Asymptotic Theory of Bayes Factor in Stochastic Differential Equations: Part II

Trisha Maitra and Sourabh Bhattacharya

Trisha Maitra is a PhD student and Sourabh Bhattacharya

is an Associate Professor in

Interdisciplinary Statistical Research Unit, Indian Statistical

Institute, 203, B. T. Road, Kolkata 700108.

Corresponding e-mail: sourabh@isical.ac.in.

Abstract

The problem of model selection in the context of a system of stochastic differential equations (’s)

has not been touched upon in the literature. Indeed, properties of Bayes factors have not been studied even

in single based model comparison problems.

In this article, we first develop an asymptotic theory of Bayes factors when two ’s are compared,

assuming the time domain expands. Using this we then develop an asymptotic theory of Bayes factors

when systems of ’s are compared,

assuming that the number of equations in each system, as

well as the time domain, increase indefinitely.

Our asymptotic theory covers situations when the observed processes associated with the

’s are independently and identically distributed (), as well as when they are independently

but not identically distributed (non-). Quite importantly, we allow inclusion of available time-dependent

covariate information into each through a multiplicative factor of the drift function in a random effects set-up;

different initial values for the ’s are also permitted.

Thus, our general model-selection framework includes simultaneously the variable selection problem associated with

time-varying covariates, as well as choice of the part of the drift function free of covariates.

It is to be noted that given that the underlying process is wholly observed, the diffusion coefficient becomes known,

and hence is not involved in the model selection problem.

For both and non- set-ups we establish almost sure exponential convergence

of the Bayes factor. As we show, the Bayes factor is inconsistent for comparing individual ’s,

in the sense that the log-Bayes factor converges only in expectation, while

the relevant variance does not converge to zero.

Nevertheless, it has been possible to exploit this result to establish

almost sure exponential convergence of the Bayes factor when, in addition, the number of individuals

are also allowed to increase

indefinitely.

We carry out simulated and real data analyses to demonstrate that Bayes factor is a suitable candidate

for covariate selection in our models even in non-asymptotic situations.

Keywords: Bayes factor consistency; Kullback-Leibler divergence; Martingale;

Stochastic differential equations; Time-dependent covariates and random effects; Variable selection.

1 Introduction

Stochastic differential equations (’s) have important standing in statistical applications

where “within” subject variability is caused by some random component

varying continuously in time. It also seems worthwhile to incorporate available time-dependent covariate

information into the subject-wise ’s.

Apart from the covariates there may also be random effects

associated with the individuals, which may be useful in modeling variabilities between the individuals.

-based models with time-dependent covariates are considered in

Oravecz et al. (2011), Overgaard et al. (2005), Leander et al. (2015); moreover, Oravecz et al. (2011) analyse their covariate-based model in

the hierarchical Bayesian paradigm. In the literature, random effects models without covariates seem to be

more popular than those based on covariates.

A brief overview of random effects models is provided in

Delattre et al. (2013) who undertake theoretical and classical asymptotic

investigation of a class of

random effects models based on ’s. Specifically, they model the -th individual

by

(1.1)

where, for , is the initial value of the stochastic process , which

is assumed to be continuously observed on the time interval ; assumed to be known.

The function , which is the drift function, is a known, real-valued function on

( is the real line and is the dimension), and the function is the known

diffusion coefficient.

The ’s given by (1.1) are driven by independent standard Wiener processes ,

and , which are to be interpreted as the random effect parameters associated

with the individuals, which are assumed by Delattre et al. (2013) to be independent of the Brownian motions and

independently and identically distributed () random variables with some common distribution.

For the sake of convenience

Delattre et al. (2013) (see also Maitra and Bhattacharya (2016) and Maitra and Bhattacharya (2015)) assume .

Thus, the random effect is a multiplicative factor of the drift function. In this work,

we generalize this to a random effects set-up consisting of time-dependent covariates.

Note that model selection constitutes an important part of research in both Bayesian and

classical paradigms; see, for example,

Dey et al. (2000), Jiang (2007), Claeskens and Hjort (2008), Müller et al. (2013).

In the case of -based mixed effects models as well, model selection constitutes an important issue

involving the choice of the drift function and selection of the appropriate subset of (time-dependent) covariates.

Here Bayes factors are expected to play the central role as their effectiveness in model selection

in complex problems is well-established (see, for example, Kass and Raftery (1995) for a good account of Bayes factors).

Unavailability of closed form expressions in the traditional set-ups usually

prompt usage of numerical approximations based on Markov chain Monte Carlo or

related criteria such as the Akaike Information Criterion (Akaike (1973))

and Bayes Information Criterion (Schwarz (1978)). For details, see, for example, Fuchs (2013), Iacus (2008).

But we are not aware of any research existing in the literature that attempts to address covariate selection in ’s.

We are also not aware of any existing literature on asymptotic investigation of Bayes factors in the context

although Sivaganesan and Lingham (2002) present some asymptotic investigation of intrinsic

and fractional Bayes factors in the context of three specific diffusion models.

The only investigation available in this context seems to be

that of Maitra and Bhattacharya (2018), who model a multiplicative part of the drift function using time-varying covariates, and

address Bayes factor asymptotics in a general set-up consisting of the

covariate selection problem as well as selection of

the part of the drift function independent of the covariates. Different initial values

and domains of observations pertaining to different individuals, are also considered in their set-up.

Assuming that only the number of individuals increase without bound, Maitra and Bhattacharya (2018) establish

almost sure exponential convergence of Bayes factor in both and non- situations.

Here we recall that the set-up is the case when there is no covariate associated with

the model and when the initial values and the domains of observations

are the same for every individual.

The non- set-up, on the other hand, consists of time-varying covariates, different

initial values and domains of observations; in this work we also consider random effects.

Thus, unlike the case, here the model selection problem also deals with covariate selection

apart from selection of the part of the drift functions free of the covariates.

In this article, we prove almost sure exponential convergence of the relevant Bayes

factors in both and non- cases, assuming that the number

of individuals, as well as the domains of observations, increase without bound.

Hence, for our current purpose, the asymptotic theory developed by Maitra and Bhattacharya (2018) when only the number of individuals

tends to infinity, is clearly inapplicable.

Indeed, incorporation of random effects is asymptotically feasible only in our current asymptotic framework;

Maitra and Bhattacharya (2018) elucidate that inclusion of random effects does not make sense asymptotically unless the domains

of observations are also increased indefinitely.

Also, only our current asymptotic framework allows different sets of time-dependent covariates for different individuals.

It is important to remark that the diffusion coefficient becomes known once the continuous process is completely

observed; see Roberts and Stramer (2001). Hence, following Maitra and Bhattacharya (2018) we assume that the diffusion coefficient is known,

and is not involved in the model selection problem.

We begin by establishing an asymptotic theory of Bayes factor for two

competing individual ’s, and then extend the theory to systems of ’s. In this context it

is important to draw attention

to the fact that even this relatively simple problem of comparing any two individual ’s using Bayes factors

has not yet been considered in the literature.

Our investigation in this simpler case, however, faced with an apparently negative result;

the associated Bayes factor failed to be consistent in the sense that the relevant variance failed

to converge to zero, even though convergence of the log-Bayes factor in expectation is ensured.

Despite this, we have been able to utilise this result to establish almost sure exponential convergence of the

Bayes factor when the number of individuals are also allowed to increase indefinitely.

The rest of our article is structured as follows.

We begin with formalization of our set-up in Section 2, while

we provide the necessary assumptions and results in Section 3.

In Section 4

we investigate the asymptotics of Bayes factor for comparing two individual ’s.

We illustrate our results with a special case in Section 5.

In Section 6 we exploit the asymptotic theory of Bayes factors developed for

comparing individual ’s to construct a convergence theory of Bayes factors comparing

systems of ’s in both and non- cases.

In Section 7 we carry out two simulation studies to demonstrate

that Bayes factor yields the correct set of covariates in our models even in non-asymptotic

cases, and in Section 8, we model a real, company-wise national stock exchange data set,

using a system of ’s, each consisting of a plausible set of covariates,

and obtain the best possible sets of covariate combinations

for the companies, using Bayes factor.

We summarize our contributions and provide concluding remarks in Section 9.

2 Formalization of the model selection problem in the set-up when

and for every

That the systems considered by us are well-defined and the exact likelihoods are computable, are guaranteed by

assumption (H2′′) in Section 3.

For our purpose we consider the filtration (),

where . Each process is a -adapted Brownian

motion.

Here we consider the set-up where, for ,

(2.1)

and

(2.2)

where, is the initial value of the stochastic process ,

which is assumed to be continuously observed on the time interval ; .

We consider (2.1) as representing the true model and (2.2) is any other model.

It is useful to remark that we must analyze the same data set with respect to two different models for the purpose

of model selection. Hence, even though the distribution of the underlying stochastic process under the two models are different,

for notational convenience we denote the process by under both the models, relying on the context

and the model-specific parameters to naturally clarify the distinction.

2.1 Inclusion of time-dependent covariates

We model for , and , as

(2.3)

where is the set of available covariate information

corresponding to the -th individual, depending upon time . Following Maitra and Bhattacharya (2018)

we assume is continuous in ,

where is compact and

is continuous, for .

We let , and

.

Hence, for all .

2.2 The random effects set-up

In (2.1), stands for

the true parameters, and

are

the parameters associated with (2.2).

Let for all ,

where both and are compact spaces.

We also assume that for ,

where is some specified distribution on .

Hence, the above describes a random effects set-up.

Observe that if for , and for , then it reduces

to the random effects model of Delattre et al. (2013), showing that the latter is a special case of our model.

As is well-known, even though the term “prior” is not appropiate

for the random effects coefficients, operationally there is no difference between

a prior and a distribution for random effects in the Bayesian paradigm. Somewhat abusing the terminology, we continue

to refer to the distribution of the random effects coeffcients, , as the relevant prior.

2.3 Covariate and drift function selection

The key difference between our current model selection idea and that of Maitra and Bhattacharya (2018) is that

here, for every individual, there is an independent model selection problem. In other words, for each ,

one needs to choose between and . This involves selection of

perhaps different sets of covariates for different with respect to the coefficients

, and different drift functions .

Obviously, the dimensions of and are allowed to differ for each ;

likewise, for every , the dimensions of and may be different as well.

Thus, from this perspective, our current model selection framework appears to be more general compared to that

of Maitra and Bhattacharya (2018), who consider

the same set of parameters and for all the individuals, allowing only a fixed set of covariates

for every subject.

2.4 Form of the Bayes factor in our set-up

For , we

first define the following quantities:

(2.4)

for and .

Let denote the space of real continuous functions defined on ,

endowed with the -field associated with the topology of uniform convergence

on . We consider the distribution on

of given by (2.1) and (2.2) for .

We choose the dominating measure as the distribution of (2.1) and (2.2) with null

drift. So, for ,

(2.5)

where denotes the true density and stands for the other density

associated with the modeled .

For each , letting denote the -th process

observed on for any ,

(2.6)

denotes the Bayes factor associated with the -th equation of the above two systems of equations.

Assuming that the ’s (2.1) and (2.2) are independent for ,

is the Bayes factor comparing the entire systems of ’s (2.1) and (2.2).

Comparisons between a collection of different models using Bayes factor, none of which may be the true model, is

expected to favour that model which minimizes the Kullback-Leibler

divergence from the true model.

2.5 The and the non- cases

We are interested in studying the properties of in both and non- cases

when and .

In the set-up, we assume that , and ,

for and . In the non- case we relax these assumptions.

However, for simplicity, we assume

for each , even in the non- set-up, so that in our asymptotic framework we study convergence of

(2.7)

as and , where .

2.6 A key relation between and in the context

of model selection using Bayes factors

An useful relation between and which we will often make use of

in this paper is as follows.

(2.8)

with

(2.9)

Note that and

.

Also note that, for , for each ,

(2.10)

so that .

3 Requisite assumptions and results for the asymptotic theory of Bayes factor

when and

All our following assumptions and results are true for each , in particular true for each

and consequently for . For the sake of notational simplicity

we provide all the assumptions and results without mentioning at every stage.

We make the following assumptions:

(H1′′)

The parameter space such that

and are compact.

(H2′′)

For , given any , ,

, are on ;

we also assume that

and

for all , , for some .

By (H1′′) it follows as before that for ,

and

for all , for some .

Because of (H2′′) it follows from Theorem 4.4 of Mao (2011), page 61, that

for all , and any ,

(3.1)

where

Specifically, for any , we can write, as ,

(3.2)

We further assume the following conditions.

(H3′′)

is continuous

in .

(H4′′)

For and ,

and

satisfy the following:

(3.3)

and

(3.4)

where , are some constants;

are positive, continuous functions of ;

is a continuous function of ;

, are continuous in , for ,

and , are continuous in .

(H5′′)

(i) We assume that is the space of the covariates

where is compact for , and for every ,

for .

Also, we assume that are continuous in for every , so that , for every .

(ii) For , and for , we assume that the vector of covariates is related to the -th

of the -th model via

where, for , is

continuous. Notationally, when reference to the -th individual is self-explanatory,

we shall denote the function

by .

(iii) For , for , and for ,

(3.5)

and

(3.6)

as , where are real constants for .

(iv) For , and for ,

(3.7)

and

(3.8)

where and are real constants.

Remark 1

Observe that although (H4′′) is seemingly restrictive in the sense that the ratios

and

are approximately independent of the underlying stochastic process, assumption (H5′′)

attempts to compensate for the restrictions by providing a rich structure to consisting of

covariate information varying continuously with time.

Hence, assumption (H4′′) need not be viewed as restrictive.

Maitra and Bhattacharya (2018) argue that (3.5) and (3.6) hold

if one assumes that for , and

, the covariates are observed realizations

of stochastic processes that are for , for all , and that

for , the processes generating and are independent.

In other words, although we assume the covariates to be non-random, in

essence, it may be assumed and are

uncorrelated for .

In order that (H5′′) (iv) holds, one needs to further assume that

the relevant stochastic processes converge to appropriate stationary distributions.

For example, may be realizations of Markov processes which are

irreducible (with respect to some appropriate measure), aperiodic, positive recurrent and possses invariant

distributions; see, for example, Kontoyiannis and Meyn (2003).

It follows from (H5′′) (iv), that,

(3.9)

(3.10)

and

(3.11)

When is clear from the context, we shall often use the notations

, and .

Note that, (3.9), (3.10) and (3.11) are limits of expectations

with respect to the uniform distribution on . Hence, by the Cauchy-Schwartz inequality it follows that

(3.12)

The following lemmas will be useful in our proceedings. The proofs of these lemmas are provided in sections S-1, S-2 and S-3 of the supplement.

Lemma 2

The limits

, and

are continuous in .

Lemma 3

Assume (H1′′) – (H5′′). Then, the following hold:

(3.13)

(3.14)

(3.15)

(3.16)

(3.17)

(3.18)

(3.19)

(3.20)

(3.21)

In the above, denotes convergence “almost surely” as

with respect to (under ), and the expectations are also with respect to (under ).

Lemma 4

Assume (H1′′) – (H5′′). Then, the following holds:

(3.22)

4 Convergence of Bayes factor with respect to time when two individual ’s are compared

From the system of ’s defined by (2.1) and (2.2) we now consider the -th individual only.

To avoid notational complexity we denote simply by . Consequently, and

will be denoted by and , respectively. In connection with the -th individual

we consider the following two ’s:

(4.1)

and

(4.2)

For any , for , let

(4.3)

Note that and

.

We also let

(4.4)

Here we are interested in asymptotic properties of the Bayes factor, given by

(4.5)

as .

For our purpose, let us define, for any ,

(4.6)

Observe, as before, that

and .

We let

(4.7)

where, for any , denotes a path of the process from to .

For any and , we define

(4.8)

where .

Note that although the expectation is with respect to , which is not the same as ,

(4.8) is still the Kullback-Leibler divergence between and .

Also since in our case, for ,

(4.9)

it follows that

(4.10)

where and

are proper Kullback-Leibler divergences between , ,

and , , respectively.

We now define

(4.11)

The expression (4.11) easily follows using (4.9),

the relation (2.8) and (2.10).

4.1 Pseudo Kullback-Leibler property

We make the following assumption:

(H6′′)

For a fixed , the prior satisfies

(4.12)

Let us define

(4.13)

We assume the following:

(H7′′)

Given associated with (H6′′), for any , the prior satisfies

(4.14)

We refer to property (H7′′) as the pseudo Kullback-Leibler () property of the prior .

Note that, (4.11), (3.13) and (3.14) imply

(4.15)

by Lemma 4.

Provided that (4.12) holds and the prior is dominated by the Lebesgue measure,

the pseudo Kullback-Leibler ()

property holds because of continuity of (4.15)

in ensured by Lemma 2.

4.2 property

For , let be the -algebra generated by and the history of the process upto

(and including) time , and let be the posterior

of given . Also, let

(4.16)

be the posterior predictive density.

Further, for any Borel set such that , let

(4.17)

where

is the posterior restricted to the set .

We assume the following:

(H8′′)

(4.18)

whenever

(4.19)

We refer to (H8′′) as the property.

4.3 Main result on convergence of Bayes factor when two individual ’s are compared

The following lemma, proved in section S-4 of the supplement, will prove useful in proving our main theorem on convergence of Bayes factor.

Lemma 5

(4.21)

We make the following further assumption:

(H9′′)

For any ,

converges in expectation

for all sequences converging to zero as , with limit independent

of . We refer to the limiting process as . In other words,

(4.22)

for any sequence such that as .

Because of Lemma 5 it follows from (H9′′), using uniform integrability

(which is easily seen to hold because of (H1′′) – (H4′′) and (3.2)), that

converges in expectation

for all sequences converging to zero as , with limit independent

of . We refer to the limiting process as . That is,

for any ,

Note that for all sequences such that as ,

is measurable with respect to

, for all .

Hence, .

Regarding convergence of , we are now ready to present our main theorem whose proof is provided in section S-5 of the supplement.

Theorem 6

Assume the set-up and conditions (H1′′) – (H9′′).

Then

(4.27)

but

(4.28)

as .

Corollary 7

For , let , where

and are two different finite sets of parameters, perhaps with different dimensionalities,

associated with the two models

to be compared. For , let

where is the prior on .

Let denote

the Bayes factor for comparing the two models associated with and .

Assume that both

the models satisfy (H1′′) – (H9′′), and

have the pseudo Kullback-Leibler property with and respectively.

Then

(4.29)

as .

5 Illustration of our asymptotic result for comparing two individual ’s with a special case

Let the parameter space be compact, so that (H1′′) holds.

Let and satisfy

(H2′′) such that

(5.1)

so that

(5.2)

In the above, is continuous in .

Hence, (H3′′) and (H4′′) are satisfied.

We assume that the relevant covariates and the functions are such that (H5′′) holds.

which is continuous in , due to the continuity assumption of in and

Lemma 2, which guarantees continuity of

and in .

Since the right-most side of (5.13) is a continuous function of ,

it follows that (H7′′) is clearly satisfied if the prior is dominated by the Lebesgue measure.

We now verify the property (H8′′).

Recall that , since . Since

(5.14)

where , is the maximizer of in the compact set .

Hence,

(5.15)

Now, let be the conditional

density of given , the latter having density . The dominating probability measure associated with this conditional density

is , which is the same dominating probability measure associated with . Then as in Maitra and Bhattacharya (2018) we have

(5.16)

Since the first term of (4.11) is the Kullback-Leibler divergence between and , it is positive for almost all .

Hence,

(5.17)

Also, by Jensen’s inequality, .

Assuming the distribution of is dominated by the Lebesgue measure, we have .

As in Maitra and Bhattacharya (2018),

once again we argue that the compact space can be rescaled appropriately with respect to suitable reparameterization such that for all ,

.

Hence, , which finally implies in accordance with (5.17), that

. Hence, ,

showing that the property is satisfied.

To see that (H9′′) holds, first observe that it follows from the proof of Lemma 5

that

, which implies

(5.18)

Now,

(5.19)

by the mean value theorem for integrals, where , as .

Hence, using continuity of in , we obtain

(5.20)

To deal with ,

note that

for any , by the mean value theorem for integrals,

where

.

It is clear that

almost surely,

as .

Hence,

where

(5.21)

where , associated with the mean value theorem for integrals. Hence,

and , almost surely as .

Continuity of and the results

, , , almost surely,

as , in conjunction with the dominated convergence theorem exploiting boundedness of the functions

, , and , imply, using continuity of

in , that

In other words, the limit of (5.18) exists and is unique as .

Now, equations (5.19) and (5.21) along with dominated convergence theorem imply that (H9′′) holds.

Thus, all the assumptions required for Theorem 6 and Corollary 7

are satisfied.

Hence, both (4.27) and (4.29) hold.

6 Asymptotic convergence of Bayes factor in the set-up with respect to

number of individuals and time

6.1 Convergence of Bayes factor in the set-up

Although Theorem 6 fails to ensure consistency of the Bayes factor as

in the sense that the relevant variance is asymptotically positive,

the theorem is useful to prove almost sure consistency when as well as , for

both and non- situations. Theorem 8 formalizes this for the set-up,

while Theorem 12 establishes almost sure consistency of the Bayes factor

in the non- situation. Proofs of these theorems are contained in section S-6 and S-9 respectively in the supplement.

Theorem 8

Assume the set-up;

also assume that conditions (H1′′) – (H9′′) hold for each

in the systems (2.1) and (2.2). Then

(6.1)

almost surely, as and .

The following corollary is obvious.

Corollary 9

For , and ,

let , where, for each ,

and are two different finite sets of parameters, perhaps with different dimensionalities,

associated with the two systems (2.1) and (2.2)

to be compared. For , let

where is the prior on , for .

Let denote

the Bayes factor for comparing the two models associated with and .

Assume the case and suppose

that both

the systems satisfy (H1′′) – (H9′′), and

have the pseudo Kullback-Leibler property with and respectively.

Then

almost surely, as and .

6.2 Convergence of Bayes factor in the non- set-up

We now relax the assumptions and for .

Thus, we are now in a non- situation

where the processes , are independently,

but not identically distributed.

As mentioned in Section 2.1 we assume that .

In this set-up, for each ,

it holds, due to Theorem 6, that

(6.2)

as , where depends upon the initial value

and the set of time-dependent covariates

.

The following lemma shows that is continuous in .

Lemma 10

Assume the conditions of Theorem 6. Then,

is continuous in .

Now consider the following limit:

(6.3)

The following lemma shows that the above limit exists for all sequences

.

Proof of these two lemmas are provided in section S-7 and S-8 respectively in the supplement.

Now, we have the following theorem.

Theorem 12

Assume the non- set-up, and conditions (H1′′) – (H9′′), for each

in the systems (2.1) and (2.2). Then

(6.4)

almost surely, as and .

We then have the following corollary for the non- case.

Corollary 13

For , and ,

let ,

where, for each ,

and are two different finite sets of parameters, perhaps with different dimensionalities,

associated with the two systems (2.1) and (2.2)

to be compared. For , let

where is the prior on .

Let denote

the Bayes factor for comparing the two models associated with and .

Assume the non- case and suppose

that both

the systems satisfy (H1′′) – (H9′′), and

have the pseudo Kullback-Leibler property with and respectively.

Let, for ,

Then

almost surely, as and .

7 Simulation studies

7.1 Covariate selection when ,

We first demonstrate with simulation study the finite sample analogue of Bayes factor analysis

associated with a single individual, when . In this regard,

we consider modeling a single individual by

(7.1)

where we fix our diffusion coefficient as .

We consider the initial value and the time interval with .

To achieve numerical stability of the marginal likelihood corresponding to data we choose

the true values of ; as follows:

, where

. This is not to be interpreted as the prior; this

is just a means to set the true values of the parameters of the data-generating model.

We assume that the time dependent covariates satisfy the following s

(7.2)

where ; , are independent Wiener processes, and

for .

We obtain the covariates by first simulating for ,

fixing the values, and then by simulating the covariates using the s (7.2)

by discretizing the time interval into equispaced time points.

In all our applications we have standardized the covariates over time so that they have zero means

and unit variances.

Once the covariates are thus obtained, we assume that the data are generated from the (true) model where all the covariates

are present. For the true values of the parameters, we simulated from

the prior and treated the obtained values as the true set of parameters .

We then generated the data using (7.1) by discretizing the time interval

into equispaced time points.

As we have three covariates so we will have different models. Denoting

a model by the presence and absence of the respective covariates, it then is the case that

is the true, data-generating model, while , , , , ,

, and are the other possible models.

As per our theory, for a single individual, the Bayes factor is not consistent for increasing time domain.

However, we have shown that

as . Thus, the Bayes factor is consistent with respect to the expectation.

Our simulation results show that this holds even for the time domain ,

where we approximate the expectation with the average of realizations of

associated with as many simulated data sets.

7.1.1 Case 1: the true parameter set is fixed

Prior on

We first obtain the maximum likelihood estimator () of using simulated annealing

and then consider a normal prior with the as the mean and variance , where

is the identity matrix of order .

Form of the Bayes factor

In this case the related Bayes factor has the form

(7.3)

where is the true parameter set

and is the unknown set of parameters corresponding to

any other model.

Table 7.1 describes the results of our Bayes factor analyses.

Table 7.1: Bayes factor results

Model

Averaged

-2.5756029

-0.913546

-0.5454860

-0.763952

-2.5774163

-0.9312218

-0.7628154

It is clear from the 7 values of the table that the correct model is always preferred.

7.1.2 Case 2: the parameter set is random and has the prior distribution

As before, we consider the same form of the prior as in Section 7.1.1,

but with variance .

In this case we calculate marginal likelihood of the 8 possible models, and approximate

for by

averaging over replications of the data obtained from the true model.

Denoting its values by , Table 7.2 shows that

is the highest, implying consistency of the averaged Bayes factor.

Table 7.2: Averages of marginal log-likelihood

Model

-1.21923

-0.21428

1.47992

2.102966

-1.222362

-0.21898

1.459921

2.121237 (true model)

7.2 Bayes factor analysis for and

In this case we allow our parameter and the covariate sets to vary from individual to individual.

We consider individuals modeled by

(7.4)

for . We fix our diffusion coefficients as for

where . We consider the initial value and the interval , with .

As before, we generated the observed data after discretizing the time interval into equispaced time points.

Here our covariates and the parameter set

; ,

are simulated in a similar way as mentioned in Section 7.1.

For each of the individuals, the true set of covariate combination is randomly selected.

Thus, for a given model, there are sets of covariate combinations to be compared with other models

consisting of different sets of covariate combinations.

To decrease computational burden we compare the true model with other models consisting of

different sets of covariate combinations.

The Bayes factor corresponding to the -th covariate combination is given by

(7.5)

for , where , and is the true parameter set corresponding to

the -th individual.

We obtain the of the parameter sets by simulated annealing. Then we calculate the Bayes factor

with the prior such that the parameter components are independent normal with means as the respective s and variances .

In all the cases corresponding to covariate combinations we obtain

for .

Thus, Bayes factor indicated the correct covariate combination in all the cases considered.

We also considered the case when a normal prior is considered for the parameters of the true model.

In this case with respect to the component-wise independent normal prior with individual mean as obtained

from simulated annealing and component-wise variance , we obtain

(7.6)

for . Indeed, it turned out that

and the maximum of

is .

In other words, the Bayes factor consistently selects the correct model even in this situation.

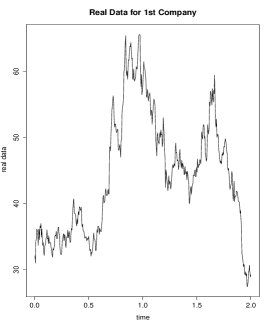

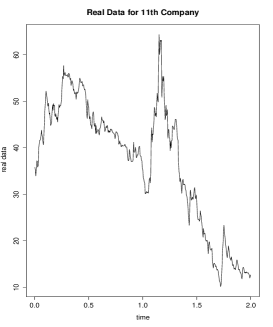

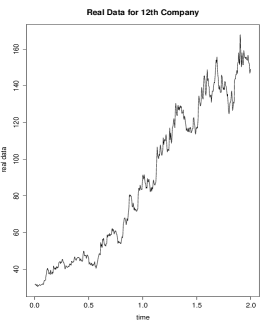

8 Company-wise data from national stock exchange

To deal with real data we collect the stock market data

( observations during the time range August , 2013, to June , 2015)

for companies which is available on

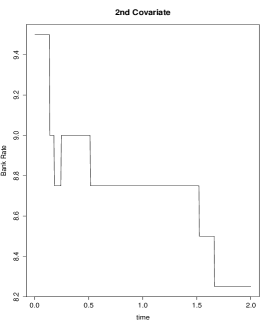

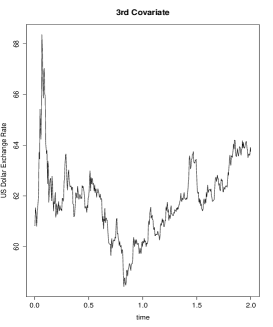

www.nseindia.com. The nature of some company-wise data are shown in Figure 8.1.

Figure 8.1: Some company-wise time-series data.

Each company-wise data is modeled by various availabe standard financial

models with the available “fitsde” package in . After obtaining the BIC (Bayesian Information Criterion)

for each company corresponding to each available financial model, we find that the minimum value of BIC corresponds to

the model, given, for process , by

As per our theory we treat the diffusion coefficient as a fixed quantity.

So, after obtaining the estimated value of the coefficients by the “fitsde” function,

we fix the values of and , so that the diffusion coefficient becomes fixed.

We let , .

In this model, we now wish to include time varying covariates.

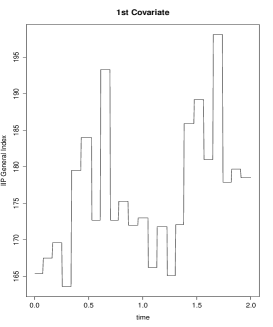

In our work we consider the “close price” of each company. The stock market data is assumed to

be dependent on IIP general index, bank interest rate, US dollar exchange rate and on various other quantities.

But we assume only these three quantities as possibly the most important time dependent covariates.

Briefly, IIP, that is, index of industrial production, is a measurement which represents

the status of production in the industrial sector for a given period of time compared to a reference period of time.

It is one of the best statistical data, which helps us measure the level of industrial activity in Indian economy.

Its importance lies in the fact that low industrial production will result in lower corporate sales and profits,

which will directly affect stock prices. So a direct impact of weak IIP data is a sudden fall in stock prices.

As the IIP data is purely industrial data, banking sector is not included in it. So,

we also consider the bank interest rate as another covariate. Note that, higher the bank interest rate,

fixed deposits become more attractive and one will preferably deposit money in bank rather than invest in stock market.

Besides, companies with a high amount of loans in their balance sheets would be affected very seriously.

Interest cost on existing debt would go up affecting their EPS (Earning per Share) and ultimately the stock prices.

But during low interest rate these companies would stand to gain. Banking sector is likely to benefit most due

to high interest rates. The Net Interest Margins (it is the difference between the interest they

earn on the money they lend and the interest they pay to the depositors) for banks is likely to

increase leading to growth in profits and the stock prices. Hence, it is clear that, the interest rates

and stock markets are inversely related. As the interest rates go up, stock market

activities tend to come down.

Finally, exchange rates directly affect the realized return on

an investment portfolio with overseas holdings. If one own stock in a foreign company and the

local currency goes up, the value of the investment also goes up.

Foreign investment is also related very much to US dollar exchange rate.

Hence, we collect the values of the aforementioned time varying covariates

during the time range August , 2013, to June , 2015. The pattern of the covariates are

displayed in Figure 8.2.

Figure 8.2: Covariates.

We denote these three covariates by respectively. Now, our considered models

for national stock exchange data associated with the companies are the

following:

(8.1)

for .

8.1 Selection of covariates by Bayes factor

Among the considered three time varying covariates we now select the best set of covariate combinations

for the companies among such sets through Bayes factor,

computing the log-marginal-likelihoods with respect to the normal prior

on the parameter set, assuming a priori independence of the parameter components

with individual means being the corresponding (based on simulated annealing)

and variance (relatively small variance ensured numerical stability of th marginal likelihood).

Table 8.1 provides the sets of covariates for the companies obtained

by our Bayes factor analysis. Also observe that each of the three covariates occurs about times

among the companies, demonstrating that overall impact of these on national stock exchange is

undeniable.

Table 8.1: Company-wise covariates obtained by Bayes factor analysis

Company

Covariates

Bank rate

US dollar exchange rate

None

None

Bank rate and US dollar exchange rate

Bank rate and US dollar exchange rate

IIP general index and US dollar exchange rate

Bank rate

IIP general index and Bank rate

IIP general index

IIP general index, Bank rate and US dollar exchange rate

IIP general index and Bank rate

US dollar exchange rate

IIP general index, Bank rate and US dollar exchange rate

IIP general index

9 Summary and discussion

This article establishes the asymptotic theory of Bayes factors when the models to be compared are

systems of ’s consisting of time-dependent covariates and random effects, assuming that the

number of individuals as well as the domains of observations of the individuals increase

indefinitely. Different initial values for different ’s are also allowed.

The only instance of related effort in this direction is that of Maitra and Bhattacharya (2018).

The main difference of our undertaking with that of Maitra and Bhattacharya (2018) is that

they assumed the domains of observations to be fixed for the individuals, a consequence

being that incorporation of random effects in their model was not possible from the asymptotic

perspective. Moreover, in their case, a single set of covariates was associated with all the individuals,

but here our random effects set-up allows different sets of time-dependent covariates for different individuals.

To proceed, we first needed to build

an asymptotic theory of Bayes factors for comparing two individual ’s, rather than two systems of ’s,

as the domain of observation expands. Our results in this regard, which help

formulate our asymptotic theory for comparing two systems of ’s using Bayes factors,

are perhaps also of independent interest, being possibly the first ever results in this direction of research.

Although the relevant variance did not converge to zero when two individual ’s are compared,

we are able to establish almost sure exponential convergence of the Bayes factor when the number of subjects are allowed to

increase indefinitely.

Importantly, our theory covers both and non- cases.

Our simulation studies associated with covariate selection demonstrate that Bayes factor yields

consistent results even in non-asymptotic situations. Bayes factor analysis of a real data on company-wise national

stock exchange also yielded plausible sets of covariates for the companies.

Note that our current asymptotic Bayes factor theory remains valid

for comparison between and non- models.

For instance, if the true model consititutes an system, then ;

the rest remains the same as the theory for our non- setting. The situation is analogous when the other model forms

an system.

Acknowledgments

We are thankful to Dr. Diganta Mukherjee for drawing our attention towards the website

www.nseindia.com at which the real data was available.

The first author gratefully acknowledges her CSIR Fellowship, Govt. of India.

Supplementary Material

Throughout, we refer to our main manuscript as MB.

S-1 Proof of Lemma 2 of MB

Due to compactness of it follows, using the form of provided in

(H5′′), that the convergences (3.9), (3.10) and (3.11) of MB are uniform over . The same form shows that the above integrals

are continuous in , for every . Hence, due to uniform convergence, the limits

, and

are continuous in .

S-2 Proof of Lemma 3 of MB

The proofs of (i) – (iv) follow from (H1′′), (H4′′), the results

(3.10) and (3.11) of MB

following from (H5′′), (3.1) and its asymptotic form (3.2) (with ),

using the relation (2.8) of MB. To prove (v),

note that, since for any ,

it holds, due to (H4′′), (3.1) of MB and boundedness of on , that for ,

it follows from Theorem 7.1 of Mao (2011), page 39, that

(S-2.1)

Hence, using Chebychev’s inequality, it follows that for any ,

(S-2.2)

In particular, if is chosen, then it

follows from the above inequality, (H4′′) , (3.2) of MB, and boundedness of

on , that

proving that

To prove (vi), first note that

(S-2.3)

for some finite constant .

The second last inequality is by Hölder’s inequality, and the last inequality

holds because

is uniformly bounded on thanks to compactness of and continuity of

the functions . Hence, for any ,

In the same way as the proof of (v), it follows, using the above inequality,

(3.3) and (3.2) of MB, that

That is,

almost surely, as . Since, as ,

by (3.10) of MB, the result follows.

Using (3.4) instead of (3.3), (vii) can be proved in the same way as (vi).

The proofs of

(viii) and (ix) follow from (v), (vi) and (vii), using the relation (2.8).

S-3 Proof of Lemma 4 of MB

Using the Cauchy-Schwartz inequality twice we obtain

(S-3.1)

Taking the limit of both sides of (S-3.1) as , using (ii) of

Lemma 3 and the limits (3.10), the result follows.

S-4 Proof of Lemma 5 of MB

For any ,

(S-4.1)

Hence, the result holds.

S-5 Proof of Theorem 6 of MB

Let us consider

(S-5.1)

where , where, given , is the

number of intervals partitioning each of length . We assume that as ,

.

It follows, using (H9′′), that for any ,

(S-5.2)

as , for any given .

Also, since due to (4.26) of MB, ,

we must have , for any .

Hence, for any .

Thus, it follows from (S-5.2), that

(S-5.3)

We now deal with the second term of the left hand side of (S-5.3).

Since, by (H6′′),

it holds that for all with probability 1,

so that

where is given by (4.19) of MB. The property implies that

the second line following from (4.15) of MB. Using Jensen’s inequality, we obtain

(S-5.7)

By (vi) – (ix) of Lemma 3 of MB, the integrand of the right hand side of the above

inequality, which we denote by , converges to

, pointwise for every , given any

path of the process in the complement of the null set.

Due to (H1′′), (H4′′) and (3.2) of MB, ,

so that is uniformly integrable. Hence,

given any path of the process in the complement of the null set.

Let us denote the left hand side of the above by let denote the right hand side.

We just proved that converges to almost surely. Now observe that

Again, due to (H1′′), (H4′′) and (3.2) of MB, the last expression is finite, proving uniform integrability

of . Hence,

It follows that

(S-5.8)

Since the above holds for arbitrary ,

it holds that

(S-5.9)

Thus (S-5.5) and (S-5.9) together help us conclude that

as .

We now show that the variance of is , as .

First note, due to compactness of , the mean value theorem for integrals

ensure existence of , depending

on the Wiener process such that

(S-5.10)

Now note that the results presented in Lemma 3 of MB continue to hold even when

is replaced with . Specifically, the following hold

in addition to the results of Lemma 3:

It follows that, as ,

By uniform integrability arguments, which follow in similar lines as the proofs of Lemmas 1 and 10 of Maitra and Bhattacharya (2018) using

(H4′′), compactness, and Cauchy-Schwartz, it holds that

(S-5.11)

Hence,

(S-5.12)

By (S-5.11), the first term of (S-5.12) goes to zero as , and

the third, covariance term tends to zero by Cauchy-Schwartz and (S-5.11). In other words,

as ,

(S-5.13)

However,

unless is constant almost surely.

It then follows from (S-5.13) that

(S-5.14)

S-6 Proof of Theorem 8 of MB

In our set-up it follows from (2.7) of MB that

(S-6.1)

In the case, given ,

using the above form, it follows by the strong law of large numbers, that

(S-6.2)

almost surely. Now, in the situation, for each ,

, as .

Hence, taking limit as on both sides of (S-6.2) yields

(S-6.3)

almost surely, proving the theorem.

S-7 Proof of Lemma 10 of MB

Note that, due to compactness of and and continuity of the covariates

in time , there exists and , such that

(S-7.1)

as , where the convergence is due to (6.2) of MB. Also, is clearly

continuous in for every (the proof of this follows in the same way as that of Theorem 5 of Maitra and Bhattacharya (2016)).

Combining this with the uniform convergence (S-7.1)

it follows that is also continuous in .

S-8 Proof of Lemma 11 of MB

Note that the limit (6.3) of MB can be represented as

(S-8.1)

where is some continuous function satisfying

for .

For the remaining points , we set ,

where is such that is continuous in . Since

is continuous in , can be thus constructed.

Note that, it is possible to relate to by some continuous mapping

, taking to .

Thus, in (6.3) of MB

is the limit of the Riemann sum (S-8.1) associated with the continuous

function ; the limit is given by the integral .

Since the domain of integration is , it follows, using continuity of ,

that the integral is finite. Observe that for any given sequence , one

can construct a continuous function such that .

In other words,

exists for all sequences .

S-9 Proof of Theorem 12 of MB

For given , it follows from (S-5.14), compactness of , , ,

and continuity of the relevant functions ,

, , , and , that

(S-9.1)

Hence, given ,

It then follows due to Kolmogorov’s strong law of large numbers for independent random variables that

(S-9.2)

almost surely.

Now observe that the right hand side of (S-9.2) admits the following representation

(S-9.3)

where is some continuous function depending upon with

.

Since is continuous in , can be constructed

as in Lemma 11 of MB. Then, for almost all , as , for appropriate

associated with via as in Lemma 11. Also, it follows from (S-5.10) that

so constructed is uniformly bounded in .

Thus, the conditions

of the dominated convergence theorem are satisfied.

Since (S-9.3) is nothing but the Riemann sum associated with , it follows that

(S-9.4)

By construction of , the dominated convergence theorem holds for the right hand side

of (S-9.4). Hence,

Akaike (1973)

Akaike, H. (1973).

Information theory and an extension of the maximum likelihood

principle.

In B. N. Petrov and F. Csaki, editors, Second International

Symposium on Information Theory, pages 267–281, Budapest. Academiai

Kiado.

Reprinted in S. Kotz and N. L. Johnson (Eds) (1992). Breakthroughs in Statistics Volume I: Foundations and Basic Theory, pp.

610–624. Springer-Verlag.

Claeskens and Hjort (2008)

Claeskens, G. and Hjort, N. L. (2008).

Model Selection and Model Averaging.

Cambridge University Press, Cambridge, UK.

Delattre et al. (2013)

Delattre, M., Genon-Catalot, V., and Samson, A. (2013).

Maximum Likelihood Estimation for Stochastic Differential

Equations with Random Effects.

Scandinavian Journal of Statistics, 40, 322–343.

Dey et al. (2000)

Dey, D. K., Ghosh, S. K., and Mallick, B. K. (2000).

Generalized Linear Models: A Bayesian Perspective.

Fuchs (2013)

Fuchs, C. (2013).

Inference for Diffusion Processes: With Applications

in Life Sciences.

Springer, New York.

Iacus (2008)

Iacus, S. M. (2008).

Simulation and Inference for Stochastic Differential

Equations: With R Examples.

Springer, New York.

Jiang (2007)

Jiang, J. (2007).

Linear and Generalized Linear Mixed Models and Their

Applications.

Springer, New York, USA.

Kass and Raftery (1995)

Kass, R. E. and Raftery, R. E. (1995).

Bayes factors.

Journal of the American Statistical Association, 90(430), 773–795.

Kontoyiannis and Meyn (2003)

Kontoyiannis, I. and Meyn, S. P. (2003).

Spectral Theory and Limit Theorems for Geometrically

Ergodic Markov Processes.

The Annals of Applied Probability, 13, 304–362.

Leander et al. (2015)

Leander, J., Almquist, J., Ahlström, C., Gabrielsson, J., and Jirstrand, M.

(2015).

Mixed Effects Modeling Using Stochastic Differential

Equations: Illustrated by Pharmacokinetic Data of Nicotinic Acid

in Obese Zucker Rats.

The AAPS Journal, 17, 586–596.

Maitra and Bhattacharya (2015)

Maitra, T. and Bhattacharya, S. (2015).

On Bayesian Asymptotics in Stochastic Differential

Equations with Random Effects.

Statistics and Probability Letters, 103, 148–159.

Also available at “http://arxiv.org/abs/1407.3971”.

Maitra and Bhattacharya (2016)

Maitra, T. and Bhattacharya, S. (2016).

On Asymptotics Related to Classical Inference in

Stochastic Differential Equations with Random Effects.

Statistics and Probability Letters, 110, 278–288.

Also available at “http://arxiv.org/abs/1407.3968”.

Maitra and Bhattacharya (2018)

Maitra, T. and Bhattacharya, S. (2018).

Asymptotic Theory of Bayes Factor in Stochastic

Differential Equations: Part I.

ArXiv Preprint.

Mao (2011)

Mao, X. (2011).

Stochastic Differential Equations and Applications.

Woodhead Publishing India Private Limited, New Delhi, India.

Müller et al. (2013)

Müller, A., Scealy, J. L., and Welsh, A. H. (2013).

Model Selection in Linear Mixed Models.

Statistical Science, 28, 135–167.

Oravecz et al. (2011)

Oravecz, Z., Tuerlinckx, F., and Vandekerckhove, J. (2011).

A hierarchical latent stochastic differential equation model for

affective dynamics.

Psychological Methods, 16, 468–490.

Overgaard et al. (2005)

Overgaard, R. V., Jonsson, N., Tornœ, C. W., and Madsen, H. (2005).

Non-Linear Mixed-Effects Models with Stochastic

Differential Equations: Implementation of an Estimation Algorithm.

Journal of Pharmacokinetics and Pharmacodynamics, 32,

85–107.

Roberts and Stramer (2001)

Roberts, G. and Stramer, O. (2001).

On Inference for Partially Observed Nonlinear Diffusion

Models Using the Metropolis-hastings Algorithm.

Biometrika, 88, 603–621.

Schwarz (1978)

Schwarz, G. (1978).

Estimating the Dimension of a Model.

The Annals of Statistics, 6, 461–464.

Sivaganesan and Lingham (2002)

Sivaganesan, S. and Lingham, R. T. (2002).

On the Asymptotic of the Intrinsic and Fractional Bayes

Factors for Testing Some Diffusion Models.

Annals of the Institute of Statistical Mathematics, 54,

500–516.