Slide Statistics And Financial Returns

Abstract.

We present a new approach to financial returns based on an infinite family of statistics called slide statistics that we introduce. The evidence these statistics provide suggests that certain distributions such as the stable distributions are not good models for the financial returns from various securities or indexes like the SP and the Dow Jones. Formally, we associate with any finite subset of a metric space an infinite sequence of scale invariant numbers derived from a variant of differential entropy called the genial entropy. We give explicit formulas for and that are easily evaluated by a computer and make this theory particularly suitable for applications. As statistics for point processes, these numbers often appear to converge in simulations and we give examples where converges to the Hausdorff dimension and we prove that . For a uniform random variable on , the evidence from simulations suggests that and which yields new tests for spatial randomness. The slide statistics describe continuous random variables in an entirely new way. For example, if is any normal variable then simulations suggest that and which provides new goodness of fit tests for normality.

Key words and phrases:

financial mathematics, stochastic process, Hausdorff dimension,spatial statistics, fractal analysis, slide statistics, tangible process,1991 Mathematics Subject Classification:

Primary 91G70, Secondary 28A781. Introduction

We develop new entropy based statistics called slide statistics which can be computed from any sample data in a metric space. As an application, we use these statistics to test whether financial returns are independent observations from a particular distribution. For example, Figure 1 shows plots of against for data consisting of n-tuples of consecutive returns regarded as a subset of the metric space with the usual metric. As can be seen, the lower curve corresponding to the SP is very different from the ones obtained for either the Normal or Laplace distributions. Any potential model for the returns of the SP must be able simulate the curve in Figure 1 which is a new requirement that is apparently difficult to meet. The statistics contain information about the interplay between the dimension of a space and distributions on that space and provide a new way of describing continuous random variables and stochastic processes in general. The will take some time to define but we will provide explicit formulas for slide statistics and that are easily computed for any sample in a metric space.

Our applications will focus on financial returns but many other important processes in science and mathematics also yield data in the form of a set of points in a metric space that must be quantified and interpreted. Fields like fractal analysis have developed in order to obtain dimensional information from a wide range of real world data using quantities like the Hausdorff, information and correlation dimensions [9, 11]. One of the problems with these traditional measures of dimension is that they tend to concentrate on the geometric properties of a set while ignoring the statistical origins of the data. We will give examples where appears to converge to the reciprocal of the Hausdorff dimension when is taken to be a a larger and larger random sample from a fractal.

It is not clear in general how to assign a dimension to a point process but our theory and simulations suggest a purely statistical way to identify a class of them for which it does make sense to assign a dimension. Specifically, we think the dimension of a point process should be defined to be provided and for in which case we say the process is tangible with dimension . In the case of a tangible process, the values of are entirely determined by the number but this relationship does not hold in general. A possible example of a tangible process is the random generation of points in , where the are chosen independently and uniformly at random from , for which we provide evidence that and . In particular, and are new spatial statistics for testing hypotheses concerning the distribution of points in .

Although we will sometimes use fractals as examples, these statistics can be applied to any random variable with values in a metric space. In particular, the slide statistics appear to describe continuous random variables in an entirely new way that has nothing to do with mean and standard deviation since for . For example, the first two slide statistics for any normal variable appear to converge to and which provide the basis for a new goodness of fit test for normality. For any exponential random variable , simulation gives that and and we conjecture from these and other simulations that for any continuous real-valued random variable . If we think of as the dimension of the random variable , then this last conjecture says the uniform distribution on has the maximum dimension of any continuous real-valued random variable. The second slide statistic is negative for the examples given so far but is positive for the Cauchy distribution and is often found to be positive for the log daily returns of the Standard and Poor 500 Index which is yet another demonstration of the non-normality of these returns.

The construction of requires several ideas working in concert and can be summarized as follows. In Section 2, we introduce a variant of the differential entropy called the genial entropy which is the starting point for defining the slide statistics. Unlike the differential entropy, the genial entropy is scale invariant and in Section 3 we prove it is never negative which will give a new lower bound for the differential entropy. Given a finite set of distinct points in a metric space, we find the distance from each point to its nearest neighbour and arrange these distances in descending order so . Let be the function on whose value on is . Let be the area under and let denote the genial entropy of the density which turns out to be at . We then define to be the th derivative from the right at of the function which is developed in Section 4.

In Section 4, we derive an explicit formula for and state a conjectured formula for . The fact that and are easily evaluated using a computer makes them particularly suitable for practical applications. The results obtained from the simulation of and in a variety of contexts are summarized in Section 5 and demonstrate the interplay between dimension and distribution that is captured by these statistics. As applications in Section 6, we consider a variety of possible distributions as models for financial returns and use the slide statistics to illustrate how poorly these models fit the empirical data.

2. The genial Entropy

Our starting point for the development of the slide statistics is the differential entropy of a density which is well known in statistics and information theory [7]. Our focus will be on a variant of the differential entropy called the genial entropy or g-entropy which will be described in Definition 2. In the simplest case of a probability density that has an inverse function such as on , the genial entropy is just the sum of the differential entropies of and . The next proposition shows how this sum can be written in a form that makes sense for densities that may not have inverses.

Proposition 1.

Suppose is a continuous function on with the properties that the derivative of exists and is negative on , and . Also assume the differential entropies of and both exist. Then the sum of their differential entropies is given by .

Proof.

Substitute into the integral to get which equals . After integrating by parts this last integral becomes and the result follows. ∎

The genial entropy will only be defined for densities of the following special form.

Definition 1.

A corner density is a function where is a connected interval contained in , is monotone decreasing and .

Here is our definition of genial entropy which is motivated by the conclusion of Proposition 1.

Definition 2.

Let be a corner density. The genial entropy or g-entropy of is defined by when this integral exists, with the usual convention that .

If satisfies the conditions of Proposition 1, then so in particular and must have the same genial entropy which happens to be Euler’s constant as shown in Table 1. In Section 3, we will prove the genial entropy is always nonnegative.

The genial entropy of some corner densities.

| Density | Domain | Genial Entropy |

|---|---|---|

| for | ||

Unlike the differential entropy, the genial entropy is invariant under changes of scale.

Proposition 2.

Let be any corner density. Then for any the function defined by for is a corner density with the same genial entropy as .

Proof.

. After substituting , this last integral becomes . ∎

In Section 5, we will consider data consisting of a finite set of distinct points in a metric space. The first steps in computing the slide statistics will be to find the distances from each point to its nearest neighbour, arrange them in decreasing order and use them to construct the corner density discussed in the next definition and theorem.

Definition 3.

Let be any sequence with and let be the sequence where is the mean of the .

-

(1)

Define to have the value on the interval . In particular, is the corner density whose value on is .

-

(2)

Define by where is the number of elements of that are less than or equal to . In other words, is the restriction of the empirical cumulative distribution function for the data in to the interval .

The next theorem shows that the genial entropy of can be computed using the empirical cumulative distribution function.

Theorem 1.

Let be any sequence with . Then and are corner densities with the same genial entropy.

Proof.

The sequence may contain repetitions, so assume that the discontinuities of in occur at with and let and . Suppose the value of on is for and let so . We can then describe as the function that takes the value on for and the value on . Since , we must also have that . Rearranging this last sum gives so and is a corner density. To see that and have the same genial entropy, we use , and the convention to obtain:

| (1) |

∎

In view of Proposition 2, we could have defined on any interval and obtained a function with the same genial entropy. The interval was chosen in particular to insure the relationship between the genial entropies of and stated in part (2) of Theorem 1. We now show that the genial entropy is never negative.

3. The genial entropy Inequality

Our goal in this section is to prove that the genial entropy of a corner density can never be negative which we will use to prove that the first slide statistic . The idea is to first prove the necessary inequalities for step functions and then use the fact that monotone functions can be uniformly approximated by step functions. We begin with an inequality for step functions.

Lemma 1.

Suppose that and . Let . Then

Proof.

Given vectors , recall from [17] that majorizes provided

for all with equality for and where the components of and have been sorted in descending order so and . Alternatively, majorizes if vector can be obtained from vector by a sequence of ”transfers” that allow us to change a vector into a vector provided and .

We now show that the vector majorizes

so the required inequality follows immediately from Karamata’s Inequality [17] and the convexity of on . Since and , we can transfer an amount from the first to the last entry of which means that majorizes . Now transfer an amount from the first to the 2nd last entry of and continue similarly with the other entries to obtain the required majorization.

∎

Lemma 2.

Suppose that and . Let be the function whose value is on and let and . Then

Proof.

Let be the constant function whose value is on where . Then with the usual convention that in the case when . Then , after applying Lemma 1 with .

∎

Lemma 3.

Let be a positive monotone decreasing function on where . Let and . Then .

Proof.

Lemma 4.

Let be a positive monotone decreasing function on for which is finite. Then .

Proof.

Suppose is between and and let , . Since is finite, . By Lemma 3, and the result follows by taking the limit as on both sides of this inequality. ∎

Lemma 5.

Let be a positive monotone decreasing function on for which is finite. Then .

Proof.

Let for ,. By Lemma 4, and the result follows by taking the limit as on both sides of this inequality. ∎

Theorem 2.

(The Genial Entropy Inequality) For any corner density , .

Proof.

Follows from Lemma 5 by taking . ∎

If the density function of a random variable happens to be a corner density, then the Genial Entropy Inequality gives a new lower bound for the differential entropy.

Theorem 3.

Let be a random variable whose pdf is a corner density and let be the differential entropy of . Then .

Proof.

Follows from Theorem 2. ∎

4. The Slide Derivatives

With each corner density, we now associate a function called a slide function that describes how the genial entropy changes as the density is deformed to a constant function. In Section 5, the slide numbers will be defined as the derivatives of a particular slide functions at .

Definition 4.

Suppose is monotone decreasing and .Then will be called the slide function of and its domain will be the set of all at which and both exist.

By the Genial Entropy Inequality in Theorem 2, we always have . Note also that and if then . The next theorem says that the function is invariant under changes of scale. It follows from a simple change of variables argument similar to the proof of Proposition 2.

Theorem 4.

Suppose is monotone decreasing and is defined by for some and any . Then .

We now show that under mild conditions there must be an for which the interval is contained in the domain of and furthermore that must be continuous from the right at .

Lemma 6.

Suppose is monotone decreasing with for some . Then is defined on and continuous from the right at .

Proof.

We can assume by Proposition 2. Then for , the function in Definition 4 is finite since . To see that , choose and with and consider . In this last sum, the first and third terms are independent of and can be made as small as desired by choosing and appropriately. Since converges uniformly to on as , the results follow.

We now show that is finite for and continuous from the right at as follows:

It remains to show that each of the three terms in this last sum is finite for and goes to as . For the first term, clearly

.

For the second term, converges since the integrand is the product of square integrable functions. To see that , choose and with and consider the inequality . Now follow the argument given above for .

For the third term, use the inequality for to get which converges since the last integrand is the product of square integrable functions. Now show as before.

∎

The information we wish to extract from a corner density is captured by the derivatives of its slide function at which we now describe.

Definition 5.

Suppose is monotone decreasing with for some . Then the ’th slide derivative of is defined by where all derivatives are taken from the right. If all of these derivatives exist, then the slide series of is defined to be .

Here are some elementary properties of .

Theorem 5.

Suppose is monotone decreasing with for some .

-

(1)

If exists then .

-

(2)

If exists then so does for and .

-

(3)

If is a constant function, then for all n.

Proof.

(1) The slide function is non-negative on its domain and so the first derivative must be nonnegative.

(2) For sufficiently small and nonnegative, we have and the result follows from the chain rule.

(3) If is a constant function, then for all .

∎

Here is an example of a slide derivative calculation that we will connect with the uniform distribution on in Section 5.

Theorem 6.

Let for . Then for , and the slide derivatives of are given by and by for .

Proof.

Let so . Then

| (2) |

The result now follows by differentiating from the right at . ∎

Corollary 1.

Let for and . Then and for . The slide series for is given by .

Example 1.

for the function on .

In order to apply the slide derivatives to samples in a metric space, we first find the distance from the ’th point to its nearest neighbour. These distances can be used to construct the function in Definition 3 and we can then compute the first slide derivative using the explicit formula provided in the next theorem.

Theorem 7.

Suppose where we assume and let be the function on whose value on the interval is as in Definition 3. Then the first slide derivative of is given by .

Proof.

By Definition 5, we have to calculate the right hand derivative of the slide function at so we first find an expression for . Let where so takes the value on where .

To find the derivative of , we now use the facts that and .

At , each is equal to so this derivative becomes

The terms are defined and calculated as follows. The term consists of the parts of this last expression that involve the isolated s.

is the sum of all of the terms containing .

is what remains after and are subtracted from .

∎

The following formula for the second slide derivative is motivated by calculations for small values of . In the next section, we will see that the results from simulations based on this formula agree with what we would expect from theoretical considerations.

Conjecture 1.

Suppose and let be the function on whose value on the interval is . Let , and . Then the second slide derivative of is given by

The next section define the slide numbers and illustrates their application to some standard point processes.

5. The Slide Numbers

Sample data often consists of a set of distinct points in a metric space. With the help of Definition 5, we can now associate with each of these samples an infinite family of new statistics called the slide numbers.

Definition 6.

Let M be a metric space and let be a set of k distinct points in . For each , let be the distance from to its nearest neighbour in . Define a sequence by ordering the in descending order as . As in Definition 3, let be the function on whose value on the interval is . Define the ’th slide number of by and define the slide series of to be .

Values of for various random variables are shown in Table 2 which shows the connection between and the Hausdorff dimension of , the Cantor set and the Sierpinski triangle. For certain point processes P, the statistics appear to converge as the sample size gets large. For example, for any normal random variable , the quantity appears to converge to in which case it makes sense to write . More generally we define for an arbitrary point process as follows.

Definition 7.

Let be a metric space and let be a sequence of distinct points in generated by some point process and let . If converges in probability as , then is defined to be the value of this limit. If all of the limits exist, then we define the slide series of the process to be . In the case where is a sample of a random variable , we will use the notation instead of .

The following proposition follows immediately from the definitions and shows that adjusting the mean or standard deviation of a random variable has no effect on .

Proposition 3.

If is a random variable, then for all real number and with .

Some evidence for the convergence of the slide statistics is given in Table 2 and Table 3. In these tables, the points in the Cantor set were generated using where the are either or with probability . Points in the Sierpinski triangle were generated using the Chaos Game [1]. The generation of all random numbers used in these simulations was based on the Mersenne Twister.

Simulated Values of for Various Random Variables

| Density | conjectured | |||

|---|---|---|---|---|

| uniform on | ||||

| normal | ||||

| exponential | ? | |||

| on | ? | |||

| uniform on | ||||

| uniform on | ||||

| uniform on | ||||

| bivariate normal | ? | |||

| Cantor | ||||

| Sierpinski |

Simulated Values of for Various Random Variables

| Density | conjectured | ||

| uniform on | |||

| normal | |||

| exponential | ? | ||

| on | ? | ||

| uniform on | |||

| uniform on | |||

| uniform on | |||

| bivariate normal | ? | ||

| Cantor | |||

| Sierpinski |

Consider the following thin outline for a possible argument to explain the empirical results obtained for in Table 2 and Table 3. Suppose is a very large sample of points in where the are chosen independently and uniformly at random from , and let be a particular point in . By [21], the probability that a point is within of is approximately for some . If the sample is large enough, then the set of nearest neighbour distances will be sufficiently independent [14, 18] that their empirical cumulative distribution will also be approximately equal to . If is the ordered sequence of nearest neighbour distances, then in Definition 3 will be approximately for some and will be approximately with inverse . Now has the same genial entropy as by Theorem 1 so Corollary 1 now suggests the following conjecture which is supported by the empirical results shown in Table 2 and Table 3.

Conjecture 2.

Let be a sequence of points in , where the are chosen independently and uniformly at random from and let . Then as , converges in probability to and converges in probability to for .

There appear to be cases other than for which the dimension equals and converges to . For example, if we take then which is close to the value shown in Table 3 for the Cantor set. A similar result holds for the Sierpinski triangle and prompts us to make the following definition.

Definition 8.

In the context of Definition 7, we say that a point process is tangible provided there is a number with and for . The number will be called the slide dimension of the process. If there is no such number, the process will be called intangible.

The values for and given in Table 2 and Table 3 suggest that the normal distribution does not satisfy the conditions for tangibility in Definition 8 so cannot be assigned a slide dimension. In the case of a tangible process, we can recover the dimension by rearranging the second derivative to obtain . This relationship is particularly useful for spatial statistics because it provides considerably better estimates for the dimension of than the values for shown in Table 2. For a tangible process , we would like to know in general if the statistics converge more quickly to the dimension for larger values of .

For the subset of generated by iterations of with , the value of is approximately . But values of less than cannot occur for continuous real-valued random variables according to the next conjecture which is supported by the results in Table 2.

Conjecture 3.

If is a continuous real-valued random variable for which exists, then .

If consists of the first primes, then the value of is approximately which is interesting in view of Conjecture 3.

The values of are all negative in Table 3 but appears to be positive when has a Cauchy distribution which raises the following question.

Question 1.

What conditions on a random variable determine the sign of when ?

6. Applications of the slide statistics to financial returns.

If the daily closing prices of an index or stock are and the daily returns are given by , then a central question of financial mathematics is the problem of describing the distribution of the returns . We now show that the slide statistics impose strict constraints that allow us to quickly reject many possible candidates for this return distribution. Our approach will be to fix a sample size and use the standard metric on to calculate and for the subset of given by . Note that by the same reasoning used in Proposition 3, the values of are not changed if we replace the by with . In other words, is detecting information about the returns that has nothing to do with their mean and standard deviation.

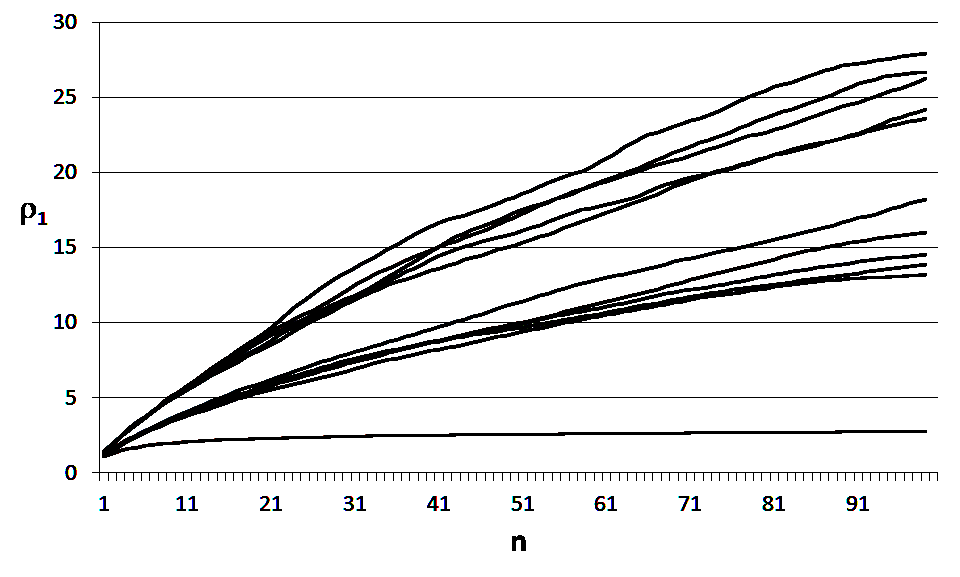

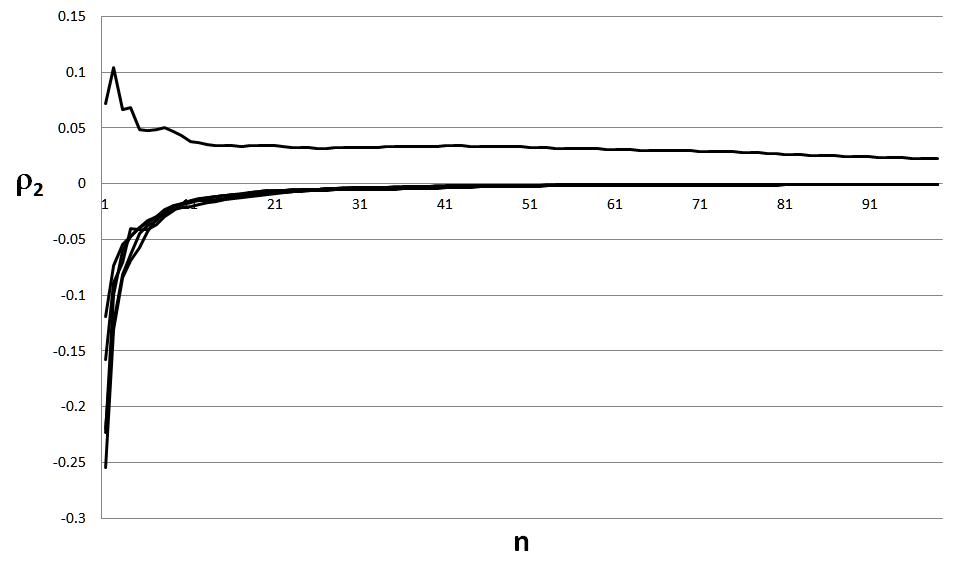

Figure 1 shows that the values of obtained for the SP are very different than the values obtained for either the Normal or Laplace distributions. The lowest of the curves shown in Figure 1 is the plot of against for the SP for the trading days ending December 31, 2014. The middle cluster of five curves are the corresponding plots obtained for five different simulated sequences of returns having the Laplace distribution. The upper cluster of five curves was obtained for the Normal distribution and we see that these curves are a bad fit to the curve for the SP . Any suggested model for the returns of the SP must be able to generate an approximation of this curve which places a tight constraint on potential stochastic processes. In Figure 2, the values of shown on the upper graph were obtained for the SP for the trading days ending December 31, 2014. For this particular time period, was positive but the values obtained for samples from Normal distributions are typically negative as shown by the graphs below the horizontal axis in Figure 2.

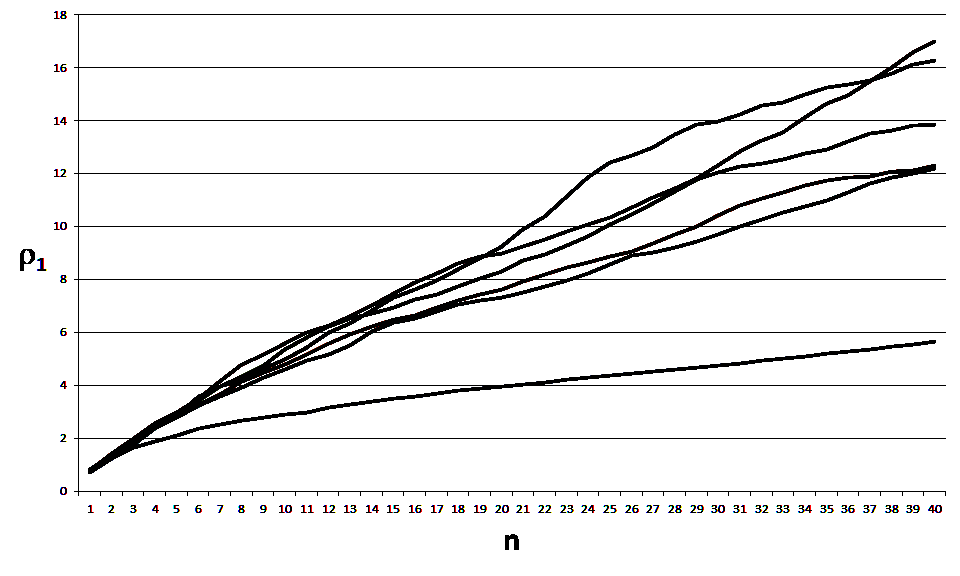

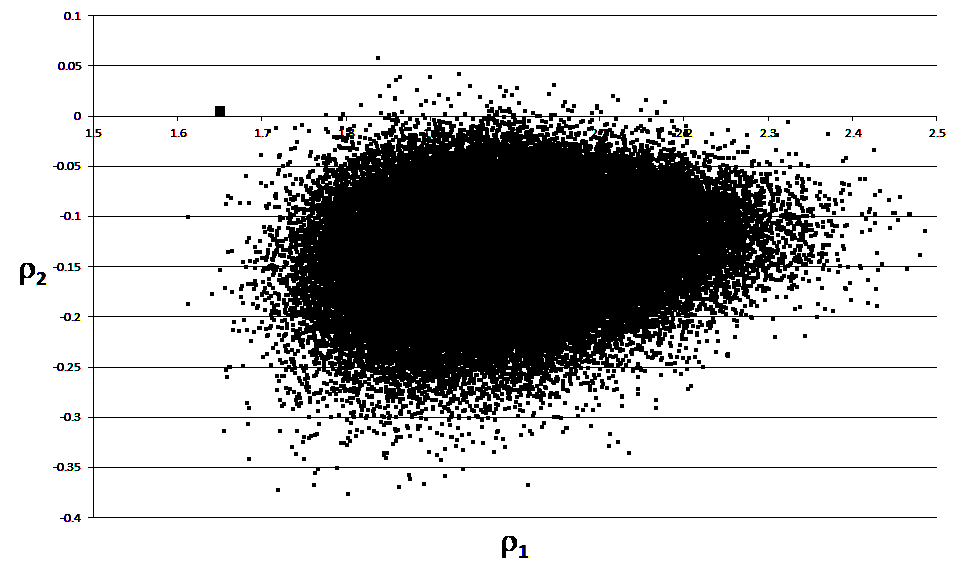

The failure of the daily returns to be normal might be due to dependencies in the consecutive daily returns and it is possible that we might obtain a better fit using the monthly returns instead. The bottom curve in Figure 2 shows plotted against for the monthly returns of the SP up to the end of . The group of five curves at the top of Figure 2 are the corresponding plots obtained for five different simulated sequences of returns having a Normal distribution. The fit is better than what we obtained for the daily returns but once again the normal curves are not a match for the curve for the SP which is consistent with the non-normality of such returns found in [5]. As another point of view on the non-normality of the monthly returns, Figure 3 shows the points plotted for samples from a normal distribution as well as the point obtained for the monthly returns of the SP up to the end of . The possibility of describing these monthly returns as a mixture of two Gaussians is considered in [5] but we find for their models but we sometimes find for the SP .

Values of and for Various Stocks and Indexes

| Name | ||

|---|---|---|

| Exxon | ||

| FTSE | ||

| IBM | ||

| 3M | ||

| NASDAQ | ||

| Russell | ||

| SP |

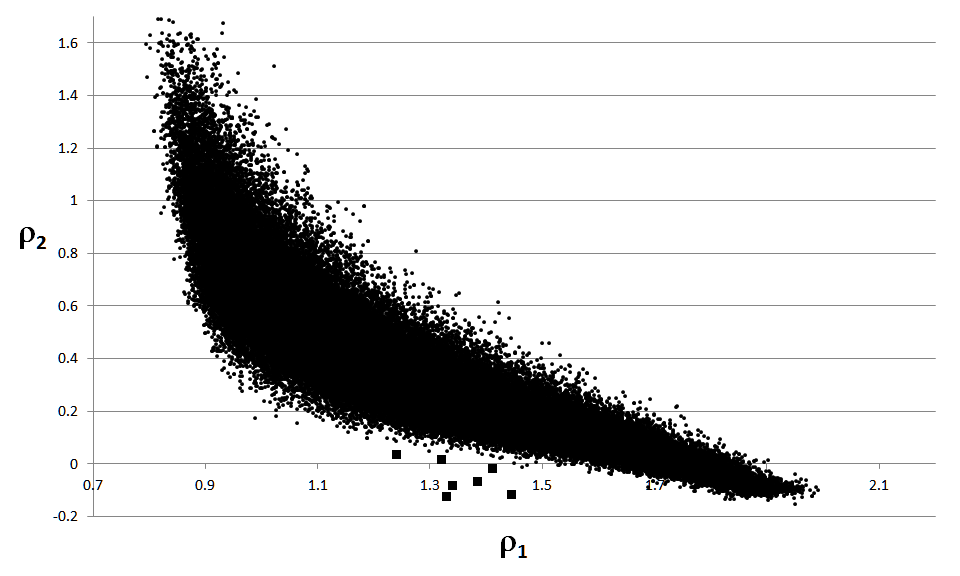

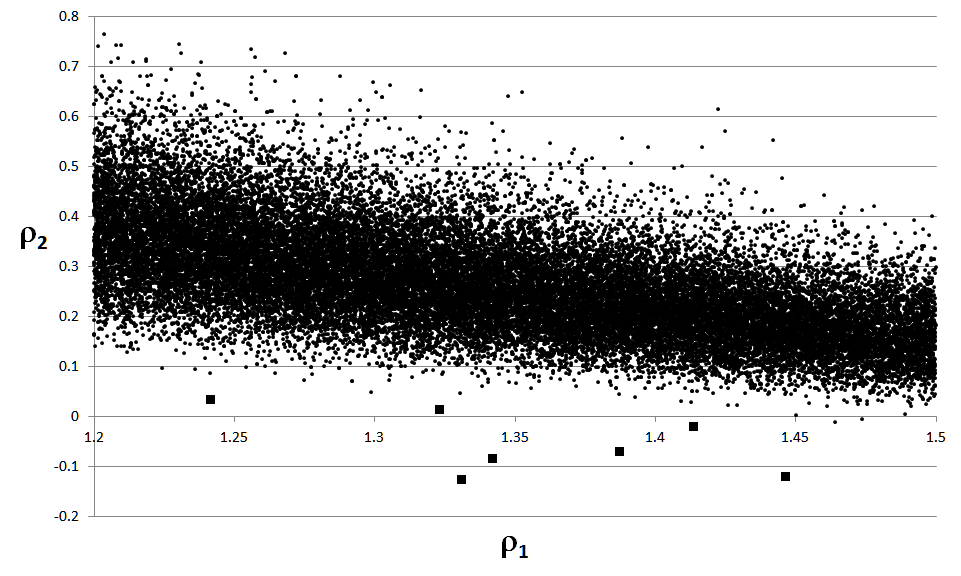

The stable distributions are often considered [19, 4, 12] as possible models for financial returns. We now consider the family of stable distributions described in [22] where is the stable parameter, is the skewness parameter, is the scale parameter and is the location parameter. By Proposition 3, the values of are not affected by changes in and so we will simply work with the family which we write as . Figure 5 shows the points from Table 4 plotted together with samples from stable distributions with parameters and chosen uniformly at random from the intervals and respectively. We see that the values in Table 4 lie outside the region corresponding to the stable distributions. Figure 6 show an expanded view of Figure 5 showing that the slide statistics for the financial returns in Table 4 are well outside the region corresponding to samples from stable distributions. This failure of the stable distributions to fit financial returns is consistent with the findings of [16, 4].

7. Conclusions and Future Work

As we have seen, the statistics and can be used as the basis for goodness of fit test for financial returns. Much more research needs to be done to better understand the role of the slide statistics in characterizing financial data. In particular, we would like to understand the relationship between the sign of and the behaviour of financial markets. The simulations we have described suggest that and can be used to distinguish between probability distributions and are capapble of detecting dimensional information. The values of we obtained through simulation point to a larger theory of these statistics which is currently being developed. At present however, the are quite mysterious and much work will need to be done to understand all they are telling us about sets of points in metric spaces, random variables or point processes in general.

We gave examples of point processes on the Cantor set and the Sierpinski triangle for which converged to the dimension of the fractal. We would like to understand when this occurs in general and also the relationship between and the usual definitions of dimension. More generally, we would like to know when a point process is tangible in the sense of Definition 8. When a process is tangible it is possible to use the expression as a statistic for estimating the dimension. We gave examples in which it converged to the dimension faster for than for and we would like to know what happens for larger values of .

In terms of calculations, we need to prove Conjecture 1 concerning the calculation of and we need formulas for for . Given the complexity of our conjecture for , the formulas for larger values of are likely to be very complicated. The convergence of the for real-valued random variables can sometimes be improved by using the distances between consecutive points rather than the distances to nearest neighbours. We would like to have a better understanding of this situation and also to know if there are any higher dimensional analogues.

In defining the slide statistics, we used the functions which can be thought of as a continuous deformation of at into the constant function at . We can achieve the same effect using the functions and calculate the derivatives corresponding to the slide derivatives in Section 4. It turns out that only the first of these statistics is interesting and while it is easier to calculate than it often doesn’t converge.

References

- [1] Barnsley, M., Fractals Everywhere, Academic Press, 1988.

- [2] Billingsley, P., Probability and Measure, John Wiley and Sons Ltd, 1995.

- [3] Bonetti, M., Forsberg, L., Ozonoff, A. and Pagano, M., The distribution of interpoint distances. Mathematical Modeling Applications in Homeland Security, HT Banks and C Castillo Chavez, Eds., 2003,87-106.

- [4] Belov,I., Kabašinskas,A.,Sakalauskas,L., A Study of Stable Models of Stock Markets, Information Technology and Control, 2006, Vol.35, No.1

- [5] Behr, A.,Pötter, U., Alternatives to the normal model of stock returns: Gaussian mixture, generalised logF and generalised hyperbolic models, Annals of Finance, 2009, 5:49–68

- [6] Chambers, J.M.,Mallows,C.L., Stuck,B.W., Method for Simulating Stable Random Variables, Journal of the American Statistical Association, 1976, Vol. 71, No. 354, pages 340-344

- [7] Cover, T.,Thomas, J. Elements of Information Theory, John Wiley and Sons, 2006.

- [8] Edgar, G., Measure, Topology, and Fractal Geometry, Springer-Verlag, 1990.

- [9] Falconer, K., Fractal Geometry: Mathematical Foundations and Applications, John Wiley and Sons, Ltd., 2003.

- [10] Grassberger, P. P., Procaccia, I., Measuring the strangeness of strange attractors, Physica, 9D, 1983, 189-208.

- [11] Harte, D., Multifractals, London: Chapman and Hall, 2001.

- [12] Haas,M.,Pigorsch,C., Financial Economics, Fat-Tailed Distributions, Complex Systems in Finance and Econometrics, 2011, pp 308-339

- [13] Kayll, M., Integrals Don’t Have Anything to Do with Discrete Math, Do They?, Mathematics Magazine 84(2);2011, 108-119

- [14] Kester, A., Asymptotic Normality of the Number of Small Sistances between Random Points in a Cube, Stoch. Proc. Appl. 3,1975, 45-54.

- [15] Klement, E. P., Mesiar, R., Pap, E., Quasi- and pseudo-inverses of monotone functions, and the construction of t-norms, Fuzzy Sets and Systems, 104, 1999, 3-13.

- [16] Lau,A., Lau,H., Wingender,J., The Distribution of Stock Returns: New Evidence against the Stable Model, Journal of Business and Economic Statistics, 1990, vol. 8, issue 2, pages 217-23

- [17] Marshall, A., Olkin, I., Inequalities: Theory of Majorization and Its Applications, Academic Press, 1980.

- [18] Shurygin, A., Using interpoint distances for pattern recognition, Pattern Recognition and Image Analysis,16(4),2006,726-729.

- [19] Simkowitz,M., and Beedles,W., Asymmetric Stable Distributed Security Returns, Journal of the American Statistical Association Vol. 75, No. 370 (Jun., 1980), pp. 306-312

- [20] Sohrab, H., Basic Real Analysis, Birkhauser Boston, 2003.

- [21] Stoyan, D., Kendall, W., Mecke, J., Stochastic Geometry and its Applications, John Wiley and Sons Ltd, 2008.

- [22] Weron, R., On the Chambers-Mallows-Stuck method for simulating skewed stable random variables, Statistics and Probability Letters 28 (1996) 165-1771