On multivariate associated kernels for smoothing

general density functions

Abstract

Multivariate associated kernel estimators, which depend on both target point and bandwidth matrix, are appropriate for partially or totally bounded distributions and generalize the classical ones as Gaussian. Previous studies on multivariate associated kernels have been restricted to product of univariate associated kernels, also considered having diagonal bandwidth matrices. However, it is shown in classical cases that for certain forms of target density such as multimodal, the use of full bandwidth matrices offers the potential for significantly improved density estimation. In this paper, general associated kernel estimators with correlation structure are introduced. Properties of these estimators are presented; in particular, the boundary bias is investigated. Then, the generalized bivariate beta kernels are handled with more details. The associated kernel with a correlation structure is built with a variant of the mode-dispersion method and two families of bandwidth matrices are discussed under the criterion of cross-validation. Several simulation studies are done. In the particular situation of bivariate beta kernels, it is therefore pointed out the very good performance of associated kernel estimators with correlation structure compared to the diagonal case. Finally, an illustration on real dataset of paired rates in a framework of political elections is presented.

keywords:

Asymmetric kernel , boundary bias , correlation structure , bandwidth matrix , nonparametric estimation , mode-dispersion.Mathematics Subject Classification 2010: 62G07(08); 62H12 Short Running Title: Multivariate associated kernels

1 Introduction

Nonparametric estimation of unknown densities on partially or totally bounded supports, with or without correlation in its multivariate components, is a recurrent practical problem. Because of symmetry, the multivariate classical or symmetric kernels, not depending on any parameter, are not appropriate for these densities. In fact, these estimators give weights outside the support causing a bias in boundary regions. In order to reduce the boundary problem with multivariate symmetric kernels as Gaussian, Sain (2002) and recently Zougab et al. (2014) have proposed adaptive full bandwidth matrix selection; but the bias does not disappear completely. Chen (1999, 2000) is one of the pioneers who has proposed, in univariate continuous case, some asymmetric kernels (i.e. beta and gamma) whose supports coincide with those of the densities to be estimated. Also recently, Libengué (2013) investigated several families of these univariate continuous kernels that he called univariate associated kernels; see also Kokonendji et al. (2007), Kokonendji and Senga Kiéssé (2011), Zougab et al. (2012, 2013) for univariate discrete situations. This procedure cancels of course the boundary bias; however, it creates a quantity in the bias of the estimator which needs reduction; see, for instance, Malec and Schienle (2014), Hirukawa and Sakudo (2014) and Igarashi and Kakizawa (2015).

Several approaches on multivariate kernel estimation have been proposed for various processings. Garcìa-Portugués et al. (2013) used product of kernels for estimating the different nature of both directional and linear components of a random vector. A classical kernel density estimation on the rotation group appropriate for crystallographic texture analysis has been investigated by Hielscher (2013). Symmetric kernel smoothers with univariate local bandwidth have been studied by González-Manteiga et al. (2013) for semiparametric mixed effect models. Girard et al. (2013) presented frontier estimation with classical kernel regression on high order moments. In discrete case, Aitchison and Aitken (1976) provided kernel estimators for binary data while Racine and Li (2004) proposed the product of them with classical continuous one for smoothing regression on both categorical and continuous data. In the same spirit of Racine and Li (2004), Bouerzmarni and Rombouts (2010) considered some products of different univariate associated kernels in continuous case; i.e. the bandwidth matrix obtained is diagonal. In the classical kernels case, Chacón and Duong (2011) and Chacón et al. (2011) have shown the importance of full bandwidth matrices for certain target densities. See also Hazelton and Marshall (2009) for a support with arbitrary shape.

The main goal of this work is to introduce the multivariate associated kernels with the most general bandwidth matrix. In other words, the support of the suggested associated kernels coincides to the support of the densities to be estimated; also, the full bandwidth matrices take into account different correlation structures in the sample. Note that, a full bandwidth matrix significantly improves some complex target densities (e.g. multimodal); see Sain (2002). In high dimensions, the computational choice of this full bandwidth matrix needs some special techniques. We can refer to Chacón and Duong (2010, 2011) and Chacón et al. (2011) for classical (symmetric) kernels. For illustrations in the present paper, we then focus on a bivariate case as beta kernel with correlation structure introduced by Sarmanov (1966); see also Lee (1996). A motivation to investigate the smoothing of these densities on comes from a joint distribution of two comparable proportions. Many datasets in can be found in statistical problems, for example, for comparing two rates. We shall examine the theoretical bias reduction and practical performances of the full bandwidth selection and two others bandwidth matrix parametrization using least squares or unbiased cross validation; see, e.g., Wand and Jones (1993).

The rest of the paper is organized as follows. Section 2 gives a complete definition of multivariate associated kernels which includes both the product and the classical symmetric ones. A method to construct any multivariate associated kernel from a parametric probability density function (pdf) is then provided. Some pointwise properties of the corresponding estimator are investigated, in particular the convergence in the sense of mean integrated squared error (MISE) and an algorithm of the bias reduction. Section 3 provides a particular study of a bivariate beta kernel with a correlation structure introduced by Sarmanov (1966). Also, some algorithms for the choice of the optimal bandwidth matrix by unbiased cross validation method are presented. This is followed, in Section 4, by simulation studies and a real data analysis of electoral behaviour of a population with regard to a candidate. Especially, the role of forms of bandwidth matrices is explored in details. Section 5 concludes with summary and final remarks, while the proof of a proposition is deferred to the appendix of Section 6.

2 Multivariate associated kernel estimators

Let be independent and identically distributed (iid) random vectors with an unknown density function on , a subset of (). As frequently observed in practice, the subset might be unbounded, partially bounded or totally bounded as:

| (2.1) |

for given reals and with nonnegative values of , and in such that . A multivariate associated kernel estimator of is simply defined by

| (2.2) |

where is a bandwidth matrix (i.e. symmetric and positive definite) such that (the null matrix) as , and is the so-called associated kernel, parametrized by and , and precisely defined as follows.

Definition 2.1

Let be the support of the pdf to be estimated, a target vector and a bandwidth matrix. A parametrized pdf of support is called “multivariate (or general) associated kernel” if the following conditions are satisfied:

| (2.3) | |||

| (2.4) | |||

| (2.5) |

where denotes the random vector with pdf and both and tend, respectively, to the null vector and the null matrix as goes to .

Remark 2.2

-

(i)

The function is not necessary symmetric and is intrinsically linked to and .

-

(ii)

The support is not necessary symmetric around of ; it can depend or not on and .

-

(iii)

The condition (2.3) can be viewed as and it implies that the associated kernel takes into account the support of the density , to be estimated.

-

(iv)

If does not contain then this is the well-known problem of boundary bias.

- (v)

-

(vi)

The form of orientation of the kernel is controlled by the parametrization of bandwidth matrix ; i.e. a full bandwidth matrix allows any orientation of the kernel and therefore any correlation structure.

The following two examples provide well-known and also interesting particular cases of multivariate associated kernel estimators. The first can be seen as an interpretation of associated kernels through symmetric kernels. The second deals on associated kernels without correlation structure.

Example 2.3

(Classical kernels) The kernel estimator of the density , appropriate for unbounded supports in particular , is usually defined by:

| (2.6) |

where is a target, a bandwidth matrix and or sometimes for all . The function is the multivariate kernel assumed to be spherically symmetric and it does not depend on any parameter in particular and . The kernel function has also mean vector and covariance matrix respectively equal to zero and ; in general, the covariance matrix is the identity matrix: . This function is here called classical kernel.

The following result connects a classical kernel to its corresponding symmetric or classical (multivariate) associated kernel.

Proposition 2.4

Let be the support of the density to be estimated. Let be a classical kernel with support , mean vector and covariance matrix . Given a target vector and a bandwidth matrix , then the classical kernel induces the so-called classical (multivariate) associated kernel: (i)

| (2.7) |

on with (i.e. ) and ; (ii)

on with (i.e. ) and .

Proof. We only proof (i) because (ii) is similar. From (2.2) and (2.6) with , we easily deduce the expression (2.7). From (2.7) and Definition 2.1, for a fixed and for all , there exists such that and therefore . This implies, from (2.3), that . The last two results are simply derived from calculating the covariance matrix and the mean vector of (the random vector of pdf ) by making the previous substitution .

It is known that the choice of classical kernels is not important; nevertheless, the best classical kernel is the Epanechnikov (1969) one in the sense of MISE with bounded support . The most popular is the Gaussian kernel with , and therefore ; see Chacón and Duong (2010) and Zougab et al. (2014). An interpretation of any classical multivariate associated kernel can be presented as follows: through the symmetry property of the classical kernel, the mean coincides with the mode which is the target ; separately and in contrario to the general case (2.5), the dispersion measure around of the target , which does not here depend on , serves essentially to the smoothing parameters or to the bandwidth matrix. This is the basic concept of general associated kernels and it is a different approach with respect to the convolution point of view. Note that the bandwidth matrix is similar to the dispersion matrix, which is symmetric and positive definite; see for instance Jørgensen (2013). For univariate dispersion parameter, we can refer to Jørgensen (1997) and Jørgensen and Kokonendji (2011) for different uses.

Example 2.5

(Multiple kernels) The product kernel estimator introduced by Bouerzmarni and Rombouts (2010) can be defined as a product of univariate associated kernel estimators of Libengué (2013). We here call it “multiple associated kernel estimator” of the density :

| (2.8) |

where is the support of univariate margin of for , , for , and are the univariate bandwidth parameters. The function is the th univariate associated kernel on the support . In principle, this estimator is more appropriate for bounded or partially bounded distributions without correlation in its components. A particular multiple associated kernel estimator is obtained by using univariate classical kernels.

In the following proposition, we point out that all multiple associated kernels are multivariate associated kernels without correlation structure in the bandwidth matrix.

Proposition 2.6

Let be the support of the density to be estimated with the supports of univariate margins of . Let and with . Let be a univariate associated kernel (see Definition 2.1 for ) with its corresponding random variable on for all . Then, the multiple associated kernel is also a multivariate associated kernel:

| (2.9) |

on with and = . In other words, the random variables are independent components of the random vector .

Proof. From (2.2) and (2.8), the expression (2.9) is easily deduced. The remainder results are obtained directly by calculating the mean vector and covariance matrix of which is the random vector of the pdf (2.9).

The multiple associated kernels have been illustrated in bivariate case by Bouerzmarni and Rombouts (2010). For simulation studies, the authors used two independent univariate beta kernels and also two independent univariate gamma kernels. It is easy to generalize the investigation from two to more independent univariate associated kernels.

If we have an associated kernel, an estimator can be easily deduced as in (2.2). Otherwise, a construction of associated kernels is possible by using an appropriate pdf. The pdf used must have at least the same numbers of parameters than the number of components in the couple as parameters of the expected associated kernel. The rest of this section is devoted to a construction of the multivariate associated kernels and then to some properties of the corresponding estimators.

2.1 Construction of general associated kernels

In order to build a multivariate associated kernel , we have to evaluate the dimensions of and . We always have components for the target vector which is completely separate from the bandwidth matrix in the classical multivariate associated kernel; but, in general, is intrinsically linked to .

| General | Multiple | Classical | |

|---|---|---|---|

| Full | |||

| Scott | |||

| Diagonal |

Table 2.1 gives the exact or minimal numbers () of parameters in according to different forms of . The bandwidth matrix is said full (i.e. with complete structure of correlations) and admits parameters. It is said diagonal if , i.e. without correlation, and has only parameters. We denote by the Scott bandwidth matrix the form with only one parameter and fixed ; see Scott (1992, page 154). In practice, the matrix can be fixed empirically from the data. Although is the same for classical and general associated kernels in Table 2.1, the differences arise because of separation or not between and and, also, the presented are exact numbers for classical and minimal numbers for both general and multiple associated kernels. It becomes clear that any pdf, with at least parameters and having a unique mode and a dispersion matrix, can lead to an associated kernel. Now, we introduce the notion of type of kernel which is necessary for the construction from a given pdf.

Definition 2.7

A type of kernel is a parametrized pdf with support , , such that is squared integrable, unimodal with mode and admitting a dispersion matrix (which is symmetric and positive definite); i.e. a vector with given in Table 2.1 and the first coordinates of corresponds to those of .

Let us denote by the dispersion matrix of around the fixed vector . Here is a series of facts to have in mind.

Lemma 2.8

Let be a type of kernel on . The three following assertions are satisfied:

-

(i)

the mode vector of always belongs in ;

-

(ii)

where is the mean vector of ;

-

(iii)

if tends to the null matrix, then also goes to the null matrix.

Proof. (i) and (ii) are trivial. As for (iii), it is easy to check that . Thus, tends to the null matrix means goes to the Dirac probability in the sense of distribution; then, goes to the null vector and therefore also goes to the null matrix.

Without loss of generality, we only present a construction of general (or multivariate) associated kernels excluding both multiple and classical ones. In fact, Libengué (2013) built some univariate associated kernels that can be used in multiple associated kernels. For this, he proposed a “mode-dispersion principle” saying that it must put the mode on the target and the dispersion parameter on the bandwidth. In the same spirit, we here propose a construction of general associated kernels using the multivariate mode-dispersion method given in (2.11) below.

Indeed, since is a vector, we must vectorize the couple where is the target and is the bandwidth matrix. According to the symmetry of , we use the so-called half vectorization of . That is defined as , where

| (2.10) |

is a vector obtained by stacking the columns of the lower triangular of ; see, e.g., Henderson and Searle (1979). Making general associated kernels from a type of kernel on with by multivariate mode-dispersion method requires solving the system of the equations

| (2.11) |

The solution of (2.11), if there exists, is a vector denoted by . For , the system (2.11) provides the result in Libengué (2013). A light version will be presented for bivariate case () in Section 3.2. For classical associated kernels, the system (2.11) means to solve directly . More generally, the solution of (2.11) depends on the flexibility of the type of kernel and leads to the corresponding associated kernel denoted . The constructed associated kernel satisfies Definition 2.1 of multivariate associated kernel:

Proposition 2.9

The associated kernel function , obtained from (2.11) and having support , is such that:

| (2.12) | |||

| (2.13) | |||

| (2.14) |

where is the random vector with pdf and both and tend, respectively, to the null vector and the null matrix as goes to .

Proof. The multivariate mode-dispersion method (2.11) implies which leads to . Since is unimodal of mode (see Part (i) of Lemma 2.8), we obviously have (2.12), and then (2.3) is checked, because is identified to in (2.11). Let be the random vector with unimodal pdf as the type of kernel . From Part (ii) of Lemma 2.8 we can write

where is the difference between the mean vector and the mode vector of . Thus, from the mode-dispersion method (2.11), we have and ; taking , Part (iii) of Lemma 2.8 leads to the second result (2.13), and therefore (2.4) is verified. Also, since admits a moment of second order, the covariance matrix of exists and that can be written as ; solving (2.11) and then taking , the last result (2.14) holds in the sense of (2.5) using again Part (iii) of Lemma 2.8.

In practice, both characteristics and are derived from the calculation of the mean vector and covariance matrix of in terms of the mode vector and the dispersion matrix . In a general way, a given or the constructed associated kernel in Proposition 2.9 (that we will call standard version) creates a quantity in the bias of the kernel density estimation. In order to eliminate this quantity in the larger part of the support of the density to be estimated, we will also study a modified version of the standard one. The following two subsections investigate some properties of these estimators.

2.2 Standard version of the estimator

Here, we give some properties of the estimator of through a given associated kernel presented in Definition 2.1 or the constructed associated kernel in Proposition 2.9; i.e. . For a given bandwidth matrix , similarly to (2.2) we consider

| (2.15) |

Proposition 2.10

For given ,

| (2.16) |

and . Furthermore, one has

| (2.17) |

where the total mass is a positive real and, it is also a finite constant if for all .

Proof. The first result (2.16) is straightforwardly obtained from (2.15) as follows:

Also, the estimates and the total mass stem immediately from the fact that is a pdf. Finally, the values of belonging to the set , we have (2.17) as

since the integration vector of is on the target which is a parameter of .

From the above Proposition 2.10, the total mass of by a non-classical associated kernel generally fails to be equal to 1; an illustration for is given in Table 3.2 below. Hence, non-classical associated kernel estimators are improper density estimates or as kind of “balloon estimators”; see Sain (2002) and Zougab et al. (2014). The fact that is close to 1 can find a statistical explanation in both Examples 1 and 2 of Romano and Thombs (1996), or by showing which does not depend on : with for all . Without loss of generality, we study up to normalizing constant which is used at the end of the density estimation process.

Proposition 2.11

Let be a target and a bandwidth matrix as . Assume in the class , then

| (2.18) | |||||

Furthermore, if is bounded on then there exists the largest positive real number such that , and

| (2.19) |

with and where “” stands for “ and then approximation as ”.

Proof. See Appendix in Section 6.

The univariate case () of Proposition 2.11 can be found in Libengué (2013); see Chen (1999, 2000) for both beta and gamma kernels with and, also, Hirukawa and Sakudo (2014) for other values of . In the situation of multiple associated kernels (2.9), in contrario to (2.18) the general representation (2.19) is simply expressed in terms of univariate associated kernels as follows:

Corollary 2.12

Proof. Easy.

Now, we recall natural measures for assessing the similarity of the multivariate associated kernel estimator according to the true pdf , to be estimated. Since the pointwise measure is the mean squared error (MSE) and expressed by

| (2.20) |

the integrated form of MSE on is and its approximate expression satisfies

| (2.21) | |||||

In the general case of associated kernels with correlation structure, an optimal bandwidth matrix that minimizes the AMISE (2.21) still remains challenging problem, even in the bivariate case. However, the particular case of diagonal bandwidth matrix is for multiple gamma kernels; see Bouerzmarni and Rombouts (2010) for further details. So, the next result only gives the optimal bandwidth matrix for the Scott form which still has a correlation structure.

In fact, let us consider be a Scott bandwidth matrix with fixed matrix and positive as . From Definition 2.1, Proposition 2.4 and Proposition 2.9, it follows that there exists a vector and a matrix of finite constants connected respectively to and such that for all , and . Using Proposition 2.11 and assuming such that its all first and second partial derivatives are bounded, one has:

where and are positive scalars. From (2.20), it follows that . By integration of , one obtains

| (2.22) |

with and the anti-derivatives of respectively and on . Taking the derivative of the second member of the inequality (2.22) equal to leads to the following proposition.

Proposition 2.13

Note that we can use the Scott bandwidth matrix if (2.23) holds. However, in practice, we cannot check (2.23) because is unknown. But, if the quantity of (2.23) becomes 0 (resp. ) then one observes an undersmoothing (resp. oversmoothing). Finally, the practical choice of in (2.24) can be the sample covariance matrix.

Unlike to classical associated kernels for (Example 2.3), the choice of non-classical associated kernels is very important for the support of the pdf to be estimated; see Parts (i)-(iv) of Remark 2.2. Also, from Parts (v)-(vi) of Remark 2.2, different positions of the target and correlation structure need a suitable general associated kernel. Nevertheless, the selection of bandwidth matrix remains crucial when the general associated kernel is chosen; see, e.g. Chacón and Duong (2011) and Chacón et al. (2011). Here, we consider the multivariate least squares cross validation (LSCV) method to select the bandwidth matrix. From (2.15), the LSCV method is based on the minimization of the integrated squared error (ISE) which can be written as

Minimizing this means to minimize the two first terms. However, we need to estimate the second term since it depends on the unknown pdf . The LSCV estimator of is

where is being computed as excluding the observation . The bandwidth matrix obtained by the LSCV rule selection is defined as follows:

| (2.25) |

where is the set of all positive definite full bandwidth matrices. The LSCV rule is the same for the Scott and diagonal bandwidth matrices where and are their respective sets. The difficulty comes from the level of dimension of which is, respectively, , and for , and . Thus, for high dimension , the set of the Scott bandwidth matrices might be a good compromise between computational problems and correlation structures in the sample.

2.3 Modified version of the estimator

Following Chen (1999, 2000), Libengué (2013), Malec and Schienle (2014), Hirukawa and Sakudo (2014) and Igarashi and Kakizawa (2015) in univariate case, a second version of the estimator (2.15) is sometimes necessary. Indeed, the presence of the non null term with the gradient in (2.18) increases the pointwise bias of . Thus, we propose below an algorithm for eliminating the term of gradient in the largest region of . Since Bouerzmarni and Rombouts (2010) has shown the results for multiple associated kernels, we here investigate the case of general associated kernels with .

The algorithm of bias reduction has two steps. The first step consists to define both inside and boundary regions. The second one deals on the modified associated kernel which leads to the bias reduction in the interior domain.

First step. Partitioning into two regions of order which is a vector, and where tends to the null vector as goes to the null matrix :

-

a.

interior region is the largest one inside the interior of in order to contain at least 95 percent of observations, and it is denoted by ;

-

b.

boundary regions representing the complementary of in , and it is denoted by which could be empty; recall that and .

Since might have each one of its convex components as unbounded, partially bounded or totally bounded interval as in (2.1), there is only one but

| (2.26) |

boundary subregions of . In the below Section 3.3.2 an illustration is provided for with and, therefore, the number of boundary subregions (2.26) is .

Second step. Changing the general associated kernel into its modified version ; that leads to replace the couple into with because in the interior, and . This modified associated kernel is such that, for any fixed bandwidth matrix ,

| (2.27) |

must be continuous on and constant on .

Proposition 2.14

The function on its support and obtained from (2.27) is also a general associated kernel.

Proof. Since is a general associated kernel for all , one gets the first condition of Definition 2.1 because . According to Proposition 2.9 it follows that, for a given random variable with pdf , we obtain the last two conditions of Definition 2.1 as

Both quantities and tend, respectively, to and as goes to . In particular, from (2.27) we have

Similar to both (2.2) and (2.15), the modified associated kernel estimator using is then defined by

| (2.28) |

The following result gives only in the interior of the pointwise expressions of the bias and the variance of . Of course, the corresponding expressions in the boundary regions are tedious to write with respect to the (2.26) boundary situations from (2.27).

Proposition 2.15

Proof. We have the first result (2.29) by replacing in (2.18) , and by , and , respectively. For the last result, considering (2.19) it is sufficient to show that

Since and are general associated kernels of the same type with and , then there exists a common largest positive real number such that

with . Taking , we have and . Since then .

Thus, we define the asymptotic expression of the MISE of in the interior as follows:

All the results in this section can be easily deduced for both cases of diagonal and Scott bandwidth matrices. The following section provides some detailed results for with a bivariate beta kernel having correlation structure on . The corresponding associated kernel is built from a technique due to Sarmanov (1966) and using two independent univariate beta pdfs. See Balakrishnan and Lai (2009), Kundu et al. (2010) for some other examples of bivariate types of kernels and Kotz et al. (2000) in multivariate case.

3 Bivariate beta kernel with correlation structure

This section presents the generalizable procedure of a bivariate beta kernel estimator from a bivariate beta pdf with correlation structure to its corresponding associated kernel. The standard associated kernel is built by a variant of the mode-dispersion method deduced from (2.11). Then, we provide properties of both versions of the corresponding estimators.

3.1 Type of bivariate beta kernel

In order to control better the effects of correlation, we here consider a flexible type of bivariate beta kernel for which the correlation structure is introduced by Sarmanov (1966); see also Lee (1996). Let us take two independent univariate beta distributions with pdfs

| (3.1) |

where is the usual beta function with and . Their means and variances are, respectively,

| (3.2) |

Also, are unimodal for , and , with mode and dispersion parameters:

| (3.3) |

The corresponding pdf (or type of kernel) of the bivariate beta-Sarmanov with correlation and from of (3.1) is then denoted by () and defined as:

| (3.4) |

with and . Depending on and , the correlation parameter belongs to the following interval

| (3.5) |

with nonnegative reals

and

Thus, the mean vector and covariance matrix of are, respectively,

The unimodality of in (3.4) also occurs for , and with . However, the corresponding mode vector of does not have an explicit expression; but, we numerically verified that this mode vector is slightly shifted with respect to the modal vector (3.3) of the two independent margins that we denote by for .

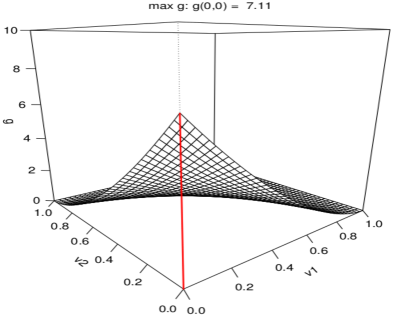

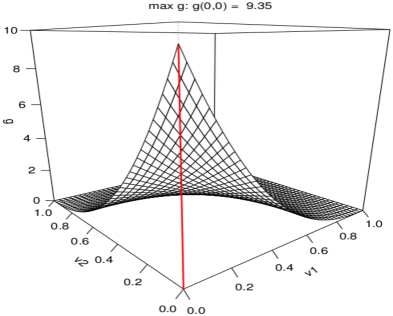

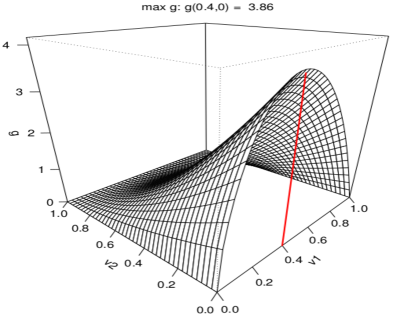

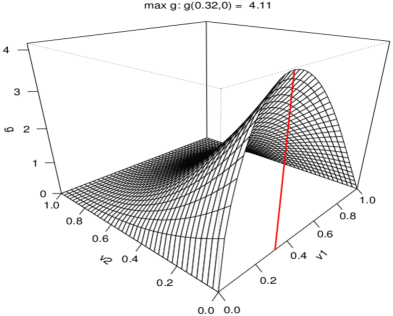

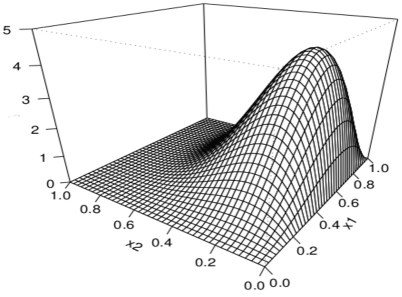

Figure 3.1 illustrates some different effects of both null and positive correlations (3.5) on the unimodality of (3.4). The negative correlations will show the opposite effects in terms of positions according to the modal vector for . In other words, the correlation parameter enables the pdf to reach points which are inaccessible with the null correlation. The parameter values of both univariate beta (3.1) used for Figure 3.1 produce the following intervals (3.5) of correlation:

-

1.

if for an angle;

-

2.

if for an edge;

-

3.

if for the interior.

Concerning the dispersion matrix of the bivariate beta-Sarmanov type we consider

| (3.6) |

where and are the dispersion parameters (3.3) of margins and the correlation parameter. This dispersion matrix is the analogue of the covariance one. Since we do not have a closed expression of the modal vector , we cannot use the bivariate mode-dispersion method (2.11) for a construction of the bivariate beta-Sarmanov kernel.

3.2 Bivariate beta-Sarmanov kernel

From the previous section, the standard version of the bivariate beta-Sarmanov kernel is here constructed by using the modal vector of instead of as a variant of the mode-dispersion method (2.11). This choice will be compensated in the bandwidth matrix connected to the complete dispersion matrix with correlation structure (3.6).

Indeed, solving in the sense of and leads to the new reparametrization of of (3.4) from into

| (3.7) |

Rewriting (3.2) in terms of (3.7), the means and variances of the univariate beta pdfs become

Finally, the bivariate beta-Sarmanov kernel is defined as such that

| (3.8) | |||||

with the constraints

| (3.9) |

and

The first interval of (3.9) is the equivalent in (3.5) and the second one of (3.9) is due to the constraints from the bandwidth matrix , which is symmetric and positive definite. In practice, one often has: . Of course, the beta-Sarmanov kernel satisfies Definition 2.1 of associated kernel:

| (3.10) |

Table 3.1 shows some effects of the correlation parameter in on the modal vector and maximum values, which are obtained by using corresponding values of for Figure 3.1.

3.3 Bivariate beta-Sarmanov kernel estimators

3.3.1 Standard version of the estimator

In this particular case, the beta-Sarmanov kernel estimator

| (3.11) |

also satisfies Proposition 2.10. Table 3.2 allows to observe the effect of correlation (3.9) on the total mass by using four samples of simulated data.

| sample 1 | sample 2 | sample 3 | sample 4 | |

|---|---|---|---|---|

| -0.0003 | 1.034019 | 0.9954256 | 1.002369 | 1.025671 |

| 1.034078 | 0.9955653 | 1.002418 | 1.025731 | |

| 1.034157 | 0.9957517 | 1.002483 | 1.025811 |

Fixing in , the pointwise bias is written as

and, the pointwise variance is

with

Using (3.10) the AMISE (2.21) becomes here

The bandwidth matrix is selected by the LSCV method (2.25) on the set of diagonal bandwidth matrices. Concerning full and Scott cases, this LSCV method is used under and , respectively, subsets of and verifying the constraint of the beta-Sarmanov kernel (3.9). Their algorithms are described below and used for numerical studies in Section 4.

Algorithms of LSCV method (2.25) for three forms of bandwidth matrices in two dimensions ()

-

A1.

Full bandwidth matrices.

-

1.

Choose two intervals and related to and , respectively.

-

2.

For and ,

-

(a)

Compute the interval related to from constraints (3.9);

-

(b)

For ,

Compose the full bandwidth matrix with , and .

-

(a)

-

3.

Apply LSCV method on the set of all full bandwidth matrices .

-

1.

-

A2.

Scott bandwidth matrices.

-

1.

Choose an interval related to and a fixed bandwidth matrix .

-

2.

For ,

-

(a)

Compute the interval related to from constraints (3.9);

-

(b)

For ,

Compose the given bandwidth matrix with , and ; -

(c)

Compose then the Scott bandwidth matrix .

-

(a)

-

3.

Apply LSCV method on the set of all Scott bandwidth matrices .

-

1.

-

A3.

Diagonal bandwidth matrices.

-

1.

Choose two intervals and related to and , respectively.

-

2.

For and ,

Compose the diagonal bandwidth matrix . -

3.

Apply LSCV method on the set of all diagonal bandwidth matrices .

-

1.

Let us conclude these algorithms by the following precisions. For a given interval , the notation is the total number of subdivisions of and denotes the real value at the subdivision of . Also, for practical uses of (A1) and (A3), both intervals and are generally chosen to be . In the case of the Scott bandwidth matrix (A2), we retain the interval and the fixed bandwidth matrix , where is the sample covariance matrix. See Figure 4.2 for graphical illustrations.

3.3.2 Modified version of the estimator

Being large in the standard version, the pointwise bias of the beta-Sarmanov kernel estimator (3.11) must be reduced. Following the algorithm of Section 2.3 and without numerical illustration in this paper, the first step divides in nine subregions of order with for :

-

a.

only one interior subregion denoted as ;

-

b.

eight boundary subregions divided in two parts as

-

(i)

four angle subregions denoted by

-

(ii)

four edge subregions denoted by

-

(i)

As for the second step, we consider the three functions and such that

| (3.12) |

Each axis of has one interior subregion and two boundary regions and for . Thus, from (2.27) with , one gets the new parametrization of each margin beta kernel used in of (3.8) with : for ,

| (3.13) |

Therefore, using of (3.12) and by combination of (3.13) for each of the nine subregions of , then is expressed by

| (3.14) |

Notice that the last component of does not change in all subregions of the support. This is because of the choice of related to the construction of the beta-Sarmanov kernel (3.8). According to Proposition 2.14 the modified beta-Sarmanov kernel obtained from (3.14) and denoted by is an associated kernel with ,

| (3.15) |

and, such that and is detailed as

The corresponding modified beta-Sarmanov kernel estimator

| (3.17) |

has, for all ,

and

Thus, the asymptotic expression of the MISE of on is given by

The modified beta-Sarmanov kernel also depend on the choice of scalars for . The user can set the values of according to his practical objective. For example in univariate case, Chen (1999, 2000) took . From (3.7) to (3.17) and when , we have the same formulas for multiple associated kernels of Bouerzmarni and Rombouts (2010). Also, similar results can be obtained for the Scott bandwidth matrices. However, numerical illustrations are so long and tedious tasks; see, e.g., Hirukawa and Sakudo (2014) for .

4 Simulation studies and real data analysis

In this section, we compare the performance of the three forms of bandwidth matrices of Table 2.1. The optimal bandwidth matrix is chosen by LSCV method (2.25) using the algorithms A1, A2 and A3 given at the end of Section 3.3.1 and their indications. All computations were done on the computational resource111Dell Poweredge R900, Processor Xeon X7350, 2.93 GHz, 32 Go RAM of Laboratoire de Mathématiques de Besançon by using the R software; see R Development Core Team (2012). The comparisons will be done using the standard version of the beta-Sarmanov kernel estimator (3.11) through simulations studies and an illustration on real dataset.

4.1 Simulation studies

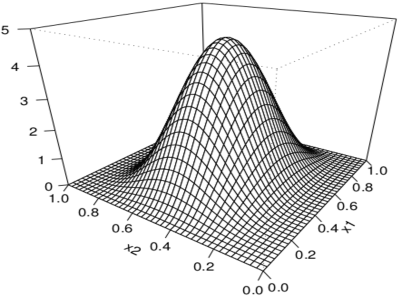

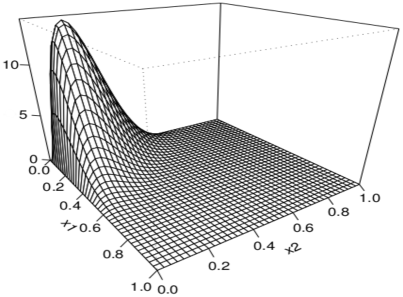

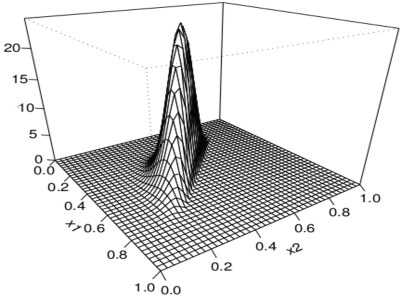

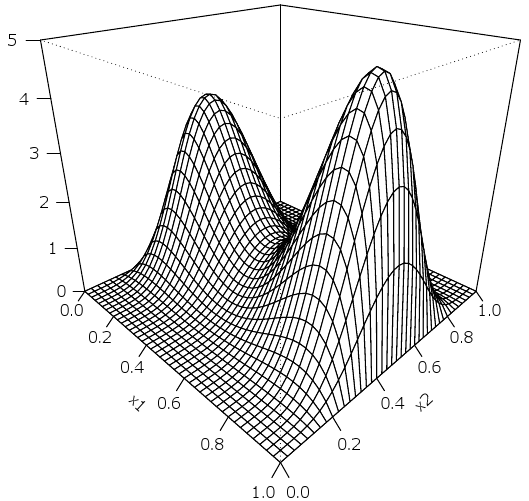

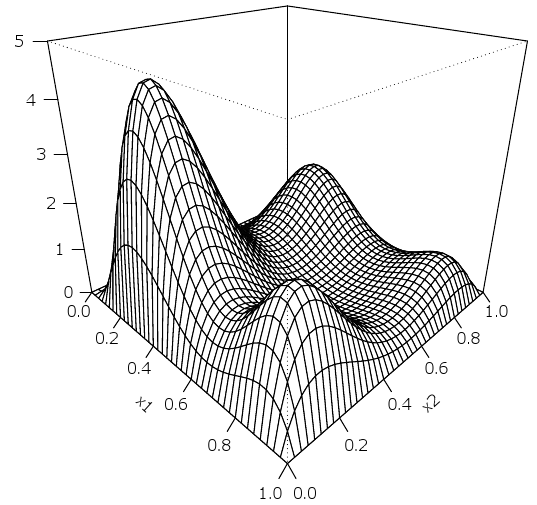

We consider six target densities with supports included in and labeled A, B, C, D, E and F respectively. They have different correlation structure and some local modes. The plots for these densities are given in Figure 4.1.

-

1.

Density A is the bivariate beta density without correlation such that and as parameters values in univariate beta density (3.1), respectively;

-

2.

density B is the bivariate Dirichlet density

where is the classical gamma function, with parameters values , and, therefore, the moderate value of ;

-

3.

density C is the bivariate beta density without correlation such that and in (3.1), respectively;

-

4.

density D is the bivariate Dirichlet as the density B but with , and then .

-

5.

density E is the bivariate density without correlation defined as follows:

such that , and are univariate beta densities (3.1) with parameters values and and .

-

6.

density F is the bivariate density without correlation :

such that , , and are univariate beta densities (3.1) with parameters values and , and .

Table 4.1 presents the execution times needed for computing the LSCV method for each of the three types of bandwidth matrix with respect to only one replication of sample sizes and for each of the target densities A, B, C, D, E and F of Figure 4.1. For the computational times of the LSCV method for full bandwidth matrix are longer than both the Scott and diagonal bandwidth matrices, which have the almost identical Central Processing Unit (CPU) times. The constraints (3.9) of the correlation of Sarmanov induce that execution times of the Scott bandwidth matrix are relatively a bit longer than for the diagonal ones. Let us note that for full bandwidth matrices, the execution times become very large when the number of observations is large as seen in Table 4.1; however, these CPU times can be considerably reduced by parallelism processing, in particular for for the full LSCV method. These constraints (3.9) reflect the difficulty of finding the appropriate bandwidth matrix with correlation structure by LSCV method (2.25). Hence, we are able to infer that the Scott and diagonal LSCV method do not impose excessive computation burdens; and, the Scott procedure takes into account the structure of (null and moderate) correlations in the sample.

| A | B | C | D | E | F | ||

|---|---|---|---|---|---|---|---|

| Full | 2.8310 | 2.7570 | 2.8793 | 2.7931 | 27940 | 2.8362 | |

| Scott | 0.2173 | 0.2251 | 0.2207 | 0.2202 | 0.2212 | 0.2204 | |

| Diagonal | 0.1436 | 0.1456 | 0.1526 | 0.1536 | 1.1531 | 1.1446 |

We now examine the efficiency of various bandwidth matrices in Table 2.1 via

where is the number of replications. Table 4.2 shows some expected values of for the three forms of bandwidth matrices with respect to the densities A, B, C, D, E and F of Figure 4.1, and according only to the sample size because of excess of computational times (see Table 4.1). Globally, the full and Scott bandwidth matrices with correlation structure perform better in terms of the quality of smoothing than the diagonal one without correlation. Even if the correlation is almost non-existent in the sample (e.g. models A and C of Table 4.2), we attend the good behavior of the full and Scott bandwidth matrices. Also, these bandwidth matrices with correlation structure suit for multimodal target densities (e.g. E and F of Table 4.2). For moderate correlation (e.g. models B of Table 4.2) we can recommend the light version of bandwidth matrices with correlation structure which is the Scott one. As for strong correlation in the sample (e.g. models D of Table 4.2) it is not preferable to use the Scott bandwidth matrix.

| Models | Full | Scott | Diagonal |

|---|---|---|---|

| A | 0.2554(0.2253) | 0.1887(0.0890) | 0.2963(0.2121) |

| B | 0.8571(0.2422) | 0.5999(0.2582) | 0.9743(0.5973) |

| C | 0.1985(0.0737) | 0.2150(0.0828) | 0.2384(0.1740) |

| D | 1.1481(0.0937) | 9.1188(0.7466) | 1.6420(0.5735) |

| E | 0.2786(0.0785) | 0.2498(0.0985) | 0.5056(0.1526) |

| F | 0.6025(0.1122) | 0.6791(0.1475) | 0.8025(0.1254) |

4.2 Real data analysis

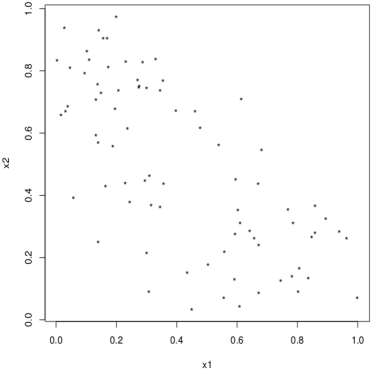

We applied the standard version of the beta-Sarmanov estimator (3.11) on paired rates data set according to the three types of bandwidth matrices in Table 2.1. The dataset of sample size in Graph (o) of Figure 4.3 has been provided by Francial G. Libengué (2013) during his last stay in Burkina Faso. It represents the popular ratings, for the two first consecutive ballots of the same electoral mandate of five years, of a political figure in different departments. Note that, for both elections, the prominent politician was finally elected in the second round. We are here interested to the opposite behavior of peoples during first rounds of both elections since the second round is governed by political alliances, which do not constitute a reference for the own popularity of a candidate.

Indeed, for many African countries, political elections are generally fought on tribal ethnic origins and partisan interests. The data displays opposed viewpoints between the results of the first round of the first election () and the first round of the second one (). In fact, the first election saw the candidate program mostly adopted by its clan (tribe and allied tribes) and rejected by the others. A few years later, facing the social discontent, he assumed a new political program which ends to another consultation of the people in a time . This reversal made him loose the support of his supporters but he received the backing up of formers opponents. It is thus noticeable that its own popularity is not much different between the first round of both elections; the first gave an average and the second . However, there is a significant negative correlation in the dataset: . Unlike overall trends , and , the empirical distribution Graph (o) of Figure 4.3 gives more details of the electoral situation department by department. Hence, we need a nonparametric smoothing of this joint distribution by using associated kernels.

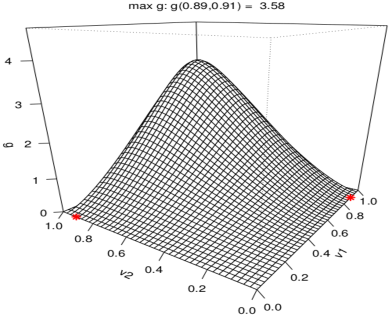

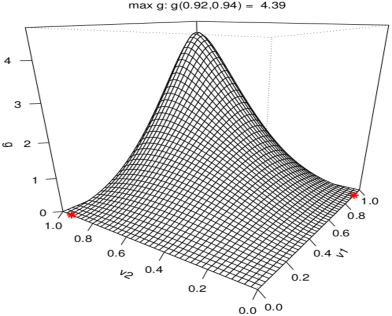

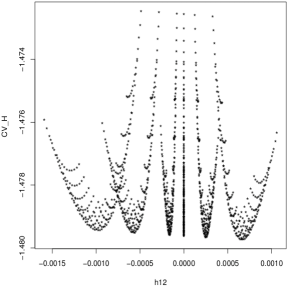

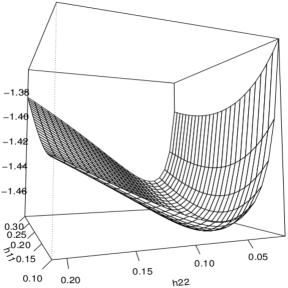

In order to smooth the joint empirical distribution of these paired data, we apply the beta-Sarmanov kernel estimator in its standard version (3.11). Figure 4.2 shows the results of the LSCV algorithms A1, A2 and A3 with the ratings dataset; see (2.25) and the end of Section 3.3.1. The computation time of the LSCV is in the same trend as in Table 4.1 for . To simplify the presentations in Figure 4.2 for both the Scott and full bandwidth matrices, we only plot for some values of and . In all cases we observe that there is a global minimum.

The obtained optimal bandwidth matrices are

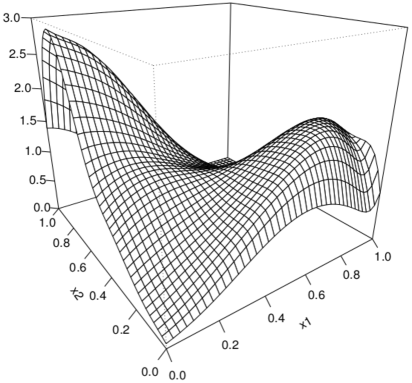

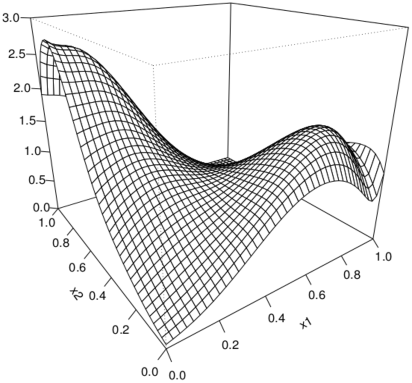

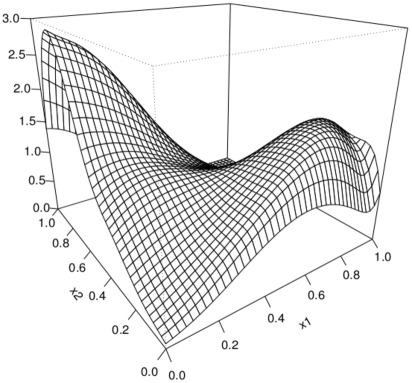

and . The resulting estimates are displayed in Figure 4.3.

From simulation studies of previous section, the full bandwidth matrix provides the reference smoothing which is appropriated for correlated data; see Graph (a) of Figure 4.3. In record time, the Scott bandwidth matrix delivers similar smoothing in Graph (b) of Figure 4.3 as the full and diagonal ones (see respectively Graphs (a) and (c) of Figure 4.3). In conclusion, we found anywhere the shape of a “carpet flying” in balance, smoothing thus the joint empirical distribution of the electoral situation of the candidate. This balance situation makes him to win in the second round of both elections.

5 Summary and final remarks

We have presented general associated kernels (with or without correlation structure) that varying their shape according to the target point along the support. Excluding the classical associated kernels, the local adaptability of these associated kernels (depending on the target point and the bandwidth matrix ) means that they are free of boundary bias but have a slightly bias different. Furthermore, the forms of bandwidth matrices used in the case with correlation structure have both theoretical and practical significances. Under the criterion of cross-validation, we therefore recommend the Scott bandwidth matrix which is more workable than the full one. A method of construction, called multivariate mode dispersion method, for these kernels are introduced. Also, we have proposed an algorithm of bias-reductions of their corresponding associated kernel estimators. An extension to discrete multivariate associated kernels is obviously possible. Similarly, a work is in progress on nonparametric multiple regression composed by continuous and discrete univariate associated kernels (e.g. Proposition 2.6).

Constructed by the correlation structure of Sarmanov (1966) and by a variant of mode dispersion method, the bivariate beta-Sarmanov kernel estimator is completely study with the optimal bandwidth matrix chosen by cross-validation. This technique can be extended in multivariate case for different type of kernels which are continuous and also discrete. In fact, from two or more univariate independent pdfs or probability mass functions, the correlation structure of Sarmanov (1966) and a variant of mode dispersion method can always allow to build a multivariate type of kernel with correlation structure; and, therefore, produced the corresponding multivariate Sarmanov kernel. In terms of execution times from using the cross-validation method, we advise to use the Scott bandwidth matrix because of its flexibility and efficiency for no very strong correlation in the dataset.

Simulation experiments and analysis of a real dataset provide insight into the behavior of the bandwidth matrix for small and moderate sample sizes. Tables 4.1 and 4.2 and Figure 4.3 can be conceptually summarized as follows. As expected, the full bandwidth matrix is frequently better than the others. An alternative with correlation structure has been proposed for the cross-validation technique: the Scott bandwidth matrix which has a comparable gain in execution times than the diagonal one; also, it produces better results than the diagonal in most cases. So, we recommend the Scott bandwidth matrix for multivariate use with the cross-validation technique. Further research in this direction are in progress, especially on the choice of optimal bandwidth matrix by using Bayesian approaches; see, e.g., Zougab et al. (2014).

6 Appendix

This section is dedicated to the proof of Proposition 2.11. Indeed, using successively (2.16) and Taylor’s formula around and then , and also the invariance under cyclic permutations of the operator , the result (2.18) is shown by

In fact, the rest comes from deduced from Proposition 2.4 of classical associated kernels and

where is the probability rate of convergence.

Concerning the variance (2.19) one first has

From (2.16) and (2.18), one has the following behavior of the second term

since is bounded for all . By using Taylor’s expansion around of , the first term becomes

with

A similar argument from Chen (1999, Lemma) with bounded on shows the existence of and then the condition leads successively to

Acknowledgements

We sincerely thank Francial G. Libengué for useful discussions and for the dataset of illustration.

References

References

- Aitchison and Aitken (1976) Aitchison, J., Aitken, C.G.G., 1976. Multivariate binary discrimination by the kernel method. Biometrika 63, 413-420.

- Balakrishnan and Lai (2009) Balakrishnan, N., Lai, C.D., 2009. Continuous Bivariate Distributions, Springer, New York.

- Bouerzmarni and Rombouts (2010) Bouezmarni, T., Rombouts, J.V.K., 2010. Nonparametric density estimation for multivariate bounded data, Journal of Statistical Planning and Inference 140, 139–152.

- Chacón and Duong (2010) Chacón, J.E., Duong, T., 2010. Multivariate plug-in bandwidth selection with unconstrained pilot bandwidth matrices, Test 19, 375–398.

- Chacón and Duong (2011) Chacón, J.E., Duong, T., 2011. Unconstrained pilot selectors for smoothed cross validation, Australian and New Zealand Journal of Statistics 53, 331–351.

- Chacón et al. (2011) Chacón, J.E., Duong, T., Wand, M.P., 2011. Asymptotics for general multivariate kernel density derivative estimators, Statistica Sinica, 21, 807–840.

- Chen (1999) Chen, S.X., 1999. A beta kernel estimation for density functions, Computational Statistics and Data Analysis 31, 131–145.

- Chen (2000) Chen, S.X., 2000. Probability density function estimation using gamma kernels, Annals of the Institute of Statistical Mathematics 52, 471–480.

- Epanechnikov (1969) Epanechnikov, V.A., 1969. Nonparametric estimation of a multivariate probability density, Theory of Probability and Its Applications 14, 153–158.

- Garcìa-Portugués et al. (2013) Garcìa-Portugués, E., González-Rodríguez, W., Crujeiras, R.M., González-Manteiga, W., 2013. Kernel density estimation for directional–linear data, Journal of Multivariate Analysis 121, 152–175.

- Girard et al. (2013) Girard, S., Guillou, A., Stupfler, G., 2013. Frontier estimation with kernel regression on high order moments, Journal of Multivariate Analysis 116, 172–189.

- González-Manteiga et al. (2013) González-Manteiga, W., Lombardía, M.J., Martínez-Miranda, M.D., Sperlich, S., 2013. Kernel smoothers and bootstrapping for semiparametric mixed effects models, Journal of Multivariate Analysis 114, 288–302.

- Hazelton and Marshall (2009) Hazelton, M.L., Marshall, J.C., 2009. Linear boundary kernels for bivariate density estimation, Statistics and Probability Letters 79, 999–1003.

- Henderson and Searle (1979) Henderson, H.V., Searle, S.R., 1979. Vec and vech operators for matrices, with some uses in Jacobians and multivariate statistics, Canadian Journal of Statistics 7, 65–81.

- Hielscher (2013) Hielscher, R., 2013. Kernel density estimation on the rotation group and its application to crystallographic texture analysis, Journal of Multivariate Analysis 119, 119–143.

- Hirukawa and Sakudo (2014) Hirukawa, M., Sakudo, M., 2014. Nonnegative bias reduction methods for density estimation using asymmetric kernels, Computational Statistics and Data Analysis 75, 112–123.

- Igarashi and Kakizawa (2015) Igarashi, G., Kakizawa, Y., 2015. Bias correction for some asymmetric kernel estimators, Journal of Statistical Planning and Inference 159, 37–63.

- Jørgensen (1997) Jørgensen, B., 1997. The Theory of Dispersion Models, Chapman & Hall, London.

- Jørgensen (2013) Jørgensen, B., 2013. Construction of multivariate dispersion models, Brazilian Journal of Probability and Statistics 27, 285–309.

- Jørgensen and Kokonendji (2011) Jørgensen, B., Kokonendji, C.C., 2011. Dispersion models for geometric sums, Brazilian Journal of Probability and Statistics 25, 263–293.

- Kokonendji and Senga Kiéssé (2011) Kokonendji, C.C., Senga Kiéssé, T., 2011. Discrete associated kernels method and extensions, Statistical Methodology 8, 497–516.

- Kokonendji et al. (2007) Kokonendji, C.C., Senga Kiéssé, T., Zocchi, S.S., 2007. Discrete triangular distributions and non-parametric estimation for probability mass function, Journal of Nonparametric Statistics 19, 241–254.

- Kotz et al. (2000) Kotz, S., Balakrishnan, N., Johnson, L.N., 2000. Continuous Multivariate Distributions, John Wiley and Sons, Chicester.

- Kundu et al. (2010) Kundu, D., Balakrishnan, N., Jamalizadeh, A., 2010. Bivariate Birnbaum-Saunders distribution and associated inference, Journal of Multivariate Analysis 101, 113–125.

- Lee (1996) Lee, M-L.T., 1996. Properties and applications of the Sarmanov family of bivariate distributions, Communications in Statistics - Theory and Methods 25, 1207–1222.

- Libengué (2013) Libengué, F.G., 2013. Méthode Non-Paramétrique par Noyaux Associés Mixtes et Applications. Ph.D. Thesis Manuscript (in French) to Université de Franche-Comté, Besançon, France & Université de Ouagadougou, Burkina Faso, June 2013, LMB no. 14334, Besançon.

- Malec and Schienle (2014) Malec, P., Schienle, M., 2014. Nonparametric kernel density estimation near the boundary, Computational Statistics and Data Analysis 72, 57–76.

- Racine and Li (2004) Racine, J., Li, Q., 2004. Nonparametric estimation of regression functions with both categorical and continuous data, Journal of Econometrics 119, 99–130.

- R Development Core Team (2012) R Development Core Team., 2013. R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0, URL http://cran.r-project.org/.

- Romano and Thombs (1996) Romano, J.P., Thombs, L.A., 1996. Inference for autocorrelations under weak assumptions, Journal of the American Statistical Association 91, 590–600.

- Sain (2002) Sain, S.R., 2002. Multivariate locally adaptive density estimation, Computational Statistics and Data Analysis 39, 165–186.

- Sarmanov (1966) Sarmanov, O.V., 1966. Generalized normal correlation and two-dimensionnal Frechet classes, Doklady (Soviet Mathematics) 168, 596–599.

- Scott (1992) Scott, W.D., 1992. Multivariate Density Estimation, John Wiley and Sons, New York.

- Wand and Jones (1993) Wand, M.P., Jones, M.C., 1993. Comparison of smoothing parameterizations in bivariate kernel density estimation, Journal of the American Statistical Association 88, 520–528.

- Zougab et al. (2012) Zougab, N., Adjabi, S., Kokonendji, C.C., 2012. Binomial kernel and Bayes local bandwith in discrete functions estimation, Journal of Nonparametrics Statistics 24, 783–795.

- Zougab et al. (2013) Zougab, N., Adjabi, S., Kokonendji, C.C., 2013. A Bayesian approach to bandwidth selection in univariate associate kernel estimation, Journal of Statistical Theory and Practice 7, 8–23.

- Zougab et al. (2014) Zougab, N., Adjabi, S., Kokonendji, C.C., 2014. Bayesian estimation of adaptive bandwidth matrices in multivariate kernel density estimation, Computational Statistics and Data Analysis 75, 28–38.