Time-varying nonlinear regression models: Nonparametric estimation and model selection

Abstract

This paper considers a general class of nonparametric time series regression models where the regression function can be time-dependent. We establish an asymptotic theory for estimates of the time-varying regression functions. For this general class of models, an important issue in practice is to address the necessity of modeling the regression function as nonlinear and time-varying. To tackle this, we propose an information criterion and prove its selection consistency property. The results are applied to the U.S. Treasury interest rate data.

doi:

10.1214/14-AOS1299keywords:

[class=AMS]keywords:

FLA

and C1Supported in part by NSF Grant DMS-14-61796. C2Supported in part by NSF Grants DMS-14-05410 and DMS-11-06790.

1 Introduction

Consider the time-varying regression model

| (1) |

where , and are the responses, the predictors and the errors, respectively, and is a time-varying regression function. Here is a smooth function, and , , represents the time rescaled to the unit interval. Model is very general. If is not time-varying, then (1) becomes

Model has been extensively studied in the literature; see Robinson (1983), Györfi et al. (1989), Fan and Yao (2003) and Li and Racine (2007), among others. As an important example, (1) can be viewed as the discretized version of the nonstationary diffusion process

| (2) |

where is a standard Brownian motion, and are, respectively, the drift and the volatility functions, which can both be time-varying, and is the time horizon under consideration. If the functions and do not depend on time, then (2) becomes the stationary diffusion process

| (3) |

which relates to model . There is a huge literature on modeling interest rates data by (3). For example, Vasicek (1977) considered model (3) with linear drift function and constant volatility , where are unknown parameters. Courtadon (1982), Cox, Ingersoll and Ross (1985) and Chan et al. (1992) considered nonconstant volatility functions. Aït-Sahalia (1996), Stanton (1997) and Liu and Wu (2010) studied model (3) with nonlinear drift functions. See Zhao (2008) for a review. However, due to policy and societal changes, those models with static relationship between responses and predictors may not be suitable. Here we shall study estimates of time-varying regression function for model (1).

For model , let be a -dimensional kernel function

| (4) |

where be a bandwidth sequence. We can then apply the traditional Nadaraya–Watson estimate for the regression function ,

| (5) |

If the process is stationary, then is the kernel density estimate of its marginal density. For stationary processes, an asymptotic theory for these nonparametric estimators has been developed by many researchers, including Robinson (1983), Castellana and Leadbetter (1986), Silverman (1986), Györfi et al. (1989), Yu (1993), Tjøstheim (1994), Wand and Jones (1995), Bosq (1996), Neumann (1998), Neumann and Kreiss (1998), Fan and Yao (2003) and Li and Racine (2007), among others. However, the case of nonstationary processes has been rarely touched. Hall, Müller and Wu (2006) considered the situation that the underlying distribution evolves with time and proposed a nonparametric time-dynamic density estimator. Assuming independence, they proved the consistency of their kernel-type estimators and applied the results to fast mode tracking. Following the spirit of Hall, Müller and Wu (2006), Vogt (2012) considered a kernel estimator of the time-varying regression model (1), and established its asymptotic normality and uniform bound under the classical strong mixing conditions. In Sections 3.1 and 3.2, we advance the nonparametric estimation theory for the time-varying regression model (1) under the framework of Draghicescu, Guillas and Wu (2009), which is convenient to use and often leads to optimal asymptotic results.

Apart from model , model contains another important special case: the time-varying coefficient linear regression model

where ⊤ is the transpose and for some smooth function . The traditional linear regression model

where is the regression coefficient, is a special case of model . Estimation of has been considered by Hoover et al. (1998), Fan and Zhang (2000a, 2000b), Huang, Wu and Zhou (2004), Ramsay and Silverman (2005), Cai (2007) and Zhou and Wu (2010), among others. The problem of distinguishing between models and has been studied in the literature mainly by means of hypothesis testings; see, for example, Chow (1960), Brown, Durbin and Evans (1975), Nabeya and Tanaka (1988), Leybourne and McCabe (1989), Nyblom (1989), Ploberger, Krämer and Kontrus (1989), Andrews (1993), Davis, Huang and Yao (1995), Lin and Teräsvirta (1999) and He, Teräsvirta and González (2009). On the other hand, model specifies a linear relationship upon model , and there is a huge literature on testing parametric forms of ; see Azzalini and Bowman (1993), González Manteiga and Cao (1993), Härdle and Mammen (1993), Zheng (1996), Dette (1999), Fan, Zhang and Zhang (2001), Zhang and Dette (2004) and Zhang and Wu (2011), among others. Nevertheless, model selection between models and received much less attention. Note that both of them are nested in the general model , and they all cover the linear regression model . It is desirable to develop a model selection criterion. An information criterion is proposed in Section 3.3, where its consistency property is obtained.

The rest of the paper is organized as follows. Section 2 introduces the model setting. Main results are stated in Section 3 and are proved in Section 6 with some of the proofs postponed to the supplementary material [Zhang and Wu (2015)]. A simulation study is given in Section 4 along with an application to the U.S. Treasury interest rate data.

2 Model setting

For estimation of model , temporal dynamics should be taken into consideration. Let be a temporal kernel function (kernel function for time), be another sequence of bandwidths and be the local linear weights, where , . Let ,

we consider the time-varying kernel regression estimator

| (7) |

Hall, Müller and Wu (2006) proved the uniform consistency of in (2) by assuming that are independent. To allow nonstationary and dependent observations, we assume

| (8) |

and , , are independent and identically distributed (i.i.d.) random vectors, and is a measurable function such that is well defined for each . Following Draghicescu, Guillas and Wu (2009), the framework (8) suggests locally strict stationarity and is convenient for asymptotic study. For the error process, we assume that

| (9) |

where is a smooth function, and is a sequence of random variables satisfying and . At the outset (cf. Sections 3.1–3.3) we assume that , , are i.i.d. and independent of , . The latter assumption can be relaxed (though technically much more tedious) to allow models with correlated errors and nonlinear autoregressive processes; see Section 3.4.

For a random vector , we write , if where is the Euclidean vector norm, and we denote . Let be the one-step ahead predictive or conditional distribution function and be the corresponding conditional density. Let be an i.i.d. copy of and be the coupled shift process. We define the predictive dependence measure

| (10) |

Quantity (10) measures the contribution of , the innovation at step 0, on the conditional or predictive distribution at step . We shall make the following assumptions: {longlist}[(A1)]

smoothness (third order continuous differentiability): ;

short-range dependence: , where ;

there exists a constant such that almost surely,

Condition (A3) implies that the marginal density .

3 Main results

3.1 Nonparametric kernel estimation

Throughout the paper, we assume that the kernel functions and are both symmetric and twice continuously differentiable on their support and , respectively, and . Denote by “” convergence in distribution. Theorem 3.1 provides the asymptotic normality of the time-varying kernel estimators (2) and (7), while Theorem 3.2 concerns the time-constant estimators (4) and (5).

Theorem 3.1.

Assume (A1)–(A3) and , are i.i.d. Let be a fixed point. If , and , then

| (11) |

where and . If in addition, then

| (12) |

Let be the Hessian matrix of the density function with respect to . Denote , and we use the same notation for the product function . Then for any point with , we have

where is the trace operator

and

Hence (2) and (7) are consistent estimates of the local density function and the regression function , respectively. The asymptotic mean squared error (AMSE) optimal bandwidths satisfy and . Here for positive sequences and , we write if is bounded for all large .

Theorem 3.2.

Assume (A1)–(A3) and , . If and , then

| (13) |

where . If in addition , then

| (14) |

where, letting , the variance function

For any point with , we have

and

Therefore, (4) and (5) provide consistent estimators of and ,(weighted) temporal averages of the local density function and the regression function , respectively. For stationary processes, Theorem 3.2 relates to traditional results on nonparametric kernel estimators; see, for example, Robinson (1983), Bosq (1996) and Wu (2005). The AMSE optimal bandwidth for the time-constant kernel estimators (4) and (5) satisfies .

3.2 Uniform bounds

For stationary or independent observations, uniform bounds for kernel estimators have been obtained by Peligrad (1992), Andrews (1995), Bosq (1996), Masry (1996), Fan and Yao (2003) and Hansen (2008), among others. Hall, Müller and Wu (2006) obtained a uniform bound for time-varying kernel density estimators for independent observations, while Vogt (2012) considered kernel regression estimators under strong mixing conditions. We shall here establish uniform bounds for the time-varying kernel estimators (2) and (7) under the locally strict stationarity framework (8). We need the following assumptions: {longlist}[(A4)]

there exists a such that and for some ;

let be a compact set, and assume .

Theorem 3.3.

Assume (A1), (A3)–(A5), , and . (i) If there exists such that and , then

(ii) If for some , and , then

If the bandwidths and have the optimal AMSE rate, and for some , then the bound in Theorem 3.3(ii) can be simplified to . Theorem 3.4 provides a uniform bound for (4) and (5).

Theorem 3.4.

Assume (A1), (A3)–(A5), and . (i) If there exists such that and , then

(ii) If for some , and , then

If the bandwidth is AMSE-optimal, and for some , then the bound in Theorem 3.4(ii) can be simplified to.

3.3 Model selection

Model is quite general in the sense that it does not impose any specific parametric form on the regression function and allows it to change over time. However, in practice it is useful to check whether model can be reduced to its simpler special cases, namely models –. Model selection between models and , or between models and , has been studied in the literature mainly by means of hypothesis testing; see references in Section 1. Nevertheless, less attention has been paid to distinguishing between models and . We shall here propose an information criterion that can consistently select the underlying true model among candidate models –. Let be a compact set and . We consider the restricted residual sum of squares for model , which takes the form

where is the indicator function. Similarly, we can define , and for models –, respectively. For the simple linear regression model , the parameter can be estimated by the least squares estimate

| (15) |

For the time-varying coefficient model , let , and we can use the kernel estimator of Priestley and Chao (1972),

| (16) |

For a candidate model , we define the generalized information criterion

| (17) |

where is a tuning parameter indicating the amount of penalization and represents the model complexity for model determined as follows. For the simple linear regression model , following the convention we set the model complexity or degree of freedom to be the number of potential predictors, namely . For the time-varying coefficient model , the effective number of parameters used in kernel smoothing is for each one of the predictors [see, e.g., Hurvich, Simonoff and Tsai (1998)], and thus we set . Let , , be the componentwise interquartile ranges of , and motivated by the same spirit as in Hurvich, Simonoff and Tsai (1998), we set and , where for random variables having a uniform distribution on . The final model is selected by minimizing the information criterion (17). We shall make the following assumption: {longlist}[(A6)]

eigenvalues of are bounded away from zero and infinity on .

In order to establish the selection consistency of (17), in addition to the results developed in Sections 3.1 and 3.2 regarding models and , we need the following conditions on estimators (15) and (16) for models and , respectively: {longlist}[(P1)]

There exists a nonrandom sequence such that . If model is correctly specified, then can be replaced by the true value .

There exists a sequence of nonrandom functions such that

where . If model is correctly specified, then can be replaced by the true coefficient function and

where , .

Remark 3.1.

Conditions (P1) and (P2) can be verified for locally stationary processes with short-range dependence. For example, for the linear regression model , by Lemma 5.1 of Zhang and Wu (2012), we have and . Hence we can use

which equals to if , . This verifies condition (P1). For the time-varying coefficient model , by Lemma 5.3 of Zhang and Wu (2012), we have and . Hence we can use

and condition (P2) follows by the proof of Theorem 3 in Zhou and Wu (2010).

Recall that the AMSE optimal bandwidths satisfy and for model , for model and for model . Theorem 3.5 provides the selection consistency of the information criterion (17), where the true model is denoted by .

Theorem 3.5.

Assume (A1), (A3)–(A6) with , (P1), (P2), for some , , and bandwidths with optimal AMSE rates are used for models –. If

then for any and , we have

3.4 Extensions

Recall that in Theorems 3.1–3.5 error process (9) has i.i.d. , which are also independent of . In Section 3.4.1 we allow serially correlated . Section 3.4.2 concerns time-varying autoregressive processes in which and are naturally dependent.

3.4.1 Models with serially correlated errors

To allow errors with serial correlation, similarly to (8) we assume that

| (18) |

where with , , being i.i.d. random variables and independent of , . Therefore, is a dependent nonstationary process that is independent of , and the error process can exhibit both serial correlation and heteroscedasticity; see Robinson (1983), Orbe, Ferreira and Rodriguez-Poo (2005, 2006) and references therein for similar error structures. Let , be i.i.d. and . Assume , and define the functional dependence measure

The following theorem states that the results presented in Sections 3.1–3.3 will continue to hold (except for a difference of on the uniform bounds) if the process in (18) satisfies the geometric moment contraction (GMC) condition [Shao and Wu (2007)]. The proof is available in the supplementary material [Zhang and Wu (2015)].

3.4.2 Time-varying nonlinear autoregressive models

In this section we shall consider the autoregressive version of (1),

| (19) | |||

| (20) |

where are i.i.d. random variables with and . We can view (3.4.2) as a time-varying or locally stationary autoregressive process, and the corresponding shift processes and . We shall here present analogous versions of Theorems 3.1–3.5. Note that in this case cannot be written in the form of (8). However, Proposition 3.1 implies that it can be well approximated by a process in the form of (8). For each , we define the process by

Lemma 3.1.

Assume that there exist constants with, such that, for all and ,

| (22) | |||

Then (i) the recursion (3.4.2) has a stationary solution of the form which satisfies the geometric moment contraction (GMC) property: for some ,

(ii) If in (3.4.2) the initial values , then can be written in the form , where is a measurable function, and it also satisfies the GMC property

| (23) |

Lemma 3.1(i) concerns the stationarity of the process , which follows from Theorem 5.1 of Shao and Wu (2007). For (ii), denote by the left-hand side of (23). Then by (3.1), satisfies , implying (23) via recursion.

For presentational simplicity suppose we observe from model (3.4.2) with the initial values . Estimates (2) and (7) can be computed in the same way. Proposition 3.1 implies that, for such that , the process can be approximated by the stationary process , thus suggesting local strictly stationarity. The proof is available in the supplementary material [Zhang and Wu (2015)].

Proposition 3.1.

4 Numerical implementation

4.1 Bandwidth and tuning parameter selection

Selecting bandwidths that optimize the performance of (17) can be quite nontrivial, and in our case, it is further complicated by the presence of dependence and nonstationarity. Assuming independence, the problem of bandwidth selection has been considered for model by Härdle and Marron (1985), Härdle, Hall and Marron (1988), Park and Marron (1990), Ruppert, Sheather and Wand (1995), Wand and Jones (1995), Xia (1998) and Gao and Gijbels (2008), among others. Hoover et al. (1998), Fan and Zhang (2000a) and Ramsay and Silverman (2005) considered the problem for model for longitudinal data, where multiple independent realizations are available. For the time-varying kernel density estimator (2) with independent observations, Hall, Müller and Wu (2006) coupled the selection of spatial and temporal bandwidths and adopted the least squares cross validation [Silverman (1986)]. Nevertheless, bandwidths selectors derived under independence can break down for dependent data [Wang (1998) and Opsomer, Wang and Yang (2001)]. We propose using the AMSE optimal bandwidths and for model , for model and for model , where are constants. Due to the presence of both dependence and nonstationarity, estimation of these constants is difficult. Throughout this section, as a rule of thumb, we use and . Our numerical examples suggest that these simple choices have a reasonably good performance.

We shall here discuss the choice of the tuning parameter that controls the amount of penalization on models complexities. The problem has been extensively studied for the linear model by Akaike (1973), Mallows (1973), Schwarz (1978), Shao (1997) and Yang (2005) among others. For the generalized information criterion (17), given conditions in Theorem 3.5, one can choose , where is a constant, which satisfies all the required conditions and thus guarantees the selection consistency. Note that the choice of does not affect the asymptotic result, namely the proposed method will select the true model for any given as long as the sample size is large enough; see Theorem 3.5. Therefore, one can simply use to devise a consistent model selection procedure. As an alternative, following Fan and Li (2001) and Tibshirani and Tibshirani (2009), we shall here consider a data-driven selector based on the -fold cross-validation (CV). In particular, we first split the data into parts, denoted by , then for each , we remove the th part from the data and use the information criterion (17) to select the model, based on which predictions can be made for the removed part and are denoted by , . The selected value is obtained by minimizing the cross-validation criterion

It can be seen from the simulation results in Section 4.2 that this CV-based tuning parameter selector performs reasonably well.

4.2 Simulation results

We shall in this section carry out a simulation study to examine the finite-sample performance of the generalized information criterion (17). Let and , and , be i.i.d. standard normal, , and , , . For the regressor and error processes with and , , we consider model (1) with the following four specifications: {longlist}[(a)]

and ;

and ;

and ;

and , where is a constant indicating the noise level. Cases (a)–(d) correspond to models –, respectively, and their signal-to-noise ratios (SNRs) are roughly of the same order given the same . The Epanechnikov kernel , , is used hereafter for both the spatial and temporal kernel functions. Let and . The tuning parameter is selected by using the tenfold CV-based method described in Section 4.1. The results are summarized in Table 1 for different noise levels and sample sizes , . For each configuration, the results are based on 1000 simulated realizations of models (a)–(d).

= Selected model Selected model Selected model Case SNR SNR SNR 250 (a) 4.36 0.967 0.000 0.000 0.033 2.16 0.920 0.000 0.000 0.080 1.45 0.840 0.000 0.000 0.160 (b) 4.09 0.116 0.882 0.000 0.002 2.04 0.119 0.857 0.000 0.024 1.36 0.132 0.784 0.002 0.082 (c) 3.73 0.016 0.000 0.984 0.000 1.86 0.032 0.000 0.968 0.000 1.24 0.032 0.000 0.968 0.000 (d) 5.44 0.017 0.043 0.005 0.935 2.72 0.014 0.040 0.001 0.945 1.82 0.024 0.040 0.003 0.933 500 (a) 4.29 0.985 0.000 0.000 0.015 2.15 0.945 0.000 0.000 0.055 1.44 0.896 0.000 0.000 0.104 (b) 4.17 0.044 0.949 0.000 0.008 2.08 0.058 0.906 0.000 0.036 1.40 0.037 0.926 0.000 0.037 (c) 3.71 0.001 0.000 0.999 0.000 1.86 0.008 0.000 0.992 0.000 1.24 0.012 0.000 0.988 0.000 (d) 5.42 0.007 0.037 0.000 0.956 2.71 0.012 0.042 0.001 0.945 1.81 0.005 0.026 0.006 0.963 1000 (a) 4.29 0.994 0.000 0.000 0.006 2.15 0.970 0.000 0.000 0.030 1.44 0.921 0.000 0.000 0.079 (b) 4.17 0.004 0.992 0.000 0.004 2.08 0.005 0.975 0.000 0.020 1.40 0.015 0.957 0.000 0.028 (c) 3.71 0.000 0.000 1.000 0.000 1.86 0.001 0.000 0.999 0.000 1.24 0.004 0.000 0.996 0.000 (d) 5.42 0.001 0.028 0.002 0.969 2.71 0.002 0.024 0.003 0.971 1.81 0.001 0.025 0.002 0.972 2000 (a) 4.29 0.999 0.000 0.000 0.001 2.15 0.979 0.000 0.000 0.021 1.44 0.948 0.000 0.000 0.052 (b) 4.17 0.000 0.997 0.000 0.003 2.08 0.000 0.982 0.000 0.018 1.40 0.000 0.965 0.000 0.035 (c) 3.71 0.000 0.000 1.000 0.000 1.86 0.000 0.000 1.000 0.000 1.24 0.001 0.000 0.999 0.000 (d) 5.42 0.000 0.014 0.001 0.985 2.71 0.000 0.014 0.001 0.985 1.81 0.000 0.014 0.000 0.986

It can be seen from Table 1 that the proposed model selection procedure performs reasonably well as it has very high empirical probabilities of identifying the true model, even when the sample size is moderate to small. For example, if the sample size , which is usually considered to be small for conducting time-varying nonparametric inference, and the data are generated by model (a) with , then 967 out of 1000 realizations are correctly identified as the time-varying nonparametric regression model , while 33 out of 1000 realizations are under-fitted as the simple linear regression model . Hence, for each combination of and , in the ideal case, we expect the block to have unit diagonal components and zero off-diagonal components. For each configuration, medians of the SNR are also reported, where for each realization , , the SNR is defined as . It can be seen that the proposed model selection procedure with the CV-based tuning parameter selector has a reasonably robust performance with respect to the noise level, and the performance improves quickly if we increase the sample size. Note that a sample size of 1000 is considered to be reasonable if one would like to conduct time-varying nonparametric inference.

4.3 Application on modeling interest rates

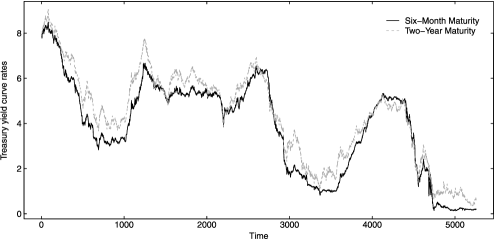

Modeling interest rates is an important problem in finance. In Black and Scholes (1973) and Merton (1974) interest rates were assumed to be constants. A popular model is the time-homogeneous diffusion process (3) with linear drift function; see, for example, Vasicek (1977), Courtadon (1982), Cox, Ingersoll and Ross (1985) and Chan et al. (1992). Its discretized version is given by model . Aït-Sahalia (1996), Stanton (1997) and Liu and Wu (2010) considered model (3) with nonlinear drift function, which relates to model . We consider the daily U.S. treasury yield curve rates with six-month and two-year maturities during 01/02/1990–12/31/2010. The data can be obtained from the U.S. Department of the Treasury website at http://www.treasury.gov/. Both series contain daily rates, and their time series plots are shown in Figure 1.

We shall here model the data by the time-varying diffusion process (2), and apply the proposed model selection procedure to determine the forms of the drift functions. Let be the observation at day . Since a year has 250 transaction days, . Following Liu and Wu (2010), we consider the following discretized version of (2):

| (24) | |||

| (25) |

Note that are i.i.d. random variables. We shall here write and in (4.3) as and in the sequel. Then specifications of Vasicek (1977) and Liu and Wu (2010) become models and , respectively.

For the treasury yield curve rates with six-month maturity, let , and which includes 95.5% of the daily rates . The selected bandwidths and tuning parameter are , , , and . The results are summarized in Table 2. Hence, the time-varying coefficient model is selected, and we conclude that the treasury yield curve rates with six-month maturity should be modeled by (2) with for some smoothly varying functions and , which serves as a time-varying version of Chan et al. (1992).

| Six-month maturity | Two-year maturity | |||||

|---|---|---|---|---|---|---|

| Model | df | gic | df | gic | ||

We then consider the treasury yield curve rates with two-year maturity. Let and which includes 95.1% of the daily rates . The selected bandwidths and tuning parameter are , , , and . Based on Table 2, the linear regression model is selected. In comparison with the results with six-month maturity, our analysis suggests that treasury yield rates with longer maturity are more stable over time.

5 Conclusion

The paper considers a time-varying nonparametric regression model, namely model , which is able to capture time-varying and nonlinear relationships between the response variable and the explanatory variables. It includes the popular nonparametric regression model and time-varying coefficient model as special cases, and all of them are generalizations of the simple linear regression model . In comparison with existing results, the current paper makes two major contributions. First, we develop an asymptotic theory on nonparametric estimation of the time-varying regression model (1) under the new framework of Draghicescu, Guillas and Wu (2009). Compared with the classical strong mixing conditions as used by Vogt (2012), the current framework is convenient to work with and often leads to optimal asymptotic results. In the proof, we use both the martingale decomposition and the -dependence approximation techniques to obtain sharp results. Second, although the time-varying regression model is quite general by allowing a time-varying nonlinear relationship between the response variable and the explanatory variables, it can be useful in practice to check whether it can be reduced to its simpler special cases, namely models – which have been extensively used in the literature. However, existing results on model selection usually focused on distinguishing between models and and between models and , and much less attention has been paid to distinguishing between models and . Note that models and are both generalizations of the simple linear regression model but in completely different aspects, and therefore it is desirable if we can have a statistically valid method to decide which generalization (or the more general model ) should be used for a given data set. The current paper fills this gap by proposing an information criterion (17) in Section 3.3, which can be used to select the true model among candidate models – and its selection consistency is provided by Theorem 3.5. Therefore, the current paper sheds new light on distinguishing between nonlinear and nonstationary generalizations of simple linear regression models, and the results are applied to find appropriate models for short-term and long-term interest rates.

6 Technical proofs

We shall in this section provide technical proofs for Theorems 3.1–3.5. Because of the time-varying feature and nonstationarity, the proofs are much more involved than existing ones for stationary processes. We shall here use techniques of martingale approximation and -dependent approximation. Let and be the corresponding shift process. We define the projection operator

Throughout this section, denotes a constant whose value may vary from place to place. Let , , be a triangular array of deterministic nonnegative weight functions, . Lemma 6.1 provides a bound for the quantity

Lemma 6.1.

Let and define . Then .

Since , form a sequence of martingale differences, we have

and the result follows by observing that and .

Lemma 6.2.

Assume (A1)–(A3) and , , . (i) If , and , then for any ,

where . (ii) If and , then for any ,

Write

where

has summands of martingale differences, and

is the remaining term. Let , and by Lemma 6.1,

We apply the martingale central limit theorem on to show (i). Since

the Lindeberg condition is satisfied by observing that . Let

Then by (A1) and Lemma 6.1,

Also, write . Then we have

and (i) follows by . Case (ii) can be similarly proved.

Proofs of Theorems 3.1 and 3.2 Letting and in Lemma 6.2, (11) and (13) follow directly. For (12), write

where

and

Note that

by Lemma 6.2(i),

Since in probability, (12) follows by Slutsky’s theorem. Case (14) can be similarly proved.

Proofs of Theorems 3.3 and 3.4 We shall first prove Theorem 3.3(i). For this, since , we have for any . Hence, almost surely, and . Therefore, it suffices to deal with the case in which . We shall here assume that . Cases with higher dimensions can be similarly proved without extra essential difficulties, but they aew technically tedious. Let

Observe that , , form a sequence of bounded martingale differences. By the inequality of Freedman (1975) and the proof of Theorem 2 in Wu, Huang and Huang (2010), we obtain that, for some large constant ,

Let and . By (6) and the proof of Lemma 5.3 in Zhang and Wu (2012), it suffices to show that for all ,

| (27) |

Let and . By Theorem 2(ii) in Liu, Xiao and Wu (2013), under condition (A4),

| (28) | |||

By (A3), , (27) follows. For Theorem 3.3(ii), by Lemma 6.3, . Since

the result follows. Theorem 3.4 can be similarly proved.

Recall that is a compact set. Lemma 6.3 provides uniform bounds for

Lemma 6.3.

Assume (A1), (A3), (A4), for some , , and . Let . (i) If and , then

| (29) | |||||

| (30) |

(ii) If and , then

| (31) | |||||

| (32) |

The proof of (29) is similar to that of Theorem 3.3(i), and we shall only outline the key differences. First, the supreme in (29) is taken over , a compact set, instead of . Hence the truncation argument is no longer needed, and the term in (6) can be replaced by . Second, , where . By (A1), satisfies condition (A3), and its predictive dependence measure is of order (10). Hence the proof of Theorem 3.3(i) applies. Case (31) can be similarly handled. For (30) and (32), we shall only provide the proof of (32) since (30) can be similarly derived. Let and be the counterpart of with therein replaced by , . Also, let , and we can similarly define . Since are i.i.d., we have and . In addition,

Since , we have , and by (31), it suffices to show that (32) holds with . Let , , and under (A1). Recall from (A3), then and

Let . Applying the inequality of Freedman (1975) to , we obtain that, for some large constant ,

Let , Lemmas 6.4–6.7 provide asymptotic properties of the restricted residual sum of squares for models –, respectively, and are useful in proving Theorem 3.5. We shall here only provide the proof of Lemmas 6.4 and 6.5, which relate to nonparametric kernel estimation of nonlinear regression functions that have been studied in Sections 3.1 and 3.2. Lemmas 6.6 and 6.7 relate to linear models with time-varying and time-constant coefficients, and the proof is available in the supplementary material [Zhang and Wu (2015)].

Lemma 6.4.

Assume (A1), (A3)–(A5), for some , , , and . If and , then

Note that one can have the decomposition

where by Theorem 3.3, and

We shall now deal with the term . By Lemma 6.3(i) and Theorem 3.3, and thus

Let , and we can then write

where

and

Using the orthogonality of martingale differences and Lemma 2 of Wu, Huang and Huang (2010), we have . Also, by splitting the sum in for cases with and , one can have . Lemma 6.4 follows by .

Lemma 6.5.

Assume (A1), (A3)–(A5), for some , , and . If and , then (i)

(ii) If in addition model is correctly specified, then

By Theorem 3.4,

where by Lemma 2 in Wu, Huang and Huang (2010),

Since is a compact set, by the proof of Lemma 6.2, we have

and (i) follows. Case (ii) follows by a similar argument as in Lemma 6.4.

Lemma 6.6.

Assume (A1)–(A3), (A6), (P2) and for some , . If and , then (i)

(ii) If in addition model is correctly specified, then

Lemma 6.7.

Assume (A1)–(A3), (A6), (P1) and for some , . Then (i)

(ii) If in addition model is correctly specified, then

Proof of Theorem 3.5 For model , the AMSE optimal bandwidths satisfy and . By Lemma 6.4, we have

Under the stated conditions on the tuning parameter, we have , and thus the estimation error is dominated by which goes to zero as . By Lemmas 6.5–6.7, similar results can be derived for models –. Note that

which will be dominated by any model misspecification. The result follows by .

Acknowledgments

We are grateful to the Editor, an Associate Editor, and two anonymous referees for their helpful comments and suggestions.

References

- Aït-Sahalia (1996) {barticle}[auto:parserefs-M02] \bauthor\bsnmAït-Sahalia, \bfnmY.\binitsY. (\byear1996). \btitleTesting continuous-time models of the spot interest rate. \bjournalRev. Finan. Stud. \bvolume9 \bpages385–426. \bptokimsref\endbibitem

- Akaike (1973) {bincollection}[mr] \bauthor\bsnmAkaike, \bfnmH.\binitsH. (\byear1973). \btitleInformation theory and an extension of the maximum likelihood principle. In \bbooktitleSecond International Symposium on Information Theory (Tsahkadsor, 1971) (\beditor\binitsB. N.\bfnmB. N. \bsnmPetrov and \beditor\binitsF.\bfnmF. \bsnmCsaski, eds.) \bpages267–281. \bpublisherAkadémiai Kiadó, \blocationBudapest. \bidmr=0483125 \bptokimsref\endbibitem

- Andrews (1993) {barticle}[mr] \bauthor\bsnmAndrews, \bfnmDonald W. K.\binitsD. W. K. (\byear1993). \btitleTests for parameter instability and structural change with unknown change point. \bjournalEconometrica \bvolume61 \bpages821–856. \biddoi=10.2307/2951764, issn=0012-9682, mr=1231678 \bptokimsref\endbibitem

- Andrews (1995) {barticle}[mr] \bauthor\bsnmAndrews, \bfnmDonald W. K.\binitsD. W. K. (\byear1995). \btitleNonparametric kernel estimation for semiparametric models. \bjournalEconometric Theory \bvolume11 \bpages560–596. \biddoi=10.1017/S0266466600009427, issn=0266-4666, mr=1349935 \bptokimsref\endbibitem

- Azzalini and Bowman (1993) {barticle}[mr] \bauthor\bsnmAzzalini, \bfnmAdelchi\binitsA. and \bauthor\bsnmBowman, \bfnmAdrian\binitsA. (\byear1993). \btitleOn the use of nonparametric regression for checking linear relationships. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume55 \bpages549–557. \bidissn=0035-9246, mr=1224417 \bptokimsref\endbibitem

- Black and Scholes (1973) {barticle}[auto:parserefs-M02] \bauthor\bsnmBlack, \bfnmF.\binitsF. and \bauthor\bsnmScholes, \bfnmM.\binitsM. (\byear1973). \btitleThe pricing of options and corporate liabilities. \bjournalJ. Polit. Economy \bvolume81 \bpages637–654. \bptokimsref\endbibitem

- Bosq (1996) {bbook}[mr] \bauthor\bsnmBosq, \bfnmD.\binitsD. (\byear1996). \btitleNonparametric Statistics for Stochastic Processes: Estimation and Prediction. \bseriesLecture Notes in Statistics \bvolume110. \bpublisherSpringer, \blocationNew York. \biddoi=10.1007/978-1-4684-0489-0, mr=1441072 \bptokimsref\endbibitem

- Brown, Durbin and Evans (1975) {barticle}[mr] \bauthor\bsnmBrown, \bfnmR. L.\binitsR. L., \bauthor\bsnmDurbin, \bfnmJames\binitsJ. and \bauthor\bsnmEvans, \bfnmJ. M.\binitsJ. M. (\byear1975). \btitleTechniques for testing the constancy of regression relationships over time. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume37 \bpages149–192. \bidissn=0035-9246, mr=0378310 \bptnotecheck related \bptokimsref\endbibitem

- Cai (2007) {barticle}[mr] \bauthor\bsnmCai, \bfnmZongwu\binitsZ. (\byear2007). \btitleTrending time-varying coefficient time series models with serially correlated errors. \bjournalJ. Econometrics \bvolume136 \bpages163–188. \biddoi=10.1016/j.jeconom.2005.08.004, issn=0304-4076, mr=2328589 \bptokimsref\endbibitem

- Castellana and Leadbetter (1986) {barticle}[mr] \bauthor\bsnmCastellana, \bfnmJ. V.\binitsJ. V. and \bauthor\bsnmLeadbetter, \bfnmM. R.\binitsM. R. (\byear1986). \btitleOn smoothed probability density estimation for stationary processes. \bjournalStochastic Process. Appl. \bvolume21 \bpages179–193. \biddoi=10.1016/0304-4149(86)90095-5, issn=0304-4149, mr=0833950 \bptokimsref\endbibitem

- Chan et al. (1992) {barticle}[auto:parserefs-M02] \bauthor\bsnmChan, \bfnmK. C.\binitsK. C., \bauthor\bsnmKarolyi, \bfnmA. G.\binitsA. G., \bauthor\bsnmLongstaff, \bfnmF. A.\binitsF. A. and \bauthor\bsnmSanders, \bfnmA. B.\binitsA. B. (\byear1992). \btitleAn empirical comparison of alternative models of the short-term interest rate. \bjournalJ. Finance \bvolume47 \bpages1209–1227. \bptokimsref\endbibitem

- Chow (1960) {barticle}[mr] \bauthor\bsnmChow, \bfnmGregory C.\binitsG. C. (\byear1960). \btitleTests of equality between sets of coefficients in two linear regressions. \bjournalEconometrica \bvolume28 \bpages591–605. \bidissn=0012-9682, mr=0141193 \bptokimsref\endbibitem

- Courtadon (1982) {barticle}[auto:parserefs-M02] \bauthor\bsnmCourtadon, \bfnmG.\binitsG. (\byear1982). \btitleThe pricing of options on default-free bonds. \bjournalJ. Finan. Quant. Anal. \bvolume17 \bpages75–100. \bptokimsref\endbibitem

- Cox, Ingersoll and Ross (1985) {barticle}[mr] \bauthor\bsnmCox, \bfnmJohn C.\binitsJ. C., \bauthor\bsnmIngersoll, \bfnmJonathan E.\binitsJ. E. \bsuffixJr. and \bauthor\bsnmRoss, \bfnmStephen A.\binitsS. A. (\byear1985). \btitleA theory of the term structure of interest rates. \bjournalEconometrica \bvolume53 \bpages385–407. \biddoi=10.2307/1911242, issn=0012-9682, mr=0785475 \bptokimsref\endbibitem

- Davis, Huang and Yao (1995) {barticle}[mr] \bauthor\bsnmDavis, \bfnmRichard A.\binitsR. A., \bauthor\bsnmHuang, \bfnmDa Wei\binitsD. W. and \bauthor\bsnmYao, \bfnmYi-Ching\binitsY.-C. (\byear1995). \btitleTesting for a change in the parameter values and order of an autoregressive model. \bjournalAnn. Statist. \bvolume23 \bpages282–304. \biddoi=10.1214/aos/1176324468, issn=0090-5364, mr=1331669 \bptokimsref\endbibitem

- Dette (1999) {barticle}[mr] \bauthor\bsnmDette, \bfnmHolger\binitsH. (\byear1999). \btitleA consistent test for the functional form of a regression based on a difference of variance estimators. \bjournalAnn. Statist. \bvolume27 \bpages1012–1040. \biddoi=10.1214/aos/1018031266, issn=0090-5364, mr=1724039 \bptokimsref\endbibitem

- Draghicescu, Guillas and Wu (2009) {barticle}[mr] \bauthor\bsnmDraghicescu, \bfnmDana\binitsD., \bauthor\bsnmGuillas, \bfnmSerge\binitsS. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2009). \btitleQuantile curve estimation and visualization for nonstationary time series. \bjournalJ. Comput. Graph. Statist. \bvolume18 \bpages1–20. \biddoi=10.1198/jcgs.2009.0001, issn=1061-8600, mr=2511058 \bptokimsref\endbibitem

- Fan and Li (2001) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2001). \btitleVariable selection via nonconcave penalized likelihood and its oracle properties. \bjournalJ. Amer. Statist. Assoc. \bvolume96 \bpages1348–1360. \biddoi=10.1198/016214501753382273, issn=0162-1459, mr=1946581 \bptokimsref\endbibitem

- Fan and Yao (2003) {bbook}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmYao, \bfnmQiwei\binitsQ. (\byear2003). \btitleNonlinear Time Series: Nonparametric and Parametric Methods. \bpublisherSpringer, \blocationNew York. \biddoi=10.1007/b97702, mr=1964455 \bptokimsref\endbibitem

- Fan and Zhang (2000a) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmZhang, \bfnmJin-Ting\binitsJ.-T. (\byear2000a). \btitleTwo-step estimation of functional linear models with applications to longitudinal data. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume62 \bpages303–322. \biddoi=10.1111/1467-9868.00233, issn=1369-7412, mr=1749541 \bptokimsref\endbibitem

- Fan and Zhang (2000b) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmZhang, \bfnmWenyang\binitsW. (\byear2000b). \btitleSimultaneous confidence bands and hypothesis testing in varying-coefficient models. \bjournalScand. J. Stat. \bvolume27 \bpages715–731. \biddoi=10.1111/1467-9469.00218, issn=0303-6898, mr=1804172 \bptokimsref\endbibitem

- Fan, Zhang and Zhang (2001) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmZhang, \bfnmChunming\binitsC. and \bauthor\bsnmZhang, \bfnmJian\binitsJ. (\byear2001). \btitleGeneralized likelihood ratio statistics and Wilks phenomenon. \bjournalAnn. Statist. \bvolume29 \bpages153–193. \biddoi=10.1214/aos/996986505, issn=0090-5364, mr=1833962 \bptokimsref\endbibitem

- Freedman (1975) {barticle}[mr] \bauthor\bsnmFreedman, \bfnmDavid A.\binitsD. A. (\byear1975). \btitleOn tail probabilities for martingales. \bjournalAnn. Probab. \bvolume3 \bpages100–118. \bidmr=0380971 \bptokimsref\endbibitem

- Gao and Gijbels (2008) {barticle}[mr] \bauthor\bsnmGao, \bfnmJiti\binitsJ. and \bauthor\bsnmGijbels, \bfnmIrène\binitsI. (\byear2008). \btitleBandwidth selection in nonparametric kernel testing. \bjournalJ. Amer. Statist. Assoc. \bvolume103 \bpages1584–1594. \biddoi=10.1198/016214508000000968, issn=0162-1459, mr=2504206 \bptokimsref\endbibitem

- González Manteiga and Cao (1993) {barticle}[mr] \bauthor\bsnmGonzález Manteiga, \bfnmW.\binitsW. and \bauthor\bsnmCao, \bfnmR.\binitsR. (\byear1993). \btitleTesting the hypothesis of a general linear model using nonparametric regression estimation. \bjournalTEST \bvolume2 \bpages161–188. \biddoi=10.1007/BF02562674, issn=1133-0686, mr=1265489 \bptokimsref\endbibitem

- Györfi et al. (1989) {bbook}[mr] \bauthor\bsnmGyörfi, \bfnmLázló\binitsL., \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW., \bauthor\bsnmSarda, \bfnmPascal\binitsP. and \bauthor\bsnmVieu, \bfnmPhilippe\binitsP. (\byear1989). \btitleNonparametric Curve Estimation from Time Series. \bseriesLecture Notes in Statistics \bvolume60. \bpublisherSpringer, \blocationBerlin. \biddoi=10.1007/978-1-4612-3686-3, mr=1027837 \bptokimsref\endbibitem

- Hall, Müller and Wu (2006) {barticle}[mr] \bauthor\bsnmHall, \bfnmPeter\binitsP., \bauthor\bsnmMüller, \bfnmHans-Georg\binitsH.-G. and \bauthor\bsnmWu, \bfnmPing-Shi\binitsP.-S. (\byear2006). \btitleReal-time density and mode estimation with application to time-dynamic mode tracking. \bjournalJ. Comput. Graph. Statist. \bvolume15 \bpages82–100. \biddoi=10.1198/106186006X94333, issn=1061-8600, mr=2269364 \bptokimsref\endbibitem

- Hansen (2008) {barticle}[mr] \bauthor\bsnmHansen, \bfnmBruce E.\binitsB. E. (\byear2008). \btitleUniform convergence rates for kernel estimation with dependent data. \bjournalEconometric Theory \bvolume24 \bpages726–748. \biddoi=10.1017/S0266466608080304, issn=0266-4666, mr=2409261 \bptokimsref\endbibitem

- Härdle, Hall and Marron (1988) {barticle}[mr] \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW., \bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmMarron, \bfnmJ. S.\binitsJ. S. (\byear1988). \btitleHow far are automatically chosen regression smoothing parameters from their optimum? \bjournalJ. Amer. Statist. Assoc. \bvolume83 \bpages86–101. \bidissn=0162-1459, mr=0941001 \bptnotecheck related \bptokimsref\endbibitem

- Härdle and Mammen (1993) {barticle}[mr] \bauthor\bsnmHärdle, \bfnmW.\binitsW. and \bauthor\bsnmMammen, \bfnmE.\binitsE. (\byear1993). \btitleComparing nonparametric versus parametric regression fits. \bjournalAnn. Statist. \bvolume21 \bpages1926–1947. \biddoi=10.1214/aos/1176349403, issn=0090-5364, mr=1245774 \bptokimsref\endbibitem

- Härdle and Marron (1985) {barticle}[mr] \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW. and \bauthor\bsnmMarron, \bfnmJames Stephen\binitsJ. S. (\byear1985). \btitleOptimal bandwidth selection in nonparametric regression function estimation. \bjournalAnn. Statist. \bvolume13 \bpages1465–1481. \biddoi=10.1214/aos/1176349748, issn=0090-5364, mr=0811503 \bptokimsref\endbibitem

- He, Teräsvirta and González (2009) {barticle}[mr] \bauthor\bsnmHe, \bfnmChangli\binitsC., \bauthor\bsnmTeräsvirta, \bfnmTimo\binitsT. and \bauthor\bsnmGonzález, \bfnmAndrés\binitsA. (\byear2009). \btitleTesting parameter constancy in stationary vector autoregressive models against continuous change. \bjournalEconometric Rev. \bvolume28 \bpages225–245. \biddoi=10.1080/07474930802388041, issn=0747-4938, mr=2655626 \bptokimsref\endbibitem

- Hoover et al. (1998) {barticle}[mr] \bauthor\bsnmHoover, \bfnmDonald R.\binitsD. R., \bauthor\bsnmRice, \bfnmJohn A.\binitsJ. A., \bauthor\bsnmWu, \bfnmColin O.\binitsC. O. and \bauthor\bsnmYang, \bfnmLi-Ping\binitsL.-P. (\byear1998). \btitleNonparametric smoothing estimates of time-varying coefficient models with longitudinal data. \bjournalBiometrika \bvolume85 \bpages809–822. \biddoi=10.1093/biomet/85.4.809, issn=0006-3444, mr=1666699 \bptokimsref\endbibitem

- Huang, Wu and Zhou (2004) {barticle}[mr] \bauthor\bsnmHuang, \bfnmJianhua Z.\binitsJ. Z., \bauthor\bsnmWu, \bfnmColin O.\binitsC. O. and \bauthor\bsnmZhou, \bfnmLan\binitsL. (\byear2004). \btitlePolynomial spline estimation and inference for varying coefficient models with longitudinal data. \bjournalStatist. Sinica \bvolume14 \bpages763–788. \bidissn=1017-0405, mr=2087972 \bptokimsref\endbibitem

- Hurvich, Simonoff and Tsai (1998) {barticle}[mr] \bauthor\bsnmHurvich, \bfnmClifford M.\binitsC. M., \bauthor\bsnmSimonoff, \bfnmJeffrey S.\binitsJ. S. and \bauthor\bsnmTsai, \bfnmChih-Ling\binitsC.-L. (\byear1998). \btitleSmoothing parameter selection in nonparametric regression using an improved Akaike information criterion. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume60 \bpages271–293. \biddoi=10.1111/1467-9868.00125, issn=1369-7412, mr=1616041 \bptokimsref\endbibitem

- Leybourne and McCabe (1989) {barticle}[mr] \bauthor\bsnmLeybourne, \bfnmS. J.\binitsS. J. and \bauthor\bsnmMcCabe, \bfnmB. P. M.\binitsB. P. M. (\byear1989). \btitleOn the distribution of some test statistics for coefficient constancy. \bjournalBiometrika \bvolume76 \bpages169–177. \biddoi=10.1093/biomet/76.1.169, issn=0006-3444, mr=0991435 \bptokimsref\endbibitem

- Li and Racine (2007) {bbook}[mr] \bauthor\bsnmLi, \bfnmQi\binitsQ. and \bauthor\bsnmRacine, \bfnmJeffrey Scott\binitsJ. S. (\byear2007). \btitleNonparametric Econometrics: Theory and Practice. \bpublisherPrinceton Univ. Press, \blocationPrinceton, NJ. \bidmr=2283034 \bptokimsref\endbibitem

- Lin and Teräsvirta (1999) {barticle}[mr] \bauthor\bsnmLin, \bfnmChien-Fu Jeff\binitsC.-F. J. and \bauthor\bsnmTeräsvirta, \bfnmTimo\binitsT. (\byear1999). \btitleTesting parameter constancy in linear models against stochastic stationary parameters. \bjournalJ. Econometrics \bvolume90 \bpages193–213. \biddoi=10.1016/S0304-4076(98)00041-4, issn=0304-4076, mr=1703341 \bptokimsref\endbibitem

- Liu and Wu (2010) {barticle}[mr] \bauthor\bsnmLiu, \bfnmWeidong\binitsW. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2010). \btitleSimultaneous nonparametric inference of time series. \bjournalAnn. Statist. \bvolume38 \bpages2388–2421. \biddoi=10.1214/09-AOS789, issn=0090-5364, mr=2676893 \bptokimsref\endbibitem

- Liu, Xiao and Wu (2013) {barticle}[mr] \bauthor\bsnmLiu, \bfnmWeidong\binitsW., \bauthor\bsnmXiao, \bfnmHan\binitsH. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2013). \btitleProbability and moment inequalities under dependence. \bjournalStatist. Sinica \bvolume23 \bpages1257–1272. \bidissn=1017-0405, mr=3114713 \bptokimsref\endbibitem

- Mallows (1973) {barticle}[auto:parserefs-M02] \bauthor\bsnmMallows, \bfnmC. L.\binitsC. L. (\byear1973). \btitleSome comments on . \bjournalTechnometrics \bvolume15 \bpages661–675. \bptokimsref\endbibitem

- Masry (1996) {barticle}[mr] \bauthor\bsnmMasry, \bfnmElias\binitsE. (\byear1996). \btitleMultivariate local polynomial regression for time series: Uniform strong consistency and rates. \bjournalJ. Time Series Anal. \bvolume17 \bpages571–599. \biddoi=10.1111/j.1467-9892.1996.tb00294.x, issn=0143-9782, mr=1424907 \bptokimsref\endbibitem

- Merton (1974) {barticle}[auto:parserefs-M02] \bauthor\bsnmMerton, \bfnmR. C.\binitsR. C. (\byear1974). \btitleOn the pricing of corporate debt: The risk structure of interest rates. \bjournalJ. Finan. Econ. \bvolume3 \bpages125–144. \bptokimsref\endbibitem

- Nabeya and Tanaka (1988) {barticle}[mr] \bauthor\bsnmNabeya, \bfnmSeiji\binitsS. and \bauthor\bsnmTanaka, \bfnmKatsuto\binitsK. (\byear1988). \btitleAsymptotic theory of a test for the constancy of regression coefficients against the random walk alternative. \bjournalAnn. Statist. \bvolume16 \bpages218–235. \biddoi=10.1214/aos/1176350701, issn=0090-5364, mr=0924867 \bptokimsref\endbibitem

- Neumann (1998) {barticle}[mr] \bauthor\bsnmNeumann, \bfnmMichael H.\binitsM. H. (\byear1998). \btitleStrong approximation of density estimators from weakly dependent observations by density estimators from independent observations. \bjournalAnn. Statist. \bvolume26 \bpages2014–2048. \biddoi=10.1214/aos/1024691367, issn=0090-5364, mr=1673288 \bptokimsref\endbibitem

- Neumann and Kreiss (1998) {barticle}[mr] \bauthor\bsnmNeumann, \bfnmMichael H.\binitsM. H. and \bauthor\bsnmKreiss, \bfnmJens-Peter\binitsJ.-P. (\byear1998). \btitleRegression-type inference in nonparametric autoregression. \bjournalAnn. Statist. \bvolume26 \bpages1570–1613. \biddoi=10.1214/aos/1024691254, issn=0090-5364, mr=1647701 \bptokimsref\endbibitem

- Nyblom (1989) {barticle}[mr] \bauthor\bsnmNyblom, \bfnmJukka\binitsJ. (\byear1989). \btitleTesting for the constancy of parameters over time. \bjournalJ. Amer. Statist. Assoc. \bvolume84 \bpages223–230. \bidissn=0162-1459, mr=0999682 \bptokimsref\endbibitem

- Opsomer, Wang and Yang (2001) {barticle}[mr] \bauthor\bsnmOpsomer, \bfnmJean\binitsJ., \bauthor\bsnmWang, \bfnmYuedong\binitsY. and \bauthor\bsnmYang, \bfnmYuhong\binitsY. (\byear2001). \btitleNonparametric regression with correlated errors. \bjournalStatist. Sci. \bvolume16 \bpages134–153. \biddoi=10.1214/ss/1009213287, issn=0883-4237, mr=1861070 \bptokimsref\endbibitem

- Orbe, Ferreira and Rodriguez-Poo (2005) {barticle}[mr] \bauthor\bsnmOrbe, \bfnmSusan\binitsS., \bauthor\bsnmFerreira, \bfnmEva\binitsE. and \bauthor\bsnmRodriguez-Poo, \bfnmJuan\binitsJ. (\byear2005). \btitleNonparametric estimation of time varying parameters under shape restrictions. \bjournalJ. Econometrics \bvolume126 \bpages53–77. \biddoi=10.1016/j.jeconom.2004.02.006, issn=0304-4076, mr=2118278 \bptokimsref\endbibitem

- Orbe, Ferreira and Rodriguez-Poo (2006) {barticle}[mr] \bauthor\bsnmOrbe, \bfnmSusan\binitsS., \bauthor\bsnmFerreira, \bfnmEva\binitsE. and \bauthor\bsnmRodriguez-Poo, \bfnmJuan\binitsJ. (\byear2006). \btitleOn the estimation and testing of time varying constraints in econometric models. \bjournalStatist. Sinica \bvolume16 \bpages1313–1333. \bidissn=1017-0405, mr=2327493 \bptokimsref\endbibitem

- Park and Marron (1990) {barticle}[auto:parserefs-M02] \bauthor\bsnmPark, \bfnmB. U.\binitsB. U. and \bauthor\bsnmMarron, \bfnmJ. S.\binitsJ. S. (\byear1990). \btitleComparison of data-driven bandwidth selectors. \bjournalJ. Amer. Statist. Assoc. \bvolume85 \bpages66–72. \bptokimsref\endbibitem

- Peligrad (1992) {barticle}[mr] \bauthor\bsnmPeligrad, \bfnmMagda\binitsM. (\byear1992). \btitleProperties of uniform consistency of the kernel estimators of density and of regression functions under dependence assumptions. \bjournalStochastics Stochastics Rep. \bvolume40 \bpages147–168. \bidissn=1045-1129, mr=1275130 \bptnotecheck year \bptokimsref\endbibitem

- Ploberger, Krämer and Kontrus (1989) {barticle}[mr] \bauthor\bsnmPloberger, \bfnmWerner\binitsW., \bauthor\bsnmKrämer, \bfnmWalter\binitsW. and \bauthor\bsnmKontrus, \bfnmKarl\binitsK. (\byear1989). \btitleA new test for structural stability in the linear regression model. \bjournalJ. Econometrics \bvolume40 \bpages307–318. \biddoi=10.1016/0304-4076(89)90087-0, issn=0304-4076, mr=0994952 \bptokimsref\endbibitem

- Priestley and Chao (1972) {barticle}[mr] \bauthor\bsnmPriestley, \bfnmM. B.\binitsM. B. and \bauthor\bsnmChao, \bfnmM. T.\binitsM. T. (\byear1972). \btitleNon-parametric function fitting. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume34 \bpages385–392. \bidissn=0035-9246, mr=0331616 \bptokimsref\endbibitem

- Ramsay and Silverman (2005) {bbook}[mr] \bauthor\bsnmRamsay, \bfnmJ. O.\binitsJ. O. and \bauthor\bsnmSilverman, \bfnmB. W.\binitsB. W. (\byear2005). \btitleFunctional Data Analysis, \bedition2nd ed. \bpublisherSpringer, \blocationNew York. \bidmr=2168993 \bptokimsref\endbibitem

- Robinson (1983) {barticle}[mr] \bauthor\bsnmRobinson, \bfnmP. M.\binitsP. M. (\byear1983). \btitleNonparametric estimators for time series. \bjournalJ. Time Series Anal. \bvolume4 \bpages185–207. \biddoi=10.1111/j.1467-9892.1983.tb00368.x, issn=0143-9782, mr=0732897 \bptokimsref\endbibitem

- Ruppert, Sheather and Wand (1995) {barticle}[mr] \bauthor\bsnmRuppert, \bfnmD.\binitsD., \bauthor\bsnmSheather, \bfnmS. J.\binitsS. J. and \bauthor\bsnmWand, \bfnmM. P.\binitsM. P. (\byear1995). \btitleAn effective bandwidth selector for local least squares regression. \bjournalJ. Amer. Statist. Assoc. \bvolume90 \bpages1257–1270. \bidissn=0162-1459, mr=1379468 \bptokimsref\endbibitem

- Schwarz (1978) {barticle}[mr] \bauthor\bsnmSchwarz, \bfnmGideon\binitsG. (\byear1978). \btitleEstimating the dimension of a model. \bjournalAnn. Statist. \bvolume6 \bpages461–464. \bidissn=0090-5364, mr=0468014 \bptokimsref\endbibitem

- Shao (1997) {barticle}[mr] \bauthor\bsnmShao, \bfnmJun\binitsJ. (\byear1997). \btitleAn asymptotic theory for linear model selection. \bjournalStatist. Sinica \bvolume7 \bpages221–264. \bidissn=1017-0405, mr=1466682 \bptnotecheck related \bptokimsref\endbibitem

- Shao and Wu (2007) {barticle}[mr] \bauthor\bsnmShao, \bfnmXiaofeng\binitsX. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2007). \btitleAsymptotic spectral theory for nonlinear time series. \bjournalAnn. Statist. \bvolume35 \bpages1773–1801. \biddoi=10.1214/009053606000001479, issn=0090-5364, mr=2351105 \bptokimsref\endbibitem

- Silverman (1986) {bbook}[mr] \bauthor\bsnmSilverman, \bfnmB. W.\binitsB. W. (\byear1986). \btitleDensity Estimation for Statistics and Data Analysis. \bpublisherChapman & Hall, \blocationLondon. \biddoi=10.1007/978-1-4899-3324-9, mr=0848134 \bptokimsref\endbibitem

- Stanton (1997) {barticle}[auto:parserefs-M02] \bauthor\bsnmStanton, \bfnmR.\binitsR. (\byear1997). \btitleA nonparametric model of term structure dynamics and the market price of interest rate risk. \bjournalJ. Finance \bvolume52 \bpages1973–2002. \bptokimsref\endbibitem

- Tibshirani and Tibshirani (2009) {barticle}[mr] \bauthor\bsnmTibshirani, \bfnmRyan J.\binitsR. J. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2009). \btitleA bias correction for the minimum error rate in cross-validation. \bjournalAnn. Appl. Stat. \bvolume3 \bpages822–829. \biddoi=10.1214/08-AOAS224, issn=1932-6157, mr=2750683 \bptokimsref\endbibitem

- Tjøstheim (1994) {barticle}[mr] \bauthor\bsnmTjøstheim, \bfnmDag\binitsD. (\byear1994). \btitleNon-linear time series: A selective review. \bjournalScand. J. Stat. \bvolume21 \bpages97–130. \bidissn=0303-6898, mr=1294588 \bptokimsref\endbibitem

- Vasicek (1977) {barticle}[auto:parserefs-M02] \bauthor\bsnmVasicek, \bfnmO.\binitsO. (\byear1977). \btitleAn equilibrium characterization of the term structure. \bjournalJ. Finan. Econ. \bvolume5 \bpages177–188. \bptokimsref\endbibitem

- Vogt (2012) {barticle}[mr] \bauthor\bsnmVogt, \bfnmMichael\binitsM. (\byear2012). \btitleNonparametric regression for locally stationary time series. \bjournalAnn. Statist. \bvolume40 \bpages2601–2633. \biddoi=10.1214/12-AOS1043, issn=0090-5364, mr=3097614 \bptokimsref\endbibitem

- Wand and Jones (1995) {bbook}[mr] \bauthor\bsnmWand, \bfnmM. P.\binitsM. P. and \bauthor\bsnmJones, \bfnmM. C.\binitsM. C. (\byear1995). \btitleKernel Smoothing. \bseriesMonographs on Statistics and Applied Probability \bvolume60. \bpublisherChapman & Hall, \blocationLondon. \biddoi=10.1007/978-1-4899-4493-1, mr=1319818 \bptokimsref\endbibitem

- Wang (1998) {barticle}[auto:parserefs-M02] \bauthor\bsnmWang, \bfnmY. D.\binitsY. D. (\byear1998). \btitleSmoothing spline models with correlated random errors. \bjournalJ. Amer. Statist. Assoc. \bvolume93 \bpages341–348. \bptokimsref\endbibitem

- Wu (2005) {barticle}[mr] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2005). \btitleNonlinear system theory: Another look at dependence. \bjournalProc. Natl. Acad. Sci. USA \bvolume102 \bpages14150–14154 (electronic). \biddoi=10.1073/pnas.0506715102, issn=1091-6490, mr=2172215 \bptokimsref\endbibitem

- Wu, Huang and Huang (2010) {barticle}[mr] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B., \bauthor\bsnmHuang, \bfnmYinxiao\binitsY. and \bauthor\bsnmHuang, \bfnmYibi\binitsY. (\byear2010). \btitleKernel estimation for time series: An asymptotic theory. \bjournalStochastic Process. Appl. \bvolume120 \bpages2412–2431. \biddoi=10.1016/j.spa.2010.08.001, issn=0304-4149, mr=2728171 \bptokimsref\endbibitem

- Xia (1998) {barticle}[mr] \bauthor\bsnmXia, \bfnmYingcun\binitsY. (\byear1998). \btitleBias-corrected confidence bands in nonparametric regression. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume60 \bpages797–811. \biddoi=10.1111/1467-9868.00155, issn=1369-7412, mr=1649488 \bptokimsref\endbibitem

- Yang (2005) {barticle}[mr] \bauthor\bsnmYang, \bfnmYuhong\binitsY. (\byear2005). \btitleCan the strengths of AIC and BIC be shared? A conflict between model indentification and regression estimation. \bjournalBiometrika \bvolume92 \bpages937–950. \biddoi=10.1093/biomet/92.4.937, issn=0006-3444, mr=2234196 \bptokimsref\endbibitem

- Yu (1993) {barticle}[mr] \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear1993). \btitleDensity estimation in the -norm for dependent data with applications to the Gibbs sampler. \bjournalAnn. Statist. \bvolume21 \bpages711–735. \biddoi=10.1214/aos/1176349146, issn=0090-5364, mr=1232514 \bptokimsref\endbibitem

- Zhang and Dette (2004) {barticle}[mr] \bauthor\bsnmZhang, \bfnmChunming\binitsC. and \bauthor\bsnmDette, \bfnmHolger\binitsH. (\byear2004). \btitleA power comparison between nonparametric regression tests. \bjournalStatist. Probab. Lett. \bvolume66 \bpages289–301. \biddoi=10.1016/j.spl.2003.11.005, issn=0167-7152, mr=2045474 \bptokimsref\endbibitem

- Zhang and Wu (2011) {barticle}[mr] \bauthor\bsnmZhang, \bfnmTing\binitsT. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2011). \btitleTesting parametric assumptions of trends of a nonstationary time series. \bjournalBiometrika \bvolume98 \bpages599–614. \biddoi=10.1093/biomet/asr017, issn=0006-3444, mr=2836409 \bptokimsref\endbibitem

- Zhang and Wu (2012) {barticle}[mr] \bauthor\bsnmZhang, \bfnmTing\binitsT. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2012). \btitleInference of time-varying regression models. \bjournalAnn. Statist. \bvolume40 \bpages1376–1402. \biddoi=10.1214/12-AOS1010, issn=0090-5364, mr=3015029 \bptokimsref\endbibitem

- Zhang and Wu (2015) {bmisc}[author] \bauthor\bsnmZhang, \binitsT. and \bauthor\bsnmWu, \binitsW. B. (\byear2015). \bhowpublishedSupplement to “Time-varying nonlinear regression models: Nonparametric estimation and model selection.” DOI:\doiurl10.1214/14-AOS1299SUPP. \bptokimsref \endbibitem

- Zhao (2008) {barticle}[mr] \bauthor\bsnmZhao, \bfnmZhibiao\binitsZ. (\byear2008). \btitleParametric and nonparametric models and methods in financial econometrics. \bjournalStat. Surv. \bvolume2 \bpages1–42. \biddoi=10.1214/08-SS034, issn=1935-7516, mr=2520979 \bptokimsref\endbibitem

- Zheng (1996) {barticle}[mr] \bauthor\bsnmZheng, \bfnmJohn Xu\binitsJ. X. (\byear1996). \btitleA consistent test of functional form via nonparametric estimation techniques. \bjournalJ. Econometrics \bvolume75 \bpages263–289. \biddoi=10.1016/0304-4076(95)01760-7, issn=0304-4076, mr=1413644 \bptokimsref\endbibitem

- Zhou and Wu (2010) {barticle}[mr] \bauthor\bsnmZhou, \bfnmZhou\binitsZ. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2010). \btitleSimultaneous inference of linear models with time varying coefficients. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume72 \bpages513–531. \biddoi=10.1111/j.1467-9868.2010.00743.x, issn=1369-7412, mr=2758526 \bptokimsref\endbibitem