Model risk on credit risk

Abstract

This paper develops the Jungle model in a credit portfolio framework. The Jungle model is able to model credit contagion, produce doubly-peaked probability distributions for the total default loss and endogenously generate quasi phase transitions, potentially leading to systemic credit events which happen unexpectedly and without an underlying single cause. We show the Jungle model provides the optimal probability distribution for credit losses, under some reasonable empirical constraints. The Dandelion model, a particular case of the Jungle model, is presented, motivated and exactly solved. The Dandelion model provides an explicit example of doubly-peaked probability distribution for the credit losses. The Diamond model, another instance of the Jungle model, experiences the so called quasi phase transitions; in particular, both the U.S. subprime and the European sovereign crises are shown to be potential examples of quasi phase transitions. We argue the three known sources of default clustering (contagion, macroeconomic risk factors and frailty) can be understood under the unifying framework of contagion. We suggest how the Jungle model is able to explain a series of empirical stylized facts in credit portfolios, hard to reconcile by some standard credit portfolio models. We show the Jungle model can handle inhomogeneous portfolios with state-dependent recovery rates. We look at model risk in a credit risk framework under the Jungle model, especially in relation to systemic risks posed by doubly-peaked distributions and quasi phase transitions.

keywords:

Credit Risk; Model Risk; Banking Crises; Default Clustering; Contagion; Default CorrelationIndex

1. Introduction 1.1. Related literature 2. The data 3. Credit portfolio modelling 4. The Jungle model and credit risk 5. The Jungle model, hands on 5.1. The binomial model 5.2. Small contagion 5.3. The Dandelion model 5.4. The Diamond model 5.5. The Jungle model and the real world 6. The Jungle model and model risk 7. Modelling inhomogeneous portfolios and recovery rates 7.1. Modelling inhomogeneous portfolios, no modelling for recovery rates 7.2. Homogeneous portfolios with state-dependent recovery rates 7.3. Inhomogeneous portfolios with state-dependent recovery rates 8. Contagion, macroeconomic risk factors and frailty 8.1. Macroeconomic risk factors as contagion 8.2. Frailty as contagion 9. Policy implications of contagion 9.1. The U.S. subprime and the European sovereign crises as quasi-phase transitions 9.2. Understanding the historical probability distributions of credit losses 9.3. How should the Jungle model be used in practice? 9.4. It’s the correlations, stupid! 9.5. ”Too Big To Fail” banks 10. Conclusions

1 Introduction

Clustering of corporate defaults is relevant for both macroprudential regulators and banks’ senior management. With a robust modelling of credit losses, macroprudential regulators may analyse and manage the risk of systemic events in the economy, and banks’ senior management may compute the capital needs out of their core credit portfolios.

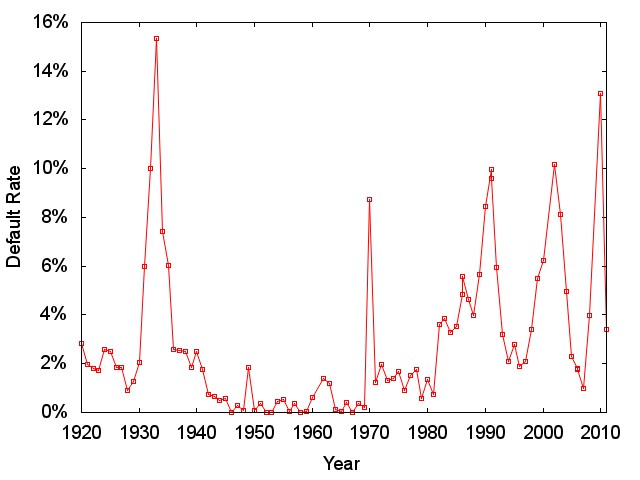

Historical corporate default rate data, as described in (Moody’s Investors Service, 2011) and (Giesecke et al., 2011), signal the sensitivity of credit defaults to systemic events in the economy, from the Great Depression and the 2007-2009 Great Recession, to the savings and loans crisis and the burst of the dotcom bubble, as it can be seen from Figure 1.

Standard credit portfolio models were not able to model the tail risks in credit portfolios when the U.S. subprime and the Spanish Real Estate bubbles bursted. Some of these models introduce default correlations through the dependency of the probabilities of default on macroeconomic factors describing the state of the economy. As a consequence, when the state of the economy is ”good”, the probabilities of default tend to go down. Conversely, when the state of the economy is ”bad”, the probabilities of default tend to go up. Averaging over the business cycle induces default clustering.

However, these predicted default correlations tend to be low in comparison to empirical evidence, and the corresponding probability distribution of the losses shows ”thin tails”. It is widely accepted that in addition to the dependence on macroeconomic risk factors, a reasonable credit risk model should include contagion effects, too.

Contagion effects should often give rise to doubly-peaked probability distributions for the credit losses, with the first peak being close to the peak of an equivalent binomial distribution (when contagion effects are weak, and the defaults can be considered as roughly independent, which is usually the case when the state of the economy is ”good”) and a second peak, at higher losses, corresponding to avalanches / domino effects of credit defaults due to contagion.

This paper has the purpose to show a particular class of credit risk model, the Jungle model 111The name ”Jungle” provides intuition for the complex network of dependencies among the constituents of a credit portfolio. Moreover, since the lion is the King of the Jungle, we will see the Dandelion model (from the French ”dent-de-lion”, or lion’s tooth) is the King of the Jungle of contagion models, since the Dandelion may describe the contagion arising from banks, which are the main source of systemic risks., is able to:

-

1.

Model contagion among borrowers

-

2.

Endogenously generate doubly-peaked probability distributions for the credit losses. As opposed to the case of single-peaked probability distributions, for which higher credit losses are always less likely than lower losses (at the large loss regime), doubly-peaked probability distributions show the distressing phenomenon that very large losses may be more likely to happen than moderately large losses

-

3.

Show how credit systemic events may occur suddenly and unexpectedly. A credit portfolio may inadvertently cross a ”quasi phase transition point”, and its collective behaviour change all of a sudden, potentially creating systemic events. We want to emphasize that intuition usually tells us a systemic crisis requires a strong single cause originating it; however, this is not necessarily true. We will show a systemic crisis can be created without a strong underlying, single cause, and we will learn how to recognize those ”quasi phase transition points”

Section 4 presents the Jungle model and shows the Jungle model is the optimal probability distribution for modelling losses in a general credit portfolio, under two assumptions:

-

1.

The Maximum Entropy principle (to be described in Section 3) is the right guiding principle to select the probability distribution of losses in the framework of credit risk modelling

-

2.

All the empirical information of a given credit portfolio can be summarized as probabilities of default and default correlations of its constituents

In Section 4, we restrict to (close to) homogeneous portfolios, binomial default indicators and no modelling of recovery rates, without loss of generality as discussed in Section 7.

Section 5 tries to motivate the use of the Jungle model. In particular, we show that when there is no empirical information available on default correlations, the Jungle model becomes the binomial distribution (as it should). We also introduce contagion perturbatively around the binomial model, and we show the behaviour of the corresponding interacting system is the one we would expect intuitively.

Section 5 continues with the presentation of a two particular cases of the Jungle model, the Dandelion model and the Diamond model, both of them are interacting models through contagion.

The Dandelion model assumes a central element in the credit portfolio is connected through contagion with the rest of the nodes in the portfolio, and no other pair of nodes is connected. Intuitively, the Dandelion model mimics the relationship between a bank and its many borrowers, or even between a Central Bank with the rest of the economy, see (Bundesbank, 2011).

We show the Dandelion model displays a doubly-peaked loss distribution, endogenously generated through contagion. We also find the results of this model can be interpreted as an endogenously generated two-valued mixture model: the two states of the central node can be understood as the two states of the economy, with the probability of default in the ”bad” state of the economy being higher than the probability of default in the ”good” state of the economy, by an amount given by the variable representing contagion. In a sense, the Dandelion model provides a unifying way to think about both contagion and macroeconomic risk factors.

We argue the Diamond model experiences a quasi phase transition for a not unreasonable set of empirical parameters, showing quantitatively that a small change in the empirical data may result in significant changes for the profile of the probability loss distribution, leading to severe systemic risks. There is a pictorial analogy with the phase transition of water into steam: if we increase one degree Celsius the temperature of water at degrees Celsius, the resulting water at degrees Celsius continues ”being water” (small details will change, for example a thermometer inside the water will show a small increase in its readings, but water will remain ”being water”). However, when the temperature increases a further degree Celsius, there is a sudden change in the collective behaviour of water, becoming steam. In an analogous way, when the default correlation in the Diamond model is increased a bit above the ”quasi phase transition point’s default correlation” (to be calculated from the model), the shape of the probability loss distribution (basically the same for all default correlations below that default correlation) changes to a qualitatively different one (which remains basically the same for all default correlations above that default correlation).

In Section 6, we motivate the use of the Jungle model to study model risk in a credit risk framework, i.e. we show how and when the Jungle model can cope with the inherent uncertainty under systemic credit events, such as the ones presented in the previous section (doubly peaked distributions and quasi phase transitions).

In Section 7, we show the Jungle model can be used to model inhomogeneous portfolios, generalizing straightforwardly the binomial loss indicators in Section 4. Even more, we show the Jungle model can straightforwardly be generalized to cope with state-dependent recovery rates, modelling the stylized fact that recovery rates go down when default rates increase.

In Section 8, we argue the three known sources of default clustering (contagion, macroeconomic risk factors and frailty; see the next subsection, ”Related literature”, for further details) can be understood under the unifying framework of contagion.

In Section 9, we provide a series of policy implications arising from our contagion models. In particular, we show both the U.S. subprime and the European peripheral crises can be understood as particular instances of quasi phase transitions. Also, we are able to understand qualitatively other empirical evidence, such as the thick tails in the historical probability distributions of credit losses presented in Section 2, as well as the surprising fact that quite often, the worst quality credit portfolios end up with default rates lower than the corresponding ones with a better rating. We also pictorially analyse the ”Too Big To Fail” phenomenon under our framework based on contagion, and we compare systemic risks out of contagion for a ”financial economy of big corporates” versus an economy of ”industrial entrepreneurs”.

The final section concludes with a summary of the results.

1.1 Related literature

Recent literature suggest there are three main sources of credit clustering: macroeconomic risk factors, contagion and frailty.

Macroeconomic risk factors, such as S&P 500 returns or short term rates, are common to all credits in the portfolio. When the economy grows strongly, the conditional probabilities of default are low. On the contrary, when the economy weakens, the conditional probabilities of default increase. The passage in time of the business cycle induces in a natural way a correlation among credits. Many standard credit portfolio models can be understood as particular instances of a mixed binomial model, see (Embrechts et al., 2003).

(Azizpour et al., 2014) and (Das et al., 2007) reject the hypothesis that macroeconomic risk factors are able to fully explain the clustering of corporate defaults by themselves, even though (Lando et al., 2010) argues on the contrary.

Contagion can be understood as direct links among credits, such as the ones in a supply chain, or the bank-creditor relationship. A financial crisis may be a prototypical case of contagion, since banks tend to be highly connected with large parts of the economy, and their financial failure may create a deleveraging, impacting directly on the balance sheet of their borrowers. Contagion was analysed with a dynamical approach in (Davis et al., 2001), (Jarrow et al., 2001), (Giesecke et al., 2004), (Schönbucher, 2004), (Lütkebohmert, 2009), (Steinbacher et al., 2013) and in an Ising setting by (Molins et al., 2005), followed by (Kitsukawa et al., 2006) and (Filiz et al., 2012).

Frailty can be described as the ”Enron effect”: once the disputable accounting practices were revealed to the public, the probabilities of default of many other companies, in different sectors and regions, readjusted according to the new information. Most likely, no direct links out of contagion between Enron and those companies ever existed, but default correlations arose nonetheless.

(Azizpour et al., 2014), (Duffie et al., 2009), (Lando et al., 2010) and (Koopman et al., 2011) include frailty, contagion or both in order to try and explain the clustering of corporate defaults, on top of macroeconomic risk factors. (Azizpour et al., 2014) and (Koopman et al., 2011) conclude both frailty and contagion are necessary to fully explain the clustering of corporate defaults in their datasets, on top of the macroeconomic risk factors.

This paper differentiates from the rest of the literature on contagion networks in the credit arena by arguing its results are independent from the specific details of the ”microscopic” credit interactions. In particular, the Maximum Entropy principle argues that given a set of empirical moments of an, in principle, unknown probability distribution, the ”best” probability distribution is the Jungle model. The relevant empirical data in the credit arena is known by market participants to be probabilities of default and default correlations. We show that assuming both the probabilities of default and the default correlations correspond to the empirical moments of the unknown probability distribution of credit losses, the Jungle model arises ”naturally” and without the need to impose the specific knowledge of the credit interactions among the constituents of the considered credit portfolio.

2 The data

We use Moody’s All rated Annual Issuer-Weighted Corporate Default Rates, from 1920 to 2010, see (Moody’s Investors Service, 2011), and (Giesecke et al., 2011) value-weighted default rates on bonds issued by U.S. domestic nonfinancial firms from 1866 to 2008.

As often discussed in the literature and among practitioners, default rate data tends to have issues regarding its interpretation as default losses. This is even more the case for such a long term data set as the ones we use. Our approach is pragmatic: (Moody’s Investors Service, 2011) and (Giesecke et al., 2011) data are no-nonsense, since even though the data definition process is probably not ”rigorous” enough (and it cannot be), the data probably is robust enough (the data contains several full business cycles in both cases).

One of the reasons we use a longer data set than is customary in the literature ((Azizpour et al., 2014) uses data starting on 1970; (Das et al., 2007) on 1979; (Lando et al., 2010), on 1982; (Duffie et al., 2009), on 1979) is that our models do not require the use of macroeconomic or firm-specific data, so we can go backwards as far as we want, while there is still default rate empirical data. On the contrary, for example the S&P 500 was launched on 1957, so a researcher needs a lot of ingenuity to be able to find the corresponding macroeconomic and firm-specific data corresponding to several decades ago.

From (Moody’s Investors Service, 2011), using the default rate for speculative grade bonds, as well as the number of defaults corresponding to speculative grade bonds, we are able to compute approximately the total amount of speculative grade bonds for each year. For the rest of the paper, when we try to model speculative grade bonds, we will use the average number, close to 800.

Unfortunately, the corresponding data for single ratings is not provided in the paper. As a consequence, when we deal with Caa-C ratings, we arbitrarily reduce the number for speculative grade bonds by one order of magnitude, 80.

3 Credit portfolio modelling

A credit portfolio consists of N credit instruments. A credit portfolio model is a theoretical construct providing as an output the unconditional probability distribution for the losses of a given credit portfolio (the unknown we will focus our attention on for the rest of the paper).

Moody’s KMV (Merton, 1974), CreditMetrics (Gupton et al., 1997), CreditRisk+ (CreditSuisse, 1997) and CreditPortfolioView (Wilson, 1997) are commercially available credit portfolio models. Additionally, the Gaussian copula (Li, 2000) became a widespread tool to value credit derivatives. None of these credit portfolio models were able to model tail risks adequately during either the U.S. subprime crisis or the sovereign and banking crisis in peripheral Europe. Especially, some observers believe the Gaussian copula was a ”recipe for disaster”, see (Wired, 2009), (FT, 2009), when modelling credit tail risks.

The losses of a credit portfolio can be calculated as:

| (1) |

where denotes the Exposure at Default, i.e. the maximum potential loss out of the credit instrument (usually, the nominal of the bond or loan), denotes the Loss Given Default (RR stands for Recovery Rate) describing the fraction of the Exposure at Default that is effectively lost when the -th borrower defaults, and is an indicator taking values in , and which describes if the -th borrower is defaulted or not.

In general, real world cases, variables are stochastic, as well as the recovery rates, and the portfolio is inhomogeneous (in general, for at last some ). The modelling for the related probability distribution of losses is challenging.

We will state our credit portfolio model has been solved when we have found the probability distribution for the losses of that portfolio, . Our target for the rest of the paper will be to motivate, calculate and analyse the probability distribution of .

From now on and until Section 7, we will make the simplification of analysing homogeneous portfolios (with Exposure at Default set at 1), and we will not model Recovery Rates (which is analogous to assume the Recovery Rates are constant and the same for all borrowers). In Section 7, we will deal with the general case of inhomogeneous portfolios and state-dependent Recovery Rates. We will show the simplifications described above do not represent a loss of generality. As a consequence, the state space simplifies to a set of discrete variables taking values 0 or 1, . The loss simplifies to .

The probability distribution of a random variable is, in general, unknown and unobservable per se. One possible way to derive it is to aggregate the dynamical, ”microscopic” processes underlying the random variable. For example, modern physics has been successful at stating microscopic dynamical laws from first principles (quantum mechanics and quantum field theory), and finding the related macroscopic equations (thermodynamics) through an averaging process called Statistical Mechanics.

However, in social sciences this process is fraught with difficulties. In general, the underlying dynamical processes are unknown. The usual methodology then is as follows:

The probability distribution of a random variable is not an observable. But there are observables of the random variable which can be understood as direct calculations from using the probability distribution. For example, the expected value of the random variable is the first moment of the corresponding probability distribution. The variance and the correlation correspond to the second moments of the probability distribution. Skewness and kurtosis, which are widely used empirical observables, are the third and fourth moments of the distribution.

A mathematically well behaved probability distribution can be fully described by its moments. In particular, our underlying random variable, the loss in a credit portfolio, is a bound variable, so we are not concerned about the possibility of moments becoming infinite when the tail of an unbound probability distribution is ”fat enough”, see (Bouchaud et al., 2003). As a consequence, it makes sense to assume that despite the probability distribution being not observable, an analyst may finally recover it through the empirical knowledge of its moments (or in general, through the knowledge of the expected value of a general function; the moments are expected values of polynomials).

The question is then: given the knowledge of all or some of its moments, is there a way to find the general form of the probability distribution of the underlying random variables?

The Maximum Entropy principle, or Maxent, provides a specific answer to this question. Maxent asserts:

Given a finite state space , the probability distribution in that maximizes the entropy and satisfies the following constraints, given different functions in , , and fixed numbers :

| (2) |

as well as a normalization condition:

| (3) |

is:

| (4) |

where is called the partition function:

| (5) |

The Lagrange multipliers are found by inverting the following set of equations:

| (6) |

The intuition behind Maxent is is the ”best” 222We leave the ”best” concept undefined probability distribution an analyst can come up with, assuming all the empirical evidence about the problem at hand is summarized as expected values of functions (the numbers and the functions, respectively). The expected values are taken over the (unknown) probability distribution . The claim above is further discussed at Appendix A.

It often happens that while the ”real” probability distribution of a given system is unknown, some constraints are naturally known. For example, in the trivial case of throwing a dice, we know that whatever the correct probability distribution is, the probabilities for each state (each of the six faces of the dice) must add up to one. In fact, Maxent for the dice gives a uniform probability distribution, with a for each of the faces of the dice.

In the same way, if we know, in addition to the fact that all probabilities must add up to one, the expected value of the random variable, Maxent produces the binomial distribution. We will see below that when, in addition to the fact that all probabilities must add up to one, both the expected value of the random variable and its correlations are known, Maxent gives the Jungle model.

Maxent is a general principle which pervades science, see (Jaynes, 2004). As a consequence, we feel comfortable enough by stating that Maxent is a reasonable principle to pick the probability distribution of losses for a credit portfolio, consistent with the available empirical data.

Let us apply Maxent to a given credit portfolio:

Our state space is , a set of discrete variables, , taking 0 or 1 values, and representing the default / non-default state of the -th credit. As a consequence, the potential moments we might derive from the (unknown) probability distribution of losses are:

-

•

The first order moment, . This is the so called probability of default of the -th borrower,

-

•

The second order moment, , for . This is directly related to the so called default correlation between the -th and -th borrower,

(7) -

•

The second order moment, , for . However, since only takes values in , it is true that , so the knowledge of this second moment becomes irrelevant

-

•

In general, any power of , , with being a natural number, becomes

-

•

The third order moment, , for , would correspond to the effect on the creditworthiness of the -th borrower, assuming both the -th and -th borrower also default. This effect is conceivable in theory. However, and as far as we know, there is no serious discussion of this phenomenon in the credit literature.

-

•

Any moment of order higher than three is bound to the same discussion as the one for the third order moment above

There is a general consensus among practitioners that the corresponding available empirical information for a credit portfolio can be summarized as:

-

•

The probability of default of a borrower can generally be estimated, either from CDS for liquid names, or from Internal Ratings models for illiquid bonds or loans. Estimates tend not to be too noisy

-

•

The default correlation between two borrowers is harder to estimate that the corresponding probabilities of default. There are no financial instruments similar to the CDS to imply the default correlation, or if there are, they tend to be illiquid and over-the-counter (opaque information), and providing noisy estimates. Having said that, and despite the practical difficulties for its estimation, the consensus is the default correlation exists, it can at least be measured in some cases, and it is a key variable to understand default clustering

-

•

Third, and higher, order moments bear no specific names in the credit arena

As a consequence, we claim that (at least in our mental framework, which consists of disregarding dynamical, ”from-first-principle” equations, and only considering probability distributions arising from imposing empirical constraints to Maxent) the empirical available information for credit portfolios can be summarized in the probabilities of default and default correlations of its constituents.

Maxent selects the Jungle model as its preferred probability distribution for credit losses, consistent with the available empirical data, as seen in the next section.

4 The Jungle model and credit risk

We consider a credit portfolio of credit instruments, with a space state .

We consider the set ”labeling” the nodes, and the set ”labelling” the pairs of nodes, (the pair and the pair are considered to be the same), and two subsets of those, and .

In consistency with the previous section, we assume the full available empirical information of the corresponding credit portfolio can be summarized as the probabilities of default and the default correlations of its constituents.

We will always consider , or in other words, we assume it is possible to give estimates of the probabilities of default for all the constituents in the portfolio, but will usually be a proper subset of , meaning some of, but not all, the default probabilities can be estimated. The general case will be one in which .

Using the framework of Maxent, we claim that given the following empirical data, consisting of default probabilities and default correlations:

-

•

, with

-

•

, with ; we define such that the relationship holds

Leading to the following empirical constraints:

-

•

,

-

•

Maxent picks the Jungle model among all the probability distributions consistent with those constraints 333In the physics literature, the Jungle model is called the Ising model with external field, with both space dependent external fields and space dependent local interactions:

| (8) |

where

| (9) |

The unknown parameters and have to be found by forcing the probability distribution gives the right estimates for the empirical information at our disposal, i.e. the following constraints are satisfied:

| (10) |

| (11) |

5 The Jungle model, hands on

After showing the Maxent principle picks the Jungle model as the probability distribution of choice to analyse credit risk (assuming the full empirical information of the credit portfolio can be summarized as the probabilities of default and the default correlations of its constituents), we try and motivate the Jungle model, by studying some particular instances of the general model.

To accomplish that goal, this section presents a few particular cases of the general Jungle model: the binomial model, adding small contagion to the binomial model, the Dandelion model and the Diamond model.

As discussed in Section 3, we will state a probabilistic credit model has been solved once its probability distribution has been computed, either analytically or numerically. There are two ways to solve a model:

-

•

, the partition function, has been summed analytically. We will show the explicit calculation of for the Dandelion model below. We will use this methodology for the rest of Section 5.

-

•

If the partition function cannot be summed analytically, Markov Chain Monte Carlo methods may allow to generate realisations of the underlying probability distribution, , without having to know its explicit form. With those realisations, all kind of averages of the distribution can be computed. We will apply this methodology in Section 7, when dealing with inhomogeneous portfolios and state-dependent recovery rates.

In this section, we will show the Jungle model is able to introduce credit contagion in a way the standard credit portfolio models cannot. In particular, the Jungle model will be shown to model credit correlations under ”normal economic conditions” (in a similar way to a Gaussian copula, at least at a non-quantitative level of discourse), but also to endogenously generate quasi-phase transitions, which can be understood as modelling systemic credit crises, arising ”out of nowhere”, a phenomenon that by definition, a Gaussian copula cannot cope with (in other words, a model under a Gaussian copula never suffers from systemic crises).

5.1 The binomial model

For a credit portfolio whose probabilities of default are known and equal to each other, but whose default correlations are unknown, the probability distribution chosen by the Maximum Entropy principle is:

| (12) |

Due to homogeneity, the distribution above becomes the binomial distribution:

| (13) |

with the identification . In other words, for the uncorrelated portfolio, the parameter can be interpreted as (a simple function of) the probability of default. The proof of this result is given in Appendix B.

Since the binomial distribution corresponds to independent defaults, it makes intuitive sense the Maximum Entropy principle selects it when there is no information whatsoever on empirical correlations.

5.2 Small contagion

In the previous subsection, we have seen the Jungle model with and , becomes the binomial distribution. Then, the probability of default of the credit instruments becomes (a simple function of) .

We might ask ourselves which would be the effect on the portfolio of adding the minimum amount possible of (a small to only a pair of nodes, say , and for any other pair of nodes different from ) to the Jungle model corresponding to the binomial distribution (only with ), or in other words, we are interested in expanding perturbatively around the binomial model, in order to single out the effect of , i.e. to see if can be interpreted in relation to the empirical parameters, and , in the same way for the binomial distribution we could interpret as (a simple function of) the underlying .

The corresponding probability distribution for the losses of that portfolio is:

| (14) |

The answer to our question is is proportional to , for small and for a given probability of default, as it can be seen from Appendix C. In other words, when small amounts of contagion are added to an uncorrelated credit portfolio, the default correlation increases (from 0). And the rate of increase is proportional to , so for small contagion, the coefficient can be interpreted as (a simple function of) the default correlation, in the same way that for no contagion, can be interpreted as (a simple function of) the probability of default.

Also, we can see that , by symmetry. But , with the increase being proportional to . Instead, , since the nodes are not affected by contagion.

In other words, when some contagion is added, it is not true any more that is (a simple function of) , since there is a ”mixing” between and and their relationships with respect to and .

We want to emphasize that the model above does not correspond to a credit portfolio whose probabilities of default are known and equal to each other, and the default correlation is only known for the pair of nodes , and for .

As we have seen above, the probabilities of default for the model described by:

| (15) |

are not the same for all nodes: credit instruments with a contagion link, such as , experience an increase in their probabilities of default, with respect to those nodes without a contagion link, such as .

The probability distribution satisfying the empirical conditions such that the probabilities of default are known and equal to each other, and the default correlation is only known for the pair of nodes , and for is:

| (16) |

Where is such that the constraint is satisfied, being different from the required to satisfy the constraint . For this case, it is also true that for small , the default correlation of the pair is proportional to .

In the general Jungle case in which the model contains both and :

| (17) |

it will not be true any more that is (a simple function of) the probability of default, and is (a simple function of) the default correlation: for the general Jungle case, there is a ”mixing” between and and their relationships with respect to and .

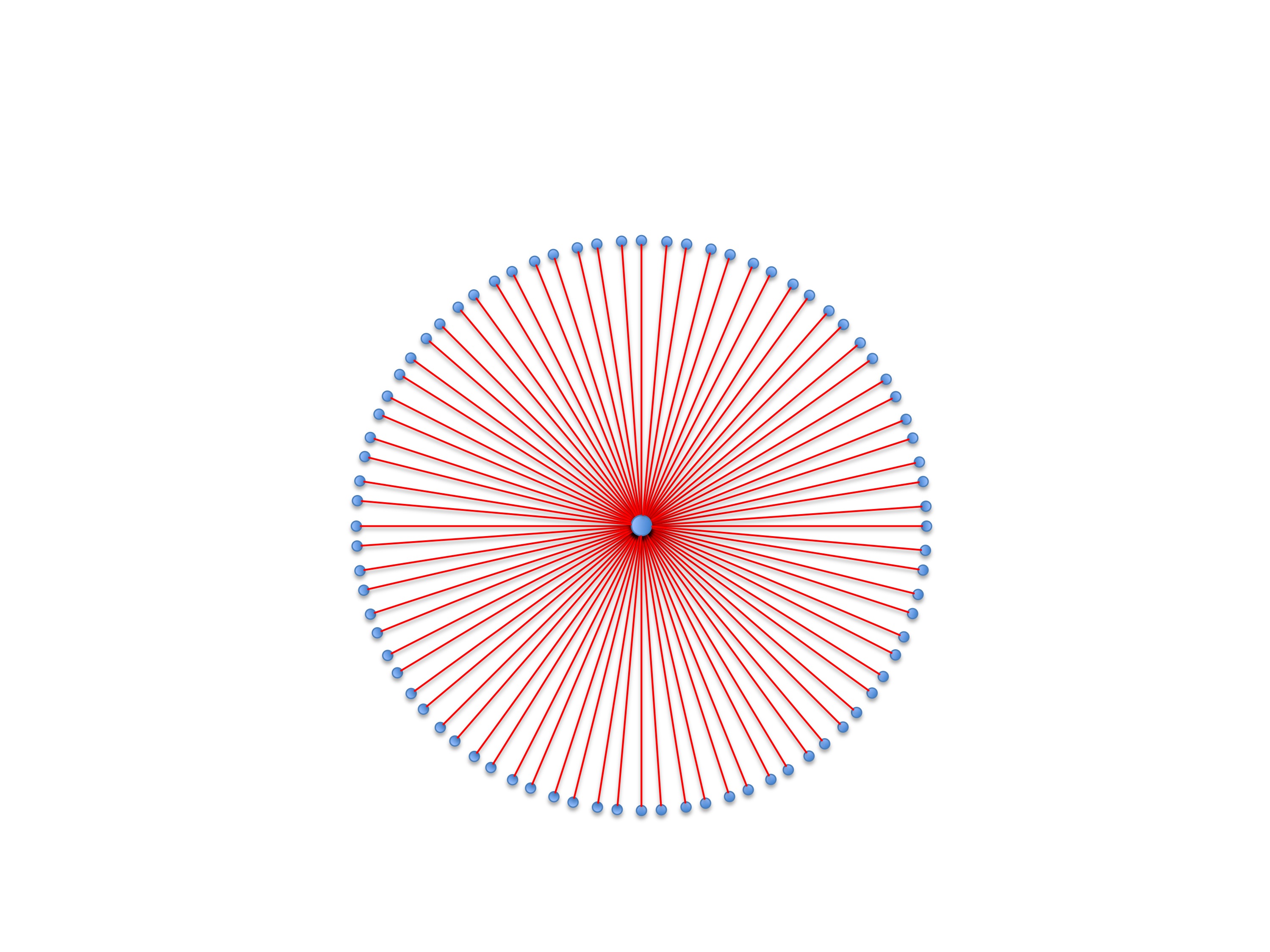

5.3 The Dandelion model

The Dandelion model corresponds to a Jungle model with borrowers, such that the first one, defined as and considered to be at the centre of the Dandelion, is ”connected” to all remaining borrowers, at the external surface of the Dandelion, such that for . Any other borrowers remain unconnected, for . For simplicity, we assume for .

The probability distribution for the Dandelion model is:

| (18) |

The Dandelion model, despite being interacting, can be fully solved, with the probability distribution for its losses given by:

| (19) |

where Z is given by:

| (20) |

and , and are given explicitly as functions of the empirical data, , and :

| (21) | |||

| (22) | |||

| (23) |

where can be derived from the definition of default correlation:

| (24) |

The proof can be found in Appendix D.

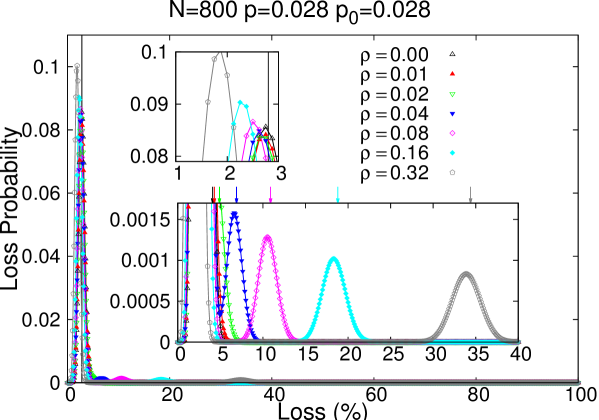

To provide intuition for the Dandelion model, we have calculated its probability distribution for a set of reasonable parameters, and , which correspond to the historical default rate average for global speculative-grade bonds, as per (Moody’s Investors Service, 2011), and for a given range of possible default correlations. The result can be found in Figure 4:

The probability distributions in the chart show a ”double peak” pattern: on one hand, a first peak, centred at low losses and not unlike the corresponding peak for a binomial distribution. On the other hand, a smaller but not insignificant second peak, corresponding to a high level of losses, and consistent with avalanches / domino effects due to contagion.

The higher the default correlation, the higher the extreme losses (the second peak moves further to the right on the chart). Also, the higher the default correlation, the lower losses on the first peak. Contagion works both ways: defaults lead to more defaults (with respect to the binomial case), non-defaults lead to more non-defaults (with respect to the binomial case). These two effects can be seen more specifically from the two insets in the chart.

Also, the higher the correlation of default, the higher the Value at Risk and the Expected Shortfall. The dependency of these two risk measures with respect to the corresponding default correlation is exemplified by the following table (at the confidence level).

| VaR | ES | |

|---|---|---|

| 0.00 | 0.041 | 0.044 |

| 0.01 | 0.043 | 0.046 |

| 0.02 | 0.049 | 0.055 |

| 0.04 | 0.069 | 0.076 |

| 0.08 | 0.109 | 0.117 |

| 0.16 | 0.188 | 0.198 |

| 0.32 | 0.344 | 0.356 |

The Dandelion model can be understood as a bridge between macroeconomic risk factors and contagion. Specifically, in the derivation of the Dandelion model in Appendix D, the following equation arises:

| (25) |

where

| (26) |

corresponds to the relationship between and described for the binomial (non-interacting) case.

As a consequence, the central node in the Dandelion could be interpreted as endogenously generating a ”macroeconomic state of the economy”, whereby for a fraction of time given by the economy remains in a ”good” state of the economy, with a probability of default for its constituents given by , and for a fraction of time given by the economy remains in a ”bad” state of the economy, with a probability of default for its constituents given by , where , and the difference is accounted by the ”contagion factor” .

In other words, the Dandelion model endogenously generates a kind of mixture of binomials, able to generate a doubly peaked distribution and clustering of defaults.

5.4 The Diamond model

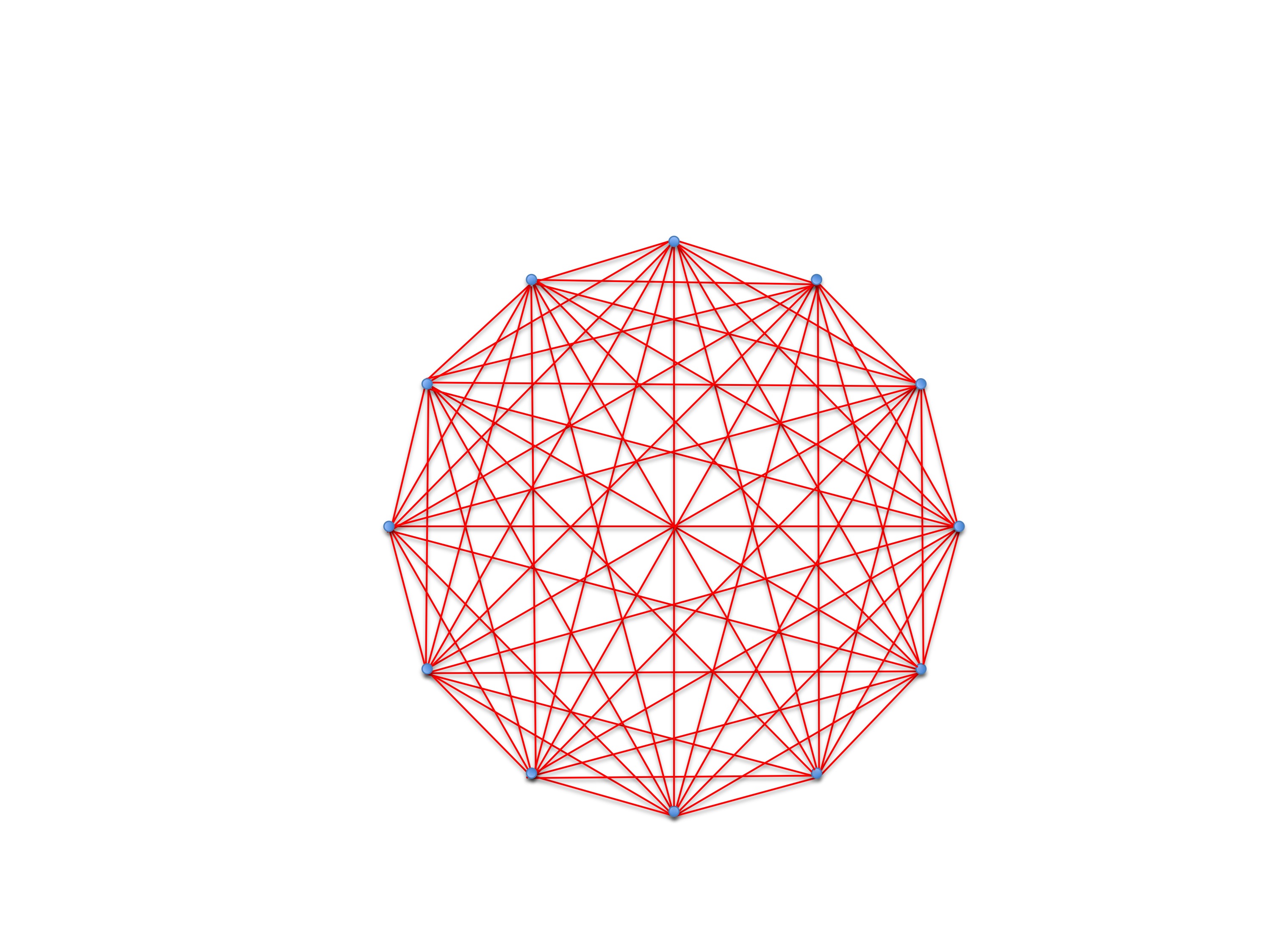

The Diamond model is defined by:

| (27) |

The Diamond model describes a set of credits, all interacting among each other. For example, if , node 1 could be a bank, node 2 a cement producer, node 3 a real estate developer and node 4, a car dealer. The cement producer, the real estate developer and the car dealer get financing from the bank, so there are correlations of defaults between the pairs 12, 13 and 14. Also, the cement producer is a supplier to the real estate developer, so the pair 23 is also correlated. Finally, workers at firms 2 and 3 purchase cars from the car dealer, so a default of 2 or 3 would impact on 4 business, creating also default correlations between 24 and 34.

The partition function for the Diamond model is given by:

| (28) |

And the corresponding probability distribution for the losses will be:

| (29) |

We can relate the empirical data, and to the model parameters and , from the following two equations which can be inverted numerically:

| (30) | |||

| (31) |

Appendix E gives a proof of the previous statements.

The Diamond model clearly exemplifies one of the most interesting phenomena of the Jungle model: quasi phase transitions.

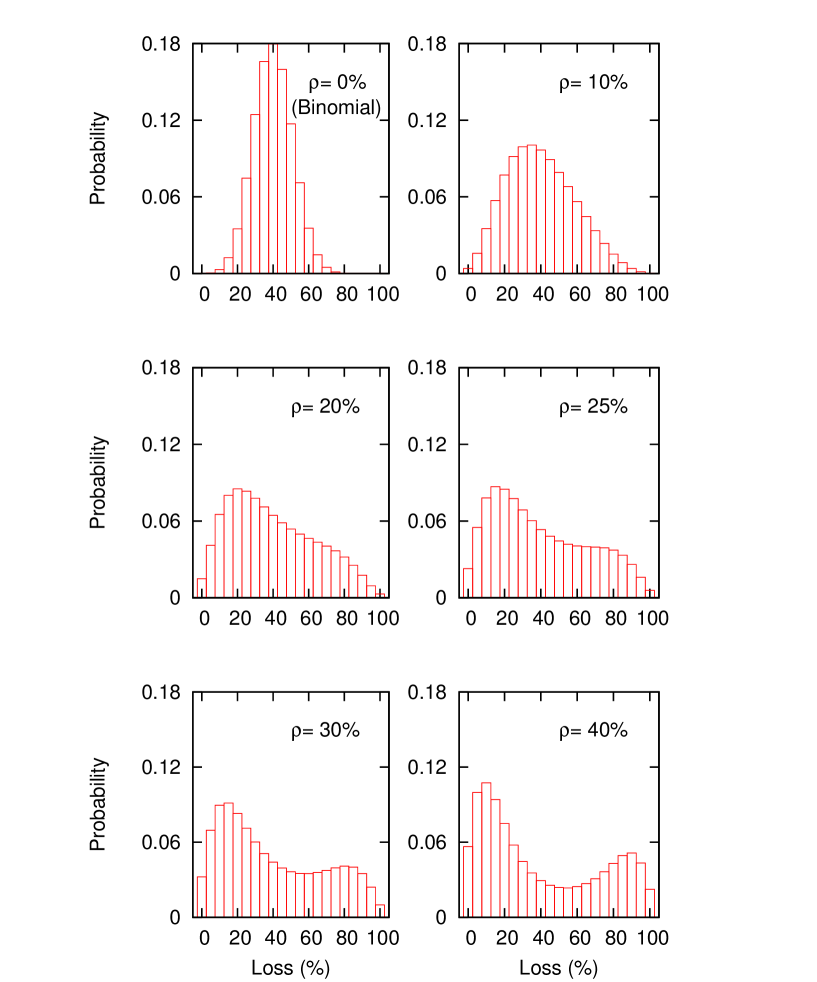

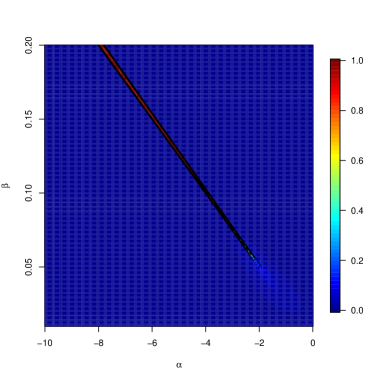

Let us see how the probability distribution of losses for the Diamond model changes, when we smoothly change default correlations, for the probability of default fixed at a given level (with parameters and , for easiness of visual inspection; below, we will provide another example, with and ):

We can see there is a sudden change of collective behaviour for the probability distribution of losses when we smoothly change from 10% to 20% to 30%, at some point between these default correlations:

For default correlations at around 10% or below, the Diamond model presents a standard behaviour with losses spread with a given width around the expected value, 40%. However, when the default correlation increases only slightly (to 25%, say), a different behaviour for the probability distribution of losses starts to emerge: the probability distribution for the losses becomes bimodal, as it can be seen from Figure 5. And the more the default correlation increases, the larger the potential losses out of the second peak on the right.

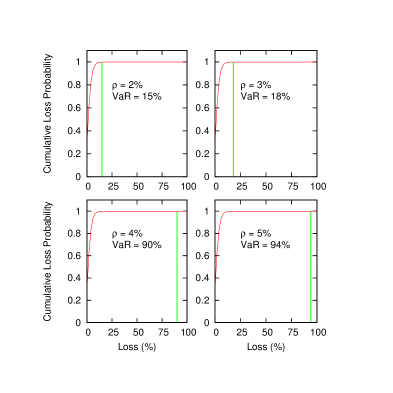

Another numerical example, this time with and , the average default rate for speculative-grade bonds in the (Moody’s Investors Service, 2011) sample, shows how a quasi phase transition changes dramatically the risk profile of the loss probability distribution, given small changes of the empirical values determining the portfolio (probabilities of default and, especially, default correlations):

From Figure 6, we can see a sudden jump for the Value at Risk at the confidence level, given a small increase in the default correlation 111This is the explanation for the use of the ”phase transition” concept, borrowed from Statistical Mechanics. Phase transitions suffer a sudden jump in a given variable, induced by a small change in another, underlying variable. However, a quasi phase transition is not a phase transition, as properly defined in Statistical Mechanics. For example, phase transitions for the Ising model, the equivalent of the Jungle model in Physics, cannot happen for finite , and throughout the paper we assume is always finite..

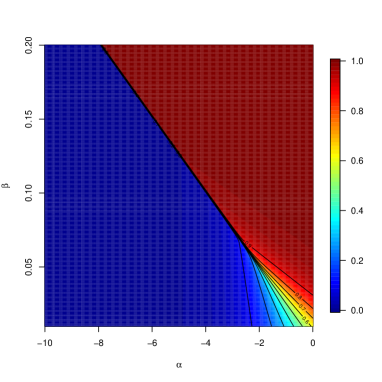

The above phenomenon can also be analysed by looking at how the empirical variables, both the probability of default and the default correlation, change when the model parameters, and , change, as shown in Figure 7.

Despite the fact that for a finite , there can be no (exactly discontinuous) phase transition, from the figures above we can see a sharp, almost discontinuous behaviour throughout a clearly visible diagonal line in the space of model parameters. By analogy, we give the name ”quasi phase transition” to that phenomenon. The existence of such a line, ending in the so called ”critical point”222It is known in the Physics literature the critical point lies at , in the large limit, corresponding approximately to a probability of default of and a default correlation of for ., is well known in the Condensed Matter physics literature.

Since there is a known relationship between the empirical parameters, the probability of default and the default correlation, and the model parameters, and , an analyst can use either the empirical parameters or the model parameters to describe the behaviour of the model. The model parameters tend to be more useful to analyse the behaviour of such systems, because as observed from Figure 7, a small change in the empirical parameters always results in a small change for the model parameters, but the opposite is clearly not true (at the line of quasi phase transitions):

Also, any credit portfolio is driven by underlying, fundamental economic factors (both macroeconomic and microeconomic). As a consequence, we can understand the evolution in time of a credit portfolio described by such a model as the smooth change of the model parameters when the underlying, fundamental economic factors change. Usually, the empirical parameters will be such that the system will move around the bottom left corner of the figure 7 (relatively low probabilities of default and default correlations).

However, when the economic conditions are such that the system is close to (but still below) the line of quasi phase transitions, a small change in the underlying, fundamental economic factors may lead to a small change in the model parameters, such that the system may inadvertently cross the line of quasi phase transitions, resulting in an abrupt, almost discontinuous, change in the empirical parameters.

As a consequence, the Diamond model shows anti-intuitively that the collective behaviour of the portfolio may significantly change due to small changes of the empirical values determining it.

This phenomena is not unlike the phase transition of water into steam: if we increase one degree Celsius the temperature of water at degrees Celsius, the resulting water at degrees Celsius continues ”being water” (small details will change, for example a thermometer inside the water will show a small increase in its readings, but water will remain ”being water”). However, when the temperature increases a further degree Celsius, there is a sudden change in the collective behaviour of water, becoming a coexistence of steam bubbles and liquid.

So, a small change of the underlying parameters leads to a significant change of the behaviour for the whole system. This is surprising, since if we could solve all the dynamical equations of motion for the say particles in a litre of water, it seems unlikely that with that knowledge we could have forecasted such a dramatic change of behaviour. It is the averaging out of ”irrelevant” degrees of freedom, undertaken by statistical mechanics, which allows to keep only the (small set of) parameters which really matter at the level of one litre of water.

Analogously, the Diamond model shows a quasi phase transition from a phase dominated by a ”binomial-like” behaviour, whereby losses spread over a given width, centred around the expected loss, towards a coexistence region, dominated by avalanches due to credit contagion, and determined by a doubly peaked distribution. The transition from one phase to the coexistence region is caused by a smooth change of the empirical parameters defining the portfolio (probabilities of default and default correlations). However, the variation in the global shape of the probability distribution changes significantly the risk profile of the portfolio, potentially inducing systemic risks.

5.5 The Jungle model and the real world

In a general, real world credit portfolio, a Jungle model will be defined by its topology, and , as well as by the given empirical data, consisting of and over and .

The data will always be such that , or in other words, we consider it is possible to give estimates of the probabilities of default to all the constituents in the portfolio, but will usually be a proper subset of , meaning some of, but not all, the default probabilities can be estimated. The general case will be one in which .

Pictorially, the network corresponding to that credit portfolio will be a possibly random combination of links connecting many nodes in the network. But quite often, the analyst will be able to recognize Dandelion shapes (possibly centred at banks or other large corporates) and Diamond shapes, among others. As a consequence, the ability to solve exactly these three interacting models may prove helpful.

6 The Jungle model and model risk

Above, we have shown the Jungle model becomes the binomial model when no information whatsoever about correlations is known. This result is intuitive, since the binomial model describes losses for independent defaults.

In general, when there is correlation among some of the underlying credit instruments, the Jungle model will naturally depart from the binomial model.

Model risk in the framework of credit portfolio modelling is the risk that a given probability distribution for the losses underestimates the tail risks (with respect to empirical evidence).

Pictorially, we could think of a ”functorial” assigning a probability distribution of losses for each theory. For example, the functorial would assign the binomial probability distribution to the ”binomial theory”, and it would assign the Jungle probability distribution to the ”Jungle theory”.

We could try to parametrize the space of potential theories. For example, we could assign parameter to the binomial theory (given that the binomial theory depends on a parameter , directly related to its first moment), we could assign parameter to the Jungle theory (given that the Jungle model depends on parameters and , directly related to its first and second moments) and so on.

It seems clear that restricting to parameter (most standard credit models can be understood as straightforward generalizations of the binomial theory) creates a significant model risk. Empirically, this has been seen during the recent financial crises in the Western world.

An analyst could believe modelling credit risk with theories with parameter , i.e. the Jungle model, would be clearly better than restricting to parameter (since the binomial theory is a particular case of the Jungle model). However, it seems that theories with parameter are only slightly ”larger” than theories with parameter , but the whole space of theories is vastly larger than . We could see ourselves then climbing the ladder, enlarging progressively the space of theories, but always aware that we would suffering from a massive model risk, since the ”real theory” could be one with parameter, whatever could be.

Empirically, probabilities of default can be obtained easily for a wide range of companies. Default correlation data is not as easily available as probabilities of default are, but it is a relevant parameter for practitioners and academics alike. However, expected values of cross-products of three or more , such as , for , are not known. As far as we know, these terms have not been seriously considered in the related literature.

As a consequence, probably the Jungle model is not the most general credit risk model. The ”correct” credit risk model could be one with parameter 444If new empirical data were known in the form of higher order moments, the framework in this paper could cope with that. In fact, in Statistical Physics this kind of extended Jungle models, including trios and higher order interactions, have been studied extensively, and this is unknown to us. Having said that, Maxent picks the Jungle model as its credit risk model of choice, in consistency with the available empirical data (probabilities of default and default correlations).

In other words, the Jungle model is the best we can do with the empirical credit data at our disposal.

Another issue related to model risk is what do we mean by ”available empirical data”: any sample data is bound to intrinsic uncertainty. Not only because of fluctuations over time, but also due to imperfections in how data is presented and collected (there are hundreds of different day count conventions in finance, for example).

And small fluctuations in the empirical data may have a big impact on the selected model. In the presentation so far, we have not discussed how do we select in practice the parameters in the Jungle model, and , to fit with the empirical data and , apart from stating (as per Maxent) that the constraints:

| (32) |

| (33) |

have to be satisfied. In the previous section, we were able to invert analytically the relationship of and with respect to and for the Dandelion model. For the Diamond model, we showed the corresponding equations can be solved numerically.

However, for a general Jungle model, the situation is probably much more precarious. We might have a large amount of bonds and loans, , also probabilities of default, and a large number (much larger than , but much smaller than the maximum possible amount of links, ) of default correlations among the borrowers. And it could perfectly be possible we could not sum the partition function analytically, so we would need to resort to MCMC methods.

In this situation, a ”Jungle inverter” (i.e., a function providing and on and , given a set of empirical values for and on and , see for example (Roudi et al., 2009)) would be noisy. A good ”Jungle inverter” could give the ”correct” and if supplied with the ”correct” and . But as discussed above, it will never be possible to provide the ”correct” empirical data, we will always be using sample data, prone to an unavoidable margin of error.

We suggest the following way of thinking about model risk:

The empirical data and has not to be thought as a point in a -dimensional space, but as a -dimensional cube centred at and , with a certain width, and .

We should then sample randomly a point from that cube, and . The Jungle inverter would give us a set of and . Sampling again from the cube, we would get another set of parameters, and so on.

Due to the large scale of the inversion, it seems reasonable to assume that even for small and , different samples will yield significantly different topologies and and parameters, resulting in potentially large and .

Our position on that issue is as follows: since we have by hypothesis gathered all the possible empirical information on our portfolio (summarized in probabilities of default and default correlations), and since we have argued Maxent picks the Jungle model as the credit risk model of choice in consistency with that data, and since the uncertainty on our empirical information is unavoidable, all those different models are to be considered.

As a consequence, model risk analysis would be adamant to analyse not only ”the” model consistent with our empirical data, but all the models consistent with our empirical data (probably, there are many of them). This is not only a theoretical argument. For example, the Diamond model case shows that for a not too unreasonable set of probability of default and default correlation data, the probability distribution of the losses suffers a dramatic transformation (a quasi phase transition) when changing smoothly the empirical variables, especially the default correlation.

If one of the theories consistent with our empirical data were a theory having a quasi phase transition point in the vicinity of the parameters and consistent with our empirical data and , by disregarding that model we would be inadvertently creating a significant model risk.

This way of thinking is consistent with ”what if” scenario analysis: it does not matter so much precision (i.e., being able to derive the ”correct” and consistent with our empirical data and ), but robustness, i.e., we know that our data gathering process is imperfect and we know our Jungle inverter may not be able to find always the ”right” and consistent with our empirical data and ; for this reason, we consider a set of potential future variations of the empirical parameters (possibly hard coded through ”expert opinion”) and we analyse what would happen in case those scenarios are realized.

Finally, we would like to analyse when our procedure to select the Jungle model as a relevant credit risk model, the Maxent principle under a set of empirical constraints, could fail to be a valid one. In other words, we would like to make ”model risk on model risk”.

The underlying hypothesis in this paper (apart from the conditions on empirical data outlined above) is we can model credit portfolios without the need to resort to the underlying, ”microscopic” dynamical processes.

In particular, this hypothesis is implicit when we apply Maxent to a given credit portfolio, provided the empirical data, consisting of default probabilities and default correlations, can be obtained as follows:

-

•

, with

-

•

, with ; we define such that the relationship holds

Maxent leads to the following empirical constraints:

-

•

,

-

•

The underlying hypothesis is that during the time frame in which and are fixed numbers (i.e., a time period below the typical time frames of change in those empirical variables), the ”microscopic” variables fluctuate fast enough in order to be able to sample the whole space of states, and generate a meaningful value for both and .

If that is not the case, i.e. if the ”microscopic” variables fluctuate slowly, or conversely, the empirical variables and fluctuate fast (in comparison to each other), the Maxent results do not need to hold in practice.

It seems reasonable to assume that under a ”good” state of the economy, the and empirical values will fluctuate smoothly. Also, a credit portfolio with a low degree of default correlations (such that a binomial provides a good approximation for it) will probably ”relax” fast towards its equilibrium configuration. As a consequence, a not-too-correlated portfolio, under ”good” economic conditions, will probably satisfy the implicit conditions in Maxent, so the Jungle model framework will hold.

However, under a ”bad” state of the economy, the and empirical values will probably suffer strong and sudden fluctuations. Also, a credit portfolio with a high level of default correlations might ”relax” slowly towards its equilibrium configuration. For example, it could be the dynamical processes (unknown to us) generate a state space with many local minima, and the system might be trapped in a local minimum which is not the global one, and the more the time passes, the more likely it becomes that eventually the system jumps out of that local minimum towards the another local minimum, searching the global one. In that case, the averages we would measure, and , would not be measurements on the whole probability distribution, but only on a small part of the state space, making the overall effort worthless (or even outright dangerous, for macroprudential purposes).

As a consequence, a highly correlated portfolio, under ”bad” economic conditions, may not be correctly described by Maxent, so the Jungle model framework will not necessarily hold true.

To sum up:

-

•

The Jungle model may not be the ”best” possible credit portfolio model (whatever ”best” means), but at least, the Jungle model is selected by Maxent to be the credit portfolio model of choice, in consistency with the available empirical data.

-

•

Model risk under the Jungle model should be thought of as an ensemble of Jungle models, defined by and , which are consistent with the empirical data and . In particular, and could be large, even for small and . An analyst should study the possibility of the existence of double peaks and quasi phase transitions for the corresponding models, since a small change in the underlying empirical data, i.e. small and , may lead to sudden and dramatic systemic events 555In the same way we could not know water at 99 degrees Celsius was going to become steam when increasing temperature by one more degree..

7 Modelling inhomogeneous portfolios and recovery rates

In Section 3, we have discussed the modelling of credit losses for a general credit portfolio, including not only stochastic bi-valued indicators, but also possibly state-dependent recovery rates, and inhomogeneous exposure at default values.

In Section 4, we have simplified the above general case by only considering stochastic bi-valued indicators.

We now show the general case of Section 3 can be handled with the Jungle probability distributions of Section 4. In other words, the problem of obtaining the general probability distribution for the losses of an inhomogeneous portfolio with state-dependent recovery rates can be decoupled into two smaller problems:

-

•

First, find the Jungle probability distribution for the losses of the corresponding homogeneous portfolio with no recovery rate modelling (using the empirical probabilities of default and default correlations of the borrowers in the portfolio)

-

•

Once the Jungle probability distribution is found, model the general case of the inhomogeneous portfolio with state-dependent recovery rates, by sampling the Jungle probability distribution with Markov Chain Monte Carlo methodology, and calculate trivially the corresponding losses in the general case for each realization of the Jungle probability distribution

Let us show the procedure outlined above for both inhomogeneous portfolios with no recovery rate modelling, and for homogeneous portfolios with state-dependent recovery rates, before handling the general case.

7.1 Modelling inhomogeneous portfolios, no modelling for recovery rates

First, let us consider the intermediate case of a credit portfolio being modelled by stochastic bi-valued indicators and inhomogeneous exposure at default values, but no recovery rates. In that case, the total loss of the portfolio can be described as:

| (34) |

The probability distribution for can be computed numerically, using the equation above, by using the probability distribution arising from the corresponding homogeneous Jungle model.

7.2 Homogeneous portfolios with state-dependent recovery rates

The Jungle model can also handle the case of state-dependent recovery rates for homogeneous portfolios, when the recovery rates follow the stylized fact of being lower when the overall default rate increases (and vice versa), see (Mora, 2012).

For simplicity purposes (and without loss of generality, as shown in the next subsection), let us assume a linear dependence of the recovery rate with the overall default rate, , where is and being the expected value of .

The expected value of is one. However, since the recovery rate decreases when the default rate increases, the total loss will show the non-trivial correlations between the recovery rate and the default rate through an increase in the high loss region (with respect to the case of no state-dependent recovery rate).

7.3 Inhomogeneous portfolios with state-dependent recovery rates

In general, a real world portfolio will be inhomogeneous, and the recovery rates of its constituents will be state-dependent, possibly in a specific way for each borrower.

This general case is amenable to computation with the MCMC methods outlined above, and the generalization is straightforward for:

-

•

Inhomogeneous portfolios

-

•

State-dependent recovery rates such as

-

•

State-dependent recovery rates with a more general functional than , for example with non-linear terms in , or with borrower specific coefficients

-

•

State-dependent recovery rates that depend not only on , but on the states of individual borrowers, , for the -th borrower

-

•

In general, MCMC allows to compute the probability distribution of any function whose domain is the state space,

In particular, we want to highlight another suggestive possibility: , with being the indicator of the central node in a Dandelion model. We have discussed above the Dandelion model introduces a relationship between macroeconomic risk factors and contagion, unifying both of them. In particular, macroeconomic risk factors could be understood as a specific, large Dandelion effect.

As a consequence, a functional form of would mean that in the ”good” state of the economy, with , the loss given default would be ”low” (, say 20%). Instead, in the ”bad” state of the economy, with , the loss given default would be ”high” (, say 70%). Again, such a modelling is amenable to MCMC calculations for the corresponding Jungle model.

8 Contagion, macroeconomic risk factors and frailty

In this section, we point out the three factors contributing to default clustering (macroeconomic risk factors, contagion and frailty) can be understood under the unifying framework of contagion.

In particular, we show macroeconomic risk factors can be modelled as a particular case of contagion, generalizing the ”Dandelion trick”.

Also, we motivate frailty can be interpreted as an instance of contagion: when suddenly a hidden risk factor is revealed to the market, the effect is an abrupt and discontinuous change of the empirical parameters defining the credit portfolio, i.e. its probabilities of default and default correlations. Frailty can be thought of as the effect of this jump on the parameters of the loss probability distribution.

8.1 Macroeconomic risk factors as contagion

Earlier, we have seen the Dandelion model can be understood as a mixture of binomials, whereby the probability of default of a node in the periphery of the Dandelion can be decomposed as a mixture of ”good” and ”bad” probabilities of default, each corresponding to the two binomials in the mixture.

Here, we want to show the ”Dandelion trick” can be generalized for the Jungle case, to generate a mixture not only of binomial distributions, but of any distribution arising from an interacting model:

Given a Jungle model of credit instruments, defined by , and , the corresponding probabilities of default and default correlations of its constituents, we can define a mixture model by:

-

•

For a fraction of time , the probabilities of default of the credit instruments are

-

•

For a fraction of time , the probabilities of default of the credit instruments are

By extending straightforwardly, but rather lengthily, the ”Dandelion trick” for a general Jungle model, we can create mixture models of credit portfolios in a natural way. As a consequence, mixture models arising from the variation over time of macroeconomic risk factors can be embedded naturally into the framework of contagion.

8.2 Frailty as contagion

In this subsection, we want to motivate the use of contagion to explain, at least pictorially, the phenomenon of frailty:

Frailty is described as the ”Enron effect”: when ”Enron” was considered to be a good company, its probability of default was low. However, some day the market discovered ”Enron” had ”cooked its books”. Immediately, ”Enron”’s probability of default sky-rocketed.

But the impact of that discovery did not end there: analysts started wondering if other companies, in other geographic regions and in other economic sectors, probably completely unrelated to ”Enron”, had been cooking their books, too.

As a consequence, once the corresponding ”hidden factor” was ”revealed” to the market, the probabilities of default of many different companies throughout the ”credit network” jumped upwards, in analogy to what happened to ”Enron”’s probability of default. This behaviour is not unlike asthma (pollution may trigger a common response among people suffering asthma; but asthma is not like flu, the prototype of direct contagion).

The net result of the ”Enron effect” was the probabilities of default of a multitude of nodes in the ”credit network” increased suddenly. The reason was not direct contagion, but the revelation of new information to the market which had been hidden so far.

We could argue then that dealing with frailty, in the contagion framework outlined by the Jungle model, is adamant to applying ”what if” scenario analysis to a given configuration of the ”credit network”. By definition, we cannot know what the ”hidden factors” are. However, we know that whatever they are, their effect once they are discovered by the market, is a sudden jump for some of the empirical and .

Frailty can then be understood as the change in the loss probability distribution of a Jungle model, when the empirical and transform into a set of stressed values throughout the network, which can be quantified by the derivative of the model parameters, and , with respect to the empirical parameters, and .

As a consequence, frailty and contagion are intimately related, since the effect of frailty will largely depend on the contagion structure of the credit network.

9 Policy implications of contagion

In Section 5, we have described how the Jungle model depends on the probabilities of default and default correlations of its constituents, plus the topology of the ”contagion network”.

We have seen that for several topologies, with not-too-unreasonable values for the probabilities of default and default correlations, the probability distributions of the credit losses become doubly peaked, out of credit avalanches triggered by contagion.

In particular, we have analysed how increasing the default correlation for the Dandelion model, leads to the second peak moving to more extreme losses (more extreme domino effects), as well as the first peak moving towards zero losses. The inability of some credit portfolio models to accommodate these stylized facts, even for some models used in practice for regulatory purposes such as (Vasicek, 1987), has been highlighted by (Kupiec, 2009).

In the following sections, we will describe the policy implications suggested by the effects above.

9.1 The U.S. subprime and the European sovereign crises as quasi-phase transitions

Both the U.S. subprime and the European sovereign crises caused sharp spikes in probabilities of default ”across the board”. However, such increases were mostly concentrated in specific sectors of the economy (e.g., financial corporates, such as Lehman and AIG, during the U.S. subprime crisis).

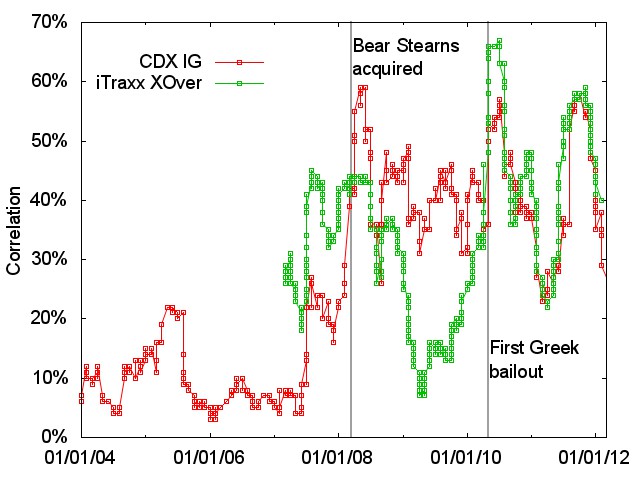

For the following argument, it will be important to highlight that not only the probabilities of default jumped during the financial crises, but also the (average pairwise) default correlations, as it can be seen from Figure 8.

Before the crisis, market expectations implied low probabilities of default and default correlations for the overall economy, in particular the same held true for the financial sector. Also, risk aversion was probably ”low”, and as a consequence, the risk premium associated to the market values of both empirical parameters was also ”low”.

However, when the crisis erupted, both probabilities of default and default correlations spiked up for the financial sector as a whole. Even more, if it were possible to define the sub-sector of the most speculative parts of the financial sector (those companies exposed the most to subprime assets), it seems reasonable to assume the probability of default of such sub-sector reached exceedingly high levels, of the order of magnitude of .

From the analysis of the Diamond model, we have seen quasi phase transitions arise naturally. And the Diamond model, with equally pairwise default correlations, is the corresponding Jungle model associated to a homogeneous portfolio whereby all nodes are connected to each other. And the sub-sector of the most speculative parts of the financial sector constitutes a credit portfolio which probably can be correctly approximated as homogeneous, with each node connected to any other node in the network. In fact, the standard methodology to imply default correlations from traded credit indices, such as CDX IG or iTraxx XOver, assumes all their individual components have the same default correlation with every other name in the index.

Then, for a Diamond model, and under ”normal” (non-crisis) conditions, the fundamental situation of the economy is such that both the probabilities of default and the default correlations are ”low”, resulting in an economy located around the bottom-left corner of Figure 7. However, in a crisis, and for that sub-sector of the economy exposed the most to the key fundamentals of the crisis, the model parameters and may get closer to the ”line of quasi phase transitions”, from below. As we have observed before, the ”critical point” of such line corresponds to a probability of default of and a default correlation of for a reasonable set of parameters.

As a consequence, if for such a sub-sector, the impact of the deterioration in the fundamental situation of the economy implies that the corresponding probabilities of default and default correlations are close (from below) to and , resp., just a little bit of further economic deterioration may result in the model parameters, and , crossing up the ”line of quasi phase transitions” (from the bottom left corner, to the top right corner). Such a small change may be immaterial in the model parameters space, but in the empirical parameters space, the impact is huge: both the probability of default and the default correlation spike up, from low levels (close to ) to high levels (close to ).

The policy implication of the discussion above is then as follows: monitor closely the model parameters, and , of the sectors of the economy most exposed to potential future systemic crises (the financial sector being always one of such sectors), and raise a red flag once and if the model parameters are getting closer to the ”line of quasi phase transitions”, or at least, a reasonable stress test suggests the model parameters might cross such line in case of a sudden macroeconomic / microeconomic shock.

In particular, let us highlight that such a policy would have resulted in a ”red flag” for both the U.S. subprime and the European sovereign crises at the beginning of such crises, and even possibly a bit before their sudden eruption, as it can be seen intuitively from the default correlation figures above.

9.2 Understanding the historical probability distributions of credit losses

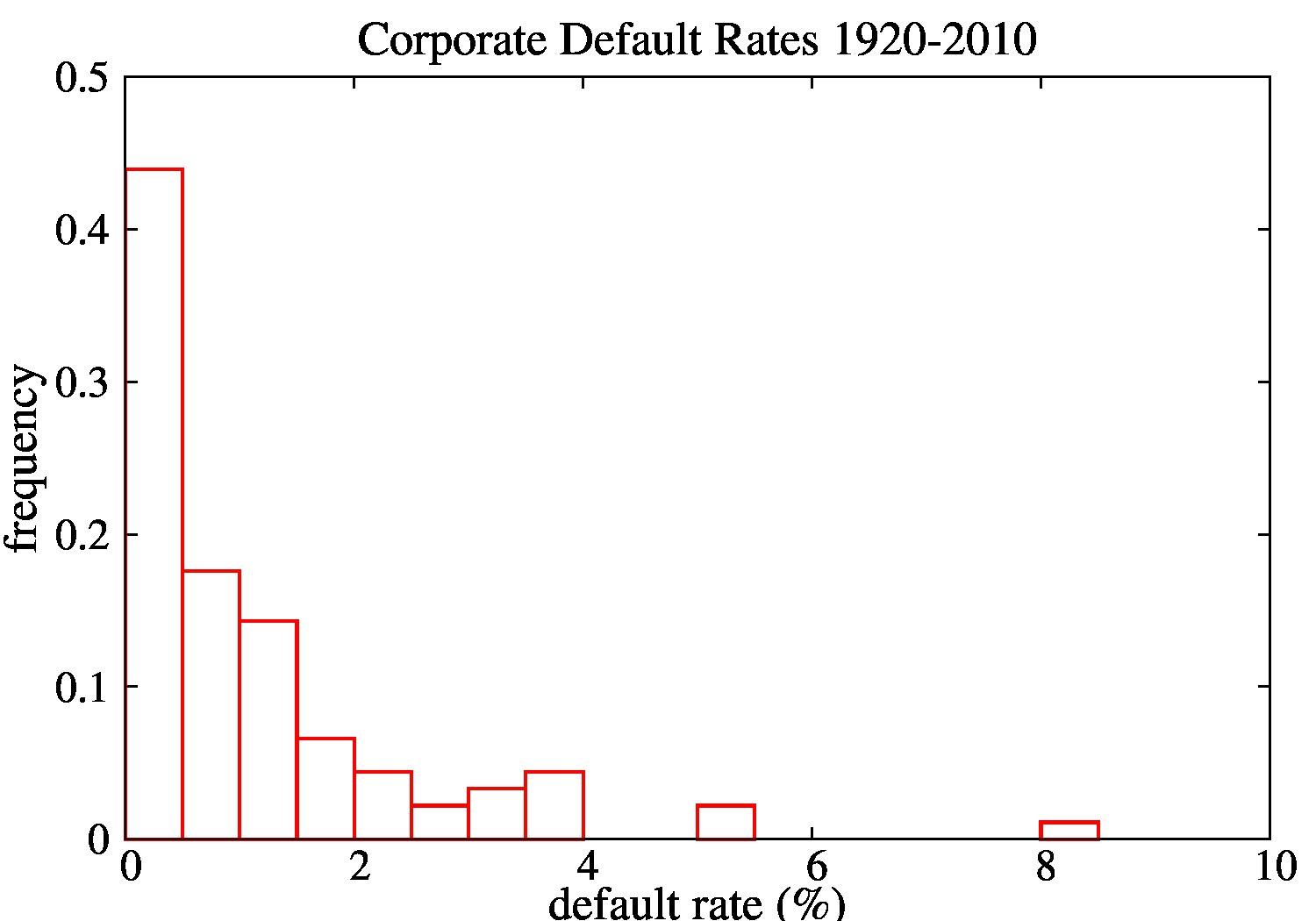

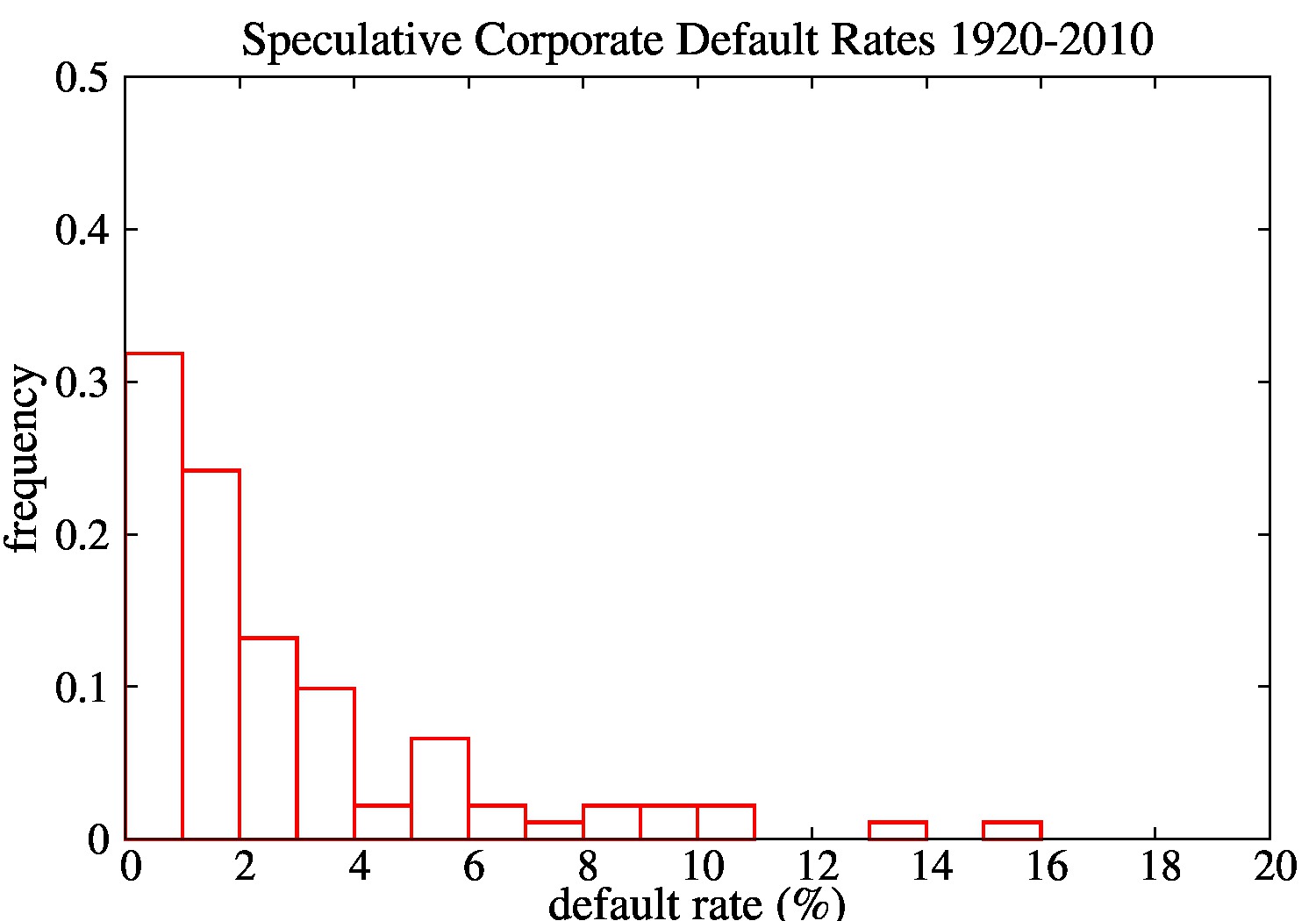

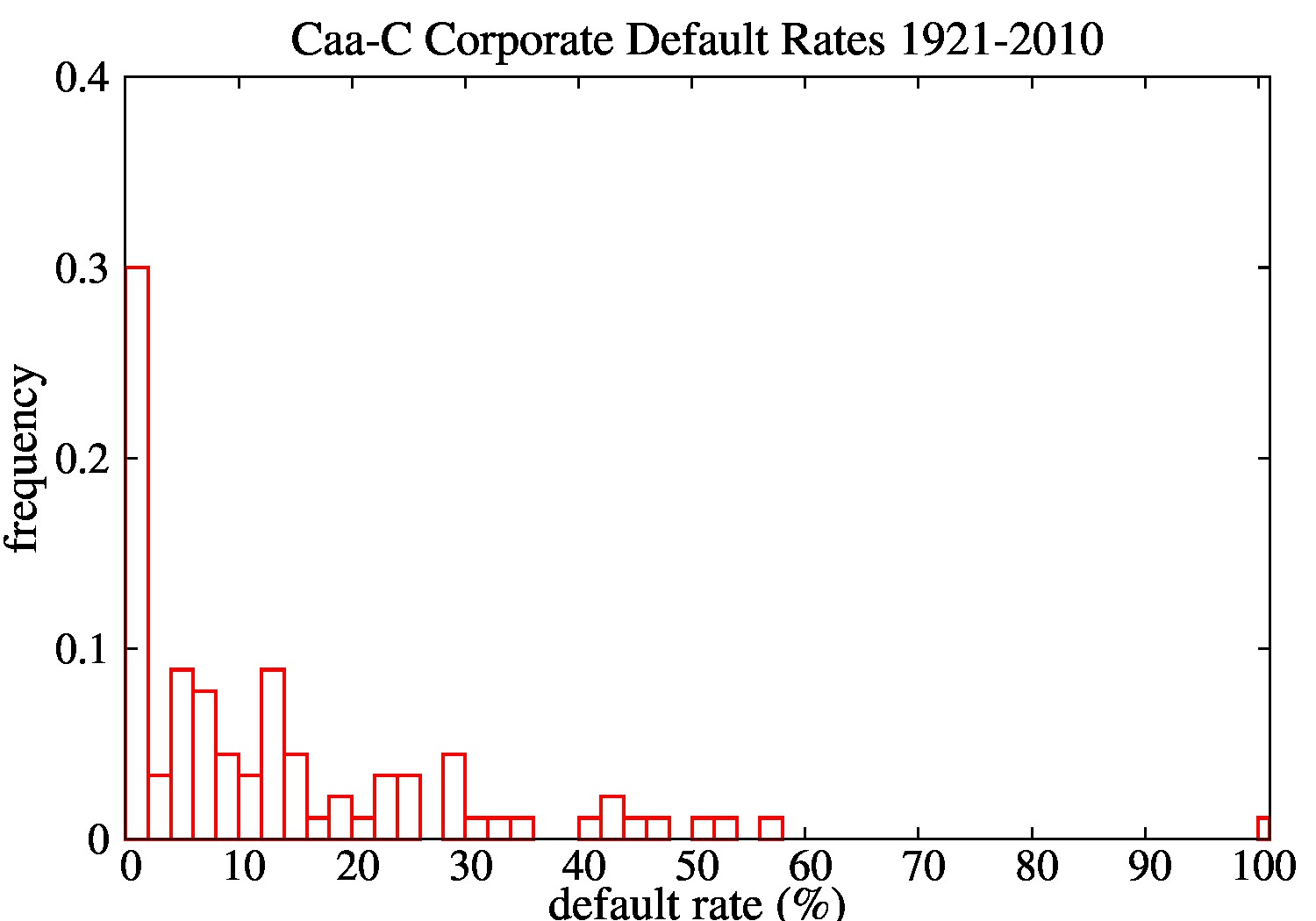

The historical default rates provided by (Moody’s Investors Service, 2011) (also data from (Giesecke et al., 2011) would allow us to reach similar conclusions), presented in Section 2, yield the following histograms:

From visual inspection for the three figures above, there are too few data points to robustly ascertain if the probability distributions for the default rates have one peak or more. Intuitively, it seems the tail is a fat one, with credit loss realizations up to 100%, in the case of Caa-C rating.

The question is then if this evidence contradicts our claim that the fact that Maxent picks the Jungle model as its probability distribution of losses of choice suggests the Jungle model is a reasonable credit risk model to be considered in practice, since the Jungle model is often (for several topologies) doubly peaked, as for example the Dandelion model.

The answer is that it does not. The historical distribution of losses presented above can be understood as follows:

Let us assume, without loss of generality, that the empirical probabilities of default and default correlations only change once per year, on Jan 1st. Let us assume the corresponding topology gives rise to a Jungle model generating doubly-peaked probability distributions. Then, the losses that year will be a realization of that particular Jungle model. Probably, the realization will fall under the first peak. But the more years we repeat the same procedure (with their corresponding probabilities of default, default correlations and topology), the more likely is a realization occurs on the second peak (contagion effects, generating an avalanche / domino effect of credit defaults).

From the Dandelion model, we have found out the position of the second peak is largely determined by the default correlation (the probabilities of default also matter).

As time passes by, we will have a series of realizations of the second peak. But importantly, the empirical data for each realization (probabilities of default, default correlations and topology) will most likely be different for each year, probably generating a double peak at different location on the axis of losses for each realization of the second peak.

As a consequence, the historical probability distribution of losses will probably have only a first peak, consistent with the fact that in the majority of realizations, losses are basically contagion-less, so that first peak will be roughly similar to the one of a binomial model, but wider due to the mixing with different macroeconomic conditions over several business cycles, and a fat tail generated by realizations of the doubly-peaked probability distributions arising from the Jungle model.

This way of thinking allows us to understand how is it possible the tail of the empirical probability distributions is so ”thick”: the tail is generated through individual realizations of double peaks. This way of thinking relaxes the need to include extreme probability distributions which are able to cope by themselves with the difficult task to model both extreme default events, and default events in a ”good” economy state.

Even more, the Jungle model allows us to understand a stylized fact of the probability distribution of losses for highly risky portfolios, exemplified by Moody’s Caa-C rating data: despite the fact Caa-C rating bonds are highly risky (and there is even one year where 100% of bonds in the sample defaulted), it also happens very often that Caa-C rating bonds enjoy a default rate close to 0% (on the sample, there are several years with 0% default rate). In fact, this phenomenon of 0% default rate happens more often for Caa-C than for bonds with a much better rating, which seems intuitively odd, see (Kupiec, 2009).

However, the Dandelion model is able to explain this stylized fact: for Caa-C rating bonds, it seems likely that the individual bonds are described not only by high probabilities of default, but also by high default correlations among themselves (or with a central node, in a similar way to the Dandelion model; possibly banks or other financial suppliers specialized on risky lending).

From the charts in the Dandelion model section, we can see that in this region of parameters, the higher the default correlation, the larger the losses for the double peak. But in addition to this effect, also the higher the default correlation, the lower the losses for the first peak. This is consistent with a contagion effect: contagion not only works on ”bad” situations (a default in a node induces a default in another node nearby), but also on ”good” situations (a non-default in a node induces a non-default in another node nearby).

As a consequence, this framework of thinking leads us to suggest that the most relevant variable to ascertain default clustering is not the probability of default (as standard rating classifications appear implicitly to suggest) but default correlations.

9.3 How should the Jungle model be used in practice?

The Jungle model could be extended straightforwardly to introduce macroeconomic risk factors. The Jungle model is based under the assumption that the probabilities of default and default correlations are known fixed numbers. An analyst could include into the modelling a specific pattern of conditional default probabilities (and possibly conditional default correlations as well), in the same way mixture models introduce default correlations by mixing the binomial model (independent defaults) with a specific choice of conditional default probabilities.

However, the interest to do so is limited. On one hand, the Jungle model does not need to follow the above procedure to include default correlations, since default correlations appear endogenously in the model. This is unlike the case for the binomial model, which needs a mixture in order to be able to model default clustering. On the other hand, averaging over a conditional default probability means the corresponding probability distribution of losses is the one for the whole business cycle.