On the convergence of monotone schemes for path-dependent PDEs 111The authors gratefully acknowledge the financial support of the ERC 321111 Rofirm, the ANR Isotace, the Chairs Financial Risks (Risk Foundation, sponsored by Société Générale), Finance and Sustainable Development (IEF sponsored by EDF and CA), and the grant of the region of l’île de France. The authors are also grateful to Ibrahim Ekren and Nizar Touzi for their helpful remarks and suggestions.

Abstract

We propose a reformulation of the convergence theorem of monotone numerical schemes introduced by Zhang and Zhuo [34] for viscosity solutions to path-dependent PDEs (PPDE), which extends the seminal work of Barles and Souganidis [1] on the viscosity solution to PDE. We prove the convergence theorem under conditions similar to those of the classical theorem in [1]. These conditions are satisfied, to the best of our knowledge, by all classical monotone numerical schemes in the context of stochastic control theory. In particular, the paper provides a unified approach to prove the convergence of numerical schemes for non-Markovian stochastic control problems, second order BSDEs, stochastic differential games etc.

Key words. Numerical analysis, monotone schemes, viscosity solution, path-dependent PDE

1 Introduction

In their seminal work [1], Barles and Souganidis proved a convergence theorem for the monotone numerical schemes for viscosity solutions to fully nonlinear PDEs. Assuming that a strong comparison principle holds true for viscosity sub- and super-solutions of a PDE, they show that for all numerical schemes satisfying the three properties, “monotonicity”, “consistency” and “stability”, the numerical solutions converge locally uniformly to the unique viscosity solution of the PDE as the discretization parameters converge to zero. They mainly use the stability of viscosity solutions to PDEs and the local compactness of the state space. Due to their result, one only needs to check some local properties of a numerical scheme in order to get a global convergence result. Also, their result and method are widely used in the numerical analysis of viscosity solutions to PDEs.

It is well known that, by the Feynman-Kac formula, the conditional expectation of a random variable can be characterized by a viscosity solution of the corresponding parabolic linear PDE. This relationship has been generalized by the theory of backward SDE (corresponding to semi-linear PDE) and that of second-order backward SDE (corresponding to fully nonlinear PDE). However, these probabilistic tools have their PDE counterparts only in the Markovian case. Recently, a notion of viscosity solutions to path-dependent PDE (PPDE) was introduced by [10], which permits to study non-Markovian problems. In particular, it provides a unified approach for many Markovian, or non-Markovian stochastic dynamic problems, e.g. stochastic control problems, stochastic differential games, etc.

It would be interesting to extend the convergence theorem of Barles and Souganidis [1] in the context of PPDE. The main obstacle for a direct extension of their arguments is that the state space is no longer locally compact. Zhang and Zhuo [34] provided recently a formulation of the convergence theorem of monotone schemes for PPDEs. They mainly use the stability of the viscosity solution to PPDE, and overcome the difficulty of non-local compactness by an optimal stopping argument as in the wellposedness theory of PPDE. They also provide an illustrative numerical scheme which satisfies all the conditions of their convergence theorem. However, this illustrative numerical scheme is not applicable in the general case. Moreover, most of the monotone numerical schemes in the sense of Barles and Souganidis [1], for example the finite difference scheme, do not satisfy their conditions.

Our main objective is to provide a new formulation of the convergence theorem for numerical schemes of PPDE. Our conditions are slightly stronger than the classical conditions of Barles and Souganidis [1], as PPDEs degenerate to be PDEs. Nevertheless, to the best of our knowledge these conditions are satisfied by all classical monotone numerical schemes in the optimal control context, including the classical finite difference scheme, the Monte-Carlo scheme of Fahim, Touzi and Warin [14], the semi-Lagrangian scheme, the trinomial tree scheme of Guo, Zhang and Zhuo [16], the switching system scheme of Kharroubi, Langrené and Pham [20], etc. Therefore, our result extends all these numerical schemes to the path-dependent case. In particular, it provides numerical schemes for non-Markovian second order BSDEs, and stochastic differential games, which is new in the literature, see also Possamaï and Tan [25].

Similar to [34], we use an optimal stopping argument to overcome the difficulty of non-local compactness. Instead of looking into an optimal stopping problem of a controlled diffusion as in [34], we consider a discrete time optimal stopping problem of a controlled process. Therefore, our argument is quite different from that in [34].

The paper is organized as follows. In Section 2 we provide some preliminary notations used in the paper. In Section 3 we recall the definition of viscosity solution to the path-dependent PDE, and present our main result, that is, a convergence theorem of monotone schemes for PPDEs. Further we compare with the result of Guo, Zhang and Zhuo [16] and that of Barles and Souganidis [1]. In Section 4 we review some classical monotone schemes for PDEs, and verify that they satisfy the technical conditions of our main convergence theorem, and thus can be applied in the PPDE context. Finally, we complete the proof of the main theorem in Section 6.

2 Preliminaries

Throughout this paper let be a given finite maturity, the set of continuous paths starting from the origin, and . We denote by the canonical process on , the canonical filtration, the set of all -stopping times taking values in , and the Wiener measure on . Moreover, let denote the subset of taking values in , and for , let and be the subset of taking values in and , respectively.

Following Dupire [9], we introduce the following pseudo-distance on : for all ,

Let be a metric space, we say a process is in whenever is continuous. and denote the set of all -measurable random variables and -progressively measurable processes, respectively. We remark that , and when , we shall omit it in these notations. We also denote by the set of all functions bounded and uniformly continuous with respect to .

For any , , , and , define respectively the shifted set, the shifted random variable and the shifted process by

where is the concatenated path defined as

Following the standard arguments with monotone class theorem, we have the following results.

Lemma 2.1.

Let and . Then for all , for all , for all , and for all .

Next, let us introduce the nonlinear expectation. As in [12], we fix a constant throughout the paper, and denote by the collection of all continuous semimartingale measures on whose drift and diffusion coefficients are bounded by . More precisely, a probability measure if under , the canonical process is a semimartingale with natural decomposition , where is a process of finite variation, is a continuous martingale with quadratic variation , such that and are absolutely continuous in , and

| (2.1) |

We then define the nonlinear expectations:

| (2.2) |

3 Convergence of monotone schemes for PPDE

3.1 Definition of viscosity solution to PPDE

We introduce the following assumptions on a function ( is the set of all symmetric matrices).

Assumption 3.1.

The function satisfies that

-

•

is non-decreasing in ;

-

•

is continuous in all arguments.

Consider the PPDE in the following form

| (3.1) |

with the terminal condition . The path derivatives are defined as follows.

Definition 3.2.

We say that if and there exist processes valued in , and , respectively, such that:

The processes , and are called the time derivative, spacial gradient and spatial Hessian, respectively, and we denote , , .

In [10] and the following works [12, 13], the authors introduced a notion of viscosity solutions to PPDEs, by using the test functions in . Indeed, as observed in [26], one does not need to consider all test functions but only the paraboloids. For , we define the paraboloid on the real space:

| for all |

where . We also abuse a little the notation to define the corresponding ‘paraboloid’ on the path space:

Note that the path derivatives at the point of the paraboloid are clearly:

The sub- and super-jets of a function at are as follows

where .

Definition 3.3.

Let .

(i) is a -viscosity subsolution (resp. supersolution) of the path dependent PDE (3.1), if at any point it holds for all (resp. ) that

For the arguments below, we need to introduce an equivalent definition using constant localization and test functions in , i.e. the class of all scalar functions of which the partial derivatives are of compact support. Consider the set of test functions:

where we abuse the notation again, by denoting .

Proposition 3.4.

A function is a -viscosity subsolution (resp. supersolution) of Equation (3.1), if and only if at any point it holds for all (resp. ) that

| (3.2) |

We will report the proof of the above proposition in Section 6.

One of the motivations of the PPDE theory is to characterize the value functions of non-Markovian stochastic control problems.

Example 3.5.

Consider a second-order backward SDE (see e.g. Cheridito, Soner, Touzi and Victoir [5], Soner, Touzi and Zhang [30]) with generator and the controlled process with diffusion coefficient , where is some set in which the control processes take values. Then the solution of the second-order backward SDE corresponds to a viscosity solution to the PPDE with the nonlinearity:

| (3.3) |

We refer to Section 4 of Ekren, Touzi and Zhang [12] for more details. Another example is the application of PPDEs in the stochastic differential games (see e.g. Pham and Zhang [24]), where the nonlinearity of the PPDE is of the form:

| (3.4) |

3.2 Main results

For parabolic PDEs with terminal conditions of the form (3.1), the numerical schemes are usually given as a backward iteration. Let , and then given the value of , we compute the value of . More precisely, we will introduce the numerical scheme as an operator : for each and , is a function from to , then the backward iteration is given by

As illustrated by Kushner and Dupuis [21], in the context of Markovian stochastic control problem, the numerical result can be interpreted as the value function of a controlled Markov chain problem, or equivalently the numerical scheme can be treated as a discrete time nonlinear expectation. Moreover, such an interpretation implies the monotonicity condition in sense of Barles and Souganidis [1]. Inspired by this observation, we would like to introduce a discrete time version of nonlinear expectations of and , in preparation of our new formulation of the monotonicity condition in this general path-dependent context.

Definition 3.6.

Let be a sequence of independent random variables defined on a probability space , such that each follows the uniform distribution on . Let , be a subset of a metric space, be a Borel measurable function such that for all we have

| (3.5) |

Denote the filtration , where . Let . For all , we define

| (3.6) |

Further, we denote by the linear interpolation of the discrete process such that for all . Finally, for any function , we define the nonlinear expectation:

| (3.7) |

Let us now formulate the conditions on the numerical scheme .

Assumption 3.7.

(i) Consistency: for every and ,

| (3.8) |

(ii) Monotonicity: there exists a nonlinear expectation as in Definition 3.6 such that, for any we have

| (3.9) |

where is a function such that .

(iii) Stability: are uniformly bounded and uniformly continuous in , uniformly in .

Remark 3.8.

Our main result is the following convergence of the monotone scheme for PPDE (3.1).

Theorem 3.9.

Here are some remarks on our main result.

Remark 3.10.

In the case of semilinear PPDEs, i.e. the nonlinearity , a comparison result is proved in Ren, Touzi and Zhang [27] under quite general assumptions. As for viscosity solutions of fully nonlinear PPDEs, a comparison result was first proved in Ekren, Touzi and Zhang [13] for PPDE (3.1) under certain conditions. A recent improvement can be found in [28].

Remark 3.11 (Comparison with Zhang and Zhuo [34]).

Let us compare our Assumption 3.7 with that in [34]. Our condition (i) is weaker and thus easier to verify comparing to that in [34]. The essential difference is between our condition (ii) and theirs. Our condition (ii), although stated in a complicated way, is satisfied by all (to the best of our knowledge) classical monotone schemes in PDE context. We also emphasize that in [34], a convergence rate has been obtained under additional smoothness conditions on the solution of PPDE. Without smoothness conditions, a convergence rate has been obtained for HJB PDEs using Krylov’s shaking coefficient technique. However, it seems not trivial to extend this shaking coefficient technique to the path-dependent case. Nevertheless, for a class of path-dependent stochastic control problems, a convergence rate has been obtained in [8] and [32], using strong invariance principle techniques.

Comparison with Barles and Souganidis’s theorem

When a PPDE degenerates to be a PDE:

| on | (3.12) |

with the terminal condition . Note that the definition of viscosity solution to PDE is slightly different from that to PPDE recalled in Section 3.1, but under general conditions a viscosity solution to PDE (3.12) is a viscosity solution of the corresponding PPDE.

Assumption 3.12.

(i) The terminal condition is bounded continuous.

(ii) The function is continuous and is non-decreasing in .

For any and , let be an operator on the set of bounded functions defined on . For , denote , , , let the numerical solution be defined by

Assumption 3.13.

(i) Consistency: for any and any smooth function ,

(ii) Monotonicity: whenever .

(iii) Stability: is bounded uniformly in whenever is bounded.

(iv) Boundary condition: for any .

We now recall the convergence theorem of the monotone scheme, deduced from Barles and Souganidis [1] in this context of the parabolic PDE (3.12).

Theorem 3.14.

Remark 3.15 (Comparison with Assumption 3.7).

(2) Assumption 3.7 (ii) is stronger than Assumption 3.13 . However, as we mentioned at the beginning of this section, Kushner and Dupuis [21] studied the classical finite-difference scheme, and highlighted that the monotonicity condition is in fact equivalent to a controlled Markov chain interpretation, where the increments of the Markov chain satisfy (3.5). Our formulation of the monotonicity in Assumption 3.7 (ii) matches this observation. Moreover, the new monotonicity condition is satisfied by all classical monotone scheme, to the best of our knowledge, in the context of stochastic control theory. See our review in Section 4.

(3) The stability condition in Assumption 3.7 (iii) is also stronger than Assumption 3.13 . Nevertheless, in the classical numerical analysis for parabolic PDE (3.12), in order to check Assumption 3.13 , one needs (explicitly or implicitly) to prove a uniform continuity property of numerical solutions uniformly on the discretization parameter, which leads to the same condition as in Assumption 3.7 . See also our review in Section 4.

4 Examples of monotone schemes

We discuss here some classical monotone numerical schemes in the stochastic control context, and provide some sufficient conditions Assumption 3.7 to hold true. Let us first add some assumptions on the functions and for PPDE (3.1).

Assumption 4.1.

The terminal condition is Lipschitz in , is increasing in , and is Lipschitz in : i.e. there is some constant such that for all and ,

In this section, we denote for . Given a sequence of points in , we denote by the linear interpolation of such that for all . Further, for , and , we define a path

Let be some normed vector space, then for maps , we introduce the norm and by

| and |

4.1 Finite difference scheme

For simplicity, we assume that the state space is of dimension one (). Let be the space discretization size. For every , and -measurable random variable , we define the discrete derivatives

where

Then an explicit finite difference scheme is given by

| (4.2) |

Proposition 4.2.

Suppose that Assumption 4.1 holds true and is Lipschitz in , i.e. there is a constant such that for all and all ,

Assume in addition the CFL (Courant-Friedrichs-Lewy) condition, i.e.

| (4.3) |

and that for some small constant . Then Assumption 3.7 holds true for finite difference scheme (4.2). In particular, the numerical solution is –Hölder in and Lipschitz in , uniformly on .

Proof. We will check each condition in Assumption 3.7. For the simplicity of presentation, we assume that is independent of . Clearly, the argument still works if is Lipschitz in .

(i) The consistency condition (Assumption 3.7 (i)) is obviously satisfied by (4.2) as in the non-path-dependent case.

(ii) For the monotonicity in Assumption 3.7 (ii), let us consider two different bounded functions and . Denote , then by direct computation,

where , and depend on and , but are uniformly bounded by the Lipschitz constant of . Let and be two constants, and be a random variable defined on a probability space such that

The law of is well defined for small enough, because every term above is positive and the sum of all terms equals to under condition (4.3). Further, we have

| and | (4.4) |

where the last terms follows by .

Then let be the distribution function of and be the generalized inverse function of , i.e.

| (4.5) |

In view of (4.4), we may verify (3.10), and the monotonicity condition of Assumption 3.7 (ii) follows.

(iii) To prove Assumption 3.7 , we will prove that there is a constant independent of such that

| (4.6) |

Let us first prove that is Lipschtiz in . Denote

By direct computation, we have

| (4.7) |

where

with , and uniformly bounded by . Then there is a constant independent of such that

Notice that the terminal condition is Lipschitz, it follows by the discrete Gronwall inequality, we have for a constant independent of . Hence, there is a constant independent of such that

| (4.8) |

We next consider the regularity of in . Let and . Note that

By a direct computation, we have

| (4.9) |

where is a discrete process defined as ,

with be given by (4.5), and is the linear interpolation of . Define

Clearly, is a martingale and is a predictable process. Further, it follows from the property of in (4.4) that

| and |

Then by (4.9), we have

| (4.10) |

Further, by Doob’s inequality, it follows that

Finally, combining the above estimation with (4.8) and (4.10), we obtain (4.6).

Remark 4.3.

We here assume that the PPDE is non-degenerate (). When and , the scheme is still monotone. When and , it is possible to redefine the first order discrete derivative by

to obtain a monotone scheme.

Remark 4.4.

In the multidimensional case, is a matrix. If is diagonal dominated, then following Kushner and Dupuis [21, Chapter 5.3], it is easy to construct a monotone scheme under similar CFL condition (4.3). When is not diagonal dominated, it is possible to use the generalized finite difference scheme proposed by Bonnans, Ottenwaelter and Zidani [2].

4.2 The trinomial tree scheme of Guo-Zhang-Zhuo [16]

We consider the PPDE of the form (3.1). Let be some symmetric matrix, denote

Let a random vector defined on a probability space such that are i.i.d and

For every -measurable function , let us define with

where for any matrix , denotes the diagonal matrix whose -th component is . Then the numerical scheme is defined as

| (4.11) |

Proposition 4.5.

Proof. The consistency and monotonicity condition in Assumption 3.7 (i) and (ii) can be justified by almost the same argument as in [16]. Similarly to the finite difference scheme, the monotonicity in sense of Barles and Souganidis [1] implies the interpretation of the controlled discrete processes of the numerical scheme, which implies the monotonicity condition (3.10) in our context. Further, using the same argument as in Proposition 4.2, it is easy to show that

for some constant independent of , which implies in particular (iii) of Assumption 3.7.

4.3 The probabilistic scheme of Fahim-Touzi-Warin [14]

We consider PPDE (3.1) in which is in the form of

Before introducing the numerical scheme, we first define a random vector

where is a Gaussian vector. For every bounded function , we define

where with

Then the probabilistic scheme is given by

| (4.12) |

Remark 4.7.

The probabilistic scheme in [14] is inspired by the second order BSDE theory of Cheridito, Soner, Touzi and Victoir [5], and extends the classical numerical scheme of BSDE (see e.g. Bouchard and Touzi [3], Zhang [33]). In practice, one can use the simulation-regression method to estimate the conditional expectation in the above scheme (see e.g. Gobet, Lemor and Warin [15]). We refer to Guyon and Henry-Labordère [17] for more details on the use of the scheme, to Tan [31] for an extension to a degenerate case, and to Tan [32] for an extension to path-dependent control problems.

Assumption 4.8.

(i) The nonlinearity is Lipschtiz w.r.t. uniformly in and .

(ii) is elliptic and dominated by the diffusion term of , that is,

| on | (4.13) |

(iii) and .

(iv) and is invertible and is bounded Lipschitz.

Proposition 4.9.

(ii) Further, using probabilistic interpretation of this scheme in Tan [32, Section 3.2], we may verify (ii) of Assumption 3.7. See also the estimation given by Lemma 3.1 of [32].

(iii) For (iii) of Assumption 3.7, we shall prove that the numerical solution is Lipschitz in and -Hölder in . In [14], the authors proved this property in the case of PDEs. Their arguments for the Lipschitz continuity in can be easily adapted to this path-dependent case. For the regularity of in , they used a regularization technique, which seems impossible to be adapted to the path-dependent case. However, we can still use similar arguments as in Proposition 4.2, i.e. use the discrete-time controlled semimartingale interpretation, to prove the Hölder property of in .

4.4 The semi-Lagrangian scheme

For the semi-Lagrangian scheme, we shall consider the PPDE (3.1) of the Bellman-Issac type, i.e. the function is in the form of

where and are some sets, are functionals defined on .

Let be a random vector satisfying

| and | (4.14) |

Then the semi-Lagrangian scheme is defined as

| (4.15) | |||||

Proposition 4.11.

Proof. (i) The consistency condition (Assumption 3.7 (i)) is easy to check.

(ii) Let be a set, be an arbitrary mapping, and be two bounded functions. Note that

| (4.16) |

Notice that is isomorphic to , we can always consider the random vector as a one-dimensional random variable. By consider the inverse function of its distribution function, then there is a family such that in law with , for all . Then it follows from (4.16) that the monotonicity condition in Assumption 3.7 (ii) holds true with and .

(iii) Finally, by the same arguments as in Proposition 4.2, we can easily deduce that is Lipschitz in and -Hölder in , uniformly on , and hence complete the proof for the stability condition in Assumption 3.7.

Remark 4.12.

Solutions of path dependent Bellman-Issac equations can characterize value functions of stochastic differential games (see e.g. Pham and Zhang [24]).

Remark 4.13.

(i) For Bellman-Issac PDE, Debrabant and Jakobsen [6] studied the semi-Lagrangian scheme with a random variable following a discrete distribution, together with an interpolation technique for the implementation.

(ii) For Bellman equation (PDE), Kharroubi, Langrené and Pham [20] propose a semi-Lagrangian type numerical scheme with , and provide a simulation-regression technique for the implementation. It is worth of mentioning that [20] provides a convergence rate for the scheme, while we only prove in this paper a general convergence theorem as in Barles and Souganidis [1].

5 Numerical examples

We will provide two toy examples of numerical implementation in low-dimensional case. Notice also that the main focus of the paper is on a general convergence theorem for numerical analysis of non-Markovian control problems, and we will not propose any new numerical schemes. For more numerical examples (in high-dimensional case) of difference numerical schemes, we would like to refer to [14, 16, 17, 20, 31], etc.

In our two toy examples, we implement the finite difference scheme in Section 4.1 and the probabilistic scheme in Section 4.3. In this low dimensional case, the finite difference scheme is quite easy to be implemented given some boundary conditions. For the probabilistic scheme, we do not need the boundary conditions, but need a simulation-regression technique (as studied in Gobet, Lemor and Warin [15]) to estimate the conditional expectations appearing in the scheme. More concretely, we will use the local polynomial functions as regression basis, as introduced by Bouchard and Warin [4].

A first numerical example

For a first numerical example, we consider the PPDE

| (5.1) |

where , , and are two functions. In this case, the value function dependents only on , so that the numerical solution can be written as .

The above PPDE (5.1) is motivated by a stochastic differential game:

where is controlled diffusion such that

and (see e.g. Pham and Zhang [24] for more details).

We choose the terminal condition and the function

so that the solution to PPDE (5.1) is given explicitly by , which serves as a reference value for the numerical examples (this idea is borrowed from Guo, Zhang and Zhuo [16]). For finite difference scheme, we use as boundary conditions since it is the exact solution of the PPDE. For the probabilistic scheme, we simulate paths of a diffusion process on discrete time grids. The diffusion process is defined by , with a Brownian motion , and also denote . Then for regression function basis, we use the local polynomial of order 2 (as introduced in [4]), i.e. on each local hypercube. To define the local hypercube, we will find the minimum and maximum of as well as of all simulations, and then divide uniformly the domain into small hypercubes.

A second numerical example

The second example of PPDE we considered is given by

| (5.2) | |||

which is taken from Matoussi, Possamaï and Zhou [22]. The above equation is motivated by solving a robust utility maximization problem using 2BSDE, which can be instead characterized by a PPDE (see e.g. (3.3)).

We consider the terminal condition

Then the solution to PPDE (5.2) can also be characterized by the PDE, by adding an associated variable ,

| (5.3) | |||

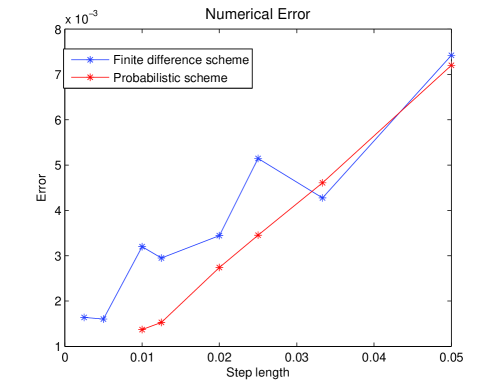

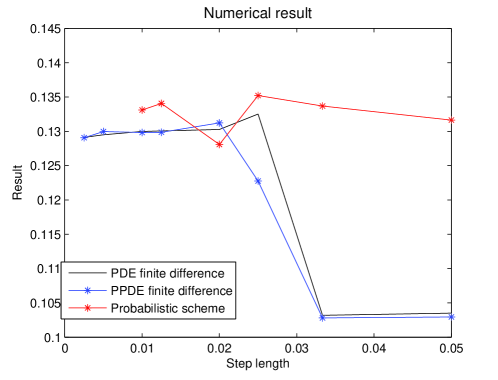

We implemented the finite difference scheme (Section 4.1) and the probabilistic scheme (Section 4.3) for PPDE (5.2). As reference, we implemented the classical finite difference scheme of PDE (5.3). Here for the finite difference scheme, we fixe the computation domain as , and use a fictive Neumann boundary conditions for and a fictive Dirichlet boundary conditions and . For the probabilistic scheme, we use the same simulation-regression techniques as previous PPDE to estimate the conditional expectations appearing in the scheme. We also notice that the generator in PPDE (5.2) is in fact not Lipschitz but quadratic in , however, the convergence of the numerical solutions can be still observed, see Figure 2.

6 Proofs

6.1 Preliminary results

In preparation of the proof of Theorem 3.9, we prove the following lemmas.

Lemma 6.1 (Fatou’s Lemma).

Assume that the random variables are uniformly bounded. Then we have

Proof. In order to prove Fatou’s lemma, it is enough to show the monotone convergence theorem, i.e. given a sequence of increasing random variables, we have

| (6.1) |

Since for each , it follows from Theorem 31 in [7] that (6.1) holds true.

Recall the nonlinear expectation defined in (3.7).

Lemma 6.2.

Let be bounded uniformly continuous. Then there exists a modulus of continuity which depends only on the moduli of continuity of and , such that

Proof. Denote as a continuity modulus of . Let and be defined by (3.6) and its linear interpolation on . Then under the condition (3.5), it follows from Lemma 4.8 of Tan [32] (see also Dolinsky [8]) that we can construct a process and another process in the same probability space , such that the image measure of lies in , and for some constant independent of ,

Let , then it follows that

which concludes the proof by the arbitrariness of .

Lemma 6.3.

Let be lower semicontinuous and bounded from below, then it holds for all that

In particular, by defining for some , we have

Proof. Define the approximation for the function :

Clearly, for each , function is Lipschitz continuous, and . By Lemma 6.2, we obtain that

Since , by Fatou’s lemma we have

Therefore

| (6.2) |

Then we easily get the symmetric result for upper semicontinuous function , i.e.

To conclude, it remains to prove that the function is upper semicontinuous. Note that

Since the function is continuous, the set is closed. Consequently, the function is upper semicontinuous.

Lemma 6.4.

For any and , define and . Then, for small enough we have

| (6.3) |

Proof. Note that

By the definition of above (2.1), for all , the canonical process admits the canonical decomposition , where is a finite variation process and is a -martingale. Moreover, for each ,

Further, by the time-change for martingales (see e.g. Theorem 4.6 on page 174 of [19]), there is a scalar Brownian motion defined on a probability space such that

Since when is small enough, we have

We then conclude that .

6.2 Proof of Proposition 3.4

We only discuss the case of subsolution. The result about the supersolution follows similarly.

1. We first prove the only if part. Let and with a localizing time . Clearly, there is a function such that on the set , where is defined as in Lemma 6.4. Thus,

where with be defined as in Lemma 6.4. We have

| (6.4) |

For the second term on the right hand side of (6.4), we have

Take . By Lemma 6.4, there is a constant such that for all we have . Then it follows from (6.4) that

We next consider the optimal stopping problem:

According to Ekren, Touzi and Zhang [11], is an optimal stopping rule. Suppose that we always have . Then we obtain that

However, this is in contradiction with the optimality of . Therefore, there is such that and

So we have

By letting and then , we obtain

Finally, since , this provides that .

2. For the if part, one may apply the same argument as in Proposition 3.11 in [26]. For completeness, we provide the full argument. Let and with a localizing time . Without loss of generality, we assume that and . Denote

| (6.5) |

For any , since is smooth, by otherwise choosing a stopping time we may assume

Denote . Then, for all ,

where the last inequality is due to the Itô’s formula. Note that, for any , we have

By the arbitrariness of , we see that

That is, . Since is a -viscosity subsolution, it follows that

Let , then the desired result follows.

6.3 Proof of Theorem 3.9

We first introduce two functions:

| (6.6) |

Note that inherit the uniform modulus of continuity of , so . It is also clear that and . Then it is enough to prove that is a -viscosity supersolution and is a -viscosity subsolution, so that by the comparison principle we may obtain , to conclude the proof of Theorem 3.9.

Proposition 6.5.

The functions and defined in (6.6) are -viscosity supersolution and subsolution, respectively.

Proof. We only prove the result for . The corresponding result for can be proved similarly.

1. Without loss of generality, we only verify the viscosity supersolution property at the point . Let function , and by adding a constant to , we assume that , so that

| (6.7) |

Assume that and are both bounded by a constant . Take a subsequence still named as such that . Now fix a constant , and denote . By Lemma 6.4, there is a constant such that for all , we have

| (6.8) |

Since is uniformly continuous uniformly in , by considering small enough we may assume that on , where . It follows from (6.7) that

| (6.9) |

It follows from (iii) of Assumption 3.7 that is uniformly bounded and uniformly continuous uniformly in . By Lemma 6.1 and 6.2, we obtain that

It follows from (6.8) and (6.3) that for sufficiently small we have

| (6.11) |

Then by the optimal stopping argument in Step 2, we may find such that

| (6.12) |

where and is the collection of all processes defined by for some -measurable functions taking value in . In particular, (6.3) implies that

| (6.13) |

Since , we have , and thus

So it follows from (6.13) that

By (ii) of Assumption 3.7, we obtain

Since , it follows that

Since , we have as , and note that

| (6.15) |

where is the common modulus of continuity of the functions . Further, by (6.3) and (6.15), it follows from (i) of Assumption 3.7

Finally, we conclude the proof by letting and then .

2. We now complete the proof of the claim (6.3). Consider the mixed control and optimal stopping problem in finite discrete-time:

| (6.16) |

By standard argument, we have

It remains to prove that there exists such that

| (6.17) |

Recall that on for small enough. Then since , we have

| (6.18) | |||||

On the other hand, we obtain from Lemma 6.3 that for small enough it holds

| (6.19) |

It follows from (6.18) and (6.19) that

Further, it follows from (6.8) that . Therefore,

| (6.20) |

Suppose that contrary to (6.17) we have

| (6.21) |

Note that

| (6.22) |

It follows from (6.8) and (6.19) that

On the other hand, we have

| (6.24) | |||||

where are moduli of continuity of function , , and are chosen to be bounded and continuous. Again by Lemma 6.3, we have for sufficiently small that

| (6.25) | |||||

It follows from (6.24), (6.25) and that

| (6.26) |

Plugging the estimates of (6.3) and (6.26) into (6.22), we obtain

| (6.27) |

Finally, by (6.11), (6.20) and (6.27) we have

which contradicts the definition of in (6.16). Therefore, (6.21) is wrong. The proof is complete.

7 Conclusion

We provide a convergence theorem of monotone numerical schemes for a class of parabolic PPDE, which generalizes the classical convergence theorem of Barles and Souganidis [1]. In contrast to the formulation of [34], our conditions are satisfied by all classical monotone numerical scheme for PDEs, to the best of our knowledge. Moreover, our results permit to deduce some numerical schemes for path-dependent stochastic differential game problems and the second order BSDEs whose generator depends on (see (3.3), (3.4)), which are new in literatures.

Other numerical schemes, such as the branching process scheme of Henry-Labordère, Tan and Touzi [18], are possible for some PPDE, but it is not analyzed by the monotone scheme arguments.

References

- [1] G. Barles and P.E. Souganidis, Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Analysis 4:271-283, 1991.

- [2] J.F. Bonnans, E. Ottenwaelter and H. Zidani, A fast algorithm for the two dimensional HJB equation of stochastic control, M2AN Math. Model. Numer. Anal., 38(4):723–735, 2004.

- [3] B. Bouchard and N. Touzi, Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations, Stochastic Process. Appl., 111(2):175-206, 2004.

- [4] B. Bouchard and X. Warin, Monte-Carlo valorisation of American options: facts and new algorithms to improve existing methods, Numerical Methods in Finance , Springer Proceedings in Mathematics, ed. R. Carmona, P. Del Moral, P. Hu and N. Oudjane , 2011.

- [5] P. Cheridito, H.M. Soner, N. Touzi, and N. Victoir, Second-order backward stochastic differential equations and fully nonlinear parabolic PDEs, Comm. Pure Appl. Math., 60(7):1081-1110, 2007.

- [6] K. Debrabant and E.R. Jakobsen, Semi-Lagrangian schemes for linear and fully nonlinear diffusion equations, Math. Comp. 82:1433-1462, 2013.

- [7] L. Denis, M. Hu and S. Peng, Function spaces and capacity related to a Sublinear Expectation: application to G-Brownian Motion Paths, Potential Analysis, 34(2):139-161, 2011.

- [8] Y. Dolinsky, Numerical Schemes for G–Expectations, Electronic Journal of Probability, 17(1):1-15, 2012.

- [9] B. Dupire, Functional Itô calculus, ssrn, 2009, http://ssrn.com/abstract=1435551.

- [10] I. Ekren, C. Keller, N. Touzi and J. Zhang, On Viscosity Solutions of Path Dependent PDEs, Annals of Probability, Volume 42, Number 1, 204-236.

- [11] I. Ekren, N. Touzi and J. Zhang, Optimal Stopping under Nonlinear Expectation, Stochastic processes and their applications, 100, 397-453.

- [12] I. Ekren, N. Touzi and J. Zhang, Viscosity Solutions of Fully Nonlinear Path Dependent PDEs: Part I, Annals of probability, to appear.

- [13] I. Ekren, N. Touzi and J. Zhang, Viscosity Solutions of Fully Nonlinear Path Dependent PDEs: Part II, Annals of probability, to appear.

- [14] A. Fahim, N. Touzi and X. Warin, A probabilistic numerical method for fully nonlinear parabolic PDEs, Ann. Appl. Probab. Volume 21, Number 4, 1322-1364, 2011.

- [15] E. Gobet, J.P. Lemor, and X. Warin, A regression-based Monte-Carlo method to solve backward stochastic differential equations, Ann. Appl. Probab., 15(3):2172-2202, 2005.

- [16] W. Guo, J. Zhang and J. Zhuo, A Monotone Scheme for High Dimensional Fully Nonlinear PDEs, Annals of Applied Probability, to appear.

- [17] J. Guyon and P. Henry-Labordère, Uncertain Volatility Model: A Monte-Carlo Approach, Journal of Computational Finance, 14(3), 2011.

- [18] P. Henry-Labordère, X. Tan and N. Touzi, A numerical algorithm for a class of BSDE via branching process, Stochastic Processes and their Applications, 124:1112-1140, 2014.

- [19] I. Karatzas and S.E. Shreve, Brownian motion and stochastic calculus, second edition, Springer, 1991.

- [20] I. Kharroubi, N. Langrené and H. Pham, Discrete time approximation of fully nonlinear HJB equations via BSDEs with nonpositive jumps, Annals of Applied Probability, to appear.

- [21] H.J. Kushner and P. Dupuis, Numerical methods for stochastic control problems in continuous time, Vol 24 of Applications of Mathematics, Springer-Verlag, 1992.

- [22] A. Matoussi, D. Possamaï, and C. Zhou Robust utility maximization in non-dominated models with 2BSDE: the uncertain volatility model, Mathematical Finance, to appear.

- [23] S. Peng, G-Expectation, G-Brownian motion, and related stochastic calculus of Itô type, Stochastic Analysis and Applications, volume 2 of Abel Symp., Springer Berlin, 541-567, 2007.

- [24] T. Pham and J. Zhang, Two Person Zero-sum Game in Weak Formulation and Path Dependent Bellman-Isaacs Equation, SIAM Journal of Control and Optimization, 52, 2090-2121, 2014.

- [25] D. Possamai and X. Tan, Weak approximation of second order BSDEs, Annals of Applied Probability, to appear.

- [26] Z. Ren, N. Touzi and J. Zhang, An Overview of Viscosity Solutions of Path Dependent PDEs, Stochastic Analysis and Applications, to appear.

- [27] Z. Ren, N. Touzi and J. Zhang, Comparison of Viscosity Solutions of Semi-linear Path-Dependent PDEs, preprint

- [28] Z. Ren, N. Touzi and J. Zhang, Comparison of viscosity solutions of fully nonlinear degenerate parabolic Path-dependent PDEs, preprint.

- [29] A.I. Sakhanenko, A new way to obtain estimates in the invariance principle, High Dimensional Probability II, 221-243, 2000.

- [30] H.M. Soner, N. Touzi and J. Zhang, Wellposedness of second order backward SDEs, Probability Theory and Related Fields, 153(1-2):149-190, 2012.

- [31] X. Tan, A splitting method for fully nonlinear degenerate parabolic PDEs, Electron. J. Probab. 18(15):1-24, 2013.

- [32] X. Tan, Discrete-time probabilistic approximation of path-dependent stochastic control problems, Annals of Applied Probability, 24(5):1803-1834, 2014.

- [33] J. Zhang, A numerical scheme for backward stochastic differential equations, Annals of Applied Probability, 14(1), 459-488, 2004.

- [34] J. Zhang and J. Zhuo, Monotone schemes for fully nonlinear parabolic path dependent PDEs, Journal of Financial Engineering, 1, 2014.