Secure State Estimation: Optimal Guarantees against Sensor Attacks in the Presence of Noise

Abstract

Motivated by the need to secure cyber-physical systems against attacks, we consider the problem of estimating the state of a noisy linear dynamical system when a subset of sensors is arbitrarily corrupted by an adversary. We propose a secure state estimation algorithm and derive (optimal) bounds on the achievable state estimation error. In addition, as a result of independent interest, we give a coding theoretic interpretation for prior work on secure state estimation against sensor attacks in a noiseless dynamical system.

I Introduction

Cyber-physical systems (CPS) manage the vast majority of today’s critical infrastructure and securing such CPS against malicious attacks is a problem of growing importance [1]. As a stepping stone towards securing complex CPS deployed in practice, several recent works have studied security problems in the context of linear dynamical systems [1, 2, 3, 4, 5, 6] leading to a fundamental understanding of how the system dynamics can be leveraged for security guarantees. With this motivation, in this paper we focus on securely estimating the state of a linear dynamical system from a set of noisy and maliciously corrupted sensor measurements. We restrict the sensor attacks to be sparse in nature, i.e., an adversary can arbitrarily corrupt a subset of sensors in the system.

Prior work related to secure state estimation against sensor attacks in linear dynamical systems can be broadly categorized into three classes depending on the noise model for sensor measurements: 1) noiseless 2) bounded non-stochastic noise, and 3) Gaussian noise. For the noiseless setting, the work reported in [1, 2, 3] shows that, under a strong notion of observability, sensor attacks (modeled as a sparse attack vector) can always be detected and isolated, and hence the state of the system can be exactly estimated. In contrast, when the sensor measurements are affected by noise as well as maliciously corrupted, the problem of distinguishing between noise and attack vector arises. Results reported in [5, 6, 7] are representative of the second class: bounded non-stochastic noise. They provide sufficient conditions for distinguishing the sparse attack vector from bounded noise but do not guarantee the optimality of their estimation algorithm. The work reported in this paper falls in the third class: Gaussian noise. Prior work in this class includes [8, 9, 10, 11]. In [8], the analysis is restricted to detecting a class of sensor attacks called replay attacks (i.e., attacks in which legitimate sensor outputs are replaced with outputs from previous time instants). In [9], the authors focus on the performance degradation of a scalar Kalman filter (i.e., scalar state and a single sensor) when the sensor is under attack. Since they consider a single sensor setup, attack sparsity across multiple sensors is not studied, and in addition, they focus on an adversary whose objective is to degrade the estimation performance and stay undetected at the same time (thereby restricting the class of sensor attacks). In [10] and [11], robustification approaches for state estimation against sparse sensor attacks are proposed, but they lack optimality guarantees against arbitrary sensor attacks.

In contrast to prior work in the Gaussian noise setup, we consider a general linear dynamical system and give (optimal) guarantees on the achievable state estimation error against arbitrary sensor attacks. The following toy example is illustrative of the nature of the problem addressed in this paper and some of the ideas behind our solution.

Example 1

Consider a linear dynamical system with a scalar state such that , where is the process noise following a Gaussian distribution with zero mean and is instantiated i.i.d. over time. The system has three sensors (indexed by ) with outputs , where is the sensor noise at sensor . Similarly to the process noise, is Gaussian distributed with zero mean and is instantiated i.i.d. over time. The sensor noise is also independent across sensors. Now, consider an adversary which can attack any one of the sensors and arbitrarily change its output. In the absence of sensor noise, it is trivial to detect such an attack since the two good sensors (not attacked by the adversary) will have the same output. Hence, a majority based rule on the outputs leads to the exact state. However, in the presence of sensor noise, even the good sensors may not have the same output and a simple majority based rule cannot be used for estimation. In this paper, we build on the intuition that we may still be able to identify sensors whose outputs can lead to a good state estimate by leveraging the noise statistics over a large enough time window. In particular, our approach for this example would be to hypothesize a subset of two sensors as good, and then check whether the outputs from the two sensors are consistent with the Kalman state estimate based on outputs from the same subset of sensors. Furthermore, we show in this paper that such an approach leads to the optimal state estimation error for the given adversarial setup.

In this paper, we generalize the Kalman filter based approach in the above example to a general linear dynamical system with sensor and process noise. Our main contributions can be listed as follows:

-

•

We give optimal guarantees on the achievable state estimation error against arbitrary sensor attacks and propose an algorithm to achieve the same guarantees;

- •

The remainder of this paper is organized as follows. Section II deals with the setup. The main results are stated in Section III. Section IV considers the simpler setting of a scalar state and illustrates the main ideas behind our estimation algorithm and Section V considers its generalization to a vector state. Finally, we discuss the coding theoretic view of the sparse observability condition [3] in Section VI.

II Setup

II-A System model

We consider a linear dynamical system with sensor attacks as shown below:

| (1) |

where denotes the state of the plant at time , denotes the process noise at time , denotes the output of the plant at time and denotes the sensor noise at time . The process noise , i.e., is Gaussian distributed with zero mean and covariance matrix , where is the identity matrix of dimension and . Similarly, sensor noise . Both and are instantiated i.i.d. over time, and is independent of .

The sensor attack vector in (1) is introduced by a -adversary defined as follows. A -adversary has access to any out of the sensors in the system. Specifically, let denote the set of attacked sensors (with ). The -adversary can observe the actual outputs in the attacked sensors and change them arbitrarily. Specifically, the output of an attacked sensor can be expressed as

| (2) |

where denotes the matrix transpose operation, is the th row of , is the noise at sensor and is the adversarial corruption introduced at sensor . For , . The adversary’s choice of is unknown but is assumed to be constant over time (static adversary). The adversary is assumed to have unbounded computational power, and knows the system parameters (e.g., and ) and noise statistics (e.g., and ). However, the adversary is limited to have only causal knowledge of the process noise and the sensor noise in good sensors (not attacked by the adversary). We discuss this assumption in more detail in Section II-C.

II-B State estimation: prediction and filtering

In this paper, we address two state estimation problems: (1) state prediction and (2) state filtering.

In the state prediction problem, the goal is to estimate the state at time based on outputs till time . In the absence of sensor attacks, using a Kalman filter for predicting the state in (1) leads to the optimal (MMSE) error covariance asymptotically [12]. In particular, the Kalman filter update rule can be written as:

| (3) |

where is the state estimate at time and is the Kalman filter gain. For a Kalman filter in steady state [12], the steady state gain satisfies . Also, we use to denote the trace of steady state (prediction) error covariance matrix [12] obtained by using a Kalman filter on a sensor subset .

In contrast to the prediction problem, the goal in the state filtering problem is to estimate the state at time based on outputs till time . In the absence of sensor attacks, a Kalman filter update rule similar to (3) can be used for the filtering problem [12] (see Appendix -C for details) and we use to denote the trace of steady state (filtering) error covariance matrix obtained by using a Kalman filter on a sensor subset .

II-C Causal knowledge assumptions

At time , the attack vector in (1) depends on the knowledge of the adversary at time , and in this context, we limit the adversary’s knowledge of the process and sensor noise along the lines of causality. In particular, for the prediction problem we assume the following for a -adversary:

-

(A1)

The adversary’s knowledge at time is statistically independent of for , i.e., is statistically independent of ;

-

(A2)

For a good sensor , the adversary’s knowledge at time (and hence ) is statistically independent of .

Intuitively, assumptions (A1) and (A2) limit the adversary to have only causal knowledge of the process noise and the sensor noise in good sensors (not attacked by the adversary). Note that, apart from (A1) and (A2), we do not impose any restrictions on the statistical properties, boundedness and the time evolution of the corruptions introduced by the -adversary. In the filtering problem, we replace assumptions (A1) and (A2) with (A3) and (A4) as described below:

-

(A3)

The adversary’s knowledge at time is statistically independent of for , i.e., is statistically independent of ;

-

(A4)

For a good sensor , the adversary’s knowledge at time (and hence ) is statistically independent of .

Clearly, (A3) is a stronger version of (A1), requiring to be independent of . Similarly, (A4) is a stronger version of (A2).

II-D Sparse observability condition

For the matrix pair , the observability matrix with observability index is defined as shown below:

| (4) |

In this context, a linear dynamical system, characterized by the pair , is said to be observable if there exists a positive integer such that has full column rank. In the absence of sensor and process noise, the conditions under which state estimation can be done despite sensor attacks have been studied in [2, 3, 6]. In particular, a linear dynamical system as shown in (1) is called -sparse observable if for every subset of size , the pair is observable (where is formed by the rows of corresponding to sensors indexed by the elements of ). Also, is the smallest positive integer to satisfy the above observability property. The condition:

| (5) |

is necessary and sufficient for exact state estimation against a -adversary in the absence of process and sensor noise [3]; we will refer to this condition as the sparse observability condition. We provide a coding theoretic interpretation for the same in Section VI.

III Main results

We first state our achievability result followed by an impossibility result.

Theorem 1 (Achievability)

Consider the linear dynamical system defined in (1) satisfying the sparse observability condition (5) against a -adversary. Assuming (A1) and (A2), and a time window for the state prediction problem, the following bound on the prediction error is achievable against a -adversary. For any and , there exists a large enough such that:

| (6) |

where is the estimation error for the state estimate . In other words, with high probability (w.h.p.), the bound is achievable. Similarly, for the state filtering problem, assuming (A3) and (A4) against a -adversary, the following bound on the corresponding filtering error is achievable w.h.p.:

| (7) |

The achievability in Theorem 1 is through our proposed algorithms, which we discuss in the following sections. The impossibility result can be stated as follows.

Theorem 2 (Impossibility)

Consider the linear dynamical system defined in (1) and an oracle MMSE estimator that has knowledge of , i.e., the set of sensors attacked by a -adversary. Then, there exists an attack sequence such that the trace of the prediction error covariance of the oracle estimator is bounded from below as follows:

| (8) |

where above is the oracle estimator’s prediction error and . Similarly, for the filtering problem,

| (9) |

Proof:

Consider the attack scenario where the outputs from all attacked sensors are equal to zero, i.e., the corruption . Hence, the information collected from the attacked sensors cannot enhance the estimation performance. Accordingly, the estimation performance from the remaining sensors is the best one can expect to achieve.

Clearly, for the adversary’s best choice of , the guarantees given in our achievability match the impossibility bound (in an empirical average sense), and hence, we consider our guarantees optimal. We measure the performance of our proposed algorithms in terms of empirical average (and not expectation) since the resultant error in the presence of attacks may not be ergodic.

IV Secure state estimation: scalar state

In this section, we illustrate the main ideas behind our general scheme in the simpler setting of estimating a scalar state variable against a -adversary. In particular, we focus on the state prediction problem for the system in (1) when the state is a scalar and there are sensors (i.e., -sparse observability condition against -adversary). For clarifying the presence of scalar terms in our analysis, we use the scalar version (regular instead of bold face) of the notation developed in Section II, i.e., for the plant’s state, for the estimate, and for the output of a good sensor . We first describe our proposed algorithm for a time window of size , and then analyze its performance.

Secure scalar state prediction algorithm

Considering a time window , Algorithm 1 shows the secure state prediction algorithm for the case when the state is a scalar. The algorithm runs a bank of Kalman filters in parallel; one Kalman filter associated with each distinct set of sensors. For each distinct set of sensors, the corresponding Kalman filter fuses all the measurements from these sensors in order to calculate (prediction) estimate . Using the calculated estimate , we calculate the individual residues for each sensor as shown in (10). The algorithm, then, exhaustively searches for the set of sensors which satisfy the residue test shown in (11). If a set satisfies the residue test, it is declared good and the corresponding Kalman estimate is used as the state estimate for the given time window. Intuitively, the residue test checks if the outputs from a given sensor set are consistent with the corresponding Kalman estimate over the time window .

| (10) |

| (11) |

Performance analysis

Consider the set of sensors which are not attacked by the -adversary. Assuming that the Kalman filter corresponding to set is in steady state, it can be shown that , [12] (where residue is as defined in (10)). For large enough , due to the (strong) law of large numbers (LLN), the residue test will be satisfied w.h.p. for at least this set of good sensors. This ensures that w.h.p., the algorithm will not return an empty set. Also, the estimate from this set of good sensors trivially achieves the error bound (6). But, since the algorithm can return any set of size which satisfies the residue test, it may be possible that some of the sensors in the returned set are corrupt. In the remainder of our analysis, we show that for any set returned by the algorithm, the corresponding Kalman estimate achieves (6).

Suppose the algorithm returns a set of sensors. There is definitely one good sensor (say sensor ) in this set because there can be at most attacked sensors and . Since the residue test is satisfied for this sensor, we have the following constraint:

| (12) |

where (a) follows from for a good sensor and (b) follows from the residue test. The error above is the state estimation (prediction) error at time (in the presence of a -adversary) when is used as the state estimate. Using LLN, we can make an additional simplification as follows. For any , there exists a large enough such that:

| (13) | |||

| (14) |

where (a) follows from (12), and (b) follows w.h.p. due to LLN. Our next step will be to show that the cross term in (13) is vanishingly small w.h.p. as ; this leads to the required bound on using (14). We do so in two steps: first we show that the mean of the cross term is zero and then show that its variance is vanishingly small as .

The mean of the cross term can be computed as shown below:

| (15) |

where (a) follows from the independence of from (due to assumption (A2), is independent of good sensor noise despite sensor attacks). Also, using (15) and taking the expectation in (13):

| (16) |

As the final step in our analysis, we will now show that the variance of cross term is vanishingly small as . For any , there exists a large enough such that:

| (17) |

where (a) follows from the independence of from and the independence of from (for ), (b) follows from (16). The above result implies that the cross term (with zero mean) has vanishingly small variance as . As a result, using Chebyshev’s inequality and (14), we have the error bound (6).

V Secure state estimation: vector state

In this section, we consider the state estimation problem (against a -adversary) for the general linear dynamical system described in (1), when the state is a vector. We focus on the prediction problem in this section; the filtering problem is studied in Appendix -C. We assume that the system is -sparse observable such that it satisfies the sparse observability condition (5) against a -adversary. We first introduce some additional notation required for our proposed algorithm.

Additional notation

Consider a set of sensors. Such a set has sensor subsets of size , and we index these subsets of by . Due to the -sparse observability condition, each subset forms an observable pair with observability matrix and observability index ; is formed by rows of corresponding to subset of . We define matrices and as shown below:

| (18) |

The pseudo-inverse of is denoted by . The output from sensor subset (of size ) at time is denoted by . We consider the state estimation problem for a time window of size and assume without loss of generality that divides such that .

Secure state prediction algorithm

| (19) |

Similar to the scalar setting, Algorithm 2 runs a bank of Kalman filters in parallel. For each distinct set of sensors, the corresponding Kalman filter fuses all the measurements from these sensors in order to calculate an estimate . For a sensor set of size to satisfy the block residue test, each of its subsets should satisfy (19) for each group . If a set satisfies the residue test, it is declared good and the corresponding Kalman estimate is used as the state estimate for the given time window. Intuitively, the residue test checks if the outputs from every observable sensor subset of size within set are consistent with the corresponding Kalman estimate over the time window . We analyze the performance of Algorithm 2 in Appendix -A.

VI Sparse observability: Coding theoretic view

In this section, we revisit the sparse observability condition (5) against a -adversary and give a coding theoretic interpretation for the same. We first describe our interpretation for a linear system, and then discuss how it can be generalized for non-linear systems.

Consider the linear dynamical system in (1) without the process and sensor noise (i.e., ). If the system’s initial state is and the system is -sparse observable, then clearly in the absence of sensor attacks, by observing the outputs from any out of sensors for time instants () we can exactly recover and hence, exactly estimate the state of the plant. A coding theoretic view of this can be given as follows. Consider the outputs from sensor for time instants as a symbol . Thus, in the (symbol) observation vector , due to -sparse observability, any symbols are sufficient (in the absence of attacks) to recover the initial state . Now, let us consider the case of a -adversary which can arbitrarily corrupt any sensors. In the coding theoretic view, this corresponds to arbitrarily corrupting any (out of ) symbols in the observation vector. Intuitively, based on the relationship between error correcting codes and the Hamming distance between codewords in classical coding theory [13], one can expect the recovery of the initial state despite such corruptions to depend on the (symbol) Hamming distance between the observation vectors corresponding to two distinct initial states (say and with ). In this context, the following lemma relates -sparse observability to the minimum Hamming distance between observation vectors in the absence of attacks; this leads to a (tight) bound on the number of attacked sensors that can be tolerated for state estimation.

Lemma 1

For a -sparse observable system with sensors, the minimum (symbol) Hamming distance between observation vectors corresponding to distinct initial states is .

Proof:

Consider observation vectors and corresponding to distinct initial states and . Due to -sparse observability, at most symbols in and can be identical; if any of the symbols are identical, this would imply . Hence, the (symbol) Hamming distance between the observation vectors and (corresponding to and ) is at least symbols. Furthermore, there exists a pair of initial states , such that the corresponding observation vectors and are identical in exactly symbols111If there is no such pair of initial states, the initial state can be recovered by observing any sensors. By definition, in a -sparse observable system, is the smallest positive integer, such that the initial state can be recovered by observing any sensors. and differ in the rest symbols. Hence, the minimum (symbol) Hamming distance between the observation vectors is . ∎

The above lemma connects the problem of state estimation with sensor attacks in a dynamical system to error correction in classical coding theory. Since the minimum Hamming distance between the observation vectors corresponding to distinct initial states is , we can correct up to sensor corruptions; this is equivalent to the condition , which is precisely the sparse observability condition required against a -adversary222In addition, since the minimum Hamming distance is , we can detect attacks up to sensor corruptions.. It should be noted that a -adversary can attack any set of (out of ) sensors, and the condition is both necessary and sufficient for exact state estimation despite such attacks. When , it is straightforward to show a scenario where the observation vector (after attacks) can be explained by multiple initial states, and hence exact state estimation is not possible. The following example illustrates such an attack scenario in view of the coding theoretic interpretation discussed above.

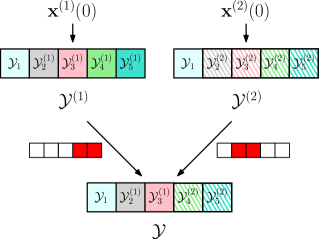

Example 2

Consider a -sparse observable system with , number of sensors , and a -adversary with . Clearly, the condition is not satisfied in this example. Let and be distinct initial states, such that the corresponding observation vectors and have (minimum) Hamming distance symbols. Figure 1 depicts the observation vectors and , and for the sake of this example, we assume that the observation vectors have the same first symbol (i.e., ) and differ in the rest symbols (hence, a Hamming distance of ).

Now, as shown in Figure 1, suppose the observation vector after attacks was . Clearly, there are two possible explanations for this (attacked) observation vector: (a) the initial state was and sensors and were attacked, or (b) the initial state was and sensors and were attacked. Since there are two possibilities, we cannot estimate the initial state exactly given the attacked observation vector. This example can be easily generalized to show the necessity of the condition .

For (noiseless) non-linear systems, by analogously defining -sparse observability, the same coding theoretic interpretation holds. Hence, this leads to an alternative proof for the necessary and sufficient conditions for secure state estimation in any noiseless dynamical system.

References

- [1] F. Pasqualetti, F. Dorfler, and F. Bullo, “Control-theoretic methods for cyber-physical security,” IEEE Control Systems Magazine, Aug. 2014, to appear. [Online]. Available: http://motion.me.ucsb.edu/pdf/2013u-pdb.pdf

- [2] H. Fawzi, P. Tabuada, and S. Diggavi, “Secure estimation and control for cyber-physical systems under adversarial attacks,” IEEE Transactions on Automatic Control, vol. 59, no. 6, pp. 1454–1467, June 2014.

- [3] Y. Shoukry and P. Tabuada, “Event-triggered state observers for sparse sensor noise/attacks,” arXiv pre-print, Sep. 2013. [Online]. Available: http://arxiv.org/abs/1309.3511

- [4] S. Mishra, N. Karamchandani, P. Tabuada, and S. Diggavi, “Secure state estimation and control using multiple (insecure) observers,” in IEEE Conference on Decision and Control (CDC), 2014.

- [5] Y. Shoukry, P. Nuzzo, A. Puggelli, A. L. Sangiovanni-Vincentelli, S. A. Seshia, and P. Tabuada, “Secure state estimation for cyber physical systems under sensor attacks: a satisfiability modulo theory approach,” arXiv pre-print, Dec. 2014.

- [6] M. S. Chong, M. Wakaiki, and J. P. Hespanha, “Observability of linear systems under adversarial attacks,” in American Control Conference (ACC), 2015.

- [7] M. Pajic, J. Weimer, N. Bezzo, P. Tabuada, O. Sokolsky, I. Lee, and G. Pappas, “Robustness of attack-resilient state estimators,” in ACM/IEEE International Conference on Cyber-Physical Systems (ICCPS), 2014.

- [8] Y. Mo and B. Sinopoli, “Secure control against replay attacks,” in Allerton Conference on Communication, Control, and Computing, 2009.

- [9] C.-Z. Bai and V. Gupta, “On kalman filtering in the presence of a compromised sensor: fundamental performance bounds,” in American Control Conference (ACC), 2014.

- [10] J. Mattingley and S. Boyd, “Real-time convex optimization in signal processing,” IEEE Signal Processing Magazine, vol. 27, no. 3, pp. 50–61, May 2010.

- [11] S. Farahmand, G. B. Giannakis, and D. Angelosante, “Doubly robust smoothing of dynamical processes via outlier sparsity constraints,” IEEE Trans. on Signal Processing, vol. 59, no. 10, pp. 4529–4543, Oct. 2011.

- [12] T. Kailath, A. Sayed, and B. Hassibi, Linear Estimation. Prentice Hall, 2000.

- [13] R. Blahut, Algebraic Codes for Data Transmission. Cambridge University Press, 2003.

- [14] S.-D. Wang, T.-S. Kuo, and C.-F. Hsu, “Trace bounds on the solution of the algebraic matrix Riccati and Lyapunov equation,” IEEE Transactions on Automatic Control, vol. 31, no. 7, pp. 654–656, Jul 1986.

-A Algorithm 2: performance analysis

In this section, we analyze the performance of Algorithm 2. Similar to the analysis done for the scalar setting in Section IV, we first derive a bound using LLN, and then analyze the cross term in the bound to obtain final guarantees on the state estimation error in the presence of attacks. The details of the analysis are described below.

Consider the set of sensors which are not attacked by the -adversary. For such a set , the block residue for a subset of (subset of size ) can be expressed as shown below:

| (20) | ||||

| (21) |

and assuming that the Kalman filter corresponding to sensor set is in steady state:

where (a) follows from . Hence, due to LLN, the block residue test (19) will be satisfied w.h.p. for at least this set of good sensors and w.h.p. the algorithm will not return an empty set. Also, the estimate from this set of good sensors trivially satisfies the error bound (6). But, since the algorithm can return any set of size which satisfies the block residue test, it may be possible that some of the sensors in the returned set are corrupt. In the remainder of our analysis, we show that for any set returned by the algorithm, the corresponding Kalman estimate achieves the error bound (6).

Suppose the algorithm returns a set of sensors. Since (sparse observability condition), there exists a subset of good sensors in . The following can be inferred when the block residue test (19) is satisfied for such a subset (of size ):

| (22) |

where in (a) is the state estimation error at time (in the presence of a -adversary) when is used as the state estimate, and (b) follows from the block residue test (19). Using (a) and (b) above, for any there exists a large enough such that:

| (23) | |||

| (24) |

where (c) follows w.h.p. from LLN; for different time indices in , corresponds to i.i.d. realizations of the same random variable. Along the lines of the analysis done in the scalar setting in Section IV, we can show that the cross term in (23) has zero mean and vanishingly small variance as ; this leads to the required bound on . To complete our analysis we calculate the mean and the variance of the cross term as shown below.

The mean of can be computed as shown below:

| (25) |

where (a) follows from the independence of from . This is true since both and are independent333The adversary’s corruptions till time can influence which is based on outputs till time . Due to assumption (A1), the adversary’s corruptions till time are independent of and hence is independent of . Also, is independent of . Due to assumption (A2), is independent of . of and . Also, using (25) and taking the expectation in (23):

| (26) |

Now, we will show that the variance of the cross term is vanishingly small as . For any , there exists a large enough such that:

| (27) |

where (a) follows from (25), (b) follows from the independence of from for , (c) follows from , (d) follows from being a scalar, (e) follows from the independence of from , (f) follows from Lemma 2 (discussed in Appendix -B) with eigen value (i.e., is the maximum eigen value of ). Finally, (g) follows from (26). This completes the variance analysis and clearly the cross term has vanishingly small variance as . As a result, using Chebyshev’s inequality and (24), we have the following bound: for any and , there exists a large enough such that:

| (28) |

Since implies , we have the required bound on from (28) as follows. For any and , there exists a large enough such that:

| (29) |

This completes our performance analysis.

-B Bounds on the trace of product of symmetric matrices

A useful lemma from [14] providing bounds on the trace of product of symmetric matrices is as follows.

Lemma 2

If and are two symmetric matrices in , and is positive semi-definite (i.e., ), then the following inequality holds:

| (30) |

where and denote the minimum and maximum eigen values of matrix .

-C Secure state filtering

In this section, for the general linear dynamical system defined in (1), we study the filtering problem where the goal is to estimate the state at time based on outputs till time (in contrast to using outputs till time in the prediction problem). In the absence of sensor attacks, using a Kalman filter for state filtering in (1) leads to the optimal (MMSE) error covariance asymptotically [12]. The Kalman filter update rule (in steady state) for the filtering problem (without sensor attacks) is as shown below:

| (31) |

where is the state (filtering) estimate (see [12] for further details). The filtering error is defined as , and as shown in (31), the state estimate at time depends on the outputs at time . Also, in the absence of sensor attacks, is the trace of steady state (filtering) error covariance matrix obtained by using the Kalman filter on a sensor subset .

For the secure state filtering problem, we assume that sparse observability condition (5), and assumptions (A3) and (A4) hold against a -adversary. In addition to the notation developed in Section V for the prediction problem, we will require the following definition: denotes the matrix formed by columns of corresponding to sensor subset of set (subset is of size ). The algorithm for secure state filtering (and its analysis) is similar to that for the prediction setting. In the remainder of this section, we first describe the secure state filtering algorithm and then analyze its performance.

Secure state filtering algorithm

| (32) |

Performance analysis

The performance analysis is similar to the analysis done for the prediction problem in Appendix -A and we describe the details below.

Consider the set of sensors which are not attacked by the -adversary. For such a set , the block residue for a subset of (subset of size ) can be expressed as shown below:

| (33) |

and assuming that the Kalman filter corresponding to sensor set is in steady state, it can be shown that:

| (34) |

Hence, due to LLN, the block residue test (32) will be satisfied w.h.p. for at least this set of good sensors and w.h.p. the algorithm will not return an empty set. Also, the estimate from this set of good sensors trivially satisfies the error bound (7). But, since the algorithm can return any set of size which satisfies the block residue test, it may be possible that some of the sensors in the returned set are corrupt. In the remainder of our analysis, we show that for any set returned by the algorithm, the corresponding Kalman estimate achieves the error bound (7).

Suppose the algorithm returns a set of sensors. Since (sparse observability condition), there exists a subset of good sensors in . The following can be inferred when the block residue test is satisfied for such a subset (of size ):

| (35) |

where in (a) is the state estimation error at time (in the presence of a -adversary) when is used as the state estimate, and (b) follows from the block residue test (32). Using (a) and (b) above, for any there exists a large enough such that:

| (36) | |||

| (37) |

where (c) follows w.h.p. from LLN as for different time indices in , corresponds to i.i.d. realizations of the same random variable. Similar to the prediction problem, it can be shown that the cross term in (36) has mean and has vanishingly small variance as . This leads to the claimed bound (7) on state estimation error and we describe the details below.

For simplifying our calculations, we introduce the term . Due to assumptions (A3) and (A4), is independent from and , and hence independent from . Now, the mean of the cross term can be computed as follows:

| (38) |

where (a) follows from the independence of from . Also, using (38) and taking the expectation in (36):

| (39) |

We now state the following claim which is useful in our variance calculation for the cross term .

Claim 1

Proof:

See Appendix -D. ∎

Now, we will show that the variance of is vanishingly small as . For any , there exists a large enough such that:

| (41) |

where (a) follows from the independence of from , (b) follows from the independence of from , (c) follows from the independence of from , (d) follows from Lemma 2 (see Appendix -B) with , and (e) follows from Claim 1.

The above result implies that the variance of the cross term is vanishingly small as . As a result, using Chebyshev’s inequality and (37), we have the following bound: for any and , there exists a large enough such that:

| (42) |

Since implies , we have the required bound on from (42) as follows. For any and , there exists a large enough such that:

| (43) |

This completes our performance analysis.