1 Introduction

Let be an i.i.d. sample from a

bivariate distribution function (d.f.) with marginal d.f.’s and for .

Suppose that is in the max-domain of attraction of some bivariate

d.f. with nondegenerate marginals. That is, suppose that there exist

normalizing sequences and such that

|

|

|

(1) |

as , for all continuity points

of . Of course, (1) is equivalent to

|

|

|

(2) |

and the d.f. is, by definition, an extreme value d.f.

It is a classical result in extreme value theory [see de Haan and Ferreira (2006), Theorem 1.1.3] that the normalizing sequences

and can be chosen in such a way that the marginal

d.f.’s and are of the form

|

|

|

|

|

|

|

|

|

|

for some . [Here, and in the rest of

the paper, expressions of the form

should be interpreted as when .] We will

assume throughout that the normalizing sequences are chosen in this

way. Then is necessarily continuous, as it has continuous marginal

d.f.’s, and the equivalent convergences (1) and (2) hold for all . Also, can

be fully characterized by the marginal extreme value indices , and a description of the dependence structure between

the marginal d.f.’s and . Due to de Haan and Resnick (1977), it

is known that the class of possible dependence structures for bivariate

extreme value distributions does not form a finite-dimensional

parametric family. Nevertheless, there are various equivalent ways of

describing extreme value (or tail) dependence structures, each with its

own advantages in applications. For an overview, we refer to Beirlant et al. (2004), Chapter 8 or de Haan and Ferreira (2006), Part II.

In this paper, we will focus on one possible description of the

bivariate tail dependence structure, namely the tail copula. For

a bivariate extreme value d.f. with marginal d.f.’s as given in (LABEL:hazaza), the tail copula is defined as

|

|

|

(4) |

We say that a bivariate d.f. belonging to the domain of attraction of

has associated tail copula . It is clear that tail copulas are

not copula functions in the usual sense (since they are not

distribution functions of probability measures, e.g.), yet they fully

capture the asymptotic dependence structure of the component-wise

maxima, just like copulas capture the dependence structure of random

vectors. Indeed, it is easily checked that , with

|

|

|

(5) |

In other words, is the unique d.f. characterized by the marginal d.f.’s

(LABEL:hazaza) and the copula (5).

We conclude that the asymptotic joint behavior of the standardizedcomponent-wise maxima and is

fully characterized by the marginal extreme value indices appearing in (LABEL:hazaza) and the tail copula defined

in (4). Statistical inference about extreme value indices is

a classical and well-studied problem in univariate extreme value

theory; we refer to Beirlant et al. (2004), Chapters 4 and 5 or

de Haan and Ferreira (2006), Chapter 3 for more information. There is

also a growing literature on inference about the tail dependence

structure; see Beirlant et al. (2004), Chapter 9 or

de Haan and Ferreira (2006), Chapter 7, for an overview. In this paper, we

will focus on inference about . In particular, we will propose a

semi-parametric estimator of , describe a transformation of the

empirical process derived from it and demonstrate how this transformed

empirical process can serve as a basis to construct asymptotically

distribution-free goodness-of-fit tests for .

1.1 More on tail dependence

The tail copula can also be obtained (and its domain extended) in

the following way from the d.f. :

|

|

|

|

|

|

|

|

|

|

(7) |

where denotes a random vector with d.f. . If has

continuous marginals, (LABEL:R.def.2) can also be written as

|

|

|

(8) |

where denotes the “survival copula” of , that is,

the copula associated with . Observe that for all and for all . It is also clear from (LABEL:R.def.2) that is

homogeneous of order 1, so the restriction of on, for example,

determines on its entire domain. The characterization

(LABEL:R.def.2) stems from Huang (1992), where it is used to

derive a nonparametric estimator for . We will use an alternative,

semi-parametric estimator better suited for our purposes; see Section 2.

The value is known in the applied extreme value literature as

the (upper) tail dependence coefficient and is widely used as a

measure of tail dependence. When , which is equivalent to on , we call and tail independent. When

, we say that and exhibit tail dependence. Other

ways of describing the tail dependence structure include the

stable tail dependence function, the exponent measure, the

spectral measure and the Pickands dependence function;

see the monographs Kotz and Nadarajah (2000), Beirlant et al. (2004), de Haan and Ferreira (2006) and the many

references therein.

We also note here that the function generates a -finite

measure, which we will also, without confusion, denote by , on Borel

subsets of , through the identity

|

|

|

(9) |

1.2 Goodness-of-fit testing

In the literature and in practice, often a parametric model is used for

the tail copula ; see, for example, Coles and Tawn (1991) or Joe, Smith and Weissman (1992). Testing the goodness-of-fit of the parametric model to

a given data sample is therefore an important problem with abundant

applications in many fields such as insurance and risk management,

finance and econometrics and hydrology and meteorology. In this paper,

we develop a procedure for constructing asymptotically

distribution-free goodness-of-fit tests for the tail copula of a

bivariate d.f. . We consider null hypotheses of the form , where is a parametric family of tail copulas. Of

course, by taking the parameter space to consist of a single

point, our results can also be used to test the goodness-of-fit of a

fully specified tail copula to the data.

Our approach is based on a semi-parametric estimator of

, to be defined below. We consider a suitably normalized difference,

, between and (with denoting a suitable

estimator of ), and we show that, under the null

hypothesis, a proper transformation of converges

weakly to a standard Wiener process . This fundamental result allows

one to construct a myriad of goodness-of-fit tests based on comparisons

of appropriate functionals of (the test statistics

the practitioner may prefer to use) with the same functionals of .

We emphasize that, since is a standard Wiener process, our

approach leads to asymptotically distribution-free

goodness-of-fit tests: under the null hypothesis, the asymptotic

distributions of the test statistics do not depend on or

the true . A simulation study confirms the

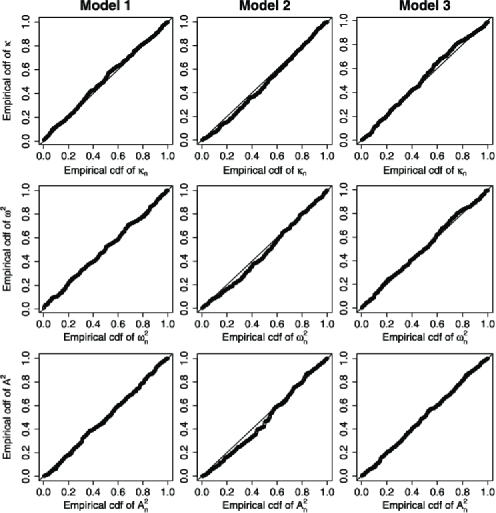

applicability of our approach for finite samples.

Testing (and estimation) problems for the tail copula have been studied

in the recent literature. In Einmahl, de Haan and Li (2006) the existence of

is tested, rather than its membership of a parametric family. In

de Haan, Neves and Peng (2008) a specific Cramér–von Mises type statistic

for is studied for two-dimensional data and a one-dimensional parameter;

the test statistic has a complicated limiting distribution under the

null hypothesis. In Einmahl, Krajina and Segers (2012) it is assumed that , and it

is then tested if is a member of a smaller parametric family,

obtained by setting some components of equal to

fixed values.

The remainder of the paper is organized as follows. In Section 2, we

describe the semi-parametric estimator , introduce the

empirical process , which is the normalized

difference between and , and describe the weak limit of as . In Section 3, we describe our key

transformation from into a standard Wiener process. In

Section 4, we show that the same transformation (or rather an empirical

version of it, with unknown parameters replaced by estimators) applied

to produces a process whose weak limit is a standard

Wiener process. This is our main result. In Section 5, we extend this

result to the -dimensional setting, for . Finally, in Section 6, we demonstrate through Monte Carlo simulations the applicability of

our limit theorems in finite samples and the high power properties of

tests based on our results. Proofs are deferred to Section 7. The paper

is supplemented by an online appendix, see Can et al. (2015), which

contains some details suppressed in Section 2 as well

as technical specifics about the Monte Carlo simulations, including the

computer code.

2 An estimator for and its asymptotic behavior

As in Section 1, we let

denote an i.i.d. sample from a bivariate d.f. with marginal d.f.’s

and . We assume that the bivariate domain of attraction condition

(1) holds, with the normalizing sequences and

chosen such that the marginal d.f.’s and are as in

(LABEL:hazaza). Taking logarithms in (2), and replacing

the discrete index by a continuous index , we obtain

|

|

|

Combining this with the corresponding marginal results and (5) leads to

|

|

|

|

|

|

or equivalently,

|

|

|

with

|

|

|

|

|

|

|

|

|

|

for . We conclude that if we let denote an

intermediate sequence, that is, and as , then

|

|

|

(11) |

as , for all .

We estimate and hence by replacing the unknown quantities

, and , , by appropriate

estimators , and , and the probability by the corresponding empirical

measure. We define, therefore,

|

|

|

|

|

|

|

|

|

|

and

|

|

|

(13) |

for ; cf. de Haan and Resnick (1993).

We consider the empirical process

|

|

|

(14) |

We will establish the asymptotic behavior of on , for any , but we introduce some

definitions and assumptions first. Note that from now on we will omit

the arguments where appropriate, for ease of notation.

Let denote a Wiener process on with “time” , that is, a zero-mean Gaussian

process with covariance

|

|

|

Also write [cf. (11)]

|

|

|

(15) |

It is known, by Einmahl, de Haan and Sinha (1997), Lemma 3.1, that in , where

“” denotes weak convergence and

denotes the Skorohod space of functions defined on .

In order to leave the estimators , and

, , general at this stage, we simply assume

that they are chosen in such a way that:

For some 6-variate random vector , we have the joint weak convergence

|

|

|

|

|

|

(16) |

|

|

|

in .

Assumption A1 is fulfilled for, for example, the moment estimators of

, and , provided that is chosen appropriately;

see de Haan and Ferreira (2006), Sections 4.2 and 3.5. We further

assume the following:

The partial derivatives

|

|

|

exist and are continuous on .

The sequence is chosen such that

|

|

|

Finally, for , we define the following functions on :

|

|

|

|

|

|

|

|

|

|

(17) |

|

|

|

|

|

We are now ready to state the basic convergence result for .

Theorem 1.

Let . If assumptions A1–A3 hold, then

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

in .

{rem*}

Note that we take , since the result does not

hold true in general for : the functions in (17)

are unbounded near zero for . This theorem is very

similar to Theorem 5.1 in de Haan and Resnick (1993), where instead of

the stable tail dependence function is

estimated. We nevertheless offer a detailed proof of Theorem 1 in Can et al. (2015), since the statement and proof of

Theorem 5.1 in de Haan and Resnick (1993) are not completely correct;

in particular, our is taken to be 0 there.

2.1 Parametric empirical process

Now suppose that the tail copula is a member of some parametric

family of tail copulas, , where is an open subset of

. Then there is a such that . Let denote an

estimator of , and consider the empirical process

|

|

|

(19) |

the parametric version of (14). Our next result will establish

the asymptotic behavior of . Since

|

|

|

(20) |

the asymptotic behavior of is an easy consequence of

Theorem 1, under proper assumptions. We state those

assumptions below.

There is a -variate random vector

such that

|

|

|

|

|

|

(21) |

|

|

|

in .

The first-order partial derivatives

|

|

|

|

|

|

|

|

|

|

exist and are continuous for , for some neighborhood

of in .

The sequence is chosen such that

|

|

|

(22) |

Note that B3 is the same as A3; we restate it here for ease of

presentation. Also note that by virtue of B2 the second term on the

right-hand side of (20) is asymptotically equal in

probability to

|

|

|

which, by B1, converges weakly to . Thus we obtain the following corollary to

Theorem 1.

Corollary 2.

Let . If assumptions B1–B3 hold, then

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

in .

3 Transforming into a standard

Wiener process

The limiting process in (LABEL:asymp.2) is of the

general form

|

|

|

(24) |

where denotes a Wiener process with time , is a fixed

integer, are deterministic functions mapping

into and are random

variables.

It will be more convenient to consider the set-indexed version of (24),

|

|

|

(25) |

where is a Borel subset of , is a set-indexed

Wiener process with time measure and are

deterministic signed measures. In the right-hand side of (25),

denotes the column vector consisting of and denotes the column vector consisting of

.

We will state a general transformation result about set-indexed

processes of the form (25), which we will then apply to

the process in (LABEL:asymp.2). The transformation is

a suitable extension of the “innovation martingale transform” first

discussed in Khmaladze (1981, 1988, 1993) in

connection with parametric goodness-of-fit testing for univariate and

multivariate distribution functions; see, in particular, Khmaladze (1993), Theorem 3.9.

A good summary of the innovation

martingale transform idea can be found in Koul and Swordson (2011);

for a variety of statistical applications we refer to McKeague, Nikabadze and Sun (1995), Nikabadze and Stute (1997),

Stute, Thies and Zhu (1998), Koenker and Xiao (2002, 2006),

Khmaladze and Koul

(2004, 2009), Delgado, Hidalgo and Velasco (2005)

and Dette and Hetzler (2009), among others.

As in Khmaladze (1993), we will call a collection of subsets of a scanning family over

if the following hold:

{longlist}[(iii)]

,

if ,

,

with Leb denoting Lebesgue measure. Note that for any and Borel subset of , the function generates a signed measure on .

Theorem 3.

Let be a set-indexed process of the form (25). Suppose

there are functions that are square-integrable with respect to and that satisfy

|

|

|

for any Borel set . Let be a scanning family over . Then the process

|

|

|

(26) |

is a Wiener process with time , where denotes the

column vector consisting of , and the

matrices are defined by

|

|

|

and are assumed to be invertible.

Now let us return to the setup of Section 2.1. We state

the following assumption.

For each , the

measure can be decomposed as , where satisfies

and

is absolutely continuous with respect

to the Lebesgue measure on , with a positive density

that has continuous first-order partial

derivatives with respect to for all

, for some neighborhood of in .

Note that B4 allows arbitrarily large masses on the “axes at

infinity”

for , but excludes the case

, which

corresponds to (strict) tail independence.

Let us define the following functions on , with and as defined in (17):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

Furthermore, let denote the Radon–Nikodym derivatives for , or more explicitly:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

As before, will denote the column vector consisting

of for .

We are now ready to apply Theorem 3 to in (LABEL:asymp.2). Instead of arbitrary Borel sets , we consider

rectangles , with

|

|

|

We also introduce the scanning family for and define the corresponding matrices

|

|

|

(27) |

{rem*}

From a likelihood theory point of view, the functions

can be seen as score functions corresponding to

the estimated values , , and the matrix can be seen

as a partial Fisher information matrix constructed from these score functions.

Corollary 4.

If assumptions B2 and B4, restricted to , hold, and the matrices in (27) are invertible, then the process

|

|

|

|

|

|

|

|

|

is a Wiener process with time on .

In order to obtain a standard Wiener process from , we normalize in the usual way, as follows.

Corollary 5.

If assumptions B2 and B4, restricted to , hold, and the matrices in (27) are invertible, then the process

|

|

|

|

|

|

|

|

|

(28) |

|

|

|

|

|

|

is a standard Wiener process on .

4 Goodness-of-fit testing

In Section 2 we introduced the parametric empirical

process as the normalized difference between

and the semi-parametric estimator

, and derived its weak limit . In

Section 3 we described a transformation from into a standard Wiener process . In this section, we will

apply the empirical version of the same transformation to , and prove that the resulting empirical process converges weakly

to a standard Wiener process. This is the main result of this paper.

Define the empirical version of in (28) as follows, for :

|

|

|

|

|

|

(29) |

|

|

|

Here, the vectors and the matrices are obtained by replacing the unknown marginal tail

indices and the unknown parameter in the definition of by their estimators

.

For functions , we introduce the seminorm

|

|

|

|

|

|

|

|

|

|

where denotes the univariate total variation over , and denotes the bivariate (Vitali) total variation over

, as defined in Owen (2005), for example. The

seminorm is sometimes called the Hardy–Krause variation in the literature, in recognition of Hardy (1905) and Krause (1903).

For notational convenience, let us also denote

|

|

|

|

|

|

|

|

|

|

and

|

|

|

Similarly, let

|

|

|

We introduce the following assumption:

{longlist}[B5.]

For , and

. Furthermore, and .

Given the consistency of , which is

implied by B1, a sufficient (but not necessary) condition for B5 is the

existence and continuity of the partial derivatives

|

|

|

on , for some neighborhood of

in , for and

, .

We can now present the main result of this paper.

Theorem 6.

Let , and let and be defined as in

(28) and (29). If assumptions B1–B5 hold, then

|

|

|

in .

Note that Theorem 6 yields that under the null hypothesis

, we obtain a distribution-free limiting

process (a standard bivariate Wiener process). Hence can be

used as a “test process” for producing a myriad of asymptotically

distribution-free test statistics to test this null hypothesis. We

will consider examples of such tests in Section 6.

{rem*}

By taking , where is a

fully specified tail copula, we can use Theorem 6 for

testing the null hypothesis . In this case, the process

in the definition of [see (29)] reduces

to as defined in , reduces to and and are determined by and

. We will consider an example

of testing in Section 6.

5 Multivariate extension

In this section we extend Theorem 6 from the bivariate to

the -dimensional setting, for . The proof will be omitted, but

it follows very similar lines as in the bivariate case. In particular,

Theorem 3 immediately generalizes to dimension

and then serves as a basis for the main result of this section.

So suppose that we have an i.i.d. sample from an -variate d.f. with marginal d.f.’s .

We write, for each , , where has d.f. . We assume that

is in the max-domain of attraction of an -variate extreme value d.f.

, so there exist normalizing sequences

and such that

|

|

|

with . We

assume, as in the bivariate case, that the sequences and ,

, are chosen in such a way that has marginal d.f.’s of

the form

|

|

|

for some . We will denote

. The d.f.

is then characterized by the marginal tail indices and the -variate tail copula

|

|

|

where denotes the point .

{rem*}

In the remainder of this section we consider defined

on the restricted domain [cf. (4)] because

our processes and transformations are not defined outside this region.

The bivariate tail copula defined on determines

on the full domain . In

contrast, for the tail copula defined on in

general does not determine on the full domain .

Let denote a parametric family of -variate tail copulas on

, parametrized by , an open subset of . Our aim

is to enable the construction of tests for the null hypothesis against the alternative .

For fixed ,

can be seen as an equivalence class of tail dependence structures

(i.e., tail copulas defined on the full domain) containing one or more

elements. Under the additional assumption that puts no mass on , contains exactly one

element (as in the bivariate case).

Suppose the null hypothesis holds true, with , for some . Let denote an estimator for .

As in Section 2, we let denote an

intermediate sequence and define the parametric empirical process

|

|

|

where

|

|

|

with , defined similarly as in (LABEL:XhatYhat). Let and

denote the obvious -variate extensions of (11) and (15), let and let C1–C4 denote the

natural -variate extensions of assumptions B1–B4 of Sections 2 and 3.

To state the analog of assumption B5 for the -variate case, we

extend the seminorm (LABEL:hk.norm) to -variate functions by

induction, as follows: For any function , and , we define to be the restriction of

to the subset of with the th coordinate fixed at

, and we define analogously. Then we let

|

|

|

(31) |

with denoting the -variate (Vitali) total variation over

and as defined in (LABEL:hk.norm). We also let

be defined as in Section 4, for .

For , and . Furthermore, and .

Now, let us introduce the functions and , for , as the natural

-variate extensions of the bivariate functions introduced before

Corollary 4, and let us denote by the column vector consisting of . Further, let us write , , and introduce matrices

|

|

|

which are assumed to be invertible. Then the -variate analog of the

transformed empirical process in (29) is

|

|

|

|

|

|

|

|

|

|

where and are obtained by

replacing and by and in the

definition of .

We are now ready to state the multivariate analog of Theorem 6. As in the bivariate case, this result can be used as a

basis for producing a multitude of asymptotically distribution-free

goodness-of-fit tests for a parametric model (as well as

for a fully specified tail copula ).

Theorem 7.

Let . Furthermore, let , and let be

defined as in (LABEL:Wn.multi). If assumptions C1–C5 hold, then

|

|

|

in , where is a standard -variate Wiener process.

7 Proofs

{pf*}Proof of Theorem 3

First note that the

terms following in (25) are “annihilated” by the

transformation (26):

|

|

|

|

|

|

Thus we can now compute, for Borel sets ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Splitting the double integral into two double integrals, one over the

region and the other over the region , we

see that all the integral terms cancel each other. This implies that

has the covariance structure of a Wiener process with time .

Let denote the empirical version of in Corollary 4,

|

|

|

|

|

|

|

|

|

The following result will be useful for the proof of Theorem 6.

Proposition 8.

Let . If assumptions B1–B5 hold, then

|

|

|

in .

{pf}

Applying Skorohod’s representation theorem [see, e.g., Billingsley (1999), Theorem 6.7] to Theorem 2, we

obtain a probability space that supports probabilistically equivalent

versions of and satisfying

|

|

|

with . We will work on this space. Let us denote

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We have to show that

|

|

|

(40) |

For this, it suffices to prove the two statements

|

|

|

(41) |

The first convergence in (41) follows from the continuity of

over and the continuity of

over . The second convergence in

(41) follows from

|

|

|

(42) |

since .

We establish (42) by proving the two statements

|

|

|

(43) |

Consider the second statement in (43). Its left-hand side is

equal to

|

|

|

with . The vector

function is bounded on , by continuity. So it will suffice to show

|

|

|

(44) |

The double integral inside the absolute value bars can be rewritten,

using integration by parts [see Hildebrandt (1963), Section III.8], as follows:

|

|

|

|

|

|

|

|

|

|

|

|

Each of the first four terms is bounded in absolute value by , where the first

factor is finite by continuity and the second factor vanishes in

probability. Moreover, each integral term is bounded in absolute value

by , which also

vanishes in probability because , by

virtue of the assumptions for , and Proposition 1 of Blümlinger and Tichy (1989). Hence (44) follows, and the second

convergence in (43) is established.

It remains to prove the first convergence in (43). By virtue of

the second convergence there, and an analogous result for and , it will suffice to prove . Note that

|

|

|

|

|

|

(45) |

|

|

|

where should be interpreted component-wise.

Let us write to denote the

vector with the values of and

replaced by variables and , and the values replaced by variables . Then

and .

Now consider the first term on the right-hand side of (45).

Since the vector is continuous

over , we have that is

uniformly over . Moreover, an integration by

parts argument as above yields that

|

|

|

for , where the right-hand side is . We

conclude that the first term on the right-hand side of (45)

is uniformly over .

Next, consider the second term on the right-hand side of (45). It follows from the discussion above that the vector is

uniformly over , so it will suffice

to show that

|

|

|

(46) |

with , for . Once

again, an integration by parts argument shows that the left-hand side

of (46) is bounded from above by

|

|

|

where a.s. and by continuity. It remains to

establish . For ,

this follows directly from assumption B5. For , we have

|

|

|

|

|

|

|

|

|

|

Using Proposition 1 of Blümlinger and Tichy (1989), differentiability

properties of , on and assumption B5, each

term on the right-hand side can be shown to be . The cases

are similar. Thus (46) follows.

{pf*}

Proof of Theorem 6

Note that we have

|

|

|

|

|

|

|

|

|

|

Now, by Proposition 8 and Skorohod’s representation

theorem, there exists a probability space supporting versions of

and which satisfy

|

|

|

|

|

|

We work with this probability space. We have

|

|

|

|

|

|

(47) |

|

|

|

Applying integration by parts as in the proof of Proposition 8, we see that the first term on the right-hand side of (47) is bounded by

|

|

|

(48) |

Since is a.s. bounded on , by continuity, and by assumption B5, (48) vanishes in probability.

Similarly, the second term on the right-hand side of (47) is

bounded by

|

|

|

which also vanishes in probability since and the two summands in the parentheses are . Thus the

left-hand side of (47) is uniformly over .