Of Quantiles and Expectiles:

Consistent Scoring Functions, Choquet Representations, and Forecast Rankings

Werner Ehm1, Tilmann Gneiting1,2, Alexander Jordan1,2, Fabian Krüger1

1Heidelberger Institut für Theoretische Studien, Computational Statistics Group

2Karlsruher Institut für Technologie, Institut für Stochastik

Abstract

In the practice of point prediction, it is desirable that forecasters receive a directive in the form of a statistical functional, such as the mean or a quantile of the predictive distribution. When evaluating and comparing competing forecasts, it is then critical that the scoring function used for these purposes be consistent for the functional at hand, in the sense that the expected score is minimized when following the directive.

We show that any scoring function that is consistent for a quantile or an expectile functional, respectively, can be represented as a mixture of extremal scoring functions that form a linearly parameterized family. Scoring functions for the mean value and probability forecasts of binary events constitute important examples. The quantile and expectile functionals along with the respective extremal scoring functions admit appealing economic interpretations in terms of thresholds in decision making.

The Choquet type mixture representations give rise to simple checks of whether a forecast dominates another in the sense that it is preferable under any consistent scoring function. In empirical settings it suffices to compare the average scores for only a finite number of extremal elements. Plots of the average scores with respect to the extremal scoring functions, which we call Murphy diagrams, permit detailed comparisons of the relative merits of competing forecasts.

Key words and phrases: Choquet representation; consistent scoring function; decision theory; economic utility; elicitable; expectile; forecast ranking; order sensitivity; point forecast; probability forecast; quantile

1 Introduction

Over the past two decades, a broad transdisciplinary consensus has developed that forecasts ought to be probabilistic in nature, i.e., they ought to take the form of predictive probability distributions over future quantities or events (Gneiting and Katzfuss 2014). Nevertheless, a wealth of applied settings require point forecasts, be it for reasons of decision making, tradition, reporting requirements, or ease of communication. In this situation, a directive is required as to the specific feature or functional of the predictive distribution that is being sought.

We follow Gneiting (2011) and consider a functional to be a potentially set-valued mapping from a class of probability distributions, , to the real line, , with the mean or expectation functional, quantiles, and expectiles being key examples. Competing point forecasts are then compared by using a nonnegative scoring function, , that represents the loss or penalty when the point forecast is issued and the observation realizes. A critically important requirement on the scoring function is that it be consistent for the functional relative to the class , in the sense that

| (1) |

for all probability distributions , all , and all . If equality in (1) implies that , then the scoring function is strictly consistent.

To give a prominent example, the ubiquitous squared error scoring function, , is strictly consistent for the mean or expectation functional relative to the class of probability distributions with finite variance. However, there are many alternatives. In a classical paper, Savage (1971) showed, subject to weak regularity conditions, that a scoring function is consistent for the mean functional if and only if it is of the form

| (2) |

where the function is convex with subgradient ; squared error arises when . Holzmann and Eulert (2014) proved that when forecasts make ideal use of nested information bases, the forecast with the broader information basis is preferable under any consistent scoring function.

However, in real world settings, as pointed out by Patton (2015), forecasts are hardly ever ideal, and the ranking of competing forecasts might depend on the choice of the scoring function. This had already been observed by Murphy (1977), Schervish (1989), and Merkle and Steyvers (2013), among others, in the important special case of a binary predictand, where corresponds to a success and to a non-success, so that the mean of the predictive distribution provides a probability forecast for a success. As there is no obvious reason for a consistent scoring function to be preferred over any other, this raises the question which one of the many alternatives to use.

Our work is motivated by the quest for guidance in this setting. Theoretically, the respective key result is that, subject to unimportant regularity conditions, any function of the form (2) admits a mixture representation of the form

where is a nonnegative measure, and

for . (Here and in what follows, we write for the positive part of and for the indicator function of the event .) Thus every scoring function consistent for the mean can be written as a weighted average over elementary or extremal scores . As an important consequence, a point forecast that is preferable in terms of each extremal score is preferable in terms of any consistent scoring function. The elementary scores can be seen as representing the loss, relative to an oracle, in an investment problem with cost basis and future revenue ; see Section 2.3.

In empirical settings, point forecasts are compared based on their average scores. Specifically, let us consider a sequence of triplets for , where and are competing point forecasts and is the subsequent outcome. We may compare the two forecasts graphically, by plotting the respective empirical scores,

| (3) |

for and , versus . An example of this type of display, which we term a Murphy diagram, is shown in Figure 1, where we consider point forecasts of wind speed at a major wind energy center.

More generally, for both quantiles and expectiles the apparent wealth of consistent scoring functions can be reduced to a one-dimensional family of readily interpretable elementary scores, in the sense that every consistent scoring function can be represented as a mixture from that family. The case of the mean or expectation functional, which includes probability forecasts for binary events as a further special case, corresponds to the expectile at level .

The remainder of the paper is organized as follows. Section 2 is devoted to the key theoretical development, in which we state and discuss the mixture representations, relate to Choquet theory and order sensitivity, and provide economic interpretations of the elementary scores and the associated functionals. In particular, we show that expectiles are optimal decision thresholds in binary investment problems with fixed cost basis and differential taxation of profits versus losses. In Section 3, we apply the mixture representations to study forecast rankings and propose the aforementioned Murphy diagram for forecast comparisons. Illustrations on data examples follow in Section 4, where we revisit meteorological and economic case studies in the work of Gneiting et al. (2006), Rudebusch and Williams (2009), and Patton (2015). The paper closes with a discussion in Section 5. Proofs and computational details are deferred to Appendices.

2 Consistent scoring functions for quantiles and expectiles

Before focusing on the specific cases of quantiles and expectiles, we review general background material on the assessment of point forecasts, with emphasis on consistent scoring functions.

2.1 Consistent scoring functions

We first introduce notation and expose conventions. Let denote the class of the probability measures on the Borel-Lebesgue sets of the real line, . For simplicity, we do not distinguish between a measure and the associated cumulative distribution function (CDF). We follow standard conventions and assume CDFs to be right-continuous. A function S defined on a rectangle is called a scoring function if for all with if . Here, is interpreted as the loss or cost accrued when the point forecast is issued and the observation realizes. The scoring function is regular if it is jointly measurable and left-continuous in its first argument, , for every .

In point prediction problems, it is rarely evident which functional of the predictive distribution should be reported. Guidance can be given implicitly, by specifying a loss function, or explicitly, by specifying a functional. The notion of consistency originates in this setting.

Consider a functional on a class on which the mapping is well-defined. Usually, the functional is single-valued, as in the case of the mean functional where we take as the class of the probability measures with finite first moment. More generally, the expectile at level of a probability measure is the unique solution to the equation

where corresponds to the mean functional (Newey and Powell 1987). In the case of quantiles, the functional might be set-valued. Specifically, the quantile functional at level maps a probability measure to the closed interval , with lower limit and upper limit . The two limits differ only when the level set contains more than one point, so typically the functional is single-valued. Any number between and represents an -quantile and will be denoted .

The scoring function S is consistent for a functional relative to the class if

| (4) |

for all probability measures , all , and all point forecasts . A functional that admits a strictly consistent scoring function is called elicitable, and can then be represented as the solution to an optimization problem, in that

Hence, if the goal is to minimize expected loss, the optimal strategy is to follow the requested directive in the form of a functional.

In what follows, we restrict attention to the quantile and expectile functionals. These are critically important in a gamut of applications, including quantile and expectile regression in general, and least squares (i.e., mean) and probit and logit (i.e., binary probability) regression in particular.

2.2 Mixture representations

The classes of the consistent scoring functions for quantiles and expectiles have been described by Savage (1971), Thomson (1979), and Gneiting (2011), and we review the respective characterizations in the setting of the latter paper, where further detail is available.

Up to mild regularity conditions, a scoring function S is consistent for the quantile functional at level relative to the class if and only if it is of the form

| (5) |

where is non-decreasing. The most prominent example arises when , which yields the asymmetric piecewise linear scoring function,

| (6) |

that lies at the heart of quantile regression (Koenker and Bassett 1978; Koenker 2005). Similarly, a scoring function is consistent for the expectile at level relative to the class if and only if it is of the form

| (7) |

where is convex with subgradient . The key example arises when , where

| (8) |

This is the loss function used for estimation in expectile regression (Newey and Powell 1987; Efron 1991), including the ubiquitous case of ordinary least squares regression.

In view of the representations (5) and (7), the scoring functions that are consistent for quantiles and expectiles are parameterized by the non-decreasing functions , and the convex functions with subgradient , respectively. In general, neither nor and are uniquely determined. We therefore select special versions of these functions. Furthermore, in the interest of simplicity we generally assume that , adding comments in cases where there are finite boundary points. Let denote the class of all left-continuous non-decreasing real functions, and let denote the class of all convex real functions with subgradient . This last condition is satisfied when is chosen to be the left-hand derivative of , which exists everywhere and is left-continuous by construction.

In what follows, we use the symbol to denote the class of the scoring functions S of the form (5) where . Similarly, we write for the class of the scoring functions S of the form (7) where . For all practical purposes, the families and can be identified with the classes of the regular scoring functions that are consistent for quantiles and expectiles, respectively. These classes appear to be rather large. However, in either case the apparent multitude can be reduced to a one-dimensional family of elementary scoring functions, in the sense that every consistent scoring function admits a representation as a mixture of elementary elements.

Theorem 1a (quantiles). Any member of the class admits a representation of the form

| (9) |

where is a nonnegative measure and

| (13) | |||||

The mixing measure is unique and satisfies for , where is the nondecreasing function in the representation (5). Furthermore, we have for .

Theorem 1b (expectiles). Any member of the class admits a representation of the form

| (14) |

where is a nonnegative measure and

| (18) | |||||

The mixing measure is unique and satisfies for , where is the left-hand derivative of the convex function in the representation (7). Furthermore, we have for , where denotes the left-hand derivative with respect to the second argument.

Note that the relations in (9) and (14) hold pointwise. In particular, the respective integrals are pointwise well-defined. This is because for the functions and are right-continuous, non-negative, and uniformly bounded with bounded support, and because the non-decreasing functions and define non-negative measures and that assign finite mass to any finite interval.

In the case of quantiles, the asymmetric piecewise linear scoring function corresponds to the choice in (5), so the mixing measure in the representation (9) is the Lebesgue measure. The elementary scoring function arises when , i.e., when is a one-point measure in .

In the case of expectiles, the mixing measure for the asymmetric squared error scoring function is twice the Lebesgue measure. The choice recovers the mean or expectation functional, for which existing parametric subfamilies emerge as special cases of our mixture representation. Patton’s (2015) exponential Bregman family,

which nests the squared error loss in the limit as , corresponds to the choice in (7). The mixing measure in the representation (14) then has Lebesgue density for . For Patton’s (2011) family

of homogeneous scoring functions on the positive half line the mixing measure has Lebesgue density , remarkably with no case distinction being required. The elementary scoring function emerges when in (7); here the mixing measure in (14) is a one-point measure in .

From a theoretical perspective, a natural question is whether the mixture representations (9) and (14) can be considered Choquet representations in the sense of functional analysis (Phelps 2001). Recall that a member S of a convex class is an extreme point of if it cannot be written as an average of two other members, i.e., if with implies . Our mixture representations qualify as Choquet representations if the elementary scores and form extreme points of the underlying classes of scoring functions. This cannot possibly be true for our classes and because they are invariant under dilations, hence admit trivial average representations built with multiples of one and the same scoring function. Therefore, the families and need to be restricted suitably. Specifically, let the class consist of all functions such that and . Similarly, let denote the family of all such that and . These classes are convex, and so are the associated subclasses of the families and , which we denote by and , respectively. The elementary scores and evidently are members of these restricted families.

Proposition 1a (quantiles). For every and , the scoring function is an extreme point of the class .

Proposition 1b (expectiles). For every and , the scoring function is an extreme point of the class .

We thus have furnished Choquet representations for subclasses of the consistent scoring functions for quantiles and expectiles. In the extant literature, such Choquet representations have been known in the binary case only, where corresponds to a success and to a non-success, so that the mean, , of the predictive distribution provides a probability forecast for a success. In this setting, the Savage representation (7) for the members of the respective class reduces to

The mixture representation (14) can then be written as

| (19) |

where is a nonnegative measure and

| (20) |

The parameter can be interpreted as the cost-loss ratio in the classical simple cost-loss decision model (Richardson 2012). Up to unimportant conventions regarding coding, scaling, and gain-loss orientation, this recovers the well known mixture representation of the proper scoring rules for probability forecasts of binary events (Shuford, Albert, and Massengill 1966; Schervish 1989). Different choices of the mixing measure yield the standard examples of scoring rules in this case; see Buja et al. (2005) and Table 1 in Gneiting and Raftery (2007). The widely used Brier score,

| (21) |

arises when is twice the Lebesgue measure.

2.3 Economic interpretation

Our results in the previous section give rise to natural economic interpretations of the extremal scoring functions and , along with the quantile and expectile functionals themselves. In either case, the interpretation relates to a binary betting or investment decision with random outcome, .

In the case of the extremal quantile scoring function in (13), the payoff takes on only two possible values, relating to a bet on whether or not the outcome will exceed the threshold . Specifically, consider the following payoff scheme, which is realized in spread betting in prediction markets (Wolfers and Zitzewitz 2008):

-

•

If Quinn refrains from betting, his payoff will be zero, independently of the outcome .

-

•

If Quinn enters the bet and realizes, he loses his wager, .

-

•

If Quinn enters the bet and realizes, his winnings are , for a gain of .

How should Quinn act under this payoff scheme? If Quinn does not enter the bet, his actual and expected payoffs equal zero. If he does enter, his expected payoff is

where is Quinn’s predictive CDF for the future outcome, , which for simplicity we assume to be strictly increasing. This expression is strictly positive if and only if , where

| (23) |

Hence, Quinn’s optimal decision rule is determined by the -quantile of , in that he enters the bet if and only if . Motivated by the specific format of the optimal decision or Bayes rule, the top left matrix in Table 1 summarizes the payoff from just any strategy of the form enter the bet if and only if .

It remains to draw the connection to the extremal scoring function . To this end, we shift attention from positively oriented payoffs to negatively oriented regrets, which we define as the difference between the payoff for an oracle and Quinn’s payoff. Here the term oracle refers to a (hypothetical) omniscient bettor who enters the bet if and only if realizes, which would yield an ideal payoff if , and zero otherwise. If Quinn uses some decision threshold , his regret equals the extremal score except for an irrelevant multiplicative factor. This is illustrated in the bottom left matrix in the table and corresponds to the classical, simple cost-loss decision model (Richardson 2012). In decision theoretic terms, the distinction between payoff and regret is inessential, because the difference depends on the outcome, , only. In either case, the optimal strategy is to choose the decision threshold .

| Quantiles | Expectiles | ||||||||||||||||||

| Monetary Payoff | Monetary Payoff | ||||||||||||||||||

|

|

||||||||||||||||||

| Score (Regret) | Score (Regret) | ||||||||||||||||||

|

|

In the case of the extremal expectile scoring function in (7), the payoff is real-valued. Specifically, suppose that Eve considers investing a fixed amount into a start-up company, in exchange for an unknown, future amount of the company’s profits or losses. The payoff structure then is as follows:

-

•

If Eve refrains from the deal, her payoff will be zero, independently of the outcome .

-

•

If Eve invests and realizes, her payoff is negative, at . Here, is the sheer monetary loss, and the factor accounts for Eve’s reduction in income tax, with representing the deduction rate.111In financial terms, the loss acts as a tax shield. The linear functional form assumed here is not unrealistic, even though it is simpler than many real-world tax schemes, where nonlinearities may arise from tax exemptions, progression, etc.

-

•

If Eve invests and realizes, her payoff is positive, at , where denotes the tax rate that applies to her profits.

How should Eve act under this payoff scheme? If Eve does not enter the deal, her actual and expected payoffs vanish. In case she invests, the expected payoff is

This expression is strictly positive if and only if the expectile at level

| (24) |

of Eve’s predictive CDF, , exceeds . In analogy to the quantile case, the top right matrix in Table 1 represents Eve’s payoff from just any strategy of the form invest if and only if .

To relate to the extremal scoring function , we again shift attention to regrets relative to an omniscient investor or oracle who enters the deal if and only if occurs, which would yield the ideal payoff . As seen in the table, if Eve uses the threshold to determine whether or not to invest, the regret equals the extremal score , up to a multiplicative factor.222The elementary score for probability forecasts of a binary event in (20) is obtained when and . The parameter can then be interpreted as a cost-loss ratio.

Therefore, expectiles can be interpreted as optimal decision thresholds in investment problems with fixed costs and differential tax rates for profits versus losses. The mean arises in the special case when in (24). It corresponds to situations in which losses are fully tax deductible () and nests situations without taxes (). Tough taxation settings where shift Eve’s incentives toward not entering the deal and correspond to expectiles at levels . For example, if losses cannot be deducted at all , whereas profits are taxed at a rate of , Eve will invest only if the expectile at level of her predictive CDF, , exceeds the deal’s fixed costs, . Note that we permit the case , which may reflect subsidies or tax credits, say.

The above interpretation of expectiles as optimal thresholds in decision problems attaches an economic meaning to this class of functionals, which thus far seems to have been missing; e.g., Schulze Waltrup et al. (2014, p. 2) note that “expectiles lack an intuitive interpretation”. The foregoing may also bear on the debate about the revision of the Basel protocol for banking regulation, which involves contention about the choice of the functional of in-house risk distributions that banks are supposed to report to regulators (Embrechts et al. 2014). Recently, expectiles have been put forth as potential candidates, as it has been proved that they are the only elicitable law-invariant coherent risk measures (Delbaen et al. 2014; Ziegel 2014; Bellini and Bignozzi 2015).

2.4 Order sensitivity

The extremal scoring functions and are not only consistent for their respective functional, they in fact enjoy the stronger property of order sensitivity. Generally, a scoring function S is order sensitive for the functional relative to the class if, for all , all , and all ,

and

The order sensitivity is strict if the above continues to hold when the inequalities involving and are strict. As before, we denote the class of the Borel probability measures on by , and we write for the subclass of the probability measures with finite first moment.

Proposition 2a (quantiles). For every and , the extremal scoring function is order sensitive for the -quantile functional relative to .

Proposition 2b (expectiles). For every and , the extremal scoring function is order sensitive for the -expectile functional relative to .

Owing to the mixture representations (9) and (14), the order sensitivity of the extremal scoring functions transfers to all regular consistent scoring functions. Strict order sensitivity applies if the function in the representation (5) and the derivative in the representation (7), respectively, are strictly increasing, relative to subclasses of probability measures with suitable moment constraints. Closely related results have recently been obtained in studies of elicitability (Steinwart et al. 2014; Ziegel 2014; Bellini and Bignozzi 2015). In this strand of literature, the ambitious goal of characterizing all elicitable functionals necessitates regularity conditions that are not satisfied by our discontinuous, compactly supported extremal scoring functions.

3 Forecast rankings

In this section, we turn to the task of comparing and ranking forecasts. Before applying our mixture representations to this problem, we introduce the prediction space setting of Gneiting and Ranjan (2013) and define notions of forecast dominance.

3.1 Prediction spaces

A prediction space is a probability space tailored to the study of forecasting problems. Following the seminal work of Murphy and Winkler (1987), the prediction space setting of Gneiting and Ranjan (2013) considers the joint distribution of forecasts and observations. We first focus on probabilistic forecasts, , which we identify with the associated cumulative distribution functions (CDFs) for the real-valued outcome, . The elements of the respective sample space can be identified with tuples of the form

| (25) |

where the predictive distributions utilize information sets , respectively, with being a sigma field on the sample space . In measure theoretic language, the information sets correspond to sub sigma fields, and is a CDF-valued random quantity measurable with respect to . The joint distribution of the quantities in (25) is encoded by a probability measure on . In this setting, a predictive distribution is ideal relative to if it corresponds to the conditional distribution of the outcome under given .

| Forecaster | Predictive Distribution | -Quantile | Mean | Prob |

|---|---|---|---|---|

| Perfect | ||||

| Climatological | 0 | |||

| Unfocused | ||||

| Sign-reversed |

In a nutshell, a prediction space specifies the joint distribution of tuples of the form (25). To give an example, Table 2 revisits a scenario studied by Gneiting et al. (2007) and Gneiting and Ranjan (2013).333The only difference is that we let the random variable attain the values and 2, rather than the values and 1 as in Gneiting et al. (2007) and Gneiting and Ranjan (2013). Here, the outcome is generated as where . The perfect forecaster is ideal relative to the sigma field generated by the random variable . The unfocused and sign-reversed forecasters also have knowledge of , but fail to be ideal. The climatological forecaster, issuing the unconditional distribution of the outcome as predictive distribution, is ideal relative to the uninformative sigma field generated by the empty set.

Any predictive distribution, , can be reduced to a point forecast by extracting the sought functional, . In what follows, we focus on quantiles, the mean or expectation functional, and probability forecasts of the binary event that the outcome exceeds a threshold value. The respective point forecasts for the perfect, climatological, unfocused, and sign-reversed forecaster are shown in Table 2.

In practice, point forecasts might be an end to themselves, i.e., they might have been issued without there being an underlying predictive distribution. To accommodate such cases, we define a point prediction space to be a probability space , where the elements of the sample space can be identified with tuples of the form

| (26) |

where the random variables represent point forecasts and utilize information sets , respectively.444For simplicity, we let be single-valued. Extensions to set-valued random quantities, as might occur in the case of quantiles, are straightforward. The joint distribution of the point forecasts and the observation in (26) is specified by the probability measure . Similarly, it is sometimes useful to consider a mixed prediction space, by specifying the joint distribution of tuples of the form

| (27) |

where represent CDF-valued random quantities, and represent point forecasts.

3.2 Notions of forecast dominance

We now define notions of forecast dominance, starting with probabilistic forecasts that take the form of predictive CDFs, and then turning to point forecasts. In the former setting, a scoring rule is a suitably measurable function that assigns a loss or penalty when we issue the predictive distribution and realizes. A scoring rule is proper if

| (28) |

for all probability measures and in its domain of definition (Gneiting and Raftery 2007). Proper scoring rules therefore encourage honest and careful assessments. As is well known, a scoring function S that is consistent for a single-valued functional relative to a class induces a proper scoring rule, by defining for and .

Definition 1 (predictive CDFs). Let and be probabilistic forecasts, and let be the outcome, in a prediction space. Then dominates relative to a class of proper scoring rules if for every .

We now turn to quantiles and expectiles and the respective families and of the regular consistent scoring functions for these functionals.

Definition 2a (quantiles). Let and be point forecasts, and let be the outcome, in a point prediction space. Then dominates as an -quantile forecast if for every scoring function .

Definition 2b (expectiles). Let and be point forecasts, and let be the outcome, in a point prediction space. Then dominates as an -expectile forecast if for every scoring function .

It is important to note that the expectations in the definitions are taken with respect to the joint distribution of the probabilistic forecasts and the outcome. The notions provide partial orderings for the predictive distributions in (25) and in (26), respectively.555In the special case of probability forecasts of a binary event, related notions of sufficiency and dominance have been studied by DeGroot and Fienberg (1983), Vardeman and Meeden (1983), Schervish (1989), Krämer (2005), and Bröcker (2009). Essentially, a probabilistic forecast that dominates another is preferable, or at least not inferior, in any type of decision that involves the respective predictive distributions. In the case of quantiles or expectiles, a point forecast that dominates another is preferable, or at least not inferior, in any type of decision problem that depends on the respective predictive distributions via the considered functional only. Adaptations to functionals other than quantiles or expectiles are straightforward.

Under which conditions does a forecast dominate another? Holzmann and Eulert (2014) recently showed that if two predictive distributions are ideal, then the one with the richer information set dominates the other. Furthermore, the result carries over to ideal forecasters’ induced point predictions, including but not limited to the cases of quantiles and expectiles that we consider here. To give an example in the setting of Table 2, the perfect and the climatological forecasters are ideal relative to the sigma fields generated by , and generated by the empty set, respectively. Therefore, the perfect forecaster dominates the climatological forecaster, in any of the above senses.

Tsyplakov (2014) went on to show that if a predictive distribution is ideal relative to a certain information set, then it dominates any predictive distribution that is measurable with respect to the information set. Again, the result carries over to the induced point forecasts. In the setting of Table 2, the perfect forecaster is ideal relative to the sigma field generated by the random variables and . The climatological, unfocused, and sign-reversed forecasters are measurable with respect to this sigma field, and so they are dominated by the perfect forecaster, in any of the above senses.

In the practice of forecasting, predictive distributions are hardly ever ideal, and information sets may not be nested, as emphasized by Patton (2015). Therefore, the above theoretical results are not readily applicable, and distinct soring rules, or distinct consistent scoring functions, may yield distinct forecast rankings, as in empirical examples given by Schervish (1989), Merkle and Steyvers (2013), and Patton (2015), among others. Furthermore, in general it is not feasible to check the validity of the expectation inequalities in Definitions 1, 2a, and 2b for any proper scoring rule , or consistent scoring function , or , respectively.

Fortunately, in the case of quantile and expectile forecasts, the mixture representations in Theorems 1a and 1b reduce checks for dominance to the respective one-dimensional families of elementary scoring functions.

Corollary 1a (quantiles). In a point prediction space, dominates as an -quantile forecast if for every .

Corollary 1b (expectiles). In a point prediction space, dominates as an -expectile forecast if for every .

The reduction to a one-dimensional problem suggests graphical comparisons via Murphy diagrams. Before we discuss this tool, we note that order sensitivity can sometimes be invoked to prove dominance. For example, consider the mixed prediction space setting (27) with and . Suppose that the CDF-valued random quantity is ideal relative to the sigma field , and let denote its -quantile. Suppose furthermore that and are measurable with respect to . By Corollary 1a in concert with Proposition 1a and a conditioning argument, dominates as an -quantile forecast if with probability one either

holds true. An analogous argument applies in the case of the -expectile.

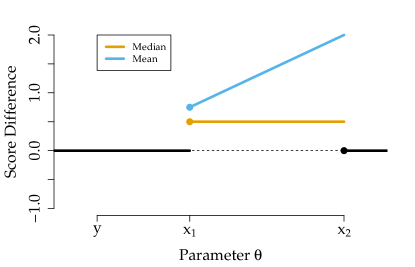

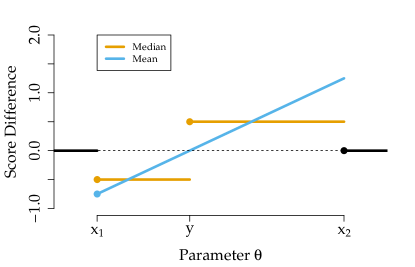

In the scenario of Table 2, the argument can be put to work in the case that corresponds to median and mean forecasts, respectively. Specifically, let be the perfect forecast, which has median and mean , let be the sigma field generated by , and let and . Invoking the order sensitivity argument, we see that the climatological forecaster dominates the sign-reversed forecaster for both median and mean predictions.

3.3 The Murphy diagram as a diagnostic tool

As noted, Corollaries 1a and 1b suggest graphical tools for the comparison of quantile and expectile forecasts, including the special cases of the mean or expectation functional, and the further special case of probability forecasts of a binary event. We describe these diagnostic tools in the setting of a point prediction space (26), where denote point forecasts for the outcome , and the probability measure represents their joint distribution. In the case of probability forecasts, we use the more suggestive notation for the forecasts.

-

•

For quantile forecasts at level , we plot the graph of the expected elementary quantile score ,

(29) for . By Corollary 1a, forecast dominates forecast if and only if for . The area under equals the respective expected asymmetric piecewise linear score (6).

-

•

For expectile forecasts at level , we plot the graph of the expected elementary expectile score ,

(30) for . By Corollary 1b, forecast dominates forecast if and only if for . The area under equals half the respective expected asymmetric squared error (8).

-

•

For probability forecasts of a binary event, we plot the graph of the expected elementary score ,

(31) for . By Corollary 1b, the probability forecast dominates if and only if for . The area under equals half the expected Brier score (21).

In the context of probability forecasts for binary weather events, displays of this type have a rich tradition that can be traced to Thompson and Brier (1955) and Murphy (1977). More recent examples include the papers by Schervish (1989), Richardson (2000), Wilks (2001), Mylne (2002), and Berrocal et al. (2010), among many others. Murphy (1977) distinguished three kinds of diagrams that reflect the economic decisions involved. The negatively oriented expense diagram shows the mean raw loss or expense of a given forecast scheme; the positively oriented value diagram takes the unconditional or climatological forecast as reference and plots the difference in expense between this reference forecast and the forecast at hand, and lastly, the relative-value diagram plots the ratio of the utility of a given forecast and the utility of an oracle forecast. The displays introduced above are similar to the value diagrams of Murphy, and we refer to them as Murphy diagrams. Our Murphy diagrams are by default negatively oriented and plot the expected elementary score for competing quantile, expectile, and probability forecasters. For better visual appearance, we generally connect the left- and right-hand limits at the jump points of the empirical score curves.

Mean

Quantile ()

Quantile ()

Mean

Probability ()

Probability ()

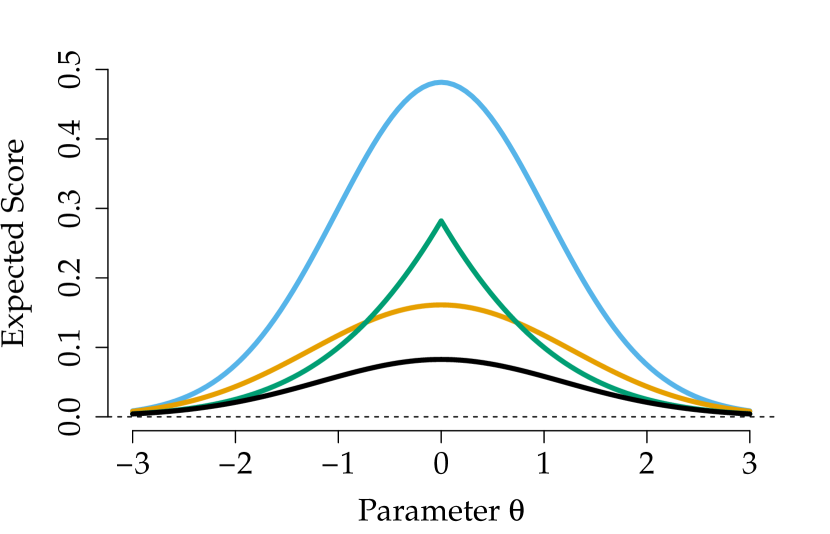

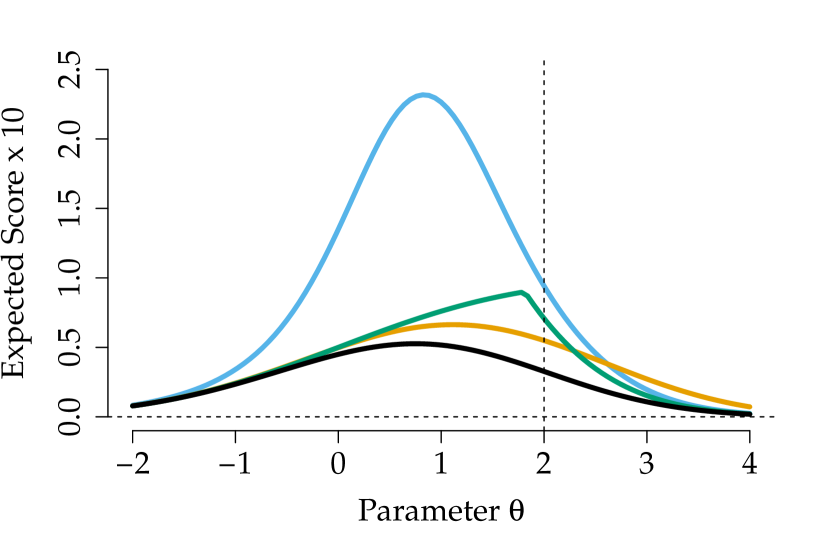

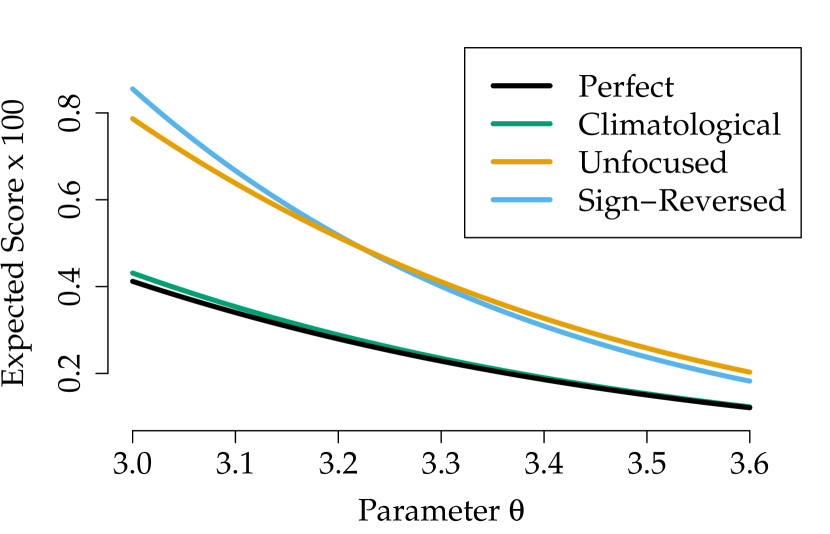

Figure 2 shows Murphy diagrams for the perfect, climatological, unfocused, and sign-reversed forecasters in Table 2. We compare point predictions for the mean or expectation functional, and the quantile at level , along with probability forecasts for the binary event that the outcome exceeds the threshold value 2. Analytic expressions for the respective expected scores are given in Appendix B. As proved in the previous section, the perfect forecaster dominates the other forecasters for all functionals considered. The expected score curves for the climatological and the unfocused, and for the unfocused and the sign-reversed forecasters, intersect in all three cases, so there are no order relations between these forecasters. Finally, the Murphy diagrams suggest that the climatological forecaster dominates the sign-reversed forecaster for all three functionals, and in the case of the mean functional, the order sensitivity argument in the previous section confirms the visual impression. In the cases of the quantile and probability forecasts, final confirmation would need to be based on tedious analytic investigations of the asymptotic behavior of the expected score functions.

By default, our Murphy diagrams show the expected elementary scores. If interest focuses on binary comparisons, it is natural to consider Murphy diagrams for the difference,

| (32) |

between the expected elementary scores of two point forecasters.

3.4 Murphy diagrams for empirical forecasters

We now turn to the comparison and ranking of empirical forecasts. Specifically, we consider tuples

| (33) |

where are the th forecaster’s point predictions, for , and , are the respective outcomes. Thus, we have competing forecasters, and each of them issues a set of point predictions. A convenient interpretation of the empirical setting is as a special case of a point prediction space, in which the tuples in (26) attain each of the values in (33) with probability . Then the probability measure is the corresponding empirical measure, and with this identification, the (average) empirical scores

where is either , , or , become the expected elementary scores from (29), (30), and (31), respectively. To compare forecasters and , say, it is convenient to show a Murphy plot of the equivalent of the difference (32), namely

where

| (34) |

for , and again is either , , or , respectively.

Murphy diagrams can be used efficiently to show a lack of domination when forecasters’ expected elementary score curves intersect. However, in general it is not possible to conclude domination, unless the visual impression is supported by tedious analytic investigations of the behavior of the expected score functions as . Fortunately, these complications do not arise in the empirical case, where dominance can be established by comparing the empirical score functions at a well-defined, finite set of arguments only, as follows.

Corollary 2a (quantiles). An empirical forecast dominates for -quantile predictions if

for .

Corollary 2b (expectiles). An empirical forecast dominates for -expectile predictions if

for and in the left-hand limit as , . In the case evaluations at can be omitted.

To see why these results hold, note that in either case the score differential is right-continuous, and that it vanishes unless . Furthermore, in the case of quantiles is piecewise constant with no other jump points than , or . Similarly, in the case of expectiles is piecewise linear with no other jump points than and , and no other change of slope than at . The change of slope disappears when . Figure 3 illustrates the behavior of in the cases of the median and the mean, respectively.

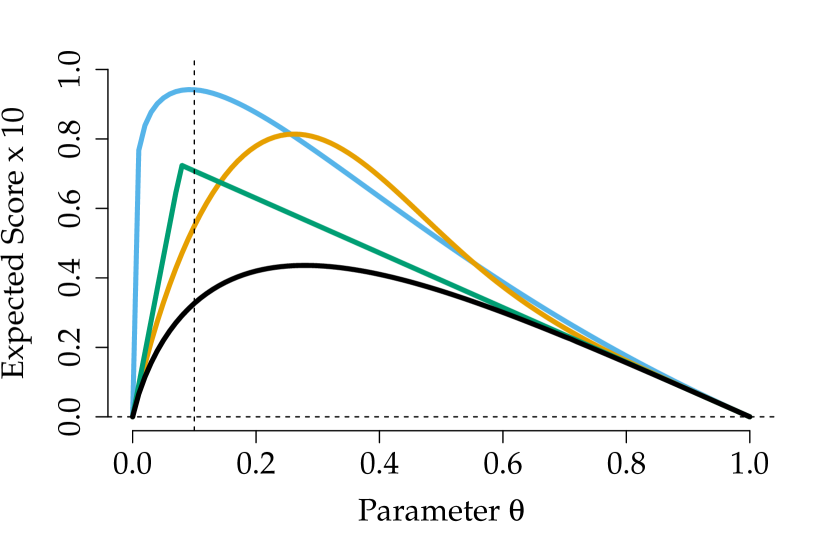

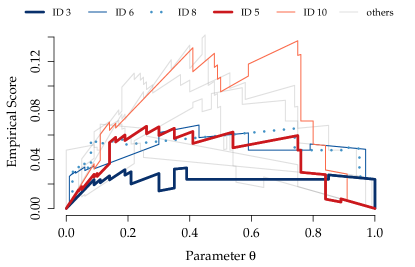

To give an example, we consider the 10 forecasters in Table A.1 of Merkle and Steyvers (2013), each of whom issues probability forecasts for 21 binary events. The data are artificial but mimic forecasters in the Aggregate Contingent Estimation System (ACES), a web based survey that solicited probability forecasts for world events from the general public. The Murphy diagram in the left-hand panel of Figure 4 shows the empirical score curves

where is forecaster ’s stated probability for world event to materialize, and is the respective binary realization. By Corollary 2b, dominance relations can be inferred by evaluating at the forecasters’ stated probabilities. We note that ID 3 dominates IDs 6 and 8, and that ID 5 dominates ID 10. The remaining pairwise comparisons do not give rise to dominance relations. The induced partial order between the IDs applies to comparisons under any proper scoring rule, as reflected by the rankings in Table 1 of Merkle and Steyvers (2013). The right-hand panel in Figure 4 considers joint comparisons. We see that ID 3 attains the lowest score over a wide range of . However, IDs 2, 5, 7, and 9 show the unique best empirical score under for other values of and, therefore, have superior economic utility under the associated cost-loss ratios.

4 Empirical examples

We now demonstrate the use of Murphy diagrams in economic and meteorological case studies in time series settings. In each example, interest is in a comparison of two forecasts, and so we show Murphy diagrams for the empirical scores and their difference. The jagged visual appearance stems from the behavior of the empirical score functions just explained and depends on the number of forecast cases. We supplement the Murphy diagrams for a difference by confidence bands based on Diebold and Mariano (1995) tests with a heteroscedasticity and autocorrelation robust variance estimator (Newey and West 1987). The approach of Diebold and Mariano (1995) views empirical data of the form (33) as a sample from an underlying population and tests the hypothesis of equal expected scores. The confidence bands are pointwise and have a nominal level of 95%.

| Mean Inflation, Patton (2015); |

|

| Probability of Recession, Rudebusch and Williams (2009); |

|

| 90% Quantile of Wind Speed, Gneiting et al. (2006); |

|

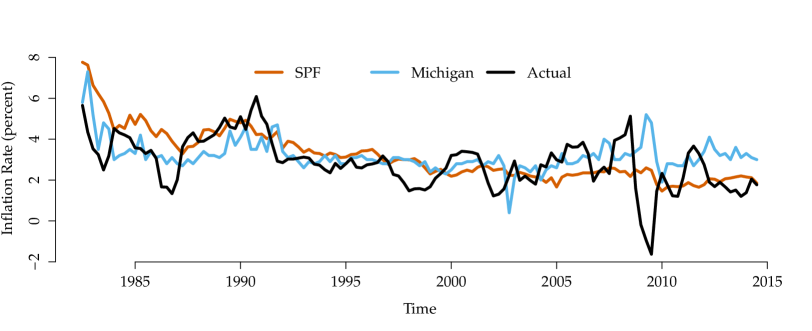

4.1 Mean forecasts of inflation

In macroeconomics, subjective expert forecasts often compare favorably to statistical forecasting approaches; see Faust and Wright (2013) for evidence and discussion. For the United States, the Survey of Professional Forecasters (SPF) run by the Federal Reserve Bank of Philadelphia is a key data source; see, e.g., Engelberg et al. (2009). Patton (2015) uses SPF data to illustrate the use of various scoring functions that are consistent for the mean functional.

Motivated by Patton’s analysis, we analyze SPF mean forecasts for the annual inflation rate of the Consumer Price Index (CPI). We compare the SPF forecasts to forecasts from another survey, the Michigan Survey of Consumers, based on data from the third quarter of 1982 to the third quarter of 2014, for a test period of 129 quarters. Our implementation choices are as in Section 5 of Patton (2015), except that we update the data set to cover the observations for the second and third quarters in 2014, and that we use the slightly newer fourth quarter of 2014 vintage for the CPI realizations. The top panel of Figure 5 shows the forecasts along with the realizing values.

The respective Murphy diagrams are shown in the top panel of Figure 6. At left, the curves for the empirical elementary score of the SPF and the Michigan survey intersect prominently, suggesting that neither of the two surveys dominates the other. Specifically, the SPF is preferred for smaller values, whereas the Michigan survey is preferred for larger values of . This may be explained by a series of high inflation rates up until 1992, which were better matched by the Michigan survey than by the SPF. At right, the confidence bands for the score differences are fairly broad and include zero for all values of .

4.2 Probability forecasts of recession

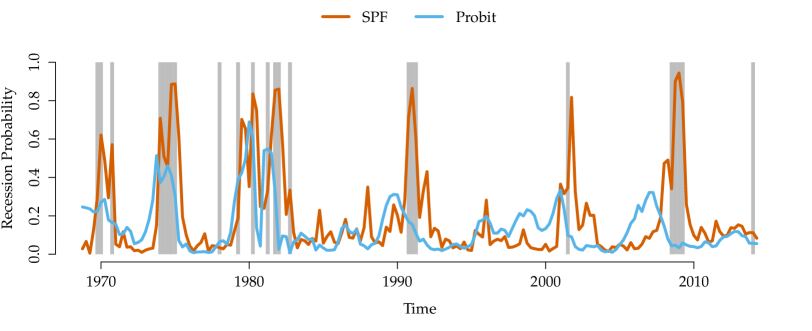

We now relate to the rich literature on binary regression and prediction and analyze probability forecasts of United States recessions, as proxied by negative real gross domestic product (GDP) growth. The SPF covers probability forecasts for this event since the fourth quarter of 1968. Following Rudebusch and Williams (2009), we compare current quarter probability forecasts from the SPF to forecasts from a probit model based on the term spread, i.e., the difference between long and short term interest rates. We follow Rudebusch and Williams (2009) in all data and implementation choices, except that we update their sample through the second quarter of 2014, for a test period of 186 quarters. Detailed economic and/or statistical justification of these choices can be found in the original paper.

The middle row of Figure 5 shows the SPF and probit model based probability forecasts for a recession, with the gray vertical bars indicating actual recessions. During recessionary periods, the SPF tends to assign higher forecast probabilities than the probit model. Also, the SPF tends to assign lower forecast probabilities during non-recessionary periods. The respective Murphy diagrams in the middle row of Figure 6 show that the SPF attains lower empirical elementary scores at all thresholds . The confidence bands for the score differences exclude zero for small values of the cost-loss ratio and confirm the superiority of the SPF over the probit model for current quarter forecasts. This can partly be attributed to the fact that SPF panelists have access to timely within-quarter information that is not available to the probit model. As demonstrated by Rudebusch and Williams (2009), the relative performance of the probit model improves at longer forecast horizons, where within-quarter information plays a lesser role.

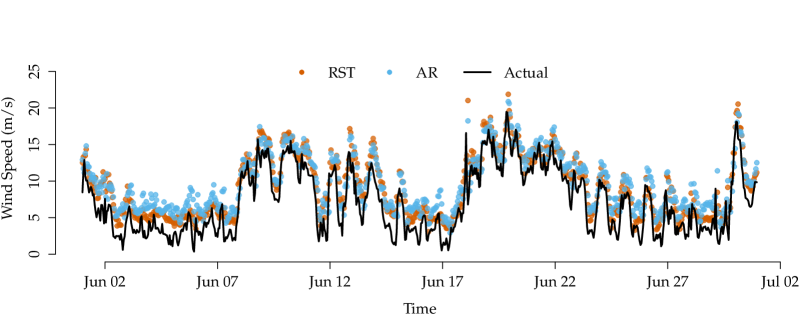

4.3 Quantile forecasts for wind speed

We return to the meteorological example in Figure 1, but instead of the mean or expectation functional we now consider quantile forecasts at level . We compare the regime-switching space-time (RST) approach introduced by Gneiting et al. (2006) to a simple autoregressive (AR) benchmark for two-hour ahead forecasts of hourly average wind speed at the Stateline wind energy center in the Pacific Northwest of the United States. The original paper refers to the specifications considered here as RST-D-CH and AR-D-CH, respectively. This terminology indicates that the methods account for the diurnal cycle and conditional heteroscedasticity. The data set, evaluation period, estimation and forecast methods for this example are identical to those in Gneiting et al. (2006), and we refer to the original paper for detailed descriptions. Both methods yield predictive distributions, from which we extract the quantile forecasts. The evaluation period ranges from May 1 through November 30, 2003, for a total of 5,136 hourly forecast cases.

The bottom panel in Figure 5 shows the quantile forecasts and realizations. The quantile forecasts exceed the outcomes at about the nominal level, at 89.7% for the RST forecast and 90.9% for the AR forecast, respectively, indicating good calibration. However, the RST forecasts are sharper, in that the average forecast value over the evaluation period is 9.2 meters per second, as compared to 9.7 meters per second in the case of the AR forecast. To see why the sharpness interpretation applies here, note that wind speed is a nonnegative quantity, so quantile forecasts can be identified with one-sided prediction intervals with a left limit of zero. These observations suggest the superiority of the RST forecasts over the benchmark AR forecasts, and the Murphy diagrams for the empirical elementary scores in the bottom row of Figure 6 confirm this intuition, in line with what we saw in Figure 1 for the mean functional.

5 Discussion

We have studied mixture representations of Choquet type for the scoring functions that are consistent for quantiles and expectiles, respectively, including the ubiquitous case of the mean or expectation functional, and nesting probability forecasts for binary events as a further special case. A particularly interesting aspect of these results is that they allow for an economic interpretation of consistent scoring functions in terms of betting and investment problems. Our interpretation of expectiles as optimal decision thresholds in investment problems with fixed costs and differential tax rates appears to be original and may bear on the current debate about the revision of the Basel protocol for banking regulation.

From a general applied perspective, Gneiting (2011, p. 757) had argued that if point forecasts are to be issued and evaluated,

“it is essential that either the scoring function be specified ex ante, or an elicitable target function be named, such as the mean or a quantile of the predictive distribution, and scoring functions be used that are consistent for the target functional.”

Patton (2015, p. 1) took this argument a step further, by positing that

“rather than merely specifying the target functional, which narrows the set of relevant loss functions only to the class of loss functions consistent for that functional […] forecast consumers or survey designers should specify the single specific loss function that will be used to evaluate forecasts.”

This is a very valid point. Whenever forecasters are to be compensated for their efforts in one way or another, the scoring function ought to be disclosed. To give an example of this best practice, the participants of forecast competitions hosted on the Kaggle platform (www.kaggle.com) are routinely informed about the relevant scoring function prior to the start of the competition. See, e.g., Hong et al. (2014) for a description of the Global Energy Forecasting Competition 2012.

However, there remain many situations in which point forecasters receive directives in the form of a functional, without an accompanying scoring function being available. This might be, because the forecasts are utilized by a myriad of communities, a situation often faced by national and international weather centers, because costs and losses are unknown or confidential, because the goal is general methodological development, as opposed to a specific applied task, because interest centers on an understanding of forecasters’ behaviors and performance, or simply because of negligence of best practices. In such settings, our findings suggest the routine use of new diagnostic tools in the evaluation and ranking of forecasts, which we call Murphy diagrams. Interest sometimes centers on decompositions of expected or empirical scores into uncertainty, resolution, and reliability components, as studied by DeGroot and Fienberg (1983), Bröcker (2009), and Bentzien and Friederichs (2014), among others. Extensions of Murphy diagrams in these directions may be worthwhile.

Our results also bear on estimation problems, in that scoring functions connect naturally to M-estimation (Huber 1964; Koltchinskii 1997). An interesting observation is that the loss functions that have traditionally been employed for estimation in quantile regression, ordinary least squares regression, and expectile regression, namely the asymmetric piecewise linear and squared error scoring functions (6) and (8), correspond to the choice of the Lebesgue measure in the mixture representations (9) and (14), respectively. This is in contrast to binary regression, where estimation is typically based on the logarithmic score, which corresponds to the choice of the infinite measure with density in the mixture representation (19), rather than the Lebesgue or uniform measure that yields (half) the Brier score (21). Quite generally, this raises the question of the optimal choice of the loss or scoring function to be used for estimation in regression problems. Focusing on the binary case, Hand and Vinciotti (2003), Buja et al. (2005), Lieli and Springborn (2013) and Elliott et al. (2015) have considered the use of economically motivated criteria. The interpretations developed in the present paper can help design economically motivated criteria in more general settings.

Mixture representations of Choquet type can be found for other, more general classes of consistent scoring functions. For instance, our results extend to the class of functionals known as generalized quantiles or M-quantiles (Breckling and Chambers 1988; Koltchinskii 1997; Bellini et al. 2014; Steinwart et al. 2014), which subsume both quantiles and expectiles. Related, but more complex mixture representations apply in the case of scoring functions that are consistent for multi-dimensional functionals, as recently studied by Fissler and Ziegel (2015).

An interesting question is whether there might be mixture representations in terms of economically interpretable elementary scores for proper scoring rules. As noted, a scoring rule assigns a loss or penalty when we issue the predictive CDF and realizes, and for a scoring rule to be proper, the expectation inequalities in (28) need to hold. As we have seen, a predictive distribution for a binary variable can be identified with a probability forecast, so the representation (19) applies and the answer is well known to be positive in this case. However, an extension from probability forecasts of binary to ternary or general discrete variables does not appear to be feasible, due to results by Johansen (1974) and Bronshtein (1978) in convex analysis.666In a nutshell, Savage (1971) showed that in the case of categories, the proper scoring rules for probability forecasts essentially are parameterized by the convex functions on the unit simplex in . Johansen (1974) and Bronshtein (1978) proved that if then the extremal members of that class lie dense. Despite this negative result, a closer look at a popular score is encouraging. Specifically, the widely used continuous ranked probability score (CRPS; Matheson and Winkler 1976),

equals the integral of the Brier score (21) for the induced probability forecast, namely , of the binary event over all thresholds . For simplicity, let us assume that has unique quantiles. We may then invoke the mixture representation (19) along with the relationships (20) and (22) to yield777An expected or empirical CRPS then corresponds to the volume under the surface spanned by the Murphy diagrams for all -quantile predictions, or by the Murphy diagrams for all threshold-determined binary probability forecasts.

Depending on the order of integration, the mixture representation recovers the quantile or the threshold decomposition of the CRPS (Gneiting and Ranjan 2011) after evaluating the first integral. More complex weighting schemes depending on and can be employed, for a general family of proper scoring rules that can be economically motivated and justified. Related ideas have recently been put forward in the hydrologic and meteorological literatures (Laio and Tamea 2007; Bradley and Schwartz 2011; Smet et al. 2012).

Acknowledgement

This work has been funded by the European Union Seventh Framework Programme under grant agreement no. 290976.

References

-

Bellini, F., Klar, B., Müller, A. and Rosazza Gianin, E. R. (2014) Generalized quantiles as risk measures. Insurance: Mathematics and Economics, 54, 41–48.

Bellini, F. and Bignozzi, V. (2015) On elicitable risk measures. Quantitative Finance, 15, 725–733.

Bentzien, S. and Friederichs, P. (2014) Decomposition and graphical portrayal of the quantile score. Quarterly Journal of the Royal Meteorological Society, 140, 1924–1934.

Berrocal, V. J., Raftery, A. E., Gneiting, T. and Steed, R. C. (2010) Probabilistic weather forecasting for winter road maintenance. Journal of the American Statistical Association, 105, 522–537.

Bradley, A. A. and Schwartz, S. S. (2011) Summary Verification measures and their interpretation for ensemble forecasts. Monthly Weather Review, 139, 3075–3089.

Breckling, J. and Chambers, R. (1988) M-Quantiles. Biometrika, 75, 761–771.

Bröcker, J. (2009) Reliability, sufficiency, and the decomposition of proper scores. Quarterly Journal of the Royal Meteorological Society, 135, 1512–1519.

Bronshtein, E. M. (1978) Extremal convex functions. Siberian Journal of Mathematics, 19, 6–12.

Buja, A., Stuetzle, W. and Shen, Y. (2005) Loss functions for binary class probability estimation and classification: Structure and applications. Working paper, http://www-stat.wharton.upenn.edu/~buja/PAPERS/paper-proper-scoring.pdf.

DeGroot, M. H. and Fienberg, S. E. (1983) The comparison and evaluation of forecasters. Statistician, 32, 12–22.

Delbaen, F., Bellini, F., Bignozzi, V. and Ziegel, J. F. (2014) Risk measures with the CxLS property. Preprint, arXiv:1411.0426.

Diebold, F. X. and Mariano, R. S. (1995) Comparing predictive accuracy. Journal of Business and Economic Statistics, 13, 253–263.

Efron, B. (1991) Regression percentiles using asymmetric squared error Loss. Statistica Sinica, 1, 93–125.

Elliott, G., Ghanem, D. and Krüger, F. (2015) Forecasting conditional probabilities of binary outcomes under misspecification. Working paper, Department of Economics, University of California at San Diego, https://sites.google.com/site/fk83research/papers.

Embrechts, P., Puccetti, G., Rüschendorf, L., Wang, R. and Beleraj, A. (2014) An academic response to Basel 3.5. Risks, 2, 25–48.

Engelberg, J., Manski, C. F. and Williams, J. (2009) Comparing the point predictions and subjective probability distributions of professional forecasters. Journal of Business and Economic Statistics, 27, 30–41.

Faust, J. and Wright, J. H. (2013) Forecasting inflation. In Handbook of Economic Forecasting (eds G. Elliott and A. Timmermann), vol. 2A, pp. 2–56. Amsterdam: Elsevier.

Fissler, T. and Ziegel, J. F. (2015) Higher order elicitability and Osband’s principle. Preprint, arXiv:1503.08123.

Gneiting, T. (2011) Making and evaluating point forecasts. Journal of the American Statistical Association, 106, 746–762.

Gneiting, T. and Katzfuss, M. (2014) Probabilistic forecasting. Annual Review of Statistics and Its Application, 1, 125–151.

Gneiting, T. and Raftery, A. E. (2007) Strictly proper scoring Rules, prediction, and estimation. Journal of the American Statistical Association, 102, 359–378.

Gneiting, T. and Ranjan, R. (2011) Comparing density forecasts using threshold and quantile weighted proper scoring rules. Journal of Business and Economic Statistics, 29, 411–422.

Gneiting, T. and Ranjan, R. (2013) Combining predictive distributions. Electronic Journal of Statistics, 7, 1747–1782.

Gneiting, T., Balabdaoui, F. and Raftery, A. E. (2007) Probabilistic forecasts, calibration and sharpness. Journal of the Royal Statistical Society Series B: Statistical Methodology, 69, 243–268.

Gneiting, T., Larson, K., Westrick, K., Genton, M. G. and Aldrich, E. (2006) Calibrated probabilistic forecasting at the Stateline wind energy center: The regime-switching space-time method. Journal of the American Statistical Association, 101, 968–979.

Hand, D. J. and Vinciotti, V. (2003) Local versus global Models for classification problems: Fitting models where it matters. The American Statistician, 57, 124–131.

Holzmann, H. and Eulert, M. (2014) The role of the information set for forecasting – with applications to risk management. Annals of Applied Statistics, 8, 595–621.

Hong, T., Pinson, P. and Fan, S. (2014) Global Energy Forecasting Competition 2012. International Journal of Forecasting, 30, 357–363.

Huber, P. J. (1964) Robust estimation of a location parameter. Annals of Mathematical Statistics, 35, 73–101.

Johansen, S. (1974) The extremal convex functions. Mathematica Scandinavica, 34, 61–68.

Koenker, R. (2005) Quantile Regression. Cambridge: Cambridge University Press.

Koenker, R. and Bassett, G. (1978) Regression quantiles. Econometrica, 46, 33–50.

Koltchinskii, V. I. (1997) M-Estimation, convexity and quantiles. Annals of Statistics, 25, 435–477.

Krämer, W. (2005) On the ordering of probability forecasts. Sankhy, 67, 662–669.

Laio, F. and S. Tamea (2007) Verification tools for probabilistic forecasts of continuous hydrological variables. Hydrology and Earth System Sciences, 11, 1267–1277.

Lieli, R. P. and Springborn, M. (2013) Closing the gap between risk estimation and decision making: Efficient management of trade-related invasive species risk. Review of Economics and Statistics, 95, 632–645.

Matheson, J. E. and Winkler, R. L. (1976) Scoring rules for continuous probability distributions. Management Science, 22, 1087–1096.

Merkle, E. and Steyvers, M. (2013) Choosing a strictly proper scoring rule. Decision Analysis, 10, 292–304.

Murphy, A. H. (1977) The value of climatological, categorical and probabilistic forecasts in the cost-loss ratio situation. Monthly Weather Review, 105, 803–816.

Murphy, A. H. and Winkler, R. L. (1987) A general framework for forecast verification. Monthly Weather Review, 115, 1330–1338.

Mylne, K. R. (2002) Decision making from probability forecasts based on forecast value. Meteorological Applications, 9, 307–315.

Newey, W. K. and Powell, J. L. (1987) Asymmetric least squares estimation and testing. Econometrica, 55, 819–847.

Newey, W. K. and West, K. D. (1987) A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent correlation matrix. Econometrica, 55, 703–708.

Patton, A. J. (2011) Volatility forecast comparison using imperfect volatility proxies. Journal of Econometrics, 160, 246–256.

Patton, A. J. (2015) Comparing possibly misspecified forecasts. Working paper, Department of Economics, Duke University, http://public.econ.duke.edu/~ap172/Patton_bregman_comparison_27mar15.pdf.

Phelps, R. R. (2001) Lectures on Choquet’s Theorem, 2nd edn. Heidelberg: Springer.

Richardson, D. S. (2000) Skill and relative economic value of of the ECMWF ensemble prediction system. Quarterly Journal of the Royal Meteorological Society, 126, 649–667.

Richardson, D. S. (2012) Economic value and skill. In Forecast Verification: A Practitioner’s Guide in Atmospheric Science (eds I. T Jolliffe and D. B. Stephenson), 2nd edn., pp. 167–184. Chichester: Wiley.

Rudebusch, G. D. and Williams, J. C. (2009) Forecasting recessions: The puzzle of the enduring power of the yield curve. Journal of Business and Economic Statistics, 27, 492–503.

Savage, L. J. (1971) Elicitation of personal probabilities and expectations. Journal of the American Statistical Association, 66, 783–810.

Schervish, M. J. (1989) A general method for comparing probability assessors. Annals of Statistics, 17, 1856–1879.

Schulze Waltrup, L., Sobotka, F., Kneib, T. and Kauermann, G. (2014) Expectile and quantile regression — David and Goliath? Statistical Modelling, doi:10.1177/1471082X14561155.

Shuford Jr, E. H., Albert, A. and Massengill, H. E. (1966) Admissible probability measurement procedures. Psychometrika, 31, 125–145.

Smet, G., Termonia, P. and Deckmyn, A. (2012) Added economic value of limited-area multi-EPS weather forecasting applications. Tellus Series A, 64, 18901.

Steinwart, I., C. Pasin, R. C. Williamson and Zhang, S. (2014) Elicitation and identification of properties. Journal of Machine Learning Research, 35, 1–45.

Thompson, J. C. and Brier, G. W. (1955) The economic utility of weather forecasts. Monthly Weather Review, 83, 249–253.

Thomson, W. (1979) Eliciting production possibilities from a well-informed manager. Journal of Economic Theory, 20, 360–380.

Tsyplakov, A. (2014) Theoretical guidelines for a partially informed forecast examiner. Working paper, http://mpra.ub.uni-muenchen.de/55017/.

Vardeman, X. and Meeden, G. (1983) Calibration, sufficiency, and dominance relations for Bayesian probability assessors. Journal of the American Statistical Association, 78, 808–816.

Wilks, D. S. (2001) A skill score based on economic value for probability forecasts. Meteorological Applications, 8, 209–219.

Wolfers, J. and Zitzewitz, E. (2008) Prediction markets in theory and practice. In The New Palgrave Dictionary of Economics (eds S. N. Durlauf and L. E. Blume), 2nd edn. London: Palgrave McMillan.

Ziegel, J. F. (2014) Coherence and elicitability. Mathematical Finance, DOI:10.1111/mafi.12080.

Appendix A: Proofs

The specific structure of the scoring functions in (5) and (7) permits us to focus on the case in the subsequent proofs, with the general case then being immediate.

A1 Proof of Theorems 1a and 1b

In the case of quantiles, the mixture representation (9), the fact that for , and the relationship for , are straightforward consequences of the fact that for every and ,

As the increments of are determined by S, the mixing measure is unique.

Turning now to the case of expectiles, we associate with any function the Bregman type function of two variables

| (35) |

Then the mixture representation (14), the fact that for , and the relationship for , are immediate consequences of the fact that for all and ,

The case is handled analogously, and the case is trivial. Finally, as the increments of are determined by S, the mixing measure is unique.

A2 Proof of Propositions 1a and 1b

In the case of the elementary quantile scoring function (18), suppose that , where and are of the form (5) with associated functions . Then

As we have if , and if , where . It follows that in the first case, in the second case, and in the third case. This coincides with the value distribution of when , whence indeed .

In the case of the elementary expectile scoring function (18), suppose that , where and are of the form (7) with associated functions . Let be defined as in (35). Then

Taking left-hand derivatives with respect to , we obtain

As , we may apply the same argument as in the quantile case to show that , whence .

A3 Proof of Propositions 2a and 2b

In the case of the elementary quantile scoring function in (13) suppose first that . Since

we have

The second factor on the right-hand side vanishes unless , and under this latter condition we have and , whence the desired expectation inequality. The case is handled analogously.

In the case of the elementary expectile scoring function in (18) we assume first that , where denotes the -expectile of . Since

we get

As the first term on the right-hand side is strictly increasing in and has a unique zero at the -expectile of , the proof can be completed in the same way as above.

Appendix B: Details for the synthetic example

| Forecast | -Quantile | Mean |

|---|---|---|

| Perfect | ||

| Climatological | ||

| Unfocused | ||

| Sign-reversed |

Here we give details for the synthetic example introduced in Table 2 and discussed throughout Section 3. Table 3 shows analytic expressions for the expected score

where is either the perfect, the climatological, the unfocused, or the sign-reversed forecaster, and the functional is either the -quantile, , or the mean, , of the CDF-valued random quantity . The scoring function S is the elementary quantile scoring function in (13) or the elementary scoring function in (18). For example, if is a quantile forecast for at level then

| (36) |

decomposes into three terms, the first depending on the outcome only, the second depending on the forecast only, and the third accounting for the joint distribution. In view of the relationships (20) and (22), the foregoing covers the case of the extremal scoring function for event probabilities, too.