Variational Bayes with Intractable Likelihood

Abstract

Variational Bayes (VB) is rapidly becoming a popular tool for Bayesian inference in statistical modeling. However, the existing VB algorithms are restricted to cases where the likelihood is tractable, which precludes the use of VB in many interesting situations such as in state space models and in approximate Bayesian computation (ABC), where application of VB methods was previously impossible. This paper extends the scope of application of VB to cases where the likelihood is intractable, but can be estimated unbiasedly. The proposed VB method therefore makes it possible to carry out Bayesian inference in many statistical applications, including state space models and ABC. The method is generic in the sense that it can be applied to almost all statistical models without requiring too much model-based derivation, which is a drawback of many existing VB algorithms. We also show how the proposed method can be used to obtain highly accurate VB approximations of marginal posterior distributions.

Keywords. Approximate Bayesian computation, marginal likelihood, natural gradient, quasi-Monte Carlo, state space models, stochastic optimization.

1 Introduction

Let be the data and the vector of model parameters. We are interested in Bayesian inference about , based on the posterior distribution , with the prior and the likelihood function. In this paper, we are interested in Variational Bayes (VB), which is widely used as a computationally effective method for approximating the posterior distribution (Attias,, 1999; Bishop,, 2006). VB approximates the posterior by a distribution within some tractable class, such as an exponential family, chosen to minimize the Kullback-Leibler divergence between and . Most of the VB algorithms in the literature require that the likelihood can be computed analytically for any .

In many applications, however, the likelihood is intractable in the sense that it is infeasible to compute exactly at each value of , which makes it difficult to use VB for inference. For example, in state space models (Durbin and Koopman,, 2001), which are widely used in economics, finance and engineering, the likelihood is a high dimensional integral over the state variables governed by a Markov process. Ghahramani and Hinton, (2000) were the first to use VB for inference in state space models. However, they only consider the special case in which the time series is segmented into regimes with each regime assumed to follow a linear-Gaussian state space model. For general state space models, it is still a challenging problem to do inference with VB. Turner and Sahani, (2011) discuss some of the difficulties in applying VB methods to time series models. Another example of a situation where implementing VB is difficult is approximate Bayesian computation (ABC) (Tavare et al.,, 1997; Marin et al.,, 2012; Peters et al.,, 2012). ABC methods provide a way of approximating the posterior when the likelihood is difficult to compute but it is possible to simulate data from the model. We are not aware of any work that uses VB for inference in ABC, although a closely related technique called Expectation Propagation has been used (Barthelme and Chopin,, 2014). This paper proposes a VB algorithm that approximates when the likelihood is intractable. The only requirement is that the intractable likelihood can be estimated unbiasedly. The proposed algorithm therefore makes it possible to carry out variational Bayes inference in many statistical models with an intractable likelihood, where this was previously impossible.

In many models, by introducing a latent variable , the joint density is tractable. This makes it much easier to work with the joint posterior rather than the marginal posterior of interest itself. In this situation many VB algorithms in the literature approximate the joint posterior by a factorized distribution , and then use as an approximation to . The main drawback of this approach is that the (usually high) posterior dependence between and is ignored, which might lead to a poor VB approximation (Neville et al.,, 2014). Our VB algorithm approximates directly with the latent variable integrated out and thus overcomes this drawback; see the example in Section 5.1.

Section 2 presents our approach, which we call Variational Bayes with Intractable Likelihood (VBIL), when the likelihood can be estimated unbiasedly. VBIL transforms the problem of approximating the posterior into a stochastic optimization problem using a noisy gradient. It is essential for the success of stochastic optimization algorithms to have a gradient estimator with a sufficiently small variance. Section 3 describes several techniques, including control variate and quasi-Monte Carlo, for variance reduction in estimating the gradient. This section also discusses the importance of the natural gradient (Amari,, 1998), which takes into account the geometry of the variational distribution being learned.

Unlike many VB algorithms that are derived on a model-by-model basis and require analytical computation of some model-based expectations, one of the main advantages of VBIL is that it can be applied to almost all statistical models without requiring an analytical solution to model-based expectations. The only requirement is that we are able to estimate the intractable likelihood unbiasedly. The VBIL methodology is therefore generic and widely applicable. As a by-product, VBIL provides an estimate of the marginal likelihood, which is useful for model choice.

There are several lines of work related to ours in terms of working with an intractable likelihood. Beaumont, (2003) and Andrieu and Roberts, (2009) show that Markov chain Monte Carlo simulation based on an unbiased estimator of the likelihood is still able to generate samples from the posterior. This method is known in the literature as Pseudo-Marginal Metropolis-Hasting (PMMH). More efficient variants of PMMH, called correlated PMMH and blockwise PMMH, have been proposed recently (Deligiannidis et al.,, 2015; Tran et al.,, 2016). Tran et al., (2013) show that importance sampling with the likelihood replaced by its unbiased estimator is still valid for estimating expectations with respect to the posterior, and name their method as Importance Sampling Squared (). Also, Duan and Fulop, (2013) and Tran et al., (2014) use sequential Monte Carlo for inference based on an unbiased likelihood estimator. The main advantage of VBIL is that it is several orders of magnitude faster than these competitors.

Section 4 studies the link between the precision of the likelihood estimator to the variance of the VBIL estimator. This helps to understand how much accuracy is lost when working with an estimated likelihood compared to the case the likelihood is available. In this spirit, Pitt et al., (2012) and Tran et al., (2013) show that the asymptotic variance of PMMH and estimators increases exponentially with the variance of the likelihood estimator. Therefore, it is critical for these methods to have a likelihood estimator that is accurate enough. They show that the variance of the likelihood estimator should be around 1 in order to minimize the computing time that is needed for the variance of PMMH/ estimators to have a fixed precision. For VBIL, we show that the asymptotic variance of VBIL estimators increases linearly with the variance of the likelihood estimator. The proposed methodology is therefore useful in cases when only highly variable estimates of the likelihood are available. We discuss such a situation in Section 5.1 where VBIL works well while its competitors fail.

Several interesting applications of VBIL are presented in Section 5. Section 5.1 shows the use of VBIL for generalized linear mixed models and demonstrates the high accuracy of VBIL compared to the existing VB algorithms. Section 5.2 applies VBIL to Bayesian inference in state space models and Section 5.3 shows how VBIL can be used for ABC. To the best of our knowledge, our paper is the first to use a VB method in the most general way for Bayesian inference in state space models and ABC. Another interesting application of VBIL is presented in Section 5.4, in which we illustrate that VBIL provides an attractive way to improve the accuracy of VB approximations of marginal posteriors.

2 Variational Bayes with an intractable likelihood

This section describes the basic form of the proposed VBIL algorithm, where an unbiased estimator of the likelihood is available. Denote by an unbiased estimator of the likelihood . Here is an algorithmic parameter relating to the precision in estimating the likelihood, such as the number of samples if the likelihood is estimated by importance sampling or the number of particles if the likelihood in state space models is estimated by a particle filter. Using the terminology in Pitt et al., (2012), we refer to as the number of particles. Let , so that , and denote by the density of . Note that is unknown as we do not know and there is no need to compute in practice, but, as will become clear shortly, it is very convenient to work with . We sometimes write as . We note that because of the unbiasedness of the estimator . Define the following density on the extended space

This augmented density admits the posterior of interest as its marginal. It is useful to work with as the high-dimensional vector of random variables involved in estimating the likelihood is transformed into the scalar . A direct approximation of is , where is the variational distribution with the variational parameter to be estimated, and then can be used as an approximation of . However, it turns out that it is impossible to estimate the gradient of the Kullback-Leibler divergence between and as this requires knowing .

We propose instead to approximate by . This augmented density has the attractive features that is its marginal for and it is possible to estimate the gradient of the Kullback-Leibler divergence KL() between and (c.f. (2) below). Although does not provide a good approximation of the posterior marginal of , the latter is not of interest to us. Furthermore, under Assumptions 1 and 2 given in Section 4, the minimization of KL() is equivalent to the minimization of the KL divergence between and .

The Kullback-Leibler divergence between and is

| (1) |

where we omit to indicate dependence on for notational convenience. The gradient of is

| (2) | |||||

Here, we have used the facts that and that . It follows from (2) that, by generating and , it is straightforward to obtain an unbiased estimator of the gradient . Therefore, we can use stochastic optimization to optimize . We note that the unknown is implicitly generated when the unbiased likelihood estimator is computed. In practice, is never dealt with explicitly and it only plays a theoretical role in the mathematical derivations. The basic algorithm is as follows

Algorithm 1.

-

•

Initialize and stop the following iteration if the stopping criterion is met.

-

•

For , compute .

We will refer to this algorithm as Variational Bayes with Intractable Likelihood (VBIL). The sequence should satisfy , and . We choose in this paper. It is also possible to train adaptively.

It is important to note that each iteration is parallelizable, as the gradient is estimated by independent samples from .

2.1 Stopping criterion and marginal likelihood estimation

An easy-to-implement stopping rule is to stop the updating procedure if the change between and , e.g. in terms of the Euclidean distance, is less than some threshold (Ranganath et al.,, 2014). However, it is difficult to select as such a distance depends on the scales and the length of the vector . It is easy to show that

| (3) |

where

| (4) | |||||

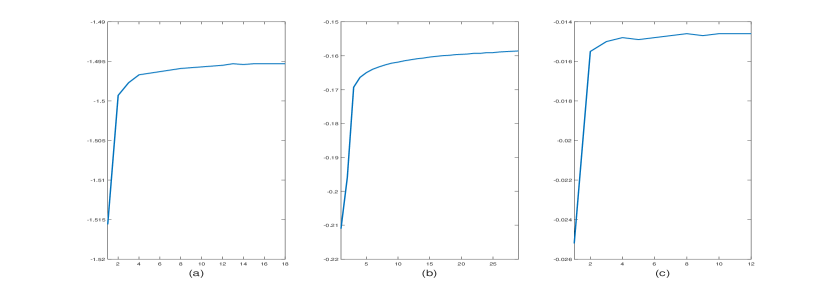

is the lower bound on the log of the marginal likelihood . This lower bound after convergence can be used as an approximation to , which is useful for model selection purposes. The expectation of the first two terms in (4) can be computed analytically, while the last term can be estimated unbiasedly by samples from . However, in our experience, estimating the entire expectation (4) based on samples from leads to a smaller variance. Denote by the resulting unbiased estimate of . Although is strictly non-decreasing over iterations, its sample estimate might not be. To account for this, we suggest to stop the updating procedure if the change in an averaged value of the lower bounds over a window of iterations, , is less than some threshold . At convergence, the values stay the same, therefore will average out the noise in and is stable. Furthermore, we suggest to replace by a scaled version of it, with the size of the dataset such as the number of observations. The scaled lower bound is more or less independent of the size of the dataset (c.f., Figure 3). We set and in this paper.

3 Variance reduction and natural gradient

As is typical of stochastic optimization algorithms, the performance of Algorithm 1 depends greatly on the variance of the noisy gradient. This section describes several techniques for variance reduction.

3.1 Control variate

Denote for notational simplicity. Let and , , be samples from the variational distribution . A naive estimator of the th element of is

| (5) |

whose variance is often too large to be useful. For any number , consider

| (6) |

which is still an unbiased estimator of since , whose variance can be greatly reduced by an appropriate choice of . Similar ideas are considered in the literature, see Paisley et al., (2012), Nott et al., (2012) and Ranganath et al., (2014). The variance of is

The optimal that minimizes this variance is

| (7) |

Then

where is the correlation between and . Often, is very close to 1.

We estimate the numbers by samples as in (7). In order to ensure the unbiasedness of the gradient estimator, the samples used to estimate must be independent of the samples used to estimate the gradient. In practice, the can be updated sequentially as follows. At iteration , we use the computed in the previous iteration , i.e. based on the samples from , to estimate the gradient , which is estimated using new samples from . We then update the using this new set of samples. By doing so, the unbiasedness is guaranteed while no extra samples are needed in updating the numbers .

The gradient in the form of (2) can be written as a sum of two terms, where the first term can be in most cases computed analytically. However, as pointed out by a referee, this term should be estimated using the same samples of as we do in (6). Doing so helps to reduce the noises in estimating the gradient. This is because the first term plays the role of a control variate. This phenomenon is discussed in detail in Salimans and Knowles, (2013).

3.2 Natural gradient

Intuitively, a different learning rate should be used for each scale in the gradient vector. That is, the traditional gradient vector should be multiplied by an appropriate scale matrix. It is well-known that the traditional gradient defined on the Euclidean space does not adequately capture the geometry of the variational distribution (Amari,, 1998). A small Euclidean distance between and does not necessarily mean a small Kullback-Leibler divergence between and . Amari, (1998) defines the natural gradient as

| (8) |

with the Fisher information matrix, and suggests using the natural gradient as an efficient alternative to the traditional gradient. See also Hoffman et al., (2013).

If the variational distribution has the exponential family form

| (9) |

with the vector of sufficient statistics and the vector of natural parameters, then is computed analytically.

The use of the natural gradient in VB algorithms is considered, among others, by Honkela et al., (2010), Hoffman et al., (2013) and Salimans and Knowles, (2013). We demonstrate the importance of the natural gradient using a simple example where the likelihood is available. We consider a model where the data - the Bernoulli distribution with probability . We generate observations from and obtain . We use a uniform prior on . Then, the posterior is Beta(). The variational distribution is chosen to be Beta() which belongs to the exponential family with the natural parameter . The Fisher information matrix is

where is the trigamma function. In this simple example, the gradient in (2) can be computed analytically

with

Using the traditional gradient, the update in Algorithm 1 is

Using the natural gradient, the update is

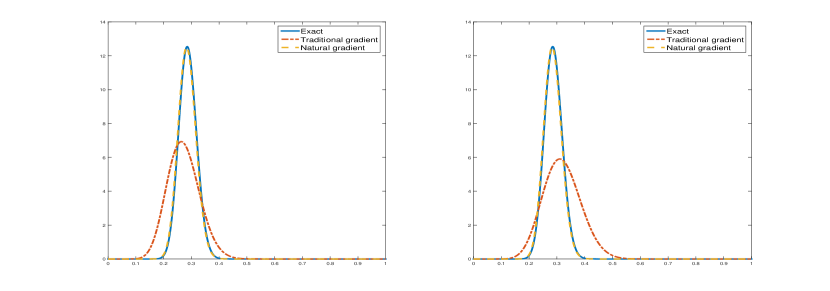

Figure 1 plots the densities of the exact posterior and the variational distributions estimated by the VBIL using the traditional gradient and the natural gradient, with two different random initializations. The figure shows that the VBIL algorithm using the natural gradient is superior to using the traditional gradient. Furthermore, the VBIL algorithm based on the natural gradient is insensitive to the initial .

3.3 Factorized variational distribution

Often, the variational distribution is factorized into factors

| (10) |

Then, each factor is updated separately and the variance of the estimate of the corresponding gradient can be reduced. Salimans and Knowles, (2013) and Ranganath et al., (2014) consider variance reduction using factorization. Denote by the terms in that involve only and . From (2), and noting that , the traditional gradient corresponding to factor is

| (11) |

In the case belongs to an exponential family, the natural gradient corresponding to factor is

| (12) |

where is the Fisher information matrix of distribution .

3.4 Randomised quasi-Monte Carlo

Numerical integration using quasi-Monte Carlo (QMC) has been proven efficient in many applications. Instead of generating uniform random numbers as in plain Monte Carlo methods, QMC generates deterministic sequences that are more evenly distributed in (0,1) in the sense that they minimise the so-called star-discrepancy. Dick and Pillichshammer, (2010) provide an extensive background on QMC. It is shown that, in many cases, QMC integration achieves a better convergence rate than Monte Carlo integration. In this paper, we use randomised quasi-Monte Carlo (RQMC) as VBIL requires an unbiased estimator of the gradient. By introducing a random element into a QMC sequence, RQMC preserves the low-discrepancy property and, at the same time, leads to unbiased estimators (Owen,, 1997; Dick and Pillichshammer,, 2010).

Here, we use RQMC to sample . This will help to reduce the variance of the noisy gradient if the dimension of is not too high. Of course, one can also use RQMC in the likelihood estimation, but given some time constraint we do not pursue this idea in this paper.

4 The effect of estimating the likelihood

This section studies the effect of the variance of the noisy likelihood on the VBIL estimators, and provides guidelines for selecting the number of particles . A large gives a precise likelihood estimate and therefore an accurate estimate of , but at a greater computational cost. A small leads to a large variance of the likelihood estimator, so a larger number of iterations is needed for the procedure to settle down. It is therefore useful in practice to have some guidelines for selecting .

In order to understand the effect of estimating the likelihood, we follow Pitt et al., (2012) and make the following assumption.

Assumption 1.

There is a function such that and .

More precisely, Pitt et al., (2012) assume further that in order to derive a theory for selecting an optimal . This assumption is justified in Tran et al., (2013) and Doucet et al., (2015) making use of the unbiasedness of the likelihood estimate. The reason that the mean of is times its variance is because in order for the likelihood estimator to be unbiased.

Assumption 2.

For a given , let be a function of and such that , i.e. . Then and .

Suppose that the equation , with in (1), has the unique solution . Let be the estimator of obtained by Algorithm 1 or 2 after iterations, and be the corresponding estimator obtained when the exact likelihood is available. Denote and denote by and the expectation and variance operators with respect to . For simplicity, we consider the case that is scalar; the case with a multivariate can be obtained using Theorem 5 of Sacks, (1958). We obtain the following results whose proof is in the Appendix.

Theorem 1.

Suppose that Assumptions 1 and 2 are satisfied,

and that the regularity conditions in Theorem 1 of Sacks, (1958) hold.

(i) Then,

| (13) |

where is a positive constant that depends only on geometric properties of the function

and is independent of the random variables involving in estimating , i.e. is independent of .

(ii) Let be the asymptotic variance of as .

Similarly, let be the asymptotic variance of .

Then,

| (14) |

where if the noisy traditional gradient is used, and if the noisy natural gradient in (8) is used.

These results show that the variance of VBIL estimators increases linearly with . For PMMH and estimators, Pitt et al., (2012) and Tran et al., (2013) show that their variances increase exponentially with . This means that VBIL is useful in cases where only a rough estimate of the likelihood is available, or it is expensive to obtain an accurate estimate of the likelihood.

We now discuss the issue of selecting . We note that under Assumption 2, is tuned depending on as , so the time to compute the likelihood estimate is proportional to . Then, Pitt et al., (2012) and Tran et al., (2013) show that, for the PMMH and methods, the optimal that gives an optimal trade-off between the CPU time and the variance of the estimators is 1. For VBIL, the computing time can be defined as

| (15) |

where neither nor depends on . These results suggest that should be set to a large value, as long as it is not too large for the stochastic search procedure in Algorithms 1 and 2 to converge.

5 Applications

5.1 Application to generalized linear mixed models and panel data models

Generalized linear mixed models (GLMM) (see, e.g. Fitzmaurice et al.,, 2011), also known as panel data models, use a vector of random effects to account for the dependence between the observations measured on the same individual . Given the random effects , the conditional density belongs to an exponential family. The joint likelihood function of the model parameters and the random effects , is tractable

Typically in the VB literature the joint posterior is approximated by a variational distribution of the form , and then is used as an approximation to the marginal posterior . For example, Tan and Nott, (2013) take this approach but use partially non-centered parameterizations to reduce dependence between parameter blocks. Ormerod and Wand, (2012) consider frequentist estimation of , but using VB methods to integrate out . As discussed in the introduction, factorization of the VB distribution generally ignores the posterior dependence between and , which often leads to underestimating the variance in the posterior distribution of . Below, we refer to such a VB method as classical VB.

The likelihood, with an integral over the random effects , is in most cases analytically intractable but can be easily estimated unbiasedly using importance sampling. Let be an importance density for . The integral is estimated unbiasedly by

| (16) |

It is possible to use different for each . Hence, is an unbiased estimator of the likelihood . The variance of is

| (17) |

which can be estimated by with

| (18) |

Given a fixed , it is therefore straightforward to target by selecting such that .

Six City data

We now illustrate the VBIL algorithm using the Six City data in Fitzmaurice and Laird, (1993). The data consist of binary responses which indicate the wheezing status (1 if wheezing, 0 if not wheezing) of the th child at time-point , and . Covariates are the age of the child at time-point , centered at 9 years, and the maternal smoking status (0 or 1). We consider the following logistic regression model with a random intercept

The model parameters are . We use a normal prior for and a Gamma prior for .

We use the variational distribution , where is a variate normal and is an inverse gamma distribution. We then run Algorithm 2, see the Appendix for the detail, with samples to estimate the gradient. The likelihood is estimated as in (16) with the natural sampler , which is the normal distribution in our case. The in Section 4 is set to , which on average requires particles. Using a larger will lead to too small that makes the estimate in (18) unreliable. Figure 3(a) plots the scaled lower bounds over the iterations.

We compare the performance of the classical VB and VBIL algorithms to the pseudo-marginal MCMC simulation (Andrieu and Roberts,, 2009). We set as suggested in Pitt et al., (2012). The MCMC chain, based on the adaptive random walk Metropolis-Hastings algorithm in Haario et al., (2001), consists of 20000 iterates with another 10000 iterates used as burn-in.

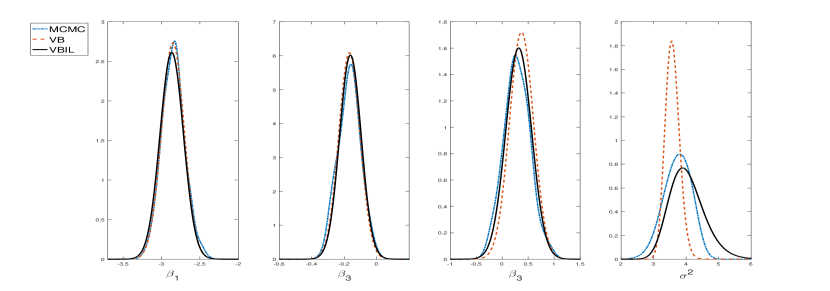

Figure 2 plots the classical VB estimates (dashed line), MCMC estimates (dotted line) and the VBIL estimates (solid line) of the marginal posteriors and . The MCMC density estimates are carried out using the kernel density estimation method based on the built-in Matlab function ksdensity. The figure shows that the VBIL estimates are very close to the MCMC estimates. The classical VB underestimates the posterior variance of in this example. The clock times taken to run the VB, VBIL and MCMC procedures are 4, 2.9 and 505 minutes respectively. However, we note that the running time depends on many factors such as the programming language being used and the initialization of the procedures. All the examples in this paper are run on an Intel Core 16 i7 3.2GHz desktop supported by the Matlab Parallel Toolbox with 8 local processors. Obviously, the more processors we have, the faster the VBIL procerdure is.

Large data example

One of the main advantages of VBIL is its scalability, i.e. it is applicable in large data cases. This section describes a scenario where it is difficult to use the PMMH and methods. Consider a large data case with a large number of panels . From (17), for fixed , the variance of the log-likelihood estimator increases linearly with . Therefore, when is large enough, the PMMH and methods will not work in a practical sense, because can be very large (Flury and Shephard,, 2011). In this GLMM setting, PMMH and do not work when is as large as 6 or 7. One can decrease by increasing , but this can be too computationally expensive to be practical.

We generate a data set of from the following logistic model with a random intercept

| (19) | |||||

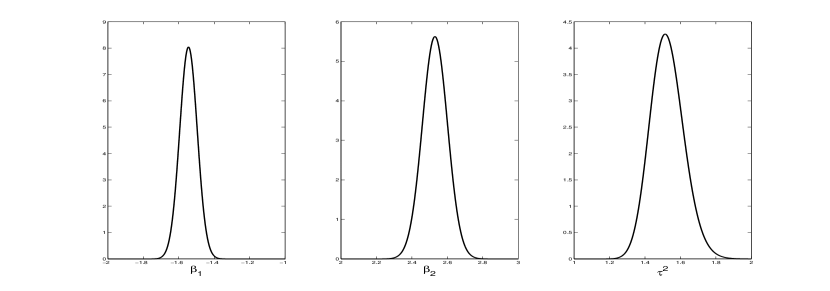

with , . It takes, on average across different , 30 seconds to carry out each likelihood estimation with the numbers of particles tuned to target , which requires particles. So if an optimal PMMH procedure was run on our computer to generate a chain of 30000 iterations as done in the Six City data example, it would take 10.4 days. We now run VBIL with set to 30, which on average requires particles and 0.7 seconds for each likelihood estimation. The VBIL procedure stopped after 15 iterations with the clock time taken was 23 minutes. Figure 4 plots the variational approximations of the marginal posteriors, which are bell shaped as expected with a large dataset.

5.2 Application to state space models

In state space models, the observations are observed in time order. At time , the distribution of conditional on a state variable is independently distributed as

and the state variables are a Markov chain with

The likelihood of the data is given by

| (20) |

with and

Given a value of , the likelihood can be unbiasedly estimated by an importance sampling estimator (Shephard and Pitt,, 1997; Durbin and Koopman,, 1997) or by a particle filter estimator (Del Moral,, 2004; Pitt et al.,, 2012), , with the number of particles.

An important example of state space models is the stochastic volatility (SV) model. The time series data is modeled as

with and . Let ; we will estimate but report results for . The model parameters are . We follow Kim et al., (1998) and use a normal prior for , a Beta prior for and an inverse gamma IG(2.5,0.025) for .

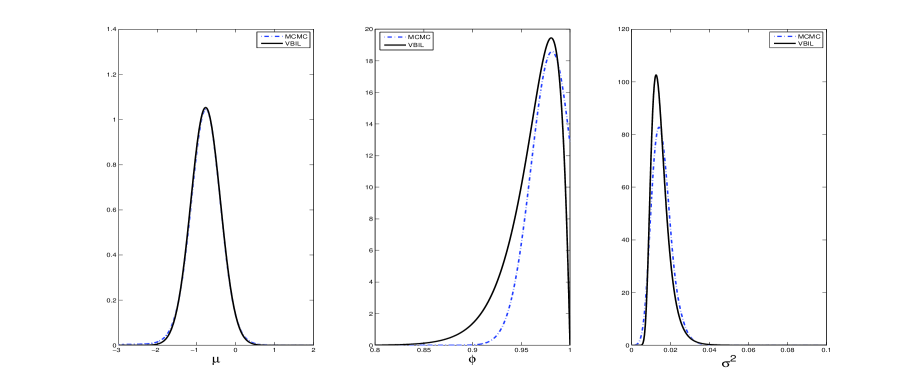

To illustrate the VBIL algorithm for state space models, we analyze the weekday close exchange rates for the Australian Dollar/US Dollar from 5/1/2010 to 31/12/2013. The data are available from the Reserve Bank of Australia. The data is

We use the variational distribution , where is , is Beta and is inverse gamma IG. We employ the constraint and to make sure that has a mode. The likelihood estimator is computed by a basic particle filter. We then run the VBIL algorithm with samples, starting with , , . This initial point is set so that the initial mean values of and are and respectively, which is pretty far away from the posterior means; see Figure 5. The VBIL algorithm stops after 28 iterations. Figure 3(b) plots the scaled lower bounds over the iterations.

The VBIL is compared to pseudo-marginal MCMC simulation, based on an adaptive random walk Metropolis-Hastings algorithm, with 100,000 iterations starting from the same values , and . The number of particles used in MCMC is fixed at , so that at the initial value . The number of particles used in VBIL is fixed at as the use of randomised QMC for generating helps reduce greatly the variance in estimating the gradient. We fix in this example as it is difficult to estimate the variance of log-likelihood estimates obtained by the particle filter.

Figure 5 plots the MCMC estimates (dotted line) and the VBIL estimates (solid line) of the marginal posteriors. The figure shows that the VBIL estimates are close to the MCMC estimates but consume significantly less computational resources. The CPU times taken to run the VBIL and MCMC procedures are 0.7 and 28 minutes respectively.

5.3 Application to ABC

In many modern applications, such as in genetics (Tavare et al.,, 1997), we either cannot evaluate the likelihood pointwise or do not wish to do so, but we can sample from it, i.e. we can simulate . Approximate Bayesian computation (Tavare et al.,, 1997) approximates the likelihood by

| (21) |

where is a kernel with the bandwidth and is a vector of summary statistics. Inference is then based on the approximate posterior . Because the likelihood-free function can be unbiasedly estimated by

it is straightforward to use the VBIL algorithm to approximate .

We illustrate the application of the VBIL algorithm to ABC by using it to fit an -stable distribution. -stable distributions (Nolan,, 2007) are a class of heavy-tailed distributions used in many statistical applications. An -stable distribution is parameterized by the stability parameter , skewness , scale and location . The main difficulty when working with -stable distributions is that they do not have closed form densities, which makes it difficult to do inference. However, as it is easy to sample from an -stable distribution, one can use ABC techniques for Bayesian inference (Peters et al.,, 2012). We illustrate in this example that VBIL provides an efficient approach for fitting -stable distributions.

We generate a data set with observations from a univariate -stable distribution . Let be the th quantile of a pseudo-data set generated from . We follow Peters et al., (2012) and use the summary statistics with

For the observed data , the parameter in is estimated using McCulloch’s method (McCulloch,, 1986). As the parameterization is discontinuous at , resulting in poor estimates of the summary statistics, we consider the case with and restrict the support of to the interval as in Peters et al., (2012).

We reparameterize

and estimate but report the results for . We use a normal prior and approximate the posterior by a normal variational distribution . One can work with the original parameterization and use some form of factorization . We choose to work with to account for the posterior dependence between the parameters. This also illustrates the flexibility of the VBIL method in the sense that it can be used without requiring factorization.

We use the Gaussian kernel with covariance matrix for the likelihood-free in (21). The VBIL is compared to pseudo-marginal Metropolis-Hastings methods with 20,000 iterations after 5000 burnins. For the standard PMMH (Andrieu and Roberts,, 2009), the number of pseudo-data sets is selected set after some trials in order to have a well-mixing chain. Efficient versions of PMMH has been proposed recently, which are more tolerant of noise in the likelihood estimates. Here we compare VBIL to the blockwise PMMH method of Tran et al., (2016). For the blockwise PMMH, we set . We also use this value of in VBIL. Table 1 shows the VBIL and MCMC estimates, and the CPU times. As shown, VBIL is orders of magnitude faster than MCMC in this example. Figure 3(c) plots the scaled lower bounds over the iterations.

| True | Standard PMMH | Blockwise PMMH | VBIL | |

|---|---|---|---|---|

| 1.5 | 1.57 (0.15) | 1.58 (0.14) | 1.57 (0.11) | |

| 0.5 | 0.46 (0.21) | 0.45 (0.21) | 0.48 (0.16) | |

| 1 | 1.04 (0.12) | 1.04 (0.12) | 1.02 (0.12) | |

| 0 | -0.08 (0.21) | -0.09 (0.18) | -0.08 (0.14) | |

| CPU time (min) | 12.56 | 7.62 | 0.12 |

5.4 Using VBIL to improve marginal posterior estimates

A drawback of VB methods in general is that the factorization assumption as in (10) ignores the posterior dependence between the factors, which might lead to poor approximations of the posterior variances (Neville et al.,, 2014). We now show how the VBIL algorithm can be used to help overcome this problem.

Suppose that we would like to have a highly accurate VB approximation to the marginal posterior . We restrict ourselves to the case with a tractable likelihood for simplicity, but the following discussion also applies when the likelihood is intractable. The likelihood of ,

| (22) |

with , is in general intractable but can be estimated unbiasedly. Let be an approximation to the marginal posterior resulting from a classical VB method that uses the factorization (10). The integral in (22) can be estimated unbiasedly using importance sampling with the proposal density or a tail-flattened version of it. This is accurate enough in practice because VBIL does not require a very accurate estimate of as discussed in Section 4. The VBIL algorithm can then be used to approximate the marginal posterior directly with integrated out. The resulting approximation is often highly accurate as the dependence between and is taken into account.

A formal justification is as follows. We use the notation as in (10) and write . Suppose that we estimate the marginal posterior of by which belongs to a family . VBIL proceeds by minimizing

over . Let be the VBIL estimator. Under Assumptions 1 and 2 or when the number of samples used to estimate (22) is large enough, is guaranteed to be a minimizer of . Assume further that is convex, then

| (23) |

If we use a VB procedure with a factorization of the form where belongs to the same family , then VB proceeds by minimizing the KL divergence

| (24) | |||||

Let be a minimizer of (24). Because of the decomposition in (24), the estimator is not necessarily the minimizer of . From (23),

| (25) |

So the VBIL estimator is no worse than the factorization-based VB estimator in terms of KL divergence.

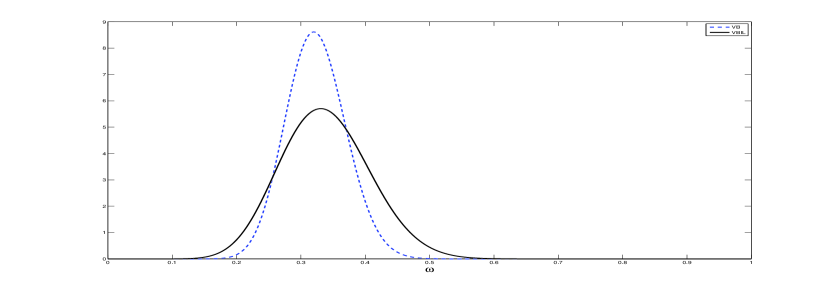

We illustrate this application by generating observations from a univariate mixture of two normals

with , , , and . Suppose that we are interested in getting an accurate variational approximation of the posterior . Getting an accurate estimate of is often more challenging than the other parameters. We use diffuse priors , , , and , and run VBIL to approximate by a Beta distribution. We use the VB algorithm of McGrory and Titterington, (2007), in which the variational distribution is factorized as , to design the proposal density to obtain an importance sampling estimator of .

Figure 6 plots the McGrory-Titterington estimate (dashed line) and VBIL estimate (solid line) of the posterior . As shown, the VBIL estimate has heavier tails than the VB estimate. By (25), it follows that the difference between the two estimates gives an indication of the extent to which the McGrory-Titterington estimate is suboptimal. This example shows that the VBIL method provides an attractive way to obtain accurate approximation of marginal posteriors.

6 Conclusion

We have proposed the VBIL, a useful VB algorithm for Bayesian inference in statistical modeling where the likelihood is intractable. The method makes it possible to do inference in statistical models using VB in some situations where that was previously impossible. The main advantage of VBIL over its competitors, such as PMMH and , is its scalability. We show in the examples that VBIL is several orders of magnitude faster than these existing methods.

Acknowledgement

The research of Tran and Kohn was partially supported by the ARC COE grant CE140100049. Nott’s research was supported by a Singapore Ministry of Education Academic Research Fund Tier 2 grant (R-155-000-143-112).

Appendix

Proof of Theorem 1.

(i) Under Assumptions 1 and 2, we have that

| (26) |

where is the Kullback-Leibler divergence between the variational distribution and the posterior .

So, is independent of , and minimizing with respect to is equivalent to minimizing .

Algorithm 1 and 2 are the Robbins-Monro procedure for finding the root of the equation .

Then, (13) follows from Theorem 1 of Sacks, (1958)

with the constant independent of .

(ii) Denote .

We consider the case with the noisy traditional gradient in (6);

the proof for the other cases is similar.

We denote by the noisy gradient obtained when the likelihood is available.

Then, noting that ,

the constant in (7) is

We note that is the control variate constant we would use to compute if the likelihood was known.

Therefore,

∎

Derivation for Section 5.1

The density of the variate normal is

A simplified form of the inverse Fisher matrix for a multivariate normal under the natural parameterization is given in Wand, (2014). For a matrix , denote by the -vector obtained by stacking the columns of , by the -vector obtained by stacking the columns of the lower triangular part of . The duplication matrix of order , , is the matrix of zeros and ones such that for any symmetric matrix

Let be the Moore-Penrose inverse of , and be the inverse of the operator vec. Then, the exponential family form of the normal distribution is with

| (27) |

The usual mean and variance parameterization is

Wand, (2014) derives the following very useful formula

| (28) |

with

where is the Kronecker product and the identity matrix of order . The gradient is

| (29) |

For the inverse gamma distribution with density

the natural parameters are . The Fisher information matrix for the inverse gamma is

and the gradient

References

- Amari, (1998) Amari, S. (1998). Natural gradient works efficiently in learning. Neural computation, 10(2):251–276.

- Andrieu et al., (2010) Andrieu, C., Doucet, A., and Holenstein, R. (2010). Particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society, Series B, 72:1–33.

- Andrieu and Roberts, (2009) Andrieu, C. and Roberts, G. (2009). The pseudo-marginal approach for efficient Monte Carlo computations. The Annals of Statistics, 37:697–725.

- Attias, (1999) Attias, H. (1999). Inferring parameters and structure of latent variable models by variational Bayes. In Proceedings of the 15th Conference on Uncertainty in Artificial Intelligence, pages 21–30.

- Barthelme and Chopin, (2014) Barthelme, S. and Chopin, N. (2014). Expectation propagation for likelihood-free inference. Journal of the American Statistical Association, 109(505):315–333.

- Beaumont, (2003) Beaumont, M. A. (2003). Estimation of population growth or decline in genetically monitored populations. Genetics, 164:1139–1160.

- Bishop, (2006) Bishop, C. M. (2006). Pattern Recognition and Machine Learning. New York: Springer.

- Del Moral, (2004) Del Moral, P. (2004). Feynman-Kac Formulae: Genealogical and Interacting Particle Systems with Applications. Springer, New York.

- Deligiannidis et al., (2015) Deligiannidis, G., Doucet, A., and Pitt, M. (2015). The correlated pseudo-marginal method. Technical report. arXiv:1511.04992v3.

- Dick and Pillichshammer, (2010) Dick, J. and Pillichshammer, F. (2010). Digital nets and sequences. Discrepancy theory and quasi-Monte Carlo integration. Cambridge University Press, Cambridge.

- Doucet et al., (2015) Doucet, A., Pitt, M. K., Deligiannidis, G., and Kohn, R. (2015). Efficient implementation of Markov chain Monte Carlo when using an unbiased likelihood estimator. arXiv:1210.1871.

- Duan and Fulop, (2013) Duan, J.-C. and Fulop, A. (2013). Density-tempered marginalized sequential Monte Carlo sampler. Technical report, National University of Singapore. Available at http://dx.doi.org/10.2139/ssrn.1837772.

- Durbin and Koopman, (1997) Durbin, J. and Koopman, S. J. (1997). Monte Carlo maximum likelihood estimation for non-Gaussian state space models. Biometrika, 84:669–684.

- Durbin and Koopman, (2001) Durbin, J. and Koopman, S. J. (2001). Time Series Analysis by State Space Methods. Oxford University Press.

- Fitzmaurice and Laird, (1993) Fitzmaurice, G. M. and Laird, N. M. (1993). A likelihood-based method for analysing longitudinal binary responses. Biometrika, 80(1):141–151.

- Fitzmaurice et al., (2011) Fitzmaurice, G. M., Laird, N. M., and Ware, J. H. (2011). Applied Longitudinal Analysis. John Wiley & Sons, Ltd, New Jersey, 2nd edition.

- Flury and Shephard, (2011) Flury, T. and Shephard, N. (2011). Bayesian inference based only on simulated likelihood: Particle filter analysis of dynamic economic models. Econometric Theory, 1:1–24.

- Ghahramani and Hinton, (2000) Ghahramani, Z. and Hinton, G. E. (2000). Variational learning for switching state-space models. Neural computation, 12(4):831–864.

- Haario et al., (2001) Haario, H., Saksman, E., and Tamminen, J. (2001). An adaptive Metropolis algorithm. Bernoulli, 7:223–242.

- Hoffman et al., (2013) Hoffman, M. D., Blei, D. M., Wang, C., and Paisley, J. (2013). Stochastic variational inference. Journal of Machine Learning Research, 14:1303–1347.

- Honkela et al., (2010) Honkela, A., Raiko, T., Kuusela, M., Tornio, M., and Karhunen, J. (2010). Approximate Riemannian conjugate gradient learning for fixed-form variational Bayes. Journal of Machine Learning Research, 11:3235–3268.

- Kim et al., (1998) Kim, S., Shephard, N., and Chib, S. (1998). Stochastic volatility: Likelihood inference and comparison with arch models. The Review of Economic Studies, 65(3):361–393.

- Marin et al., (2012) Marin, J.-M., Pudlo, P., Robert, C., and Ryder, R. (2012). Approximate Bayesian computational methods. Statistics and Computing, 22(6):1167–1180.

- McCulloch, (1986) McCulloch, J. H. (1986). Simple consistent estimators of stable distribution parameters. Communications in Statistics - Simulation and Computation, 15(4):1109–1136.

- McGrory and Titterington, (2007) McGrory, C. and Titterington, D. (2007). Variational approximations in Bayesian model selection for finite mixture distributions. Computational Statistics & Data Analysis, 51(11):5352 – 5367. Advances in Mixture Models.

- Neville et al., (2014) Neville, S. E., Ormerod, J. T., and Wand, M. P. (2014). Mean field variational Bayes for continuous sparse signal shrinkage: Pitfalls and remedies. Electronic Journal of Statistics, 8(1):1113–1151.

- Nolan, (2007) Nolan, J. (2007). Stable Distributions: Models for Heavy-Tailed Data. Birkhauser, Boston.

- Nott et al., (2012) Nott, D. J., Tan, S., Villani, M., and Kohn, R. (2012). Regression density estimation with variational methods and stochastic approximation. Journal of Computational and Graphical Statistics, 21:797–820.

- Ormerod and Wand, (2012) Ormerod, J. T. and Wand, M. P. (2012). Gaussian variational approximate inference for generalized linear mixed models. J. Comput. Graph. Stat., 21:2–17.

- Owen, (1997) Owen, A. (1997). Monte carlo variance of scrambled net quadrature. SIAM J. Numer. Anal., 34:1884–1910.

- Paisley et al., (2012) Paisley, J., Blei, D., and Jordan, M. (2012). Variational Bayesian inference with stochastic search. In International Conference on Machine Learning, Edinburgh, Scotland, UK.

- Peters et al., (2012) Peters, G., Sisson, S., and Fan, Y. (2012). Likelihood-free Bayesian inference for -stable models. Computational Statistics & Data Analysis, 56(11):3743 – 3756.

- Pitt et al., (2012) Pitt, M. K., Silva, R. S., Giordani, P., and Kohn, R. (2012). On some properties of Markov chain Monte Carlo simulation methods based on the particle filter. Journal of Econometrics, 171(2):134–151.

- Ranganath et al., (2014) Ranganath, R., Gerrish, S., and Blei, D. M. (2014). Black box variational inference. In International Conference on Artificial Intelligence and Statistics, volume 33, Reykjavik, Iceland.

- Sacks, (1958) Sacks, J. (1958). Asymptotic distribution of stochastic approximation procedures. The Annals of Mathematical Statistics, 29(2):373–405.

- Salimans and Knowles, (2013) Salimans, T. and Knowles, D. A. (2013). Fixed-form variational posterior approximation through stochastic linear regression. Bayesian Analysis, 8(4):741–908.

- Shephard and Pitt, (1997) Shephard, N. and Pitt, M. K. (1997). Likelihood analysis of non-Gaussian measurement time series. Biometrika, 84:653–667.

- Tan and Nott, (2013) Tan, L. S. L. and Nott, D. J. (2013). Variational inference for generalized linear mixed models using partially noncentered parametrizations. Statistical Science, 28:168–188.

- Tavare et al., (1997) Tavare, S., Balding, D. J., Griffiths, R. C., and Donnelly, P. (1997). Inferring coalescence times from DNA sequence data. Genetics, 145(2):505–518.

- Tran et al., (2016) Tran, M.-N., Kohn, R., Quiroz, M., and Villani, M. (2016). Block-wise pseudo-marginal metropolis-hastings. Technical report. arXiv:1603.02485.

- Tran et al., (2014) Tran, M.-N., Pitt, M. K., and Kohn, R. (2014). Annealed important sampling for models with latent variables. http://arxiv.org/abs/1402.6035.

- Tran et al., (2013) Tran, M.-N., Scharth, M., Pitt, M. K., and Kohn, R. (2013). Importance sampling squared for Bayesian inference in latent variable models. http://arxiv.org/abs/1309.3339.

- Turner and Sahani, (2011) Turner, R. E. and Sahani, M. (2011). Two problems with variational expectation maximisation for time-series models. In Barber, D., Cemgil, A. T., and Chiappa, S., editors, Bayesian Time Series Models. Cambridge University Press.

- Wand, (2014) Wand, M. P. (2014). Fully simplified multivariate normal updates in non-conjugate variational message passing. Journal of Machine Learning Research, 15:1351–1369.