On econometric inference

and multiple use of the same data

Abstract.

In fields that are mainly nonexperimental, such as economics and finance, it is inescapable to compute test statistics and confidence regions that are not probabilistically independent from previously examined data. The Bayesian and Neyman-Pearson inference theories are known to be inadequate for such a practice. We show that these inadequacies also hold m.a.e. (modulo approximation error). We develop a general econometric theory, called the neoclassical inference theory, that is immune to this inadequacy m.a.e. The neoclassical inference theory appears to nest model calibration, and most econometric practices, whether they are labelled Bayesian or à la Neyman-Pearson. We derive a general, but simple adjustment to make standard errors account for the approximation error.

Keywords: Hypothesis testing; Confidence region; Estimation; Model calibration.

JEL classification: C1.

1. Introduction

By definition, in nonexperimental fields, new data cannot be generated. Consequently, it is inescapable to compute test statistics and confidence regions that are not probabilistically independent from previously examined data. By the Skorohod’s representation (1976), this practice is equivalent to using twice the same data, so that we call it multiple use of the same data.111The Skorohod’s representation (1976) states that, for any two Borel random variables and , there exist a Borel random variable independent from , and a Borel function such that . Thus, if and are not independent, using first , and then is equivalent to using first , and then reusing with . The main objective of this paper is to develop a general econometric theory, called the neoclassical inference theory,222There are two reasons for this name. Firstly, it is a classical theory, in the statistical sense of the term, i.e., in this theory, the unknown parameter is not treated as a random variable, but as a constant. Secondly, it is neoclassical in the historical sense of the term: it seems to formalize underlying principles of work by classical authors (e.g., Laplace, 1812/1820, livre II, chap. 3; Fisher, 1925/1973, part V). that is adequate for multiple use of the same data m.a.e. (modulo approximation error). The Bayesian and Neyman-Pearson inference theories are not adequate for such a practice, even m.a.e. Thus, if we set aside approximation errors, for which we provide an adjustment, this paper elucidates why econometric inference is possible in fields that are mainly nonexperimental, such as economics and finance.

1.1. Key idea

In Bayesian and Neyman-Pearson theories, test statistics and confidence regions are not independent from data as the former are functions of the latter even m.a.e. Then, if the same realized data are re-used to compute new test statistics or confidence regions, distributions conditional on the previously observed statistics should be considered (e.g., Lehmann and Romano, 1959/2005, sec. 10.1 for Neyman-Pearson theory; Savage, 1954/1972, sec. 3.5 for Bayesian theory). We show that this conditioning, which is typically ignored in practice, is a challenge for Bayesian and Neyman-Pearson theories. The neoclassical inference theory circumvents this conditioning. The key idea is to use realized data to approximate the distribution of random variables, called generic proxies, that have the same unconditional distribution as data-based statistics, but are probabilistically independent from the realized data.

Example.

Let be data that are assumed to be i.i.d. (independent and identically distributed) random variables following a Gaussian distribution with mean and standard deviation , denoted . The realized data are where denotes an element of the sample space . We want to make inference about the unknown parameter through its finite-sample proxy, the average. Now, consider generic data that are independently generated by the same Gaussian distribution as the data , i.e., and are independent, but have the same unconditional distribution. Then, the average of the data , denoted , and the average of the generic data, denoted , have the same unconditional distribution, , and are equally informative about . Nevertheless, previous knowledge of the realized data typically affects the distribution of , but does not affect the distribution of the generic proxy . For example, if the realized average is known from a previous study, there is no uncertainty about it, so that its distribution is a Dirac at the realized average (i.e., ), while the distribution of is still the same Gaussian distribution, . Thus, the idea of the neoclassical inference theory is to rely on an approximation of the distribution of to make inference about . Although the data are independent from the generic proxy , their observation provides an approximation of its distribution. For example, by the Lindeberg-Lévy CLT (central limit theorem), a Gaussian distribution centered at the realized average, , with standard deviation , is an approximation of the distribution of , which is .

A similar idea is present in Monte-Carlo simulation methods : The observation of realized random variables enables the approximation of the distribution of a generic random variable, which is independent from the realized ones. In fact, this similarity has a mathematical underpinning under the standard assumption of ergodicity, which stipulates an equivalence between exploration of the sample space and exploration of the time dimension.

In a way, the neoclassical inference theory generalizes the immunity of the standard justification of point estimators, consistency, to confidence intervals and tests. Unlike the Neyman-Pearson justifications for tests and confidence regions, consistency is immune to multiple use of the same data m.a.e. A consistent point estimator of a parameter does not depend on the realized data m.a.e.: by the definition of consistency, for almost all possible realizations of the data, such a point estimator is arbitrary close to the fixed parameter m.a.e. See Appendix A on p. A for a formal statement.

1.2. Literature overview

In the statistical and econometric literature, the issue raised by multiple use of the same data for Neyman-Pearson and Bayesian inference theories has been occasionally discussed. E.g., Lehmann and Romano, 1959/2005, sec. 10.1 for Neyman-Pearson theory; Berger, 1980/2006, pp. 112–113 and 284 for Bayesian theory; Leamer, 1978, pp. v–vii for an assessment of the acuteness of the issue, and chap. 9 for an ad hoc proposal to mitigate the issue for Bayesian inference. The common wisdom seems to be that the issue is unavoidable. To the best of our knowledge, no general formal solution has been proposed even m.a.e. Holcblat (2012) relies on the idea behind the neoclassical theory only in the particular case of the empirical saddlepoint (ESP) approximation.

Multiple use of the same data is not treated in the large literature about multiple hypothesis testing (e.g., Lehmann and Romano, 1959/2005, chap. 9 for a perspective à la Neyman-Pearson; Berger, 1980/2006, chap. 7 for a Bayesian perspective). In this literature, it is assumed that the set of all statistics to be potentially computed is determined before examination of the data. This situation does not correspond to nonexperimental fields as their evolution is often the result of a hard-to-predict dialogue between theory and empirical studies based on more or less the same realized data. For example, Compustat, CRSP (Center for Research in Security Prices) and BEA (Bureau of Economic Analysis) data have been re-used in numerous empirical studies in corporate finance, asset pricing and macroeconomics, respectively.

1.3. Organization of the paper

The paper is organized as follows. Section 2 and 3, respectively, show that Neyman-Pearson and Bayesian inference theories are inadequate for multiple use of the same data even m.a.e. Section 4 presents elements of the neoclassical theory, and proves its immunity to multiple use of the same data m.a.e. Section 5 revisits model calibration and prominent econometric practices from a neoclassical point of view, and presents a simple adjustment to make standard errors account for the approximation error. An important point to note is that this standard-error adjustment holds under the usual -asymptotic normality assumption, thus applying to a large part of econometric practice. Some readers may find sections 2 and 3 obvious, but the latter should be considered in comparison with section 4. The contribution of this paper is essentially theoretical, and not mathematical. Applied econometricians might want to focus on subsection 5.3, which assesses the most common econometric practice from a neoclassical point of view.

Remark 1.

In accordance with the main objective of this paper, we reason m.a.e. in sections 2- 4. For the Neyman-Pearson theory, ignoring approximation errors means that we consider the asymptotic limit superior (or limit inferior) of the outer (or inner) probability distribution to be exact for the given sample size, when the sampling distribution is not available. For the Bayesian theory, this has no bearing because probability distributions are assumed to be perfectly known by the econometrician (e.g., Savage, 1954/1972, pp. 59–60). For the neoclassical inference theory, this means that we consider the approximation of the sampling distribution of the generic proxy to be exact. Unlike sections 2- 4, section 5 does not reason m.a.e., and treats of the approximation error from a neoclassical point of view.

2. Neyman-Pearson theory and multiple use of the same data

In this section, we explain the m.a.e. inadequacy of the Neyman-Pearson theory for multiple use of the same data. Subsection 2.1 informally explains it in the standard case of asymptotic -statistics. Subsection 2.2 formalizes it in the general case.

2.1. The case of asymptotic -statistics

Asymptotic -statistics are among the most widely-used statistics to compute confidence regions or carry out hypothesis tests. The Neyman-Pearson theoretical justification of an asymptotic -test of size is that the -statistic has a probability m.a.e. to be between the and quantiles of a standard Gaussian distribution under the test hypothesis. However, once computed, the -statistic is in the non-rejection region with probability 0 or 1, i.e., it is or it is not in the non-rejection region. Thus, if the result of this first test leads the econometrician to compute a second -test of size , the corresponding -statistic cannot typically have a probability of m.a.e. to be between the and quantiles of a standard Gaussian distribution under the test hypothesis. The observation of the first -statistic has removed a part of the randomness of the second -statistic. Except in a few cases (e.g., Gouriéroux and Monfort, 1989/1996, chap. 19), -statistics computed on the same data set are not independent. This means that the Neyman-Pearson theoretical justification does not hold for the second -test. Because of the duality between hypothesis testing and confidence regions in the Neyman-Pearson theory, there is the same concern for confidence intervals based on -statistics. Subsection 2.2 proves that this concern about the Neyman-Pearson theoretical justification of confidence regions and tests is not limited to -statistics.

2.2. The general case

Assumption 1 sets up the minimal elements of the Neyman-Pearson theory that are necessary to formalize multiple use of the same data.

Assumption 1.

(a) Let be a measurable space where denotes a -algebra of . (b) Let be the unknown parameter, where denotes the parameter space. (c) Let be some data, i.e., a measurable mapping from to a measurable space , where and denote the sample size and the observation space, respectively.

Remark 2.

There is no restriction on the parameter space , so that it can be Euclidean or infinite-dimensional.

Definition 1 (Neyman-Pearson confidence region).

Let , and a probability measure on . Under , a Neyman-Pearson confidence region is a measurable random subset of the parameter space that has a probability of at least m.a.e. to contain the unknown parameter , i.e., (i) for all , , (ii) m.a.e., and (iii) m.a.e.

Definition 2 (Neyman-Pearson test).

Let be a test hypothesis, and a probability measure on . Define the measurable decision space where , and denotes the power set of . The decisions and , respectively, correspond to the non-rejection and the rejection of the test hypothesis . Under , a Neyman-Pearson test of level is a decision rule that leads to the rejection of with a probability of at most m.a.e. under , i.e., a -measurable function m.a.e. s.t. m.a.e., if is true.

Remark 3.

As indicated by the qualification “m.a.e.,” when no finite-sample distribution is available, we consider the asymptotic limit superior (or limit inferior) of the outer (or inner) probability distribution. (see Remark 1 on p. 1). Thus, our setup covers asymptotic Neyman-Pearson tests and confidence regions, and the case à la Hoffmann-Jørgensen (see Wellner and van der Vaart, 1996), in which finite-sample statistics are not measurable although their limit is measurable. In the latter case, in Definitions 1 and 2, and , respectively, stand for and where and , respectively, denote the inner and outer probabilities implied by .

Theorem 1 formalizes the concern raised by previous knowledge of realized data that are not probabilistically independent from Neyman-Pearson confidence regions and tests.

Theorem 1 (Neyman-Pearson inadequacy).

Let be the unknown probability measure on , and a nonzero-probability event, i.e., . For all , define . Denote a Neyman-Pearson confidence region for under with , and a Neyman-Pearson test of level under with . Under Assumption 1,

-

i)

if and are not independent m.a.e., then

-

ii)

if and are not independent m.a.e., then

Proof.

It is definition chasing, essentially. For (i) and (ii), respectively denote and with . By definition of independence between events, m.a.e., , where equivalences can be seen as follows. (a) By assumption, . (b) By definition, . See Appendix B on p. B for more details regarding the possible approximation error. ∎

The key defining properties of a Neyman-Pearson confidence region and test are, respectively, the probability that the confidence region contains the unknown parameter, and the probability of rejecting the hypothesis under the test hypothesis. Theorem 1 proves that these key defining properties are affected by the previous observation of a nonzero-probability event that is not probabilistically independent from the corresponding confidence region and test. Before the observation of , the probability of the Neyman-Pearson Definitions 1 and 2 is m.a.e., but, after observation of , is m.a.e.

A solution would be to systematically account for previous knowledge of the data by determining conditional probability, such as . However, most of the time, this is operationally impossible, especially in nonexperimental fields. In nonexperimental fields, this previous knowledge can correspond to computed statistics or plots, but also to historical events personally experienced or studied. For example, defining valid Neyman-Pearson tests or confidence regions for an applied American econometrician who studies the US economy appears an impossible task. Moreover, even if it was possible, it would make criteria of validity of statistical discoveries path-dependent, and thus difficult to understand. Therefore, the Neyman-Pearson inference theory appears practically inadequate for nonexperimental fields.

Remark 4.

Because of our focus on multiple use of the same data, in this paper, we present the operational impossibility to condition on previous knowledge of the realized data as the source of the Neyman-Pearson inadequacy. In fact, if one makes the distinction between unknown and random quantities as the Neyman-Pearson theory does (e.g., is unknown, but constant), it is the realization of the data and not the knowledge of them that matters. Thus, one needs to condition on all the data that have been realized prior to the determination of the test statistics and confidence regions to be computed. When only part of the data at use have been previously realized, we are back to Theorem 1 and the generic operational impossibility to determine conditional probability. When all the data at use have been previously realized, the conditioning is trivial, but then tests should should have zero probability type I error m.a.e., and, under additional but general assumptions, m.a.e. -a.s. See Appendix C on p. C.

3. Bayesian theory and multiple use of the same data

“In a strictly logical sense, this criticism of (practical) prior dependence

on the data cannot be refuted.”

Berger (1980/2006, p. 112).

As for Neyman-Pearson theory, multiple use of the same data is a challenge for Bayesian inference theory. Subsection 3.1 explains the concern in the basic case in which Bayes’ formula holds, and subsection 3.2 formalizes it in the general case.

3.1. The basic case

Taken literally, Bayesian theory regards inference as a two-stage game between nature and an econometrician (e.g., Ferguson, 1967; Borovkov, 1984/1998). In the first stage, nature draws the parameter according to a prior distribution , and then draws data according to a conditional probability density function (p.d.f.), . In the second stage, the econometrician makes inferences about the realized parameter value given the sample at hand.333To avoid additional notations, the random parameter is defined as the identity mapping on the parameter space , so that its realized value is also denoted by . As usual in game theory, the p.d.f. and are common knowledge. Thus, the econometrician updates the prior distribution, , thanks to data according to Bayes’ formula

to obtain the posterior distribution .

But, after the p.d.f. of the unknown parameter given the data has been computed, the data are known and fixed. Their randomness has disappeared. Thus, the econometrician cannot learn anymore from them. If the Bayes formula is applied a second time to the same data, the p.d.f. of data conditional on the unknown parameter is one, so that the second posterior is equal to the first posterior. Mathematically, Bayesian updating becomes

Therefore, Bayes inference theory cannot justify multiple use of the same data. Subsection 3.2 shows that the conclusion remains unchanged in the general case, in which densities do not necessarily exist.

3.2. The general case

Assumption 2 defines the general structure of Bayesian inference along the lines of Florens, Mouchart and Rolin (1990).444The main difference between their notations and our notations is the following. Unlike them, we do not identify -algebras with their inverse image by the coordinate map. See Florens, Mouchart and Rolin, 1990, p. 11, warning. Our choice makes the presentation less elegant, but it allows us to maintain notational consistency within this paper.

Assumption 2.

(a) Let be a probability space, where is the parameter space, and where denotes the product -algebra of the -algebras and . (b) Let be a filtration in . Define a filtration in s.t., for all , .

The filtration corresponds to the accumulation of information that comes from the sample space. In other words, is the information set of the econometrician after Bayesian updates. Definition 3 reminds the general definition of posterior probabilities.

Definition 3 (Posterior probability).

For all and , the -posterior probability of is the expectation of the indicator function conditional on , i.e., .

Implicitly, Definition 3 also defines priors as the distinction between a prior and a posterior depends on the update of reference. After Bayesian updates, is the prior, while is the posterior.

Remark 5.

The framework is general: We do not impose restrictions on the parameter space , or require the existence of regular conditional probabilities.

Assumption 3 specify the minimal additional ingredients necessary to study multiple use of the same data.

Assumption 3.

(a) Let be some data, i.e., a measurable mapping from to the measurable space , where denotes the observation space. (b) There exists s.t. , where denotes the -algebra generated by , and the -algebra generated by the union of and , i.e., .

Assumption 3(a) requires the existence of data, , while Assumption 3(b) requires that update comes from the use of the data . Theorem 2 formalizes the effect of a second use of the same data .

Theorem 2 (Bayesian inadequacy).

Proof.

It is definition chasing. By definition, , where equalities can be seen as follows. (a) By Assumption 3(b), . (b) is itself a -algebra by definition of a filtration. ∎

The update corresponds to the first use of the data , while the update corresponds to the second use. Theorem 2 proves that the second use of the same data does not increase the information set, , and thus the posterior remains the same. An immediate corollary of this result is the absence of formal Bayesian justification for analyses, in which an econometrician claims to have obtained a different “posterior” after a first use of the same data. Theorem 2 shows that such analyses are incompatible with Bayesian inference theory.

Remark 6.

For brevity and relevance, we mainly consider the Neyman-Pearson and Bayesian inadequacy when there is partial, and complete previous knowledge of the realized data, respectively. However, in parallel, complete, and partial previous knowledge causes Neyman-Pearson and Bayesian inadequacy, respectively. Complete previous knowledge causes Neyman-Pearson inadequacy when the randomness needed to justify a new test or a new confidence region has completely disappeared. For example, when one wants a -test of size after computation of a confidence interval based on the same statistic, the -statistic is between the and quantiles with probability or because a confidence interval corresponds to the set of hypothesis that would not have been rejected. See also Proposition 3 on p. 3, which can be seen as a formalization of the case, in which all the data have been previously examined. Partial knowledge causes Bayesian inadequacy when it is impossible to incorporate previous information through a formal Bayesian updating. For example, Bayesian inference theory is typically inadequate when partial previous knowledge corresponds to historical events personally experienced. See also Savage (1954/1972, pp. 59–60) for more details about this inadequacy.

As Neyman-Pearson theory, Bayesian inference theory is inadequate for multiple use of the same data. Both theories rely on a randomness, which is disappearing as data are used, so that multiple use of the same data appears difficult to justify. However, in nonexperimental fields, multiple use of the same data is inescapable. Thus, the relevance of Neyman-Pearson and Bayesian inference theories to nonexperimental fields is not obvious.

4. Elements of neoclassical inference theory

The purpose of this section is to introduce elements of a theory that is immune to multiple use of the same data m.a.e., and that provides a common framework for point estimation, confidence regions and hypothesis testing. There does not seem to exist such an inference theory in the literature.

This section is organized as follows. Subsection 4.1 presents the main idea of the neoclassical theory, subsection 4.2 its main elements, and subsection 4.3 proves that it is theoretically immune to multiple use the same data m.a.e. Hereafter, for simplicity, we only consider the parameter space to be an Euclidean space.

4.1. Main idea

The setup of the neoclassical inference theory is standard (e.g., Borovkov, 1984/1998, chap. 2). An econometrician wants to infer a constant and unknown parameter of an econometric model . The parameter is assumed to belong to a known parameter space, denoted . The only difference between the unknown parameter, , and other elements of the parameter space is that the former one equals a mapping of the generating probability measure, , i.e.,

| (1) |

where maps probability measures to elements of the parameter space . The econometrician does not know , but has access to some data that are assumed to be generated by the econometric model . Thus, the econometrician approximates using the data , i.e., defines a proxy

| (2) |

where is a mapping from the observation space to the parameter space . Often, , where is the empirical measure with denoting the Dirac measure at . We call a finite-sample proxy of the unknown parameter .

Now, if there exist some data with the same unconditional distribution as (i.e., ) but independent from them, these data induce an equally informative finite-sample proxy of

| (3) |

Building on this remark, the idea of the neoclassical inference theory is to base inference of on an approximation of the distribution of a generic finite-sample proxy of that has the same unconditional distribution as , but is independent from the data . We denote the generic finite-sample proxy with . In this paper, we take the finite-sample proxy (i.e., the choice of ) as given, in order to stay away from the question of the properties of the generic proxy .555This question, which can be seen as one of the main topic of the statistical and econometric literature, corresponds to the study of the properties of what is called the estimator in the Neyman-Pearson theory.

4.2. Definitions

We require the following assumptions, in addition to Assumption 1, to outline the neoclassical theory.

Assumption 4.

(a) Let be the unknown probability measure on . (b) Let be a measurable space s.t. is a Borel subset of with , and denotes the Borel -algebra on . (c) Let be a uniformly distributed random variable with support on the probability space, , s.t. and are independent for all .

Assumption 4(c) is the only assumption that is new with respect to Neyman-Pearson theory. Nevertheless, its novelty is limited as econometric reasoning (e.g., asymptotic theory) and implementations of the Neyman-Pearson theory (e.g., bootstrap) often implicitly require it. The random variable is a randomization device that ensures the existence of the generic finite-sample proxy . More generally, Assumption 4(c) ensure the existence of a countable number of random variables with any probability distribution (e.g., Kallenberg, 1997/2002, Lemmas 3.21 and 3.22). Such an assumption is innocuous. We can always redefine the probability space as the product of an original probability space with the probability space , where and , respectively, denote the Borel -algebra on and the Lebesgue measure (e.g., Kallenberg, 1997/2002, pp. 111–112).

Thanks to Assumption 4(c), given a (data-based) finite-sample proxy of , Lemma 1 proves the existence of a corresponding generic proxy of .

Lemma 1 (Existence of a generic proxy).

Proof.

This is an application of a known generalization of the standard inverse transform method that is used to simulate random variables from a uniform distribution (e.g., Kallenberg, 1997/2002, p. 56, Lemma 3.22). By Assumption 4(b), is a Borel space, i.e., there exists a Borel measurable bijection , with , s.t. is also measurable. Denote the c.d.f. of with and put , . Then, under Assumption 4(a), for all , , where (a) and (c) are a consequence of the bimeasurability and bijectivity of , and (b) is an application of the standard inverse transform method by Assumption 4(c). Now, again by Assumption 4(c), is independent from data. Thus, put . ∎

In this paper, the definitions of neoclassical estimators and confidence regions and test are based on the generic proxy. To simplify their statements, we require the following assumption.

Assumption 5.

Denote the Borel -algebra on with . There is a -measurable p.d.f. s.t., for all , m.a.e., where is the Lebesgue measure , or the counting measure .

By the Radon-Nikodyn theorem, Assumption 5 requires the distribution of the generic finite-sample proxy , or its approximation to be a probability measure dominated by the Lebesgue or the counting measure. In practice, because is unknown, it requires the approximation of to be a probability measure dominated by the Lebesgue or the counting measure. Instead of requiring the existence of , we could apply the Lebesgue decomposition theorem to write m.a.e. the measure as the sum of a continuous, a discreet and a singular measure. However, it would complicate the upcoming definitions without much tangible gain. In particular, under Assumption 5, the neoclassical estimator is simply a maximizer of the p.d.f. m.a.e.

Definition 4 (Neoclassical estimator).

A neoclassical estimator, denoted , is a maximizer of the p.d.f. m.a.e., i.e.,

Example.

(continued) m.a.e. Thus, the neoclassical estimate is the mode of , i.e., m.a.e.

By Definition 4, a neoclassical estimator is an element of the parameter space that has the highest probability density to be the generic finite-sample proxy m.a.e. Thus, it is a maximum-probability based estimator. In the neoclassical theory, confidence regions are also maximum-probability based.

Definition 5 (Neoclassical confidence region).

Denote the support of with , i.e., . A -measurable set, , is a neoclassical confidence region of level with if, and only if,

where .

Example.

(continued) Because a Gaussian distribution is unimodal and symmetric with respect to its mean, m.a.e., where denotes the quantile of a standard Gaussian distribution.

Remark 7.

By construction, a neoclassical confidence region is an indicator of the confidence we can have in a neoclassical estimate. It is the set of parameter values that are the closest to being the neoclassical estimate, such that the whole set has a probability at least to contain the generic finite-sample proxy m.a.e. Thus, a small connected neoclassical confidence region indicates a well-separated estimate, which is reliable. In contrast, a large neoclassical confidence region or a neoclassical confidence region that consists of the union of disjoint sets indicates an unreliable estimate.

Remark 8.

If the purpose of confidence regions is to indicate the confidence we can have in an estimate, their neoclassical definition is more satisfactory than their Neyman-Pearson definition (inadequacies caused by multiple use of the data and their past realization set aside). The Neyman-Pearson definition of confidence regions is not about the estimate, but about coverage. In particular, Neyman-Pearson confidence regions do not necessarily contain the estimate.

Remark 9.

In Definition 5, the definition of neoclassical estimator is formally close to the definition of Bayesian highest posterior density (HPD) sets (e.g., Berger, 1980/2006, sec. 4.3.2., Definition 5), although their theoretical justification and meaning are fundamentally different.

Although Definition 5 corresponds to a joint confidence region, marginal and conditional neoclassical confidence regions can also be defined by considering the marginal and conditional distribution of . From neoclassical confidence regions, we define neoclassical tests.

Definition 6 (Neoclassical test).

Let be a test hypothesis, and a neoclassical confidence region, where . As in Definition 2, denote the decision space with . A neoclassical test of level for is a decision rule, denoted , s.t. if

then ; otherwise .

Definition 6 leads the econometrician to reject hypotheses that do not correspond to the set of parameter values with the highest probability density of being equal to the generic proxy m.a.e. By Definitions 5, all elements in a neoclassical confidence region have a higher probability density of being equal to the generic finite-sample proxy than the ones outside it m.a.e.

Example.

(continued) If , then we do not reject the test hypothesis, i.e., . Note that, in this example, the neoclassical estimate, confidence region and test are practically equivalent to their usual Neyman-Pearson counterparts, although their theoretical justification is different. Nevertheless, there are Neyman-Pearson confidence regions and tests that do not practically correspond to neoclassical confidence regions or tests. E.g. under the assumption that data have not been realized prior to the decision to compute the confidence interval , the latter is a valid Neyman-Pearson confidence region, while it is not a neoclassical confidence region.

Remark 10.

While the neoclassical definition of confidence regions appears more satisfactory than their Neyman-Pearson definition (see Remark 8, p. 8), the reverse seems to be true for tests (inadequacies caused by multiple use of the data and their past realization set aside). Unlike Neyman-Pearson tests, neoclassical tests do not directly control the probability of making an error, so that their outcome should be understood in terms of evidence in favor of, or against the hypothesis. However, it should be noted that Neyman-Pearson tests control the probability of type I error only ex ante: after computation of the test statistic, the probability of error is or . Moreover, work in progress by the authors suggest that the direct control of type I error can be regained within the neoclassical theory.

Remark 11.

When , the precise choice of is typically crucial for Definitions 4-6 : a modifications of the p.d.f. on a -null set yields another p.d.f. of w.r.t. m.a.e. that can lead to a completely different estimate, confidence region and result of a test (see subsection 5.2). This peculiarity, from which we take advantage in subsection 5.2 (see Remark 17, p. 17), also arises in Neyman-Pearson and Bayesian theories (e.g., Gouriéroux and Monfort, 1989/1996, sec. 7.A.2). Nevertheless, under the mild assumption that is a Lebesgue point, by Lebesgue’s differentiation theorem (e.g., Folland, 1984/1999, Theorem 3.21), is often s.t. m.a.e., where denotes a ball in centered at with radius .

4.3. Neoclassical theory and multiple use of the same data

The upcoming Theorem 3 investigates the adequacy of the neoclassical theory when data have already been used, and thus are known. Because the neoclassical theory is based on the distribution of the generic proxy , it is sufficient to investigate the effect of previous knowledge of the realized data on this distribution.

Theorem 3 (Neoclassical adequacy).

Proof.

Theorem 3 shows that the distribution of the generic proxy is immune to previous knowledge (or realization) of the data. Then, the inadequacy of neoclassical confidence regions and tests follow.

Corollary 1 (Neoclassical confidence region and test adequacy).

Proof.

Apply Theorem 3(ii) putting . ∎

Example.

(continued) For clarity, we now explicitly distinguish between the fixed due to the approximation error and the random elements of the sample space. We denote the latter ones with . By Theorem 3 (i), m.a.e.,

By Corollary 1, m.a.e.,

The distinction between the fixed and the varying is essential. The fixed can be ignored as long as the approximation error is negligible, i.e., the approximation is justified.

Remark 13.

Corollary 1(ii) does not mean or imply that, for all , . First, in the neoclassical theory, approximation errors do not necessarily come from asymptotic approximation (see Remark 1). Second, even in the case, in which the whole approximation error would come from an asymptotic approximation, Corollary 1(ii) only implies independence between and any neoclassical confidence region deduced from , where denotes an approximation of the distribution of the generic proxy . E.g., in the Example, , so that -a.s., which, in turn, implies, -a.s. Therefore, has probability one, and is independent from the data . Note that, in the Neyman-Pearson theory, we would need to consider , where depends on the data, and is random even asymptotically. This difference between the two theories should help to understand why, in the Example, the same finite-sample confidence interval depends on the data m.a.e. for the Neyman-Pearson theory, while it is does not depend on the data m.a.e. for the neoclassical theory.

Remark 14.

In this paper, the generic proxy is introduced for expository purpose, i.e., to allow the use of probability symbolism. From a strict logical point of view, the immunity of the unconditional distribution of to multiple use of the same data is all that is needed for the neoclassical adequacy: by definition the unconditional distribution of is about all the possible values of induced by all the possible samples that could have been observed. In other words, the key difference between the Neyman-Pearson and Bayesian theories on the one hand, and the neoclassical theory on the other hand is that, in the latter, inference exclusively relies on a unconditional distribution m.a.e., while, in the other, inference relies on the realized data, even m.a.e.

The probabilistic statements, on which neoclassical estimators, confidence regions and tests are based, are immune to previous information about the data, and thus to multiple use of the same data m.a.e. To our knowledge, the neoclassical theory is the first general inference theory immune to multiple use of the same data m.a.e.

5. A neoclassical point of view on some calibration and econometric practices.

This section aims at presenting some prominent practices from the point of view of the neoclassical inference theory. The elementary version of the theory outlined in the subsection 4.2 is sufficient for this purpose. By-products of the current section are examples of implementation of the neoclassical theory, novel theoretical justifications for the presented calibration and econometric practices, and a standard-error adjustment to account for approximation errors.

Subsection 5.1 discusses requirements for proxies and approximations of their distribution. Subsection 5.2 presents choices of proxies and of approximations that correspond to different econometric and calibration practices. Subsection 5.3 assesses the most common econometric practice through Monte-Carlo simulations, and presents the standard-error adjustment. Because, in this section, we discuss the choice of approximations, we distinguish between the distribution of the generic proxy , and its chosen approximation, which we denote .

5.1. On generic proxies and approximations of their distribution

An implementation of the neoclassical theory requires two inputs: a generic proxy and an approximation of its distribution. These inputs do not have to satisfy any particular criteria other than being considered a proxy of , and an approximation of , respectively. In particular, the neoclassical theory does not require consistency of any of the two: consistency is about situations where the number of observations can be infinitely increased, while practice is necessarily based on a bounded number of them. Nevertheless, hereafter, except in the subsection 5.2.1 about calibration, we focus on asymptotically normal proxies and consistent approximations, so that we can rely on insights from the asymptotic theory: the proxy typically corresponds to what is called an estimator in the Bayesian or Neyman-Pearson theory. The following Assumption 6 requires asymptotic normality of , which is a property of most estimators considered in the Neyman-Pearson and Bayesian theories (e.g., Chernozhukov and Hong, 2003).

Assumption 6 (Asymptotic normality of ).

The generic proxy of is asymptotically normal, i.e., (by Assumption 4(c)) there exist a random variable , and a sequence of random variables on s.t.

where , and , as .

Assumption 6 means that the generic proxy asymptotically converges to as a Gaussian random variable centered at with a standard deviation that goes to zero at rate . We could weaken Assumption 6 to allow rates of convergence different from , or to allow different distributions for (e.g., Dickey-Fuller distributions), but it would complicate the presentation. The following Assumption 7 requires the approximation of the distribution of the generic proxy to be consistent.

Assumption 7 (Consistency of ).

The approximation of the distribution of the generic proxy is consistent, i.e., as ,

where denotes a metric on the space of probability measures on .

Assumption 7 means that the distribution of the generic proxy and its approximation converge to each other as the number of observations increases. In Appendix F, we verify Assumption 7 for the approximations considered in this paper. In practice, the distribution of the generic proxy, , is typically unknown, so that Assumption 7 cannot be directly verified. Nevertheless, the asymptotic limit of is often known, so that the following lemma provides a usable criterion for checking Assumption 7.

Lemma 2.

Proof.

Triangle inequality yields , where the two terms of the RHS go to zero in probability as by (a) and (b), respectively. ∎

Example.

(continued) Let be the Prokhorov metric on the space of probability measures on . The Prokhorov metric generates the topology of the convergence in law (e.g., Billingsley, 1968/1999, pp. 72–73), which, in turn, corresponds to the point-wise convergence of cumulative distribution functions (c.d.f.) at continuity points of the limiting c.d.f. (Portmanteau theorem). Denote the c.d.f. of the Gaussian distribution with . Then, for all , , because , and , if , and otherwise. Similarly, for all , , and -a.s. (see also Appendix F.2.1, Proposition 6 on p. 6) Thus, by Lemma 2, and are consistent approximations of the distribution of the generic proxy , .

Remark 15.

Unlike for Neyman-Pearson and Bayesian theories, implementations of the elementary version of the neoclassical inference theory presented in this paper seem to always rely on an approximation, the approximation of the distribution of the generic proxy. This is a disadvantage of the elementary version of the neoclassical theory. However, firstly, most of econometric practices rely on approximations: implementation of the Neyman-Pearson and Bayesian theories typically requires asymptotic (e.g. CLT) or computational (e.g., Markov Chain Monte Carlo algorithms) approximations. Secondly, in some particular cases, we can bound the approximation error in probability, or even derive the exact distribution of , and of : see Appendix E on p. E. Thirdly, in practice, there is a trade-off between approximations and the approximative assumptions that are needed to avoid the (explicit) approximations.

5.2. Some practices in neoclassical terms

In this subsection, we frame some calibration and econometric practices in terms of the neoclassical theory, so that they are provided with a theoretical foundation immune to multiple use of the same data m.a.e. For convenience and brevity, we present the practices according to the kind of approximations of they rely on. Thus, practices that combine different approximations (e.g., mix of calibration and econometrics in Canova, 2007, chap. 7) are only indirectly treated. Appendix F studies the asymptotic limit of the approximations considered in this subsection, while Table 5 in Appendix G on p. 5 provides a panoramic view of them.

5.2.1. Model-calibration approximations

By calibration, we mean the more or less formal process through which the parameter values of a model are selected in view of data. In finance and economics, this process often correspond to the minimization of some goodness-of-fit measure, or to the choice of estimates from various existing empirical studies. While model calibration is used in many fields (e.g., Oreskes, Shrader-Frechette and Belitz, 1994), it has become common in economics and finance with the development of general-equilibrium models (Johansen, 1960; Kydland and Prescott, 1982; Shoven and Walley, 1984) and derivatives pricing, respectively. We distinguish two types of calibration: plain calibration and criterion-adjusted calibration.

Plain calibration. In plain calibration, the selected parameter values are just plugged in the model in lieu of the unknown parameter . No information about potential calibration error or model-specification error is reported. Plain calibration is widely used to price derivatives in finance (e.g., Cont, 2010, p. 1217). If the selected parameter values are assumed to be a realization of a random variable , under Assumptions 1 and 4, plain calibration can be regarded as an implementation of the neoclassical theory s.t.

-

•

the generic proxy is a random variable that has the same unconditional distribution as , i.e., where denotes the inverse of the unconditional c.d.f. of , and a random variable uniformly distributed on that is independent from the data;

-

•

the approximation of the unconditional distribution of the proxy is the unit point mass at the selected parameter value , i.e., for all ,

Then, by Definitions 4 and 5, both the neoclassical estimate and confidence region correspond to the calibrated value, i.e., and m.a.e. If the selected parameter value is close to (e.g., the proxy is consistent and the number of observations is large as in Proposition 5(i) in Appendix F.1), plain calibration may be sufficient. However, in economics and finance, this is not often the case, so that indication of the potential calibration error and model-specification error are often needed.

Criterion-adjusted calibration. By criterion-adjusted calibration, we mean a plain calibration accompanied by indications of calibration error and model-specification error based on nonstatistical criteria. The indication of calibration error comes from the determination of a range of plausible values for the model parameter. The indication of model-specification error comes from the computation of measures of discrepancy between the calibrated model and the data (e.g., difference between moments of the calibrated model and moments of the data).

To cast criterion-adjusted calibration as an implementation of the neoclassical theory, it is useful to introduce new notation. We denote the model parameter and the measures of discrepancy with and , respectively. We also denote the selected value for with , and the measure of discrepancy implied by with . The parameter of the model of interest are not to be confused with the global parameter . The determination of the range of plausible values for and acceptable values for can be formalized by a positive criterion function , which indicates the adequacy between its two arguments, and which equal zero outside . The criterion function is maximized when its two arguments are equal, i.e., for all and , . With this notation, and under the assum ption that the following quantities exist, criterion-adjusted calibration can be regarded as an implementation of the neoclassical theory s.t.

-

•

the generic proxy is , where is a conditional c.d.f. s.t. with for , and where is a random variable uniformly distributed on that is independent from the data and ;

-

•

the approximation of the distribution of the generic proxy is the normalized criterion function, i.e., for all ,

5.2.2. Gaussian approximation

The Gaussian approximation is one of the most-widely used approximations. Under the assumption that the unconditional distribution of the -statistic converges asymptotically to a standard Gaussian , econometricians typically deduce univariate confidence regions and sets of nonrejected point hypotheses, , where , and , respectively, denote the -th element of the random vector , the -th diagonal element of the matrix , and the quantile of a standard univariate Gaussian . As in the Example of this paper, such practice can be regarded as an implementation of the neoclassical theory s.t.

-

•

the generic proxy is a random variable that has the same unconditional distribution as , i.e., where denotes the inverse of the unconditional c.d.f. of , and a random variable uniformly distributed on that is independent from the data;

-

•

the approximation of the unconditional distribution of the proxy is the Gaussian distribution centered at with variance-covariance matrix the diagonal matrix of the diagonal elements of , i.e., for all ,

(4) with , and where is the diagonal matrix that has the same diagonal elements as .

In the Appendix F, we show that the approximation (4) is consistent under Assumptions 1, 4 and 6. (see Proposition 6 in Appendix F.2)

5.2.3. Laplace approximation and “Bayesian” practice

In most econometric practices, the unknown parameter is approximated by a maximizer of a converging objective function , i.e.,

| (5) |

where, as , with . See Bierens (1981), Amemiya (1985, chap. 4), Gallant and White (1988), Newey and McFadden (1994), and Pötscher and Prucha (1997), all of which follow from earlier contributions by Wald (1950), Malinvaud (1964/1970, chap. 9; 1970), and Jennrich (1969). If is a log-likelihood , for all and , the function

| (6) |

is numerically equal to the Bayesian distribution of the data conditional on , denoted (see subsection 3.1). Thus, by analogy, often motivated by the Laplace approximation, several papers (e.g., Zellner, 1997; Kim, 2002; Yin, 2009) have used the function

| (7) |

in lieu of , even when the former is not numerically equal to the latter. Then, they consider that the Bayesian posterior distribution equals

| (8) |

where is a function that they regard as the Bayesian prior . As previously noticed (e.g., Chernozhukov and Hong, 2003), such a practice is not in line with Bayesian theory, even if we set aside the invalidation due to multiple use of the same data: approximations are not compatible with Bayesian inference theory, which requires an econometrician to know exactly the distribution of the data conditional on true parameter (Savage, 1954/1972, pp. 59–60). However, such a practice is in line with the neoclassical inference theory whether the function (7) is numerically equal to or not.

Under general assumptions, a strand of literature that goes back at least to Laplace (1774/1878) has shown that (8) is a consistent approximation of the unconditional distribution of . See literature on consistency of Bayesian posteriors (e.g., Doob, 1949), and the Bernstein-von Mises theorem (e.g., Le Cam, 1953, 1958; Chen, 1985; Kim, 1998; Chernozhukov and Hong, 2003), which implies consistency under (see Appendix F.2.3 on p. F.2.3). We distinguish three types of Laplace approximations: plain Laplace approximation, weighted Laplace approximation, and criterion-adjusted weighted Laplace approximation. For brevity, we do not treat the plain Laplace approximation separately from the weighted Laplace approximation, as the former is a particular case of the latter with , for all .

Plain and weighted Laplace approximation. The neoclassical theory justifies practices that treats (8) as a Bayesian posterior, and report the counterpart of a mode and of an HPD region. Such practices can be seen as an implementation of the neoclassical theory s.t.

-

•

the generic proxy is a random variable that has the same unconditional distribution as , i.e., where denotes the inverse of the unconditional c.d.f. of , and a random variable uniformly distributed on that is independent from the data;

-

•

the approximation of the unconditional distribution of the proxy is the expression (8) viewed as a function of , i.e., for all ,

From a neoclassical point of view, weights the evidence from data. Mathematically, it corresponds to a change of measure from the plain Laplace approximation, , to the weighted Laplace approximation, , i.e., for all ,

The weighting function allows to incorporate additional information in the proxy of . While, in Bayesian theory, the dependance of a prior on data is typically problematic, in the neoclassical theory, the weighting function can depend on the data. The neoclassical theory only requires and the integral of (8) to be considered a proxy of , and an approximation of , respectively. Thus, in particular, the neoclassical theory provides a theoretical foundation to the practice called parametric empirical Bayes (Morris, 1983). Petrone, Rousseau, Scricciolo (2014) present conditions under which the weighted Laplace approximation (8) is a consistent approximation of when depends on data through an estimated hyperparameter.

Criterion-adjusted weighted Laplace approximation. When (8) is treated as if it was a Bayesian posterior, the counterpart of a mode and of an HPD region are not always reported. Instead, the econometrician chooses a utility function (i.e., opposite of a loss function), , and then maximizes w.r.t. the expected utility . If is nonnegative (see upcoming Remark 16), such a practice can be seen as an implementation of the neoclassical theory s.t.

-

•

the generic proxy is where , and where is a random variable uniformly distributed on that is independent from the data and ;

-

•

the approximation of the distribution of the generic proxy is the expected criterion function , i.e., for all ,

(9)

In Appendix F, we show that the criterion-adjusted weighted Laplace approximation (• ‣ 5.2.3) is consistent under general assumptions. The Bayesian approach and the neoclassical approach based on the criterion-adjusted weighted Laplace approximation (• ‣ 5.2.3) are fundamentally different, although they are numerically equivalent when is a log-likelihood (and the data have not been previously used). For Bayesian inference theory, an econometrician faces a known probabilized uncertainty of a random parameter , while from a neoclassical perspective an econometrician faces an estimated probabilized uncertainty of a random proxy of a constant parameter . Thus, the neoclassical theory acknowledges the existence of an “unmeasurable” uncertainty described by Knight (1921, chap. 7–8).

Remark 16.

In this paper, we assume nonnegative criterion functions to remain within the framework of the elementary version of the neoclassical theory presented in section 4. This requirement limits the type of neoclassical confidence regions considered in this paper. Nevertheless, under the mild assumption that , this requirement is without loss of generality for neoclassical point estimation: we can define the criterion function which yields the same point estimate.

Remark 17.

As explained in the introduction of this subsection, our presentation does not present hybrid practices, so that we do not explicitly cover the diversity of the econometric practices labelled Bayesian. However, they appear to also be implementations of the elementary version of the neoclassical theory presented in the subsection 4.2. For example, reporting the HPD region of a Bayesian posterior with its mean can be seen as an implementation of the neoclassical theory s.t. the generic proxy is , and the approximation of its distribution is

where , and . Similarly, reporting marginal equal-tailed 68% confidence interval of a Bayesian posterior with its mean can be seen as an implementation of the neoclassical theory s.t. the generic proxy is , and the approximation of its distribution is the product of Gaussian p.d.f. centered at the midpoint of the -th interval with a standard deviation approximately equal to half of the length of the same interval, i.e.,

with , and where denotes the reported intervals, , and is a Gaussian p.d.f. with expectation and standard deviation .

5.3. Assessment of the Gaussian approximation and a standard-error adjustment

From a neoclassical point of view, the issue raised by multiple use of the same data boils down to the question of approximation errors. This subsection studies the average effect of approximations errors, and develops a standard-error adjustment to account for it. For brevity and relevance, we focus on the Gaussian approximation, which corresponds to a large part of econometric practice. Assessments of other approximations are left for future research.

| RMSE | RMSE | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| .045b | .007b | .089 | .311 | .5 | .732 | .811 | .912 | .658 | .878 | .932 | .981 | ||

| .028 | .003 | .07 | .303 | .51 | .746 | .825 | .924 | .671 | .892 | .943 | .987 | ||

| .02 | .001 | .058 | .299 | .515 | .752 | .831 | .929 | .677 | .897 | .948 | .989 | ||

| .09 | .015 | .126 | .311 | .5 | .732 | .811 | .912 | .658 | .878 | .932 | .981 | ||

| .057 | .006 | .099 | .303 | .51 | .746 | .825 | .924 | .671 | .892 | .943 | .987 | ||

| .04 | .003 | .082 | .299 | .515 | .752 | .831 | .929 | .677 | .897 | .948 | .989 | ||

| .056 | .043 | .117 | .37 | .345 | .638 | .677 | .726 | .568 | .725 | .728 | .74 | ||

| .035 | .027 | .083 | .405 | .48 | .74 | .794 | .885 | .632 | .87 | .89 | .937 | ||

| .025 | .019 | .067 | .374 | .501 | .741 | .824 | .918 | .683 | .881 | .929 | .971 | ||

| .113 | .053 | .143 | .375 | .566 | .729 | .838 | .911 | .686 | .88 | .931 | .981 | ||

| .071 | .035 | .111 | .346 | .515 | .728 | .806 | .922 | .631d | .898 | .942 | .987 | ||

| .05 | .025 | .093 | .332 | .474 | .768 | .82 | .922 | .682 | .895 | .943 | .988 | ||

We do no report the bias as we know that and are unbiased (e.g., Gouriéroux and Monfort, 1989/1996, Example 6.4). RMSE, which elucidates why RMSE. c As in the Gaussian case, this Bernoulli parameter is chosen to halves the standard deviation of the other Bernoulli, i.e., . d The non-monotonic convergence to .68 is due to the discontinuities induced by the Bernoulli distribution. See for example Brown, Cai and DasGupta (2002) for a similar phenomenon.

.

The basic algorithm of our Monte-Carlo simulations is the following.

For

-

(1)

Draw i.i.d. data

-

(2)

Compute

-

•

;

-

•

-

•

;

-

•

, where .

-

•

We draw data either from a Gaussian distribution, or from a Bernoulli distribution. Both families of distributions are interesting for different reasons. Data from a Bernoulli distribution are known to be relatively challenging for Gaussian approximations, especially when the Bernoulli parameter is close to 0 or 1 (e.g., Agresti and Coull, 1998; Brown , Cai and DasGupta, 2002 and references therein). Data from a Gaussian distribution neutralizes the part of the approximation error coming from the distribution family: the average of Gaussian random variables is also a Gaussian random variable.

Table 1 shows that, in both cases, Gaussian approximations globally converge in terms of the first two moments, of the norm, and of the norm. However, the probability of neoclassical confidence regions to contain the generic proxy appears downward biased. Proposition 1 formalizes this downward bias, and proposes an asymptotic adjustment for it.

|

|

Proposition 1 (Downward bias and standard-error adjustment).

-

i)

-

ii)

where , and , respectively, denote the -th element of the random vector , the -th diagonal element of the matrix , and the quantile of a standard univariate Gaussian .

Proof.

It is an immediate consequence of the asymptotic normality of . For all , by iterated conditioning,

(a) On one hand, . On the other hand, similarly, . (b) Add and subtract . (c) Under Assumption 6, by the continuous mapping theorem (e.g., Kallenberg, 1997/2002, Lemma 4.3), as , , where is independent from . ∎

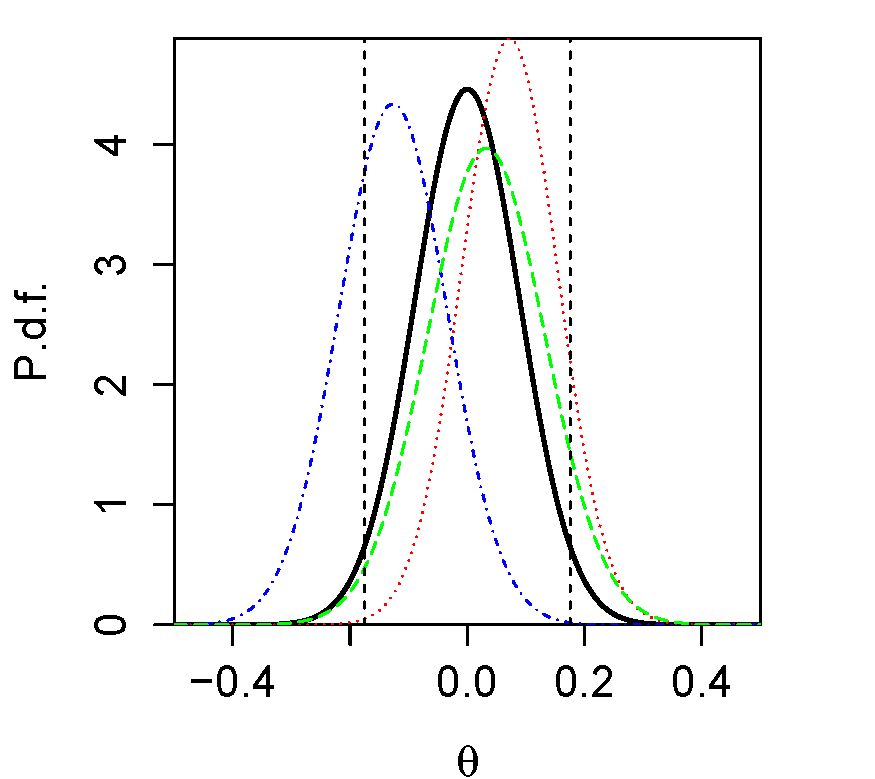

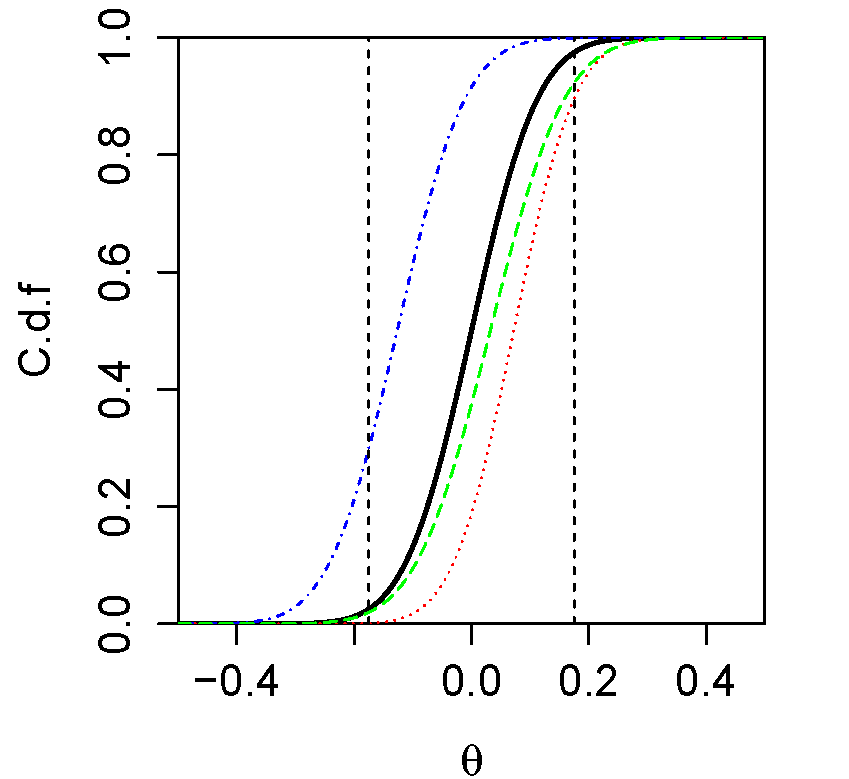

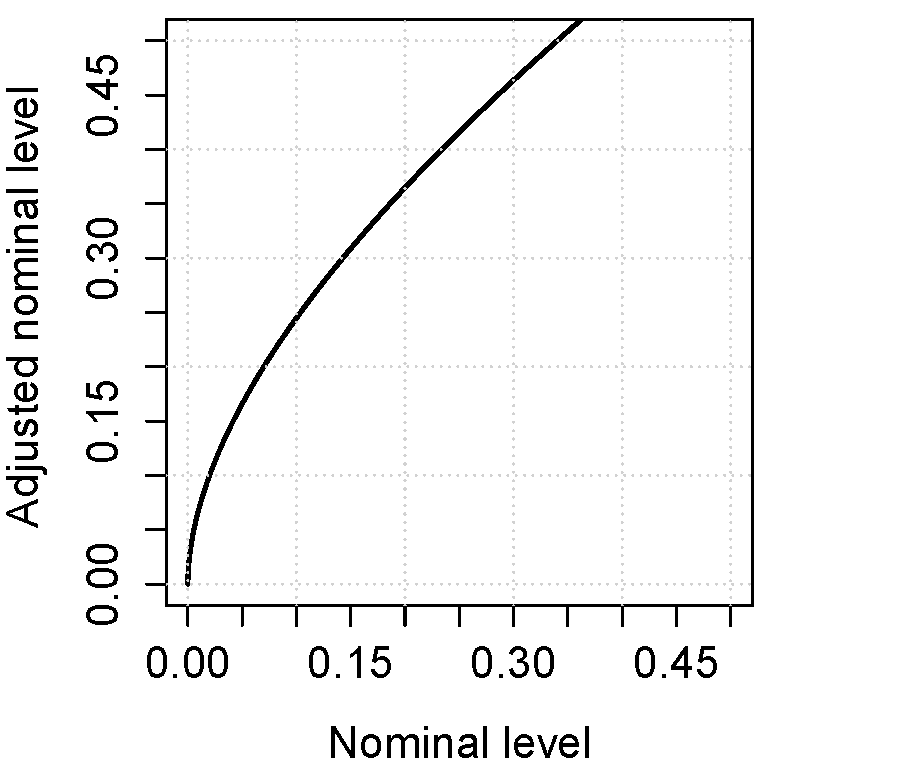

Proposition 1i) shows that the downward bias holds under general assumptions, independently of the sub-sigma algebra of the data we condition on. Figure 1 (p. 1) illustrates the reason of this downward bias : the Gaussian approximation does not account for the fact that its mean and standard deviation are not known, but estimated, so that there is an approximation error. Proposition 1ii) shows that multiplying the standard error by asymptotically accounts for the average approximation error, independently of the sub-sigma algebra of the data we condition on. The RHS columns of Table 1 suggest that this asymptotic adjustment is effective in finite sample. The proof of Proposition 1 formalizes the rationale behind the adjustment: asymptotically, after centering and scaling by , the average approximation error exactly corresponds to the uncertainty about , so that the variance is doubled by independence, which means that the standard error is multiplied by .

As can be seen from Figure 2 (p. 2), the adjustment has a nonlinear effect on confidence region and test levels. The adjustment has a stronger effect in the tails because Gaussian distributions are exponentially decreasing in the tails. Tables 2, 3 and 4 are conversion tables that documents the effect of the adjustment at conventional levels. They should be of special interest to applied econometricians. Table 2 shows that tests at nominal levels .01, .05 and .1 are tests at approximate adjusted nominal levels .069, .166 and .245, respectively. Conversely, Table 3 shows that tests at adjusted nominal level .01, .05, and .1 respectively requires the non-adjusted p-values computed by standard software to be approximately below , , and for rejection of the test hypothesis. Table 4 shows the effect of the adjustment on critical values for the non-adjusted computed by standard software. Tables 2, 3 and 4 shed a new light on results published in nonexperimental fields. In particular, in view of the data collected by Brodeur, Lé, Sangnier and Zylberberg (2013, Figure I), the adjustment appears to affect the significance at conventional levels of many results in the economic literature.

| Nominal Level | .01 | .05 | .1 | .32 |

|---|---|---|---|---|

| Adj. nominal level (appr.) | .069 | .166 | .245 | .482 |

| Adj. and appr. respectively stand for adjusted and approximation. | ||||

| Adj. nominal level | .01 | .05 | .1 | .32 |

|---|---|---|---|---|

| Nominal Level (appr.) | .020 | .16 | ||

| Adj. and appr. respectively stand for adjusted and approximation. | ||||

| Non-adjusted critical values | 2.58 | 1.96 | 1.64 | .99 |

|---|---|---|---|---|

| Adj. critical values (appr.) | 2.33 | 1.41 | ||

| Adj. and appr. respectively stand for adjusted and approximation. | ||||

6. Conclusion

In nonexperimental fields, it is inescapable to compute test statistics and confidence regions that are not probabilistically independent from previously examined data. It has been known for decades that Neyman-Pearson and Bayesian inference theories are inadequate for such a practice. This paper recalls these inadequacies, and formally shows that they also hold m.a.e. A novel inadequacy of the Neyman-Pearson theory for past-realized data is also established. Then, a general inference theory compatible with multiple use of the same data m.a.e. is outlined. We call it the neoclassical inference theory.

The starting point of the neoclassical theory is the acknowledgement that econometric inference relies on the use of a sample counterpart of the unknown parameter as a proxy for the latter one. Then, the idea is to base inference on an approximation of the unconditional distribution of the proxy. By definition, the unconditional distribution of the proxy is about all the possible values of the proxy induced by all the possible samples that could have been observed. Thus, neoclassical inference does not depend on the realized data m.a.e. Therefore, if we set aside approximation errors, the neoclassical theory explains why econometric inference can rely on multiple use of the same data.

The other side of the coin is that, from a neoclassical point of view, the issue raised by multiple use of the same data boils down to the question of the approximation errors, which is the topic of most of the econometric and statistical literature. Nevertheless, Monte-Carlo simulations show that finding accurate approximations is not sufficient. Even when the approximation method is known to be accurate, errors can have a consequential effect on tests and confidence regions. In particular, we prove that the Gaussian approximation yields a downward bias in the probability of neoclassical confidence regions to contain the generic proxy. Thus, we derive a general, but simple asymptotic standard-error adjustment to remove this bias. Monte-Carlo simulations suggest that the adjustment is effective in finite sample. However, more work would be needed to study the impact of approximation errors in other situations. The authors have work in progress in that direction.

Beyond the question of multiple use of the same data, the neoclassical inference theory is promising. The neoclassical inference theory sheds a new light on foundational and methodological debates in statistics, economics and finance (e.g., calibration vs. estimation, and Bayesian inference vs. classical inference). The Example and section 5 show that the neoclassical theory provides a unifying framework for model calibration and several common econometric practices, whether they are labelled Bayesian or à la Neyman-Pearson. Moreover, work in progress by the authors indicates that the version of the neoclassical developed in this paper is generalizable.

References

- AgrestiCoull (1998) Agresti, A., and Coul, A., B.: 1998. Approximate Is Better than ”Exact” for Interval Estimation of Binomial Proportions. The American Statistician, Vol. 52, No. 2, pp. 119–126.

- Amemiya (1985) Amemiya, T.: 1985. Advanced Econometrics. Harvard University Press.

- Berger (1980) Berger, J. O.: 2006 (1980). Statistical Decision Theory and Bayesian Analysis. Springer, Series in Statistics. Second Edition.

- Bhatia (1997) Bhatia, R.: 1997. Matrix Analysis. Springer, Graduate Texts in Mathematics.

- Bierens (1981) Bierens, H. J.: 1981. Robust Methods and Asymptotic Theory in Nonlinear Econometrics. Springer, Lecture Notes in Economics and Mathematical Systems, Vol. 192.

- Billingsley (1968) Billingsley, P.: 1999 (1968). Convergence of Probability Measures. Wiley, Series in Probability and Statistics. Second Edition.

- Borovkov (1984) Borovkov, A. A.: 1998 (1984). Mathematical Statistics. Gordon and Breach Science. Translated from Russian by A. Moullagaliev.

- BrodeurLeSangnierZylberberg (2013) Brodeur, A, Lé, M., Sangnier M., Zylberberg Y.: 2013. Star Wars: The Empirics Strike Back. IZA Discussion Paper No. 7268, March 2013.

- BrownCaiDasGupta (2002) Brown, L., Cai, T., T., and Dasgupta A.: 2002. Confidence intervals for a Binomial proportion and asymptotic expansions. The Annals of Statistics, Vol. 30, No. 1, pp. 160–201.

- Canova (2007) Canova, F.: 2007. Methods for Applied Macroeconomic Research. Princeton University Press.

- Chen (1985) Chen, C.-F.: 1985. On asymptotic normality of limiting density functions with Bayesian implications. Journal of the Royal Statistical Society. Series B (Methodological), Vol. 47, No 3, pp. 540–546.

- Chernozhukov and Hong (2003) Chernozhukov, V. and Hong, H.: 2003. An MCMC approach to classical estimation. Journal of Econometrics. Vol. 115, No. 2, pp. 293–346.

- Cont (2010) Cont, R.: 2010. Model Calibration. In Cont R. (Ed.), Encyclopedia of Quantitative Finance, pp. 1210–1219, Wiley.

- Doob (1949) Doob, J. L.: 1949. Application of the theory of martingales. Actes du Colloque International Le Calcul des Probabilités et ses applications (Lyon, 28 juin - 3 juillet 1948), Paris CNRS, pp. 23–27.

- Ferguson (1967) Ferguson T. S.: 1967. Mathematical Statistics. Academic Press, Pure and Probability and Mathematical Statistics.

- Fisher (1925) Fisher, R. A.: 1973 (1925). Statistical Methods for Research Workers. Hafner. Fourteenth edition. Reprinted in Statistical Methods Experimental Design and Scientific Inference by John Henry Bennett.

- FlorensMouchartRolin (1990) Florens, J-P., Mouchart, M., and Rolin, J-M.: 1990. Elements of Bayesian Statistics. Marcel Dekker. Pure and Applied Mathematics.

- Folland (1984) Folland, G. B.: 1999 (1984). Real Analysis. Modern Techniques and Their Applications, Pure & Applied Mathematics, Wiley-Interscience.

- GallantWhite (1988) Gallant , R. and White, H.: 1988. A Unified Theory of Estimation and Inference for Nonlinear Dynamic Models. Blackwell.

- GibbsSu (2002) Gibbs, A. L. and Su, F. E.: 2003. On choosing and bounding probability metrics. International Statistical Review / Revue Internationale de Statistique,. Vol. 70, No. 3, pp. 419–435.

- GivSho (1984) Givens, C. R. and Shortt, R. M.: 1984. A class of Wasserstein metrics for probability distributions. The Michigan Mathematical Journal,. Vol. 31, No. 2, pp. 231–240.

- GouriérouxMonfort (1989) Gouriéroux, C. and Monfort, A.: 1996 (1989). Statistique et modèles économétriques. Economica. Translated to English by Quang Vuong under the title Statistics and Econometric Models.

- GouriérouxMonfort (1996) Gouriéroux, C. and Monfort, A.: 1996. Simulation-Based Econometric Methods. Oxford University Press. CORE lectures.

- Holcblat (2012) Holcblat, B.: 2012. A Classical Moment-Based Approach with Bayesian Properties. PhD dissertation. Carnegie Mellon University.

- Johansen (1960) Johansen, L.: 1960. A multi-sectoral study of economic growth, Amsterdam: North-Holland.

- Jennrich (1969) Jennrich, R. I.: 1969, Asymptotic properties of non-linear least squares estimators. The Annals of Mathematical Statistics Vol. 40, No. 2, pp. 633–643.

- Kallenberg (2002) Kallenberg, O.: 2002 (1997). Foundations of Modern Probability. Springer. Probability and Its Applications. Second Edition.

- Khmaladze (1981) Khmaladze, E. V.: 1981. Martingale Approach in the Theory of Goodness-of-Fit Tests. Theory of Probability and its Applications, Vol. 26, No. 2, pp. 240–257. Translated from Russian by B. Aries.

- KydlandPrescott (1982) Kydland F. E. and Prescott E. C.: 1982. Time To Build And Aggregate Fluctuations. Econometrica, Vol. 50, No. 6, pp. 1345–1370.

- Kim (2002) Kim, J.-Y.: 2002. Limited information likelihood and Bayesian analysis. Journal of Econometrics, Vol. 107, No. 1-2, pp. 175–193.

- Knight (1921) Knight, F. H.: 1921, Risk, Uncertainty and Profit, Boston, MA: Hart, Schaffner & Marx; Houghton Mifflin Co.

- Laplace (1774) Laplace, P.-S.: 1774. Mémoire sur la probabilité des causes par les événements. Reprinted in Œuvres complètes de Laplace, Vol. 8, 1891, Gauthier-Villars.

- Laplace (1812) Laplace, P.-S.: 1820 (1812). Théorie analytique des probabilités. Third Edition. Reprinted in Œuvres complètes de Laplace, Vol. 7, 1886, Gauthier-Villars.

- LeCam, (1953) Le Cam, L.: 1953. On some asymptotic properties of maximum likelihood estimates and related Bayes estimates. University of California Publications in Statistics, Vol. 1, No. 11, pp. 277–330.

- LeCam, (1958) Le Cam, L.: 1958. Les propriétés asymptotiques des solutions de Bayes. Publications de l’Institut de Statistique de l’Université de Paris, pp. 17–35.

- Leamer (1978) Leamer, E. E.: 1978. Specification searches. Ad Hoc Inference with Nonexperimental Data. John Wiley & Sons. Available on the homepage of the author.

- LehmannRomano (1959) Lehmann, E. L. and Romano, J. P.: 2005 (1959). Testing Statistical Hypotheses. Springer. Texts in Statistics. Third Edition.

- Malinvaud (1970) Malinvaud, E.: 1970 (1964). Statistical Methods of Econometrics. North-Holland. Second Edition revised. Translated from French by MRS. A. Silvey.

- Malinvaud (1970) Malinvaud, E.: 1970, The Consistency of Nonlinear Regressions. The Annals of Mathematical Statistics, Vol. 41, No. 3, pp. 956–969.

- Morris (1983) Morris, C. N.: 1983. Parametric Empirical Bayes Inference: Theory and Applications. Journal of the American Statistical Association. Vol. 78, No. 381, pp. 47–55.

- NeweyMcFadden (1994) Newey, W. K. and McFadden, D. L.: 1994. Large Sample Estimation and Hypothesis Testing. In Engle R. F. and McFadden D. L. (Ed.), Handbook of Econometrics, Vol. 4, pp. 2113–2247, Elsevier Science.

- NeymanPearson (1933) Neyman, J. and Pearson, E. S.: 1933. On the Problem of the Most Efficient Tests of Statistical Hypotheses. Philosophical Transactions of the Royal Society of London. Series A, Containing Papers of a Mathematical or Physical Character. Vol. 231, pp. 289–337.

- Oreskes, Shrader-Frechette and Belitz (1994) Oreskes, N., Shrader-Frechette, K. and Belitz, K.: 1994. Verification, Validation, and Confirmation of Numerical Models in the Earth Sciences. Science. Vol. 263, No. 5147, pp. 641–646.

- Petrone, Rousseau and Scricciolo (2014) Petrone, S., Rousseau, J., and Scricciolo C.: 2014. Bayes and empirical Bayes: do they merge? Biometrika. Vol. 101, No. 2, pp. 285–302.

- PotscherPrucha (1997) Pötscher, B. M. and Prucha, I.: 1997. Dynamic Nonlinear Econometric Models: Asymptotic Theory. Springer.

- Savage (1954) Savage, L. J.: 1972 (1954). The Foundations of Statistics. Dover. Second revised Edition.

- Shevtsova (2011) Shevtsova I.: 2011. On the absolute constants in the Berry Esseen type inequalities for identically distributed summands. arXiv:1111.6554.

- ShovenWalley (1984) Shoven J. B. and Whalley J.: 1984. Applied General-Equilibrium Models of Taxation and International Trade: An Introduction and Survey. Journal of Economic Literature. Vol. 22, No. 3 (Sep., 1984), pp. 1007–1051.

- Skorohod (1976) Skorohod, A. V.: 1976. On a representation of random variables. Teoriya Veroyatnostei i ee Primeneniya, Vol. 21, No. 3, pp. 645–648. Available at: www.mathnet.ru. Translated to English in Theory of Probability and its Applications.

- VaartWellner (1996) van der Vaart, A. W. and Wellner, J. A.: 1996. Weak Convergence and Empirical Processes. Springer. Series in Statistics.

- Wald (1949) Wald, A.: 1949, Note on the consistency of the maximum likelihood estimate. The Annals of Mathematical Statistics, Vol. 20, No. 4, pp. 595–601.

- Yin (2009) Yin G.: 2009. Bayesian generalized method of moments. Bayesian Analysis, Vol. 4, No. 2, pp. 191–207.

- YoungWang (1998) Young, V. R. and Wang S. S.: 1998. Updating non-additive measures with fuzzy information. Fuzzy Sets and Systems, Vol. 94, pp. 355–366.

- Zellner (1997) Zellner, A.: 1997. The Bayesian Method Of Moments (BMOM). In Fomby T. B., Carter Hill R. (Ed.), Applying Maximum Entropy to Econometric Problems. Advances in Econometrics, Vol. 12, pp. 85–105, Emerald Group.

Acknowledgements

Helpful comments were provided by seminar participants at BI (finance and economics), Université Catholique de Louvain (CORE), University of Oslo (statistics), RCEF 2014 (Bayesian econometrics), SIPTA 2014, Tinbergen Institute (ector), CFE-ERCIM 2014, and Institut Henri Poincaré (semstats). Benjamin Holcblat acknowledges support from the Centre for Asset Pricing Research.

Appendix A Consistency adequacy

The following proposition shows that multiple use of the same data does not affect the consistency of a point estimator. In this Appendix A, m.a.e. means that we always consider the asymptotic limit to be exact for any sample size . Nevertheless, for simplicity, we also exclude the case à la Hoffmann-Jørgensen (see Wellner and van der Vaart, 1996) in which finite-sample statistics do not need to be measurable.

Proposition 2 (Consistency adequacy).

Let be an estimator of , i.e., a measurable mapping from to , where denotes a -algebra on . Under Assumption 1,

-

i)

if is strongly consistent, then, for all , and are independent m.a.e., i.e.,

-

ii)

if is weakly consistent, then, for all , and for all neighborhood of , and are independent m.a.e., i.e.,

Proof.

It is definition chasing. By a standard property of probability, for all , . Thus, if , adding on both sides yields

| (10) |

because .

i) By definition of strong consistency, , which means that m.a.e. Then, apply (10) with and .

ii) By definition of weak consistency, for all neighborhood of , , which means that m.a.e. Then, apply (10) with and . ∎

Remark 18.

Inspection of the proof shows that consistency is independent of any event, i.e., we can replace by any event in the proof, and thus in the statement of Proposition 2.

Appendix B Details of the proof of Theorem 1

In this appendix, we provide a detailed proof of Theorem 1, i.e., we provide details regarding the qualification “m.a.e.” We only consider the case à la Hoffmann-Jørgensen, as the standard asymptotic case follows easily from it.

Proof.

i) and are not independent m.a.e. if, and only if,

(a) By assumption, . (b) , where for all , .

ii) Replace in the proof of (i), , , and by , , and , respectively. ∎

Remark 19.

In the above proof, the assumption can be weakened to . However, the non-existence of the limit or the non-measurability of the conditioning event would make the proof more difficult. In particular, in the latter case, we would need a conditional version of nonadditive outer and inner measures, and there does not seem to be a consensus on this subject (e.g., Young and Wang, 1998). These difficulties do not affect the main conclusion of section 2 as they are the counterpart of the difficulties to establish the Neyman-Pearson validity of a confidence region or a test.

Appendix C Neyman-Pearson inadequacy for past-realized data

As pointed out in Remark 4 on p. 4, Theorem 1 can be viewed as a formalization of the Neyman-Pearson inadequacy for past-realized data when only part of the data have been realized before the determination of the confidence regions and tests. This appendix formalizes this inadequacy in the case in which all data at use have been previously realized. For simplicity, we rule out the case à la Hoffmann-Jørgensen in which finite-sample statistics do not need to be measurable. We also require the following assumption for the determination of the confidence intervals.

Assumption 8.

Let be the probability measure on s.t. is the unconditional physical and unknown distribution of . (a)There exists a mapping from the space of all probability measures on to the parameter space s.t. . (b) There exists a family of probability measures on s.t., for all , , and is dominated by , i.e., .