Empirical Relevance of Ambiguity in First Price Auction Models∗

Abstract.

We study the identification and estimation of first-price auction models where bidders have ambiguity about the valuation distribution and their preferences are represented by maxmin expected utility. When entry is exogenous, the distribution and ambiguity structure are nonparametrically identified, separately from risk aversion (CRRA). We propose a flexible Bayesian method based on Bernstein polynomials. Monte Carlo experiments show that our method estimates parameters precisely, and chooses reserve prices with (nearly) optimal revenues, whether there is ambiguity or not. Furthermore, if the model is misspecified – incorrectly assuming no ambiguity among bidders – it may induce estimation bias with a substantial revenue loss.

Keywords: first-price auction, identification, ambiguity aversion, maxmin expected utility, Bayesian estimation

JEL classification: C11, C44, D44

University of Chicago. e-mail: aryalg@uchicago.edu

Vanderbilt University. e-mail: dong-hyuk.kim@vanderbilt.edu

1. Introduction

We study the identification and estimation of first-price auction models with independent private values where symmetric risk averse bidders do not know the valuation distribution, i.e., the distribution is ambiguous. In particular, we depart from the current literature on empirical auctions by relaxing the assumption that there is a unique valuation distribution that is commonly known among the bidders. Instead, we consider an environment where the bidders regard many distributions as equally reasonable. The main contribution of the paper is three-fold. First, we introduce the maximin expected utility model with multiple distributions, (Gilboa and Schmeidler, 1989), to capture the presence of ambiguity in empirical auctions.111 An ambiguity averse decision maker prefers a lottery with a known distribution to the one with an unknown distribution. Second, we provide sufficient conditions to nonparametrically identify the valuation distribution and the bidders’ attitude toward ambiguity separately from their risk (CRRA) preference. Third, we develop a Bayesian method that employs Bernstein polynomials to estimate the model parameters and propose policy recommendations.

Almost all papers in empirical auction use the expected utility (EU) framework. See Donald and Paarsch (1993); Guerre, Perrigne, and Vuong (2000); Athey and Haile (2007); Hendricks and Porter (2007); Guerre, Perrigne, and Vuong (2009) among others. Under this framework, bidders know the valuation distribution, while the econometrician does not. Recently, research in decision theory and experimental economics, Gilboa (2009); Camerer and Karjalainen (1994); Fox and Tversky (1995); Halevy (2007) have convincingly illustrated that in many situations economic agents might not be “probabilistically sophisticated” and unable to pin-point the exact distribution. In such environments, it is conceivable that both the bidders and econometrician are uncertain about the distribution.222 Hansen (2014) refers to them as economic models with outside uncertainty and inside uncertainty, respectively and articulates the need and benefits of allowing both such uncertainties. How can such uncertainties be introduced in empirical auction? Are such models identified? Can we use bids data to determine whether bidders are uncertain about the true distribution? We provide answers to these questions.

To model bidders’ uncertainty about the distribution we consider an environment with multiple distributions: where bidders have a set of infinitely many, equally reasonable, distributions. This leads to decisions under ambiguity. Ambiguity in probability judgements has been studied since Keynes (1921); Knight (1921), culminating to a position of eminence with Ellsberg (1961). More recently decision under ambiguity has become an influential subfield of economics; see Gilboa and Schmeidler (1989); Epstein (1999); Hansen and Sargent (2001) and Gilboa (2009) for a comprehensive treatment. It is crucial for the seller to determine the presence of ambiguity from auction data and draw an optimal policy under ambiguity for the following reasons: First, ambiguity nests EU as a special case and hence leads to more robust analysis of the data. Second, if bidders are ambiguity averse the revenue equivalence fails, Lo (1998). Third, first price auction is suboptimal and the optimal reserve price should decrease with ambiguity, Bose, Ozdenoren, and Pape (2006); Bose and Renou (2014); Bodoh-Creed (2012). Thus this paper contributes to the empirical auction literature by providing a tractable framework to introduce and estimate a model with ambiguity aversion.

We follow (Bose, Ozdenoren, and Pape, 2006) and assume that bidders have the maxmin expected utility (henceforth, MEU) which also provides a natural generalization of EU. Gilboa and Schmeidler (1989) laid a formal foundation for MEU and showed that under some axioms there is a set of equally reasonable distributions and each bidder maximizes the expected utility, where the expectation is taken with respect to the most pessimistic distribution in . The theory, however, is silent about , so it has to be specified by the econometrician. A strong parametrization of , however, may cause a misspecification bias or can even nullify any effect of ambiguity; see Example 1. So we only assume that is a convex subset of all absolutely continuous distributions over a compact support, each with nowhere vanishing density. This specification is sufficiently flexible enough to minimize misspecification bias and at the same time allows us to consider the kind of ambiguity that has meaningful empirical content. The set is assumed to include the true distribution. In each auction bidders independently and privately draw their valuations (IPV) from this common, but unknown, (true) distribution. Thus we consider static first price auctions with symmetric players. Since ambiguity in empirical auction is a new topic, focusing on static auction will allow for meaningful analysis of ambiguity as it keeps the model tractable by allowing us to abstract away from modeling forward looking and learning behavior with multiple distributions in a dynamic game; see Gilboa and Schmeidler (1993); Epstein and Schneider (2003); Siniscalchi (2011).

A maxmin bidder uses the most pessimistic distribution to determine her bid. To model this pessimism we innovate a mapping, and call it the D-function, that assigns each quantile of the true distribution to a quantile of the most pessimistic distribution so that whenever there is ambiguity the D-function is (strictly) below the identity in the interior of the unit interval. The model primitives to identify are then the valuation distribution, the D-function, and the utility function. We assume that bid data are generated from the symmetric Bayesian Nash equilibrium (BNE) of the game with incomplete information in which every bidder computes her winning probability using the most pessimistic distribution. The BNE is characterized by a unique, strictly increasing, bidding strategy (Maskin and Riley, 1984; Athey, 2001), which is useful for identification. (Guerre, Perrigne, and Vuong, 2009) showed that the model even without ambiguity is unidentified, and they identified the model additionally assuming that bidders’ participation is exogenous. Even under this restriction, however, we find that the MEU model is observationally equivalent to the EU model. So, we need more structure to identify the model primitives from bid data. To that end, we assume that the utility exhibits constant relative risk aversion (CRRA). Under these assumptions, we establish the identification of the model primitives. Specifically, the slope of the bidding strategy at the lowest value depends on the utility function only, which isolates the CRRA coefficient. Then, the difference in bid quantiles across auctions with different numbers of bidders identifies the D-function. Finally, the strict monotonicity of the bidding strategy, which is a functional of the D-function and the utility function, uncovers the valuation distribution from the bid distributions. We acknowledge that (Grundl and Zhu, 2013) simultaneously and independently obtained similar identification results, but our paper differs substantially in terms of estimation and analysis.

We propose a Bayesian method to estimate the model primitives and choose a revenue maximizing reserve price. We directly specify the valuation density and the D-function using a mixture of Bernstein polynomials. Bernstein polynomials form a dense subset in the space of functions with a bounded support. The direct approach provides a natural environment for the Bayesian decision rule to choose a reserve price, (Aryal and Kim, 2013; Kim, 2013), and it allows us to impose shape restrictions implied by the theoretical model, such as monotonicity of the bidding function and D-function below the identity function, with ease. As a result our empirical method is always in sync with the theoretical model, which not only improves efficiency but also leads to valid policy recommendations; see (Kim, 2014). Another advantage of the Bayesian method arises when we assume ambiguity, and restrict the D-function to be below the identity function, but bidders know the true distribution, so the D-function is an identity function. This might then lead to a bias because the true D-function is the boundary of the space of all D-functions while we restrict it below the boundary. We can reduce this bias by putting a positive prior mass on the boundary. This prior mass then enables the data (likelihood) to increase the probability on the true D on the boundary, and as a result, improves the accuracy of posterior prediction. Such a bias reduction procedure would be difficult, if not impossible, in a frequentist framework. Moreover, the support of the bid data depends on the model primitives, in which case, unlike the MLE, the Bayesian method continues to be efficient; see (Hirano and Porter, 2003).

We document the performance of our method in a Monte Carlo study. We consider three different environments, each with a number of alternative data configurations by varying sample sizes and the numbers of bidders. In the first (second) environment, bid data are generated from the model with (without) ambiguity. In both cases, our method precisely estimates the model primitives and chooses reserve prices that produce nearly the largest revenues for all the configurations under consideration. It is noticeable that even when there is no ambiguity our method performs well. This is not only because MEU nests EU but also because in our method we can put a prior mass on the boundary of the space of D-functions. Lastly to understand the effect of ignoring ambiguity we consider an environment where bid data are generated from the model with ambiguity but the econometrician ignores ambiguity. We find that then the estimates are inaccurate – the mean integrated squared errors of the estimated valuation densities are roughly four to twenty times larger than the case of the first environment. This misspecification leads to about three percent lower revenues than the first environment above. To summarize: our method performs well whether there is ambiguity or not, but if we incorrectly ignore ambiguity, the estimates can be severely biased and policy recommendations may be unreliable.

2. Model And Identification

An indivisible object is to be allocated to one of bidders in a first-price auction without a positive reserve price. Each bidder observes only her own value and bids . The highest bidder wins the object and gets utility while the rest get . A bidder with value solves:

| (1) |

The values are all independent and identically distributed (i.i.d) from , defined over , where, is a vector of auction covariates that is observed by both the bidders and the econometrician. For notational ease, we shall suppress the dependence on . Bidders, however, do not know , and they cannot compute the “winning probability,” which is essential to solve (1) under the EU framework. To model the bidders’ bidding behavior, therefore, we follow the literature on decision under ambiguity and assume:

Assumption 1.

Bidders are ambiguity averse and their preferences have maxmin expected utility representation.

If denotes the set of all possible states of nature, the utility function, and the set of all feasible actions, Gilboa and Schmeidler (1989) provides necessary and sufficient behavioral conditions such that there is a unique convex set of equally reasonable distributions over such that a decision maker prefers an action to with whenever

where is the expectation with respect to the probability measure and . Furthermore, for empirical implementation, it is desirable that the set contains countably additive distributions. To that end, we follow Chateauneuf, Maccheroni, Marinacci, and Tallon (2005) and assume that the preference ordering is monotone continuous.

We begin by proposing a way to adapt the set of distributions to represent the strategic effects of ambiguity. Let be a set of all distribution functions defined over for a given , such that . In addition, we make the following assumption:

Assumption 2.

It is common knowledge among the bidders that:

-

(1)

There are bidders with an identical utility function with , , and .

-

(2)

Their values are independently and identically distributed.

-

(3)

The true valuation distribution is unknown to the bidders, but any information about other than realized values is shared among the bidders.

The first two parts of the assumptions are self explanatory. The last part implies that bidders have access to a common training data that is used to form their beliefs. For instance, in the timber auction every bidder “cruises” the same tract before bidding.

Following the tradition of Harsanyi (1967), we interpret the auction as a game of incomplete information among the bidders with an identical information structure. From assumptions 1 and 2, this implies that every bidder uses the most pessimistic distribution in the set of equally reasonable distributions to determine her expected utility and chooses a bid accordingly. Since Gilboa and Schmeidler (1989) is silent about what the set should be, in practice an econometrician has to choose the set. The choice will affect the estimation and inference. To illustrate the importance of choosing we consider a widely used model (in statistics and economics), called the -contamination model,333 See Huber (1973); Berger (1985); Berger and Berliner (1986); Nishimura and Ozaki (2004); Cerreia-Vioglio, Maccheroni, Marinacci, and Montrucchio (2013) for usage of -contamination model. where is the set of all distributions that can be written as a and combination of the true distribution and some other distribution , and show that such a parametrization neutralizes any strategic effects arising due to ambiguity.

Example 1.

( contamination) Let be commonly known to bidders. Under the -contaminated model, the set of distributions is defined as

which is unknown to the econometrician. Even though the bidders know they do not know . Let be a strictly increasing bidding function. Under Assumptions 1 and 2, then, the objective function (1) can be written as

where with an indicator for the event . We reserve the notation to denote the most pessimistic distribution. The solution to the MEU model with also solves the EU model, since

Intuitively, this transpires because the ambiguity, as measured by , scales the true distribution for all the bidders by a factor of , and hence does not affect the relative probability of winning. In this model, the first order condition (FOC) is

| (2) |

suggesting that even if there is ambiguity about , as long as her inverse hazard rate is unaffected, such ambiguity is strategically irrelevant. This conclusion holds for any other parametrization of the set, not just for the -contaminated model.

Therefore we ought be careful as to how we specify the set . Instead of parametrizing , we only assume that is a weakly compact and convex neighborhood around , which is sufficient to guarantee that a unique absolutely continuous least-favorable distribution (and density) exists.

Assumption 3.

For all , it is common knowledge among bidders that the set forms a weakly compact and convex neighborhood of strictly increasing and continuously differentiable distributions around , such that for all and has a density , a.e.

Under Assumptions 1 – 3, each bidder chooses a bid to maximize her expected utility with respect to in such that for all and for all . Assumption 3 guarantees that and it is unique. The assumption implies that all distributions in are mutually absolutely continuous with the common support, . (Hence, the -contamination in Example 1 is excluded.) Moreover, since only the lower envelop is common knowledge, not the entire set , we implicitly allow bidders to have asymmetric beliefs, i.e., for each , as long as each set, , has the identical lower envelop, .

We focus only on a symmetric pure strategy Bayesian Nash equilibrium. In particular, every bidder conjectures that her opponents use a strictly increasing (pure) bidding strategy, and announces a bid that is a best response to that conjecture and at the equilibrium the conjecture turns out to be true. Once we recognize plays the same role under MEU as under EU, the existence of a unique, symmetric Bayesian Nash equilibrium characterized by a strictly increasing follows from Maskin and Riley (1984); Athey (2001). This bidding strategy maps the latent value to the observed bid. Guerre, Perrigne, and Vuong (2000) showed that when bidders are risk neutral, this map can be inverted to link each bid to a unique value, thereby identifying . Guerre, Perrigne, and Vuong (2009); Campo, Guerre, Perrigne, and Vuong (2011) extended this result to allow for risk averse bidders. Now, we extend these results to the MEU representation.

Let solve the part of the bidder’s objective, such that . Equivalently, for all

| (3) |

and hence it maps the true probability to the most pessimistic one . So, and . Whenever there is ambiguity, would be less than for all so that the distance of from the line measures the extent of ambiguity. When all bidders follow , a bidder with value solves:

The first-order condition with respect to , when evaluated at gives

Rearranging the terms gives a differential equation that characterizes the optimal bidding strategy as:

| (4) |

Lemma 1.

Let for . For all the equilibrium bidding strategy for risk averse bidders satisfies the differential equation (4), and .

The first part of the lemma means bidder with lowest value will bid her true value, Maskin and Riley (1984), while the second part of the lemma shows that the slope of bidding strategy at the lower boundary is independent of the distribution, Guerre, Perrigne, and Vuong (2009).

Let for , or alternatively

Substituting and in the FOC (4) gives

| (5) |

Before addressing the problem of identification, we define the observables. Let be the distribution of equilibrium bid for , i.e., and its density is

Let and be the -th quantile of the value and the equilibrium bid. Since , for every quantile , (5) becomes

| (6) |

Under the i.i.d. assumption, is nonparametrically identified from the bid data, but the model primitives are not in general identified without additional assumptions, including the ones on the set

Proposition 1.

Proof.

Let and be the model. Then the equilibrium bidding strategy is given by

Consider another model with risk neutral bidders, and some a new CDF (to be determined shortly below). Then the equilibrium bidding strategy is given by

The two models are observationally equivalent if

∎

In view of this result, we consider auctions with exogenous participation.

Assumption 4.

Exogenous Participation: and .444 So the set is the same for all and because will also be the same, so will be .

Assumption 4 has been used in the literature by Athey and Haile (2002); Bajari and Hortaçsu (2005); Guerre, Perrigne, and Vuong (2009); Aradillas-Lopez, Gandhi, and Quint (2013) among others. It is equivalent to assuming that there is some potential bidders with values out of which a random subset of bidders participate in a given auction. This identifying assumption is appropriate for the experiment data where the number of bidders are exogenously chosen by the experimenter. When the utility function is unspecified, however, this exclusion restriction is still insufficient for identification.

Proposition 2.

Proof.

We begin by stating (without a proof) the rationalizability lemma from Guerre, Perrigne, and Vuong (2009), adapted to our setting.

Lemma 2.

Let be the joint distribution of , conditional on for There is an IPV auction model with maxmin expected utility, i.e., , that rationalizes both and if and only if the following conditions hold:

-

(1)

, where is the bid distribution form auction with bidders.

-

(2)

and such that , is continuously differentiable and such that on where is such that:

-

(a)

-

(b)

For each quantile ,

-

(a)

Then, we can identify by following Guerre, Perrigne, and Vuong (2009).555 is invertible because . Let and , with be two model structures, and be the distribution of defined as follows: for every quantile compute and determine and

Since the two model structures satisfy condition 2-b of Lemma 2, they both rationalize the same data and hence, are observationally equivalent. ∎

This result is important because it shows that MEU and EU are observationally equivalent even under exogenous variation of the number of bidders. This equivalence is not because we use MEU. For instance, consider the multiplier preference of Hansen and Sargent (2001) as an alternative to MEU. There, it can be shown that this model with ambiguity is equivalent to a model where bidders are more risk averse but do not have any ambiguity.666 The proof of this equivalence uses results from Strzalecki (2011) and Dupuis and Ellis (1997), and is available upon request. Moreover, without ambiguity the model structure is just-identified by the knowledge of and with , and with ambiguity we have to identify an extra parameter, the ambiguity-function . In view of this result, we restrict ourselves to CRRA family, which is also the most widely used in the empirical literature.

Assumption 5.

The utility function is CRRA, i.e., .

Thus we impose a parametric functional form for risk aversion and treat ambiguity aversion nonparametrically. Whether or not this way of prioritizing the estimation task is the right way depends on the effect of risk aversion that cannot be captured by CRRA utility. For that we would need to estimate a model of nonparametric utility and nonparametric ambiguity, but the only paper that estimates risk aversion nonparametrically is Lu and Perrigne (2008) and find that CRRA utility partly captures the nonparametric utility. This provides some justification for our priority of ambiguity over risk aversion.777 This also suggests that, like in Lu and Perrigne (2008); Athey, Levin, and Seira (2011), if we have exogenous variation in auction formats and there is exclusion restriction we might be able to identify both the utility and ambiguity nonparametrically. We do not pursue this line of enquiry because such data are very rare. For estimating nonparametric utility is see Kim (2015).

Then under assumption 5, when . As propositions 1 and 2 argue, the model is not identified without the exclusion restriction, Assumption 4. This is true even with the parametrized utility functions. We now formally establish the identification of the model primitives with the exclusion restriction, under CRRA.

Proof.

We identify the risk aversion parameter and then identify the valuation distribution. Using for and we get

where the second equality followed from assumption 4, i.e. . Evaluating the above equation at the lower boundary , and using (assumption 5) in Lemma 1, i.e. gives

and thus identifying as

| (7) |

Then using in (6), we get

For each quantile , let such that , and . Then, since , for each , we have

| (8) |

where . Equating the quantiles for under two auctions, we identify

Once is identified, can be identified from equation (8). ∎

The bid distributions are directly identified by the observed bid data and the CRRA parameter is identified by the lowest bidder’s bidding behavior. After controlling for the effect of risk aversion, any deviation from the EU model explains bidders’ attitude toward ambiguity, identifying , from which the identification of follows. An immediate corollary is the identification with risk neutral bidders, which is the case of .

3. Estimation Methodology

In this section, we propose a flexible Bayesian method to estimate the model primitives – the valuation distribution, the -function, and the risk aversion coefficient – and propose policy recommendations. We first specify the model primitives and explain our econometric procedure by applying it to simulated data.

3.1. Specification of Model Primitives

We specify the model primitives directly to obtain the posterior distribution by evaluating the likelihood at each proposed parameters. Thus the estimation method is similar to Kim (2014) and different from the indirect approach of Guerre, Perrigne, and Vuong (2000).

First, we model the valuation density with the support normalized to be , using a Bernstein polynomial density (henceforth, BPD)

| (9) |

where , is the Beta density with parameters and , and , a dimensional unit simplex.

|

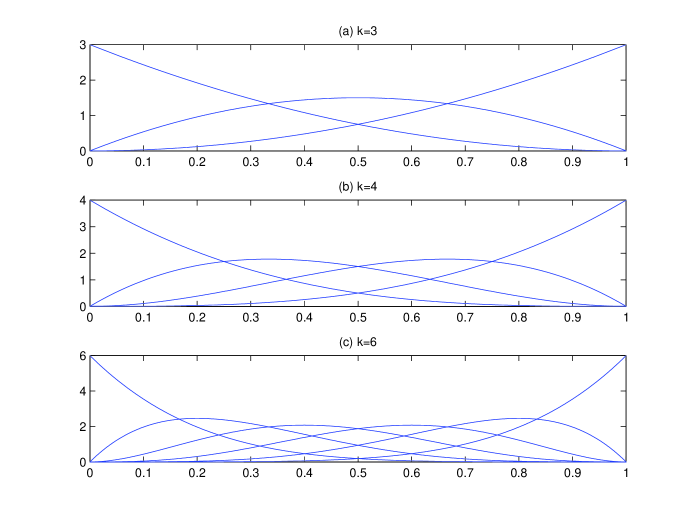

Panels (a)–(c) show the basis functions for the Bernstein Polynomial Densities with 3,4 and 6 components, respectively.

As seen in Figure 2, are general and flexible. Since BPD is a mixture of the -many Beta densities, as increases the set of BPD in Equation (9) forms a dense subset in the space of continuous densities with support. Therefore our specification is flexible enough to represent almost any density for suitably large . Petrone (1999a, b) relied on this property of BPD to develop a nonparametric Bayesian estimation method.

Next, we specify the -function. Observe that, in Figure 2, only in the sequence is strictly positive at 0 and only is strictly positive at 1. So, if the coefficients for and are zero, then the BPD in (9) is zero at 0 and 1. Using this property, we specify the -function as:

| (10) |

where and is the indicator function. The second term in (10), after the negative sign, is equal to zero at 0 and 1, and it is bounded as it is proportional to the BPD. Therefore, in (10) passes through and and always bounded from above by the line. When is equal to the line, there is no distortion and hence, no ambiguity. This specification is useful to determine ambiguity because the presence of ambiguity is completely represented by one parameter . We would conclude that the bidders are ambiguity averse (respectively, neutral) if the posterior probability of the event is less (respectively, greater) than the posterior probability of .888 Note: every model under consideration must have a positive prior mass. With the specification (10), it is easy to put a positive prior mass on the model of no ambiguity because .

When there is no ambiguity, the estimate of the function will be downwardly biased, irrespective of the estimation method, because we have to impose constraint. This is a well known problem, Andrews (1999), that arises when the parameter is on the boundary of the parameter space. Under the Bayesian method, we can reduce the bias by putting a positive prior mass on , because then the posterior probability of no ambiguity will exceed the prior probability, if indeed there is no ambiguity. For implementation of this idea see subsections 3.3 – 3.4 and section 4.

Finally, let be the CRRA coefficient, and let be the vector of model parameters where denotes the parameter space.

3.2. Empirical Environment and the Likelihood

We observe a sample of bid data from auctions with bidders in each auction. Let represent the entire sample, i.e., such that total sample size is . We assume that for every and every

and the bids are equilibrium outcomes so that . Following Assumption 4 we note that does not depend on . Since the values are independent across auctions and bidders, the bids are also independent across all auctions and bidders in the sample.

Let be the equilibrium bidding strategy and its derivative, where is a parameter, and let be the highest bid. The joint density of the data can be written as

| (11) |

Since there is no closed form expression for the likelihood (11), the inverse bidding function and its derivative have to be numerically approximated at every observed bid in , which can be time consuming especially when is large. To circumvent this we follow Kim (2014) and discretize the bid space and use the associated multinomial likelihood.999 Kim (2014) developed a Bayesian method with a simulated likliehood, which does not have simulation errors.

To develop the multinomial likelihood we need to introduce some new notations. Let include all bids for a given , and let denote the sequence of bins such that . Let be the inverse bid for all knot points in . The bin probability is then given by

Since is strictly increasing, we can determine using the piecewise cubic Hermite interpolating polynomial method and evaluate at the knot points with ease because is a mixture of the Beta densities.

In addition, let be the number of bids in for . The associated sample histogram for each is then , which can be viewed as a nonparametric estimate of the bid density, up to a normalization. The joint probability mass of is then given as

| (12) |

We use the likelihood to draw random parameters from the posterior

with a prior density function over , using a Markov Chain Monte Carlo (MCMC) method such as the Gaussian Metropolis-Hastings algorithm.

3.3. Illustration

In this subsection, we explain the implementation of the method using a simulated bid sample. We first outline the data generating process (DGP), describe the prior distribution, and we provide a detailed steps to compute the posterior and use the posterior for inference and decision making.

3.3.1. Simulated Data

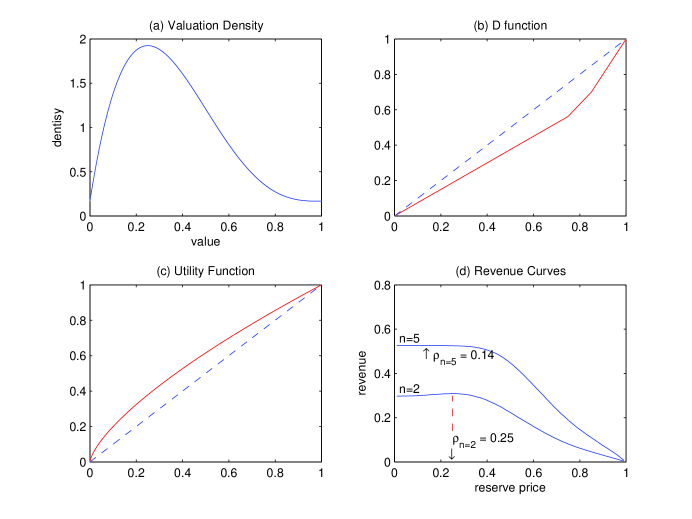

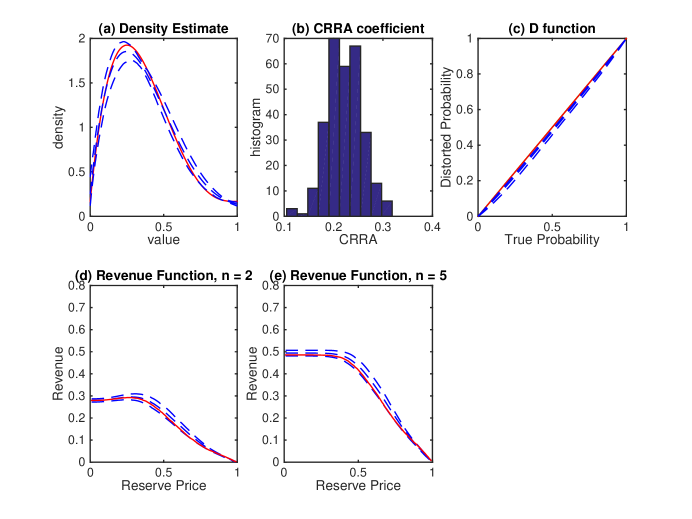

The valuation density in this subsection is a mixture of the uniform density on and Beta densities with parameters (2,4) with mixing weights of and , respectively. The density is not nested in the BPD in (9). We use the superscript to denote the true parameter. The DGP we use is presented in Figure 4: Panel (a) shows , panel (b) shows the -function (solid line), and panel (c) shows the CRRA utility function with (solid). The dashed lines in panels (b) and (c) are the -lines that represent ambiguity and risk neutrality, respectively. The triplet collects the model primitives.

|

Panal (a) shows the valuation density, panel (b) plots the function in solid line and the -line in dashed line. Panel (c) shows the CRRA utility function () with the -line. Finally, panel (d) demonstrates the seller’s expected revenues as a function of reserve price for bidder auctions.

Panel (d) represents the seller’s expected revenue, , as a function of reserve price, .

We consider auctions with . Let denote the revenue maximizing reserve price (henceforth, RMRP). The RMRPs are and and the corresponding (maximized) revenues are and , respectively. The RMRP depends on unless bidders are both risk and ambiguity neutral. Choosing the right RMRP is more important than using zero reserve price when than when , because is more than while, because of competition, .

|

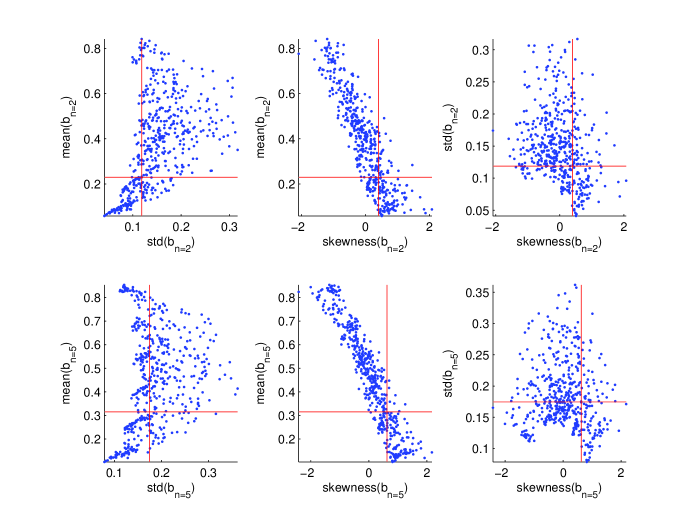

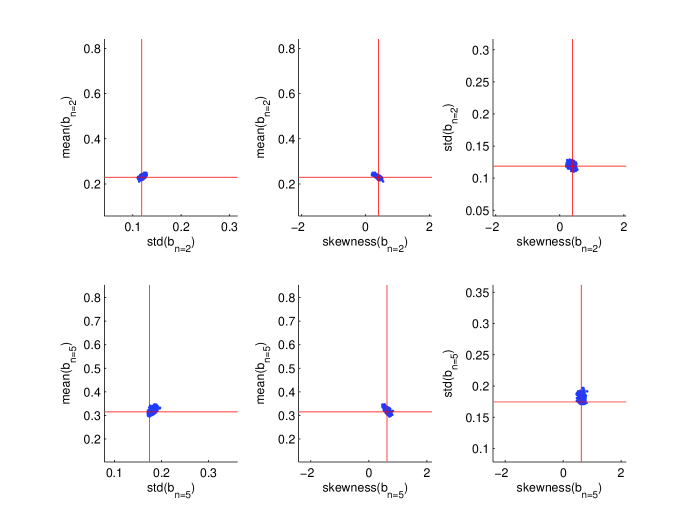

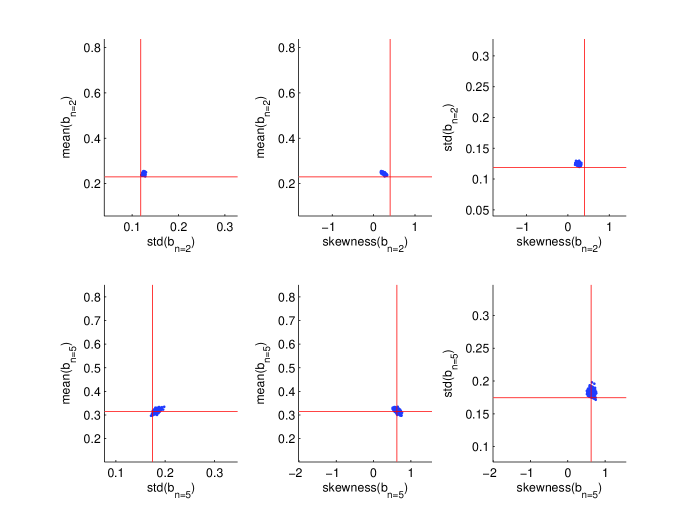

Each panel demonstrate the distribution of the summary statistics by dots of the bid data under the prior, and the summary statistics (sample mean, standard deviation, and skewness) of the original data in solid lines. When the statistics are and , respectively.

From this DGP we draw 300 bids for each auction with bidders, so , with 600 total bids. Let denote this simulated data.101010 We index the data by 1 because it is the first dataset in the Monte Carlo experiment, and we will have more later. In Figure 6 we present the summary statistics (sample mean, standard deviation, and skewness) of the sample by the solid lines.

3.3.2. Prior Specification

The econometrician should choose a prior distribution to reflect his beliefs and uncertainty about . In this section, however, since we know the DGP, our prior beliefs would be a degenerate distribution that approximates the DGP. Using such a strong prior would prevent us from effectively examining the performance of our method, so we choose a prior distribution that is fairly diffuse and relatively easy to specify and evaluate. We assume that , , and are jointly independent under the prior:

| (13) |

We adopt the prior independence only for convenience, but the posterior would coherently update the inter-dependency as suggested by the data . Now, we can specify each component on the RHS of (13). First, we use the uniform prior on for by which we will rule out unreasonably strong risk aversion and avoid numerical errors that arise when is too close to 1. Second, we use the Dirichlet process prior for , i.e.,

where and . This form of prior has been widely used in nonparametric Bayesian analysis with being a random parameter with full support over . Here, represents the prior belief on the probability that when , the BPD in (9), and represents the strength of this belief. For more formal treatment see Ferguson (1973); Escobar and West (1995); Petrone (1999a, b). We set for all , which is a weak belief on the uniform distribution. Third, we construct the prior for as:

where and set for all . The first two indicators impose the sign and shape restrictions on the - function that it be positive and strictly increasing so that is always a valid CDF. The last indicator allows the smallest value for to be , which is related to the prior beliefs for ambiguity neutrality. But, the upper bound is sufficiently large so that it does not impose any restriction on the shape of -function. Finally, we set .111111 We could use different smoothing parameters for the valuation density and the -function, but we use the same for both only for computational convenience. In addition, we could formally choose using the Bayesian model selection or allow to be random (Bayesian nonparametric analysis), but we choose because it seems sufficiently flexible for all exercises in this paper and yet its computation cost is reasonable in the Monte Carlo experiments where we implement the method many times. Aryal and Kim (2013); Kim (2013, 2014) chose formally and Petrone (1999a, b) treated as a random parameter.

Before computing the posterior it is useful to check the information content in the prior and the model about the data by a prior predictive analysis (Geweke, 2005). We draw from the prior and use it to generate a bid sample of size equal as , and calculate the same summary statistics (sample mean, standard deviation and skewness) as before. We repeat this exercise five hundred times and in Figure 6 present the scatter plots of these statistics to visualize the implications of the prior. The fact that the points are scattered around the statistics of suggests that the chosen prior is diffuse and the data can be rationalized by the prior (the intersection of the red lines are contained in the support of the prior). We find that the prior probability of ambiguity neutrality is about 26%.

3.3.3. Posterior Computation

In order to explore the posterior distribution, we employ the Adaptive Metropolis (henceforth, AM) algorithm of Haario, Saksman, and Tamminen (2001), which is a (slight) variation of the Gaussian Metropolis-Hastings (henceforth, GMH) algorithm.

Let be the draw from the algorithm and be a covariance matrix of appropriate dimension that confirms with . Under the GMH algorithm, we draw a candidate from and define with probability

| (14) |

and with the remaining probability. Since has a full support on the Euclidean space, from Theorem 4.5.5 in Geweke (2005) we know that irrespective of the initial point for any measurable function , as ,

For example, can be the valuation density (9) or the -function. In practice, the performance of the GMH algorithm, however, depends on the choice of the scale parameter . If is too small, will be very close to and the GMH algorithm would not effectively explore the parameter space , and if is too large, the proposal function often generates candidates that is unlikely under the posterior and would most likely be rejected. If is a low dimensional vector, it is possible to choose an appropriate , but not so if it is a high dimensional vector.

To address this problem we employ the AM algorithm, which automatically tunes using the history of at each step. Specifically, Haario, Saksman, and Tamminen (2001) suggested using

| (17) |

where is a constant that depends on , the dimension of , is an initial covariance matrix, is a small positive constant, and is the identity matrix. The AM algorithm, which uses instead of , converges to the posterior if the posterior is bounded from above and has a bounded support. Both conditions are satisfied in our case because the prior has bounded support and the multinomial likelihood is bounded from above.

Like Haario, Saksman, and Tamminen (2001), we use , and .121212 Small ensures that the algorithm accepts some candidates at early steps and, therefore, the early history of before updating is not degenerate. Then, we draw the parameters from the posterior distribution using the AM algorithm, and to reduce autocorrelation across draws we record only every outcomes. To check the convergence of the parameter draws, we use the separated partial means test in Geweke (2005), section 4.7. The idea of the test is as follows: Suppose we have a sample drawn from a fixed distribution and divide the sample into four equal blocks. Then the null hypothesis must be true that the mean of second block is equal to the mean of the fourth block . We test the null for each component of , so we have many -values, and terminate the algorithm when the smallest -value exceeds 0.01.

We run the test at the iteration for the first time. If some -values are smaller than 0.01, we additionally iterate the AM algorithm 10,000 times and again check the convergence. We continue this until the algorithm stops. Therefore the final is random. We use the last seventy five percent of the iterations, , for inference and decision making. The test ensures that these parameters are drawn from the posterior and can therefore be used for policy analysis. Since our stopping criteria requires the worst case to pass the test, this decision rule is conservative.

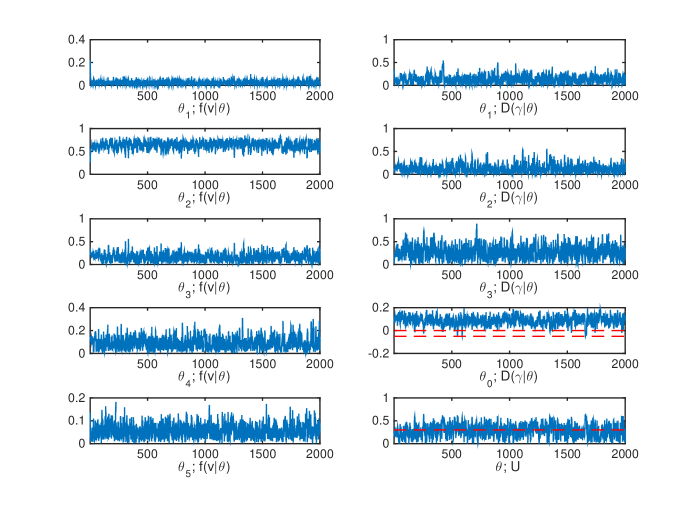

In our exercise with the data , the smallest and the average -value we record for convergence are 0.19 and , respectively, at the iteration.

|

The left panels show the parameters of valuation density, and the right panels show the parameters for -function and the utility function (bottom).

See Figure 8 for the times series of outcomes. The X-axis is the length of the series, which is 2,000 because we record every outcome. The left panels show the parameters of valuation density, and the right panels show the parameters for -function and the utility function (bottom). The two dashed horizontal lines in panel for , (fourth from top) indicate the negative range of – recall that can be negative in which case the -function is the identity, i.e. no ambiguity aversion. The red dashed line in the panel for is the true CRRA coefficient which is set at .

3.3.4. Posterior Analysis and Decision Making

We begin with a posterior predictive analysis, just like the prior predictive analysis. For each , drawn from the posterior, we generate a bid sample of size and compute the same summary statistics: sample mean, standard deviation, and skewness. The results are presented in Figure 10, and as can be seen, the posterior distribution accurately predicts the summary statistics of the actual data very precisely.

|

Each panel demonstrate the distribution of the summary statistics by dots of the bid data under the posterior along with the summary statistics of the original data in solid lines. Note that the ranges for each panel and the solid lines are the same as the ones in Figure 6.

Before discussing the posterior analysis further, it would be useful to make a formal distinction between the concepts of accuracy and precision, which are often confused, though widely used. An estimate is said to be accurate, when it is in a small neighborhood of the true quantity. Since we know the DGP in this section, we can measure the accuracy by computing the -distance. On the other hand, the estimate is precise, if there is little uncertainty around the estimate where the concepts of uncertainty further depends on the philosophical views on statistics. In Bayesian statistics, the parameter is random whereas data are fixed. The posterior captures the parameter uncertainty conditional on the fixed data, and the posterior credible sets and/or the posterior standard deviation are often reported as a measure of uncertainty. In contrast, in a frequentist analysis, the parameter is fixed, but there is uncertainty about the estimate because data are random. This kind of uncertainty is quantified by the sampling distribution of the estimator, which is often measured by an asymptotic standard errors or confidence sets. The estimate is, therefore, precise when the posterior (sampling) distribution is condensed from the Bayesian (frequentist) point of view. In this section, we use the Bayesian precision, but we examine, in section 4, the frequentist uncertainty by repeated sampling, .

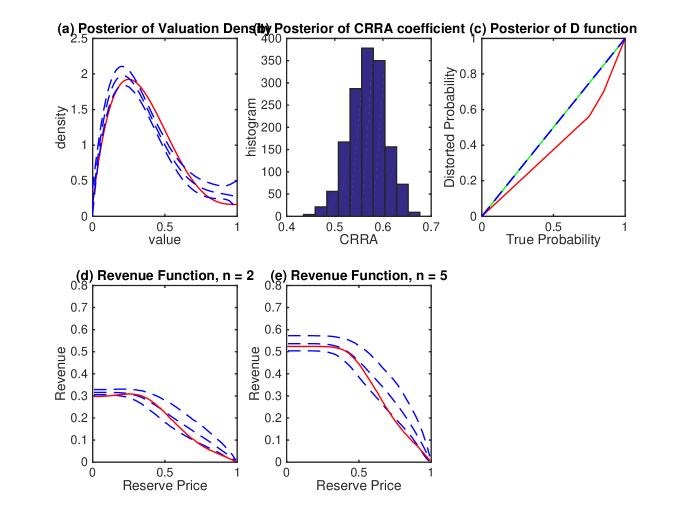

The posterior predictive valuation density is given by the most widely used Bayesian density estimate

| (18) |

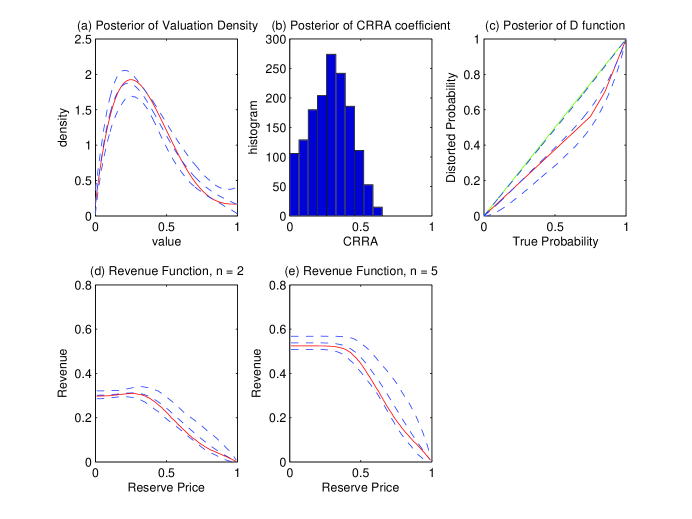

as for . Figure 12 (a) shows the estimate with its point-wise 2.5 and 97.5 percentiles posterior credible band in dashed lines and the true density in a solid line. More specifically, recall that we use 1,500 parameters drawn from the posterior, which means we have 1,500 valuation densities. For every point , the middle dashed line represents the average of these 1,500 densities, i.e, (18), and 95% of the densities pass between the upper and the lower dashed lines. The 95% credible band is narrow, which means the posterior inference on the valuation density is precise. Moreover, the narrow credible band contains and over the entire support ; the estimate is accurate. Furthermore, because we know , we can measure the accuracy by the -distance between estimate and the true density:

|

Panel (a) shows the posterior of the valuation density by its point-wise mean and a 95% credible band. Panel (b) is the posterior of the CRRA coefficients. Panel (c) summarizes the posterior of the -function. Panels (d) and (e) show the posterior of revenue functions for and cases. On panels (a), (c), (d), and (e), the true quantities are the solid line. (Panel (c) shows the identity.)

Figure 12 (b) is the histogram of (CRRA coefficient) drawn from the posterior distribution. Define the Bayesian estimate for the CRRA coefficient as

which is the posterior mean of . We obtain with the posterior standard deviation of 0.14. The posterior predictive for is given by

Figure 12 (c) shows and its pointwise 2.5 and 97.5 posterior percentiles (dashed line). It appears that the credible band contains (solid line), and , which suggests the high accuracy of our estimate. The posterior probability that bidders are ambiguity neutral is estimated by

| (19) |

We find that the posterior probability is only 2.13%, thus providing a strong evidence of ambiguity aversion.

Next, we consider the decision problem of choosing a reserve price to maximize the seller’s expected revenue. Let denote the seller’s expected revenue at under in a first price auction with bidders. Then, the posterior predictive revenue is given as

| (20) |

The subjective expected utility theory Savage (1954); Anscombe and Aumann (1963) postulates that it is rational to maximize (20). Let which is called the Bayes action.131313 The solution is also optimal under the average risk principle, a widely used frequentist decision criteria; see Berger (1985); Kim (2013, 2014). Moreover, we note that estimation problem is a special case of decision making problem where the posterior mean of the parameter is the Bayes action with respect to the squared error loss. Therefore, the Bayesian estimates are decision theoretically optimal. In order to choose , we estimate (20) by

| (21) |

which is shown in Figure 12 (d) for ( and Figure 12 (e) for ) along with a 95% posterior credible band (dashed line). The line of Table 2 shows that at which the posterior predicts the revenue . Moreover, the 2.5 and 97.5 posterior percentiles of form a 95% posterior credible interval for the revenue at . This interval includes the true revenue, , which is essentially equal to where . Hence, there is no revenue loss of using relative to using . The line of Table 2 summarizes the policy implications for .

3.4. Discussion

Before we conclude this section, we discuss why we employ the direct approach in the Bayesian framework instead of adopting the indirect approach that has been used since Guerre, Perrigne, and Vuong (2000) – the latter first estimates the bid distribution functions and recovers the primitives from the estimates by the first order conditions. First, since it is relatively straightforward to impose shape restrictions under the direct approach, we may easily develop an empirical framework where the econometric method is internally consistent with the underlying economic model. For example, the monotonicity of bidding functions is automatically satisfied under the direct approach, but the inverse bidding function associated with the estimated bid distribution functions (indirect approach) may not be monotone unless explicitly imposed. Such a violation of shape conditions may lower efficiency because the available information is not fully exploited, and it would also invalidate policy recommendations because counterfactual analysis under an alternative policy should be valid only when the model assumption(s), like bidding monotonicity, are satisfied, see Kim (2014).

Second, today, computing is far more powerful than that of a few decades ago and it is much cheaper. By providing a computationally feasible nonparametric framework, Guerre, Perrigne, and Vuong (2000) has widely broadened the scope of the empirical auction literature, which had, in 90’s or before, relied upon tightly specified statistical models within a few very simple theoretical paradigms mostly because of the computational difficulties for evaluating the likelihoods. We no longer have such computational restrictions. In the next sections, we run our empirical methods in many Monte Carlo experiments using authors’ desktop/laptop computers.

Once the direct approach is chosen, the Bayesian approach has several advantages over frequentist methods. The statistical model for bid data from first price auctions is irregular because the support of bids depends on parameters of interest. Hirano and Porter (2003) shows that in this case the Bayesian estimator is efficient but the maximum likelihood estimator (MLE) is not.141414 The results of Hirano and Porter (2003) hold under fairly weak assumptions on loss functions and priors, including the ones we use in this paper – the error squared loss and the expected revenue. (The negative of the revenue is the loss for our analysis.) Moreover, the Bayesian method provides a natural environment of decision theoretic framework that is useful for the seller who wishes to choose a reserve price to maximize the expected revenues; see Aryal and Kim (2013); Kim (2013, 2014). Finally, the Bayesian method can be more useful in a case of the parameter on the boundary of the parameter space, where both the Bayesian estimator and the MLE are typically biased. As mentioned earlier, by putting a positive prior mass on the subspace of the parameter space, however, we may reduce the bias of the Bayesian analysis. For example, even if the true -function is the identity (no ambiguity), the empirical method that restricts -function to be bounded above by the identity function will produce downwardly biased estimates. We handle this problem by putting a positive prior mass on the event that . In the next section, we confirm that such a prior mass enables the posterior to predict the - function to be the identity mapping when there is no ambiguity. The cost of this is that when there is ambiguity, the posterior puts a positive albeit negligible probability on the identity.

| Bayes | Predictive | 95 % Credible | True Rev. at | Rev. Loss (%) | ||

|---|---|---|---|---|---|---|

| Action | Revenue | Interval for | B. Action, | wrt Max. Rev. | ||

| Revenue | [(D)-(B)]/(B) | |||||

| (A) | (B) | (C) | (D) | (E) | ||

| Correct | 0.26 | 0.312 | [0.296,0.329] | 0.309 | 0.000 | |

| Redundant | 0.28 | 0.297 | [0.283,0.310] | 0.292 | 0.083 | |

| Misspecified | 0.12 | 0.316 | [0.308,0.324] | 0.301 | 2.651 | |

| Correct | 0.11 | 0.538 | [0.513,0.563] | 0.524 | 0.000 | |

| Redundant | 0.12 | 0.496 | [0.480,0.512] | 0.485 | 0.000 | |

| Misspecified | 0.10 | 0.537 | [0.513,0.557] | 0.524 | 0.000 |

Column (A) shows the Bayes action and columns (B) and (C) summarizes the posterior distribution of the revenue at the Bayes action by the mean and a 95% credible interval. Column (D) shows the true revenue at the Bayes action and column (E) the revenue loss of using the Bayes action relative to the true maximum revenue.

4. Monte Carlo Study

In this section, we examine the performance of our Bayesian method in a repeated sampling for three different cases: (i) Correct model – where bidders are ambiguity averse and the econometrician allows ambiguity aversion; (ii) Redundant model – bidders are ambiguity neutral, but the econometrician allows ambiguity aversion; and (iii) Misspecified model – bidders are ambiguity averse but the econometrician ignores it. For each case, we study the sampling distributions of the Bayesian predictive estimates and quantify the effect of the model choice on seller’s expected revenue. To summarize our result: we show that our method performs well when there is ambiguity (correct) and it does still so even when there is no ambiguity (redundant). Especially, there is no discernible effect of over specification – redundantly modeling ambiguity when there is none – on the seller’s revenue. However, if we use a misspecified model and ignore ambiguity, then it may cause a substantial revenue loss. We conclude this section by studying the case where we have a larger set of .

4.1. Correct Model

We draw datasets independently from the DGP shown in Figure 4. Then, for each data realization, we apply our method in subsection 3.3. This Monte Carlo study generates estimates and the Bayes actions and associated true revenues for . We use and analyze in subsection 3.3.

|

Panel (a) shows the sampling distribution of the estimated valuation densities by its pointwise mean and a 95% frequency band. Panel (c) is the histogram of the CRRA estimates. Panel (c) demonstrates the sampling distribution of the estimated functions. Panels (d) and (e) are for the estimated revenue functions with alternative numbers of bidders. The solid lines represent the true quantities.

Figure 14(a) summarizes the sampling distribution of by their pointwise mean, and the 2.5 and 97.5 percentiles (dashed line). The pointwise mean closely approximates (solid line) and the 95% frequency band is narrow. As discussed in subsection 3.3.4, the sampling distribution of estimates here is different from the posterior distribution in subsection 3.3: the latter quantifies the uncertainty regarding for a given data whereas the former represents the variation of the Bayesian estimate (posterior mean) associated with the randomness of .

The sampling distribution of is similarly shown in panel (c). All other curves in the panel have the same interpretation as before. Table 4 documents that the mean integrated squared error (MISE) of is 0.0083 and the MISE of is 0.0009, which shows the high accuracy of our method.151515 Let be an estimate constructed by data for the true function . Then, . The MISE is small only when the variance and the bias are both small. Panel (b) presents the histogram of – the sample mean is 0.293 and the standard deviation is 0.017. The mean squared error (MSE) is given as where the expectation is taken over the sample .

Panels (d) and (e) in Figure 14 display the sampling distributions of and , respectively. Recall that denotes the posterior predictive revenue in (21) and the Bayes action is . Moreover, is the true revenue, unknown to the seller; see Figure 4(d), and , which is infeasible. The seller can, therefore, choose and obtain the true revenue of – we focus on the sampling distribution of . The average of is 0.248 with standard deviation of and the average of is with standard deviation of . Moreover, the average revenue loss of employing with respect to is only 0.398%.

| Total N. | Rev. Loss (%) | ||||

|---|---|---|---|---|---|

| Specification | of bids | (A) | (B) | (C) | (D) |

| Correct | 600 | 0.0083 | 0.0009 | 0.007 | 0.398 |

| 1,200 | 0.0054 | 0.0006 | 0.006 | 0.307 | |

| 2,400 | 0.0040 | 0.0004 | 0.005 | 0.165 | |

| Redundant | 600 | 0.0049 | 0.0004 | 0.007 | 0.189 |

| 1,200 | 0.0025 | 0.0004 | 0.005 | 0.094 | |

| 2,400 | 0.0015 | 0.0003 | 0.004 | 0.010 | |

| Misspecified | 600 | 0.0214 | 0.0128 | 0.078 | 2.898 |

| 1200 | 0.0230 | 0.0128 | 0.087 | 3.246 | |

| 2400 | 0.0253 | 0.0128 | 0.092 | 3.439 |

Columns (A) and (B) documents the MISEs of the valuation density estimate and the function estimate, respectively. Column (C) shows the MSE of the estimate for the CRRA coefficient. Column (D) provides the revenue loss of the Bayes auction relative to the true maximum revenue.

Finally, we consider larger samples: (i) , i.e., ; and (ii) , i.e., . For each case, we repeat the Monte Carlo experiments with replications, as described above, and find that the estimates get more accurate and the revenue loss decreases as the sample size increases, see Table 4.

4.2. Redundant Model

We generate datasets independently from the DGP shown in Figure 4 except that we use , i.e., the model of no ambiguity aversion. In other words, there is no ambiguity among bidders. Then, for each , we apply our method as before that allows ambiguity aversion.

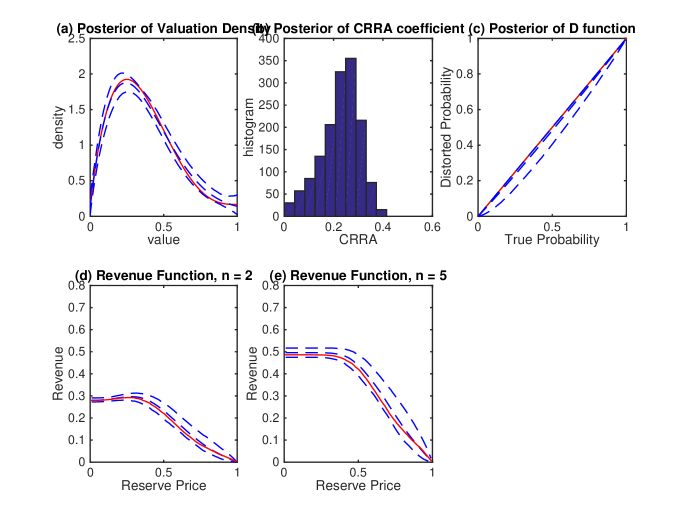

We discuss first the posterior analysis for the first dataset and then investigate the sampling distribution using many datasets, . The prior and posterior predictive analyses on the summary statistics of produce almost identical results as Figures 6 and 10. Figure 16 presents the posterior distributions for the quantities of interest as in Figure 12. It is noticeable that and its 95% credible band is narrow, correctly predicting that the bidders would not be ambiguity averse.161616 Since is restricted to be below the identity; see (10), the pointwise upper bound cannot be larger than . Moreover, we find that the posterior probability for no ambiguity aversion (19) is 55% whereas the prior probability is 26%. If we choose a model between ambiguity averse model and ambiguity neutral model, according to the Bayesian model selection, we would select the one with the largest posterior probability.171717 The Bayesian model comparison is often approximated by the Bayesian information criteria or the Akaike Information criteria, each assuming a different prior. Thus, since the posterior odd ratio is

we would choose the model of no ambiguity aversion.

Figure 16 also shows that and closely approximate and with narrow credible bands, even when the redundant modeling of ambiguity aversion creates additional parameter uncertainty. Furthermore, the redundant modeling does not invalidate the policy recommendation of our method. The line of Table 2 shows that at which the posterior predicts the revenue . Moreover, the 2.5 and 97.5 posterior percentiles of form a 95% posterior credible interval for the revenue at . This interval includes the true revenue, , which is very close to – the revenue loss of using relative to using is only 0.083%. The line of Table 2 also summarizes the policy implications on the seller’s revenue for . Note that the true revenue function is different from the one in the previous subsection because here is the identity.

|

Panel (a) shows the posterior of the valuation density by its pointwise mean and a 95% credible band. Panel (b) is the posterior of the CRRA coefficients. Panel (c) summarizes the posterior of the -function. Panels (d) and (e) show the posterior of revenue functions for and cases. On panels (a), (c), (d), and (e), the true quantities are the solid line. (Panel (c) shows the identity.)

|

Panel (a) shows the sampling distribution of the estimated valuation densities by its pointwise mean and a 95% frequency band. Panel (c) is the histogram of the CRRA estimates. Panel (c) demonstrates the sampling distribution of the estimated functions. Panels (d) and (e) are for the estimated revenue functions with alternative numbers of bidders. The solid lines represent the true quantities.

Now, we consider the repeated sampling, which generates estimates and the Bayes actions and associated true revenues for . Figure 18 summarizes the sampling distribution of the estimates of interest. The distributions of , , and closely approximate the true quantities (accurate) and their 95% frequency bands are all narrow (precise). Table 4 documents that the mean integrated squared error (MISE) of is 0.0049 and the MISE of is 0.0004, which also shows the high accuracy of our method. Panel (b) shows the histogram of – the estimate is slightly underestimated, but Table 4 documents that the accuracy measured by MSE is , which is the same as the correct model. Moreover, the Bayes action generates essentially optimal revenues. Finally, we find that the estimates get more accurate and the revenue loss decreases as the sample size grows; see Table 4.

In summary: even if bidders are not ambiguity averse, the redundant modeling of -function would neither lower accuracy/precision of the estimates nor invalidate policy recommendations.

4.3. Misspecified Model

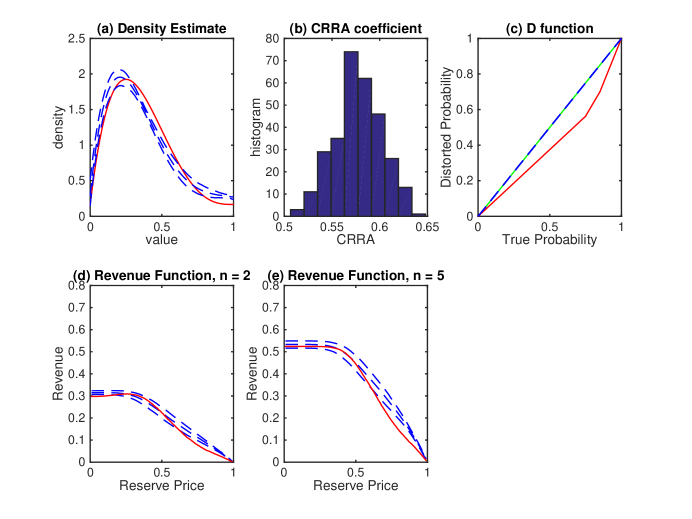

We generate datasets independently from the DGP shown in Figure 4 with the on panel (b), i.e., bidders are ambiguity averse. So, the DGP is the same as the one in subsection 4.1, but we assume that the econometrician ignores the presence of ambiguity. That is, for each , we apply our method constraining to be the identity to investigate the effect of such misspecification on estimates and policy implications.

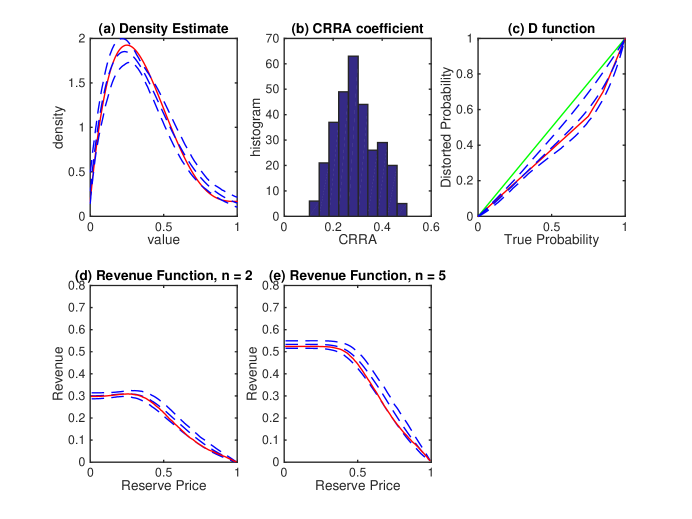

We examine the posterior analysis first for the first data set . The prior predictive analysis on the summary statistics of is almost identical to the results as Figure 6 in the sense that the data can be regarded as a typical realization under the prior, which is diffuse. However, the posterior distribution of the summary statistics, especially for , does not predict the data; see Figure 20, which suggests that econometrician may need to improve the specification or revise the model. In addition, Figure 22 shows that the posterior credible band for the valuation density does not include over a large portion of the support and the support of the posterior of does not contain true , i.e., the estimates are inaccurate.

|

Each panel demonstrate the distribution of the summary statistics by dots of the bid data under the posterior along with the summary statistics of the original data in solid lines.

|

Panel (a) shows the posterior of the valuation density by its pointwise mean and a 95% credible band. Panel (b) is the posterior of the CRRA coefficients. Panel (c) summarizes the posterior of the -function. Panels (d) and (e) show the posterior of revenue functions for and cases. On panels (a), (c), (d), and (e), the true quantities are the solid line. (Panel (c) shows the identity.)

|

Panel (a) shows the sampling distribution of the estimated valuation densities by its pointwise mean and a 95% frequency band. Panel (c) is the histogram of the CRRA estimates. Panel (c) demonstrates the sampling distribution of the estimated functions. Panels (d) and (e) are for the estimated revenue functions with alternative numbers of bidders. The solid lines represent the true quantities.

The failure of modeling ambiguity aversion can invalidate the policy recommendation. Table 2 shows that which predicts the revenue of with the 95% credible interval of . But, this credible interval does not contain the true revenue and, thereby, the revenue prediction is not accurate. Furthermore, the revenue loss of using under the misspecification relative to the largest revenue is approximately 2.65%. This revenue loss can also be regarded as the revenue loss relative to the correct model because the latter produces essentially the true maximum revenue.

Now, we investigate the sampling distribution of the estimates and the Bayes actions and associated true revenues for . Figure 24 summarizes the sampling distribution of the estimates of interest. The distributions of does not approximate the true and the CRRA coefficients are so overestimated that the true is not in the support of the histogram. Table 4 documents that the MISE of is 0.0214, which is 2.57 times larger than the MISE of for the correctly specified case, and the MSE of is ten times larger. Moreover, the revenue loss of under the misspecification is about 2.9% relative to the true optimal revenue . Finally, we find that the estimates does not get more accurate (MISE of ) as the sample size grows and the revenue loss does not disappear.

Therefore, when the empirical analysis does not take into account the ambiguity aversion, the estimates can be inaccurate and the policy recommendations can be invalid, unlike the case where the ambiguity is redundantly modeled when there is no ambiguity.

4.4. Rich variation in

Until now, we have considered , i.e., we observe auctions with two bidders and auctions with five bidders. Here, we examine the empirical environment in which there is a richer variation in the number of bidders – we consider and then . For both and , as before, we study the cases that we observe 600 bids in total, 1,200 bids, and 2,400 bids with each bidder auction equally sharing the bids. For example, when we observe 1,200 bids for , then we observe 400 bids for each of bidder auctions, i.e. we observe two bidder auctions, four bidder auctions, and five bidder auctions. Since we consider two ’s and three sample sizes , we have six pairs of and sample sizes, for each of which we consider Correct model, Redundant model, and Misspecified model. We run 18 experiments in this subsection in addition to the 9 experiments with in the previous subsections.

| Total N. | Rev. Loss (%) | ||||

|---|---|---|---|---|---|

| Specification | of bids | (A) | (B) | (C) | (D) |

| Correct | 600 | 0.0075 | 0.0011 | 0.007 | 0.432 |

| 1200 | 0.0046 | 0.0007 | 0.005 | 0.315 | |

| 2400 | 0.0033 | 0.0004 | 0.004 | 0.122 | |

| Redundant | 600 | 0.0043 | 0.0004 | 0.006 | 0.148 |

| 1200 | 0.0024 | 0.0004 | 0.005 | 0.076 | |

| 2400 | 0.0012 | 0.0003 | 0.003 | 0.045 | |

| Misspecified | 600 | 0.0197 | 0.0128 | 0.078 | 2.900 |

| 1200 | 0.0208 | 0.0128 | 0.082 | 3.103 | |

| 2400 | 0.0228 | 0.0128 | 0.084 | 3.261 |

Columns (A) and (B) documents the MISEs of the valuation density estimate and the function estimate, respectively. Column (C) shows the MSE of the estimate for the CRRA coefficient. Column (D) provides the revenue loss of the Bayes auction relative to the true maximum revenue.

Tables 6 and 8 document the results of the Monte Carlo study with and , respectively. In both cases, we observe the same pattern as we do in the case of . The correct model and redundant model generate accurate estimates on the model primitives and the Bayes action on reserve price produces essentially maximum revenues. In addition, as sample size grows, the method becomes more accurate and precise, and the revenue loss decreases. On the other hand, the misspecified model that ignores the ambiguity results in far less accurate estimates on the model primitives and the revenue loss of about 3%.

| Total N. | Rev. Loss (%) | ||||

|---|---|---|---|---|---|

| Specification | of bids | (A) | (B) | (C) | (D) |

| Correct | 600 | 0.0075 | 0.0013 | 0.009 | 0.596 |

| 1200 | 0.0042 | 0.0006 | 0.004 | 0.260 | |

| 2400 | 0.0030 | 0.0004 | 0.003 | 0.084 | |

| Redundant | 600 | 0.0040 | 0.0004 | 0.005 | 0.139 |

| 1200 | 0.0020 | 0.0004 | 0.004 | 0.058 | |

| 2400 | 0.0010 | 0.0004 | 0.003 | 0.034 | |

| Misspecified | 600 | 0.0180 | 0.0128 | 0.084 | 3.024 |

| 1200 | 0.0185 | 0.0128 | 0.091 | 3.299 | |

| 2400 | 0.0208 | 0.0128 | 0.096 | 3.483 |

Columns (A) and (B) documents the MISEs of the valuation density estimate and the function estimate, respectively. Column (C) shows the MSE of the estimate for the CRRA coefficient. Column (D) provides the revenue loss of the Bayes auction relative to the true maximum revenue.

5. Conclusion

We study first-price auction models where risk averse bidders have ambiguity about the valuation distribution. In an environment where bidders consider multiple distributions as equally reasonable and their preferences are represented by the maxmin expected utility, we characterize a symmetric and monotonic equilibrium (bidding) strategy. We show that exogenous entry of bidders is sufficient to identify model structure (true valuation distribution, the D-function that measures the level of ambiguity and the risk aversion (CRRA) coefficient). To decide whether there is ambiguity in the data it is enough to check if the -function is strictly below an identity function.

Then we propose a flexible Bayesian estimation method that uses Bernstein polynomials. Since the main objective of empirical auction is to use data to design optimal auctions, we consider a multitude of simulation exercises to asses the performance of our method and to analyze the importance of ambiguity for the seller. We show that our method detects ambiguity correctly when there is ambiguity, and when there is no ambiguity yet we allow for ambiguity, there is no discernible loss to the seller from using our method. On the other hand, if there is ambiguity and we ignore it, we show the estimates are biased and as a result the seller can lose substantial (3% in our exercises) of revenue. These exercises suggest that in empirical auction it is always better to allow for ambiguity, unless the econometrician is absolutely certain that there is no ambiguity among bidders.

We conclude by pointing out few avenues to explore for extension. First, one could consider the possibility that entry is endogenous. With appropriate exclusion restriction, as in Bajari and Hortaçsu (2003); Haile, Hong, and Shum (2006); Krasnokutskaya and Seim (2011), the model can still be identified. Second, we can consider dynamic auctions with learning where bidders begin with an exogenously specified set of distributions and update their beliefs after every auction. It is well-known that the MEU model need not be dynamically consistent with full Bayesian updating, see Hanany and Klibanoff (2007) and Epstein and Schneider (2003); Epstein and Scheider (2007). Aryal and Stauber (2014) showed that the method proposed by Epstein and Schneider (2003) to address dynamic inconsistency cannot be extended to games with multiple players. So it is not even clear how we can characterize equilibrium strategies. Moreover, if bidders have incentive to learn then the seller might have incentive to obfuscate by withholding the bids, simultaneously leading to the problem of determining optimal disclosure rule, Bergemann and Wambach (2013) and the informed principal problem Myerson (1983); Maskin and Tirole (1990).

References

- (1)

- Andrews (1999) Andrews, D. W. K. (1999): “Estimation When a Parameter is on a Boundary,” Econometrica, 67, 1341–1383.

- Anscombe and Aumann (1963) Anscombe, F. J., and R. J. Aumann (1963): “A Definition of Subjective Probability,” Annals of Mathematical Statistics, 34(1), 199–205.

- Aradillas-Lopez, Gandhi, and Quint (2013) Aradillas-Lopez, A., A. Gandhi, and D. Quint (2013): “Identification and Testing in Ascending Auctions with Correlated Private Values,” Econometrica, 81(2), 489–534.

- Aryal and Kim (2013) Aryal, G., and D.-H. Kim (2013): “A Point Decision for Partially Identified Auction Models,” Journal of Business & Economic Statistics, 31(4), 384–397.

- Aryal and Stauber (2014) Aryal, G., and R. Stauber (2014): “A Note on Kuhn’s Theorem with Ambiguity Averse Players,” Economic Letters, 125(1), 110–114.

- Athey (2001) Athey, S. (2001): “Single Crossing Properties and The Existence of Pure Strategy Equilibria in Games of Incomplete Information,” Econometrica, 69(4), 861–889.

- Athey and Haile (2002) Athey, S., and P. A. Haile (2002): “Identification of Standard Auction Models,” Econometrica, 70(6), 2107–2140.

- Athey and Haile (2007) (2007): “Nonparametric Approaches to Auctions,” Handbook of Econometrics, 6A.

- Athey, Levin, and Seira (2011) Athey, S., J. Levin, and E. Seira (2011): “Comparing Open and Sealed Bid Auctions: Evidence from Timber Auctions,” The Quaterly Journal of Economics, 126(1), 207–257.

- Bajari and Hortaçsu (2003) Bajari, P., and A. Hortaçsu (2003): “The Winner’s Curse, Reserve Prices, and Endogenous Entry: Empirical Insights from eBay Auctions,” The RAND Journal of Economics, 34(2), 329–355.

- Bajari and Hortaçsu (2005) (2005): “Are Structural Estimates of Auction Models Reasonable? Evidence from Experimental Data,” Journal of Political Economy, 113(4), 703–741.

- Bergemann and Wambach (2013) Bergemann, D., and A. Wambach (2013): “Sequential Information Disclosure in Auctions,” Cowles Foundation Discussion Paper No. 1900.

- Berger (1985) Berger, J. O. (1985): Statistical Decision Theory and Bayesian Analysis., Springer Series in Statistics. Springer, New York.

- Berger and Berliner (1986) Berger, J. O., and L. M. Berliner (1986): “Robust Bayes and empirical Bayes analysis with contaminated priors,” Annals of Statistics, 14, 461–486.

- Bodoh-Creed (2012) Bodoh-Creed, A. L. (2012): “Ambiguous Beleifs and Mechanism Design,” Games and Economic Behavior, 75(2), 518–537.

- Bose, Ozdenoren, and Pape (2006) Bose, S., E. Ozdenoren, and A. Pape (2006): “Optimal Auctions with Ambiguity,” Theoretical Economics, 1(4), 411–438.

- Bose and Renou (2014) Bose, S., and L. Renou (2014): “Mechanism Design With Ambiguous Communication Devices,” Econometrica, 82(5), 1853–1872.

- Camerer and Karjalainen (1994) Camerer, C. F., and R. Karjalainen (1994): “Ambiguity-aversion and Non-additive Beliefs in Non-Cooperative Games: Experimental evidence,” Models and Experiments in Risk and Rationality, 29, 325–358.

- Campo, Guerre, Perrigne, and Vuong (2011) Campo, S., E. Guerre, I. Perrigne, and Q. Vuong (2011): “Semiparametric Estimation of First-Price Auctions with Risk Averse Bidders,” Review of Economic Studies, 78(1), 112–147.

- Cerreia-Vioglio, Maccheroni, Marinacci, and Montrucchio (2013) Cerreia-Vioglio, S., F. Maccheroni, M. Marinacci, and L. Montrucchio (2013): “Ambiguity and Robust Statistics,” Journal of Economic Theory, 148(3), 974–1049.

- Chateauneuf, Maccheroni, Marinacci, and Tallon (2005) Chateauneuf, A., F. Maccheroni, M. Marinacci, and J.-M. Tallon (2005): “Monotone Continuous Multiple Priors,” Economic Theory, 26, 973–982.

- Donald and Paarsch (1993) Donald, S., and H. Paarsch (1993): “Piecewise Pseudo-Maximum Likelihood Estimation in Empirical Models of Auctions,” International Economic Review, 34, 121–148.

- Dupuis and Ellis (1997) Dupuis, P., and R. S. Ellis (1997): A Weak Convergence Approach to the Theory of Large Deviations, Wiley Series in Probability and Statistics. Wiley.

- Ellsberg (1961) Ellsberg, D. (1961): “Risk, Ambiguity, and the Savage Axioms,” Quarterly Journal of Economics, 75(4), 643–669.

- Epstein (1999) Epstein, L. (1999): “A Definition of Uncertinaty Aversion,” The Review of Economic Studies, 66(3), 579–608.

- Epstein and Scheider (2007) Epstein, L., and M. Scheider (2007): “Learning Under Ambiguity,” Review of Economic Studies, 7(4), 1275–1303.

- Epstein and Schneider (2003) Epstein, L. G., and M. Schneider (2003): “Recursive Multiple-Priors,” Journal of Economic Theory, 113(1), 1–31.

- Escobar and West (1995) Escobar, M. D., and M. West (1995): “Bayesian Density Estimation and Inference Using Mixtures,” Journal of the American Statistical Association, 90(430), 577–588.

- Ferguson (1973) Ferguson, T. S. (1973): “A Bayesian Analysis of Some Nonparametric Problems,” Annals of Statistics, 1(2), 209–230.

- Fox and Tversky (1995) Fox, C. R., and A. Tversky (1995): “Ambiguity Aversion and Comparative Ignorance,” The Quarterly Jounral of Economics, 110, 585–603.

- Geweke (2005) Geweke, J. (2005): Contemporary Bayesian Econometrics and Statistics. John Wiley & Sons, Inc, Hoboken, New Jersey.

- Gilboa (2009) Gilboa, I. (2009): Theory of Decision Under Uncertainty. Cambridge University Press.

- Gilboa and Schmeidler (1989) Gilboa, I., and D. Schmeidler (1989): “Maxmin Expected Utility with Non-Unique Prior,” Journal of Mathematical Economics, 18, 141–153.

- Gilboa and Schmeidler (1993) (1993): “Updating Ambiguous Beliefs,” Journal of Economic Theory, 59(1), 33–49.

- Grundl and Zhu (2013) Grundl, S., and Y. Zhu (2013): “Identification and Estimation of Frist-Price Auctions With Ambiguous beliefs,” Mimeo.

- Guerre, Perrigne, and Vuong (2000) Guerre, E., I. Perrigne, and Q. Vuong (2000): “Optimal Nonparametric Estimation of First-Price Auctions,” Econometrica, 68(3), 525–574.

- Guerre, Perrigne, and Vuong (2009) (2009): “Nonparametric Identification of Risk Aversion in First-Price Auctions under Exclusion Restrictions,” Econometrica, 77(4), 1193–1227.

- Haario, Saksman, and Tamminen (2001) Haario, H., E. Saksman, and J. Tamminen (2001): “An Adaptive Metropolis Algorithm,” Bernoulli, 7, 223–242.

- Haile, Hong, and Shum (2006) Haile, P., H. Hong, and M. Shum (2006): “Nonparametric Tests for Common Values In First-Price Sealed-Bid Auctions,” NBER Working Paper Series.

- Halevy (2007) Halevy, Y. (2007): “Ellsberg Revisited: An Experimental Study,” Econometrica, 75, 503–536.

- Hanany and Klibanoff (2007) Hanany, E., and P. Klibanoff (2007): “Updating Preferences with Multiple Priors,” Theoretical Economics, 2, 261–298.

- Hansen (2014) Hansen, L. P. (2014): “Nobel Lecture: Uncertainty Outside and Inside Economic Models,” Journal of Political Economy, 122(5), 945–987.

- Hansen and Sargent (2001) Hansen, L. P., and T. J. Sargent (2001): “Robust Control and Model Uncertainty,” American Economic Review, P&P, 91(2), 60–66.

- Harsanyi (1967) Harsanyi, J. C. (1967): “Games with Incomplete Information Played by “Bayesian” Players, I-III Part I. The Basic Model,” Management Science, 14(3), 320–334.

- Hendricks and Porter (2007) Hendricks, K., and R. H. Porter (2007): “An Empirical Perspective On Auctions,” Handbook of Industrial Organization, Chapter 32.

- Hirano and Porter (2003) Hirano, K., and J. Porter (2003): “Asymptotic Efficiency in Parametric Structural Models with Parameter-Dependent Support,” Econometrica, 71, 1307–1338.

- Huber (1973) Huber, P. J. (1973): “The use of Choquet capacities in statistics,” Bulletin of the International Statistical Institute, 45, 181–191.

- Keynes (1921) Keynes, J. M. (1921): A Treatise on Probability. MacMillan.

- Kim (2013) Kim, D.-H. (2013): “Optimal Choice of a Reserve Price under Uncertainty,” International Journal of Industrial Organization, 31(5), 587–602.

- Kim (2014) (2014): “Flexible Bayesian Analysis of First Price Auctions Using a Simulated Likelihood,” Quantitative Economics, forthcoming.

- Kim (2015) (2015): “Nonparametric Analysis of Utility Functions in First Price Auctions,” Economics Letters, 126(1), 101–106.

- Knight (1921) Knight, F. (1921): Risk, Uncertainty and Profit. Houghton Mifflin Co.

- Krasnokutskaya and Seim (2011) Krasnokutskaya, E., and K. Seim (2011): “Bid Preference Programs and Participation in Highway Procurement Auctions,” American Economic Review, 101(6), 2653–2686.

- Lo (1998) Lo, K. C. (1998): “Sealed Bid Auctions with Uncertainty Averse Bidders,” Economic Theory, 12, 1–20.

- Lu and Perrigne (2008) Lu, J., and I. Perrigne (2008): “Estimating Risk Aversion from Ascending and Sealed-Bid Auctions: The Case of Timber Auction Data,” Journal of Applied Econometrics, 23(7), 871–896.

- Maskin and Riley (1984) Maskin, E., and J. Riley (1984): “Optimal Auctions With Risk Averse Buyers,” Econometrica, 52(6), 1473 – 1518.

- Maskin and Tirole (1990) Maskin, E., and J. Tirole (1990): “The Principal-Agent Relationship With an Informed Principal: The Case of Private Values,” Econometrica, 58(2), 379–409.

- Myerson (1983) Myerson, R. B. (1983): “Mechanism Design by an Informed Principal,” Econometrica, 51(6), 1767–1797.

- Nishimura and Ozaki (2004) Nishimura, K. G., and H. Ozaki (2004): “Search and Knightian Uncertainty,” Journal of Economic Theory, 119(2), 299–333.

- Petrone (1999a) Petrone, S. (1999a): “Bayesian Density Estimation Using Bernstein Polynomials,” Canadian Journal of Statistics, 27, 105–126.

- Petrone (1999b) (1999b): “Random Bernstein Polynomials,” Scandinavian Journal of Statistics, 26, 373–393.

- Savage (1954) Savage, L. (1954): Foundation of Statistics. Wiley, reissued in 1972 by Dover, New York.

- Siniscalchi (2011) Siniscalchi, M. (2011): “Dyanamic Choice under Ambiguity,” Theoretical Economics, 6(3), 379–421.

- Strzalecki (2011) Strzalecki, T. (2011): “Axiomatic Foundations of Multimplier Preferences,” Econometrica, 79(1), 47–73.