Rational Multi-Curve Models with

Counterparty-Risk Valuation Adjustments

Abstract

We develop a multi-curve term structure setup in which the modelling ingredients are expressed by rational functionals of Markov processes. We calibrate to LIBOR swaptions data and show that a rational two-factor lognormal multi-curve model is sufficient to match market data with accuracy.

We elucidate the relationship between the models developed and calibrated under a risk-neutral measure and their consistent equivalence class under the real-world probability measure . The consistent -pricing models are applied to compute the risk exposures which may be required to comply with regulatory obligations. In order to compute counterparty-risk valuation adjustments, such as CVA, we show how positive default intensity processes with rational form can be derived. We flesh out our study by applying the results to a basis swap contract.

Keywords:

Multi-curve interest rate term structure, forward LIBOR process, rational asset pricing models, calibration, counterparty-risk, risk management, Markov functionals, basis swap.

1 Introduction

In this work we endeavour to develop multi-curve interest rate models which extend to counterparty risk models in a consistent fashion. The aim is the pricing and risk management of financial instruments with price models capable of discounting at multiple rates (e.g. OIS and LIBOR) and which allow for corrections in the asset’s valuation scheme so to adjust for counterparty-risk inclusive of credit, debt, and liquidity risk. We thus propose factor-models for (i) the Overnight Index Swap (OIS) rate, (ii) the London Interbank Offer Rate (LIBOR), and (iii) the default intensities of two counterparties involved in bilateral OTC derivative transactions. The three ingredients are characterised by a feature they share in common: the rate and intensity models are all rational functions of the underlying factor processes. In choosing this class of models, we look at a number of properties we would like the models to exhibit. They should be flexible enough to allow for the pricing of a range of financial assets given that all need discounting and no security is insulated from counterparty-risk. Since we have in mind the pricing of assets as well as the management of risk exposures, we also need to work within a setup that maintains price consistency under various probability measures. We will for instance want to price derivatives by making use of a risk-neutral measure while analysing the statistics of risk exposures under the real-world measure . This point is particularly important when we calibrate the interest rate models to derivatives data, such as (implied) volatilities, and then apply the calibrated models to compute counterparty-risk valuation adjustments to comply with regulatory requirements. The presented rational models allow us to develop a comprehensive framework that begins with an OIS model, evolves to an approach for constructing the LIBOR process, includes the pricing of fixed-income assets and model calibration, analyses risk exposures, and concludes with a credit risk model that leads to the analysis of counterparty-risk valuation adjustments (XVA).

The issue of how to model multi-curve interest rates and incorporate counterparty-risk valuation adjustments in a pricing framework has motivated much research. For instance, research on multi-curve interest rate modelling is presented in \citeNKijimaTanakaWong09, \citeNKenyon10, \citeANPHenrard07 (\citeyearNPHenrard07, \citeyearNPHenrard09, \citeyearNPHenrard14), \citeNBianchetti10, Mercurio (\citeyearNPMercurio2010, \citeyearNPMercurio2010a, \citeyearNPmerc), \citeANPFujii2009 (\citeyearNPFujii2009, \citeyearNPFujii2010), \citeNMoreniPallavicini10, \citeNBianchettiMorini13, \citeNFilipovicTrolle11 and \citeNCrepeyGrbacNgorSkovmand13. On counterparty-risk valuation adjustment, we mention two recent books by \citeNBrigoMoriniPallavicini12 and \citeNCrepeyBieleckiBrigo14; more references are given as we go along. Pricing models with rational form have also appeared before. \citeNfh pioneered such pricing models and in particular introduced the so-called rational log-normal model for discount bond prices. For further contributions and studies in this context we refer to \citeNRut, \citeNds and \citeNHuntKennedy. More recent work on rational pricing models include \citeNBH, \citeNhr, \citeNBHMackie, \citeNahtt, \citeNFLT, \citeNAMPAP, and \citeNNguyenSeifried2014. However, as far as we know, the present paper is the first to apply such models in a multi-curve setup, along with \citeNNguyenSeifried2014, who develop a rational multi-curve model based on a multiplicative spread. It is the only one to deal with XVA computations. We shall see that, despite the simplicity of these models, their performances in these regards are comparable to those by \citeNCrepeyGrbacNgorSkovmand13 or \citeANPMoreniPallavicini10 (\citeyearNPMoreniPallavicini13, \citeyearNPMoreniPallavicini10). Other recent related research includes \citeNFLT, for the study of unspanned volatility and its regulatory implications, \citeNCuchieroKeller-ResselTeichmann12, for moment computations in financial applications, and \citeNChengTehranchi, motivated by stochastic volatility modelling.

We give a brief overview of this paper. In Section 2, we introduce the rational models for multi-curve term structures whereby we derive the forward LIBOR process by pricing a forward rate agreement under the real-world probability measure. In doing so we apply a pricing kernel model. The short rate model arising from the pricing kernel process is then assumed to be a proxy model for the OIS rate. In view of derivative pricing in subsequent sections, we also derive the multi-curve interest rate models by starting with the risk-neutral measure. We call this method “bottom-up risk-neutral approach”. In Section 3, we perform the so-called “clean valuation” of swaptions written on LIBOR, and analyse three different specifications for the OIS-LIBOR dynamics. We explain the advantages one gains from the chosen “codebook” for the LIBOR process, which we model as a rational function where the denominator is in fact the stochastic discount factor associated with the utilised probability measure. In Section 4, we calibrate the three specified multi-curve models and assess them for the quality of fit and on positivity of rates and spread. We conclude by singling out a two-factor lognormal OIS-LIBOR model for its satisfactory calibration properties and acceptable level of tractability. In Section 5, we price a basis swap in closed form without taking into account counterparty-risk, that is we again perform a “clean valuation”. In this section we take the opportunity to show the explicit relationship in our setup between pricing under an equivalent measure and the real-world measure. We compute the risk exposure associated with holding a basis swap and plot the quantiles under both probability measures for comparison. As an example, we apply Lévy random bridges to describe the dynamics of the factor processes under . This enables us to interpret the re-weighting of the risk exposure under as an effect that could be related to, e.g., “forward guidance” provided by a central bank. In the last section, we present default intensity processes with rational form and compute XVA, that is, the valuation adjustments due to credit, debt, and liquidity risk.

2 Rational multi-curve term structures

We model a financial market by a filtered probability space , where denotes the real probability measure and is the market filtration. The no-arbitrage pricing formula for a generic (non-dividend-paying) financial asset with price process , which is characterised by a cash flow at the fixed date , is given by

| (2.1) |

where is the pricing kernel embodying the inter-temporal discounting and risk-adjustments, see e.g. \citeNHuntKennedy. Once the model for the pricing kernel is specified, the OIS discount bond price process is determined as a special case of formula (2.1) by

| (2.2) |

The associated OIS short rate of interest is obtained by

| (2.3) |

where it is assumed that the discount bond system is differentiable in its maturity parameter . The rate is non-negative if the pricing kernel is a supermartingale and vice versa. We next go on to infer a pricing formula for financial derivatives written on LIBOR. In doing so, we also derive a price process (2.6) that we identify as determining the dynamics of the forward LIBOR or, as we shall call it, the LIBOR process. It is this formula for the LIBOR process that reveals the nature of the so-called multi-curve term structure whereby the OIS rate and the LIBOR rates of different tenors are treated as distinct discount rates.

2.1 Generic multi-curve interest rate models

We derive multi-curve pricing models for securities written on the LIBOR by starting with the valuation of a forward rate agreement (FRA). We consider , where are fixed dates, and let be a notional, a strike rate and . The fixed leg of the FRA contract is given by and the floating leg payable in arrear at time is modelled by where the random rate is -measurable. Then we define the net cash flow at the maturity date of the FRA contract to be

| (2.4) |

The FRA price process is then given by an application of (2.1), that is, for by

| (2.5) | |||||

where we define the (forward) LIBOR process by

| (2.6) |

The fair spread of the FRA at time (the value at time such that ) is then expressed in terms of by

| (2.7) |

For times up to and including our LIBOR process can be written in terms of a conditional expectation of an -measurable random variable. In fact, for

| (2.8) | |||||

| (2.9) |

and thus

| (2.10) |

The (pre-crisis) classical approach to LIBOR modelling defines the price process of a FRA by

| (2.11) |

see, e.g., \citeNHuntKennedy. By equating with (2.5), we see that the classical single-curve LIBOR model is obtained in the special case where

| (2.12) |

Remark 2.1.

In normal market conditions, one expects the positive-spread relation , for tenors , to hold. We will return to this relationship in Section 4 where various model specifications are calibrated and the positivity of the spread is checked. LIBOR tenor spreads play a role in the pricing of basis swaps, which are contracts that exchange LIBOR with one tenor for LIBOR with another, different tenor (see Section 5). For recent work on multi-curve modelling with focus on spread modelling, we refer to \citeNCuchieroFontanaGnoatto14.

2.2 Multi-curve models with rational form

In order to construct explicit LIBOR processes, the pricing kernel and the random variable need to be specified in the definition (2.6). For reasons that will become apparent as we move forward in this paper, we opt to apply the rational pricing models proposed in \citeNMac. These models bestow a rational form on the price processes, here intended as a “quotient of summands” (slightly abusing the terminology that usually refers to a “quotient of polynomials”). This explains the terminology in this paper when referring to the class of multi-curve term structures, or to generic asset price models, and later also to the models for counterparty risk valuation adjustments.

The basic pricing model with rational form for a generic financial asset (for short “rational pricing model”) that we consider is given by

| (2.13) |

where is the value of the asset at . There may be more -terms in the numerator, but two (at most) will be enough for all our purposes in this work. For and , are deterministic functions and are martingale processes, not necessarily under but under an equivalent martingale measure , which are driven by -Markov processes . The details of how the expression (2.13) is derived from the formula (2.1), and in particular how explicit examples for can be constructed, are shown in \citeNMac. Here we only give the pricing kernel model associated with the price process (2.13), that is

| (2.14) |

where is the -martingale that induces the change of measure from to an auxiliary measure under which the are martingales. The deterministic functions and are defined such that is a non-negative -supermartingale (see e.g. Example 2.1), and thus in such a way that is a non-negative -supermartingale. By the equations (2.2) and (2.3), it is straightforward to see that

| (2.15) |

where the “dot-notation” means differentiation with respect to time .

Let us return to the modelling of rational multi-curve term structures and in particular to the definition of the (forward) LIBOR process. Putting equations (2.6) and (2.1) in relation, we see that the model (2.13) naturally offers itself as a model for the LIBOR process (2.6) in the considered setup. Since (2.13) satisfies (2.1) by construction, so does the LIBOR model

| (2.16) |

satisfy the martingale equation (2.6) and in particular (2.10) for . In \citeNMac a method based on the use of weighted heat kernels is provided for the explicit construction of the -martingales and thus in turn for explicit LIBOR processes. The method allows for the development of LIBOR processes, which, if circumstances in financial markets require it, by construction take positive values at all times.

2.3 Bottom-up risk-neutral approach

Since we also deal with counterparty-risk valuation adjustments, we present another scheme for the construction of the LIBOR models, which we call “bottom-up risk-neutral approach”. As the name suggest, we model the multi-curve term structure by making use of the risk-neutral measure (via the auxiliary measure ) while the connection to the -dynamics of prices can be reintroduced at a later stage, which is important for the calculation of risk exposures and their management. “Bottom-up” refers to the fact that the short interest rate will be modelled first, then followed by the discount bond price and LIBOR processes. Similarly, in Section 6.1, the hazard rate processes for contractual default will be modelled first, and thereafter the price processes of counterparty risky assets will be derived thereof. We utilise the notation . In the bottom-up setting, we directly model the short risk-free rate in the manner of the right-hand side in (2.15), i.e.

| (2.17) |

by postulating (i) non-increasing deterministic functions and with (later will be seen to coincide with ), and (ii) an -martingale with such that

| (2.18) |

is a positive )-supermartingale for all .

Example 2.1.

Let where is a positive -martingale with ; for example exponential Lévy martingales. The supermartingale (2.18) is positive for any given if .

Associated with the supermartingale (2.18), we characterise the (risk-neutral) pricing measure by the -density process , given by

| (2.19) |

which is taken to be a positive -martingale. Furthermore, we denote by the discount factor associated with the risk-neutral measure .

Lemma 2.1.

.

Proof.

The Ito semimartingale formula applied to and to gives the following relations:

where (2.17) was used in the first line, and

| (2.21) | |||||

where

Therefore, . Moreover, Hence

It then follows that the price process of the OIS discount bond with maturity can be expressed by

| (2.22) |

for , Thus, the process plays the role of the pricing kernel associated with the OIS market under the measure . In particular, we note that for and . A construction inspired by the above formula for the OIS bond leads to the rational model for the LIBOR prevailing over the interval . The -measurable spot LIBOR rate is modelled in terms of and, in this paper, at most two other -martingales and evaluated at :

| (2.23) |

The (forward) LIBOR process is then defined by an application of the risk-neutral valuation formula (which is equivalent to the pricing formula (2.1) under ) as follows. For we let

| (2.24) | |||||

| (2.25) |

and thus, by applying (2.18) and (2.23),

| (2.26) |

Hence, we recover the same model (and expression) as in (2.16). The LIBOR models (2.26) (or (2.16)) are compatible with an HJM multi-curve setup where, in the spirit of \citeNhjm, the initial term structures and are fitted by construction.

Example 2.2.

Let where is a positive -martingale with . For example, one could consider a unit-initialised exponential Lévy martingale defined in terms of a function of an -Lévy process , for . Such a construction produces non-negative LIBOR rates if

| (2.27) |

If this condition is not satisfied, then the LIBOR model may be viewed as a shifted model, in which the LIBOR rates may become negative with positive probability. For different kinds of shifts used in the multi-curve term structure literature we refer to, e.g., \citeNMercurio2010a or \citeNMoreniPallavicini10.

3 Clean valuation

The next questions we address are centred around the pricing of LIBOR derivatives and their calibration to market data, especially LIBOR swaptions, which are the most liquidly traded (nonlinear) interest rate derivatives. Since market data typically reflect prices of fully collaterallised transactions, which are funded at a remuneration rate of the collateral that is best proxied by the OIS rate, we consider in this section, in the perspective of model calibration, clean valuation ignoring counterparty risk and assume funding at the rate

An interest rate swap (see, e.g., \citeNbm) is an agreement between two counterparties, where one stream of future interest payments is exchanged for another based on a specified nominal amount . A popular interest rate swap is the exchange of a fixed rate (contractual swap spread) against the LIBOR at the end of successive time intervals of length . Such a swap can also be viewed as a collection of forward rate agreements. The swap price at time is given by the following model-independent formula:

A swaption is an option between two parties to enter a swap at the expiry date (the maturity date of the option). Its price at time is given by the following -pricing formula:

| (3.28) |

using the formulae (2.22) and (2.26) for and . In particular, the swaption prices at time can be rewritten by use of so that

| (3.29) |

where

As we will see in several instance of interest, these expectations can be computed efficiently with high accuracy by various numerical schemes.

Remark 3.2.

The advantages of modelling the LIBOR process by a rational function of which denominator is the discount factor (pricing kernel) associated with the employed pricing measure (in this case ) are: (i) The rational form of and also of produces, when multiplied with the discount factor , a linear expression in the -martingale drivers . This is in contrast to other akin pricing formulae in which the factors appear as sums of exponentials, see e.g. \citeNCrepeyGrbacNgorSkovmand13, Equation (33). (ii) The dependence structure between the LIBOR process and the OIS discount factor —or the pricing kernel under the -measure—is clear-cut. The numerator of is driven only by idiosyncratic stochastic factors that influence the dynamics of the LIBOR process. We may call such drivers the “LIBOR risk factors”. Dependence on the “OIS risk factors”, in our model example , is produced solely by the denominator of the LIBOR process. (iii) Usually, the FRA process is modelled directly and more commonly applied to develop multi-curve frameworks. With such models, however, it is not guaranteed that simple pricing formulae like (3) can be derived. We think that the “codebook” (2.6), and (2.26) in the considered example, is more suitable for the development of consistent, flexible and tractable multi-curve models.

3.1 Univariate Fourier pricing

Since in current markets there are no liquidly-traded OIS derivatives and hence no useful data is available, a pragmatic simplification is to assume deterministic OIS rates . That is to say , and hence plays no role either, so that it can be assumed equal to zero. Furthermore, for a start, we assume and , and (3.29) simplifies to

where here . For the price is simply . For , and in the case of an exponential-Lévy martingale model with

where is a Lévy process with cumulant such that

| (3.30) |

we have

| (3.31) |

where

and is an arbitrary constant ensuring finiteness of for . For details concerning (3.31), we refer to, e.g., \citeNEberleinGlauPapapantoleon.

3.2 One-factor lognormal model

In the event that and is of the form

| (3.32) |

where is a standard Brownian motion and is a real constant, it follows from simple calculations that the swaption price is given, for by

| (3.33) | ||||

| (3.34) |

where is the standard normal distribution function.

3.3 Two-factor lognormal model

We return to the price formula (3.29) and consider the case where the martingales are given, for by

| (3.35) |

for real constants and standard Brownian motions and with correlation . Then it follows that

| (3.36) |

where , , . Hence,

where

This expression can be simplified further to obtain

The calculation of the swaption price is then reduced to calculating two one-dimensional integrals. Since the regions of integration are not explicitly known, one has to numerically solve for the roots of , which may have up to two roots. Nevertheless a full swaption smile can be calculated in a small fraction of a second by means of this formula.

4 Calibration

The counterparty-risk valuation adjustments, abbreviated by XVAs (CVA, DVA, LVA, etc.), can be viewed as long-term options on the underlying contracts. For their computation, the effects by the volatility smile and term structure matter. Furthermore, for the planned XVA computations of the multi-curve products in Section 6, it is necessary to calibrate the proposed pricing model to financial instruments with underlying tenors of m and m (the most liquid tenors). Similar to \citeNCrepeyGrbacNgorSkovmand13, we make use of the following EUR market Bloomberg data of January 4, 2011 to calibrate our model: EONIA, three-month EURIBOR and six-month EURIBOR initial term structures on the one hand, and three-month and six-month tenor swaptions on the other. As in the HJM framework of \citeNCrepeyGrbacNgorSkovmand13, to which the reader is referred for more detail in this regard, the initial term structures are fitted by construction in our setup. Regarding swaption calibration, at first, we calibrate the non-maturity/tenor-dependent parameters to the swaption smile for the 91 years swaption with a three-month tenor underlying. The market smile corresponds to a vector of strikes bps around the underlying swap spread. Then, we make use of at-the-money swaptions on three and six-month tenor swaps all terminating at exactly ten years, but with maturities from one to nine years. This co-terminal procedure is chosen with a view towards the XVA application in Section 6, where a basis swap with a ten-year terminal date is considered.

In particular, in a single factor setting:

-

1.

First, we calibrate the parameters of the driving martingale to the smile of the 91 years swaption with tenor m. This part of the calibration procedure gives us also the values of , , and which we assume to be equal.

-

2.

Next, we consider the co-terminal, , ATM swaptions with 1, 2,, 9 years. These are available written on the three and six-month rates. We calibrate the remaining values of one maturity at a time, going backwards and starting with the 82 years for the three-month tenor and with the 91 years for the six-month tenor. This is done assuming that the parameters are piecewise constant such that for each and that hold for each .

4.1 Calibration of the one-factor lognormal model

In the one-factor lognormal specification of Section 3.2, we calibrate the parameter and with Matlab utilising the procedure “lsqnonlin” based on the pricing formula (3.33) (if , otherwise ). This calibration yields:

Forcing positivity of the underlying LIBOR rates means, in this particular case, restricting (cf. (2.27)). The constrained calibration yields:

The two resulting smiles can be found in Figure 1, where we can see that the unconstrained model achieves a reasonably good calibration. However, enforcing positivity is highly restrictive since the Gaussian model, in this setting, cannot produce a downward sloping smile.

Next we calibrate the parameters to the ATM swaption term structures of 3 months and 6 months tenors. The results are shown in Figure 2. When positivity is not enforced the model can be calibrated with no error to the market quotes of the ATM co-terminal swaptions. However, one can see from the figure that the positivity constraint does not allow the function to take the necessary values, and thus a very poor fit to the data is obtained, in particular for shorter maturities.

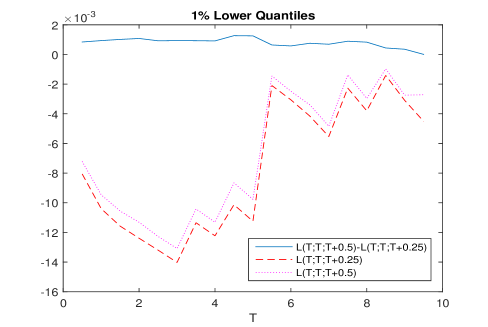

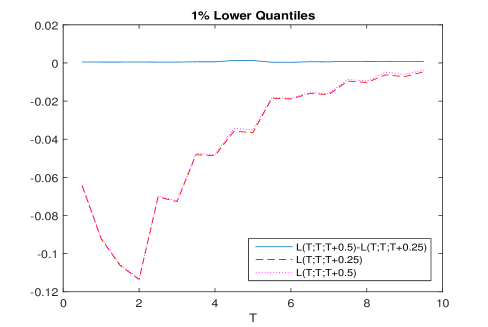

With this in mind the natural question is whether the positivity constraint is too restrictive. Informal discussions with market participants reveal that positive probability for negative rates is not such a critical issue for a model. As long as the probability mass for negative values is not substantial, it is a feature that can be lived with. Indeed assigning a small probability to this event may even be realistic.111As with EONIA since the end of 2014 or Swiss rates in the crisis. In order to investigate the significance of the negative rates and spreads mentioned in remark 2.1, we calculate lower quantiles for spot rates as well as the spot spread for the model calibrated without the positivity constraint. As Figure 3 shows, the lower quantiles for the rates are of no concern. Indeed it can hardly be considered pathological that rates will be below -14 basis points with 1% probability on a three year time horizon. Similarly, with regard to the spot spread, the lower quantile is in fact positive for all time horizons. Further calculations reveal that the probabilities of the eight year spot spread being negative is and the nine year is 0.008 – which again can hardly be deemed pathologically high.

We find that the model performs surprisingly well despite the parsimony of a one-factor lognormal setup. While positivity of rates and spreads are not achieved, the model assigns only small probabilities to the negatives. However, the ability of fitting the smile with such a parsimonious model is not satisfactory (cf. Fig. 1), which is our motivation for the next specification.

4.2 Calibration of exponential normal inverse Gaussian model

The one-factor model, which is driven by a Gaussian factor , is able to capture the level of the volatility smile. Nevertheless, the model implied skew is slightly different from the market skew. To overcome this issue, we now consider a one-factor model driven by a richer family of Lévy processes. The process is now assumed to be the exponential normal inverse Gaussian (NIG) -martingale

| (4.37) |

where is an -NIG-process with cumulant , see (3.30), expressed in terms of the parametrisation222The \citeNBarndorff-Nielsen97 parametrisation is recovered by setting , and . from \citeNContTankov03 as

| (4.38) |

where and The parameters that need to be calibrated at first are and . After the calibration, we obtain

Imposing to get positive rates we obtain instead

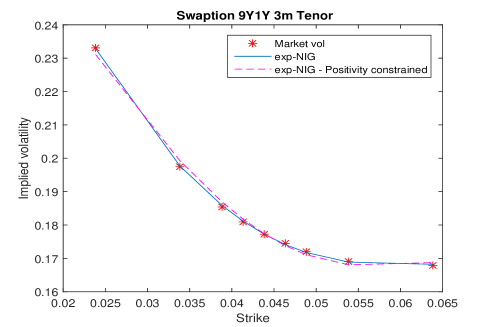

The two fits are plotted in Figure 4. Here, imposing positivity comes at a much smaller cost when compared to the one factor Gaussian case. The NIG process has a richer structure (more parametric freedom) and therefore is able to compensate for an imposed smaller level of the parameter .

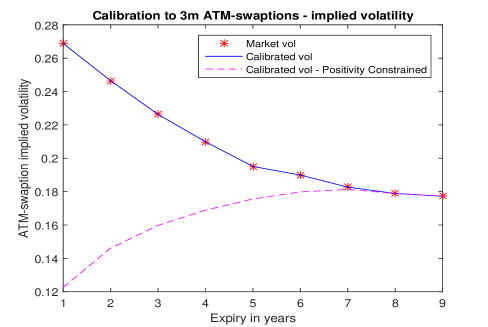

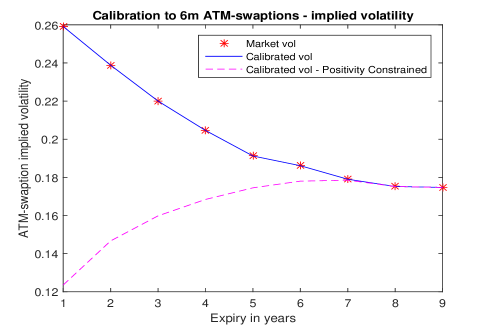

We continue with the second part of the calibration of which results are found in Figure 5. Here we see that enforcing positivity may have a small effect on the smile but it means that the volatility structure cannot be made to match swaptions with maturity smaller than 7 years. Thus, enforcing positivity in this model produces limitations which we wish to avoid.

In Figure 6, we plot lower quantiles for the rates and spreads as for the one-factor lognormal model. While spot spreads remain positive, the levels do not, and, as shown, the model assigns an unrealistically high probability mass to negative values. In fact the model assigns a 1% probability to rates falling below -12% within 2 years! Thus, the one-factor exponential-NIG model loses much of its appeal for it cannot, in a realistic manner, be made to fit long-term smiles and shorter-term ATM volatilities.

4.3 Calibration of a two-factor lognormal model

The necessity to produce a better fit to the smile than what can be achieved with the one-factor Gaussian model, while maintaining positive rates and spreads, leads us to proposing the two-factor specification presented in Section 3.3. This model is heavily parametrised and the parameters at hand are not all identified by the considered data. We therefore fix the following parameters:

| (4.39) | |||

| (4.40) | |||

| (4.41) |

We assume that is constant, i.e. for , and that outside of the region defined above, is piecewise constant such that for each and holds for each . We furthermore assume that . These somewhat ad hoc choices are done with a view towards and being fairly smooth functions of time. We herewith apply a slightly altered procedure to calibrate the remaining parameters if compared to the scheme utilised for the one-factor models.

-

1.

We first calibrate to the smile of the years swaption which gives us the parameters , the assumed constant value of , and to which are assumed equal to a constant . Similar to the exponential-NIG model, we make use of four parameters in total to fit the smile.

-

2.

The remaining parameters are determined a priori, so what remains is to calibrate the values of . The three-month tenor values for are calibrated to ATM, co-terminal swaptions starting from the 82 years and then continuing backwards to the 19 years instruments. For the six-month tenor products, we calibrate for starting with 91 years and proceed backwards.

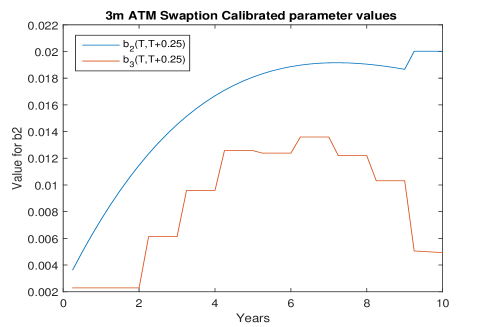

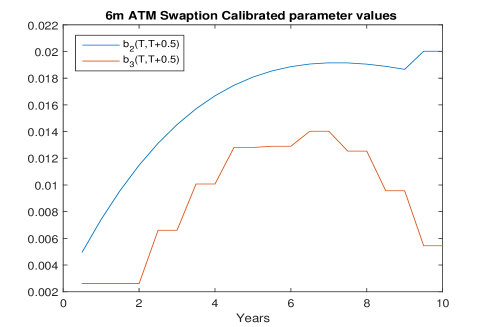

These are the values we obtain from the first calibration phase: . The corresponding fit is plotted in the upper left quadrant of Figure 7.

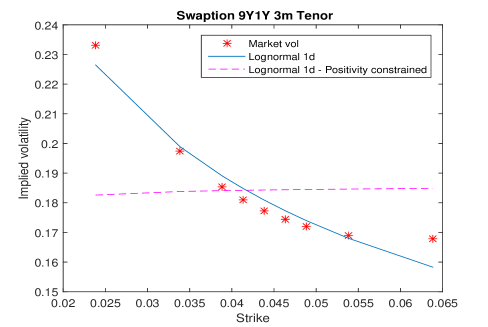

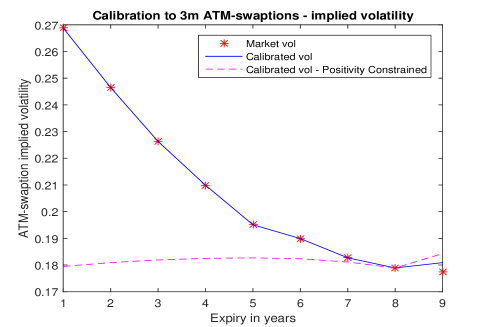

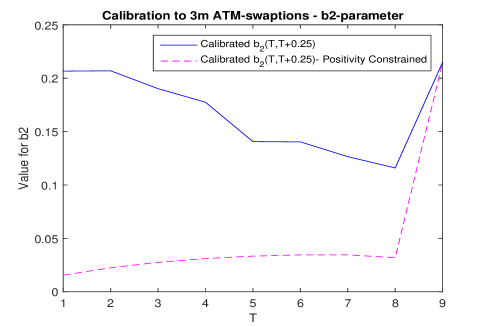

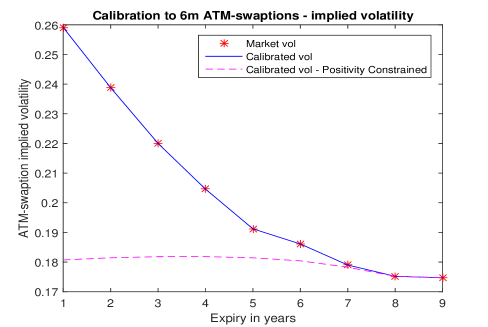

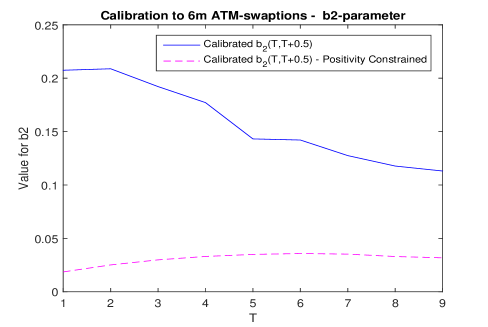

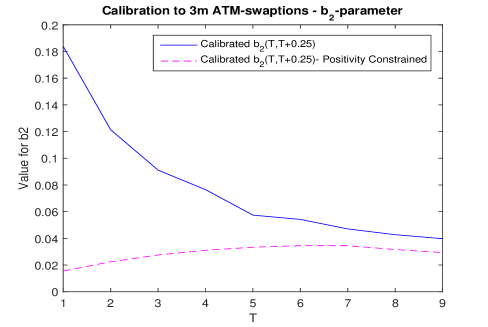

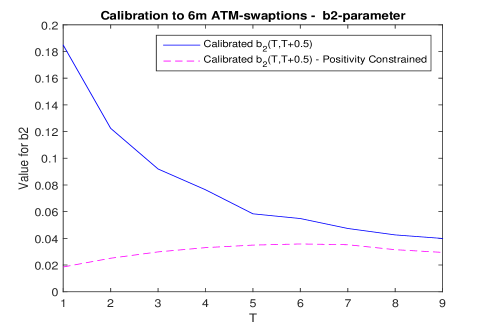

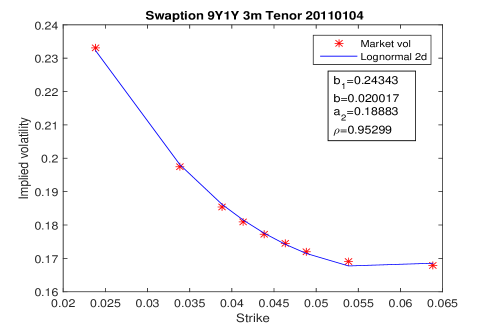

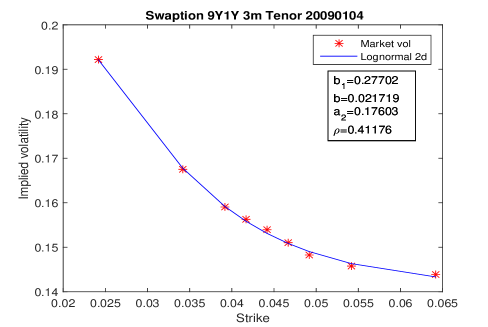

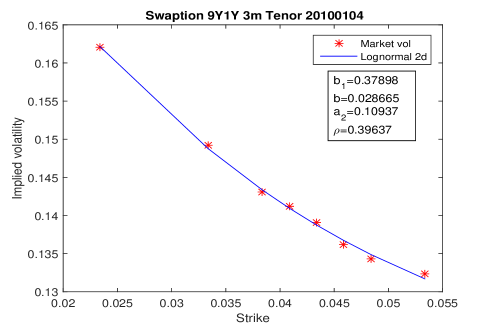

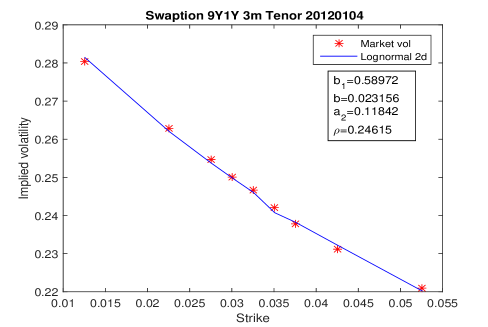

In order to check the robustness of the calibrated fit through time, we also calibrate to three alternative dates. The quality of the fit appears quite satisfactory and comparable to the exponential-NIG model. For all four dates the calibration is done enforcing the positivity condition . However, the procedure yields the exact same parameters even if the constraint is relaxed. We thus conclude that a better calibration appears not to be possible for these datasets by allowing negative rates. Note that it is only for our first data set that the calibrated correlation is as high as . In the other three cases we have , , and . Figure 8 shows the parameters and obtained at the second phase of the calibration to the data of 4 January 2011. As with the previous model (cf. the left graphs of Figures 2 and 5), the volatilities are matched to market data without any error.

We add here that, although not visible from the graphs, the calibrated parameters satisfy the LIBOR spread positivity discussed in Remark 2.1.

In conclusion, we find that the two-factor log-normal has the ability to fit the swaption smile very well, it can be controlled to generate positive rates and positive spreads, and it is tractable with numerically-efficient closed-form expressions for the swaption prices. Given these desirable properties, we discard the one-factor models and retain the two-factor log-normal model for all the analyses in the remaining part of the paper.

5 Basis swap

In this section, we prepare the ground for counterparty-risk analysis, which we shall treat in detail in Section 6. A typical multi-curve financial product, i.e. one that significantly manifests the difference between single-curve and a multi-curve discounting, is the so-called basis swap. Such an instrument uconsists of exchanging two streams of floating payments based on a nominal cash amount or, more generally, a floating leg against another floating leg plus a fixed leg. In the classical single-curve setup, the value of a basis swap (without fixed leg) is zero throughout its life. Since the onset of the financial crisis in 2007, markets quote positive basis swap spreads that have to be added to the smaller tenor leg, which is clear evidence that LIBOR is no longer accepted as an interest rate free of credit or liquidity risk. We consider a basis swap with a duration of ten years where payments based on LIBOR of six-month tenor are exchanged against payments based on LIBOR of three-month tenor plus a fixed spread. The two payment streams start and end at the same times , . The value at time of the basis swap with spread is given by

for . After the swap has begun, i.e. for , the value is given by

where (respectively ) denotes the smallest (respectively ) that is strictly greater than . The spread is chosen to be the fair basis swap spread at so that the basis swap has value zero at inception. We have

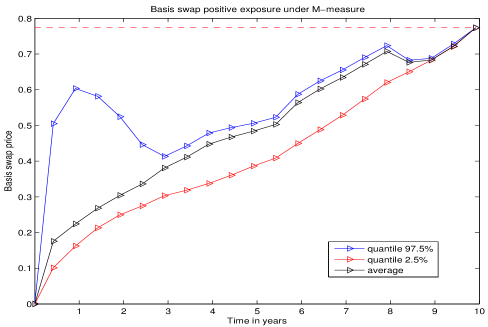

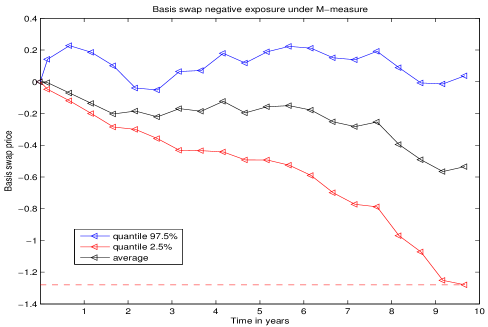

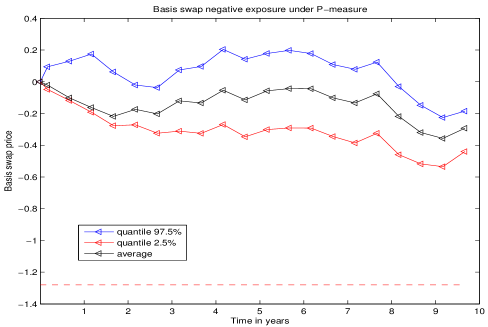

The price processes on which the numerical illustration in Figure 9 have been obtained was simulated by applying the calibrated two-factor lognormal model developed in Section 4.3. The basis swap is assumed to have a notional cash amount and maturity years. In the two-factor lognormal setup, the basis swap spread at time is basis points, which is added to the three-month leg so that the basis swap is incepted at par. The value of both legs is then equal to EUR 27.96. The resulting risk exposure, in the sense of the expectation and quantiles of the corresponding price process at each point in time, is shown in the left graphs of Figure 9, where the right plots correspond to the exposure discussed in Section 5.1. Due to the discrete coupon payments, there are two distinct patterns of the price process exposure, most clearly visible at times preceding payments of the six-month tenor coupons for the first one and at times preceding payments of the three-month tenor coupons without the payments of the six-month tenor coupons for the second one. We show the exposures at such respective dates on the upper and lower plots in Figure 9.

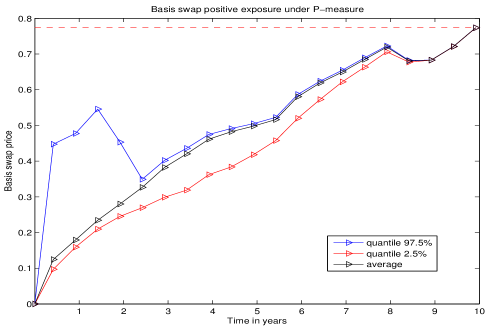

5.1 Lévy random bridges

The basis swap exposures in Figure 9 are computed under the auxiliary -measure. The XVAs that are computed in later sections are derived from these -exposures. However, exposures are also needed for risk management and as such need to be evaluated under the real-world measure . This means that a measure change from to needs to be defined, which requires some thoughts as to what features of a price dynamics under one might like to capture through a specific type of measure change and hence by the induced -model. In other words, we design a measure change so as to induce a particular stochastic behaviour of the processes under , and in particular of the underlying Markov processes driving them.

A special case we consider in what follows is where is a Lévy process under while it adopts the law of a corresponding (possibly multivariate, componentwise) Lévy random bridge (LRB) under . Several explicit asset price models driven by LRBs have been developed in \citeNMac. The LRB-driven rational pricing models have a finite time horizon. The LRB is characterised, apart from the type of underlying Lévy process, by the terminal -marginal distribution to which it is pinned at a fixed time horizon . The terminal distribution can be arbitrarily chosen, but its specification influences the behaviour of the LRB as time approaches . In turn, the properties of a specified LRB influence the behaviour of and hence the dynamics of the considered price process. We see an advantage in having the freedom of specifying the -distribution of the factor process at some fixed future date. This way, we can implement experts’ opinions (e.g. personal beliefs based on some expert analysis) in the -dynamics of the price process as to what level, say, an interest rate (e.g. OIS, LIBOR) is likely to be centred around at a fixed future date.

The recipe for the construction of an LRB can be found in \citeNhhm1, Definition 3.1, which is extended for the development of a multivariate LRB in \citeNMac. LRBs have the property, as shown in Proposition 3.7 of \citeNhhm1, that there exists a measure change to an auxiliary measure with respect to which the LRB has the law of the constituting Lévy process. That is, we suppose the auxiliary measure is and we have an LRB defined on the finite time interval where is fixed. Under and on , has the law of the underlying Lévy process. To illustrate further, let us assume a univariate LRB; the analogous measure change for multivariate LRBs is given in \citeNMac. Under , which stands in relation with via the measure change

| (5.42) |

where is the density function of the underlying Lévy process for all and is the -marginal law of the LRB at the terminal date , the process is an LRB (note that the change of measure is singular at ).

Now, returning to the calibrated two-factor lognormal model of Section 4.3, but similarly also to the other models in Section 4, we may model the drivers and by two dependent Brownian random bridges under . The computed exposures in Figure 9 thus need to be re-weighted by the corresponding amount in order to obtain the -exposures of the basis swap. Since here we employ LRBs, we have the opportunity to include an expert opinion through the LRB marginals as to what level one believes the interest rates will tend to by time . The re-weighted -exposures of the basis swap are plotted in the graphs of the right-hand side of Figure 9. The maximum of the upper quantile curves shown in the graphs is known as the potential future exposure (PFE) at the level 333In practice, people rather consider the expected positive exposure (expectation of the positive part of the price rather than the price) in the PFE computation, but the methodology is the same..

Hence, we now have the means to propose a risk-neutral model that can be calibrated to option data, and which after an explicit measure change can be applied for risk management purposes while offering a way to incorporate economic views in the dynamic of asset prices. Recalling (2.19) and (5.42), the -to- measure change is obtained by

| (5.43) |

and the pricing formula for financial assets (2.1) may be utilised under the various measures as follows:

| (5.44) | |||||

for (since we consider price models driven by LRBs). It follows that the pricing kernel is given by . Measure changes from a risk-neutral to the real-world probability measure are discussed for similar applications also elsewhere. For a recent study in this area of research, we refer to, e.g., \citeNhjs.

6 Adjustments

So far we have focused on so-called “clean computations”, i.e. ignoring counterparty risk and assuming that funding is obtained at the risk-free OIS rate. In reality, contractually specified counterparties at the ends of a financial agreement may default, and funding to enter or honour a financial agreement may come at a higher cost than at OIS rate. Thus, various valuation adjustments need to be included in the pricing of a financial position. The price of a counterparty-risky financial contract is computed as the difference between the clean price, as in Section 3, and an adjustment accounting for counterparty risk and funding costs.

6.1 Rational credit model

As we shall see below, in addition to their use for the computation of PFE, the exposures in Section 5 can be used to compute various adjustments: CVA (credit valuation adjustment), DVA (debt valuation adjustment) and LVA (liquidity-funding valuation adjustment). With this goal in mind, we equip the bottom-up construction in Section 2.3, the notation of which is used henceforth, with a credit component in the following manner.

We consider , which are assumed to be -Markov processes. For any multi-index we write The (market) filtration is given by . For the application in the present section, we fix . The Markov processes and are utilised to drive the OIS and LIBOR models as described in Section 2.3, in particular the zero-initialised -martingales . The Markov processes , , which are assumed to be -independent betweeen them and of the Markov processes , are applied to model -adapted processes defined by

| (6.45) |

where and , with , are non-increasing deterministic functions, and where are zero-initialised -martingales of the form . Comparing with (2.17), we see that (6.45) is modelled in the same way as the OIS rate (2.17), non-negative in particular, as an intensity should be (see Remark 6.3).

In line with the “bottom-up” construction in Section (2.3), we now introduce a density -martingale that induces a measure change from to the risk-neutral measure :

where is defined as in Section 2.3. Here, we furthermore define where the processes

are assumed to be positive true -martingales.

Lemma 6.2.

Let denote any non-negative -measurable random variable and let where, for , is -measurable. Then

| (6.46) |

for or and for .

Proof.

Since is independent of and of ,

Therefore,

Next, the Girsanov formula in combination with the result for -conditional expectation yields:

The result remains to be proven for the case , which is done similarly.

For the XVA computations, we shall use a reduced-form counterparty risk approach in the spirit of \citeNcrepey, where the default times of a bank “b” (we adopt its point of view) and of its counterparty “c” are modeled in terms of three Cox times defined by

| (6.47) |

Under , the random variables () are independent and exponentially distributed. Furthermore, , hence .

We write

which are the so called -hazard intensity processes of the stopping times and where the full model filtration is given as the market filtration -progressively enlarged by and (see, e.g., \citeNBielecki2009, Chapter 5). Writing as before , we note that Lemma 2.1 still holds in the present setup. That is,

an -supermartingale, assumed to be positive (e.g. under an exponential Lévy martingale specification for as of Example 2.2). Further, we introduce , for , and obtain analogously that

| (6.48) |

With these observations at hand, the following results follow from Lemma 6.2. We write and .

Proposition 6.1.

The identities (2.22) and (2.26) still hold in the present setup, that is

| (6.49) |

and, for ,

| (6.50) |

Likewise,

| (6.51) |

| (6.52) | |||||

| (6.53) |

Proof.

Using Lemma 6.2, we compute

| (6.54) | |||||

where the last equality holds by Lemma 2.1. This proves (6.49). The other identities are proven similarly.

Remark 6.3.

Equations (6.49) and (6.51) are similar in nature and appearance. As it is the case for the resulting OIS rate (2.17), the fact that (6.48) is designed to be a supermartingale has as a consequence that the associated intensity (6.45) is a non-negative process. This is readily seen by observing that is a martingale and thus the drift of the supermartingale (6.48) is given by the necessarily non-negative process that drives .

At time , all the hence only the terms remain in these formulas. Since the formulas (6.49) and (6.50) are not affected by the inclusion of the credit component in this approach, the valuation of the basis swap of Section 5 remains unchanged. By making use of the so-called “Key Lemma” of credit risk, see for instance \citeNBielecki2009, the identity (6.53) is the main building block for the pre-default price process of a “clean” CDS on the counterparty (respectively the bank, substituting for in this formula). In particular, the identities at

| (6.55) | |||||

| (6.56) |

for can be applied to calibrate the functions , to CDS curves of the counterparty and the bank, once the dependence on the respective credit risk factors has been specified. The calibration of the “noisy” credit model components , would require CDS option data or views on CDS option volatilities. If the entire model is judged underdetermined, more parsimonious specifications may be obtained by removing the common default component (just letting ) and/or restricting oneself to deterministic default intensities by settting some of the stochastic terms equal to zero, i.e. and/or (as is the case for the one-factor interest rate models in Section 3). The core building blocks of our multi-curve LIBOR model with counterparty-risk are the couterparty-risk kernels , , the OIS kernel , and the LIBOR kernel given by the numerator of the LIBOR process (2.26). We may view all kernels as defined under the -measure, a priori. The respective kernels under the -measure, e.g. the pricing kernel , are obtained as explained at the end of Section 5.

6.2 XVA analysis

In the above reduced-form counterparty-risk setup following \citeNcrepey, given a contract (or portfolio of contracts) with “clean” price process and a time horizon , the total valuation adjustment (TVA) process accounting for counterparty risk and funding cost, can be modelled as a solution to an equation of the form

| (6.57) |

for some coefficient . We note that (6.57) is a backward stochastic differential equation (BSDE) for the TVA process . For accounts on BSDEs and their use in mathematical finance in general and counterparty risk in particular, we refer to, e.g., \citeNElkarouiPengQuenez97, \shortciteNBrigoMoriniPallavicini12 and \citeNcrepey or \shortcite[Part III]CrepeyBieleckiBrigo14. An analysis in line with \citeNcrepey yields a coefficient of the BSDE (6.57) given, for by:

| (6.58) |

where:

-

–

and are the recovery rates of the bank towards the counterparty and vice versa.

-

–

, where (resp. ) denotes the value process of the collateral posted by the counterparty to the bank (resp. by the bank to the counterparty), for instance (used henceforth unless otherwise stated) or .

-

–

The processes and are the spreads with respect to the OIS short rate for the remuneration of the collateral and posted by the counterparty and the bank to each other.

-

–

The process (resp. ) is the liquidity funding (resp. investment) spread of the bank with respect to . By liquidity funding spreads we mean that these are free of credit risk. In particular,

(6.59) where is the all-inclusive funding borrowing spread of the bank and where stands for a recovery rate of the bank to its unsecured lender (which is assumed risk-free, for simplicity, so that in the case of there is no credit risk involved in any case).

The data , and are specified in a credit support annex (CSA) contracted between the two parties. We note that

| (6.60) | |||||

Hence, by setting one obtains the following equivalent formulation of (6.57) and (6.58) under :

| (6.61) |

for and where

| (6.62) |

For the numerical implementations presented in the following section, unless stated otherwise, we set:

| (6.63) |

In the simulation grid one time-step corresponds to one month and or scenarios are produced. We recall the comments made after (6.55) and note that (i) this is a case where default intensities are assumed deterministic, that is () and (ii) the counterparty and the bank may default jointly which is reflected by the fact that

6.2.1 BSDE-based computations

The BSDE (6.61)-(6.62) can be solved numerically by simulation/regression schemes similar to those used for the pricing of American-style options, see \citeNCrepeyGerboudGrbacNgor12, and \citeNCrepeyGrbacNgorSkovmand13. Since in (6.63) we have , the coefficients of the terms coincide in (6.62). This is the case of a “linear TVA” where the coefficient depends linearly on . The results emerging from the numerical BSDE scheme for (6.62) can thus be verified by a standard Monte Carlo computation. Table 1 displays the value of the TVA and its CVA, DVA and LVA components at time zero, where the components are obtained by substituting for in the respective term of (6.62), the TVA process computed by simulation/regression in the first place (see Section 5.2 in \shortciteNCrepeyGerboudGrbacNgor12 for the details of this procedure). The sum of the CVA, DVA and LVA, which in theory equals the TVA, is shown in the sixth column. Therefore, columns two, six and seven yield three different estimates for . Table 2 displays the relative differences between these estimates, as well as the Monte Carlo confidence interval in a comparable scale, which is shown in the last column. The TVA repriced by the sum of its components is more accurate than the regressed TVA. This observation is consistent with the better performance of \citeNLongstaff-Schwartz-98 when compared with \citeNTsitsiklis-VanRoy-2000 in the case of American-style option pricing by Monte Carlo methods (see, e.g., Chapter 10 in \citeNCrepey12).

| m | Regr TVA | CVA | DVA | LVA | Sum | MC TVA |

|---|---|---|---|---|---|---|

| 0.0447 | 0.0614 | -0.0243 | 0.0067 | 0.0438 | 0.0438 | |

| 0.0443 | 0.0602 | -0.0234 | 0.0067 | 0.0435 | 0.0435 |

| m | Sum/TVA | TVA/MC | Sum/MC | CI//MC |

|---|---|---|---|---|

| -2.0114% | 2.0637% | 0.0108 % | 9.7471% | |

| -1.7344 % | 1.7386 % | -0.0259% | 2.9380% |

In Table 3, in order to compare alternative CSA specifications, we repeat the above numerical implementation in each of the following four cases, with set equal to the constant everywhere and all other parameters as in (6.63):

| (6.68) |

| Case | Regr TVA | CVA | DVA | LVA | Sum | Sum/TVA |

|---|---|---|---|---|---|---|

| 1 | 0.0776 | 0.0602 | -0.0234 | 0.0408 | 0.0776 | -0.0464 % |

| 2 | 0.0095 | 0.0000 | 0.0000 | 0.0092 | 0.0092 | -3.6499% |

| 3 | 0.0443 | 0.0602 | -0.0234 | 0.0067 | 0.0435 | -1.7344 % |

| 4 | 0.0964 | 0.0602 | 0.0000 | 0.0376 | 0.0978 | 1.4472% |

Remembering that the value of both legs of the basis swap is equal to EUR 27.96, the number in Table 3 may seem quite small, but one must also bear in mind that the toy model that is used here doesn’t account for any wrong-way risk effect (see \citeNCrepeySong15). In fact, the most informative conclusion of the table is the impact of the choice of the parameters on the relative weight of the different XVA components.

6.2.2 Exposure-based computations

Let’s restrict attention to the case of interest rate derivatives with adapted with respect to We introduce and the function of time

called the expected positive exposure, resp. expected negative exposure. For an interest-rate swap, the EPE and ENE correspond to the mark-to-market of swaptions with maturity written on the swap, which can be recovered analytically if available in a suitable model specification. In general, the EPE/ENE can be retrieved numerically by simulating the exposure.

In view of (6.61)-(6.62), by the time forms of (6.51) and (6.52), the noncollateralised CVA at satisfies (for otherwise =0):

Similarly, for the DVA (for , otherwise ) we have:

For the basis swap of Section 5 and the counterparty risk data (6.63), we obtain by this manner and , quite consistent with the corresponding entries of the second row (i.e. for ) in Table 1. As for the LVA, to simplify its computation, one may be tempted to neglect the nonlinearity that is inherent to (unless ), replacing by 0 in Then, assuming by (6.57)-(6.58), one can compute a linearised LVA at time zero given by

by (6.51) for This is based on the expected (linearised) liquidity exposure

In case of no collateralisation () and of deterministic and , we have

In case of continuous collateralisation () and of deterministic and , the formulas read

As for CVA/DVA, the LVA exposure is controlled by the EPE/ENE functions, but for different “weighting functions”, depending on the CSA. For instance,

for the data (6.63),

the LVA on the basis swap of Section 5 (collateralised or not, since in this case ), we obtain

quite different in relative terms (but these are small numbers) from the exact (as opposed to linearised) value of 0.0067 in Table 1. We note that the stochasticity of the default intensities is averaged out in all these pricing formulas,

but it would appear in more general pricing formulas or in the XVA Greeks even for .

Acknowledgments

The authors thank M. A. Crisafi, C. Cuchiero, C. A. Garcia Trillos and Y. Jiang for useful discussions, and participants of the first Financial Mathematics Team Challenge, University of Cape Town (July 2014), the 5th International Conference of Mathematics in Finance, Kruger Park, South Africa (August 2014), and of the London-Paris Bachelier Workshop, Paris, France (September 2014) for helpful comments. The research of S. Crépey benefited from the support of the “Chair Markets in Transition” under the aegis of Louis Bachelier Laboratory, a joint initiative of École Polytechnique, Université d’Évry Val d’Essonne and Fédération Bancaire Française.

References

- [\citeauthoryearAkahori, Hishida, Teichmann and TsuchiyaAkahori Akahori2014] Akahori, J. , Y. Hishida, J. Teichmann and T. Tsuchiya, A Heat Kernel Approach to Interest Rate Models, Japan Journal of Industrial and Applied Mathematics, DOI 10.1007/s13160-014-0147-3 (2014).

- [\citeauthoryearBarndorff-NielsenBarndorff-Nielsen1997] Barndorff-Nielsen, O. E.. Normal inverse Gaussian distributions and stochastic volatility modelling. Scandavian Journal of Statistics 24, 1–13 (1997).

- [\citeauthoryearBianchettiBianchetti2010] Bianchetti, M.. Two curves, one price. Risk Magazine, August 74–80 (2010).

- [\citeauthoryearBianchetti and MoriniBianchetti and Morini2013] Bianchetti, M. and M. Morini (Eds.) Interest Rate Modelling After the Financial Crisis (2013). Risk Books.

- [\citeauthoryearBielecki, Jeanblanc, and RutkowskiBielecki et al.2009] Bielecki, T. R., M. Jeanblanc, and M. Rutkowski (2009). Credit Risk Modeling. Osaka University Press, Osaka University CSFI Lecture Notes Series 2.

- [\citeauthoryearBrigo and MercurioBrigo and Mercurio2006] Brigo, D. and F. Mercurio, Interest Rate Models - Theory and Practice: With Smile, Inflation and Credit. Springer Verlag (2006).

- [\citeauthoryearBrigo, Morini, and PallaviciniBrigo et al.2013] Brigo, D., M. Morini, and A. Pallavicini. Counterparty Credit Risk, Collateral and Funding: With Pricing Cases For All Asset Classes (2013). Wiley.

- [\citeauthoryearBrody and HughstonBrody and Hughston2004] Brody, D. C., and L. P. Hughston, Chaos and coherence: a new framework for interest-rate modelling, Proceedings of the Royal Society A 460, 2041, 85-110 (2005).

- [\citeauthoryearBrody, Hughston and MackieBrody et al.2012] Brody, D. C., L. P. Hughston, E. Mackie, General theory of geometric Levy models for dynamic asset pricing, Proceedings of the Royal Society A: Mathematical, 468, 1778-1798 (2012).

- [\citeauthoryearCheng and TehranchiCheng and Tehranchi2014] Cheng, S. and M. R. Tehranchi, Polynomial Models for interest rates and stochastic volatility, arXiv 1404.6190 (2014).

- [\citeauthoryearCont and TankovCont and Tankov2003] Cont, R. and P. Tankov. Financial Modelling with Jump Processes. Chapman and Hall/CRC Press (2003).

- [\citeauthoryearCrépeyCrépey2013] Crépey, S. (2013). Financial Modeling: A Backward Stochastic Differential Equations Perspective. Springer Finance Textbooks.

- [\citeauthoryearCrépeyCrépey2012] Crépey, S., Bilateral counterparty risk under funding constraints—Part II: CVA. Mathematical Finance 25(1), 23–50.

- [\citeauthoryearCrépey, Bielecki and BrigoCrépey et al.2014] Crépey, S., T. R. Bielecki, and D. Brigo. Counterparty Risk and Funding–A Tale of Two Puzzles. Chapman and Hall/CRC Financial Mathematics Series (2014).

- [\citeauthoryearCrépey, Gerboud, Grbac, and NgorCrépey et al.2013] Crépey, S., R. Gerboud, Z. Grbac, and N. Ngor. Counterparty risk and funding: The four wings of the TVA. International Journal of Theoretical and Applied Finance 16(2), 1350006 (2013).

- [\citeauthoryearCrépey, Grbac, Ngor and SkovmandCrépey et al.2014] Crépey, S., Z. Grbac, N. Ngor, and D. Skovmand. A Lévy HJM multiple-curve model with application to CVA computation. Quantitative Finance, forthcoming.

- [\citeauthoryearCrépey and SongCrépey and Song2015] Crépey, S. and S. Song (2015). Counterparty risk and funding: Immersion and beyond. LaMME preprint (available on HAL).

- [\citeauthoryearCuchiero, Keller-Ressel and TeichmannCuchiero et al.2012] Cuchiero, C., M. Keller-Ressel, J. Teichmann. Polynomial processes and their applications to mathematical finance. arXiv 0812.4740v2 (2012).

- [\citeauthoryearCuchiero, Fontana and GnoattoCuchiero et al.2014] Cuchiero, C., C. Fontana, A. Gnoatto. A General HJM Framework for multiple yield curve modeling. arXiv 1406.4301v1 (2014).

- [\citeauthoryearDöberlein and SchweizerDöberlein and Schweizer2001] Döberlein, F. and M. Schweizer. On Savings Accounts in Semimartingale Term Structure Models. Stochastic Analysis and Applications 19, 605-626 (2001).

- [\citeauthoryearEberlein, Glau and Papapantoleon Eberlein et al.2010] Eberlein, E., K. Glau and A. Papapantoleon, Analysis of Fourier transform valuation formulas and applications. Applied Mathematical Finance 17 211–240 (2010).

- [\citeauthoryearEl Karoui, Peng, and QuenezEl Karoui et al.1997] El Karoui, N., S. Peng, and M.-C. Quenez. Backward stochastic differential equations in finance. Mathematical Finance 7, 1–71 (1997).

- [\citeauthoryearFilipović and TrolleFilipović and Trolle2013] Filipović, D. and A. B. Trolle. The term structure of interbank risk. Journal of Financial Economics 109, 707–733 (2013).

- [\citeauthoryearFilipović, Larsson and TrolleFilipović et al.2014] Filipović, D., M. Larsson and A. B. Trolle, Linear-Rational Term Stucture Models, ssrn:2397898 (2014).

- [\citeauthoryearFlesaker and HughstonFlesaker and Hughston1996] Flesaker, B. and L. P. Hughston. Positive Interest, Risk Magazine, 9, 46-49 (1996).

- [\citeauthoryearFujii, Shimada, and TakahashiFujii et al.2010] Fujii, M., Y. Shimada, and A. Takahashi. A note on construction of multiple swap curves with and without collateral. FSA Research Review 6, 139–157 (2010).

- [\citeauthoryearFujii, Shimada, and TakahashiFujii et al.2011] Fujii, M., Y. Shimada, and A. Takahashi. A market model of interest rates with dynamic basis spreads in the presence of collateral and multiple currencies. Wilmott Magazine 54, 61–73 (2011).

- [\citeauthoryearHeath, Jarrow and MortonHeath et al.1992] Heath, D., R. Jarrow, A. Morton, Bond Pricing and the Term Structure of Interest Rates: A New Methodology for Contingent Claims Valuation, Econometrica, 60, 77-105 (1992).

- [\citeauthoryearHenrardHenrard2007] Henrard, M.. The irony in the derivatives discounting. Wilmott Magazine 30, 92–98(2007).

- [\citeauthoryearHenrardHenrard2010] Henrard, M.. The irony in the derivatives discounting part II: the crisis. Wilmott Magazine 2, 301–316 (2010).

- [\citeauthoryearHenrardHenrard2014] Henrard, M.. Interest Rate Modelling in the Multi-curve Framework. Palgrave Macmillan, (2014).

- [\citeauthoryearHoyle, Hughston and MacrinaHoyle et al.2011] Hoyle, E., L. P. Hughston, A. Macrina, Lévy Random Bridges and the Modelling of Financial Information, Stochastic Processes and their Applications, 121, 856-884 (2011).

- [\citeauthoryearHughston and RafailidisHughston and Rafailidis2005] Hughston, L. P. and A. Rafailidis, A chaotic approach to interest rate modelling, Finance and Stochastics, 9, 43-65 (2005).

- [\citeauthoryearHull, Sokol and WhiteHull et al.2014] Hull, J. C., A. Sokol and A. White, modelling the short rate: the real and risk-neutral worlds, http://dx.doi.org/10.2139/ssrn.2403067 (2014).

- [\citeauthoryearHunt and KennedyHunt and Kennedy2004] Hunt, P. and J. Kennedy. Financial Derivatives in Theory and Practice. Wiley, revised edition, (2004).

- [\citeauthoryearKenyonKenyon2010] Kenyon, C.. Short-rate pricing after the liquidity and credit shocks: including the basis. Risk Magazine, November 83–87 (2010).

- [\citeauthoryearKijima, Tanaka, and WongKijima et al.2009] Kijima, M., K. Tanaka and T. Wong. A multi-quality model of interest rates. Quantitative Finance 9(2), 133–145 (2009).

- [\citeauthoryearLongstaff and SchwartzLongstaff and Schwartz2001] Longstaff, F. A. and E. S. Schwartz. Valuing American options by simulations: a simple least-squares approach, Review of Financial Studies 14 (1), pp. 113–147 (2001).

- [\citeauthoryearMacrinaMacrina2014] Macrina, A., Heat Kernel Models for Asset Pricing, International Journal of Theoretical and Applied Finance 17 (7), 1-34 (2014).

- [\citeauthoryearMacrina and ParbhooMacrina and Parbhoo2014] Macrina, A. and P. A. Parbhoo, Randomised Mixture Models for Pricing Kernels. Asia-Pacific Financial Markets 21, 281-315 (2014).

- [\citeauthoryearMercurioMercurio2010a] Mercurio, F., A LIBOR market model with stochastic basis. Risk Magazine, December 84–89 (2010).

- [\citeauthoryearMercurioMercurio2010b] Mercurio, F., Interest rates and the credit crunch: new formulas and market models. Technical report, Bloomberg Portfolio Research Paper No. 2010-01-FRONTIERS (2010).

- [\citeauthoryearMercurioMercurio2010c] Mercurio, F., Modern LIBOR Market Models: Using Different Curves for Projecting Rates and for Discounting, International Journal of Theoretical and Applied Finance, 13, 113-137 (2010).

- [\citeauthoryearMoreni and PallaviciniMoreni and Pallavicini2013] Moreni, N. and A. Pallavicini. Parsimonious multi-curve HJM modelling with stochastic volatility. In M. Bianchetti and M. Morini (Eds.), Interest Rate Modelling After the Financial Crisis. Risk Books (2013).

- [\citeauthoryearMoreni and PallaviciniMoreni and Pallavicini2014] Moreni, N. and A. Pallavicini. Parsimonious HJM modelling for multiple yield-curve dynamics. Quantitative Finance 14(2), 199–210 (2014).

- [\citeauthoryearNguyen and SeifriedNguyen and Seifried2014] Nguyen, T. and F. Seifried. The multi-curve potential model. http://ssrn.com/abstract=2502374 (2014).

- [\citeauthoryearParbhooParbhoo2013] Parbhoo, P. A. Information-driven pricing kernel models. PhD Thesis, University of the Witwatersrand (2013).

- [\citeauthoryearRogersRogers1997] Rogers, L. C. G. The Potential Approach to the Term Structure of Interest Rates and Foreign Exchange Rates, Mathematical Finance 7, 157-176 (1997).

- [\citeauthoryearRutkowskiRutkowski1997] Rutkowski, M., A note on the Flesaker-Hughston model of the term structure of interest rates, Applied Mathematical Finance 4, 151-163.

- [\citeauthoryearTsitsiklis and Van RoyTsitsiklis and Van Roy2001] Tsitsiklis, J.N. and B. Van Roy. Regression methods for pricing complex American-style options, IEEE Transactions on Neural Networks 12, pp. 694–703 (2001).