Structured Matrix Completion with Applications to Genomic Data Integration1

Abstract

Matrix completion has attracted significant recent attention in many fields including statistics, applied mathematics and electrical engineering. Current literature on matrix completion focuses primarily on independent sampling models under which the individual observed entries are sampled independently. Motivated by applications in genomic data integration, we propose a new framework of structured matrix completion (SMC) to treat structured missingness by design. Specifically, our proposed method aims at efficient matrix recovery when a subset of the rows and columns of an approximately low-rank matrix are observed. We provide theoretical justification for the proposed SMC method and derive lower bound for the estimation errors, which together establish the optimal rate of recovery over certain classes of approximately low-rank matrices. Simulation studies show that the method performs well in finite sample under a variety of configurations. The method is applied to integrate several ovarian cancer genomic studies with different extent of genomic measurements, which enables us to construct more accurate prediction rules for ovarian cancer survival.

Abstract

In this supplement we provide additional simulation results and the proofs of the main theorems. Some key technical tools used in the proofs of the main results are also developed and proved.

Keywords: Constrained minimization, genomic data integration, low-rank matrix, matrix completion, singular value decomposition, structured matrix completion.

1 Introduction

Motivated by an array of applications, matrix completion has attracted significant recent attention in different fields including statistics, applied mathematics and electrical engineering. The central goal of matrix completion is to recover a high-dimensional low-rank matrix based on a subset of its entries. Applications include recommender systems (Koren et al., 2009), genomics (Chi et al., 2013), multi-task learning (Argyriou et al., 2008), sensor localization (Biswas et al., 2006; Singer and Cucuringu, 2010), and computer vision (Chen and Suter, 2004; Tomasi and Kanade, 1992), among many others.

Matrix completion has been well studied under the uniform sampling model, where observed entries are assumed to be sampled uniformly at random. The best known approach is perhaps the constrained nuclear norm minimization (NNM), which has been shown to yield near-optimal results when the sampling distribution of the observed entries is uniform (Candès and Recht, 2009; Candès and Tao, 2010; Gross, 2011; Recht, 2011; Candes and Plan, 2011). For estimating approximately low-rank matrices from uniformly sampled noisy observations, several penalized or constrained NNM estimators, which are based on the same principle as the well-known Lasso and Dantzig selector for sparse signal recovery, were proposed and analyzed (Keshavan et al., 2010; Mazumder et al., 2010; Koltchinskii, 2011; Koltchinskii et al., 2011; Rohde et al., 2011). In many applications, the entries are sampled independently but not uniformly. In such a setting, Salakhutdinov and Srebro (2010) showed that the standard NNM methods do not perform well, and proposed a weighted NNM method, which depends on the true sampling distribution. In the case of unknown sampling distribution, Foygel et al. (2011) introduced an empirically-weighted NNM method. Cai and Zhou (2013) studied a max-norm constrained minimization method for the recovery of a low-rank matrix based on the noisy observations under the non-uniform sampling model. It was shown that the max-norm constrained least squares estimator is rate-optimal under the Frobenius norm loss and yields a more stable approximate recovery guarantee with respect to the sampling distributions.

The focus of matrix completion has so far been on the recovery of a low-rank matrix based on independently sampled entries. Motivated by applications in genomic data integration, we introduce in this paper a new framework of matrix completion called structured matrix completion (SMC), where a subset of the rows and a subset of the columns of an approximately low-rank matrix are observed and the goal is to reconstruct the whole matrix based on the observed rows and columns. We first discuss the genomic data integration problem before introducing the SMC model.

1.1 Genomic Data Integration

When analyzing genome-wide studies (GWS) of association, expression profiling or methylation, ensuring adequate power of the analysis is one of the most crucial goals due to the high dimensionality of the genomic markers under consideration. Because of cost constraints, GWS typically have small to moderate sample sizes and hence limited power. One approach to increase the power is to integrate information from multiple GWS of the same phenotype. However, some practical complications may hamper the feasibility of such integrative analysis. Different GWS often involve different platforms with distinct genomic coverage. For example, whole genome next generation sequencing (NGS) studies would provide mutation information on all loci while older technologies for genome-wide association studies (GWAS) would only provide information on a small subset of loci. In some settings, certain studies may provide a wider range of genomic data than others. For example, one study may provide extensive genomic measurements including gene expression, miRNA and DNA methylation while other studies may only measure gene expression.

To perform integrative analysis of studies with different extent of genomic measurements, the naive complete observation only approach may suffer from low power. For the GWAS setting with a small fraction of loci missing, many imputation methods have been proposed in recent years to improve the power of the studies. Examples of useful methods include haplotype reconstruction, -nearest neighbor, regression and singular value decomposition methods (Scheet and Stephens, 2006; Li and Abecasis, 2006; Browning and Browning, 2009; Troyanskaya et al., 2001; Kim et al., 2005; Wang et al., 2006). Many of the haplotype phasing methods are considered to be highly effective in recovering missing genotype information (Yu and Schaid, 2007). These methods, while useful, are often computationally intensive. In addition, when one study has a much denser coverage than the other, the fraction of missingness could be high and an exceedingly large number of observation would need to be imputed. It is unclear whether it is statistically or computationally feasible to extend these methods to such settings. Moreover, haplotype based methods cannot be extended to incorporate other types of genomic data such as gene expression and miRNA data.

When integrating multiple studies with different extent of genomic measurements, the observed data can be viewed as complete rows and columns of a large matrix and the missing components can be arranged as a submatrix of . As such, the missingness in is structured by design. In this paper, we propose a novel SMC method for imputing the missing submatrix of . As shown in Section 5, by imputing the missing miRNA measurements and constructing prediction rules based on the imputed data, it is possible to significantly improve the prediction performance.

1.2 Structured Matrix Completion Model

Motivated by the applications mentioned above, this paper considers SMC where a subset of rows and columns are observed. Specifically, we observe rows and columns of a matrix and the goal is to recover the whole matrix. Since the singular values are invariant under row/column permutations, it can be assumed without loss of generality that we observe the first rows and columns of which can be written in a block form:

| (1) |

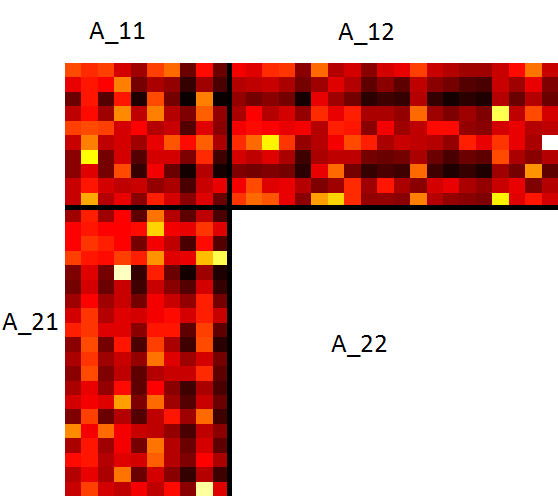

where , , and are observed and the goal is to recover the missing block . See Figure 1(a) in Section 2 for a graphical display of the data. Clearly there is no way to recover if is an arbitrary matrix. However, in many applications such as genomic data integration discussed earlier, is approximately low-rank, which makes it possible to recover with accuracy. In this paper, we introduce a method based on the singular value decomposition (SVD) for the recovery of when is approximately low-rank.

It is important to note that the observations here are much more “structured” comparing to the previous settings of matrix completion. As the observed entries are in full rows or full columns, the existing methods based on NNM are not suitable. As mentioned earlier, constrained NNM methods have been widely used in matrix completion problems based on independently observed entries. However, for the problem considered in the present paper, these methods do not utilize the structure of the observations and do not guarantee precise recovery even for exactly low-rank matrix (See Remark 1 in Section 2). Numerical results in Section 4 show that NNM methods do not perform well in SMC.

In this paper we propose a new SMC method that can be easily implemented by a fast algorithm which only involves basic matrix operations and the SVD. The main idea of our recovery procedure is based on the Schur Complement. In the ideal case when is exactly low rank, the Schur complement of the missing block, , is zero and thus can be used to recover exactly. When is approximately low rank, cannot be used directly to estimate . For this case, we transform the observed blocks using SVD; remove some unimportant rows and columns based on thresholding rules; and subsequently apply a similar procedure to recover .

Both its theoretical and numerical properties are studied. It is shown that the estimator recovers low-rank matrices accurately and is robust against small perturbations. A lower bound result shows that the estimator is rate optimal for a class of approximately low-rank matrices. Although it is required for the theoretical analysis that there is a significant gap between the singular values of the true low-rank matrix and those of the perturbation, simulation results indicate that this gap is not really necessary in practice and the estimator recovers accurately whenever the singular values of decay sufficiently fast.

1.3 Organization of the Paper

The rest of the paper is organized as follows. In Section 2, we introduce in detail the proposed SMC methods when is exactly or approximately low-rank. The theoretical properties of the estimators are analyzed in Section 3. Both upper and lower bounds for the recovery accuracy under the Schatten- norm loss are established. Simulation results are shown in Section 4 to investigate the numerical performance of the proposed methods. A real data application to genomic data integration is given in Section 5. Section 6 discusses a few practical issues related to real data applications. For reasons of space, the proofs of the main results and additional simulation results are given in the supplement (Cai et al., 2014). Some key technical tools used in the proofs of the main theorems are also developed and proved in the supplement.

2 Structured Matrix Completion: Methodology

In this section, we propose procedures to recover the submatrix based on the observed blocks , , and . We begin with basic notation and definitions that will be used in the rest of the paper.

For a matrix , we use to represent its sub-matrix with row indices and column indices . We also use the Matlab syntax to represent index sets. Specifically for integers , “” represents ; and “:” alone represents the entire index set. Therefore, stands for the first columns of while stands for the rows of . For the matrix given in (1), we use the notation and to denote and , respectively. For a matrix , let be the SVD, where with being the singular values of in decreasing order. The smallest singular value , which will be denoted by , plays an important role in our analysis. We also define and . For , the Schatten- norm is defined to be the vector -norm of the singular values of , i.e. . Three special cases are of particular interest: when , is the nuclear (or trace) norm of and will be denoted as ; when , is the Frobenius norm of and will be denoted as ; when , is the spectral norm of that we simply denote as . For any matrix , we use to denote the projection operator onto the column space of . Throughout, we assume that is approximately rank in that for some integer , there is a significant gap between and and the tail is small. The gap assumption enables us to provide a theoretical upper bound on the accuracy of the estimator, while it is not necessary in practice (see Section 4 for more details).

2.1 Exact Low-rank Matrix Recovery

We begin with the relatively easy case where is exactly of rank . In this case, a simple analysis indicates that can be perfectly recovered as shown in the following proposition.

Proposition 1

Suppose is of rank , the SVD of is , where and . If

then and is exactly given by

| (2) |

Remark 1

Under the same conditions as Proposition 1, the NNM

| (3) |

fails to guarantee the exact recovery of . Consider the case where is a matrix with all entries being 1. Suppose we observe arbitrary rows and columns, the NNM would yield with all entries being (See Lemma 4 in the Supplement). Hence when , i.e., when the size of the observed blocks are much smaller than that of , the NNM fails to recover exactly the missing block . See also the numerical comparison in Section 4. The NNM (3) also fails to recover with high probability in a random matrix setting where with and being i.i.d. standard Gaussian matrices. See Lemma 3 in the Supplement for further details. In addition to (3), other variations of NNM have been proposed in the literature, including penalized NNM (Toh and Yun, 2010; Mazumder et al., 2010),

| (4) |

and constrained NNM with relaxation (Cai et al., 2010),

| (5) |

where and is the tunning parameter. However, these NNM methods may not be suitable for SMC especially when only a small number of rows and columns are observed. In particular, when , is well spread in each block , we have , . Thus,

In the other words, imputing with all zero yields a much smaller nuclear norm than imputing with the true and hence NNM methods would generally fail to recover under such settings.

Proposition 1 shows that, when is exactly low-rank, can be recovered precisely by . Unfortunately, this result heavily relies on the exactly low-rank assumption that cannot be directly used for approximately low-rank matrices. In fact, even with a small perturbation to , the inverse of makes the formula unstable, which may lead to the failure of recovery. In practice, is often not exactly low rank but approximately low rank. Thus for the rest of the paper, we focus on the latter setting.

2.2 Approximate Low-rank Matrix Recovery

Let be the SVD of an approximately low rank matrix and partition and into blocks as

| (6) |

Then can be decomposed as where is of rank with the largest singular values of and is general but with small singular values. Then

| (7) |

Here and in the sequel, we use the notation and to denote and , respectively. Thus, can be viewed as a rank- approximation to and obviously

We will use the observed , and to obtain estimates of , and and subsequently recover using an estimated .

When is known, i.e., we know where the gap is located in the singular values of , a simple procedure can be implemented to estimate as described in Algorithm 1 below by estimating and using the principal components of and .

| (8) |

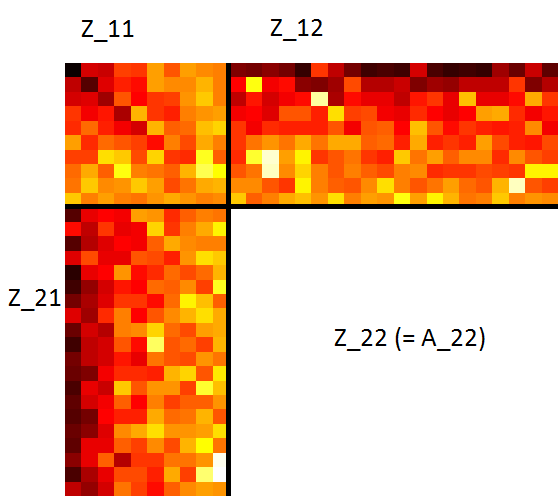

However, Algorithm 1 has several major limitations. First, it relies on a given which is typically unknown in practice. Second, the algorithm need to calculate the matrix divisions, which may cause serious precision issues when the matrix is near-singular or the rank is mis-specified. To overcome these difficulties, we propose another Algorithm which essentially first estimates with and then apply Algorithm 1 to recover . Before introducing the algorithm of recovery without knowing , it is helpful to illustrate the idea with heat maps in Figures 1 and 2.

Our procedure has three steps.

-

1.

First, we move the significant factors of and to the front by rotating the columns of and the rows of based on the SVD,

After the transformation, we have ,

Clearly and have the same singular values since the transformation is orthogonal. As shown in Figure 1(b), the amplitudes of the columns of and the rows of are decaying.

-

2.

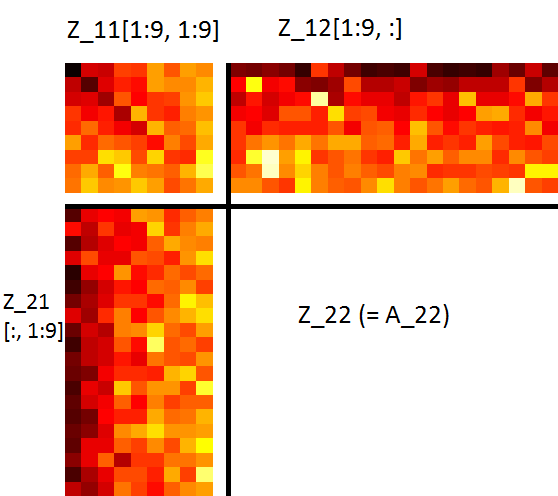

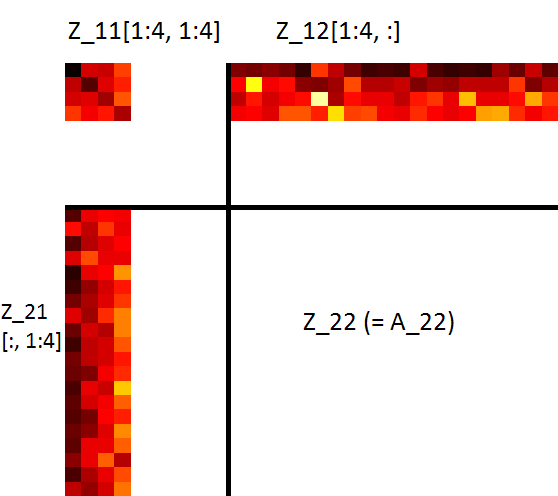

When is exactly of rank , the rows and columns of are zero. Due to the small perturbation term , the back columns of and rows of are small but non-zero. In order to recover , the best rank approximation to , a natural idea is to first delete these back rows of and columns of , i.e. the rows and columns of .

However, since is unknown, it is unclear how many back rows and columns should be removed. It will be helpful to have an estimate for , , and then use , and to recover . It will be shown that a good choice of would satisfy that is non-singular and , where is some constant to be specified later. Our final estimator for would be the largest that satisfies this condition, which can be identified recursively from to 1 (See Figure 2).

-

3.

Finally, similar to (2), can be estimated by

(9)

The method we propose can be summarized as the following algorithm.

It can also be seen from Algorithm 2 that the estimator is constructed based on either the row thresholding rule or the column thresholding rule . Discussions on the choice between and are given in the next section. Let us focus for now on the row thresholding based on . It is important to note that and approximate and , respectively. The idea behind the proposed is that when , and are nearly singular and hence may either be deemed singular or with unbounded norm. When , is non-singular with bounded by some constant, as we show in Theorem 2. Thus, we estimate as the largest such that is non-singular with .

3 Theoretical Analysis

In this section, we investigate the theoretical properties of the algorithms introduced in Section 2. Upper bounds for the estimation errors of Algorithms 1 and 2 are presented in Theorems 1 and 2, respectively, and the lower-bound results are given in Theorem 3. These bounds together establish the optimal rate of recovery over certain classes of approximately low-rank matrices. The choices of tuning parameters and are discussed in Corollaries 1 and 2.

Theorem 1

Suppose is given by the procedure of Algorithm 1. Assume

| (10) |

Then for any ,

| (11) |

Remark 2

It is helpful to explain intuitively why Condition (10) is needed. When is approximately low-rank, the dominant low-rank component of , , serves as a good approximation to , while the residual is “small”. The goal is to recover well. Among the three observed blocks, is the most important and it is necessary to have dominating in . Note that ,

We thus require Condition (10) in Theorem 1 for the theoretical analysis.

Theorem 1 gives an upper bound for the estimation accuracy of Algorithm 1 under the assumption that there is a significant gap between and for some known . It is noteworthy that there are possibly multiple values of that satisfy Condition (10). In such a case, the bound (11) applies to all such and the largest yields the strongest result.

We now turn to Algorithm 2, where the knowledge of is not assumed. Theorem 2 below shows that for properly chosen or , Algorithm 2 can lead to accurate recovery of .

Theorem 2

Assume that there exists such that

| (12) |

Let and be two constants satisfying

Then for , given by Algorithm 2 satisfies

| (13) | ||||

| or |

when is estimated based on the thresholding rule or , respectively.

Besides and , Theorems 1 and 2 involve and , two important quantities that reflect how much the low-rank matrix is concentrated on the first rows and columns. We should note that and depend on the singular vectors of and and are the singular values of . The lower bound in Theorem 3 below indicates that , , and the singular values of together quantify the difficulty of the problem: recovery of gets harder as and become smaller or the singular values become larger. Define the class of approximately rank- matrices by

| (14) |

Theorem 3 (Lower Bound)

Suppose and , then for all ,

| (15) |

Remark 3

Since and are determined by the SVD of and and are unknown based only on and , it is thus not straightforward to choose the tuning parameters and in a principled way. Theorem 2 also does not provide information on the choice between row and column thresholding. Such a choice generally depends on the problem setting. We consider below two settings where either the row/columns of are randomly sampled or is itself a random low-rank matrix. In such settings, when is approximately rank and at least number of rows and columns are observed, Algorithm 2 gives accurate recovery of with fully specified tuning parameter. We first consider in Corollary 1 a fixed matrix with the observed rows and columns selected uniformly randomly.

Corollary 1 (Random Rows/Columns)

Let be the SVD of . Set

| (17) |

Let and be respectively the index set of the observed rows and columns. Then can be decomposed as

| (18) |

-

1.

Let and be independently and uniformly selected from and with or without replacement, respectively. Suppose there exists such that

and the number of rows and number of columns we observed satisfy

Algorithm 2 with either column thresholding with the break condition where or row thresholding with the break condition where satisfies, for all ,

-

2.

If is uniformly randomly selected from with or without replacement ( is not necessarily random), and there exists such that

and the number of observed rows satisfies

(19) then Algorithm 2 with the break condition where satisfies, for all ,

-

3.

Similarly, if is uniformly randomly selected from with or without replacement ( is not necessarily random) and there exists such that

and the number of observed columns satisfies

(20) then Algorithm 2 with the break condition where satisfies, for all ,

Remark 4

The quantities and in Corollary 1 measure the variation of amplitude of each row or each column of . When and become larger, a small number of rows and columns in would have larger amplitude than others, while these rows and columns would be missed with large probability in the sampling of , which means the problem would become harder. Hence, more observations for the matrix with larger and are needed as shown in (19).

We now consider the case where is a random matrix.

Corollary 2 (Random Matrix)

Suppose is a random matrix generated by , where the singular values and singular space are fixed, and has orthonormal columns that are randomly sampled based on the Haar measure. Suppose we observe the first rows and first columns of . Assume there exists such that

Then there exist uniform constants such that if , is given by Algorithm 2 with the break condition , where , we have for all ,

Parallel results hold for the case when is fixed and has orthonormal columns that are randomly sampled based on the Haar measure, and we observe the first rows and first columns of . Assume there exists such that

Then there exist unifrom constants such that if , is given by Algorithm 2 with column thresholding with the break condition , where , we have for all ,

4 Simulation

In this section, we show results from extensive simulation studies that examine the numerical performance of Algorithm 2 on randomly generated matrices for various values of , , and . We first consider settings where a gap between some adjacent singular values exists, as required by our theoretical analysis. Then we investigate settings where the singular values decay smoothly with no significant gap between adjacent singular values. The results show that the proposed procedure performs well even when there is no significant gap, as long as the singular values decay at a reasonable rate.

We also examine how sensitive the proposed estimators are to the choice of the threshold and the choice between row and column thresholding. In addition, we compare the performance of the SMC method with that of the NNM method. Finally, we consider a setting similar to the real data application discussed in the next section. Results shown below are based on 200-500 replications for each configuration. Additional simulation results on the effect of , and ratio are provided in the supplement. Throughout, we generate the random matrix A from , where the singular values of the diagonal matrix are chosen accordingly for different settings. The singular spaces and are drawn randomly from the Haar measure. Specifically, we generate i.i.d. standard Gaussian matrix and , then apply the QR decomposition to and and assign and with the part of the result.

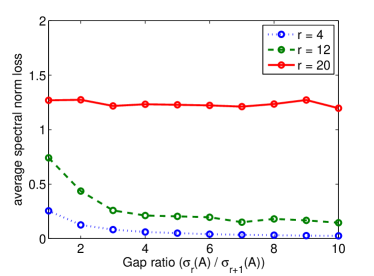

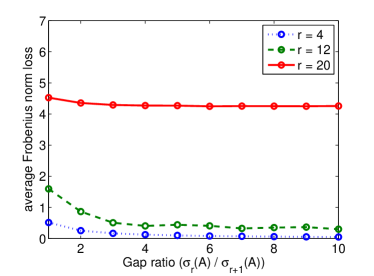

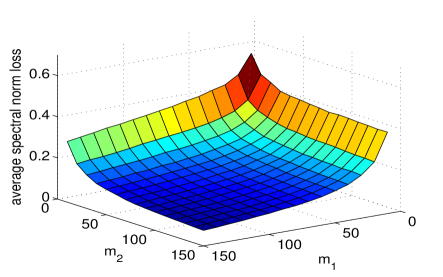

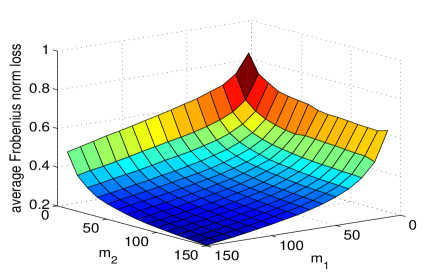

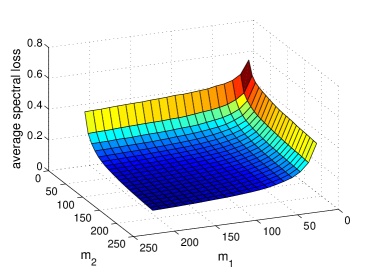

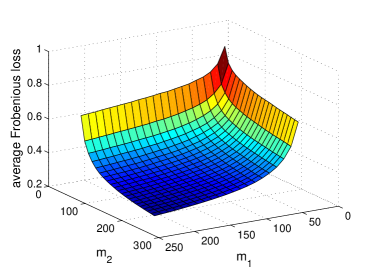

We first consider the performance of Algorithm 2 when a significant gap between the and singular values of . We fixed and choose the singular values as

| (21) |

Here is the rank of the major low-rank part , is the gap ratio between the and singular values of . The average loss of from Algorithm 2 with the row thresholding and under both the spectral norm and Frobenius norm losses are given in Figure 3. The results suggest that our algorithm performs better when gets smaller and gap ratio gets larger. Moreover, even when , namely there is no significant gap between any adjacent singular values, our algorithm still works well for small . As will be seen in the following simulation studies, this is generally the case as long as the singular values of decay sufficiently fast.

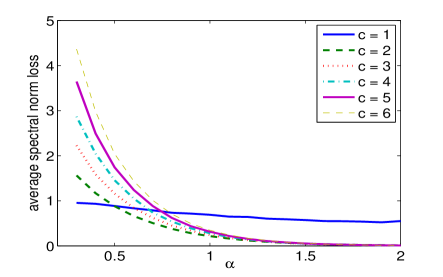

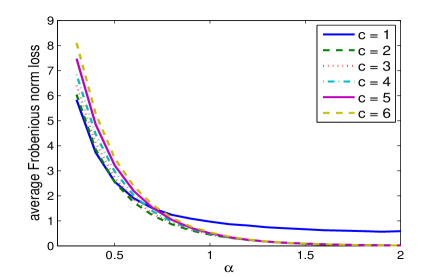

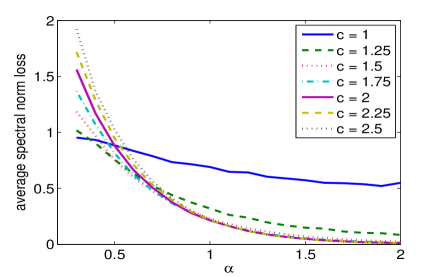

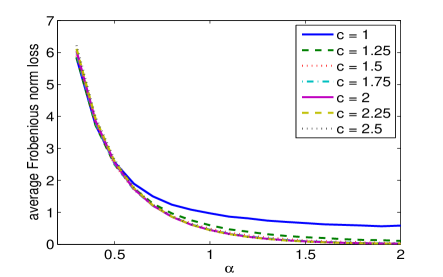

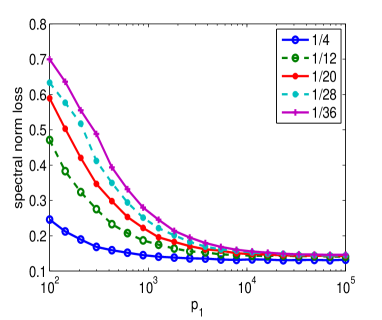

We now turn to the settings with the singular values being and various choices of , and . Hence, no significant gap between adjacent singular values exists under these settings and we aim to demonstrate that our method continues to work well. We first consider , and let range from 0.3 to 2. Under this setting, we also study how the choice of thresholds affect the performance of our algorithm. For simplicity, we report results only for row thresholding as results for column thresholding are similar. The average loss of from Algorithm 2 with under both the spectral norm and Frobenius norm are given in Figure 4. In general, the algorithm performs well provided that is not too small and as expected, the average loss decreases with a higher decay rate in the singular values. This indicates that the existence of a significant gap between adjacent singular values is not necessary in practice, provided that the singular values decay sufficiently fast. When comparing the results across different choices of the threshold, as suggested in our theoretical analysis is indeed the optimal choice. Thus, in all subsequent numerical analysis, we fix .

|

|

|

|

To investigate the impact of row versus column thresholding, we let the singular value decay rate be , , and and varying from 10 to 150. The original matrix is generated the same way as before. We apply row and column thresholding with and . It can be seen from Figure 5 that when the observed rows and columns are selected randomly, the results are not sensitive to the choice between row and column thresholding.

We next turn to the comparison between our proposed SMC algorithm and the penalized NNM method which recovers by (4). The solution to (4) can be solved by the spectral regularization algorithm by Mazumder et al. (2010) or the accelerated proximal gradient algorithm by Toh and Yun (2010), where these two methods provide similar results. We use 5-fold cross-validation to select the tuning parameter . Details on the implementation can be found in the Supplement.

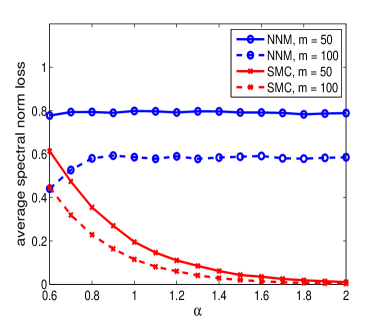

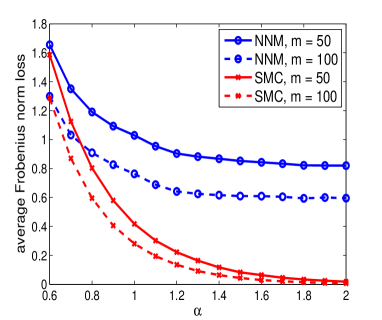

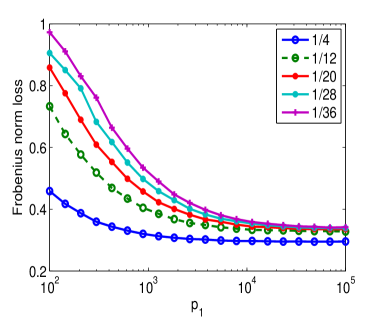

We consider the setting where , and the singular value decay rate ranges from 0.6 to 2. As shown in Figure 6, the proposed SMC method substantially outperform the penalized NNM method with respect to both the spectral and Frobenius norm loss, especially as increases.

Finally, we consider a simulation setting that mimics the ovarian cancer data application considered in the next section, where , , , and the singular values of decay at a polynomial rate . Although the singular values of the full matrix are unknown, we estimate the decay rate based on the singular values of the fully observed 552 rows of the matrix from the TCGA study, denoted by . A simple linear regression of on estimates as . In the simulation, we randomly generate such that the singular values are fixed as . For comparison, we also obtained results for as well as those based on the penalized NNM method with 5-cross-validation. As shown in Table 1, the relative spectral norm loss and relative Frobenius norm loss of the proposed method are reasonably small and substantially smaller than those from the penalized NNM method.

| Relative spectral norm loss | Relative Frobenius norm loss | |||

|---|---|---|---|---|

| SMC | NNM | SMC | NNM | |

| 0.1253 | 0.4614 | 0.2879 | 0.6122 | |

| 0.0732 | 0.4543 | 0.1794 | 0.5671 | |

5 Application in Genomic Data Integration

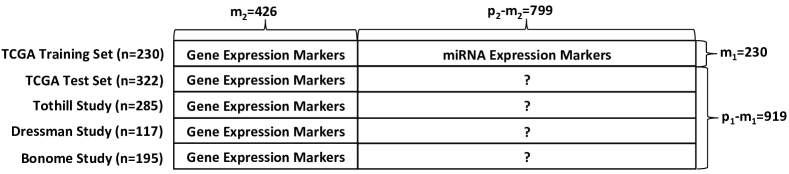

In this section, we apply our proposed procedures to integrate multiple genomic studies of ovarian cancer (OC). OC is the fifth leading cause of cancer mortality among women, attributing to 14,000 deaths annually (Siegel et al., 2013). OC is a relatively heterogeneous disease with 5-year survival rate varying substantially among different subgroups. The overall 5-year survival rate is near 90% for stage I cancer. But the majority of the OC patients are diagnosed as stage III/IV diseases and tend to develop resistance to chemotherapy, resulting a 5-year survival rate only about 30% (Holschneider and Berek, 2000). On the other hand, a small minority of advanced cancers are sensitive to chemotherapy and do not replapse after treatment completion. Such a heterogeneity in disease progression is likely to be in part attributable to variations in underlying biological characteristics of OC (Berchuck et al., 2005). This heterogeneity and the lack of successful treatment strategies motivated multiple genomic studies of OC to identify molecular signatures that can distinguish OC subtypes, and in turn help to optimize and personalize treatment. For example, the Cancer Genome Atlas (TCGA) comprehensively measured genomic and epigenetic abnormalities on high grade OC samples (Cancer Genome Atlas Research Network, 2011). A gene expression risk score based on 193 genes, , was trained on 230 training samples, denoted by , and shown as highly predictive of OC survival when validated on the TCGA independent validation set of size 322, denoted by , as well as on several independent OC gene expression studies including those from Bonome et al. (2005) (BONO), Dressman et al. (2007) (DRES) and Tothill et al. (2008) (TOTH).

The TCGA study also showed that clustering of miRNA levels overlaps with gene-expression based clusters and is predictive of survival. It would be interesting to examine whether combining miRNA with could improve survival prediction when compared to alone. One may use to evaluate the added value of miRNA. However, is of limited sample size. Furthermore, since miRNA was only measured for the TCGA study, its utility in prediction cannot be directly validated using these independent studies. Here, we apply our proposed SMC method to impute the missing miRNA values and subsequently construct prediction rules based on both and the imputed miRNA, denoted by , for these independent validation sets. To facilitate the comparison with the analysis based on alone where miRNA measurements are observed, we only used the miRNA from for imputation and reserved the miRNA data from for validation purposes. To improve the imputation, we also included additional 300 genes that were previously used in a prognostic gene expression signature for predicting ovarian cancer survival (Denkert et al., 2009). This results in a total of unique gene expression variables available for imputation. Detailed information on the data used for imputation is shown in Figure 7. Prior to imputation, all gene expression and miRNA levels are log transformed and centered to have mean zero within each study to remove potential platform or batch effects. Since the observable rows (indexing subjects) can be viewed as random whereas the observable columns (indexing genes and miRNAs) are not random, we used row thresholding with threshold as suggested in the theoretical and simulation results. For comparison, we also imputed data using the penalized NNM method with tuning parameter selected via 5-fold cross-validation.

We first compared to the observed miRNA on . Our imputation yielded a rank 2 matrix for and the correlations between the two right and left singular vectors to that of the observed miRNA variables are .90, .71, .34, .14, substantially higher than that of those from the NNM method, with the corresponding values 0.45, 0.06, 0.10, 0.05. This suggests that the SMC imputation does a good job in recovering the leading projections of the miRNA measurements and outperforms the NNM method.

To evaluate the utility of for predicting OC survival, we used the to select 117 miRNA markers that are marginally associated with survival with a nominal -value threshold of .05. We use the two leading principal components (PCs) of the 117 miRNA markers, , as predictors for the survival outcome in addition to . The imputation enables us to integrate information from 4 studies including , which could substantially improve efficiency and prediction performance. We first assessed the association between and OC survival by fitting a stratified Cox model (Kalbfleisch and Prentice, 2011) to the integrated data that combines and the three additional studies via either the SMC or NNM methods. In addition, we fit the Cox model to (i) set alone with obtained from the observed miRNA; and (ii) each individual study separately with imputed . As shown in Table 2(a), the log hazard ratio (logHR) estimates for from the integrated analysis, based on both SMC and NNM methods, are similar in magnitude to those obtained based on the observed miRNA values with . However, the integrated analysis has substantially smaller standard error (SE) estimates due the increased sample sizes. The estimated logHRs are also reasonably consistent across studies when separate models were fit to individual studies.

We also compared the prediction performance of the model based on alone to the model that includes both and the imputed . Combining information from all 4 studies via standard meta analysis, the average improvement in C-statistic was (SE = ) for the SMC method and (SE = ) for the NNM method, suggesting that the imputed from the SMC method has much higher predictive value compared to those obtained from the NNM method.

(a) Integrated Analysis with Imputed miRNA vs Single study with observed miRNA

| logHR | SE | -value | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Ori. | SMC | NNM | Ori. | SMC | NNM | Ori. | SMC | NNM | |

| .067 | .143 | .168 | .041 | .034 | .028 | .104 | .000 | .000 | |

| -.012 | -.019 | -.013 | .009 | .006 | .012 | .218 | .001 | .283 | |

| .023 | .018 | -.005 | .014 | .009 | .014 | .092 | .039 | .725 | |

(b) Estimates for Individual Studies with Imputed miRNA from the SMC method

| logHR | SE | -value | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCGA | TOTH | DRES | BONO | TCGA | TOTH | DRES | BONO | TCGA | TOTH | DRES | BONO | |

| .051 | .377 | .174 | .311 | .048 | .069 | .132 | .117 | .286 | .000 | .187 | .008 | |

| -.014 | -.021 | -.031 | -.010 | .011 | .012 | .014 | .014 | .207 | .082 | .030 | .484 | |

| .014 | .045 | -.021 | .036 | .016 | .018 | .022 | .019 | .391 | .009 | .336 | .054 | |

(c) Estimates for Individual Studies with Imputed miRNA from the NNM method

| logHR | SE | -value | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCGA | TOTH | DRES | BONO | TCGA | TOTH | DRES | BONO | TCGA | TOTH | DRES | BONO | |

| .082 | .405 | .361 | .258 | .037 | .066 | .114 | .088 | .028 | .000 | .002 | .003 | |

| -.045 | .016 | .055 | -.008 | .021 | .026 | .031 | .023 | .034 | .544 | .076 | .721 | |

| .008 | -.086 | -.043 | .019 | .026 | .027 | .034 | .029 | .758 | .002 | .201 | .496 | |

In summary, the results shown above suggest that our SMC procedure accurately recovers the leading PCs of the miRNA variables. In addition, adding obtained from imputation using the proposed SMC method could significantly improve the prediction performance, which confirms the value of our method for integrative genomic analysis. When comparing to the NNM method, the proposed SMC method produces summaries of miRNA that is more correlated with the truth and yields leading PCs that are more predictive of OC survival.

6 Discussions

The present paper introduced a new framework of SMC where a subset of the rows and columns of an approximately low-rank matrix are observed. We proposed an SMC method for the recovery of the whole matrix with theoretical guarantees. The proposed procedure significantly outperforms the conventional NNM method for matrix completion, which does not take into account the special structure of the observations. As shown by our theoretical and numerical analyses, the widely adopted NNM methods for matrix completion are not suitable for the SMC setting. These NNM methods perform particularly poorly when a small number of rows and columns are observed.

The key assumption in matrix completion is the matrix being approximately low rank. This is reasonable in the ovarian cancer application since as indicated in the results from the TCGA study (Cancer Genome Atlas Research Network, 2011), the patterns observed in the miRNA signature are highly correlated with the patterns observed in the gene expression signature. This suggests the high correlation among the selected gene expression and miRNA variables. Results from the imputation based on the approximate low rank assumption given in Section 5 are also encouraging with promising correlations with true signals and good prediction performance from the imputed miRNA signatures. We expect that this imputation method will also work well in genotyping and sequencing applications, particularly for regions with reasonably high linkage disequilibrium.

Another main assumption that is needed in the theoretical analysis is that there is a significant gap between the and singular values of . This assumption may not be valid in real practice. In particular, the singular values of the ovarian dataset analyzed in Section 5 is decreasing smoothly without a significant gap. However, it has been shown in the simulation studies presented in Section 4 that, although there is no significant gap between any adjacent singular values of the matrix to be recovered, the proposed SMC method works well as long as the singular values decay sufficiently fast. Theoretical analysis for the proposed SMC method under more general patterns of singular value decay warrants future research.

To implement the proposed Algorithm 2, major decisions include the choice of threshold values and choosing between column thresholding and row thresholding. Based on both theoretical and numerical studies, optimal threshold values can be set as for column thresholding and for row thresholding. Simulation results in Section 4 show that when both rows and columns are randomly chosen, the results are very similar. In the real data applications, the choice between row thresholding and column thresholding depends on whether the rows or columns are more “homogeneous”, or closer to being randomly sampled. For example, in the ovarian cancer dataset analyzed in Section 5, the rows correspond to the patients and the columns correspond to the gene expression levels and miRNA levels. Thus the rows are closer to random sample than the columns, consequently it is more natural to use the row thresholding in this case.

We have shown both theoretically and numerically in Sections 3 and 4 that Algorithm 2 provides a good recovery of . However, the naive implementation of this algorithm requires matrix inversions and multiplication operations in the for loop that calculates (or ), . Taking into account the relationship among (or ) for different ’s, it is possible to simultaneously calculate all (or ) and accelerate the computations. For reasons of space, we leave optimal implementation of Algorithm 2 as future work.

Acknowledgments

We thank the Editor, Associate Editor and referee for their detailed and constructive comments which have helped to improve the presentation of the paper.

References

- Argyriou et al. (2008) Argyriou, A., Evgeniou, T., and Pontil, M. (2008). Convex multi-task feature learning. Machine Learning, 73(3):243–272.

- Berchuck et al. (2005) Berchuck, A., Iversen, E. S., Lancaster, J. M., Pittman, J., Luo, J., Lee, P., Murphy, S., Dressman, H. K., Febbo, P. G., West, M., et al. (2005). Patterns of gene expression that characterize long-term survival in advanced stage serous ovarian cancers. Clinical Cancer Research, 11(10):3686–3696.

- Biswas et al. (2006) Biswas, P., Lian, T.-C., Wang, T.-C., and Ye, Y. (2006). Semidefinite programming based algorithms for sensor network localization. ACM Transactions on Sensor Networks (TOSN), 2(2):188–220.

- Bonome et al. (2005) Bonome, T., Lee, J.-Y., Park, D.-C., Radonovich, M., Pise-Masison, C., Brady, J., Gardner, G. J., Hao, K., Wong, W. H., Barrett, J. C., et al. (2005). Expression profiling of serous low malignant potential, low-grade, and high-grade tumors of the ovary. Cancer Research, 65(22):10602–10612.

- Browning and Browning (2009) Browning, B. L. and Browning, S. R. (2009). A unified approach to genotype imputation and haplotype-phase inference for large data sets of trios and unrelated individuals. The American Journal of Human Genetics, 84(2):210–223.

- Cai et al. (2010) Cai, J.-F., Candès, E., and Shen, Z. (2010). A singular value thresholding algorithm for matrix completion. SIAM J. Optim., 20(4):1956–1982.

- Cai et al. (2014) Cai, T., Cai, T. T., and Zhang, A. (2014). Supplement to “structured matrix completion with applications to genomic data integration”. Technical Report.

- Cai and Zhang (2014) Cai, T. T. and Zhang, A. (2014). Perturbation bound on unilateral singular vectors. Technical report.

- Cai and Zhou (2013) Cai, T. T. and Zhou, W. (2013). Matrix completion via max-norm constrained optimization. arXiv preprint arXiv:1303.0341.

- Cancer Genome Atlas Research Network (2011) Cancer Genome Atlas Research Network (2011). Integrated genomic analyses of ovarian carcinoma. Nature, 474(7353):609–615.

- Candes and Plan (2011) Candes, E. J. and Plan, Y. (2011). Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. Information Theory, IEEE Transactions on, 57(4):2342–2359.

- Candès and Recht (2009) Candès, E. J. and Recht, B. (2009). Exact matrix completion via convex optimization. Foundations of Computational Mathematics, 9(6):717–772.

- Candès and Tao (2010) Candès, E. J. and Tao, T. (2010). The power of convex relaxation: Near-optimal matrix completion. Information Theory, IEEE Transactions on, 56(5):2053–2080.

- Chen and Suter (2004) Chen, P. and Suter, D. (2004). Recovering the missing components in a large noisy low-rank matrix: Application to sfm. Pattern Analysis and Machine Intelligence, IEEE Transactions on, 26(8):1051–1063.

- Chi et al. (2013) Chi, E. C., Zhou, H., Chen, G. K., Del Vecchyo, D. O., and Lange, K. (2013). Genotype imputation via matrix completion. Genome Research, 23(3):509–518.

- Denkert et al. (2009) Denkert, C., Budczies, J., Darb-Esfahani, S., Györffy, B., Sehouli, J., Könsgen, D., Zeillinger, R., Weichert, W., Noske, A., Buckendahl, A.-C., et al. (2009). A prognostic gene expression index in ovarian cancervalidation across different independent data sets. The Journal of pathology, 218(2):273–280.

- Dressman et al. (2007) Dressman, H. K., Berchuck, A., Chan, G., Zhai, J., Bild, A., Sayer, R., Cragun, J., Clarke, J., Whitaker, R. S., Li, L., et al. (2007). An integrated genomic-based approach to individualized treatment of patients with advanced-stage ovarian cancer. Journal of Clinical Oncology, 25(5):517–525.

- Foygel et al. (2011) Foygel, R., Salakhutdinov, R., Shamir, O., and Srebro, N. (2011). Learning with the weighted trace-norm under arbitrary sampling distributions. In NIPS, pages 2133–2141.

- Gross (2011) Gross, D. (2011). Recovering low-rank matrices from few coefficients in any basis. Information Theory, IEEE Transactions on, 57(3):1548–1566.

- Gross and Nesme (2010) Gross, D. and Nesme, V. (2010). Note on sampling without replacing from a finite collection of matrices. arXiv preprint, arXiv:1001.2738.

- Holschneider and Berek (2000) Holschneider, C. H. and Berek, J. S. (2000). Ovarian cancer: epidemiology, biology, and prognostic factors. In Seminars in surgical oncology, volume 19, pages 3–10. Wiley Online Library.

- Kalbfleisch and Prentice (2011) Kalbfleisch, J. D. and Prentice, R. L. (2011). The statistical analysis of failure time data, volume 360. John Wiley & Sons.

- Keshavan et al. (2010) Keshavan, R. H., Montanari, A., and Oh, S. (2010). Matrix completion from noisy entries. J. Mach. Learn. Res., 11(1):2057–2078.

- Kim et al. (2005) Kim, H., Golub, G. H., and Park, H. (2005). Missing value estimation for dna microarray gene expression data: local least squares imputation. Bioinformatics, 21(2):187–198.

- Koltchinskii (2011) Koltchinskii, V. (2011). Von neumann entropy penalization and low-rank matrix estimation. Ann. Statist., 39(6):2936–2973.

- Koltchinskii et al. (2011) Koltchinskii, V., Lounici, K., Tsybakov, A. B., et al. (2011). Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. Ann. Statist., 39(5):2302–2329.

- Koren et al. (2009) Koren, Y., Bell, R., and Volinsky, C. (2009). Matrix factorization techniques for recommender systems. Computer, 42(8):30–37.

- Laurent and Massart (2000) Laurent, B. and Massart, P. (2000). Adaptive estimation of a quadratic functional by model selection. Ann. Statist., 28:1302–1338.

- Li and Abecasis (2006) Li, Y. and Abecasis, G. R. (2006). Mach 1.0: rapid haplotype reconstruction and missing genotype inference. Am J Hum Genet S, 79(3):2290.

- Mazumder et al. (2010) Mazumder, R., Hastie, T., and Tibshirani, R. (2010). Spectral regularization algorithms for learning large incomplete matrices. Journal of Machine Learning Research, 11:2287–2322.

- Recht (2011) Recht, B. (2011). A simpler approach to matrix completion. J. Mach. Learn. Res., 12:3413–3430.

- Rohde et al. (2011) Rohde, A., Tsybakov, A. B., et al. (2011). Estimation of high-dimensional low-rank matrices. Ann. Statist., 39(2):887–930.

- Salakhutdinov and Srebro (2010) Salakhutdinov, R. and Srebro, N. (2010). Collaborative filtering in a non-uniform world: Learning with the weighted trace norm. arXiv preprint arXiv:1002.2780.

- Scheet and Stephens (2006) Scheet, P. and Stephens, M. (2006). A fast and flexible statistical model for large-scale population genotype data: applications to inferring missing genotypes and haplotypic phase. The American Journal of Human Genetics, 78(4):629–644.

- Siegel et al. (2013) Siegel, R., Naishadham, D., and Jemal, A. (2013). Cancer statistics, 2013. CA: a cancer journal for clinicians, 63(1):11–30.

- Singer and Cucuringu (2010) Singer, A. and Cucuringu, M. (2010). Uniqueness of low-rank matrix completion by rigidity theory. SIAM Journal on Matrix Analysis and Applications, 31(4):1621–1641.

- Toh and Yun (2010) Toh, K.-C. and Yun, S. (2010). An accelerated proximal gradient algorithm for nuclear norm regularized least squares problems. Pacific J. Optimization, 6:615–640.

- Tomasi and Kanade (1992) Tomasi, C. and Kanade, T. (1992). Shape and motion from image streams: a factorization method parts 2, 8, 10 full report on the orthographic case.

- Tothill et al. (2008) Tothill, R. W., Tinker, A. V., George, J., Brown, R., Fox, S. B., Lade, S., Johnson, D. S., Trivett, M. K., Etemadmoghadam, D., Locandro, B., et al. (2008). Novel molecular subtypes of serous and endometrioid ovarian cancer linked to clinical outcome. Clinical Cancer Research, 14(16):5198–5208.

- Troyanskaya et al. (2001) Troyanskaya, O., Cantor, M., Sherlock, G., Brown, P., Hastie, T., Tibshirani, R., Botstein, D., and Altman, R. B. (2001). Missing value estimation methods for dna microarrays. Bioinformatics, 17(6):520–525.

- Vershynin (2010) Vershynin, R. (2010). Introduction to the non-asymptotic analysis of random matrices. Cambridge Univ. Press, Cambridge.

- Vershynin (2013) Vershynin, R. (2013). Spectral norm of products of random and deterministic matrices. Probab. Theory Relat. Fields, 150:471—509.

- Wang et al. (2006) Wang, X., Li, A., Jiang, Z., and Feng, H. (2006). Missing value estimation for DNA microarray gene expression data by support vector regression imputation and orthogonal coding scheme. BMC Bioinformatics, 7(1):32.

- Yu and Schaid (2007) Yu, Z. and Schaid, D. J. (2007). Methods to impute missing genotypes for population data. Human Genetics, 122(5):495–504.

Supplement to “Structured Matrix Completion With

Applications to Genomic Data Integration” 111Tianxi Cai is Professor of Biostatistics, Department of Biostatistics, Harvard School of Public Health, Harvard University, Boston, MA (E-mail: tcai@hsph.harvard.edu); T. Tony Cai is Dorothy Silberberg Professor of Statistics, Department of Statistics, The Wharton School, University of Pennsylvania, Philadelphia, PA (E-mail: tcai@wharton.upenn.edu); Anru Zhang is a Ph.D. student, Department of Statistics, The Wharton School, University of Pennsylvania, Philadelphia, PA (E-mail: anrzhang@wharton.upenn.edu). The research of Tianxi Cai was supported in part by NIH Grants R01 GM079330 and U54 LM008748; the research of Tony Cai and Anru Zhang was supported in part by NSF Grant DMS-1208982 and NIH Grant R01 CA127334.

Tianxi Cai, T. Tony Cai and Anru Zhang

1 Additional Simulation Results

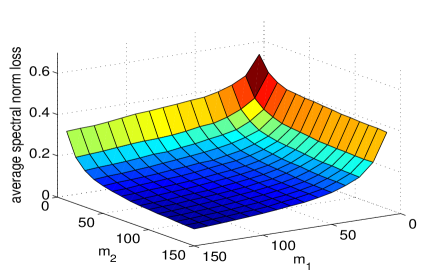

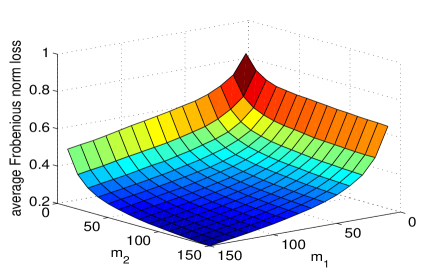

We consider the effect of the number of the observed rows and columns on the estimation accuracy. We let , let the singular values of be and let and vary from to . The singular spaces and are again generated randomly from the Haar measure. The estimation errors of from Algorithm 2 with row thresholding and over different choices of and are shown in Figure 8.

As expected, the average loss decreases as or grows. Another interesting fact is that the average loss is approximately symmetric with respect to and . This implies that even with different numbers of observed rows and columns, Algorithm 2 has similar performance with row thresholding or column thresholding.

We are also interested in the performance of Algorithm 2 as and the ratio vary. To this end, we consider the setting where , , and the singular values of are chosen as . The results are shown in Figure 9. It can be seen that when increases, the recovery is generally more accurate; when is kept as a constant, the average loss does decrease but not converge to zero as increases.

2 Technical Tools

We collect important technical tools in this section. The first lemma is about the inequalities of singular values in the perturbed matrix.

Lemma 1

Suppose , , , ,

-

1.

for ;

-

2.

if we further have , we must have , for .

Lemma 2

Suppose are two arbitrary matrices, denote , as the Schatten- norm and spectral norm respectively, then we have

| (22) |

The following two lemmas provide examples that illustrate NNM fails to recover .

Lemma 3

Lemma 4

The following result is on the norm of a random submatrix of a given orthonormal matrix.

Lemma 5

Suppose is a fixed matrix with orthonormal columns (hence ). Denote . Suppose we uniform randomly draw rows (with or without replacement) from and note the index as and denote

When for some and , we have

with probability .

The following results is about the spectral norm of the submatrix of a random orthonormal matrix.

Lemma 6

Suppose () is with random orthonormal columns with Haar measure. For all , there exists constant depending only on such that when , we have

| (24) |

with probability at least .

Proof of the Technical Lemmas

Proof of Lemma 1.

-

1.

First, by a well-known fact about best low-rank approximation,

Hence,

similarly .

-

2.

When we further have , we know the column space of and are orthogonal, then we have , which means . Next, note that

if we note as the -th largest eigenvalue of the matrix, then we have

Proof of Lemma 2. Since

it suffices to show . To this end, we have

which finishes the proof of this lemma.

Proof of Lemma 3. Since and and their submatrices are all i.i.d. standard matrices, by the random matrix theory (Corollary 5.35 in Vershynin (2010)), for , we have with probability at least , the following inequalities hold,

| (25) |

| (26) |

and

| (27) |

Denote

and set . Since , , we have

| (28) |

and

| (29) |

Hence, with probability at least , , which implies that the NNM (3) fails to recover .

Proof of Lemma 4. For convenience, we denote for any two real numbers . First, we can extend the unit vectors , and into orthogonal matrices, which we denote as , , , . Next, for all , we must have

where are with the first entry , and respectively and other entries 0. Therefore, we can see

and the equality holds if and only if is zero except the first entry.

By some calculation, we can see the nuclear norm of 2-by-2 matrix

achieves its minimum if and only if

Hence, achieves the minimum of if and only if

which means the minimizer .

Proof of Lemma 5. The proof of this lemma relies on operator-Bernstein’s inequality for sampling (Theorem 1 in Gross and Nesme (2010)). For two symmetric matrices , , we say if is positive definite. By assumption, {} are uniformly random samples (with or without replacement) from . Suppose

| (30) |

then are symmetric matrices, are uniformly random samples (with or without replacement) from . In addition, we have

For all , by Theorem 1 in Gross and Nesme (2010),

The last inequality is due to the assumption that

Proof of Lemma 6. By the assumption on , we have or . When , we know and is an orthogonal matrix, which means (24) is clearly true. Hence, we only need to prove the theorem under the assumption that is true. In this case, we must have .

Since has random orthonormal columns with Haar measure, for any fixed vector , is identitical distributed as

Hence, is identical distributed with and

| (31) |

which is the also the square root of Beta distribution. Denote

| (32) |

By Lemma 1 in Laurent and Massart (2000), when are i.i.d. standard normal, we have

both hold with probability at least . Here we let be small enough and only depending on such that

Combining the previous inequalities and (31), we have for any fixed unit vector ,

| (33) |

with probability at least , where only depends on . Next, based on Lemma 2.5 in Vershynin (2013), we can construct an -net on the unit sphere of as , such that , where is to be determined later. Under the event that , we suppose

For any in the unit sphere of , there must exists such that , which yields,

These implies that , . Hence, we can take depending on such that , , which implies (24).

Finally we estimate the probability that the event happens. We choose that only depends on and . If ,

so

Finally, we finish the proof of the lemma by setting .

3 Proofs of the Results in the Main Paper

We prove Proposition 1, Theorems 1 and 2, Lemma 7, Lemma 8, Theorem 3, Corollary 1 and Corollary 2 in this section.

Proof of Proposition 1

Since is of rank , which is the same as , all rows of must be linear combinations of the rows of . This implies all rows of is a linear combination of . Since rank(), we must have . Besides, since is a submatrix of . So . Simiarly, rows of is the linear combination of , so we have

namely rows of is a linear combination of . By the argument before, we know can be represented as the same linear combination of as by , so we have which concludes the proof.

Proof of Theorem 1

Suppose are column orthonormalized matrices of and . and are the first left singular vectors of and , respectively. Also, recall that we use to represent the projection onto the column space of .

-

1.

We first give the lower bound for , by the unilateral perturbation bound result in Cai and Zhang (2014). Since,

by is an orthogonal matrix, we can see

So . Besides, . Apply the unilateral perturbation bound result in Cai and Zhang (2014) by setting , , we have

(34) Moreover, and hence,

When , let denote the projection of onto the column space of . Then and is in the column space of . Hence,

which implies . Hence for all such that ,

This yields Combining (34), we have

(35) Since , we have

Similarly, we also have .

- 2.

Proof of Theorem 2

We only present proof for row thresholding as the column thresholding is essentially the same by working with . Suppose are orthonormal basis of column vectors of . We denote , , which are exactly the same as the and in Algorithm 1. Similarly to the proof of Theorem 1, we have (35). Due to the assumption that , (35) yields

| (46) |

As shown in the Supplementary material, we have

Lemma 7

Under the assumption of Theorem 2, we have .

We next show (13) with the condition that in steps.

-

1.

Note that , we consider the decompositions of and let

(47) (48) (49) Note that the square matrix is a submatrix of , we know

(50) Similarly, . By are the orthonormal basis of column vectors of , we have , , and

(51) similarly, we also have

(52) (51) and (52) immediately yield

(53) Besides, we also have

(54) -

2.

Next, we consider the SVD of

(55) For convenience, we denote

(56) Suppose is an orthonormal basis of the column space of ; is an orthonormal basis of the column space of . Denote as the linear span of the column space of the matrix. We want to show is close to ; while is close to . So in the rest of this step, we try to establish bounds for and . Actually,

Now we set , , then we have

Besides, by the definition of and we know . Also based on the definition of , we know . Now the unilateral perturbation bound in Cai and Zhang (2014) yields

(57) The right hand side of the inequality above is an increasing function of . Since ,

(58) Similarly, we also have

(59) -

3.

We next derive useful expressions of and . First we introduce the following quantities,

(60) (61) (62) (63) (64) (65) Since

(66) we can characterize by these new notations as

(67) (68) -

4.

Lemma 8

Based on the assumptions above, we have

(69) (70) (71) (72) (73) The proof of Lemma 8 is given in the Supplement.

- 5.

Proof of Lemma 7.

In order to prove this lemma, we just need to prove that the for-loop in Algorithm 2 will break for some . This can be shown by proving the break condition

| (78) |

hold for .

Proof of Lemma 8.

First, since and are an orthonormal basis of and , we have and and

| (79) |

which gives (69).

| (80) |

which gives the first part of (70). Here we used the fact that is a square matrix; is the orthonormal basis of the column space of . Similarly we have the later part of (70),

| (81) |

Based on the definitions, we have the bound for all “ ” terms in (60)-(65), i.e. (71). Now we move on to (72). By the SVD of (55) and the partition (56), we know

Hence, we have

| (82) |

which proves (72). Since and by definition, , by Lemma 1, we know

| (83) |

Then

| (84) |

Same to the process of (80), we know

| (85) |

Also, . Hence,

| (86) |

which proves (73).

Proof of Theorem 3.

The idea of proof is to construct two matrices both in such that they have the identical first rows and columns, but differ much in the remaining block. Suppose are fixed numbers, is a small real number. We first consider the following 2-by-2 matrix

| (87) |

Suppose the larger and smaller singular value of are and , then we have

| (88) |

as ; since , we also have

| (89) |

as . If defined in (87) has SVD

| (90) |

then we also have

| (91) |

as .

Now we set , , , , where is some small positive number to be specify later. We construct and such that,

| (92) |

| (93) |

Here we use to note the identity matrix of dimension . Then we construct and as

| (94) |

where and are with identical first rows and columns. Since the SVD of is given as (90), the SVD of can be written as

where

Hence,

Also, as . So we have when is small enough. Similarly when is small enough. Now we also have , . .

Finally for any estimate , we must have

| (95) |

as . Since and are with identical first rows and columns, we must have

Let , since , we have

| (96) |

which finished the proof of theorem.

Proof of Corollary 1.

We first prove the second part of the corollary. We set . Since is with orthonormal columns, by Lemma 5 and

we have

| (97) |

with probability at least . When (97) holds, by the condition, we know

When , we have

Hence we can apply Theorem 2, for we must have

| (98) |

which finishes the proof of the second part of Corollary 1. Besides, the proof for the third part is the same as the second part after we take the transpose of the matrix.

Proof of Corollary 2.

3.1 Description of Cross-Validation

In this section, we describe the cross-validation used in penalized nuclear norm minimization (4) in the numerical comparison in Sections 4 and 5.

First, we construct a grid of non-negative numbers based on a pre-selected positive integer . Denote

i.e. the largest singular value of the observed blocks. For penalized nuclear norm minimization, we let .

Next, for a given positive integer , we randomly divide the integer set into two groups of size , for times. For , we denote by and the index sets of the two groups for the -th split. Then the penalized nuclear norm minimization estimator (4) is applied to the first group of data: , i.e. the data of the observation set , with each value of the tuning parameter and denote the result by . Note that we did not use the observed block in calculating . Instead, is used to evaluate the performance of the tunning parameter . Set

| (102) |

Finally, the tuning parameter is chosen as

and the final estimator is calculated using this choice of the tuning parameter .