Multivariate Tail Estimation: Conditioning on an extreme event

Abstract

We consider regularly varying random vectors. Our goal is to estimate in a non-parametric way some characteristics related to conditioning on an extreme event, like the tail dependence coefficient. We introduce a quasi-spectral decomposition that allow to improve efficiency of estimators. Asymptotic normality of estimators is based on weak convergence of tail empirical processes. Theoretical results are supported by simulation studies.

1 Introduction

Assume that is a regularly varying random vector with index and is the marginal distribution of . When dealing with extreme observations, we are often interested in estimating

| (1) |

where , is a suitably chosen subset of and is large. For example, can be chosen as , where is small (The value is called in financial applications the Value-at-Risk). Special cases include estimation of the conditional tail distribution

| (2) |

estimation of the conditional tail expectation (expected shortfall)

or extremal dependence measure

where is a vector norm on . The first problem is linked to estimation of the tail dependence coefficient, the second one to modeling of the expected shortfall ([4]), while the last one was introduced and studied in [13].

In specific cases estimators of (1) can be obtained in a parametric or semi-parametric way and rely on a particular model chosen. Alternatively, one can consider nonparametric approaches (see [2, Chapter 9] for related theory and methods, as well as an extensive list of references). Specifically, having an i.i.d. sample , , from , estimation of the conditional tail distribution in (2) can be achieved by

| (3) |

where is a deterministic sequence such that , and are order statistics.

However, in order to provide reliable estimates of the conditional tail distribution one needs an appropriate number of pairs of observations such that the both components exceed the level . This usually requires a very large number of observations. In summary, the estimator (3) may not be particularly useful in practice.

We propose an alternative nonparametric approach to estimating the conditional tail distribution and more generally to estimating the expressions like the one in (1). The idea comes from [1], who considered regularly varying time series and defined a spectral and a tail spectral process. More specifically, in our context of bivariate vectors, regular variation implies that conditionally on converges in distribution (when ) to a random vector , where has a standard Pareto distribution, is concentrated at , while is independent of . Furthermore, is a distributional limit of given that and . The representation of the limiting vector is similar to the standard spectral decomposition (see [2, Section 8.2.3] or [15, Section 6.1.2]), however, in our case the vector does not lie on a unit circle. Hence, we will call the quasi-spectral decomposition.

As a consequence, if we assume for simplicity that all random variables are nonnegative, then the conditional tail distribution can be expressed in terms of as

Thus, the estimator (3) can be replaced with

| (4) |

We will argue below that the estimator (4) is more efficient than the one in (3) (see also [7] in a different context of time series). Of course, if is unknown, it needs to be replaced with its estimator, however, we will provide conditions that guarantee that estimation of does not influence the limiting behaviour of the estimator of the conditional tail distribution. This observation will be also confirmed by simulation studies. Also, we note that the bivariate case can be easily extended to a general multivariate situation, still requiring only one component to be large.

Furthermore, the quasi-spectral decomposition can be useful in approximating the expected shortfall. It turns out that

whenever . Using the above identity we can construct two estimators of the expected shortfall. Asymptotic normality of an estimator that is based on the left-hand side of the above expression requires finiteness of the second moment, while an estimator motivated by the quasi-spectral representation on the right-hand side may have finite variance even when .

In summary, the proposed estimation procedure based on the quasi-spectral representation may lead to improvement in terms of efficiency or in terms of the conditions required to achieve asymptotic normality, as compared to other nonparametric methods.

In order to support our statement, we proceed as follows. In Section 2 we recall the concept of multivariate regular variation (see [15]), followed by the quasi-spectral decomposition (Section 2.2). We link it to the conditional tail distribution (Section 2.3) and the conditional tail expectation (Section 2.4). We note that we present that section in a general framework of -dimensional vectors. In Section 3 we consider weak convergence of tail empirical processes based on deterministic and random levels. The theory is used to construct estimators of (1). Furthermore, some of the results in [13] and [4] can be concluded from ours. The specific cases of the conditional tail distribution and the conditional tail expectation are discussed in Sections 4 and 5, respectively. In the latter section we link our results to the estimation procedure in [4]. In Section 6 we conduct extensive simulation studies that show usefulness of our approach, while in the following one we apply our procedure to estimation of the tail dependence coefficient for some real data. Some technical details of proofs can be found in Section 8. We finish our paper by addressing several technical issues like different marginals and directions of future research.

2 Preliminaries

We start with some notation that will be used throughout the paper. Unless otherwise stated, by we denote a vector . For a vector we write . For and we denote . As usual, for a given distribution , we write .

2.1 Multivariate regular variation

We start with the following definition (see e.g. [15, Theorem 6.1]).

Definition 1.

A vector in is (multivariate) regularly varying if there exists a non zero Radon measure on , called the exponent measure of , such that and a scaling sequence such that the measure converges vaguely on to the measure , i.e.

| (5) |

The limiting measure is homogeneous with some index , that is for any and a relatively compact set . We call the index of regular variation of .

In what follows, we will assume that all components have the same distribution (see also Section 8 for extensions) and are nonnegative (the latter assumption is purely technical and can be easily relaxed). Then

2.2 Quasi-spectral decomposition

We can link vague convergence to weak convergence of conditional probabilities. In particular, for relatively compact sets , in , ,

In this spirit, regular variation implies a quasi-spectral decomposition. In time series context this approach was used in [1].

Proposition 1.

Let be a regularly varying random vector with non-negative regularly varying components with index . Then conditionally on , as

converge in distribution to and , where

-

1.

has the Pareto distribution with index ;

-

2.

, and is independent of .

Proof.

A proof is given in Section 8.1 ∎

Remark 1.

Throughout the paper the quasi spectral-decomposition into and is obtained by conditioning on . We can condition on for any . Note however that for each different we get different vectors (that depend formally on ).

2.3 Representation of conditional tail distribution

We use the quasi-spectral representation to express the conditional tail distribution.

Corollary 2.

Let be a regularly varying random vector with non-negative regularly varying components with index . Then for and we have

| (6) |

Proof.

2.4 Representation of conditional tail expectation

Corollary 3.

Let be a regularly varying random vector with non-negative regularly varying components with index . Assume moreover that for some we have

| (8) |

Then

Proof.

In particular, if then setting again ,

| (9) |

and the limit is strictly positive in case of extremal dependence, that is when the limiting exponent measure in (5) is not concentrated on the axes.

3 Weak convergence of tail empirical process

For clarity of notation we consider the case and a vector is written as . Recall that all random variables are non-negative with the distribution function and regularly varying with the same index . Assume that we have an i.i.d. sample , , from the distribution of . Let . In what follows denotes a scaling sequence, that is the sequence such that and . For , define the tail empirical function

| (10) |

and . If is homogeneous with index then Lemma 7 implies

| (11) |

whenever satisfies the appropriate integrability condition (see (39) below).

Consider the tail empirical process

| (12) |

Also, define to be the process for the function and the set .

The main result of this section is the following weak convergence for the tail empirical function. A proof is given in Section 8.

Theorem 4.

Let . Assume that are i.i.d. regularly varying random vectors with non-negative regularly varying components with index . If moreover

-

1.

and ;

-

2.

The function is homogenous with order ;

-

3.

For we have ;

-

4.

There exists such that ;

then

| (13) |

in , where , are Gaussian processes with the covariance functions

3.1 Tail empirical process with random levels

To apply the weak convergence established in Theorem 4 one needs to choose . The sequence depends on the marginal distribution which is unknown. Hence, we consider the tail empirical process with random levels. We refer the reader to [16] and [10].

The second issue is that the centering in the tail empirical process (12) is not its limit . This will be handled by an appropriate ”no-bias” condition.

To proceed, choose a sequence such that and and define by . Let be order statistics from , . First, from Theorem 4 we conclude the following weak convergence. Let .

Corollary 5.

Assume that the conditions of Theorem 4 are satisfied. Furthermore, assume that the distribution function is continuous and that

| (14) |

uniformly in a neighborhood of 1. Then

We note that the normal convergence of the order statistics is standard (see e.g. [5, Theorem 2.4.1]), but we need to argue that the convergence holds jointly.

Furthermore, we impose the following no-bias condition:

| (15) |

This leads to the following empirical processes

where

| (16) |

and

4 Conditional tail distribution

If we choose and , , then in (10) becomes

| (19) |

Furthermore,

Hence, is the limiting conditional tail distribution and is the tail dependence coefficient. We note that in terms of the quasi-spectral representation the limiting variance is

| (20) |

If we choose and then

| (21) |

In particular, using (7),

Theorem 4 implies that converges to a Gaussian process with the limiting variance

| (22) |

which is smaller than the one given in (20) whenever .

Hence, both tail empirical functions in (19) and (21) can be used to construct estimators of the limiting conditional tail distribution. Specifically, we can use

| (23) |

| (24) |

the latter one when is known. The above discussion indicates that the second estimator can be asymptotically more efficient than the first one.

4.1 Unknown

Let be an estimator of . We redefine from (24) as

| (25) |

We have

We already know (cf. (17)) that

Using the first order Taylor expansion for , we have

Let and be the Hill estimator. We know that converges to a normal random variable. Hence, in order to show that is of a smaller order than it suffices to justify that

is bounded in probability,uniformly in . Assume that for we have

Then recalling that and ,

Hence, is negligible and there is no effect of estimation of .

5 Conditional Tail Expectation

If we choose and then in (10) becomes

| (26) |

We note that the limiting variance can be represented as

| (27) |

If we choose and then

| (28) |

In particular, by (9)

| (29) |

We have furthermore

| (30) | ||||

| (31) |

The integral in (31) is finite whenever . However, the integral in (30) may exists even when (take trivially the situation of or , where , is regularly varying with index and support contained in , , independent of a standard normal random variable .)

The limiting variance can be written as

| (32) |

We note that for the limiting variance in (32) is smaller than the one in (27). Furthermore, the effect of estimating is negligible if we use an estimator of with a faster rate of convergence, as described in Section 4.1.

5.1 Modelling Conditional Tail Expectation

Let be the upper quantile function. For a small we have . Our goal is to estimate

when is small. In case of extremal dependence we have (cf. (9)) whenever ,

| (33) |

where . If we model the tail by a generalized extreme value distribution, then can be estimated using the representation (5.9) in [2], while can be estimated using the tail empirical functions (26) and (28) as follows. We take and and then replace with to obtain

| (34) | |||

| (35) |

Then, can be chosen to be one of the estimators defined in (34)-(35).

Let now be regularly varying. The function is regularly varying as . If is the empirical distribution function associated with and we set , then . Thus, when , we have the following approximation (see [2, p. 119]):

| (36) |

Hence, we can estimate

where is an estimator of .

Equation (34) leads to the following estimators of :

| (37) |

We note that (37) is precisely the estimator used in [4] and our Theorem 6 can be used to conclude their Theorem 1 under slightly different conditions. Indeed, using (36) and noting that we have

| (38) |

We can recognize to be

and its convergence can be concluded from (17), while the bias term in (38) can be handled by imposing a second order condition as in [4].

Now, the case of estimated in . Applying the first order Taylor expansion, we have

so that

If for some and a random variable we have

and , then estimation of yields an additional contribution . This is exactly the situation of Theorem 1 in [4], however note that they did not require that the vector is regularly varying. Nevertheless, their Theorem 1 can be recovered from our results.

6 Implementation. Simulation studies

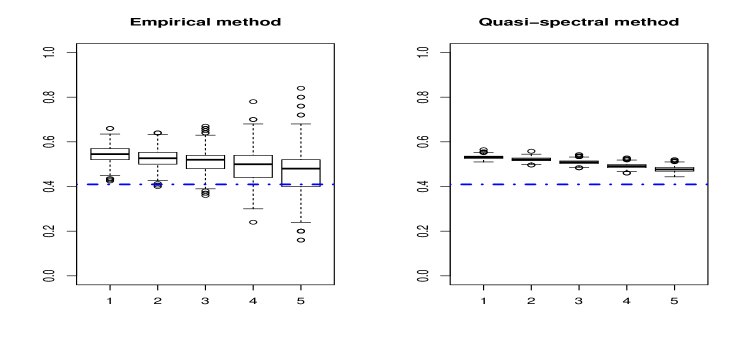

We perform simulation studies to illustrate our theoretical results. We illustrate estimation of the tail dependence coefficient

We use the estimators , , defined in (23), (24), (25). At the first step we plot estimates computed for different numbers of order statistics. Next, we conduct Monte Carlo estimation for particular choices of (5%, 10%, 20%, 30% and 40% of observations). Number of Monte Carlo iterations is chosen to be 1000.

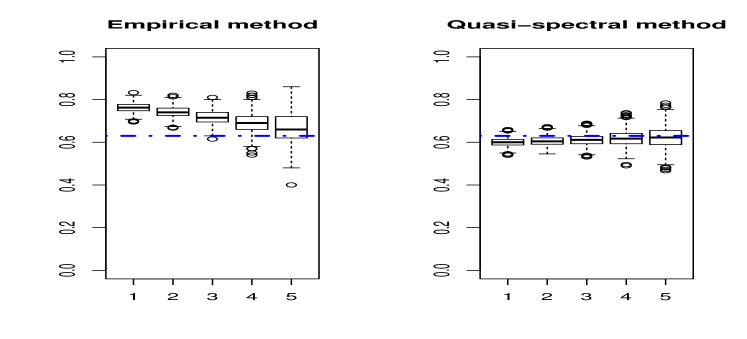

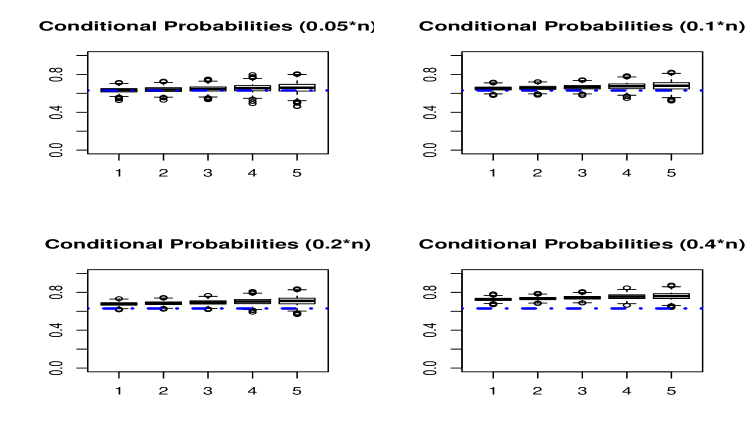

Our simulations indicate that the quasi-spectral method is less variable more robust (in terms of the choice of ) than the standard empirical method, even if the parameter has to be estimated.

6.1 A toy example: simple linear model

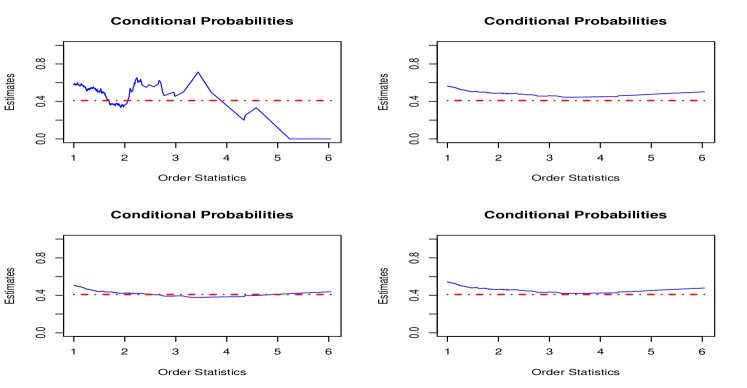

We simulate 1000 observations from the model , where , , is standard Pareto with and is standard normal. In this case the tail dependence coefficient is .

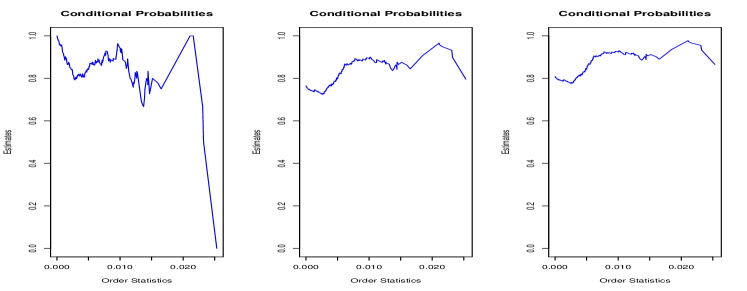

Figure 1 shows shows the estimated values using the three estimators, computed for different values of , where is the number of order statistics being used. On the -axes actual values of order statistics are plotted in the increasing order. Hence, the estimators computed at the left-end of each picture use a large number of order statistics, while at the right-end use few order statistics. This is different as compared to the Hill plot. The first observation (not surprisingly) is that the empirical estimator is very sensitive with respect to the number of order statistics , and is completely useless when plotted against large values of order statistics. The estimators motivated by the quasi-spectral representation are more ”stable”, even if the parameter has to be estimated.

Figures 2 and 3 show Monte Carlo estimates of TDC using , (Figure 2) and (Figure 3), where the estimators are computed based on upper order statistics. The parameter in is estimated using the Hill estimator based on of upper order statistics.

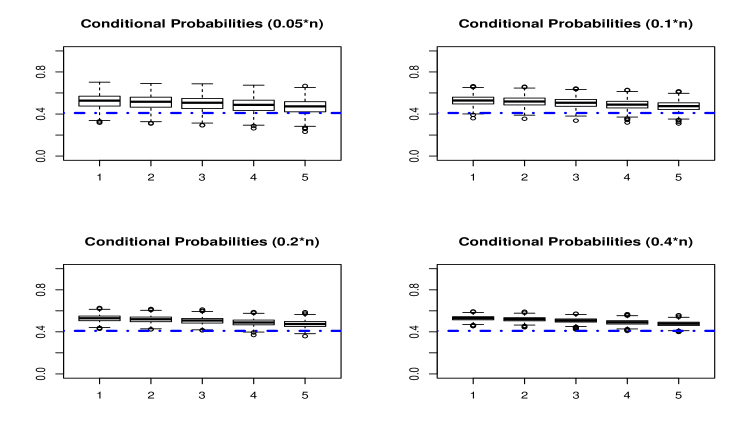

6.2 Bivariate

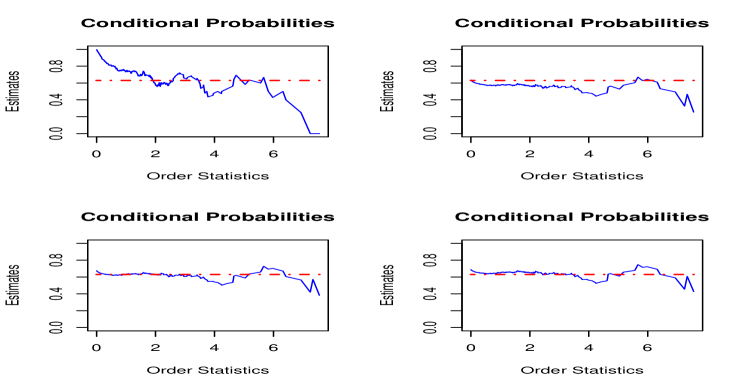

We simulate 1000 observations from the bivariate -distribution, that is , where is chi-square with degrees of freedom and are standard normal with correlation . In this case the tail dependence coefficient is , see [14] .

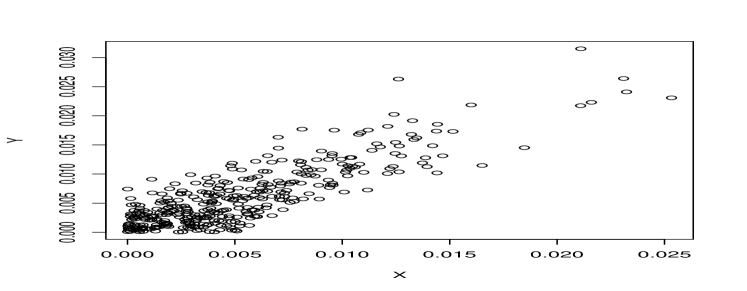

7 Data Analysis

We analyse absolut log-returns of S&P500 and NASDAQ composite indices from January 2, 2013 until June 24, 2014. The scatter plot indicates strong dependence in the upper tail. This is confirmed by the estimation of the tail dependence coefficient. Again, the quasi-spectral method is less variable than the empirical one and robust with respect to the number of the order statistics and estimation of .

8 Technical Details

We state the following lemma without a proof.

Lemma 7.

Let be a regularly varying random vector such that all components are regularly varying with the same index . Let be homogenous with index and assume that for some ,

| (39) |

Then for and a relatively compact set in we have

8.1 Proof of Proposition 1

Proof.

Since is regularly varying we have for ,

If moreover , the left hand side becomes the conditional probability

In other words, conditionally on , converges weakly to a random vector, say . Therefore, for any bounded and continuous we have

Now, let be bounded and continuous. Then

where is also bounded and continuous whenever . Hence,

Hence, conditionally on ,

converges in distribution to . It is obvious that has a standard Pareto distribution. We claim that is independent of . Indeed, for , ,

On the other hand,

Hence, and are independent. ∎

8.2 Proof of Theorem 4

The proof is relatively standard, but we provide it for completeness. We start with the central limit theorem. Multivariate convergence follows by the Cramer-Wald device. We prove the result only for .

Lemma 8.

Under the conditions of Theorem 4, for each , converges in distribution to a centered normal random variable.

Proof.

We prove the central limit theorem by checking Lindeberg’s conditions. Let

so that . Clearly, . Furthermore,

Since as , Lemma 7 implies that the first term dominates and

exists.

Furthermore, noting that for arbitrary and any random variable , we have

and hence

Using Lemma 7 and since , the expression on the right hand side converges to 0. ∎

Lemma 9.

Under the conditions of Theorem 4 the sequence of processes , , is tight in equipped with the Skorokhod topology.

Proof.

In what follow, since the set is fixed, in our notation we omit a dependence on it, unless it is necessary. For , define and

We note that uniformly on . Then

where we write shortly for . We use Theorem 13.5 in [3]. For we have

| (40) |

By noting that for we have , we evaluate

so that

Next, we deal with the second term in (8.2). For we have

Hence, the term is bounded by

The tightness follows. ∎

8.3 Proof of Corollary 5

The argument is similar to that of [16].

-

•

By Theorem 4 and the Skorokhod representation theorem, there exists a probability space, a sequence of processes and processes , with the same distributions as, respectively, , and , such that

(41) almost surely, uniformly on compact subsets of . In what follows, for simplicity of notation we will write , , and .

-

•

Let and be the right continuous inverses of and , respectively. Then, , and, since is continuous, for all , .

- •

- •

-

•

Assumption (14) implies that is continuous and strictly decreasing in a neighborhood of 1. Thus, there exists such that for and

(42) almost surely uniformly with respect to .

-

•

Since and , (42) implies that converges almost surely to 1. Since and converges uniformly to in a neighborhood of 1, this implies that converges almost surely to 1.

-

•

By Taylor’s expansion, there exists such that and

(43) - •

-

•

Since the convergences and (44) hold almost surely, they hold jointly. Coming back to the original probability space, we obtain the joint weak convergence.

8.4 Proof of Theorem 6

Proof.

Denote , where and are the tail empirical functions defined in (10) and (16), respectively. Then, by the homogeneity property (11),

By Corollary 5

| (45) |

jointly with . In particular, converges in probability to 1. Thus, by Theorem 4, the term converges weakly to , while by the delta method the term converges weakly to

This finishes the proof of (17). Furthermore,

Again, by Theorem 4 and , the first term converges weakly to . The second term vanishes by (15). Furthermore, the delta method, the first order Taylor expansion of around 1 and (45) yield that converges to

The convergence (18) is proven. ∎

9 Additional comments and future research

We finish our paper by addressing several technical issues and discussing directions of future research.

- 1.

-

2.

In expense of additional technical considerations one can study tightness with respect to a class of sets , which in particular will imply tightness with respect to in case of the conditional tail distribution.

-

3.

The results are meaningful in case of extremal dependence, that is when the exponent measure is not concentrated on axes. In case of extremal independence, if one wants to estimate quantities like the conditional tail distribution or conditional tail expectation, a different scaling is required. We will address this issue in a following paper, based upon the ideas developed in [9], [8], [11, 12].

-

4.

The quasi-spectral method should be compared with semiparametric or parametric ones. It could be particularly attractive in case of time series where very few parametric models for multivariate extremes are available.

-

5.

We would like to address estimation of conditional tail expectation in a context of multivariate time series, using the tools developed in [6].

-

6.

It is a common practice in extreme value theory to standardize marginals. Assume that we have a positive bivariate vector with marginal distribution functions and . Define

Then and are standard Pareto. All results in the paper remain valid if one assumes that is regularly varying (with index ). If is the quasi-spectral decomposition of , then is standard Pareto, however still contains information about the marginal behaviour. For example, if we start with being regularly varying with and is its quasi-spectral decomposition, then . In other words, by transforming marginals we do not avoid the problem of estimating in (24).

Acknowledgement

Research supported by NSERC grant.

References

- [1] Bojan Basrak and Johan Segers. Regularly varying multivariate time series. Stochastic Process. Appl., 119(4):1055–1080, 2009.

- [2] Jan Beirlant, Yuri Goegebeur, Johann Segers, and Josef Teugels. Statistics for Extremes: Theory and Applications. Wiley, 2004.

- [3] Patrick Billingsley. Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition, 1999.

- [4] Juan-Juan Cai, John J.H.J Einmahl, Laurens de Haan, and Chen Zhou. Estimation of the marginal expected shortfall: the mean when a related variable is extreme. Preprint, 2014.

- [5] Laurens de Haan and Ana Ferreira. Extreme value theory. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2006. An introduction.

- [6] Holger Drees and Holger Rootzén. Limit theorems for empirical processes of cluster functionals. Ann. Statist., 38(4):2145–2186, 2010.

- [7] Holger Drees, Johan Segers, and Michał Warchoł. Statistics for tail processes of markov chains. arxiv:1405.7721, 2014.

- [8] Anne-Laure Fougères and Philippe Soulier. Estimation of conditional laws given an extreme component. Extremes, 15(1):1–34, 2012.

- [9] Janet E. Heffernan and Sidney I. Resnick. Limit laws for random vectors with an extreme component. The Annals of Applied Probability, 17(2):537–571, 2007.

- [10] Rafał Kulik and Philippe Soulier. The tail empirical process for long memory stochastic volatility sequences. Stochastic Processes and their Applications, 121(1):109 – 134, 2011.

- [11] Rafał Kulik and Philippe Soulier. Heavy tailed time series with extremal independence. arxiv:1307.1501v2, 2014.

- [12] Rafał Kulik and Philippe Soulier. Heavy tailed time series with extremal independence: statistical inference. Submitted, 2014.

- [13] Martin Larsson and Sideny I. Resnick. Long range tail dependence: Edm vs. extremogram. preprint, 2009.

- [14] Stefano Demartaand Alexander McNeil. The copula nad related copulas. Unpublished manuscript, 2004.

- [15] Sidney I. Resnick. Heavy-Tail Phenomena. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2007. Probabilistic and statistical modeling.

- [16] Holger Rootzén. Weak convergence of the tail empirical process for dependent sequences. Stoch. Proc. Appl., 119(2):468–490, 2009.

- [17] Ward Whitt. Some useful functions for functional limit theorems. Mathematics of Operations Research, 5(1):67–85, 1980.