Approximating explicitly the mean reverting CEV process

Abstract.

In this paper we want to exploit further the semi-discrete method appeared in Halidias and Stamatiou (2015). We are interested in the numerical solution of mean reverting CEV processes that appear in financial mathematics models and are described as non negative solutions of certain stochastic differential equations with sub-linear diffusion coefficients of the form where Our goal is to construct explicit numerical schemes that preserve positivity. We prove convergence of the proposed SD scheme with rate depending on the parameter Furthermore, we verify our findings through numerical experiments and compare with other positivity preserving schemes. Finally, we show how to treat the whole two-dimensional stochastic volatility model, with instantaneous variance process given by the above mean reverting CEV process.

Key words and phrases:

Explicit numerical scheme, mean reverting CEV process, positivity preserving, strong approximation error, order of convergence, stochastic volatility model.AMS subject classification 2010: 60H10, 60H35.

1. Introduction.

Consider the following stochastic models

| (1.1) |

where represents the underlying financially observable variable, is the instantaneous volatility when or the instantaneous variance when and the Wiener processes have correlation

We assume that is a mean reverting CEV process of the above form, with the coefficients for and since the process has to be non-negative. To be more precise the above restriction on implies that is positive, i.e. is unattainable, as well as non explosive, i.e. is unattainable, as can be verified by the Feller’s classification of boundaries [17, Prop. 5.22]. The steady-state level of is and the rate of mean reversion is .

The system (1.1) for is the Heston model. When we get the Brennan-Schwartz model [4, Sec. II], which apparent its simple form, cannot provide analytical expressions for

Process for also know as the CIR process [6, Rel 13], by the initials of the authors that proposed it for the term structure of interest rates, has received a lot of attention and we just mention two latest contributions to the study of such processes (see [1], [12] and references therein).

Process for has been also considered for the dynamics of the short-term interest rate [5, Rel (1)]. The stationary distribution of the process has also been derived in [2, Prop 2.2].

We aim for a positive preserving scheme for the process The scheme which we propose, and denote it semi-discrete (SD), preserves this analytical property of staying positive. The explicit Euler scheme fails to preserve positivity, as well as the standard Milstein scheme. We intend to apply the semi-discrete method for the numerical approximation of in model (1.1) with and compare with other positivity preserving methods such as the balanced implicit method (BIM) (introduced by [23, Rel (3.2)] with the positive preserving property [16, Sec. 5]) and the balanced Milstein method (BMM) [16, Th. 5.9].111We give in the Appendix the form of all the above schemes for the approximation of . Finally, we approximate the stochastic volatility model of (1.1) with In [15] a thorough treatment can be found, where also another stochastic volatility model is suggested.

Section 2 provides the setting and the main results, Theorems 2.1 and 2.2, concerning the convergence of the proposed Semi Discrete (SD) method to the true solution of mean reverting CEV processes of the form of the stochastic volatility in (1.1), as well as Theorem 2.3 which concerns the analogues of Theorems 2.1 and 2.2, following an alternative approach. The main ingredient of this approach, inspired by [12], is the simplification of the numerical scheme proposed, by altering the initial Brownian motion to another Brownian motion justified by Levy’s martingale characterization of Brownian motion, yielding to the same logarithmic rate as in Theorem 2.1, but to a better polynomial rate instead of as shown in Theorem 2.2.

Section 3 is devoted to the proof of Theorem 2.1, while Section 4 and 5 concern the proofs of Theorems 2.2 and 2.3 respectively. Finally, Section 6 presents illustrative figures where the behavior of the proposed scheme, regarding the order of convergence, is shown and a comparison with BIM and BMM schemes is given. In Section 7 we treat the full model (1.1) for a special case. Concluding remarks are in Section 8 and in Appendix A we briefly present numerical schemes for the integration of the variance-volatility process

2. The setting and the main results.

We consider the following SDE

| (2.1) |

where are positive and Then, Feller’s test implies that there is a unique strong solution such that a.s. when a.s. Let

| (2.2) |

and

| (2.3) |

where and

Let the partition with and consider the following process

with a.s. or more explicitly

| (2.4) |

for where represents the level of implicitness and

| (2.5) |

with

| (2.6) |

Process (2.4) is well defined when and this is true when and Furthermore, (2.4) has jumps at nodes Solving for we end up with the following explicit scheme

| (2.7) |

with solution in each step given by [19, Rel. (4.39), p.123]

which has the pleasant feature

Assumption A Let the parameters be positive and such that and consider such that for Moreover assume a.s. and for some

Theorem 2.1.

Assumption B Let Assumption A hold where now and

Theorem 2.2.

[Polynomial rate of convergence] Let Assumption B hold. The semi-discrete scheme (2.7) converges to the true solution of (2.1) in the mean square sense with rate given by,

| (2.9) |

where

and is a constant described in (4.11) and is an appropriately chosen positive parameter which satisfies (4.12) and always exist, quantity is given in Lemma 3.4 and

Inspired by [12] we remove the term from (2.4) by considering the process

| (2.10) |

which is a martingale with quadratic variation and thus a standard Brownian motion w.r.t. its own filtration, justified by Levy’s theorem [17, Th. 3.16, p.157]. Therefore, the compact form of (2.4) becomes

for Consider also the process

| (2.11) |

The process of (2.1) and the process of (2.11) have the same distribution. We show in the following that as thus the same holds for the unique solution of (2.1), i.e. as To simplify notation we write as We end up with the following explicit scheme

| (2.12) |

where is as in (2.6).

Theorem 2.3.

[Logarithmic and Polynomial rate of convergence]

Let Assumption A hold. The semi-discrete scheme (2.12) converges to the true solution of (2.1) in the mean square sense with rate given by

| (2.13) |

where is independent of and given by

where is such that

In case Assumption B holds, the semi-discrete scheme (2.12) converges to the true solution of (2.1) in the mean square sense with rate given by,

| (2.14) |

where

and is the constant described in (4.11) and is an appropriately chosen positive parameter which satisfies (4.12) and always exist, quantity is given in Lemma 3.4 and

In the following sections we write for simplicity or for

3. Logarithmic rate of convergence.

3.1. Moment bounds

Lemma 3.1 (Moment bound for SD approximation).

It holds that

for any where

Proof of Lemma 3.1.

We first observe that is bounded in the following way

a.s., where the lower bound comes from the construction of and the upper bound follows from a comparison theorem. We will bound and therefore since a.s. Set the stopping time for with the convention Application of Ito’s formula on implies

where in the second step we have used that in the third step the inequality valid for and with in the final step the fact and Taking expectations in the above inequality and using that is a local martingale vanishing at we get

where we have applied Gronwall inequality [9, Rel. 7]. We have that

thus taking expectations in the above inequality and using the estimated upper bound for we arrive at

and taking the limit as we get

Let us fix The sequence of stopping times is increasing in and as thus the sequence is nondecreasing in and as Application of the monotone convergence theorem implies

| (3.1) |

for any Using again Ito’s formula on , taking the supremum and then using Doob’s martingale inequality on the diffusion term we bound and thus ∎

Lemma 3.2 (Error bound for SD scheme).

Let integer such that It holds that

for any where the positive quantities do not depend on

Proof of Lemma 3.2.

First we take a It holds that

where we have used Cauchy-Schwarz inequality. Taking expectations in the above inequality and using Lemma 3.1 and Doob’s martingale inequality on the diffusion term we conclude

| (3.2) |

where the positive quantity except on depends also on the parameters but not on Now, for we get

where we have used Jensen inequality for the concave function Following the same lines, we can show that

| (3.3) |

for any where the positive quantity except on depends also on the parameters but not on ∎

For the rest of this section we rewrite again the compact form of (2.4) in the following way

| (3.4) |

where is given by (2.2) and the auxiliary process is close to as shown in the next result.

Lemma 3.3 (Moment bounds involving the auxiliary process).

For any it holds that

| (3.5) |

and for we have that

| (3.6) |

for any where the positive quantities do not depend on

Proof of Lemma 3.3.

We have that

for any where we have used (3.4). Using Lemma 3.1 we get the left part of (3.5). Now for and noting that

we get the right part of (3.5), where we have used Lemma 3.1. The case follows by Jensen’s inequality as in Lemma 3.2.

Furthermore, for and it holds

where we have used (3.2) and in the same manner

The case follows by Jensen’s inequality. ∎

3.2. Convergence of the auxiliary process to in

We first estimate the probability of being negative when at the same time for

Lemma 3.4.

Proof of Lemma 3.4.

By the definition (2.5) of for and for we have that

| (3.8) | |||||

where

and

The following inclusion relations hold for the event

when and where It holds that

| (3.9) |

for every standard normal random variable , where in the last step we have used [17, Ineq. (9.20), p.112] valid for . Using the fact that is a standard normal r.v. and ignoring the exponential term in (3.9), since its exponent is negative, we get that

| (3.10) |

The following inclusion relations hold for the event

when and Using again (3.9) we have that

| (3.11) | |||||

Taking probabilities in the inclusion relation (3.8) and using (3.10) and (3.11) we get

since as Finally, note that as which justifies the notation, (see for example [24]). ∎

We will use the representation (3.4) and write

| (3.12) |

Proposition 3.5.

Let Assumption A hold. Then we have

| (3.13) |

for any where and

Proof of Proposition 3.5.

Let the non increasing sequence with and We introduce the following sequence of smooth approximations of (method of Yamada and Watanabe, [27])

where the existence of the continuous function with and support in is justified by The following relations hold for with

We have that

| (3.14) |

It holds that

| (3.15) | |||||

and

| (3.16) | |||||

where we have used properties of Holder continuous functions and namely the fact that is Holder continuous for , i.e. and that is Holder continuous since Application of Ito’s formula to the sequence implies

where in the second step we have used (3.15) and (3.16) and the properties of and

Taking expectations in the above inequality yields

where we have used Lemma 3.3 in the second step and Holder inequality, Lemmata 3.1 and 3.2 in the third step and the fact that .222The function belongs to the space of real valued measurable adapted processes such that thus [21, Th. 1.5.8] implies . It holds for that

where we have used Holder inequality and Lemma 3.4 in the third step and Lemmata 3.2 and 3.1 in the final step. For we get the estimate

| (3.17) |

Thus (3.14) becomes

where in the second step we have used the asymptotic relations, as for any as for any as in the last step we have used the Gronwall inequality and is as defined in Proposition 3.5 while

Taking the supremum over all gives (3.13). ∎

3.3. Convergence of the auxiliary process to in .

Proposition 3.6.

Let Assumption A hold. Then we have

| (3.18) |

where is independent of and given by where is such that

Proof of Proposition 3.6.

We estimate the difference It holds that

where in the second step we have used Cauchy-Schwarz inequality and (3.15) and

Taking the supremum over all and then expectations we have

| (3.19) | |||||

where in the second step we have used Lemma 3.2 and Doob’s martingale inequality with since is an valued martingale that belongs to It holds that

where we have used (3.16). Now, we use again the estimate (3.17) to get

where we have used the asymptotic relations, for all as the quantity is given by and is as given in the statement of Proposition 3.5 and depends on through where as already stated before we have that as

Relation (3.19) becomes

where we have used Proposition 3.5 in the second step with the sequence as defined there, Gronwall inequality in the last step and the asymptotic relation as for any and is independent of and given by

We take with to be specified soon and note that , as since , as Moreover it holds that

Now, since there is an small enough such that We take and conclude that

as which in turn implies the asymptotic relation as with the logarithmic rate stated before. In the same way we can show as by taking We finally arrive at

by taking which implies (3.18). ∎

3.4. Proof of Theorem 2.1.

4. Polynomial rate of convergence.

We work with the stochastic time change inspired by [3]. We define the process

and the stopping time

The process is well defined since a.s. and (see Section 2).

The difference is estimated as in Section 3 and we get, as in (3.19), that

| (4.1) |

where a stopping time and independent of is as in proof of Proposition 3.6. The main difference here will be the estimation of the last term in (4.1). The approach in Section 3 resulted in the estimation where we used the Yamada-Watanabe approach. Now, we use the Berkaoui approach. Relation (3.16) becomes

where we have used the inequality

| (4.2) |

valid for all and Consequently, we get the upper bound

where we used the estimate (3.17) and Holder inequality is as in the statement of Proposition 3.5 and independent of is as in proof of Proposition 3.6. Relation (4.1) becomes

where we have used Lemma 3.3 in the second step. At this point we want to estimate the inverse moments of and to do so we consider the transformation and apply Ito’s formula to get

| (4.3) |

for where Denote the drift coefficient of the process by and consider the function

| (4.4) |

where Some elementary calculations show that this function attains its minimum at and thus

Consider the process defined through

| (4.5) |

for with Process (4.5) is a square root diffusion process and when or

| (4.6) |

is a CIR process which remains positive if By a comparison theorem [17, Prop. 5.2.18] it holds that a.s. or a.s. or equivalently a.s. The inverse moment bounds of follow by [8, Rel. 3.1]

by choosing big enough and particularly such that (4.6) holds strictly. Therefore,

| (4.7) |

Relation (4.7) for implies

| (4.8) | |||||

where in the last step we have used Gronwall’s inequality. Using again relation (4.7) for and under the change of variables we get,

where in the last steps we have used (4.8). We proceed by showing that It holds that

| (4.9) |

for any by Markov inequality. The following bound holds

thus

| (4.10) |

where It remains to bound the exponential inverse moments of defined through the stochastic integral equation (2.1). Exponential inverse moments for the CIR process are known [14, Th. 3.1] and are given by

| (4.11) |

for where the positive constant is explicitly given in [14, Rel. (10)] depends on the parameters but is independent of Thus the other condition that we require for parameter is

| (4.12) |

When (4.12) is satisfied then (4.6) is satisfied too, thus there is actually no restriction on the coefficient in (4.11) since we can always choose appropriately a such that (4.12) holds. Relation (4.10) becomes

| (4.13) |

We therefore require that

| (4.14) |

and can always find a such the above relation holds by choosing appropriately as discussed before. Relation (4.13) becomes

and therefore

where is chosen such that (4.14) holds with We conclude

by choosing where is as given in statement of Theorem 2.2.

5. Alternative approach improving the rate of convergence.

Proof of Theorem 2.3.

We will discuss the proof and highlight the differences since one can follow the proofs of Theorems 2.1 and 2.2. First of all note that Lemmata 3.1, 3.2 and 3.3 still hold, i.e. the moment bounds and error bounds of as well as the moment bounds involving the auxiliary process are true. The error now reads as

| (5.1) |

As regards the first part of Theorem 2.3, we now have that

| (5.2) |

for any where and as stated in Proposition 3.5. The bound (5.2) follows in the same lines as in the proof of Proposition 3.5 where now (3.16) becomes

| (5.3) |

and the term (3.17) disappears. Moreover, we have that

| (5.4) |

where is independent of and given by where is such that The bound (5.4) follows in the same lines as in the proof of Proposition 3.6 where now and

implying

which in turn gives

where now we take

As regards the second part of Theorem 2.3, we follow Section 4, where now we use the process

and the estimate

to get the upper bound

which in turn implies first

and then

Finally, in order to bound we require that

| (5.5) |

and can always find a such that (5.5) holds yielding

where is as given in statement of Theorem 2.3. ∎

6. Numerical Experiments.

We discretize the interval with a number of steps in power of The semi-discrete (SD) scheme is given by

| (6.1) |

for where are the increments of the Brownian motion which are standard normal r.v’s.

The ALF (Alfonsi) scheme [1, Sec. 3] is an implicit scheme which requires solving the nonlinear equation

| (6.2) |

and then computing The estimation of in (6.2) can be done for example with Newton’s method, but requires a small enough 333In the CIR case, i.e. when (6.2) simplifies to a solution of a quadratic equation. We also consider a scheme recently proposed in [12] using again the SD method, but in a different way,

| (6.3) |

for Note the similarity in the expressions of (6.3) and the SD scheme (6.1) proposed here. This is not strange, because they both rely in the same way of splitting the drift coefficient. In particular, in the explicit HAL scheme, the following process is considered

for with a.s. where now

| (6.4) |

and

| (6.5) |

A comparison with (2.2) and (2.3) shows and for We write (6.4) again as

| (6.6) |

and the process (6.6) is well defined when

| (6.7) |

The reader can compare again with (2.4) for Solving for we end up with The main result in [12] is

when (6.7) holds, implying a rate of convergence at least which is bigger than the rate of convergence of the SD scheme proposed here which is at least (see Th.2.3).

We also consider two more linear-implicit schemes that were stated in the introduction and discussed in Appendix A. Namely, we compare with the balanced implicit method (BIM) with appropriate weight functions to guarantee positivity ([16, Th. 5.9]), which reads

| (6.8) |

and the balanced Milstein method (BMM) with the suggested weight functions [16, Th. 5.9] that is given by

| (6.9) |

We take the relaxation parameter to be as recommended in [16, Rel. 5.10].

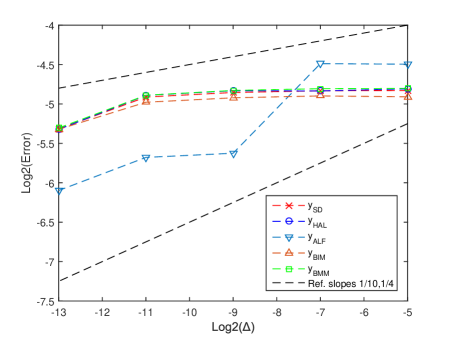

We aim to show experimentally the order of convergence for the above positivity preserving methods for the estimation of the true solution of the CEV model (2.1), i.e the semi-discrete methods SD method (6.1) and the HAL scheme (6.3), as well as the implicit ALF scheme (6.2) and the linear-implicit schemes BIM and BMM. The choice of the parameters is the same as in [15, Fig. 6] with In particular

Furthermore, we would also like to reveal the dependence of the order of the semi discrete methods on i.e. we want to verify our theoretical results and in particular the order shown in Theorem 2.3. We take the level of implicitness of SD method (6.1) to be i.e. we consider the fully implicit scheme. We also discuss about the fully explicit scheme, i.e. when but also an intermediate scheme in Section 7.

We want to estimate the endpoint norm of the difference between the numerical scheme evaluated at step size and the exact solution of (2.1). For that purpose, we compute batches of simulation paths, where each batch is estimated by and the Monte Carlo estimator of the error is

| (6.10) |

and requires Monte Carlo sample paths. The reference solution is evaluated at step size of the numerical scheme. For the SD case, we have shown in Theorems 2.1, 2.2 and 2.3, that it strongly converges to the exact solution. We simulate paths, where the choice for is as in [20, p.118]. The choice of the number of trajectories is also considered in [26, Sec.5] where a fundamental mean-square theorem is proved for SDEs with superlinear growing coefficients satisfying a one-side Lipschitz condition, but unfortunately it is not positivity preserving. Of course, the number of Monte Carlo paths has to be sufficiently large, so as not to significantly hinder the mean square errors.

We plot in a scale and error bars represent confidence intervals. The results are shown in Table 1 and Figure 1. Table 1 does not present the computed Monte Carlo errors with confidence, since they were at least times smaller that the mean-square errors.

| Step | SD-Error | HAL-Error | ALF-Error | BIM-Error | BMM-Error |

|---|---|---|---|---|---|

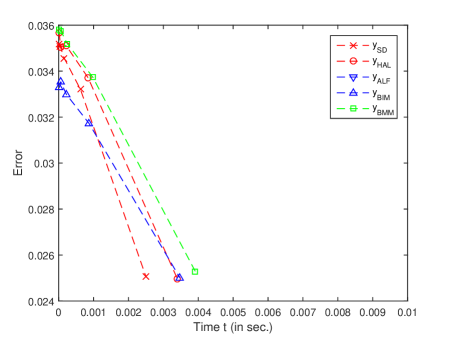

In Table 2 we present the computational times,444We simulate with GHz Intel Pentium, GB of RAM in Matlab Software. The random number generator is Mersenne Twister. The evaluated times do not include the random number generation time, since all the methods we compare, involve the same amount of random numbers. of fully implicit SD, HAL, ALF, BIM and BMM, for the same problem. Figure 2 shows the relation between the error and computer time consumption. As one can see from Table 2 the CPU times for ALF are at least times bigger than the other schemes, thus we choose in Figure 2 to restrict our attention to the rest of the methods.

| Step | Implicit SD | HAL | ALF | BIM | BMM | |

|---|---|---|---|---|---|---|

| Time/Path(in sec) | ||||||

| Time/Path(in sec) | ||||||

| Time/Path(in sec) | ||||||

| Time/Path(in sec) | ||||||

| Time/Path(in sec) |

Finally, Table 3 presents the exact values of order of convergence for SD, HAL,ALF, BIM and BMM produced by linear regression with the method of least squares fit, in the case one considers in one case points with steps and in other case all points including

| of Points | SD | HAL | ALF | BIM | BMM | |

|---|---|---|---|---|---|---|

We show below, in Table 4, the distance between our proposed method and the other methods for the numerical approximation of (2.1). We work as before and estimate the distance

| (6.11) |

between method and by considering sufficient small and in particular for

| Step | ||||

|---|---|---|---|---|

Finally, we examine the behavior of SD w.r.t the parameter . We want to examine the impact of in the order of convergence and verify our theoretical results and in particular Theorem 2.3. Table 5 shows the order of SD w.r.t

| Order of Fully Implicit SD | |

|---|---|

The following points of discussion are worth mentioning.

-

•

The performance of all methods, as shown in Table 1 and Figure 1, implies, in terms of error estimates, that the implicit ALF scheme performs better, for values of discretization steps All the other methods, i.e. the semi discrete SD and HAL, and the BIM and BMM have a similar behavior for all ’s in the sense above as Figure 1 shows. The similarity of SD, HAL, BIM and BMM is also indicated in Table 4, where we see how close they are w.r.t. the norm, and in Table 3 where the convergence order is considered. Nevertheless, Table 4 also shows that in order to get an accuracy to at least decimal digits, which in practice may be adequate concerning that we want for example to evaluate an option and thus our results are in euros, there is no actual harm in choosing whatever of the above available methods. We may then choose the fastest one, as will be discussed later on.

-

•

We see that the strong order of convergence of implicit SD for problem (2.1) is at least as shown theoretically and presented in Table 3. We also see that all methods converge with similar orders and the theoretically rate of the ALF method [1] does not hold for these ’s. Thus, again we see that the rate in practical situations does not necessarily matter, if one has to compute with very small ’s to achieve it. Moreover, we present in Table 6 the performance of the explicit SD method and see that it is very close to the implicit, which is of course natural to happen.

-

•

In practice, the computer time consumed to provide a desired level of accuracy, is of great importance. Especially, in financial applications, a scheme is considered better when except of its accuracy, it is implemented faster. As mentioned before, the SD method as well as the HAL method performs well in that aspect, compared to the implicit ALF method, which requires the estimation of a root of a nonlinear equation in each step and is therefore time consuming. This is presented in Table 2 and Figure 2 which illustrates the advantage of the semi-discrete method SD, performing slightly better than HAL and BMM, better than BIM, and of course a lot better compared with ALF (over times quicker to achieve an accuracy of almost decimal digits.) Moreover, the explicit SD, performs slightly better in that aspect, as shown in Table 7.

Step Fully Explicit SD (Implicit) Time/Path(in sec) Time/Path(in sec) Time/Path(in sec) Time/Path(in sec) Time/Path(in sec) Table 7. Average computational time for a path (in seconds) for fully explicit SD method for -

•

A negative step of a numerical method appears when the computer-generated random variable exceeds a certain threshold, which tends to increase as the step size decreases. Thus, the undesirable effect of negative values that are produced by some numerical schemes (such as the explicit Euler (EM) and standard Milsten (M) ), tends to disappear, since after a certain small step size, the threshold exceeds the maximum standard normal random number attainable by the computer system.

7. Approximation of stochastic model (1.1).

So far we have focused on the process which is one part of the two-dimensional system (1.1). Nevertheless, it can be treated independently, since the only way that it interacts with the process is through the correlation of the Wiener processes. First we apply Ito’s formula on to get,

| (7.1) |

Then, we consider two different schemes for the integration of (7.1).555The reason for not considering other schemes such as the two-dimensional Milstein is that they generally are time consuming, since they involve additional random number generation for the approximation of double Wiener integrals. The first is the EM scheme which reads

| (7.2) |

has strong convergence order and is easy to implement. The second scheme, which is based on an interpolation of the drift term and an interpolation of the diffusion term, considering decorrelation of the diffusion term, including a higher order Milstein term [15, Sec.4.2], is denoted IJK and is given by [15, Rel.(137)]

| (7.3) | |||||

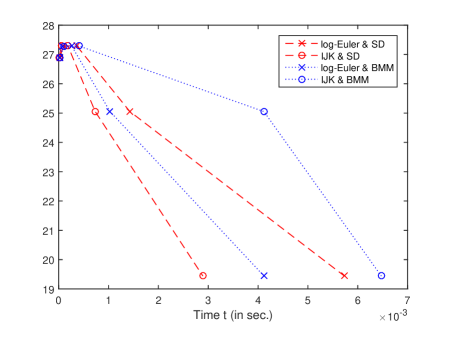

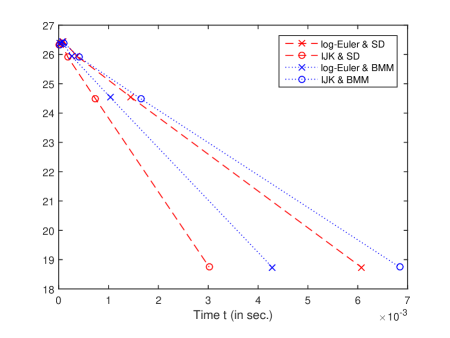

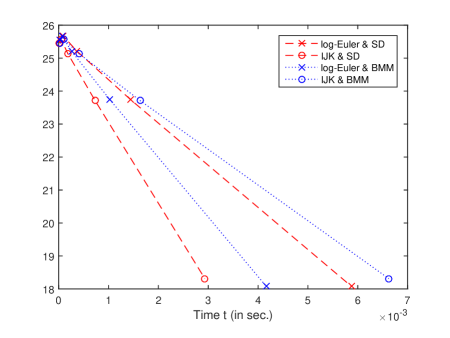

We therefore consider the EM scheme (7.2) combined with SD (6.1), the IJK scheme (7.3) combined with SD (6.1) and compare with the case where the stochastic variance is integrated with BMM scheme (6.9), for three different correlation parameters, and with as in [15, Sec.5]. We present in Tables 8, 9 and 10 and Figures 3, 4 and 5, the errors, in the sense of distance (6.11), for all the above considered ways of numerical integration of process for different step sizes, as well as the average computational time (in seconds) consumed for each discretization.

| Step | EMSD-Error | IJKSD-Error | EMBMM-Error | IJK BMM-Error |

|---|---|---|---|---|

| Step | EMSD-Error | IJKSD-Error | EMBMM-Error | IJK BMM-Error |

|---|---|---|---|---|

| Step | EMSD-Error | IJKSD-Error | EMBMM-Error | IJK BMM-Error |

|---|---|---|---|---|

8. Conclusion.

In this paper, we exploit further the semi-discrete method (SD), originally appeared in [10], to numerically approximate stochastic processes that appear in financial mathematics and are meant to be non negative. In [13] we examined the Heston model, that is a mean reverting process with super-linear diffusion, described by a SDE of the form (2.1) with Now, we deal with SDEs with sub-linear diffusion coefficients of the type with These kind of SDEs, called mean reverting CEV processes, appear in stochastic models, where they represent the instantaneous volatility-variance of an underlying financially observable variable. We prove theoretically the strong convergence of our proposed SD scheme, revealing the order of convergence. The resulting polynomial rate in Theorem 2.3, may not appear appealing at first sight, because of its low magnitude. Nevertheless, as it is shown in the numerical experiment section, where a comparative study is presented between various positivity preserving schemes, the SD method seems to be the best w.r.t. CPU time consumption. The advantage of the SD method here is that although implicit, has an explicit formula and thus requires fewer arithmetic operations and consequently less computational time. Moreover, our method can cover cases where (2.1) has time varying coefficients, i.e.

We also treat the whole two-dimensional stochastic volatility model (1.1). In order to do that, we actually integrate the process which satisfies a SDE of the form (7.1) and in the end transform back for We only consider two different schemes for the integration of namely the Euler Maruyama (EM) scheme, which is easy to implement and the IJK scheme [15, Rel.(137)] which is shown to be the most efficient method, robust and simple as EM [15]. We do not apply other two-dimensional schemes, such as for example the Milstein scheme, since they are in general time consuming, as they involve approximations of double Wiener integrals which require additional random number generation. We therefore combine the EM scheme with SD ((7.2) (6.1)), the IJK scheme with SD ((7.3) (6.1)) and compare with the case where the stochastic variance is integrated with BMM scheme (6.9), for three different correlation parameters, and with as in [15, Sec.5]. The combination IJK with SD seems to be the most favorable w.r.t. CPU time, for all the cases.

References

- [1] A. Alfonsi, Strong order one convergence of a drift implicit Euler scheme: Application to the CIR process, Stat. Prob. Let., 83 (2013), pp. 602-607.

- [2] L.B.G. Andersen, V.V. Piterbarg, Moment explosions in stochastic volatility models, Finance Stoch., 11 (2007), pp. 29-50.

- [3] A. Berkaoui, Euler scheme for solutions of stochastic differential equations, Portugalia Mathematica Journal, 61, (2004), pp. 461-478.

- [4] M.J. Brennan, E.S. Schwartz, Analyzing convertible bonds, Journal of Financial and Quantitative Finance, 4, (1980), pp. 907-929.

- [5] K.C. Chan, G.A Karolyi, F.A. Longstaff, A.B. Sanders, An empirical comparison of short-term interest rate, Journal of Finance, 47(3), (1992), pp. 1209-1227.

- [6] J.C. Cox, J.E. Ingersoll, S.A. Ross, A theory of the term structure of interest rates, Econometrica, 53, (1985), pp. 385-407.

- [7] S.G. Cox, M. Hutzenthaler, A. Jentzen, Local Lipschitz continuity in the initial value and strong completeness for nonlinear stochastic differential equations, arXiv:1309.5595v1, (2013).

- [8] S. Dereich, A. Neunkirch, L. Szpruch, An Euler-type method for the strong approximation of the Cox-Ingersoll-Ross process, Proceedings of The Royal Society, (2011).

- [9] T.H. Gronwall, Note on the derivatives with respect to a parameter of the solutions of a system of differential equations, Annals of Mathematics, 20, (1919), pp. 292-296.

- [10] N. Halidias, Semi-discrete approximations for stochastic differential equations and applications, International Journal of Computer Mathematics, 89(6), (2012), pp. 1-15.

- [11] N. Halidias, A new numerical scheme for the CIR process, Monte Carlo Methods Appl., (2015a).

- [12] N. Halidias, An explicit and positivity preserving numerical scheme for the mean reverting CEV model, http://arxiv.org/pdf/1501.03434, (2015b).

- [13] N. Halidias, I.S. Stamatiou, On the numerical solution of some nonlinear stochastic differential equations using the semi-discrete method, to appear in Computational Methods in Applied Mathematics, Special Issue, (2015).

- [14] T.R. Hurd, A. Kuznetsov, Explicit formulas for Laplace transforms of stochastic integrals, Markov Process. Relat. Fields, 14, (2008), pp. 277-290.

- [15] C. Kahl, P. Jackel, Fast strong approximation Monte Carlo schemes for stochastic volatility models, Quantitative Finance, 6, (2006), pp. 513-536.

- [16] C. Kahl, H. Schurz, Balanced Milstein Methods for ordinary SDEs, Monte Carlo Methods and Appl, 12(6), (2006), pp. 143-170.

- [17] I. Karatzas, S.E. Shreve, Brownian motion and stochastic calculus, Springer-Verlag New York, (1988).

- [18] P. Kloeden, A. Neuenkirch, Convergence of numerical methods for stochastic differential equations in mathematical finance, Recent developments in Computational Finance, (T. Gerstner and P. Kloeden, eds), (2013), pp. 49-80.

- [19] P. Kloeden, E. Platen, Numerical solution of stochastic differential equations, Vol 23, Stochastic Modeling and Applied Probability, Springer-Verlag Berlin, corrected 2nd printing, (1995).

- [20] P. Kloeden, E. Platen, H. Schurz, Numerical solution of stochastic differential equations through computer experiments, Springer-Verlag Berlin, corrected 3rd printing, (2003).

- [21] X. Mao, Stochastic Differential Equations and Applications, Horwood Publishing, (1997).

- [22] G. Maruyama, Continuous Markov processes and stochastic equations, Rend. Circ. Mat. Palermo, 4(1), (1955), pp. 48-90.

- [23] G.N. Milstein, E. Platen, H. Schurz, Balanced implicit methods for stiff stochastic systems, SIAM J. Numer. Anal., 35(3), (1998), pp. 1010-1019.

- [24] F.W.J. Olver, Asymptotics and special functions, AKP classics, Wellesley, Mass, (1997).

- [25] H. Schurz, Numerical regularization for SDEs: construction of nonnegative solutions, Dyn. Systems Appl., 5, (1996), pp. 323-352.

- [26] M.V. Tretyakov, Z. Zhang, A fundamental mean-square convergence theorem for SDEs with locally Lipshcitz coefficients and its applications, SIAM J. Numer. Anal., (2013), pp. 3135-3162.

- [27] T. Yamada, S. Watanabe, On the uniqueness of solutions of stochastic differential equations, J. Math. Kyoto Univ., 11, (1971), pp. 155-167.

Appendix A Some numerical schemes for the integration of the variance-volatility process

We consider a partition of the time interval with and discretization steps for Moreover, we denote by the increments of the Brownian motion. We show in the following subsections some numerical schemes for the approximation of

| (A.1) |

and make some brief comments on them. We also denote

Standard Euler-Maruyama scheme

The Euler method, applied to the SDE setting, already appeared in the through Maruyama [22] and thereafter there has been an extensive study on numerical approximations of solutions of SDEs (we just mention [18] for a recent review on numerical methods for SDEs with applications in finance and references therein).

Standard Milstein scheme

The standard one dimensional Milstein (M) scheme contains some extra terms derived by Ito-Taylor expansion [19, Sec.5], and applied to reads

| (A.3) |

for where we have retained terms of order Again (M) scheme has a finite life time.

Balanced Implicit Method

The balanced implicit method (BIM) [23, Rel (3.2)] was the first attempt to treat the problem of invariance-preserving of specific domains of the underlying process and reads

| (A.4) |

for where and are appropriate weight functions. The choice and preserves positivity [16, Sec. 5]. Rearranging the above equation, we get the expression

| (A.5) |

Balanced Milstein Method

The balanced Milstein method (BMM), was proposed in [16], for an improvement of the BIM in the stability behavior but also both in the rate of convergence. It is given by the following linear implicit relation

for where and are appropriate weight functions. The choice where and implies an eternal life time for the scheme [16, Th. 5.9], in the sense that The step sizes have to be such that The relaxation parameter resembles to the implicitness parameter ( in our notation). For there is no restriction in the step size, but it is recommended when possible [16, Rem. 5.10] to take Rearranging with the above specifications leads to

| (A.6) |

Finally, the proposed semi-discrete (SD) scheme reads

| (A.7) |

Increasing the time horizon results in an increase of the percentage of negative paths of EM and M. On the other hand BIM, BMM and of course SD are not affected by that, since they preserve their positivity on any interval