Extreme eigenvalues of large-dimensional spiked Fisher matrices with application

Abstract

Consider two -variate populations, not necessarily Gaussian, with covariance matrices and , respectively, and let and be the sample covariances matrices from samples of the populations with degrees of freedom and , respectively. When the difference between and is of small rank compared to and , the Fisher matrix is called a spiked Fisher matrix. When and grow to infinity proportionally, we establish a phase transition for the extreme eigenvalues of : when the eigenvalues of (spikes) are above (or under) a critical value, the associated extreme eigenvalues of the Fisher matrix will converge to some point outside the support of the global limit (LSD) of other eigenvalues; otherwise, they will converge to the edge points of the LSD. Furthermore, we derive central limit theorems for these extreme eigenvalues of the spiked Fisher matrix. The limiting distributions are found to be Gaussian if and only if the corresponding population spike eigenvalues in are simple. Numerical examples are provided to demonstrate the finite sample performance of the results. In addition to classical applications of a Fisher matrix in high-dimensional data analysis, we propose a new method for the detection of signals allowing an arbitrary covariance structure of the noise. Simulation experiments are conducted to illustrate the performance of this detector.

keywords:

[class=AMS]keywords:

and

1 Introduction

Consider two -variate populations with covariance matrices and , respectively, and let and be the sample covariances matrices from samples of the populations with degrees of freedom and , respectively. Specifically, if both populations are Gaussian, and are distributed as Wishart and , respectively. For testing the equality hypothesis , the likelihood ratio statistic relies on the characteristic roots of the determinental equation

| (1.1) |

Here and throughout the paper, the determinant of a matrix is denoted by either or . As a famous story in multivariate analysis of last century, the joint distribution of these characteristic roots for Gaussian populations was simultaneously and independently published in 1939 by R. A. Fisher, S. N. Roy, P. L. Hsu and M. A. Girshick. When is invertible, these roots are simply the eigenvalues of the matrix , widely known as a Fisher matrix in the literature, which generalises the one-dimensional Fisher ratio.

Another breakthrough is the work of Wachter (1980) where he finds a deterministic limit, the celebrated Wacheter distribution, for the empirical measure of these roots when the dimension grows to infinity proportionally to the degrees of freedom and (under the Gaussian assumption). Wachter’s result has been later extended to non-Gaussian populations in what is now called the random matrix theory and two early examples of such extensions are Silverstein (1985) and Bai et al. (1987) . It is also important to notice that the determinental equation (1.1) arises not only in the classical hypothesis testing problem mentioned above, it indeed covers also similar equations arising in important fields of multivariate analysis such as discriminant analysis, canonical correlation analysis and MANOVA, see Wachter (1980).

Needless to say that such limiting results allowing large values of dimension comparable to the degrees of freedom (i.e. sample sizes) are going to have much impact on today’s high-dimensional data analysis. A particularly important question is to investigate the properties of the characteristic roots under an alternative of form

| (1.2) |

where is a nonnegative definite matrix of rank . When , and are all large, the discrimination between the null hypothesis and the alternative is not difficult if the rank difference is all large. The real challenge here lies in detecting a small rank- alternative. In this perspective and assuming is a fixed integer while , and grow to infinity proportionally, the empirical measure of the characteristic roots of (1.1) will be affected by a difference of order which vanishes, so that its limit remains the same as in the null hypothesis, i.e. the Wachter distribution. In other words, such global limit from all the characteristic roots will be of little help for distinguishing the two hypotheses.

It happens that the useful information to detect a small rank alternative is encoded in a few largest characteristic roots of (1.1). In a recent preprint Dharmawansa et al. (2014), by assuming both population are Gaussian and , these authors show that, when the norm of the rank-1 difference (spike) exceeds a phase transition threshold, the asymptotic behaviour of the log-ratio of the joint density of these characteristic roots under a local deviation from the spike depends only on the largest characteristic root and the statistical experiment of observing all the characteristic roots is locally asymptotically normal (LAN). As a by-product of their analysis, the authors also establish joint asymptotic normality of a few of the largest roots when the corresponding spikes in (with ) exceed the phase transition threshold. As it can be guessed, the analysis given in this reference highly rely on the Gaussian assumption so that the joint density function of the characteristic roots has indeed an explicit form under both the null and the alternative, and the main results are obtained via an accurate analytic approximation of the log-ratio of these density functions when the dimension , and grow to infinity proportionally.

Intrigued by these findings, in this paper, we explore the same questions for general populations without Gaussian assumption. It is thus apparent that the joint density of the characteristic roots no more exist and new techniques are needed to solve the questions. Our approach relies on the tools borrowed from the theory of random matrices. This theory is closely connected to modern high-dimensional statistics, and has provided in recent years many efficient estimation and testing procedures for high-dimensional data analysis. Excellent introduction and surveys on this approach can be found in Bai (2005), Johnstone (2007), Johnstone and Titterington (2009) and Paul and Aue (2014). A methodology particularly successful both in theory and applications within this approach relies on the spiked population model coined in Johnstone (2001). This model deals with one population only with a unit population covariance matrix and the hypotheses are simply versus where is a rank- difference as in (1.2). Again for small rank , the discrimination between both hypotheses will rely on the extreme eigenvalues of the sample covariance matrix . Important results have been obtained in the last decade on the behaviour of these extreme eigenvalues. For example, the fluctuation of largest eigenvalues of a sample covariance matrix from a complex spiked Gaussian population is studied in Baik et al. (2005). These authors uncover a phase transition phenomenon: the weak limit and the scaling of these extreme eigenvalues are different depending on whether the eigenvalues of (spikes) are above, equal or below a critical value, situations refereed as super-critical, critical and sub-critical, respectively. In Baik and Silverstein (2006), the authors consider the spiked population model with general populations (not necessarily Gaussian). For the almost sure limits of the extreme sample eigenvalues of , they find that if a population spike (in ) is large or small enough, the corresponding sample spike eigenvalues will converge to a limit outside the support of the limiting spectrum (outliers). In Paul (2007), a CLT is established for these outliers, i.e. the super-critical case, under the Gaussian assumption and assuming that population spikes are simple (multiplicity 1). The CLT for super-critical outliers with general populations and arbitrary multiplicity numbers is developed in Bai and Yao (2008). This theory has been later extended for generalised spiked population model in Bai and Yao (2012).

In summary, from the perspective of spiked population model, the Fisher matrix under the alternative (1.2) can be viewed as a spiked Fisher matrix and it is important to establish a theory for this two-population Fisher matrix in the vein of the results discussed above on the one-population spiked covariance matrix . As said before, in Dharmawansa et al. (2014), the authors have already identified the transition phenomenon for the extreme eigenvalues under the Gaussian assumption, and these eigenvalues are proved to be asymptotic normal assuming that the spike eigenvalues in are simple. The main contributions of the paper are the following. We prove that this phase transition phenomenon for extreme eigenvalues of a spiked Fisher matrix is universal, valid for general populations under some suitable moment conditions. Next, we provide a general CLT for the extreme sample eigenvalues of in the super-critical regime: the limiting distributions are not necessarily Gaussian; they are Gaussian if and only if the population spikes in are simple.

In addition to the motivations given so far on the importance of a spiked Fisher matrix, we are able to implement an application of the general theory developed in this paper in the context of a signal detection problem with a large number of detectors, see Section 7. Indeed, this problem has its own interests and even with quite limited experiments, we show that our implementation can lead to very reliable solutions.

Finally, within the theory of random matrices, the techniques we use in this paper for spiked models are closely connected to other random matrix ensembles through the concept of small-rank perturbations. The goal is again to examine the effect caused on the extreme sample eigenvalues by such perturbations. Theories on perturbed Wigner matrices can be found in Péché (2006), Féral and Péché (2007), Capitaine et al. (2009), Pizzo et al. (2013) and Renfrew and Soshnikov (2013). In a more general setting of finite-rank perturbation including both the additive and the multiplicative one, point-wisely convergence of extreme eigenvalues is established in Benaych-Georges and Nadakuditi (2011) while their fluctuations are studied in Benaych-Georges et al. (2011). In addition, Benaych-Georges and Nadakuditi (2011) contain also results on spiked eigenvectors.

The rest of the paper is organised as follows. First, the exact setting of the spiked Fisher matrix is introduced in Section 2. Then in Section 3, we establish the phase transition phenomenon for the extreme eigenvalues of where the transition boundary is explicitly obtained. Next, CLTs for those extreme eigenvalues fluctuating around some outliers (i.e. the super-critical case) are established first in Section 4 for one group of sample eigenvalues corresponding to a same population spike, and then in Section 6 for all the groups jointly. Section 5 contains numerical illustrations that demonstrate the finite sample performance of our results. In Section 7, we develop in details a signal detection technique with prewhitening. Proofs of the main theorems are included in these sections while some technical lemmas are postponed into the Appendix A.

2 Spiked Fisher matrix and preliminary results

In what follows, we will assume that . This assumption does not loss any generality since the eigenvalues of the Fisher matrix are invariant under the transformation , . Also we will write for to signify the dependence on the dimension . Therefore, the sample covariance matrices and that make up the Fisher matrix are assumed to have the following structure. Let

| (2.1) |

and

| (2.2) |

be two independent arrays, with respective size and , of independent real-valued random variables with mean 0 and variance 1. The sample covariance matrix is

| (2.3) |

Next, is a rank perturbation of ; therefore, we can assume that it has the spiked structure of form

| (2.4) |

where is a covariance matrix, being a fixed constant, containing spike eigenvalues , , of respective multiplicity numbers (). That is, , where is a orthogonal matrix. Consider a sample of size that can be expressed as and let . The sample covariance matrix is

| (2.5) |

Throughout the paper, we consider an asymptotic regime of Marčenko-Pastur type, i.e.

| (2.6) |

Recall that the empirical spectral distribution (ESD) of a matrix with eigenvalues is the distribution where denotes the Dirac mass at . Since the total rank generated by the spikes is fixed, the ESD of will have the same limit (LSD) as there were no spikes. This limiting spectral distribution, the celebrated Wachter distribution, has been known for a long time.

Proposition 2.1.

For the Fisher matrix with the sample covariance matrices ’s given in (2.3)-(2.5), assume that the dimension and the two sample sizes grow to infinity proportionally as in (2.6). Then almost surely, the ESD of weakly converges to a deterministic distribution with a bounded support and a density function given by

| (2.9) |

where

| (2.10) |

Furthermore, if , then has a point mass at the origin. Also, the Stieltjes transform of equals:

| (2.11) |

Remark 2.1.

Assuming both populations are Gaussian, (Wachter, 1980, Theorem 3.1) derives the limiting distribution for roots of the determinental equation ,

The continuous component of the distribution has a compact support with density function proportional to . It can be readily checked that by the change of variable , the density of the continuous component of the LSD of is exactly (2.9). The validity of this limit for general populations (non necessarily Gaussian) is due to Silverstein (1985) and Bai et al. (1987).

For a complex number , we define the following integrals with respect to :

| (2.12) |

3 Phase transition of the extreme eigenvalues of

In this section, we establish a phase transition phenomenon for the extreme eigenvalues of , that is, when a population spike with multiplicity is larger (or smaller) than a critical value, a packet of corresponding sample eigenvalues of will jump outside the support of its LSD and converge all to a fixed limit. Otherwise, these associated sample eigenvalues will converge to one of the edges and .

For notation convenience, let . Define the function

| (3.1) |

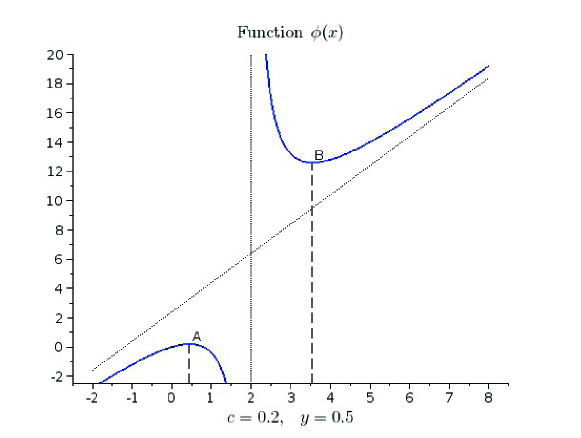

which is a rational function with a single pole . An example is depicted in Figure 1 with parameters . The function has an asymptote of equation when .

By assumption, the population spike eigenvalues are all positive and non unit. We order them with their multiplicities in descending order together with the unit eigenvalues as

| (3.2) |

That is, of these spike eigenvalues are larger than 1 while the other are smaller. Let

Notice that the cardinality of each is . Next, the sample eigenvalues of the Fisher matrix are also sorted in the descending order as . Therefore, for each spike eigenvalue , there are associated sample eigenvalues .

Theorem 3.1.

Basically, the theorem establishes a phase transition phenomenon for the largest and smallest sample eigenvalues of a Fisher matrix. Consider again the example shown in Figure 1. The transition boundary is indicated with the boundary points and with respective coordinates

When the spike is large enough or small enough, the corresponding sample eigenvalues converge to located outside the support of the LSD of . Otherwise, they converge to one of its edges and .

It is worth observing that when , the function tends to the function well-known in the literature for similar transition phenomenon of a spiked sample covariance matrix, i.e.

| (3.4) |

see e.g. the -function on Figure 4 of Bai and Yao (2012). These functions share a same shape; however the pole here equals which is larger than the pole 1 for the case of a spiked sample covariance matrix.

As said in Introduction, this transition phenomenon has already been established in a preprint Dharmawansa et al. (2014) (their Proposition 5) under Gaussian assumption and using a completely different approach. Theorem 3.1 proves that such a phase transition phenomenon is indeed universal.

Proof.

(of Theorem 3.1) The proof is divided into the following three steps:

-

•

Step 1: we derive the almost sure limit of an outlier eigenvalue of ;

-

•

Step 2: we show that in order for the extreme eigenvalue of to be an outlier, the population spike should be larger (or smaller) than a critical value;

-

•

Step 3: if not so, the extreme eigenvalue of will converge to one of the edge points and .

Step 1: Let be the outlier eigenvalue of corresponding to the population spike . Then must satisfy the following equation:

and it is equivalent to

| (3.5) |

Now we make some short-hands. Denote , where is the observations of its first coordinates and the remaining. We partition accordingly as where is the observations of its first coordinates and the remaining. Using such a representation, we have

| (3.10) |

Then, (3.5) could be written in the block form:

| (3.13) |

Since is an outlier, it holds , and for block matrix, we have when is invertible. Therefore, (3.13) reduces to

More specifically, we have

| (3.14) |

In all the following, we denote by the Fisher matrix , which has a LSD . And in order to find the limit of , we simply find the limit on the left hand side of (3), then it will generate an equation. Solving this equation will give the value of its limit.

First, consider the terms and . Since is independent of , using Lemma A.2, we see these two terms will converge to some constant multiplied by the covariance matrix between and . On the other hand, is also independent of , we have

Therefore, these two terms will both tend to a zero matrix almost surely.

So the remaining task is to find the limit of and . We recall the expression of and that

According to Lemma A.2, we have

| (3.15) |

here, we denote as the limit of the outlier . For the same reason,

| (3.19) | ||||

| (3.23) |

Therefore, combining (3), (3) and (3), we have the determinant of the following matrix

equal to zero, which is also to say that satisfies the equation:

| (3.24) |

Finally, together with the expression of the Stieltjes transform of a Fisher matrix in (2.11), we have

where the function is defined in (3.4).

Step 2: Define as the Stieltjes transform of the LSD of , who shares the same non-zero eigenvalues as . Then we have the relationship:

| (3.25) |

Recall the expression of in (2.11), we have

| (3.26) |

On the other hand, due to (3.24) and (3.25), we have the value for :

| (3.27) |

Since is outside the support of the LSD, we have

which is also to say that

| (3.28) |

or

| (3.29) |

Then (3.28) says that must be smaller than the minimum value on its right hand side, whose minimum value is attained when (the right hand side of (3.28) is a decreasing function of ). Similarly, (3.29) says that must be larger than the maximum value on its right hand side, which is attained when . Therefore, the condition for be an outlier is:

| (3.30) |

Finally, using (3.26) together with the value of and , we have:

which is equivalent to say that (recall the expression of that ):

Step 3: In this step, we show that if the condition in Step 2 is not fulfilled, then the extreme eigenvalues of will tend to one of the edge points and . For simplicity, we only show the convergence to the right edge : the proof for the convergence to the left edge is similar. Thus suppose all the for . For now, we make some short-hands. Let

and

where and are the corresponding blocks with size . Using the inverse formula for block matrix, the major sub-matrix of is

| (3.31) |

The part

is of rank ; besides, we have

since is independent of . Therefore, the nonzero eigenvalues of the matrix will all tend to zero (so is its largest one). Then consider the second part of (3.31) as follows.

Since is a projection matrix of rank , it has the spectral decomposition:

where is a orthogonal matrix. Since is fixed, the ESD of tends to , which leads to the fact that the LSD of the matrix is the standard Marčenko-Pastur law. Then the matrix is a standard Fisher matrix, and its largest eigenvalues (finitely many) will tend to the right edge of the Wachter distribution. It follows then the two largest eigenvalues of , say and , also tend to .

Next since is the major sub-matrix of , we have by Cauchy interlacing theorem

Thus either. On the other hand, we have

so that for some positive constant , . Consequently, almost surely,

in particular the whole family is bounded. Now let be fixed and assume that a subsequence converges to a limit . Either or . However, according to Step 2, implies that , and otherwise, we have . Therefore, accordingly to one of these two conditions, all subsequences converge to a same limit or , which is thus also the unique limit of the whole sequence . The proof of Theorem 3.1 is complete. ∎

4 Central limit theorem for the outlier eigenvalues of

The aim of this section is to give a CLT for the -packed outlier eigenvalues:

Denote where each is a matrix that corresponds to the -packed spike eigenvalue .

Theorem 4.1.

Assume the same assumptions as in Theorem 3.1 and in addition, the variables (in (2.1)) and (in (2.2)) have the same first four moments and denote as their common fourth moment:

Then for any population spike satisfying , the normalised -packed outlier eigenvalues of : converge weakly to the distribution of the eigenvalues of the random matrix . Here,

| (4.1) |

is a symmetric random matrix, made with independent Gaussian entries of mean zero and variance

| (4.4) |

where

| (4.5) | |||

| (4.6) |

Numerical illustrations of this theorem are detailed in the next section.

Remark 4.1.

Notice that the result above involves the -th block of the eigen-matrix . When the spike is simple, is unique up to its sign, then is uniquely determined. But when has multiplicities greater than 1, is not unique; actually, any rotation of can be an eigenvector matrix corresponding to . Therefore, Lemma A.1 in the Appendix states that, such a rotation will not affect the eigenvalues of the matrix .

Proof.

(proof of Theorem 4.1)

Step 1: Convergence to the eigenvalues of the random matrix . We start from (3). First we make some short hands. Define

| (4.7) |

then (3) could be written as

| (4.8) |

The remaining is to find second order approximation of the four terms on the left hand side of (4.8).

Using Lemma A.5 in the appendix, we have

| (4.9) |

| (4.13) | ||||

| (4.20) | ||||

| (4.21) |

| (4.22) |

| (4.23) |

Denote

| (4.24) |

where denotes the total expectation of all the preceding terms in the equation, and

Combining (4.8), (4), (4), (4), (4) and considering the diagonal block that corresponds to the row and column index in leads to:

| (4.25) |

Furthermore, it will be established in Step 2 below that

| (4.26) |

for some random matrix . Using the device of Skorokhod strong representation (Skorokhod, 1956; Hu and Bai, 2014), we may assume that this convergence hold almost surely by considering an enlarged probability space. Under this device, (4.25) is equivalent to say that tends to an eigenvalue of the matrix . Finally, as the index is arbitrary over the set , all the random variables

converge almost surely to the set of eigenvalues of the random matrix . Besides, due to Lemma A.3, we have

Step 2: Proof of the convergence (4.26) and structure of the random matrix . In the second step, we aim to find the matrix limit of the block random matrix . First, we show equals to another random matrix , here is the type of random sesquilinear form. Then using the results in Bai and Yao (2008) (Proposition 3.1 and Remark 1), we are able to find the matrix limit of .

By assumption (b) that , we have its first components

Recall the definition of in (4.24), we have

| (4.33) | ||||

| (4.40) | ||||

| (4.41) |

Therefore, if we consider its -th block that corresponds to the row and column index in the set :

| (4.44) | |||

| (4.45) |

where

Finally, using Lemma A.6 in the appendix leads to the result. The proof of Theorem 4.1 is complete. ∎

Next we consider a special case where is diagonal, whose eigenvalues being all simple. In other words, we have and for all . Hence . Following Theorem 4.1, we can derive the asymptotic normality for the normalised outlier eigenvalues of when .

Proposition 4.1.

Under the same assumptions as in Theorem 3.1, with additional conditions that is diagonal and all its eigenvalues () are simple, we have when , the outlier eigenvalue of is asymptotically Gaussian:

where

Remark 4.2.

Notice that when the data are standard Gaussian, we have , then the above theorem reduces to

which is exactly the result in Dharmawansa et al. (2014), see setting 1 in their Proposition 11.

5 Numerical illustrations

In this section, numerical results are provided to illustrate the results of our Theorem 4.1 and Proposition 4.1. We fix , , with 1000 replications, thus and . The critical interval is then and the limiting support . Consider spike eigenvalues with respective multiplicity . Let be the ordered eigenvalues of the Fisher matrix . We are particularly interested in the distributions of , and , which corresponds to the spike eigenvalues , and , respectively.

5.1 Case of

In this subsection, we consider a simple case that . Therefore, following Theorem 4.1, we have

-

•

for , . Here, for , , and ; and for , , and .

-

•

for and , the two dimensional random vector converges to the eigenvalues of the random matrix . Here, , and is the symmetric random matrix, made with independent Gaussian entries of mean zero and variance

(5.3)

Simulations are conducted to compare the distributions of the empirical extreme eigenvalues with their limits.

5.1.1 Gaussian case

First, we assume all the and are i.i.d. standard Gaussian, thus . And according to (5.3), is the standard Gaussian Wigner matrix (GOE). Therefore, we have

-

•

,

-

•

,

-

•

The two-dimensional random vector converges to the eigenvalues of the random matrix , here is a GOE.

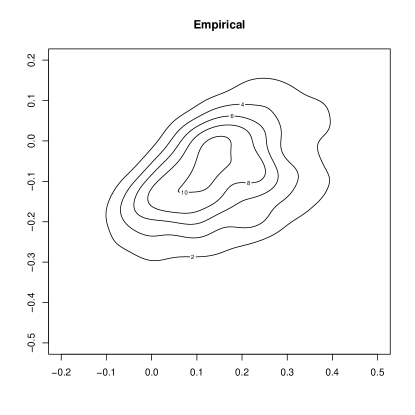

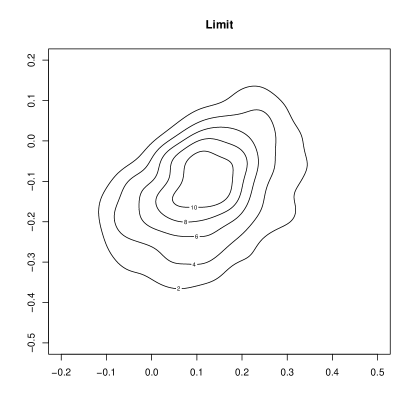

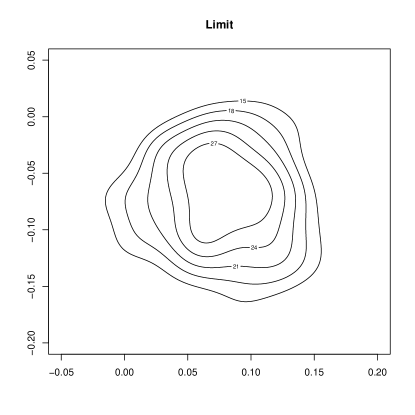

Figure 2, upper panels, show the empirical kernel density estimates (in solid lines) of and from 1000 independent replications, compared to their Gaussian limits and , respectively (dashed lines). When considering the empirical distribution of the two-dimensional random vector , we run the two-dimensional kernel density estimation from 1000 independent replications and display their contour lines, see the lower-left panel of the figure, while the lower-right panel plot shows the contour lines of the kernel density estimation of the eigenvalues of the random matrix (their limits).

5.1.2 Binary case

Second, we assume all the and are i.i.d. binary variables taking values with probability , and in this case we have . Similarly, we have

-

•

,

-

•

,

-

•

The two-dimensional random vector converges to the eigenvalues of the random matrix . Here, is the symmetric random matrix, made with independent Gaussian entries of mean zero and variance

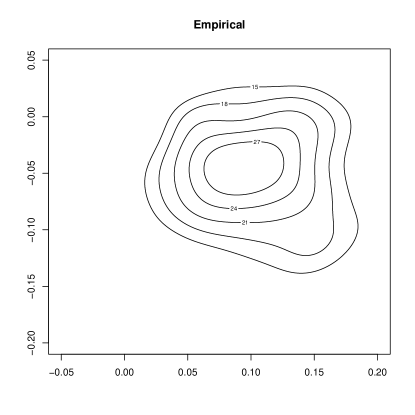

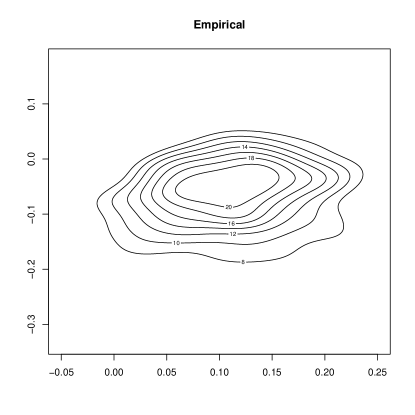

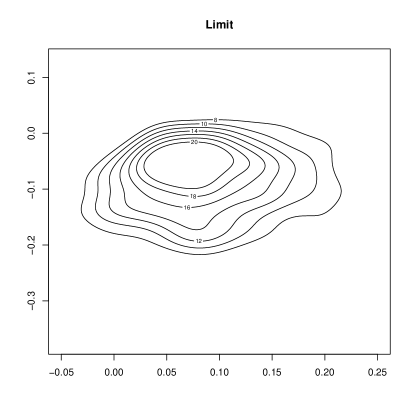

Figure 3, upper panels, show the empirical kernel density estimates of and from 1000 independent replications (in solid lines), compared to their Gaussian limits (in dashed lines). Also, the lower panel on the figure show the contour lines of the empirical joint density of the (the left plot), with the right plot displaying the contour lines of their limit.

5.2 Case of general U

In this subsection, we consider the following non unit orthogonal matrix

| (5.4) |

i.e., we have

Since Gaussian distribution is invariant under orthogonal transformation, we only consider the case that all the and to be i.i.d. binary variables taking values with probability , with all the other settings fixed as in Section 5.1. Then according to Theorem 4.1, we have

-

•

,

-

•

,

-

•

The two-dimensional random vector converges to the eigenvalues of the random matrix . Here, is the symmetric random matrix, made with independent Gaussian entries of mean zero and variance

Figure 4, upper panels, show the empirical kernel density estimates of and from 1000 independent replications (in solid lines), compared to their Gaussian limits (in dashed lines). Also, the lower panel of the figure shows the contour lines of the empirical joint density of (the lower-left plot), with the lower-right plot showing the contour lines of their limit.

6 Joint distribution of the outlier eigenvalues

In the previous section, we have obtained the following result for the outlier eigenvalues: the -dimensional real random vector converges to the distribution of the eigenvalues of random matrix . It is in fact possible to derive their joint distribution, i.e. the limit of the -dimensional real random vector

| (6.4) |

Such joint convergence results are useful for inference procedures where consecutive sample eigenvalues are used such as their differences or ratios, see e.g. Onatski (2009) and Passemier and Yao (2014).

Theorem 6.1.

Assume the same condition as in Theorem 4.1 and that all the population spikes satisfy the condition . Then the -dimensional vector in (6.4) converges in distribution to the eigenvalues of the random matrix

| (6.8) |

where the matrices , made with zero-mean independent Gaussian random variables, are defined in Theorem 4.1, with the the following covariance function between different blocks (): for ,

where

and is defined in (A.21).

The proof of this theorem is very close to that of Theorem 2.3 in Wang et al. (2014), thus omitted.

In principle, the limiting parameters and can be completely specified for a given spiked structure. However, this will lead to quite complex formula. Here, we prefer explain a simple case where is diagonal whose eigenvalues () are all simple, we have , and (). Therefore, in (6.8) reduces to the -th element of , which is a Gaussian random variable. Besides, from Theorem 6.1, we see that the random variables are jointly independent since the index sets are disjoint. Finally, we have the following joint distribution of the outlier eigenvalues of .

Proposition 6.1.

Under the same assumptions as in Theorem 4.1, when is diagonal with all its eigenvalues being simple, the outlier eigenvalues () of are asymptotically independent Gaussian:

where

7 Application to large-dimensional signal detection

In this section, we develop an application of the previous results to an inference problem where spiked Fisher matrices arise naturally. In a signal detection equipment, records are of form

| (7.1) |

where is -dimensional, is a low-dimensional signal with unit covariance matrix, a mixing matrix, and is an i.i.d. noise with covariance matrix . Therefore, the covariance matrix of can be considered as a -dimensional perturbation of , denoted as in the following. Notice that none of the quantities in the r.h.s. of (7.1) is observed. One of the fundamental problem here is to estimate , the number of signals present in the system. This problem is challenging when the dimension is large, say has a comparable magnitude with the sample size . When the noise has the simplest covariance structure, i.e. , this problem has been much investigated recently and several solutions are proposed, see e.g. Kritchman and Nadler (2008), Nadler (2010), Passemier and Yao (2012, 2014). However the problem with an arbitrary noise covariance matrix , say diagonal to simplify, remains unsolved in the large-dimensional context (to the best of our knowledge). Nevertheless, there exists an astute engineering device where the system can be tuned in a signal-free environment, for example in laboratory: that is we can directly record a sequence of pure-noise observations , , which have the same distribution as the above. These signal-free records can then be used to whiten the observations as follows. Let , and be the eigenvalues of . Notice that the eigenvalues are invariant under the transformation , ; they are in fact independent of . Therefore, these eigenvalues can be thought as if , that is becomes a spiked Fisher matrix as introduced in Section 2. This is actually the reason why the two sample procedure developed here can deal with an arbitrary covariance matrix of the noise while the existing one-sample procedures cannot. Based on Theorem 3.1, we propose our estimator of the number of signals as the number of eigenvalues of larger than the right edge point of the support of its LSD:

| (7.2) |

where is a sequence of vanishing constants.

Theorem 7.1.

Assume all the spike eigenvalues () satisfy . Let be a sequence of positive numbers such that , and as , then the estimator is constant, i.e. in probability as .

Remark 7.1.

Notice here that there’s no need for those spikes to be simple, the only requirement is that they should be properly strong enough for detection.

Proof.

(of Theorem 7.1). Since

we have

| (7.3) |

For ,

| (7.4) |

which is due to the assumption that . Then the part in (7) will tend to since we have always when . On the other hand, by Theorem 4.1, in (7) has a limiting distribution; it is then bounded in probability. Therefore, we have

| (7.5) |

Also

and the part is asymptotically Tracy-Widom distributed (see Bao et al. (2015) where the Tracy-Widom distribution for the largest eigenvalue of general sample covariance matrix is derived). As tend to infinity as assumed, we have

| (7.6) |

Combine (7), (7.5) and (7.6), we have as . The proof of Theorem 7.1 is complete. ∎

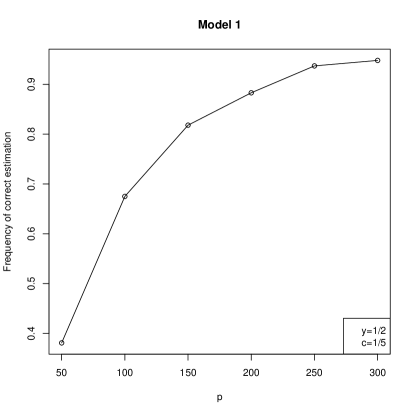

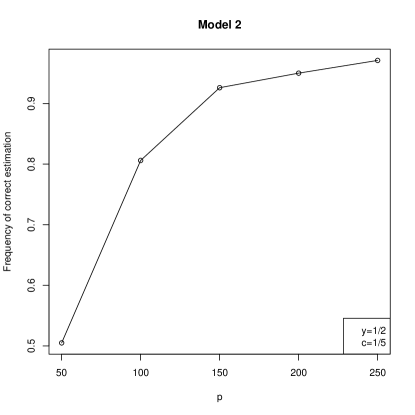

We conduct a short simulation to illustrate the performance of our estimator. We fix and as in Section 5, and the value of varies from to , therefore, the critical value for in the model (2.4) (after whitening) is . For each given pair of , we repeat times. The tuning parameter is chosen to be .

Next, suppose and is a matrix of form , where , ,

Besides, assume . In this setting, we have two spike eigenvalues , (before whitening) with multiplicity , , respectively. Finally, we choose to be either diagonal or non-diagonal as below.

| 50 | 100 | 150 | 200 | 250 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 200 | 300 | 400 | 500 | |||||||

| 250 | 500 | 750 | 1000 | 1250 | |||||||

| 0.038 | 0.003 | 0 | 0 | 0.001 | |||||||

| 0.578 | 0.317 | 0.166 | 0.103 | 0.047 | |||||||

| 0.381 | 0.675 | 0.818 | 0.883 | 0.937 | |||||||

| 0.003 | 0.005 | 0.016 | 0.014 | 0.015 |

-

•

For Model 1: set . In this case, we have the three non-zero eigenvalues of equal , respectively, which are all larger than the critical value , therefore, the number of detectable signals is three;

-

•

For Model 2: set be compound symmetric with all the diagonal elements equal and all the off-diagonal elements equal . In this case, we have for each given , the three non-zero eigenvalues of are all larger than . The number of detectable signals is again three.

| 50 | 100 | 150 | 200 | 250 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 200 | 300 | 400 | 500 | |||||||

| 250 | 500 | 750 | 1000 | 1250 | |||||||

| 0.016 | 0 | 0 | 0 | 0 | |||||||

| 0.475 | 0.186 | 0.053 | 0.028 | 0.008 | |||||||

| 0.505 | 0.806 | 0.926 | 0.950 | 0.971 | |||||||

| 0.004 | 0.008 | 0.021 | 0.022 | 0.021 |

Tables 1 and 2 report the empirical frequency of our estimator in Model 1 and Model 2, respectively, where the true number of signals is . Also, Figure 5 shows more clearly the trends of the frequency of correct estimation in both cases. We can see the frequency both increase as gets larger, which confirms the consistency of our estimator.

References

- Bai (2005) Bai, Z. (2005). High dimensional data analysis. Cosmos, 1(1), 17–27.

- Bai and Ding (2012) Bai, Z. and Ding, X. (2012). Estimation of spiked eigenvalues in spiked models. Random Matrices Theory Appl., 1(2), 1150011, 21.

- Bai and Yao (2008) Bai, Z. and Yao, J. (2008). Central limit theorems for eigenvalues in a spiked population model. Ann. Inst. Henri Poincaré Probab. Stat., 44(3), 447–474.

- Bai and Yao (2012) Bai, Z. and Yao, J. (2012). On sample eigenvalues in a generalized spiked population model. J. Multivariate. Anal., 106, 167–177.

- Bai et al. (1987) Bai, Z., Yin, Y.Q. and Krishnaiah P.R., (1987). On the limiting empirical distribution function of the eigenvalues of a multivariate -matrix. Probab. Theo. Appli. 32, 490–500.

- Baik et al. (2005) Baik, J., Ben Arous, G., and Péché, S. 2005. Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices. Ann. Probab., 33(5), 1643–1697.

- Baik and Silverstein (2006) Baik, J. and Silverstein, J.W. (2006). Eigenvalues of Large Sample Covariance Matrices of Spiked Population Models. J. Multivariate. Anal., 97, 1382–1408.

- Bao et al. (2015) Bao, Z. G., Pan, G.M. and Zhou, W. 2014. Universality for the largest eigenvalue of sample covariance matrices with general population. Ann. Statistics, 43(1), 382–421.

- Benaych-Georges et al. (2011) Benaych-Georges, F., Guionnet, A. and Maïda, M. (2011). Fluctuations of the extreme eigenvalues of finite rank deformations of random matrices. Electron. J. Probab. 16(60), 1621–1662.

- Benaych-Georges and Nadakuditi (2011) Benaych-Georges, F. and Nadakuditi, R.R. (2011). The eigenvalues and eigenvectors of finite, low rank perturbations of large random matrices. Adv. Math., 227(2), 494–521.

- Capitaine et al. (2009) Capitaine, M., Donati-Martin, C. and Féral, D. (2009). The largest eigenvalues of finite rank deformation of large Wigner matrices: convergence and nonuniversality of the fluctuations. Ann. Probab., 37(1), 1–47.

- Dharmawansa et al. (2014) Dharmawansa, P., Johnstone, I.M. and Onatski, A. (2014). Local asymptotic normality of the spectrum of high-dimensional spiked F-ratios. Preprint, available at arXiv:1411.3875.

- Féral and Péché (2007) Féral, D. and Péché, S. (2007). The largest eigenvalue of rank one deformation of large Wigner matrices. Comm. Math. Phys., 272(1), 185–228.

- Hu and Bai (2014) Hu, J. and Bai, Z.D. (2014). Strong representation of weak convergence. Science China (Mathematics) 57(11), 2399-2406.

- Johnstone (2001) Johnstone, I. (2001). On the distribution of the largest eigenvalue in principal components analysis. Ann. Statistics, 29(2), 295–327.

- Johnstone (2007) Johnstone, I. (2007). High dimensional statistical inference and random matrices. Pages 307–333 of: International Congress of Mathematicians. Vol. I. Eur. Math. Soc., Zürich.

- Johnstone and Titterington (2009) Johnstone, I. and Titterington, D. (2009). Statistical challenges of high-dimensional data. Philos. Trans. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci., 367(1906), 4237–4253.

- Kritchman and Nadler (2008) Kritchman, S. and Nadler, B. (2008). Determining the number of components in a factor model from limited noisy data. Chem. Int. Lab. Syst., 94, 19–32.

- Nadler (2010) Nadler, B. (2010). Nonparametric detection of signals by information theoretic criteria: performance analysis and an improved estimator. IEEE Trans. Signal Process., 58(5), 2746–2756.

- Onatski (2009) Onatski, A. (2009). Testing hypotheses about the numbers of factors in large factor models. Econometrica 77, 1447–1479.

- Passemier and Yao (2012) Passemier, D. and Yao, J. (2012). On determining the number of spikes in a high-dimensional spiked population model. Random Matrix: Theory and Applciations, doi, 10.1142/S201032631150002X.

- Passemier and Yao (2014) Passemier, D. and Yao, J. 2014. On the detection of the number of spikes, possibly equal, in the high-dimensional case. J. Multivariate Analysis, 127, 173–183.

- Paul (2007) Paul, D. (2007). Asymptotics of sample eigenstruture for a large dimensional spiked covariance mode. Statistica Sinica, 17, 1617–1642.

- Paul and Aue (2014) Paul, D. and Aue, A. (2014). Random matrix theory in statistics: A review. J. Statist. Planning and Inference 150, 1-29.

- Péché (2006) Péché, S. (2006). The largest eigenvalue of small rank perturbations of Hermitian random matrices. Probab. Theory Related Fields, 134(1), 127–173.

- Pizzo et al. (2013) Pizzo, A., Renfrew, D. and Soshnikov, A. (2013). On finite rank deformations of Wigner matrices. Ann. Inst. Henri Poincaré Probab. Stat., 49(1), 64–94.

- Renfrew and Soshnikov (2013) Renfrew, D., and Soshnikov, A. (2013). On finite rank deformations of Wigner matrices II: Delocalized perturbations. Random Matrices Theory Appl., 2(1), 1250015, 36.

- Silverstein (1985) Silverstein, J. W. (1985). The limiting eigenvalue distribution of a multivariate matrix. SIAM J. Math. Anal. 16 (3), 641–646.

- Skorokhod (1956) Skorokhod A. V. (1956). Limit theorems for stochastic processes. Theory Probab. Appli. 1, 261-290.

- Wachter (1980) Wachter K. W. (1980). The limiting empirical measure of multiple discriminant ratios. Ann. Statist. 8(5), 937-957.

- Wang et al. (2014) Wang, Q.W., Su, Z.G. and Yao, J.F. (2014). Joint CLT for several random sesquilinear forms with applications to large-dimensional spiked population models. Electron. J. Probab. 19(103), 1–28.

- Zheng (2012) Zheng, S.R. (2012). Central Limit Theorem for Linear Spectral Statistics of Large Dimensional Matrix. journal=Ann. Institut Henri Poincaré Probab. Statist. 48, 444-476.

- Zheng et al. (2013) Zheng, S.R., Bai, Z.D. and Yao, J.F. (2013). CLT for linear spectral statistics of random matrix . Preprint, available at arXiv:1305.1376.

Appendix A Some lemmas

Lemma A.1.

Let R be a real-valued matrix, and are two orthogonal bases of some subspace of dimension , where both and are of size , satisfying . Then the two matrices and have the same eigenvalues.

Proof.

(of Lemma A.1) It is sufficient to prove that there exists a orthogonal matrix , such that . If it is true, then , and since is orthogonal, we have the eigenvalues of and are the same. Now let and Define , such that

Put in matrix form:

i.e. . Since by orthogonality of , where , therefore, the matrix is orthogonal. ∎

Lemma A.2.

Suppose is a matrix, whose columns are independent random vectors. is also similarly defined. Let be the covariance matrix of and , is a deterministic matrix, then we have

Moreover, if A is random but independent of and , then we have

| (A.1) |

Proof.

In all the following, refers to the outlier limit that

Lemma A.3.

We have

Proof.

(sketch of the proof of Lemma A.3) In this short proof, we skip all the detailed calculations. Recall the definition of in (3.26), its value at is

| (A.3) |

Also, (3.26) says that is the solution of the following equation:

| (A.4) |

Taking derivatives on both sides of (A.4) and combing with (A.3) will give the value of . On the other hand, since it holds

| (A.5) |

see (3.25), taking derivatives on both sides again will give the value of . Finally, the above five values is just a combination of and .

The proof of Lemma A.3 is complete. ∎

Lemma A.4.

Under assumptions (a)-(d),

Proof.

(of Lemma A.4) We first fix , then we can use the result in Zheng et al. (2013) (Lemma 4.3), which says that

where is the unique solution to the equation

| (A.6) |

satisfying

here, is the LSD of (deterministic), which is the standard M-P law with parameter . Besides, if we denote its Stieltjes transform as , then (A.6) could be written as

| (A.7) |

Since we know that the Stieltjes transform of the LSD of a standard sample covariance matrix satisfies:

| (A.8) |

then we bring (A.7) into (A.8) leads to

whose nonnegative solution is unique, which is

| (A.9) |

Therefore, we have for fixed ,

almost surely. Finally, due to the fact that for each , the ESD of will tend to the same limit (standard M-P distribution), which is independent of the choice of . Therefore, we have for all (not necessarily deterministic but independent of ),

almost surely.

The proof of Lemma A.4 is complete. ∎

Lemma A.5.

, , and are defined in (4), then

| (A.10) | |||

| (A.11) | |||

| (A.15) | |||

| (A.16) | |||

| (A.17) |

Proof.

(of Lemma A.5)

Proof of (A.10): Since is independent of and , we combine this fact with Lemma A.2:

| (A.18) |

Considering the expression of , we have

Therefore, combine with (A.18), we have

Proof of (A.11): Bringing the expression of into consideration, we first have

Then using Lemma A.2 for the same reason, we have

and

Therefore, we have

Proof of (A.15):

First recall the fact that

and is independent of . Using Lemma A.2,we have

The part

Therefore, we have

The proof of Lemma A.5 is complete. ∎

Lemma A.6.

Define

then weakly converges to a symmetric random matrix , which is made with independent Gaussian entries of mean zero and variance

where

Proof.

Since and are independent, having the same first four moments, both are made with i.i.d. components, we can now view as a table , made with i.i.d elements of mean 0 and variance 1. Besides, we can rewrite the expression of , , and as follows:

It holds

therefore, the matrix

is symmetric. Define

| (A.21) |

Now we can apply the results in Bai and Yao (2008) (Proposition 3.1 and Remark 1), which says that weakly converges to a symmetric random matrix , which is made with i.i.d. Gaussian entries of mean zero and variance

The following is devoted to the calculation of the values of and .

Calculating of : From the definition of (see Bai and Yao (2008) for details), we have

| (A.26) | ||||

| (A.29) | ||||

| (A.30) |

| (A.31) |

| (A.32) |

| (A.33) |

Calculating of :

| (A.34) |

In the following, we will show that and both tend to some limits that is independent of .

| (A.35) |

If we denote as the -th column of , we have

where is independent of . Since

we have

| (A.36) |

whose denominator of (A.37) equals

| (A.37) |

Since is independent of , (A.37) converges to the value according to Lemma A.4. Therefore, we have

| (A.38) |

which is independent of the choice of .

For the same reason, we have

| (A.39) |

If we denote as the -th column of , then we have

and

So we have

| (A.40) |

Combine (A) and (A.40), we have

| (A.41) |

Using the independence between and and Lemma A.4 again, we have

Therefore, we have

which is also independent of the choice of .

Finally, taking the definition of in (A.34) into consideration, we have

| (A.42) |

The proof of Lemma A.6 is complete.

∎