A Directional Multivariate Value at Risk

Abstract

In economics, insurance and finance, value at risk (VaR) is a widely used measure of the risk of loss on a specific portfolio of financial assets. For a given portfolio, time horizon, and probability , the VaR is defined as a threshold loss value, such that the probability that the loss on the portfolio over the given time horizon exceeds this value is . That is to say, it is a quantile of the distribution of the losses, which has both good analytic properties and easy interpretation as a risk measure. However, its extension to the multivariate framework is not unique because a unique definition of multivariate quantile does not exist. In the current literature, the multivariate quantiles are related to a specific partial order considered in , or to a property of the univariate quantile that is desirable to be extended to . In this work, we introduce a multivariate value at risk as a vector-valued directional risk measure, based on a directional multivariate quantile, which has recently been introduced in the literature. The directional approach allows the manager to consider external information or risk preferences in her/his analysis. We have derived some properties of the risk measure and we have compared the univariate VaR over the marginals with the components of the directional multivariate VaR. We have also analyzed the relationship between some families of copulas, for which it is possible to obtain closed forms of the multivariate VaR that we propose. Finally, comparisons with other alternative multivariate VaR given in the literature, are provided in terms of robustness.

1 Introduction

Value at risk (VaR) has become a benchmark for risk management which is defined as the threshold quantity that does not exceed a certain probability level which is considered to be dangerous. It is commonly implemented by investment banks to measure the market risk of their asset portfolios. Although (VaR) has been broadly criticized from the work of [Artzner et al. (1999)] since it does not verify the diversification property, it has also been defended by [Heyde et al. (2009)] for its robustness. For univariate risks, the VaR is simply the quantile of the loss distribution function. Thus, the VaR is a risk measure easily interpretable, and it still remains the most popular measure used by risk managers. Unfortunately, a unique definition of multivariate VaR is more complicated because there are different possible definitions of multidimensional quantiles that try to generalize some desirable properties of the univariate quantile. For instance, the proposals given by [Koltchinskii (1997)] of multivariate quantiles as inversions of mappings, multivariate quantiles in terms based on norm minimization as in [Chaudhuri (1996)], multivariate quantiles as level-sets given by [Fernández-Ponce and Suárez-Llorens (2002)], multivariate quantiles based on depth functions developed in [Serfling (2002)], and finally, multivariate quantiles based on projections as in [Fraiman and Pateiro-López (2012)], [Hallin et al. (2010)], [Kong and Mizera (2012)].

Currently business and financial activities generate data for which it has been shown that it is insufficient to consider single real-value measures over marginal aspects, in order to quantify risks jointly associated to the data. For instance, one of the drawbacks detected in the global banking regulatory Basel II is the solvency and liabilities dependence among the financial institution branches, or even the domino effect in the markets that could be generated by dependence among filial products. Thus, the solvability of each individual branch may strongly be affected, not only by its activities, but also by the level of dependence among all the branches. In consequence, it is necessary to quantify the risk, considering both the multivariate nature of the data and the dependence among the marginal risks.

In Basel III, a new liquidity regulation was proposed in order to avoid the weakness detected in the 2007-2009 crisis; but these regulations have to be complemented by internal models in the institutions, in order to obtain better hedge results. These models have to include multivariate risk measures computable in high dimensions and also, to consider possible internal and external risks, even if the nature of those risks is strongly heterogeneous.

In recent decades, literature devoted to extend the VaR measure to the multivariate setting has been published. For instance, bivariate versions have been studied in [Arbia (2002)], [Tibiletti (2001)], [Nappo and Spizzichino (2009)]. Also, for multivariate distributions in general, some notions of VaR have been introduced (e.g. [Lee and Prékopa (2012), Embrechts and Puccetti (2006), Cousin and Di Bernardino (2013)]).[Embrechts and Puccetti (2006)] linked the risk measure to the level surface defined when the distribution function of risk or the survival function accumulate some -value, which is considered as a quantile surface. Recently, [Cousin and Di Bernardino (2013)] introduced a new notion of multivariate VaR based on those level surfaces studied in [Embrechts and Puccetti (2006)]. They commented that considering the whole surface as a risk measure could induce interpretation problems. Therefore, they defined the multivariate VaR as the mean of the points belonging to the surface considered in [Embrechts and Puccetti (2006)] and hence, the output is a point with the same dimension as the random vector of losses. Specifically, they define the upper–orthant Value–at–Risk (lower–orthant Value–at–Risk) at –level (–level) as the conditional expectation of , given that stands in the -set of its distribution (survival) function.

In this paper, we introduce a directional multivariate Value at Risk, based on the extremality level sets introduced in [Laniado et al. (2012)], which permit the concept of directional multivariate quantile to be defined. The extremality level sets are surfaces defined by following the same idea as in [Embrechts and Puccetti (2006)] but linked to rotations of the multivariate distribution; that is, a directional approach is considered. We share with [Cousin and Di Bernardino (2013)] the idea that a multivariate VaR seen as a surface could bring problems in relation to its interpretation. Hence, we highlight the idea of considering the multivariate VaR as a vector-valued point that defines the vertex of an oriented orthant in the direction of analysis. The vertex is obtained using the mean of to fix a reference system. The risk measure that we propose considers the high dimension nature of the real problems, and the dependence among the risks is implied in the analysis. Finally, we give the possibility of considering manager preferences, introducing a parameter of direction . For instance, directions like the maximum variability given for the principal components in the portfolio, or the assets weight composition could be more interesting to analyze than the classic directions given for the information summarized in the survival or cumulative distribution functions. Besides, the directional approach allows us to give bounds for the VaR related to linear combination of random variables, mainly when they are statistically dependent.

We have proved properties of the directional VaR that we consider as relevant for a multivariate risk measure, such as consistency with respect to a particular stochastic order and tail subadditivity in the mean loss direction, as well as some invariance properties. We have compared the components of the directional multivariate VaR with the univariate VaR on the marginals, in order to show that the vector given by the VaR on the marginals provides incomplete information about the joint risk.

We have also obtained closed expressions of the VaR when bivariate copulas are considered or when a multivariate Archimedean’s copulas governed the dependence among the components of the portfolio. Finally, we will present comparisons in terms of robustness with the alternative vector-valued multivariate VaR, introduced by [Cousin and Di Bernardino (2013)].

The paper is structured as follows. In Section 2, we introduce some preliminary concepts and notation necessary in order to understand the main contributions of the paper. In Section 3, the directional multivariate Value at Risk ( is introduced and we provide analytic properties, which can be viewed as extensions of those given in [Artzner et al. (1999)], to the multivariate setting. Section 4 contains the comparisons between the univariate VaR over the marginals and the components of the directional multivariate VaR. Section 5 is devoted to theoretical results and closed forms of the multivariate VaR when particular families of copulas are considered. In Section 6, we develop the robustness analysis. Finally, some conclusions are outlined as well as some possible directions for future work.

2 Preliminaries

The main objective of this paper is to introduce a directional multivariate Value at Risk, based on the notion of directional multivariate quantile given in [Laniado et al. (2010)]. In order to make the paper self contained, we have devoted this section to revise the main concepts that are necessary to properly define the risk measure introduced in this paper.

Definition 2.1.

An oriented orthant in with vertex in the direction is defined as,

| (2.1) |

where and is the orthogonal matrix such that , with .

Based on the oriented orthant concept, we can define a partial data order (denoted by ) in as,

| (2.2) |

where . Or equivalently,

where the order on the right side is component-wise.

Throughout the paper we will use the following notation related to subsets in . Given , , and , the sets and are defined as,

| (2.3) |

We recall some results on oriented orthants that will be useful in the main sections of the paper.

Lemma 2.2.

Given a direction and a vertex , then

| (2.4) |

The proof is given in the Appendix.

Lemma 2.3.

Given and , then

| (2.5) |

Proof. The proof is straightforward using the definitions given in (2.3).

We also recall some definitions of useful stochastic orders; see [Shaked and Shanthikumar (2007)], for more details.

Definition 2.4.

Given two random vectors and , is said to be smaller than in:

-

(i)

usual stochastic order (denoted by ) if , for any increasing function with finite expectations.

-

(ii)

upper orthant order (denoted by ) if , for all , where , denote the survival function of and , respectively.

-

(iii)

lower orthant order (denoted by ) if , for all , where , denote the distribution function of and , respectively.

It is easy to verify that both orders, the upper orthant and the lower orthant, are implied by the usual stochastic order. The following stochastic order defined in [Laniado et al. (2012)] will be a key tool in providing some properties of the multivariate VaR that we will define in the next Section.

Definition 2.5.

Let and be two random vectors in , is said smaller than in the extremality order in the direction (denoted by ) if,

It is easy to show that . Moreover, if then , as it is proven in [[Laniado et al. (2012)], Property 3.4]. Since the multivariate VaR is based on the definition of a quantile, we also need to introduce the directional multivariate quantile given in [Laniado et al. (2010)].

Definition 2.6.

Let be a random vector with associated probability distribution function . Then the directional multivariate quantile at level , in direction is defined as

| (2.6) |

with .

From now on, we will focus on an absolutely-continuous random vector (with respect to the Lebesgue measure on ) with increasing marginal distribution functions and such that , for . These conditions will be called regularity conditions.

3 Directional Multivariate Value at Risk

In the univariate setting, the relationship between the quantiles related to the loss distribution and the VaR is obvious. In this Section, we propose a definition of multivariate VaR for a portfolio of -dependent risks, linked with the directional multivariate quantile defined in (2.6). Besides, the output is a point in ; that is, a vector of the same dimension as the considered portfolio of risks. Specifically, as in the univariate case, this point defines the vertex of an oriented orthant that accumulates a probability , but in the direction that the investor or the risk management considers more convenient.

Definition 3.1.

Let be a random vector satisfying the regularity conditions and . Then the directional multivariate Value at Risk of in direction at probability level is given by

| (3.1) |

where .

We must highlight that given a direction , the is the intersection between the directional quantile at level , and the line defined by both the direction and the mean of . We want to point out that the centrality tool chosen, the mean, will represent a central reference point for the random vector space, i.e., for the support of the associated probability distribution. As we will demostrate, the choice of the mean in the definition of (3.1) allows us to derive desirable and interpretable analytic properties related to the risk measure. However, other options as central reference point are possible; for example the median seen as the deepest point associated with a multivariate depth measure, which may provide a more robust risk measure (e.g. [Zuo and Serfling (2000), Cascos et al. (2011)]).

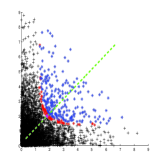

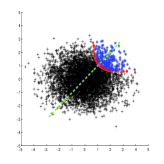

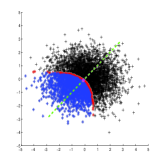

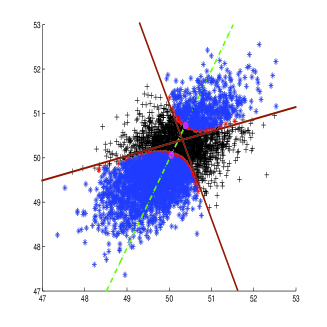

To illustrate this concept, you can see in Figure 1 some examples of the risk measure defined in (3.1), for three different bivariate distributions in the direction with . This direction makes reference to the analysis of the distribution function of . Figure 2 presents examples with the same bivariate distributions, but in the direction and for ; that is, taking into account the information given by the survival function of . We call these two directions classical directions, but the aim of this work is to show that it could be interesting to consider other directions in the analysis of risk.

Observe that in the figures, the line in direction crossing the mean in green is displayed while the quantile curve is displayed in red. The VaR that we propose is just the intersection between the line and the quantile curve. On the other hand, the points in blue are the points "below" the level of risk in the corresponding direction; meanwhile the black points are those "exceeding" the level risk. Observe Figure 1, if you take any point on the blue region as a vertex of an oriented orthant in direction , then the probability of that orthant will be greater than . It will be equal to or smaller than if the point is taken from the red line or black region, respectively. The same conclusion can be drawn from Figure 2 but in direction .

(A) Bivariate Uniform (B) Bivariate Exponential (C) Bivariate Normal

(A) Bivariate Uniform (B) Bivariate Exponential (C) Bivariate Normal

It is desirable that the classical univariate VaR agrees with our definition of VaR in the case ; this fact will be seen in the following; remember that the univariate VaR is defined as,

| (3.2) |

where is usually considered closed to 1. Moreover, the VaR may also be defined in terms of the distribution function as,

| (3.3) |

As in the univariate setting under regularity conditions, then (3.2) and (3.3) are the same. To be consistent with the univariate VaR, our definition of multivaritate VaR agrees with the classical definition for . That is, we have that in terms of ,

where is related to definition (3.2) and is related to definition (3.3). However, this fact does not hold in the multivariate context where is not true in general, being

| (3.4) | ||||

| (3.5) |

The remainder of this section is devoted to providing some properties of which are similar to those properties considered in the risk literature; (see [Artzner et al. (1999), Burgert and Ruschendorf (2006), Cardin and Pagani (2010), Rachev et al. (2008), Cascos and Molchanov (2007), Cascos and Molchanov (2013)]). Specifically, we provide properties of the multivariate in terms of the [Artzner et al. (1999)]’s properties related to coherent risk measures in the univariate setting. Besides, we have explored other properties inherent to the multivariate response such as invariance under orthogonal transformations. All the proof for the following results is given in the Appendix.

Property 3.2 (Non-Negative Loading).

If in (3.1), then

| (3.6) |

This property reflects that the risk measure is a bound of the mean value of the losses, with respect to the partial order given in 2.2. Note that the hypothesis is necessary, especially when is chosen to be close to 0.

Property 3.3 (Quasi-Odd Measure).

holds the property:

| (3.7) |

This property shows symmetry with respect to the random losses distribution.

Property 3.4 (Positive Homogeneity and Translation Invariance).

Let , and , then,

| (3.8) |

Property 3.5 (Consistency w.r.t. extremality stochastic order).

Let and be random vectors satisfying the regularity conditions. If with , and , then:

| (3.9) |

Property 3.6 (Orthogonal Quasi-Invariance).

Let be an orthogonal transformation. Then,

| (3.10) |

Property 3.7 (Non-Excessive Loading).

Let be the orthogonal matrix described in (2.1). Then,

| (3.11) |

This property shows that is upper bounded by the supreme of the losses in the direction considered. Another good property which is desirable in the literature for risk measures is the subadditivity. As is well-known, the classical univariate VaR is not a subadditivity measure. However, there are conditions that ensure the tail region subadditivity property (see [Artzner et al. (1999), Heyde et al. (2009), Daníelson et al. (2013)]). In the same way, we highlighted that the is not subadditive in general, but we will prove that this property holds under some conditions. A previous definition is necessary.

Definition 3.8.

A random vector has regularity varying, with tail index if there is a function that is regularly varying at infinity with exponent and a non-zero measure on the Borel field such that,

| (3.12) |

when (see [Jessen and Mikosh (2006), Resnick (1987)]).

In this case, the measure has the property

| (3.13) |

for any and a Borel set.

With this definition, we can state the tail region subadditivity property of the .

Property 3.9 (Tail Region Subadditivity).

Let and be random vectors, with the same mean . If is a regularly varying random vector with index and non-degenerate tails then, the is subadditive in the tail region in direction , i.e.,

| (3.14) |

Note that the Property 3.9 could be extended to random vectors with means satisfying for . As you can see, the property ensures that at least in the direction of the mean loss, it is useful to merge two risky activities in order to diversify the risk.

4 Comparison of the univariate VaR componentwise and the Directional Multivariate VaR

The aim of this section is to compare the components of with the univariate VaR related to each marginal distribution of . But prior to this we need to remember the definition of a multivariate quasi-concave function.

Definition 4.1.

A multivariate function is a quasi-concave function if the upper-level set is a convex set for all . Or equivalently, the complementary of the lower set is a convex set for all .

We want to point out that both the distribution and survival functions, in general, satisfy Definition 4.1. This fact was proved in [Tibiletti (1995)], and therefore it is not a restrictive condition for the functions considered in this paper. Let us denote by the -th marginal of the random vector and by the -th component related to a point in . The following result provides comparisons between the components of the multivariate VaR introduced in this work and the classical univariate VaR.

Proposition 4.2.

Consider a random vector satisfying the regularity conditions. Assume that its survival function is quasi-concave. Then, for all :

Moreover, if its multivariate distribution function is quasi-concave, then, for all , we have that

The proof is given in the Appendix. As you can see, the preceding result can be extended considering other directions as follows.

Corollary 4.3.

Let be a random variable satisfying the regularity conditions and fix a direction . If the survival function of is a quasi-concave function, then, for all ,

Besides, if has a quasi-concavity cumulative distribution, then

where is the orthogonal transformation defined in (2.1).

The proof is straightforward from Proposition 3.6 and Proposition 4.2. Therefore, by linking the previous results we have the following inequality for all pairs , .

| (4.1) |

This relationship allows us to define a directional upper VaR and a directional lower VaR in a similar way to [Embrechts and Puccetti (2006)] and [Cousin and Di Bernardino (2013)], but with a unified notation. Specifically, we have introduced the following definitions:

The upper VaR in direction is,

| (4.2) |

The lower VaR in a direction is,

| (4.3) |

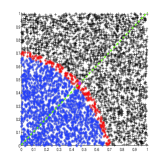

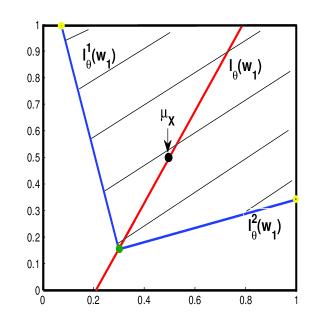

An example of these concepts is displayed in Figure 3, where we can see in a bivariate normal distribution, the upper VaR in direction for a level of risk , and the corresponding lower VaR in direction and level risk . Note that we can describe in the plot types of asymptotes for the quantile curves, furthermore these asymptotes will be the univariate quantiles for each marginal of the rotated random vector at the same , where the rotation matrix is the same as in (2.1). These asymptotes can be seen as a generalization of those defined in [Belzunce et al. (2007)] for the quantile curves in the classical directions.

Another practical situation where the link between the multivariate VaR and the univariate VaR is interesting (see e.g. [Embrechts and Puccetti (2006), Wang et al. (2013), Bernard et al. (2014)]), is when it is necessary to give bounds of the univariate VaR over a linear transformation of the marginal losses; for instance, when the transformation by the portfolio weights vector is considered, i.e., when the objective random variable is

where is the vector of the portfolio weights. Since it is difficult to obtain the VaR of mainly when the components of the portfolio are not independent, there is special interest in obtaining at least a bound for . Fortunately, we can give an upper-bound using our directional approach.

Proposition 4.4.

Let be the unitary vector in direction of the portfolio weights. If , then .

The proof is given in the Appendix.

Specifically as a consequence of Proposition 4.4, we have that

| (4.4) |

This result is another justification to consider a directional approach of the multivariate VaR, as well as its utility in financial applications.

5 Directional multivariate VaR and copulas

Researchers refer to copulas as "the multivariate distribution functions whose one-dimensional marginal distributions are uniform in ". For an extensive discussion of copulas, we refer the reader to [Nelsen (2006)]. This powerful tool allows the definition of scale-free measures of dependence and families of multivariate distributions. Two aspects are important in multivariate distributions, the distribution of the marginals and the dependence structure among them. The concept of copula fully describes the overall structure of dependence between the marginal variables and provides a global model for their stochastic behavior. The important result that links these two aspects is Sklar’s theorem that allows, in terms of a copula, to write the multivariate distribution function as,

| (5.1) |

where is the join distribution function, its marginals distribution and the copula, which according to Sklar’s theorem always exists. The copulas become a powerful tool to find closed expression of multivariate quantiles for special families of copulas. For example, in finance when the losses are modeled in percentage terms, it is of practical importance to find closed expressions for the risk measures expressed in terms of the copula since the support of the losses will be the unitary hyper cube of dimension .

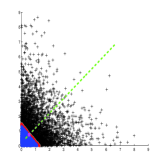

Hence, the objective of this section is to analyze how the can be obtained in terms of some families of copulas. The first result shows the representation of the restricted to bivariate copulas. Let be a bivariate random vector with marginals uniformly distributed in the interval . In this case, the distribution function of is a copula with density . It is well known that . Note that assuming , a direction can be characterized by a angle such that , and then, . Following with the notation given by the angles, the must be a point on the line defined by,

| (5.2) |

Therefore, given a direction , is characterized by its first component and the second one is obtained using (5.2). Now, the first component can be obtained by solving the following integral equation,

| (5.3) |

where is given by the intersection of the unitary square and the oriented quadrant with direction determined by and vertex . Specifically, can be expressed in terms of the unknown by using the semi-lines , that bound the corresponding quadrant which are defined as,

For instance, if , we can write the integral equation as follows:

| (5.4) |

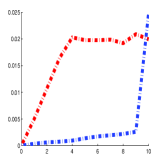

Figure 4 shows a case of the region with being the solution to (5.4), a point over the line . In summary, we can obtain for a given bivariate vector with copula density .

Now, we will focus on the Archimedean family of copulas broadly used in the literature whose definition is the following:

Definition 5.1 (Archimedean Copulas).

Let be a continuous, convex and strictly decreasing function with . Let be a pseudo-inverse function of . Then an Archimedean copula is defined by

| (5.5) |

In this case, for an -dimensional random variable with distribution function as belonging to the Archimedean family of copulas with generator , is given by the vector with all components equal to

| (5.6) |

Moreover, if has a survival copula belonging to the Archimedean family with generator , the equivalent Sklar’s representation gives the relation , where is the join survival function and its marginal survival functions. Hence, we obtain that:

| (5.7) |

Remember that if a vector has a copula , then the survival copula of will also be . Therefore, if , then the copula of and its survival copula are the same; for example, Frank’s copula in the Archimedean family holds this property as well as the elliptical family of copulas. Then, in this case the closed expression for is the reflection point of with respect to the point .

Now we will present some examples using some Archimedean copulas. Firstly, we are going to use Frank’s subclass to present an example of for any direction in the bivariate case. Later we will present some comparisons between the lower orthant VaR and the upper orthant VaR developed by [Cousin and Di Bernardino (2013)] with the but considering a -dimensional copula belonging to Clayton’s subclass. Let’s define these two subclasses.

-

(i)

Frank Copula: The generated function of this copula is

(5.8) (5.9) (5.10) where .

-

(ii)

Clayton Copula: This family is generated by

(5.11) (5.12) where .

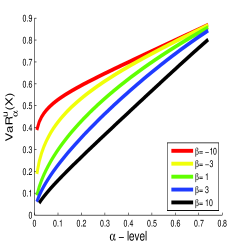

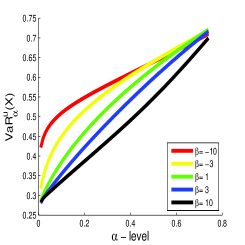

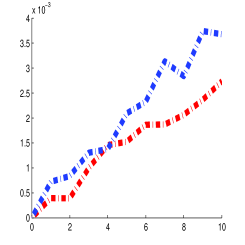

In Figure 5 we have drawn the first component of the directional for a bivariate random vector, with density given by the Frank copula density. The left plot is related to and the right plot is related to . Both plots present the changes as for different values of the dependence parameter .

a) Direction b) Direction

We can see in Figure 5 the dependence of with respect to . Note that as and the direction is , we will get the extreme cases known as comonotonic and counter-monotonic, respectively. In the left plot, it can be seen that the comonotonic case matches with the vector composed of the univariate VaR on the marginals, which in this case is given by the vector . In addition, it is well known that rotations over random vectors do not preserve the dependence structure in the rotated distribution; furthermore, this fact is captured in the right plot where the change of direction shows the rotations of the measure in each dependence parameter considered.

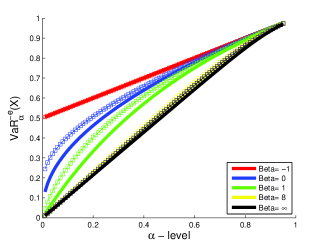

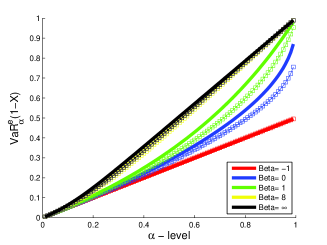

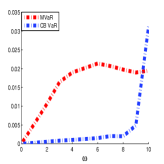

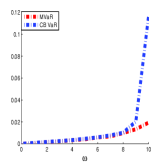

Let be a random vector with distribution function belonging to the Clayton copula subclass. Hence is a random vector with Clayton survival copula. We have presented the comparison of the first component of with and with , the correspondent lower orthant VaR and upper orthant VaR developed by [Cousin and Di Bernardino (2013)].

Table 1 contains the explicit expressions of and in dimension , and the generalized expressions for our proposal in terms of , in any dimension. Figure 6 shows the graphical comparison for ; the left plot presents the results for in solid line and in dashed line, while the right plot presents the results for in solid line and in dashed line.

| Directional | [Cousin and Di Bernardino (2013)]’s VaR | |

|---|---|---|

The results in Figure 6 also shows us that in the case of random vectors with Clayton copula class, increases with respect to the parameter and decreases in the parameter . On the other side, is an increasing function of the parameter , but also an increasing function of the dependence parameter . These features for this class of copulas were commented on and proved by [Cousin and Di Bernardino (2013)] and for our risk measure can be easily proved following the same scheme. In addition, we need to highlight that for each fixed pair (, ), the following relationships hold,

| (5.13) |

where the inequalities are componentwise. Hence, we can say that our measurement is more conservative in the upper case and we are more optimistic in the lower case. This can be taken into consideration by the manager according to her/his preferences.

a) Lower Case b) Upper Case

6 Robustness

The previous section presents the analytic results for random vectors with -uniform marginals distributions. However, in practical situations, it is necessary to obtain for any random vector . In this case, we use the following computational approach summarized in the following pseudo-algorithm:

Input: , , and the multivariate sample .

,

,

end

,

end

end

where is the sample of the random vector , the sample mean, the sample quantile curve with a slack and is the empirical probability distribution of . Using this procedure, we are able to deal with high dimension random vectors. We are aware that this procedures can be improved using more sophisticated tools of the non-parametric statistics, but they are material for another project.

On the other hand, it is well known that in risk theory, it is desirable that a measure be robust, (see [Artzner et al. (1999), Burgert and Ruschendorf (2006), Cardin and Pagani (2010), Rachev et al. (2008)]). But in general, most of the measures are sensitive to atypical observations. In this section, we present a simulation study in order to describe the sensitivity of our proposal, using the [Cousin and Di Bernardino (2013)]’s measure as a benchmark.

The contamination model that we will use in the simulations is the following:

| (6.1) |

where , and . The parameters of are,

remains fixed in the analysis, but the parameters of the normal distribution of are changed to different steps to generate outliers. As a measure to quantify the effect of the outliers, we define,

where is the risk measure evaluated in , with and is a risk measure evaluated with the sample with a level of contamination .

| Scenarios | Parameters of distribution |

|---|---|

| Variance Analysis | , |

| Covariance Matrix Analysis | , |

| Mean Analysis | , |

| Join Analysis | , |

We have considered the scenarios for , described in Table 2. The procedure is the following: firstly, we have generated a non-contaminated sample , with 5000 observations and we calculate both and .

Secondly, we have used the contamination model (6.1) taking values for from to . Then, we generated for each , samples of with an expected value of outliers . We have evaluated the risk measure as well as the percentage of variation for each level of contamination, performing this procedure times and we have reported the average of in the following plots.

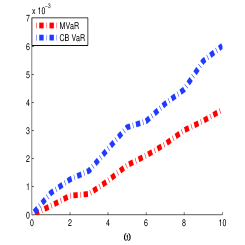

The first scenario suggests outliers given by changes on the variance of the marginals, which are difficult to detect in practice. We can see in Figure 7 that the behavior of is better than that corresponding to upper-VaR in [Cousin and Di Bernardino (2013)] for any level of contamination. "Better", in this context, means that is smaller.

The second scenario considers changes in all the components of the covariance matrix. The results are reported in Figure 8 that shows again the better behaviour of with respect to robustness. The last scenarios consist of changes in the mean. Firstly, we affected the first component of the mean and then we affected the second one and finally both of them simultaneously.

Figure 9 summarizes the results. As we can see, shows robustness under the presence of outliers of high dimension, but an extra-sensitivity under outliers in a unique component. The use of the mean of the random loss as the central point in the definition of our could be the cause of this lack of robustness.

a) b) c)

7 Conclusions

In this paper we have defined a multivariate extension of the classical risk measure VaR based on a directional multivariate quantile recently introduced in the literature. Specifically, we have proposed the directional multivariate Value at Risk () as a tool to analyze a portfolio of heterogeneous and dependent risks considering external information or manager preferences.

We have analyzed the analytic properties of in the same way as the [Artzner et al. (1999)]’s axiomatic. We have provided some invariance properties as well as consistency and tail subadditivity property, which are desirable in a risk measure. We have shown relations between the components of the output of with respect to the corresponding univariate VaR over the marginals. A link between the univariate VaR over the linear transformation using the portfolio weights vector , and the value of this transformation over is given. We have also presented closed expressions for in terms of some families of copulas, considering particular dimensions or particular directions.

Finally we have presented a simulation study of robustness comparing the behavior of with respect to the risk measure proposed in [Cousin and Di Bernardino (2013)]. The simulations show advantages of our proposal in relation to the presence of outliers. We have also detected in this study an open question to be taken into consideration in future work. The idea is to consider another central point instead of the mean as the center of the reference system, in order to improve the robustness of the risk measure, but, at the same time, keeping the good properties that have been proved. One option is to use a multivariate depth measure to choose the central point.

Acknowledgements

This research was partially supported by a Spanish Ministry of Economyand Competition grant ECO2012-38442.

Appendix

Proof of Lemma 2.2. Since,

| (7.1) |

we have that . Then using (7.1), we have that,

and hence,

Then,

Proof of Property 3.5. Since , we get:

Besides, and . Therefore, using the partial order defined in (2.2) there are three possibilities for :

-

(i)

,

-

(ii)

and ,

-

(iii)

.

We can prove that the two first options are not possible for the points and . Suppose that

which implies that,

Hence,

In which case we arrive at a contradiction,if we assume the regularity conditions. Moreover, the hypothesis , for all and the conclusion derived in [Laniado et al. (2012)] (Property 3.4.), permits us to reject the second possibility of ordering between the two points. Thus, the only option possible is,

Proof of Property 3.6. First, note that:

Besides, we have the following relationship:

Then , which implies that , and . Then, we get

| (7.3) |

which proves the result.

Proof of Property 3.9. It is easy to see that the equality in the mean implies that the vectors , and lie on the same line with direction vector . Then, we can write:

| (7.4) | ||||

where is the vector whose components are and denotes the first component of the vector.

For small, , and then,

On the other hand, we have the fact that the Borel set satisfies the following relation:

| (7.5) |

In the same way,

| (7.6) |

Now, in the case of the random variable , we have;

| (7.7) | ||||

where the inequalities in the expression are componentwise. As a consequence we get,

Then using the last equality in (7.7), we finally get,

| (7.8) |

Since in all the norms are equivalent, i.e., for two norms and , there are positive constants such that . Then, whatever norm is taken, we use the transformation [[Resnick (1987)], pg. 267.+], and rewrite in terms of a new measure in as , due to the property of the measure in (3.13). The relationship satisfying both measures for a Borel set in , it is given by,

| (7.9) |

| (7.10) | ||||

| (7.11) | ||||

| (7.12) |

Now using the Mikowski inequality we obtain:

| (7.13) |

Hence combining (7.5), (7.6), (7.8) and (7.13), we have the result

| (7.14) |

| (7.15) |

Since , we obtain,

Proof of Proposition 4.2. The proof follows the same outline as that of [[Cousin and Di Bernardino (2013)], Proposition 2.4.]. Note that in direction ,

Then we can write,

And we can assume the convexity of the by the quasi-concavity of the survival function , where denotes the complementary set. Now, as , belongs to the set . Moreover, from the definition of survival function we have that,

Then each component of a vector belonging to is superiorly bounded by the univariate VaR at level of the corresponding marginal. As a consequence, each component of is superiorly bounded by the univariate VaR at level of the corresponding marginal and hence, the first inequality holds. Now for the second inequality,

Then, we have,

But, if is a quasi-concave function, we have that is a convex set and . Therefore belongs to the set . Additionally, from the definition of distribution function, it is easy to show that each component of an element in is inferiorly bounded by the univariate VaR at level of the corresponding marginal; hence, we obtain the result.

References

- [Arbia (2002)] Arbia, G., Bivariate value at risk. Statistica LXII, 231-247, 2002.

- [Artzner et al. (1999)] Artzner P., Delbae F., Heath J. Eber D., Coherent measures of risk. Mathematical Finance 3, 203-228, 1999.

- [Bernard et al. (2014)] Bernard C., Jiang X. and Wang R., Risk aggregation with dependence uncertainty. Insurance: Mathematics and Economics 54(1), 93-108, 2014.

- [Burgert and Ruschendorf (2006)] Burgert C. and Ruschendorf L., Consistent risk measures for portfolio vectors. Insurance: Mathematics and Economics 38, 289-297, 2006.

- [Belzunce et al. (2007)] Belzunce F., Castaño A., Olvera-Cervantes A. and Suárez-Llorens A., Quantile curves and dependence structure for bivariate distributions. Computational Statistical Data Analysis 51, 5112-5129, 2007.

- [Cardin and Pagani (2010)] Cardin M. and Pagani E., Some classes of multivariate risk measures. Mathematical and Statistical Methods for Actuarial Sciences and Finance, 63-73, 2010.

- [Cascos et al. (2011)] Cascos I., López Á. and Romo J., Data Depth in Multivariate Statistics. Boletín de Estadística e Investigación Operativa, CEIO 27(3), 151-174, 2011.

- [Cascos and Molchanov (2007)] Cascos I. and Molchanov I., Multivariate risks and depth-trimmed regions. Finance and stochastics 11(3), 373-397, 2007.

- [Cascos and Molchanov (2013)] Cascos I. and Molchanov I., Multivariate risk measures: a constructive approach based on selections. Mathematical Finance 0(0), 1-34, 2014.

- [Chaudhuri (1996)] Chaudhuri P., On a geometric notion of quantiles for multivariate data. Journal of the American Statistical Association 91, 862-872. 1996

- [Cousin and Di Bernardino (2013)] Cousin A. and Di Bernardino E., On multivariate extensions of Value-at-Risk. Journal of Multivariate Analysis 119, 32-46, 2013.

- [Daníelson et al. (2013)] Daníelson J., Jorgensen B., Samorodnitsky G., Sarma M. and De Vries C., Fat tails, VaR and subadditivity. Journal of econometrics 172(2), 283-291, 2013.

- [Embrechts and Puccetti (2006)] Embrechts P. and Puccetti G., Bounds for functions of multivariate risks. Journal of Multivariate Analysis 97, 526-547, 2006.

- [Fernández-Ponce and Suárez-Llorens (2002)] Fernández-Ponce J. and Suárez-Llorens A., Central regions for bivariate distributions. Austrian Journal of Statistics 31, 141-156, 2002.

- [Fraiman and Pateiro-López (2012)] Fraiman R. and Pateiro-López B., Quantiles for finite and infinite dimensional data. Journal Multivariate Analysis 108, 1-14, 2012.

- [Hallin et al. (2010)] Hallin M., Paindaveine D. and Šiman M., Multivariate quantiles and multiple-output regression quantiles: from optimization to halfspace depth. Annals of Statistics 38, 635-669, 2010.

- [Heyde et al. (2009)] Heyde C., Kou S. and Peng X., What is a good external risk measure: bridging the gaps between robustness, subadditivity, and insurance risk measure. (Preprint), 2009.

- [Jessen and Mikosh (2006)] Jessen A. and Mikosh T., Regularly varying functions. Publications de l’institute mathématique 79, 2006.

- [Koltchinskii (1997)] Koltchinskii V., M-estimation, convexity and quantiles. Ann. Statist. 25(2), 435-477, 1997.

- [Kong and Mizera (2012)] Kong L. and Mizera I., Quantile tomography: Using quantiles with multivariate data. Statistica Sinica 22(4), 1589-1610, 2012.

- [Lee and Prékopa (2012)] Lee J. and Prékopa A., Properties and calculations of multivariate risk measures: MVaR and MCVaR. Rutcor Research Report 25, 2012.

- [Laniado et al. (2012)] Laniado H., Lillo R., Pellerey F. and Romo J., Portfolio selection through an extremality stochastic order. Insurance: Mathematics and Economics, 51, 1-9, 2012.

- [Laniado et al. (2010)] Laniado H., Lillo R. and Romo J., Multivariate extremality measure. Working Paper, Statistics and Econometrics Series 08, Universidad Carlos III de Madrid, 2010.

- [Nappo and Spizzichino (2009)] Nappo G. and Spizzichino F., Kendall distributions and level sets in bivariate exchangeable survival models. Information Sciences 179, 2878-2890, 2009.

- [Nelsen (2006)] Nelsen R., An Introduction to copulas. (2nd edn), Springer-Verlag: New York, 2006.

- [Rachev et al. (2008)] Rachev S., Ortobelli S., Stoyanov S. and Fabozzi F., Desirable Properties of an Ideal Risk Measure in Portfolio Theory. International Journal of Theoretical and Applied Finance 11(1), 19-54, 2008.

- [Resnick (1987)] Resnick S., Extreme values, regular variation and point process. Springer-Verlag, 1987.

- [Serfling (2002)] Serfling R., Generalized quantile processes based on multivariate depth function, with applications in nonparametric multivariate analysis. Journal of Multivariate Analysis 83, 232-247. 2002

- [Shaked and Shanthikumar (2007)] Shaked M. and Shanthikumar J., Stochastic Orders. Springer Series in Statistics, 2007.

- [Tibiletti (1995)] Tibiletti L., Quasi-concavity property of multivariate distribution functions. Ratio Mathematica 9, 27-36, 1995.

- [Tibiletti (2001)] Tibiletti L., Incremental value at risk: traps and misinterpretations. Birkhauser Verlag, Basel (Switzerland), 355-364, 2001.

- [Wang et al. (2013)] Wang R., Peng L. and Yang J., Bounds for the sum of dependent risks and worst value at risk with monotone marginal densities. Finance and Stochastics 17(2), 395-417, 2013.

- [Zuo and Serfling (2000)] Zuo Y. and Serfling R., General notions of statistical depth function. Annals of Statistics 28(2), 461-482, 2000.