Continuous-time Random Walks for the Numerical Solution of Stochastic Differential Equations

Abstract.

This paper introduces time-continuous numerical schemes to simulate stochastic differential equations (SDEs) arising in mathematical finance, population dynamics, chemical kinetics, epidemiology, biophysics, and polymeric fluids. These schemes are obtained by spatially discretizing the Kolmogorov equation associated with the SDE in such a way that the resulting semi-discrete equation generates a Markov jump process that can be realized exactly using a Monte Carlo method. In this construction the spatial increment of the approximation can be bounded uniformly in space, which guarantees that the schemes are numerically stable for both finite and long time simulation of SDEs. By directly analyzing the generator of the approximation, we prove that the approximation has a sharp stochastic Lyapunov function when applied to an SDE with a drift field that is locally Lipschitz continuous and weakly dissipative. We use this stochastic Lyapunov function to extend a local semimartingale representation of the approximation. This extension permits to analyze the complexity of the approximation. Using the theory of semigroups of linear operators on Banach spaces, we show that the approximation is (weakly) accurate in representing finite and infinite-time statistics, with an order of accuracy identical to that of its generator. The proofs are carried out in the context of both fixed and variable spatial step sizes. Theoretical and numerical studies confirm these statements, and provide evidence that these schemes have several advantages over standard methods based on time-discretization. In particular, they are accurate, eliminate nonphysical moves in simulating SDEs with boundaries (or confined domains), prevent exploding trajectories from occurring when simulating stiff SDEs, and solve first exit problems without time-interpolation errors.

Key words and phrases:

stochastic differential equations; non-self-adjoint diffusions; parabolic partial differential equation; finite difference methods; upwind approximations; Kolmogorov equation; Fokker-Planck equation; invariant measure; Markov semigroups; Markov jump process; stochastic Lyapunov function; stochastic simulation algorithm; geometric ergodicity2010 Mathematics Subject Classification:

Primary 65C30; Secondary, 60J25, 60J75Chapter 1 Introduction

1.1. Motivation

Stochastic differential equations (SDEs) are commonly used to model the effects of random fluctuations in applications such as molecular dynamics [124, 16, 3, 34], molecular motors [6], microfluidics [83, 129], atmosphere/ocean sciences [95], epidemiology [98, 122], population dynamics [2, 15], and mathematical finance [66, 112]. In most of these applications, the SDEs cannot be solved analytically and numerical methods are used to approximate their solutions. By and large the development of such methods has paralleled what has been done in the context of ordinary differential equations (ODEs) and this work has led to popular schemes such as Euler-Maruyama, Milstein’s, etc [72, 133, 107]. While the design and analysis of these schemes differ for ODEs and SDEs due to peculiarities of stochastic calculus, the strategy is the same in both cases and relies on discretizing in time the solution of the ODE or the SDE. For ODEs, this is natural: their solution is unique and smooth, and it makes sense to interpolate their path at a given order of accuracy between snapshots taken at discrete times. This objective is what ODE integrators are designed for. The situation is somewhat different for SDEs, however. While their solutions (in a pathwise sense) may seem like an ODE solution when the Wiener process driving them is given in advance, these solutions are continuous but not differentiable in general, and an ensemble of trajectories originates from any initial point once one considers different realizations of the Wiener process.

The simulation of SDEs rather than ODEs presents additional challenges for standard integration schemes based on time-discretization. One is related to the long time stability of schemes, and their capability to capture the invariant distribution of the SDE when it exists. Such questions are usually not addressed in the context of ODEs: indeed, except in the simplest cases, it is extremely difficult to make precise statements about the long time behavior of their solutions since this typically involves addressing very hard questions from dynamical systems theory. The situation is different with SDEs: it is typically simpler to prove their ergodicity with respect to some invariant distribution, and one of the goals of the integrator is often to sample this distribution when it is not available in closed analytical form. This aim, however, is one that is difficult to achieve with standard integrators, because they typically fail to be ergodic even if the underlying SDE is. Indeed the numerical drift in standard schemes can become destabilizing if the drift field is only locally Lipschitz continuous, which is often the case in applications. These destabilizing effects typically also affect the accuracy of the scheme on finite time intervals, making the problem even more severe. Another important difference between SDEs and ODEs is that the solutions of the former can be confined to a certain region of their state space, and it is sometimes necessary to impose boundary conditions at the edge of this domain. Imposing these boundary conditions, or even guaranteeing that the numerical solution of the scheme remains in the correct domain, is typically difficult with standard integration schemes.

In view of these difficulties, it is natural to ask whether one can take a different viewpoint to simulating SDEs, and adopt an approach that is more tailored to the probabilistic structure of their solution to design stable and (weakly) accurate schemes for their simulation that are both provably ergodic when the underlying SDE is and faithful to the geometry of their domain of integration. The aim of this paper is to propose one such novel strategy. The basic idea is to discretize their solution in space rather than in time via discretization of their infinitesimal generator. Numerous approximations of this second-order partial differential operator are permissible including finite difference or finite volume discretizations [31, 142, 103, 104, 85]. As long as this discretization satisfies a realizability condition, namely that the discretized operator be the generator of a Markov jump process on a discrete state space, it defines a process which can be exactly simulated using the Stochastic Simulation Algorithm (SSA) [37, 31, 142, 85]. Note that this construction alleviates the curse of dimensionality that limits numerical PDE approaches to low dimensional systems while at the same time permitting to borrow design and analysis tools that have been developed in the numerical PDE context. The new method gets around the issues of standard integrators by permitting the displacement of the approximation to be bounded uniformly and adaptively in space. This feature leads to simple schemes that can provably sample the stationary distribution of general SDEs, and that remain in the domain of definition of the SDE, by construction. In the next section, we describe the main results of the paper and discuss in detail the applications where these SDE problems arise.

1.2. Main Results

If the state space of the approximating Markov jump process, or approximation for short, is finite-dimensional, then a large collection of analysis tools can be transported from the theory of numerical PDE methods to assess the stability and accuracy of the approximation. However, if the state space is not finite-dimensional, then the theoretical framework presented in this paper and described below can be used instead. It is important to underscore that the Monte Carlo method we use to realize this approximation is local in character, and hence, our approach applies to SDE problems which are unreachable by standard methods for numerically solving PDEs. In fact, the approximation does not have to be tailored to a grid. Leveraging this flexibility, in this paper we derive realizable discretizations for SDE problems with general domains using simple finite difference methods such as upwinded and central difference schemes [131, 86, 42], though we stress that other types of discretizations that satisfy the realizablility condition also fit our framework.

Since an outcome of this construction is the generator of the approximation, the proposed methods have a transparent probabilistic structure that make them straightforward to analyze using probabilistic tools. We carry out this analysis in the context of an SDE with unbounded coefficients and an unbounded domain. Our structural assumptions permit the drift field of the SDE to be locally Lipschitz continuous, but require the drift field to satisfy weak dissipativity and polynomial growth conditions. Our definition of stability is that the approximation has a stochastic Lyapunov function whenever the underlying SDE has one. This definition is natural when one deals with SDEs with locally Lipschitz drift fields. Indeed, global existence and uniqueness theorems for such SDEs typically rely on the existence of a stochastic Lyapunov function [67, 97].

In this context, here are the main results of the paper regarding realizable discretizations with gridded state spaces. We emphasize that we do not assume that the set of all grid points is finite.

-

(1)

We use Harris Theorem to prove that the approximation is geometrically ergodic with respect to an invariant probability measure [106, 53, 46]. To invoke Harris theorem, we prove that the approximation preserves a sharp stochastic Lyapunov function from the true dynamics. Sharp, here, means that this stochastic Lyapunov function dominates the exponential of the magnitude of the drift field, and can therefore be used to prove that a large class of observables (including all moments of the approximation) are integrable.

-

(2)

In addition to playing an important role in proving existence of an invariant probability measure and geometric ergodicity, this stochastic Lyapunov function also helps solve a martingale problem associated to the approximation [75, 116, 32]. This solution justifies a global semimartingale representation of the approximation, and implies that Dynkins formula holds for the conditional expectation of observables that satisfy a mild growth condition. We apply this semimartingale representation to analyze the complexity of the approximation. Specifically, we obtain an estimate for the average number of computational steps on a finite-time interval in terms of the spatial step size parameter.

-

(3)

We use a variation of constants formula to quantify the global error of the approximation [111]. This formula is a continuous-time analog of the Talay-Tubaro expansion of the global error of a discrete-time SDE method [135]. An analysis of this formula reveals that the order of accuracy of the approximation in representing finite-time conditional expectations and equilibrium expectations is given by the order of accuracy of its generator. Geometric ergodicity and finite-time accuracy imply that the approximation can accurately represent long-time dynamics, such as equilibrium correlation functions [14].

This paper also expands on these results by considering space-discrete generators that use variable spatial step sizes, and whose state space may not be confined to a grid. In these cases, we embed the ‘gridless’ state space of the approximation into , and the main issues are:

-

•

the semigroup of the approximation may not be irreducible with respect to the standard topology on ; and

- •

To deal with this lack of irreducibility and regularity, we use a weight function to mollify the spatial discretization so that the resulting generator is a bounded linear operator. This mollification needs to be done carefully in order for the approximation to preserve a sharp stochastic Lyapunov function from the true dynamics. In short, if the effect of the mollification is too strong, then the approximation does not have a sharp stochastic Lyapunov function; however, if the mollification is too weak, then the operator associated to the approximation is unbounded.

The semigroup associated to this mollified generator is Feller, but not strongly Feller, because the driving noise is still discrete and does not have a regularizing effect. However, since the process is Feller and has a stochastic Lyapunov function, we are able to invoke the Krylov-Bogolyubov Theorem to obtain existence of an invariant probability measure for the approximation [113]. This existence of an invariant probability measure is sufficient to prove accuracy of the approximation with respect to equilibrium expectations. To summarize, here are the main results of the paper regarding realizable discretizations with gridless state spaces.

-

(1)

The approximation is stable in the sense that it has a sharp stochastic Lyapunov function, and accurate in the sense that the global error of the approximation is identical to the accuracy of its generator. The proof of both of these properties entails analyzing the action of the generator on certain test functions, which is straightforward to do.

-

(2)

A semimartingale representation for suitable observables of the approximation is proven to hold globally. This representation implies Dynkins formula holds for this class of observables.

-

(3)

The approximation has an invariant probability measure, which may not be unique. This existence is sufficient to prove that equilibrium expectations of the SDE solution are accurately represented by the approximation.

To be clear, the paper does not prove or disprove uniqueness of an invariant probability measure of the approximation on a gridless state space. One way to resolve this open question is to show that the semigroup associated to the approximation is asymptotically strong Feller [44].

Besides these theoretical results, below we also apply the new approach to a variety of examples to show that the new approach is not only practical, but also permits to alleviate several issues that commonly arise in applications and impede existing schemes.

-

(1)

Stiffness problems. Stiffness in SDEs can cause the numerical trajectory to artificially “explode.” For a precise statement and proof of this divergence in the context of forward Euler applied to a general SDE see [59]. This numerical instability is a well-known issue with explicit discretizations of nonlinear SDEs [134, 53, 108, 52, 60], and it is especially acute if the SDE is stiff e.g. due to coefficients with limited regularity, which is typically the case in applications. Intuitively speaking, this instability is due to explicit integrators being only conditionally stable, i.e. for any fixed time-step they are numerically stable if and only if the numerical solution remains within a sufficiently large compact set. Since noise can drive the numerical solution outside of this compact set, exploding trajectories occur almost surely. The proposed approximation can be constructed to be unconditionally stable, since its spatial step size can be bounded uniformly in space. As a result, the mean time lag between successive jumps adapts to the stiffness of the drift coefficients.

-

(2)

Long-time issues. SDEs are often used to sample their stationary distribution, which is generically not known, meaning there is no explicit formula for its associated density even up to a normalization constant. Examples include polymer dynamics in extensional, shear, and mixed planar flows [84, 58, 57, 62, 125, 126]; polymers in confined flows [19, 63, 64, 65, 143, 144, 50, 49, 48, 51, 41, 24, 146]; polymer conformational transitions in electrophoretic flows [68, 115, 69, 136, 54, 55]; polymer translocation through a nanopore [91, 88, 101, 56, 4]; and molecular systems with multiple heat baths at different temperatures [30, 29, 117, 99, 45, 87, 1] as in temperature accelerated molecular dynamics [99, 139, 1]. Unknown stationary distributions also arise in a variety of diffusions with nongradient drift fields like those used in atmosphere/ocean dynamics or epidemiology. The stationary distribution in these situations is implicitly defined as the steady-state solution to a PDE, which cannot be solved in practice. Long-time simulations are therefore needed to sample from the stationary distribution of these SDEs to compute quantities such as the equilibrium concentration of a species in population dynamics or, the polymer contribution to the stress tensor or equilibrium radius of gyration in Brownian dynamics. This however requires to use numerical schemes that are ergodic when the underlying SDEs they approximate are, which is by no means guaranteed. We show that the proposed approximation is long-time stable as a consequence of preserving a stochastic Lyapunov function from the true dynamics. In fact, this stochastic Lyapunov function can be used to prove that the approximation on a gridded state space is geometrically ergodic with respect to a unique invariant probability measure nearby the stationary distribution of the SDE, as we do in this paper.

-

(3)

Influence of boundaries. SDEs with boundaries arise in chemical kinetics, population dynamics, epidemiology, and mathematical finance, where the solution (e.g., population densities or interest rates) must always be non-negative [37, 23, 122, 22, 2, 15, 89, 5]. Boundaries also arise in Brownian dynamics simulations. For example, in bead-spring chain models upper bounds are imposed on bond lengths in order to model the experimentally observed extension of semi-flexible polymers [110]. In this context standard integrators may produce updated states that are not within the domain of the SDE problem, which in this paper we refer to as nonphysical moves. The proposed approximation can eliminate such nonphysical moves by allowing the spatial step size to be set such that no update lies outside the domain of definition of the SDE.

-

(4)

First Exit Problems. It is known that standard integrators do not work well in simulating first exits from a given region because, simply put, they fail to account for the probability that the system exits the region in between each discrete time step [38, 39, 40]. Building this capability into time integrators is nontrivial, e.g., one technique requires locally solving a boundary value problem per step, which is prohibitive to do in many dimensions [96]. By using a grid whose boundary conforms to the boundary of the first exit problem, the proposed approximation does not make such time interpolation errors.

In addition, the examples illustrate other interesting properties of realizable discretizations such as their accuracy with respect to the spectrum of the infinitesimal generator of non-symmetric diffusions.

1.3. Relation to Other Works

When the diffusion matrix is diagonally dominant, H. Kushner developed realizable finite difference approximations to SDEs and used probabilistic methods to prove that these finite difference schemes are convergent [76, 80, 81, 77, 78, 79]. When the SDE is self-adjoint and the noise is additive, realizable discretizations combined with SSA have also been developed, see [31, 142, 103, 104, 85], and to be specific, this combined approach seems to go back to at least [31]. Among these papers, the most general and geometrically flexible realizable discretizations seem to be the finite volume methods developed in [85]. This paper generalizes these realizable discretizations to diffusion processes with multiplicative noise.

Our approach is related to multiscale methods for approximating SDEs that leverage the spectrum of suitably defined stochastic matrices [127, 128, 21, 20, 109, 103, 104, 104, 85]. However, to be clear, this paper is primarily about approximating the SDE solution, not coarse-graining the dynamics of the SDE.

Our approach also seems to be foreshadowed by Metropolis integrators for SDEs, in the sense that the proportion of time a Metropolis integrator spends in a given region of state space is set by the equilibrium distribution of the SDE, not the time step size [120, 12, 13, 14, 11, 10, 9]. The idea behind Metropolis integrators is to combine an explicit time integrator for the SDE with a Monte Carlo method so that the resulting scheme is ergodic with respect to the stationary distribution of the SDE and finite-time accurate [13]. However, a drawback of these methods is that they are typically limited to diffusions that are self-adjoint [10], whereas the methods presented in this paper do not require this structure. Moreover, Metropolis integrators are typically ergodic with respect to the stationary distribution of the SDE, but they may not be geometrically ergodic when the SDE is [120, 13, 11]. Intuitively speaking, the reason Metropolis integrators lack geometric ergodicity is that they use as proposal moves conditionally stable integrators for the SDE. Hence, outside the region of stability of these integrators the Metropolis rejection rate tends to one. In these unstable regions, Metropolis integrators may get stuck, and as a consequence, typically do not have a stochastic Lyapunov function. In contrast, the proposed approximations do have a stochastic Lyapunov function for a large class of diffusion processes.

Our approach is also related to, but different from, variable time step integrators for SDEs [36, 132, 82]. These integrators are not all adapted to the filtration given by the noise driving the approximation. Let us comment on the adapted (or non-anticipating) technique proposed in [82], which is based on a simple and elegant design principle. The technique has the nice feature that it does not require iterated stochastic integrals. The method adjusts its time step size at each step according to an estimate of the ‘deterministic accuracy’ of the integrator, that is, how well the scheme captures the dynamics in the zero noise limit. The time step size is reduced until this estimate is below a certain tolerance. The aim of this method is to achieve stability by being deterministically accurate. In fact, as a consequence of this accuracy, the approximation ‘inherits’ a stochastic Lyapunov function from the SDE and is provably geometrically ergodic. This paper [82] also addresses what happens if the noise is large compared to the drift. The difference between these variable time step integrators and the proposed approximation is that the latter sets its mean time step according to the Kolmogorov equation and achieves stability by bounding its spatial step size.

1.4. Organization of Paper

The remainder of this paper is structured as follows.

- Chapter 2:

-

details our strategy to spatially discretize an SDE problem.

-

•:

§2.1 defines what it means for a spatial discretization to be realizable.

-

•:

§2.2 describes the differences and pros/cons between a gridded and gridless state space.

-

•:

§2.3 derives realizable discretizations in one dimension using an upwinded finite difference, finite volume, and a probabilistic discretization.

-

•:

§2.4 derives realizable discretizations in two dimension using an upwinded finite difference method.

-

•:

§2.5 presents realizable discretizations in -dimension, which are based on central and upwinded finite differences on a gridless state space.

-

•:

§2.6 discusses and analyzes the scaling of the approximation with respect to the dimension of the SDE problem.

-

•:

§2.7 generalizes realizable discretizations in -dimension to diffusion matrices that can be written as a sum of rank one matrices.

-

•:

§2.8 considers the special case of weakly diagonally dominant diffusion matrices, and proves that a second-order accurate, upwinded finite difference discretization is realizable on a gridded state space.

-

•:

- Chapter 3:

-

applies realizable discretizations to SDE problems.

-

•:

§3.2 (resp. §3.5) provides numerical evidence that the approximation is stable (i.e. geometrically ergodic) and accurate in representing moments at finite times, mean first passage times, exit probabilities, and the stationary distribution of a one-dimensional process with additive (resp. multiplicative) noise.

-

•:

§3.3 presents an asymptotic analysis of the mean-holding time of the approximation, which is used to validate some numerical results.

-

•:

§3.6 shows that the approximation eliminates nonphysical moves in the Cox-Ingersoll-Ross model from mathematical finance, is accurate in representing the stationary distribution of this process, and can efficiently handle singularities in SDE problems by using adaptive mesh refinement.

-

•:

§3.7 illustrates that the approximation accurately represents the spectrum of the generator in a variety of non-symmetric diffusion processes with additive noise including SDE problems with nonlinear drift fields, internal discontinuities, and singular drift fields.

-

•:

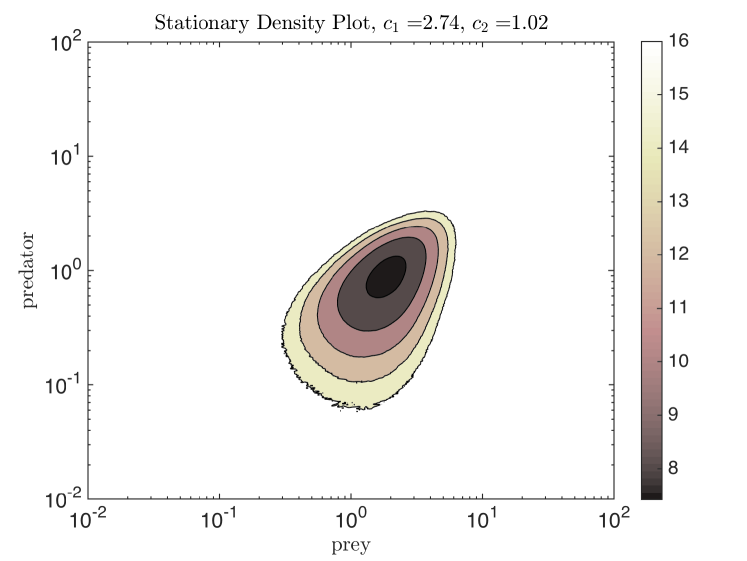

§3.9 shows that the approximation on a gridded state space (with variable step sizes) is accurate in representing the stationary distribution of a two-dimensional process with multiplicative noise.

-

•:

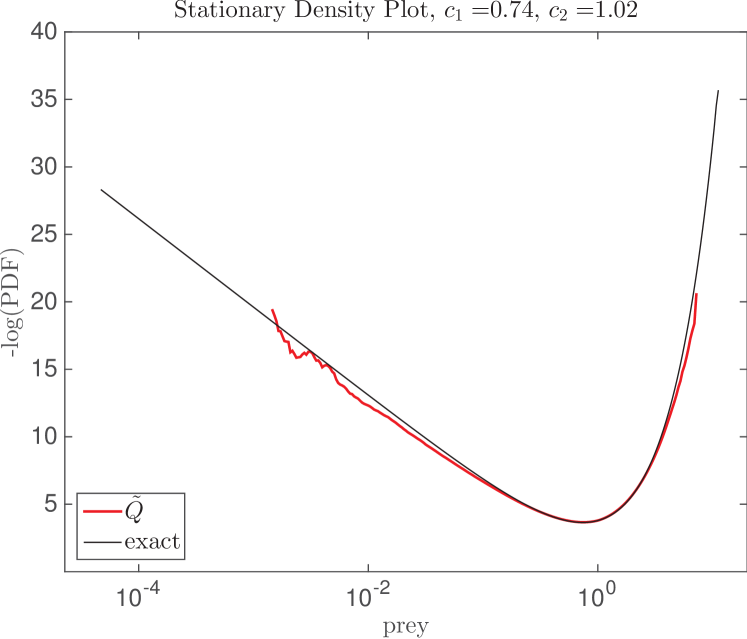

§3.10 applies the approximation to a Lotka-Volterra process from population dynamics, which shows that the approximation eliminates nonphysical moves, is suitable for long-time simulation, and can capture extinction.

-

•:

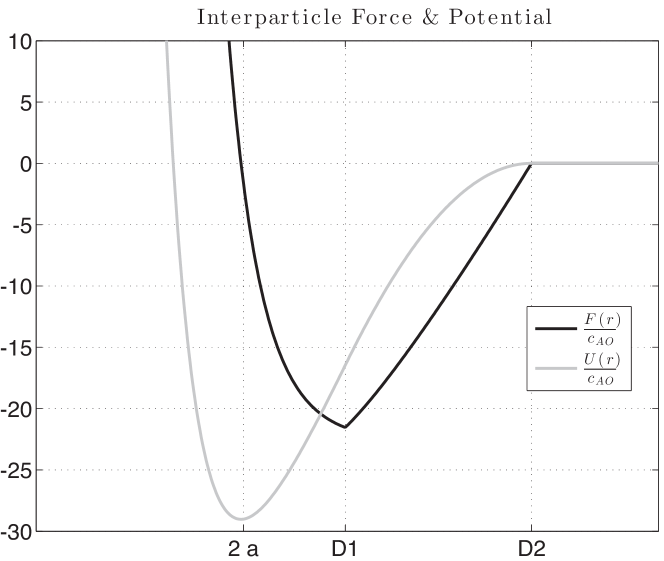

§3.11 tests the approximation on a Brownian dynamics simulation of a colloidal cluster immersed in an unbounded solvent, and shows that the jump size can be set according to a characteristic length scale in an SDE problem, namely the Lennard-Jones radius.

-

•:

- Chapter 4:

-

analyzes a realizable discretization on a gridded state space.

- •:

-

•:

§4.2 derives a sharp stochastic Lyapunov function for the SDE solution and the approximation, and uses this Lyapunov function to show that both the SDE solution and the approximation are geometrically ergodic with respect to an invariant probability measure.

-

•:

§4.3 solves a martingale problem associated to the approximation, justifies a Dynkins formula for a large class of observables of the approximation, and applies this solution to analyze basic properties of realizations of the approximation.

-

•:

§4.5 proves that the approximation is accurate with respect to finite-time conditional expectations and equilibrium expectations by using a continuous-time analog of the Talay-Tubaro expansion of the global error.

- Chapter 5:

-

analyzes a realizable discretization on a gridless state space.

-

•:

§5.1 introduces a mollified generator that uses variable step sizes.

-

•:

§5.2 shows that this generator defines a bounded operator with respect to Borel bounded functions and induces a Feller semigroup.

-

•:

§5.3 proves that this generator is accurate with respect to the infinitesimal generator of the SDE.

-

•:

§5.4 shows that the associated approximation has a sharp stochastic Lyapunov function provided that the mollification is not too strong.

-

•:

§5.5 proves that the associated approximation is accurate with respect to finite-time conditional expectations and equilibrium expectations by using a continuous-time analog of the Talay-Tubaro expansion of the global error.

-

•:

- Chapter 6:

-

analyzes tridiagonal, realizable discretizations on gridded state spaces.

-

•:

§6.1 derives an explicit formula for the invariant density of the approximation.

-

•:

§6.2 quantifies the accuracy of the stationary density of the approximation.

-

•:

§6.3 derives an explicit formula for the exit probability (or committor function) of the approximation.

-

•:

§6.4 derives an explicit formula for the mean first passage time of the approximation.

-

•:

- Chapter 7:

-

concludes the paper.

1.5. Acknowledgements

We wish to thank Aleksandar Donev, Weinan E, Denis Talay, Raúl Tempone and Jonathan Weare for useful discussions.

Chapter 2 Algorithms

2.1. Realizability Condition

Here we present a time-continuous approach to numerically solve an -dimensional SDE with domain . The starting point is the infinitesimal generator:

| (2.1.1) |

associated to the stochastic process that satisfies the SDE:

| (2.1.2) |

where is an -dimensional Brownian motion and and are the drift and noise fields, respectively. (The test function in (2.1.1) is assumed to be twice differentiable.) Let be the (formal) adjoint operator to . Given an initial density , the Fokker-Planck equation:

| (2.1.3) |

describes the evolution of the probability density of . The time evolution of a conditional expectation of an observable is described by the Kolmogorov equation:

| (2.1.4) |

with initial condition . A weak solution to the SDE (2.1.2) can be obtained by solving (2.1.3) or (2.1.4). In this paper we consider solvers for (2.1.2) that exploit this connection.

The essential idea is to approximate the infinitesimal generator of the SDE in (2.1.1) by a discrete-space generator of the form:

| (2.1.5) |

where we have introduced a reaction rate function , and reaction channels: for and for every . (This terminology comes from chemical kinetics [37].) Let be a spatial step size parameter and be a positive parameter, which sets the order of accuracy of the method. We require that the generator satisfies

- (Q1) th-order accuracy:

-

- (Q2) realizability:

-

Condition (Q1) is a basic requirement for any spatial discretization of a PDE. If (Q1) holds, and assuming numerically stability, then the approximation is th-order accurate on finite-time intervals (see e.g. Theorem 4.5.1 for a precise statement). Condition (Q2) is not a standard requirement, and is related to the structure of the Kolmogorov equation. In words, (Q2) states that the weights in the finite differences appearing in (2.1.5) must be non-negative. We call an operator that satisfies this condition realizable. Without this requirement the approximation would be a standard numerical PDE solver and limited to low-dimensional systems by the curse of dimensionality. In contrast, when (Q2) holds the generator is realizable, in the sense that it induces a Markov jump process which can be simulated exactly in time using the Stochastic Simulation Algorithm (SSA) [37, 31, 142, 85]. This simulation does not require explicitly gridding up any part of state space, since its inputs – including rate functions and reaction channels – can be computed online. We stress that the channels in (2.1.5) can be picked so that the spatial displacement is bounded for , where as a reminder is the # of channels.

To emphasize that simulating is simple, let us briefly recall how SSA works.

Algorithm 2.1 (Stochastic Simulation Algorithm [37]).

Given the current time , the current state of the process , and the jump rates evaluated at this state , the algorithm outputs the state of the system at time in two sub-steps.

- (Step 1):

-

obtains by generating an exponentially distributed random variable with parameter

- (Step 2):

-

updates the state of the system by assuming that the process moves to state with probability:

Algorithm 2.1 suggests the following compact way to write the action of the generator in (2.1.5):

| (2.1.6) |

where the expectation is over the random -vector , whose state space is the set of all reaction channels from the state and whose probability distribution is

To summarize, this paper proposes to (weakly) approximate the solution of a general SDE using a Markov process that can be simulated using Algorithm 2.1, whose updating procedure entails generating a random time increment in (Step 1) and firing a reaction in (Step 2). By restricting the firings in (Step 2) to reaction channels that are a bounded distance away from the current state , the approximation is numerically stable, a point we elaborate on in §4.2. Note that the mean time increment (or mean holding time) in (Step 1) is . Thus, the spatial discretization of determines the average amount of time the process spends at any state. Morever, note that the process satisfies: for . The latter property implies that sample paths of the process are right-continuous in time with left limits (or càdlàg). Also note that the process only changes its state by jumps, and hence, is a pure jump process. Since the time and state updates only depend on the current state , and the holding time in (Step 1) is exponentially distributed, this approximation has the Markov property and is adapted to the filtration of the driving noise. Thus, the approximation is a Markov jump process. As we show in Chapter 4, the Markov and non-anticipating property of the approximation greatly simplify the analysis.

Next we discuss the state space of the approximation, and then derive schemes that meet the requirements (Q1) and (Q2).

2.2. Gridded vs Gridless State Spaces

We distinguish between two types of discretization based on the structure of the graph that represents the state space of the approximation. We say that a graph is connected if there is a finite path joining any pair of its vertices.

Definition 2.2.1.

A gridded (resp. gridless) state space consists of points which form a connected (resp. disconnected) graph.

We stress that both state spaces permit capping the spatial step size of the approximation. Moreover, the SSA on either state space only requires local evaluation of the SDE coefficients. Gridded state spaces are appealing theoretically because a generator on such a space can often be represented as a matrix, and in low dimensional problems, the spectral properties of these matrices (e.g. low-lying eigenvalues, leading left eigenfunction, or a spectral decomposition) can be computed using a standard sparse matrix eigensolver. When the state space is unbounded this matrix is infinite. However, this matrix can still be approximated by a finite-dimensional matrix, and the validity of this approximation can be tested by making sure that numerically computed quantities like the spectrum do not depend on the truncation order. We will return to this point when we consider concrete examples in Chapter 3. In order to be realizable, the matrix associated to the linear operator on a gridded state space must satisfy the -matrix property:

| (2.2.1) |

Indeed, the -matrix property is satisfied by the matrix if and only if its associated linear operator is realizable. Traditional finite difference and finite volume discretizations have been successfully used to design -matrix discretizations when the generator of the SDE is self-adjoint and the noise entering the SDE is additive, see [31, 142, 103, 104, 85]. However, -matrix discretizations on a gridded state space become trickier to design when the noise is multiplicative even in low dimension. This issue motivates designing spatial discretizations on gridless state spaces. Let us elaborate on this point by considering realizable discretizations in one, two, and then many dimensions. With a slight abuse of notation, we may use the same symbol to denote an operator and its associated matrix. The meaning should be clear from the context. The most general realizable discretization is given in §2.7.

2.3. Realizable Discretizations in 1D

SDEs in one dimension possess a symmetry property, which we briefly recall since we expect the proposed schemes to accurately represent this structure. To prove this property, it is sufficient to assume that the noise coefficient is differentiable and satisfies for all , where is the state space of the approximation. Under these assumptions the generator (2.1.1) can be written in conservative form as:

| (2.3.1) |

where and is given by:

for some . Similarly, the SDE (2.1.2) can be written in self-adjoint form:

| (2.3.2) |

where is the free energy of defined as:

Let denote the -weighted inner product defined as:

where the functions and are square integrable with respect to the measure . The generator for scalar, elliptic diffusions is self-adjoint with respect to this inner product i.e.

| (2.3.3) |

for smooth and compactly supported functions and . Note that by taking for every , then for all smooth and compactly supported , which implies that

Thus, is an invariant density of the SDE. Furthermore, if the function is integrable over , i.e. , then is an invariant probability density (or stationary density) of the SDE.

We stress that the generator of SDEs in more than one dimension often do not satisfy the self-adjoint property (2.3.3). Thus, to avoid losing generality, we will not assume the generator of the SDE is self-adjoint. In this context we present finite difference, finite volume, and probabilistic discretizations of .

2.3.1. Finite Difference

Let be a collection of grid points over as shown in Figure 2.1. The distance between neighboring points is allowed to be variable. Thus, it helps to define forward, backward and average spatial step sizes:

| (2.3.4) |

at every grid point . The simplest way to construct a realizable discretization of is to use an upwinded and a central finite difference approximation of the first and second-order derivatives in , respectively. To derive this discretization, it is helpful to write the generator in (2.3.1) in terms of the functions and as follows:

| (2.3.5) |

To obtain a realizable discretization, the first term of (2.3.5) is discretized using a variable step size, first-order upwind method:

Here we employ the shorthand notation: for all grid points (and likewise for other functions), and

for any real numbers and . By taking the finite difference approximation on the upstream side of the flow, i.e., going backward or forward in the finite difference approximation of according to the sign of the coefficient , this discretization is able to simultaneously satisfy first-order accuracy (Q1) and realizability (Q2). A variable step size, central scheme can be used to approximate the second-order term in (2.3.5):

It is straightforward to verify that this part of the discretization obeys (Q1) with and since satisfies (Q2) as well. The resulting discrete generator is a -matrix with off-diagonal entries

| (2.3.6) |

Note that to specify a -matrix, it suffices to specify its off-diagonal entries and then use (2.2.1) to determine its diagonal entries. Also, note that this scheme does not require computing the derivative of , which appears in the drift coefficient of (2.3.2). The overall accuracy of the scheme is first-order in space. The approximation also preserves an invariant density, see Proposition 6.1.1 for a precise statement and proof. Remarkably, the asymptotic mean holding time of this generator is exact when, roughly speaking, the drift is large compared to the noise. We will prove and numerically validate this statement in §3.3.

2.3.2. Finite Volume

Next we present a finite volume discretization of . This derivation illustrates the approach taken in [85] to construct realizable discretizations for self-adjoint diffusions. For this purpose discretize the region using the partition shown in Figure 2.2. This partition consists of a set of cells with centers spaced according to (2.3.4). The cells are defined as where the midpoint between cell centers gives the location of each cell edge. From (2.3.4) note that the length of each cell is .

Integrating the Fokker-Planck equation (2.1.3) over cell yields:

Here we have introduced and , which are the probability fluxes at the right and left cell edge, respectively. Approximate the solution to the Fokker-Planck equation by its cell average:

In terms of which, approximate the probability flux using

| (2.3.7) |

These approximations lead to a semi-discrete Fokker-Planck equation of the form:

where is the transpose of the matrix , whose off-diagonal entries are

| (2.3.8) |

This generator is a second-order accurate approximation of and it preserves the invariant density of the SDE in the following way. Let be the invariant density weighted by the length of each cell

It follows from (2.3.8) that

since from (2.3.4) . This identity implies that is an invariant density of , see Proposition 6.1.1 for a detailed proof. Other approximations to the probability flux also have this property e.g. the midpoint approximation of in (2.3.7) can be replaced by:

(As a caveat, note that the former choice reduces the order of accuracy of the discretization because it uses the minimum function.) In fact, the evaluation of can be bypassed by approximating the forward and backward potential energy differences appearing in (2.3.8) by the potential force to obtain the following -matrix approximation:

| (2.3.9) |

In terms of function evaluations, (2.3.9) is a bit cheaper than (2.3.8), and this difference in cost increases with dimension. Under natural conditions on and , we will prove that (2.3.9) possesses a second-order accurate stationary density, see Proposition 6.2.1.

For a more general theoretical and numerical treatment of realizable finite-volume methods for self-adjoint diffusions with additive noise we refer to [85].

2.3.3. Time-Continuous Milestoning

Finally, we consider a ‘probabilistic’ discretization of the generator . The idea behind this Q-matrix approximation is to determine the jump rates according to the exit probability and the mean holding time of the SDE solution at each grid point.

To this end, let be the first time the SDE solution hits the state ‘a’ given that it starts at the state ‘x’. Define the exit probability (or the committor function) to be , which gives the probability that the process first hits ‘b’ before it hits ‘a’ starting from any state ‘x’ that is between them: . This function satisfies the following boundary value problem:

| (2.3.10) |

Let for every grid point . Solving (2.3.10) with and yields the following exit probabilities conditional on the process starting at the grid point

| (2.3.11) | |||

We use these expressions below to define the transition rates of the approximation from to its nearest neighbors.

To obtain the mean holding time of the approximation, recall that the mean first passage time (MFPT) to given that is the unique solution to the following boundary value problem:

| (2.3.12) |

In particular, the MFPT to given that the process starts at the grid point is given by

Since the process initiated at spends on average time units before it first hits a nearest neighbor of , the exact mean holding time in state is given by:

| (2.3.13) |

Similarly, the solution (2.3.11) specifies the transition probabilities:

| (2.3.14) | |||

Incidentally, these are the transition probabilities used in discrete-time optimal milestoning [140], where the milestones correspond to the grid points depicted in Figure 2.3. Combining (2.3.13) and (2.3.14) yields:

| (2.3.15) |

which shows that a -matrix can be constructed in one-dimension based on the exact mean holding time and exit probability. We emphasize that this discretization is still an approximation, and in particular, does not exactly reproduce other statistics of the SDE solution as pointed out in [140]. We will return to this point in §6.4 where we analyze some properties of this discretization. In §3.3, we will use this discretization to validate an asymptotic analysis of the mean holding time of finite-difference approximations in one dimension.

To recap, the construction of requires the exit probability (or committor function) to compute the transition probabilities, and the MFPT to compute the mean holding time. Obtaining these quantities entails solving the boundary value problems (2.3.10) and (2.3.12). Thus, it is nontrivial to generalize to many dimensions and we stress our main purpose in constructing is to benchmark other (more practical) approximations in one dimension.

2.4. Realizable Discretizations in 2D

Here we derive realizable finite difference schemes for planar SDEs. The main issue in this part is the discretization of the mixed partial derivatives appearing in (2.1.1), subject to the constraint that the realizability condition (Q2) holds. To be specific, consider an SDE whose domain is in and write its drift and noise fields as:

Here is the diffusion field. Let be a collection of grid points on a rectangular grid in two-space as illustrated in Figure 2.4. Given , we adopt the notation:

| shorthand | meaning | ||||

|---|---|---|---|---|---|

| grid point function evaluation | |||||

|

|

|

||||

|

|

|

The distance between neighboring vertical or horizontal grid points is permitted to be variable. Hence, it helps to define:

at all grid points .

We first consider a generalization of the first-order scheme (2.3.6). The drift term in is approximated using an upwinded finite difference:

| (2.4.1) |

and similarly,

| (2.4.2) |

We recruit all of the channels that appear in Figure 2.4 in order to discretize the second-order partial derivatives in . Specifically,

| (2.4.3) | ||||

where we introduced the following labels for the rate functions: , , and . To be clear there are eight rate functions and eight finite differences in this approximation. We determine the eight rate functions by expanding the horizontal/vertical finite differences in this approximation to obtain

| (2.4.4) | ||||

Similarly, we expand the diagonal/antidiagonal differences to obtain

| (2.4.5) | ||||

Note that the first order partial derivatives appearing in these expansions appear in plus and minus pairs, and ultimately cancel out. This cancellation is necessary to obtain an approximation to the second-order pure and mixed partial derivatives in (2.4.3). Using these expansions it is straightforward to show that the following choice of rate functions

imply that the approximation in (2.4.3) holds. Note here that we have used an upwinded finite difference to approximate the mixed partial derivatives of . Combining the above approximations to the drift and diffusion terms yields:

| (2.4.6) | ||||

This generator is a two-dimensional generalization of (2.3.5). However, unlike in 1D, to approximate mixed partial derivatives finite differences in the diagonal and antidiagonal channel directions are used. To be accurate, the spurious pure derivatives produced by these differences, however, must be subtracted off the vertical and horizontal finite differences. This subtraction affects the realizability condition (Q2), and in particular, the weights in the horizontal and vertical finite differences may become negative. Note that this issue becomes a bit moot if the diffusion matrix is uniformly diagonally dominant, since this property implies that

and hence, satisfies the realizability condition (Q2) on a gridded state space, with evenly spaced points in the and directions.

Alternatively, if we approximate the first and second-order ‘pure’ partial derivatives in using a weighted central difference, and use an upwinded finite difference to handle the mixed partials, we obtain the following generator:

| (2.4.7) | ||||

Here we have defined as the solution to the linear system

Like , if the diffusion matrix is diagonally dominant, then this generator is realizable on an evenly spaced grid. In §3.9 and §3.10, we test on planar SDE problems. In these problems the diffusion matrices are not diagonally dominant, and we must use variable step sizes in order to obtain a realizable discretization. In §2.8 we generalize the upwinded finite difference approximation to multiple dimensions and prove that if the diffusion matrix is uniformly diagonally dominant, then this generalized discretization is realizable.

To avoid assuming the diffusion matrix is diagonally dominant, we next consider approximations whose state space is gridless.

2.5. Realizable Discretizations in nD

We now present a realization discretization on a gridless state space contained in . To introduce this approximation, set the number of channel directions equal to the dimension of the space and let be an index over these reaction channel directions . Let be forward/backward spatial step sizes at state , let be the average step size at state defined as

let be the columns of the noise matrix , and let be a transformed drift field defined as:

| (2.5.1) |

where is the diffusion matrix. (If is positive definite, then this linear system has a unique solution for every . This condition holds in the interior of for all of the SDE problems we consider in this paper.) With this notation in hand, here is a second order accurate, realizable discretization in -dimensions.

| (2.5.2) |

The generator is a weighted central finite difference scheme in the directions of the columns of the noise coefficient matrix evaluated at the state . When the noise coefficient matrix is additive (state-independent) and isotropic (direction-independent), then the state space of this generator is gridded and the generator can be represented as matrix. In general, we stress that the state space of this approximation is gridless, and thus the generator cannot be represented as a matrix. Nevertheless it can be realized by using the SSA algorithm. A realization of this process is a continuous-time random walk with a user-defined jump size, jump directions given by the columns of the noise coefficient matrix, and a mean holding time that is determined by the discretized generator. This generator extends realizable spatial discretizations appearing in previous work [31, 142, 103, 104, 85] to the SDE (2.1.2), which generically has a non-symmetric infinitesimal generator and multiplicative noise.

The next proposition states that this generator satisfies (Q1) and (Q2).

Proposition 2.5.1.

Proof.

This proof is somewhat informal. A formal proof requires hypotheses on the SDE and the test function . For clarity of presentation, we defer these technical issues to Chapter 4. Here we concentrate on showing in simple terms that the approximation meets the requirements (Q1) and (Q2).

Let denote the th-derivative of applied to the vectors for any . Note that the rate functions appearing in are all positive, and thus, the realizability condition (Q2) is satisfied. To check second-order accuracy or (Q1) with , Taylor expand the forward and backward finite differences appearing in the function to obtain:

In order to obtain a crude estimate of the remainder term in this expansion, we used the identity with and , and the relation . A similar Taylor expansion of the exponentials yields,

where we used the cyclic property of the trace operator, the basic linear algebra fact that the product is the sum of the outer products of the columns of , and elementary identities to estimate the remainder terms, like with and . Thus, is second-order accurate as claimed. ∎

The analysis in Chapter 4 focusses on the stability, accuracy and complexity of the generator , mainly because it is second-order accurate. However, let us briefly consider two simpler alternatives, which are first-order accurate. To avoid evaluating the exponential function appearing in the transition rates of in (2.5.2), an upwinded generator is useful

| (2.5.3) | ||||

Let be the standard basis of . To avoid solving the linear system in (2.5.1), an upwinded generator that uses the standard basis to discretize the drift term in is useful

| (2.5.4) | ||||

Proposition 2.5.2.

Assuming that:

then the operators and satisfy (Q2) and (Q1) with .

2.6. Scaling of Approximation with System Size

Here we briefly discuss the complexity of the SSA induced by the generator in (2.5.2). We will return to this point in Chapter 4 where we quantify the complexity of sample paths as a function of the spatial step size parameter.

First we compare the complexity of the SSA to a standard numerical PDE solver for the Kolmogorov equation. When the grid is bounded, even though the matrix associated to standard PDE discretizations (like finite difference, volume and element methods) is often sparse, the computational effort required to construct its entries in order to time integrate the resulting semi-discrete ODE (either exactly or approximately) scales exponentially with the number of dimensions. On an unbounded grid, this ODE is infinite-dimensional and a standard numerical PDE approach does not apply.

In contrast, note from Algorithm 2.1 that an SSA simulation of the Markov process induced by the generator in (2.5.2) takes as input the reaction rates and channels, which can be peeled off of (2.5.2). More to the point, both the spatial and temporal updates in each SSA step use local information. (Put another way, in the case of a gridded state space, a step of the SSA method only requires computing a row of a typically sparse matrix associated to the generator, not the entire matrix.) Thus, the cost of each SSA step in high dimension is much less severe than standard numerical PDE solvers and remains practical.

Next consider the average number of SSA steps required to reach a finite time. Referring to Algorithm 2.1, the random time increment gives the amount of time the process spends in state before jumping to a new state . In each step of the SSA method, only a single degree of freedom is updated because the process moves from the current position to a new position in the direction of only one of the columns of the noise matrix. In other words, the method involves local moves, and in this way, it is related to splitting methods for SDEs and ODEs based on local moves, for example the per-particle splitting integrator proposed for Metropolis-corrected Langevin integrators in [14] or J-splitting schemes for Hamiltonian systems [33]. However, the physical clock in splitting algorithms does not tick with each local move as it does in (Step 1) of the SSA method. Instead the physical time in a splitting scheme does not pass until all of the local moves have happened. In contrast, the physical clock ticks with each local move of the SSA method. This difference implies that the mean holding time of the SSA method is inversely proportional to dimension.

The easiest way to confirm this point is to consider a concrete example, like evolving decoupled oscillators using the SSA induced by (2.5.2). In this example, the mean time step for a global move of the system – where each oscillator has taken a step – cannot depend on dimension because the oscillators are decoupled. For simplicity assume the SDE for each oscillator is and the spatial step size in every reaction channel direction is uniform and equal to , and let . Then, from (2.5.2) the total jump rate is:

where is the jump rate of the th oscillator:

Expanding the total jump rate about yields

Similarly, expanding the mean holding time about yields

Thus, the total jump rate is roughly and the mean holding time scales like with dimension , as expected.

To summarize, we see that given the nature of the SSA method, accuracy necessitates a smaller mean time step for each local move and the overall complexity of the SSA method is no different from a splitting temporal integrator that uses local moves.

2.7. Generalization of Realizable Discretizations in nD

Suppose the diffusion matrix can be written as a sum of rank- matrices:

| (2.7.1) |

where is an -vector and is a non-negative weight function for all , and for . Since the diffusion matrix is positive definite, it must be that and that the set of vectors spans for every . For example, since , the diffusion matrix can always be put in the form of (2.7.1) with , unit weights , and for , or equivalently,

The following generator generalizes (2.5.2) to diffusion matrices of the form (2.7.1).

| (2.7.2) |

This generator is a weighted, central finite difference approximation along the directions given by the vectors . To be sure in (2.7.2) is the transformed drift field introduced earlier in (2.5.1). The next proposition states that this generalization of meets the requirements (Q1) and (Q2).

Proposition 2.7.1.

Proof.

The operator satisfies the realizability condition (Q2) since by hypothesis on the diffusion field . To check accuracy, Taylor expand the forward/backward differences appearing in to obtain:

A similar Taylor expansion of the exponentials yields,

where we used (2.7.1). Thus, is second-order accurate as claimed. ∎

As an application of Proposition 2.7.1 we next show that realizable discretizations on gridded state spaces are possible to construct if the diffusion matrix of the SDE is diagonally dominant.

2.8. Weakly Diagonally Dominant Case

Here we extend the upwinded finite-difference approximation in (2.4.7) from two to many dimensional SDEs assuming that the diffusion matrix is weakly diagonally dominant. We prove that this extension is realizable and second-order accurate under this assumption. Let us quickly recall what it means for a matrix to be weakly diagonally dominant.

Definition 2.8.1.

An matrix is weakly diagonally dominant if there exists an -vector with positive entries such that

| (2.8.1) |

for all .

The following lemma is straightforward to derive from this definition.

Lemma 2.8.1.

Let be a square matrix satisfying (2.8.1). Then there exists a positive diagonal matrix such that the square matrix is diagonally dominant.

Let be a field of spatial step sizes, which permit a different spatial step size for each coordinate axis. Let be the transformed drift field defined in (2.5.1). Here is a multi-dimensional generalization of

| (2.8.2) |

where the expectation is over the random vector which has a discrete probability distribution given by:

| (2.8.3) | ||||

where is a point mass concentrated at , is a normalization constant, is the mean holding time, and we have introduced the following reaction channels:

| (2.8.4) |

The superscripts and in the reaction channels above refer to the diagonal and anti-diagonal directions in the -plane, respectively.

The following proposition states that satisfies (Q1) and (Q2).

Proposition 2.8.2.

Proof.

This proof is an application of Proposition 2.7.1. To apply this proposition we show that if the Cholesky factorization of has at most two nonzero entries per column, then can be put in the form of (2.7.1). According to Theorem 9 of [8], the Cholesky factorization of a symmetric matrix with positive diagonals has at most two nonzero entries in every column if and only if it is weakly diagonally dominant. Since is symmetric positive definite by hypothesis, and since the Cholesky factorization of has at most two nonzero entries per column also by hypothesis, is weakly diagonally dominant for all . Hence, by Lemma 2.8.1 there exists a positive diagonal matrix such that:

| (2.8.5) |

is diagonally dominant for each . Define a field of step sizes by setting . Hence, we have that:

where we used the forward direction channels defined in (2.8.4). Note that the coefficient of each rank one matrix in this last expression is non-negative because is diagonally dominant. Thus, is in the form of (2.7.1) with and note that is a special case of in (2.7.2) with . The desired result follows from Proposition 2.7.1. ∎

We have the following corollary.

Corollary 2.8.3.

If the diffusion matrix is diagonally dominant for all , then in (2.8.2) is realizable on a gridded state space in .

As far as we can tell, realizable, finite difference discretizations of this type seem to have been first developed by H. Kushner [77, 78, 79].

Proof.

In this case the diffusion matrix can be written as:

and the coefficient of each rank one matrix in this last expression is non-negative because is diagonally dominant by hypothesis. Thus, is in the form of (2.7.1) with and note that is a special case of in (2.7.2) with . Note also that the state space is gridded since the jumps are either to nearest neighbor grid points: for all , or to next to nearest neighbor grid points: and for all and . ∎

Chapter 3 Examples & Applications

3.1. Introduction

In this chapter we apply realizable discretizations to

-

(1)

a cubic oscillator in 1D with additive noise as described in §3.2;

-

(2)

a log-normal process in 1D with multiplicative noise as described in §3.5;

-

(3)

the Cox-Ingersoll-Ross process in 1D with multiplicative noise as described in §3.6;

-

(4)

a non-symmetric Ornstein-Uhlenbeck process as described in §3.7.1;

-

(5)

the Maier-Stein SDE in 2D with additive noise as described in §3.7.2;

-

(6)

simulation of a particle in a planar square-well potential well in 2D with additive noise as described in §3.7.3;

-

(7)

simulation of a particle in a worm-like chain potential well in 2D with additive noise as described in §3.7.4;

-

(8)

a log-normal process in 2D with multiplicative noise as described in §3.9;

-

(9)

a Lotka-Volterra process in 2D with multiplicative noise as described in §3.10; and,

-

(10)

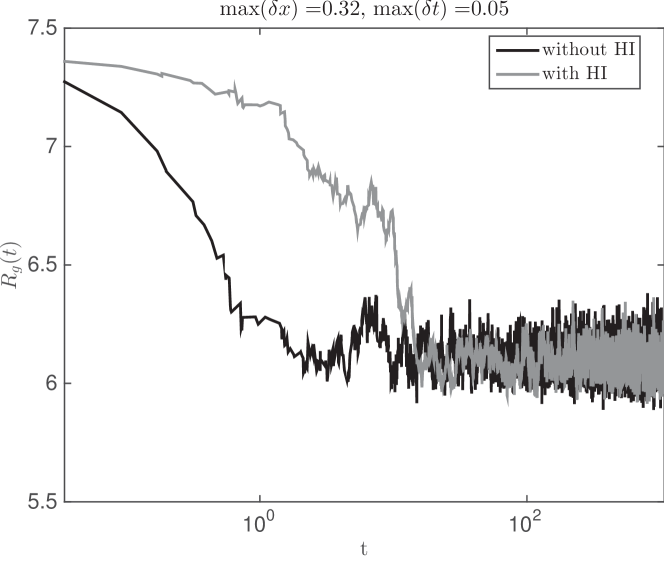

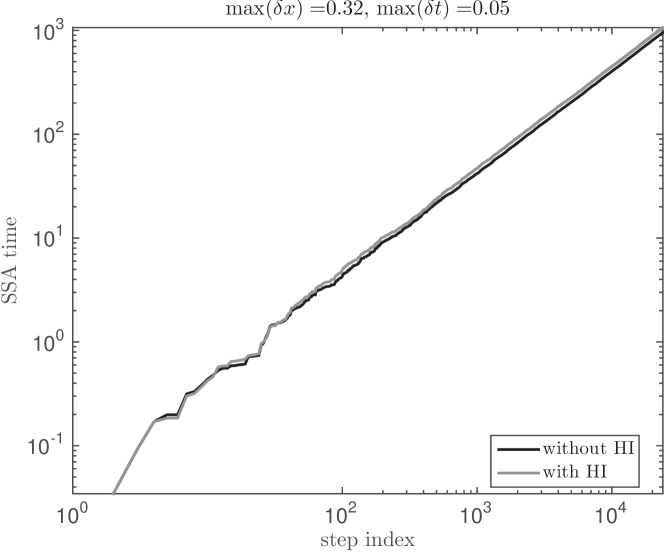

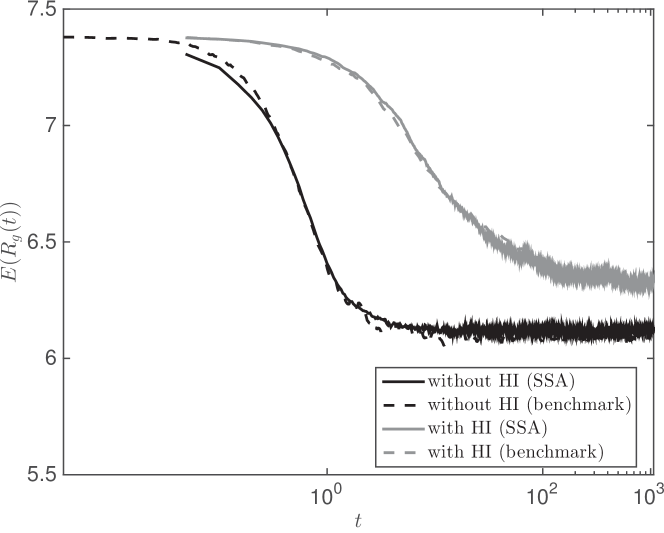

a Brownian dynamics simulation of the collapse of a colloidal cluster in 39D with and without hydrodynamic interactions as described in §3.11.

For the 1D SDE problems, we numerically test two realizable spatial discretizations with a gridded state space. The first uses an upwinded (resp. central) finite difference method to approximate the first (resp. second) order derivative in (2.1.1).

| (3.1.1) |

The second generator uses a weighted central finite difference scheme to approximate the derivatives in (2.1.1).

| (3.1.2) |

These discretizations are slight modifications to the discretizations given in (2.3.6) and (2.3.9), respectively. For the planar SDE problems, we apply a 2D version of (3.1.2) given in (2.4.7). When the noise is additive, we use an evenly spaced grid. When the noise is multiplicative, we use adaptive mesh refinement as described in §3.4 in 1D and §3.8 in 2D. For the 39D SDE problem, we apply the generator on a gridless state space given in (2.5.2).

3.2. Cubic Oscillator in 1D with Additive Noise

This SDE problem is a concrete example of exploding numerical trajectories. Consider (2.1.2) with , , and i.e.

| (3.2.1) |

The solution to (3.2.1) is geometrically ergodic with respect to a stationary distribution with density

| (3.2.2) |

However, explicit methods are transient in this example since the drift entering (3.2.1) is only locally Lipschitz continuous. More concretely, let denote a (discrete-time) Markov chain produced by forward Euler with time step size . Then, for any this Markov chain satisfies

where denotes expectation conditional on . (See Lemma 6.3 of [53] for a simple proof, and [60] for a generalization.) Metropolizing explicit integrators, like forward Euler, mitigates this divergence. Indeed, the (discrete-time) Markov chain produced by a Metropolis integrator is ergodic with respect to the stationary distribution of the SDE, and hence,

However, the rate of convergence of this chain to equilibrium is not geometric, even though the SDE solution is geometrically ergodic [119, 13]. The severity of this lack of geometric ergodicity was recently studied in [11], where it was shown that the deviation from geometric ergodicity is exponentially small in the time step size. This result, however, does not prevent the chain from “getting stuck” (rarely accepting proposal moves) in the tails of the stationary density in (3.2.2).

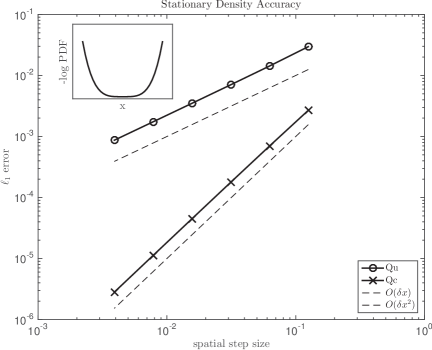

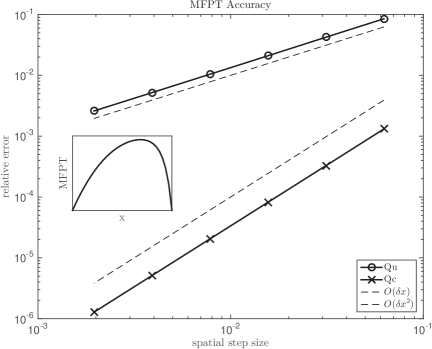

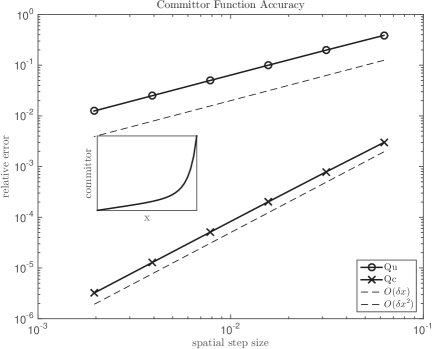

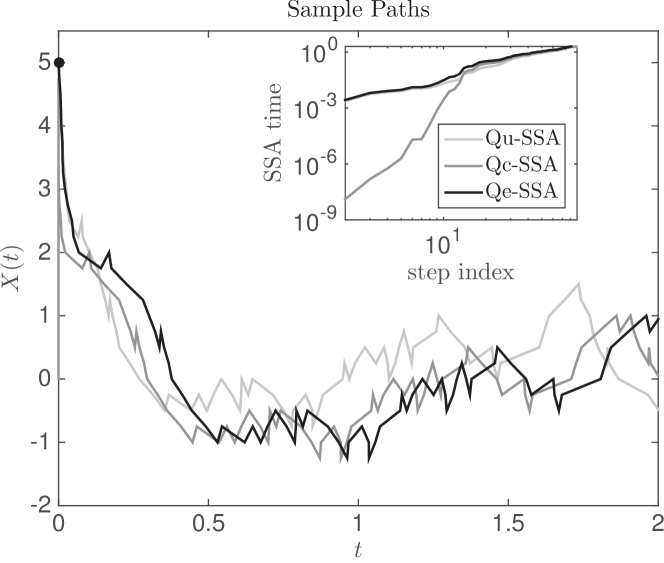

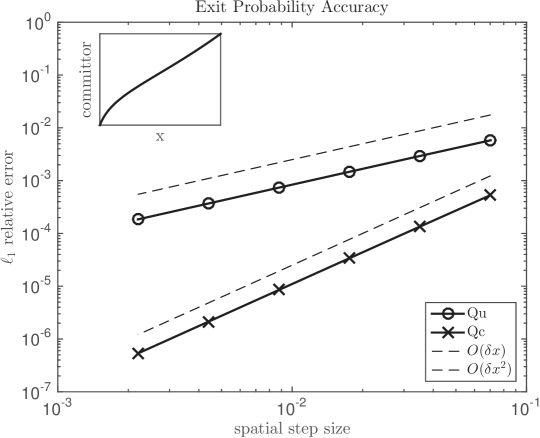

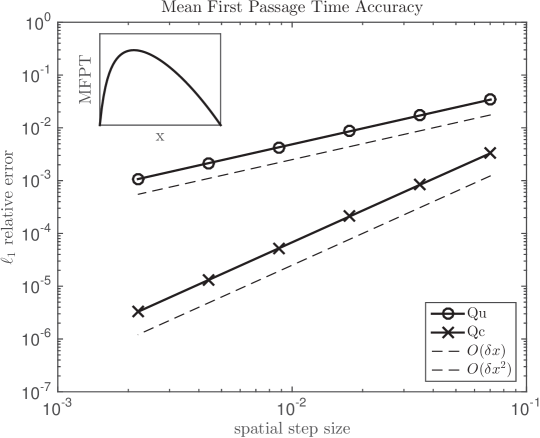

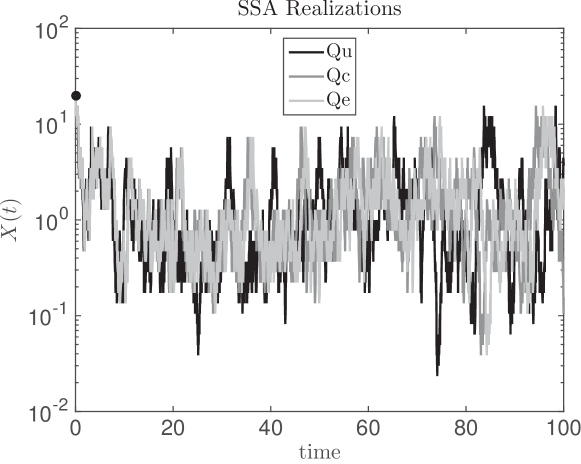

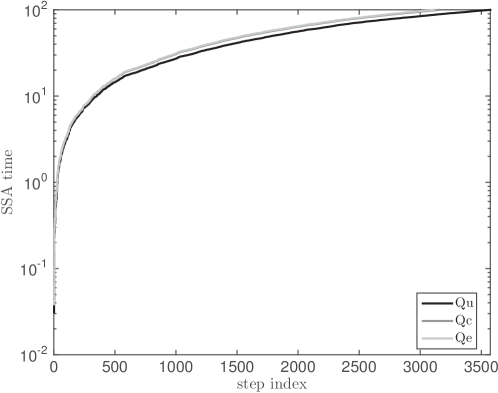

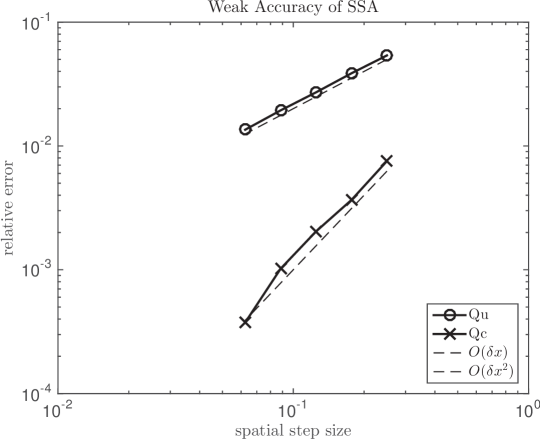

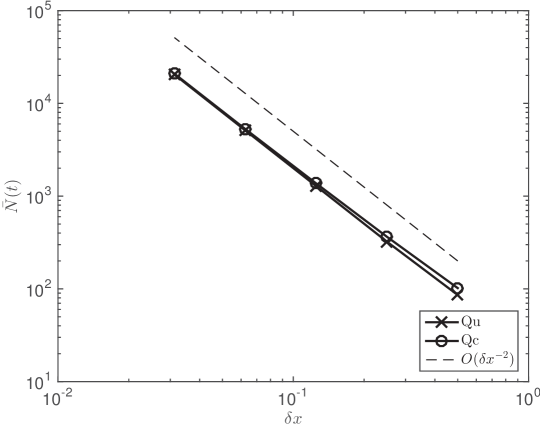

In this context we test the generators in (3.1.1) and in (3.1.2) on an infinite, evenly spaced grid on . Figure 3.1 plots sample paths produced by the SSA induced by these generators. The initial condition is large and positive. For comparison, we plot a sample path (in light grey) of a Metropolis integrator with the same initial condition. At this initial condition, the Metropolis integrator rarely accepts proposal moves and gets stuck for the duration of the simulation. In contrast, the figure shows that the proposed approximations do not get stuck, which is consistent with Theorem 4.2.8. The inset in the figure illustrates that the time lag between jumps in the SSA method is small (resp. moderate) at the tails (resp. middle) of the stationary density. This numerical result manifests that the mean holding time adapts to the size of the drift. Note that the time lag for is smaller than for . In the next section, this difference in time lags is theoretically accounted for by an asymptotic analysis of the mean holding time. Figure 3.2 provides evidence that the approximations are accurate in representing the stationary distribution, mean first passage time, and committor function. To produce this figure, we use results described in Chapter 6. In particular, in the scalar case, the numerical stationary density, mean first passage time and committor satisfy a three-term recurrence relation, which can be exactly solved as detailed in Sections 6.1, 6.4 and 6.3, respectively. We also checked that these solutions agree – up to statistical error – with empirical estimates obtained by an SSA simulation.

Remark 3.2.1.

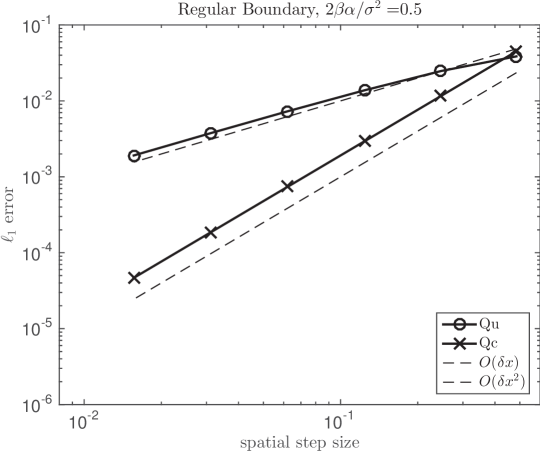

It is known that the rate of convergence (and hence accuracy) of the solution of standard time integrators to first exit problems drops because they fail to account for the probability that the system exits in between each discrete time step [38, 39, 40]. Building this capability into time integrators may require solving a boundary value problem per step, which is prohibitive to do in many dimensions [96]. By keeping time continuous, and provided that the grid is adjusted to fit the boundaries of the region of the first exit problem, the proposed approximations take these probabilities into account. As a consequence, in the middle panel of Figure 3.2 we observe that the order of accuracy of the approximations with respect to first exit times is identical to the accuracy of the generator, that is, there is no drop of accuracy as happens with time discretizations. To be precise, this figure illustrates the accuracy in these approximations with respect to the mean first passage time of the cubic oscillator to and shows that the generators and are and , respectively.

3.3. Asymptotic Analysis of Mean Holding Time

Consider the following instance of (2.1.2)

| (3.3.1) |

Assume the drift entering (3.3.1) is differentiable and satisfies a dissipativity condition, like

Hence, for sufficiently large the SDE dynamics is dominated by the drift, and asymptotically, the time it takes for the SDE solution to move a fixed distance in space can be derived from analyzing the ODE

| (3.3.2) |

Equation (3.3.2) implies that the time lapse between and where satisfies

| (3.3.3) |

By using integration by parts and the mean value theorem, observe that (3.3.3) can be written as:

| (3.3.4) |

for some , and where we have introduced: . Let us compare to the mean holding times predicted by the generators: in (3.1.1) and in (3.1.2). For clarity, we assume that .

By hypothesis, is less than zero if is large and positive, and hence, from (3.1.1) the mean holding time of can be written as:

This expression can be rewritten as

| (3.3.5) |

From (3.3.5), we see that approaches , as the next Proposition states.

Proposition 3.3.1.

For any , the mean holding time of satisfies:

Likewise, if the second term in (3.3.4) decays faster than the first term, then the relative error between and also tends to zero, and thus, the estimate predicted by for the mean holding time asymptotically agrees with the exact mean holding time. This convergence happens if, e.g., the leading order term in is of the form for and .

Repeating these steps for the mean holding time predicted by yields:

| (3.3.6) |

It follows from this expression that even though is a second-order accurate approximation to , it does not capture the right asymptotic mean holding time, as the next Proposition states.

Proposition 3.3.2.

For any , the mean holding time of satisfies:

Simply put, the mean holding time of converges to zero too fast. This analysis is confirmed in Figure 3.3, which shows that the mean holding time for agrees with the mean holding time of the generator that uses the exact mean holding time. This generator was introduced in §2.3.3, see (2.3.15) for its definition. This numerical result agrees with the preceding asymptotic analysis. In contrast, note that the mean holding time of is asymptotically an underestimate of the exact mean holding time, as predicted by (3.3.6).

3.4. Adaptive Mesh Refinement in 1D

The subsequent scalar SDE problems have a domain , and may have a singularity at the origin for certain parameter values. To efficiently resolve this singularity, we will use adaptive mesh refinement, and specifically, a variable step size infinite grid that contains more points near the singularity at . We will construct this grid by mapping the grid to logspace to obtain a transformed grid on defined as

Note that as (resp. ) we have that (resp. ). For the transformed grid in logspace, we assume that the distance between neighboring grid points is fixed and given by , i.e.,

Since

it follows from the definitions introduced in (2.3.4) that:

| (3.4.1) |

3.5. Log-normal Process in 1D with Multiplicative Noise

Consider (2.1.2) with

and initial condition . This process has a lognormal stationary distribution with probability density:

| (3.5.1) |

In fact, satisfies an Ornstein-Uhlenbeck equation with initial condition . Exponentiating the solution to this Ornstein-Uhlenbeck equation yields

It follows that:

| (3.5.2) |

The formulas (3.5.1) and (3.5.2) are useful to numerically validate the approximations.

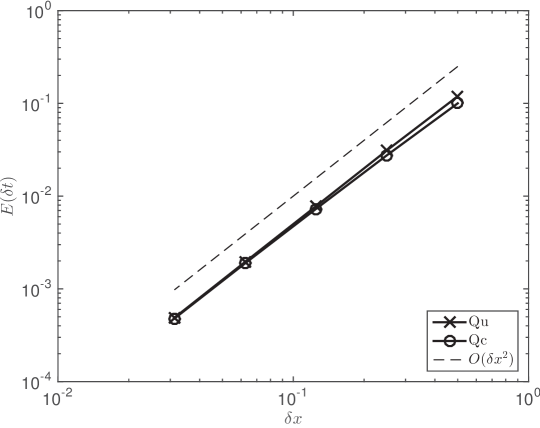

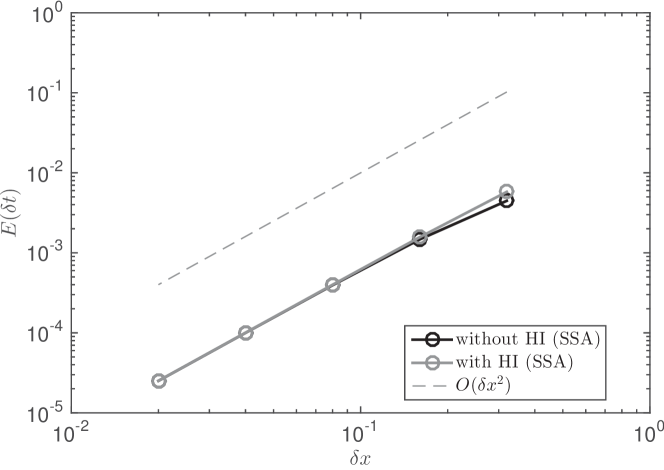

Figure 3.4 show numerical results of applying the generators in (3.1.1) and (3.1.2) to solve the boundary value problems associated to the mean first passage time and exit probability (or committor function) on the interval and using an evenly spaced mesh. Figure 3.5 illustrates that these generators are accurate with respect to the stationary density (3.5.1) using the adaptive mesh refinement described in §3.4. Figure 3.6 plots sample paths produced by SSA for these generators and the SSA time as a function of the step index. Figure 3.7 illustrates the accuracy of the proposed approximations with respect to the mean-squared displacement with an initial condition of . The relative error is plotted as both a function of the spatial step size (top panel) and the mean lag time (bottom panel). Finally, Figure 3.8 plots the average number of computational steps (top panel) and the mean lag time (bottom panel) as a function of the spatial step size. The statistics are obtained by averaging this data over SSA realizations with initial condition and time interval of simulation of .

3.6. Cox-Ingersoll-Ross Process in 1D with Multiplicative Noise

Consider a scalar SDE problem with boundary

| (3.6.1) |

In quantitative finance, this example is a simple model for short-term interest rates [23]. It is known that discrete-time integrators may not satisfy the non-negativity condition: for all [89, 5]. Corrections to these integrators that enforce this condition tend to be involved, specific to this example, or lower the accuracy of the approximation. This issue motivates applying realizable discretizations to this problem, which can preserve non-negativity by construction.

According to the Feller criteria, the boundary at zero is classified as:

-

•

natural if ;

-

•

regular if ; and,

-

•

absorbing if .

When the boundary at zero is natural (resp. regular), the process is positive (resp. non-negative). When the origin is attainable, the boundary condition at the origin is treated as reflective. If and , the SDE solution is ergodic with respect to a stationary distribution with density proportional to:

| (3.6.2) |

We emphasize that is integrable over if and only if and . Note that when the boundary at zero is regular, the stationary density in (3.6.2) is unbounded at the origin.

The numerical tests assess how well the approximation captures the true long-time behavior of the SDE. To carry out this assessment, we estimate the difference between the numerical stationary densities and

| (3.6.3) |

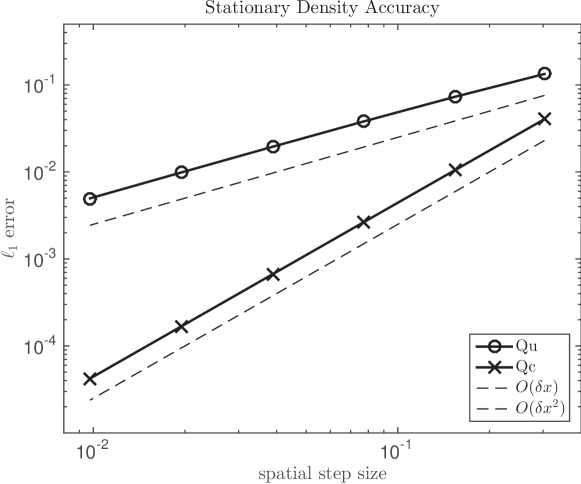

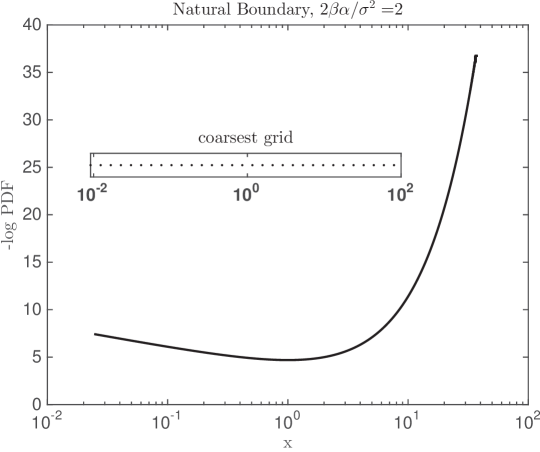

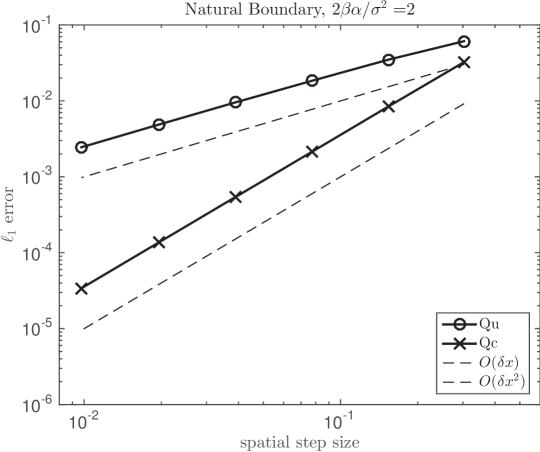

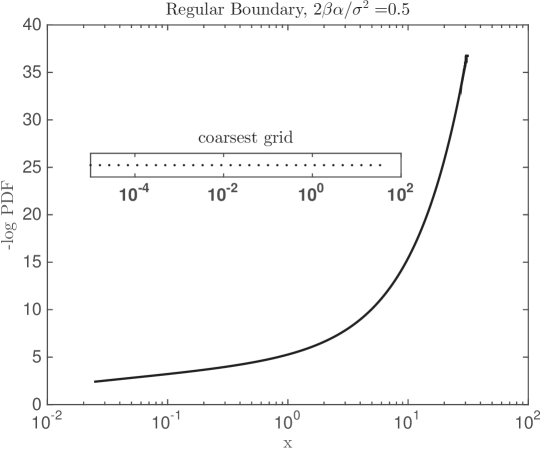

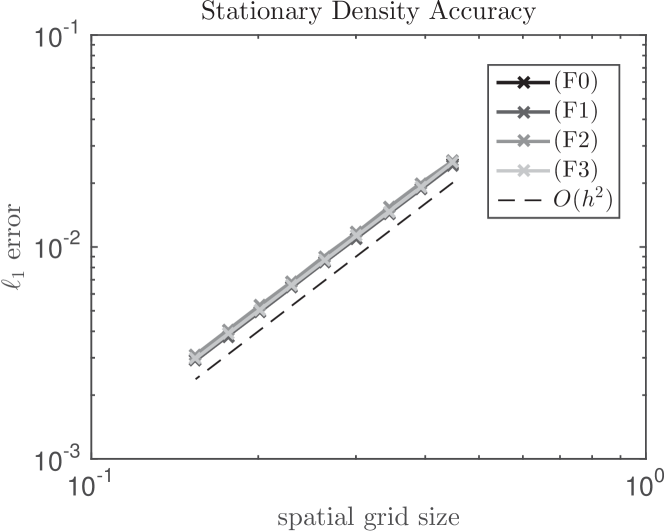

where the constant is chosen so that . Figures 3.9 and 3.10 illustrate the results of using adaptive mesh refinement. The top panels of Figures 3.9 and 3.10 plot the free energy of the stationary density when the boundary at zero is natural and regular, respectively. The benchmark solution is the cell-averaged stationary density (3.6.2) on the adaptive mesh shown in the inset. Note that when the boundary at zero is natural, the minimum of the free energy of the stationary density is centered away from zero. In contrast, when the boundary is regular, the minimum of the free energy is attained at the grid point closest to zero. The bottom panels of Figures 3.9 and 3.10 plot the error in the numerical stationary densities as a function of the mesh size in logspace . These numerical results confirm the theoretically expected rates of convergence when the mesh size is variable.

3.7. SDEs in 2D with Additive Noise

The examples in this part are two-dimensional SDEs of the form

| (3.7.1) |

where is a potential energy function (which will vary for each example), is the inverse ‘temperature’, and is one of the following flow fields:

| (3.7.2) |

where is a flow strength parameter. In the flow-free case () and in the examples we consider, the generator of the SDE in (3.7.1) is self-adjoint with respect to the probability density:

Moreover, the process is reversible [47]. Realizable discretizations have been developed for such diffusions with additive noise in arbitrary dimensions, see [104, 85]. With flow (), however, the generator is no longer self-adjoint, the equilibrium probability current is nonzero, and the stationary density of this SDE is no longer , and in fact, is not explicitly known. In this context we will assess how well the second-order accurate generator in (2.4.7) reproduces the spectrum of the infinitesimal generator of the SDE . Since the noise is additive, the state space of the approximation given by is a grid over . Moreover, this generator can be represented as an infinite-dimensional matrix. In order to use sparse matrix eigensolvers to compute eigenvalues of largest real part and the leading left eigenfunction of , we will approximate this infinite-dimensional matrix using a finite-dimensional matrix. For this purpose, we truncate the grid as discussed next.

Remark 3.7.1 (Pruned Grid).

Let be the set of all grid points and consider the magnitude of the drift field evaluated at these grid points: . In order to truncate the infinite-dimensional matrix associated to , grid points at which the magnitude of the drift field is above a critical value are pruned from the grid, and the jump rates to these grid points are set equal to zero. The price of this type of truncation is an unstructured grid that requires using an additional data structure to store a list of neighbors to each unpruned grid point. To control errors introduced in this pruning, we verify that computed quantities do not depend on the parameter .

Remark 3.7.2 (Error Estimates).

In the linear context, we compare to the exact analytical solution. In the nonlinear context, and in the absence of an analytical solution, we measure error relative to a converged numerical solution.

3.7.1. Planar, Asymmetric Ornstein-Uhlenbeck Process

Consider (3.7.1) with the following two dimensional potential energy:

| (3.7.3) |

and the linear flows defined in (3.7.2). We will use this test problem to assess the accuracy of the generator in representing the spectrum of .

In the linear context (3.7.1) with , the SDE (3.7.1) can be written as:

| (3.7.4) |

where is a matrix. The associated generator is a two-dimensional, non-symmetric Ornstein-Uhlenbeck operator. Let and denote the eigenvalues of the matrix . If and , then admits a unique Gaussian stationary density [61, See Section 4.8], and in addition, the spectrum of in (for ) is given by:

| (3.7.5) |

The original statement and proof of (3.7.5) in arbitrary, but finite, dimension can be found in [102]. This result serves as a benchmark for the approximation. In the numerical tests, we select the flow rate to be , which ensures that the eigenvalues of the matrix have strictly negative real parts for each of the linear flow fields considered.

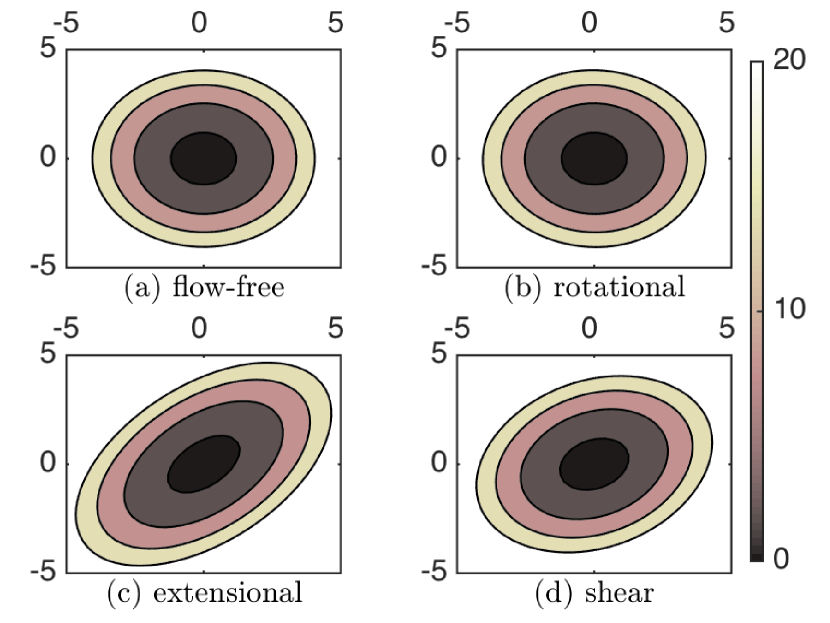

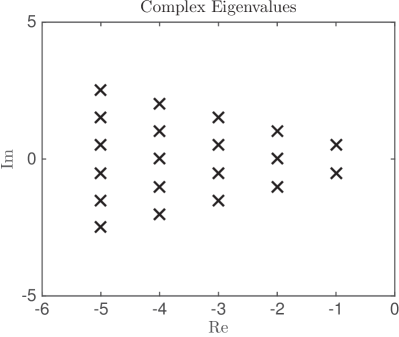

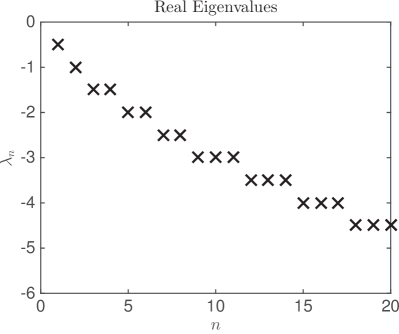

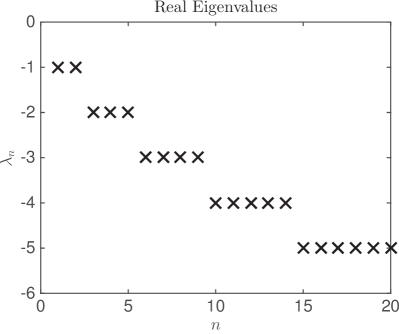

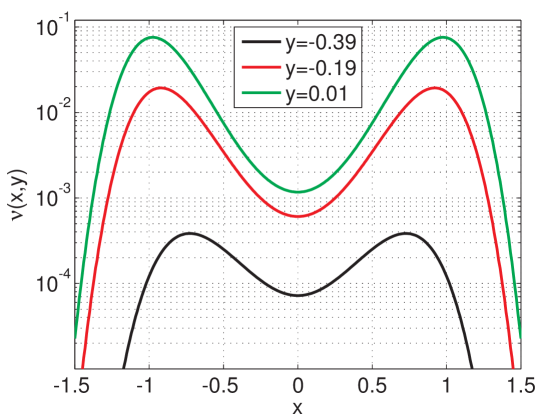

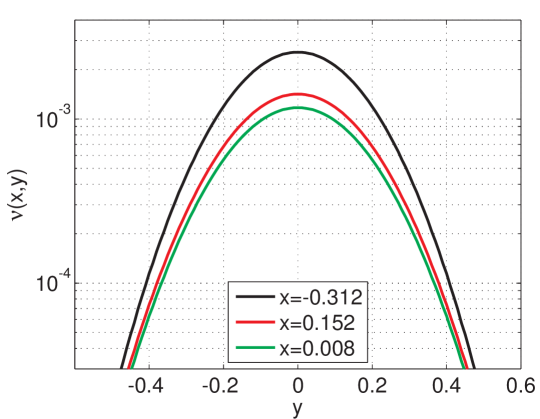

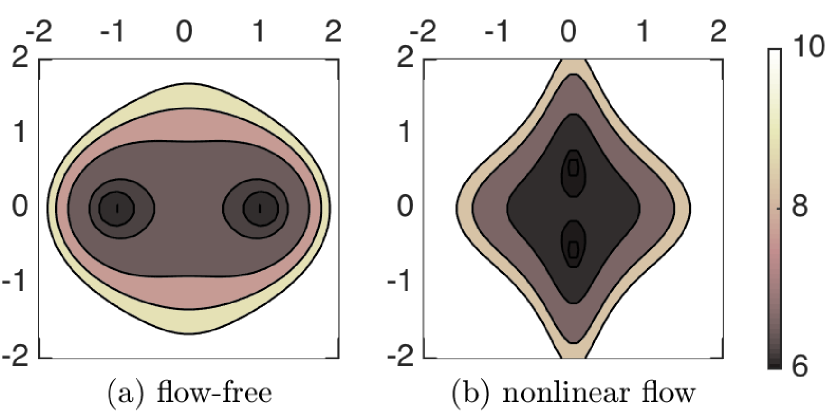

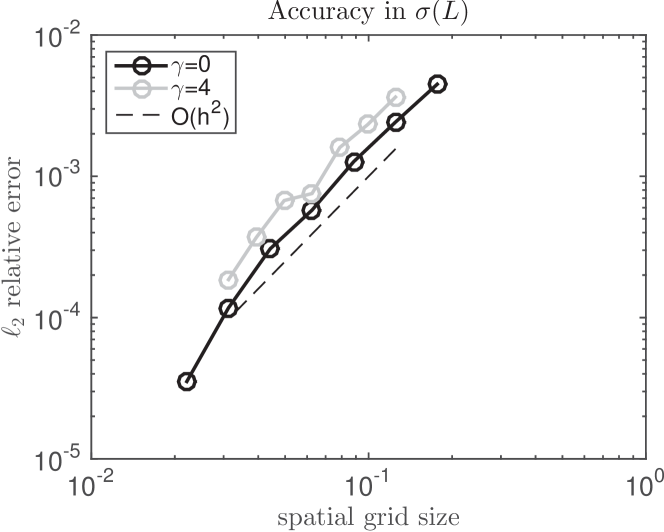

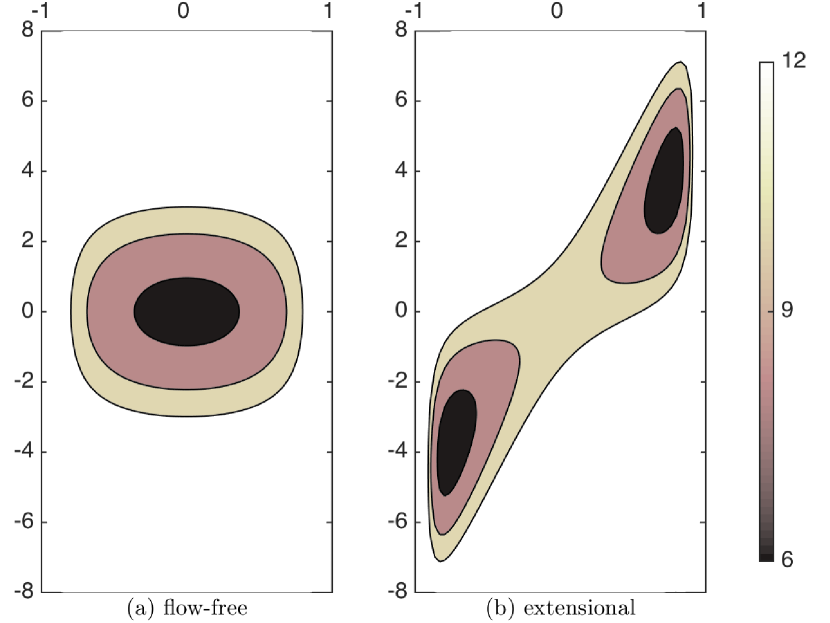

Figure 3.11 plots contours of the free energy of the numerical stationary density at for the linear flow fields considered. At this spatial step, the error in the stationary densities shown is about . Figure 3.12 plots the difference between the numerical and exact stationary densities. Figure 3.13 plots the first twenty eigenvalues of as predicted by (3.7.5). Figure 3.14 plots the relative error between the twenty eigenvalues of largest real part of and . The eigenvalues of are obtained from (3.7.5), and the eigenvalues of are obtained from using a sparse matrix eigensolver and the truncation of described in Remark 3.7.1. This last figure suggests that the accuracy of in representing the spectrum of is, in general, first-order.

(a) flow-free (b) rotational

(c) extensional (d) shear

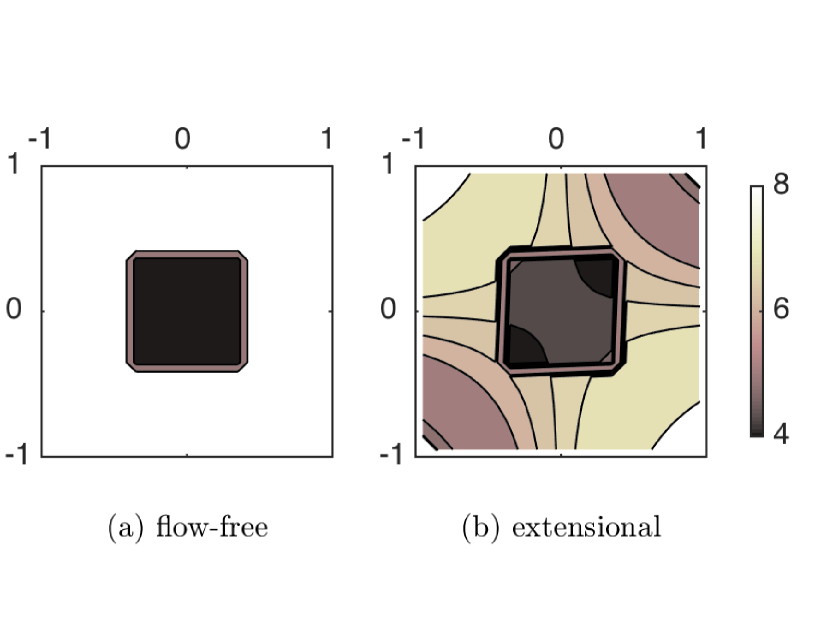

3.7.2. Maier-Stein SDE: Locally Lipschitz Drift & Nonlinear Flow

The Maier-Stein system is governed by an SDE of the form (3.7.1) with , the nonlinear flow field in (3.7.2), , and

| (3.7.6) |