Optimal allocation of Monte Carlo simulations to multiple hypothesis tests

Abstract

Multiple hypothesis tests are often carried out in practice using p-value estimates obtained with bootstrap or permutation tests since the analytical p-values underlying all hypotheses are usually unknown. This article considers the allocation of a pre-specified total number of Monte Carlo simulations (i.e., permutations or draws from a bootstrap distribution) to a given number of hypotheses in order to approximate their p-values in an optimal way, in the sense that the allocation minimises the total expected number of misclassified hypotheses. A misclassification occurs if a decision on a single hypothesis, obtained with an approximated p-value, differs from the one obtained if its p-value was known analytically. The contribution of this article is threefold: Under the assumption that is known and , and using a normal approximation of the Binomial distribution, the optimal real-valued allocation of simulations to hypotheses is derived when correcting for multiplicity with the Bonferroni correction, both when computing the p-value estimates with or without a pseudo-count. Computational subtleties arising in the former case will be discussed. Second, with the help of an algorithm based on simulated annealing, empirical evidence is given that the optimal integer allocation is likely of the same form as the optimal real-valued allocation, and that both seem to coincide asympotically. Third, an empirical study on simulated and real data demonstrates that a recently proposed sampling algorithm based on Thompson sampling asympotically mimics the optimal (real-valued) allocation when the p-values are unknown and thus estimated at runtime.

Keywords: Bonferroni correction; multiple testing; Monte Carlo simulation; optimal allocation; Thompson sampling; QuickMMCTest.

1 Introduction

Scientific studies are often evaluated by correcting for multiple comparisons using, for instance, the Bonferroni correction (Bonferroni,, 1936) or the procedures of Sidak, (1967), Holm, (1979), Simes, (1986), Hochberg, (1988), or Benjamini and Hochberg, (1995).

Although testing procedures such as the Bonferroni correction require exact knowledge of the p-value underlying each statistical test, p-values are usually not available analytically in practice and thus have to be approximated using Monte Carlo methods, for instance, bootstrap or permutation tests (Gandy and Hahn,, 2014, 2016, 2017; Silva and Assunção,, 2018). In the context of such Monte Carlo tests, the (analytical) p-value refers to the one obtained by integrating over the theoretical bootstrap distribution (in case of bootstrap tests) or by exhaustively generating all permutations (in case of permutation tests). This scenario is common in scientific studies involving real data, see, for instance, Tang et al., (2017), Chen and Chen, (2017), Wei et al., (2016), or Shen et al., (2014) for recent testing applications involving Monte Carlo approximated p-values and Mrkvic̆ka et al., (2017) or Pesarin et al., (2016) for Monte Carlo extensions of multiple testing.

When testing given hypotheses in practice, a researcher is faced with the task of allocating a number of Monte Carlo simulations (which in practice is always finite) according to some criterion of choice in order to approximate the p-values of the hypotheses. It is assumed throughout the article that are tested using independent test statistics. For simplicity, the classical Bonferroni correction is considered in the remainder of this article to correct for multiplicity, though it will be discussed how the results of this article extend to other multiple testing procedures. Recent examples for scientific works utilising the Bonferroni correction include Gallagher et al., (2018), Zhang et al., (2017), or Mestres et al., (2017).

This article considers the optimal allocation of Monte Carlo simulations to hypotheses, in the sense that the allocation minimises the total expected number of misclassified hypotheses, under the assumption of a testing scenario in which independent test statistics are available and multiplicity is corrected with the Bonferroni correction.

To this end, two approaches are explored. First, it is assumed that the number of simulations to be allocated to each hypothesis is real-valued as opposed to integer-valued, and the Binomial distribution arising in the expression for the expected number of misclassifications is replaced by a normal approximation. This simplifies the problem and allows for the computation of gradients, thus making it possible to solve for the optimal real-valued allocation using the Karush-Kuhn-Tucker (KKT) formalism (Karush,, 1939; Kuhn and Tucker,, 1951). This is done in two cases, precisely when p-value estimates are computed both with or without a pseudo-count (Davison and Hinkley,, 1997). In the former case, an optimal solution does not always exist and further computational subtleties arise, which will be discussed. Second, the computation of the optimal integer-valued allocation is attempted with the help of a scheme based on the simulated annealing (SA) algorithm (Kirkpatrick et al.,, 1983) which, under conditions, allows to find integer solutions which converge to an optimal solution (Henderson et al.,, 2003).

Several algorithms to compute significant and non-significant hypotheses via approximated p-values are available in the literature. For instance, the method of Besag and Clifford, (1991), the approaches of Guo and Peddada, (2008) and van Wieringen et al., (2008), the MCFDR algorithm of Sandve et al., (2011), the method of Jiang and Salzman, (2012) or the MMCTest algorithm of Gandy and Hahn, (2014). However, to the best of our knowledge, it is unclear how the allocation of Monte Carlo simulations computed by such algorithms available in the literature compares to the optimal allocation (in the above sense). Nevertheless, for the QuickMMCTest algorithm of Gandy and Hahn, (2017), a simulation study included in this article empirically demonstrates that its allocation asympotically mimics the optimal allocation of Monte Carlo simulations (as and go to infinity). This is of importance for practical applications: Generating simulations, for instance via permutations, can be computationally very expensive. An optimal (or nearly optimal) allocation of Monte Carlo simulations thus minimises computational resources while maximising the accuracy of the multiple testing result or makes the evaluation of real data possible in the first place.

For the special case of one hypothesis, a related field to the one of this article pertains to the sequential design of Monte Carlo testing while minimising the total number of simulations (Lan and Wittes,, 1988; Besag and Clifford,, 1991; Gandy,, 2009; Fay et al.,, 2007; Silva et al.,, 2009; Silva and Assunção,, 2013).

The article is organised as follows. Section 2 introduces the mathematical formulation of the problem under consideration (Section 2.1), simplifies it by allowing to be real-valued and by using a normal approximation of the Binomial distribution (Section 2.2), and solves for the optimal allocation using the KKT conditions (Section 2.3). Computational issues arising when solving the KKT conditions without (Section 2.3.1) and with a pseudo-count (Section 2.3.2) are discussed. As in practice any allocation is discrete, the related discrete optimisation problem is heuristically solved with the simulated annealing algorithm (Section 3). A simulation study (Section 4) visualises how the optimal allocation of Monte Carlo simulations to hypotheses relates to their underlying p-value distribution (Section 4.1), and empirically demonstrates that the real-valued KKT as well as the integer-valued SA solutions are qualitatively similar both for a finite and asympotically (Section 4.2). Moreover, in contrast to the aforementioned algorithms published in the literature, it is shown empirically that the QuickMMCTest algorithm (Gandy and Hahn,, 2017) asympotically mimics the optimal (real-valued) allocation on simulated (Section 4.3) and real data (Section 4.4). The article concludes with a discussion in Section 5. Supplementary material containing code (R Development Core Team,, 2011) to reproduce all figures is provided.

Throughout the article, let denote the Euclidean norm of a vector. Let denote the natural numbers including zero and let be the strictly positive part of the real line.

2 The optimal allocation for the Bonferroni correction

This section states a mathematical formulation of the optimisation problem of minimising the expected number of misclassified hypotheses (Section 2.1) and derives a real-valued solution using the KKT formalism (Section 2.2). Solving the KKT conditions (Section 2.3) is not straightforward if the p-value estimates for all hypotheses are computed with a pseudo-count (Davison and Hinkley,, 1997), and computational subtleties are discussed in Sections 2.3.1 and 2.3.2. Extensions of all results to other multiple testing procedures (apart from the Bonferroni correction) are discussed in Section 2.4.

2.1 Formulation of the problem

A researcher is faced with testing hypotheses for statistical significance using some test statistics and the Bonferroni correction at a given testing threshold . Throughout the article, it is assumed that the test statistics for testing are independent. Typically, , where is an uncorrected threshold such as . Let and denote the unknown p-value underlying each hypothesis as , . The Bonferroni correction returning the indices of all rejected hypotheses is defined as , where .

As the p-values are unknown, it is assumed that Monte Carlo methods are used to approximate them as , where is the total number of Monte Carlo simulations generated for and is the number of exceedances over the observed test statistic (computed with some given data for each hypothesis) among those simulations, . The parameter determines if a pseudo-count (Davison and Hinkley,, 1997) is used in the numerator and denominator of which bounds the estimates away from zero. Such a pseudo-count is recommended and commonplace in practice (Phipson and Smyth,, 2010). Instead of generating Monte Carlo simulations, the number of significances can equivalently be modeled as .

The hypothesis is rejected if and only if , where . All remaining hypotheses are non-rejected. The aim of this article is to find the optimal allocation of Monte Carlo simulations to the hypotheses which minimises the expected number of misclassifications, defined below, subject to the constraint that for a given total number of simulations specified in advance.

Let be the event that hypothesis is misclassified, that is the event that the unknown p-value of and its estimate lie on two different sides of the testing threshold. Using the event , the total number of misclassifications can be expressed as , where is the indicator function. When allocating simulations to hypothesis to estimate its p-value, the probability of a misclassification of hypothesis is

| (1) |

where the dependence of on , and is omitted for notational simplicity. The probability in (1) is also called the resampling risk, a popular error measure which many algorithms published in the literature on Monte Carlo hypothesis testing aim to control (Davidson and MacKinnon,, 2000; Fay and Follmann,, 2002; Fay et al.,, 2007; Gandy,, 2009; Kim,, 2010; Ding et al.,, 2018). The total expected number of misclassifications which occur when allocating simulations to is thus

| (2) |

where the expectation is taken over the random , . The goal is to minimise the total number of misclassifications for a suitable choice with . The functions go to zero as . This is to be expected as by the law of large numbers, each estimate converges to the p-value as more Monte Carlo simulations are generated. To summarise, the constrained optimisation problem under investigation can be formalised as

| (3) |

2.2 The optimal allocation for a normal approximation

The constrained optimisation in (3) can be solved with the help of the KKT formalism. As derivatives are needed for KKT, (1) is relaxed by allowing and by approximating in (1) with a normal distribution with mean and variance . This yields

where is the cumulative distribution function of the standard normal distribution and where it was used that for .

Now, for all and consequently, (2) can be approximated as . By the de Moivre–Laplace theorem, the ratio of to tends to one as for each . Thus as , given each hypothesis receives an amount of of those simulations with , the approximation will be very accurate. For small , however, might be a poor approximation of and (3) should be solved directly for an integer solution as attempted in Section 3 (this is easier for small than for large ones).

The derivative of each (which is a function of only), , is given by

| (4) |

where is the density function of the standard normal distribution. The partial derivative depends on only, thus allowing to essentially separate the optimisation problem into problems, each finding an optimal number of simulations for hypothesis .

The function needs to be optimised under the constraints for and , meaning that each hypothesis receives a positive number of simulations and that the total number of simulations allocated equals . The optimal solution minimising satisfies the Lagrangian associated with the constrained optimisation problem, given by

| (5) |

where and , . The functions encode the constraint (primal feasibility) with (dual feasibility) and satisfy (complementary slackness), where .

Complementary slackness and the condition imply that for all . As each partial derivative only depends on , (5) simplifies to

| (6) |

for and an optimal value ensuring .

2.3 Computational considerations when solving the KKT conditions

Finding the optimal value in (6) and the corresponding which satisfies is straightforward if no pseudo-count is used when computing p-value estimates ( in (4)) and more challenging with a pseudo-count ( in (4)). In particular, the optimal solution allocating Monte Carlo simulations to hypotheses might not always exist in the latter case. The following two Sections 2.3.1 and 2.3.2 provide computational details.

2.3.1 P-value estimates without a pseudo-count

If no pseudo-count is used ( in (4)), the qualitative behaviour of is as depicted in Figure 1. The derivative is negative (given ) and strictly increases to zero as . This is proven in Lemma 1 in Section A.

Solving for the optimal allocation is thus straightforward and computationally efficient: First, suppose a value and the index of a particular hypothesis are given and the task is to find the value of such that , formalised as the following problem:

| (7) |

To solve (7) a double binary search can be employed: Starting with an arbitrary starting value (e.g., ), double or halve until an interval is obtained such that . A binary search applied to that interval then finds the solution of in logarithmic time (in the size of the search space). Both steps rely on the fact that are strictly increasing for all . Since the size (length) of the search space is bounded by , this operation takes for each .

Since the derivatives are negative but strictly increasing for all , lower (higher) values of yield larger (smaller) across all . Thus in a second step, choose an arbitrary starting value (e.g., ), determine the corresponding vector by solving for all and check if is positive or negative. If it is positive, will be doubled (thus decreasing ) and otherwise halved until an interval is found which contains the optimal value whose corresponding solution of for all satisfies . A binary search then finds within in logarithmic time. The total effort for finding both and the optimal allocation of Monte Carlo simulations can thus be expressed as . Section 4 shows that for typical testing scenarios, is of the order of around to . In principle, any number of simulations can be allocated to the hypotheses in this way.

2.3.2 P-value estimates with a pseudo-count

When using a pseudo-count, finding , , for a given as well as finding the optimal becomes more challenging. This is due to the fact that the derivatives are not strictly increasing any more and neither do they attain all values in . Figure 2 shows examples of the qualitative behaviour of for a p-value below (left) and above (right) the testing threshold .

Since in both cases, the derivative is still negative in a limited region, it might nevertheless be possible to find a that satisfies the KKT conditions. To this end, first determine the range of admissible values of for each hypothesis , , defined as the range of values for which is negative and strictly increasing. To apply binary search as done for solving (7), find the range extending from the unique minimum (see Figure 2) of the derivative to the maximal number of Monte Carlo simulations to be allocated, a natural upper bound of .

However, since can be large it is non-trivial to locate (or even any non-zero value of the derivative subject to machine precision), and it is helpful to have a guess of the location of the minimum. This guess can be computed as the point at which the derivative (4) changes from being positive to negative. In (4), the function is always strictly positive, so it suffices to consider the zero of its prefactor, which is easily computed as

| (8) |

The quantity is referred to as the guess for the minimum of hypothesis (depicted as dotted vertical line in Figure 2). Note that (8) remains valid for the case in which the minimum is at for all (see Figure 1).

Using , a binary search determines the two points to the left and to the right of at which the derivative is first non-zero (subject to machine precision). This gives a search window for (computable in time), and is then efficiently found with, for instance, a golden section minimisation procedure (Kiefer,, 1953; Avriel and Wilde,, 1966) as implemented in the function optimise (R Development Core Team,, 2011). The complexity of the golden section search is , where is the computational precision (Luenberger,, 2003). Once is found, the resulting range of admissible values for can be set as for each .

After is determined for each hypothesis , , the optimal value has to be found. For this, a search window for the binary search on is again needed: this search window precisely consists of all those values for which has a solution within the admissible range for all indices . However, finding such an interval for is not always possible as shown in the following paragraphs and empirically in Section 4.2.

Since by construction, is strictly increasing within for all , the window of admissible values for each can be translated to a search window for the admissible values of that correspond to it. To be precise, this search interval is for all , since large (small) values of correspond to low (high) values of .

It remains to compute the intersection of all , , that is the range of values which guarantees that has a solution for all . However, it can happen that a few single hypotheses cause , precisely those in . In this case, a global optimal allocation might not exist. However, the existence of an optimal allocation can be guaranteed again if the hypotheses in are removed from .

If is an interval of non-zero length, then by construction can be solved for all and for any . In particular, for any given , is solved with a binary search on the individual search window for each as in Section 2.3.1, and the optimal is likewise found with a binary search within , again with total computational effort .

Conversely, the final range of admissible values can be translated into the minimal and maximal number of Monte Carlo simulations that can be allocated in an optimal way for the given p-values . The minimal and maximal numbers are and , respectively, where is the solution of for all and is the solution of for all (the minimal optimal allocation is obtained for the largest admissible value of and likewise for the maximal optimal allocation). These bounds on the minimal and maximal numbers of simulations which can be allocated in an optimal way will be used in Section 4.2.

2.4 Extension to other multiple testing procedures

The previous derivations specifically addressed the Bonferroni correction with constant threshold . However, since the computation of the optimal allocation assumes full knowledge of both the p-values and the threshold , this is not a restriction. This is due to the fact that the result of any multiple testing procedure can equivalently be obtained by applying the Bonferroni correction to with constant threshold set to the p-value of the last rejected hypothesis by .

3 A simulated annealing algorithm to attempt the computation of the optimal integer allocation

Section 2 considered the computation of the optimal allocation of Monte Carlo simulations under the assumption that using a normal approximation of the Binomial distribution in (1). In this section, a scheme based on simulated annealing (SA) of Kirkpatrick et al., (1983) is derived in order to attempt to solve (3) directly. To this end, Section 3.1 first considers the behaviour of the functions occurring in (3). Section 3.2 discusses the design of a suitable proposal function for SA and Section 3.3 introduces the actual SA algorithm. Although the optimality of the found integer allocation cannot be guaranteed any more, a simulation study (Section 4.2) will later give empirical evidence that the optimal integer allocation is likely of the same form as the optimal real-valued KKT allocation.

3.1 Qualitative behaviour of the probability of misclassifications

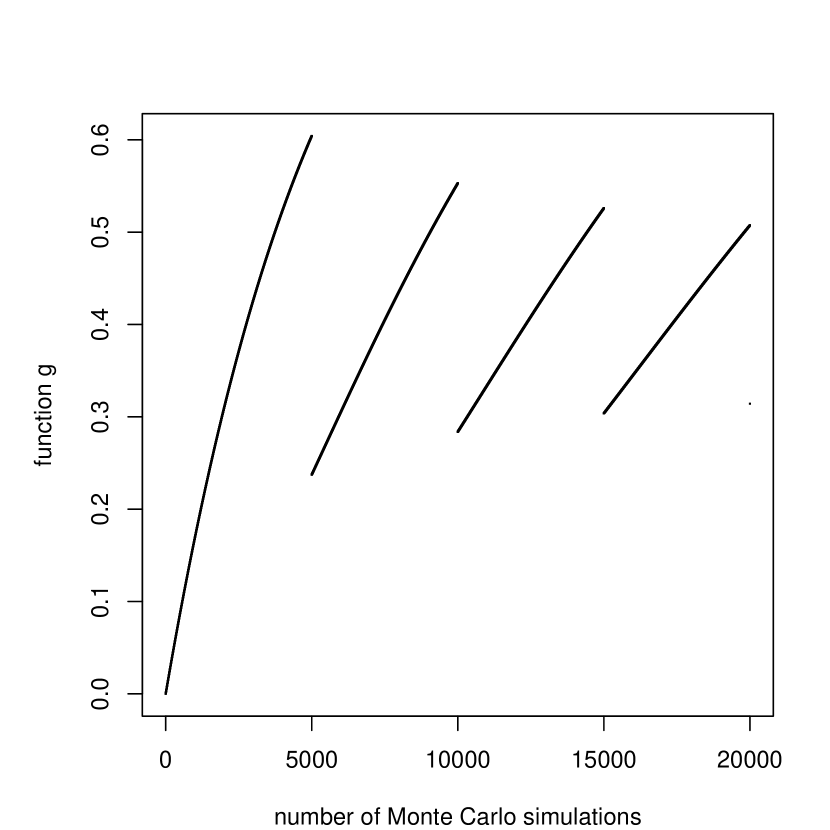

In order to motivate the design of the SA proposal in Section 3.2, consider the behaviour of the function depicted exemplarily in Figure 3 for a p-value below (left) and above (right) the testing threshold .

In Figure 3, the absence of a pseudo-count ( in (4)) is crucial. A rejection is obtained if a p-value estimate is below , where generating simulations is defined to yield a p-value of and hence a correct rejection. Thus when generating less than simulations for a p-value below (left), only the case of simulations leads to a sure rejection (and thus to a correct decision, that is a probability of misclassification of zero). Generating more than simulations results in a non-zero probability of observing at least exceedance (in which case the hypothesis under consideration will be erroneously non-rejected), thus increasing the probability of a misclassification. On reaching simulations, both or exceedances will lead to a rejection and hence to a correct decision, thus causing the expected number of misclassifications to drop again.

For a p-value above (right), the inverse effect happens. Generating no simulations leads to a p-value of (resulting in a rejection) and thus to a sure misclassification. Generating more simulations decreases the expected number of misclassifications. On reaching simulations, observing both and exceedances leads to a rejection and thus to a misclassification, causing the expected number of misclassifications to increase again.

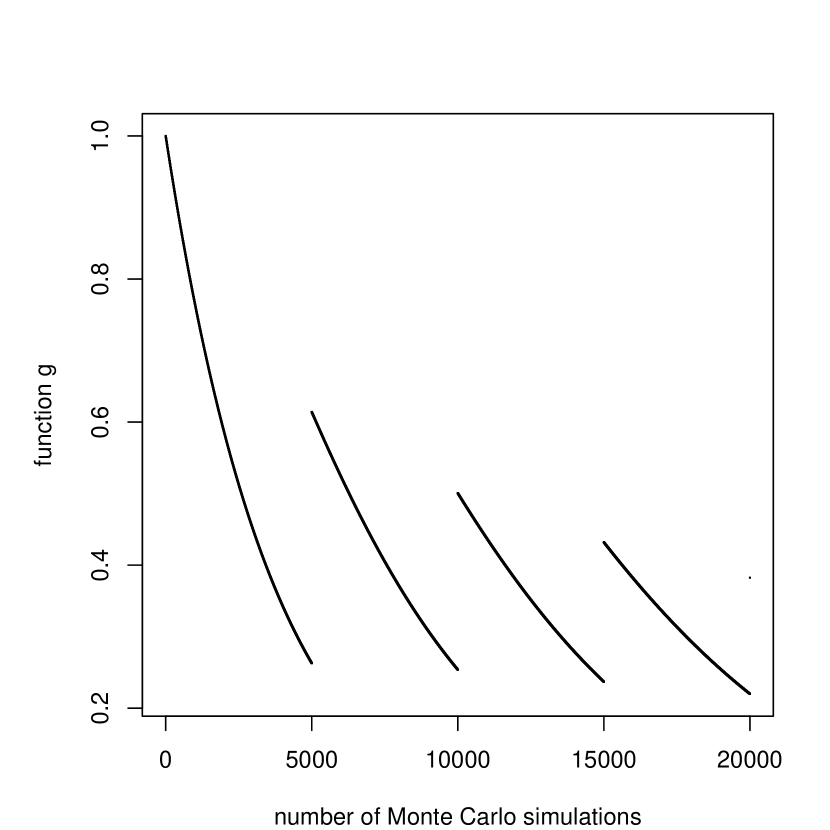

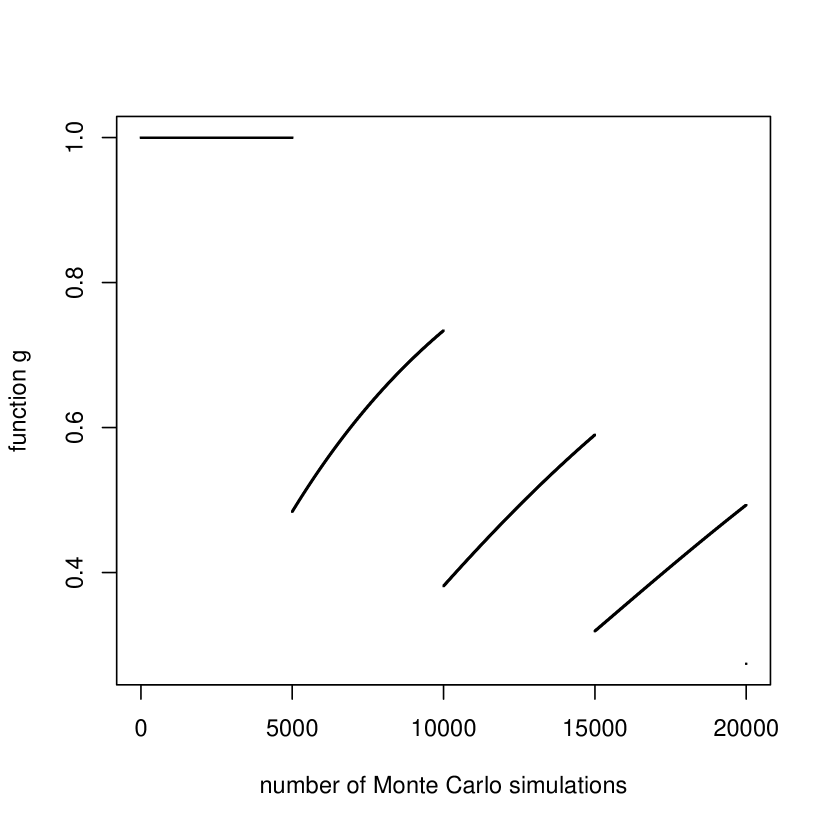

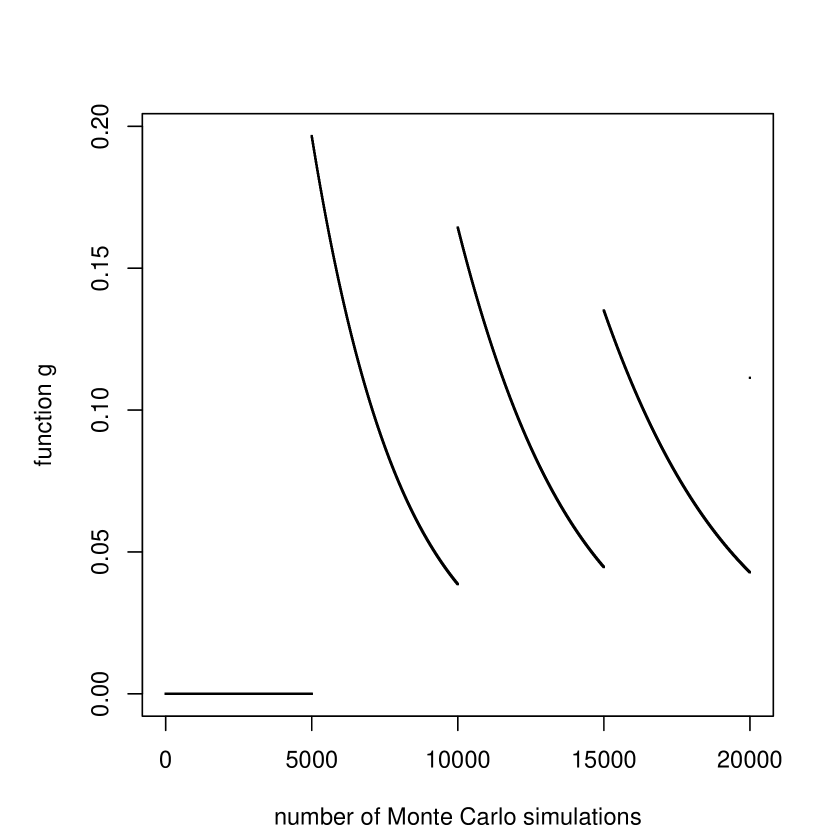

Figure 4 depicts a similar behaviour of the number of misclassifications when computing p-value estimates with a pseudo-count ( in (4)). Here, generating no simulations results in a p-value estimate of and thus in a sure non-rejection, and likewise generating any number of simulations less than leads to a p-value estimate strictly above irrespective of the number of observed exceedances. As expected, in Figures 3 and 4 the probability of a misclassification vanishes for any hypothesis as , .

3.2 The choice of the simulated annealing proposal

When no pseudo-count is used ( in (4)), according to Figure 3, it is only sensible to allocate batches of Monte Carlo simulations to hypotheses with p-values below the testing threshold. The same applies to hypotheses with p-values above the threshold, except when a hypothesis receives less than simulations, in which case the probability of a misclassification for that hypothesis decreases as more simulations are being allocated to it (corresponding to the first branch in Figure 3, right). A similar observation holds true for p-values computed with a pseudo-count (Figure 4).

Based on this observation, Algorithm 1 offers a sensible proposal for an SA algorithm. The function proposal takes as inputs the current allocation of Monte Carlo simulations to all hypotheses, a finite set indicating which hypotheses ought to be eligible for a fine tuning of their currently allocated number of simulations, the threshold and a jump size which is preset to .

Algorithm 1 works as follows. First, the actual jump size to be used is set to either or with probability each. This ensures that the SA algorithm will not be restricted to allocating batches of simulations only, but will be able to fine-tune the allocation. If there exists at least one hypothesis from which simulations can be taken for re-allocation, then an index is drawn uniformly among all those hypotheses currently receiving at least simulations, is substracted from , and the simulations are allocated in a greedy fashion to the hypothesis which yields the largest decrease in its expected number of misclassifications. The greedy allocation is not necessary but employed here to speed up the slow SA scheme. Alternatively, the simulations can also be allocated to any randomly chosen hypothesis.

3.3 A simulated annealing approach

Using the proposal in Algorithm 1, the minimisation in (3) can now be attempted with the help of a simple SA scheme (Kirkpatrick et al.,, 1983) given in Algorithm 2.

Algorithm 2 works as follows. In each iteration, the proposal function is called with the current allocation (initialised with some allocation ) and its proposed new allocation is saved in . Both the current allocation and the proposed new allocation are evaluated on (the function to be minimised, in our case defined in (2)) and a standard SA acceptance probability is computed. If then the argument of the exponential function will be non-negative and thus , leading to a sure acceptance of the proposal in line 2. If then the proposal will only be accepted with probability in line 2. Since in this case the proposal actually increases the objective function, SA has the ability to leave local minima. The aforementioned steps are repeated over a pre-specified number of iterations . The last accepted proposal is returned as the output of Algorithm 2.

To turn SA into a steepest descent optimiser over time, the argument of the exponential function is weighted by using a temperature which is decreased in every step (line 2). Employing a logarithmic decrease ensures, under conditions, that SA will find the global minimum of as (Henderson et al.,, 2003).

The initial allocation can be chosen as follows. If then it is sensible to set to a multiple of plus one for all indices in , and likewise is set to a multiple of for all (see Figure 3). Similarly, for , is set to a multiple of for all indices in , and to a multiple of minus one otherwise. If at the end, , one Monte Carlo simulation each is added to a randomly drawn entry among () for () until is satisfied. Afterwards, the two calls

optimise the allocation of Monte Carlo simulations both above and below the threshold, where is as defined in (2). Since , , and since the proposal in Algorithm 1 only performs swaps of an integer number of simulations between hypotheses, it is guaranteed that and that both sum up to . The integer allocation of Monte Carlo simulations in vector is returned as the SA approximation of the optimal allocation solving (3).

4 Simulation study

This section discusses the optimal allocation for a given distribution of p-values (Section 4.1) and shows that the optimal real-valued and integer allocations are qualitatively similar (Section 4.2), both for a finite and asympotically. Section 4.3 empirically demonstrates that while adaptively generating Monte Carlo simulations at runtime to approximate the unknown p-values of multiple hypotheses, the QuickMMCTest algorithm of Gandy and Hahn, (2017) allocates simulations in a way that asympotically coincides with the optimal (real-valued) allocation. A comparison on a real dataset to the other algorithms listed in Section 1 is given in Section 4.4.

4.1 Relationship between p-value distribution and optimal allocation

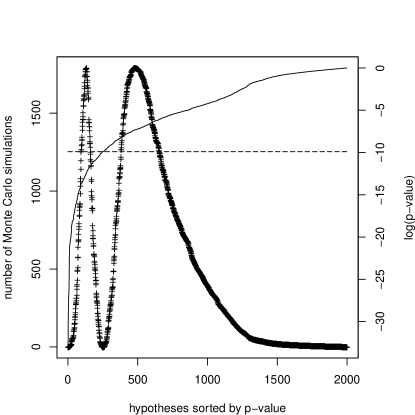

This section visualises how the distribution of p-values is related to the optimal (real-valued) allocation of Monte Carlo simulations to all hypotheses. For this, p-values are drawn from the mixture distribution proposed in Sandve et al., (2011): The mixture distribution consists of a proportion of true null hypotheses drawn from a uniform distribution in , and a proportion drawn from a distribution. This distribution resembles p-value distributions observed in real data studies (e.g., genome testing) and has already been used in Gandy and Hahn, (2014, 2016, 2017).

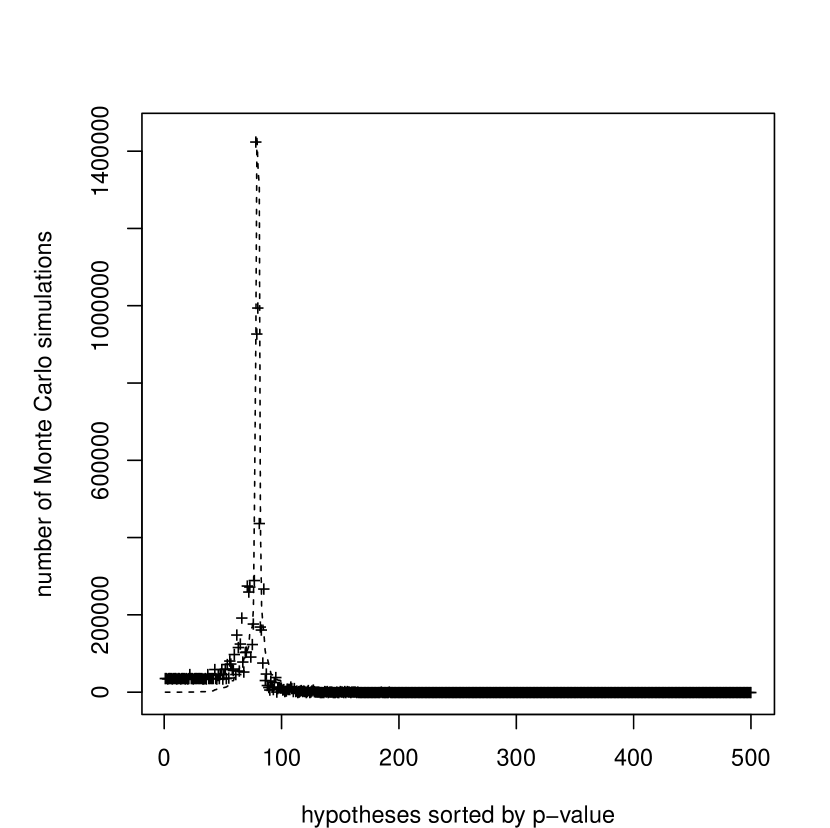

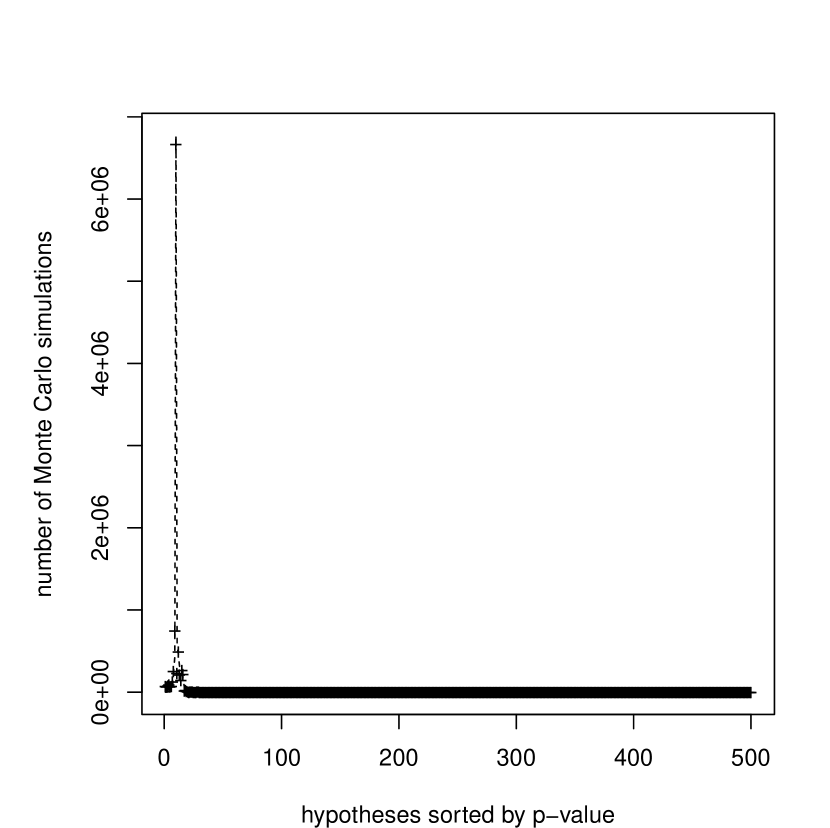

Figure 5 shows the distribution of p-values drawn with (logarithmic axis on the right). The relatively low proportion of true null hypotheses is employed in this and the following sections to better visualise the p-value distribution and the resulting allocation of simulations. The testing threshold is set to . Using the known p-values, the optimal allocation of simulations was computed as described in Section 2.3.1 (without a pseudo-count, case ) and added to Figure 5 as crosses (numbers given on the left axis). The optimal allocation was found with .

As expected, and as confirmed by empirical studies (Gandy and Hahn,, 2017), hypotheses with very small or very large p-values only require relatively few Monte Carlo simulations for stable decisions. As the p-value distribution approaches a neighbourhood of the testing threshold from either side, more simulations are required to minimise the total number of misclassifications in the optimal allocation. However, it turns out that in this example, hypotheses with p-values too close to the testing threshold are not worth being invested too many simulations in since the numbers required for a (reasonably) low probability of a misclassification are too large. Therefore, in the optimal allocation, those misclassifications are traded in for being able to use the unspent simulations on other hypotheses instead which are slightly further away from the threshold.

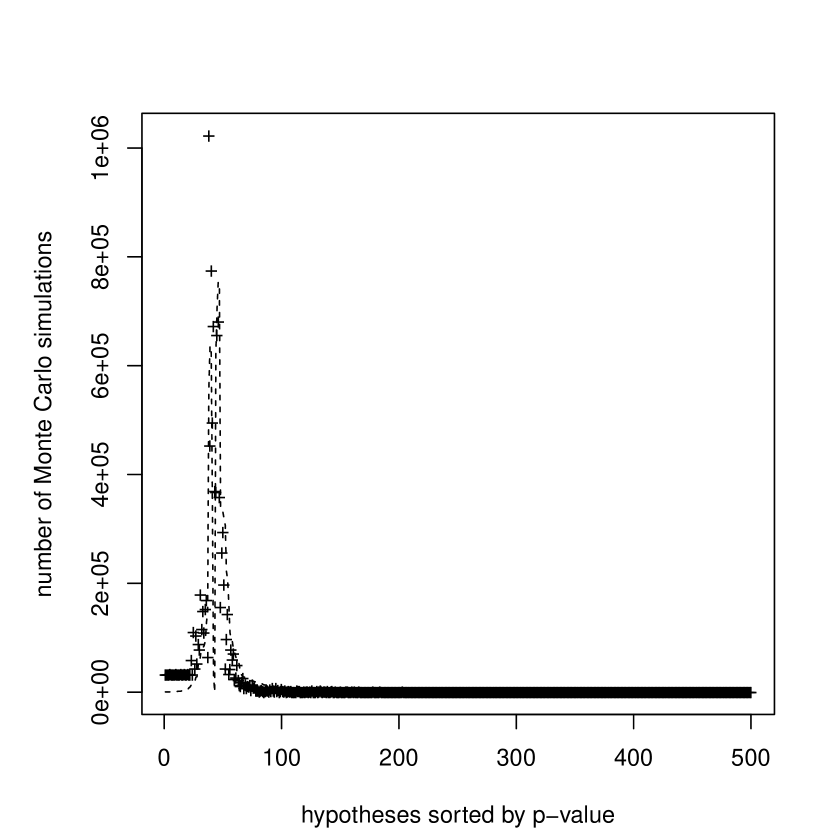

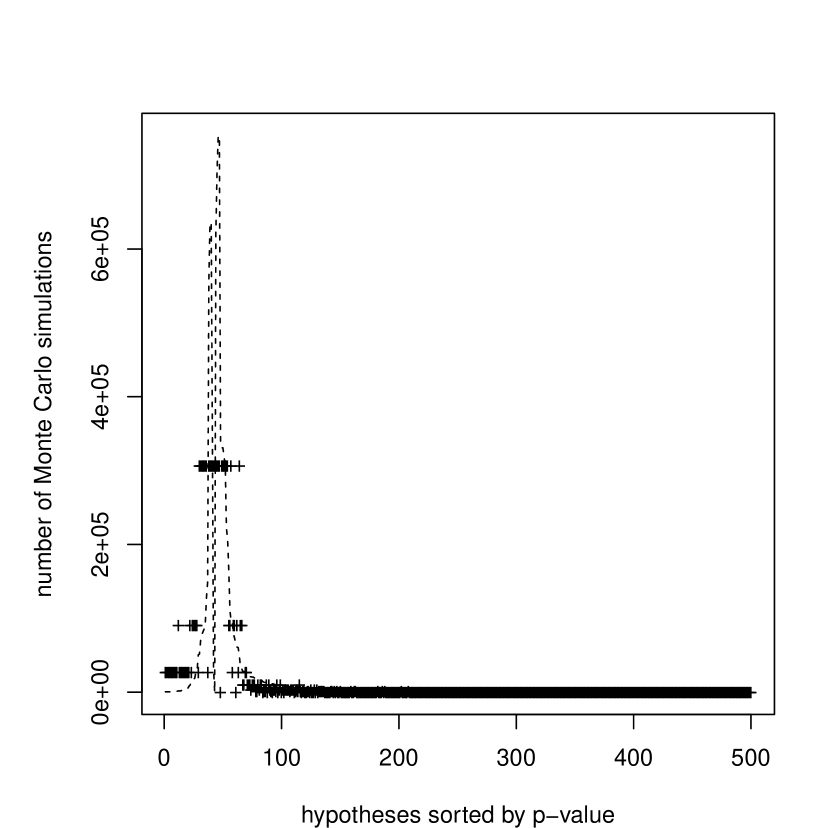

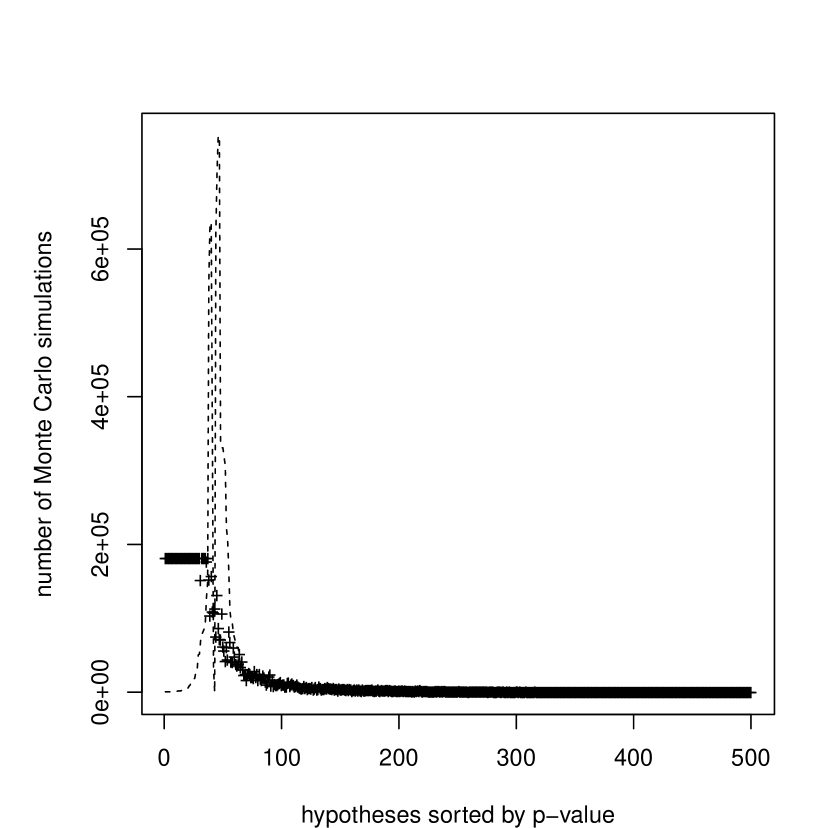

It is not always the case that hypotheses too close to the threshold receive less Monte Carlo simulations than those in an immediate neighbourhood. Figure 6 shows the optimal real-valued allocations for three scenarios using and sets of p-values drawn from the Sandve et al., (2011) distribution with parameter . For hypotheses and threshold (left), hypotheses close to the threshold do not receive many simulations. However, when increasing the threshold to (middle), this effect disappears and the optimal allocation invests most simulations in the hypotheses closest to the threshold. When increasing the number of hypotheses to while keeping constant, hypotheses close to the threshold again receive less simulations.

This can be explained as follows. Suppose the optimal was known. The optimal allocation consists of the for each hypothesis , , which satisfies (6). The derivative in (6) is of the order

for both cases and , where it was used that . The quantity of interest is : For a p-value () further away from the threshold, is of the order of (of the order of ), and has to be sufficiently large to ensure . If is very close to , can be magnitudes smaller than both and , and the satisfying need only be relatively small.

Figure 6 confirms this picture: The p-value distribution of Sandve et al., (2011) consists of a proportion of very small p-values from a distribution, which cluster close to zero, and a proportion of p-values drawn from a uniform distribution which scatter within the entire interval . In Figure 6 (left), falls within the p-values from the Beta cluster, causing to be small (of the order of ) and the optimal allocation to spend less Monte Carlo simulations right at the threshold. When increasing the threshold to (middle) while keeping fixed, now falls within the uniform p-values which are scattered over the entire interval , thus causing to increase to the point that hypotheses at the threshold receive most simulations. However, can be made smaller again simply by increasing , for instance to (thus increasing the p-value density in which leads to ), causing the optimal allocation to again spend less simulations at the threshold (right).

4.2 Comparison of the optimal real-valued and integer allocations

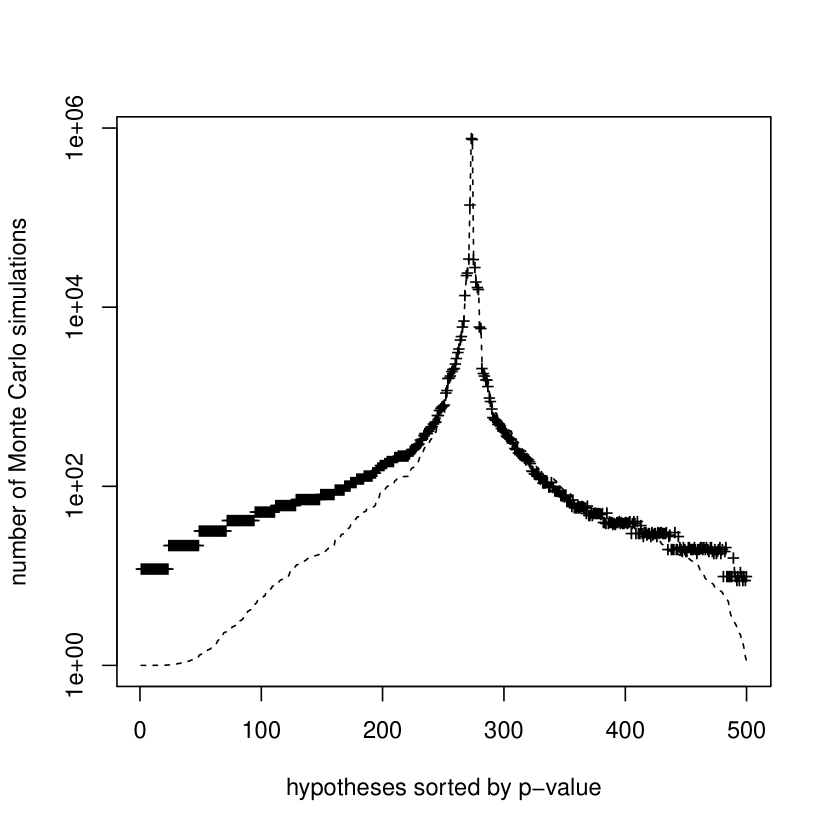

Figure 7 compares the optimal real-valued allocation (dashed line), computed both without (left) and with (right) a pseudo-count (Sections 2.3.1 and 2.3.2), to the SA integer solution of Section 3 (crosses). The p-value distribution is again the mixture distribution of Sandve et al., (2011) (see Section 4.1) with parameters , , and .

As seen in Figure 7, the two allocations are qualitatively similar. The KKT solution (dashed line) is smoother (since it is allowed to allocate a real-valued number of Monte Carlo simulations to each hypothesis) and has a more pronounced spike at the threshold, whereas SA seems to allocate less simulations to hypotheses at the threshold and more simulations to those hypotheses further away from the threshold.

For the case (Figure 7, left), the optimal allocation of simulations is found for (in this example run). For the case (Figure 7, right), the computation of the optimal allocation was initially not possible since the hypotheses with ranks (based on the ordered p-values) caused the search interval for the optimal to be empty (see Section 2.3.2). Removing the hypotheses with indices in led to which translates to the range of simulations that can be allocated in an optimal way using KKT. Since falls within that range, the optimal was efficiently found.

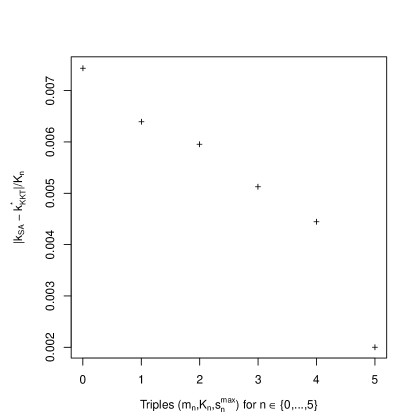

To quantify the similarity between the SA and KKT solutions, Figure 8 compares both allocations as the number of hypotheses , the number of Monte Carlo simulations , and the number of iterations of SA increase. Naturally, when increasing , it is necessary to increase as well to ensure that enough simulations are available for all hypotheses, and likewise with increasing parameters and the SA algorithm requires more iterations to compute allocations. The parameters , and are thus increased together as for . As SA allocates an integer number of simulations, it seems unreasonable to assume that the SA allocation in vector and the optimal real-valued KKT allocation will coincide in an sense. Instead, Figure 8 shows , the relative difference in norm between the two allocation vectors which is normalised with respect to the number of simulations spent. Each datapoint is the median of repetitions. Figure 8 indicates that the normalised difference between both allocation vectors seems to decrease.

4.3 Comparison to Thompson sampling in the QuickMMCTest algorithm

This section compares the optimal KKT allocation computed in Section 2.3 with the allocation returned by the QuickMMCTest algorithm of Gandy and Hahn, (2017).

QuickMMCTest can be used to compute a decision (rejection or non-rejection) for a given set of hypotheses with unknown p-values based solely on Monte Carlo simulations. The algorithm aims to use more simulations for hypotheses with an (analytical and unknown) p-value close to the testing threshold (thus having a less stable decision, in the sense that their decision switches from being rejected to non-rejected if the data were analysed repeatedly), and less simulations for hypotheses with a p-value further away from the threshold (thus having a more stable decision). To compute a stability measure, QuickMMCTest starts with a uniform prior on the p-value of each hypothesis and updates a Beta-Binomial model for each p-value as more simulations are generated. Based on Thompson sampling (Thompson,, 1933; Agrawal and Goyal,, 2012), in each iteration, a new p-value is drawn from each posterior and new rejections and non-rejections are computed for the sampled p-value distribution. Repeating this step several times gives a measure of how stable the current decision on each hypothesis is, which is then used to compute weights employed to allocate a new batch of simulations. Further details can be found in Gandy and Hahn, (2017).

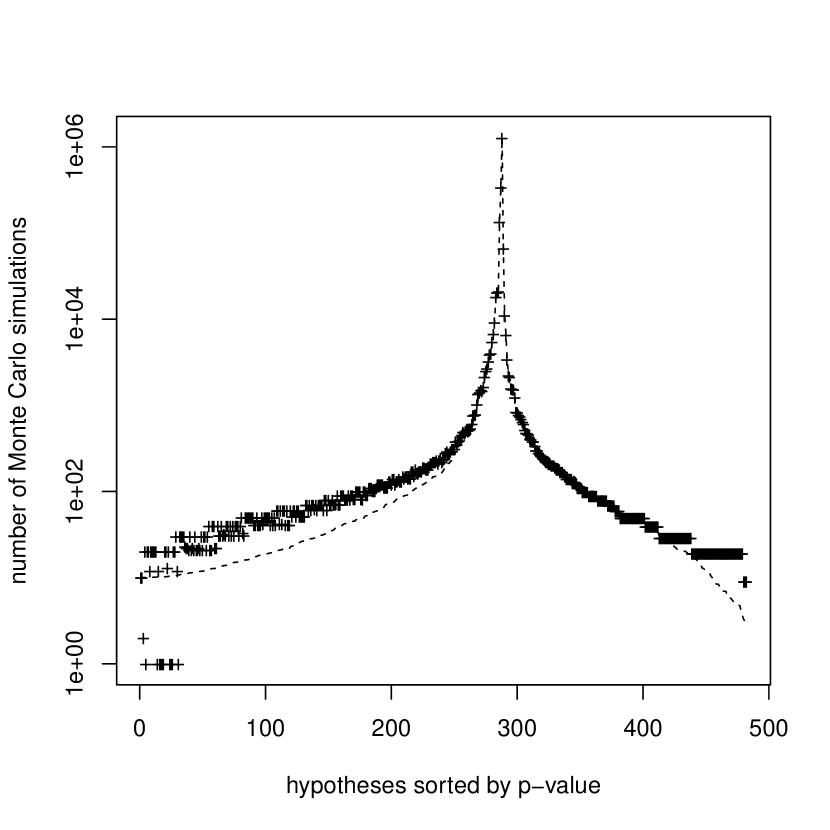

Figure 9 (left) shows the number of Monte Carlo simulations allocated to each hypothesis in an example run of QuickMMCTest (crosses), as well as the optimal KKT allocation (dashed line). For this, p-values were generated using the Sandve et al., (2011) distribution (see Section 4.1) with and the two allocations were computed with and . To ensure a fine-tuned allocation, QuickMMCTest was run with parameter (that is with a low average number of simulations spent per hypothesis in each iteration), all other parameters were kept at the default values given in Gandy and Hahn, (2017). As visible in Figure 9 (left), QuickMMCTest manages to allocate simulations without knowledge of the p-values in a qualitatively similar fashion to the optimal allocation.

To quantify this similarity, as in Section 4.2, both the QuickMMCTest allocation and the optimal KKT allocation are compared as both the number of hypotheses and the number of simulations increase. Like SA, QuickMMCTest is a probabilistic method which allocates integer numbers of simulations and thus Figure 9 (right) shows , the relative difference in norm between the two allocation vectors which is normalised with respect to the number of simulations spent. The parameters and are increased together as for . Each datapoint is the median of repetitions. As visible in the plot, the normalised difference between both allocation vectors seems to decrease.

A repetition of this experiment for a higher proportion of null hypotheses can be found in Section B, again confirming the asympotic similarity of the two allocation vectors.

4.4 Comparison to other algorithms on a real dataset

This section compares QuickMMCTest to other algorithms on a dataset of gene modifications (so-called H3K4me2 modifications) of Pekowska et al., (2010). This dataset was used as a motivating example in the original publication of QuickMMCTest in Gandy and Hahn, (2017). The dataset contains midpoints of gene modifications on a genome, and the permutation test of (Sandve et al.,, 2011, Section 3.2) is used in Gandy and Hahn, (2017) to test if gene modifications appear more often in the lower half of the genome. Preparing the dataset as outlined in (Gandy and Hahn,, 2017, Section 3) leads to hypotheses under consideration.

QuickMMCTest is compared to the seven algorithms listed in Section 1, precisely the naïve method which generates a constant number of simulations per hypothesis as well as the algorithms of Besag and Clifford, (1991), Guo and Peddada, (2008), van Wieringen et al., (2008), Sandve et al., (2011), Jiang and Salzman, (2012), and Gandy and Hahn, (2014). Each of those algorithms relies on one or more parameter, and the specific choice of parameters employed in this section is given in Section C for each algorithm.

The optimal allocation derived in Section 2.2 requires full knowledge of the p-values of all hypotheses, which are actually unavailable for a real dataset. Therefore, the p-values of all hypotheses are approximated once using permutations per hypothesis. The resulting p-value estimates (computed with a pseudo-count) are used to both compute the optimal KKT allocation of Monte Carlo simulations as well as to model the number of exceedances by drawing Binomial samples as described in Section 2.1. Moreover, computing the optimal allocation for a p-value distribution with many hypotheses and a high proportion of true nulls can be computationally challenging due to numerical instabilities of the KKT derivatives. Therefore, to simply computations, a subsample of size of the p-values of the Pekowska et al., (2010) dataset is taken once without replacement, since such a subsample preserves the overall shape of the p-value distribution. All algorithms are applied to this subsample in a single run.

All algorithms were given simulations to allocate. Testing was carried out using a corrected Bonferroni threshold of .

Figure 10 shows the allocation of simulations for QuickMMCTest (left) as well as for Guo and Peddada, (2008) (middle) and Sandve et al., (2011) (right). As observed in Figure 9, QuickMMCTest yields an allocation of a qualitative similar shape as the optimal KKT allocation. The algorithm of Guo and Peddada, (2008) approximates the shape of the optimal KKT allocation by allocating large numbers of batches to the left and to the right of the KKT peak. Though not shown here, the algorithms of van Wieringen et al., (2008) and Gandy and Hahn, (2014) produce similar allocations. In contrast, the algorithm of Sandve et al., (2011) closely approximates the right half of the KKT allocation (corresponding to larger p-values), and uses an upper bound on the number of simulations that hypotheses with small p-values receive. The algorithms of Besag and Clifford, (1991) and Jiang and Salzman, (2012) produce similar allocations (figures not shown here). The naïve method distributes a constant number of Monte Carlo simulations to each hypothesis which results in the worst approximation of the KKT allocation.

| algorithm | |

|---|---|

| QuickMMCTest | 0.115 |

| naïve method | 0.196 |

| Besag and Clifford, (1991) | 0.193 |

| Guo and Peddada, (2008) | 0.134 |

| van Wieringen et al., (2008) | 0.187 |

| Sandve et al., (2011) | 0.191 |

| Jiang and Salzman, (2012) | 0.174 |

| Gandy and Hahn, (2014) | 0.173 |

Table 1 shows the normalised difference of the allocation vector of each algorithm to the optimal KKT allocation (see Section 4.2). The table shows that indeed, the allocation of QuickMMCTest yields the closest allocation to the KKT one, followed by the algorithm of Guo and Peddada, (2008). Empirically it turns out that QuickMMCTest often allocates considerably more simulations than the optimal KKT allocation in the peak around the threshold (see Figure 10, left), a fact which worsens the quality of its allocation, and that as increases, the discrepancy of QuickMMCTest to the other algorithms decreases.

5 Discussion

This article considered the problem of allocating a fixed number of Monte Carlo simulations to hypotheses tested with the Bonferroni correction in order to approximate p-values. When estimating p-values both with or without a pseudo-count (Davison and Hinkley,, 1997), the optimal real-valued (and normally approximated) allocation is derived and computed, and a scheme based on simulated annealing is proposed to compute an approximation to the optimal integer allocation.

A simulation study shows that the real-valued and normally approximated optimal KKT solution is qualitatively similar to the SA integer solution, and moreover that the relative difference between both allocations seems to decrease (to zero) as . Moreover, the allocation returned by the QuickMMCTest algorithm of Gandy and Hahn, (2017) is compared to the optimal KKT solution. QuickMMCTest approximates unknown p-values at runtime while the testing of all hypotheses is in progress, and aims to efficiently allocate the Monte Carlo simulations to the hypotheses whose decision (rejected or non-rejected) is most “unstable” (see Section 4.3). Simulations show that the allocation of QuickMMCTest computed at runtime seems to asympotically coincide with the optimal KKT solution, thus making QuickMMCTest a very attractive method to carry out multiple testing in practice. The results also give an intuition behind the low numbers of misclassifications already observed for this algorithm in Gandy and Hahn, (2017).

The current article leaves scope for further avenues of research. First, since a derivation of the optimal integer allocation seems infeasible (due to the fact that the problem is non-convex), it would be worth investigating how far away the optimal real-valued KKT solution is from (one of the) optima of the integer allocation: this could, in principle, be approached using subdifferential versions of the KKT conditions (Ruszczynski,, 2006). Second, a theoretical analysis of QuickMMCTest could lead to an intuition for a formal proof that its allocation indeed satisfies some kind of asympotic optimality. This is not entirely unlikely since QuickMMCTest essentially borrows its strength from Thompson sampling (Thompson,, 1933), for which optimality statements have already been proven in the related context of multi-armed bandit methodology (Agrawal and Goyal,, 2012).

Appendix A Auxiliary lemma

Lemma 1.

If and , the derivatives defined in (4) are negative and strictly increase to zero as for all .

Proof.

Case : Substitute into (4) and write , where

Since , and (since ), and as is positive, it follows that and , thus .

As and , both functions and converge to zero as , thus as .

For , . Likewise, for . Thus both functions and are strictly decreasing, and so is their product , implying that is strictly increasing.

The case is proven similarly. ∎

Under the assumption that the p-values are drawn from a distribution which is absolutely continuous with respect to the Lebesgue measure, and since for a finite , the probability of the event is zero. The condition in Lemma 1 is therefore not a restriction when computing the optimal (real-valued) allocation for randomly drawn p-values.

Appendix B Repetition of the comparison with QuickMMCTest

Figure 11 repeats the comparison of the optimal real-valued KKT allocation to the one of the QuickMMCTest algorithm for a dataset of p-values generated from the Sandve et al., (2011) distribution with . A proportion of true null hypotheses close to one is what would be expected in real data studies.

As in Section 4.3, the total number of simulations was , a standard Bonferroni type threshold of was employed, and QuickMMCTest was run with parameter .

Figure 11 (left) shows that QuickMMCTest again captures well the spike in the optimal allocation of Monte Carlo simulations. Figure 11 (right) shows the relative difference in norm between the two allocation vectors, which is normalised with respect to the number of simulations . As in Section 4.3, the parameters and are increased together as for . Each datapoint is the median of repetitions. The figure shows that after an initial slight increase, the difference between the optimal KKT allocation and the one of QuickMMCTest decreases as increases. The origin of the initial slight increase is unknown and remains for further research.

Appendix C Choice of parameters for published methods

The algorithms employed in Section 4.4 were run with the following choice of parameters:

-

1.

The naïve method generated simulations per hypothesis.

-

2.

Besag and Clifford, (1991) sequentially generated one Monte Carlo simulation at a time for each hypothesis until either exceedances (as proposed by the authors) were observed (in which case this hypothesis was excluded from receiving further simulations) or the total number of simulations was reached.

- 3.

-

4.

van Wieringen et al., (2008) was employed using the upper quantile of the standard Normal distribution (as proposed by the authors) and a batch size of simulations.

- 5.

-

6.

Jiang and Salzman, (2012) was employed with parameters , , and a batch size of one (as proposed by the authors in their simulation study).

- 7.

References

- Agrawal and Goyal, (2012) Agrawal, S. and Goyal, N. (2012). Analysis of Thompson Sampling for the Multi-armed Bandit Problem. Proceedings of the 25th Annual Conference on Learning Theory, 23(39):1–26.

- Avriel and Wilde, (1966) Avriel, M. and Wilde, D. (1966). Optimality proof for the symmetric Fibonacci search technique. Fibonacci Quart, 4:265–269.

- Benjamini and Hochberg, (1995) Benjamini, Y. and Hochberg, Y. (1995). Controlling the false discovery rate: A practical and powerful approach to multiple testing. J Roy Stat Soc B Met, 57(1):289–300.

- Besag and Clifford, (1991) Besag, J. and Clifford, P. (1991). Sequential Monte Carlo p-values. Biometrika, 78(2):301–304.

- Bonferroni, (1936) Bonferroni, C. (1936). Teoria statistica delle classi e calcolo delle probabilità. Pubblicazioni del R Istituto Superiore di Scienze Economiche e Commerciali di Firenze, 8:3–62.

- Chen and Chen, (2017) Chen, Y. and Chen, Y. (2017). An Efficient Sampling Algorithm for Network Motif Detection. J Comput Graph Stat, pages 1–31.

- Clopper and Pearson, (1934) Clopper, C. and Pearson, E. (1934). The Use of Confidence or Fiducial Limits Illustrated in the Case of the Binomial. Biometrika, 26(4):404–413.

- Davidson and MacKinnon, (2000) Davidson, R. and MacKinnon, J. (2000). Bootstrap tests: How many bootstraps? Economet Rev, 19(1):55–68.

- Davison and Hinkley, (1997) Davison, A. and Hinkley, D. (1997). Bootstrap Methods and Their Application. Cambridge University Press.

- Ding et al., (2018) Ding, D., Gandy, A., and Hahn, G. (2018). A simple method for implementing Monte Carlo tests. arXiv:1611.01675, pages 1–17.

- Fay and Follmann, (2002) Fay, M. and Follmann, D. (2002). Designing Monte Carlo implementations of permutation or bootstrap hypothesis tests. Amer Statist, 56(1):63–70.

- Fay et al., (2007) Fay, M., Kim, H.-J., and Hachey, M. (2007). On using truncated sequential probability ratio test boundaries for Monte Carlo implementation of hypothesis tests. J Comput Graph Stat, 16(4):946–967.

- Gallagher et al., (2018) Gallagher, S., Richardson, L., Ventura, S., and Eddy, W. (2018). SPEW: Synthetic Populations and Ecosystems of the World. J Comput Graph Stat, pages 1–30.

- Gandy, (2009) Gandy, A. (2009). Sequential Implementation of Monte Carlo Tests With Uniformly Bounded Resampling Risk. J Am Stat Assoc, 104(488):1504–1511.

- Gandy and Hahn, (2014) Gandy, A. and Hahn, G. (2014). MMCTest – A Safe Algorithm for Implementing Multiple Monte Carlo Tests. Scand J Stat, 41(4):1083–1101.

- Gandy and Hahn, (2016) Gandy, A. and Hahn, G. (2016). A Framework for Monte Carlo based Multiple Testing. Scand J Stat, 43(4):1046–1063.

- Gandy and Hahn, (2017) Gandy, A. and Hahn, G. (2017). QuickMMCTest: quick multiple Monte Carlo testing. Stat Comput, 27(3):823–832.

- Guo and Peddada, (2008) Guo, W. and Peddada, S. (2008). Adaptive Choice of the Number of Bootstrap Samples in Large Scale Multiple Testing. Stat Appl Genet Mol Biol, 7(1):1–16.

- Henderson et al., (2003) Henderson, D., Jacobson, S., and Johnson, A. (2003). The Theory and Practice of Simulated Annealing (in the ’Handbook of Metaheuristics’ of Glover and Kochenberger), volume 57. Springer, Boston, MA.

- Hochberg, (1988) Hochberg, Y. (1988). A sharper Bonferroni procedure for multiple tests of significance. Biometrika, 75(4):800–802.

- Holm, (1979) Holm, S. (1979). A Simple Sequentially Rejective Multiple Test Procedure. Scand J Stat, 6(2):65–70.

- Jiang and Salzman, (2012) Jiang, H. and Salzman, J. (2012). Statistical properties of an early stopping rule for resampling-based multiple testing. Biometrika, 99(4):973–980.

- Karush, (1939) Karush, W. (1939). Minima of Functions of Several Variables with Inequalities as Side Constraints. MSc Dissertation, Dept of Mathematics, Univ of Chicago, Chicago, Illinois.

- Kiefer, (1953) Kiefer, J. (1953). Sequential minimax search for a maximum. P Am Math Soc, 4(3):502–506.

- Kim, (2010) Kim, H.-J. (2010). Bounding the resampling risk for sequential Monte Carlo implementation of hypothesis tests. J Stat Plan Infer, 140(7):1834–1843.

- Kirkpatrick et al., (1983) Kirkpatrick, S., Gelatt Jr, C., and Vecchi, M. (1983). Optimization by Simulated Annealing. Science, 220(4598):671–680.

- Kuhn and Tucker, (1951) Kuhn, H. and Tucker, A. (1951). Nonlinear Programming. Proc Second Berkeley Symp on Math Statist and Prob, pages 481–492.

- Lai, (1976) Lai, T. (1976). On confidence sequences. Ann Stat, 4(2):265–280.

- Lan and Wittes, (1988) Lan, K. and Wittes, J. (1988). The b-value: a tool for monitoring data. Biometrics, 44(2):579–585.

- Luenberger, (2003) Luenberger, D. (2003). Linear and Nonlinear Programming. Springer, 2nd edition.

- Mestres et al., (2017) Mestres, A., Bochkina, N., and Mayer, C. (2017). Selection of the Regularization Parameter in Graphical Models using Network Characteristics. J Comput Graph Stat, pages 1–27.

- Mrkvic̆ka et al., (2017) Mrkvic̆ka, T., Myllymäki, M., and Hahn, U. (2017). Multiple Monte Carlo testing, with applications in spatial point processes. Stat Comput, 27:1239–1255.

- Pekowska et al., (2010) Pekowska, A., Benoukraf, T., Ferrier, P., and Spicuglia, S. (2010). A unique h3k4me2 profile marks tissue-specific gene regulation. Genome Research, 20(11):1493–1502.

- Pesarin et al., (2016) Pesarin, F., Salmaso, L., Carrozzo, E., and Arboretti, R. (2016). Union-intersection permutation solution for two-sample equivalence testing. Stat Comput, 26:693–701.

- Phipson and Smyth, (2010) Phipson, B. and Smyth, G. (2010). Permutation P-values Should Never Be Zero: Calculating Exact P-values When Permutations Are Randomly Drawn. Stat Appl Genet Molec Biol, 9(1).

- R Development Core Team, (2011) R Development Core Team (2011). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Ruszczynski, (2006) Ruszczynski, A. (2006). Nonlinear Optimization. Princeton University Press.

- Sandve et al., (2011) Sandve, G., Ferkingstad, E., and Nygard, S. (2011). Sequential Monte Carlo multiple testing. Bioinformatics, 27(23):3235–3241.

- Shen et al., (2014) Shen, D., Shen, H., Bhamidi, S., Maldonado, Y., Kim, Y., and Marron, J. (2014). Functional Data Analysis of Tree Data Objects. J Comput Graph Stat, 23(2):418–438.

- Sidak, (1967) Sidak, Z. (1967). Rectangular confidence regions for the means of multivariate normal distributions. J Am Stat Assoc, 62(318):626–633.

- Silva and Assunção, (2013) Silva, I. and Assunção, R. (2013). Optimal generalized truncated sequential Monte Carlo test. J Multivariate Anal, 121:33–49.

- Silva and Assunção, (2018) Silva, I. and Assunção, R. (2018). Truncated sequential Monte Carlo test with exact power. Brazilian Journal of Probability and Statistics, 32(2):215–238.

- Silva et al., (2009) Silva, I., Assunção, R., and Costa, M. (2009). Power of the sequential Monte Carlo test. Sequential Anal, 28(2):163–174.

- Simes, (1986) Simes, R. (1986). An improved Bonferroni procedure for multiple tests of significance. Biometrika, 73(3):751–754.

- Tang et al., (2017) Tang, M., Athreya, A., Sussman, D., Lyzinski, V., Park, Y., and Priebe, C. (2017). A Semiparametric Two-Sample Hypothesis Testing Problem for Random Graphs. J Comput Graph Stat, 26(2):344–354.

- Thompson, (1933) Thompson, W. (1933). On the Likelihood that One Unknown Probability Exceeds Another in View of the Evidence of Two Samples. Biometrika, 25(3/4):285–294.

- van Wieringen et al., (2008) van Wieringen, W., van de Wiel, M., and van der Vaart, A. (2008). A Test for Partial Differential Expression. J Am Stat Assoc, 103(483):1039–1049.

- Wei et al., (2016) Wei, S., Lee, C., Wichers, L., and Marron, J. (2016). Direction-Projection-Permutation for High-Dimensional Hypothesis Tests. J Comput Graph Stat, 25(2):549–569.

- Zhang et al., (2017) Zhang, Y., Zhou, H., Zhou, J., and Sun, W. (2017). Regression Models for Multivariate Count Data. J Comput Graph Stat, 26(1):1–13.