An Optimal Multiple Stopping Approach to Infrastructure Investment Decisions

Abstract

The energy and material processing industries are traditionally characterized by very large-scale physical capital that is custom-built with long lead times and long lifetimes. However, recent technological advancement in low-cost automation has made possible the parallel operation of large numbers of small-scale and modular production units. Amenable to mass-production, these units can be more rapidly deployed but they are also likely to have a much quicker turnover. Such a paradigm shift motivates the analysis of the combined effect of lead time and lifetime on infrastructure investment decisions. In order to value the underlying real option, we introduce an optimal multiple stopping approach that accounts for operational flexibility, delay induced by lead time, and multiple (finite/infinite) future investment opportunities. We provide an analytical characterization of the firm’s value function and optimal stopping rule. This leads us to develop an iterative numerical scheme, and examine how the investment decisions depend on lead time and lifetime, as well as other parameters. Furthermore, our model can be used to analyze the critical investment cost that makes small-scale (short lead time, short lifetime) alternatives competitive with traditional large-scale infrastructure.

keywords:

optimal multiple stopping , real option , infrastructure investments , lead time , operational flexibilityMSC:

[2010] 60G40 , 62L15, 62L20JEL:

C41 , G13 , H541 Introduction

The energy and material (e.g. water and petrochemicals) processing industries are traditionally characterized by very large unit-scale physical capital. For example, individual electric power generators rated in the 100s of MW, distillation towers in refineries measuring 100,000s of barrels-per-day of capacity, and mining trucks capable of hauling 400 tons of ore are common sizes in their respective industries. However, the recent emergence of low-cost automation technologies makes a modular, small-scale, and potentially distributed approach possible with comparable aggregate production capacity. This calls for a re-examination of the current “bigger-is-better” paradigm. Indeed, abandoning economies of unit scale in favor of economies of mass-production presents several opportunities, as discussed in Dahlgren et al. (2013). In contrast to the very long lifetimes of 25 years or more for typical large-scale capital, small and mass-produced equipment might be endowed with a much shorter physical lifespan. This could be either by design in construction or in operation with a limited maintenance schedule. Furthermore, with a smaller unit scale comes the ability to build to stock and drastically shorten lead times between the investment and operation. These factors provide the firm with additional flexibility to engage and disengage a given activity, which should be accounted for in the investment valuation and decision.

Motivated by this anticipated paradigm shift, we introduce here a framework that incorporates operational flexibility, lead time, capital lifespan, and multiple (finite/infinite) future investment opportunities. To this end, we formulate an optimal multiple stopping problem, where the firm maximizes the expected discounted reward from sequential investments. In particular, the project’s reward function captures the operational flexibility of temporarily suspending production to avoid negative cash flows. Additionally, it depends explicitly on two crucial elements, namely, lifetime and lead time. Under capacity constraint, the firm’s consecutive investments are separated (or refracted) by the capital lifetime. Hence, the firm’s investment decision bears similarity to the valuation of a forward-starting swing call option written on the reward.

Our main result is the characterization of the firm’s value function and optimal stopping rule. The optimal timing for multiple investments is described by a sequence of critical price thresholds. Furthermore, these thresholds are shown to be decreasing and converge to that corresponding to the case with infinite investment opportunities. Our analysis lends itself to an iterative algorithm that numerically solves for the optimal value function and all exercise thresholds, as opposed to the simulation approach commonly found in existing literature for swing-type options (Meinshausen and Hambly, 2004; Chiara et al., 2007; Bender, 2011). We examine the impacts of lead time and lifetime, as well as other parameters, on the investment decisions. Moreover, our model is also useful for analyzing the critical investment cost that makes small-scale (short lead time, short lifetime) alternatives competitive with traditional large-scale infrastructure.

As is well known, the real option approach to investment decisions can increase the project value above and beyond those rooted in classical net present value (NPV) arguments (Sick and Gamba, 2010; Dixit and Pindyck, 1994). In its inherent myopia, the NPV approach falls short of capturing the flexibility of timing since it, at best, only gives the decision maker an indication of whether or not a single investment should be made at the current time. Standard real investment option analysis addresses this limitation. Examples of the implementation of such an analysis regarding individual investment decisions can be found in, among others, Kaslow and Pindyck (1994); Frayer and Uludere (2001); Lumley and Zervos (2001); Carelli et al. (2010) and Westner and Madlener (2012). Nevertheless, the valuation of multiple consecutive investments has not received a great deal of attention in the industries in question. In the current paradigm, the individual investment is typically both large and long-lived, so the firm’s next investment decision, including capacity replacement, will be an issue of the far future. With such a long horizon, discounting would reduce future cash flows to minimal present values. However, with shorter lead times and lifetimes, future investments can potentially have significant bearing on current capital budgeting decisions, as we will show in this paper.

Our valuation approach accounts for multiple and possibly infinite future investment options, which in turn allows for a comparison of capital investments with different lifetimes. To illustrate, let us compare two projects with different lifetimes, namely, one with years and another with years. To address the difference in investment horizon, one approach would be to consider a longer horizon of 30 years, the smallest common multiple of 3 and 10, and compare the corresponding net present values. However, this method implicitly assumes seamless consecutive investments at the end of each lifetime. This may not be optimal to the firm since it ignores the embedded timing option in each investment decision.

Another feature of our valuation framework is to incorporate the flexibility to delay future investments depending on market conditions. Another advantage over the pairwise comparison is that we can easily examine how sensitive the investment timing is with respect to different model parameters, especially for all lead times and lifetimes. We do acknowledge that durability of capital is a path-dependent variable, leading to a variable lifetime. In contrast, our approach uses a fixed lifetime independent of the frequency of operation, and it may favor the posited status quo of capital with a longer prescribed lifetime. Our choice of a fixed lifetime, albeit a simplification, results from the trade-off between model tractability and realistic details.

The use of swing options has been most prevalent in energy delivery contracts where the holder has the right to alter, or ‘swing’, volumes up or down at the start of each time period (Jaillet et al., 2004; Deng and Oren, 2006). Rather than fixed-period contracts, the only constraint on the timing in our setting is a minimum refraction time between consecutive investments. As such, the valuation of the swing contract can be formulated as a refracted optimal multiple stopping problem (see e.g. Carmona and Touzi (2008); Carmona and Dayanik (2008)). Other financial applications involving multiple exercises include employee stock option valuation (Leung and Sircar, 2009; Grasselli and Henderson, 2009), and the operation of a physical asset (Ludkovski, 2008).

This paper is structured as follows. In Section 2 we introduce the investment decision as a general optimal multiple stopping problem. We also introduce a reward function that incorporates the flexibility to temporarily shut down production to avoid a negative cash flow. In the following section we state and prove sufficient conditions on a general reward function for the multiple stopping problem to have a well defined stopping boundary. We also present an algorithmic approach to finding the solution. In Section 4 we further motivate and analyze the specific reward function in the context of basic infrastructure investments and present numerical results. These results include a comparison of investment scenarios with short lifetimes and short lead times versus a traditional scenario with comparatively long lifetimes and lead times. Finally, concluding remarks and potential extensions are discussed in Section 5.

2 Problem Formulation

We consider a firm that has the ability to invest in capital equipment that produces a single good in a given market. Furthermore, we assume that this firm is acting as a price taker in this market, with a finite capacity constraint. These conditions imply that the investment decision will be of ‘bang-bang’ type, that is, either invest up to this limit or not at all. From an operational cost perspective, we are agnostic to whether the total capacity comes in one big unit or in 10,000 smaller units. Under such circumstances, we can without loss of generality analyze the investment timing on a per-unit-capacity basis.

We consider an exogenous and deterministic investment cost, , which depends on lifetime, , and lead time, , among other factors. These two parameters, both considered deterministic, also affect directly the net present value, , of a single investment. Moreover, we consider the discount rate, , used by the firm to also be exogenous and constant. In the background, we fix a complete probability space , equipped with a filtration . Let be an -adapted output price process. An investment generates a random cash flow-process of the form , where is a function known to the firm.

The expected discounted stream of future cash flows, minus the initial investment cost, yields the net present value

| (1) |

where we have introduced the conditional notation . The expression in (1) helps clarify the role of the lead time as the time between the expenditure and start of operation and access to the cash flow .

The limitation on the amount of capacity that can be active at any given point in time, as implied by the assumption of the role as a price taker discussed above, naturally introduces the notion of a refraction time. That is, two consecutive investments have to be separated with at least a time , the lifetime of the capital. With this being the only restriction on the investment strategy of the firm, the value of consecutive investments can be formulated as an optimal multiple stopping problem

| (2) |

The set is the set of all refracted stopping times , i.e. for . Under this requirement, nothing prevents the firm from having two consecutive investments operating with a seamless transition. This is because the decision to invest in future capital can be made before the current investment expires. Provided that a least upper bound in (2) actually exists, we can include in the stopping vector where , . For such a stopping rule, can be interpreted as the value of the contract when not every exercise is being called.

The tacit assumption that the supremum in (2) exists implies that is integrable and for every choice of and . For brevity we will suppress the parameters and in , and , unless such a dependence is specifically required. Since the firm is free to choose the timing of every investment, up to the condition of a refraction time , the following proposition highlights the optionality embedded in the investment decision. A proof is provided in A.

Proposition 1.

The value function , , satisfies,

| (3) |

with .

Proposition 1 reveals that it is never optimal to make the investment in the negative region of . This is because the firm has the flexibility to delay investment, and therefore, can always avoid value destruction.

We now consider the formulation in (1) and (2) under the geometric Brownian motion (GBM) model. Specifically, we model an output price process by the stochastic differential equation (SDE):

| (4) |

where is a standard Brownian motion. The drift rate and the variance parameter are both assumed constant. We denote to be the filtration generated by .

From the firm’s perspective, we assume that the investment cash flow is the difference between an uncertain output price , modeled by (4), and a constant operational cost . (In Section 4 we show that such a formulation is equivalent to a cash flow being the difference of two GBMs, possibly correlated, through a change of measure.) Moreover, the firm has the operational flexibility to temporarily suspend production if cost exceeds output price. Hence, the effective investment cash flow at any future time is given by

| (5) |

where . As such, the expectation of in (5) can be seen as the price of a European call option on with a strike price and maturity (see McDonald and Siegel (1985)), namely,

where is the standard normal cumulative distribution function, and where

Applying this to (1), the reward function becomes

Under this setting, we recast the optimal multiple stopping problem as a sequence of optimal single stopping problems. More precisely, we express the value as

| (6) |

The set is the set of all -stopping times and

By construction, the admissible stopping times are again refracted by at least (years). By standard optimal stopping theory, the Snell envelope is constructed to be the smallest supermartingale dominating the process , for every . For further details regarding this approach under a more general framework, we refer to Carmona and Touzi (2008).

3 Analytical Results

In this section we provide an analytical study for the optimal stopping problem in (6). Our main result is the characterization of the value function and optimal stopping rule, for every opportunities to invest (see Theorem 1). This leads us to develop an iterative approach to finding the value functions and the optimal exercise boundaries (see Corollary 1), which will be the foundation for our numerical algorithm to be presented in Section 4.1.

In the context of real investments, let us discuss some conditions on the general reward function . First, we assume that is continuous, increasing and sufficiently smooth. Additionally, we assume that there is a unique break-even point, , where , and for and for . Finally, we note that is bounded by some affine function of . Such a bound, together with an assumption that the discount rate exceeds the drift rate of the underlying process, ensures that perpetual waiting will lead to zero expected reward, i.e. . Under these conditions, we will first analyze the real option problem with a single investment opportunity, which will be the building block for solving the optimal multiple stopping problem.

3.1 Optimal Single Stopping Problem

We first consider the optimal single stopping problem

| (7) |

This problem is similar to the pricing of a perpetual American option with the payoff . Consider a candidate stopping time for problem (7):

with threshold . By the well-known Laplace transform of the first passage time of , see e.g. (Shreve, 2004, p.346), we have for ,

| (8) |

where

Note that the condition implies that . If , then and . From (8) we see that a necessary condition for to be an optimal stopping boundary is that maximizes . The linear bound on ensures the existence of such a maximum.

The first order condition for a maximum at is given by

| (9) |

where we have introduced the operator notation . The second order condition, sufficient to prove a maximum together with the first order condition above, can then be stated as

Note that a maximum of at is not a sufficient condition for an optimal stopping rule for a general reward function . One would also have to prove that satisfies the supermartingale property for this choice of . The following lemma gives the sufficient conditions for to be an optimal stopping rule for problem (7).

Lemma 1.

Let be a reward function in the single stopping problem (7). If is a global maximum for on and if

| (10) |

then

where is continuous on .

Remark 1.

The first order condition in (9), together with the condition that , , bounds the second derivative (convexity) of the reward function for large . Up to the condition of a maximum of at , the behavior of the function to the left of is irrelevant. The conditions in Lemma 1 are therefore less restrictive than imposing that the drift term of be monotone for all , as presented in (Dixit and Pindyck, 1994, pp.128-130) as a part of the sufficient conditions for a connected stopping boundary at for a perpetual American call on .

Proof: From (8) we know that , where

| (11) |

is a candidate for the solution. From the conditions on , it follows that, for ,

| (12) | |||||

| (13) |

Looking at the drift term111For a general underlying process , a localization procedure may be applied to eliminate the martingale term of upon expectation. of ,

| (14) | |||||

we observe that the first term vanishes identically, and the second term is non-positive following from (12) and (13). Hence, is a supermartingale, which implies that

| (15) |

3.2 Optimal Multiple Stopping Problem

Theorem 1.

Let be a reward function with a break-even point . If is convex for , with increasing for large , then, for every , there exists an such that

| (18) |

where

| (19) |

Moreover, the sequence is strictly decreasing, and is a strictly increasing sequence of continuous functions on . Also, for any bounded subset there exists a constant , such that , for and .

From a computational perspective it is convenient to introduce the auxiliary function through

| (20) |

With the conditions imposed on (bounded by a linear function, convexity of on and being increasing for large ) one can, in a similar way as for in the proof of Theorem 1, show that is an increasing sequence of continuous functions bounded on every bounded subset . Given the function we can reconstruct the value function through

| (21) |

Note that since for there are no convergence issues in (21). As a consequence of Theorem 1 we have the following result.

Corollary 1.

The functions , for , satisfy

| (22) |

The boundary point is the unique solution to

| (23) |

Corollary 1, together with equation (21), outlines the inductive algorithm used to find the solution to (6). Details of the implementation are found in the next section.

It now remains to consider the behavior of the solution to the optimal multiple stopping problem in the limit of infinitely many exercise rights. That is, we will investigate the value function

| (24) |

Since , where , is a supermartingale for all and since the refracted stopping times satisfy , we have

| (25) |

That is, is bounded on every bounded subset of . Defined through an integral in (24), this bound ensures continuity of on every bounded subset of . Finally, we state the following convergence result.

Proposition 2.

The sequence converges uniformly to on every bounded interval of .

Proof: Without loss of substantial generality, we assume that . Let be an optimal stopping rule for the value function in (24). Employing a similar argument as in (25), with bounding , we obtain

| (26) | |||||

In the second step we have used the fact that is an admissible, but not necessarily optimal, stopping rule for . With it follows from Theorem 1 that is strictly increasing and bounded, and hence convergent on . The uniform convergence of on then follows from (26).

4 Application to Infrastructure Investments

In this section, we apply our analytical results in Section 3 to the infrastructure investment problem and discuss a numerical implementation. Moreover, we study the sensitivity of the result with respect to the key parameters of lifetime and lead time , as well as the process parameters. Lastly, the proposed framework is employed to compare investment scenarios with relatively short lifetimes and lead times to a scenario with both a long lifetime and lead time. Such a comparison will reveal a critical investment cost of the short-lived scenario below which it will be competitive with the long-lived counterpart.

Recall from Section 2 the cash flow , in which we have incorporated the flexibility to temporarily suspend production to avoid a negative cash flow, namely,

The reward function associated with this cash flow is

| (27) |

where

| (28) |

Since is bounded by , one realizes that there is a linear function bounding . Investigating the derivatives of yields

| (29) |

In the second step, we have identified the derivative inside the integral as the Delta of the European call option. From (27)-(29) we see that is continuous and increasing in . Furthermore, since there exists a unique break-even point . Thus, satisfies all the conditions in the definition of a reward function presented in Section 3.1. By differentiation, we find that

where is the density function of the normal distribution. It can be seen that is convex for all , where . In turn, if , which is ensured by imposing a lower bound on , then is convex on , and consequently, all the conditions for Theorem 1 are satisfied and the algorithm outlined in Corollary 1 can be applied.

If the operational flexibility to suspend operation is removed then the expected cash flow can be readily integrated and the reward function in this case would be

where and are functions of the lead-time and lifetime only. That is, without the operational flexibility the reward function is clearly linear in , rendering convex on , and thus Theorem 1 is also applicable to this case.

4.1 Numerical Implementation

The expressions for and in (20) and (21) above form the basis of our numerical algorithm, whereby , , and are computed iteratively for The calculations below were carried out on a grid of 500 points regularly spaced between 0 and , where the latter was determined by the process and model paramenters. The computation of the expectation in (22) is complicated by the fact that is not bounded on . However, since our choice of reward function, in (27), is approximately affine for large , so are and . Rather than truncating the distribution we can instead linearly extrapolate outside the given grid. Since is decreasing, the necessary range of the grid depends mainly on . Specifically, was chosen to be the upper bound on a two-sided 99.9% confidence interval around ,

This choice of , together with the number of gridpoints, was an acceptable compromise between having a large enough grid to ensure a linear behavior of without undue computational complexity. When comparing different scenarios, i.e. different values for and , the largest grid was used throughout.

Using a trapezoidal method, the expectation in (22) was calculated as

| (30) |

where is the linear extrapolation of for and where is the density function of the lognormal distribution. The upper limit in (30) was chosen so that the support of the distribution contained a two-sided confidence interval around , for every .

The boundary points were found using a simple bisection method on the convex function in (23). The calculations of , and therefore also of and , were terminated once a tolerance , defined by

| (31) |

had reached . Such a tolerance yields a solution that is within % of , an accuracy that is likely good enough considering reasonable errors in the estimation of the underlying parameters. In the results below we denote by and the stopping boundary and the value function respectively at the termination of the algorithm according to the tolerance in (31).

Figure 1 demonstrates the convergence of the algorithm for the value function and the stopping boundary respectively. Default parameter values used in the calculations below are given in Table 1. The choice of fixed cost parameters ( and ), or their ratio , stems from observations in pertinent industries. Recent studies on energy investments and commodities report price volatilities in the neighborhood of 20% though they can occasionally experience short-term drastic increases (see Westner and Madlener (2012); Geman and Ohana (2009)). Therefore, setting corresponds to a relatively conservative choice as lower volatility favors the status quo. However, we will also examine a relatively high volatility () scenario in Figure 5. Additionally, the use of an effective discount rate of 5% is also in line with examples found in the literature in related fields, such as Frayer and Uludere (2001). Overall, the choices of parameter values are, albeit reasonable, mainly for illustrative purposes.

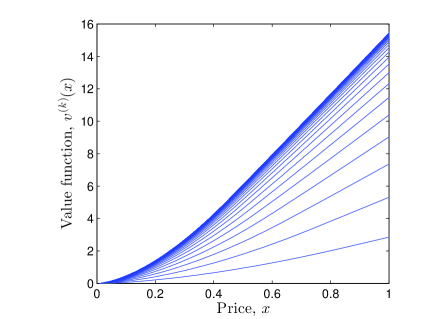

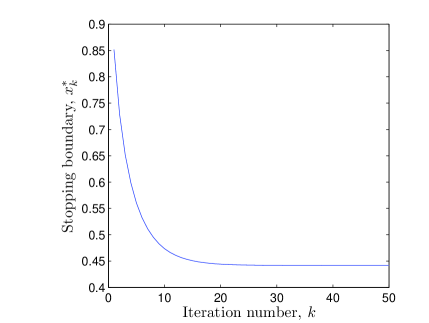

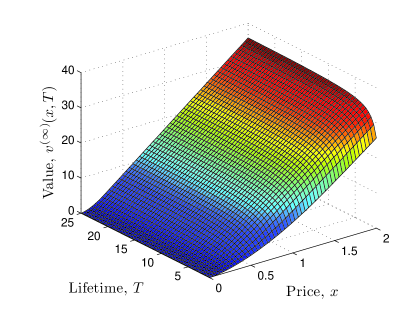

According to Theorem 1, is strictly increasing and the sequence of stopping boundaries is strictly decreasing. In Figure 1 (left), we see that the value function increases monotonically with each iteration. After 50 iterations the tolerance , defined above, was less than . Moreover, we notice that the value function appears linear for large . In Figure 1 (right), the stopping boundary decreases rapidly from 0.85 to 0.44 and we mention that the break-even point was . The convergence is clear even after 20 iterations. In particular, the stopping boundary (see (9)) from the first iteration helps us define the upper bound of the grid.

The stopping boundary is the price level at or above which the first investment should be made, given the option to make more investments later, each separated in time by at least the lifetime . Since firms rarely have an imposed number of investment renewals, the boundary is of primary interest. Contrasting the value of to reveals the impact of including future investment options on current investment decision. In Figure 1, the number of exercises (iterations) is , which together with the lifetime of years, gives a time horizon of more than years. Such a time horizon is practically infinite under reasonable circumstances. On the other hand, with a large , the number of remaining investment opportunities should have a smaller impact on the first investment timing. This is evidenced by the convergence of to a constant level as increases.

From our numerical tests, we find that the refraction time (lifetime) strongly influences the speed of convergence. This is intuitive due to the discount factor in the definition of in (22), reducing the differences over iterations. On the other hand, the lead time has much less bearing on the rate of convergence since it only affects the first investment timing. We will further examine the impacts of lifetime and lead time in the next subsection.

| Description | Parameter | Value |

|---|---|---|

| Lifetime | 5 | |

| Lead time | 1 | |

| Investment cost | 1 | |

| Operational cost | 0.1 | |

| Discount rate | 10% | |

| Drift rate | 5% | |

| Volatility | 20% |

4.2 Sensitivity Analysis

We will first investigate the sensitivity of with respect to the process parameters and . Later we investigate the sensitivity of both and the value function with respect to the main model parameters of lifetime and lead time .

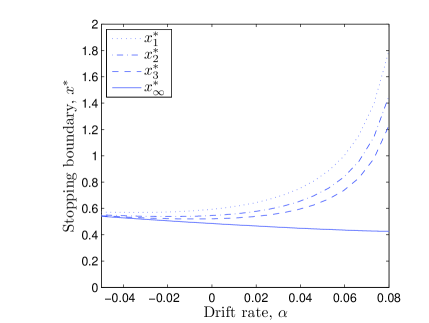

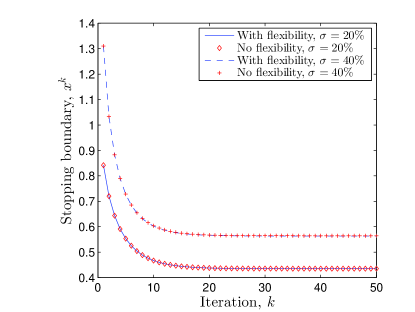

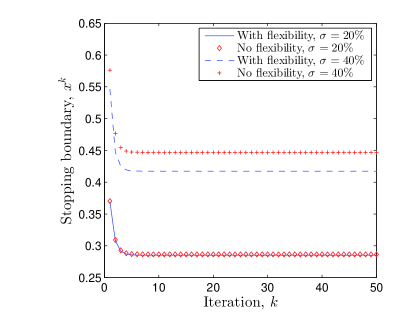

Low values of the drift rate corresponds to a higher ‘effective’ discount rate , sometimes called the convenience yield. This decreases the present value of future investment, which explains the minor difference between and for small , see Figure 2 (left). Conversely, a higher drift rate of the underlying enhances the value of future investments. This drives a greater wedge between the stopping boundary of a single investment compared to the stopping boundary of multiple consecutive investments for large . Consequently, this emphasizes the importance of including future investments in current decisions in environments with a high drift rate. Note that the same result is to be expected if decreasing the discount rate , still with the condition that . In the figure, we observe that as approaches (10%) the exercise boundaries , , increases rapidly. This is intuitive because theoretically the optimal exercise boundary would be infinite for . The same phenomenon also occurs for when is very close to .

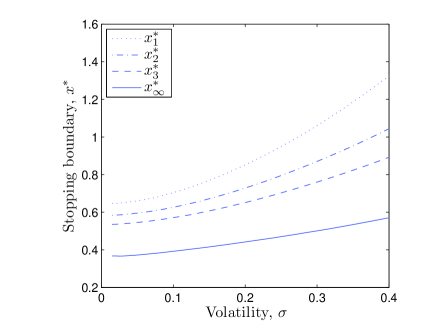

In Figure 2 (right), we see that the optimal exercise boundary increases with volatility . This suggests that in a more volatile environment the firm will demand a higher output price level in order to enter the market. We observe that the increasing pattern holds for finite , , as well as for the infinite case.

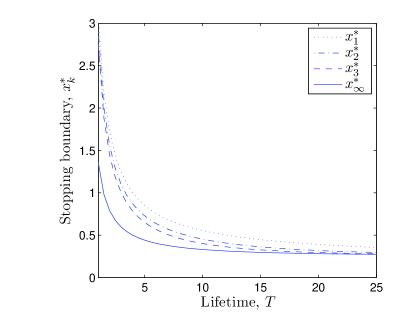

Now, we turn to examine the impact of lifetime , the parameter of main interest, on the stopping boundaries and value , with the same fixed cost . First, in Figure 3, we observe a minor difference between and for long lifetimes (for ). Intuitively, the incremental value of an additional investment 20 years or more from now is minimal due to the discount factor in (22) and (23). Therefore, for very long lifetimes, future investment decisions will not significantly influence the current decision to invest. However, for very short lifetimes, , there is a substantial difference between the optimal exercise levels with one and infinite investment opportunities (i.e. vs. for small ). In an intermediate regime, with lifetimes of 5 to 15 years, we observe that including only one or two future investment decisions will significantly affect the decision regarding the first investment. In both finite and infinite cases, the optimal exercise boundary decays rapidly with respect to lifetime. For instance, is almost flat for lifetime of 10 years or longer.

Considering the value of the multiple investment scenario for different lifetimes we observe a trend similar to the one regarding stopping boundary. The marginal impact of adding one year of life to short-lived capital is significant. However, this impact drastically decreases for longer-lived capital. For instance, as seen in Figure 3, the value of multiple investments in capital with a 25 year lifespan is virtually the same as capital with a life of 5 years, at the same investment cost and the same lead time . Even though the investment cost is the same, the increased flexibility in timing future investments in the scenario with the shorter lifetime makes them almost equally attractive.

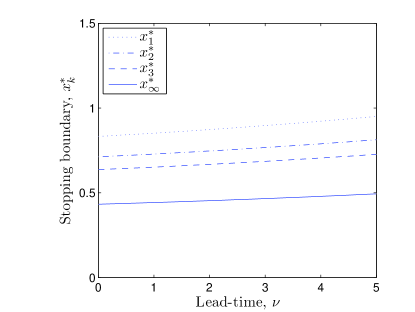

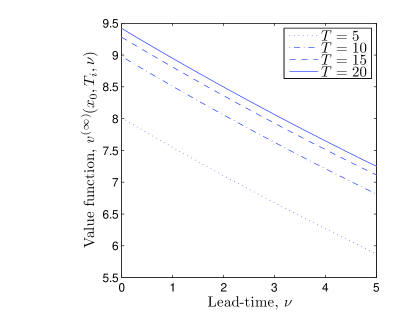

As seen in Figure 4 (left), the lead time does not substantially influence , nor the difference between and at fixed . In other words, varying lead times (within the given range) will barely affect the firm’s decision to invest. This is expected since seamless consecutive investments are possible regardless of the length of lead time. On the other hand, a longer lead time delays revenue generation relative to the outlay of the investment cost . Increasing lead time therefore decreases the net present value of every future investment. This explains the decreasing trend of the value function with respect to lead time in Figure 4 (right). In summary, the firm will realize a lower value with longer lead times of the investments, even though the corresponding exercise boundary changes only marginally. Displaying the value at different lead times and at a fixed price level but for several values of the lifetime again shows the diminishing returns of adding lifetime to capital.

From Section 2, we know that the reward function can be interpreted as the sum (integral) of European call options on the uncertain output price , with strike and maturities ranging over the lifetime. Since increasing the strike price of a European call decreases its value, the cost parameter has the same effects on the value , which in turn raises the stopping boundary . By similar reasoning, the same holds for .

Lastly, we examine the value of the option to temporarily suspend production for investments with short and long lifetimes. Two scenarios are compared in Figure 5, short-lived investments (, ) and long-lived investments (, ) at two levels of volatility and respectively. Note that in both cases an investment cost of was used, which explains a relatively higher stopping boundary for the short-lived capital. In this example, the operational flexibility appears to barely affect the investment decision in the short-lived scenario regardless of volatility. For low volatility the same indifference appears in the long-lived scenario as well, Figure 5 (right). However, in contrast to the short-lived scenario, the operational option leads to earlier investment timing under high volatility in the long-lived scenario. Comparing the left and right panels of Figure 5, we see that a shorter lifespan yields higher thresholds for future investments.

This operational flexibility feature is typically associated with competitive and unregulated markets, whereas many of the relevant industries for this paper traditionally have operated in regulated environments. Moreover, it could be argued that the conventional ‘bigger-is-better’ paradigm has historically invited regulations on the market since monopolies are often observed in industries with a large production scale. However, it is conceivable that these conditions may change as new technological advances allows for more competitive distributed small-scale production models.

As an example, these changes are occurring and subsequently making operational flexibility available in the electric power generation. In the United States, more than half of the states have moved towards deregulated power markets. While power producers face many different costs the dispatch order of the various available generators in a given market is to zeroth order a function of operational cost. That is, it is up to the individual producers to decide a price point where operation commences. It should be noted that the interpretation of a unit not operating is dependent on the time scales involved. For instance, hour-to-hour decisions typically implies putting generators into an synchronized reserve capacity called spinning reserves, whereas seasonal interruptions correspond to complete cold stop. Some technologies, like nuclear power, currently have a relatively low operational cost and are thus ahead in the dispatch order to meet demand (also called base load generation). In general, the value of the operational flexibility option is expected to be higher if the production involves lowers costs of suspension and resumption. Lastly, we remark that our standing assumption that the firm acts as a price taker would have to be revisited if the resulting change in supply should significantly impact the market price.

4.3 Critical Investment Cost

Many, if not all, of the fundamental process industries, such as e.g. energy, water and petrochemicals, have followed the trend of ‘bigger-is-better’ over the past century. Experience from a given industry gives us the investment cost (per unit of capacity) , as well as the lifetime and lead time of large-scale capital in the current paradigm. Transitioning to a paradigm of small-scale, mass-produced, and modular equipment will give rise to a new parameter ensemble, , where we a priori only infer shorter lifetimes and lead times. By considering an infinite time horizon, we can use the framework in this paper to find the critical investment cost that would render a small-scale approach competitive. That is, for a given reference ensemble , we find for every choice of and an such that , provided that .

The observed historical trend of increasing unit sizes seemingly suggests that total cost decrease with size. Nevertheless, we will here let the operational cost be independent of the parameters and . To motivate this setting for our examples below, we consider the total capacity to be installed at a single location, so ancillary costs, such as transportation costs of inputs and outputs to and from the plant, administrative costs, cost of security etc., ought not depend on the granularity of the hardware inside this black box. This leaves primarily two potentially size-dependent factors that can affect operational costs; labor and efficiency. Historically, the necessary amount of operational labor increases with the number of individual units employed. Operating fewer and larger units therefore increases labor productivity and lowers labor cost per unit output. However, advances in automation make it possible today to decouple the amount of required labor from the number of individual units at reasonable cost. As to efficiency, from a physical perspective one can in some cases claim that larger units have lower dissipative losses (e.g. through friction and unwanted heat transfer) and hence are more efficient and therefore less costly to operate. On the other hand, it is not always clear how important these effects are. For instance, a statistical analysis on the size-dependency of cost in four different electricity generating technologies showed that once labor cost is removed, unit size is not a significant factor affecting total operational cost (Dahlgren et al., 2013).

As an illustration, we can compare a single-cycle thermal power plant to an internal combustion engine, both performing fundamentally the same task of converting chemical energy into mechanical work. Under reasonable circumstances, they can do so at comparable efficiencies. The car engine is mass-produced on the order of days. The power plant, on the other hand, is typically not ready for operation until several years have passed since the decision to invest was made. Moreover, the power plant is designed to last for decades while the car engine presumably will have a lifetime on the order of years under constant operation. How much would one be willing to pay for an engine that is fully automated, retrofitted to run on the same fuel and equipped with a generator to produce electricity? Such a mini-power plant can reasonably be assumed to incur similar levels of operational costs per kWh produced as its large-scale counterpart. This leaves investment cost, lifetime and lead time as the main distinguishing features from the large-scale power plant.

We start by analyzing the reward function in (27) for large . It can be seen that for , and therefore, is asymptotically affine with

| (32) | |||||

For large enough values of the function is affine as well and

where . Using (32) to substitute for , we obtain for large :

where the slope is independent of the lifetime and decreasing in the lead time . From the definition of in (20) it follows that the same properties can be ascribed to the value function for large . Consequently, comparing different scenarios, i.e. different , and , the scenario with the shortest lead time will always have the higher value for large enough values of .

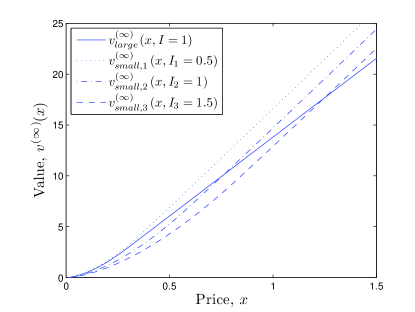

Now we compare the value of small-scale capital, here characterized by years, years, against a benchmark of years, years, representing traditional large-scale capital. Furthermore, as a point of reference we set , which together with the constant operational cost (assumed the same for every choice of , and ) provides a relative monetary scale.

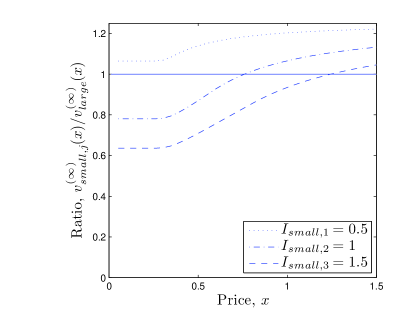

In Figure 6, the value of the large-scale parameter ensemble is displayed alongside with , for three different investment costs, . With their shorter lead time, the values is seen to exceed for large values of , verifying the analysis above.

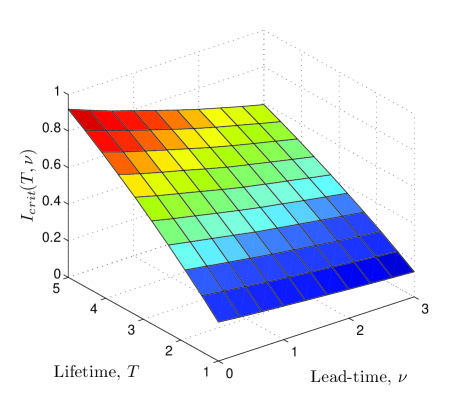

From Theorem 1 we know that is proportional to for small enough values of . This explains the constant appearance of the ratio in Figure 6 for small . The value of the scenario with the lowest investment cost clearly exceeds the value of the ‘large’ scenario for all prices . Indeed, given , and we can find a critical value , such that the value of the ‘small’ scenario is greater at any price level, as long as . This leads to the contour plot in Figure 7, which displays the critical values for different lifetimes, and lead times, . In Section 4.2, it has been observed that the value increases with lifetime (see Figure 3) and decreases with lead time (see Figure 4). This helps explain the trend of with respect to and in Figure 7. Precisely, in this domain of short lifetimes, a reduction in lead time yields a higher critical investment cost, which in turn increases the competitiveness of the small-scale approach.

As an example, with years and we can infer from Figure 7 that . That is, despite a difference of a factor 10 in lifetime ( years), the investment cost is required to differ only by a factor of 2 between the short and long lifetime scenarios in order for the short-lived one to be preferable.

The closest resemblance of an estimation of using a simplistic NPV argument without any optionality would be to compare the discounted investment costs over an infinite horizon. That is, we can assume that capital is replaced every (resp. ) years under the long (resp. short) lifetime scenarios. For simplicity, disregarding features like lead times, operational flexibility, stochastic prices, and optimal multiple stopping, we equate the discounted costs over an infinite horizon to get

where denotes the critical investment cost of the short-lived scenario under the NPV argument. Using the same example as above, with years, years, and , we find that . Comparing to the critical investment cost above, the value of the optionality in this particular example permits twice the investment cost that would be suggested by standard net present cost arguments.

Lastly, we note that, in the example with the car engine and the power plant, the cost per kW of capacity of the car engine is almost two orders of magnitude less than that of the power plant (Larminie and Dick, 2003). Clearly, the critical costs suggested in Figure 7 are not nearly as dramatic. This suggests great potential in abandoning the customized, large-scale investments in favor of mass-produced and modular capital.

5 Conclusions

We have developed a framework for valuing repeated infrastructure investments and comparing traditional capital with long lifetimes and lead times to a mass-produced version with a much shorter lifespan and lead times. We found that including future investments in present valuations significantly affects the exercise boundary, especially when the individual investment is short-lived. Also, the marginal benefit of increasing lifetime rapidly diminishes when considering multiple investments. Furthermore, this framework allows for a determination of a critical investment cost of capital with lifetimes and lead times that deviate from industry standards. One of examples (see Figure 7) reveals that reducing lifetime of capital from a typical 25 years to 2.5 years need only be accompanied by a decrease of a factor of 2 in investment cost in order to be superior, in overall value terms.

For our analysis and tractability, we have worked with a lognormal stochastic cash flow. Working with the lognormal process, we obtain analytical value function for the single stopping problem and analytical results like Theorem 1. Alternatively, for more realistic representation of commodity price dynamics, other processes, e.g. with mean reversion and jumps, can be used, though these settings may not be as amenable to mathematical analysis and the numerical implementation can be much more challenging and cumbersome. For instance, under the exponential Ornstein-Uhlenbeck price dynamics, the single stopping problem does not admit a closed-form solution, and the optimal exercise threshold can only be found from an implicit equation (see Leung et al. (2014)). However, under mean reversion, the value of an investment with considerable lead time and lifetime is expected to generate a cash flow close to the finite long-run mean. Shorter lived, and more quickly deployed capital would, on the other hand, be more suited to both exploit positive deviations from the mean, and also avoid periods of low prices. In the mean reversion framework, we would therefore anticipate that the critical investment cost, , of the small-scale investment to achieve parity between the small-scale and large-scale scenarios to be higher than those found in Figure 7. This suggests that a small-scale and modular approach may be attractive to large infrastructure investments.

There are a number of directions for future research. First, one can incorporate the firm’s aversion to risk and ambiguity associated with the stochastic investment returns, as discussed in Henderson (2007) and Jaimungal (2011) in the case of single investment. Moreover, additional information on the technological change, industry outlook, and future investment cost will enhance the decision analysis. For instance, intuition suggests that frequent technological advancement is more easily harnessed with a more rapid turnover since outdated technology can be abandoned without sacrificing investments with a long remaining horizon. Similarly, regulatory risk is less of an issue with shorter investment windows. This issue is very much in focus in the energy sector today with the looming threat of climate change and related concerns about carbon emissions. For instance, burning cleaner than coal and oil, natural gas is touted as a bridge fuel to cleaner technologies in the future. However, in the current paradigm of large-scale units with long lifetimes, the dramatic increase in natural gas-fired capacity in recent years means a commitment to a fossil fuel for at least another quarter of a century.

Acknowledgements

The authors are grateful to Klaus Lackner, Garrett van Ryzin and Caner Göçmen for their useful suggestions and conversations. Tim Leung’s research is partially supported by NSF grant DMS-0908295.

Appendix A Proof of Proposition 1

For every fixed stopping rule , we define a subsequence , , of by recording only those stopping times at which the reward is non-negative:

In the case of finite we can append the subsequence with infinite stopping times, to create the full sequence . Since the stopping times within are refracted with at least the constant time , the same is true for those in by construction, and therefore .

By avoiding those stopping times with a negative reward, the total discounted reward:

is dominated by in expectation, namely,

| (33) |

In addition, when is taken to be , we have the equality , almost surely. That means that maximizing over the stopping rules for the original problem will achieve the upper bound (RHS of (3)) with the non-negative reward . In summary, we obtain

Appendix B Proof of Theorem 1

Proof: Be the definition of the reward function with a break-even point , we know that and for , and . This implies that

Particularly, since is convex on and increasing for large , there is exactly one solution, , to , and furthermore, for . Recall from Lemma 1 that

| (34) |

where . In addition,

| (35) |

Since for any integrable function , we apply (35) to get

| (36) | |||||

where in the second step we have used the fact that vanishes in the continuation region of , i.e. for . Since is assumed convex on , the expectation is also convex on . Being the sum of two convex functions, is also convex on . Moreover, since is an increasing function (and strictly positive for ), (36) implies that is increasing for large enough .

We observe from (34) and (35) that is a continuously differentiable increasing function with . Furthermore, if is bounded by , for some , then one can show that , and therefore

| (37) |

This ensures the existence of a maximum at to the function , and consequently also the existence of a solution to . Also, Proposition 1 implies that as it is never optimal to exercise with negative payoff. The convexity of on ensures that there is exactly one such maximum, uniquely defined by

Hence, applying Lemma 1 again we obtain

Also, from the bound on in (37) we infer that .

Repeating the argument above, we can similarly show the existence and uniqueness of a stopping boundary , for every , and also derive an upper bound for each :

| (38) |

Next, we proceed to prove by induction that , which together with the previous part of the proof would imply that . As previously remarked, is positive for . From (36) it follows that

Now, assume that . From the definition of in (19) we have

As for the monotonicity of the sequence , we first show that . Since from Lemma 1, it follows from (19) that

| (39) |

By the fact that and , the inequality

holds for . Moreover, since is maximized at , we see that

Similarly, for ,

| (40) |

Hence, we have shown that . By induction, we obtain

With this inequality we can follow the steps from (39) to (40) to arrive at . Finally, the inequality in (38) implies that the value function admits the following bound for any :

References

- Bender (2011) Bender, C. (2011). Dual pricing of multi-exercise options under volume constraints. Finance and Stochastics, 15:1–26.

- Carelli et al. (2010) Carelli, M., Garrone, P., Locatelli, G., Mancini, M., Mycoff, C., Trucco, P., and Ricotti, M. (2010). Economic features of integral, modular, small-to-medium size reactors. Progress in Nuclear Energy, 52(4):403–414.

- Carmona and Dayanik (2008) Carmona, R. and Dayanik, S. (2008). Optimal multiple stopping of linear diffusions. Mathematics of Operations Research, 33(2):446–460.

- Carmona and Touzi (2008) Carmona, R. and Touzi, N. (2008). Optimal multiple stopping and valuation of swing options. Mathematical Finance, 18(2):239–268.

- Chiara et al. (2007) Chiara, N., Garvin, M., and Vecer, J. (2007). Valuing simple multiple-exercise real options in infrastructure projects. Journal of Infrastructure Systems, 13(2):97–104.

- Dahlgren et al. (2013) Dahlgren, E., Göçmen, C., Lackner, K. S., and van Ryzin, G. (2013). Small modular infrastructure. The Engineering Economist, 58(4):231.

- Deng and Oren (2006) Deng, S. and Oren, S. (2006). Electricity derivatives and risk management. Energy, 31(6-7):940–953. Electricity Market Reform and Deregulation.

- Dixit and Pindyck (1994) Dixit, A. and Pindyck, R. (1994). Investment Under Uncertainty. Princeton University Press.

- Frayer and Uludere (2001) Frayer, J. and Uludere, N. (2001). What is it worth? Application of real options theory to the valuation of generation assets. The Electricity Journal, 14(8):40–51.

- Geman and Ohana (2009) Geman, H. and Ohana, S. (2009). Forward curves, scarcity and price volatility in oil and natural gas markets. Energy Economics, 31(4):576 – 585.

- Grasselli and Henderson (2009) Grasselli, M. and Henderson, V. (2009). Risk aversion and block exercise of executive stock options. Journal of Economic Dynamics and Control, 33(1):109–127.

- Henderson (2007) Henderson, V. (2007). Valuing the option to invest in an incomplete market. Mathematics and Financial Economics, 1(2):103–128.

- Jaillet et al. (2004) Jaillet, P., Ronn, E. I., and Tompaidis, S. (2004). Valuation of commodity-based swing options. Management Science, 50(7):909–921.

- Jaimungal (2011) Jaimungal, S. (2011). Irreversible investments and ambiguity aversion. Working Paper, University of Toronto.

- Kaslow and Pindyck (1994) Kaslow, T. and Pindyck, R. (1994). Valuing flexibility in utility planning. The Electricity Journal, 7(2):60 – 65.

- Larminie and Dick (2003) Larminie, J. and Dick, A. (2003). Fuel Cell Systems Explained. John Wiley & Sons Ltd.

- Leung et al. (2014) Leung, T., Li, X., and Wang, Z. (2014). Optimal multiple trading times under the exponential OU model with transaction costs. Working Paper.

- Leung and Sircar (2009) Leung, T. and Sircar, R. (2009). Accounting for risk aversion, vesting, job termination risk and multiple exercises in valuation of employee stock options. Mathematical Finance, 19(1):99–128.

- Ludkovski (2008) Ludkovski, M. (2008). Financial hedging of operational flexibility. International Journal of Theoretical and Applied Finance, 11(8):799–839.

- Lumley and Zervos (2001) Lumley, R. and Zervos, M. (2001). A model for investments in the natural resource industry with switching costs. Mathematics of Operations Research, 26(4):637–653.

- McDonald and Siegel (1985) McDonald, R. and Siegel, D. (1985). Investment and the valuation of firms when there is an option to shut down. International Economic Review, 26(2):331–349.

- Meinshausen and Hambly (2004) Meinshausen, N. and Hambly, B. M. (2004). Monte Carlo methods for the valuation of multiple-exercise options. Mathematical Finance, 14(4):557–583.

- Shreve (2004) Shreve, S. (2004). Stochastic Calculus for Finance II: Continuous-Time Models. New York, NY: Springer.

- Sick and Gamba (2010) Sick, G. and Gamba, A. (2010). Some important issues involving real options: An overview. Multinational Finance Journal, 14(1/2):73–123.

- Westner and Madlener (2012) Westner, G. and Madlener, R. (2012). Investment in new power generation under uncertainty: Benefits of CHP vs. condensing plants in a copula-based analysis. Energy Economics, 34(1):31–44.