Optimal Multiple Trading Times Under the Exponential OU Model with Transaction Costs††thanks: We thank two anonymous referees for their thorough reviews of our paper and their helpful remarks.

Abstract

This paper studies the timing of trades under mean-reverting price dynamics subject to fixed transaction costs. We solve an optimal double stopping problem to determine the optimal times to enter and subsequently exit the market, when prices are driven by an exponential Ornstein-Uhlenbeck process. In addition, we analyze a related optimal switching problem that involves an infinite sequence of trades, and identify the conditions under which the double stopping and switching problems admit the same optimal entry and/or exit timing strategies. Among our results, we find that the investor generally enters when the price is low, but may find it optimal to wait if the current price is sufficiently close to zero. In other words, the continuation (waiting) region for entry is disconnected. Numerical results are provided to illustrate the dependence of timing strategies on model parameters and transaction costs.

Keywords: optimal double stopping, optimal switching, exponential OU process, transaction costs

JEL Classification: C41, G11, G12

Mathematics Subject Classification (2010): 60G40, 91G10, 62L15

1 Introduction

One important problem commonly faced by individual and institutional investors is to determine when to buy and sell an asset. As a potential investor observes the price process of an asset, she can decide to enter the market immediately or wait for a future opportunity. After completing the first trade, the investor will need to select the time to close the position. This motivates us to investigate the optimal sequential timing of trades.

Naturally, the optimal sequence of trading times should depend on the price dynamics of the risky asset. For instance, if the price process is a super/sub-martingale, then the investor, who seeks to maximize the expected liquidation value, will either sell immediately or wait forever. Such a trivial timing arises when the underlying price follows a geometric Brownian motion. Similar observations can also be found in, among others, Shiryaev et al. (2008). On the other hand, it has been widely observed that many asset prices exhibit mean reversion, ranging from equities and commodities to currencies and volatility indices (see Metcalf and Hassett (1995), Bessembinder et al. (1995), Casassus and Collin-Dufresne (2005), and references therein). To incorporate mean-reversion for positive price processes, one popular choice for pricing and investment applications is the exponential Ornstein-Uhlenbeck (XOU) model, as proposed by Schwartz (1997) for commodity prices, due to its analytical tractability. It also serves as the building block of more sophisticated mean-reverting models.

In this paper, we study the optimal timing of trades under the XOU model subject to transaction costs. We consider two different but related formulations. First, we consider the trading problem with a single entry and single exit with a fixed cost incurred at each transaction. This leads us to analyze an optimal double stopping problem. In the second formulation, the investor is assumed to enter and exit the market infinitely many times with transaction costs. This gives rise to an optimal switching problem.

We analytically derive the non-trivial entry and exit timing strategies. Under both approaches, it is optimal to sell when the asset price is sufficiently high, though at different levels. As for entry timing, we find that, under some conditions, it is optimal for the investor not to enter the market at all when facing the optimal switching problem. In this case for the investor who has a long position, the optimal switching problem reduces into an optimal stopping problem, where the optimal liquidation level is identical to that of the optimal double stopping problem. Otherwise, the optimal entry timing strategies for the double stopping and switching problem are described by the underlying’s first passage time to an interval that lies above level zero. In other words, the continuation region for entry is disconnected of the form , with critical price levels and (see Theorems 3.2 and 3.4 below). This means that the investor generally enters when the price is low, but may find it optimal to wait if the current price is too close to zero. We find that this phenomenon is a distinct consequence due to fixed transaction costs under the XOU model. Indeed, when there is no fixed costs, even if there are proportional transaction costs (see Zhang and Zhang (2008)), the entry timing is simply characterized by a single price level.

A typical solution approach for optimal stopping problems driven by diffusion involves the analytical and numerical studies of the associated free boundary problems or variational inequalities (VIs); see e.g. Bensoussan and Lions (1982), Øksendal (2003), and Sun (1992). This approach is very useful when the structure of the optimal buy/sell strategies are known. In contrast to the VI approach, we solve the double stopping problem by characterizing the value functions (for entry and exit) as the smallest concave majorant of the corresponding reward functions (see Dayanik and Karatzas (2003) and references therein). This allows us to directly construct the value function, without a priori finding a candidate value function or imposing conditions on the stopping and continuation regions, such as whether they are connected or not. In other words, our method will derive the structure of the stopping and continuation regions as an output. Moreover, the VI method becomes more challenging when the form of the reward function does not possess some amenable properties, such as convexity, monotonicity, and positivity. This gives another reason for our probabilistic approach since the reward function for the entry problem is neither convex/concave, nor monotone, nor always positive. Having solved the optimal double stopping problem, we determine the optimal structures of the buy/sell/wait regions. We then apply this to infer a similar solution structure for the optimal switching problem and verify using the variational inequalities.

In the literature, Zhang and Zhang (2008) investigate the optimal switching problem under the XOU price dynamics, with slippage (proportional transaction cost). As extension, Kong and Zhang (2010) allow for short selling so that the investor can enter the market with either long or short position, and close it out in the next trade. As a numerical approach, Song et al. (2009) discuss a stochastic approximation scheme to compute the optimal buying and selling price levels by a priori assuming a buy-low-sell-high strategy under the XOU model. In contrast to these studies, we study both optimal double stopping and switching problems specifically under exponential OU with fixed transaction costs. In particular, the optimal entry timing with fixed transaction costs is characteristically different from that with slippage.

Zervos et al. (2013) consider an optimal switching problem with fixed transaction costs under a class of time-homogeneous diffusions, including the GBM, mean-reverting CEV underlying, and other models. However, their results are not applicable to the exponential OU model as it violates Assumption 4 of their paper (see also Remark 4.5 below). Indeed, their model assumptions restrict the optimal entry region to be represented by a single critical threshold, whereas we show that in the XOU model the optimal entry region is characterized by two positive price levels.

As for related applications of optimal double stopping, Leung and Li (2015) study the optimal timing to trade an OU price spread with a stop-loss constraint. Karpowicz and Szajowski (2007) analyze the double stopping times for a risk process from the insurance company’s perspective. The problem of timing to buy/sell derivatives has also been studied in Leung and Ludkovski (2011) (European and American options) and Leung and Liu (2012) (credit derivatives). Menaldi et al. (1996) study an optimal starting-stopping problem for general Markov processes, and provide the mathematical characterization of the value functions.

The rest of the paper is structured as follows. In Section 2, we formulate both the optimal double stopping and optimal switching problems. Then, we present our analytical and numerical results in Section 3. The proofs of our main results are detailed in Section 4. Finally, the Appendix contains the proofs for a number of lemmas.

2 Problem Overview

In the background, we fix a probability space , where is the historical probability measure. In this section, we provide an overview of our optimal double stopping and switching problems, which will involve an exponential Ornstein-Uhlenbeck (XOU) process. The XOU process is defined by

| (2.1) |

Here, is an OU process driven by a standard Brownian motion , with constant parameters , . In other words, is the log-price of the positive XOU process .

2.1 Optimal Double Stopping Problems

Given a risky asset with an XOU price process, we first consider the optimal timing to sell. If the share of the asset is sold at some time , then the investor will receive the value and pay a constant transaction cost . Denote by the filtration generated by , and the set of all -stopping times. To maximize the expected discounted value, the investor solves the optimal stopping problem

| (2.2) |

where is the constant discount rate, and .

The value function represents the expected liquidation value associated with . On the other hand, the current price plus the transaction cost constitute the total cost to enter the trade. Before even holding the risky asset, the investor can always choose the optimal timing to start the trade, or not to enter at all. This leads us to analyze the entry timing inherent in the trading problem. Precisely, we solve

| (2.3) |

with the constant transaction cost incurred at the time of purchase. In other words, the trader seeks to maximize the expected difference between the value function and the current , minus transaction cost . The value function represents the maximum expected value of the investment opportunity in the price process , with transaction costs and incurred, respectively, at entry and exit. For our analysis, the transaction costs and can be different. To facilitate presentation, we denote the functions

| (2.4) |

If it turns out that for some initial value , then the investor will not start to trade . It is important to identify the trivial cases under any given dynamics. Under the XOU model, since implies that for , we shall therefore focus on the case with

| (2.5) |

and solve for the non-trivial optimal timing strategy.

2.2 Optimal Switching Problems

Under the optimal switching approach, the investor is assumed to commit to an infinite number of trades. The sequential trading times are modeled by the stopping times such that

A share of the risky asset is bought and sold, respectively, at times and , . The investor’s optimal timing to trade would depend on the initial position. Precisely, under the XOU model, if the investor starts with a zero position, then the first trading decision is when to buy and the corresponding optimal switching problem is

| (2.6) |

with the set of admissible stopping times , and the reward functions and defined in (2.4). On the other hand, if the investor is initially holding a share of the asset, then the investor first determines when to sell and solves

| (2.7) |

with .

In summary, the optimal double stopping and switching problems differ in the number of trades. Observe that any strategy for the double stopping problems (2.2) and (2.3) are also candidate strategies for the switching problems (2.7) and (2.6) respectively. Therefore, it follows that and Our objective is to derive and compare the corresponding optimal timing strategies under these two approaches.

3 Summary of Analytical Results

We first summarize our analytical results and illustrate the optimal trading strategies. The method of solutions and their proofs will be discussed in Section 4. We begin with the optimal stopping problems (2.2) and (2.3) under the XOU model. Denote the infinitesimal generator of the OU process in (2.1) by

| (3.1) |

Recall that the classical solutions of the differential equation

| (3.2) |

for , are (see e.g. p.542 of Borodin and Salminen (2002) and Prop. 2.1 of Alili et al. (2005)):

| (3.3) | |||

| (3.4) |

Direct differentiation yields that , , and . Hence, we observe that both and are strictly positive and convex, and they are, respectively, strictly increasing and decreasing.

Define the first passage time of to some level by . As is well known, and admit the probabilistic expressions (see Itō and McKean (1965) and Rogers and Williams (2000)):

| (3.5) |

3.1 Optimal Double Stopping Problems

We now present the result for the optimal exit timing problem.

Theorem 3.1

The optimal liquidation problem (2.2) admits the solution

| (3.6) |

where the optimal log-price level for liquidation is uniquely found from the equation

| (3.7) |

The optimal liquidation time is given by

| (3.8) |

Theorem 3.2

Under the XOU model, the optimal entry timing problem (2.3) admits the solution

| (3.9) |

with the constants

| (3.10) |

and the critical levels and satisfying, respectively,

| (3.11) | |||

| (3.12) |

The optimal entry time is given by

| (3.13) |

In summary, the investor should exit the market as soon as the price reaches the upper level . In contrast, the optimal entry timing is the first time that the XOU price enters the interval . In other words, it is optimal to wait if the current price is too close to zero, i.e. if . Moreover, the interval is contained in , and thus, the continuation region for market entry is disconnected.

3.2 Optimal Switching Problems

We now turn to the optimal switching problems defined in (2.6) and (2.7) under the XOU model. To facilitate the presentation, we denote

| (3.14) | |||

| (3.15) |

Applying the operator (see (3.1)) to and (see (2.4)), it follows that and . Therefore, (resp. ) preserves the sign of (resp. ). It can be shown that has a unique root, denoted by . However,

| (3.16) |

may have no root, a single root, or two distinct roots, denoted by and , if they exist. The following observations will also be useful:

| (3.17) |

The optimal switching problems have two different sets of solutions depending on the problem data.

Theorem 3.3

In Theorem 3.3, means that it is optimal not to enter the market at all. On the other hand, if one starts with a unit of the underlying asset, the optimal switching problem reduces to a problem of optimal single stopping. Indeed, the investor will never re-enter the market after exit. This is identical to the optimal liquidation problem (2.2) where there is only a single (exit) trade. The optimal strategy in this case is the same as in (3.6) – it is optimal to exit the market as soon as the log-price reaches the threshold .

We also address the remaining case when none of the conditions in Theorem 3.3 hold. As we show next, the optimal strategy will involve both entry and exit thresholds.

Theorem 3.4

If there are two distinct roots to (3.16), and , and there exists a number satisfying (3.19) such that

| (3.21) |

then the optimal switching problems (2.6) and (2.7) admit the solutions

| (3.22) | ||||

| (3.23) |

where satisfies (3.19), and

| (3.24) |

There exist unique critical levels and which are found from the nonlinear system of equations:

| (3.25) | |||

| (3.26) |

Moreover, the critical levels are such that and .

The optimal strategy in Theorem 3.4 is described by the stopping times , and , with

| (3.27) | ||||

| (3.28) |

In other words, it is optimal to buy if the price is within and then sell when the price reaches . The structure of the buy/sell regions is similar to that in the double stopping case (see Theorems 3.1 and 3.2). In particular, is the same as in Theorem 3.2 since the equations (3.11) and (3.19) are equivalent. The level is only relevant to the first purchase. Mathematically, is determined separately from and . If we start with a zero position, then it is optimal to enter if the price lies in the interval . However, on all subsequent trades, we enter as soon as the price hits from above (after exiting at previously). Hence, the lower level becomes irrelevant after the first entry.

Note that the conditions that differentiate Theorems 3.3 and 3.4 are exhaustive and mutually exclusive. If the conditions in Theorem 3.3 are violated, then the conditions in Theorem 3.4 must hold. In particular, condition (3.19) in Theorem 3.3 holds if and only if

| (3.29) |

where

| (3.30) |

Inequality (3.29) can be numerically verified given the model inputs.

3.3 Numerical Examples

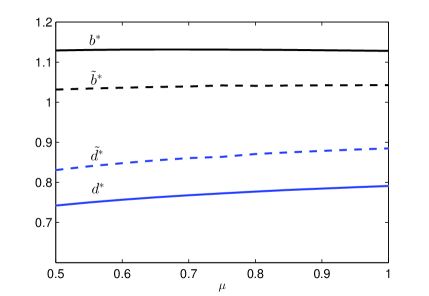

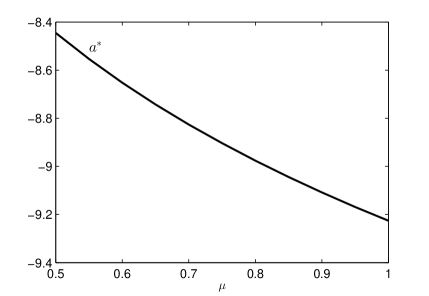

We numerically implement Theorems 3.1, 3.2, and 3.4, and illustrate the associated entry/exit thresholds. In Figure 1 (left), the optimal entry levels and rise, respectively, from 0.7425 to 0.7912 and from 0.8310 to 0.8850, as the speed of mean reversion increases from 0.5 to 1. On the other hand, the critical exit levels and remain relatively flat over . As for the critical lower level from the optimal double stopping problem, Figure 1 (right) shows that it is decreasing in . The same pattern holds for the optimal switching problem since the critical lower level is identical to , as noted above.

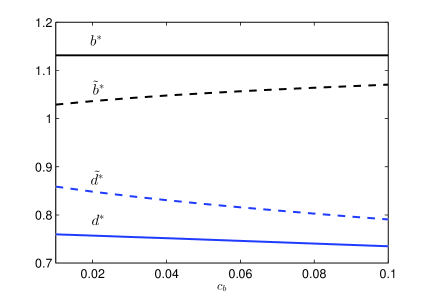

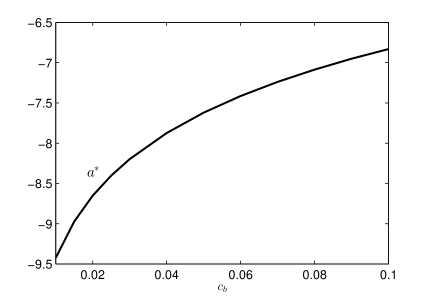

We now look at the impact of transaction cost in Figure 2. On the left panel, we observe that as the transaction cost increases, the gap between the optimal switching entry and exit levels, and , widens. This means that it is optimal to delay both entry and exit. Intuitively, to counter the fall in profit margin due to an increase in transaction cost, it is necessary to buy at a lower price and sell at a higher price to seek a wider spread. In comparison, the exit level from the double stopping problem is known analytically to be independent of the entry cost, so it stays constant as increases in the figure. In contrast, the entry level , however, decreases as increases but much less significantly than . Figure 2 (right) shows that , which is the same for both the optimal double stopping and switching problems, increases monotonically with .

In both Figures 1 and 2, we can see that the interval of the entry and exit levels, , associated with the optimal switching problem lies within the corresponding interval from the optimal double stopping problem. Intuitively, with the intention to enter the market again upon completing the current trade, the trader is more willing to enter/exit earlier, meaning a narrowed waiting region.

Figure 3 shows a simulated path and the associated entry/exit levels. As the path starts at , the investor waits to enter until the path reaches the lower level (double stopping) or (switching) according to Theorems 3.2 and 3.4. After entry, the investor exits at the optimal level (double stopping) or (switching). The optimal switching thresholds imply that the investor first enters the market on day 188 where the underlying asset price is . In contrast, the optimal double stopping timing yields a later entry on day 845 when the price first reaches . As for the exit timing, under the optimal switching setting, the investor exits the market earlier on day 268 at the price . The double stopping timing is much later on day 1160 when the price reaches . In addition, under the optimal switching problem, the investor executes more trades within the same time span. As seen in the figure, the investor would have completed two ‘round-trip’ (buy-and-sell) trades in the market before the double stopping investor liquidates for the first time.

4 Methods of Solution and Proofs

We now provide detailed proofs for our analytical results in Section 3 beginning with Theorems 3.1 and 3.2 for the optimal double stopping problems.

4.1 Optimal Double Stopping Problems

Starting at any , we denote by the exit time from an interval with . If , then we have a.s. In effect, this removes the lower exit level. Similarly, it is possible that , and a.s. Consequently, by considering interval-type strategies, we also include the class of stopping strategies of reaching a single level (as in Theorem 3.1 above).

Now, let us introduce the transformation

| (4.1) |

and define , . With the reward function , and using (4.1), we compute the corresponding expected discounted reward:

| (4.2) | ||||

| (4.3) | ||||

| (4.4) | ||||

| (4.5) |

where

| (4.6) |

The last equality (4.5) transforms the problem from coordinate to coordinate (see (4.1)).

In turn, the candidate optimal exit interval is determined by maximizing the expectation in (4.2). This is equivalent to maximizing (4.5) over and in the transformed problem. As a result, for every we have

| (4.7) |

which is the smallest concave majorant of . Applying (4.7) to (4.5), we can express the maximal expected discounted reward as

Now, it remains to prove the optimality of the proposed stopping strategy. This also provides an analytic expression for the value function.

Theorem 4.1

The proof is similar to that of Theorem 3.2 in Leung and Li (2015), and is thus omitted.

By Theorem 4.1, it is sufficient to consider interval-type strategies for the optimal liquidation problem under the XOU model. Note that the optimal levels can depend on the initial value , and they may coincide or take values or . As such, the structure of the stopping and continuation regions can potentially be characterized by multiple intervals, leading to disconnected continuation regions (see Theorem 3.2 above). In order to determine the optimal exit timing strategies and solve for , the major challenge lies in analyzing the functions and .

4.1.1 Optimal Exit Timing

In preparation for the next result, we apply (4.1) and (3.3)-(3.4) to the definition of in (4.6), and summarize the crucial properties of .

Lemma 4.2

The function is continuous on , twice differentiable on and possesses the following properties:

-

(i)

, and

-

(ii)

is strictly increasing for , and as .

-

(iii)

Based on Lemma 4.2, We sketch in Figure 4. Using the properties of , we now solve for the optimal exit timing.

Proof of Theorem 3.1

We look for the value function of the form: , where is the smallest concave majorant of . By Lemma 4.2, we observe that is concave over , strictly positive over , and as . Therefore, there exists a unique number such that

| (4.9) |

In turn, the smallest concave majorant of is given by

Substituting into (4.9), we have

and

Equivalently, we can express (4.9) in terms of :

which is equivalent to (3.7) after simplification. As a result, we have

In turn, the value function is given by (3.6).

4.1.2 Optimal Entry Timing

We can directly follow the arguments that yield Theorem 4.1, but with the reward as and define analogous to :

| (4.10) |

We will look for the value function with the form: , where is the smallest concave majorant of . The properties of is given in the next lemma.

Lemma 4.3

The function is continuous on , differentiable on , and twice differentiable on , and possesses the following properties:

-

(i)

, and there exists some such that for .

-

(ii)

is strictly decreasing for .

-

(iii)

Define the constant

There exist some constants and , with , that solve , such that

and .

Figure 5 gives a sketch of according to Lemma 4.3, and illustrate the corresponding smallest concave majorant .

Proof of Theorem 3.2

As in Lemma 4.3 and Figure 5, by the definition of the maximizer of , satisfies the equation

| (4.11) |

Also there exists a unique number such that

| (4.12) |

Using (4.11), (4.12) and Figure 5, is a straight line tangent to at on , coincides with on , and is equal to on . As a result,

Substituting into (4.12), we have

and

Equivalently, we can express condition (4.12) in terms of :

which is equivalent to (3.11) after simplification. Also, we can express in terms of :

In addition, substituting into (4.11), we have

which can be further simplified to (3.12). Furthermore, can be written in terms of :

By direct substitution of the expressions for and the associated functions, we obtain the value function in (3.9).

4.2 Optimal Switching Problems

Using the results derived in previous sections, we can infer the structure of the buy and sell regions of the switching problem and then proceed to verify its optimality. In this section, we provide detailed proofs for Theorems 3.3 and 3.4.

Proof of Theorem 3.3 (Part 1)

First, with , we differentiate to get

| (4.13) |

On the other hand, by Ito’s lemma, we have

Note that

This implies that

| (4.14) |

where is defined in (3.30) and

The last line follows from Theorem 50.7 in Rogers and Williams (2000, p. 293). Dividing both sides by and differentiating the RHS of (4.14), we obtain

where

| (4.15) |

Since , we deduce that is equivalent to . Using (4.13), we now see that (3.7) is equivalent to .

Next, it follows from (3.17) that

| (4.16) |

This, together with the fact that , implies that there exists a unique such that if and only if . Next, we show that this inequality holds. By the definition of and , we have

| (4.17) |

Since is strictly decreasing in , the above hold true if and only if . Therefore, we conclude that there exits a unique such that . Using (4.16), we see that

| (4.18) |

Observing that , we can conclude that , or equivalently .

We now verify by direct substitution that and in (3.18) satisfy the pair of variational inequalities:

| (4.19) | ||||

| (4.20) |

First, note that is identically 0 and thus satisfies the equality

| (4.21) |

To show that , we look at the disjoint intervals and separately. For we have

| (4.22) |

which implies . When the inequality

| (4.23) |

can be rewritten as

| (4.24) |

To determine the necessary conditions for this to hold, we consider the derivative of the LHS of (4.24):

| (4.25) |

If has no roots, then is negative for all . On the other hand, if there is only one root , then and for all other . In either case, is a strictly decreasing function and (4.24) is true.

Otherwise if has two distinct roots and with , then

| (4.26) |

Applying (4.26) to (4.25), the derivative is negative on . Hence, is strictly decreasing on . We further note that . Observe that on the interval , the intergrand is positive. It is therefore possible for to change sign at some . For this to happen, the positive part of the integral must be larger than the absolute value of the negative part. In other words, (3.29) must hold. If (3.29) holds, then there must exist some such that , or equivalently (3.19) holds:

If (3.19) holds, then we have

In addition, since

it follows that

This establishes the equivalence between (3.19) and (3.29). Under this condition, is strictly decreasing on . Then, either it is strictly increasing on , or there exists some such that is strictly increasing on and strictly decreasing on . In both cases, (4.24) is true if and only if (3.20) holds.

Alternatively, if (3.29) doesn’t hold, then by in (4.25), the integral will always be negative. This means that the function is strictly decreasing for all , in which case (4.24) holds.

Proof of Theorem 3.4 (Part 1)

Define the functions

| (4.32) | ||||

| (4.33) |

We look for the points such that

| (4.34) |

This is because these two equations are equivalent to (3.25) and (3.26), respectively.

Now we start to solve the equations by first narrowing down the range for and . Observe that

| (4.35) |

for all and such that . Therefore, .

Since satisfies and satisfies (3.19), we have

| (4.36) |

for all . Also, we note that

| (4.37) |

and

| (4.38) |

Then, (4.37) and (4.38) imply that there exists a unique function s.t. and

| (4.39) |

Differentiating (4.39) with respect to , we see that

| (4.40) |

for all . In addition, by the facts that satisfies , satisfies (3.19), and the definition of , we have

By (4.35), we have . By computation, we get that

for all . Therefore, there exists a unique such that if and only if

| (4.41) |

The above inequality holds if (3.21) holds. Indeed, direct computation yields the equivalence:

When this solution exists, we have

| (4.42) |

Next, we show that the functions and given in (3.22) and (3.23) satisfy the pair of VIs in (4.19) and (4.20). In the same vein as the proof for the Theorem 3.3, we show

| (4.43) |

by examining the 3 disjoint regions on which assume different forms. When

| (4.44) |

Next, when

| (4.45) |

Finally for ,

| (4.46) |

as a result of (4.26) since .

Next, we verify that

| (4.47) |

Indeed, we have for . When , we get the inequality since and due to (3.17).

It remains to show that and . When , we have

This inequality holds since we have shown in the proof of Theorem 3.3 that is strictly decreasing for . In addition,

since (4.16) (along with the ensuing explanation) implies that is increasing for all .

In the other region where , we have

When , it is clear that

To establish the inequalities for , we first denote

In turn, we compute to get

Recall the definition of and , and the fact that , we have for and for . These, together with the fact that , imply that

Furthermore, since we have

| (4.48) |

and

| (4.49) | ||||

| (4.50) |

In view of inequalities (4.48) and (4.49), the maximum principle implies that and for all . Hence, we conclude that and hold for .

Proof of Theorems 3.3 and 3.4 (Part 2)

We now show that the candidate solutions in Theorems 3.3 and 3.4, denoted by and , are equal to the optimal switching value functions and in (2.6) and (2.7), respectively. First, we note that and , since and dominate the expected discounted cash low from any admissible strategy.

Next, we show the reverse inequaities. In Part 1, we have proved that and satisfy the VIs (4.19) and (4.20). In particular, we know that , and . Then by Dynkin’s formula and Fatou’s lemma, as in Øksendal (2003, p. 226), for any stopping times and such that almost surely, we have the inequalities

| (4.51) |

For , noting that almost surely, we have

| (4.52) | ||||

| (4.53) | ||||

| (4.54) | ||||

| (4.55) | ||||

| (4.56) |

where (4.52) and (4.54) follow from (4.51). Also, (4.53) and (4.55) follow from (4.19) and (4.20) respectively. Observing that (4.56) is a recursion and in both Theorems 3.3 and 3.4, we obtain

Maximizing over all yields that . A similar proof gives .

Remark 4.4

If there is no transaction cost for entry, i.e. , then , which is now a linear function with a non-zero slope, has one root . Moreover, we have for and for . This implies that the entry region must be of the form , for some number . Hence, the continuation region for entry is the connected interval .

Remark 4.5

Let be the infinitesimal generator of the XOU process , and define the function . In other words, we have the equivalence:

| (4.57) |

Referring to (3.16) and (3.17), we have either that

| (4.58) |

where and and are two distinct roots to (3.16), or

| (4.59) |

where and is the single root to (3.16). In both cases, Assumption 4 of Zervos et al. (2013) is violated, and their results cannot be applied. Indeed, they would require that is strictly negative over a connected interval of the form , for some fixed . However, it is clear from (4.58) and (4.59) that such a region is disconnected.

In fact, the approach by Zervos et al. (2013) applies to the optimal switching problems where the optimal wait-for-entry region (in log-price) is of the form , rather than the disconnected region , as in our case with an XOU underlying. Using the new inferred structure of the wait-for-entry region, we have modified the arguments in Zervos et al. (2013) to solve our optimal switching problem for Theorems 3.3 and 3.4.

Appendix A Appendix

A.1 Proof of Lemma 4.2 (Properties of ). The continuity and twice differentiability of on follow directly from those of , and . On the other hand, we have . Hence, the continuity of at follows from

Next, we prove properties (i)-(iii) of .

(i) This follows trivially from the fact that is a strictly increasing function and .

(ii) By the definition of ,

For , , , so . Also, since both and are positive, we conclude that for .

The proof of the limit of will make use of property (iii), and is thus deferred until after the proof of property (iii).

(iii) By differentiation, we have

Since and are all positive, we only need to determine the sign of . Hence, property (iii) follows from (3.17).

To find the limit of , we first observe that

| (A.1) |

Indeed, we have

Since the first term on the RHS is non-negative and the second term is strictly increasing and convex in , the limit is zero.

Turning now to , we note that

As we have shown, for , is a positive and decreasing function. Hence the limit exists and satisfies

| (A.2) |

Observe that , , and exists, and . We apply L’Hopital’s rule to get

| (A.3) |

Comparing (A.1) and (A.3) implies that . From (A.2), we conclude that .

A.2 Proof of Lemma 4.3 (Properties of ). It is straightforward to check that is continuous and differentiable everywhere, and twice differentiable everywhere except at . The same properties hold for . Since both and are twice differentiable everywhere, the continuity and differentiability of on and twice differentiability on follow directly.

To see the continuity of at , note that and as . Then we have

and . There follows the continuity at .

(i) For , we have . Next, the limits and imply that . Therefore, there exists some such that for . For the non-trivial case in question, must be positive for some , so we must have . To conclude, we have for . This, along with the facts that is a strictly increasing function and , implies property (i).

(ii) By differentiating , we get

To determine the sign of , we observe that, for ,

Also, for . Therefore, is strictly decreasing for .

(iii) To study the convexity/concavity, we look at the second derivative

Since and are all positive, we only need to determine the sign of :

which suggests that is convex for .

Furthermore, for , we have

by the definition of . Therefore, is also convex on . Thus far, we have established that is convex on .

Next, we determine the convexity of on . Denote . Since , we must have . By its continuity and differentiability, must be concave at . Then, there must exist some interval over which is concave and .

On the other hand, for ,

where . Therefore, is strictly decreasing on , strictly increasing on , and is strictly positive at and :

If , then there exist exactly two distinct roots to the equation , denoted as and , such that and

On the other hand, if , then for all , and is convex for all , which contradicts with the existence of a concave interval. Hence, we conclude that , and is the unique interval that . Consequently, coincides with and . This completes the proof.

References

- Alili et al. (2005) Alili, L., Patie, P., and Pedersen, J. (2005). Representations of the first hitting time density of an Ornstein-Uhlenbeck process. Stochastic Models, 21(4):967–980.

- Bensoussan and Lions (1982) Bensoussan, A. and Lions, J.-L. (1982). Applications of Variational Inequalities in Stochastic Control. North-Holland Publishing Co., Amsterdam.

- Bessembinder et al. (1995) Bessembinder, H., Coughenour, J. F., Seguin, P. J., and Smoller, M. M. (1995). Mean reversion in equilibrium asset prices: Evidence from the futures term structure. The Journal of Finance, 50(1):361–375.

- Borodin and Salminen (2002) Borodin, A. and Salminen, P. (2002). Handbook of Brownian Motion: Facts and Formulae. Birkhauser, 2nd edition.

- Casassus and Collin-Dufresne (2005) Casassus, J. and Collin-Dufresne, P. (2005). Stochastic convenience yield implied from commodity futures and interest rates. The Journal of Finance, 60(5):2283–2331.

- Dayanik and Karatzas (2003) Dayanik, S. and Karatzas, I. (2003). On the optimal stopping problem for one-dimensional diffusions. Stochastic Processes and Their Applications, 107(2):173–212.

- Itō and McKean (1965) Itō, K. and McKean, H. (1965). Diffusion Processes and Their Sample Paths. Springer Verlag.

- Karpowicz and Szajowski (2007) Karpowicz, A. and Szajowski, K. (2007). Double optimal stopping of a risk process. Stochastics: An International Journal of Probability and Stochastics Processes, 79(1-2):155–167.

- Kong and Zhang (2010) Kong, H. T. and Zhang, Q. (2010). An optimal trading rule of a mean-reverting asset. Discrete and Continuous Dynamical Systems. Series B, 14(4):1403–1417.

- Leung and Li (2015) Leung, T. and Li, X. (2015). Optimal mean reversion trading with transaction costs and stop-loss exit. International Journal of Theoretical & Applied Finance.

- Leung and Liu (2012) Leung, T. and Liu, P. (2012). Risk premia and optimal liquidation of credit derivatives. International Journal of Theoretical & Applied Finance, 15(8):1–34.

- Leung and Ludkovski (2011) Leung, T. and Ludkovski, M. (2011). Optimal timing to purchase options. SIAM Journal on Financial Mathematics, 2(1):768–793.

- Menaldi et al. (1996) Menaldi, J., Robin, M., and Sun, M. (1996). Optimal starting-stopping problems for Markov-Feller processes. Stochastics: An International Journal of Probability and Stochastic Processes, 56(1-2):17–32.

- Metcalf and Hassett (1995) Metcalf, G. E. and Hassett, K. A. (1995). Investment under alternative return assumptions comparing random walks and mean reversion. Journal of Economic Dynamics and Control, 19(8):1471–1488.

- Øksendal (2003) Øksendal, B. (2003). Stochastic Differential Equations: an Introduction with Applications. Springer.

- Rogers and Williams (2000) Rogers, L. and Williams, D. (2000). Diffusions, Markov Processes and Martingales, volume 2. Cambridge University Press, UK, 2nd edition.

- Schwartz (1997) Schwartz, E. (1997). The stochastic behavior of commodity prices: Implications for valuation and hedging. The Journal of Finance, 52(3):923–973.

- Shiryaev et al. (2008) Shiryaev, A., Xu, Z., and Zhou, X. (2008). Thou shalt buy and hold. Quantitative Finance, 8(8):765–776.

- Song et al. (2009) Song, Q., Yin, G., and Zhang, Q. (2009). Stochastic optimization methods for buying-low-and-selling-high strategies. Stochastic Analysis and Applications, 27(3):523–542.

- Sun (1992) Sun, M. (1992). Nested variational inequalities and related optimal starting-stopping problems. Journal of Applied Probability, 29(1):104–115.

- Zervos et al. (2013) Zervos, M., Johnson, T., and Alazemi, F. (2013). Buy-low and sell-high investment strategies. Mathematical Finance, 23(3):560–578.

- Zhang and Zhang (2008) Zhang, H. and Zhang, Q. (2008). Trading a mean-reverting asset: Buy low and sell high. Automatica, 44(6):1511–1518.