Games and Meta-Games:

Pricing Rules for Combinatorial Mechanisms

This Version: March 20, 2015)

Abstract

In settings where full incentive-compatibility is not available, such as core-constraint combinatorial auctions and budget-balanced combinatorial exchanges, we may wish to design mechanisms that are as incentive-compatible as possible. This paper offers a new characterization of approximate incentive-compatibility by casting the pricing problem as a meta-game between the center and the participating agents. Through a suitable set of simplifications, we describe the equilibrium of this game as a variational problem. We use this to characterize the space of optimal prices, enabling closed-form solutions in restricted cases, and numerically-determined prices in the general case. We offer theory motivating this approach, and numerical experiments showing its application.

1 Introduction

Market mechanisms increase the welfare of their participants by enabling the transfer of goods and services from those with low value for their holdings to those with high value for those resources. For transacting large numbers of identical goods (like stocks), the double auction formats used in financial markets work very well. However, there are many contexts in which goods are not uniform and participants value different bundles of goods in complex ways, and we thus need a more complex design. This paper offers a novel way to frame the problem of constructing mechanisms in these complex settings, and then instantiates several concrete cases and solves them. The resulting mechanisms reduce the level of strategic manipulation of bids in equilibrium, which decreases the cognitive load of participants, in turn lowering the barrier to agent participation and, even more importantly, raising the overall efficiency of the outcome implemented.

1.1 Combinatorial Mechanisms

Combinatorial mechanisms are designed for settings where the allocation of multiple goods to multiple participants is required, and where the participants value packages of goods at either greater or less than their constituant parts. A prominent domain where such complex mechanisms are needed is in markets for the transfer of billions of dollars of radio spectrum rights from governments around the world to mobile phone carriers (Kwerel and Williams 2002). In such markets different frequency blocks have different properties and thus different values; and a single frequency in different geographical regions also can have wildly different values. Bidders are interested in packages across various geographic areas in order to implement regional or national business plans. Other such examples include the transfer of aircraft landing rights at airports (Ball et al. 2006), complex procurement and logistics markets (Sandholm 2007), and the lease of computational resources in large-scale datacenters (Guevara et al. 2014).

Most of the mechanisms that have been designed for these settings are Combinatorial Auctions (CA). In CAs the goods are all offered by a single seller, while multiple buyers use an expressive bidding language to state their bid for different bundles of goods to the mechanism. The mechanism clears the market by determining the welfare-maximizing allocation at the buyer reports, and then charges these winning bidders according to a specific payment rule, which will be a central concern of this paper. If instead (1) there is more than one seller; (2) these sellers are allowed to specify complex reserve values over the goods they are offering; and (3) participants can both buy and sell simultaneously – then this two-sided market is called a Combinatorial Exchange (CE).

Unlike the CAs that have been widely adopted, CEs have not been widely used. This is so, despite the need to reallocate goods in these same settings in secondary markets that are thus by definition two-sided in nature. For example, the upcoming “Incentive Auction” planned by the FCC is intended to facilitate reallocation of spectrum between firms, each of which have combinatorial preferences (FCC 2014). The FCC plans to run a reverse auction to recapture rights from existing holders followed by a forward CA to offer these rights to new owners. However, this design precludes participants from swapping one set of goods for another without potentially selling their goods and subsequently failing to obtain new goods. A full CE would solve this problem, but such designs have rarely been proposed (Lubin et al. 2008). One reason for this is a lack of consensus about how best to price them. The famed VCG mechanism may run at a deficit for CEs, precluding its use without undesirable subsidies; the Core may be empty for CEs, meaning that the pricing rules that have recently gotten much attention in CAs (c.f. UK bandwidth auctions (Cramton 2013)) are also not available. Our method provides high-quality pricing rules for CEs, enabling their possible use in these billion dollar markets.

1.2 The Problem With Payment Rules

When designing a combinatorial mechanism, there are design challenges in specifying the bidding language, a tractable winner-determination algorithm, and effective activity rules. But it is the payment rule that directly mediates the economic and game-theoretic aspects of the mechanism. The study of payment rules is thus of paramount importance, and is our focus here. Specifically, there are a number of desirable properties we would like our payment rules to have:

- Individual Rationality (IR)

-

Ex-post, individual bidders prefer to have participated in the mechanism, rather than remained outside it. Concretely, this means bidders receive only weakly positive profits at their reported values.

- (Weak) Budget Balance (BB)

-

The total payments paid by bidders to the mechanism is weakly greater than the total disbursements by the mechanism; e.g. no subsidy is required to run the mechanism.

- Incentive Compatibility (IC)

-

In equilibrium, bidders should not have to strategize in submitting their bids; e.g. stating one’s value truthfully should yield the maximum profit.

In addition to these properties of the payment rule, we are interested in mechanisms that use the most natural winner determination rule, one that implements the total value-maximizing allocation at the bids. In conjunction with incentive compatibility, this yields a mechanism offering:

- Efficiency (Eff)

-

The mechanism implements the total value-maximizing allocation at the participant’s true values.

For CAs, only one mechanism satisfies all four of these properties: the famous Vickrey-Clarke-Groves (VCG) Auction (Nisan 2007), which is a generalization of the second-price or Vickrey (Vickrey 1961) auction to settings with combinatorial preferences. In VCG, a participant pays his bid, less his marginal impact on the main economy (i.e., the difference in social welfare between the main economy and the economy where the participant is omitted). However, as has often been pointed out (Ausubel and Milgrom 2006), VCG yields very low revenue to the seller in the CA setting, which in turn creates incentives for undesirable behavior on the part of participants – for example, sybil attacks, where a single firm bids under several identities. Further, VCG payments in a CA can be outside the Core (Shapley and Scarf 1974). This means that VCG prices may be sufficiently low that, ex-post, the seller may prefer to transact with a coalition of the bidders at a price higher than VCG, rather than accept the VCG outcome.

To get around these problem, the most recent spectrum auctions have been built around pricing rules that implement prices in the core, and thus which may derive substantially more revenue than VCG (Day and Milgrom 2008). However, as soon as prices are chosen to obey the Core constraints, we will have to relax one of our aforementioned other properties. In this work, we choose to relax the incentive-compatibility property.

For CEs, the situation is even worse. Even without core constraints, the seminal Myerson-Satterthwaite Impossibility theorem (Myerson and Satterthwaite 1983) tells us that no design can manifest our desired four properties (IR, BB, IC, Eff) simultaneously in this setting.111In CEs, the core is often empty, so it is not typically considered in defining payments. However, it is possible to include it by instead targeting the minimal core (or nucleolus). Again, it is necessary to relax one of the four conditions. Because IR, BB and Eff are typically considered hard constraints, we again choose to relax IC.

Even designs that are not explicitly combinatorial in nature can have similar problems. For example, the Generalized Second Price (GSP) auction (Edelman et al. 2007) used by the major search engines to sell the links in the sponsored section of their results pages is not equivalent to VCG, and thus is not IC. In this case, while VCG is available, we are restricted from using it by a constraint on the simplicity of the mechanism (e.g. single-dimensional prices). One instead might want a mechanism that is maximally IC, while still obeying a constraint on simplicity.

In all these cases, what we want is a mechanism that from the participant’s perspective looks like VCG. However, we want to charge something slightly greater than VCG in order to meet the other other requirements of the domain (e.g. to be in the core of a CA, attain budget balance in a CE, or maintain simplicity in the sponsored search setting). Charging this extra amount will mean, of necessity, that our mechanism will not be IC. And consequently, the complex problem presented in this paper reduces to the simple question of: for each participant, how much more than VCG should we charge? But, this is far from straightforward, because (1) it is not clear by what measure we should define “as close to incentive compatible as possible,” and (2), having chosen a measure, it is typically an intractable optimization problem to find the optimal prices.

In this paper, we will propose a new way to define approximate incentive-compatibility, carefully chosen so as to capture the essential aspects of the design problem, while simultaneously being computationally tractable enough that the design problem can be solved.

1.3 Our Solution

The goal of this paper, then, is finding good approximately incentive-compatible prices, with a focus on the CE setting. In service of this goal, we begin with a new definition of approximate incentive compatibility. Such a definition requires a model for the information set employed by participants when they devise their strategy (Lubin and Parkes 2012). Traditionally this is either (1) ex-ante, where the agent knows only the distribution over all agent values; (2) ex-interim, where each agent additionally knows his own values exactly; or (3) ex-post, where all bidders have complete information. Instead, we model bidders as being boundedly informed about the values in the setting. Specifically, we introduce the concept of a blinding distribution, used to approximate ex-interim prices, while retaining the tractability of ex-ante and ex-post formulations.

A key insight of the paper is that when mechanisms are used in practice, payoffs are generally drawn from a distribution about which participants have imperfect knowledge. Thus by moving from the traditional framework where participants reason about values, to one where they reason about payoffs (which is, what they ultimately care about), we obtain a very useful dimensionality reduction which we can leverage computationally to better be able to minimize the incentive to manipulate bids. In this sense, the present paper generalizes VCG to the more restrictive settings described above.

Based on this new information definition, we then frame the resulting approximate IC pricing problem as a variational calculus problem, the solution of which is a novel payment rule for domains where VCG isn’t available. The full formulation can be interpreted as a Bayesian Stackelberg game (Simaan and Cruz Jr. 1973), where the mechanism designer moves first by picking the parameters of the game to be played so as to make it as incentive compatible as possible, and the participants then attempt to obtain as much individual gain as they can within this game. The chosen rules and resulting optimal agent-strategies will be the equilibria of this Stackelberg meta-game. However, because the game is a stochastic game with an infinite strategy space it is not tractable to solve for the Stackelberg equilibrium, and we therefore adopt a simpler Bayes-Nash equilibrium concept for our solution.

Having constructed this model, we then offer a description of the space of optimal rules and game equilbria consistent with the formulation, using variational methods. This analysis permits us to critique several existing rules from the literature on a theoretical basis. We close by providing multiple examples of numerical solutions to the variational pricing problem, and characterize these solutions.

In most cases, the rules obtained cannot be described in closed form, and must be determined computationally. However, provided suitable distributions are available to instantiate the information model, the methods provided can readily be employed to furnish an alternative to VCG that is as incentive-compatible as possible, and thus as efficient as possible, given the need to satisfy other hard constraints that preclude the direct use of VCG.

2 Theory

Many payment rules for combinatorial mechanisms have been proposed in the literature. We briefly review these, by way of motivating our method for achieving approximate incentive compatibility.

Parkes et al. (2001) provide the Threshold rule, which minimizes the maximum ex-post regret across agents. Several basic rules are also defined therein: Small, which gives all surplus to those with little of it; and Large, which does the opposite, among other rules. Each of these rules is optimal relative to a specified metric of payoffs at reported values. However, the analysis is not in BNE, and thus it is not clear which rule actually yields the best incentives or the highest efficiency when agents strategize. Lubin and Parkes (2009) propose a Reference rule, that seeks to minimize the KL-Divergence between the distribution on payoffs in the reference (e.g. VCG) and in the implemented mechanism, and show that rules with payoff distributions similar to the reference will have similar incentive properties in equilibrium. The work also evaluates the Threshold, Small and Large rules in approximate BNE, and finds that among the rules tested, Small often works well. However, Small gives no discount at all to those bidders who get the most under VCG, and is thus hard to argue for in practice. Further, the 2009 paper evaluates only a small set of fixed rules. The present work shows, on the other hand, that we can do better by considering a broader set of possibilities, especially rules with no closed form that must be determined computationally.

Erdil and Klemperer (2010) define a rule that minimizes the marginal incentive to deviate from truthful bidding over small misreports, arguing that this is a minimal condition for approximate strategyproofness. However, paper is silent on what to do when larger misreports are optimal for participants, given the nature of the underlying domain and design constraints. By contrast, the present work handles situations where even very large deviations from truthful bidding are strategically elicited in the best responses of bidders.

A different thread of work has sought not closed-form rules, but rules that can be calculated algorithmically, as proposed here. Conitzer and Sandholm’s Automated Mechanism Design (2004) captures the full design, including allocations and payments, within this numerical framework, but can only solve small problems, given the high computational complexity. Empirical Mechanism Design (Vorobeychik et al. 2006, 2007) parametrizes the design space and then uses computational techniques to find optimal parameter settings. This is similar in spirit to the approach taken herein. However, rather than fitting the parameters of specific functions, we instead formulate our version of the payment problem in the calculus of variations and, lacking a closed-form solution, perform computation from there. (Variational calculus goes all the way back to Bernoulli, but the major development was by Euler and Lagrange in the 18th century; a good overview of variational methods is provided by Smith (Smith 1998).)

Finally, we point the reader to recent work by Nisan et al. (2011), which identifies auction settings where, under certain informational assumptions, player best-response dynamics will lead to the efficient outcome even without fully IC prices. One view of the present work is as a generalization of this idea to settings that are only approximately IC. Another approach to avoiding complexity is to create a replication economy by increasing the number of players and goods in order to “wash out” local effects. This is the method employed by the related method of Strategyproofness in the large (Azevedo and Budish 2012); by contrast, we reason about the unmodified economy directly.

2.1 Preliminaries

Although our ideas are more broadly applicable, for simplicity we will here focus on Combinatorial Exchanges (CEs). Formally, we have a set of goods and agents. Each agent has an initial endowment , and a true value for each potential trade of goods they might buy or sell.222Without loss we will assume unique goods; all points generalize to the case of multiple identical items. We will denote those goods bought and those sold , and the vector of such trades as . Because of the Revelation Principal (Myerson 1979), we may restrict ourselves to mechanisms where agents state a claim of value (bid) on a potential bundle; however, we must capture that they may still choose to report untruthfully as . To simplify notation, we will refer to and ; we use and for the value of all agents but . We are concerned with mechanisms that implement the efficient outcome at reports, e.g. subject to feasibility , and restricted endowment . We denote such an efficient trade as , and with a slight abuse of notation, as the value to the agent of the efficient trade when he reports , and similarly for .

Our mechanism will also charge each agent payments , and we note that these may be negative (for e.g. sellers or swappers) in a CE setting. Without loss, we can describe prices by a discount instead, where for some specified by the payment rule. We will consider settings of quasi-linear utility; e.g., an agent’s utility or profit is given by . We will sometimes parametrize this as , or the agent’s profit when he has true value , reports , and all other agents’ reports .

The well known VCG mechanism uses as its discount the marginal impact of the agent, e.g. the difference in social welfare between the main economy and the economy where the agent is omitted. Formally: . We note that the VCG discount enables us to find the critical value, , which is the minimum agent could have bid while still winning when all are held fixed. This choice of payment is individually rational (), and strategyproof (agents have a dominant strategy to report ). However, as mentioned in the introduction, in a CE setting VCG is not (weak) budget-balanced in Bayes-Nash Equilibrium (BNE) (, requiring the center to subsidize the outcome).333 A consequence of the Myerson-Satterthwaite Impossibility theorem (Myerson and Satterthwaite 1983).

2.2 Defining Approximate Incentive Compatibility

As was mentioned in the introduction, we want a mechanism consistent with this CE setup that implements the efficient allocation at reports, and which uses a payment rule that is individually rational and budget-balanced. But we know that to do this we will have to give up the property of incentive compatibility. Consequently, we seek a rule that yields maximal efficency at the reported values in practice. To do this, we will want the ratio of total value in the allocation at reported values and at true values to be as close to one as possible, e.g. . A rule that yields the closest such limit, we deem to be approximately incentive compatible, and is our overall goal. More concretely, we need to specify: (a) what types of misreporting a participant can perform and (b) what information the participant has when deciding how to misreport (i.e. the nature of the BNE). For the setting outlined in the previous section, (a) is simple: we allow for all possible misreports ; e.g., particupants may state some other value than the truth for all bundles . The information-set (b), though, requires explication.

2.2.1 Participant Information-Sets

Because we are doing our analysis in full BNE, if the information-set is complex, then evaluating equilibrium is likewise computationally complex, and often prohibitively so. Consequently a number of proposals have been made in the literature for simple information-sets that lead to tractable analysis of the degree of misreporting, making the problem of finding the degree of efficiency loss solvable, and thus making design under the given approximate IC criterion possible. (See Appendix A for details, and Lubin and Parkes (2012) for a longer discussion.)

The simplest approach is to assume that participants are fully informed about all values in the market. Because this sort of analysis is using information that is typically available only after the mechanism is complete (even for decisions that are made up front), it is often referred to as an ex-post analysis. Consequently, this choice of information-set collapses our BNE calculation to a normal Nash equilibrium. While appealing for simplicity and computational reasons, it is highly unrealistic in many settings.

Instead, one can assume that participants make their strategic decisions when they have no more than an expectation as to the values in the market. In such an ex-ante model, the participant has only probabilistic information about his own value. This is unrealistic in most settings – e.g., while ex-post is too informed, ex-ante is too uninformed. Consequently an ex-interim information-set – where the participants know their own value, but have only probabilistic information about all the values of other bidders – attempts a “Goldilocks” formulation between the other two. However, such a set is computationally challenging compared to the other two, because it possesses neither the simplification of full information, nor of everything being performed in a simple expectation.

2.2.2 Simplification Via the Potential Profit

One contribution of this work is a novel information-set definition that has the tractability of an ex-post measure, but the economic intuition of an ex-interim measure.

In considering what information-set to use, we focus on the information a participant both needs and has in making his decision about how to interact with the mechanism. In practice, bidders are boundedly informed and boundedly rational, and we want a model that captures this.

It seems reasonable to assume that participants know not only their own value for a bundle of goods, but also what they will pay for a bundle, conditioned on bidding for it and winning it. Further, that they know they may lose the bundle, and in fact may have an idea of how likely this is, as a function of their bid report.

Dispite its common use in analysis, it is generally unreasonable to assume participants know the exact (ex-post) values of other bidders for all bundles, or even for the allocated bundle. However, firms often have some idea of their opponents’ business plans – after all, they are typically in the same industry. And thus they may have distributional information about the values of their opponents. That is, they may be able to view their competition as having been sampled from some IID population of competitors.

However, as it turns out, we can conveniently summarize all of this information into a single unidimensional property: the distribution on available profit under the VCG rule to a given participant. As we shall see, it is this distribution that really captures the competitive environment a participant finds himself in. Formally we have the following (proofs are left to Appendix B):

Observation 1.

Holding the bids of the other players constant, each winning bid has two additive components: (1) an amount that by definition is needed or the bidder will lose his bundle and (2) an amount in excess of this.

Observation 1 lets us focus, not on the joint trade and reported valuation profile when considering a bidder’s bid (and subsequent payment), but instead solely on the amount , the amount over the critical value that is offered in the bid. is strictly positive, because were it to ever run negative, the bidder would have reported below its critical value, and lost the bundle.

Observation 2.

For VCG, in equilibrium (e.g. the VCG profit is the discount in equilibrium).

Observation 2 lets us give a useful name and interpretation: the bidder’s profit as calculated by the VCG Rule (but in general, not necessarily at truthful bids of others). In VCG, where is truthful, this will be equivalent to the VCG discount. Alternatively, we can view as the amount of surplus attributable to at his reported value, be that truthful or otherwise. We refer to as the potential profit, i.e. the amount VCG would offer, even if our eventual rule often will not be able to provide this much and maintain its other requirements (such as budget balance).

In general, should be consided to be taken relative to the reported values of other players, i.e. when they behave in equilibrium. But it is calcuated at the true value of the player whose incentives are being considered. That is, as , the first term is ’s truthful value, while the second term is ’s critical value, which is independent of and is taken at the equilibrium reports of the other agents. In other words, it is the amount an agent would make if it told the truth, everyone else played the equilibrium, and the mechanism was charging this particular bidder as if it were VCG. As we shall see, this unusual structure enables us to capture both ’s true value and the environmental conditions faces simultaneously.

Observation 3.

Out of equilibrium but above the reported discount (e.g. the VCG formula evaluated at a non-truthful bid) shifts by exactly the amount of the misreport, such that the true profit remains the same, .

Every closed-form payment rule reported in the literature to date, including VCG, Threshold, Small, Large, etc, can be expressed as , the discount supplied when the report is above (Parkes et al. 2001). Thus is a convenient way to parametrize a payment rule, and for the same reasons it is a convenient way to think about the information available to a bidder. For example, VCG has a characteristic signature when viewed from this perspective: the discount supplied rises one-for-one with , which Observation 3 reveals to have the effect of keeping the profit constant regardless of the report. It is this that ultimately makes VCG strategyproof. Non-incentive compatible rules won’t have this property. But by focusing on profit under a given rule as a function of , we capture bidders’ incentive structure perfectly, conditioned on the behavior of other players and upon the allocation remaining fixed.

2.2.3 The Distribution of Potential Profit

Because we want to do design in BNE, we must be able to reason about the distribution on possible participant values, rather than a specific outcome. Consequently, we let represent a distribution over the potential profit that the bidder would obtain if he were paying the VCG rule, given the reported behavior (under the actual mechanism being used, not VCG) of the other bidders, and conditioned on winning . It is thus dependent on the reports of the other agents, as well as dependent on the true value of agent .

The distribution is over many counterfactual instantiations of the market domain drawn IID from some consistent underlying generation process. In the real world, such a distribution may be built up by considering the many examples in a repeated game if the dynamic process is reasonably stationary. Alternatively, one can model the participants and view the distribution as having been constructed from many instances drawn from a synthetic bid generator.

Our model is consistent with the distribution over the rest of the agent’s value either occurring at truth, or having been calculated according to the BNE of the resulting overall market mechanism. In a synthetic context, using the truth-based distribution will be easier, as finding the reported values of the other agents would require solving for the BNE of the mechanism. However, in a repeated real-world game, the observed bids are presumably approximately equilibrium bids (depending on the sophistication of the players), making the equilibrium-based distribution the easier version to obtain. Our rule is not agnostic to this distinction: it will provide different rules depending on the calculated . It is, however, well-defined and consistent for both. We will focus on the version where the other agents are bidding in equilibrium, because we view this as the more natural instantiation of the mechanism.

2.2.4 The Blinded Regret Information-Set

If bidders know exactly and they know the payment rule in place, they have ex-post information – they know exactly the topology of the incentive structure they face. This is exactly equivalent to their knowing their critical value exactly, which is functionally equivalent to knowing the bid values of all the other agents in the winning allocation. They can then behave optimally, bidding exactly their critical value, which, under any individually rational payment scheme, should give them maximum profit. Clearly this ex-post structure is undesirable. The construction of alone does not ameliorate this: tells us how frequently a given value of occurs, but if agents know this exact value when they choose their report, we are still in an ex-post scenario. By contrast, if bidders must choose their report based only on knowing in aggregate, but not which particular value of they directly face, we have an ex-ante condition – the bidder has no concrete knowledge of his own value. For the reasons described in section 2.2.1, neither of these extremes is desirable.

We would prefer an information-set that behaves more like an ex-interim condition. Our solution is to adopt an explicit model of the uncertainty that the bidder has about the value of joint bids, which we call the blinding distribution. More specifically, given that represents the actual distribution of VCG-rule profits available in the mechanism, we use a structure where bidders only have a guess about what their particular profit, , is, conditional on the overall actual distribution being . The blinding distribution represents the bidder’s belief about the value of , conditioned on being the true . We then compound with to produce

| (1) |

and it is then this function, , which we assume the bidders have access to, not . In the experiments in section 4, we use a truncated Normal for .

This approach allows us to smoothly interpolate between an ex-ante condition, which occurs when is the uniform distribution and the expected ex-post regret, which occurs when is the Dirac distribution. Cases between these, e.g. when is Normal, represent an interim information state. This state is not identical to that defined in the richer ex-interim deviation incentive (see Appendix A, although intuitively they both lie between ex-ante and expected ex-post).

2.2.5 Blinded Regret Approximate Incentive Compatibility

Given the attractive information-set just described, knowlege of and of the payment rule in place, we can quantify how much incentive an agent has to modify his bid away from truth, the Blinded Regret Deviation Incentive:

| (2) |

where is bidder ’s belief about his potential profit, when he has been blinded by some distribution that has been compounded with to form by equation 1. Further, is the true profit to bidder under the actual rule being evalated, when he reports and his available potential profit is . The first term then represents the amount the bidder believes he can profit by best misreporting under the blinded regret information-set. The second term is the amount bidder can profit if he simply reports the truth in the mechanism. Thus the difference is the potential gain of the bidder when he best responds. Given this definition of approximate incentive compatibility, we next turn to the construction of optimal rules by this criterion.

2.3 Optimal Approximately Incentive Compatible Payment Rules

If we want to computationally obtain a perfectly IC payment rule, we can cast the problem as an Automated Mechanism Design (Conitzer and Sandholm 2004), as we do in Appendix C. However, the full problem is hopelessly intractable for any but the simplest of instances. But, by focusing on instead of on the full trade and allocation space, we have reduced the complexity of the payment function definition massively. Contingent on the other bidders being fixed and on winning the bid, this reduction has been without loss and is perfectly consistent with all prior closed-form rules in the literature, and is consequently the approach we take here.

We will find it convenient to work with functions that move in the same direction as payments, unlike the discounts used so far. Consequently, we define . This function represents the amount the agent is asked to pay above the critical value (which he must alway pay in any reasonable mechanism). Consequently, the final payment the agent is asked to make will be . Further, this function has a useful interpretation as the ex-post regret a bidder has for reporting for instead of reporting exactly the critical value , which for all IR payment rules is the optimal report (i.e. represents the potential gain if the agent were able to making the ex-post optimal report). We note that all existing closed-form rules treat all bidders symmetrically, and using enables us to do the same by applying the same payment rule to all bidders. Our task, then, is to identify payment rules that are optimal under the blinded regret approximate IC criterion we have just identified.

2.3.1 The Ex-Ante Variational Problem

We first copnsider the case where the blinding distribution is Uniform over the full domain and thus, after blinding, the agent has no concrete information about his true value. This case corresponds to an ex-ante condition. Moreover, we restict ourselves to the case where the bidder adopts a strategy where he chooses but a single “shade” parameter by which to offset his true bid in the mechanism (and we generalize this in the next section). In this case, the bidder’s problem becomes an unconstrained non-convex optimization in one dimension:

| (3) |

where is a distribution over the profit that the bidder would obtain if he were paying under the VCG rule (and everyone else is in equilbrium), and is the amount that the agent shades his report down from, below his true value, and is the indicator function.

In (3), is used to construct an expectation for the regret the bidder retains for reporting instead of the ideal when is small enough that he still wins, plus his regret over the full potential profit in the case where the bidder has shaded so much that he has lost the bid. By minimizing this aggregate regret, the bidder is simultaneously maximizing his expected reward.444Because we have inverted this optimization for clarity of exposition, our problem now appears to be a min-min problem; but note that due to the structure of the coupling between this and the subsequent problem, we do indeed still have a min-max problem.

The structure of the center’s problem is specific to the mechanism being designed, and so we now specialize to budget-balanced CEs. We have a constrained linear-variational program:

| Regret at truth | (4) | ||||

| s.t. | BB | ||||

The variable in this variational program is picked to minimize the expected regret the bidder will face when bidding truthfully. The first constraint ensures that the total regret when the bidder shades must be at least . For a suitably chosen this ensures that a sufficiently small amount of discount be doled out, such that budget balance can be achieved. Next we constrain the rule to ensure that no discount is negative (or equivalently, ), as a negative discount implies you must pay more than your report, violating individual rationality for truthful bids. Lastly, we include any additional constraints from the setting we need, as additional restrictions on . Here we include the restriction that discounts must be no greater than VCG (or equivalently, ), to be consistent with the other rules from the literature. We will return to this setup in Section 4 to illustrate its solution in a typical environment.

2.3.2 The Blinded Regret Variational Problem

Now we turn to realizing the more complex case where we both have a blinding distribution, and where the bidder’s strategy is defined as a function , rather than a simple constant. With this change we obtain:

| (5) |

Note that in this formulation as we let we will move into an expected ex-post regret world and the bidder will be able to respond optimally for every . The solution then becomes , with the bidder reporting exactly everytime. We thus ensure that we always choose such that it always has a non-zero variance.

In concert with this change for the bidder, a few updates are in order for the center as well. First, if the bidder is reasoning based on partial information, it makes sense for the center to use in its objective also, so it is attempting to incentivize the agent based upon the information-set that the bidder will ultimately use. Second, the assumption that the center has a perfect model of the bidder’s strategy is also too strong. To relax it, we adopt a blinding distribution for the center as well, and apply the resulting compound distribution in the budget-balance constraint. can either model uncertainty on the center’s part about , or equivalently, uncertainty about the choice of that the bidder will employ. Both are available from the same formulation because can be moved into the argument of the distribution function in place of by a suitable change of variables in the integration, making the two interpetations valid upon the same expression simultaneously. Putting this together, we obtain:

| Regret at truth | (6) | ||||

| s.t. | BB | ||||

The use of blinding distributions significantly improves the realism of our model, moving us solidly into a partial information setting.

2.3.3 Analysis via Variational Methods

Our formulation has provided us with several variational optimization problems. Our first step is to construct the necessary boundary conditions. Our restriction that , forcing the rule to be IR and within the discount envelope of VCG, provides a necessary such condition.

With these in place, we might ideally be able to use the Euler-Lagrange equation to transform our optimization problems into sets of differential equations and then solve these for the optimal functions (Wan 1995). But because, Euler-Lagrange can only be applied where we have a non-linear variational form involving at least one set of derivatives, a general closed-form solution is not available by this path.

However, the literature on Variational forms does extend to this case, and offers us the following important insight (Wan 1995): We should expect the function that is the solution to problems with our structure, to always lie on one bound or the other (e.g. the optimal will either be or pointwise). This immediately shows that rules such as the current state-of-the-art Threshold rule, that take on intermediate values, will not be optimal under our criteria. Rules such as Small or Large are admitted in the class, but the class is far larger than just these existing rules. Additionally, if we know the shape that should take (e.g. Large), we can in fact use variational methods to solve for the parameters of this shape.

2.3.4 Characterization as a Stackelberg Meta-Game

We note that the formulations provided in the previous two sections are are in fact min-max functional programs: the center first minimizes over payment functions the expected deviation incentive functional; but this functional is itself a maximization over potential bidder misreports of the bidder’s expected gain in profit over being truthful. Because the two problems are inter-dependent and push in opposite directions, they can be interpreted as a 2-player game. Specifically, since there is a distinct first-mover in the form of the center, who must credibly declare the rules it will use before the bidders then participate, formally we have a Bayesian Stackelberg game. See Basar and Olsder (1995) for details on Stackelberg games. This is, in fact, a general property of the task of mechanism design. We can view the design process itself as a Stackelberg game: the designer/center chooses a mechanism that provides properties she likes best. The players who then participate within the chosen design move second and attempt to maximize their own reward, within the structure they have been given. In otherwords, there is a Stackelberg meta-game whose outcome determines not only play in the eventual actual game (the second move), but also the choice of game to be played itself (the first move).

Stackelberg games are typically solved by backwards induction, where we solve for the optimal behavior of the second-mover first, and then find the first-mover’s strategy that would maximize his reward given the behavior of the second player. Given that moves in our meta-game are the choice of a continuous one-dimensional function ( and respectively), such a backward induction process is prohibitively expensive, even after the above simplifications we have employed. So rather than trying to directly solve the min-max stochastic functional program needed to find the outcome of the Stackelberg meta-game directly, we recast the problem as two separate and opposed optimization problems: one for the bidder’s goal of maximizing his expected profit, and another for the center’s goal of minimizing incentives to misreport. This enables us to solve for the outcome of the BNE of the meta-game with traditional iterated best-response methods. The result, though, will be a BNE of the meta-game, not necessarily a Stackelberg equilibrium of the meta-game. The true Stackelberg equilibria will be those BNE that have maximum value for the first mover (in our case the center). In our numerical experiments, we have not been able to identify more than one stable equilibrium, and so we report on the single equilbria we have identified.

3 Methods

3.1 Parametric Distributions for , and

While it is entirely possible to define by an empirical distribution, in practice it will often be convenient to use a parametric form instead. Because and are constructed from a maximization process, their distributions are well-modeled by Generalized Extreme Value (GEV) distributions (Coles et al. 2001). We are interested in the distribution of the difference in these values, for a truthful bid, because by Observation 3, this is equal to the VCG payoff. Because the difference of uncorrelated GEV variables is a Logistic distribution, one might think that a Logistic would be appropriate. However, these variables are highly correlated. Intead it is more appropriate to think of as an exceedence over the threshold of . A model of this form results in a Generalized Pareto Distribution (GPD) (Pickands III 1975) for . This is consistent with previous work that has fit the distribution of VCG payoffs in a CE setting empirically, and found that it well matched the GPD (Lubin and Parkes 2009).555We note that that the exponential distribution is a special case of the GPD (where shape parameter is 0). As shown in Appendix D, the ratio of to drives the determination of our eventual payment rule. Because the exponential distribution has a fixed failure rate, the ratio of fixed offsets of its pdf is a constant. This means that all feasible rules are possible solutions when is exactly an exponential, under the simpler ex-ante model of Section 2.3.1. This is not true for the more complicated subsequent model.We also note that the GPD is a limiting case model, and other distributions are certainly possible in practice. We therefore also consider the Burr XII distribution which generalizes the GPD and the Log-Logistic model (Burr 1942); it is an attractive choice as it has been used to model income distributions, which is effectively what the VCG profit represents (Champernowne 1952).

In our experiments, we use simple truncated normal distributions for both and . More complex models of bidder information could easily be incorporated, but in the absence of a specific context, we opt for a simple distributions.

3.2 Finding the BNE of the Meta-Game

Ultimately, we will need to solve for the equilibrium of our game. For finite domains, min-max programming techniques might suffice (Aissi et al. 2009). However, our problem has infinite support, and thus we employ iterated best response techniques, which go all the way back to Cournot and Fisher (1897). Specifically, we proceed in rounds where we find the best response for each player to the strategy employed by their opponent in the previous round. For recent treatments of such techniques in settings similar to our own, see Reeves et. al. and Vorobeychik et al. (2004, 2008). Our numerical approach employs a damped form of this method, i.e. with fictitious play (Robinson 1951, Brown 1951). As Shapley noted 1964, this procedure may fail to converge with cycles of best-responses repeating themselves. But, we have been able to force convergence in most cases by imposing suitable (and reasonable) additional boundary conditions, and by leveraging the numerical advantages that happen to come along with the smoothing associated with the blinding distributions described in section 2.2.4.

Next, we describe how we find the best response for each of our variational problems by an appropriate numerical method:

3.3 The Bidder Problem

For the optimal strategy formulation of section 2.3.1 where is a constant, we need only solve a 1-D non-convex optimization to find . Because the problem is unconstrained, it suffices to employ a Brent Line Optimizer (Brent 2013). We note only that it will often be the case that there will be multiple minima with near-equal values. The numerical stability of the algorithm is improved if such ties are broken in a consistent way, e.g. by always picking the minima closest to zero (which is a reasonable assumption for bidder behavior anyway). To implement this, it suffices to perform a simple grid search for potential minima, local search via the Brent solver to improve these results, and then pick the closest to within the equivalence class of minimal solutions. In the more complex formulation of section 2.3.2 where is a function, we simply discretize into bins and run the above method on each. We then approximate as a simple linear interpolation over these points.

3.4 The Center Problem

The Center’s problem is more complicated as a constrained variational program. Nonetheless, if again we discretize into bins, it is straightforward to then cast the problem as an LP that can be solved with e.g. CPlex. The standard version (section 2.3.1) of the problem is then as follows:

| Regret at truth | (7) | ||||

| s.t. | BB | ||||

Where , and are the lower, mid and upper points of bin respectively, and where suitable boundary conditions are in place to ensure that the indexing stays within range regardless of the function. The more complex version of the problem is identical but uses the compound distributions instead of . In both cases we ultimately construct a continuous version of from the discrete by simple linear interpolation.

As it turns out, there is also a greedy method available that solves the above problem exactly. In the interest of space, we defer the details to Appendix D.

4 Experiments

To validate this approach, we have conducted a series of experiments, using parametrized distributions for . Leveraging the methods described in the previous section, we can quickly compute the necessary equilibria. With suitable configuration, all experiments converge in less than 50 rounds and run in a few minutes on an Intel Core i5. In all of the experiments that follow we have used a discretization of 50 bins and 200-fold sub-sampling when evaluating integrals over the bins. In all cases, we evaluated over a range . Consequently all distributions were truncated such that their support did not exceed this range.

4.1 Ex-Ante, Pareto

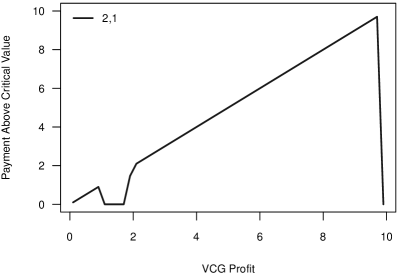

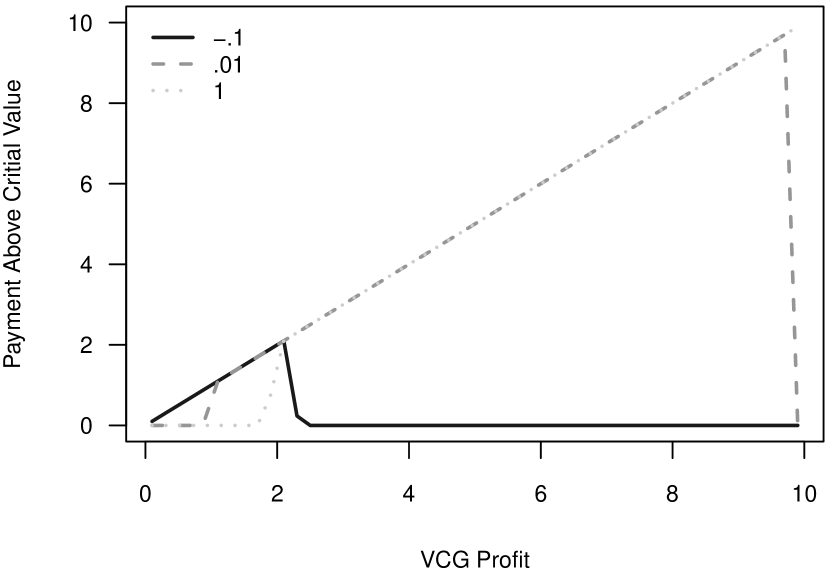

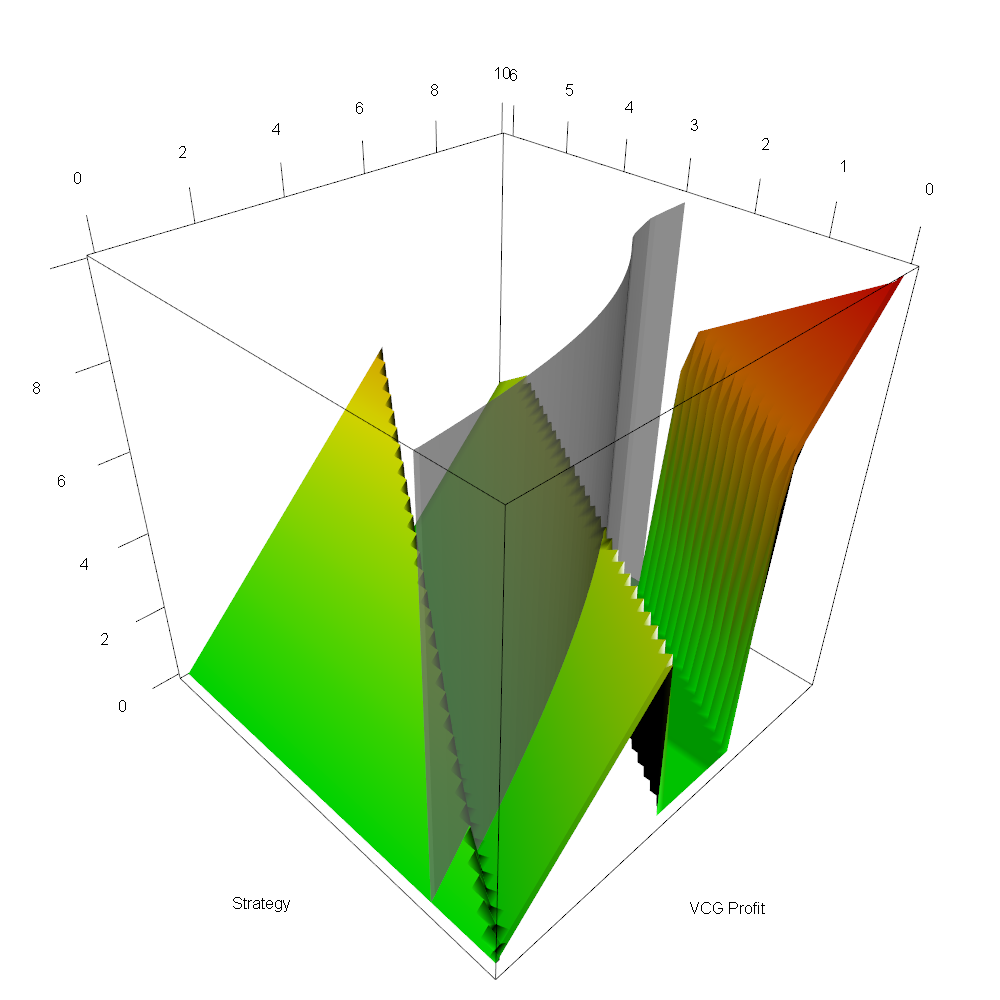

For the first experiment we used the basic ex-ante formulation from section 2.3.1. We equipped it with a Generalized Pareto Distribution for with position , and scale . We then varied the shape parameter in . We find that the optimal strategy for the bidder under all three settings is to shade by . The rules produced under this setting are shown in Figure 2. For a shape parameter of , the calculated rule charges only the bidders with small . Consequently, the rule selected in this case is the Large rule, which gives all the available surplus to bidders with large potential VCG profit. By contrast, when the scale parameter is , a heavy-tailed distribution, the obtained rule asks only those bidders with the largest to pay. Accordingly, this parametrization selects the Small rule, which gives all the available surplus to bidders with the smallest VCG potential profits. In previous work (Lubin and Parkes 2009), it was found that the GPD well-matched empirical data, and that the Small rule was observed to perform exceedingly well in restricted BNE. From these figures, we can see why. If the GPD distribution has a positive shape parameter, then the optimal rule, under our model, is likewise Small.

4.2 Ex-Ante, Pareto For Different Budgets

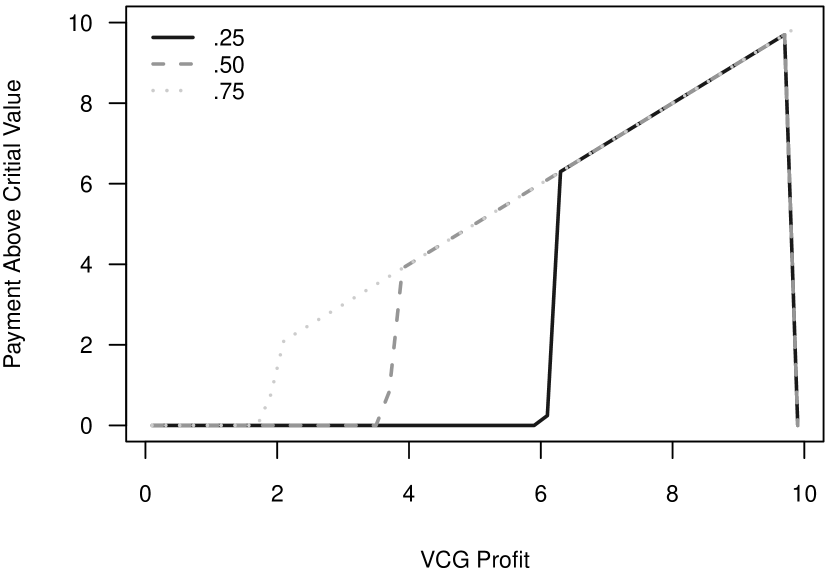

The budget balance constraint described in section 2.3.1 enforces that the rule cannot dole out more surplus than is available in the domain, . VCG violates this and gives out enough surplus to achieve full strategyproofness, an amount we can quantify as: . Because of this it is convenient to consider reparametrizing in terms of this quantity and focus on the constant . represents the fraction of the total VCG surplus that must not be given away if we are to achieve budget balance. All things equal, the larger , the more the agents are going to have to pay. This can clearly be seen in Figure 2, which shows the bidder payments above the critical value where . Further, the more surplus there is to hand out, the better the rule can do in minimizing the incentives to deviate, and thus the optimal strategy falls from shaving by when to when . Addtional results based on the ex-ante formulation, are provided in Appendix E.

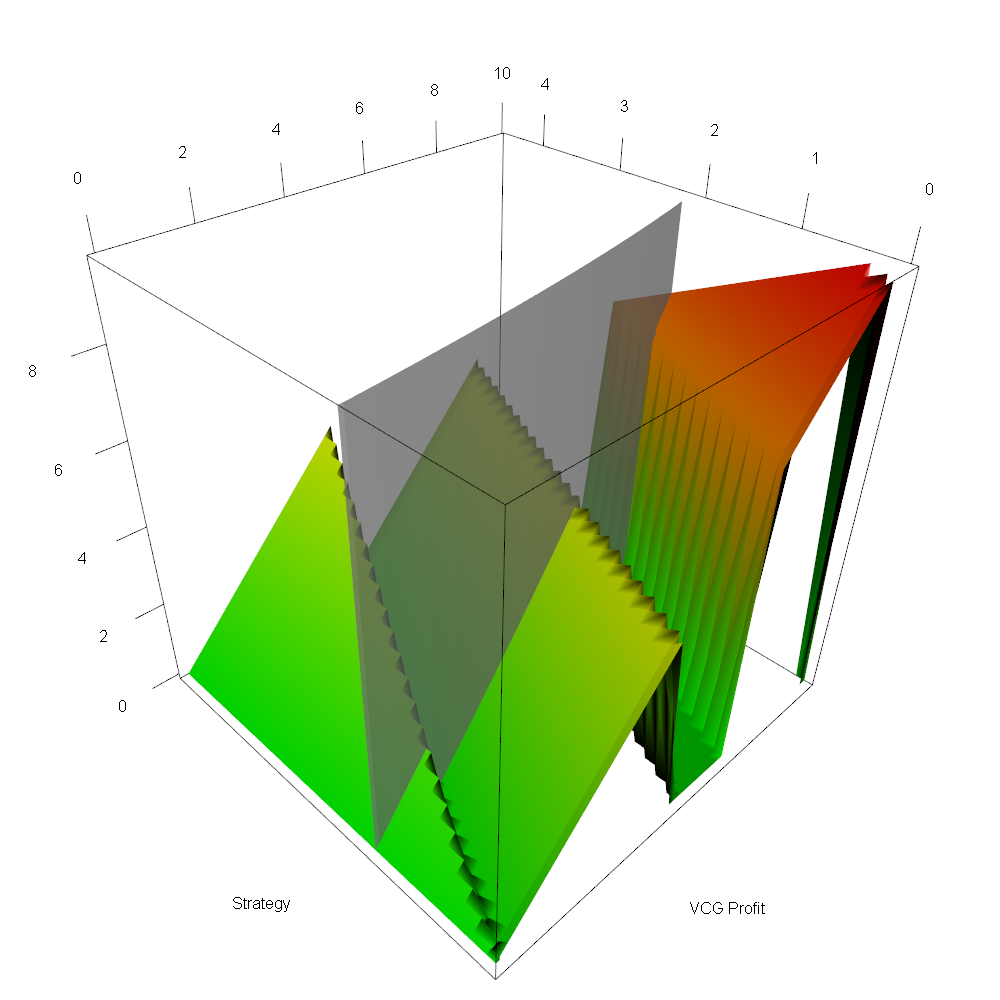

4.3 Blinded-Regret and Functional Strategy, Pareto

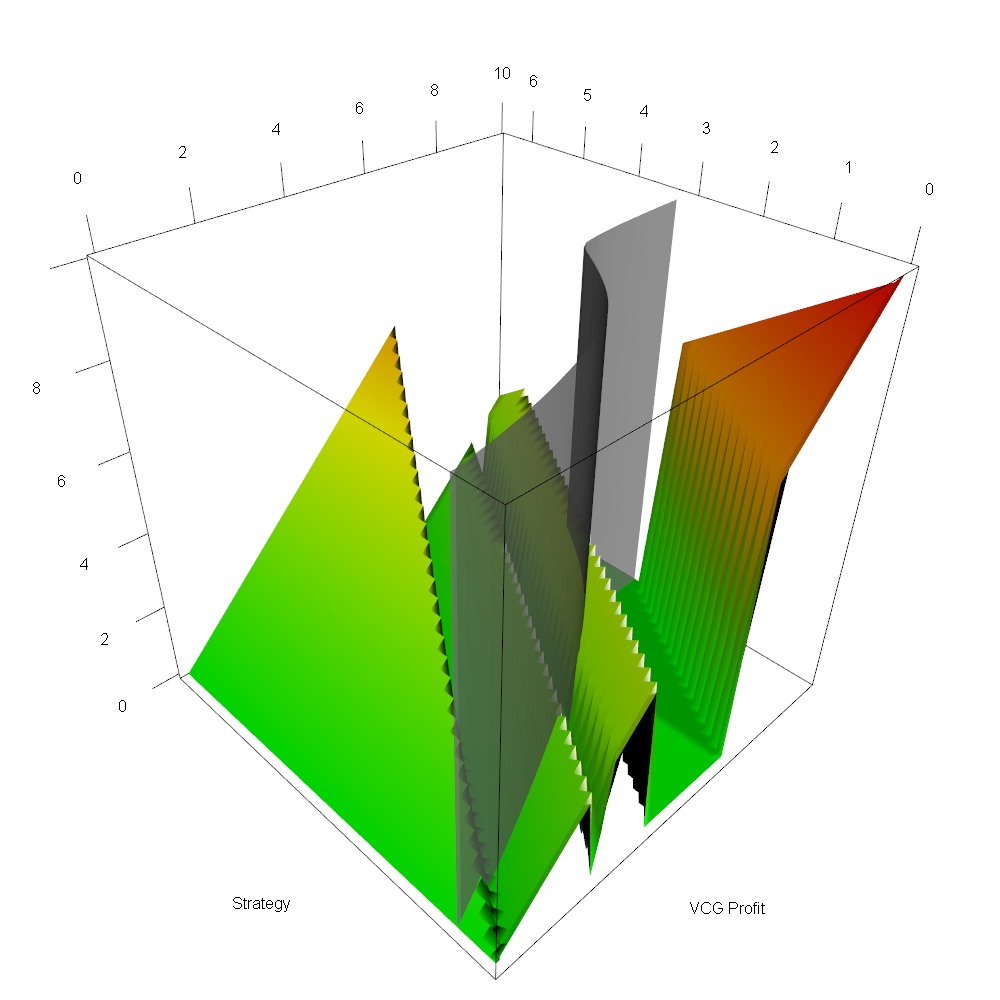

Finally, we turn our attention to our more complex formalism described in sections 2.2.4 and 2.3.2. Figure 3 illustrates an example from this setup with GPD(0,1,1) and drawn from four different Normal Distributions. These 3-D plots show the payment above the critical value that a bidder faces both as a function of , or potential profit (right axis), and as a function of potential shade he might make at that value (left axis). The figures make clear that the 1-D payment function offsets back and to the right, as the agent increases his shade.

We hasten to note that the pyramid region on the left is not technically part of the payment rule itself. Rather, in that region, the bidder has shaded more than his VCG potential profit, and has thus issued a bid below the critical value. Consequently, he is now losing, and incurring a regret equal to his full potential profit. The region rises as it goes to the right and back, since bidders with higher values have potentially more to lose.

Cutting through each of the figures, you can see a vertical surface. This is a rendering of the optimal strategy taken by the bidder (under the information set he has available), when confonted with this rule. One can see that the amount of shaving generally increases with the VCG potential profit that an agent has, but that the surface is not at 45 degrees, since the bidder only has partial information about his value of , as enforced by the blinding distribution, . Interestingly, in the Figures 3(a) and 3(b), we can see the optimal strategy “hook” around the mass of additional payment at the far right of the plot. For with large standard deviations, such as in Figures 3(c) and 3(d), the bidder doesn’t have enough information about his setting to be able to do this. Moreover, Figure 3(d) is included to illustrate that as the approaches the Uniform Distribution, the agent has effectively only ex-ante information, and thus chooses a constant shade (illustrating how the blinded regret formalism generalizes the ex ante approach.

The small dip that can be seen in the rule obtained in figure 3(a) is not an artifact, but a feature of the equilibrium of high-information set games (e.g. those with distributions with low standard deviation). The more information the bidder has, the more effective he is at contorting his bid, and the more complex the center’s chosen payment rule must be in order to attempt to thwart this strategizing. This illustrates that approximate incentive schemes under even simplified Bayesian conditions can still be highly complex for even moderately-informed bidders. This complexity stems from bidders understanding their strategic environment for exploitation. This has implications for market design in general: we want bidders to be able to easily calculate their valuation function, and to be able to bid based on it – otherwise efficiency suffers. But, we do not want bidders to know their VCG potential profit , because knowledge of this informs them of their critical point, which in turn enables them to strategize. Concretely, this means agents must be kept in the dark about the values of their competitors, which may be hard in small markets where agents can reason directly about individual competitors.

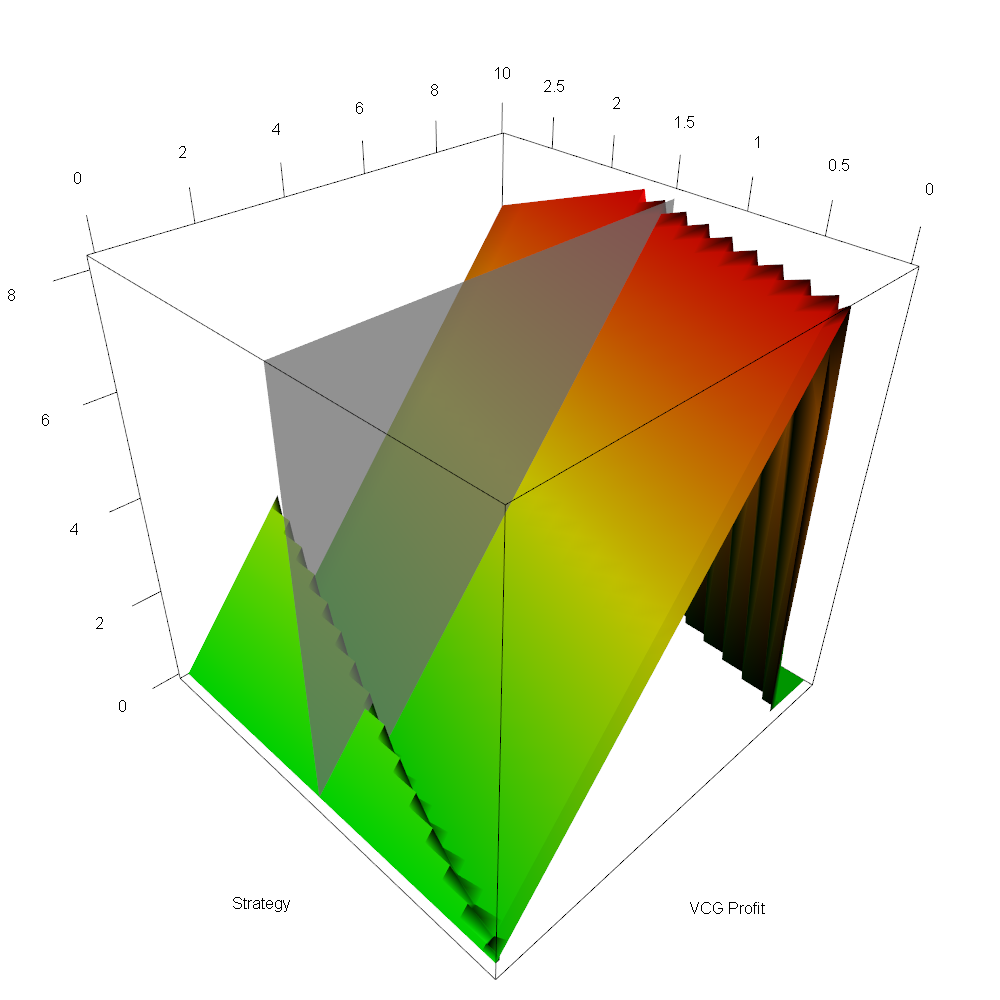

Figure 4 shows the same example as Figure 3(b), but where the payments have been scaled by the distribution. Although slightly more difficult to read than Figure 3, this approach lets you see precisely the topology that drives the decisions made by both the bidder and the center. The figure illustrates the fundamental tradeoff faced by the optimizers for a falling distribution like GPD: small values of occur frequently, so even though they are small they are important. Large values of occur rarely, but their sheer size can make them important too. Ultimately, both sides of the game must pay attention to the full range in equilibrium.

5 Discussion

Although there are numerous domains where combinatorial exchanges could provide tangible economic benefits, including spectrum reallocation and computational resource allocation, a significant obstacle has prevented them from being used in practice: a reasonable payment rule with good incentive properties.

In this work, we have presented the first comprehensive method for constructing such a rule. To do so, we have employed a construction that reduces the complexity of the payment rule design problem to a single dimension, by appealing to the same principles that enable the VCG mechanism to be strategyproof. In particular, the rule is defined as a single dimensional function, whose argument is the amount in excess of the critical value the participant has bid, and whose result is the amount in excess of the critical value that he is then asked to pay. This amount is always exactly zero for VCG, but for our rules it is a positive number for at least some bidders such that in total the budget balance constraint can be met, while simultaneously attaining our definition of approximate incentive compatibility. In this sense, it reduces to a payment rule that directly reasons about the profit that agents obtain for their allocated bundle, without worrying about the combinatorial complexities that lead to that bundle being chosen

In conjunction with this, we have also constructed a corresponding model for bidder behavior, again reduced to the single dimension of bidder profit. With this reduction, we are in a position to offer a novel definition of approximate incentive compatibility, where we consider the increased profit an agent might attain by optimally misreporting based on a distribution of the available potential VCG profit in the domain, when the other agents are playing their Bayes-Nash equilibrium strategies. Rather than assuming agents have direct access to this distribution, which would result in an ex-post information set, we instead introduce a “blinding” distribution, which represents an agent’s bounded knowledge about its potential profitability in the domain. By compounding the blinding distribution with the potential VCG profit distribution, we obtain our model of agents’ fuzzy knowledge of their domain. This model has the advantage of the tractability of a single-dimensional ex-post analysis, while retaining much of the economic structure of a far more desirable ex-interim model.

By combining this model for the center and for the agents together, we can construct the full mechanism. This mechanism operates exactly like VCG, except that it calculates different prices. These prices are based on particular distributional information about how agents bid in equilibrium, and about a given agent’s true value relative to its critical value (i.e. its true VCG discount). A critical contribution of this framing of the pricing problem is that we cast the problem as a meta-game between the center and the agents playing the game. We argue that this structure is a general property of problems in mechanism design: the mechanism and the participants are at odds with each other, each trying to box in the other in order to attain its own goals.

To obtain concrete rules in our paradigm in the general case, it is necessary to go beyond closed-form solutions and employ numerical methods to solve for the equilibrium of the meta-game. Such solutions simultaneously offer approximately IC payment rules under our new blinded regret information set, and the optimal agent strategies when agents face these rules. We offered such a numerical method, adapted from the traditional damped interated best-response algorithm for solving BNEs. We then tested the approach on several distribution classes and a wide range of parametrizations, including those that have previously been shown to be a good fit with real data. Using these distributions we were able to generate the Large and Small rules computationally, in precisely the settings where they have been shown effective in practice. Moreover, going beyond these settings, our method produces a wide variety of novel, yet easily implementable, payment rules.

References

- Aissi et al. [2009] Hassene Aissi, Cristina Bazgan, and Daniel Vanderpooten. Min–max and min–max regret versions of combinatorial optimization problems: A survey. European J. of Operational Research, 197(2):427–438, 2009.

- Ausubel and Milgrom [2006] Lawrence M. Ausubel and Paul Milgrom. The lovely but lonely vickrey auction. In Peter Cramton, Yoav Shoham, and Richard Steinberg, editors, Combinatorial auctions. MIT Press, Cambridge, MA, 2006.

- Azevedo and Budish [2012] Eduardo Azevedo and Eric Budish. Strategyproofness in the large. Technical report, Harvard University, 2012.

- Ball et al. [2006] Michael Ball, George Donohue, and Karla Hoffman. Auctions for the safe, efficient, and equitable allocation of airspace system resources. In Peter Cramton, Yoav Shoham, and Richard Steinberg, editors, Combinatorial auctions. MIT Press, Cambridge, MA, 2006.

- Basar and Olsder [1995] Tamer Basar and Geert J. Olsder. Dynamic noncooperative game theory. SIAM, 200, 1995.

- Brent [2013] Richard P Brent. Algorithms for minimization without derivatives. Dover, New York, 2013.

- Brown [1951] George W Brown. Iterative solution of games by fictitious play. Activity analysis of prod. and alloc., 13(1):374–376, 1951.

- Burr [1942] Irving W. Burr. Cumulative frequency functions. The Ann. of Mathematical Stats., 13(2):215–232, 1942.

- Champernowne [1952] David G. Champernowne. The graduation of income distributions. Econometrica, 2(4):591–615, 1952.

- Coles et al. [2001] Stuart Coles, Joanna Bawa, Lesley Trenner, and Pat Dorazio. An introduction to statistical modeling of extreme values, volume 208. Springer, London, 2001.

- Conitzer and Sandholm [2004] Vincent Conitzer and Tuomas Sandholm. Self-interested automated mechanism design and implications for optimal combinatorial auctions. In Proc. of the 5th ACM Conf. on Elec. commerce, pages 132–141, 2004.

- Cournot and Fisher [1897] Antoine Augustin Cournot and Irving Fisher. Researches into the Mathematical Principles of the Theory of Wealth. Macmillan, New York, 1897.

- Cramton [2013] Peter Cramton. Spectrum auction design. Review of Industrial Organization, 42(2):030–190, March 2013.

- Day and Milgrom [2008] Robert Day and Paul Milgrom. Core-selecting Package Auctions. Int. J. of Game Theory, 36(3):393–407, 2008.

- Edelman et al. [2007] Benjamin Edelman, Michael Ostrovsky, and Michael Schwarz. Internet Advertising and the Generalized Second Price Auction: Selling Billions of Dollars Worth of Keywords. American Economic Review, 97(1):242–259, 2007.

- Erdil and Klemperer [2010] Aytek Erdil and Paul Klemperer. A new payment rule for core-selecting package auctions. J. of the European Economic Association, 8(2-3):537–547, 2010.

- FCC [2014] FCC. FCC adopts rules for first ever incentive auction. Technical Report May 15, 2014, FCC, 445 12th Street, S.W. / Washington, D.C., May 2014. URL http://www.fcc.gov/document/fcc-adopts-rules-first-ever-incentive-auction.

- Guevara et al. [2014] Marisabel Guevara, Benjamin Lubin, and Benjamin C. Lee. Market mechanisms for managing datacenters with heterogeneous microarchitectures. ACM Transactions on Computer Systems (TOCS), 32(1):3, 2014.

- Kwerel and Williams [2002] Evan Robert Kwerel and John Williams. A proposal for a rapid transition to market allocation of spectrum. Technical Report 38, FCC, 445 12th Street, SW / Washington, D.C. 20554, November 2002.

- Lubin [2010] Benjamin Lubin. Combinatorial markets in theory and practice: Mitigating incentives and facilitating elicitation. PhD thesis, Harvard University, 2010.

- Lubin and Parkes [2009] Benjamin Lubin and David C. Parkes. Quantifying the strategyproofness of mechanisms via metrics on payoff distributions. In Proc. of the 25th Conf. on Uncert. in Art. Int., pages 349–358, 2009.

- Lubin and Parkes [2012] Benjamin Lubin and David C. Parkes. Approximate strategyproofness. Current Science, 103:1021–1032, 2012.

- Lubin et al. [2008] Benjamin Lubin, Adam I. Juda, Ruggiero Cavallo, Sébastien Lahaie, Jeffrey Shneidman, and David C. Parkes. ICE: an expressive iterative combinatorial exchange. J. of Art. Int. Research (JAIR), 33:33–77, 2008.

- Myerson [1979] Roger B. Myerson. Incentive compatibility and the bargaining problem. Econometrica, 47(1):61–73, 1979.

- Myerson and Satterthwaite [1983] Roger B. Myerson and Mark A. Satterthwaite. Efficient mechanisms for bilateral trading. J. of economic theory, 29(2):265–281, 1983.

- Nisan [2007] Noam Nisan. Algorithmic game theory. Cambridge University Press, New York, 2007.

- Nisan et al. [2011] Noam Nisan, Michael Schapira, Gregory Valiant, and Aviv Zohar. Best-response auctions. In Proc. of the 12th ACM Conf. on Elec. Comm., pages 351–360, 2011.

- Parkes et al. [2001] David C. Parkes, Jayant Kalagnanam, and Marta Eso. Achieving Budget-Balance with Vickrey-Based Payment Schemes in Exchanges. In Proc. of the 17th Int. Joint Conf. on Art. Int., pages 1161–1168, CA, 2001.

- Pickands III [1975] James Pickands III. Statistical inference using extreme order statistics. The Ann. of Stats., 3(1):119–131, 1975.

- Reeves and Wellman [2004] Daniel M. Reeves and Michael P. Wellman. Computing best-response strategies in infinite games of incomplete information. In Proc. of the 20th Conf. on Uncert. in Art. Int., pages 470–478, 2004.

- Roberts and Postlewaite [1976] Donald J. Roberts and Andrew Postlewaite. The incentives for price-taking behavior in large exchange economies. Econometrica, 44:115–127, 1976.

- Robinson [1951] Julia Robinson. An iterative method of solving a game. The Ann. of Mathematics, 54(2):296–301, 1951.

- Sandholm [2007] Tuomas Sandholm. Expressive commerce and its application to sourcing: How we conducted $35 billion of generalized combinatorial auctions. AI Magazine, 28(3):45, 2007.

- Shapley and Scarf [1974] Lloyd Shapley and Herbert Scarf. On cores and indivisibility. J. of mathematical econ., 1(1):23–37, 1974.

- Shapley et al. [1964] Lloyd S. Shapley et al. Some topics in two-person games. Advances in game theory, 52:1–29, 1964.

- Simaan and Cruz Jr. [1973] Marwaan Simaan and Jose B. Cruz Jr. On the stackelberg strategy in nonzero-sum games. J. of Optimization Theory and Applications, 11(5):533–555, 1973.

- Smith [1998] Donald R. Smith. Variational methods in optimization. Dover, New York, 1998.

- Vickrey [1961] William Vickrey. Counterspeculation, auctions, and competitive sealed tenders. The J. of Finance, 16(1):8–37, 1961.

- Vorobeychik and Wellman [2008] Yevgeniy Vorobeychik and Michael P. Wellman. Stochastic search methods for nash equilibrium approximation in simulation-based games. In Proc. of the 7th Int. Joint Conf. on AAMAS, pages 1055–1062, 2008.

- Vorobeychik et al. [2006] Yevgeniy Vorobeychik, Christopher Kiekintveld, and Michael P. Wellman. Empirical mechanism design: Methods, with application to a supply-chain scenario. In Proc. of the 7th ACM Conf. on Elec. Comm., pages 306–315, 2006.

- Vorobeychik et al. [2007] Yevgeniy Vorobeychik, Daniel M. Reeves, and Michael P. Wellman. Constrained automated mechanism design for infinite games of incomplete information. In Proc. of the 23rd Conf. on Uncert. in Art. Int., pages 400–407, 2007.

- Wan [1995] Frederic Y. M. Wan. Introduction to the Calculus of Variations and its Applications. CRC Press, New York, 1995.

Appendices

Appendix A Existing formulations of approximate incentive compatibility

The most widely used approximate incentive compatibility concept is the Worst Case Ex-Post Regret:

This measures across all possible agent values and reports the most that an agent might gain by misreporting, given what he knows after the mechanism is complete. In other words, it is the “Full Information” setting, and thus reduces our BNE to a regular Nash equilibrium. Importantly, though, it will not minimize efficiency loss. Efficiency is a global criterion, seeking to match total value (or equivalently expected value per participant) of the reported and true allocations. WCRegret, by contrast seeks to minimize the worst case difference in reported versus true allocative value for individual participants, . A given mechanism may exhibit a large such loss on certain participants in order to reduce the overall loss in aggregate, thereby improving efficiency. Yet, the measure has the virtue of being both understandable and easy to calculate. The definition works well when it can be expected to be small in magnitude, hence its other name (strategyproofness – Roberts and Postlewaite, 1976). The current state-of-the-art rule, Threshold [Parkes et al., 2001], minimizes this value, e.g. . However, when, as in the case of CEs, we expect the ex-post regret to be large, the measure is overly conservative: it tells us solely about a very rare and very massive worst case – preventing us from targeting the typical cases for design. High efficiency can require accepting significant value loss to a tiny minority of individual participants, who incur exceedingly poor WCRegret.

Consequently, we might instead an expectation over participant values instead, yielding expected ex-post regret:

Beause it is still a full information analysis, this retains appealing computational properties. However, it consequently also retains an unrealistic information set, requiring us to assume that participants have full information about each other which is unrealistic in most settings.

To improve the information assumptions, we instead may wish to consider Ex-Ante Deviation Incentive (ADI):

In this formulation agents have only probabilistic information about the value profile over all agents, including their own values. Thus the information set is problematic for the opposite reason from an ex-post analysis: we are now assuming agents know too little, rather than too much. But, because the expection over value of the other agents is taken relative to their true values, not relative to their reports, formulating the distribution does not require repeatedly solving for the BNE outcome. Consequently, ADI is relatively computationally tractable, even though it typically will require solving a winner determination problem within the stochastic optimization. We therefore consider a pricing model based on this model, when adapted to our methodology, in section 2.3.1.

What we really want, though, is an information set, where agents know their own values exactly but the values of the other agents only in expectation. This yields the Ex-Interim Deviation Incentive (IDI):

This represents a tremendous improvement in fidelity: if the expectation over the values of others in the first term is instead taken relative to BNE reports, then this would measure the value of the expected best-response and directly calculates our gold-standard measure, trending to as efficiency goes to .666 Despite this, typically the distribution is still taken relative to the truthful reports, to match the definition of ex-ante, while adding only to the information set participants’ knowledge of their own value. Regardless of which distribution is considered, though, IDI is typically computationally even more challenging than ex-ante since the maximization is now embeded within a larger expectation.

Appendix B Proof of observations

Observation 1.

(1) Follows directly from the definition of the critical value, namely that when , then by definition and the marginal economy without has greater value than the main economy and will be chosen over . (2) Is immediate. ∎

Observation 1.

Follows from the definitions of , and and from VCG being strategyproof. ∎

Observation 3.

Is equivalent to the foundational property of VCG that for reports above (truthful or otherwise) ’s profit under VCG is his marginal impact on the economy, a constant independent of the reported value , ∎

Appendix C Full computational mechanism design problem

Without the simplifications we employ in this papaer, the full Automated Mechanism Design [Conitzer and Sandholm, 2004] approach to the pricing problem, would be to solve:

| (8) | ||||

| s.t. | IR, Weak BB |

where is any of the deviation incentive measures from appendix A, or the new one definind in equation 2. Unfortunately though, the variable in this program is a vector-valued (one entry per bidder) payment function and the objective functional is a stochastic optimization containing embedded winner determination problems. Thus, the program is intractable for all but the most trivial of instances.777See [Lubin, 2010] for a simple example solved in a discretization of this formulation. Consequently, we seek to gain traction by a suitable simplification that will enable reasonable computation.

Appendix D Ratio method for solving the center problem

Here we present an alternative way to solve the problem shown in Section 3.4.

Consider the following change of variables in the original continuous BB constraint from (4): :

| (9) |

Now consider a starting choice for the function . We then wish to modify into for some that will optimally progress towards satisfying the BB constraint while simultaneously doing the least damage to the objective function. To do so, we should choose

| (10) |

because it is this ratio that determines where progress is best made trading off adding to the constraint and to the objective.

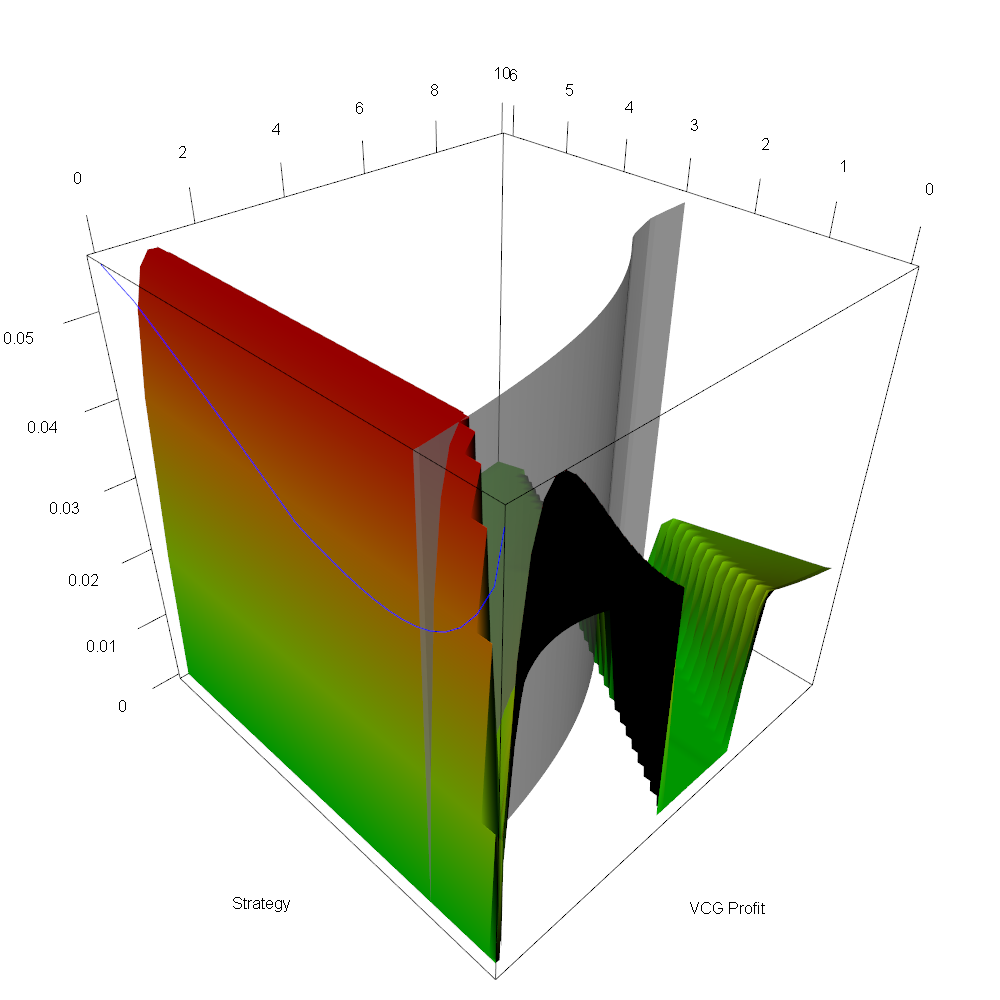

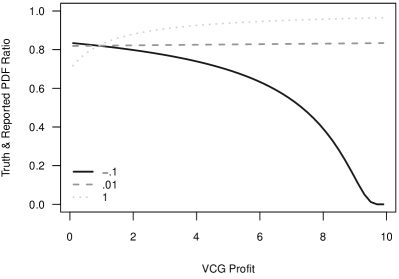

This insight offers an alternative method to solve for , provided in algorithm 1. We can also plot this ratio to gain insight into what is driving particular rule choices, as in Figure 5. Here we see a plot of the ratios, one line for each of the distributions being considered. The plot shows a very different shape for each of the parametrizations. For , a finite distribution, the ratio slopes downwards and consequently the corresponding rule shown in Figure 2 asks for payments from only the bidders with small . The rule selected in this case is the Large rule, which gives all the available surplus to bidders with large VCG potential profits. As we described in section 2.2.3, all possible rules consistent with the boundary and budget constraints are valid for the Exponential Distribution under the basic ex-ante formulation. By picking a shape parameter just larger then zero we can see the limiting case of the GPD as it approaches the exponential distribution. In this case the ratio is nearly flat (it would be perfectly flat for the Exponential Distribution). When the scale parameter is , a heavy-tailed distribution, the ratio is rising. This leads to a rule that asks only those bidders with the largest to pay. Accordingly, this parametrization selects the Small rule, which gives all the available surplus to bidders with the smallest VCG potential profits.

Appendix E Burr XII. a further Ex-Ante result

We have also run a series of experiments using a generalization of the Pareto Distribution, known as the Burr XII Distribution, which has two shape-parameters. When the first parameter is , the Burr XII Distribution is the same as a Pareto Distribution. When the second parameter is , we have a Log-Logistic Distribution [Burr, 1942]. Figure 6 shows the function obtained from a parametrization of , which produces a peaked distribution in the family of Log-Logistic functions. Here we see that the bidders near the peak receive their full VCG potential profit and obtain all the surplus. The bidders with either small or large VCG potential profits are given no discount at all. Essentially, this rule will give all of its surplus to a subset of values in the middle. This example shows how dependent the outcome of the optimal payment rule is on the shape of the distribution. Nonetheless, the optimal strategy has not changed, and remains a shade of .