A hybrid tree/finite-difference approach for

Heston-Hull-White type models

Abstract

We study a hybrid tree/finite-difference method which permits to obtain efficient and accurate European and American option prices in the Heston Hull-White and Heston Hull-White2d models. Moreover, as a by-product, we provide a new simulation scheme to be used for Monte Carlo evaluations. Numerical results show the reliability and the efficiency of the proposed methods.

Keywords: stochastic volatility; stochastic interest rate; tree methods; finite-difference; Monte Carlo; European and American options

1 Introduction

In this paper we consider the Heston-Hull-White model, which is a joint evolution for the equity value with a Heston-like stochastic volatility and a generalized Hull-White stochastic interest rate model which is consistent with the term structure of the interest rates. We consider a further situation where the dividend rate is stochastic, a case which is called here the “Heston Hull-White2d model” and can be of interest in the multi-currency (the dividend rate being interpreted as a further interest rate). We concern the problem of numerically pricing European and American options written on these models.

At the present time, the literature on this subject is quite poor and includes Fourier-Cosine methods, semi-closed approximations and finite-difference methods to price vanilla options. In [15], Grzelak and Oosterlee introduce two approximations of the non-affine models. The Fourier-Cosine method is then used on this approximating affine model. The authors remark that for accurate modeling of hybrid derivatives it is necessary to be able to describe a non-zero correlation between the processes driving the equity and the interest rate. This is possible in the approximations presented in their paper but only using approximated affine models. Haentjens and in’t Hout propose in [13] a finite-difference Alternating Direction Implicit (ADI) scheme for pricing European options solving the original three-dimensional Heston-Hull-White Partial Differential Equation (hereafter PDE). The Heston Hull-White2d model is treated using semi-closed approximations in the Foreign Exchange model [16].

In this paper, we generalize the hybrid tree/finite-difference approach that has been introduced for the Heston model in the paper [6]. In practice, this means to write down an algorithm to price European and American options by means of a backward induction that works following a finite-difference PDE method in the direction of the share process and following a recombining binomial tree method in the direction of the other random sources (volatility, interest rate and possibly dividend rate).

It is well known that there is a link between tree methods and finite-difference methods. The most remarkable benefits in using recombining binomial trees (let us stress the terms “recombining” and “binomial”: just two possible recombining jumps at each time-step for each component) are the simplicity of the implementation, the low computational costs and the efficiency of the output numerical results. In dimension 1, one can always build a recombining binomial tree (see e.g. Nelson and Ramaswamy [20]) but this is not the case in multidimensional problems. For example, in the standard (dimension 2) Heston model it is not possible to write down a recombining binomial approximating tree - roughly speaking, this follows from the fact that it is not possible to produce a function of the Heston components such that the associated Stochastic Differential Equation (SDE) has a diagonal diffusion coefficient. A binomial tree approximation for the standard Heston model has been proposed by Vellekoop and Nieuwenhuis in [22] but it is far from being recombining and, as shown in [6], it is problematic when the Feller condition is not satisfied. Finally, an approximation of the price coming from a numerical treatment of the (multidimensional) PDE can be very expensive, mainly to handle the 4-dimensional Heston-Hull-White2d model.

So, the idea underlying the approach developed in this paper is in some sense very simple: we apply the most efficient and easy to implement method whenever we can do it. In fact, wherever an efficient recombining binomial tree scheme can be settled (volatility, interest rate and possibly dividend rate), we use it. And where it cannot (share process), we use a standard (and efficient, being in dimension 1) numerical PDE approach. Hence we avoid to work with expensive (because non recombining and/or binomial) trees or with PDEs in high dimension. Moreover, for the Cox-Ingersoll-Ross (hereafter CIR) volatility component, we apply the recombining binomial tree method firstly introduced in [4], which theoretically converges and efficiently works in practice also when the Feller condition fails.

The description of the approximating processes coming from our hybrid tree/finite-difference approach, suggests a simple way to simulate paths from the Heston-Hull-White models. Therefore, we propose here also a new Monte Carlo algorithm for pricing options which seems to be a real alternative to the Monte Carlo method that makes use of the efficient simulations provided by Alfonsi [1].

Our approaches allow one to price options in the original Heston-Hull-White processes with non-zero correlations. Here, we consider the case of a non null correlation between the equity and the interest rate process, as well as between the equity and the stochastic volatility. Moreover, in the Heston-Hull-White2d model, we allow the dividend rate to be stochastic and correlated to the equity process. But it is worth noticing that other sets of correlations can surely be selected.

The paper is organized as follows. In Section 2 we introduce the Heston-Hull-White model. Then in Section 3 we construct a recombining binomial tree approximation for the pair given by the volatility and the interest rate process. Section 4 refers to the approximation of functions of the underlying asset price process by means of PDE arguments. In Section 5 we describe the hybrid tree/finite-difference scheme for the computation of American options. In Section 6 we see how to generalize the previous procedure in order to handle the Heston-Hull-White2d process. In Section 7 we show that our arguments can be used also to set-up simulations, to be applied to construct Monte Carlo algorithms. Finally, numerical results and comparisons with other existing methods are given in Section 8, showing the efficiency of the proposed methods in terms of the results and of the computational time costs.

2 The Heston-Hull-White model

The Heston Hull-White model concerns with cases where the volatility and the interest rate are assumed to be stochastic. The dynamics under the risk neutral measure of the share price and the volatility process are governed by the stochastic differential equation system

with initial data , and , where , and are suitable and possibly correlated Brownian motions. Recall that is a CIR process whereas is a generalized Ornstein-Uhlenbeck (hereafter OU) process: here is not constant but it is a deterministic function which is completely determined by the market values of the zero-coupon bonds (see [7]).

Let us fix the correlations among the Brownian motions. As observed in [15], the important correlations are between the pairs and . So, we assume that is a standard Brownian motion in and is a Brownian motion in which is correlated both with and :

| and . |

By passing to the logarithm in the first component and taking into account the above mentioned correlations, we reduce to the dynamics

where is a standard Brownian motion in and the correlation parameter is given by

As already done in [14], the process can be written in the following way:

| (2.1) |

where

| (2.2) |

So, we can consider the triple , whose dynamics is given by

| (2.3) |

where

| (2.4) | ||||

| (2.5) | ||||

| (2.6) |

The purpose of this paper is to efficiently approximate the process in order to numerically compute the price of options written on the share process .

3 The recombining binomial tree for the pair and

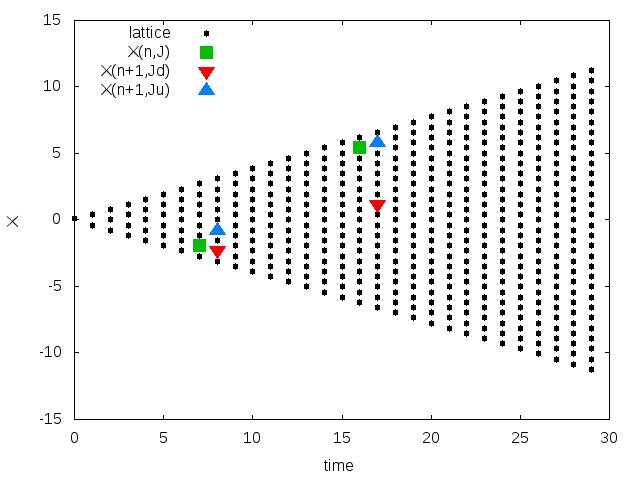

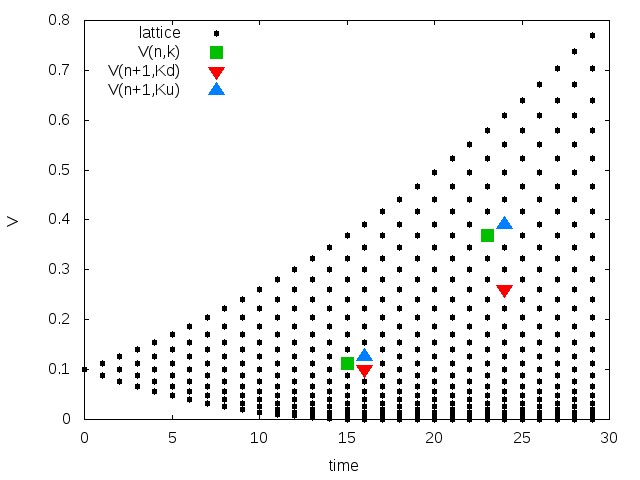

First of all, we consider an approximation for the pair on the time-interval by means of a -dimensional computationally simple tree, that is by means of a Markov chain that runs over a -dimensional recombining bivariate lattice (recombining binomial tree). In the usual case, as in the Cox-Ross-Rubinstein tree [10], at each time step the process can jump either on the nearest up-node or on the nearest down-node. Here, we consider the possibility of “multiple jumps” as introduced in Nelson and Ramaswamy [20]. Roughly speaking, the process can again jump upward or downward but the up/down jump nodes might not be the nearest ones: they are defined as the up/down positions at the next time-step whose associated transition probabilities better interpolate the theoretical expectation of the transition. As discussed in Nelson and Ramaswamy [20], this is the best way to construct an efficient tree for the approximation of one-dimensional diffusion processes, especially when the diffusion coefficient is not constant. Figure 1 shows an example of possible “multiple jumps” for the trees that approximate our processes and , that we are going to describe.

In this section, we consider a discretization of the time-interval in subintervals , , with .

3.1 The tree for

The construction of the recombining binomial tree for the process is quite standard, because here the diffusion coefficient is constant. For , consider the lattice for the process

| (3.1) |

(notice that ). For each fixed , we define the “up” and “down” jump by means of and defined by

| (3.2) | ||||

| (3.3) |

being the drift of the process , see (2.6). As usual, one sets if and if . Note that the up/down jumps in (3.2)-(3.3) might not be the nearest up/down positions in the lattice at time . An example is given in Figure 1-left, where the lattice is drawn and some possible instances of , and are shown to exhibit as the tree can be visited.

The transition probabilities are defined in order to better interpolate the expected local transition: starting from the node , the probability that the process jumps to and at time-step are set as

| (3.4) |

respectively. This gives rise to a Markov chain that weakly converges, as , to the diffusion process and turns out to be a robust tree approximation for the OU process .

3.2 The tree for

For the CIR volatility process , we consider a recombining binomial tree procedure that again follows the “multiple jumps” approach. In this case the recombining lattice is built by means of the transformation

This transformation is particularly important because turns out to be a diffusion process with unit diffusion coefficient, and this fact is useful in order to construct a recombining lattice. Many authors (see e.g. [17] or [23]) propose tree algorithms for by working on the transformed process . The unpleasant fact is that now the drift of is very bad and is such that the approximating process converges only when the Feller condition holds: . In order to overcome this fact, we use the approach in [4], that, roughly speaking, works as follows: the tree structure is built by using again (see next (3.5)) but the possible jumps and the transition probabilities are set on the dynamics of the original (and not transformed) CIR process (see next (3.6)-(3.7) and (3.8)). The main fact is that now the weak convergence on the path space is achieved for every values of , so the Feller condition is not required. Details and comparisons with other tree existing methods to approximate the CIR process are given in [4].

For , consider the lattice

| (3.5) |

(notice that ). For each fixed , we define the “up” and “down” jump by means of

| (3.6) | ||||

| (3.7) |

where the drift of is defined in (2.6) and with the understanding if and if . By construction, the up/down jumps in (3.6)-(3.7) might not be the nearest up/down positions in the lattice at time . In Figure 1-right we show an example of the lattice together with some possible instances of the triple .

The transition probabilities are defined in order to better interpolate the expected local transition: starting from the node the probability that the process jumps to and at time-step are set as

| (3.8) |

respectively. This gives rise to a Markov chain that weakly converges, as , to the diffusion process and turns out to be a robust tree approximation for the CIR process - details are given in [4].

|

|

3.3 The tree for the pair

The tree procedure for the pair is set by joining the trees built for and for . Namely, for , consider the lattice

| (3.9) |

Starting from the node , which corresponds to the position , we define the four possible jump by setting the four nodes at time following the definitions (3.2)-(3.3) and (3.6)-(3.7):

| (3.10) |

where the above probabilities , , and are defined in (3.8) and (3.4) respectively. The above factorization is due to the orthogonality of the noises driving the two processes. As a quite immediate consequence of standard results (see e.g. the techniques in [20]), one gets the following: the associated bivariate Markov chain weakly converges to the diffusion pair solution to

Remark 3.1

In the case one is interested in introducing a correlation between the noises and driving the process and respectively, the joint tree can be constructed on the same lattice but the jump probabilities are no more of a product-type: the transition probabilities , , and can be computed by matching (at the first order in ) the conditional mean and the conditional covariance between the continuous and the discrete processes of and . More precisely, for both components the conditional mean is matched by construction (this is actually the main consequence of the definition of the multiple jumps). As for the conditional covariance, assuming that , with , then one has . Therefore, the matching conditions lead to solving the following system:

where

This is done in [4] in a different context but the proof of the weak convergence on the path space is analogous - this can be done by standard arguments, as in [20] or [12].

4 Approximating the -component: the finite-difference approach

We go now back to (2.3), that is

where , and are given in (2.4), (2.5) and (2.6) respectively. By isolating in the second line and in the third one, we obtain

| (4.1) |

with

| (4.2) |

What we are going to do is mainly based on the fact that the noise is independent of the processes and .

4.1 The approximating scheme for the triple

We consider an approximating process for turning out by freezing the coefficients in (4.1): we define and for with we set

We consider now the approximating tree and we call the associated time-continuous approximating process for the pair , that is

We then assume that the noise driving the pair is independent of the Brownian motion and we insert this discretization for in the discretization scheme for . So, we obtain our final approximating process by setting and for with then

| (4.3) |

Notice that if we set

| (4.4) |

then we have

| (4.5) |

that is solves a SDE with constant coefficients and at time it starts from . Take now a function : we are interested in approximating

By using our scheme and the process in (4.4), we approximate it with the expectation done on the approximating processes, that is

Since is independent of the Brownian noise driving in (4.4), we can write

| (4.6) |

in which

| (4.7) |

Now, in order to compute the above quantity , consider a generic function and set

By (4.5) and the Feynman-Kac representation formula we can state that, for every fixed and , the function is the solution to

| (4.8) |

being given in (4.2). In order to solve the PDE problem (4.8), we use a finite-difference approach.

4.2 Finite-differences

At each time step we numerically solve (4.8) at time by applying finite-difference techniques.

We fix a grid on the -axis , with and . For fixed , and , we set the discrete solution of (4.8) at time on the point of the grid - for simplicity of notations, we do not stress in the dependence on and (from the coefficients of the PDE).

The finite difference method we are going to set is inspired from the one developed in [6]. But a main difference arises: here, we do not distinguish anymore between the diffusion dominant or reaction dominant case and we propose to apply a full implicit finite-difference approximation in time. In fact, the discrete solution to problem (4.8) at time is computed in terms of the solution at time by using the following finite-difference scheme:

| (4.9) |

Of course, (4.9) has to be coupled with suitable numerical boundary relations. We assume that the boundary values are defined by the following Neumann-type conditions:

| (4.10) |

Then, by applying the implicit finite-difference (4.9) coupled with the boundary conditions (4.10), we get the solution by solving the following linear system

| (4.11) |

where is the tridiagonal real matrix given by

| (4.12) |

with

| (4.13) |

being defined in (4.2). We stress that at each time step , the quantities and are constant and known values (defined by the tree procedure for the pair ) and then and are constant parameters too.

One can easily see that the implicit scheme (4.9) is unconditionally stable. Moreover, by applying standard results (Theorem 2.1 in [8] e.g.), the matrix is invertible for . Therefore, setting

| (4.14) |

the numerical solution to (4.8) on the grid through the above discretization procedure is given by

| (4.15) |

Remark 4.1

Other numerical boundary conditions can surely be selected, for example the two boundary values and may be a priori fixed by a known constant (this procedure typically appears in financial problems).

4.3 The scheme on the -component

We can now come back to our original problem, that is the computation of the function in (4.7) allowing one to numerically compute the expectation in (4.6).

We consider the approximating process as described in Section 4.1. This means that the pair at time-step is located on the lattice : and , for . Then (4.15) gives the following approximation: for each ,

Therefore, the expectation in (4.6) is computed on the approximating tree for by means of the above approximation:

| (4.16) |

where

and the jump probabilities are given in (3.10) (or in Remark 3.1 if a correlation is assumed between the noises driving and ).

Similar arguments can be used in order to compute the conditional expectation in the left hand side of (4.16) when the function depends on the variables and also. Then one gets

| (4.17) |

where

| (4.18) |

5 The algorithm for the pricing of American options

The natural application of the hybrid tree/finite-difference approach arises in the pricing of American options. Consider an American option with maturity and payoff function . First of all, we consider the log-price process, so the obstacle will be given by

The price of such an American option is given by (recall the relation between the interest rate and the process : , see (2.1))

where denotes the set of all stopping times taking values on . Hereafter, denotes the solution of the SDE (2.3) starting at at time .

The price at time of such an option is then approximated by a backward dynamic programming algorithm. Consider a discretization of the time interval into subintervals of length : . Then is numerically approximated through the quantity which is iteratively defined as follows: for ,

From the financial point of view, this means to allow the exercise at the fixed dates , .

Consider now the discretization scheme discussed in Section 4. We use the approximation (4.17) for the conditional expectations that have to be computed at each time step . So, for every point , (4.17) gives

| (5.1) |

where denotes the operator in (4.18) applied to the function , that is

| (5.2) |

We finally summarize the backward induction giving our approximating algorithm. For , we define for as follows:

| (5.3) |

Notice that, by (5.2), the computation of requires the knowledge of the function in points ’s that do not necessarily belong to the grid . Therefore, in practice we compute such a function by means of quadratic interpolations.

Remark 5.1

Let us stress that the r.h.s. of (5.1) can be read in two equivalents ways. First, the term

is the numerical solution to the PDE (4.8) with final condition as in (5.2), so the r.h.s. of (5.1) is actually a weighted sum of the four solutions from each jump node for the pair , with weights given by the jump probabilities. But since the differential operator is linear in the Cauchy conditions, then one can first do the weighted sum of the final conditions, that is

and then apply the matrix , i.e. solve the PDE (4.8) just once, and this is of course computationally less expensive.

We can resume the main steps of our algorithm as follows.

-

•

Preprocessing:

-

–

set the lattice , , for the process by using (3.1);

-

–

set the lattice , , for the process the by using (3.5);

-

–

merge the above lattices in a bivariate one , , by using (3.9);

-

–

compute the jump-nodes and the transition probabilities , , using (3.10);

-

–

set a mesh grid , , for the solution of all the PDE’s.

-

–

-

•

Step : for each node , , compute the option prices at maturity for each , , by using the payoff function.

- •

The theoretical proof of the convergence of our method is postponed to a further study. Although the ideas inspiring the method mainly come from [6], here the convergence problem has to be tackled differently. In fact, in [6] the numerical scheme is written through a matrix which is stochastic, so one can link the scheme to a Markov chain that approximates the process and use probabilistic methods (weak convergence) in order to study the convergence. But the scheme proposed here is purely numerical: the matrix in (4.14) is stochastic if and only if , so the link with Markov chains fails and the probabilistic weak convergence cannot be used anymore. So, here we restrict ourselves to the study of the behavior and the efficiency of the proposed approach from the numerical point of view, see next Section 8.

6 Generalization to the Heston-Hull-White2d model

The Heston-Hull-White2d model generalizes the previous model in the fact that the quantity is assumed to be stochastic and to follow a diffusion model itself. So, the underlying process is now -dimensional and is given by: the share price , the volatility process , the interest rate and the continuous dividend rate . Actually, here the process has not necessarily the meaning of a dividend rate, being for example a further interest rate process. In fact, the Heston-Hull-White2d model occurs in multi-currency models with short-rate interest rates, see e.g. [16].

Under the risk neutral measure, the dynamics are governed by the stochastic differential equation

with initial data , where , , and denote possibly correlated Brownian motions. Note that the process evolves as a generalized OU process: is a deterministic function of the time.

We consider non null correlations between the Brownian motions driving the pairs , and , that is

| , , . |

Correlations among the processes , and can be surely inserted (see next Remark 6.1).

As done in Section 2, we take into account the transformations (2.1)-(2.2) for the generalized OU processes: we set

| (6.1) |

where

| (6.2) |

So, by considering the -price process, we reduce to the -dimensional process whose dynamics is given by

| (6.3) |

where

Starting from (6.3), we set-up an approximating procedure similar to the one developed in Section 3 and Section 4. In the following, we briefly describe how to extend such algorithms to the Heston-Hull-White2d model.

6.1 Approximation of

Concerning the triple , we build an approximating tree on as follows:

-

•

we apply the procedure in Section 3.1 to the process ;

-

•

we apply the procedure in Section 3.1 to the process ;

-

•

we apply the procedure in Section 3.2 to the process .

We then get three approximating trees:

| for , for , for . |

Then, we use the null correlation between any two of , and : we concatenate the above trees in order to get a -dimensional approximating tree for by introducing product-type jump probabilities. In other words, we generalize the probabilities in (3.10) for all the possible jumps.

Remark 6.1

One might include correlations between any two of the Brownian motions driving the processes , and . As described in Remark 3.1, the jump probabilities are no more of a product-type but they solve a linear system of equations that must include the matching of the local cross-moments up to order one in .

6.2 The scheme on the -component and the approximating -dimensional process

We repeat the reasonings in Section 4.1 in order to define an approximating time-continuous process for - roughly speaking, it suffices to replace the one-dimensional process in Section 4.1 with the -dimensional process . So, we start from

| (6.4) |

with

| (6.5) |

Then, we apply the finite-difference method in Section 4.2 and we obtain a final difference scheme given by

where, being defined in (6.5) and is given in (4.12) with

| (6.6) |

Finally, we extend the approximation scheme (4.17) to the case in which and the algorithm for the pricing of European or American options described in Section 5.

Remark 6.2

Let us briefly discuss the complexity of our algorithms. At each time step one has to find the solution of a PDE on a grid with points for each fixed values of

-

•

case 1, Heston-Hull-White model: the pair ,

-

•

case 2, Heston-Hull-White2d model: the triple .

The cardinality of all these possible values in case is at most , . For each case, the system of equations (4.11) with tridiagonal matrix (4.12), can be solved by an efficient form of Gaussian elimination requiring a linear cost of order . Therefore, the total cost of our approach is of order

We notice that the use of a full finite-difference scheme could be more expensive for practical computations. Indeed, consider case 1 (Heston-Hull-White model). The solution of a -dimensional problem by applying finite-differences in all three components leads to the inversion of a big band-matrix. To reduce the computational cost, the problem requires to apply appropriate techniques such as ADI (Alternating Direction Implicit) techniques, see [13] and references therein. Specifically, in [13] the authors propose an ADI approach to solve the Heston-Hull-White partial differential equation which needs a non-trivial implementation effort with a computational cost at least of order per time step, so the total cost is of order . Furthermore, as the dimension of the problem increases, it is not clear what happens if the problem is solved with a full finite-difference scheme. In case 2 (Heston-Hull-White2d model), one should solve a 4-dimensional problem, bringing to the inversion of a very big band-matrix. This would give a cost which is hard to be quantified, and possibly in such a case the costs of the two procedures are no longer comparable.

7 The hybrid Monte Carlo algorithm

The approximation we have set-up for the Heston-Hull-White processes can be used to construct a Monte Carlo algorithm. Let us see how one can simulate a single path by using the tree approximation and the standard Euler scheme for the -component. We call it “hybrid” because two different noise sources are considered: we simulate a continuous process in space (the component ) starting from a discrete process in space (the 3-dimensional tree for ).

Concerning the Heston-Hull-White dynamics in Section 2, consider the triple as in (2.3). Let denote the Markov chain that approximates the pair . We construct a sequence approximating at times by means of the Euler scheme defined in (4.3): we set and for with then

| (7.1) |

where is defined in (4.2) and denote i.i.d. standard normal r.v.’s, independent of the noise driving the chain . So, the simulation algorithm is very simple: at each time step , one let the pair evolve on the tree and simulate the process at time by using (7.1).

A similar algorithm can be considered to simulate the Heston-Hull-White2d dynamics in Section 6, that can be seen as a function of the triple in (6.3). Here, we apply the Euler scheme to (6.4). So, let denote the Markov chain approximating , as described in Section 6.1. Starting from (6.4), we approximate the component at times , , as follows: we set and for , then

| (7.2) |

where is defined in (6.5) and denote i.i.d. standard normal r.v.’s, independent of the noise driving the chain . And again, the simulation algorithm is straightforward.

8 Numerical results

In this section we provide numerical results in order to asses the efficiency and the robustness of our hybrid numerical approach. We first consider test experiments for the Heston-Hull-White model for the computation of European, American and barrier options (Section 8.1) and, following Andersen [3], we study Vanilla options with large maturities when the Feller condition is not fulfilled (Section 8.2). Then we test European and American options in the Heston-Hull-White2d model (Section 8.3).

8.1 European, American and barrier options in the Heston-Hull-White model

In the European and American option contracts we are dealing with, we consider the following set of parameters:

-

•

initial share price , strike price , maturity , dividend rate ;

-

•

initial interest rate , speed of mean-reversion , interest rate volatility , time-varying long-term mean which fits the theoretical bond prices to the yield curve observed on the market - to this purpose, we have chosen the interest rate curve given by ;

-

•

initial volatility , long-mean , speed of mean-reversion , volatility of volatility ;

-

•

varying correlations: for the pairs , and , we set and respectively; no correlation is assumed to exist between and .

We notice that, under the above requests, the Feller condition holds. We postpone to next Section 8.2 the analysis of cases in which the Feller condition is not fulfilled.

The numerical study of the hybrid tree/finite-difference method HTFD is split in two cases:

-

-

HTFD1 refers to the (fixed) number of time steps and varying number of space steps ;

-

-

HTFD2 refers to .

Concerning the Monte Carlo method, we compare the results by using the hybrid simulation scheme in Section 7, that we call HMC. We also simulate paths by using the accurate third-order Alfonsi [1] discretization scheme for the CIR stochastic volatility process and by using an exact scheme for the interest rate. These simulating schemes are here called AMC. In both Monte Carlo methods, we consider varying number of time discretization steps and two cases for the number of Monte Carlo iterations:

-

-

HMC1 and AMC1 refer to 50 000 iterations,

-

-

HMC2 and AMC2 refer to 200 000 iterations.

In the European case, the benchmark value B-AMC is computed using the Alfonsi method with discretization time steps and the associated Monte Carlo estimator is computed with 1 million simulations. In the American case, in absence of reliable numerical methods, the benchmark values B-AMC-LS are obtained by the Longstaff-Schwartz [19] Monte Carlo algorithm with exercise dates, combined with the Alfonsi method with discretization time steps and 1 million iterations.

Table 1 reports both European call option prices and implied volatilities results. In Table 2 we provide American call option prices. Table 3 refers to the computational time cost (in seconds) of the different algorithms in the call European case.

The numerical results show that HTFD is accurate, reliable and efficient for pricing European and American options in the Heston-Hull-White model. Moreover, our hybrid Monte Carlo algorithm HMC appears to be competitive with AMC, that is the one from the accurate simulations by Alfonsi [1]: the numerical results are similar in term of precision and variance but HMC is definitely better from the computational times point of view. Additionally, because of its simplicity, HMC represents a real and interesting alternative to AMC. As a further evidence of the accuracy of our methods, in Figure 2 we study the shapes of implied volatility smiles across moneyness using HTFD1 with and and HMC1 with , and we compare the graphs with the results from the benchmark.

In order to study the convergence behavior of our approach HTFD, we consider the convergence ratio proposed in [11], defined as

| (8.1) |

where denotes here the approximated price obtained with number of time steps. Recall that means that . For the sake of comparison with the numerical convergence speed studied in [6], we report ratios for American put options. We split the numerical study in two different cases: when the Feller condition holds and when it does not, the results being given in Table 4 and Table 5 respectively (details on the option parameters are given in the table captions). Both tables give evidence of the numerical convergence, but with some differences. In fact, under the Feller condition (Table 4), the numerical speed of convergence is definitely linear (this is not really surprising because tree methods are usually linear), whereas in the opposite case (Table 5) the behavior is approximately linear.

| HTFD1 | HTFD2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 11.202744 | 11.202744 | 11.340.04 | 11.300.16 | 11.320.08 | 11.340.16 | 11.370.08 | |

| 100 | 11.319814 | 11.331040 | 11.410.16 | 11.380.08 | 11.310.16 | 11.360.08 | ||

| 150 | 11.340665 | 11.349902 | 11.360.16 | 11.360.08 | 11.350.16 | 11.380.08 | ||

| 200 | 11.346972 | 11.355772 | 11.340.16 | 11.370.08 | 11.440.16 | 11.390.08 | ||

| 50 | 12.526779 | 12.526779 | 12.770.04 | 12.660.18 | 12.690.09 | 12.680.18 | 12.790.09 | |

| 100 | 12.720651 | 12.705772 | 12.740.18 | 12.790.09 | 12.630.18 | 12.780.09 | ||

| 150 | 12.754610 | 12.749526 | 12.740.18 | 12.790.09 | 12.680.18 | 12.810.09 | ||

| 200 | 12.760365 | 12.766836 | 12.740.18 | 12.800.09 | 12.750.18 | 12.790.09 | ||

| 50 | 13.853193 | 13.853193 | 14.040.04 | 13.880.19 | 13.920.10 | 13.970.20 | 14.050.10 | |

| 100 | 14.011537 | 14.013063 | 13.910.19 | 14.010.10 | 13.890.19 | 14.060.10 | ||

| 150 | 14.031598 | 14.038361 | 13.940.19 | 14.070.10 | 13.920.20 | 14.080.10 | ||

| 200 | 14.038235 | 14.045612 | 13.990.19 | 14.070.10 | 13.900.19 | 14.060.10 |

| HTFD1 | HTFD2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 0.279002 | 0.279002 | 0.282602 | 0.281649 | 0.282117 | 0.282602 | 0.283389 | |

| 100 | 0.282073 | 0.282367 | 0.284443 | 0.283681 | 0.281815 | 0.283127 | ||

| 150 | 0.282620 | 0.282862 | 0.283034 | 0.283085 | 0.282865 | 0.283652 | ||

| 200 | 0.282785 | 0.283016 | 0.282478 | 0.283408 | 0.285226 | 0.283914 | ||

| 50 | 0.313772 | 0.313772 | 0.320169 | 0.317398 | 0.317958 | 0.317802 | 0.320695 | |

| 100 | 0.318871 | 0.318480 | 0.319306 | 0.320650 | 0.316487 | 0.320432 | ||

| 150 | 0.319764 | 0.319630 | 0.319063 | 0.320716 | 0.317802 | 0.321221 | ||

| 200 | 0.319916 | 0.320086 | 0.319288 | 0.321009 | 0.319643 | 0.320695 | ||

| 50 | 0.348697 | 0.348697 | 0.353623 | 0.349329 | 0.350359 | 0.351777 | 0.353887 | |

| 100 | 0.352873 | 0.352913 | 0.350234 | 0.352954 | 0.349667 | 0.354151 | ||

| 150 | 0.353402 | 0.353580 | 0.350960 | 0.354324 | 0.350458 | 0.354679 | ||

| 200 | 0.353577 | 0.353771 | 0.352184 | 0.354545 | 0.349931 | 0.354151 |

| HTFD1 | HTFD2 | B-AMC-LS | ||

|---|---|---|---|---|

| 50 | 12.090433 | 12.090433 | 12.220.01 | |

| 100 | 12.205014 | 12.212884 | ||

| 150 | 12.224432 | 12.231392 | ||

| 200 | 12.230288 | 12.237054 | ||

| 50 | 12.912708 | 12.912708 | 13.160.02 | |

| 100 | 13.119121 | 13.101073 | ||

| 150 | 13.156492 | 13.149182 | ||

| 200 | 13.162893 | 13.168602 | ||

| 50 | 13.944266 | 13.944266 | 14.150.02 | |

| 100 | 14.125059 | 14.122918 | ||

| 150 | 14.146240 | 14.152060 | ||

| 200 | 14.153288 | 14.160288 |

| HTFD1 | HTDF2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC | |

|---|---|---|---|---|---|---|---|

| 50 | 0.41 | 0.41 | 223.67 | 0.77 | 3.05 | 2.16 | 7.48 |

| 100 | 0.84 | 11.33 | 1.59 | 6.11 | 4.00 | 14.61 | |

| 150 | 1.37 | 49.99 | 2.33 | 9.13 | 5.87 | 21.64 | |

| 200 | 1.87 | 213.06 | 3.11 | 12.73 | 7.61 | 28.85 |

Furthermore, we study the behavior of HTFD in the case of exotic options, namely for continuously monitored barrier options. We consider call up-and-out options, whose payoff is given by

In our numerical experiments, the up barrier is set at and we choose different values for . Table 6 reports European call up-and-out option prices. In the barrier option case, we compare with a benchmark value, called B-AMC, computed by 2 millions iterations which use the Alfonsi AMC method with discretization time steps. The numerical results confirm the reliability of HTFD for barrier options.

| K | Price | Ratio | ||

|---|---|---|---|---|

| 80 | 25 | 50 | 21.494606 | |

| 50 | 100 | 21.534555 | ||

| 100 | 200 | 21.553473 | 2.111762 | |

| 200 | 400 | 21.563911 | 1.812303 | |

| 400 | 800 | 21.569080 | 2.019428 | |

| 100 | 25 | 50 | 12.607035 | |

| 50 | 100 | 12.749006 | ||

| 100 | 200 | 12.815657 | 2.130053 | |

| 200 | 400 | 12.845050 | 2.267634 | |

| 400 | 800 | 12.859561 | 2.025489 | |

| 120 | 25 | 50 | 21.444819 | |

| 50 | 100 | 21.539534 | ||

| 100 | 200 | 21.572106 | 2.907912 | |

| 200 | 400 | 21.586338 | 2.288708 | |

| 400 | 800 | 21.592706 | 2.234825 |

| K | Price | Ratio | ||

|---|---|---|---|---|

| 80 | 25 | 50 | 21.635830 | |

| 50 | 100 | 21.669504 | ||

| 100 | 200 | 21.688879 | 1.738049 | |

| 200 | 400 | 21.700965 | 1.603169 | |

| 400 | 800 | 21.710373 | 1.284610 | |

| 100 | 25 | 50 | 10.649104 | |

| 50 | 100 | 10.762867 | ||

| 100 | 200 | 10.812709 | 2.282480 | |

| 200 | 400 | 10.835512 | 2.185787 | |

| 400 | 800 | 10.848349 | 1.776369 | |

| 120 | 25 | 50 | 20.755654 | |

| 50 | 100 | 20.873859 | ||

| 100 | 200 | 20.908825 | 3.380584 | |

| 200 | 400 | 20.919694 | 3.216994 | |

| 400 | 800 | 20.924295 | 2.362300 |

| HTFD1 | HTFD2 | B-AMC | ||

|---|---|---|---|---|

| 50 | 1.211544 | 1.211544 | ||

| 100 | 1.251453 | 1.255849 | 1.282211 | |

| 150 | 1.264327 | 1.270193 | ||

| 200 | 1.269703 | 1.274332 | ||

| 50 | 1.819848 | 1.819848 | ||

| 100 | 1.941320 | 1.916440 | 1.9475650.01 | |

| 150 | 1.964666 | 1.930681 | ||

| 200 | 1.974201 | 1.933482 | ||

| 50 | 0.697718 | 0.697718 | ||

| 100 | 0.749116 | 0.725243 | 0.7284310.01 | |

| 150 | 0.762224 | 0.726872 | ||

| 200 | 0.766022 | 0.725139 |

8.2 European options with large maturity in the Heston-Hull-White model

In order to verify the robustness of the proposed algorithms we consider experiments when the Feller condition is not fulfilled and with large maturities. We test here the cases I, II, III (reordered with respect to the maturity) proposed in Andersen [3] in order to price European call options. Moreover, we add the case IV with maturity .

We consider the following values for the parameters of the model and for the maturity date:

-

Case I: , , , , , ;

-

Case II: , , , , , .

-

Case III: , , , , , .

-

Case IV: , , , , , .

We take into account varying strikes . No correlation is assumed to exist between and , that is , so we can compare the results with the semi closed-form analytic formula (SCF) for European call options which is available in [13]. We use in particular the implementation of the semi closed-form analytic formula provided in QuantLib [21]. Moreover in all cases the interest rate parameters, the initial share value and the dividend are the same of Section 8.1:

-

•

, ;

-

•

, , .

In Tables 7, 8, 9, 10 we provide European call option prices and implied volatility results. The numerical results suggest that large maturities bring to a slight loss of accuracy for both HTFD and HMC, even if each method provides a satisfactory approximation of the true option prices. It is worth noticing that for long maturities we have developed experiments with the same number of steps both in time () and space () as for . So, the numerical experiments are not slower, and it is clear that one could achieve a better accuracy for larger values of .

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 37.054163 | 37.054163 | 37.491811 | 37.360.47 | 37.320.23 | 37.38 | 37.310.23 | |

| 100 | 37.392491 | 37.395372 | 37.300.45 | 37.520.24 | 37.61 | 37.610.24 | ||

| 150 | 37.480467 | 37.521733 | 37.400.46 | 37.580.24 | 37.55 | 37.580.24 | ||

| 200 | 37.546885 | 37.570675 | 37.420.46 | 37.480.23 | 37.49 | 37.600.24 | ||

| 50 | 23.997806 | 23.997806 | 24.706195 | 24.640.43 | 24.580.21 | 24.61 | 24.540.21 | |

| 100 | 24.537750 | 24.540987 | 24.490.41 | 24.760.21 | 24.79 | 24.810.22 | ||

| 150 | 24.669356 | 24.684708 | 24.600.41 | 24.810.22 | 24.71 | 24.780.22 | ||

| 200 | 24.747161 | 24.766840 | 24.670.42 | 24.700.21 | 24.73 | 24.820.22 | ||

| 50 | 13.672435 | 13.672435 | 14.324566 | 14.330.38 | 14.240.18 | 14.22 | 14.170.18 | |

| 100 | 14.248533 | 14.205762 | 14.110.35 | 14.400.198 | 14.40 | 14.400.19 | ||

| 150 | 14.373163 | 14.318446 | 14.210.36 | 14.430.198 | 14.33 | 14.400.19 | ||

| 200 | 14.444183 | 14.404071 | 14.310.36 | 14.320.188 | 14.31 | 14.420.20 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 0.313372 | 0.313372 | 0.322137 | 0.319432 | 0.318614 | 0.319863 | 0.318541 | |

| 100 | 0.320152 | 0.320209 | 0.318384 | 0.322782 | 0.324521 | 0.324567 | ||

| 150 | 0.321910 | 0.322734 | 0.320315 | 0.323861 | 0.323277 | 0.323956 | ||

| 200 | 0.323236 | 0.323711 | 0.320737 | 0.321815 | 0.322027 | 0.324318 | ||

| 50 | 0.296912 | 0.296912 | 0.306954 | 0.306002 | 0.305124 | 0.30564 | 0.304539 | |

| 100 | 0.304563 | 0.304608 | 0.303947 | 0.307727 | 0.308148 | 0.308367 | ||

| 150 | 0.306431 | 0.306649 | 0.305385 | 0.308440 | 0.307022 | 0.307959 | ||

| 200 | 0.307536 | 0.307815 | 0.306431 | 0.306889 | 0.307262 | 0.308556 | ||

| 50 | 0.291198 | 0.291198 | 0.299737 | 0.299844 | 0.298690 | 0.298395 | 0.240057 | |

| 100 | 0.298743 | 0.298183 | 0.296939 | 0.300702 | 0.240301 | 0.239857 | ||

| 150 | 0.300373 | 0.299657 | 0.298282 | 0.301138 | 0.299848 | 0.300773 | ||

| 200 | 0.301301 | 0.300777 | 0.299533 | 0.299736 | 0.299505 | 0.301033 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 33.702753 | 33.702753 | 34.101622 | 33.590.23 | 33.760.11 | 34.12 | 34.090.11 | |

| 100 | 33.773407 | 34.120510 | 33.980.23 | 34.100.11 | 34.25 | 34.100.11 | ||

| 150 | 33.776196 | 33.818752 | 33.610.23 | 33.760.11 | 34.02 | 34.110.11 | ||

| 200 | 33.778268 | 33.944743 | 33.910.23 | 33.910.11 | 34.00 | 34.100.11 | ||

| 50 | 22.540546 | 22.540546 | 23.140518 | 22.570.21 | 22.650.10 | 23.14 | 23.090.11 | |

| 100 | 22.761622 | 23.076646 | 22.950.21 | 23.060.10 | 23.26 | 23.120.11 | ||

| 150 | 22.795766 | 22.857113 | 22.680.21 | 22.810.10 | 23.04 | 23.090.11 | ||

| 200 | 22.806087 | 22.978809 | 22.960.21 | 22.950.10 | 23.02 | 23.130.11 | ||

| 50 | 13.335726 | 13.335726 | 13.755466 | 13.180.17 | 13.210.08 | 13.72 | 13.680.09 | |

| 100 | 13.510432 | 13.726749 | 13.530.17 | 13.620.09 | 13.86 | 13.720.09 | ||

| 150 | 13.528322 | 13.553294 | 13.340.17 | 13.460.09 | 13.66 | 13.730.09 | ||

| 200 | 13.530288 | 13.639595 | 13.600.17 | 13.600.09 | 13.64 | 13.760.09 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 0.227844 | 0.227844 | 0.234811 | 0.225850 | 0.228795 | 0.235187 | 0.234676 | |

| 100 | 0.229082 | 0.235140 | 0.232714 | 0.234866 | 0.237332 | 0.234768 | ||

| 150 | 0.229131 | 0.229876 | 0.226245 | 0.228809 | 0.233392 | 0.235042 | ||

| 200 | 0.229167 | 0.232077 | 0.231443 | 0.231474 | 0.232965 | 0.234723 | ||

| 50 | 0.215548 | 0.215548 | 0.222789 | 0.215951 | 0.216908 | 0.222801 | 0.222156 | |

| 100 | 0.218214 | 0.222017 | 0.220435 | 0.221799 | 0.224184 | 0.222572 | ||

| 150 | 0.218625 | 0.219366 | 0.217216 | 0.218739 | 0.221545 | 0.222656 | ||

| 200 | 0.218750 | 0.220835 | 0.220583 | 0.220512 | 0.221377 | 0.222760 | ||

| 50 | 0.210662 | 0.210662 | 0.215154 | 0.209030 | 0.209283 | 0.214777 | 0.214386 | |

| 100 | 0.212532 | 0.214847 | 0.212764 | 0.213679 | 0.216253 | 0.214726 | ||

| 150 | 0.212723 | 0.212991 | 0.210669 | 0.212018 | 0.214162 | 0.214846 | ||

| 200 | 0.212744 | 0.213914 | 0.213460 | 0.213506 | 0.213908 | 0.215215 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 32.872766 | 32.872766 | 33.182814 | 33.170.31 | 33.260.16 | 33.130.31 | 33.180.16 | |

| 100 | 33.041266 | 33.161213 | 33.100.30 | 33.290.15 | 33.180.31 | 33.190.15 | ||

| 150 | 33.098186 | 33.159078 | 33.030.30 | 33.120.16 | 33.200.34 | 33.250.16 | ||

| 200 | 33.150052 | 33.235555 | 33.020.29 | 33.110.15 | 33.120.33 | 33.350.15 | ||

| 50 | 24.738008 | 24.738008 | 25.183109 | 25.000.30 | 25.050.15 | 25.100.30 | 25.170.15 | |

| 100 | 24.979024 | 25.089961 | 24.960.29 | 25.180.15 | 25.200.30 | 25.200.15 | ||

| 150 | 25.047214 | 25.150207 | 24.990.28 | 25.110.15 | 25.170.33 | 25.230.16 | ||

| 200 | 25.103492 | 25.224136 | 24.970.28 | 25.090.15 | 25.070.31 | 25.300.15 | ||

| 50 | 17.522401 | 17.522401 | 17.851374 | 17.490.27 | 17.530.14 | 17.760.27 | 17.840.14 | |

| 100 | 17.702990 | 17.779408 | 17.510.26 | 17.740.14 | 17.850.28 | 17.860.15 | ||

| 150 | 17.752550 | 17.858103 | 17.590.26 | 17.770.14 | 17.820.31 | 17.870.14 | ||

| 200 | 17.800293 | 17.912261 | 17.590.25 | 17.750.13 | 17.730.29 | 17.930.14 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 0.231761 | 0.231761 | 0.237013 | 0.236812 | 0.238369 | 0.236053 | 0.236928 | |

| 100 | 0.234617 | 0.236648 | 0.235577 | 0.238826 | 0.236974 | 0.237216 | ||

| 150 | 0.235581 | 0.236612 | 0.234478 | 0.235946 | 0.237321 | 0.238081 | ||

| 200 | 0.236459 | 0.237905 | 0.234214 | 0.235730 | 0.235877 | 0.239816 | ||

| 50 | 0.225390 | 0.225390 | 0.230837 | 0.228633 | 0.22926 | 0.229786 | 0.230708 | |

| 100 | 0.228336 | 0.229695 | 0.228045 | 0.230802 | 0.231012 | 0.231068 | ||

| 150 | 0.229171 | 0.230433 | 0.228424 | 0.229935 | 0.230683 | 0.231375 | ||

| 200 | 0.229861 | 0.231340 | 0.228236 | 0.229682 | 0.229474 | 0.232223 | ||

| 50 | 0.223601 | 0.223601 | 0.227024 | 0.223225 | 0.223688 | 0.226081 | 0.226894 | |

| 100 | 0.225479 | 0.226275 | 0.223424 | 0.225813 | 0.227054 | 0.227136 | ||

| 150 | 0.225995 | 0.227094 | 0.224321 | 0.226215 | 0.226728 | 0.227195 | ||

| 200 | 0.226492 | 0.227659 | 0.224316 | 0.225961 | 0.225781 | 0.227881 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 28.772135 | 28.772135 | 28.969593 | 29.010.29 | 29.050.15 | 28.920.29 | 28.980.15 | |

| 100 | 28.890859 | 29.076376 | 29.060.34 | 29.000.15 | 28.990.29 | 28.970.15 | ||

| 150 | 29.007171 | 29.225059 | 29.070.29 | 29.150.15 | 28.900.31 | 29.050.15 | ||

| 200 | 29.125812 | 29.152251 | 29.050.31 | 28.910.15 | 28.950.29 | 29.010.14 | ||

| 50 | 23.947048 | 23.947048 | 24.255944 | 24.090.28 | 24.130.15 | 24.200.29 | 24.260.15 | |

| 100 | 24.107443 | 24.300298 | 24.220.33 | 24.190.155 | 24.270.28 | 24.250.15 | ||

| 150 | 24.233382 | 24.462163 | 24.260.28 | 24.370.155 | 24.170.31 | 24.330.15 | ||

| 200 | 24.356051 | 24.436578 | 24.320.31 | 24.200.145 | 24.220.28 | 24.310.14 | ||

| 50 | 19.352114 | 19.352114 | 19.601699 | 19.210.27 | 19.240.14 | 19.520.27 | 19.590.14 | |

| 100 | 19.459177 | 19.637550 | 19.390.32 | 19.390.14 | 19.620.27 | 19.590.14 | ||

| 150 | 19.567765 | 19.778396 | 19.510.27 | 19.620.14 | 19.510.30 | 19.660.14 | ||

| 200 | 19.692584 | 19.798050 | 19.600.30 | 19.530.14 | 19.550.27 | 19.650.13 |

| HTFD1 | HTFD2 | SCF | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 50 | 0.235972 | 0.235972 | 0.239830 | 0.240620 | 0.241466 | 0.238797 | 0.240057 | |

| 100 | 0.238291 | 0.241919 | 0.241551 | 0.240401 | 0.240301 | 0.239857 | ||

| 150 | 0.240565 | 0.244831 | 0.241698 | 0.243433 | 0.239857 | 0.241365 | ||

| 200 | 0.242887 | 0.243405 | 0.241403 | 0.238618 | 0.239442 | 0.239442 | ||

| 50 | 0.231127 | 0.231127 | 0.235633 | 0.233270 | 0.233862 | 0.234826 | 0.235633 | |

| 100 | 0.233464 | 0.236283 | 0.235133 | 0.234655 | 0.235771 | 0.235536 | ||

| 150 | 0.235303 | 0.238656 | 0.235636 | 0.237270 | 0.234367 | 0.236650 | ||

| 200 | 0.237099 | 0.238281 | 0.236537 | 0.234765 | 0.235096 | 0.236425 | ||

| 50 | 0.229635 | 0.229635 | 0.232641 | 0.227954 | 0.228325 | 0.231645 | 0.232511 | |

| 100 | 0.230923 | 0.233074 | 0.230084 | 0.230128 | 0.233016 | 0.232455 | ||

| 150 | 0.2332231 | 0.234777 | 0.231504 | 0.232913 | 0.231583 | 0.233359 | ||

| 200 | 0.2333739 | 0.235015 | 0.232634 | 0.231717 | 0.232046 | 0.233281 |

8.3 European and American options in the Heston-Hull-White2d model

In the European and American option contracts we are dealing with, we consider the following set of parameters:

-

•

, , ;

-

•

, , , ;

-

•

, , , ;

-

•

, , , ;

-

•

,

As before, the time-varying long-term means and fit the theoretical bond prices and to the yield curve observed on the market. We make this choice following the multi-currency models with short-rate interest rates in [16]. We consider here only the number of space steps because the cases need a too high computational time. Tables 11, 12 and 13 report European and American call option prices and implied volatilities. As before, the benchmark value for European options is computed using the Alfonsi B-AMC method with discretization time steps and the associated Monte Carlo estimator is computed with 1 million iterations. Concerning the benchmark B-AMC-LS for American options, it is computed by means of the Longstaff-Schwartz [19] Monte Carlo algorithm with exercise dates, combined with the Alfonsi method with discretization time steps and 1 million iterations. Table 14 refers to the computational time cost (in seconds) of the different algorithms in the call European case. In Figure 3 we compare the shapes of implied volatility smiles across moneyness using HTFD1 with and and HMC1 with . The numerical results confirm the good numerical behavior of HTFD and HMC in the Heston-Hull-White2d model as well.

| HTFD1 | HTFD2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 30 | 13.470572 | 13.470572 | 13.79 0.04 | 13.820.20 | 13.740.10 | 13.830.20 | 13.790.10 | |

| 50 | 13.688842 | 13.671173 | 13.960.20 | 13.810.10 | 13.880.20 | 13.800.10 | ||

| 100 | 13.790205 | 13.781519 | 14.000.20 | 13.800.10 | 13.680.20 | 13.730.10 | ||

| 30 | 14.736242 | 14.736242 | 15.04 0.05 | 15.100.22 | 14.990.11 | 14.950.22 | 15.030.11 | |

| 50 | 14.958094 | 14.946029 | 15.230.22 | 15.040.11 | 14.980.22 | 15.010.11 | ||

| 100 | 15.019204 | 15.032709 | 15.210.22 | 15.040.11 | 14.800.21 | 14.970.11 | ||

| 30 | 15.805046 | 15.805046 | 16.19 0.03 | 16.130.23 | 16.060.11 | 16.040.23 | 16.170.12 | |

| 50 | 16.052315 | 16.032043 | 16.330.23 | 16.100.11 | 16.090.23 | 16.130.12 | ||

| 100 | 16.155354 | 16.145308 | 16.240.23 | 16.190.12 | 15.930.23 | 16.120.12 |

| HTFD1 | HTFD2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 30 | 0.338612 | 0.338612 | 0.347031 | 0.347724 | 0.345593 | 0.348085 | 0.347031 | |

| 50 | 0.344364 | 0.343898 | 0.351511 | 0.347675 | 0.349404 | 0.347294 | ||

| 100 | 0.347036 | 0.346807 | 0.352510 | 0.347205 | 0.344131 | 0.345449 | ||

| 30 | 0.372004 | 0.372004 | 0.380033 | 0.381610 | 0.378689 | 0.377653 | 0.379769 | |

| 50 | 0.377867 | 0.377549 | 0.385153 | 0.380032 | 0.378447 | 0.379240 | ||

| 100 | 0.379483 | 0.379840 | 0.384419 | 0.380061 | 0.373689 | 0.378182 | ||

| 30 | 0.400281 | 0.400281 | 0.410485 | 0.408889 | 0.407043 | 0.406508 | 0.409954 | |

| 50 | 0.406834 | 0.406297 | 0.414273 | 0.408039 | 0.407833 | 0.408894 | ||

| 100 | 0.409566 | 0.409300 | 0.411792 | 0.410506 | 0.403592 | 0.408629 |

| HTFD1 | HTFD2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 30 | 9.418513 | 9.418513 | 9.61 0.03 | 9.570.13 | 9.620.07 | 9.640.13 | 9.660.07 | |

| 50 | 9.552565 | 9.532194 | 9.570.13 | 9.610.07 | 9.650.13 | 9.660.07 | ||

| 100 | 9.633716 | 9.607339 | 9.660.13 | 9.620.07 | 9.630.13 | 9.630.07 | ||

| 30 | 10.916753 | 10.916753 | 11.18 0.03 | 11.150.15 | 11.160.08 | 11.070.15 | 11.220.08 | |

| 50 | 11.117050 | 11.100343 | 11.180.15 | 11.160.08 | 11.140.15 | 11.220.08 | ||

| 100 | 11.178119 | 11.173631 | 11.160.15 | 11.180.08 | 11.080.15 | 11.200.08 | ||

| 30 | 12.203271 | 12.203271 | 12.55 0.04 | 12.440.17 | 12.430.09 | 12.470.17 | 12.600.09 | |

| 50 | 12.443197 | 12.411406 | 12.540.17 | 12.440.09 | 12.530.17 | 12.590.09 | ||

| 100 | 12.552842 | 12.522237 | 12.450.17 | 12.550.09 | 12.450.17 | 12.580.09 |

| HTFD1 | HTFD2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | ||

|---|---|---|---|---|---|---|---|---|

| 30 | 0.232267 | 0.232267 | 0.237277 | 0.236285 | 0.237525 | 0.238062 | 0.238586 | |

| 50 | 0.235774 | 0.235241 | 0.236157 | 0.237263 | 0.238324 | 0.238586 | ||

| 100 | 0.237898 | 0.237208 | 0.238622 | 0.237412 | 0.237800 | 0.237800 | ||

| 30 | 0.271502 | 0.271502 | 0.278405 | 0.277704 | 0.277855 | 0.275520 | 0.279454 | |

| 50 | 0.276754 | 0.276316 | 0.278277 | 0.277937 | 0.277356 | 0.279454 | ||

| 100 | 0.278356 | 0.278238 | 0.277841 | 0.278435 | 0.275782 | 0.278930 | ||

| 30 | 0.305269 | 0.305269 | 0.314383 | 0.311364 | 0.311103 | 0.312279 | 0.315698 | |

| 50 | 0.311575 | 0.310739 | 0.313992 | 0.311570 | 0.313857 | 0.315435 | ||

| 100 | 0.314458 | 0.313653 | 0.311665 | 0.314463 | 0.311754 | 0.315172 |

| HTFD1 | HTFD2 | B-AMC-LS | ||

|---|---|---|---|---|

| 30 | 14.057963 | 14.057963 | 14.40 0.02 | |

| 50 | 14.290597 | 14.263254 | ||

| 100 | 14.400377 | 14.381552 | ||

| 30 | 14.989844 | 14.989844 | 15.32 0.02 | |

| 50 | 15.253011 | 15.229151 | ||

| 100 | 15.320569 | 15.331744 | ||

| 30 | 15.826696 | 15.826696 | 16.28 0.02 | |

| 50 | 16.146080 | 16.111559 | ||

| 100 | 16.270439 | 16.248656 |

| HTFD1 | HTFD2 | B-AMC-LS | ||

|---|---|---|---|---|

| 30 | 11.598655 | 11.598655 | 11.72 0.02 | |

| 50 | 11.707669 | 11.681873 | ||

| 100 | 11.775632 | 11.743388 | ||

| 30 | 12.400256 | 12.400256 | 12.60 0.02 | |

| 50 | 12.579124 | 12.561214 | ||

| 100 | 12.634969 | 12.629401 | ||

| 30 | 13.137621 | 13.137621 | 13.47 0.02 | |

| 50 | 13.380571 | 13.341882 | ||

| 100 | 13.497053 | 13.459978 |

| HTFD1 | HTDF2 | B-AMC | HMC1 | HMC2 | AMC1 | AMC2 | |

|---|---|---|---|---|---|---|---|

| 30 | 2.22 | 2.22 | 284.84 | 0.60 | 2.61 | 1.79 | 6.03 |

| 50 | 4.15 | 24.56 | 1.14 | 4.19 | 2.73 | 9.58 | |

| 100 | 7.95 | 998.1 | 2.02 | 8.06 | 5.05 | 18.70 |

9 Conclusions

We have introduced a new hybrid tree/finite-difference method and a new Monte Carlo method for numerically pricing options in a stochastic volatility framework with stochastic interest rates. The numerical comparisons show that our methods provide a good approximation of the option prices with efficient time computations.

Acknowledgements. The authors wish to thank Andrea Molent for useful remarks and for having implemented the Alfonsi Monte Carlo scheme and the Longstaff-Schwarz algorithm.

References

- [1] A. Alfonsi (2010): High order discretization schemes for the CIR process: application to affine term structure and Heston models, Mathematics of Computation, 79, 209-237.

- [2] K. Amin, A. Khanna (1994): Convergence of American option values from discrete-to continuous-time financial models , Mathematical Finance, 4, 289-304.

- [3] L. Andersen (2006): Efficient Simulation of the Heston Stochastic Volatility Model. Preprint available at http://www.ressources-actuarielles.net/

- [4] E. Appolloni, L. Caramellino, A. Zanette (2015): A robust tree method for pricing American options with CIR stochastic interest rate. IMA Journal of Management Mathematics, 26, 345-375.

- [5] A. Berman, R. J. Plemmons (1994): Nonnegative matrices in the mathematical sciences, Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA.

- [6] M. Briani, L. Caramellino, A. Zanette (2015): A hybrid approach for the implementation of the Heston model. IMA Journal of Management Mathematics, to appear. ArXiv:1307.7178.

- [7] D. Brigo, F. Mercurio (2006): Interest Rate Models-Theory and Practice. Springer, Berlin.

- [8] L. Brugnano, D. Trigiante (1992): Tridiagonal matrices: Invertibility and conditioning, Linear Algebra and its Applications, 166, 131-150.

- [9] J.C. Cox, J. Ingersoll, S. Ross (1985): A theory of the term structure of interest rates, Econometrica, 53, 385-407.

- [10] J. Cox, S.A. Ross, M. Rubinstein (1979): Option pricing: a simplifiled approach. Journal of Financial Economics 7, 229-263.

- [11] V. D’Halluin, P.A. Forsyth, G. Labahn (2005): A semi-Lagrangian Approach for American Asian options under jump-diffusion, Siam J.Sci.Comp. 27, 315-345.

- [12] S.N. Ethier, T. Kurtz (1986): Markov processes: characterization and convergence. John Wiley & Sons, New York.

- [13] T. Haentjens, K.J. in’t Hout (2012): Alternating direction implicit finite difference schemes for the Heston-Hull-White partial differential equation. J. Comp. Finan. 16, 83–110.

- [14] J. Hull, A. White A (1994): Numerical procedures for implementing term structure models I. Journal of Derivatives 2(1), 7-16.

- [15] A.L. Grzelak, C.W. Oosterlee (2011): On the Heston model with stochastic interest rates. SIAM J. Fin. Math. 2, 255-286.

- [16] A.L. Grzelak, C.W. Oosterlee (2012): On the Cross-currency with stochastic volatility and stochastic interest rate. Applied Mathematical Finance 19(1), 1-35

- [17] J.E. Hilliard, A.L. Schwartz, A.L. Tucker (1996): Bivariate binomial pricing with generalized interest rate processes. The Journal of Financial Research, XIX-4, 585-602.

- [18] D. Lamberton, G. Pagès (1990): Sur l’approximation des réduites. Ann. Inst. H. Poincaré, Probab. et Statistiques 26, 331-355.

- [19] F.A. Longstaff, E.S. Schwartz (2001): Valuing American options by simulations: a simple least squares approach. The Review of Financial Studies, 14, 113-148.

- [20] D.B. Nelson, K. Ramaswamy (1990): Simple binomial processes as diffusion approximations in financial models. The Review of Financial Studies, 3, 393-430.

- [21] QuantLib. A free/open-source library for quantitative finance. http://quantlib.org/index.shtml

- [22] M. Vellekoop, H. Nieuwenhuis (2009): A tree-based method to price American Options in the Heston Model. The Journal of Computational Finance, 13, 1–21.

- [23] J.Z. Wei (1996): Valuing American equity options with a stochastic interest rate: a note. The Journal of Financial Engineering, 2, 195-206.

- [24]