Utility maximization with random horizon: a BSDE approach

| Monique Jeanblanc 111The research of Monique Jeanblanc is supported by Chaire Markets in transition, French Banking Federation. | Thibaut Mastrolia 333Thibaut Mastrolia is grateful to Région Ile de France for financial support and acknowledges INSA de Toulouse for its warm hospitality. | |

| Université d’Evry Val d’Essonne 222Laboratoire de Mathématiques et Modélisation d’Évry (LaMME), Université d’Évry-Val-d’Essonne, UMR CNRS 8071, IBGBI, 23 Boulevard de France, 91037 Evry Cedex, France | Université Paris Dauphine 444Place du Maréchal de Lattre de Tassigny, 75775 Paris Cedex 16, France | |

| LaMME, UMR CNRS 8071 | CEREMADE UMR CNRS 7534 | |

| monique.jeanblanc@univ-evry.fr | thibaut.mastrolia@ceremade.dauphine.fr | |

| Dylan Possamaï | Anthony Réveillac | |

| Université Paris Dauphine 444Place du Maréchal de Lattre de Tassigny, 75775 Paris Cedex 16, France | INSA de Toulouse 555INSA, Département GMM, 135 avenue de Rangueil, F-31077 Toulouse Cedex 4, France | |

| CEREMADE UMR CNRS 7534 | IMT UMR CNRS 5219 | |

| dylan.possamai@ceremade.dauphine.fr | Université de Toulouse | |

| anthony.reveillac@insa-toulouse.fr |

Abstract

In this paper we study a utility maximization problem with random horizon and reduce it to the analysis of a specific BSDE, which we call BSDE with singular coefficients, when the support of the default time is assumed to be bounded. We prove existence and uniqueness of the solution for the equation under interest. Our results are illustrated by numerical simulations.

Key words: quadratic BSDEs, enlargement of filtration, credit risk.

AMS 2010 subject classification: Primary: 60H10, 91G40; Secondary: 91B16, 91G60, 93E20, 60H20.

1 Introduction

In recent years, the notion of risk in financial modeling has received a growing interest. One of the most popular direction so far is given by model uncertainty where the parameters of the stochastic processes driving the financial market are assumed to be unknown (usually referred as drift or volatility uncertainty). Another source of risk consists in an exogenous process which brings uncertainty on the market or on the economy. This kind of situation fits, for instance, in the credit risk theory. As an example, consider an investor who may not be allowed to trade on the market after the realization of some random event, at a random time , which is thought to be unpredictable and external to the market. In that context is seen as the time of a shock that affects the market or the agent. More precisely, assume that an agent initially aims at maximizing her expected utility on a given financial market during a period , where is a fixed deterministic maturi ty. However, she may not have access to the market after the random time . In that context we think of as a death time, either for the agent herself, or for the market (or a specific component of it) she is currently investing in. Though very little studied in the literature, our conviction is that such an assumption can be quite relevant in practice. Indeed, for instance many life-insurance type markets consists of products with very long maturities (up to 95 years for universal life policies and to 120 years for whole life maturity). It is therefore reasonable to consider that during such a period of time an agent in age of investing money in the market will die with probability . Another example is given by markets whose maximal lifetime is finite and known at the beginning of the investment period, like for instance carbon emission markets in the United States.

Mathematically, while her original problem writes down as

| (1.1) |

with the set of admissible strategies for the agent with associated wealth process and where is a utility function which models her preferences, due to the risk associated with the presence of , her optimization program actually has to be formulated as

| (1.2) |

which falls into the class of a priori more complicated stochastic control problems with random horizon.

The main approach to tackle (1.2) consists in rewriting it as a utility maximization problem with deterministic horizon of the form (1.1), but with an additional consumption component using the following decomposition from [10] that we recall:

with and being the underlying filtration on the market. This direction was first followed in [22] when is a -stopping time, then in [6] and in [7] if is a general random time. In all these papers, the convex duality theory (see e.g. [5] and [21]) is exploited to prove the existence of an optimal strategy. However, this approach does not provide a characterization of either the optimal strategy or of the value function (note that in [6] a dynamic programming equation can be derived if one assumes that is deterministic and is a Constant Relative Risk Aversion (CRRA) utility function). Another route is to adapt to the random horizon setting the, by now well-known, methodology in which one reduces the analysis of a stochastic control problem with fixed deterministic horizon to the one of a Backward Stochastic Differential Equation (BSDE) as in [16, 29]. This program has been successfully carried out in [24] in which Problem (1.2) has been proved to be equivalent to solving a BSDE with random horizon of the form

| (1.3) |

in the context of mean-variance hedging, with and a standard Brownian motion. The interesting feature here lies in the fact that under some assumptions on the market, the solution triplet to the previous BSDE is completely described in terms of the one of a BSDE with deterministic finite horizon. More precisely, if we assume that is the natural filtration of and if is a random time which is not a -stopping time, then the BSDE with deterministic horizon associated with BSDE (1.3) is of the form

| (1.4) |

with related to through a predictable process (see Section 2.2 for a precise statement on this relationship). The usual hypothesis, for instance in credit risk modeling, is to assume to be bounded (as in [24]). This assumption, which looks pretty harmless, leads in fact to several consequences both on the modeling of the problem and on the analysis required to solve Equation (1.3). Indeed, is bounded implies that the support111i.e. the smallest closed Borelian set such that of is unbounded. As a consequence, the probability of the event is positive. Hence it does not take into account the situation where is smaller than with probability one. Note that from the very definition of (1.2), assuming to have a bounded or an unbounded support leads to two different economic problems: if the support is unbounded, with positive probability the agent will be able to invest on the market up to time , whereas if is known to be smaller than with probability one, the agent knows she will not have access to the market on the whole time interval .

The main goal of this paper is to solve (1.2) when the support of is assumed to be a bounded interval in . As explained in the previous paragraph, this assumption leads to the unboundedness of . More precisely, it generates a singularity in Equation (1.3) (or in (1.4)) as is integrable on any interval with , and is not integrable on . This drives one to study a new class of BSDEs, named as BSDEs with singular driver according to [18], which requires a specific analysis. We stress that the study of the BSDE of interest of the form (1.4) with to be specified later is not contained in [18], and hence calls for new developments presented in this paper. Incidentally, we propose a unified theory which covers both cases of bounded and unbounded support for (see Conditions H2, H2’ for a precise statement).

The rest of this paper is organized as follows. In the next section we provide some preliminaries and notations and make precise the maximization problem under interest. Then in Section 3, we extend the results of [16, 24] allowing to reduce the maximization problem with exponential utility to the study of a Brownian BSDE. The analysis of this equation is done in Section 4. To illustrate our findings, and to compare problems of the form (1.1) and (1.2), we collect in Section 5 numerical simulations together with some discussion.

Notations: Let and let be the set of real positive numbers. Throughout this paper, for every -dimensional vector with , we denote by its coordinates and for we denote by the usual inner product, with associated norm , which we simplify to when is equal to . For any , will denote the space of matrices with real entries. When , we let . For any , will denote the usual transpose of . For any , will stand for the matrix whose diagonal is and for which off-diagonal terms are , and will be the identity of . In this pape r the integrals will stand for . For any and for any Borel measurable subset , will denote the Borel -algebra on . Finally, we set for any , for any closed subset of and for any

and

2 Preliminaries

2.1 The utility maximization problem

Set a fixed deterministic positive maturity. Let be a -dimensional Brownian motion () defined on a filtered probability space , where denotes the natural completed filtration of , satisfying the usual conditions. is a given -field which strictly contains and which will be specified later. Unless otherwise stated, all equalities between random variables on are to be understood to hold , and all equalities between processes are to be understood to hold (and are as usual extended to hold for every , if the considered processes have trajectories which are, , càdlàg222As usual, we use the french acronym ”càdlàg” for trajectories which are right-continuous and admit left limits, -a.e.). The symbol will alwa ys correspond to an expectation taken under , unless specifically stated otherwise.

We define a financial market with a riskless bond denoted by whose dynamics are given as follows:

where is a fixed deterministic non-negative real number. We enforce throughout the paper the condition

and emphasize that solving the utility maximization problem considered in this paper with a non-zero interest rate is a much more complicated problem.

Moreover, we assume that the financial market contains a -dimensional risky asset ()

In that setting, is a -valued, -predictable bounded process such that is invertible, and uniformly elliptic333i.e. there exists , s.t. ,, ., and a -valued bounded -predictable process.

We aim at studying the optimal investment problem of a small agent on the above-mentioned financial market with respect to a given utility function (that is an increasing, strictly concave and real-valued function, defined either on or on ), but with a random time horizon modeled by a (-measurable) random time . More precisely the optimization problem writes down as:

| (2.1) |

where is the set of admissible strategies which will be specified depending on the definition of . The wealth process associated to a strategy is denoted (see (3.3) below for a precise definition) and is the liability which is assumed to be bounded, and whose measurability will be specified later. The important feature of the random time is that it cannot be explained by the stock process only, in other words it brings some uncertainty in the model. This can be mathematically translated into the fact that is assumed not to be an -stopping time.

2.2 Enlargement of filtration

In a general case, can be considered as a default time (see [4] for more details). We introduce the right-continuous default indicator process by setting

We therefore use the standard approach of progressive enlargement of filtration by considering the smallest right continuous extension of that turns into a -stopping time. More precisely is defined by

for all , where , for all .

The following two assumptions on the model we consider will always be, implicitly or explicitly, in force throughout the paper

-

(H1)

(Density hypothesis) For any , there exists a map , such that is -mesurable and such that

and .

Under (H1), we recall that the "Immersion hypothesis" is satisfied, that is, any -martingale is a -martingale.

Remark 2.1.

If instead of considering Assumption H1, we had considered the following weaker assumption

For any , there exists a map , such that is -mesurable and such that

then, the immersion hypothesis may not be satisfied and in general we can only say that the Brownian motion is a -semimartingale of the form where is a -Brownian motion and . Hence, it suffices to write the dynamics of as

The difficulty is that there is no general condition to ensure that is bounded. Nonetheless, if, for instance, we were to assume that there are no arbitrage opportunities on the market and that we restricted our admissible strategies to the ones which are absolutely continuous, then we could prove that , which may be enough in order to solve the problem.

In both cases, the process admits an absolutely continuous compensator, i.e., there exists a non-negative -predictable process , called the -intensity, such that the compensated process defined by

| (2.2) |

is a -martingale.

The process vanishes after , and we can write , where

is an -predictable process, which is called the -intensity of the process . Under the density hypothesis, is not an -stopping time, and in fact, avoids -stopping times and is a totally inaccessible -stopping time, see [12, Corollary 2.2]. From now on, we use a simplified notation and write and set

Let (resp. ) be the set of -stopping times (resp. -stopping times) less or equal to .

In this paper we will work with two different assumptions. The first one corresponds to the case where the support of is unbounded, and the second one refers to the situation where this support is of the form with . In the latter, without loss of generality, we will assume for the sake of simplicity, that . More precisely, we will assume that one of the two following conditions is satisfied

-

(H2)

.

-

(H2’)

and for all and .

Under the filtration , we deduce from the tower property for conditional expectations that

-

•

(H2) .

-

•

(H2’) for all and .

We emphasize that assuming H2 or H2’ implies in particular that the martingale is in BMO (see below for more details), which implies by the well-known energy inequalities (see for instance [17]) the existence of moments of any order for . More precisely, we have for any

| (H2) | (2.3) | |||

| (H2’) | (2.4) |

Furthermore, since by [12, Proposition 4.4], , for every we have:

-

•

(H2)

-

•

(H2’) ,

where Supp denotes the support of the -stopping time .

The previous remark entails in particular that (H2) and (H2’) lead to quite different maximization problems. The model under Assumption (H2) is the one which is the most studied in the literature and expresses the fact that with positive probability, the problem (2.1) is the same as the classical maximization problem with terminal time . Naturally, the expectation formulation puts a weight on the scenarii which, indeed, lead to the classical framework. Assumption (H2’) expresses the fact that with probability the final horizon is less than (see Figure 2 for an example). This makes the problem completely different since in the first case the agent fears that some random event may happen, whereas in the second case she knows that it is going to happen. As a consequence, these two different assumptions should make some changes in the mathematical analysis. This feature will become quite transparent when solving BSDEs related to the maximi zation problem.

For any , we denote by (resp. ) the set of (resp. )-predictable processes valued in . If we simply write for , and the same for . We recall from [20, Lemma 4.4] the decomposition of any -predictable process , given by

| (2.5) |

Here the process is -predictable, and for a given non-negative , the process with is an -predictable process. Furthermore, for fixed , the mapping is -measurable. Moreover, if the process is uniformly bounded, then it is possible to choose and to be bounded.

We introduce the following spaces

In the following, let be in (resp. ), for the sake of simplicity, we use the notation (resp. ). We conclude this section with a sufficient condition for the stochastic exponential of a càdlàg martingale to be a true martingale. Given a -semimartingale , we denote by its Doléans-Dade stochastic exponential, defined as usual by:

with and where denotes the continuous part of . A càdlàg -martingale is said to be in BMO if

For simplicity, we will omit the -dependence in the space BMO and will only specify the underlying probability measure if it is different from .

Proposition 2.2.

[11, VII.76] The jumps of a BMO martingale are bounded.

The previous proposition together with the definition of a BMO martingale imply that it is enough for to be a BMO martingale, that it has bounded jumps and satisfies:

For the class of BMO martingale we have the following property.

Proposition 2.3.

[17, Theorem 2] Assume that is a martingale such that there exists such that and , and which satisfies

Then is a BMO martingale and is a uniformly integrable martingale.

We set for

and use the same convention consisting in omitting the dependence unless we are working with another probability measure.

3 Exponential utility function

We study in this article a "usual" utility function, namely the exponential function, to solve the utility maximization problem (2.1), which is open in the framework of random time horizon. By open we mean that, even though we have seen that the existence of an optimal strategy for general utility function has been given in [7] using a duality approach, we here aim at characterizing both the optimal strategy and the value function. To that purpose, we combine the martingale optimality principle and the theory of BSDEs with random time horizon. Note that in the classical utility maximization problem with time horizon this technique has been successfully applied in [29] in the exponential framework, and in [16] for the three classical utility functions, that is exponential, power and logarithm.

Recall the maximization problem (2.1)

where denotes the set of admissible strategies, that is -predictable processes with some integrability conditions (precise definitions will be given later on), and is a bounded -measurable random variable. At this stage we do not need to make precise these integrability conditions and the exact definition of the wealth process . Let us simply note that by definition an element of will satisfy that . This condition together with the characterization of -predictable processes recalled in (2.5) entails that with a -predictable process. Hence in our setting the strategies are essentially -predictable.

We now turn to a suitable decomposition of when or .

Lemma 3.1.

Let be a -measurable random variable. Then, there exist which is -measurable and an -predictable process such that

| (3.1) |

Proof.

Let be a -measurable random variable, we have

which can be rewritten as

where is an measurable random variable and is -measurable. According to [30, Theorem 2.5], since the assumption H1 holds, we get , where we recall that the -field is defined by

Hence, from the definition of , we know that there exists an -optional process denoted by such that Since is the (augmented) Brownian filtration, any -optional process is an -predictable process. ∎

Remark 3.2.

In our framework, the martingale optimality principle can be expressed as follows (we provide a proof for the comfort of the reader even though the arguments are the exact counterpart of the deterministic horizon problem).

Proposition 3.3 (Martingale optimality principle for the random horizon problem).

Let be a family of stochastic processes indexed by such that

-

,

-

is a -supermartingale for every in ,

-

,

-

there exists in , such that is a -martingale.

Then, is a solution of the maximization problem (2.1).

Proof.

Let in . Conditions (i)-(iv) immediately imply that

which concludes the proof. ∎

Note that until now, we have used neither the definition of (provided that the expectation is finite) nor the definition of . However, it remains to construct this family of processes and this is exactly at this stage that we need to specify both the utility function and the set of admissible strategies . To this end we set:

| (3.2) |

where denotes the value at time of the wealth process associated to the strategy with initial capital at time , defined below in (3.3). This amounts to say that the optimization only holds on the time interval . From now on, we consider the exponential utility function defined as

In that case we parametrize a -valued strategy as the amount of numéraire invested in the risky asset (component-wise) so that the wealth process associated to a strategy is defined as:

| (3.3) |

Note that under our assumption on (that is is invertible and uniformly elliptic), the introduction of the volatility process does not bring any additional difficulty compared to the case with volatility one. Indeed, as it is well-known, if we set and , the wealth process becomes

| (3.4) |

and a portfolio is described by the process , which is now -valued. Let be a predictable process with values in the closed subsets of . As in [15] we define the set of admissible strategies by

with

Since the liability is bounded, according to [15, Remark 2.1], optimal strategies corresponding to the utility maximization problem (2.1) coincide with those of [16]. In order to give a characterization of both the optimal strategy and of the value function defined by (3.2), we combine the martingale optimality principle of Proposition 3.3 and the theory of BSDEs with random time horizon.

Theorem 3.4.

Assume that and or hold. Assume that the BSDE

| (3.5) |

with

| (3.6) |

where denotes the usual Euclidean distance, admits a unique solution in the sense of Definition 4.1 such that and are uniformly bounded and such that is a BMO-martingale. Then, the family of processes

satisfies of Proposition 3.3, so that

and an optimal strategy for the utility maximisation problem (3.2) is given by

| (3.7) |

Proof.

Assume that the BSDE (3.5) admits a unique solution (in the sense of Definition 4.1) such that and are uniformly bounded and such that

Following the initial computations of [16] (see also [2, 27] for the discontinuous case) we set:

Clearly, the family of processes satisfies Properties (i) and (iii). By definition each process reduces to

with

and

which is a uniformly integrable martingale by Proposition 2.3. As in [16], the latter property together with the boundedness of and the notion of admissibility for the strategies imply that each process is a -supermartingale and that is a -martingale with , . We conclude with Proposition 3.3. ∎

Remark 3.5.

In this paper we have considered exponential utility, however the case of power utility and/or logarithmic utility follows the same line as soon as .

4 Analysis of the BSDE (3.5)

4.1 Some general results on BSDEs with random horizon

As we have seen in the previous section, solving the optimal portfolio problem under exponential preferences (with interest rate ) reduces to solving a BSDE with a random time horizon. This class of equations has been studied in [9], and one could construct a classical theory for these equations. However, in our setting the filtration is strongly determined by the terminal time , and the structure of predictable processes with respect to is richer than in the general framework. More precisely, from [20] we know that a -predictable process can be described using -predictable processes before and after as recalled in (2.5).

Recall that by (3.1), any bounded -measurable random variable can be written as

with a -measurable bounded random variable, and a bounded -predictable process.

Taking advantage of this decomposition, the solution triple to a BSDE with random horizon has been determined in [24] as the one of a BSDE in the Brownian filtration suitably stopped at (see (4.7)-(4.9) below for a precise statement). However we would like to stress that this result has been obtained under the assumption that is bounded which is a stronger assumption than (H2).

We consider a BSDE with random terminal horizon of the form

| (4.1) |

From (2.5) (see also (4.28) in [24]), we can write

| (4.2) |

where is -progressively measurable.

Definition 4.1.

Remark 4.2.

Remark 4.3.

Note that the term is well-defined since it reduces to . Another formulation of a solution would consist in re-writing (4.1) as:

In this case, the integrability condition on the driver basically amounts to ask

which insures that the process is locally square integrable444Consider and , and remark that a.s., justifying the definition of the stochastic integral .

Similarly given an -measurable map, and an -progressively measurable mapping, we say that a pair of -adapted processes where is predictable is a solution of the Brownian BSDE:

| (4.4) |

if Relation (4.4) is satisfied and if

| (4.5) |

We recall the following proposition which has been proved in [24].

Proposition 4.4.

Assume -. If the Brownian BSDE

| (4.6) |

admits a solution in , then defined as

| (4.7) | ||||

| (4.8) | ||||

| (4.9) |

is a solution of the BSDE (4.1) in .

The previous proposition is in fact a slight generalization of the original result in [24], since in this reference the authors assume to be bounded, which implies condition (H2). In addition, the authors in this reference work with classical solutions in . However, the proof follows the same lines as the original proof in [24], we just notice that [24, Step 1 and Step 2 of the proof of Theorem 4.3] are unchanged and Step 3 holds under Assumption (H2) noticing that

since and are in .

Proposition 4.5.

We assume and . Let be a real-valued, -measurable random variable such that . Assume that the BSDE

| (4.10) |

admits a solution in . Then given by

| (4.11) | |||||

| (4.12) | |||||

| (4.13) |

is a solution of (4.1) and belongs to .

Proof.

Remark 4.6.

Note that in the previous result, the fact that is for example bounded would not imply that is in as is not integrable.

Remark 4.7.

The previous result is very misleading since the terminal condition in (4.10) plays no role. More precisely, assume that for two different random variables and such that the associated solutions and are bounded and verify that

Then obviously , and in light of the proof of Theorem 3.4, the maximization problem (3.2) would then be ill-posed as it would have two different value functions. Even though the notion of strategy we use slightly differs from the one used in [7], this conclusion seems to contradict the well-posedness result obtained in this reference. This remark suggests that it might be possible to solve the Brownian BSDE (4.10) for only one element . For instance, in the exponential u tility setting, Relation (4.5) suggests that to solve BSDE (4.10). To illustrate this, we assume that and that there is no Brownian part. We consider the following Cauchy-Lipschitz/Picard-Lindelöf problem:

Assume that is deterministic, bounded and continuously differentiable. Set . Hence, the previous ODE can be rewritten:

Thus, we can compute explicitly the unique global solution, which is

where is in . Using an integration by part, one gets

Letting go to , we obtain that we must have . Therefore there is a solution if and only if .

4.2 BSDEs for the utility maximization problem

In this section we focus our attention on a class of BSDEs with quadratic growth, which contains in particular the one used for solving the exponential utility maximization problem. We assume that the generator of BSDE (4.1) admits for all in the following decomposition

| (4.14) |

where is a map from to . We assume moreover that satisfies

Assumption 4.8.

-

For every , is -progressively measurable.

-

There exists such that for every , , and for every ,

and

Before going further, notice that under Assumption 4.8, we have the following useful linearization for all

| (4.15) |

where is -progressively measurable and such that and is -progressively measurable and such that

For simplicity, we will write instead of and instead of . Notice that under Assumption 4.8, there exists such that for every and

4.2.1 A uniqueness result

Lemma 4.9.

Remark 4.10.

From the orthogonality of and , notice that

Proof of Lemma 4.9.

Let and be two solutions of BSDE (4.1) above with and such that

are two BMO martingales. Then solves the BSDE:

where

The equation linearizes to obtain

where is a point between and , and are given by Relation (4.15). Knowing that and are two BMO-martingales, from Assumption 4.8 we deduce that is a BMO-martingale and the previous relation re-writes again as:

| (4.16) |

with

and and . Note that is a well-defined probability measure, as soon as with

is a true martingale. In that case, the conclusion of the lemma follows by linearization and taking the -conditional expectation in (4.16) knowing that is bounded. It then remains to prove that the process is a BMO martingale which will imply that its stochastic exponential is a uniformly integrable martingale by Proposition 2.3. Note that since and are two BMO martingales, then according to Proposition 2.2, and are bounded, hence is bounded by . We deduce that the jump of at time is bounded and greater than with . Since is an element between and , it is a (random) convex combination of and . The convexity of the mapping implies for any element in that

This estimate together with the BMO properties proved so far, imply that is a BMO martingale. ∎

4.2.2 Existence results for Brownian BSDEs

We turn to the existence of a solution to the BSDE (4.1) such that is in and is a BMO martingale under Assumptions H2 and H2’. From Proposition 4.4 and Proposition 4.5, this BSDE can be reduced to the following Brownian BSDE

| (4.17) |

where satisfies Assumption 4.8 (changing in -progressively measurable by -progressively measurable) and inherits the decomposition (4.15) from the one of as

| (4.18) |

for any with and . However, neither Assumption H2 nor Assumption H2’ guarantee directly that this quadratic BSDE admits a solution. Hence, we use approximation arguments and introduce quadratic BSDEs defined for by

| (4.19) |

where . By developing the integrand in this BSDE (4.19), one obtains

| (4.20) |

where .

Lemma 4.11 (General a priori estimates under (H2)).

Proof.

Let . The proof is divided in several steps.

Step 1: Uniqueness. Assume that there exist two solutions and to BSDE (4.19) such that is uniformly bounded in . Set and , and

Thus is solution of

| (4.21) |

Hence, knowing that and are two BMO martingales and using Assumption 4.8, we know that is in and we can define a probability by

Moreover, is then a Brownian motion under . So BSDE (4.21) rewrites as

| (4.22) |

Set

Then satisfies

which admits as unique solution.

Step 2: Existence. We turn now to the existence of a solution of BSDE (4.19) in . Consider the following truncated BSDE

| (4.23) |

Then, the classical quadratic BSDE (4.23) admits a unique solution (see e.g. [25]). We can then rewrite BSDE (4.23) as

| (4.24) |

where .

Set and , we obtain from BSDE (4.2.2)

where and is a Brownian motion under the probability , since is a BMO-martingale from Assumption 4.8. Increasing the constants if necessary, we have , then taking the conditional expectation under we deduce that

Since , we deduce that . A posteriori, we deduce that the solution of BSDE (4.23) is in fact the unique solution of BSDE (4.19) in such that . Then, using a linearization and taking the conditional expectation under , we can compute explicitly from BSDE (4.20)

Step 3: BMO norm of . Let be a random horizon and a positive constant. Using Itô’s formula, we obtain

Hence, from Assumption H1, using the fact that, by Step 2, is uniformly bounded in by and taking conditional expectations, we deduce

Since we obtain

By choosing , under Assumption (H2) and using the boundedness of , we deduce that

where

Then, under Assumption H2, is uniformly bounded in . ∎

Theorem 4.12.

Let Assumptions H1-H2 and Assumption 4.8 hold. Then the Brownian BSDE

| (4.25) |

admits a unique solution in . In addition, is bounded and is a BMO-martingale.

Proof.

The proof is based on an approximation procedure using BSDE (4.20). The aim of this proof is to show that the solution to this approached BSDE converges in to the solution of BSDE (4.25). Let , we denote and for all . Then, is solution of the following BSDE

which can be rewritten as

where is a process lying between and which satisfies for all , , and where is a Brownian motion under given by

which is well defined since is a BMO martingale from Assumption 4.8. Let , using Itô’s formula

Using the non-negativity of and choosing , we deduce that

Then, using the boundedness of uniformly in , there exists a positive constant such that

Hence,

| (4.26) |

We want to obtain this kind of estimates under the probability . Notice that

From Assumption 4.8 and Lemma 4.11, is a BMO() martingale and is uniformly bounded in . Then according to [23, Theorem 3.3], is a BMO() martingale. Moreover, following the proof of [23, Theorem 3.3] together with the proof of [23, Theorem 2.4], it is easily verified that is uniformly bounded in . Thus, from [23, Theorem 3.1] there exists (its conjugate being denoted by ) such that

Since is uniformly bounded in , we deduce that there exists such that

| (4.27) |

Similarly, from the definition of there exists such that

| (4.28) |

Thus, from Inequalities (4.26), (4.27) and (4.28), we deduce that there exists a positive constant such that Inequality (4.26) rewrites

by dominated convergence and using (2.3).

Then, we deduce that is a Cauchy sequence in . Hence, converges in to a process . Besides, since is uniformly bounded in , taking a subsequence (which we still denote for simplicity), of uniformly bounded process in which converges, , to , we deduce that . Thus, by Lebesgue’s dominated convergence Theorem, converges to in for every . Recall that

where , which can be rewritten

where . Knowing that for every , we deduce from Theorem 1 in [1] that is a semimartingale such that , where for all

for some positive constant , and

Since is a BMO() martingale, there exists such that . Besides, using the fact that , there exists a positive constant which may vary from line to line such that

Then, we deduce that there exists a -predictable process such that

Following the Step 3 in the proof of Lemma 4.11, we deduce that Then, the pair built previously is the unique solution of BSDE (4.25), the uniqueness coming from Lemma 4.9 together with Proposition 4.4. ∎

We now turn to Assumption H2’. Notice that the proof of Theorem 4.12 fails under H2’ since . We need more regularity on to get a sign on , the first component of the solution of the approached BSDE (4.19) in order to prove that BSDE (4.17) admits a solution under H2’.

Assumption 4.13.

is a bounded semi-martingale such that

where are bounded processes satisfying for all , .

Before going further, to solve the utility maximization problem (2.1) according to Theorem 3.4, we have to prove that is a BMO-martingale. Under Assumption H2, this property comes for free from the BMO-martingale property of and the boundedness of . However, under H2’ it is not clear that whether the BMO-martingale property implies the BMO-martingale property. It is why we show that under H2’, BSDE (4.17) admits a unique solution in , as a consequence of the Immersion hypothesis, which is itself a consequence of H1.

Lemma 4.14.

Proof.

Assume that . We aim at showing that BSDE (4.29) admits a (unique) solution in . Consider the truncated BSDE

| (4.30) |

which can be rewritten under Assumption 4.8

with , and . Then, following Step 1 and Step 2 in the proof of Lemma 4.11 and since is non-negative under Assumption 4.13, we show that BSDE (4.30) admits a unique solution such that

| (4.31) |

where is a positive constant. We show now that the norm of does not depend on by following Step 3 of the proof of Lemma 4.11. Let be a random horizon and . Using Itô’s formula, we obtain

Hence, using the fact that is non positive and uniformly bounded in and taking conditional expectations, we have for any , from the Immersion property H1

Since , and are bounded, using the fact that , we obtain

with . Choosing and using the boundedness of uniformly in , we deduce that there exists a constant which does not depend on such that

Thus, is uniformly bounded in .

We prove now the convergence of the sequence in for every in order to apply Theorem 1 of [1]. Recall that , for every . Then, from the comparison theorem for quadratic BSDEs (see e.g. [25, Theorem 2.6]) and since is non positive, the sequence is non-decreasing. Hence, it converges almost surely to

Fix , we notice that is also the solution to the following BSDE for

Hence, for every and , by setting and reproducing the proof of Theorem 4.12 with as terminal time instead of , we deduce that for every there exists which does not depend on such that

Hence, there exists such that for every

By Lebesgue’s dominated convergence Theorem and since , we deduce that the sequence is a Cauchy sequence in , and knowing that is uniformly bounded in , is a Cauchy sequence in for every . Thus, converges to in for every . As in the proof of Theorem 4.12, we deduce from Theorem 1 in [1] that is a semimartingale such that for every ,

where for all and

for some , and

Hence, there exists a -predictable process such that for every

Thus, for we deduce that there exists a -predictable process such that for every

| (4.32) |

Moreover using (4.31)

which implies is continuous at . Then, taking the limit when goes to 0 in (4.32), the pair of processes satisfies BSDE (4.29). Besides, we have proved that is in and non positive. Hence, following the same lines of the proof of the uniform boundedness of , we deduce that . Since is bounded and since , we deduce that is the unique solution in of (4.29), in the sense of Definition 4.5.

Assume now that there exists a solution . Following the Step 1 of the proof of [18, proposition 3.1], we show that necessarily . ∎

Theorem 4.15.

Proof.

Remark 4.16.

Even if Assumption 4.13 is not too restrictive, especially from the point of view of financial application, we would like to point out the fact that it is not a necessary condition. Consider for simplicity the setting corresponding to , and assume that is a deterministic continuous function of time which may be of unbounded variation and thus not a semimartingale, and consider under H2’ the following linear BSDE

| (4.35) |

Assume that it admits a solution. Then, we necessarily have

Since is automatically uniformly continuous on , there is some modulus of continuity such that

so that we obtain when .

The previous remark leads us to hypothesize that Assumption 4.13 is not necessary to obtain existence and uniqueness of the solution to BSDE (4.33). We give the following conjecture that we leave for future research.

Conjecture.

Assume H1-H2’ hold and that is non-negative for every . Then under Assumption 4.8 the BSDE

with

admits a unique solution such that is bounded and is a BMO-martingale.

4.3 Existence and uniqueness Theorem for BSDE (4.1)

Theorem 4.17.

Proof.

We have shown the uniqueness of the solution in Lemma 4.9. The existence under H2 (resp. H2’) of a triplet of processes satisfying BSDE (4.1), comes directly from Theorem 4.12 (resp. Theorem 4.15) together with Proposition 4.4 (resp. Proposition 4.5). We know moreover that and are in and using the Immersion hypothesis, as a consequence of H1, is a BMO martingale. Recall that , where is the first component of the solution of the Brownian BSDE (4.17). We prove that is a BMO martingale

Under H2. We obtain directly from the definition of H2 and since are bounded

Under H2’. We first consider the Brownian BSDE (4.34) that we recall

where . Using Decomposition (4.18), we obtain

which can be rewritten

| (4.36) |

where . Since is bounded by , following the proof of [18, Theorem 4.4] we can easily show555Taking in [18, Theorem 4.4] and changing in [18, Relation (4.4)] by . that

where is non-negative and . For the sake of simplicity, we set and a positive constant which may vary from line to line. Since is bounded and non-positive, it holds that

where

and

On the one hand, knowing that is bounded and using the integration by part formula, we obtain

where does not depend on . On the other hand, using the fact that and from the existence of a positive constant such that , we get

where does not depend on . We have thus shown that under H2’

| (4.37) |

By considering the unique solution of BSDE (4.34), previously studied, and denoting by the unique solution of BSDE (4.33), we know that . So according to Inequality (4.37), we obtain

| (4.38) |

Finally, under H2 or H2’, is a BMO-martingale.

5 A numerical example under H2’

In this section, we solve numerically the exponential utility maximization problem (3.2). We have seen in Theorem 3.4 that it can be reduced to solving BSDE (3.5), whose solution is completely described, using Proposition 4.5, by the solution of BSDE (4.33) that we recall

where we remind the reader that

We will work for simplicity in the framework summed up in the following assumption.

Assumption 5.1.

-

-

We choose in the decomposition (3.1) equal to .

-

The coefficient is defined by for all .

Notice that

-

•

Under Condition , Assumption is satisfied.

-

•

The condition is necessary in this paper under H2’ in view of Proposition 4.5.

5.1 An implicit scheme to solve the Brownian BSDE (4.33)

In this section, we compute numerically the solution of BSDE (4.33) using an implicit scheme, studied in [8] and [3] among others, mimicking the so-called Picard iteration method to solve a Lipschitz BSDE. Our aim here is not to bring a numerical analysis of the scheme presented below, but rather to follow the method of the proof of Theorem 4.15 where the process is obtained as a monotonic limit of solutions to Lipschitz BSDEs with truncated at a level . In particular, we do not prove any speed of convergence with respect to the truncation level and leave this aspect for future research. Recall the approached Lipschitz BSDE

| (5.1) |

with and .

Let be a subdivision of such that , and denote by the increment . For the sake of simplicity, we also introduce the notation . Denoting by the solution to the Lth Picard iteration associated to (5.1), the solution of BSDE (5.1) associated to a truncation level is computed by

| (5.2) |

In all this section, we assume that the increment is constant, and we set .

Remark 5.2.

Notice that the truncation does not act as soon as . So, this numerical scheme limits us to choose smaller than . Obviously, when goes to , the truncation acts for bigger truncation level . So, limiting to be smaller than is in fact an artifact of the computation coming from the previous numerical scheme.

5.2 Numerical solution of the utility maximization problem (2.1)

In this section, we solve numerically the utility maximization problem (2.1) when for simplicity. We need to build a default time knowing that its associated intensity is given by Relation (2.2). According to [19], given a positive -local martingale and an increasing process such that , for , we can construct a probability measure such that . In particular, taking , from [19, Section 2.1], is an exponential random variable with intensity . Then, by setting an exponential random variable with intensity , the default time associated with intensity is given by

| (5.3) |

Notice that is a non-decreasing bounded sequence, which converges to defined by

Proposition 5.3.

Under Assumption 5.1, Hypothesis H1 holds for every .

Proof.

This result is a direct consequence of [14, Section 12.3.1]. ∎

We give now an explicit formula to compute . According to (5.3), satisfies the following equation for an exponential random variable

By considering the two cases and we get

If , then and if then . Thus, the simulation of can be easily achieved from the simulation of the exponentially distributed random variable .

Assume that when the default time appears before the maturity , the agent has to buy a put with strike . Then, is given by

| (5.4) |

From now on, we use the following data

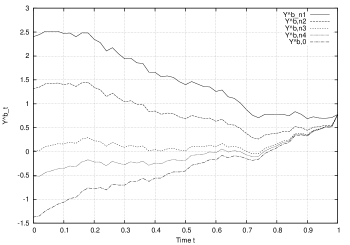

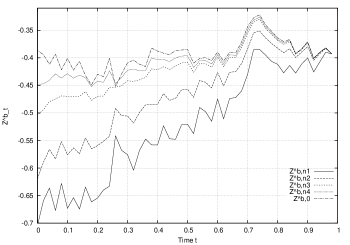

Data. . We take three truncation level and we simulate paths of the solution for . Note that as any truncation level greater than is pointless by Assumption (). Then, we obtain

The same path of the solutions of BSDE (5.1) for a truncation level , for , denoted are given in Figure 1.

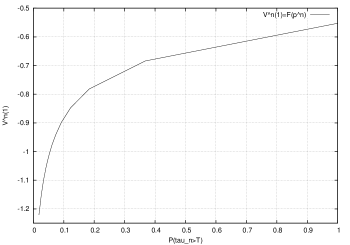

Given a truncation level , we would like emphasize the dependence between the probability that the default time appears after and the value of the utility maximization problem (2.1). Denote and notice that is non-increasing with respect to since is non-decreasing. According to [20]

We can compute easily as a function of by considering the cases and . Then we obtain

Besides, the case corresponds to the classical utility maximization problem without default time. Moreover, we know that and recall that under Assumption (H2’), the support of is we obtain . The value of the utility maximization problem (2.1) associated to the default time is given by . Since (resp. ) is non-increasing (resp. non-decreasing) with respect to , is a non-increasing function of and thus with a non-decreasing mapping.

Interpretation of Figure 2

When there is a default time, which corresponds to the case , the value of Problem 2.1 is obviously less than the case without default time (which corresponds to ). We can interpret this by the fact that the performance of the investor when she knows that her default time appears before the maturity is less than her performance in the case without default time.

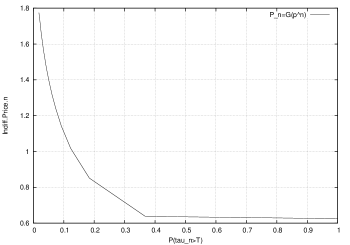

We now study the influence of on the indifference price of the claim , denoted by . Recall that:

where corresponds to the value of Problem 2.1 when . We denote by the unique solution to BSDE (5.1) when :

| (5.5) |

We deduce that satisfies

Proposition 5.4.

is a non-negative and non-increasing function of .

Proof.

Denote by a pair of adapted processes defined by , and for where (resp. ) is the unique solution of BSDE (5.1) (resp. (5.5)). Then, is the unique solution of the following (Lipschitz) BSDE

which can be rewritten, using the mean value theorem, as

with a bounded adapted process between and for . From the comparison Theorem for Lipschitz BSDEs and since given by (5.4) is a non-negative process, we deduce that is non-decreasing in . Thus is a non-increasing mapping of . Besides, by noticing that

we deduce that for all . ∎

We now compute in Figure 3.

Some remarks concerning Figure 3

-

•

seems to be a non-convex function of .

-

•

When (i.e. ), we get . Note that is the unique solution of the following BSDE

The (unique) solution is given by and for .

Now, we denote by the solution of the following BSDE

| (5.6) |

Then, from Proposition 4.5,

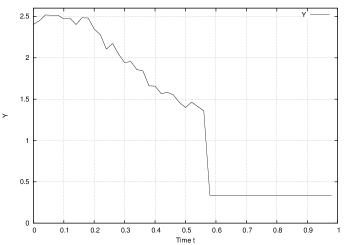

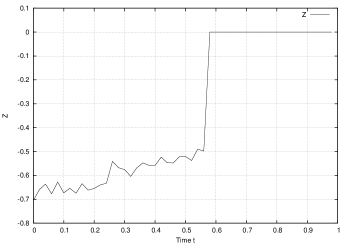

Recall that this BSDE solves the utility maximization problem (2.1) through the and the components. We give numerically a path of this BSDE in Figure 4, obtained by computing with .

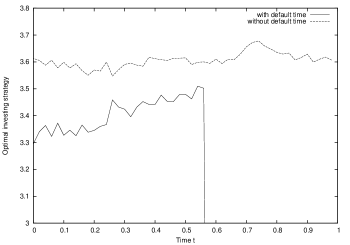

According to Theorem 3.4, an optimal strategy is given by . We compute an optimal strategy to Problem (2.1) in Figure 5 associated to an initial wealth and we compare it with the classical case without jump.

Interpretation of Figure 5

In this very particular case, when we assume that the default time appears almost surely before the maturity, the investor tends to be more cautious by investing less in the risky asset. It is quite reasonable since she knows that she will pay which is a non-negative random variable at default. Note that contrary to what happens for small times where the trading strategies are merely mirrors of each other, the strategy in the default problem becomes more and more similar to the one in the non-default case and the former tends to coalesce with the latter.

Acknowledgments

The authors thank an Associate Editor and a Referee for their careful reading of this paper and their suggestions.

References

- [1] M.T. Barlow and P. Protter. On convergence of semimartingales. In Séminaire de Probabilités, XXIV, 1988/89, volume 1426 of Lecture Notes in Math., pages 188–193. Springer, Berlin, 1990.

- [2] D. Becherer. Bounded solutions to backward SDE’s with jumps for utility optimization and indifference hedging. Ann. Appl. Probab., 16(4):2027–2054, 2006.

- [3] C. Bender and R. Denk. A forward scheme for backward SDEs. Stochastic Processes and their Applications, 117(12):1793–1812, 2007.

- [4] T.R. Bielecki, M. Jeanblanc, and M. Rutkowski. Credit risk modelling. CSFI lecture note series, Osaka University Press., 2009.

- [5] J-M. Bismut. Contrôle des systèmes linéaires quadratiques: applications de l’intégrale stochastique. In Séminaire de Probabilités, XII (Univ. Strasbourg, Strasbourg, 1976/1977), volume 649 of Lecture Notes in Math., pages 180–264. Springer, Berlin, 1978.

- [6] C. Blanchet-Scalliet, N. El Karoui, M. Jeanblanc, and L. Martellini. Optimal investment decisions when time-horizon is uncertain. Journal of Mathematical Economics, 44(11):1100–1113, 2008.

- [7] B. Bouchard and H. Pham. Wealth-path dependent utility maximization in incomplete markets. Finance Stoch., 8(4):579–603, 2004.

- [8] B. Bouchard and N. Touzi. Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. Stochastic Processes and their applications, 111(2):175–206, 2004.

- [9] R. W. R. Darling and E. Pardoux. Backwards SDE with random terminal time and applications to semilinear elliptic PDE. Ann. Probab., 25(3):1135–1159, 1997.

- [10] C. Dellacherie. Capacités et processus stochastiques. Number 67. Springer-Verlag, 1972.

- [11] C. Dellacherie and P.-A. Meyer. Probabilities and potential. B, volume 72 of North-Holland Mathematics Studies. North-Holland Publishing Co., Amsterdam, 1982. Theory of martingales, Translated from the French by J. P. Wilson.

- [12] N. El Karoui, M. Jeanblanc, and Y. Jiao. What happens after a default: the conditional density approach. Stochastic Process. Appl., 120(7):1011–1032, 2010.

- [13] N. El Karoui, S. Peng, and M. C. Quenez. Backward stochastic differential equations in finance. Math. Finance, 7(1):1–71, 1997.

- [14] D. Filipovic. Term-Structure Models. A Graduate Course. Springer Finance, Berlin, 2009.

- [15] V. Henderson and G. Liang. Pseudo linear pricing rule for utility indifference valuation. arXiv preprint arXiv:1403.7830, 2014.

- [16] Y. Hu, P. Imkeller, and M. Müller. Utility maximization in incomplete markets. Ann. Appl. Probab., 15(3):1691–1712, 2005.

- [17] M. Izumisawa, T. Sekiguchi, and Y. Shiota. Remark on a characterization of BMO-martingales. Tôhoku Math. J. (2), 31(3):281–284, 1979.

- [18] M. Jeanblanc and A. Réveillac. A Note on BSDEs with singular drivers. Proceedings of the Sino-French Research Program in Financial Mathematics Conference, Beijing, 2013.

- [19] M. Jeanblanc and S. Song. An explicit model of default time with given survival probability. Stochastic Processes and their Applications, 121(8):1678–1704, 2011.

- [20] T. Jeulin. Semi-martingales et grossissement d’une filtration, volume 833 of Lecture Notes in Mathematics. Springer, Berlin, 1980.

- [21] I. Karatzas, J.P. Lehoczky, S.E. Shreve, and G-L. Xu. Martingale and duality methods for utility maximization in an incomplete market. SIAM Journal on Control and optimization, 29(3):702–730, 1991.

- [22] I. Karatzas and H. Wang. Utility maximization with discretionary stopping. SIAM Journal on Control and Optimization, 39(1):306–329, 2000.

- [23] N. Kazamaki. Continuous exponential martingales and BMO, volume 1579 of Lecture Notes in Mathematics. Springer-Verlag, Berlin, 1994.

- [24] I. Kharroubi, T. Lim, and A. Ngoupeyou. Mean-variance hedging on uncertain time horizon in a market with a jump. Preprint., 2012.

- [25] M. Kobylanski. Backward stochastic differential equations and partial differential equations with quadratic growth. Annals of Probability, 28(2):558–602, 2000.

- [26] J-P. Lepeltier and J. San Martin. Backward stochastic differential equations with continuous coefficient. Statistics & Probability Letters, 32(4):425–430, 1997.

- [27] M. A. Morlais. Utility maximization in a jump market model. Stochastics, 81(1):1–27, 2009.

- [28] E. Pardoux and S. Peng. Backward stochastic differential equations and quasilinear parabolic partial differential equations. In Stochastic partial differential equations and their applications, pages 200–217. Springer, 1992.

- [29] R. Rouge and N. El Karoui. Pricing via utility maximization and entropy. Math. Finance, 10(2):259–276, 2000. INFORMS Applied Probability Conference (Ulm, 1999).

- [30] S. Song. Optional splitting formula in a progressively enlarged filtration. ESAIM: Probability and Statistic, 18:829–853, 2014.

- [31] C. Stricker and M. Yor. Calcul stochastique dépendant d’un paramètre. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 45:109–133, 1978.