Principal Component Analysis for Semimartingales and Stochastic PDE

Abstract.

In this work, we develop a novel principal component analysis (PCA) for semimartingales by introducing a suitable spectral analysis for the quadratic variation operator. Motivated by high-dimensional complex systems typically found in interest rate markets, we investigate correlation in high-dimensional high-frequency data generated by continuous semimartingales. In contrast to the traditional PCA methodology, the directions of large variations are not deterministic, but rather they are bounded variation adapted processes which maximize quadratic variation almost surely. This allows us to reduce dimensionality from high-dimensional semimartingale systems in terms of quadratic covariation rather than the usual covariance concept.

The proposed methodology allows us to investigate space-time data driven by multi-dimensional latent semimartingale state processes. The theory is applied to discretely-observed stochastic PDEs which admit finite-dimensional realizations. In particular, we provide consistent estimators for finite-dimensional invariant manifolds for Heath-Jarrow-Morton models. More importantly, components of the invariant manifold associated to volatility and drift dynamics are consistently estimated and identified. The proposed methodology is illustrated with both simulated and real data sets.

Key words and phrases:

Principal component analysis, factor models, semimartingales1991 Mathematics Subject Classification:

Primary: ; Secondary:1. Introduction

Dimension reduction techniques have been intensively studied over the last years due to the advent of high-dimensional data in a variety of applied fields. Towards an effective reduction dimension, it is crucial to interpret correctly what kind of lower dimensional manifold one has to find in order to represent the data properly. For instance, if the second moment structure reasonable describes the dynamics in the data, then the classical Principal Component Analysis (henceforth abbreviated by PCA) and its various extensions are the natural candidates to reduce dimensionality.

There are many cases where correlation in high-dimensional systems may not be accurately described by covariance structures. An important example is the correlation typically found in high-frequency data which is better described by the so-called quadratic variation matrix

where is a -dimensional semimartingale sampled over the time horizon and is the quadratic covariation process between and .

In a financial context, the process is called the volatility matrix (sometimes called integrated volatility). The total amount of volatility in a -dimensional semimartingale system over is fully described by the following quantity

where are the random eigenvalues of and is the usual Hilbert-Schmidt norm. Volatility is by far the most important quantity which needs to be estimated for asset pricing, asset allocation and risk management, specially in high-dimensional portfolios. The estimation of high-dimensional quadratic variation matrices has been a topic of great interest in the last years. We refer the reader to the works [10, 50, 51, 39, 52, 18, 23, 21] and other references therein.

Despite all the recent progress on volatility matrix estimation, there has been remarkably little fundamental theoretical study on dimension reduction techniques based on high-dimensional quadratic variation matrices. One notorious difficulty is the dynamic interpretation of directions and principal components over the time horizon which in typical cases is formulated in a high-frequency domain. Indeed, is fully random which makes the analysis more evolved than the standard PCA. More precisely, all the potentially optimal projections will be stochastic processes rather than deterministic vectors.

In view of the fact many correlation structures in high-dimensional data are fully represented by the quadratic variation concept, it is natural and necessary to construct a dimension reduction methodology strictly associated to rather than on classical covariance or conditional distributions. This is the program we start to carry out in this paper.

1.1. Contributions

Let be a -dimensional semimartingale. The starting point of the analysis is to solve an identification problem related to a possible singularity of the random matrix which can be typically found e.g in large portfolios of financial assets (see e.g Burashi, Porchia and Trojani [16], Ait-Sahalia and Xiu [4] and Fan, Li and Yu [23] and other references therein) and affine term structure models (see e.g Bjork and Landén [15] and Filipovic [29] and Filipovic and Sharef [27]). More precisely, in the presence of non-trivial correlation among semimartingales, one has and then, under mild assumptions, one can split the set into two complementary linear spaces such that

where and contains only elements of with non-zero and zero quadratic variation, respectively. The space fully describes the volatility structure of while is responsible for its hidden pure drift (null quadratic variation) dynamics. At this point, we stress that the potential singularity of the quadratic variation matrix introduces non-observable drift components into which cannot be discarded in a high-frequency situation. Both spaces are equally important to explain the dynamics of in a given physical probability measure. In strong contrast, directions with null variance can be fully discarded in the classical PCA. This is the first major difference between the classical PCA and the theory developed in this article.

We follow the natural and simple idea to seek random variables such that

has the largest possible instantaneous quadratic variation over , where is interpreted as a random coefficient at time rather than a process. By iterating this procedure in an orthogonal way, we shall get a linear transformation of which under some mild primitive conditions will be a finite-dimensional semimartingale ranked in terms of quadratic variation. Starting with consistent estimators for the quadratic variation matrix (see e.g [19, 50, 51, 39, 52, 18, 23, 21] and other references therein), we are able to propose consistent estimators for by means of a simple eigenvalue analysis of based on high-frequency observations of . This allows us to reduce dimensionality in terms of quadratic variation in a very clear and consistent way. Equally important, the methodology also estimates bounded variation components in which can not be neglected in multi-dimensional semimartingale systems.

The PCA for semimartingales introduced in the first part of the article is applied to the estimation of principal components of discretely-observed space-time semimartingales which describe stochastic partial differential equations (henceforth abbreviated by stochastic PDEs) admitting finite-dimensional realizations. In particular, in the second part of this article, we illustrate the theory by studying the problem of the estimation of the so-called finite-dimensional invariant manifolds w.r.t to a stochastic PDE

| (1.1) |

where is a potentially infinite-dimensional Sobolev-type space of continuous functions and satisfy standard assumptions for the existence of solution.

Many space-time phenomena in natural and social sciences can be described by solutions of stochastic PDEs like (1.1). However, the intrinsic infinite-dimensionality of space-time data generated by models like (1.1) creates a big challenge in the statistical analysis of these models. In particular cases, it is well-known that one can reduce dimensionality and still get a very rich class of space-time data generated by models of type (1.1). For instance, under Lie algebra conditions (see Filipovic and Teichmann [25] and Bjork and Svensson [14]) on the coefficients of (1.1), it is well known that there exists a family of affine manifolds of curves and a -dimensional semimartingale factor process such that

| (1.2) |

where is a finite-dimensional parameterized family of smooth curves. We shall write it as where is a -dimensional vector space generated by smooth curves and is an -valued smooth parametrization which we assume to be a zero quadratic variation function.

Two central unsolved problems in the stochastic PDE modelling are: (i) the construction of statistical tests to check existence of and (ii) the development of related estimation methods. The importance of this research agenda can be mainly understood in applications to interest rate modelling and other term-structure problems in Mathematical Finance. The literature is vast so we refer the reader to e.g [13, 14, 15, 24, 25, 28, 29, 26, 44, 49, 34, 41, 7, 46, 40] and other references therein. In short, under the assumption of existence of , the estimation of is essential for a consistent calibration of potentially infinite-dimensional term-structure models.

Under the assumption that the stochastic PDE (1.1) admits an affine finite-dimensional representation (1.2), we apply the semimartingale PCA to estimate and identify components of invariant manifolds which depicts volatility and drift dynamics in space. More precisely, let us consider the finite rank random linear operator defined by

where , is the inner product of and we set . We notice the quadratic variation of the stochastic PDE (1.1) is fully generated by . In particular, the associated Hilbert-Schmidt norm

fully describes the total amount of energy related to the quadratic variation of (1.1) over . Here, are the eigenvalues of arranged in decreasing order.

In general, , but in typical situations we do have 111The empirical literature on interest rate modelling reports strong evidence of correlation among risk factors (see e.g [3, 43, 17]) which suggest that one can typically find in case of affine models. From theoretical side, this phenomena is also related to no-arbitrage restrictions imposed on affine models. See e.g [14, 26, 27, 1, 2] and other references therein.. Let be the complementary subspace of in . Under mild assumptions, we have the following splitting

In one hand, the pair of subspaces should be considered as the analogous spaces to but in the spatial variable. On the other hand, we stress that is not observed and (1.2) is treated as a factor model

| (1.3) |

with dimension . The present methodology allows us to estimate and identify directions of the invariant manifold which come from the volatility (represented by ) and the drift (represented by ). More importantly, we are able to identify them separately which allows us to estimate null and non-null quadratic variation factors by projecting space-time data of the form (1.3) onto a pair of estimated vector spaces . We consider this separation feature as the most important aspect of the second part of this article. As a by-product, our methodology brings two contributions to the field: It provides a consistent volatility dimension reduction and a method to estimate hidden pure drift components in space-time semimartingale data generating processes.

Our methodology is a combination of classical factor models jointly with suitable random transformations over the space of latent semimartingales. More precisely, our approach consists essentially in two steps: Firstly, we apply an empirical covariance operator onto the space-time data to obtain a factor decomposition of the form

in the spirit of discrete-type factor models (see e.g Stock and Watson [47], Bai [9] and Bai and Ng [8]), but in a high-frequency setup as opposed to the usual panel data. In other words, is a refining partition of a two-dimensional set . In linear structures, the covariance operator only neglects components of null empirical variance so that, under suitable conditions, our first step does not loose information from the invariant manifold . The second step consists in using the semimartingale PCA jointly with suitable random rotations of latent factor estimators to infer the underlying semimartingale structure of the data. It is not easy to foresee that this two-step procedure would work. Indeed, to the best of our knowledge it is not known that the covariance operator decomposition is strong enough to provide a resulting process which is amenable to a consistent quadratic variation analysis. In fact, the sequence is not even associated to a semimartingale, so that the quadratic variation analysis based on this two-step procedure must be considered in a broader sense. The proof that this strategy works is the content of the second part of the paper.

It is important to stress the both steps in our methodology are equally important. For instance, the naive application of classical factor models to infer quadratic variation is non-sense when applied to semimartingale systems. Moreover, a more straightforward strategy based directly on an empirical quadratic variation does not work in full generality due to a possible singularity of the matrix. This last procedure forces the assumptions that which may not be optimal (in the mean-square sense) in typical situations when . This is the reason why the two-step procedure in this work is implemented. For instance, Pelger [42] studies principal components directly from the empirical quadratic covariation for factors with jumps and discrete loading factors. One crucial assumption in his setup is the non-singularity of the quadratic variation matrix which restricts the applicability in multivariate systems with non-trivial correlation typically found in large portfolios and interest rate models.

We should mention that another possible framework is introduced by Ait Sahalia and Xie [5] who interpret principal component analysis by means of the underlying volatility process. The main drawback of this strategy is the fact that rank of the volatility matrix may be strictly smaller than (as shown in Proposition 4.1), thus resulting in a substantial underestimation of and their associated factors. Therefore, similar to Pelger [42], the strategy introduced by [5] does not recover in full generality the whole semimartingale stricture () involved in the optimal decomposition due to a possible non-negligible dimension ( associated to the drift. In addition, the strong assumption of simple eigenvalues imposed in [5] rules out many finite-dimensional semimartingale systems typically found in applications.

1.2. Organization of the paper

The remainder of this article is structured as follows. Section 2 presents some notation and preliminary results. Section 3 presents the spectral analysis on a generic quadratic variation matrix. Section 4 illustrates the existence of bounded variation components in portfolio management and interest rate models. Section 5 presents the consistency results for the estimators of the dynamic spaces. Section 6 presents the application of semimartingale PCA to the problem of estimating finite-dimensional invariant manifolds for stochastic PDEs. Section 7 presents the numerical results and applications to real data. An Appendix is given in Section 8 which presents an estimator for .

2. Assumptions and Preliminary Results

At first, let us fix notation.

2.1. Notation

Throughout this article, we are going to work with a fixed stochastic basis of the form where is a probability space equipped with a sample space , a sigma-algebra , probability measure and a fixed terminal time . We equip the interval with the Borel sigma algebra and we assume the filtration satisfies the usual conditions.

All the algebraic setup in this article will be based on the real linear space constituted by the set of all -valued -measurable processes. In this article, the most important subclass of will be the subspace constituted by the set of all -valued continuous -semimartingales on . When , we set . We denote as the set of all -valued and -measurable random variables for and . Throughout this article, we adopt the following convention: If , then is interpreted as a column random vector in . Convergence in probability will be denoted by .

In the remainder of this article, denotes a deterministic partition and . The set denotes the space of all -real matrices and is the subspace of non-negative symmetric real matrices. The norm of linear operators between Hilbert spaces will be the standard Hilbert-Schmidt norm and denotes the transpose of a matrix . If are two linear subspaces of with , then we denote the usual projection of onto the quotient space . Throughout this article, we omit the variable when no confusion arises.

2.2. Analysis of quadratic variation matrices

In this work, the following bracket will play a key role in our analysis

| (2.1) |

in probability.

Definition 2.1.

The quadratic covariation exists for a given pair if the limit (2.1) exists for every sequence of partitions such that . We say that has null quadratic variation if

Of course, is a well-defined bounded variation adapted process for every . To shorten notation, we sometimes set for . For a given and , with a slight abuse of notation, we write to denote the following random matrix

| (2.2) |

whenever the right-hand side of (2.2) exists.

In the remainder of this section, is a given -dimensional measurable process. We say that is truly -dimensional if its components are linearly independent over the vector space . Throughout this paper, we are going to assume the following standing assumptions:

Assumption 2.1.

is a truly -dimensional measurable process.

Assumption 2.2.

The quadratic variation matrix exists and if there exists such that then we have .

Remark 2.1.

We clearly do not loose generality by imposing Assumption 2.1. Assumption 2.2 is very natural since our theory relies on the study of a realization of the quadratic variation matrix, and thus it is necessary that we do not get a realization of null quadratic variation from a non-null quadratic variation process.

Example: One typical example of semimartingale which satisfies Assumption 2.2 is given by the -Heston model with correlation in where denotes the th square-root-type stochastic volatility component for . Then, one can easily check that for every , we have

Hence, the classical Heston model satisfies Assumption 2.2.

Let be the linear space spanned by the -dimensional measurable processes over for . Assumption 2.1 yields for every . Let us now split into two orthogonal subspaces. At first, we set

| (2.3) |

Observe that is a well-defined linear subspace of for every . More importantly, the following remark holds.

Remark 2.2.

We recall that any continuous bounded variation local martingale must be constant a.s. Moreover, for every

where is the local martingale component of the special semimartingale decomposition of some . Therefore, Assumption 2.2 allows us to state that if is a truly -dimensional process, then is a subspace of only constituted by continuous bounded variation adapted processes over .

Definition 2.2.

Let be the span generated by a truly -dimensional measurable process over . If , then we say that has a null quadratic variation component over the interval . In particular, if and , then we say that has a bounded variation component over .

Let us give a toy example showing how a non-trivial dimension induced by bounded variation processes may appear in a very simple context.

Example: Let be a one-dimensional Brownian motion and let Of course, is a truly -dimensional semimartingale where for every . In particular, we clearly have for every .

For a deeper discussion of bounded variation components on semimartingale systems, we refer the reader to Section 4. Let us now provide a natural notion of “quadratic variation dimension” in . To do so, let us consider the following quotient space

| (2.4) |

By definition, can be identified by where the equivalence relation is given by

| (2.5) |

The following simple result connects the rank of with the dimension of .

Lemma 2.1.

Proof.

The result for is obvious so we fix . Let and let be the standard projection of onto . Now, we observe that for each , is a set of continuous measurable processes, each of which differs from each other by a continuous null quadratic variation measurable process over the interval . Nevertheless, for each process in its quadratic variation is equal to . Therefore, we may define its quadratic variation as . By the polarization identity, we may define

| (2.6) |

for any . In particular, this shows that is a well-defined random variable for any .

Since , then contains linearly independent components in the vector space . Therefore, equals to the number of linearly independent components in the subset .

Let us now consider a subset of equivalence classes , where is a function. Let . In the sequel, we denote by the null element of . With this notation at hand, Cauchy-Schwartz inequality yields

In particular,

By recalling that is linearly independent if, and only if,

then the statement is a linearly independent set is equivalent to the system of equations

has only the trivial solution almost surely. In other words,

Summing up the results of this section, we arrive at the following direct sum

| (2.8) |

where is the unique (up to isomorphisms) family of complementary linear subspaces of which realizes (2.8). One should notice that is formed by the null process in on and of elements in such that . Of course, is isomorphic to for every . To shorten notation, in the remainder of this article, we write , and .

3. Random directions and principal components

Let us start with some heuristics related to reduction dimension for a high-dimensional vector of semimartingales which we suspect there may be some redundancy in the sense of quadratic variation. Perhaps there may be some way to combine that captures much of the quadratic variation in a few aggregate semimartingales. In particular, we shall seek random variables such that

| (3.1) |

has the largest possible instantaneous quadratic variation over , where in (3.1) is interpreted as a random coefficient at time rather than a process. In other words, we seek a random linear combination of the form (3.1) such that

has almost surely the largest possible value over the subset of with Euclidean norm 1 for a given . Indeed, we do compute the quadratic variation of the linear combination at time by considering as a random constant over which yields

The random coefficient

encodes the way to combine to maximize instantaneous quadratic variation at time . The new variable - the leading principal component - is . We shall continue this strategy by seeking a possible lower dimensional pairwise orthogonal sequence of aggregate variables which might explain most of the quadratic variation at each time .

For simplicity of exposition, we assume that one observes all trajectories of a given truly -dimensional continuous time semimartingale satisfying Assumptions 2.1 and 2.2. Let us now interpret the eigenvalues and eigenvectors of the quadratic variation matrix in a similar manner of what we interpret in covariance matrices as in classical PCA. In the sequel, we introduce the brackets which encode quadratic variation of random linear combinations as described at the beginning of this section

| (3.2) |

The bracket is naturally defined by polarization. The bracket given in (3.2) encodes the quadratic variation of at time where is considered as a random constant over in the computation of (3.2). This is perfectly consistent to what happens in practice because at a given time , one observes a high-frequency data from a semimartingale over and one has to decide if there exist linear combinations of the elements of which summarizes the quadratic variation .

Lemma 3.1.

Let be a truly -dimensional semimartingale satisfying Assumption 2.2. Let us consider the vector of eigenvalues (ordered in such way that ) of the matrix for each . Then, for each , is an adapted bounded variation process.

Proof.

By the very definition, any eigenvalue is a root of the characteristic polynomial of the random matrix . The degree of this polynomial is and its coefficients depend on the entries of , except that its term of degree is always . This allows us to conclude that the ordered eigenvalues are -adapted. In particular, by the classical Weyl’s perturbation theorem, we know there exists a deterministic constant such that

where denotes the entrywise -norm of a symmetric matrix. By writing , we clearly see has bounded variation for almost all . ∎

We are now able to summarize our discussion with the following result.

Proposition 3.1.

Let be a semimartingale satisfying Assumptions 2.1 and 2.2. For a given , let be the list of eigenvalues of (arranged in decreasing order) and let be an associated set of eigenvectors. Then, for every

where in for . In addition, if is a generic222For a continuous real-valued function defined in a neighborhood of , the order of flatness at is defined by the supremum of all integers such that near for a continuous function . We say that two functions and meet of order at when . Let be a parameterized family of self-adjoint matrices. We say that the curve is generic, if no two of continuously parameterized eigenvalues meet of infinite order at any if they are not equal for all . We refer the reader to e.g Rutter [45] and Alekseevsky, Kriegl, Losik, and Michor [6] for further details. smooth curve a.s and is a.s constant over the time interval , then there exists a choice of adapted eigenvector processes over such that

is a semimartingale for each .

Proof.

Fix a realization and . Let be a matrix with entries given by

It follows from Assumptions 2.1 and 2.2 that is a non-negative definite matrix. Now, let us take , and let be given by . Then,

Now, the variational characterization of eigenvalues follows from standard arguments on quadratic forms over for each . For the second part, if is then from Theorem 7.6 in Alekseevsky et al [6], one can choose smooth versions for related eigenvectors with bounded variation paths. By Gaussian elimination and Lemma 3.1, one can readily see that one can choose it in such way that is a -dimensional adapted process. The usual integration by parts for stochastic integrals allows us to state that is a semimartingale. ∎

Similar to the classical PCA methodology based on covariance matrices, Proposition 3.1 yields a dimension reduction based on quadratic variation rather than covariance as follows. Let be a truly -dimensional semimartingale satisfying Assumption 2.2 and let us assume that one observes for a given . Summing up the above results, we shall reduce dimensionality as follows

| (3.3) |

At this point it is pertinent to make some remarks about (3.3). At first, the assumption in Proposition 3.1 that is constant a.s over holds in typical cases found in practice.

Remark 3.1.

In order to get semimartingale principal components, the assumption that is generic cannot be avoided. See e.g example 7.7 in Alekseevsky et al [6]. However, one should notice that if two eigenvalues meet at an infinite order at a time , then all derivatives at this point must coincide.

By the very definition, which means that presents the th largest quadratic variation among . One should notice that the principal components are orthogonal in the sense

where for . Moreover, the -th eigenvector must be interpreted as the random direction in at time which maximizes over .

Remark 3.2.

We stress that

where . Therefore, our methodology is rather different from Ait-Sahalia and Xiu [5]. In qualitative terms, our framework does not loose information in terms of the underlying quadratic variation space (See Proposition 4.1) and hence in terms of as well. In addition, we do not require a simple eigenvalue structure as required in [5].

Let us now briefly discuss the importance of the subspaces in concrete multi-dimensional semimartingale systems.

4. Bounded variation component and quadratic variation in

In this section, we discuss two concrete examples of models which exemplify the importance of analyzing the principal components of high-dimensional semimartingale systems in terms of rather than covariance matrices.

4.1. Correlation in -dimensional asset prices

Correlation among asset prices is a well-known phenomena and it has been studied by many authors in the context of covariance and, more recently, quadratic variation matrices. Let us suppose the asset log-prices form a -dimensional Itô process

| (4.1) |

where and satisfy usual conditions to get a well-defined -dimensional semimartingale. For simplicity of exposition, let us assume that is known.

One typical example of the existence of bounded variation component in is the occurrence of correlation among which can be measured by volatility, i.e., quadratic variation. This type of phenomena has been recently studied by Ait-Sahalia and Xiu [4] who identify nontrivial correlation among by means of suitable estimators . In the presence of correlation among assets as in [4], the subspace naturally emerges as a non-trivial subspace of due to the fact that . See also Buraschi, Porchia and Trojani [16] for a discussion of correlation in the context of optimal portfolio choice.

4.2. Stochastic PDEs with finite-dimensional realizations

Let us describe how arises in the context of stochastic PDEs. Let us concentrate the discussion in one major research theme related to interest rate modelling: The calibration problem of Heath-Jarrow-Morton models [32] (henceforth abbreviated by HJM) based on forward rate curves. We refer the reader to e.g [13, 14, 15, 24] and other references therein for a detailed discussion on this issue. The classical HJM model can be described by a stochastic PDE of the form

| (4.2) |

where is the first-order derivative operator acting as an infinitesimal generator of a -semigroup on a separable Hilbert space which we assume to be a space of functions . The drift vector field has great importance for pricing and hedging derivative products and it is fully determined by under a martingale measure. See e.g [24] for more details.

One central issue in the literature is the use of the stochastic PDE (4.2) in practice. In this case, it is very important to know when (4.2) admits a finite-dimensional subset where the stochastic PDE never leaves as long as the initial forward rate curve , namely

The subset can be interpreted as a finite-dimensional parameterized family of smooth curves which can be used to estimate the volatility component of the model (4.2) starting with an initial curve . See e.g [7, 14]. Therefore, one central issue in interest rate modelling is the existence, characterization and estimation of . See [13, 14, 15, 24, 25, 28, 29, 41, 44, 7, 40] and other references therein.

As far as the existence is concerned, Bjork and Svensson [15] and Filipovic and Teichmann [25] have shown that the existence of is equivalent to

in a neighborhood of , where is the Stratonovich drift induced by and is the Lie algebra generated by the vector fields . In fact, must be an affine submanifold of . In particular, there exists a parametrization , a truly -dimensional Brownian semimartimgale and a linear subspace spanned by a basis such that

| (4.3) |

Under some assumptions (see e.g Duffie and Khan [22]), the semimartingale state process can be generically written as an affine process. In contrast to the previous example of sample data from the -dimensional semimartingale (4.1), in (4.3) is not observed.

For a given pair as above, one can actually show there exists a unique splitting which realizes

for . Here, is a basis for and it is basis for such that

Moreover, and . The loading factors associated to are related to the risk factors in which in turn are associated to no-arbitrage restrictions.

Under the assumption that a stochastic PDE (one typical example is (4.2)) admits a finite-dimensional realization (4.3), we are going to present consistent estimators for the minimal invariant subspace . More precisely, based on high-frequency data and techniques from factor analysis, we take advantage of the structure induced by in order to provide consistent estimators for related to the minimal invariant subspace .

4.3. Noise dimension vs quadratic variation dimension

It is convenient to point out that the rank of a quadratic variation matrix is not the maximal rank of the underlying volatility process studied by Jacod and Podolskij [37] and Fissler and Podolskij [30]. See also Sahalia and Xiu [5] for a similar framework. In fact, let be a -dimensional Itô process of the form

Let where

Proposition 4.1.

If has continuous paths, then for every . Moreover, the inequality may be strict.

Proof.

Let us fix a realization in a set of full measure and some in . Let, also, . Then, since is a continuous matrix-valued function, and the rank is an integer-valued lower-semicontinuous function, there exists such that .

Since is a non-negative definite matrix, we can find a set of linearly independent eigenvectors for , say, , with respective eigenvalues , such that for .

Now, observe that if are real numbers such that , then by putting and using the orthogonality of the eigenvectors, we have

| (4.4) |

Note also that, for any such vector , the function is continuous, so we can find an open interval containing , with length , satisfying

| (4.5) |

Furthermore, using the non-negative definiteness of , we have that

| (4.6) |

Now, suppose, by contradiction, that . Then, we can find real numbers , with , such that, for , where are the eigenvectors of given above, we have , and, in particular,

To show that the inequality may be strict, consider the following example: Let us assume that and we take

where , with is the indicator function of the set . Then, clearly,

and , for all , whereas for . ∎

Remark 4.1.

The main message of the above proposition is that if a direction has a non-null quadratic variation for some time , then this direction has non-null quadratic variation for all times . This phenomenon does not occur with the volatility matrix , as shown above.

We also stress that Assumptions 2.1 and 2.2 yield the study of a statistical test to check the existence of a null quadratic variation component in . The full derivation of the statistical test will be further explored in a future paper.

Corollary 4.1.

Let be a truly -dimensional process satisfying Assumption 2.2. Let be the ordered eigenvalues of the associated quadratic variation matrix such that . The test versus , is a well-defined statistical test and it is equivalent to versus .

Remark 4.2.

It is pertinent to interpret from the perspective of semimartingale-based factor models. When then

where . In applications, one may think as the space of high-dimensional portfolios composed by which can be depicted into two dynamic spaces. When is singular, then the dynamic space has to be filled with zero quadratic variation dynamics which can be neglected only if one is solely interested in volatility. We stress that this phenomena is intrinsic to the principal component analysis of high-dimensional semimartingale systems.

5. Estimation of

In this section, we show how to estimate the pair which realizes

for a given observed process satisfying Assumptions 2.1 and 2.2. The reader may think as a pair of factor spaces which are not observed. We stress even if one observes all trajectories of , the components of are not visible when .

5.1. Identification of the Spaces )

Throughout this section, we are going to fix a truly -dimensional process satisfying Assumption 2.2. Let be the splitting introduced in (2.8). We assume that and , where . In order to clarify the exposition, we first assume that one is able to observe all trajectories of a given in continuous time.

Proposition 5.1.

Let be a -dimensional process satisfying Assumptions 2.1 and 2.2, and let be the quadratic variation matrix of . Let be an orthonormal basis formed by eigenvectors associated to the ordered (decreasing order) eigenvalues of . Let be the random matrix given by

where . Then there exists a set of full measure such that for each realization , is a basis for and is a basis for . Moreover,

| (5.1) |

Proof.

By applying the standard spectral theorem on , we can find a set of eigenvectors associated to which constitutes an orthonormal basis for , so that is invertible for every . Let . If then Lemma 2.1 yields . Therefore, is null a.s for every which implies that the last rows of are null for every where has full probability. Let us fix and we write , , , where . Now, since is invertible then is a linearly independent subset of . Moreover,

which by linearity implies that

| (5.2) |

More importantly, (5.2) yields . Since , we actually have and the linear independence yields . Therefore,

| (5.3) |

Since is a linearly independent subset of , than (5.3) yields

With the obvious modifications, we stress the result of Proposition 5.1 also holds over for every .

5.2. Estimation of the spaces

Let us suppose that we are in the same setup of the previous section, but now we have a high-frequency of observations at hand from a truly -dimensional process satisfying Assumption 2.2. In this section, the high-frequency data is assumed to be observed at common regular times for each . We leave the case of non-synchronous data to a future research. Throughout this section, we assume the existence of a consistent estimator for which satisfies the following assumption:

Assumption 5.1.

is a sequence of non-negative definite and self-adjoint matrices such that as .

In the sequel, we fix satisfying Assumption 5.1 and we choose 333For instance, if than choosing in such way that as allows us to take bigger than as a consistent estimator. any consistent estimator for . The goal of this section is to describe a generic estimation methodology based on the existence of satisfying Assumption 5.1. We stress the results of this section do not depend on the estimator of the quadratic variation matrix. We refer the reader to e.g [19, 50, 51, 39, 52, 18, 23, 21] and other references therein for a complete view of the estimation methods for .

We need to define a metric notion on the set of finite-dimensional subspaces embedded on a possibly infinite-dimensional vector space. For this task, we make use of the same metric between subspaces defined by Bathia et al. [11]. Let and be two finite-dimensional Hilbert subspaces of an inner product vector space with dimensions and , respectively. Let be an orthonormal basis of , . Then, we define

| (5.4) |

In the sequel, we need to compute distances for finite-dimensional subspaces which are not embedded in a natural common Hilbert space. For this reason, let be a finite-dimensional linear space. If and are finite-dimensional subspaces of , then we define

| (5.5) |

where is the canonical isomorphism and . One can easily check that is indeed a metric over the set of all finite-dimensional subspaces of . The metric in (5.5) is very convenient to study consistency of subspace estimators.

Before presenting the main result of this section, we need two preliminary lemmas.

Lemma 5.1.

Let be a sequence of self-adjoint real matrices such that as . Assume that and let us denote by a set of orthonormal eigenvectors associated to the least eigenvalues of . Let and . Then,

as .

Proof.

Let be an orthonormal basis for given by eigenvectors of . Let be an orthonormal subset of eigenvectors of associated to eigenvalues and . To shorten notation, in the sequel we denote by the inner product over Euclidean spaces. We may assume that . Let be a basis for the orthogonal complement . At first, we notice that since and have the same dimension, it is sufficient to prove that . This is equivalent to prove that

To do so, let , and note that and . Therefore,

and since we may conclude that

We now claim that

| (5.6) |

Let be the ordered eigenvalues of related to the least eigenvalues. Let be the number of non-zero eigenvalues of . We have for every sufficiently large so that

as .

On the other hand, as and hence

Lemma 5.2.

Let be a truly -dimensional process satisfying Assumption 2.2. Then, the set is deterministic 444A random set is deterministic if there exists a subset such that a.s. for every .

Proof.

For the statement is obvious, so let us fix and let be the subspace of given by (2.3). Let be the dimension of . Let be a basis of and let be a complement basis of in such a way that is a basis of . Let be the change of basis from to with matrix representation . We set where . From Lemma 2.1 and the definition of , we know that has full probability. We pick . Of course,

constitutes a set of linearly independent deterministic vectors in and by the every definition

for . Since has dimension for every , then for every . ∎

Let be the orthogonal matrix formed by orthonormal eigenvectors of . Of course, we are not able to prove that converges to due to the lack of identification of eigenvectors. What is true is the following notion of convergence. In the sequel, if is a sequence of random variables, then

means that, as . We similarly define and when both and as .

Theorem 5.1.

Let be a process satisfying Assumptions 2.1 and 2.2. Let be a consistent estimator for satisfying Assumption 5.1 and let be any consistent estimator for . Let be the orthogonal matrix whose rows are formed by eigenvectors of . If , then let us define and . Under the above conditions, we have

as . If then as . Moreover,

| (5.7) |

| (5.8) |

Proof.

Recall the definition of the isomorphism used in (5.5). From Lemma 5.2, we have and by the very definition of , we also have . Thus, from Lemma 5.1 above, we have

Now, notice that

Therefore, it follows from the definition of the metric that

Since is an integer-valued consistent estimator, we shall assume that . By the very definition, we know that

and

Let us write

A straightforward consequence is the following result.

Corollary 5.1.

Assume that hypotheses in Theorem 5.1 hold and let be discretely-observed at over , where . Then, there exists such that

| (5.9) |

as .

Proof.

Let us equip with the topology of the uniform convergence in probability. Let be the smallest finite-dimensional subspace of which contains . Let be the canonical isomorphism for some . We notice that is actually an homeomorphism when is endowed with the subspace topology. From Theorem 5.1 and the definition of the metric , we know that

| (5.10) |

as , where denotes the projection onto a closed subspace . Then from (5.10) and using the fact that is an homeomorphism, we get the existence of such that

as which implies assertion in (5.9). ∎

Under the assumptions of Theorem 5.1, if is a discretely-observed semimartingale at over , then we shall use Corollary 5.1 to estimate by OLS

the regression coefficients which provide us the precise linear contribution of non-null quadratic variation and pure drift components in and , respectively. In this case, the following linear combination

depicts into elements of over the sample in . The estimation of the factor spaces provides a tool to optimal asset allocation/dimension reduction in high-dimensional portfolios composed by semimartingales, a topic which will be further explored in a future paper.

6. Estimation of Finite-Dimensional Invariant Manifolds

In this section, we apply the theory developed in previous sections to present a methodology for the estimation of finite-dimensional invariant manifolds related to space-time data generated by stochastic PDEs of the form

| (6.1) |

where is an infinitesimal generator of a -semigroup on a separable Hilbert space which we assume to be a subspace of absolutely continuous functions where for simplicity of exposition we work with the one-dimensional space555Indeed, it is not too difficult to extend the results of this section to the multi-dimensional case where is a compact subset of . This type of flexibility is important to treat more complex space-time data such as volatility surfaces in Financial Engineering. set where . The vector fields are assumed to be Lipschitz and the dimension is fixed.

6.1. Splitting the invariant manifold

Let us now introduce the basic geometric objects related to the stochastic PDE (6.1) that we are interested in estimating. We refer the reader to Tappe [48] for a very clear treatment of these objects.

Definition 6.1.

A family of affine manifolds in is called a foliation generated by a finite-dimensional subspace if there exists such that

The map is a parametrization of .

Remark 6.1.

We notice that the parametrizations of are not unique, but for any distinct parametrizations and we have for every .

In the remainder of this paper, denotes a foliation generated by a finite-dimensional subspace.

Definition 6.2.

The foliation of affine manifolds is invariant w.r.t the stochastic PDE (6.1) if for every and we have

for .

The above objects lead us to the following definition which is the main object of statistical study in this section.

Definition 6.3.

We say that the stochastic PDE (6.1) has an affine realization generated by a finite-dimensional subspace if for each there exists a foliation generated by with which is invariant w.r.t (6.1). An affine realization with a generator is called minimal, if for another affine realization generated by some subspace we have .

Remark 6.2.

See Section 4.2 for a brief discussion on affine realizations in the context of Mathematical Finance. Throughout this paper, we assume that the stochastic PDE data generating process satisfies the following assumption.

Assumption (A1): The stochastic PDE (6.1) has an affine realization generated by a finite-dimensional subspace.

Let us now introduce the basic operators which will encode the underlying loading factors of the stochastic PDE that we are interested in estimating. We fix once and for all a terminal time , , the minimal subspace generator of (6.1) spanned by linearly independent vectors and a parametrization with null quadratic variation . Under Assumption (A1), the stochastic PDE (6.1) has a strong solution. From the reproducing kernel property of , the evaluation map is a bounded linear functional and therefore point-wise evaluation of the stochastic PDE is well-defined for every point-space and the following representation holds

| (6.2) |

where we set for and . Let us consider the following kernels

The above kernels induce random linear operators and defined almost everywhere by

By the very definition, the random linear operator can be written as

where we denote . In the remainder of this article, we denote by the supplementary subspace of in the minimal subspace .

From Assumption (A1), we know (see e.g Th. 2.11 and (2.27) in [48]) that there exists a truly -dimensional semimartingale which realizes the strong solution (6.2) as follows

| (6.3) |

Definition 6.4.

See e.g [14, 48, 24, 26] for more details on this affine construction of the stochastic PDE. Representation (6.3) is not unique but it will be the basis for our splitting scheme as follows. At first, in order to apply the spectral analysis in previous sections, we will assume the following hypothesis on the stochastic PDE (6.1):

Assumption (A2): For each initial condition , there exists a factor representation which realizes (6.3) and it satisfies Assumption 2.2.

In the sequel, if and is a list of real-valued functions on , then and we set meaning the -valued function .

Remark 6.3.

Let be a representation of the FDR of (6.1). Let be a non-singular random matrix. Then

| (6.4) |

where is a random basis for and .

We can actually write in terms of any representation (6.3) as follows

| (6.5) |

and, moreover, the following remark holds.

Remark 6.4.

In the sequel, we need to introduce new notation. For a given satisfying Assumptions 2.1 and 2.2, we denote , where and the quotient space is defined by the equivalence relation (2.5) over . We stress that and are and , respectively, which are defined in (2.4) for the specific choice .

In practice, we are not able to observe any semimartingale factor of a stochastic PDE admiting a FDR. But it will be very important for our estimation strategy to identify the pair in terms of the random matrix , or more precisely, in terms of the quadratic variation of random rotations of . Next, we recall the following result.

Lemma 6.1.

Let be the stochastic PDE (6.1) satisfying Assumptions (A1-A2) and admitting a FDR generated by the minimal foliation where and . Then, we shall represent (6.1) as follows

| (6.6) |

where is a truly -dimensional semimartingale satisfying , and , where and .

Proof.

By assumption, there exists a truly -dimensional semimartingale satisfying Assumption 2.2 and a basis for such that

From (6.5), we have so that we shall consider the random operator restricted to as follows . Moreover, from (6.5) we readily see that the random matrix of the linear operator is given by for any pair of latent semimartingale representation and a basis for . By Lemma 2.1, we have . Let be a truly -dimensional semimartingale such that is a basis for and is a basis for where . Then and satisfies Assumptions 2.1 and 2.2. Let be the linear isomorphism given by the change of basis from to . If is the matrix of , then we shall write

The main message of Lemma 6.1 is the following. When the stochastic PDE is projected onto (), then the associated latent factors are non-null quadratic variation (bounded variation) semimartingales. We remark that the form of the FDRs (6.6) has already been derived in Bjork and Landén [14] and Filipovic and Teichmann [26] in the context of HJM models. Lemma 6.1 provides an explicit splitting for by separating the loading factors which generate from its complementary subspace attached to their associated spaces and , respectively.

Summing up the above results, we arrive at the following identification result.

Proposition 6.1.

Let be the stochastic PDE (6.1) satisfying Assumptions (A1-A2). For a given , let be the minimal foliation generated by some such that . Let

be a factor semimartingale representation, where and satisfies Assumptions 2.1 and 2.2. Let be a nonsingular random matrix. Let and . Let be the random matrix whose rows are given by where is an orthonormal eigenvector set of associated to the ordered eigenvalues . Then

| (6.8) |

and

| (6.9) |

6.2. Preliminaries on Factor models

The goal of this section is to describe an estimation methodology for the pair which generates invariant foliations for stochastic PDEs of the form (6.1). The methodology will be inspired by the so-called Factor Analysis developed in the Econometrics literature (see e.g [47], [8], [9], [31]), but with some fundamental differences: (a) Unlike the classical discrete Factor Analysis, we are working with an underlying continuous time process sampled in high-frequency at discrete points in time and space. (b) The spaces cannot be identified by applying standard techniques from Factor Analysis due to the rather distinct behavior between quadratic variation and covariance matrices in the high-frequency setup. (c) More importantly, the factor analysis introduced here allows us to reduce and rank the underlying semimartingale factors in terms of quadratic variation rather than covariance, including bounded variation components.

Throughout this section, Assumptions (A1-A2) are in force. We also assume the underlying state-space is the Sobolev space of absolutely continuous functions such that

where is absolutely continuous w.r.t Lebesgue measure (see e.g [24]) and we write to denote the associated inner product. For simplicity of exposition, we work with the closed subspace of formed by functions and we set . With a slight abuse of notation we denote it by .

We are going to fix the minimal invariant foliation generated by a -dimensional subspace equipped with a basis and a truly -dimensional semimartingale satisfying Assumption 2.2 such that

| (6.10) |

In this section, we work in a high-frequency setup as follows. To shorten notation, the points of partition in time and space will be denoted by and , respectively, and we set and . We will assume the samplings in time and space will be equally spaced and equidistant. For the sake of preciseness, it should be noted we are dealing with a sequence of refining partitions and we always assume that , , , as , where both and goes to infinity.

We assume that the observations are generated by a space-time process

| (6.11) |

where represents a space-time error component satisfying some regularity conditions. In this section, we assume that one is able to sample the curves in high-frequency in time. For instance, term-structure objects like interpolated forward rate curves are examples of this type of data. See e.g [38] and other references therein.

In particular, under Assumptions (A1-A2), the -matrix of observations admits an affine noisy representation

| (6.12) |

for and . Throughout this section, we assume that is known by the observer and with a slight abuse of notation we write for the difference . In matrix representation, we shall write

where , , and .

6.3. Estimating the underlying dimension

Obviously, the first step is to estimate the underlying dimension of the finite-dimensional realization. But this is an almost straightforward application of Bai and Ng [8]. Indeed, we are interested in solving the following optimization problem (for large )

where the minimum is taken over the set of real matrices with columns

subject to either or (Identity matrix in ). Here and for . The index encodes the allowance of factors in the estimation procedure.

Remark 6.5.

In order to avoid curse of dimensionality issues, we do assume and jointly.

The factor estimator is defined as follows. Let be the random matrix defined by whose the th column

is an eigenvector associated to the -th largest eigenvalue of subject to . The loading factor estimator is given by

In the sequel, we denote

The estimation procedure for the underlying dimension of is due to Bai and Ng [8]. They propose a class of information criteria of the form

| (6.13) |

for suitable penalty functions . One can show the estimation of can be still carry out on the basis of the ideas contained in [8] even in the high-frequency setup, as long as the following assumptions hold true. The following assumptions are inspired by Bai and Ng [8] and Bai [9] but in the context of a continuous time setup sampled at discrete times. For the sake of completeness, we list them here. In the sequel, is the space of -integrable continuous Brownian semimartingales.

(D1) for each and

in probability as and is a positive definite matrix a.s

(D2) and

as . Moreover, is a -positive definite matrix.

(D3) The error process satisfies assumptions:

-

•

-

•

If then and the sum is bounded in .

-

•

.

-

•

-

•

-

•

The error and the factors are mutually independent.

(D4)

Remark 6.6.

The assumption a.s is not strong. Indeed, since is a Gramian matrix, then if does not satisfy (D1) then we shall reduce the effective dimension without losing information. More importantly, we stress that (D1) implies that factors satisfy Assumption 2.1 but it does not imply that has full rank a.s. The fact that is a positive definite matrix is equivalent to the fact that is linearly independent on the state space equipped with the -inner product666Since we work with the subspace of functions such that , then is indeed an inner product over .. In contrast to the usual factor analysis (see e.g [8, 9]), we stress that is random.

In this case, under some mild growth condition on ,

| (6.14) |

will be a consistent estimator for , where is an arbitrary integer such that . The proof of this statement will be inspired by the arguments given by Bai and Ng [8] and Bai [9]. In one hand, in contrast to [8] and [9], our asymptotic matrix is random and the sampling should be in high-frequency. On the other hand, Assumption D1 allows us to prove similar results without significant extra effort. For the sake of completeness, we give the details here. In the sequel, we denote and

for .

Lemma 6.2.

If Assumptions (D1-D2-D3-D4) hold, then

(a)

(b)

(c)

(d) .

Proof.

Let be the diagonal matrix of the eigenvalues of arranged in decreasing order. From (D1-D2-D3-D4), one can easily check that and hence . In this case, the same argument given in the proof of Lemma A1 in [9] allows us to state that

The next result was enunciated by Bai and Ng [8] in Lemma A3 (in the context of a discrete-time model and deterministic ) without a complete proof. For sake of completeness, we give the details here in our context.

Lemma 6.3.

Let be the diagonal matrix of the eigenvalues of arranged in decreasing order. If Assumptions (D1-D2-D3-D4) hold then

as , where are the eigenvalues (in decreasing order) of .

Proof.

We follow closely the idea contained in the proof of Proposition 1 in [9]. By the very definition, and hence

From the identity , we actually have

where

We shall write (LABEL:inter1) as follows

where is the pseudoinverse of . Then each column of is an eigenvector of . Since then (LABEL:inter2) and Assumptions (D1, D2) yield

as . By the continuity of the eigenvalues, we do have as . Since and have the same random eigenvalues, we conclude the proof. ∎

Lemma 6.4.

Assume that hypotheses (D1-D2-D3-D4) hold and the eigenvalues of are distinct almost surely. Then, for every , there exists a random vector such that

as . Moreover, the matrix is invertible a.s and it is given by and is the eigenvector matrix related to subject to .

Proof.

We are now able to present the following result.

Lemma 6.5.

Let us assume that assumptions (D1,D2, D3, D4) hold and let . Assume the eigenvalues of are distinct almost surely. Then, if (i) and (ii) as where .

Proof.

The same arguments given in the proof of Theorem 1 in Bai and Ng [8] apply in our context. In particular, Lemmas 2, 3 and 4 in Bai and Ng [8] can be similarly proved in our context as well by using Assumptions (D1, D2, D3, D4) and the fact that has distinct eigenvalues a.s. In particular, the fact that is not deterministic is not essential for the validity of the analogous results of Lemmas 2, 3 and 4 given by [8] in our context, as long as (Assumption D1). In particular, for let us define . In our context, Lemma 3 in [8] can be written as follows: There exists such that

in probability, where and exists due to Lemma 6.4. By construction . Assumptions (D1-D2) yield a.s. By writing

for each . If , then similar to Lemma 4 in [8], Assumptions (D1,D2, D3, D4) and the fact that the eigenvalues of are distinct almost surely yield

The rest of the proof is identical to the proof of Th 1 in [8], so we omit the details. ∎

6.4. Main Results

Let us now present the main results of this section. The following list of assumptions will also be in force throughout this section.

(Q1) The eigenvalues of are distinct almost surely.

(Q2) We assume

is bounded in probability for every .

(Q3)

as for each .

(Q4) There exists a sequence of natural numbers decaying to zero such that

(Q5) is bounded in probability and for each ,

as .

Remark 6.7.

Assumption (Q1) is essential to our estimation procedure because it yields an asymptotic and a random basis for which will allow us to construct a consistent pair of estimators for the splitting of the invariant manifold . The technical conditions (Q2, Q3, Q5) are not strong since they impose a very mild growth condition on the eigenvectors of . Assumption (Q4) is quite natural for error structures arising in space-time data generated by stochastic PDEs. For example, as far as the consistency problem of the HJM model (see section 4.2), assumption (Q4) means that the initial fitting method used to interpolate points which generates cannot introduce an extrinsic volatility for the market. In other words, (Q4) rules out pure martingale error structures.

The starting point for the estimation of is to take advantage of the identities (6.8) and (6.9) based on a quadratic variation matrix constructed from an asymptotic satisfying Assumptions 2.1 and 2.2. We define such process as follows: Let be a factor representation of (6.1) satisfying Assumption (A2) and the (D1-D2-D3-D4-Q1) and let be the associated matrix defined in Lemma 6.4. Since is nonsingular a.s and is positive definite, then the random matrix matrix given by

| (6.18) |

is non-singular a.s. Then we shall apply Remark 6.3 to state that is a truly -dimensional process and it is a factor measurable process realizing (6.4) for the basis (loading factors) . From Remark 6.4, satisfies Assumptions 2.1 and 2.2.

In the sequel, for a given factor representation of (6.1) satisfying Assumption (A2) and the assumptions in Lemma 6.4, we set . Let and be the matrices given, respectively, by

| (6.19) |

for and

We stress that has a quadratic variation matrix in the sense of Definition 2.1.

Proposition 6.2.

If Assumptions (D1, D2, D3, D4) and (Q1, Q2, Q3, Q4) hold true, then

as .

Proof.

At first, by taking large enough, assumptions (D1, D2, D3, D4, Q1) allow us to use Lemma 6.5 and we assume that because is an integer-valued consistent estimator. In the sequel, if is a real-valued process then we write . By using the definition of , one can actually write

where and is be the diagonal matrix of the eigenvalues of arranged in decreasing order (see Lemma 6.3)).

To shorten notation, we set and for . In the sequel, for we denote any random variable which is in probability, is a constant which may differ from line to line and let us denote the -matrix given by where

for . We claim that

| (6.20) |

and

| (6.21) |

as , where is the usual vectorization operator. Let . By the very definition,

By Lemma 6.3, we know that as , where are the eigenvalues of . Then Lemma 6.4 yields

as . This shows that (6.21) holds. By noting that

we only need to check (6.20) in order to conclude the proof. Let . From Lemma 6.3, we know that , so we only need to check that

| (6.23) |

At first, for each we shall write

| (6.24) | |||||

where . We divide the argument into two steps.

Analysis of . It is sufficient to prove that

for each . In fact, a simple application of Cauchy-Schwartz inequality and the fact that yield the following estimates

| (6.25) |

| (6.26) | |||||

| (6.27) |

Analysis of . The estimates for the crossing terms are more involved. Let us split according to the terms , and as follows. To shorten notation, in the sequel we denote . Cauchy-Schwartz inequalities and routine algebraic manipulations yield the following estimates

We also shall write

and

The next step is the analysis of the convergence of the loading factor estimators defined as follows. Let

and

for Since is non-singular a.s, then is a basis for for almost all . More importantly,

where .

Proposition 6.3.

If Assumptions (D1, D2, D3, D4, Q1, Q5) hold true, then

as .

Proof.

Let us fix . Since is an integer-valued consistent estimator for , then we shall assume that . Under (D1, D2, D3, D4, Q1), is a well-defined random basis for . By the very definition,

Let us recall that for any , we can compute the Sobolev norm as follows where the sup is taken over all partitions of . See e.g Prop 1.45 in [33] for further details. If is a partition of , then

Since , then (Q5) yields

as . Cauchy-Schwartz inequality and (Q5) yield

as . From Lemma 6.4, we know that so that . Since , then we obviously have as . This concludes the proof. ∎

In the sequel, is any consistent estimator for based on . See Appendix for details. Let be the matrix whose rows are given by , where is an orthonormal eigenvector set of the matrix (see (6.19)) associated to the ordered eigenvalues . Let us define

| (6.29) |

and

over a sample . By the very definition, .

Now we are able to present the main result of this article. Before this, we need an elementary lemma from linear algebra.

Lemma 6.6.

Let be a set of linearly independent vectors in a real Hilbert space with inner product and . Let be an orthogonal matrix. If is the Gram-Schmidt orthonormalization of and is the Gram-Schmidt orthonormalization of , then we have

Proof.

The proof follows by just observing that for each , and for each , we have , where ∎

Theorem 6.1.

Let be the stochastic PDE (6.1) satisfying Assumptions (A1-A2). Assume the existence of a factor representation satisfying Assumption (A2) and (D1, D2, D3, D4, Q1, Q2, Q3, Q4, Q5). For a given , let be the minimal foliation generated by such that and we set

Then, and

Moreover,

| (6.30) |

and

as .

Proof.

From Assumptions (A1-A2), we shall fix a pair which realizes

where , is a continuous semimartingale satisfying Assumption (A2) and (D1, D2, D3, D4), (Q1, Q2, Q3, Q4, Q5). Here, we set and , where is given by (6.4). From Remark 6.4, satisfies Assumption as well.

To shorten notation, we abbreviate Gram-Schmidt orthonormalization by GSO. Let

and

Following the same lines as in the proof of Theorem 5.1 and noting that (see Remark 6.4)

we obtain

| (6.31) |

as . By using the triangle inequality, we obtain

and from equation (6.31), it is enough to prove that as .

Let and be as in Proposition 6.3. Let and be large enough so that and . Let and be the GSO of and , respectively. Lemma 6.6 allows us to state that is the GSO of and is the GSO of .

From the orthonormalization procedure, for each , we have

and

Thus,

Therefore, since is an isometry, we have

Let us work with the quantity inside the brackets, and let us introduce some notation: Denote the matrix of by , i.e., for any vector ,

Note that since the transformation is orthogonal, we have

Observe that from Proposition 6.3, we have that as . Since is orthogonal and the set of orthogonal matrices is compact, the set is uniformly bounded in and , so that

and

as .

Therefore,

as , which thus implies that

and then,

as . The proof for the statement in probability follows from the same reasoning as in the proof of Theorem 5.1. Let us now check the ordering (6.30). Let be the eigenvalues of the self-adjoint non-negative matrix arranged in decreasing order a.s. By the very definition,

Moreover, the eigenvalues are continuous functions of the entries of the matrix and and for large enough. Then,

as . This shows that (6.30) holds. Lastly, by the very definition, the matrix of the random operator computed along the basis is given by . Therefore, . Proposition 6.2 yields

as . This concludes the proof. ∎

7. Simulation Studies and Applications

In this section, we present some numerical results to illustrate the methodology developed in this article.

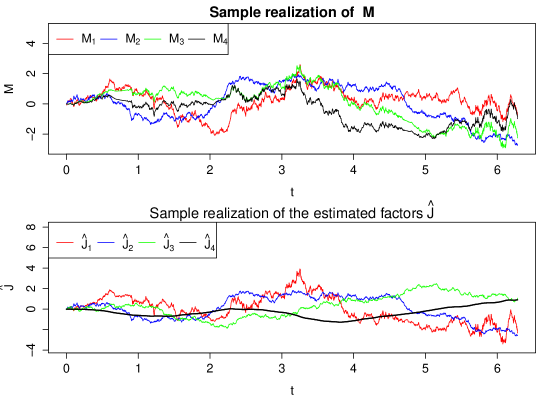

7.1. Semimartingale PCA

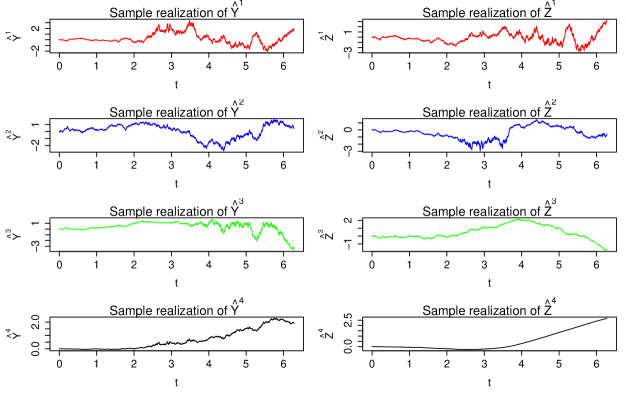

In this section, we illustrate the estimation of the factor spaces based on a finite-dimensional semimartingale system sampled in high-frequency. In particular, the goal is to illustrate Proposition 3.1. In the simulation below, we assume that one observes a 4-dimensional semimartingale as follows: We consider a Markov diffusion

driven by a 3-dimensional Brownian motion and the vector fields and are given by and

One can easily check and since is a truly 4-dimensional semimartingale, then where . The observation times are taken to be equidistant: where the total number of observations is . The estimated factors in Figure 1 are ranked in terms quadratic variation (see Theorem 5.1) and we clearly observe that identifies a null quadratic variation factor which generates . The quadratic variation explained by the principal components are given by Table 1, where and is the -th estimated eigenvalue related to -th estimated principal component .

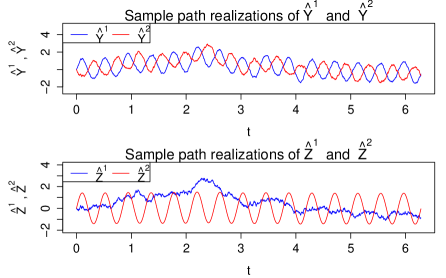

7.2. Variance versus quadratic variation

In this section, the goal is to illustrate that any naive attempt to implement standard factor models towards dimension reduction in term of quadratic variation is hopeless. For this purpose, we consider two very simple space-time two-dimensional semimartingales driven by a single Brownian motion .

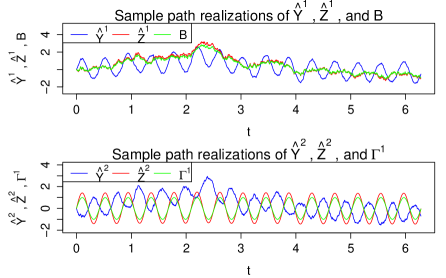

where is a one-dimensional Brownian motion, and . In the sequel, the drift components are denoted by , and we set and . Let and be the dynamic spaces generated by and , respectively. We clearly have

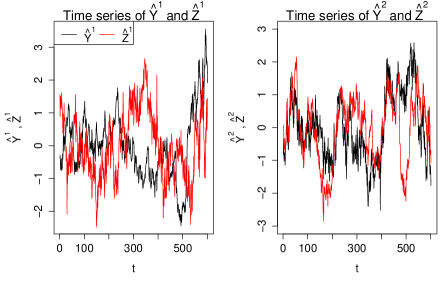

Here, in the time variable, the observation times are taken to be equidistant: where the total number of observations is . In the spatial variable, the observation times are taken to be equidistant: where the total number of observations is . The estimated pair of factors provided by the high-frequency factor model based on variance will be denoted by . Here, is the estimator of the leading factor component in terms variance. The estimated pair of factors provided by the high-frequency factor model based on quadratic variation will be denoted by . Here, is the leading factor component in terms of quadratic variation (see (6.29)).

In Figure 3, we clearly see that the factor analysis based on second moments is not able to identify . The leading component estimated factor resembles a bounded variation process with large variance and the second estimated factor is essentially the first one distorted by the Brownian paths in such way that the true pair is by no means identified. In strong contrast, Figure 3 clearly reports that the estimated pair identifies the pair . We stress that in this two-dimensional setting, the true factors can be estimated up to multiplicative constants so that the results presented in Figures 2 and 3 shows a very consistent estimation of by using our methodology. More importantly, the correct splitting and ranking in term of quadratic variation is fairly estimated. This numerical example illustrates the use of factor analysis based on variance to infer volatility (quadratic variation) does not have any sound basis even in a very simple space-time semimartingale model given by above.

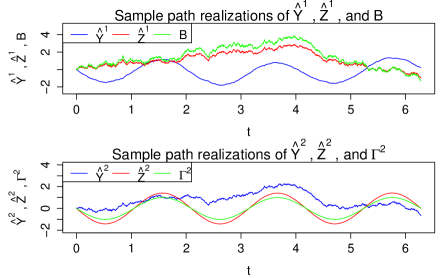

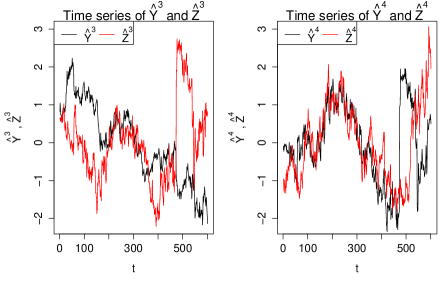

Figure 4 presents the results for the model . In this numerical experiment, the goal is to illustrate that null quadratic variation factors with large variance may be the leading component by using standard factor models in terms of variance. In Figure 4, we report that estimates well the Brownian component responsible for the quadratic variation subspace of , estimates well the bounded variation component responsible for the null quadratic variation subspace of . However, the correct leading component of the space-time semimartingale is the Brownian motion and not . This simple example shows that prioritising components with large variance by using standard factor models may be completely superfluous in terms of quadratic variation. This shows that dimension reduction for semimartingale systems can not be accurately performed by using classical dimension reduction based on variance.

7.3. Estimating finite-dimensional realizations from a SPDE

Here, we illustrate our methodology with some applications to space-time semimartingale models. The first example is based on a Markov diffusion

driven by a 3-dimensional Brownian motion and the vector fields and are given by and

where,

| (7.1) |

and , and . In this case, , , and . Figure 5 shows the estimated factors of equation (7.1) by using the variance-based factor model and the PCA semimartingale developed in this paper. Clearly, the variance-based factor model is not able to identify the subspace (and hence as well), while the PCA semimartingale does. In addition, Table 2 presents where is the -th element of the matrix (see (6.19)). Table 3 presents the variation explained by PCA semimartingale by means of where is the -th estimated eigenvalue related to -th estimated principal component . One clearly see the use of PCA semimartigale is more efficient than the variance-based factor model in identifying quadratic variation dimension.

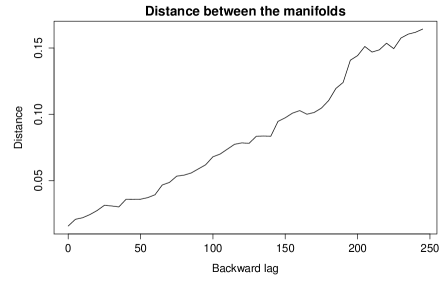

Dynamic distance between manifolds Let us now investigate the robustness of our methodology in the estimation of the minimal invariant manifold, say , for a stochastic PDE. For this purpose, we consider the following objects: Let be the estimator for based on the entire sample . Let be the same estimator but computed over the reduced sample where and is a fixed integer smaller than . To compute the distance between manifolds, we use the following approximation for the Sobolev inner product

See e.g Prop 1.45 in [33] for more details. Based on this approximation for , we perform the Gram Schmidt algorithm to orthonomalize and . We then use (5.4) computed in terms of . We repeat the above procedure for where is a prescribed integer smaller than . The idea is to compute

| (7.2) |

Under existence of a finite-dimensional invariant manifold, must be null as . In order to illustrate the invariance aspect of Theorem 6.1, we consider the following stochastic PDE

| (7.3) |

where the volatilities curves are and , , is the infinitesimal generator of the right-shift semigroup defined by the action . We set as the classical Heath-Jarrow-Morton drift (see Heath et al [32]). One can easily check that this HJM model admits a finite-dimensional realization of the form

and a parametrization

In this case,

is the strong solution of (7.3). We compute (7.2) for the model (7.3) which shows that it fluctuates between zero and so that we prefer do not report this numerical experiment in this section. More interesting than this is to illustrate (7.2) in the presence of noise. For this purpose, we consider an observational process where where is a standard Gaussian variable for every such that is independent form whenever . Figure 6 illustrates that the presence of noise may lead to an erroneous analysis for the existence of a finite-dimensional invariant manifold for the stochastic PDE (7.3). As the backward lag increases the distance between manifolds increases as well with short periods of stability.

7.4. Application to real data sets

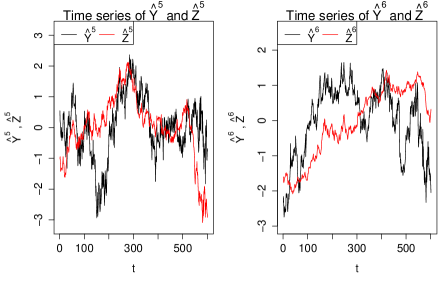

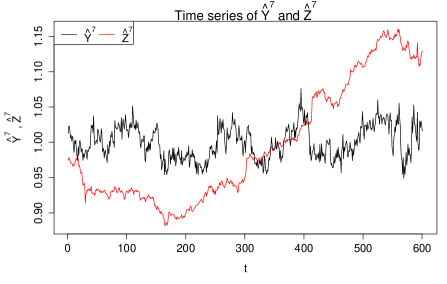

In this section, we illustrate the theoretical results of this article with an application to a real data set. We consider the UK nominal spot curve obtained by the Bank of England with maturities .5 to 25 years (50 maturities) and daily data ranging from 27 May 2005 to 9 October 2007 summing 601 observations. We postulate an affine structure in the data, for instance finite-dimensional realizations for a SPDE data generating process. The first task is to estimate the underlying dimension of the affine manifold. The penalty function used in (6.13) to estimate the number of factors is given in page 201 of [8]. Any of these penalty functions produce identical results for the estimation of the underlying dimension. The statistics (given by (6.14) estimates seven factors for this data. In order to estimate the dimension of the quadratic variation space , we make use of the Fourier-type estimator introduced by [39]. Under the assumptions of Proposition 8.1 in Appendix, we take in Corollary 8.1 in the estimation procedure. The estimation indicates , so that . Figures 7 and 8 report the time series of the estimated factors , where denotes the variance-based factor estimator and is given by (6.29).

Figure 8 and the estimation strongly indicate the presence of a non-trivial drift dynamics in the data. In particular, the estimated factor with smallest variance is not able to identify the drift while seems to estimate a bounded variation curve subject to small errors due to observational errors or microstructure effects.

In order to compare our methodology with the standard factor model, we also perform a principal component analysis in two different versions. In Table 4, and is the -th estimated eigenvalue related to the PCA semimartingale estimated principal component given by (6.29). In table 5, where is the -th element of the matrix (see (6.19)). The first PCA semimartingale component already explains 50 per cent of the total variation while only the third classical factor approximates half of the quadratic variation contained in the data.

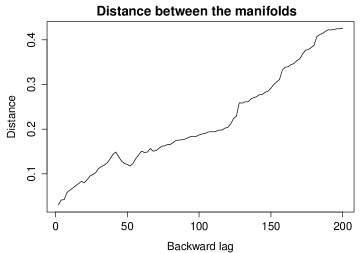

Figure 9 reports the dynamic distance (7.2) of the estimated manifold over the entire period of our sample against where As the backward lag increases, the distance increases as well but we observe some periods of stability over time.

8. Appendix: Estimating dim

In this section, we give a concrete alternative for estimating which is an important component in Theorem 6.1. From (6.5), we notice that if the stochastic PDE admits a finite-dimensional realization, then the matrix of the finite-rank linear operator is given by whenever

for each basis of a finite-dimensional subspace which generates a finite-dimensional realization. Rigorously speaking, we cannot estimate directly through high-frequency sampling of factors because they are not observed. In this case, one has to work with a high-frequency sampling of observed curves subject to noise. This section provides a feasible estimation procedure for this.

We choose to work with the Fourier-type estimator proposed by Malliavin and Mancino [39] but we stress that other quadratic variation estimators can be certainly used as well. The strategy is to find the minimum requirements on the residual process in such way that one can estimate the random operator via an observed curve process

If is negligible in the quadratic variation sense, then the method of the estimation of the kernel is fully based on any reasonable non-parametric estimator of the integrated volatility. We assume that is a well-defined semimartingale random field.