Option Pricing Beyond Black-Scholes Based on Double-Fractional Diffusion

Abstract

We show how the prices of options can be determined with the help of double-fractional differential equation in such a way that their inclusion in a portfolio of stocks provides a more reliable hedge against dramatic price drops than the use of options whose prices were fixed by the Black-Scholes formula.

pacs:

89.65.Gh, 05.40.FbI Introduction

In 1995, the Nobel prize in Economics was awarded to Merton and Scholes for the so-called Black-Scholes (BS) model first published in 1973 Black and Scholes (1973). It was hailed as a milestone in derivative trading, and led to the development of elaborate hedging strategies which promise the safe growth of appropriately composed portfolios of financial assets. Unfortunately, however, the usefulness of the formula was based on a simplifying assumption that fluctuations of assets follow Gaussian distributions. This made it possible to set up a mixture of assets and options that have a chance of growing as a safe investment. In fact, this formula was initially quite successful to a number of professional speculators. Later, however, it turned out that frivolous trading based only on Black-Scholes model and done without a deeper knowledge of market dynamics can lead to dramatic losses and to the formation of speculative bubbles Acharya and Richardson (2009); Merrouche and Nier (2010); Colander et al. (2009). The reason for this is that rare events such as drastic falls in the stock markets are much more frequent than would be expected from Gaussian distributions. From time to time catastrophic outlier events which should not have happened in hundreds of years can occur. Such events have been named ”black-swan” events, after a popular book by N. N. Taleb Taleb (2010). The existence of such events is a severe obstacle to all hedging attempts. Normally, one considers price changes as the result of random steps of a given finite size and demonstrates that these build up to Gaussian random walks. This is a consequence of the central limit theorem (CLT). But in general, some of the steps can be extremely large, and the combined random walks are of the so-called Lévy type. These possess power-like tails which may not even have finite variance. They are encountered in many rare events in nature, such as earthquakes, monster waves in the ocean, and giant drops in financial markets. Apparently, we need new option price formulas that incorporate the possibility of encountering large drops in prices, and are able to compensate for them by a corresponding rise in the price of the derivative.

Many sophisticated models that go beyond Black-Scholes have been introduced in recent decades: among them e. g. models based on Lévy distributions Carr and Wu (2003), truncated Lévy distributions Kleinert (2002), Multifractal volatility Calvet and Fisher (2008), jump processes Tankov (2003), and many other approaches. We would like to focus on models that are based on so-called stable distributions. These have found applications in many scientific fields such as multifractal thermodynamics Jizba and Arimitsu (2004), quantum field theory Kleinert (2013), evolutionary systems Lee and Yao (2004), complex dynamical systems Turcotte et al. (2002), etc. These models usually exhibit self-similarity and power-law behavior in some particular time interval. We also focus on temporal scaling and show that models based on double-fractional diffusion (i.e., self-similar scaling in both spatial and temporal variables) can successfully simulate situations, when instant fluctuations cause high short-term volatility. In this case we can redistribute the risk for short and long term options options and the volatility of the model can remain unchanged. This approach has considerable possibilities for usefulness in further applications in more complex option pricing scenarios. By fitting the data of S&P 500 options, we show that for most of the time the optimal value of temporal-scaling is very close to classical diffusion based on Lévy flight, but for some particular days, e.g., after sudden drops, the risk redistribution can be accounted for by time-fractional diffusion process.

The paper is divided as follows: in Section II stable distributions are briefly introduced, in Section III we discuss various definitions of fractional derivatives and their relation to stable distributions of the Lévy type. Section IV revises previous models of log-Lévy option pricing. In Section V we introduce double-fractional diffusion equations, and discuss their properties. We also show different ways of representing the solutions. Section VI is dedicated to the application of double-fractional diffusion to option pricing and the last section is devoted to conclusions and perspectives.

II Stable distributions

Stable distributions (also called Lévy distributions) constitute an important class of probability distributions. They are form-invariant under convolution, implying that the sum of two random variables governed by Lévy distributions follow such a distribution themselves. Gnedenko and Kolmogorov Gnedenko and Kolmogorov (1968) showed that such distributions are limiting distributions of infinite sums of independent random variables with arbitrary distribution, which is the content of generalized central limit theorem. Moreover, it is possible to express their probability density function by Fourier integrals. In probability theory, the logarithms of the Fourier transforms are referred to characteristic functions. In theoretical physics, these are the well-known Hamiltonian operators . The stable Hamiltonian operators can be expressed as a four-parameter set of the following form

| (1) |

where

Each stable hamiltonian corresponds to the stable distribution, which is denoted as . The parameters acquire following values: , , , and . Unless specified differently, we consider the standard case, i.e., and , and denote the stable Hamiltonian as .

For , regardless of , the distribution is simply the Gaussian distribution. The parameter has an interpretation of a location parameter, and for is equal to the expectation value . Parameter is a scaling parameter, for equal to the standard deviation. Parameter is an asymmetry parameter and the parameter is called stability parameter and determines the overall behavior of the probability distribution function. For the Lévy distribution exhibits power-like Lévy tails that behave like for positive (see Ref. Kleinert (2009)), so

| (2) |

with a similar behavior for negative . The only exception is the case of , where for exhibits the distribution the following behavior

| (3) |

with some constant . The proof can be found in Zolotarev (1986). A similar exponential decay holds for the negative tail and . For , the support is bounded to the interval for , resp. for . For , the distribution has infinite moments for .

The two-sided Laplace transform of does not exist, unless , so for (see Ref. Zolotarev (1986)) the logarithm of Laplace image is equal to

| (4) |

From the symmetry argument we can deduce that the expectation value for exists only when . Sometimes, it is advantageous to use an alternative representation of the stable Hamiltonian, which is

| (5) |

where and are uniquely determined by the parameters , and Sato (1999). Accessible values of the parameter satisfy condition . The corresponding area in -plane is called Feller-Takayasu diamond, and for certain values we obtain extremely asymmetric stable distributions (e.g., for , the value corresponds to the case and corresponds to the case ). Further properties of stable distributions, their representations and relations between them can be found in Refs. Kleinert (2009); Samoradnitsky and Taqqu (1994); Sato (1999).

III Fractional calculus

Fractional calculus generalizes the classical integral and differential calculus to non-integer integration and differentiation. The motivation was originally to find such an operator, for which the second power of the operator would be equal to the first derivative. Subsequently, the goal was to generalize the integral and differential calculus for all real values. This section presents a basic overview of some possible definitions.

Let us begin with the fractional integration, which generalizes the well-known Cauchy formula

in a natural way from integer values to non-integer values by defining

| (6) |

The fractional integral is a linear operator that obeys the semigroup property

| (7) |

It is easy to show that , which is the baseline for the definition of fractional derivative.

III.1 Riemann-Liouville derivative

The relation between fractional integrals and derivatives suggests the introduction the Riemann-Liouville (RL) fractional derivative

| (8) |

where denotes the associated ceiling function, i.e., the lowest integer exceeding . As with ordinary derivatives, these derivatives are linear operators, but contrary to the former, they do not satisfy a composition law like (7) , i.e.,

| (9) |

In fact, they share only a few of the properties of ordinary derivative operators. On the other hand, some particular choices of derivatives, given by special values of , recover some of the typical properties of ordinary derivatives. One example of such a fractional derivative can be inferred from the derivative of integer power functions . For arbitrary integers is the -th derivative of equal to

| (10) |

By performing a fractional integration, it is easy to show that the fractional derivative of a monomial has the same form as in Eq. (10), when . This operator will be denoted . Moreover, this property is valid for arbitrary powers and arbitrary derivatives. As an example, we obtain for that

| (11) |

Expression (11) is equal to zero only for , because of poles in the Gamma function.

III.2 Caputo fractional derivative

One has to notice that the Riemann-Liouville definition of fractional derivatives has some objectionable properties, among them non-zero derivative of constant function and unnatural initial conditions. The latter issue for the most part limits the application of the above derivative in physical and other real problems, because the fractional initial conditions have no physical meaning. These reasons compel us to introduce a different kind of fractional derivative, namely the Caputo (C) fractional derivative, which patches up some of the unwanted properties of RL derivatives. It is defined as follows

| (13) |

The Caputo derivative is more restrictive regarding its domain, because the function must have at least derivatives. On the other hand, it recovers the desired properties, because , and the Laplace transform is equal to

| (14) |

Now, natural initial conditions are recovered. In case of the Caputo derivative, we can solve the fractional differential equation

| (15) |

by introduction of the Mittag-Leffler function

| (16) |

It is easy to see that the function solves Eq. (15). Eventually, Riemann-Liouville and Caputo derivatives can be connected via the relation (to be found e.g. in Ref. Abdeljawad (2011))

| (17) |

III.3 Riesz-Feller fractional derivative

Equation (15) is a generalization of another well-known property of derivatives, which holds for exponential functions

| (18) |

In the case of the Caputo derivative, this formula is generalized in a way that the exponential function is replaced by the Mittag-Leffler function. On the other hand, this property can be preserved, when we send the lower bound to minus infinity; the operator

| (19) |

obeys Eq. (18) even for non-natural derivatives. Such an operator has to be defined on a different space, because the fractional operator of this type is convergent for functions that decay faster than for . This operator is called the Riesz-Feller derivative and is denoted by . Interestingly, we get the same operator, when we use the Caputo derivative approach. In the case of Riesz-Feller derivative it is advantageous to transform into Fourier image because it has the following form

| (20) |

The proof can be found also in Samko et al. (1993). Actually, the Riesz-Feller derivative operator is a special case of the so-called Lévy pseudo-differential operators, for which the fractional Laplacian is an important example. This class of pseudo-differential operators is defined via the Fourier transform through a Hamiltonian

| (21) |

where is the function defined in Eq. (5). Particularly, for extreme values, i.e., for we obtain operators proportional to Riesz-Feller fractional derivatives. For the choice , we have the fractional Laplacian. These differential operators are closely related to Lévy distributions and Lévy processes, because they are the solutions for the space-fractional diffusion equation

| (22) |

IV Option pricing under Log-Lévy process

In classic Black-Scholes option pricing theory Black and Scholes (1973), the price of an option is calculated with the assumption of an efficient market. The evolution of an underlying asset is modeled as a log-normal (or geometric Brownian) process

| (23) |

where is a standard Wiener process, is the drift, and is the volatility of the process. In the following, we will be using notation . The assumption of an efficient market implies that there exists another probability measure , equivalent to the real probability measure , under which the discounted price is a martingale, so , where is a filtration of the stochastic process at time , and is the maturity time. For the exponential processes, the change of measures is given by Esscher’s transform Gerber et al. (1993), which states that the Radon-Nikodym derivative is

| (24) |

where . Particularly, in case of log-normal distribution with the drift equal to interest rate , the process of price evolution has the following form

| (25) |

The price of the option can therefore be calculated as Tankov (2003)

| (26) |

For the European call option, the pricing formula is, with the notation , equal to

| (27) |

By direct differentiation it is easy to show that the option this price fulfills the celebrated Black-Scholes equation

| (28) |

with the boundary condition .

This option pricing model is the one most used worldwide, with many applications, such as estimation of implied volatility Mantegna and Stanley (2000). On the other hand, a considerable amount of effort has been made during last two decades on the development of more advanced evolution models of the underlying assets. As an example, the fractional Brownian motion Mandelbrot and Van Ness (1968) is an elegant model. Furthermore, the complexity of financial markets motivated many authors to introduce even more sophisticated option pricing rules, some examples are provided by Refs. Heston (1993); Necula (2008); Gerber et al. (1993).

We adopt the approach introduced in Ref. Carr and Wu (2003) and assume that the price evolution is driven by the log-Lévy model

| (29) |

Contrary to geometric Brownian process, the prices of log-Lévy stable process do not possess all moments . What is more, it is not possible to use Esscher transform. The only exception is the case, when , or similarly , because then the two-sided Laplace transform exists, which is expressed in Eq. (4). As a result of the exponential decay of the positive tail of the PDF, all moments exist and are finite. Such a model can better describe dramatic price drops on the market, which are more frequent than was envisaged by Black-Scholes theory Kleinert (2013). The price process becomes the following time dependence

| (30) |

where . The corresponding option price, which is given by (26), is equal to

| (31) |

where . By introduction of a new variable and change of integration variable to , we obtain

| (32) |

where is the Green function (sometimes also called fundamental solution). By further transformations and we obtain the equation for in the form

| (33) |

together with the initial condition . This equation is a fractional Black-Scholes equation for log-prices, and for , we recover the classical diffusion equation. In the Fourier image, the equation has the form of a fractional-diffusion equation

| (34) |

V Double-fractional diffusion

In some recent works, other models that involve fractional time derivatives have been studied Jumarie (2010); Song and Wang (2013); Wyss (2000). It has been discovered that complex time scaling introduces more general classes of solutions that exhibit interesting phenomena and enables one to price options more realistically. The original motivation was provided by fractional Brownian motion, originally introduced in Mandelbrot and Van Ness (1968), and later applied to option pricing in Refs. Hu et al. (2003); Necula (2008). The question at stake is which particular fractional derivative is the best when generalizing the Black-Scholes equation, driven by a Green function , obtained as a solution of a double-fractional diffusion equation

| (35) |

where we have considered two type of the temporal derivatives denoted by the parameter , namely (Caputo derivative), or (Riesz-Feller derivative). The parameter is the degree of the spatial derivative and corresponds to the stability parameter. The parameter is the degree of the temporal fractional derivative (corresponding to parameter in definitions of fractional derivatives). It is called the diffusion speed parameter, because, as discussed below, it influences the speed and type of diffusion behavior. In the following sections, we compare two classes of double-fractional diffusion equations, particularly equations with Riesz-Feller time derivatives, resp. Caputo time derivatives. Both of these equations are examples of a wide class of two-variable pseudo-differential equations, which are usually represented via the Laplace-Fourier (LF) image (which means the Fourier image in spatial variable and the Laplace image in the temporal variable) as

| (36) |

In our case, i.e. when Eq. (36) represents a LF image of the double-fractional diffusion equation, then , and is determined by the type of derivative, for the Caputo derivative , and for Riesz-Feller derivative is . We shall note that the equation requires one initial condition , which is the Fourier transform of . In the following, we consider that , which leads to . This is valid for the case, when (sometimes called slow diffusion). In the following section we focus on that case, because there exists a representation which results in a nice interpretation of double fractional diffusion. On the other hand, when we consider (fast diffusion), we can also obtain the same form of equation as in Eq. (36), we have only to add the second initial condition of the particular form, namely

| (37) |

The question at stake is, whether the solutions of Eq. (36) can be interpreted as probability distributions, i.e. whether they are positive. In Ref. Pagnini (2013) it is shown that for are solutions positive for all , while in case , the parameters have to obey the condition .

V.1 Composition rule for and smearing kernel

In the case when , we can derive a special form of the Green function, which gives a nice interpretation of the double fractional Green function as a composition of space-fractional Green functions weighted by smearing kernel equal to time-fractional Green function. We begin with Eq. (36). The solution to this equation can, in Fourier-Laplace image, be expressed as

| (38) |

Under the assumption that , we can apply Schwinger’s formula and obtain

| (39) |

Therefore, the original -dependence is given by

| (40) |

Because , we obtain that . One possible interpretation of the variable is that it represents the generic time-parameter of the system and the function represents the smearing kernel, so that the resultant solution is obtained by integration over all solutions for different time-parameters with the weight factor given by the smearing kernel.

After plugging in for and , we obtain the solution in the form

| (41) |

so the solution is given by the superposition of space-fractional-diffusion Green functions for different times . The smearing kernel obeys the differential equation

| (42) |

with an initial condition .

Riesz-Feller kernel: when we assume that the time-derivative operator is equal the Riesz fractional derivative this results in the expected property that for is Kleinert and Zatloukal (2013). We find that the Laplace image is equal to Zhang and Liu (2007):

| (43) |

with the initial condition , leading to the solution , which nothing else than the Laplace transform of the fully asymmetric stable distribution with stability parameter , asymmetry parameter equal to 1 and the support contained in . The function is not normalized, so according to Kleinert and Zatloukal (2013), we have

| (44) |

Thus, we end with

| (45) |

where is the -stable Lévy asymmetric distribution.

Caputo kernel: in case of Caputo fractional derivative , the Laplace transform of is equal to . According to Ref. Gorenflo et al. (1999), the inverse Laplace transform is equal to

| (46) |

where is the function of Wright type, which is defined by the infinite series

| (47) |

Interestingly, the connection of -function to asymmetric Lévy-distributions is provided by the relation

| (48) |

which is valid for , and . Hence, we can rewrite the Green function as

| (49) |

We compare the properties of both smearing kernels in Appendix A. Now let us turn attention to an alternative representation of the Green function, which is more computationally tractable and includes .

Representation of expectations: The composite representation can be also used in the case of calculating expectation values

| (50) |

Because the composition rule can also be formally used for , we can rewrite the previous expression as

| (51) |

where is the expectation value under Lévy-stable process in pseudo-time . This is important in the calculation of Risk-neutral measure by Esscher’s transform

| (52) |

V.2 Mellin-Barnes representation of double-fractional-diffusion Green function

It is possible to introduce an alternative, computationally effective representation of double-fractional diffusion equation which is based on the Mellin-Barnes Paris and Kaminski (2001) transform. This representation is also valid for the case . Let us again begin with equation (36). It has the solution equal to

| (53) |

where depends on the type of the derivative. For Riesz derivative is , for Caputo derivative we have . We shall note that because of computational reasons, we assume here only solutions for . The solution for negative values can be then easily obtained from the relation . Therefore, we formally leave undetermined, even if we assume only extremal cases, for which .

According to Diethelm (2010); Podlubny (1998), the inverse Laplace transform of Eq. (53) is equal to the Mittag-Leffler function

| (54) |

The Mittag-Leffler function can be represented through the Mellin integral transform which is defined as

| (55) |

and the inverse transform is defined as (for some given by the Mellin transform theorem Flajolet et al. (1995))

| (56) |

This representation can provide the Green function in a more tractable form which can be better exploited in numerical computations. The Mittag-Leffler function can be expressed as a complex integral

| (57) |

where . Plugging into the equation (54), we find that

| (58) |

Transforming the variable back to variable , we obtain

| (59) |

After change of variables and taking into account the normalization (44), which can be in both cases written as , we finally arrive at the normalized Green function

| (60) |

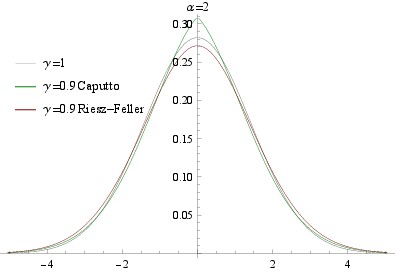

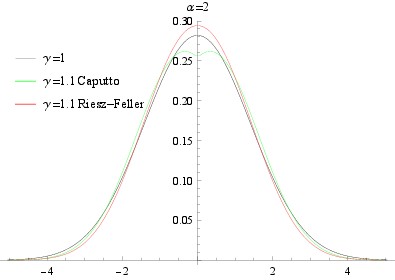

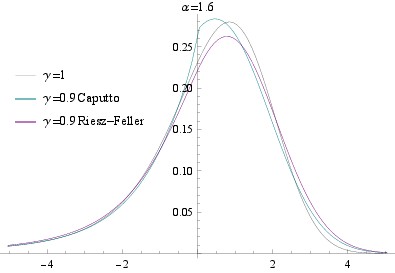

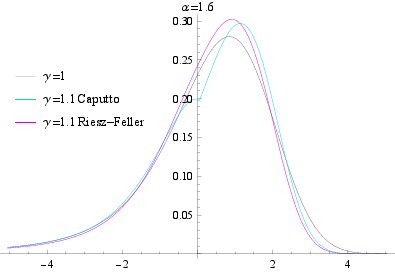

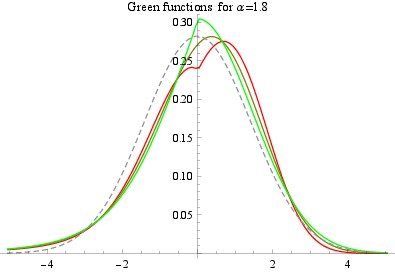

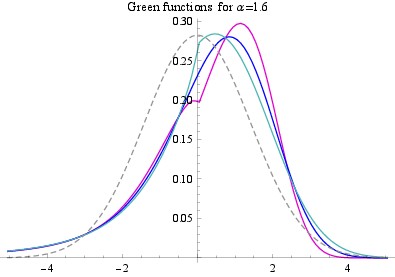

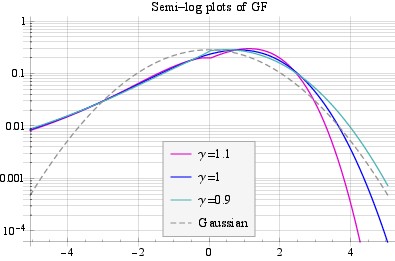

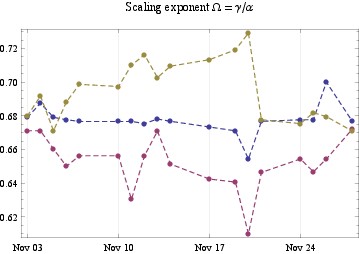

From Eq. (60) it is apparent that , so the Green function has the expected scaling with the temporal scaling exponent equal to . The ratio is called the diffusion scaling exponent. Differences between Riesz-Feller and Caputo Green functions for various values of and are displayed in Fig. 1.

VI Double-fractional Option Pricing Model

The solution of option-pricing equation driven by double-fractional diffusion under interest rate and dividend yield can be obtained by integrating over all scenarios , so it reads

| (61) |

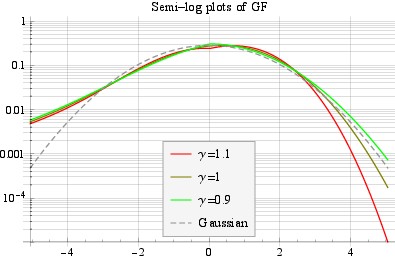

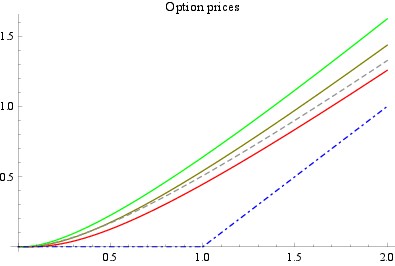

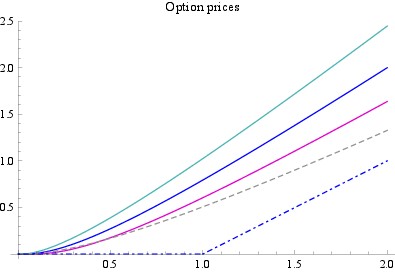

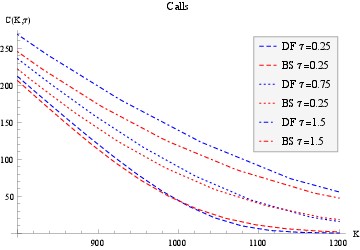

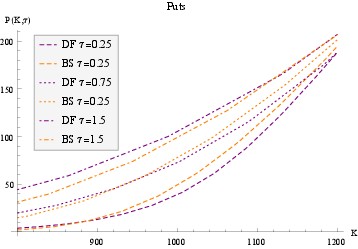

In Fig. 2 Green functions for different pairs and semi-log plots are displayed for better tail-behavior illustration. Option prices derived from Green functions are also presented. The corresponding put price can be obtained through put-call parity relation, which reads:

| (62) |

VI.1 Model calibration for S&P 500 options traded in November 2008

| All options | |||

|---|---|---|---|

| parameter | Black-Scholes | Lévy stable | Double-fractional |

| - | 1.493(0.028) | 1.503(0.037) | |

| - | - | 1.017(0.019) | |

| 0.1696(0.027) | 0.140(0.021) | 0.143(0.030) | |

| AE | 8240(638) | 6994(545) | 6931(553) |

| Call options | |||

| parameter | Black-Scholes | Lévy stable | Double-fractional |

| - | 1.563(0.041) | 1.585(0.038) | |

| - | - | 1.034(0.024) | |

| 0.140(0.021) | 0.118(0.026) | 0.137(0.020) | |

| AE | 3882(807) | 3610(812) | 3550(828) |

| Put options | |||

| parameter | Black-Scholes | Lévy stable | Double-fractional |

| - | 1.493(0.031) | 1.508(0.036) | |

| - | - | 1.047(0.017) | |

| 0.193(0.039) | 0.163(0.034) | 0.163(0.037) | |

| AE | 3741(711) | 3114(591) | 2968(594) |

We calibrate our model on the data of S&P 500 options that were traded during November 2008. The choice of this period is mainly because of the financial crisis, which brought about phenomena that are potentially interesting. We follow the methodology of Carr and Wu Carr and Wu (2003) and try to find such a triplet that minimizes the aggregated option price error

| (63) |

of all out-of-the money options, so

| (64) |

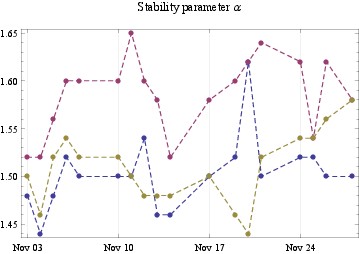

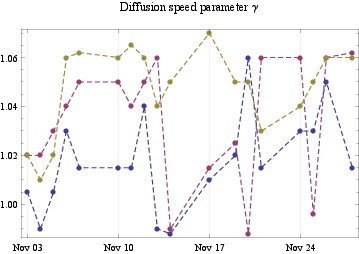

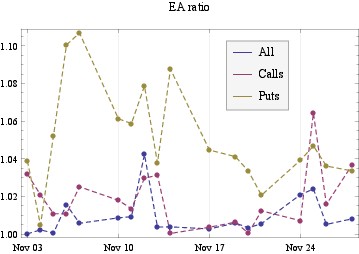

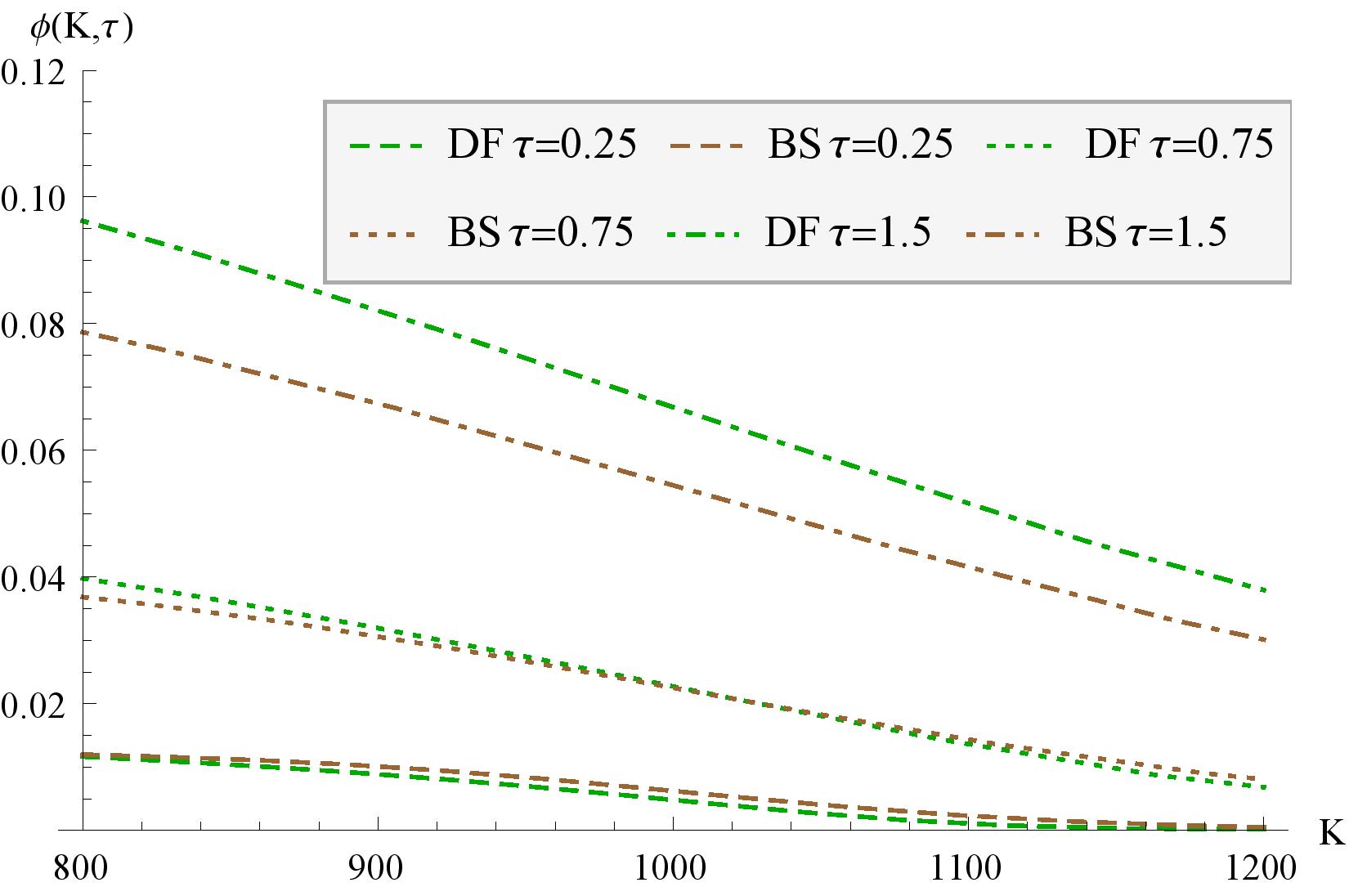

We make the optimization for each trading day. We have chosen the out-of-the-money options, because in-the-money option prices are more determined by the boundary conditions in option pricing formula, rather than by particular underlying diffusion model Carr and Wu (2003). The statistics of calibrated parameters is listed in Tab. 1 for the Black-scholes model, Lévy stable model and Double-fractional model. Because of the fact that was close to , the choice of derivative type did not have a large impact on the solutions and the results are practically the same, therefore the results are presented only for Caputo derivative, i.e., . The parameter is close to in all cases, only for call options it fluctuates around . The analysis shows that the double-fractional model brings more improvement when it is fitted separately for call and put options. This could be connected to the discussion about the general validity of put-call parity and market efficiency Brunetti and Torricelli (2005). Fig. 3 shows estimated parameters for every day and also the ratio between aggregated errors of Lévy stable model and Double-fractional model . Particularly for put options we can observe a noticeable improvement. Additionally, another interesting phenomenon connected with the decrease of parameter can be observed. In such a situation the parameter also decreases, even to values smaller than one, which could be interpreted as the risk redistribution from long-term options to short term options. The parameter , which is the ratio between parameters and , expresses the temporal scaling parameter of the system. This parameter produces more stable behavior, pointing to the simultaneous changes in both parameters and . The differences between option prices in the case of Double-fractional and Black-Scholes model are presented in Fig. 4. One can observe that the price differences are relatively small, even in some cases are Double-fractional prices below prices estimated by the Black-Scholes model. This is caused by the fact that the Double-fractional Green function redistributes the probability of particular scenarios. In cases, when the option execution is less probable than in case of Black-Scholes model, we obtain cheaper option price. Nevertheless, with increasing maturity time the Double-fractional prices become more expensive, but the difference is still not dramatic. We discuss the topic of risk redistribution and hedging in the next section.

VI.2 Risk Redistribution and Hedging Policy under Double-fractional Diffusion Model

We notice a few properties of option prices driven by double-fractional diffusion. Indeed, we recover classical BS model for and . When , the underlying return distribution is skewed and we have polynomial decay for the negative tail of the distribution. This results in an adjustment of the option price. A greater probability of fall of the underlying asset price results in an increase of option price for 111 is the forward price, i.e., ., and options, for which , become cheaper (both puts and calls). Similarly, the parameter plays analogous role in temporal risk redistribution. For , options with short expiration period become more expensive, while options with long expiration period become slightly cheaper. This behavior can be observed in situations when we face some kind of unexpected or sudden change of regime, such as a black day on the market, the bankruptcy of a company trading on the market, a natural disaster, etc. Indeed, for options with long expiration long-term equilibrium volatility is more important. Nevertheless, for options with short expiration such jumps and short-term uncertainty are the most important factors for price estimation. On the other hand, for , the diffusion is faster than in case of space-fractional diffusion, and the options with long maturity time. We should note that the change of parameters or does not change all option prices in the same direction; there are always options which become cheaper and more expensive. This essential role is played by the parameter , which is the volatility of the system.

The options are usually used for hedging the risk coming from the random nature of price evolution in financial markets. In the simplest case, with one underlying asset and one option, we use the -hedging strategy Aurell et al. (1997). We create a portfolio of an option

| (65) |

where is the amount of stocks used to hedge the short position. There exist several risk measures. Nevertheless, we work with the most popular risk measure defined as variance of portfolio between times and

| (66) |

The advantage of using this risk measure is that the optimal policy is easily expressible. The minimal risk is therefore determined by

| (67) |

In Ref. Busca et al. (2014) it was shown that the optimal hedging policy is given by

| (68) |

where is volatility of stock . For Black-Scholes model we obtain the well-known -hedging rule

| (69) |

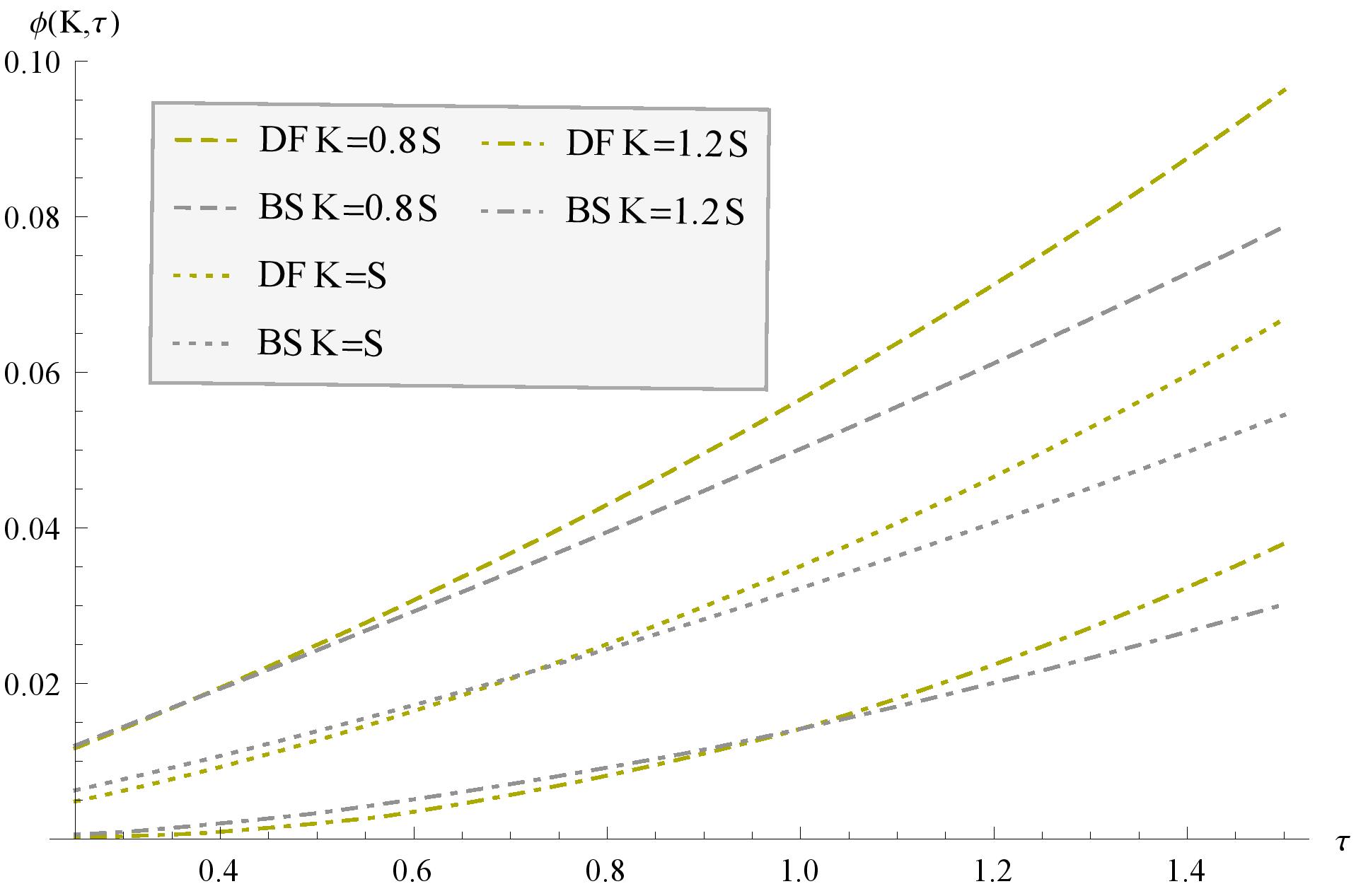

The difference in optimal policies of Black-Scholes model (-hedging) and Double fractional model is shown in Fig. 4. Due to the risk-redistribution, the resulting policies are also changed in order to minimize the risk in the environment with double-fractional diffusion. As with the prices, the risk is, in the case of changing parameter , redistributed in the spatial axis (prices) and in the case of parameter in the temporal axis (time to maturity).

Bottom: Optimal policies obtained from estimated parameters as functions of , resp. for Double-fractional model and Black-Scholes -hedging.

VII Conclusions and Perspectives

A novel method of option pricing was proposed on the basis of fully asymmetric Double-fractional diffusion and a special example was calibrated for S&P 500 options traded in November 2008. The presence of power-law behavior in prices has been discussed before in case of cotton prices Mandelbrot (1963) and options Carr and Wu (2003); Tankov (2003). There have been various alternative attempts to reduce the risks in portfolios. Examples are provided by models based on regime switching Calvet and Fisher (2008), stochastic volatility Heston (1993), jump processes Tankov (2003), etc. Alternatively, it is possible to redistribute the risk by a temporally-fractional derivative, which, similar to spatial asymmetry, redistributes the risk to either the short-period options or long-term options. Such model enables one to treat the short-term differently; instant risk coming from contemporary fluctuations, jump corrections, etc., is treated differently from the long-term risk, which is determined by the slow volatility of the system. This also influences the optimal hedging policy.

While the long-term average behavior of markets tends to be similar in systems driven by ordinary, first time-derivative diffusion (i.e., diffusion speed parameter equal to one), an adjustment of diffusion speed parameter to values can often describe the system better. Such fact coheres with the complex nature of financial markets and particularly option trading. Further investigations of the topic and its interrelation to other models will be the subject of future research. Connection with regime switching models or interpretation of parameter as a “regime-switching” time-dependent parameter and the conjunction with other models are questions of high importance and can possibly reveal additional potential of models based on double-fractional diffusion.

Acknowledgements

Authors want to thank to Petr Jizba and Václav Zatloukal for valuable discussions and Dunstan Clarke for corrections. J. K. acknowledges support from GAČR, Grant no. P402/12/J077 and Grant no. GA14-07983S.

References

- Black and Scholes (1973) F. Black and M. S. Scholes, Journal of Political Economy 81, 637 (1973).

- Acharya and Richardson (2009) V. V. Acharya and M. Richardson, Critical Review 21, 195 (2009).

- Merrouche and Nier (2010) O. Merrouche and E. Nier, What Caused the Global Financial Crisis?: Evidence on the Drivers of Financial Imbalances 1999-2007, Tech. Rep. (International Monetary Fund, 2010).

- Colander et al. (2009) D. Colander, H. F llmer, A. Haas, M. Goldberg, K. Juselius, A. Kirman, T. Lux, and B. Sloth, The Financial Crisis and the Systemic Failure of Academic Economics, WorkingPaper (Department of Economics, University of Copenhagen, 2009).

- Taleb (2010) N. Taleb, The Black Swan: The Impact of the Highly Improbable Fragility (Random House Publishing Group, 2010).

- Carr and Wu (2003) P. Carr and L. Wu, Journal of Finance 58, 753 (2003).

- Kleinert (2002) H. Kleinert, Physica A: Statistical Mechanics and its Applications 312, 217 (2002), (http://arxiv.org/abs/cond-mat/0202311).

- Calvet and Fisher (2008) L. Calvet and A. Fisher, Multifractal Volatility: Theory, Forecasting, and Pricing, Academic Press Advanced Finance (Elsevier Science, 2008).

- Tankov (2003) P. Tankov, Financial Modelling with Jump Processes, Chapman & Hall/CRC Financial Mathematics Series (Taylor & Francis, 2003).

- Jizba and Arimitsu (2004) P. Jizba and T. Arimitsu, Annals of Physics 312, 17 (2004).

- Kleinert (2013) H. Kleinert, Foundations of Physics , 1 (2013), (http://klnrt.de/409).

- Lee and Yao (2004) C.-Y. Lee and X. Yao, Evolutionary Computation, IEEE Transactions on 8, 1 (2004).

- Turcotte et al. (2002) D. Turcotte, J. Rundle, H. Frauenfelder, and N. Sciences, Self-organized Complexity in the Physical, Biological, and Social Sciences, Arthur M. Sackler Colloquia of the National Academy of Sciences (National Academy of Sciences, 2002).

- Gnedenko and Kolmogorov (1968) B. Gnedenko and A. Kolmogorov, Limit Distributions for Sums of Intependent Random Variables, edited by K. L. Chung (Adison-Wesley, 1968).

- Kleinert (2009) H. Kleinert, Path Integrals in Quantum Mechanics, Statistics, Polymer Physics and Financial Markets, 4th edn (World Scientific, 2009) (http://klnrt.de/b5).

- Zolotarev (1986) V. Zolotarev, One-dimensional Stable Distributions, Translations of mathematical monographs (American Mathematical Society, 1986).

- Sato (1999) K.-I. Sato, Lévy Processes and Infinitely Divisible Distributions, Cambridge Studies in Advanced Mathematics (Cambridge University Press, 1999).

- Samoradnitsky and Taqqu (1994) G. Samoradnitsky and S. Taqqu, Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance, Stochastic Modeling Series (Taylor & Francis, 1994).

- Podlubny (1998) I. Podlubny, Fractional Differential Equations, Volume 198: An Introduction to Fractional Derivatives, Fractional Differential Equations, to Methods of Their … (Mathematics in Science and Engineering), 1st ed. (Academic Press, 1998).

- Abdeljawad (2011) T. Abdeljawad, Comput. Math. Appl. 62, 1602 (2011).

- Samko et al. (1993) S. Samko, A. Kilbas, and O. Marichev, Fractional Integrals and Derivatives: Theory and Applications (Gordon and Breach Science Publishers, 1993).

- Gerber et al. (1993) H. Gerber, E. Shiu, et al., Option Pricing by Esscher Transforms, Cahier / Institut de sciences actuarielles (HEC Ecole des hautes études commerciales, 1993).

- Mantegna and Stanley (2000) R. N. Mantegna and H. E. Stanley, An introduction to econophysics: correlations and complexity in finance, Vol. 9 (Cambridge university press Cambridge, 2000).

- Mandelbrot and Van Ness (1968) B. B. Mandelbrot and J. W. Van Ness, SIAM review 10, 422 (1968).

- Heston (1993) S. L. Heston, The Review of Financial Studies 6, 327 (1993).

- Necula (2008) C. Necula, Option Pricing in a Fractional Brownian Motion Environment, Advances in Economic and Financial Research - DOFIN Working Paper Series 2 (Bucharest University of Economics, Center for Advanced Research in Finance and Banking - CARFIB, 2008).

- Jumarie (2010) G. Jumarie, Computers & Mathematics with Applications 59, 1142 (2010).

- Song and Wang (2013) L. Song and W. Wang, Abstract and Applied Analysis 2013 (2013).

- Wyss (2000) W. Wyss, Fractional Calculus & Applied Analysis 3 (2000).

- Hu et al. (2003) Y. Hu, B. ØKsendal, and A. Sulem, Infinite Dimensional Analysis, Quantum Probability and Related Topics 06, 519 (2003).

- Pagnini (2013) G. Pagnini, Fractional Calculus and Applied Analysis 16, 436 (2013).

- Kleinert and Zatloukal (2013) H. Kleinert and V. Zatloukal, Phys. Rev. E 88, 052106 (2013), (http://klnrt.de/407).

- Zhang and Liu (2007) H. Zhang and F. Liu, Numerical Mathematics, A Journal of Chinese Universities 16, 181 (2007).

- Gorenflo et al. (1999) R. Gorenflo, Y. Luchko, and F. Mainardi, Fractional Calculus and Applied Analysis 2, 383 (1999).

- Paris and Kaminski (2001) R. Paris and D. Kaminski, Asymptotics and Mellin-Barnes Integrals, Encyclopedia of Mathematics and its Applications (Cambridge University Press, 2001).

- Diethelm (2010) K. Diethelm, The analysis of fractional differential equations an application-oriented exposition using differential operators of Caputo type (Springer-Verlag, Heidelberg New York, 2010).

- Flajolet et al. (1995) P. Flajolet, X. Gourdon, P. Dumas, D. T. D. Knuth, N. G. D. Bruijn, and H. Mellin, Theoretical Computer Science 144, 3 (1995).

- Brunetti and Torricelli (2005) M. Brunetti and C. Torricelli, International Review of Financial Analysis 14, 508 (2005).

- Note (1) is the forward price, i.e., .

- Aurell et al. (1997) E. Aurell, J. Bouchard, M. Potters, and K. Żyzkowski, “Option pricing and hedging beyond black-scholes,” (1997).

- Busca et al. (2014) G. Busca, E. Haven, F. Jovanovic, and C. Schinckus, Theoretical Economics Letters 4, 760 (2014).

- Mandelbrot (1963) B. B. Mandelbrot, The Journal of Business 36 (1963).

- Skorohod (1961) A. Skorohod, Select. Transl. Math. Statist. and Probability 1, 157 (1961).

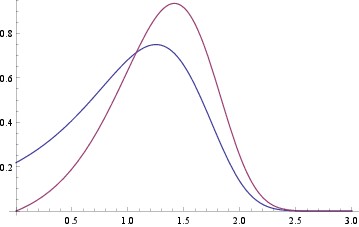

Appendix A Comparison of Smearing Kernels for Riesz-Feller and Caputo Derivatives

In this appendix, we compare Green function of Double-fractional diffusion in case when time derivative is equal to Riesz-Feller derivative and Caputo derivative and . The Green function is given by

| (70) |

where is different according to used derivative, so

| (71) |

Indeed, it is interesting to see, what happens with the smearing kernel

| (72) |

for small and large values. Firstly, when , then the argument of -stable distribution distribution goes to infinity. According to Ref. Skorohod (1961), the asymptotic expansion gives us

| (73) |

which gives us

| (74) |

For Caputo case we get non-zero value of smearing kernel for . Particularly, it is equal to

| (75) |

On the other hand, when , then it is necessary to use the Taylor expansion of , and again from Skorohod (1961) we obtain

| (76) |

where and resp. are -dependent constants. The asymptotic behavior can be therefore described as

| (77) |

and for Caputo case as

| (78) |

The -dependent constants , resp. can be determined from previous expressions. Therefore, in both cases we become exponential decay in . The graphs of both smearing kernels are depicted in Fig. 5.