Scalar conservation laws with monotone pure-jump Markov initial conditions

Abstract.

In 2010 Menon and Srinivasan published a conjecture for the statistical structure of solutions to scalar conservation laws with certain Markov initial conditions, proposing a kinetic equation that should suffice to describe as a stochastic process in with fixed. In this article we verify an analogue of the conjecture for initial conditions which are bounded, monotone, and piecewise constant. Our argument uses a particle system representation of over for , with a suitable random boundary condition at .

Key words and phrases:

Scalar conservation laws, random initial data, Markov jump processes2010 Mathematics Subject Classification:

Primary 60K35; Secondary 35L65, 60J25, 60J751. Introduction

We are interested in the statistical properties of solutions to the Cauchy problem for the scalar conservation law

| (1.1) |

where is a stochastic process. In the special case

| (1.2) |

(1.1) is the well-known inviscid Burgers’ equation, which has often been considered with random initial data. Burgers himself, in his investigation of turbulence [8], was already moving in this direction, though it would be some time before problems in this area were addressed rigorously.

Several papers, including [9, 10, 11, 27, 4, 5], have developed a theory showing a kind of integrability for the evolution of the law of for certain initial data. This article is concerned with pushing stochastic integrability results beyond the Burgers setting to general scalar conservation laws, an effort begun in earnest by Menon and Srinivasan [25, 22]. Before stating our main result, we first survey the major developments in this subject.

This work is adapted from [19].

1.1. Background

The Burgers case has seen extensive interest. Recall that if

| (1.3) |

then formally satisfies

| (1.4) |

and is determined by the Hopf-Lax formula [17]:

| (1.5) |

The backward Lagrangian is the rightmost minimizer in (1.5), and it is standard [13] that this determines both the viscosity solution to (1.4) and the entropy solution to ,

| (1.6) |

Groeneboom, in a paper [15] concerned not with PDE but concave majorants111Straightforward manipulations of (1.5) relate this to a Legendre transform. and isotonic estimators, determined the statistics of for the case where is white noise, which we understand to mean that the initial condition for in (1.4) is a standard Brownian motion . Among the results of [15] is a density for

| (1.7) |

expressed in terms of the Airy function. It has been observed (see e.g. [21]) that the Airy function seems to arise in a surprising number of seemingly unrelated stochastic problems, and it is notable that Burgers’ equation falls in this class.

Several key papers appeared in the 1990s; we rely on the introduction of Chabanol and Duchon’s 2004 paper [11], which recounts some of this history, and discuss those portions most relevant for our present purposes. In 1992, Sinai [27] explicitly connected Burgers’ equation with white noise initial data to convex minorants of Brownian motion. Three years later Avellaneda and E [3] showed for the same initial data that the solution is a Markov process in for each fixed .

Carraro and Duchon’s 1994 paper [9] defined a notion of statistical solution to Burgers’ equation. This is a time-indexed family of probability measures on a function space, and the definition of solution is stated in terms of the characteristic functional

| (1.8) |

for test functions . Namely, must satisfy for each a differential equation obtained by formal differentiation under the assumption that distributed according to solves Burgers’ equation. This statistical solution approach was further developed in 1998 by the same authors [10] and by Chabanol and Duchon [11]. It does have a drawback: given a (random) entropy solution to the inviscid Burgers’ equation, the law of is a statistical solution, but it is not clear that a statistical solution yields a entropy solution, and at least one example is known [4] when these notions differ. Nonetheless, [9, 10] realized that it was natural to consider Lévy process initial data, which set the stage for the next development.

In 1998, Bertoin [4] proved a remarkable closure theorem for Lévy initial data. We quote this, with adjustments to match our notation.

Theorem 1.1 ([4, Theorem 2]).

Consider Burgers’ equation with initial data which is a Lévy process without positive jumps for , and for . Assume that the expected value of is positive, . Then, for each fixed , the backward Lagrangian has the property that

| (1.9) |

is independent of and is in the parameter a subordinator, i.e. a nondecreasing Lévy process. Its distribution is the same as that of the first passage process

| (1.10) |

Further, denoting by and the Laplace exponents of and ,

| (1.11) | ||||

| (1.12) |

we have the functional identity

| (1.13) |

Remark.

The requirement can be relaxed, with minor modifications to the theorem, in light of the following elementary fact. Suppose that and are two different initial conditions for Burgers’ equation, which are related by . It is easily checked using (1.5) that the corresponding solutions and are related for by

| (1.14) |

This observation is found in a paper of Menon and Pego [24], but (as this is elementary) it may have been known previously. Using (1.14) we can adjust a statistical description for a case where to cover the case of a Lévy process with general mean drift.

We find Theorem 1.1 remarkable for several reasons. First, in light of (1.6), it follows immediately that the solution is for each fixed a Lévy process in the parameter , and we have an example of an infinite-dimensional, nonlinear dynamical system (the PDE, Burgers’ equation) which preserves the independence and homogeneity properties of its random initial configuration. Second, the distributional characterization of is that of a first passage process, where the definition of following (1.5) is that of a last passage process. Third, (1.13) can be used to show [23] that if is the Laplace exponent of , then

| (1.15) |

for and with nonnegative real part. This shows for entropy solutions what had previously been observed by Carraro and Duchon for statistical solutions [10], namely that the Laplace exponent (1.12) evolves according to Burgers’ equation!

In 2007 Menon and Pego [24] used the Lévy-Khintchine representation for the Laplace exponent (1.12) and observed that the evolution according to Burgers’ equation in (1.15) corresponds to a Smoluchowski coagulation equation [28, 2], with additive collision kernel, for the jump measure of the Lévy process . The jumps of correspond to shocks in the solution . The relative velocity of successive shocks can be written as a sum of two functions, one depending on the positions of the shocks and the other proportional to the sum of the sizes of the jumps in . Regarding the sizes of the jumps as the usual masses in the Smoluchowski equation, it is plausible that Smoluchowski equation with additive kernel should be relevant, and [24] provides the details that verify this.

It is natural to wonder whether this evolution through Markov processes with simple statistical descriptions is a miracle [23] confined to the Burgers-Lévy case, or an instance of a more general phenomenon. However, extending the results of Bertoin [4] beyond the Burgers case remains a challenge. A different particular case, corresponding to , is a problem of determining Lipschitz minorants, and has been investigated by Abramson and Evans [1]. From the PDE perspective this is not as natural, since corresponds to

| (1.16) |

i.e. takes the value on and is equal to elsewhere. So [1], while very interesting from a stochastic processes perspective, has a specialized structure which is rather different from those cases we will consider.

The biggest step toward understanding the problem for a wide class of is found in a 2010 paper of Menon and Srinivasan [25]. Here it is shown that when the initial condition is a spectrally negative222i.e. without positive jumps strong Markov process, the backward Lagrangian process and the solution remain Markov for fixed , the latter again being spectrally negative. The argument is adapted from that of [4] and both [4, 25] use the notion of splitting times (due to Getoor [14]) to verify the Markov property according to its bare definition. In the Burgers-Lévy case, the independence and homogeneity of the increments can be shown to survive, from which additional regularity is immediate using standard results about Lévy processes [18]. As [25] points out, without these properties it is not clear whether a Feller process initial condition leads to a Feller process in at later times. Nonetheless, [25] presents a very interesting conjecture for the evolution of the generator of , which has a remarkably nice form and follows from multiple (nonrigorous, but persuasive) calculations.

We now give a partial statement of this conjecture. The generator of a stationary, spectrally negative Feller process acts on test functions by

| (1.17) |

where characterizes the drift and describes the law of the jumps. If we allow and to depend on , we have a family of generators. The conjecture of [25] is that the evolution of the generator for is given by the Lax equation

| (1.18) |

for which acts on test functions by

| (1.19) |

An equivalent form of the conjecture (1.18) involves a kinetic equation for . The key result in the present article verifies that this kinetic equation holds in the special case we will consider. Before we state this, let us establish our working notation.

1.2. Notation

Here we collect some of the various notation used later in the article.

Write for the divided difference of through . For each this function is symmetric in its arguments, and given by the following formulas in the cases and where are distinct:

| (1.20) |

The definition for general and standard properties can be found in several numerical analysis texts, including [16].

We write for the usual point mass assigning unit mass to and zero elsewhere.

For and a positive integer, write

| (1.21) |

and for the closure of this set in . We write for the boundary of the simplex, and for its various faces:

| (1.22) | ||||

Write for the set of finite, regular (signed) measures on , which is a Banach space when equipped with the total variation norm . Call its nonnegative subset .

Let denote the set of bounded signed kernels from to , i.e. the set of which are measurable when is endowed with its Borel -algebra and is endowed with the -algebra generated by evaluation on Borel subsets of , and which satisfy

| (1.23) |

Observe that is a Banach space; completeness holds since a Cauchy sequence has Cauchy in total variation for each , and we obtain a pointwise limit . Measurability of for each Borel then holds since this is a real-valued pointwise limit of . Write for the subset of with range contained in .

1.3. Main result

In this section we provide a statistical description of solutions to the scalar conservation law when the initial condition is an increasing, pure-jump Markov process given by a rate kernel . For this we require some assumptions on the rate kernel and the Hamiltonian .

Assumption 1.2.

The initial condition is a pure-jump Markov process starting at and evolving for according to a rate kernel . We assume that for some constant the kernel is supported on

| (1.24) |

and has total rate which is constant in :

| (1.25) |

for all . In particular, .

Assumption 1.3.

The Hamiltonian function is smooth, convex, has nonnegative right-derivative at and noninfinite left-derivative at .

We provide for a statistical description consisting of a one-dimensional marginal at and a rate kernel generating the rest of the path. The evolution of the rate kernel is given by the following kinetic equation, and the evolution of the marginal will be described in terms of the solution to the kinetic equation.

Definition 1.4.

We say that a continuous mapping is a solution of the kinetic equation

| (1.26) |

where

| (1.27) | ||||

provided that is Bochner-integrable and

| (1.28) |

for all .

Definition 1.5.

We say that a continuous mapping is a solution of the marginal equation

| (1.29) |

where

| (1.30) |

provided that is Bochner-integrable and

| (1.31) |

for all .

Theorem 1.6.

The kernels described by the Theorem 1.6 are precisely what we need to describe the statistics of the solution , which brings us to our main result:

Theorem 1.7.

Remark.

Theorems 1.6 and 1.7 establish rigorously the conjectured [25] evolution according to the Lax pair (1.18), within the present hypotheses. See [25, Section 2.7] for a calculation showing the equivalence of the kinetic and Lax pair formulations, which simplifies considerably in the present case due to the absence of drift terms. The Lax pair and integrable systems approach (in the case of finitely many states, where the generator is a triangular matrix) have been further explored by Menon [22] and in a forthcoming work by Li [20].

1.4. Organization

The remainder of this article is organized as follows. In Section 2 we show that Theorem 1.7 will follow from a similar statistical characterization for the solution to the PDE over with a time-dependent random boundary condition at . The latter we can study using a sticky particle system whose dimension is random and unbounded, but almost surely finite. Elementary arguments are used to check that our candidate for the law matches the evolution of the random initial condition according to the dynamics. Next in Section 3 we show existence and uniqueness of the solutions to marginal and kinetic equations of Theorem 1.6, which are needed to construct the candidate law. The concluding Section 4 indicates some desired extensions and similar questions for future work. To keep the main development concise, proofs of lemmas have been deferred to Appendix A.

2. A random particle system

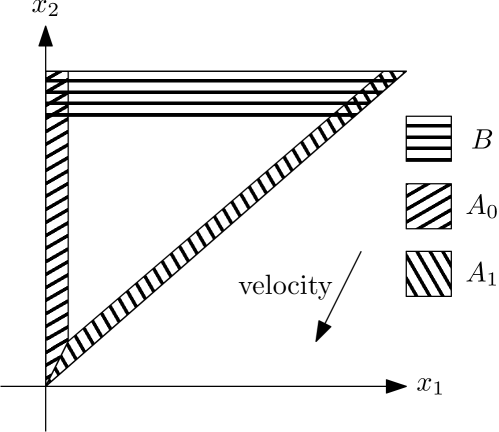

As functions of , the solutions we consider all have the form depicted in Figure 1. From a PDE perspective this situation is standard—a concatenation of Riemann problems for the scalar conservation law—and we can describe the solution completely in terms of a particle system. Each shock consists of some number of particles stuck together, and the particles move at constant velocities according to the Rankine-Hugoniot condition except when they collide. The collisions are totally inelastic.

The utility of this particle description is lessened, however, by the fact that the dynamics are quite infinite dimensional for our pure-jump initial condition , . To have a simple description as motion at constant velocities, punctuated by occasional collisions, we might argue that on each fixed bounded interval of space we have finitely many collisions in a bounded interval of time, and piece together whatever statistical descriptions we might obtain for the solution on these various intervals. Inspired by those situations in statistical mechanics where boundary conditions become irrelevant in an infinite-volume limit, we pursue a different approach. We construct solutions to a problem on a bounded space interval , and choose a random boundary condition at to obtain an exact match with the kinetic equations. The involved analysis will all pertain to the following result.

Theorem 2.1.

Suppose Assumptions 1.2 and 1.3 hold. For any fixed , consider the scalar conservation law

| (2.1) |

with initial condition (restricted to ), open boundary333Using Assumption 1.3 and , the shocks and characteristics only flow outward across . Any boundary condition we would assign, unless it involved negative values, would thus be irrelevant. at , and random boundary at . Suppose the process has and evolves according to the time-dependent rate kernel independently of given . Then for all the law of is as follows:

-

(i)

the marginal is , and

-

(ii)

the rest of the path is a pure-jump process with rate kernel .

To prove our main result we can send , applying Theorem 2.1 on each , and use bounded speed of propagation to limit the respective influences of far away particles (unbounded system) or truncation with random boundary (bounded system). The argument is quite short.

Proof of Theorem 1.7.

Fix any . We will write for the solution to (1.35) over the semi-infinite -interval with initial data . We take the right-continuous version of the solution. For to be specified shortly, write for the solution and for the initial data corresponding to (2.1).

Fix any , and let . Choose . We couple the bounded and unbounded systems by requiring

| (2.2) |

allowing the random boundary to evolve independently of given

Recall [13] that the scalar conservation law has finite speed of propagation. Our solutions are bounded in , so the speed is bounded by . Since and are a.s. equal on , we have also a.s. for . From this we deduce the distributional equality

| (2.3) |

By Theorem 2.1, the latter distribution is exactly that of a process started according to , evolving according to rate kernel . This process is terminated deterministically at , which does not alter finite-dimensional distributions prior to . Since is right-continuous and has the correct finite-dimensional distributions, the result follows. ∎

2.1. The dynamics

Our work in the remainder of this section is to prove Theorem 2.1. We begin by describing precisely those particle dynamics which determine the solution to the PDE.

Figure 1 illustrates a parametrization of a nondecreasing pure-jump process on with heights and jump locations . Our sign restriction on the jumps excludes rarefaction waves, and we have only constant values separated by shocks. Going forward in time, the shocks move according to the Rankine-Hugoniot condition

| (2.4) |

until they collide. We say that each shock consists initially of one particle moving at the velocity indicated above. Then result of a collision can be characterized in two equivalent ways:

-

(i)

At the first instant when , the particle is annihilated, and the velocity of the particle changes from to

(2.5) In the case444which will almost surely not occur for the randomness we consider where several consecutive particles collide with each other at the same instant, all but the rightmost particle is annihilated. Since we only seek a statistical description for , we annihilate the first particle when , replace with , and relabel the other particles accordingly.

- (ii)

We adopt the first viewpoint for convenience, as this is compatible with [12] (see the text following Definition 2.3 below), but a suitable argument could be given for the second alternative as well.

Definition 2.2.

For as in Theorem 2.1, the configuration space for the sticky particle dynamics is

| (2.6) |

A typical configuration is when , or when .

Definition 2.3.

Our notation for the particle dynamics is as follows:

-

(i)

For and , write

(2.7) for the deterministic evolution from time to of the configuration according to the annihilating particle dynamics for the PDE, without random entry dynamics at .

-

(ii)

Given a configuration and , write for the configuration .

-

(iii)

Write for the random evolution of the configuration according to deterministic particle dynamics interrupted with random entries at according to the boundary process of (2.1), where the latter has been started at time with value . In particular, if the jumps of between times and occur at times with values , then

(2.8)

Proposition 2.4.

For any , the process is strong Markov.

This assertion follows after recognizing as a piecewise-deterministic Markov process described in some generality by Davis [12]. Namely, we augment the configuration space to add the time parameter to each component , and then have a deterministic flow according to the vector field

| (2.9) |

With rate we jump to the indicated point in , and upon hitting a boundary we transition to for suitable , annihilating particles in the manner described above.

2.2. Checking the candidate measure

Our goal is to take distributed according to the initial condition and exactly describe the law of for each . Using the kinetic (1.27) and marginal equations (1.30), we construct for each time a candidate law on as follows. Take to be Poisson with rate , uniform on , and distributed on according to the marginal and transitions independently of the :

| (2.10) |

where and

| (2.11) |

for . When we have verified (1.32), it will be immediate that the total mass of this is one.

We decompose the mapping from configurations to solutions (as functions of over ) into the map from to the measure

| (2.12) |

and integration over . We claim that when is distributed according to , the law of the measure is identical to that of where is distributed according to .

We now describe the structure of the proof of Theorem 2.1. Fix some time and consider where takes the form of a Laplace functional:

| (2.13) |

for a continuous function on . We aim to show that

| (2.14) |

for , from which it will follow that

| (2.15) |

for all of the form in (2.13). Using the standard fact that Laplace functionals completely determine the law of any random measure [18], this will suffice to show that law of for distributed as is precisely the pushforward through of , and obtain the result.

We might verify (2.14) by establishing regularity for in and the -components of . We speculate that it should be possible to do so if is smooth with and we content ourselves to divide the configuration space into finitely many regions, each of which corresponds to a definite order of deterministic collisions in . On the other hand, the measures enjoy considerable regularity (uniformity, in fact) in , and we pursue instead an argument along these lines. Here continuity of in will suffice.

Lemma 2.5.

Let take the form of (2.13). Then is a bounded function which is uniformly continuous in uniformly in :

| (2.16) |

as .

To differentiate in (2.14) we will need to compare and for . Our next observation is that when the is small, we can separate the deterministic and stochastic portions of the dynamics over the time interval . The idea is that in an interval of time , the probability of multiple particle entries is , and a single particle entry has probability which permits additional errors.

Lemma 2.6.

Let and . There exist a random variable a.s., with law depending on and only through , and a constant independent of so that

| (2.17) |

We proceed to an analysis of the deterministic portion of the flow, , where is distributed according to . For this we introduce some notation. Given , we write

| (2.18) |

For each fixed , we consider several subsets of the set of -particle configurations . In particular we need to separate those configurations which experience an exit at or a collision in a time interval shorter than . For , write:

| (2.19) | ||||

Figure 2 illustrates these sets in the case . We observe in particular that and differ by a -null set, and that the terms associated with the boundary faces are related to configurations with one fewer particle.

Lemma 2.7.

For each positive integer and with errors bounded by

| (2.20) |

we have the following approximations:

| (2.21) | ||||

| (2.22) | ||||

| for , and | ||||

| (2.23) | ||||

Remark.

It is essential that the integral over can be approximated by an integral over . The measure below does not have any singular factors like . In particular, the result of integrating over will partially cancel with the term arising from random particle entries.

The final ingredient for the proof of Theorem 2.1 is the time derivative of , which we now record.

Lemma 2.8.

For any and any we have

| (2.24) |

where the norm is total variation and is defined to be the signed kernel

| (2.25) |

The expression for the measure above is to be understood formally; the correct interpretation involves replacement, not division. All of the “divisors” above are present as factors of , and the fractions indicate that the appearance of the denominator in this portion is to be replaced with the indicated numerator.

So that we know what to expect, before proceeding we note that when we sum over in (2.25), some of the terms arising from and cancel. Namely, the bracketed portion of (2.25) expands as

| (2.26) | ||||

The gain terms associated with the kinetic equations we leave as they are, but note that the “loss” terms telescope, and the above may be shortened to

| (2.27) |

We are ready to prove our statistical characterization of the bounded system.

Proof of Theorem 2.1.

For times and with , consider the difference :

| (2.28) |

Since is uniformly continuous in uniformly in by Lemma 2.5 and is a probability measure, (I) as . Using Lemma 2.8 and the fact that , (II) as , and in fact

| (2.29) |

as with fixed. Using both Lemmas 2.5 and 2.8, we see (III) is . Thus is continuous in ; we will show additionally that it is differentiable from below in with one-sided derivative equal to for all . In light of (2.29), our task is to show that approximates (I) up to an error.

Using Lemma 2.6 we have the following approximation of the portion of (I) involving , with error bounded by :

| (2.30) | ||||

We have because the deterministic flow maps to (modulo lower-dimensional sets) and preserve the Lebesgue measure in spatial coordinates. Making replacements using Lemma 2.7 and reordering the terms, we find with an error bounded by that

| (2.31) | ||||

for positive integers . In the case , we have , and the approximation is

| (2.32) |

We observe that the bracketed portion of (2.31) nearly matches (2.27), except that part involves and part involves . Furthermore, we have

| (2.33) | ||||

This follows since is conditionally independent of given , and a.s. so that all but volume of the -simplex is simply translated by to a region of identical volume. We make the replacement indicated by (2.33) in (2.31) without changing the form of the error.

For any positive integer we define

| (2.34) |

Summing (2.31), (2.32), and our approximation for from (2.27) gives

| (2.35) | ||||

with an error. Call the right side , so that the left derivative of is . Since is a Lipschitz function, we deduce

| (2.36) |

We have bounded uniformly in by

| (2.37) |

and thus uniformly in . It follows that

| (2.38) |

as . Recognizing the limits of and as

| (2.39) |

respectively, we have verified (2.14) and completed the proof. ∎

Having shown the candidate measure constructed using the solutions and given by Theorem 1.6, our next task is to verify the latter, which we undertake in the next section.

3. The kinetic and marginal equation

The primary goal of the present section is to prove Theorem 1.6 concerning the kernel and marginal , so that the candidate measure in the previous section is well-defined and has the properties required for the argument there.

While we introduce our notation, we also discuss the intuitive meaning of the terms of our kinetic equation, comparing with that of Menon and Srinivasan [25]. Let us write for the operator on given by the right-hand side of (1.27),

| (3.1) | ||||

so that the kinetic equation is .

The first term, which we call the gain term, corresponds to the production of a shock connecting states and by means of collision of shocks connecting states and . Such shocks have relative velocity given by

| (3.2) |

In the Burgers case, the second divided difference is constant, and the above is proportional to the sum of the increment , analogous to mass in the Smoluchowski equation.

The second line of (3.1) we call the “loss” term, though this need not be of definite sign. To better understand this, note that when we have proven Theorem 1.6, we will know that has total mass which is constant in . In this case the loss term may be rewritten equivalently as

| (3.3) |

which corresponds precisely with the kinetic equation of [25]. The meaning of the first line of (3.3) is clear: we lose a shock connecting states when a shock connecting collides with this, and the relative velocity is precisely .

The second line of (3.3) is less easily understood. One would expect to find here a loss related to a shock connecting colliding with for , particularly if we were viewing as a jump density as [25] views its corresponding . Viewed as a rate kernel, it is not clear that should suffer such a loss: in some sense we must condition on being in state for to be relevant at all. At this point we cannot offer an intuitive kinetic reason for the second line of (3.3), but in light of the rigorous results of this article we can be assured that this is correct for our model.

Remark.

The form (3.3) seems preferable in the more generic setting, since—as pointed out by the referee—the resulting equation has the property that

| (3.4) |

is (formally) conserved in time for each , without assuming that is constant. This observation will be important in attempts to generalize the results of the present paper.

We return to the task at hand, showing existence and uniqueness of . The argument proceeds through an approximation scheme for , where we can easily maintain positivity. To avoid endowing with a weak topology, we show directly the approximations are Cauchy, rather than appealing to Arzela-Ascoli.

Proof of Theorem 1.6, part I.

Write and consider for each positive integer the continuous paths defined by for all and

| (3.5) |

We claim the following properties of :

-

(a)

for all ,

-

(b)

for each the total integral is constant in ,

-

(c)

for all

(3.6) and

-

(d)

for all and all .

Since is piecewise-linear in and the properties above are preserved by convex combinations, it suffices to verify this at for all integers .

We proceed by induction. Abbreviate . The case holds by the hypotheses on . Assume now that the claim holds for , and consider . We have

| (3.7) | ||||

In particular, for any we have

| (3.8) | ||||

using property (c) for case ; thus . This and (a) give , property (a) for case . Furthermore, the total integral of the right-hand side of (3.7) is exactly

| (3.9) |

since (b) implies the bracketed portion integrates to . Also using (b) for case , the change in the total integral from to is independent of , verifying (b) for case . Using (c) for case we find

| (3.10) |

so that (c) holds for case . Finally, we observe that property (d) for implies

| (3.11) |

and thus (d) holds for case .

We now consider the matter of convergence. Pairing with any and measurable with , we find that

| (3.12) |

In particular is Lipschitz on bounded sets in . For brevity write

| (3.13) |

We compute for any and

| (3.14) |

Observe that

| (3.15) | ||||

where

| (3.16) | ||||

We have also

| (3.17) | ||||

Combining these, there is a constant so that

| (3.18) |

for all positive integers and times .

The remaining term in the integrand of (3.14) is

| (3.19) | ||||

All together,

| (3.20) |

and by Gronwall

| (3.21) |

From this we see that is Cauchy, hence convergent to a continuous satisfying

| (3.22) |

for all , having properties (a,b,d) above and .

We define , finding that

-

•

is continuous;

-

•

is continuous (using the local Lipschitz property of ), and hence Bochner-integrable; and

-

•

with by Leibniz.

Using the local Lipschitz property of , the solution is unique. Properties (a,b,d) above hold for , and (b) in particular gives for each fixed

| (3.23) |

Thus for all , . ∎

We now turn to , which is intended to serve as the marginal at for our solution for fixed . We define a time-dependent family of operators acting on measures in by

| (3.24) |

Again the integration is over only, and for each we have . Our evolution equation for is the linear, time-inhomogeneous .

Proof of Theorem 1.6, part II.

Note that (3.24) is exactly the forward equation for a pure-jump Markov process evolving according to a time-varying rate kernel

| (3.25) |

so we could obtain existence and uniqueness of solutions along these lines. We outline an argument similar to that employed for , for the sake of completeness.

Define for each the continuous path with and

| (3.26) |

Proceeding as in the proof for we verify that for each the are nonnegative and, since has total integral zero, . Observing that is linear and bounded uniformly over ,

| (3.27) |

we easily show is Cauchy on bounded time intervals, with limit satisfying

| (3.28) |

Take to find that solves

| (3.29) |

Uniqueness follows using (3.27). Finally, since as zero total integral for any , we find that for all . ∎

We close this section with a remark concerning the kinetic equation without the assumption that the initial kernel has bounded support . When the initial condition is unbounded, growing for example linearly in the case of quadratic , the solution to the scalar conservation law on the semi-infinite domain should blow up in finite time. We likewise expect that the solution to the kinetic equation will blow up, but control of certain moments prior to this blow up may allow us to run the argument of Theorem 2.1 with only superficial changes. At the moment we lack the sort of estimates one obtains in the Smoluchowski case (e.g. coming from a closed equation for the second moment), but we hope to revisit this in future work.

4. Conclusion

We review what has been accomplished: using an exact propagation of chaos calculation for a bounded system with a suitably selected random boundary condition, we have derived a complete description of the law of the solution to the scalar conservation law for when is a bounded, monotone, pure-jump Markov process with constant jump rate. Notably, we have recovered the Markov property of the solution and a statistical description of the shocks simultaneously. This may be regarded as both a strength of our present analysis and a shortcoming of our present understanding (a soft argument for the preservation of the Markov property in the particle system would be illuminating).

We emphasize how our approach using random dynamics on a bounded interval has made things considerably easier: by constructing a bounded system which has exactly the right law, we are relieved of the burden of determining precisely how wrong the law would be with deterministic boundary.

Our result lends additional support to the conjecture of Menon and Srinivasan [25] and we hope that the sticky particle methods described herein will provide another approach, quite different from that of Bertoin [4], which might be adapted to resolve the full conjecture. One of the authors is attempting a similar particle approach in the non-monotone setting, and hopes to report on this in future work.

Acknowledgments

The authors thank the anonymous referee for suggestions improving our presentation and for pointing out a recent reference.

Appendix A Proofs of lemmas

Proof of Lemma 2.5.

Boundedness of is obvious from its definition as a Laplace functional. For continuity, we begin by considering with fixed. As varies, varies continuously, with -values unchanging and -values changing with rate bounded by , except for finitely many times when collisions occur. Note depends on via , and the former varies continuously across these collision times. More concretely, because , is uniformly continuous, and so

| (A.1) |

has the property that as . Using the above,

| (A.2) |

Since the exponential is uniformly continuous for nonpositive arguments, we find that is continuous at uniformly in . Write

| (A.3) |

and observe that and .

Suppose now that ; we compare and . Write . We have a.s., coupling the random entry processes on matching intervals. Then

| (A.4) |

because the random entries occur at a rate bounded by and . Using the time homogeneity and continuity for the deterministic flow,

| (A.5) |

So, at the cost of an error bounded by , we compare with instead. Now the configuration is flowed on time intervals of equal length, but with random entry rates that have been shifted in time.

The random entry rate is given by and is TV-continuous in ; we have

| (A.6) | ||||

Let us define three kernels for according to

| (A.7) | ||||

where the minimum () of two measures is defined as usual by choosing a third measure with which the former two are absolutely continuous, and taking the pointwise minimum of their Radon-Nikodym derivatives. That this extends measurably to the parametric case (i.e. involving kernels) is immediate from a parametric version of the Radon-Nikodym theorem [26, Theorem 2.3].

Using the above we construct a coupled random entry process for times , namely let be the pure-jump Markov process started at from and evolving according to the generator acting on bounded measurable functions defined on according to

| (A.8) | ||||

Taking which does not depend on we find that for has the same law as the random boundary for , and likewise taking which does not depend on we find the has the same law as the random boundary for , verifying the coupling.

On the diagonal , the rate at which causes jumps that leave the diagonal (the second and third lines of (A.8)) is bounded by

| (A.9) |

and the probability that such a transition never occurs in a time interval of length is bounded below by

| (A.10) |

So, coupling the random entry dynamics, we find that with probability at least . Putting the above pieces together, we find

| (A.11) |

and the proof is complete. ∎

Proof of Lemma 2.6.

Using the Markov property of the random flow , we have a functional identity:

| (A.12) |

Let be fixed, and consider the following events, whose union is of full measure for computing the final expectation above:

| (A.13) | ||||

Observe that on we see only the deterministic flow over the time interval :

| (A.14) |

and this occurs with probability

| (A.15) |

We prefer an expression evaluating at only a single time, and Taylor expand the exponential around zero.

| (A.16) |

so that

| (A.17) |

and by exhaustion

| (A.18) |

with both errors bounded uniformly over . On write for the first time a random entry occurs for , and for the new boundary value, noting that the distribution of depends only on through and that the law of is determined by . We have so that

| (A.19) |

Using the strong Markov property for the random boundary at the stopping time ,

| (A.20) |

Since , we can afford to make modifications to this. Write for the modulus of continuity of in time, according to Lemma 2.5. Now a.s. on , so

| (A.21) |

Next we modify the distribution from which is selected; at present, is selected according to the random measure

| (A.22) |

Since a.s. on , the total variation difference

| (A.23) |

Let us write for an independent random variable distributed as

| (A.24) |

(note instead of ), normalized to have unit mass. Then

| (A.25) |

Note that cancels with the normalization in (A.22), up to an error, and that is independent of . With error bounded uniformly over by , we have

| (A.26) |

where the remaining expectation is now taken only over conditioned on , which is therefore distributed over . ∎

Proof of Lemma 2.7.

On any of , , we have . For such we have

| (A.27) |

The first absolute difference is the error induced by conditioning on zero particle entries on the interval , which costs less than . Lemma 2.5 bounds the second of these by . Using (A.27) we can replace the integrand over with , i.e. the projection of onto in the direction of the velocity.

Write for the velocities. We can integrate over using as a parametrization for the -variables

| (A.28) |

which has absolute Jacobian determinant . Namely,

| (A.29) | ||||

On all but a portion of with -volume bounded by we have , and we can extend the upper limit of integration to with and error bounded by this. Noting that the configurations

| (A.30) |

are equivalent under our sticky particle dynamics and relabeling, we obtain our approximation for the integral over .

The argument for , , is similar. We use the mapping

| (A.31) |

with absolute Jacobian determinant , and replace the upper limit of integration for with at the cost of an error. Relabeling gives the indicated approximation.

The range of

| (A.32) |

where , , and

| (A.33) |

is , modulo sets of lower -dimension. Using Lemma 2.5 we can replace by

| (A.34) |

with pointwise error over bounded by . For all but an portion of the -volume, the value is the minimum above, and as before we obtain the indicated approximation of the integral over . ∎

Proof of Lemma 2.8.

Essentially we are verifying the Leibniz rule, but we are unable to find a version of this to cite for kernels. We first obtain quantitative control over our linear approximations of and . Namely, fix any measurable . We have

| (A.35) |

The difference of at different times can be expressed in terms of and again,

| (A.36) | ||||

Noting that , we integrate over , then , and find that (A.35) is bounded by

| (A.37) |

Next, for any ,

| (A.38) |

and

| (A.39) | ||||

We have , so by integrating over and then we find (A.38) is bounded by

| (A.40) |

Returning to the problem of establishing our Leibniz rule, note that factors from both and . It will therefore suffice to obtain a bound on the portion.

We argue by induction. In the case , we have only the difference in (A.38), and the result holds. Now suppose that the result holds for case , and consider . Choose as a test function , which is measurable and has , and integrate it against

| (A.41) | ||||

For each , the function is bounded and measurable in , so can be replaced with

| (A.42) |

plus an error no larger than , which when integrated over the remaining variables grows by a factor .

In the third line of (A.41), noting is bounded and measurable in , we apply the inductive hypothesis, replacing the bracketed difference by

| (A.43) |

plus an error. After doing this, again noting is measurable in for each fixed , we replace with at a cost of , which gets multiplied by the other factor .

Adding the modified versions of these two lines of (A.41), we find exactly the portion of plus an error. ∎

References

- [1] Abramson, J., Evans, S.N.: Lipschitz minorants of brownian motion and lévy processes. Probability Theory and Related Fields (2013). DOI 10.1007/s00440-013-0497-9

- [2] Aldous, D.J.: Deterministic and stochastic models for coalescence (aggregation and coagulation): a review of the mean-field theory for probabilists. Bernoulli 5(1), 3–48 (1999). DOI 10.2307/3318611

- [3] Avellaneda, M., E, W.: Statistical properties of shocks in burgers turbulence. Communications in Mathematical Physics 172(1), 13–38 (1995). DOI 10.1007/BF02104509

- [4] Bertoin, J.: The inviscid burgers equation with brownian initial velocity. Communications in Mathematical Physics 193(2), 397–406 (1998). DOI 10.1007/s002200050334

- [5] Bertoin, J.: Clustering statistics for sticky particles with brownian initial velocity. Journal de Mathématiques Pures et Appliquées 79(2), 173 – 194 (2000). DOI http://dx.doi.org/10.1016/S0021-7824(00)00147-1

- [6] Brenier, Y., Gangbo, W., Savaré, G., Westdickenberg, M.: Sticky particle dynamics with interactions. J. Math. Pures Appl. (9) 99(5), 577–617 (2013). DOI 10.1016/j.matpur.2012.09.013

- [7] Brenier, Y., Grenier, E.: Sticky particles and scalar conservation laws. SIAM Journal on Numerical Analysis 35(6), 2317–2328 (1998). DOI 10.1137/S0036142997317353

- [8] Burgers, J.: A mathematics model illustrating the theory of turbulence. In: R. Von Mises, T. Von Karman (eds.) Advances in Applied Mechanics, v. 1, pp. 171–199. Elsevier Science (1948)

- [9] Carraro, L., Duchon, J.: Solutions statistiques intrinsèques de l’équation de Burgers et processus de Lévy. Comptes Rendus de l’Académie des Sciences. Série I. Mathématique 319(8), 855–858 (1994)

- [10] Carraro, L., Duchon, J.: Équation de burgers avec conditions initiales à accroissements indépendants et homogènes. Annales de l’Institut Henri Poincare (C) Non Linear Analysis 15(4), 431–458 (1998). DOI http://dx.doi.org/10.1016/S0294-1449(98)80030-9

- [11] Chabanol, M.L., Duchon, J.: Markovian solutions of inviscid burgers equation. Journal of Statistical Physics 114(1-2), 525–534 (2004). DOI 10.1023/B:JOSS.0000003120.32992.a9

- [12] Davis, M.H.A.: Piecewise-deterministic Markov processes: a general class of nondiffusion stochastic models. Journal of the Royal Statistical Society. Series B. Methodological 46(3), 353–388 (1984)

- [13] Evans, L.: Partial Differential Equations. Graduate studies in mathematics. American Mathematical Society (2010)

- [14] Getoor, R.: Splitting times and shift functionals. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete 47(1), 69–81 (1979). DOI 10.1007/BF00533252

- [15] Groeneboom, P.: Brownian motion with a parabolic drift and airy functions. Probability Theory and Related Fields 81(1), 79–109 (1989). DOI 10.1007/BF00343738

- [16] Hildebrand, F.B.: Introduction to numerical analysis, second edn. Dover Publications, Inc., New York (1987)

- [17] Hopf, E.: The partial differential equation . Communications on Pure and Applied Mathematics 3(3), 201–230 (1950). DOI 10.1002/cpa.3160030302

- [18] Kallenberg, O.: Foundations of modern probability, second edn. Probability and its Applications (New York). Springer-Verlag, New York (2002). DOI 10.1007/978-1-4757-4015-8

- [19] Kaspar, D.C.: Exactly solvable stochastic models in elastic structures and scalar conservation laws. Ph.D. thesis, University of California, Berkeley (2014)

- [20] Li, L.C.: A finite dimensional integrable system arising in the study of shock clustering (2015). Preprint

- [21] Majumdar, S.N., Comtet, A.: Airy distribution function: From the area under a brownian excursion to the maximal height of fluctuating interfaces. Journal of Statistical Physics 119(3-4), 777–826 (2005). DOI 10.1007/s10955-005-3022-4

- [22] Menon, G.: Complete integrability of shock clustering and burgers turbulence. Archive for Rational Mechanics and Analysis 203(3), 853–882 (2012). DOI 10.1007/s00205-011-0461-8

- [23] Menon, G.: Lesser known miracles of burgers equation. Acta Mathematica Scientia 32(1), 281 – 294 (2012). DOI http://dx.doi.org/10.1016/S0252-9602(12)60017-4

- [24] Menon, G., Pego, R.L.: Universality classes in burgers turbulence. Communications in Mathematical Physics 273(1), 177–202 (2007). DOI 10.1007/s00220-007-0251-1

- [25] Menon, G., Srinivasan, R.: Kinetic theory and lax equations for shock clustering and burgers turbulence. Journal of Statistical Physics 140(6), 1–29 (2010). DOI 10.1007/s10955-010-0028-3

- [26] Novikov, D.: Hahn decomposition and Radon-Nikodym theorem with a parameter. ArXiv Mathematics e-prints (2005)

- [27] Sinai, Y.: Statistics of shocks in solutions of inviscid burgers equation. Communications in Mathematical Physics 148(3), 601–621 (1992). DOI 10.1007/BF02096550

- [28] Smoluchowski, M.: Drei Vortrage über Diffusion, Brownsche Bewegung und Koagulation von Kolloidteilchen. Zeitschrift fur Physik 17, 557–585 (1916)