by the user, with the goal to minimize the number of observations required to (approximately) recover .

In [32], the problem of exactly recovering being low-rank from noiseless observations (, ) by solving a linear feasibility problem over the positive semidefinite cone is considered, which is equivalent to the proposed least squares problem (1) in a noiseless setting. Apart from the fact that we primarily study a noisy setting, we shall argue below that in the setup of compressed sensing the measurement matrices studied in [32] constitute an unfavourable choice relative to those recommended in the present paper.

In [10], recovery from rank-one measurements is considered, i.e., for

| (3) |

As opposed to [10], where estimation based on nuclear norm regularization is proposed, the present work is devoted to regularization-free estimation. While rank-one measurements as in (3) are also in the center of interest herein, our framework is not limited to this specific case.

In [5], rank-one measurements are considered for general . Specializing to , the authors discuss an application of (3) to covariance matrix estimation given only one-dimensional projections of the data points, where the are i.i.d. from a distribution with zero mean and covariance matrix . In fact, when using observations , one obtains

| (4) |

On the other hand, in [5], no specific attention is given to the spd constraint: the convex program proposed therein, which can be seen as a modification of the approach in [10], applies to general symmetric matrices and does not enforce positive semidefiniteness.

Specializing model (3) further to the case in which also has rank one, one obtains the quadratic model

| (5) |

which (with complex-valued ) is relevant to the problem of phase retrieval [17] that has received some attention recently. The approach

of [9] treats (5) as an instance of (1) and uses nuclear norm regularization to enforce rank-one solutions.

In follow-up work [6], the authors show a refined

recovery result stating that imposing an spd constraint without regularization suffices. A similar result

has been proven independently by [12]. However, the results in both [6] and [12] only concern model (5).

In [18], is

assumed to be a complex Hermitian positive semidefinite matrix of unit trace, which is the

setting in quantum state tomography. While the setting as well as the measurement matrices

under consideration are different from ours, a notable point of contact to our work can be

seen in the fact that the negative von Neumann entropy111The von Neumann entropy of a positive definite Hermitian matrix is given by the entropy of its eigenvalues, which is the proposed regularizer in [18],

does not promote low rankedness, but constitutes one possible way of enforcing positive definiteness. At the same time,

adaptivity of the approach to low rankedness is established in [18].

Outline and contributions of the paper. In Section 2, we study statistical properties of constrained least squares estimation (2) in small sample () and low-rank settings. Specifically, we introduce certain geometric conditions associated with the measurements that allow us to derive non-asymptotic upper bounds on the prediction and estimation error indicating that (2) can achieve competitive performance while being regularization-free. On the other hand, we show that without extra conditions on the measurements , the performance of (2) can be as poor as that of unconstrained least squares. Section 3 contains numerical results based on synthetic and real world data that support or complement our theoretical results. Our findings are briefly summarized in Section 4. The appendix contains the proofs.

Notation. We here gather notation and terminology used throughout the paper. For an integer , let denote the Euclidean vector space of real matrices with inner product , . The set of real symmetric matrices is a subspace of of dimension . Each element of has an eigen-decomposition , where is the sequence of real eigenvalues with corresponding orthonormal eigenvectors , , and . For , can be endowed with a norm given by the mapping called the Schatten--norm. In particular, for we speak of the nuclear norm, while yields the Frobenius norm . We set , the spectral norm of . We denote by the Schatten--norm unit sphere and set , where is the positive semidefinite cone in . The symbols are understood with respect to the semidefinite ordering, e.g. means that . For and , denotes the usual -norm. For set and a real number , , , and for , .

It is convenient to re-write model (1) as

where , and is a linear map defined by , , referred to as sampling operator. Its adjoint is given by the map .

2 Analysis

Preliminaries. Throughout this section, we consider a special instance of model (1) in which

| (6) |

The assumption that the errors follow a Gaussian distribution is made for convenience as it simplifies the stochastic part of our analysis, which could be extended to cover error distributions with sub-Gaussian tails.

Note that without loss of generality, we may assume that the are symmetric. In fact, any can be decomposed as

denote the Euclidean projections of onto and its orthogonal complement (the subspace of skew-symmetric matrices), respectively. Accordingly, since , we have .

In the sequel, we study the statistical performance of the constrained least squares estimator

| (7) |

under model (6) with respect to prediction and estimation. More specifically, under certain conditions on , we shall derive bounds on

| (8) |

where will be referred to as “prediction error” below.

The most basic method for estimating is ordinary least squares (ols) estimation

| (9) |

which is computationally much simpler than (7). While obtaining (7) requires techniques from convex programming, it is straightforward to compute (9) by solving a linear system of equations in variables. On the other hand, the prediction error of ols scales as , where can be as large as , in which case the prediction error vanishes asymptotically only if as . Moreover, the estimation error is unbounded unless . Research conducted over the past few years has consequently focused on methods that deal successfully with the situation if the target possesses additional structure, notably low-rankedness. Indeed, if has rank , the intrinsic dimension of the problem becomes (roughly) . Rank-constrained estimation or regularized estimation with the matrix rank as regularizer yield computationally intractable optimization problems in general. In a large body of work, nuclear norm regularization, which can be seen as a convex surrogate of rank regularization, is considered as a computationally convenient alternative for which a series of adaptivity properties to underlying low-rankedness has been established, e.g. [7, 19, 21, 22, 23]. Complementing (9) with nuclear norm regularization gives rise to the estimator

| (10) |

where is a regularization parameter. In case an spd constraint is imposed (10) becomes

| (11) |

Our analysis aims at elucidating potential advantages of the spd constraint in the constrained least squares problem (7) from a statistical point of view. It turns out that depending on properties of , the behaviour of can range from a performance similar to the least squares estimator on the one hand to a performance similar to the nuclear norm regularized estimator with properly chosen/tuned on the other hand. The latter case appears to be remarkable inasmuch as may enjoy similar adaptivity properties as nuclear norm regularized estimators even though is obtained from a pure data fitting problem without any explicit form of regularization.

2.1 Negative results

We first discuss examples of for which the spd-constrained estimator does not improve (substantially) over the unconstrained estimator . At the same time, these examples provide some clues on conditions that need to be imposed on to achieve substantially better performance.

Example 1: equivalence of constrained and unconstrained least squares

Let be even and consider measurement matrices of the form

for matrices , . For arbitrary, we can partition

where is the top block of etc. We have

Hence enters the least squares objective (2) via the difference of the top and bottom blocks. Since for any dimension

the spd constraint becomes vacuous and can be dropped from (7).

Example 2: Orthonormal design

The following statement indicates that for orthonormal design, the prediction error of cannot be

expected to improve over that of by substantially more than a constant factor .

Proposition 1.

Let so that , let and let be an orthonormal basis of . Then, in probability as .

By contrast, it is desired that as .

Example 3: Random Gaussian design

Consider the Gaussian orthogonal ensemble (GOE) of random matrices

Random Gaussian measurements are common in compressed sensing-type settings, see e.g. [7, 21]. It is hence of interest to study measurements , , in the context of the constrained least squares problem (7). The following statement, which follows from results in [2], points to a serious limitation associated with the use of such measurements.

Proposition 2.

Consider measurements , . Then, for any , if , with probability at least , there exists , such that .

Proposition 2 has the following implications.

-

•

If the number of measurements drops below one half of the ambient dimension , estimating based on (7) becomes ill-posed; the estimation error is unbounded, irrespective of the rank of .

-

•

Geometrically, the consequence of Proposition 2 is that the convex cone contains . Unless is contained in the boundary of (we conjecture that this event has measure zero), this means that , i.e., the spd constraint becomes vacuous.

Remarks.

-

1.

In [32], the following noiseless analog to the constrained least squares problem (7) is considered:

(12) where , . The authors prove that for all , there exists so that if , is the unique solution of the feasibility problem (12) as long as . While this implies that the spd constraint allows undersampling (i.e., ), it is not clear to what extent undersampling is possible, i.e., how small could possibly be. Proposition 2 yields that cannot be smaller than .

-

2.

It is of interest to relate Proposition 2 to corresponding results on the vector case (equivalent to having diagonal and diagonal ) in [13]. Compared to Proposition 2, the corresponding result in [13] applies to a much wider class of random measurement matrices including all random matrices with i.i.d. entries from a symmetric distribution around zero. It is thus natural to ask whether Proposition 2 holds more generally for all Wigner matrices [27].

- 3.

2.2 Slow rate bound on the prediction error

We now turn to the first positive result on the spd-constrained least squares estimator under an additional condition on the sampling operator . Specifically, the prediction error will be bounded as

| (13) |

with typically being of the order (up to logarithmic factors). The rate in (13) can be a significant improvement of what is achieved by if is small. If that rate coincides with those of the nuclear norm regularized estimators (10), (11) with regularization parameter , cf. Theorem 1 in [23]. For nuclear norm regularized estimators, the rate is achieved for any choice of and is hence slow in the sense that the squared prediction error only decays at the rate instead of . Therefore, we refer to (13) as “slow rate bound”.

Condition on . In order to arrive at a suitable condition to be imposed on so that (13) can be achieved, it makes sense to re-consider Example 3 to identify possible obstacles. Proposition 2 states that as long as is bounded away from from above, there is a non-trivial such that . Equivalently,

In this situation, it is in general not possible to derive a non-trivial upper bound on the prediction error as may imply that in which case . To rule this out, the condition appears to be a natural requirement. More strongly, one may ask for the following:

| (14) |

This condition is sufficient to obtain a slow rate bound in the vector case, cf. Theorem 1 in [25]. However, the condition required for the slow rate bound in Theorem 1 below is somewhat stronger than (14).

Condition 1.

There exist constants and such that , where for

It follows from

| (15) | ||||

that Condition 1 is in fact stronger than (14). Below, we provide a sufficient condition on that implies Condition 1.

Proposition 3.

Suppose that there exists , , and constants such that

Then for any , satisfies Condition 1 with and .

The condition of Proposition 3 can be phrased as having a positive definite matrix in the unit ball of the range of , which, after scaling by , has its smallest eigenvalues bounded away from zero and condition number bounded from above. As a simple example, suppose that . Invoking Proposition 3 with and , we find that Condition 1 is satisfied with and . A more interesting example is random design where the are (sample) covariance matrices, where the underlying random vectors satisfy appropriate tail or moment conditions.

Corollary 1.

Let be a probability distribution on with second moment matrix satisfying . Consider the random matrix ensemble

| (16) |

Suppose that and let and . Under the event , satisfies Condition 1 with

It is instructive to spell out Corollary 1 with as the standard Gaussian distribution on . The matrix equals the sample covariance matrix computed from samples. It is well-known (see e.g. [11]) that for large, and concentrate sharply around and , respectively, where . Hence, for any , there exists so that if , it holds that . Similar though weaker concentration results for are available for the broad class of distributions having finite fourth moments [30]. When specialized to , Corollary 1 yields a statement about made up from random rank-one measurements , , cf. (3). The preceding discussion indicates that Condition 1 tends to be satisfied in this case.

Main result of this subsection. We are now in position to state the following theorem.

Theorem 1.

Remarks.

- 1.

- 2.

-

3.

For later reference, it is of interest to evaluate the term for with as the standard Gaussian distribution. It is proved in Appendix F that with high probability, it holds that

as long as .

2.3 Bound on the estimation error

In the previous subsection, we did not make any assumptions about apart from . Henceforth, we suppose that is of low rank and study the performance of the constrained least squares estimator (7) for prediction and estimation in such setting.

Preliminaries. Let be the eigenvalue decomposition of , where

where is diagonal with positive diagonal entries. Consider the linear subspace

From , it follows that is contained in the orthogonal complement

which has dimension if . The image of under is denoted by .

Conditions on . We now introduce the key quantities the bound in this subsection depends on.

Separability constant.

Restricted eigenvalue.

As indicated by the following statement concerning the noiseless case, for bounding , it is inevitable to have lower bounds on the above two quantities.

Proposition 4.

Correlation constant. Moreover, we make use of the following the quantity. It is not yet clear to us whether control of this quantity is intrinsically required, or whether its appearance in our bound is for merely technical reasons.

We are now in position to provide a bound on .

Theorem 2.

Remark. Given the above bound on , it is possible to

obtain an improved bound on the prediction error scaling with in place of ,

cf. (31) in Appendix E.

The quality of the bound of Theorem 2 depends on how the quantities , and scale

with , and , which is highly design-dependent. Accordingly, the estimation error in nuclear norm can be

non-finite in the worst case and in the best case.

-

•

The quantity is specific to the geometry of the constrained least squares problem (7) and hence of critical importance. For instance, it follows from Proposition 2 that for standard Gaussian measurements, with high probability once . The situation can be much better for random spd measurements (16) as exemplified for measurements with in the subsequent section. Specifically, it turns out that as long as .

-

•

It is not restrictive to assume that the quantity is positive. Indeed, without that assumption, even an oracle estimator based on knowledge of the subspace would fail. Reasonable sampling operators have rank so that the nullspace of only has a trivial intersection with the subspace as long as .

-

•

For fixed , computing entails solving a biconvex (albeit non-convex) optimization problem in the variables and . Alternating optimization (also known as block coordinate descent) is a practical approach to such optimization problems for which a globally optimal solution is out of reach. In this manner we explore the scaling of numerically as done for . We find that so that apart from the regime , without ruling out the possibility of undersampling, i.e. .

3 Numerical results

In this section, we provide a series of empirical results regarding properties of the estimator . In particular, its performance relative to regularization-based methods is explored. We also present an application to spiked covariance estimation for the CBCL face image data set and stock prices from NASDAQ.

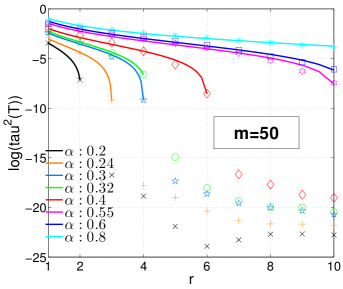

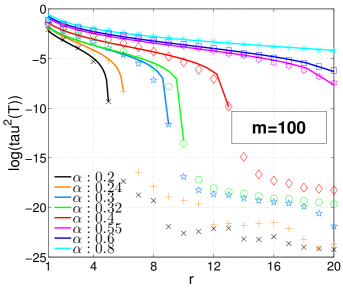

3.1 Scaling of the constant

For and given, it is possible to evaluate by solving a convex optimization problem. This is different from other conditions employed in the literature such as restricted strong convexity [21], 1-RIP [10] or restricted uniform boundedness [5] that involve a non-convex optimization problem even for fixed .

We here consider sampling operators with random i.i.d. measurements , where is a standard Gaussian random vector in (equivalently, follows a Wishart distribution) , . We expect to behave similarly for random rank-one measurements of the same form as long as the underlying probability distribution has finite fourth moments, and thus for (a broad subclass of) the ensemble (16).

In order to explore the scaling of with , and , we fix

. For each choice of , we vary , where a grid

of values ranging from to is considered . For , we consider the grid .

For each combination of , , and , we use 50 replications. Within each replication, the subspace

is generated randomly from the eigenspace associated with the non-zero eigenvalues of a random matrix

, where the entries of the matrix are i.i.d. .

The results point to the existence of a phase transition as it is typical for problems related to that

under study [2]. Specifically, it turns out that the scaling of can be

well described by the relation

| (17) |

where depend on and . In order to arrive at model (17), we first obtain the %-quantile as summary statistic of the 50 replications associated with each triple . At this point, note that the use of the mean as a summary statistic is not appropriate as it may mask the fact that the majority of the observations are zero. For each pair of , we then identify all values of for which the corresponding %-quantile drops below , which serves as effective zero here. For the remaining values, we fit model (17) using nonlinear least squares (working on a log scale). Figure 1 shows that model (17) provides a rather accurate description of the given data. Concerning and , the scalings and for constants appear to be reasonable. This gives rise to the requirement for exact recovery to be possible in the noiseless case (cf. Proposition 4) and yields that as long as ,

|

|

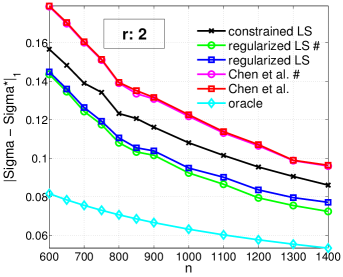

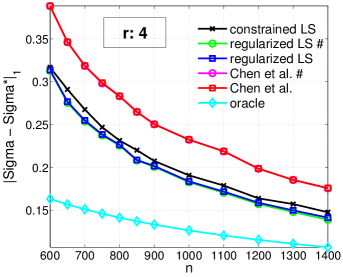

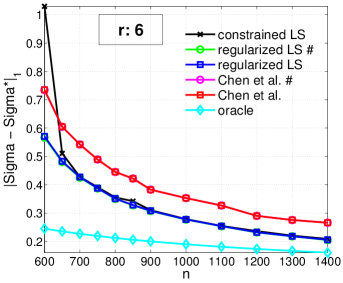

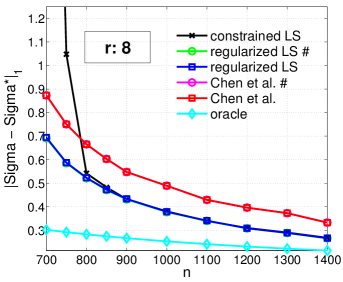

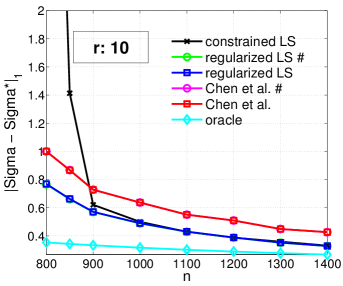

3.2 Comparison with regularization-based approaches

In this subsection, we empirically evaluate relative

to regularization-based methods proposed in the literature.

Setup. We consider Wishart measurement matrices as in the previous subsection. Again, we expect a similar behaviour for (most) other random designs from ensemble . We fix and let and vary. For each configuration of and , we consider 50 replications. In each of these replications, we generate data

| (18) |

where is generated as the sum of Wishart matrices and the are i.i.d. .

|

|

|

|

|

|

Regularization-based approaches. We compare to the corresponding nuclear norm regularized estimator in (11). Regarding the choice of the regularization parameter , we consider the grid , where as recommended in [21] and pick so that the prediction error on a separate validation data set of size generated from (18) is minimized. Note that in general, neither is known nor an extra validation data set is available. Our goal here is to ensure that the regularization parameter is properly tuned. In addition, we consider an oracular choice of where is picked from the above grid such that the performance measure of interest (the distance to the target in the nuclear norm) is minimized. We also compare to the constrained nuclear norm minimization approach of Chen et al. [10] given by

| (19) |

For the parameter , we consider the grid . This specific choice is motivated by the observation that . Apart from that, tuning of is performed as for the nuclear norm regularized estimator. In addition, we have assessed the performance of the approach in [5], which does not impose an spd constraint but adds one more constraint to the formulation (19). That additional constraint significantly complicates optimization of the problem and yields a second tuning parameter. Therefore, instead of doing a grid search over a 2D-grid, we use fixed values as specified in [5] given the knowledge of . The results are similar or worse than those of (19) (note in particular that positive semidefiniteness is not taken advantage of in the approach of [5]) and are hence not reported here.

Discussion of the results. We can conclude from Figure 2 that in most cases, the performance of the constrained least squares estimator does not differ much from that of the regularization-based methods with careful parameter tuning, which are not too far from the oracle. However, for larger values of , the constrained least squares estimator seems to require slightly more measurements to achieve competitive performance.

3.3 Real data examples

We conclude this section by presenting an application to recovery of spiked covariance matrices, a notion due to [16].

Background. A spiked covariance matrix is of the form , where and , . Note that for data following the factor model

| (20) |

for orthogonal factors and random coefficients independent from , the population covariance matrix , , is of the form given above. Model (20) is one possible way to motivate principal components analysis (PCA); this connection explains the relevance and the popularity of spiked covariance models.

Extension to the spiked case. So far, we have assumed that the target is of low rank, but it is straightforward to extend the proposed approach to the case in which is spiked as long as is known or an estimate is available. A constrained least squares estimator of takes the form , where

| (21) |

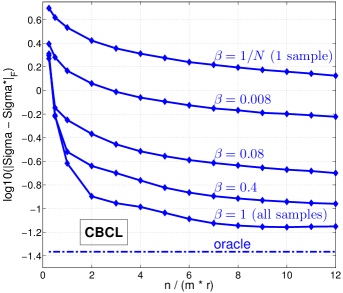

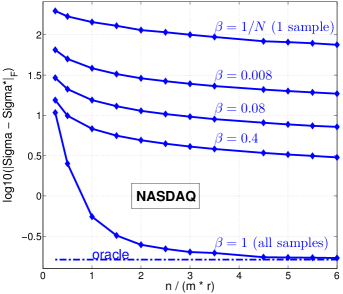

Data sets. (1) The CBCL facial image data set [1] consist of images of pixels (i.e., ). We take as the sample covariance matrix of this data set. It turns out that can be well approximated by , , where is the best rank approximation to obtained from computing its eigendecomposition and setting to zero all but the top eigenvalues. (2) We construct a second data set from the daily end prices of stocks from the technology sector in NASDAQ, starting from the beginning of the year 2000 to the end of the year 2014 (in total days, retrieved from finance.yahoo.com). We take as the resulting sampling correlation matrix and choose .

Experimental setup. As in all preceding measurements, we consider random Wishart measurements for the operator , where , where ranges from to . Since for both data sets, we work with in (21) for simplicity. To make the problem of recovering more difficult, we introduce additional noise to the problem by using observations

| (22) |

where is an approximation to obtained from the sample covariance respectively sample correlation matrix of data points randomly sampled with replacement from the entire data set, , where ranges from to ( is computed from a single data point). For each choice of and , replications are considered. The reported results are averages over these replications.

Results. For the CBCL data set, it can be seen from Figure 3 and Table 1,

that accurately approximates

(within a factor of three of the best rank- approximation ) once the number of measurements crosses

. Performance degrades once additional noise is introduced to the problem by using measurements (22) that

are taken from a perturbed version of . Even under significant perturbations (), reasonable reconstruction

of remains possible, albeit the number of required measurements increases accordingly. In the extreme case ,

the error is still decreasing with , but millions of samples seems to be required to achieve reasonable reconstruction error

(for computational reasons, we stop at ).

The general picture is similar for the NASDAQ data set, but the difference between using measurements based on the

full sample correlation matrix on the one hand and approximations based on random subsampling (22) on the other hand are more pronounced. For , the reduction in error with increasing progresses visibly faster as for the first data set, and a

smaller error relative to close to is achieved.

CBCL NASDAQ

| 1 | 1 | .4 | .4 | .08 | |

|---|---|---|---|---|---|

| 2 | 6 | 4 | 6 | 10 | |

| 1 | 1 | 1 | 1 | |

| 1 | 2 | 3 | 6 | |

4 Conclusion

In this paper, we have investigated trace regression in the situation that the underlying matrix is symmetric positive semidefinite. We have shown that under certain restrictions on the design, the constrained least squares estimator enjoys excellent statistical properties similar to methods employing nuclear norm regularization. This may come as a surprise, as regularization is widely regarded as necessary in small sample settings. On the application side, we have pointed out the usefulness of our findings for recovering spiked covariance matrices from quadratic measurements.

Acknowledgement

The work of Martin Slawski and Ping Li is partially supported by NSF-DMS-1444124, NSF-III-1360971, ONR-N00014-13-1-0764, and AFOSR-FA9550-13-1-0137.

Appendix A Proof of Proposition 1

By rotational invariance of the Gaussian distribution of , it suffices to consider the canonical orthonormal basis of given by

where denote the canonical basis vectors of . Equivalently, the corresponding map equals the symmetric vectorization operator

| (23) |

Accordingly, denote by the error terms corresponding to the entries . The minimization problem (7) can hence be expressed as

| (24) |

where the matrix has entries , , and , . Now observe that the minimizer of (24) coincides with the Euclidean projection of on . It is well-known [3] that the projection of a symmetric matrix on the positive semidefinite cone is obtained by setting all its negative eigenvalues to zero, i.e., in terms of the eigendecomposition of , we have

At this point, we note that is a Wigner matrix, whose empirical distribution of its eigenvalues follows Wigner’s semicircle law as (cf. [27]), which is symmetric around zero. Consequently, we have

Appendix B Proof of Proposition 2

Definition B.1.

Let be a convex cone. The statistical dimension of is defined as , where denotes the Euclidean projection onto and the entries of are i.i.d. .

Theorem B.1.

Proof.

(Proposition 2). Denote by the symmetric vectorization map (cf. (23)), which is an isometry with respect to the Euclidean inner product on and , and by its inverse. We can then apply Theorem B.1 to the setting of Proposition 2 by using

where is the convex indicator function of which takes the value if its argument is contained in and otherwise. Observe that . It is shown in [2], Proposition 3.2, that the statistical dimension . This concludes the proof. ∎

Appendix C Proof of Proposition 3

Proposition 3 follows from the dual problem of the convex optimization problem associated with . Below, it will be shown that the Lagrangian dual of the optimization problem

| (26) | ||||

is given by

| (27) | ||||

The assertion of Proposition 3 follows immediately from (27) by identifying and . In the remainder of the proof, duality of (26) and (27) is established. Using the shortcut , the Lagrangian of the dual problem (27) is given by

Taking derivatives w.r.t. and the setting the result equal to zero, we obtain from the KKT conditions that a primal-dual optimal pair obeys

| (28) |

Taking the inner product of the rightmost equation with , we obtain

where the second equivalence is by complementary slackness. Consider first the case . This entails and thus , so that . Substituting this result into the rightmost equation in (28) and taking norms, we obtain

| (29) |

For the second case, note that cannot be negative as is feasible for (27). Thus, implies that and in turn also (29).

Appendix D Proof of Corollary 1

Appendix E Proof of Theorem 1

The following lemma is a crucial ingredient in the proof. In the sequel, let . Let the eigendecomposition of be given by

| (30) |

Lemma E.1.

Consider the decomposition (30). We have .

Proof.

Write and for the eigendecompositions of and , respectively. Since , we must have and thus

where for the last identity, we have used that . It follows that

∎

Proof.

(Theorem 1) By definition of , we have . Using (6) and the definition of , we obtain after re-arranging terms that

| (31) |

where we have used Hölder’s inequality, the decomposition of as in Lemma E.1 and . We now upper bound the l.h.s. of (31) by invoking Condition 1 and Lemma E.1, which yields . If , we have

which is the first part in the maximum of the bound to be established. In the opposite case, suppose first that (the case is discussed at the end of this proof) and we have . Consequently,

Inserting this into (31), we obtain the following upper bound on .

where the last inequality follows from the observation that for any

which can be easily seen from the dual problem (27) associated with . Substituting the above bound on into (31) and using the bound yields the second part in the maximum of the desired bound. To finish the proof, we still need to address the case . Recalling the definition of the quantity in (14), we bound

Inserting this into (31), we obtain from (15)

Back-substitution into (31) yields a bound that is implied by that of Theorem 1. This concludes the proof. ∎

Bound on . The bound on is an application of Theorem 4.6.1 in [29].

Theorem E.1.

[29] Consider a sequence of fixed matrices in and let . Then for all

Choosing yields the desired bound.

Appendix F Proof of Theorem 1, Remark 3

The bound hinges on the following concentration result for the extreme eigenvalues of the sample covariance of a Gaussian sample.

Theorem F.1.

[11] Let be an i.i.d. sample from and let . We then have for any

In the proof, we also make use of the following fact.

Lemma F.1.

Let . Then

Proof.

First note that for any and any , we have that

where are the eigenvectors of . Accordingly, we have

∎

We now establish the bound to be shown. Each measurement matrix can be expanded as

Accordingly, we have

where follows the distribution of in Theorem F.1 with . For the first term, applying Theorem F.1 with and and using the union bound, we obtain that

Applying Theorem F.1 to with , we obtain that

Combining the two previous bounds yields the assertion.

Appendix G Proof of Proposition 4

In the sequel, we write and for the orthogonal projections on and , respectively. Note first that since the are zero, any minimizer satisfies

| (32) |

where and , where we recall that . Note that since , for to be feasible, it is necessary that .

Suppose first that . Then there exist and such that . Hence, for any with

, the choices and ensure

that is feasible and that (32) is satisfied. Since is contained in the Schatten 1-norm

sphere of radius , it is necessarily non-zero and thus .

If , there exists such that . Consequently, for any

with , (32) is satisfied with

.

Conversely, if , (32) cannot be satisfied for , . Otherwise, we could divide by , which would yield

which would imply . Therefore, we must have and , which implies as long as .

Appendix H Proof of Theorem 2

Let , and as in the preceding proof. We start with the following analog to (31)

| (33) |

Suppose that . We then have

Since and , we obtain that the term inside the curly brackets is lower bounded by and thus

| (34) |

On the other hand, expanding the quadratic term in (33), we obtain that

| (35) |

We now distinguish several cases.

References

- [1] CBCL face dataset. http://cbcl.mit.edu/software-datasets/FaceData2.html.

- [2] D. Amelunxen, M. Lotz, M. McCoy, and J. Tropp. Living on the edge: phase transitions in convex programs with random data. Information and Inference, 3:224–294, 2014.

- [3] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- [4] A. Bruckstein, M. Elad, and M. Zibulevsky. On the uniqueness of nonnegative sparse solutions to underdetermined systems of equations. IEEE Transactions on Information Theory, 54:4813–4820, 2008.

- [5] T. Cai and A. Zhang. ROP: Matrix recovery via rank-one projections. The Annals of Statistics, 43:102–138, 2015.

- [6] E. Candes and X. Li. Solving quadratic equations via PhaseLift when there are about as many equations as unknowns. Foundation of Computational Mathematics, 14:1017–1026, 2014.

- [7] E. Candes and Y. Plan. Tight oracle bounds for low-rank matrix recovery from a minimal number of noisy measurements. IEEE Transactions on Information Theory, 57:2342–2359, 2011.

- [8] E. Candes and B. Recht. Exact matrix completion via convex optimization. Foundation of Computational Mathematics, 9:2053–2080, 2009.

- [9] E. Candes, T. Strohmer, and V. Voroninski. PhaseLift: exact and stable signal recovery from magnitude measurements via convex programming. Communications on Pure and Applied Mathematics, 66:1241–1274, 2012.

- [10] Y. Chen, Y. Chi, and A. Goldsmith. Exact and Stable Covariance Estimation from Quadratic Sampling via Convex Programming. arXiv:1310.0807.

- [11] K. Davidson and S. Szarek. Handbook of the Geometry of Banach Spaces, volume 1, chapter Local operator theory, random matrices and Banach spaces, pages 317–366. 2001.

- [12] L. Demanet and P. Hand. Stable optimizationless recovery from phaseless measurements. Journal of Fourier Analysis and its Applications, to appear.

- [13] D. Donoho and J. Tanner. Counting the faces of randomly-projected hypercubes and orthants, with applications. Discrete and Computational Geometry, 43:522–541, 2010.

- [14] D. Gross, Y.-K. Liu, S. Flammia, S. Becker, and J. Eisert. Quantum State Tomography via Compressed Sensing. Physical Review Letters, 105:150401–15404, 2010.

- [15] R. Horn and C. Johnson. Matrix Analysis. Cambridge University Press, 1985.

- [16] I. Johnstone. On the distribution of the largest eigenvalue in principal components analysis. The Annals of Statistics, 29:295–327, 2001.

- [17] M. Klibanov, P. Sacks, and A. Tikhonarov. The phase retrieval problem. Inverse Problems, 11:1–28, 1995.

- [18] V. Koltchinskii. Von Neumann entropy penalization and low-rank matrix estimation. The Annals of Statistics, 39:2936–2973, 2011.

- [19] V. Koltchinskii, K. Lounici, and A. Tsybakov. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. The Annals of Statistics, 39:2302–2329, 2011.

- [20] N. Meinshausen. Sign-constrained least squares estimation for high-dimensional regression. The Electronic Journal of Statistics, 7:1607–1631, 2013.

- [21] S. Negahban and M. Wainwright. Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, 39:1069–1097, 2011.

- [22] B. Recht, M. Fazel, and P. Parillo. Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization. SIAM Review, 52:471–501, 2010.

- [23] A. Rohde and A. Tsybakov. Estimation of high-dimensional low-rank matrices. The Annals of Statistics, 39:887–930, 2011.

- [24] B. Schölkopf and A. Smola. Learning with kernels. MIT Press, Cambridge, Massachussets, 2002.

- [25] M. Slawski and M. Hein. Non-negative least squares for high-dimensional linear models: consistency and sparse recovery without regularization. The Electronic Journal of Statistics, 7:3004–3056, 2013.

- [26] N. Srebro, J. Rennie, and T. Jaakola. Maximum margin matrix factorization. In Advances in Neural Information Processing Systems 17, pages 1329–1336, 2005.

- [27] T. Tao. Topics in Random Matrix Theory. American Mathematical Society, 2012.

- [28] R. Tibshirani. Regression shrinkage and variable selection via the lasso. Journal of the Royal Statistical Society Series B, 58:671–686, 1996.

- [29] J. Tropp. User-friendly tools for random matrices: An introduction. 2014. http://users.cms.caltech.edu/~jtropp/.

- [30] R. Vershynin. How close is the sample covariance matrix to the actual covariance matrix ? Journal of Theoretical Probability, 153:405–419, 2012.

- [31] M. Wang and A. Tang. Conditions for a Unique Non-negative Solution to an Underdetermined System. In Allerton Conference on Communication, Control, and Computing, pages 301–307, 2009.

- [32] M. Wang, W. Xu, and A. Tang. A unique ’nonnegative’ solution to an underdetermined system: from vectors to matrices. IEEE Transactions on Signal Processing, 59:1007–1016, 2011.

- [33] C. Williams and M. Seeger. Using the Nyström method to speed up kernel machines. In Advances in Neural Information Processing Systems 14, pages 682–688, 2001.