Asymptotics of Empirical Eigen-structure for Ultra-high Dimensional Spiked Covariance Model

Abstract

We derive the asymptotic distributions of the spiked eigenvalues and eigenvectors under a generalized and unified asymptotic regime, which takes into account the spike magnitude of leading eigenvalues, sample size, and dimensionality. This new regime allows high dimensionality and diverging eigenvalue spikes and provides new insights into the roles the leading eigenvalues, sample size, and dimensionality play in principal component analysis. The results are proven by a technical device, which swaps the role of rows and columns and converts the high-dimensional problems into low-dimensional ones. Our results are a natural extension of those in Paul (2007) to more general setting with new insights and solve the rates of convergence problems in Shen et al. (2013). They also reveal the biases of the estimation of leading eigenvalues and eigenvectors by using principal component analysis, and lead to a new covariance estimator for the approximate factor model, called shrinkage principal orthogonal complement thresholding (S-POET), that corrects the biases. Our results are successfully applied to outstanding problems in estimation of risks of large portfolios and false discovery proportions for dependent test statistics and are illustrated by simulation studies.

Keywords: Asymptotic distributions; Principal component analysis; Spiked covariance model; Ultra-high dimension; Diverging eigenvalues; Approximate factor model; Relative risk management; False discovery proportion.

1 Introduction

Principal Component Analysis (PCA) has widely been used as a powerful tool for dimensionality reduction and data visualization. Its theoretical properties such as the consistency and asymptotic distributions of empirical eigenvalues and eigenvectors are challenging especially in high dimensional regime. For the past half century substantial amount of efforts have been devoted to understanding empirical eigen-structures. An early effort is Anderson (1963) who established the asymptotic normality of eigenvalues and eigenvectors under the classical regime with large sample size and fixed dimension . However, as dimensionality diverges at the same rate as the sample size, sample covariance matrix is a notoriously bad estimator with substantial different eigen-structure from the population one. A lot of recent literatures make the endeavor to understand the behaviors of eigenvalues and eigenvectors under high dimensional regime where both and go to infinity. See for example Baik et al. (2005); Bai (1999); Paul (2007); Johnstone and Lu (2009); Onatski (2012); Shen et al. (2013) and many related papers. For additional developments and references, see Bai and Silverstein (2009).

Most of studies focus on the situations where signals are weak or semi-weak (Onatski, 2012) with leading asymptotic eigenvalues bounded (Paul, 2007; Bai and Silverstein, 2009) or slowly growing (Onatski, 2012). However, Fan et al. (2013) shows that for factor models with pervasive factors, the leading eigenvalues can grow linearly with the dimensionality and hence their corresponding eigenvectors can be consistently estimated as long as sample size diverges. This leads to the question of how the asymptotics of engen-structure depends on the interplay of spike magnitude of leading eigenvalues, dimensionality, and sample size. An interesting study on this topic is Shen et al. (2013), which focuses only on the consistency of the problem. The question then arises naturally on the rates of convergence and asymptotic structures of empirical eigenvalues and eigenvectors. This is the subject of this study.

In this paper, we consider a high dimensional spiked covariance model with the first several eigenvalues significantly larger than the rest. Typically, the spike part is of importance and of interest. We provides new understanding on how the spiked empirical eigenvalues and eigenvectors fluctuate around their theoretical counterparts and what their asymptotic biases are. For the spiked covariance model, three quantities play an essential role in determining the asymptotic behaviors of empirical eigen-structure: the sample size , the dimension , and the magnitude of leading eigenvalues . Theoretical properties of PCA have been investigated from three different perspectives.

The first angle is through a low-rank plus sparse decomposition, where the covariance matrix is perceived as the sum of a low-rank and a sparse matrix. The low-rank part contributes to the signal to be recovered whereas the sparse part serves as noise. For example in Fan et al. (2008), the low-rank matrix corresponds to the dependence induced by the common factors or covariates whereas the sparse matrix corresponds to the idiosyncratic noise. In noiseless setting, Candès et al. (2011) considered the principal component pursuit and showed that it can recover the decomposition structure under the incoherence condition. Chandrasekaran et al. (2011a) also studied the sufficient condition for exact recovery of the low-rank and sparse matrices. The noisy decomposition recover was considered more thoroughly by Agarwal et al. (2012). In addition, a large amount of literature has contributed to the topic of sparse PCA, for example Amini and Wainwright (2008); Vu and Lei (2012); Birnbaum et al. (2013); Berthet and Rigollet (2013); Ma (2013), which leverages the extra assumption on the sparsity of eigenvectors. Specifically, Cai et al. (2013b) studied the minimax optimal rates for estimating eigenvalues and eigenvectors of spiked covariance matrices with jointly -sparse eigenvectors. This type of work assumes bounded eigenvalues, which limit the signals we can get from the data. Correspondingly, those works require additional eigenvector structure to reduce the possibility of noise accumulation such as incoherence or jointly -sparse or other similar conditions. In this paper, thanks to the diverging eigenvalue regime we will consider, our conclusions will not rely on additional structure of eigenvectors, which can be hard to verify in practice.

A different line of efforts is to analyze PCA through random matrix theories, where it is typically assumed with bounded spike sizes. It is well known that if the true covariance matrix is identity, the empirical spectral distribution converges almost surely to the Marcenko-Pastur distribution (Bai, 1999) and when the largest and smallest eigenvalues converge almost surely to and respectively (Bai and Yin, 1993; Johnstone, 2001). If the true covariance structure takes the form of a spiked matrix, Baik et al. (2005) showed that the asymptotic distribution of the empirical eigenvalues exhibit an scaling when the eigenvalue lies below a threshold , and an scaling when it is above the threshold. For the case where we have the regular scaling, Paul (2007) investigated the asymptotic behavior of the corresponding empirical eigenvectors and showed that the major part of an eigenvector which corresponds to the spiked eigenvalues is normally distributed with regular scaling . The convergence of principal component scores under this regime was considered by Lee et al. (2010). The same random matrix regime has also been considered by Onatski (2012) in studying the principal component estimator for high-dimensional factor models. More recently, Koltchinskii and Lounici (2014b, a) revealed a profound link of concentration bounds of empirical eigen-struecture with the effective rank defined as (Vershynin, 2010). Their results extend the regime of bounded eigenvalues to more general setting, although the asymptotic results in most cases still rely on the assumption . In this paper, we consider the regime , which implies . More discussions will be given in Section 3.

Deviating from the classical random matrix and sparse PCA literature, we consider the ultra-high dimensional regime allowing . If , to ensure sufficiently strong signal for PCA, it is natural to also have the spike sizes go to infinity, namely, for the first leading eigenvalues. This leads to the third perspective for understanding PCA from this ultra high dimensional setting. Shen et al. (2013) adopted this point of view and considered the regime of where for leading eigenvalues. This is more general than the bounded eigenvalue condition. Specifically if eigenvalues are bounded, we require the ratio converges to a bounded constant. On the other hand, if the dimension is much larger than the sample size, we offset the dimensionality by assuming increased signals. In particular, the pervasive factor model considered in economics and finance factor model corresponds to with the pervasive leading eigenvalues , see for example Fan et al. (2013, 2014); Stock and Watson (2002); Bai (2003); Bai and Ng (2002). The weak factor model considered by Onatski (2012) also implies , with bounded and for some . Hall et al. (2005); Jung and Marron (2009) started the research of high dimension low sample size (HDLSS) regime. With fixed, Jung and Marron (2009) concluded that consistency of leading eigenvalues and eigenvectors is granted if for , which also corresponds to . Shen et al. (2013) revealed an interesting fact that when , spiked sample eigenvalues almost surely converges to a biased quantity of the true eigenvalues; furthermore the corresponding sample eigenvectors show an asymptotic conical structure. We will consider the same regime as theirs, but focus more on the asymptotic distributions of the eigen-structure, which was not covered in their paper, and under more relaxed conditions. Our results can be seen as a natural extension of Paul (2007) to ultra high dimensional setting.

In addition to the different regimes we take on, we also introduce a simple technique to for our technical proofs. The idea is to flip the roles of rows and columns and treat as the sample size and as the dimension. When is higher than , sample covariance is clearly degenerate. Switching the roles of and allows us to utilize the existing results on eigen-structures. To be specific, if we have samples generated from where is diagonal, then all the information we have is just an by data matrix with independent entries. We can simply treat the data as independent vectors of dimension each with distribution . Even when the data are not normally distributed and hence -dimensional vectors are then not independent, the idea is still powerful and leads to better understanding of relationship between high and low dimensionality. The simple trick has been used to derive asymptotic results of empirical eigenvalues in recent papers such as Shen et al. (2013); Yata and Aoshima (2012, 2013). One of our contributions lies in successful application of the trick to study the empirical leading eigenvectors.

The rest of the paper is organized as follows. Section 2 introduces the notations, assumptions, and an important fact which serves as basis of our proofs. The fact will help unravel the relationship between high and low dimensions. Sections 3.1 and 3.2 devote to the theoretical results of the sample eigenvalues and eigenvectors of the spiked covariance matrix under our asymptotic regime. In Section 4, we discuss several applications of the theories in the previous section. Firstly a new covariance estimator for the approximate factor model, named shrinkage principal orthogonal complement thresholding (S-POET), is proposed which corrects the biases of empirical eigenvalues. Secondly, S-POET will be successfully applied to outstanding problems in estimation of risks of large portfolios and false discovery proportions for dependent test statistics. For both problems, the typical assumption on the signal strength of leading eigenvalues in order to deploy factor analysis is relaxed due to our new results in Section 3. In Section 5, simulations are conducted to illustrate the theoretical results at the finite sample. The proofs for Section 3 are provided in Section 6 and those for Section 4 are relegated to the supplementary material.

2 Assumptions and a simple fact

Asssume that is a sequence of i.i.d. random variables with zero mean and covariance matrix . Let be the eigenvalues of in descending order. We consider the spiked covariance model as follows.

Assumption 2.1.

, where the non-spiked eigenvalues are bounded, i.e. for constants and the spiked eigenvalues are well separated, i.e. such that .

The eigenvalues are divided into the spiked ones and bounded non-spiked ones. We do not have specific order assumptions on the leading eigenvalues nor require them to diverge. Thus, our results in Section 3 are applicable to both bounded and diverging leading eigenvalues; if diverging, they can have different diverging rates. For simplicity, we only consider distinguishable eigenvalues (multiplicity 1) for the largest eigenvalues and a fixed number , independent of and .

The spiked covariance model is motivated by the factor model considered by Fan et al. (2013) as follows. Assume without loss of generality that , the identity matrix. Then, the model implied covariance matrix , where . If the factor loadings (the transpose of rows of ) are an i.i.d. sample from a population with mean zero and covariance , then by the law of large numbers, . In other words, the eigenvalues of are approximately

where is the eigenvalue of . If we assume that is bounded, then by Weyl’s theorem, we conclude that

| (2.1) |

and the remaining is bounded.

In the spiked covariance models, three essential factors come into play: the sample size , dimension and the spikeness ’s. The following relationship is assumed as in Shen et al. (2013).

Assumption 2.2.

Assume . For the spiked part , is bounded, and for the non-spiked part, .

We allow in any manner, though also needs also grow fast enough to ensure bounded . In particular, is allowed as in the factor model. We do not assume the non-spiked eigenvalues are identical, as in most spiked covariance model literature (e.g. Paul (2007); Johnstone and Lu (2009)).

By spectral decomposition, , where the orthonormal matrix is constructed by the eigenvectors of and . Let . Since the empirical eigenvalues are invariant and the empirical eigenvectors are equivariant under an orthonormal transformation, we focus the analysis on the transformed domain of and the results can be translated into the original data. Note that . Let be the elementwise standardized random vector.

Assumption 2.3.

are i.i.d copies of . The standardized random vector is sub-Gaussian with independent entries of mean zero and variance one. The sub-Gaussian norms of all components are uniformly bounded: , where .

Since , the first population eigenvectors are simply unit vectors . Denote the by transformed data matrix by . Then the sample covariance matrix is

whose eigenvalues are denoted as ( for ) with corresponding eigenvectors . Note that the empirical eigenvectors of data ’s are .

Let be the column of the standardized . Then each has i.i.d sub-Gaussian entries with zero mean and unit variance. Exchanging the role of rows and columns, we get the by Gram matrix

with the same nonzero eigenvalues as and the corresponding eigenvectors . It is well known that for

| (2.2) |

while the other eigenvectors of constitute a -dimensional orthogonal complement of .

By using this simple fact, for the specific case with in Assumption 2.1, for in Assumption 2.2, and Gaussian data in Assumption 2.3, Shen et al. (2013) showed that

and

where denotes the inner product of two vectors. However, they fail to establish any results on convergence rates or asymptotic distributions of the empirical eigen-structure. This motivates the current paper.

The aim of this paper is to establish the asymptotic normality of the empirical eigenvalues and eigenvectors under more relaxed conditions. Our results are a natural extension of Paul (2007) to more general setting with new insights, where the asymptotic normality of sample eigenvectors is derived using complicated random matrix techniques for Gaussian data under the regime of . Compared to them, our proof, based on the relationship (2.2), is much simpler and insightful for understanding the behavior of ultra high dimensional PCA.

Here are some notations that we will use in the paper. For a general matrix , we denote its matrix entry-wise max norm as and define the quantities , , to be its spectral, Frobenius and induced norms. If is symmetric, we define to be the largest eigenvalue of and , to be the maximal and minimal eigenvalues respectively. We denote as the trace of . For any vector , its norm is represented by while norm is written as . We use to denote the diagonal matrix with the same diagonal entries as . For two random vectors of the same length, we say if and if . We denote for some distribution if there exists such that . In the following, is a generic constant that may differ from line to line.

3 Asymptotic behavior of empirical eigen-structure

3.1 Asymptotic normality of empirical eigenvalues

Let us first study the behavior of the first empirical eigenvalues of . Denote by the largest eigenvalue of matrix and recall that . We have the following asymptotic normality of .

Theorem 3.1.

The theorem shows that the bias of is . The second term is dominated by the first term since and it is of order if . The latter assumption is satisfied by the strong factor model in Fan et al. (2013) and a part of weak factor model in Onatski (2012). To get the asymptotically unbiased estimate, it requires for . This result is more general than that of Shen et al. (2013) and sheds a similar light to that of Koltchinskii and Lounici (2014b, a) i.e. almost surely if and only if the effective rank is of order , which is true when . Yata and Aoshima (2012, 2013) employed a similar technical trick and gave a comprehensive study on the asymptotic consistency and distributions of the eigenvalues. They got various similar results under different conditions from ours. Our framework is more general and bias reduction can also be made by using a different method; see Section 4.2. In addition, under the typical spiked covariance model as in Baik et al. (2005), Johnstone and Lu (2009) and Paul (2007), where it is assumed , we have equal to the minimum eigenvalue of the population covariance matrix. The theorem reveals the bias is controlled at the rate . Our result is also consistent with Anderson (1963)’s result that

for Gaussian distributions and fixed and ’s, where the non-spiked part does not exist and thus the bias disappears. The proof is relegated to Section 6.

3.2 Behavior of empirical eigenvectors

Let us consider the asymptotic distribution of the empirical eigenvectors ’s corresponding to , . As in Paul (2007), each is divided into two parts corresponding to the spike and non-spike components, i.e. where is of length .

Theorem 3.2.

Under Assumptions 2.1 - 2.3, we have

(i) For the spike part, if ,

| (3.2) |

while if ,

| (3.3) |

for , with

where , is the first elements of unit vector , and , which is assumed to exist.

(ii) For the noise part, if we further assume the data is Gaussian, there exists dimensional vector such that

| (3.4) |

where is a diagonal scaling matrix and denotes the uniform distribution over the centered sphere of radius . In addition, the max norm of satisfies

| (3.5) |

(iii) Furthermore,

and

. Together with (i), this implies the inner product between empirical eigenvector and the population one converges to in probability and

| (3.6) |

In the above theory, we assume that exists. This is not restrictive if eigenvalues are well separated i.e. from assumption 2.1. The assumption obviously holds for the pervasive factor model (Fan et al., 2013), in which .

Theorem 3.2 is an extension of random matrix results into ultra high dimensional regime. Its proof sheds light on how to use the smaller matrix as a tool to understand the behavior of the larger covariance matrix . Specifically, we start from or identity (6.3) and then use the simple fact (2.2) to get a relationship (6.4) of eigenvector . Then (6.4) is rearranged as (6.5) which gives a clear separation of dominating term, that is asymptotically normal, and error term. This makes the whole proof much simpler in comparison with Paul (2007) who showed a similar type of results through a complicated representation of and . From this simple trick, we can understand deeply how some important high and low dimensional quantities link together and differ from each other.

Several remarks are in order. Firstly, since is the empirical eigenvector based on observed data , we have decomposition

where . Note that converges to the true eigenvector deflated by a factor of with the convergence rate while creates a random bias, which is distributed uniformly on an ellipse of dimension and projected into the dimensional space spaned by . The two parts intertwined in such a way that correction for the bias of estimating eigenvectors is almost impossible. More details are discussed in Section 4 for factor models. Secondly, it is clearly as in the eigenvalue case, the bias term in Theorem 3.2 (i) disappears when . In particular, for the stronger factor given by (2.1), is a consistent estimator. Thirdly, the situations and have slight difference in that multiple spikes could interact with each other. Especially this reflects in the convergence of angle of empirical eigenvector to its population counterpart: the angle converges to with an extra rate which stems from estimating for (see proof of Theorem 3.2 (iii)). The difference will only be seen when the spike magnitude is higher than the order . We will verify this by a simple simulation in Section 5. Fourthly, it is the first time that the max norm bound of the non-spiked part was derived. This bound will be useful for analyzing factor models in Section 4.

Theorem 3.2 again implies the results of Shen et al. (2013). It also generalizes the asymptotic distribution of non-spiked part from pure orthogonal invariant case of Paul (2007) to more general bounded setting. In particular, when , the asymptotic distribution of the normalized non-spiked component is not uniform over a sphere any more, but over an ellipse. In addition, our result can be compared with the low dimensional case, where Anderson (1963) showed that

| (3.7) |

for fixed and ’s. Under our assumptions, if the spiked eigenvalues go to infinity, the constants in the asymptotic covariance matrix are replaced by the limits ’s. Similar to the behavior of eigenvalues, the spiked part preserves the normality property except for a bias factor caused by the high dimensionality.

Recent manuscript by Koltchinskii and Lounici (2014a) provides general asymptotic results for the empirical eigenvectors from a spectral projector point of view, but they mainly focus on the regime of . Indeed, they limit themselves to the regime that and when establishing the asymptotic normality (see conditions for Theorems 5 and 7 therein). In contrast, we consider a very different regime, requiring and allowing to diverge. Furthermore, Theorem 3.2 gives a more refined description on the behavior of empirical eigenvectors than the asymptotic normality result given in Theorem 7 of Koltchinskii and Lounici (2014a). Last but not least, it has been shown by Johnstone and Lu (2009) that PCA generates consistent eigenvector estimation if and only if when the spike sizes are fixed. This motivates the study of sparse PCA. We take the spike magnitude of eigenvalues into account and provide additional insights by showing that PCA consistently estimate eigenvalues and eigenvectors if and only if . This explains why Fan et al. (2013) can consistently estimate the eigenvalues and eigenvectors while Johnstone and Lu (2009) can not.

4 Applications to factor models

In this section, we propose a method named Shrinkage Principal Orthogonal complEment Thresholding (S-POET) for estimating large covariance matrices induced by the approximate factor models. The estimator is based on correction of the bias of empirical eigenvalues as specified in (3.1). We derive for the first time the bound of the relative estimation errors of covariance matrices under the spectral norm. The results are then applied to assessing large portfolio risk and estimation of false discovery proportion, where the conditions in existing literature are relaxed.

4.1 Approximate factor models

Factor models have been widely used in various disciplines such as finance and genomics. Consider the approximate factor model

| (4.1) |

where is the observed data for the () individual (e.g. returns of stocks) or components (e.g. expression of genes) at time ; is a vector of latent common factors and is the factor loadings for the individuals or components; is the idiosyncratic error, uncorrelated with the common factors. In genomics application, can also index individuals or repeated experiments. For simplicity we assume there is no time dependency.

The factor model can be written into a matrix form as follows:

| (4.2) |

where , , , are respectively the matrix form of observed data, factor loading matrix, factor matrix, and error matrix. For identifiability issue, we impose the condition that and is a diagonal matrix. Thus, the covariance matrix is given by

| (4.3) |

where is the covariance matrix of the idiosyncratic error at any time .

Under the assumption that is sparse with its eigenvalues bounded away from zero and infinity, the population covariance exhibit a “low-rank plus sparse” structure. The sparsity is measured by the following quantity

for some (Bickel and Levina, 2008). In particular, with is the maximum number of nonzero elements in each row of .

In order to estimate the true covariance matrix with the above factor structure, Fan et al. (2013) proposed a method called “POET” to recover the unknown factor matrix as well as the factor loadings. The idea is simply to first decompose the sample covariance matrix into the spiked part and non-spiked part and estimate them separately. Specifically, let and and be its corresponding eigenvalues and eigenvectors. They define

| (4.4) |

where is the matrix after applying thresholding method (Bickel and Levina, 2008) to .

They showed that the above estimation procedure is equivalent to the least square approach that minimizes

| (4.5) |

The columns of are the eigenvectors corresponding to the largest eigenvalues of the matrix and . After and are estimated, the sample covariance of can be formed: . Finally thresholding is applied to to generate , where

| (4.6) |

Here is the generalized shrinkage function (Antoniadis and Fan, 2001; Rothman et al., 2009) and is the entry-dependent threshold. The above adaptive threshold corresponds to applying thresholding with parameter to the correlation matrix of . The positive parameter will be determined later.

Fan et al. (2013) showed that under Assumptions A.1 - A.4 listed in Appendix A in the supplementary material (Fan and Wang, 2015),

| (4.7) |

where and is the Frobenius norm. Note that

which measures the relative error in Frobenius norm. A more natural metric is relative error under the operator norm , which can not be obtained by using the technical device of Fan et al. (2013). Via our new tools, we will establish such a result under weaker conditions than their pervasiveness assumption. Note that the relative error convergence is particularly meaningful for spiked covariance matrix, as eigenvalues are in different scales.

4.2 Shrinkage POET under relative spectral norm

The discussion above reveals several drawbacks of POET. First, the spike size has to be of order which rules out relatively weaker factors. Second, it is well known that the empirical eigenvalues are inconsistent if the spike eigenvalues do not significantly dominate the non-spike part. Therefore, proper correction or shrinkage is needed. See a recent paper by Donoho et al. (2014) for optimal shrinkage of eigenvalues.

Regarding to the first drawback, we relax the assumption in Assumption A.1 to the following weaker assumption.

Assumption 4.1.

for some with eigenvalues bounded from above and below, where . In addition, we assume , is bounded from above and below.

This assumption does not require the first eigenvalues of to take on any specific rate. They can still be much smaller than , although for simplicity we require them to diverge and share the same diverging rate. As we assume bounded , the assumption is also imposed to avoid the issue of identifiability. When does not diverge, more sophisticated condition is needed for identifiability (Chandrasekaran et al., 2011b).

In order to handle the second drawback, we propose the Shrinkage POET (S-POET) method. Inspired by (3.1), the shrinkage POET modifies the first part in POET estimator (4.4) as follows:

| (4.8) |

where , a simple soft thresholding correction. Obviously if is sufficiently large, . Since is unknown, a natural estimator is such that the total of the eigenvalues remains unchanged:

or . It has been shown by Lemma 7 of Yata and Aoshima (2012) that

Thus, replacing by , we have , i.e. the estimation error in is negligible. From Theorem 3.1, we can easily obtain asymptotic normality, that is if .

To get the convergence of relative errors under the operator norm, we also need the following additional assumptions:

Assumption 4.2.

(i) are independently and identically distributed with for all and .

(ii) There exist positive constants and such that , , and .

(iii) There exist positive constants and such that for ,

(iv) There exists such that for all , .

(v) .

The first three conditions are common in factor model literature. If we write , by Weyl’s inequality we have . Thus it is reasonable to assume the magnitude of factor loadings is of order in the fourth condition. The last condition is imposed to ease technical presentation.

Now we are ready to investigate . Suppose the SVD decomposition of ,

Then obviously

| (4.9) | |||||

and

| (4.10) |

It can be shown

| (4.11) | ||||

where and . Thus in order to find the convergence rate of relative spectral norm, we need to consider the terms and separately. Notice that measures the relative error of the estimated spiked eigenvalues, reflects the goodness of the estimated eigenvectors, and controls the error of estimating the sparse idiosyncratic covariance matrix. The following theorem reveals the rate of each term. Its proof will be provided in Appendix B of the supplementary material (Fan and Wang, 2015).

Theorem 4.1.

The relative error convergence in spectral norm characterizes the accuracy of estimation for spiked covariance matrix. In contrast with the previous results on Frobenius or max norm, this is the first time that the relative rate under spectral norm is derived. When and , we have

Comparing the rate with (4.7), we see the difference under two different norms. The term in (4.7) is enlarged to rate , which is due to the incoherence of the eigen-spaces of the low-rank signal matrix and sparse error matrix. Specifically this rate comes from . If we care only the relative error of the low-rank and sparse matrix spaces separately, we should only emphasize on and .

If , the proposed is asymptotically just the spiked empirical eigenvalue . However, when we have semi-weak factors whose corresponding eigenvalues are as weak as , shrinkage is necessary to guarantee the convergence of . On the other hand, if instead POET is applied to estimate covariance matrix, which is only bounded. However since the empirical eigenvectors are not corrected, POET and S-POET attain the same rate for , which actually dominates and in high dimensional setting. Nevertheless, as to be seen in the simulation studies, S-POET can stabilize the estimator and improve the estimation accuracy. For this reason, we recommend S-POET in practice.

4.3 Portfolio risk management

Portfolio allocation and risk management have been a fundamental problem in finance since Markowitz (1952)’s groundbreaking work on minimizing the volatility of portfolios with a given expected return. Specifically, the risk of a given portfolio with allocation vector w is conventionally measured by its variance , where is the volatility (covariance) matrix of the returns of underlying assets. To estimate large portfolio’s risks, it needs to estimate a large covariance matrix and factor models are frequently used to reduce the dimensionality. This was the idea of Fan et al. (2015) in which they used POET estimator to estimate . However, the basic method for bounding the risk error in their paper as well as another earlier paper of similar topic (Fan et al., 2012) was

They assumed that the gross exposure of the portfolio is bounded, mathematically , which made it possible to only focus on the max error norm. Technically, when is large, can be small. What an investor cares mostly is the relative risk error . Often w is a data-driven investment strategy, which is a random variable itself. Regardless of what w is,

which does not converge by Theorem 4.1. The question is what kind of portfolio w will make the relative error converge. Decompose w as a linear combination of the eigenvectors of , namely and . We have the following useful result for risk management.

Theorem 4.2.

The condition is obviously much weaker than . It does not limit the total exposure of investor’s position, but only put constraint on investment of the non-spiked section. Note that under the conditions of Theorem 4.2, , and S-POET and POET are approximately the same. The stated result hold for POET too.

4.4 Estimation of false discovery proportion

Another important application of the factor model is the estimation of false discovery proportion. For simplicity, we assume Gaussian data with an unknown correlation matrix and wish to test separately which coordinates of are nonvanishing. Consider the test statistic where is the sample mean of all data. Then with and the problem is to test

Define the number of discoveries and the number of false discoveries , where is the p-value associated with the test. Note that is observable while needs to be estimated. The false discovery proportion (FDP) is defined as .

Recently Fan and Han (2013) proposed to employ the factor structure

| (4.12) |

where and and are respectively the eigenvalue and eigenvector of as before. Then can be stochastically decomposed as

where are common factors and independent of are the idiosyncratic errors. For simplicity, assume the maximal number of nonzero elements of each row of is bounded. In Fan and Han (2013), they demonstrated that a good approximation for is

| (4.13) |

where is the -quantile of the standard normal distribution, , and is the row of .

Realized factors and the loading matrix are typically unknown. If a generic estimator is provided, then we are able to estimate and thus from its empirical eigenvalues and eigenvectors ’s and ’s. can be estimated by the least-squares estimate . Fan and Han (2013) proposed the following estimator for :

| (4.14) |

where and . The following assumptions are in their paper.

Assumption 4.3.

There exists a constant such that (i) for and as and (ii) for all .

They showed that if is based on the POET estimator with a spike size , under Assumptions A.1 - A.4 together with Assumption 4.3,

| (4.15) |

Again we can relax the assumption of spike magnitude from order to much weaker Assumption 4.1. Since is a correlation matrix, . This, together with Assumption 4.1, leads us to consider that all leading eigenvalues are of order proportional to for .

Now apply the proposed S-POET method to obtain and use it for FDP estimation. Then we have the following theorem.

Theorem 4.3.

Comparing the result with (4.15), this convergence rate attained by S-POET is more general than the rate achieved before. The only difference is the second term, which is if and if . So we relax the condition from in Fan and Han (2013) to . This means a weaker signal than order is actually allowed to obtain a consistent estimate of false discovery proportion.

5 Simulations

We conducted some simulations to demonstrate the finite sample behaviors of empirical eigen-structure, the performance of S-POET, and validity of applying it to estimate false discovery proportion.

5.1 Eigen-structure

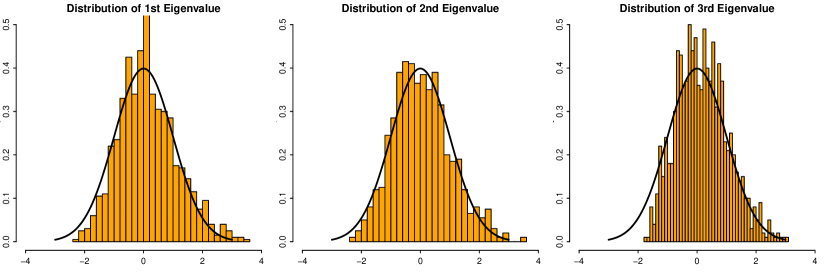

In this simulation, we set , and , which has three spikes () and corresponding . Data was generated from multivariate Gaussian. The number of simulations is . The histograms of the standardized empirical eigenvalues , and their associated asymptotic distributions (standard normal) are plotted in Figure 1. The approximations are very good even for this low sample size .

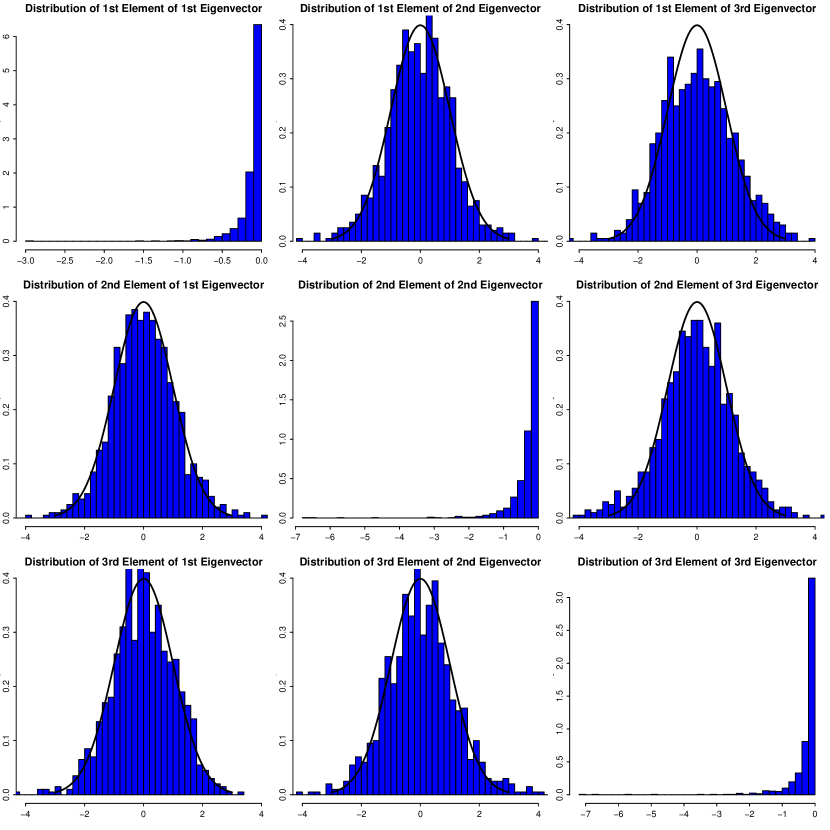

Figure 2 shows the histograms of for the first three elements (the spiked part) of the first three eigenvectors. According to the asymptotic result, the values in the diagonal position should stochastically converge to as observed. On the other hand, plots in the off-diagonal position should converge in distribution to for after standardization, which is indeed the case. We also report the correlations between the first three elements for the three eigenvectors based on those repetitions in Table 1. The correlations are all quite close to , which is consistent with the theory.

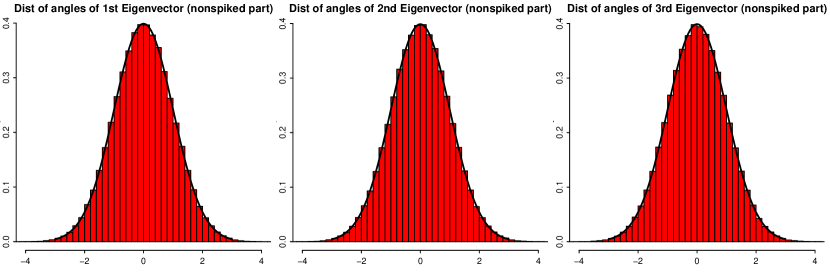

For the normalized nonspiked part , it should be distributed uniformly over the unit sphere. This can be tested by the results of Cai et al. (2013a). For any data points on -dimensional sphere, define the normalized empirical distribution of angles of each pair of vectors as

where is the angle between vectors and . When the data are generated uniformly from a sphere, converges to the standard normal distribution with probability . Figure 3 shows the empirical distributions of all pairwise angles of the realized in 1000 simulations. Since number of such pairwise angels is , the empirical distributions and the asymptotic distributions are almost identical. The normality holds even for a small subset of the angles.

| 1st & 2nd elements | 1st & 3rd elements | 2nd & 3rd elements | |

|---|---|---|---|

| 1st Eigenvector | 0.00156 | -0.00192 | -0.04112 |

| 2nd Eigenvector | -0.02318 | -0.00403 | 0.01483 |

| 3rd Eigenvector | -0.02529 | -0.04004 | 0.12524 |

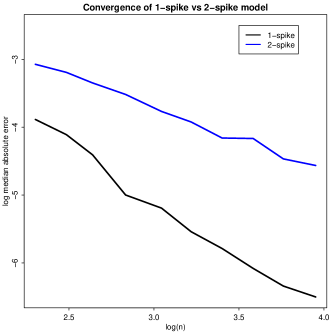

Lastly, we did simulation to verify the rate difference of for and , revealed in Theorem 3.2 (iii). We choose for , , where represents rounding. We set for and consider two situations: (1) , (2) . Under both cases, simulations were carried out 500 times and the corresponding angle of empirical eigenvector and truth was calculated for each simulation. The logarithm of the median absolute error of was plotted against . Under the two situations, the rate of convergence is and respectively. Thus the slope of the curves should be for a single spike and for two spikes, which is indeed as the case as shown in Figure 4.

In short, all the simulation results match well with the theoretical results for the ultra high dimensional regime.

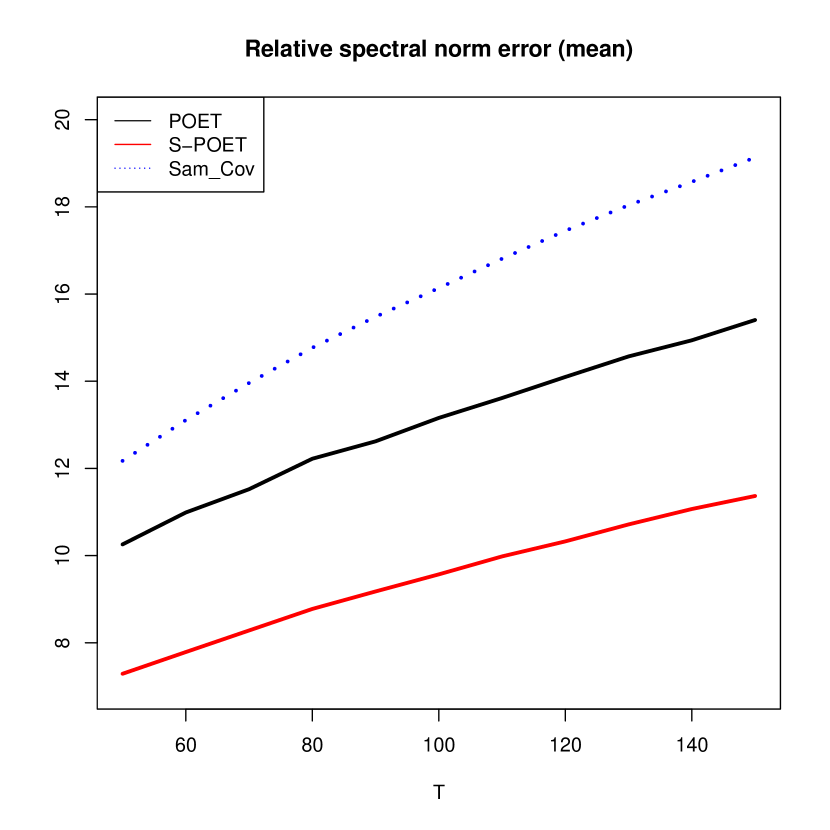

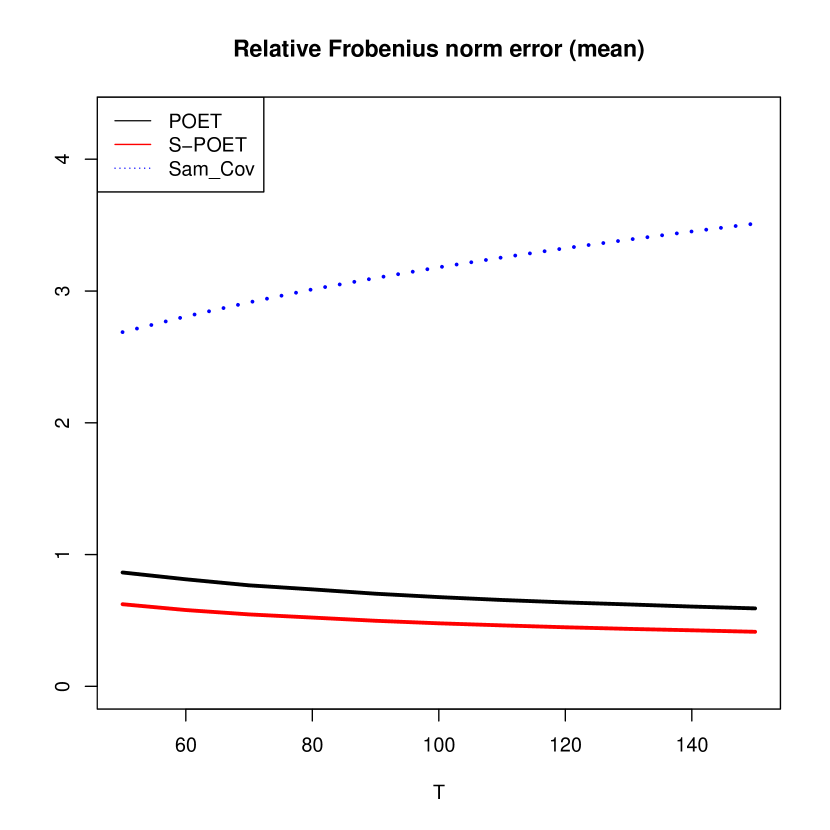

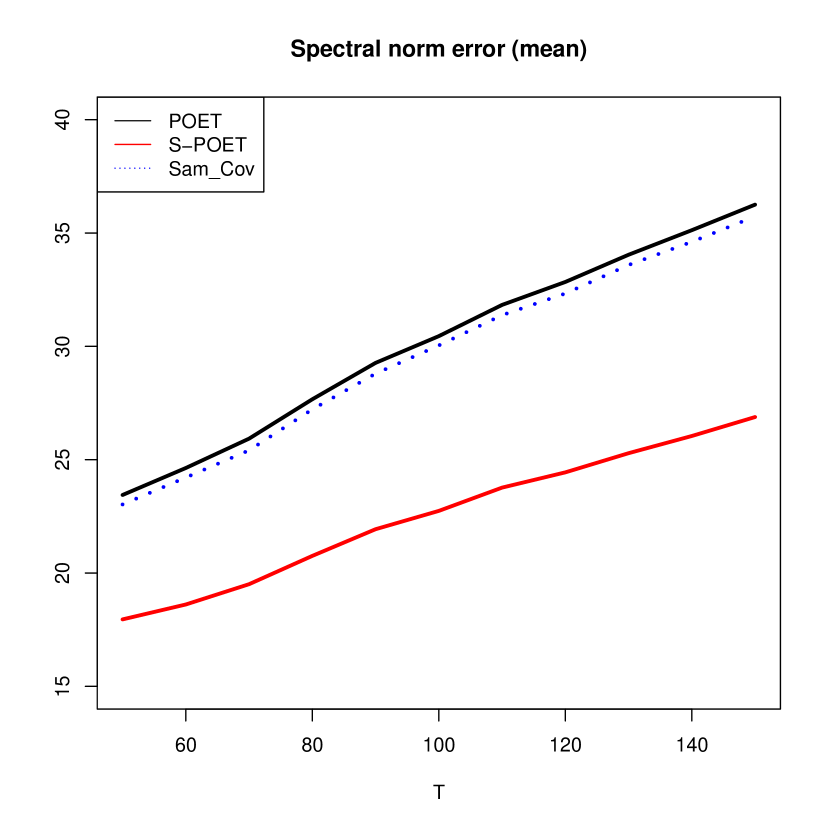

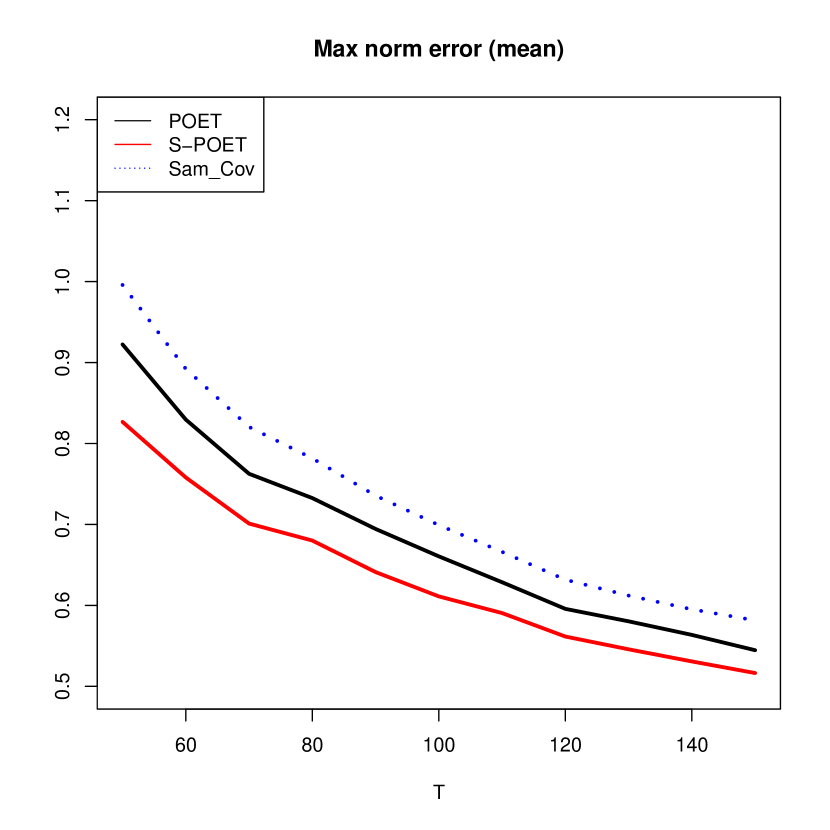

5.2 Performance of S-POET

We demonstrate the effectiveness of S-POET in comparison with the POET. A similar setting to the last section was used, i.e. and . The sample size ranges from to and . Note that when , . The spiked eigenvalues are determined from so that is of order , which is much smaller than . For each pair of and , the following steps are used to generate observed data from the factor model for times.

-

(1)

Each row of is simulated from the standard multivariate normal distribution and the column is normalized to have norm for .

-

(2)

Each row of is simulated from standard multivariate normal distribution.

-

(3)

Set where ’s are generated from Gamma() with (mean , standard deviation ). The idiosyncratic error is simulated from .

-

(4)

Compute the observed data .

Both S-POET and POET are applied to estimate the covariance matrix . Their mean estimation errors over simulations, measured in relative spectral norm , relative Frobenius norm , spectral norm and max norm , are reported in Figure 5. The errors for sample covariance matrix are also depicted for comparison. First notice that no matter in what norm, S-POET uniformly outperforms POET and sample covariance. It affirms the claim that shrinkage of spiked eigenvalues is necessary to maintain good performance when the spike is not sufficiently large. Since the low rank part is not shrunk for POET, its error under the spectral norm is comparable and even slightly larger than that of the sample covariance matrix. The error under max norm and relative Frobenius norm as expected decreases as and increase. However the relative error under the spectral norm does not converge: our theory shows it should increase in the order .

5.3 FDP estimation

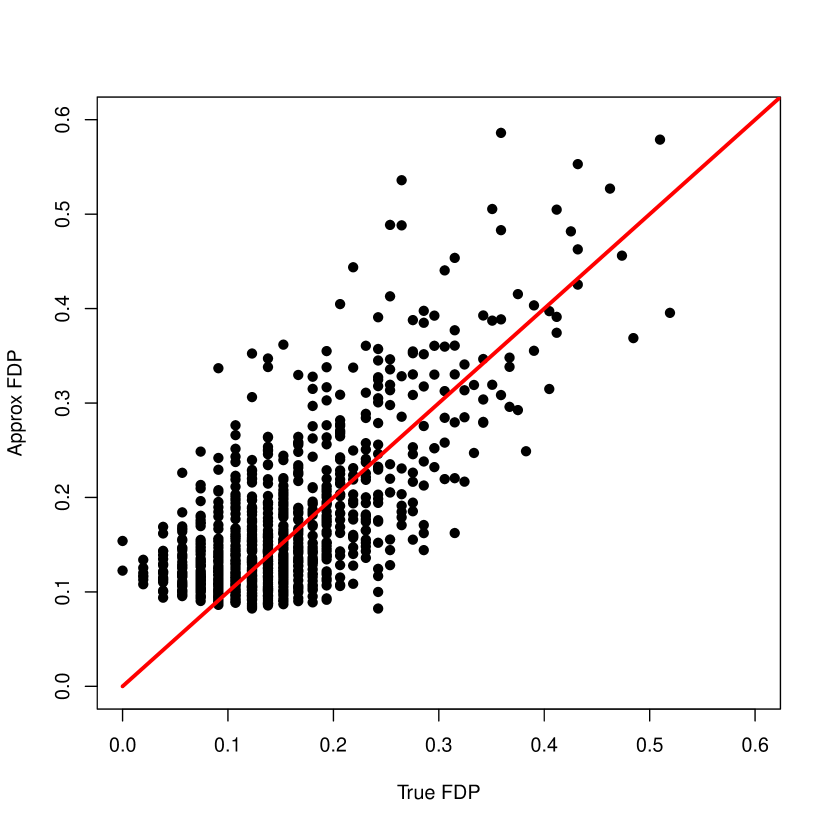

In this section, we report simulation results on FDP estimation by using both POET and S-POET. The data are simulated in a similar way as in Section 5.2 with and . The first eigenvalues have spike size proportional to which corresponds to in Theorem 4.3. The true FDP is calculated by using with . The approximate FDP, , is calculated as in (4.13) with known but estimated given by . This based on a known sample covariance matrix serves as a benchmark for our estimated covariance matrix to compare with. We employ POET and S-POET to get and .

In Figure 6, three scatter plots are drawn to compare , and with the true . The points are basically aligned along the degree line, meaning that all of them are quite close to the true FDP. With the semi-strong signal , although much weaker than order , POET accomplishes the task as well as S-POET. Both estimators performs as well as if we know the covariance matrix , the benchmark.

6 Proofs for Section 3

6.1 Proof of Theorem 3.1

We first provide three useful lemmas for the proof. Lemma 6.1 provides non-asymptotic upper and lower bound for the eigenvalues of weighted Wishart matrix for sub-Gaussian distributions.

Lemma 6.1.

Let ’s be independent dimensional sub-Gaussian random vectors with zero mean and identity variance with the sub-Gaussian norms bounded by a constant . Then for every , with probability at least , one has

where for constants , depending on . Here ’s is bounded for all and .

The above lemma is the extension of the classical Davidson-Szarek bound [Theorem II.7 of Davidson and Szarek (2001)] to the weighted sample covariance with sub-Gaussian distribution. It was shown by Vershynin (2010) that the conclusion holds with for all . With similar techniques to those developed in Vershynin (2010), we can obtain the above lemma for general bounded weights. The details are omitted.

Now in order to prove the theorem, let us define two quantities and treat them separately in the following two lemmas. Let

where is columns of . Then,

| (6.1) |

Proof.

Note that has the same eigenvalues as matrix , where is an matrix with i.i.d. rows, which are sub-Gaussian distributed with mean and variance . here is only used for normalization. Therefore, we are in the low dimensional situation as Theorem 1 of Anderson (1963). The differences here are two-fold: on one hand we encounter sub-Gaussian distribution; on the other hand the eigenvalues could diverge with different rates of convergence. The result of Anderson (1963) can be extended in both directions.

Extension from Gaussian to sub-Gaussian is trivial. The only difference is that the kurtosis of Gaussian is replaced by that of sub-Gaussian distribution. Extension to diverging eigenvalues requires careful scrutiny of Anderson’s original proof. Detailedly, following the notations of Anderson (1963) and (2.22) therein, we have

where , , and is the element of the eigenvector of multiplied by for . We claim and are bounded with high probability, so and share the same limiting distribution. Therefore the limiting distribution of for are independent and

So the lemma follows.

It remains to show and are . Following the cofactor expansion argument of Section 7 in Anderson (1963), it is not hard to see . By assumption, . Hence and so is . In addition, . Now the derivation is complete. ∎

Proof.

By definition of , where is random matrix with independent sub-Gaussian entries of zero mean and unit variance and is the diagonal matrix with entries . By Lemma 6.1 with , for any ,

Therefore,

∎

6.2 Proofs of Theorem 3.2

The proof of Theorem 3.2 is mathematically involved. The basic idea for proving part (i) is outlined in Section 2. We relegate less important technical lemmas to the end of the proof in order not to distract the readers. The proof of part (ii) utilizes the invariance of standard Gaussian distribution under orthogonal transformations.

Proof of Theorem 3.2.

(i) Let us start by proving the asymptotic normality of for the case . Write

where each follows a sub-Gaussian distribution with mean and identity variance . Then by the eigenvalue relationship of equation (2.2), we have

| (6.2) |

Recall is the eigenvector of the matrix , that is, . Using , we obtain

| (6.3) |

where we denote , . We then left-multiply equation (6.3) by and employ relationship (6.2) to replace by and as follows:

| (6.4) | ||||

Further define

Then we have . Note that is only well defined if . Therefore, by left multiplying to equation (6.4),

| (6.5) | ||||

where . Dividing both side by , we are able to write

| (6.6) |

where

| (6.7) | ||||

We will show in Lemma 6.4 below that is a smaller order term. By Lemma 6.4, noticing that ,

| (6.8) |

Now let us derive normality of the right hand side of (6.8). According to definition of ,

| (6.9) |

Let and be the dimension vector without the element in . Since the diagonal element of is zero, depends only on . Therefore, by Lemma 6.5 below and Slutsky’s theorem,

Now let us turn to the case of . Since is not defined for , we need to find a different derivation. Equivalently, (6.3) can be written as

Left-multiplying and using relationship (6.2), we obtain easily

where is defined as before and according to Lemma 6.4. Expanding at the point of , we have

Note that from Lemmas 6.2 and 6.3, . Therefore due to the fact is asymptotically , we conclude

This completes the first part of the proof.

(ii) We now prove the conclusion for non-spiked part . Recall that follows . Consider where as defined in the theorem . Here the index means rescaled data by . After rescaling, we have . Correspondingly, the data matrix where and as the notations before. Assume and are eigenvectors given by and of the rescaled data and . It has been proved by Paul (2007) that is distributed uniformly over the unit sphere and is independent of due to the orthogonal invariance of the non-spiked part of . Hence it only remains to link with .

Note that and , so

where the last term is of order by Lemma 6.1. Thus by the theorem of Davis and Kahan (1970), . Next we convert from to using the basic relationship (2.2). We have,

First we claim since , , and according to Lemma 6.6. Now we show . From the proof of Lemma 6.6, we have

Then some elementary calculation gives the rate of . Therefore, . The conclusion (3.4) follows.

To prove the max norm bound (3.5) of , we first show . Recall that is uniformly distributed on unit sphere of dimension . This follows easily from its normal representation. Let to be dimensional multivariate standard normal distributed, then . It then follows

From the derivation above,

which gives , given the fact that by Lemma 6.6. Thus we are done with the second part of the proof.

(iii) The proof for the convergence of and are given in Lemma 6.6. If , the result for directly gives (3.6) with the same rate. For , from 6.6 we have

On the other hand, from Theorem 3.2 (i), for and . So , which implies (3.6).

∎

Lemma 6.4.

As , .

Proof.

Define and , and as follows:

We claim that and . Then the rate of could be easily derived from its definition (6.7) and the above results. To be specific, first notice the following two inequalities: by (6.5), ; by orthogonal decomposition , we have . Note that we always choose so that is positive. Therefore

| (6.10) | ||||

Hence, by (6.7),

It remains to show the claims above. Let us first show the rate of convergence of . In order to prove this, we need the rate of . By Lemma 6.1, , so we have

Hence

since the other terms except are all . Indeed, (6.9) says the first term is asymptotically bounded. We have shown in the proofs of Lemmas 6.2 and 6.3 that the second, third and fifth terms are . In addition, the facts that , imply the last term is .

Then let us show that and are . The rate of is needed. By Lemma 6.1, . Thus,

Then easily we get . Note that from Theorem 3.1 that , so

where similar to (6.9), and are .

Finally, . The proof is complete. ∎

Lemma 6.5.

.

Proof.

Recall . Then, by the definition of ,

Its component is for where . Denote and . We claim as , . So . In order to prove the lemma, it suffices to show that follows . That is, for any vector of dimension, almost surely.

where is the characteristic function of each element of . The sub index means we actually allow different characteristic functions for the columns of and .

By Taylor expansion, we can easily derive

from which it holds that

goes to as and is dominated by the integrable function . So by Dominated Convergence Theorem the right hand side is . Therefore, . Using this result, we have

which implies follows .

Now let us validate . Clearly

We have shown that and . It suffices to show .

So by Markov inequality, we have is , which generates . So is since is of fixed length . The proof is complete. ∎

Lemma 6.6.

and

.

Proof.

If , Theorem 3.2 (i) directly implies the conclusions. So in the following, we only consider . Recall that . Let , then

where and . Define

and consider the eigenvalue of the matrix . The -th diagonal element of the matrix must lie in between its minimum and maximum eigenvalues. That is

where is the -th element of the -th empirical eigenvector for . Divided by , then by Theorem 3.1 and Lemma 6.1 both the left and right hand side converge to

So also converges to the above quantity. Also, by definition, for while the ratio is 1 for . By Theorem 3.2 (i), for . Hence, again converges to the above quantity, which implies the rates of convergence for and . ∎

Appendix A Comparison on assumptions

The following assumptions are from Fan et al. (2013), where the results were established for the mixing sequence. But we only consider i.i.d. data in this paper. The assumptions are listed for completeness and comparison with Assumptions 4.1 and 4.2.

Assumption A.1.

for some symmetric positive definite matrix such that has distinct eigenvalues and that and are bounded away from both zero and infinity.

Assumption A.2.

(i) is strictly stationary. In addition, for all and .

(ii) There exist positive constants and such that , , and .

(iii) There exist positive constants and such that for ,

We introduce the strong mixing conditions. Let and denote the -algebras generated by and respectively. In addition, define the mixing coefficient

Assumption A.3.

There exists such that and satisfying for all .

Note that for the independence case, Assumption A.3 is trivially satisfied since for all .

Assumption A.4.

There exists such that for all and ,

(i) ,

(ii) ,

(iii) .

Appendix B Proofs of Theorems in Section 4

In order to prove theorems in Section 4, convergence rate of the sparse error matrix is required. The following theorem states the convergence rate for estimating by the thresholding procedure in (4.6). Its proof and related technical lemmas are given in Appendix C.

Theorem B.1.

Given Theorem B.1, we are ready to start showing theorems in Section 4. The proofs are built based on conclusions in Section 3.

Proof of Theorem 4.1.

We first prove the theorem for term . Write and the minimizer of (4.5) as . Since is just the eigenvectors (unnormalized) of , we have:

Then or if is unknown. Let be the diagonal matrix of the first empirical eigenvalues and be the empirical eigenvector matrix. In Sections 3.1 and 3.2, our results for empirical eigenvalues and eigenvectors imply the following:

| (B.1) |

and

| (B.2) |

where . Now let us start to bound and .

We handle the two terms separately.

where we used . The right hand side is further bounded by with

By equations (B.1) and (B.2), we conclude that and are of order and is of smaller order. Thus . In order to derive rate of , denote and so that . We could treat similar to . could be bounded by with

By Weyl’s theorem, , so . By theorem,

so is . Since is of smaller order, we conclude . Therefore, .

The bound for term is derived in the following. Recall that

which is bounded by

because by Lemma 6.6, .

as by Theorem. Finally, .

Finally let us look at term . Since , it suffices to bound , which has already been done in Theorem B.1. So

∎

Proof of Theorem 4.2.

The numerator of the relative risk is bounded by

The second term is bounded by , thus is . By using , the first term can be written as

where . It is easy to see from the proof of Theorem 4.1 that

The denominator is lower bounded by . Thus the relative risk is of order

for if we plug in the convergence rate of and in Theorem 4.1. If , the relative risk is . Note the rate comes from in the numerator. If we further assume , this rate becomes dominated by , thus the relative risk is again of order . ∎

Proof of Theorem 4.3.

The proof follows Theorem 1 of Fan and Han (2013). Using their notation, we have

where with ,

We just need to bound , then can be bound similarly. As shown in Fan and Han (2013),

where and are the eigenvalue and eigenvector of defined in (4.8). So by Weyl’s theorem and Theorem 4.1,

By theorem, we also have . So finally

Since ,

∎

Appendix C Convergence rate of error matrix

In order to achieve convergence rate Theorem B.1 for the covariance matrix of idiosyncratic error, we employ the following lemma from Fan et al. (2013).

Lemma C.1.

The essential step of applying the previous lemma is to find . We start by getting the convergence rate of and . Let denote the diagonal matrix of the first largest eigenvalues of the sample covariance matrix in decreasing order. Recall that

Define

Lemma C.2.

The rates of convergence of are as follows:

(i) ,

(ii) ,

Proof.

(i) By definition of and

Since , from Theorem 3.1, we have

where we used the fact . By Lemma 6.1,

and since from Assumption 4.2,

Therefore by Markov inequalty,

Hence,

(ii) From (i) we conclude

Let us bound each term separately. For the first term, and

The second term is bounded as and

since . The third term can be bounded similarly. Together with the fact that and from Assumption 4.2, we obtain

∎

Lemma C.3.

The rates of convergence for are as follows. Two regimes are considered.

If for constant , we have

(i) ,

(ii) .

If for constant , we have

(i’) ,

(ii’) .

Proof.

(i’) From Lemma C.2 (i) we have

We claim . Hence,. With this, we bound . First obviously since is bounded. Then from Fan et al. (2013), we know

It remains to show that . By definition,

where is a -net of the unit sphere and . Since, using Chernoff bound, we have

is sub-Gaussian, so choosing , we obtain that .

(i) In (i’), we showed . If in addition, we know , then so that . So we conclude with probability approaching one according to Weyl’s Theorem. Thus .

(ii) Decompose as follows:

Fan et al. (2013) showed that

Thus the max norm of the last term is . The max norms of the first and second terms are bounded respectively by

and by

Simplify and Combine the rates together, and note in this case and , we obtain,

(ii’) Now let us consider the other situation. We have a different decomposition of :

As before, the max norm of the last term is . The max norms of the first three terms are bounded respectively by

and

where is quite small.

Simplify and Combine the rates together, we obtain,

∎

Proof of Theorem B.1

Proof.

Recall that . We separately consider the two cases in Lemma C.3. If , so is well defined. We have

Therefore by Cauchy-Schwarz,

It follows from Lemma C.2 and C.3 (ii) that

Replacing the average over in the above inequality with maximum over and with , we can also derive bound for . Since from Assumption 4.2 we have , we get .

Now if , we apply a different way of decomposing .

Therefore by Cauchy-Schwarz,

It follows from Lemma C.2 and C.3 (ii’) that

Again, it is not hard to show .

Finally, Lemma C.1 concludes the theorem by choosing in both cases. ∎

References

- Agarwal et al. (2012) Agarwal, A., Negahban, S. and Wainwright, M. J. (2012). Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions. The Annals of Statistics 40 1171–1197.

- Amini and Wainwright (2008) Amini, A. A. and Wainwright, M. J. (2008). High-dimensional analysis of semidefinite relaxations for sparse principal components. In Information Theory, 2008. ISIT 2008. IEEE International Symposium on. IEEE.

- Anderson (1963) Anderson, T. W. (1963). Asymptotic theory for principal component analysis. The Annals of Mathematical Statistics 34 122–148.

- Antoniadis and Fan (2001) Antoniadis, A. and Fan, J. (2001). Regularization of wavelet approximations. Journal of the American Statistical Association 96.

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica 71 135–171.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica 70 191–221.

- Bai (1999) Bai, Z. (1999). Methodologies in spectral analysis of large-dimensional random matrices, a review. Statist. Sinica 9 611–677.

- Bai and Silverstein (2009) Bai, Z. and Silverstein, J. W. (2009). Spectral analysis of large dimensional random matrices (2nd ed.). Springer.

- Bai and Yin (1993) Bai, Z. and Yin, Y. (1993). Limit of the smallest eigenvalue of a large dimensional sample covariance matrix. The annals of Probability 1275–1294.

- Baik et al. (2005) Baik, J., Ben Arous, G. and Péché, S. (2005). Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices. Annals of Probability 1643–1697.

- Berthet and Rigollet (2013) Berthet, Q. and Rigollet, P. (2013). Optimal detection of sparse principal components in high dimension. The Annals of Statistics 41 1780–1815.

- Bickel and Levina (2008) Bickel, P. J. and Levina, E. (2008). Covariance regularization by thresholding. The Annals of Statistics 2577–2604.

- Birnbaum et al. (2013) Birnbaum, A., Johnstone, I. M., Nadler, B. and Paul, D. (2013). Minimax bounds for sparse pca with noisy high-dimensional data. Annals of statistics 41 1055.

- Cai et al. (2013a) Cai, T., Fan, J. and Jiang, T. (2013a). Distributions of angles in random packing on spheres. arXiv preprint arXiv:1306.0256 .

-

Cai et al. (2013b)

Cai, T., Ma, Z. and Wu, Y. (2013b).

Optimal estimation and rank detection for sparse spiked covariance

matrices .

URL http://arxiv.org/abs/1305.3235 -

Candès et al. (2011)

Candès, E. J., Li, X., Ma, Y. and

Wright, J. (2011).

Robust principal component analysis?

J. ACM 58 11:1–11:37.

URL http://doi.acm.org/10.1145/1970392.1970395 - Chandrasekaran et al. (2011a) Chandrasekaran, V., Sanghavi, S., Parrilo, P. A. and Willsky, A. S. (2011a). Rank-sparsity incoherence for matrix decomposition. SIAM Journal on Optimization 21 572–596.

- Chandrasekaran et al. (2011b) Chandrasekaran, V., Sanghavi, S., Parrilo, P. A. and Willsky, A. S. (2011b). Rank-sparsity incoherence for matrix decomposition. SIAM Journal on Optimization 21 572–596.

-

Davidson and Szarek (2001)

Davidson, K. R. and Szarek, S. J. (2001).

Chapter 8 local operator theory, random matrices and banach spaces.

In Handbook of the Geometry of Banach Spaces (W. Johnson and

J. Lindenstrauss, eds.), vol. 1. Elsevier Science B.V., 317 – 366.

URL http://www.sciencedirect.com/science/article/pii/S1874584901800103 - Davis and Kahan (1970) Davis, C. and Kahan, W. M. (1970). The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis 7 1–46.

- Donoho et al. (2014) Donoho, D. L., Gavish, M. and Johnstone, I. M. (2014). Optimal shrinkage of eigenvalues in the spiked covariance model. arXiv preprint arXiv:1311.0851 .

- Fan et al. (2008) Fan, J., Fan, Y. and Lv, J. (2008). High dimensional covariance matrix estimation using a factor model. Journal of Econometrics 147 186–197.

- Fan and Han (2013) Fan, J. and Han, X. (2013). Estimation of false discovery proportion with unknown dependence. arXiv preprint arXiv:1305.7007 .

- Fan et al. (2013) Fan, J., Liao, Y. and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B 75 1–44.

- Fan et al. (2015) Fan, J., Liao, Y. and Shi, X. (2015). Risks of large portfolios. Journal of Econometrics 186 367–387.

- Fan et al. (2014) Fan, J., Liao, Y. and Wang, W. (2014). Projected principal component analysis in factor models. arXiv preprint arXiv:1406.3836 .

- Fan and Wang (2015) Fan, J. and Wang, W. (2015). Supplementary appendix to the paper “asymptotics of empirical eigen-structure for ultra-high dimensional spiked covariance model” .

- Fan et al. (2012) Fan, J., Zhang, J. and Yu, K. (2012). Vast portfolio selection with gross-exposure constraints. Journal of the American Statistical Association 107 592–606.

- Hall et al. (2005) Hall, P., Marron, J. and Neeman, A. (2005). Geometric representation of high dimension, low sample size data. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 67 427–444.

- Johnstone (2001) Johnstone, I. M. (2001). On the distribution of the largest eigenvalue in principal components analysis. Annals of statistics 295–327.

-

Johnstone and Lu (2009)

Johnstone, I. M. and Lu, A. Y. (2009).

On consistency and sparsity for principal components analysis in high

dimensions.

Journal of the American Statistical Association 104

682–693.

URL http://amstat.tandfonline.com/doi/abs/10.1198/jasa.2009.0121 - Jung and Marron (2009) Jung, S. and Marron, J. (2009). Pca consistency in high dimension, low sample size context. The Annals of Statistics 37 4104–4130.

- Koltchinskii and Lounici (2014a) Koltchinskii, V. and Lounici, K. (2014a). Asymptotics and concentration bounds for spectral projectors of sample covariance. arXiv preprint arXiv:1408.4643 .

- Koltchinskii and Lounici (2014b) Koltchinskii, V. and Lounici, K. (2014b). Concentration inequalities and moment bounds for sample covariance operators. arXiv preprint arXiv:1405.2468 .

- Lee et al. (2010) Lee, S., Zou, F. and Wright, F. A. (2010). Convergence and prediction of principal component scores in high-dimensional settings. Annals of statistics 38 3605.

- Ma (2013) Ma, Z. (2013). Sparse principal component analysis and iterative thresholding. The Annals of Statistics 41 772–801.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection*. The journal of finance 7 77–91.

- Onatski (2012) Onatski, A. (2012). Asymptotics of the principal components estimator of large factor models with weakly influential factors. Journal of Econometrics 168 244–258.

- Paul (2007) Paul, D. (2007). Asymptotics of sample eigenstructure for a large dimensional spiked covariance model. Statistica Sinica 17 1617–1642.

- Rothman et al. (2009) Rothman, A. J., Levina, E. and Zhu, J. (2009). Generalized thresholding of large covariance matrices. Journal of the American Statistical Association 104 177–186.

-

Shen et al. (2013)

Shen, D., Shen, H., Zhu, H. and Marron,

J. S. (2013).

Surprising asymptotic conical structure in critical sample

eigen-directions .

URL http://arxiv.org/abs/1303.6171 - Stock and Watson (2002) Stock, J. and Watson, M. (2002). Forecasting using principal components from a large number of predictors 97 1167–1179.

- Vershynin (2010) Vershynin, R. (2010). Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027 .

- Vu and Lei (2012) Vu, V. Q. and Lei, J. (2012). Minimax rates of estimation for sparse pca in high dimensions. arXiv preprint arXiv:1202.0786 .

- Yata and Aoshima (2012) Yata, K. and Aoshima, M. (2012). Effective pca for high-dimension, low-sample-size data with noise reduction via geometric representations. Journal of multivariate analysis 105 193–215.

- Yata and Aoshima (2013) Yata, K. and Aoshima, M. (2013). Pca consistency for the power spiked model in high-dimensional settings. Journal of multivariate analysis 122 334–354.