Long signal change-point detection

Abstract

The detection of change-points in a spatially or time-ordered data sequence is an important problem in many fields such as genetics and finance. We derive the asymptotic distribution of a statistic recently suggested for detecting change-points. Simulation of its estimated limit distribution leads to a new and computationally efficient change-point detection algorithm, which can be used on very long signals. We assess the algorithm experimentally under various conditions.

I. Introduction

When met with a data set ordered by time or space, it is often important to predict when or where something “changed” as we move temporally or spatially through it. In biology, for example, changes in an array Comparative Genomic Hybridization (aCGH) or Chip-Seq data signal as one moves across the genome can represent an event such as a change in genomic copy number, which is extremely important in cancer gene detection [17, 22]. In the financial world, detecting changes in multivariate time-series data is important for decision-making [27]. Change-point detection can also be used to detect financial anomalies [3] and significant changes in a sequence of images [11].

Change-point detection analysis is a well-studied field and there are numerous approaches to the problem. Its extensive literature ranges from parametric methods using log-likelihood functions [4, 14] to nonparametric ones based on Wilcoxon-type statistics, U-statistics and sequential ranks. The reader is referred to the monograph [5] for an in-depth treatment of these methods.

In change-point modeling it is generally supposed that we are dealing with a random process evolving in time or space. The aim is to develop a method to search for a point where possible changes occur in the mean, variance, distribution, etc. of the process. All in all, this comes down to finding ways to decide whether a given signal can be considered homogeneous in a statistical (stochastic) sense.

The present article builds upon an interesting nonparametric change-point detection method that was recently proposed by Matteson and James [15]. It uses U-statistics (see [9]) as the basis of its change-point test. Its interest lies in its ability to detect quite general types of change in distribution. Several theoretical results are presented in [15] to highlight some of the mathematical foundations of their method. These in turn lead to a simple and useful data-driven statistical test for change-point detection. The authors then apply this test successfully to simulated and real-world data.

There are however several weaknesses in [15] both from theoretical and practical points of view. Certain fundamental theoretical considerations are incompletely treated, especially the assertion that a limit distribution exists for the important statistic, upon which the rest of the approach hangs. On the practical side, the method is computationally prohibitive for signals of more than a few thousand points, which is unfortunate because real-world signals can be typically much longer.

Our paper has two main objectives. First, it fills in missing theoretical results in [15] including a derivation of the limit distribution of the statistic. This requires the effective application of large sample theory techniques, which were developed to study degenerate U-statistics. Second, we provide a method to simulate from an approximate version of the limit distribution. This leads to a new computationally efficient strategy for change-point detection that can be run on much longer signals.

The article is structured as follows. In Section II we provide some context and present the main theoretical results. In Section III we show how to approximate the limit distribution of the statistic, which leads to a new test strategy for change-point detection. We then show how to extend the method to much longer sequences. Simulations are provided in Section IV. A short discussion follows in Section V, and a proof of the paper’s main result is given in Section VI. Some important technical results are detailed in the Appendix.

II. Theoretical results

I. Measuring differences between multivariate distributions

Let us first briefly describe the origins of the nonparametric change-point detection method described in [15]. For random variables taking values in , , let and denote their respective characteristic functions. A measure of the divergence (or “difference”) between the distributions of and is as follows:

where is an arbitrary positive weight function for which this integral exists. It turns out that for the specific weight function

which depends on a , one can obtain a not immediately obvious but very useful result. Let be i.i.d. and be i.i.d. , with , and mutually independent. Denote by the Euclidean norm on . Then, if

| (1) |

Theorem 2 of [25] yields that

| (2) |

where we have written instead of to highlight dependence on . Therefore (1) implies that . Furthermore, Theorem 2 of [25] says that if and only if and have the same distribution. This remarkable result leads to a simple data-driven divergence measure for distributions. Seen in the context of hypothesizing a change-point in a signal of independent observations after the -th observation , we simply calculate an empirical version of (2):

| (3) |

Matteson and James [15] state without proof that under the null hypothesis of being i.i.d. (no change-points), the sample divergence given in (3) scaled by converges in distribution to a non-degenerate random variable as long as . Furthermore, they state that if there is a change-point between two distinct i.i.d. distributions after the -th point, the sample divergence scaled by tends a.s. to infinity as long as . These claims clearly point to a useful statistical test for detecting change-points. However, we cannot find rigorous mathematical arguments to substantiate them in [15], nor in the earlier work [25].

As this is of fundamental importance to the theoretical and practical validity of this change-point detection method, we shall show the existence of the non-degenerate random variable hinted at in [15] by deriving its distribution. Our approach relies on the asymptotic behavior of U-statistic type processes, which were introduced for the first time for change-point detection in random sequences in [6]; see also Chapter 2 of the book [5]. We also show that in the presence of a change-point the correctly-scaled sample divergence indeed tends to infinity with probability 1.

II. Main result

Let us first begin in a more general setup. Let be independent -valued random variables. For any symmetric measurable function , whenever the indices make sense we define the following four terms:

Otherwise, define the term to be zero; for instance, and for and . Note that in the context of the change-point algorithm we have in mind, , , but the following results are valid for the more general defined above. Notice also that the last three terms are U-statistics absent their normalization constants. Next, let us define

Observe that is a general version of the empirical divergence given in (3). Notice that

| (4) |

While is not a U-statistic, we can use (4) to express it as a linear combination of U-statistics. Indeed, we find that

Therefore, we now have an expression for made up of U-statistics, which will be useful in the following.

Our aim is to use a test based on for the null hypothesis have the same distribution, versus the alternative hypothesis that there is a change-point in the sequence , i.e.,

For , , means that each component of is less than or equal to the corresponding component of . Also note that for any , stands for its integer part.

Let us now examine the asymptotic properties of . We shall be using notation, methods and results from Section 5.5.2 of monograph [21] to provide the groundwork. In the following, we shall denote by the common (unknown) distribution function of the under , a generic random variable with distribution function , and an independent copy of . We assume that

| (5) |

and set . We also denote , and define

| (6) |

With this notation, we see that , and therefore that . Furthermore,

| (7) |

since

where . As in Section 5.5.2 of [21], we then define the operator on by

| (8) |

Let , , be the eigenvalues of this operator with corresponding orthonormal eigenfunctions , . Since for all ,

we see with , Thus is an eigenvalue and normalized eigenfunction pair of the operator . This implies that for every eigenvalue and normalized eigenfunction pair , where is nonzero,

Moreover, we have that in ,

From this we get that

| (9) |

For further details and theoretical justification of these claims, refer to Section 5.5.2 of [21] and both Exercise 44 on pg. 1083 and Exercise 56 on pg. 1087 of [7]. In fact, we shall assume further that

| (10) |

It is crucial for the change-point testing procedure that we shall propose that the function defined as in (10) with , , satisfies (10) whenever (5) holds. A proof of this is given in the Appendix.

Next, for any fixed , , set

| (11) | ||||

We define , , , and , which gives

One can readily check that , the space of bounded measurable real-valued functions defined on that are right-continuous with left-hand limits. Notice that on account of (7) we can also write , and we will do so from now on. In the following theorem, denotes a sequence of independent standard Brownian bridges.

Theorem II.1

The proof of this theorem is deferred to Section VI.

Remark II.1

Note that a special case of Theorem II.1 says that for each ,

| (12) |

This fixed result can be derived from part (a) of Theorem 1.1 of [16]. [24] point out that convergence in distribution of a statistic asymptotically equivalent to the left side of (12) to a nondegenerate random variable should follow from [16] under the null hypothesis of equal distributions in the two sample case that they consider. Also see [18]. ([18] also discuss the consistency of their statistic.) To the best of our knowledge, we are the first to identify the limit distribution of the . We should point out here that the weak convergence result in Theorem II.1 does not follow from Neuhaus’ theorem [16], since his result is based on two independent samples, whereas ours concerns one sample.

As suggested in [15], under the following assumption, a convergence with probability 1 result can be proved for the empirical statistic in (3). We shall show that this is indeed the case.

Assumption 1

Let , , and , , be independent i.i.d. sequences, respectively and . Also let be i.i.d. and be i.i.d. , with and mutually independent. Assume that for some , . Choose . For any given , let , for , and , for .

Lemma II.1

Whenever for a given Assumption 1 holds, with probability 1 we have:

| (13) |

The proof of this can be found in the Appendix. Next, let , . We see that for any for all large enough ,

where it is understood that Assumption 1 holds. Thus by Lemma II.1, under Assumption 1, whenever , with probability 1,

This shows that change-point tests based on the statistic , under the sequence of alternatives of the type given by Assumption 1, are consistent. This also has great practical use when looking for change-points. Intuitively, the that maximizes (3) would be a good candidate for a change-point location.

III. From theory to practice

Theorem II.1 and the consistency result that follows it lay a firm theoretical foundation to justify the change-point method introduced in [15]. For the present article, since we are not aware of a closed form expression for the distribution function of the limit process, we may imagine that this asymptotic result is of limited practical use. Remarkably, it turns out that we can efficiently approximate via simulation the distribution of its supremum, leading to a new change-point detection algorithm with similar performance to [15] but much faster for longer signals. For instance, finding and testing one change-point in a signal of length takes eight seconds with our method and eight minutes using [15].

To simulate the process we need true or estimated values of the . Recall that these are the eigenvalues of the operator defined in (8). Following [12], the (usually infinite) spectrum of can be consistently approximated by the (finite) spectrum of the empirical matrix whose -th entry is given by

where is the vector of row means (excluding the diagonal entry) of matrix and the mean of its upper-diagonal elements.

In our experience, the estimated in this way tend to be quite

accurate for even small . We assert this because upon simulating longer

and longer i.i.d. signals, rapid convergence of the is clear.

Furthermore, as there is an exponential drop-off in their magnitude, working

with only a small number (say 20 or 50) of the largest ones appears to be

sufficient for obtaining good results. We illustrate these claims in Section

IV. Let us now present our basic algorithm for detecting and

testing for one potential change-point.

Algorithm for detecting and testing one change-point

- 1.

-

2.

Calculate the largest (in absolute value) eigenvalues of the matrix , where and .

-

3.

Simulate times the -truncated version of using the eigenvalues from the previous step. Record the values of the (absolute) supremum of the process obtained.

-

4.

Reject the null hypothesis of no distributional change (at level ) if , where . In this case, we deduce a change-point at the at which is found. Typically, we set .

Remark III.1

One may imagine extending this approach to the multiple change-point case by simply iterating the above algorithm to the left and right of the first-found change-point, and so on. However, as soon as we suppose there can be more than one change-point, the assumption that we may have i.i.d., with a different distribution to i.i.d., is immediately broken. Therefore the theory we have presented does not directly follow over to the multiple change-point case. It would be interesting to cleanly extend the results to this, but this would require further theory and multiple testing developments, which are out of the scope of the present article (for references in this direction, see, e.g., [13]).

The E-divisive algorithm described in [15] follows a similar logic to our approach except that is calculated via permutation (see [19]). Instead of steps 2 and 3, the order of the data is permuted times and for the -th permuted signal, , step 1 is performed to obtain the absolute maximum . The same step 4 is then used to accept or reject the change-point.

The permutation approach (E-divisive) of [15] is effective for short signals. Indeed, [10] showed that if one can perform all possible permutations, the method produces a test that is level . However, a signal with points already implies more than three million permutations, so a Monte Carlo strategy (i.e., subsampling permutations with replacement) becomes necessary, typically with . This also gives a test that is theoretically level (see [19]) but with much-diminished power.

One could propose increasing the value of but there is an unfortunate computational bottleneck in the approach. Usually, one stores in memory the matrix of in order to efficiently permute rows/columns and therefore recalculate each time. But for more than a few thousand points, manipulating this matrix is slow if not impossible due to memory constraints. The only alternative to storing and permuting this matrix is simply to recalculate it each time for each permutation, but this is very computationally expensive as increases. Consequently, the E-divisive approach is only useful for signals up to a few thousand points.

In contrast to this, our algorithm, based on an asymptotic result, risks underperforming on extremely short signals, and its performance will also depend on our ability to estimate well the set of largest . In reality though, it works quite well, even on short signals. The matrix with entries needs only to be stored once in memory, and all standard mathematical software (such as Matlab and R) have efficient functions for finding its largest eigenvalues (the eigs function in Matlab and the eigs function in the R package rARPACK). Each iteration of the algorithm’s simulation step requires summing the columns of an matrix of standard normal variables, where is the number of retained and the number of grid points over which we approximate the Brownian bridge processes between 0 and 1. For and it takes about one second to perform this times, and is independent of the number of points in the signal. In contrast, the E-divisive method takes about ten seconds for , one minute for , eight minutes for , etc. One clearly sees the advantage of our approach for longer signals.

IV. Experimental validation and analysis

I. Simulated examples

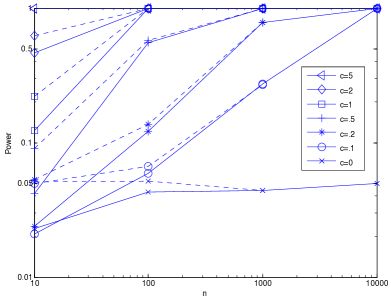

It is very important to start with the simplest possible case in order to demonstrate the fundamental validity of the new method. A basis for comparison is the E-divisive method from [15]. Here, we consider signals of length for which either the whole signal is i.i.d. or else there is a change-point of height after the -th point, i.e., the second half of the signal is i.i.d. .

In the former case, we look at the behavior of the Type I error, i.e., the probability of detecting a change-point when there was none. We have fixed and want to see how close each method is to this as increases. In the latter case, we look at the power of the test associated to each method, i.e., the probability that an actual change-point is correctly detected as and increase. We averaged over trials. In the following, unless otherwise mentioned we fix . For the asymptotic method, the Brownian bridge processes were simulated 499 times; similarly, for E-divisive we permuted 499 times. Both null distributions were therefore estimated using the same number of repeats. Note that we did not test the E-divisive method for because each of the 1 000 trials would have taken around two hours to run. All times given in this paper are with respect to a laptop with a 2.13 GHz Intel Core 2 Duo processor with 4Gb of memory. Results are presented in Figure 1.

For the Type I error, we see that both methods hover around the intended value of .05, except for extremely short signals (). As for the statistical power, it increases as and increase. Furthermore, the asymptotic method rapidly reaches a similar performance as E-divisive: for , E-divisive is better (but still with quite poor power), for the asymptotic method has almost caught up, and somewhere between and the results become essentially identical; the asymptotic method has a slight edge at .

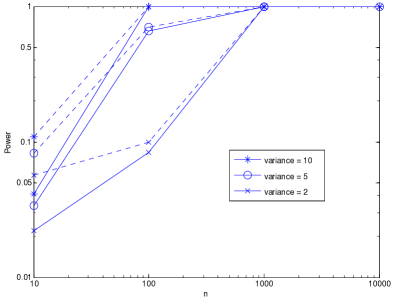

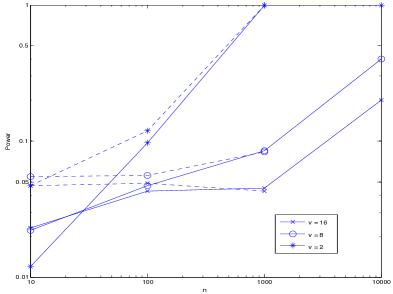

Let us now see to what extent our method is able to detect changes in variance and tail shape. We considered Gaussian signals of length for which there is a change-point after the -th point, i.e., the first half of the signal is i.i.d. and the second half either i.i.d. for or i.i.d. Student’s distributions with . Results were averaged over 1 000 trials and are shown in Figure 2.

As before, the statistical power tends to increase as increases and either increases or decreases. The asymptotic method matches or beats the performance of E-divisive starting somewhere between and .

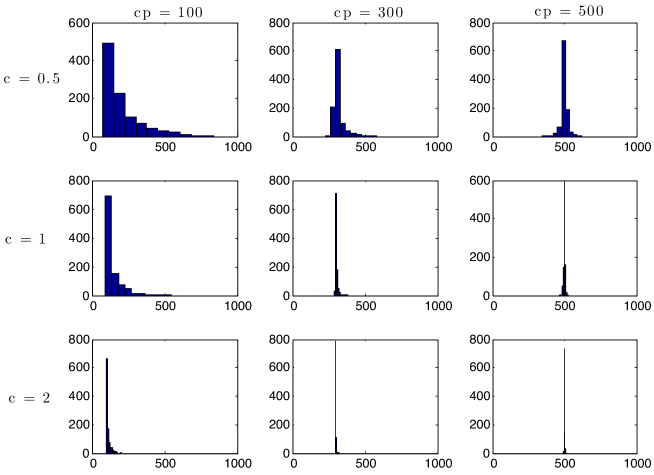

Next, we take a look at the performance of the algorithm when the change-point location moves closer to the boundary. As an illustrative example, we work with sequences of length 1 000 and either place the change-point after the 100th, 300th or 500th point. Figure 3 shows histograms of 1 000 repetitions for the predicted location of the change-point, here a change in mean of (hardest), (medium) and (easiest).

We see that moving towards the boundary increases the variance and bias in the prediction. However, as the problem becomes easier (bigger jump in mean), both the variance and bias decrease. Similar results are found when looking at change in variance and tail distribution.

II. Algorithm for long signals

Remember that as it currently stands, the longest signal that we can treat

depends on the largest matrix that can be stored, which depends in turn on

the memory of a given computer (memory problems for simply manipulating a matrix

on a standard PC typically start to occur around -). For

this reason, we now propose a modified algorithm that can treat vastly

longer signals.

Long-signal algorithm

-

1.

Extract sub-signal of equidistant points of length 2 000.

-

2.

Run the one change-point algorithm on this. If the null hypothesis is rejected, output the index of the predicted change-point in this sub-signal. Otherwise, state that no change-point was found.

-

3.

If a change-point was indeed predicted, get the location in the original signal corresponding to in the sub-signal and repeat step 1 of the one change-point algorithm in the interval to refine the prediction, where is user-chosen. If is the length of the interval between sub-signal points, one possibility is , where the 1 000 simply ensures this refining step receives a computationally feasible signal length of at most 2 000 points.

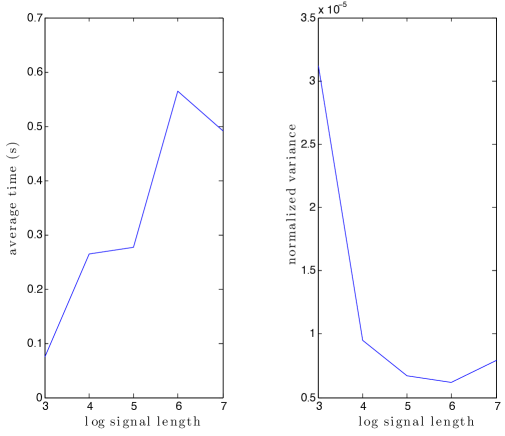

We tested this strategy on simulated standard Gaussian signals of length and with one change-point at the midpoint, a jump of in the mean. Figure 4 (left) shows the time required to locate the potential change-point.

Clearly, this is rapid for even extremely long signals. Looking at the algorithm, we see that it merely involves finding a change-point twice, once in the sub-signal, then once in a contiguous block of the original signal of at most length 2 000. As these two tasks are extremely rapid, the increase in computation time seen mostly comes from the computing overhead of having to extract the sub-signal from longer and longer vectors in memory. In Figure 4 (right), we plot the log signal length against the normalized variance, which means that we calculate the variance in predicted change-point location over 1 000 trials after first dividing the predictions by the length of the signal. Thus all transformed predictions are in the interval before their variance is taken. This shows that relative to the length of the signal, subsampling does not deteriorate the change-point prediction quality. Instead, what deteriorates due to subsampling is the absolute prediction quality, i.e., the variance in predicted change-point location does increase as the signal length increases. However, we cannot get around this without introducing significantly more sophisticated subsampling procedures, beyond the scope of the work here.

V. Discussion

We have derived the asymptotic distribution of a statistic that was previously used to build algorithms for finding change-points in signals. Our new result led to a novel way to construct a practical algorithm for general change-point detection in long signals, which came from the surprising realization that it was possible to approximately simulate from this quite complicated asymptotic distribution. Furthermore, the method appears to have higher power (in the statistical sense) than previous methods based on permutation tests for signals of a thousand points or more. We tested the algorithm on several simulated data sets, as well as a subsampling variant for dealing with extremely long signals.

An interesting line of future research would be to find ways to segment the original signal without requiring stocking a matrix in memory with the same number of rows and columns as there are points in the signal, currently a bottleneck for our approach and even more so for previous permutation approaches. Furthermore, the pertinent choice of the power remains an open question. Lastly, theoretically valid and experimentally feasible extensions of this framework to the multiple change-point case could be a fruitful line of future research.

VI. Proof of Theorem II.1

To prove Theorem II.1, we require a useful technical result. Let us begin with some notation. For each integer , let denote the space of bounded measurable functions defined on taking values in that are right-continuous with left-hand limits. For each integer , let , , be a sequence of processes taking values in such that for some , uniformly in and ,

| (14) |

For each integer , define the process taking values in by

Assume that for each integer , converges weakly as to the –valued process defined as

where , is a sequence of –valued processes such that for some , uniformly in ,

| (15) |

We shall establish the following useful result.

Proposition VI.1

With the notation and assumptions introduced above, for any choice of constants , , satisfying , the sequence of –valued processes

converges weakly in to the –valued process

Proof. Notice that by (14)

From this we get that with probability , for each ,

which in turn implies that with probability , for each ,

| (16) |

where

Since for each and , , where , by completeness of in the supremum metric (see page 150 of monograph [2]), we infer that . In the same way we get using (15) that

| (17) |

where

and thus that . Also, since by assumption for each integer , converges weakly as to the –valued process , we get that converges weakly in to , where

We complete the proof by combining this with (16) and (17), and then appealing to Theorem 4.2 of [2].

We are now ready to prove Theorem II.1. It turns out that it is more convenient to prove the result for the following version of the process , namely

which is readily shown to be asymptotically equivalent to . Following pages 196-197 of [21], we see that

and

Thus,

| (18) |

Let be a sequence of standard Wiener processes on . Write

where, for ,

| (19) |

A simple application of Doob’s inequality shows that there exists a constant such that (14) and (15) hold, for and defined as in (18) and (19).

For any integer , let be the random vector such that . We see that and . For any let be i.i.d. . Consider the process defined on by

where for any ,

Notice that as processes in ,

Clearly by Donsker’s theorem the process converges weakly as to the –valued Wiener process with mean vector zero and covariance matrix , , where

Using this fact along with the law of large numbers one readily verifies that for each integer , converges weakly as to , where and are defined as in (18) and (19). All the conditions for Proposition VI.1 to hold have been verified. Thus the proof of Theorem II.1 is complete, after we note that a little algebra shows that is equal to

where , , are independent Brownian bridges.

VII. Appendix

I. Proof of Lemma II.1

Notice that for each , is equal to the statistic in (3) with . By the law of large numbers for U-statistics (see Theorem 1 of [20]) for any , with probability 1,

and

Next for any , write

Applying the strong law of large numbers for generalized U-statistics given in Theorem 1 of [20], we get for any , with probability 1,

Also observe that

By the usual law of large numbers for each , with probability 1,

Thus, with probability 1, for all ,

In the same way we get that, with probability 1,

Finally, note that, by the -inequality,

By the law of large numbers this converges, with probability 1, to

Obviously as ,

and

Putting everything together we get that (13) holds.

II. A technical result

Let and be i.i.d. and let be a symmetric measurable function from such that . Recall the notation (6). Let be the operator defined on as in (8).

Notice that

Let us now introduce some useful definitions. Given and , define as in (6),

The aim here is to verify that the function satisfies the conditions of Theorem II.1 as long as

| (20) |

Let denote the integral operator

Clearly (20) implies (5) with , which, in turn, by (9) implies

where , , are the eigenvalues of the operator , with corresponding orthonormal eigenfunctions , .

Next we shall prove that when (20) holds then the eigenvalues , , of this integral operator satisfy (10). This is summarized in the following lemma, whose proof is postponed to the next paragraph.

The technical results that follow will imply that for all and is finite, from which we can infer (10), and thus Lemma VII.1. Let us begin with two definitions.

Definition VII.1

Let be a nonempty set. A symmetric function is called positive definite if

for all , and .

Definition VII.2

Let be a nonempty set. A symmetric function is called conditionally negative definite if

for all , such that and .

Next, we shall be using part of Lemma 2.1 on page 74 of [1], which we state here for convenience as Lemma VII.2.

Lemma VII.2

Let be a symmetric function on . Then, for any , the function

is positive definite if and only if is conditionally negative definite.

The following lemma can be proved just as Corollary 2.1 in [8].

Lemma VII.3

We recall that an operator on is called positive definite if for all , .

Proposition VII.1

Let be a symmetric continuous function that is a conditionally negative definite function in the sense of Definition VII.2. Assume that for all and . Then defines a positive definite operator on given by

where is defined as in (6). Furthermore the operator on given by

is also a positive definite operator on .

Proof. We must show that for all ,

For any , let us write

Since is assumed to be conditionally negative definite, by Lemma VII.2 we have that for any fixed , is positive definite in the sense of Definition VII.1. Hence, since is also assumed to be continuous, by Lemma VII.3 for all ,

Noting that if has distribution function , , we get, assuming that , and are independent, that

Next, notice that for any eigenvalue and normalized eigenfunction pair, , of the operator , we have

Now,

implies that is an eigenvalue and normalized eigenfunction pair of . From this we get that whenever , , , which says that for such ,

This implies that whenever for some , with is an eigenvalue and normalized eigenfunction pair of the operator it is also an eigenvalue and normalized eigenfunction pair of the operator . Moreover, since the integral operator is positive definite on , this implies that for any such nonzero (where necessarily )

which says that the operator is positive definite on .

III. Proof of Lemma VII.1

A special case of Theorem 3.2.2 in [1] says that the function , , is conditionally negative definite. Also see Exercise 3.2.13b in [1] and the discussion after Proposition 3 in [26]. Therefore by Proposition VII.1 the integral operator defined by the function

is positive definite as well as the integral operator defined by the function

Next, as in the proof of Proposition VII.1, any eigenvalue and normalized eigenfunction

pair, with , , of the operator is also an eigenvalue and normalized eigenfunction pair of the operator .

We shall apply Theorem 2 of [23] to show that uniformly on compact subsets of ,

where , , are the eigenvalues of the operator with corresponding normalized eigenfunctions , . In particular

and thus since , , and , we get

Therefore since, as pointed out above, the eigenvalue and normalized eigenfunction pairs of , with , are also eigenvalue and normalized eigenfunction pairs of the operator this implies that .

Our proof will be complete once we have checked that satisfies the conditions of Theorem 2 of [23].

Since the function , is conditionally negative definite, by Lemma VII.2 the function is positive definite. To see this note that by Lemma VII.2 for any fixed the function

is positive definite. Therefore we readily see that

is positive definite. In addition, is symmetric and continuous, and thus is a Mercer kernel in the terminology of [23]. We must also verify the following assumptions.

Assumption A. For each ,

Assumption B. is a bounded and positive definite operator on and for every , the function

is a continuous function on .

Assumption C. has at most countably many positive eigenvalues and orthonormal eigenfunctions.

Since is a symmetric continuous function that is conditionally negative definite in the sense of Definition VII.2 satisfying for all and , we get by Proposition VII.1 that is a positive definite operator on . Also (20) obviously implies that Assumption A holds and

which by Proposition 1 of [23] implies that the operator is bounded and compact. (From Sun’s Proposition 1 one can also infer that is positive definite. However, he does not provide a proof. Therefore we invoke our Lemma VII.3 here.) An elementary argument based on the dominated convergence theorem implies that is a continuous function on . Thus Assumption B is satisfied. Finally, since the operator is compact, Theorem VII.4.5 of [7] implies that Assumption C is fulfilled. Thus the assumptions of Theorem 2 of [23] hold. This completes the proof of Lemma VII.1.

References

- [1] C. Berg, J. P. R. Christensen, and P. Ressel. Harmonic Analysis on Semigroups. Springer, New York, 1984.

- [2] P. Billingsley. Convergence of Probability Measures. Wiley, New York, 1968.

- [3] R. Bolton and D. Hand. Statistical fraud detection: A review. Statistical Science, 17:235–255, 2002.

- [4] B. P. Carlin, A. E. Gelfand, and A. F. Smith. Hierarchical Bayesian analysis of changepoint problems. Applied Statistics, 41:389–405, 1992.

- [5] M. Csörgő and L. Horváth. Limit Theorems in Change-Point Analysis. Wiley, New York, 1997.

- [6] M. Csörgő and L. Horváth. Invariance principles for changepoint problems. Journal of Multivariate Analysis, 27:151–168, 1988.

- [7] N. Dunford and J. T. Schwartz. Linear Operators. Wiley, New York, 1963.

- [8] J. C. Ferreira and V. A. Menegatto. Eigenvalues of integral operators defined by smooth positive definite kernels. Integral Equations and Operator Theory, 64:61–81, 2009.

- [9] W. Hoeffding. A class of statistics with asymptotically normal distribution. The Annals of Mathematical Statistics, 19:293–325, 1948.

- [10] W. Hoeffding. The large-sample power of tests based on permutations of observations. The Annals of Mathematical Statistics, 23:169–192, 1952.

- [11] A. Kim, C. Marzban, D. Percival, and W. Stuetzie. Using labeled data to evaluate change detectors in a multivariate streaming environment. Signal Processing, 89:2529–2536, 2009.

- [12] V. Koltchinskii and E. Giné. Random matrix approximation of spectra of integral operators. Bernoulli, 6:113–167, 2000.

- [13] K. Korkas and P. Fryzlewicz. Multiple change-point detection for non-stationary time series using Wild Binary Segmentation. http://stats.lse.ac.uk/fryzlewicz/articles.html, 2014.

- [14] M. Lavielle and G. Teyssière. Detection of multiple change-points in multivariate time series. Lithuanian Mathematical Journal, 46:287–306, 2006.

- [15] D. S. Matteson and N. A. James. A nonparametric approach for multiple change point analysis of multivariate data. Journal of the American Statistical Association, 109:334–345, 2014.

- [16] G. Neuhaus. Functional limit theorems for U-statistics in the degenerate case. Journal of Multivariate Analysis, 7(3):424–439, 1977.

- [17] F. Picard, S. Robin, M. Lavielle, C. Vaisse, and J.-J. Daudin. A statistical approach for array CGH data analysis. BMC Bioinformatics, 6:27, 2005.

- [18] M. L. Rizzo. A test of homogeneity for two multivariate populations. Proceedings of the American Statistical Association, Physical and Engineering Sciences Section, 2002.

- [19] J. P. Romano and M. Wolf. Exact and approximate stepdown methods for multiple hypothesis testing. Journal of the American Statistical Association, 100:94–108, 2005.

- [20] P. K. Sen. Almost sure convergence of generalized U-statistics. The Annals of Probability, 5:287–290, 1977.

- [21] R. J. Serfling. Approximation Theorems of Mathematical Statistics. Wiley, New York, 1980.

- [22] S. P. Shah, W. L. Lam, R. T. Ng, and K. P. Murphy. Modeling recurrent DNA copy number alterations in array CGH data. Bioinformatics, 23:i450–i458, 2007.

- [23] H. Sun. Mercer theorem for RKHS on noncompact sets. Journal of Complexity, 21:337–349, 2005.

- [24] G. J. Székely and M. L. Rizzo. Testing for equal distributions in high dimension. InterStat, 5:1–6, 2004.

- [25] G. J. Székely and M. L. Rizzo. Hierarchical clustering via joint between-within distances: Extending Ward’s minimum variance method. Journal of Classification, 22:151–183, 2005.

- [26] G. J. Székely and M. L. Rizzo. Energy statistics: A class of statistics based on distances. Journal of Statistical Planning and Inference, 143:1249–1272, 2013.

- [27] M. Talih and N. Hengartner. Structural learning with time-varying components: Tracking the cross-section of financial time series. Journal of the Royal Statistical Society: Series B, 67:321–341, 2005.