Consumption investment optimization with Epstein-Zin utility in incomplete markets

Abstract.

In a market with stochastic investment opportunities, we study an optimal consumption investment problem for an agent with recursive utility of Epstein-Zin type. Focusing on the empirically relevant specification where both risk aversion and elasticity of intertemporal substitution are in excess of one, we characterize optimal consumption and investment strategies via backward stochastic differential equations. The supperdifferential of indirect utility is also obtained, meeting demands from applications in which Epstein-Zin utilities were used to resolve several asset pricing puzzles. The empirically relevant utility specification introduces difficulties to the optimization problem due to the fact that the Epstein-Zin aggregator is neither Lipschitz nor jointly concave in all its variables.

Key words and phrases:

Consumption investment optimization, Epstein-Zin utility, Backward stochastic differential equation1. Introduction

Risk aversion and elasticity of intertemporal substitution (EIS) are two parameters describing two different aspects of preferences: risk aversion measures agent’s attitude toward risk, while EIS regulates agent’s willingness to substitute consumption over time. However commonly used time separable utilities force EIS to be the reciprocal of risk aversion, leading to a rich literature on asset pricing anomalies, such as the equity premium puzzle, the risk-free rate puzzle, the excess volatility puzzle, the credit spread puzzle, and etc.

Recursive utilities of Kreps-Porteus or Epstein-Zin type and their continuous-time analogue disentangle risk aversion and EIS, providing a framework to resolve aforementioned asset pricing puzzles, cf. [2] and [1] for the equity premium puzzle and the risk-free rate puzzle, [4] for the excess volatility puzzle, and [5] for the credit spread puzzle. All these studies require EIS to be larger than in order to match empirical observations. Bansal and Yaron [2] also empirically estimated to be around . On the other hand, empirical evidence suggests that risk aversion is in excess of . It then follows from and that . Hence an agent with such a utility specification prefers early resolution of uncertainty (cf. [30] and [41]), therefore asks a sizeable risk premium to compensate future uncertainty in the state of economy.

Other than aforementioned utility specification, two other ingredients are also important in these asset pricing applications. First, investment opportunities in these models are driven by some state variables, which usually lead to unbounded market price of risk; for example, Heston model in [9], [26], and [31], Kim and Omberg model in [24] and [43]. Second, the first step in all these applications is to understand the superdifferential of the indirect utility for the representative agent, because it is the source to read out equilibrium risk-free rate and risk premium, cf. [2, Appendix]. Therefore, it is important to rigorously study the consumption investment problem simultaneously accounting these three ingredients: utility specification, models with unbounded market price of risk, and superdifferential of indirect utility. However, the following literature review shows that, such a study, in a continuous-time setting, was still missing from the literature. This paper fills this gap.

In the seminal paper by Duffie and Epstein [13], stochastic differential utilities (the continuous-time analogue of recursive utilities, cf. [28]) are assumed to have Lipschitz continuous aggregators. Hence the Epstein-Zin aggregator, which is non-Lipschitz, is excluded. Schroder and Skiadas [38] studied the case where is positive.111The parameter in [38] is here. Hence equation (8c) therein implies . However the empirically revelent parameter specification leads to . Kraft, Seifried, and Steffensen [29] studied incomplete market models with unbounded market price of risk, however their assumption on and (cf. Equation (H) therein) excludes the case and .

Regarding market models, Schroder and Skiadas [38] studied a complete market with bounded market price of risk. Schroder and Skiadas [39, Section 5.6], Chacko and Viceira [9] both considered incomplete markets and Epstein-Zin utility with unit EIS. Chacko and Viceira [9], Kraft, Seifried, and Steffensen [29] studied a market model whose investment opportunities are driven by a square root process, leading to unbounded market price of risk.

Regarding the superdifferential of indirect utility, its form can be obtained by a heuristic calculation using the utility gradient approach, cf. [15]. However, rigorous verification needs the aggregator to satisfy a Lipschitz growth condition (cf. [13] and [15]), or joint concavity in both consumption and utility variables (cf. [16]). As we shall see later, when and , the Epstein-Zin aggregator is neither Lipschitz continuous nor joint concave. On the other hand, for Epstein-Zin utility with , Schroder and Skiadas [38] verified the superdifferential via an integrability condition (cf. [38, Lemma 2]) and the property that the sum of deflated wealth process and integral of deflated consumption stream is a supermartingale for arbitrary admissible strategy, and is a martingale for the optimal strategy (cf. [38, Equation (1)]). Both these two conditions are verified in [38, Theorem 2 and 4] for complete market models with bounded market price of risk.

In this paper, we analyze a consumption investment problem for an agent with Epstein-Zin utility with and a bequest utility at a finite time horizon. This agent invests in an incomplete market whose investment opportunities are driven by a multi-variate state variable. Rather than the Campbell-Shiller approximation, which is widely applied for utilities with non-unit EIS, we study the exact solution. As illustrated in [29, Section 6], there can be a sizeable deviation of the Campbell-Shiller approximation from the exact solution, highlighting the importance of exact solution.

A similar problem has also been studied recently by Kraft, Seiferling, and Seifried [27]. In this paper, the relation between and in [29] is removed, all configurations of and are considered including the case. Verification result is obtained following the utility gradient approach in [15] and [38], complemented by a recent note of Seiferling and Seifried [40] for the case. Nevertheless, [27] focuses on models with bounded market price of risk (cf. Assumptions (A1) and (A2) therein). This excludes models, such as Heston model and Kim-Omberg models, which are widely used in aforementioned asset pricing applications. Comparing to [27] and all other aforementioned existing results, the current paper extends the previous literature in three respects.

First, in contrast to the utility gradient approach, the verification result is obtained by comparison results for backward stochastic differential equations (BSDE). Rather than employing the dynamic programming method as in [29] and [27], optimal consumption and investment strategies are represented by a BSDE solution, cf. Theorem 2.14 below. Extending techniques of Hu, Imkeller, and Müller [20] and Cheridito and Hu [11], who studied optimal consumption investment problems for time separable utilities, we verify the candidate optimal strategies for Epstein-Zin utility.

Second, our method is designed for market models with unbounded market value of risk. Utilizing Lyapunov functions, borrowed from [42, Chapter 10], we prove in Lemma B.2 below that certain exponential local martingale is martingale, which is a key component of our verification argument.

Third, we verify the superdifferential of indirect utility. Comparing to [38], the integrability condition in Lemma 2 therein is satisfied when .222The specification is related to [38, Case 3 in page 113], which established the utility gradient inequality. Even through its proof is independent of market model, it uses the existence and concavity of Epstein-Zin utility, which are established in [38, Appendix A] under the assumption . Therefore one needs to replace [38, Appendix A] by Propositions 2.2 and 2.4 below which confirm the existence and concavity of Epstein-Zin utility when . During the revision of this paper, these properties are also confirmed in [40] for a general semimartingale setting. For the second step of verification in [38] and [27], it requires that the sum of deflated wealth process and integral of deflated consumption stream is a supermartingale for any admissible strategy, and is a martingale for the optimal one. We obtain this property (see Theorem 2.16 below) as a by-product of our verification result. This result is established for models with unbounded market price of risk, hence meets demands coming from aforementioned applications on asset pricing puzzles.

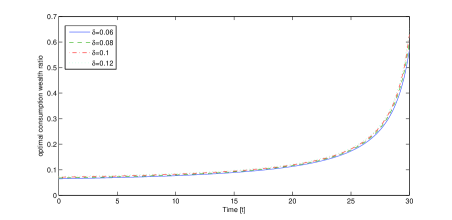

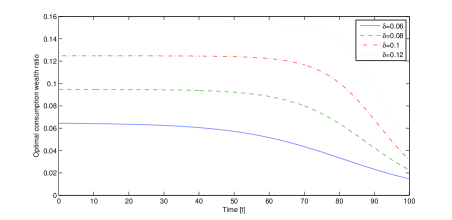

Our general results in Section 2 are specialized to two examples in Section 3. There numeric results reveal an interesting phenomenon. As time horizon goes to infinity, convergence of the finite horizon solution to its stationary long run limit is very slow when . Figure 2 shows that this convergence takes at least years in an empirically revelent utility and market setting. Moreover, the convergence is sensitive to the time discounting parameter: it is much slower when the discounting parameter decreases slightly. This is in contrast to the case, where the convergence is much faster (around years) and is less sensitive to the time discounting parameter. This observation implies that, in the setting, the finite horizon optimal strategy can be far away from its infinite horizon analogue, even when we consider a lifelong consumption investment problem.

The remaining of this paper is organized as follows. After Epstein-Zin utility is introduced in Section 2.1, the consumption investment problem is introduced and main results are presented in Section 2.2. Then main results are specialized in two examples in Section 3, where general assumptions of main results are verified under explicit parameters restrictions, which include many empirically relevant cases. All proofs are postponed to appendices.

2. Main results

2.1. Epstein-Zin preferences

We work on a filtered probability space . Here is the augmented filtration generated by a dimensional Wiener process , where and are the first and the last components, respectively, and satisfies the usual hypotheses of right-continuity and completeness.

Let be the class of nonnegative progressively measurable processes on . For and , stands for the consumption rate at and represents a lump sum consumption at . We consider an agent whose preference over valued consumption streams is described by a continuous time stochastic differential utility of Kreps-Porteus or Epstein-Zin type. To describe this preference, let represent the discounting rate, be the relative risk aversion, and be the EIS. We focus on the case. In this case, define the Epstein-Zin aggregator via

| (2.1) |

This is a standard parametrization used, for instance, in [12]. Given a bequest utility function , the Epstein-Zin utility over the consumption stream on a finite time horizon is a process which satisfies

| (2.2) |

where stands for .

Remark 2.1.

Epstein-Zin utility generalizes the standard time separable utility with constant relative risk aversion. Indeed, when , the aggregator reduces to . Then (2.2) with can be represented explicitly as the standard time separable utility:

As discussed in introduction, we are interested in the empirical relevant case where and . In this case, is violated, hence (2.2) is not time separable.

When follows a diffusion, the existence of was established by Duffie and Lions [14] via partial differential equation techniques. We work with a non-Markovian setting and construct via the following BSDE:

| (2.3) |

Denote

When , . The generator in (2.3) is

Then has super-linear growth in when . Therefore the BSDE (2.3) does not have a Lipschitz generator. Nevertheless, consider and the following transformed BSDE:

| (2.4) |

When , the generator in (2.4) satisfies the monotonicity condition, i.e., is decreasing. This allows us to establish the existence and uniqueness of solutions to (2.3), hence define satisfying (2.2).

Let us introduce the set of admissible consumption streams as

Proposition 2.2.

Remark 2.3.

When a BSDE satisfies the monotonicity condition, it is customary to assume its terminal condition to be square integrable, cf. [34, Theorem 2.2]. However this imposes unnecessary restrictions for later described utility maximization problem, in the sense that the bequest utility needs to be square integrable to define the associated Epstein-Zin utility. Therefore, Proposition 2.2 only asks for the terminal condition to be an integrable random variable.

Having defined , we expect that, as a utility functional, is concave. This would follow from the standard argument when is jointly concave in and , cf. [13, Proposition 5]. However, calculation shows that in (2.1) is not jointly concave when and .444 is jointly concave in and if and only if . Nevertheless, utilizing an orderly equivalent transformation of , introduced in [13, Example 3], the following proposition confirms the concavity of .

Let us define . Calculation shows that satisfies

| (2.5) |

Observe that the generator of (2.5) is now jointly concave in when .

Proposition 2.4.

When , for any , and , if , then

Remark 2.5.

The integrability condition in does not implies the convexity of . Indeed, since , for both and does not imply the same integrability for . However Proposition 2.4 implies the concavity of on any convex subset of , for example, .

2.2. Consumption investment optimization

Having established the existence of Epstein-Zin utility in the previous section, we consider an optimal consumption investment problem for an agent with such a utility.

Consider a model of a financial market with a risk free asset and risky assets with dynamics

| (2.6) |

where is a diagonal matrix with elements of on the diagonal, is a dimensional vector with every entry . Given a correlation function and , satisfying (the identity matrix), defines a dimensional Brownian motion. In (2.6), is a valued state variable satisfying

| (2.7) |

Here is an open domain, , , , , and . These model coefficients satisfy following assumptions.

Assumption 2.6.

, , , , , and are all locally Lipschitz in ; and are positive definite in any compact subdomain of ; is bounded from below on , moreover, dynamics of (2.7) does not hit boundary of in finite time.

In the previous assumption, local Lipschitz continuity of coefficients and the nonexplosion assumption combined imply that (2.7) admits a unique -valued strong solution . When the interest rate is bounded from below, due to , is bounded from below as well.

An agent, whose preference is described by an Epstein-Zin utility, invests in this financial market. Given an initial wealth , an investment strategy , and a consumption rate , the wealth of the agent follows

| (2.8) |

Throughout the paper, stand for , and , respectively, and the superscript is sometimes suppressed on to simplify notation. A pair of investment strategy and consumption stream is admissible if and its associated wealth process is nonnegative. The agent aims to maximize her utility .

We will further restrict admissible strategies to a permissible set. But let us first characterize the optimal value process via a heuristic argument. By homothetic property of Epstein-Zin utility, we speculate that utility evaluated at the optimal strategy has the following decomposition555The decomposition (2.9) is widely used for (time-separable) power utilities, cf. eg. [35].:

| (2.9) |

where satisfies the following BSDE

| (2.10) |

Let us determine the generator in what follows. Parameterizing by , the wealth process satisfies

We expect from the standard dynamic programming principle that is a supermartingale martingale for arbitrary strategy, and is a martingale for the optimal strategy. Let us calculate the drift of the previous process. Calculation shows that

Therefore, the drift of reads (the time subscript is omitted to simplify notation)

| (2.11) |

We expect that the drift above is negative for arbitrary and is zero for the optimal strategy. Therefore, the generator for (2.10) can be obtained by taking supremum on and in the previous drift and setting it to be zero. Following this direction, we notice that the randomness in comes only from , which is driven by , moreover, the terminal condition of (2.10) is zero. As a result, is necessarily zero. Therefore, we can reduce (2.10) to

| (2.12) |

where is given by

| (2.13) |

Here, suppressing the subscript ,

where is the -identity matrix. Recall from Assumption 2.6 that is bounded from below. Therefore implies that there exists a positive constant such that on . The infimum in (2.13) are due to , and they are attained at

| (2.14) |

where is the wealth process associated to the strategy . Therefore and are candidate optimal strategies.

Coming back to (2.12), even though the generator has an exponential term in and a quadratic term in , the parameter specification allows us to derive a priori bounds on . In particular, is bounded from above by a constant. Meanwhile, since the quadratic term of in will be shown to be nonnegative, the lower bound of can be obtained by studying a BSDE whose generator does not contain this quadratic term. As a result, a solution to (2.12) can be constructed under the following mild integrability conditions.

Assumption 2.7.

-

i)

defines a probability measure equivalent to ;

-

ii)

.

Here denotes the stochastic exponential for .

Remark 2.8.

Since the generator contains a linear term in , it is natural to apply Girsanov theorem. Assumption 2.7 i) allows us to do this and write (2.12) under . This assumption can be checked by explosion criteria; see Section 3 for examples. In ii), the standard exponential moment condition in [6] is avoid, due to the special structure of : the quadratic term in is nonnegative, and is bounded from above by .

Proposition 2.9.

Having constructed , the strategies in (2.14) are well defined. To verify their optimality, we need to further restrict the admissible strategies to a permissible set: is permissible if and is of class on .666When is bounded from below, for example, both and are bounded, (2.15) implies that is bounded from below as well. Then is permissible if and is of class on . This is exactly the definition of permissibility used in [11] for the time separable utilities with .

To verify the optimality for , let us introduce an operator . For ,

| (2.16) |

where the dependence on is suppressed on both sides. The function in the following assumption is called a Lyapunov function. Its existence facilities proving certain exponential local martingale is in fact martingale, hence verifying optimality of the candidate strategies. This strategy has been applied to portfolio optimization problems for time separable utilities, cf. [18] and [37].

Assumption 2.10.

There exists such that

-

i)

, where is a sequence of open domains in satisfying , compact, and , for each ;

-

ii)

is bounded from above on .

The final assumption before the main results imposes an integrability assumption on the market price of risk . This ensures , hence the admissibility for the candidate optimal consumption stream .

Assumption 2.11.

There exists which satisfies and defines a local martingale measure for the discounted asset price via . Moreover

| (2.17) |

where is a Brownian motion and .

Remark 2.12.

Remark 2.13.

When and are bounded, Assumption 2.11 holds automatically and Assumption 2.10 is not needed, even for non-Markovian models. Indeed, Assumption 2.10 is used to prove the stochastic exponential in Lemma B.2 below is a martingale. When and are bounded, is bounded, hence is bounded as well. Therefore, (2.15) implies that is bounded, and is a BMO-martingale, cf. eg. [33, Lemma 3.1]. Then the stochastic exponential in Lemma B.2 can be proved as a martingale directly. However many models do not have bounded market value of risk. Therefore we retain Assumptions 2.10 and 2.11 in their general forms. These conditions impose some market conditions. In particular, for Markovian models, these conditions will be specified as explicit parameter restrictions in two examples in Section 3 below.

Now we are ready to state our first main result.

Theorem 2.14.

The second main result below focuses on the superdifferential of indirect utility. Let us first define the optimal value process

| (2.18) |

where is the optimal wealth process and comes from Proposition 2.9. Schroder and Skiadas [38] conjectured in Assumption C3 therein that the superdifferential is

| (2.19) |

The constant in (2.19) normalizes to be . Indeed, combining (2.1), (2.14) and (2.18), calculation shows that

| (2.20) | |||||

Therefore the previous identity implies that and is nonnegative.

In [38, Theorems 2 and 4], is confirmed to be the superdifferential when the market is complete with bounded market price of risk. This is proved using an integrability assumption in [38, Lemma 2], together with the property that is a supermartingale for arbitrary strategy and is a martingale for the optimal strategy. The integrability assumption in [38, Lemma 2] is satisfied in our case. Indeed, (2.20) shows that , which is bounded due to and is bounded from above. Now the following result confirms aforementioned property for in markets with unbounded market price of risk.

Lemma 2.15.

Finally our second main result below confirms that is in fact a martingale. This result has been proved for recursive utilities with Lipschitz continuous aggregator which is also jointly concave in all its variables, cf. [16, Theorems 4.2 and 4.3]. However, as we have seen before, none of these conditions are satisfied when .

Theorem 2.16.

In an equilibrium setting where the representative agent has an Epstein-Zin utility, given the consumption stream, equilibrium risk-free rate and risk premium can be read out from , providing a framework to study various asset pricing puzzles as discussed in introduction.

3. Examples

This section specifies general results in the previous section to two extensively studied models, where explicit parameter restrictions are presented so that all assumptions in the previous section are satisfied, hence statements of Theorems 2.14 and 2.16 hold. These parameter restrictions covers many empirically relevant specifications.

3.1. Stochastic volatility

The following model has a dimensional state variable, following a square-root process as suggested by Heston, which simultaneously affects the interest rate, the excess return of risky assets and their volatility. This model has been studied by [9] for recursive utilities with unit EIS, and [26], [31] for the time separable utilities. This model is specified as follows:

| (3.1) |

where , , with , , and . These parameters satisfy

Assumption 3.1.

, , and .

The previous assumption ensures that takes value in and is bounded from below, hence Assumption 2.6 is satisfied with . The following result provides parameter restrictions such that statements of Theorems 2.14 and 2.16 hold.

Proposition 3.2.

In item i), either the interest rate or the excess rate of return has a linear growth component of the state variable. In item ii), the inequality asks either , the mean-reverting speed of the state variable, is large, or the volatility is small, or is close to . In particular, when (i.e., constant interest rate) and , the condition in item ii) is satisfied when

| (3.2) |

This condition covers the empirically relevant specification in [32], where the parameter values are

| (3.3) |

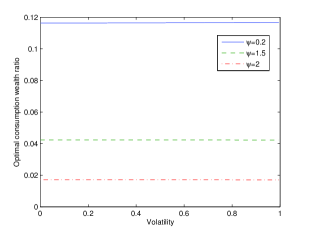

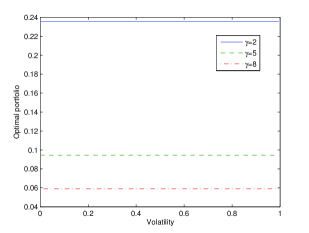

Figure 1 demonstrates the optimal consumption wealth ratio and optimal investment fraction with respect to volatility for different values of risk aversion and EIS. Meanwhile, our numeric results show that EIS has little impact on the optimal investment fraction, and different risk aversions hardly change the optimal consumption wealth ratio. Figure 2 compares the optimal consumption wealth ratio for (top panel) and (bottom panel). When , the finite horizon optimal consumption wealth ratio converges quickly to its infinite horizon stationary limit. For the parameter specification in (3.3), when the horizon is longer than years, the time- optimal consumption strategy is already close to its stationary limit. However, this convergence is much slower when , requiring at least years when the time discounting parameter . Moreover, in contrast to the case, the convergence speed is sensitive to when . In this case, the convergence is much slower for smaller value of . Intuitively, agent with small discounting parameter is more patient. But she still prefers early consumption when . Therefore these two competing forces delay the convergence. All comparative statistics is produced by solving the partial differential equation counterpart of (2.12) numerically using finite difference methods.

3.2. Linear diffusion

Both the interest rate and the excess return of risky assets in the following model are linear functions of a state variable, which follows a dimensional Ornstein-Uhlenbeck process. This model has been studied in [24] and [43] for the time separable utility setting, and in [7] for recursive utilities in a discrete time setting. The model dynamics is given by

| (3.4) |

where , , with , and . These coefficients satisfy

Assumption 3.3.

, either or .

This assumption implies that Assumption 2.6 is satisfied with . Under following parameter restrictions, statements of Theorems 2.14 and 2.16 hold.

Proposition 3.4.

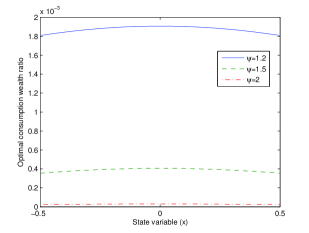

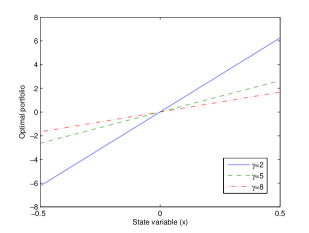

In the above item i), observe that is the drift of under . Therefore item i) assumes that either is mean-reverting under or the excess rate of return has a linear growth component of the state variable. Item ii) is interpreted similarly as Proposition 3.2 ii) . In particular, when , the inequality in item ii) is satisfied when

| (3.5) |

This condition already covers many empirically relevant specifications. For example, in [3] and [43], a single risky asset was considered and parameter values (in monthly units) are:

| (3.6) |

Figure 3 demonstrates the optimal consumption wealth ratio and optimal investment fraction with respect to the state variable .

Appendix A Proofs in Section 2.1

Let us first introduce several notation which will used throughout the appendices.

-

•

Let denote the space of all dimensional continuous adapted processes such that the norm .

-

•

Let be the subspace of such that the norm .

-

•

Denote by the set of all stopping time such that . The process is of class if the family is uniformly integrable.

-

•

Let denote the class of (multidimensional) predictable processes such that .

-

•

Denote by BMO the class of martingales such that .

Proof of Proposition 2.2.

The proof is split into several steps. First when the terminal condition is bounded, the solution is constructed by slightly modifying the proof of [34, Theorem 2.2]. For general terminal conditions, the solution is obtained by the localization technique in [6]. Finally, uniqueness is proved and (2.2) is verified. For simplicity of notation, we denote throughout this proof.

Step 1: Bounded terminal condition. When for some constant , consider the following truncated BSDE:

| (A.1) |

where . Note that is Lipschitz, in particular, it is differentiable at due to . Therefore (A.1) admits a unique solution . The first component of such solution is also nonnegative. Indeed, consider (A.1) with zero as the terminal condition. Such BSDE admits a unique solution in . Since , it follows from the comparison theorem for BSDEs with Lipschitz generators that . On the other hand, since , is decreasing in , the comparison theorem then implies that is decreasing. Hence is well defined and nonnegative.

To take the limit of , let us derive the following uniform estimate. Applying Itô’s formula to yields

where the first inequality follows from and . The previous estimate yields

| (A.2) |

Therefore there exists such that converges to weakly. Note that , , and

where the third inequality holds due to the first estimate in (A.2). The dominated convergence theorem then implies that

Now we prove the convergence of in . Applying Itô’s formula to yields

| (A.3) |

where the first inequality holds due to the fact that is decreasing and the second inequality follows from the first estimate in (A.2). Since , the dominated convergence theorem implies the right hand side of (A.3) converges to zero as . Combining the previous convergence with the weak convergence of , we obtain

The Burkholder-Davis-Gundy inequality then implies

where stands for the convergence in probability. Passing to a subsequence, we obtain almost sure convergence. Therefore, sending in (A.1), we obtain that solves (2.4) and is nonnegative. Moreover, since

after taking limits on and supremum over , we obtain

Therefore converges to uniformly in , implying that is a continuous process.

Step 2: General terminal condition. When is not bounded, set and consider

Results from the previous step imply that this BSDE admits a solution with . Moreover, since , for all and . This a priori bound allows us to construct a solution to (2.4) via the localization technique in [6]. We outline the construction below.

Consider for each . Then satisfies the following BSDE

Since , we have

Then implies . On the other hand, since and satisfies the monotonicity condition, then the comparison result (cf. [34, Theorem 2.4]) implies . Utilizing the same argument as in Step 1, we obtain and such that in , and solves the BSDE

| (A.4) |

where . Following from the definition of , and . Therefore we define

This construction implies . Indeed, on , and for any . Therefore on when . This implies , since . Now sending on both sides of (A.4), we confirm that solves (2.4). By this construction, is continuous and satisfies for , hence is of class . The same argument as in [6, Page 612] shows .

Step 3: Remaining statements. For future reference, we prove a comparison result for (2.4). Let (resp. ) be a super-solution (resp. sub-solution) to (2.4), i.e.,

with , meanwhile and are determined by Doob-Meyer decomposition and martingale representation. Assuming that both and are of class , then . Moreover, if , then for any .

To prove this comparison result, define

Since is decreasing, we have . It then follows that is a local supermartingale, hence a supermartingale, since the exponential factor is bounded and both and are of class . Therefore, implies . Moreover when , we obtain the strict comparison for any . The uniqueness follows from the comparison result directly. Since , then . Therefore follows from the strict comparison.

Finally, we verify that satisfies (2.2). To this end, since solves (2.4), satisfies (2.3), implying that is a local martingale. Taking a localizing sequence for , we obtain

Sending on both sides, note that and , therefore the integrand on the left side is negative and the integrand on the right side is positive. The monotone convergence theorem and the class property of then yield

| (A.5) |

Since , where the second inequality holds since and , the third inequality follows from and . Subtracting on both sides of (A.5), we confirm (2.2). ∎

The concavity of is proved in the following. This proof utilizes simultaneously the joint concavity of the generator for (2.5) and the class property of the solution to (2.4).

Proof of Proposition 2.4.

Denote the generator of (2.5) as . For and , denote , for and , respectively. It follows from (2.5) that

where, due to the concavity of ,

and . Set

Itô’s formula yields

where . On the other hand, . Therefore is a super-solution to (2.4). On the other hand, is of class . Indeed, since ,

| (A.6) |

where (resp. ) is the first component of the solution to (2.4) with (resp. ). Therefore, is of class , because both and are. Now consider as the first component of solution of (2.4) where is replaced by . It then follows from (A.6) and the comparison result in Step 3 of the previous proof that

Dividing the previous inequality by on both sides, we confirm . ∎

Appendix B Proofs in Section 2.2

Even though the generator in (2.12) has an exponential term in , the parameter specification and allow us to derive a priori bounds for . Then a solution to (2.12) is constructed via the localization technique in [6].

Proof of Proposition 2.9.

Due to Assumption 2.7 i), is a Brownian motion. Therefore, (2.12) can be rewritten under , and all expectations are taken with respect to throughout this proof. On the other hand, recall that and is bounded from below. Therefore there exists a constant such that . However, , in many widely used models, is an unbounded function of the state variable, hence and are not bounded from below. Therefore we introduce

| (B.1) |

where , , and

Consider a truncated version of (B.1):

| (B.2) |

where is bounded and

This truncated generator is Lipschitz in and quadratic in . Indeed, since eigenvalues of is either or , . Then and the definition of after (2.13) implies

| (B.3) |

Therefore it follows from [25, Theorem 2.3] that (B.2) admits a solution . Moreover, due to , is decreasing in . The construction of in [25, Theorem 2.3] yields . In what follows, we derive a priori bounds on uniformly in . This uniform estimate facilitates the construction of a solution to (B.1).

On the one hand, and the third inequality in (B.3) yield . Consider

which has an explicit solution . Then

| (B.4) |

On the other hand, when , the first inequality in (B.3) and imply . Therefore consider the BSDE

whose solution admits a representation .

Now since is sandwiched between two generators with simpler forms, comparison result yields

| (B.5) |

for any . These uniform bounds on allow us to construct a solution to (B.1) using the localization technique in [6, Theorem 2]; see also Step 2 in the proof of Proposition 2.2. The resulting satisfies

| (B.6) |

The previous inequalities imply that . Hence satisfies the terminal condition of (B.1). The desired estimates on follows after subtracting on both sides of the previous inequalities, in particular,

| (B.7) |

For the statement on , take a localization sequence for , (B.1) yields

Sending on both sides, applying the second inequality in (B.3) to the left-hand side, the first inequality in (B.6) to the second term on the right-hand side, and (B.7) to the third term, we confirm . ∎

The following several results prepare the proofs of Theorems 2.14 and 2.16. First we show is an upper bound for the optimal value among permissible strategies.

Lemma B.1.

Proof.

This proof extends the technique in [20] to recursive utilities. For a permissible , define

where . Then (2.11) and (2.13) imply that is a local supermartingale. Due to Doob-Meyer decomposition and martingale representation, there exist an increasing process and such that . Therefore, is a supersolution to (2.3), whose terminal condition is . Indeed, since is of class by permissibility and , we have . On the other hand, consider the utility associated to the consumption stream and the terminal lump sum . The comparison result in the proof of Proposition 2.2 confirms (B.8). ∎

In what follows we will show that is a permissible strategy and it attains the upper bound . First, we establish an important result that certain exponential local martingale associated to is a martingale.

Proof.

It follows from (2.14), the definition of and that

Here we suppress time subscripts to simplify notation. First we claim that if is a martingale, so is . Indeed, for any ,

| (B.9) |

Here , the third identity follows from [21, Lemma 4.8] since and are independent, and the fourth identity is due to the martingale assumption on . In the remaining of the proof, we will prove the martingale property of .

For the sequence of subdomains in Assumption 2.10 i), define . we first prove that is bounded. Since we have seen in Proposition 2.9 that is bounded from above, it suffices to show is bounded from below. Then (2.15) implies that is bounded as well. Due to the Markovian structure, define

The Feynman-Kac formula (see [19] when the equation is not uniformly parabolic) implies that, under Assumption 2.6, and it is the unique solution to

where is the infinitesimal generator of under . Now since is compact, the continuity of implies that is bounded.

As a solution to (2.12), satisfies

Since both and are bounded, it follows from the BMO-estimate for quadratic BSDEs (cf. eg. [33, Lemma 3.1]) that is a BMO-martingale. Note that both and are bounded. Therefore is a BMO-martingale as well. Then [23, Theorem 2.3] implies that is a martingale. Therefore defines on which is equivalent to .

Assuming that , by the monotone convergence theorem,

proving the martingale property of on .

It remains to prove . To this end, (2.12) yields

On the other hand, recall from (2.16), we have from Itô’s formula,

Taking difference of the previous two identities,

where is a Brownian motion on . On the right hand side, the quadratic term is nonnegative, is nonnegative since , and is also bounded from below due to Assumption 2.10 ii). Therefore, there exists some negative constant such that

| (B.10) |

The stochastic integral on the right hand side has zero expectation under . Indeed, since is a martingale and is bounded, hence is a martingale as well. Now since is a martingale, [23, Theorem 3.6] implies that is a martingale. Therefore its expectation under is zero. It then follows from (B.10) that

| (B.11) |

Now since is bounded from above and is bounded from below due to Assumption 2.10 i), there exists a constant , such that

Now sending in (B.11), Assumption 2.10 i) and the previous inequality confirm that . ∎

The martingale property in the previous result helps to verify the permissibility of .

Corollary B.3.

Proof.

The calculation leading to (2.13) yields

where the second identity follows from the form of in (2.14). Therefore,

Since and is bounded from above, the second exponential term on the right is bounded, uniformly in . Meanwhile, due to Lemma B.2, the stochastic exponential on the right is of class on . The statement is then confirmed. ∎

Proof.

Since , the class property of in Corollary B.3 yields . On the other hand, the expression of in (2.14) implies

Since , , and is bounded from above, the first three terms on the right hand side are bounded. Therefore it suffices to prove

| (B.12) |

To this end, it follows from Assumption 2.11 that

Here the first inequality follows from ; the second inequality holds due to Hölder’s inequality; the third inequality is obtained using the fact that is a nonnegative local martingale, hence a supermrtingale; and the fourth inequality holds thanks to (2.17). ∎

Now we are ready to prove the first main result.

Proof of Theorem 2.14.

Proof of Lemma 2.15.

Calculation using (2.8) and (2.21) shows that is a local martingale. It then remains to prove (2.21). To ease notation, suppress all time subscripts. Using (2.12) and (2.14), calculation shows

Combining the previous two identities, (2.20), and the expression for in (2.14), we confirm

where the third identity follows from . ∎

Proof of Theorem 2.16.

It follows from (2.14) and (2.20) that

| (B.14) |

Here , . Since , is bounded from above by a constant. We have already seen in Lemma 2.15 that is a nonnegative local martingale. It suffices to prove that it is of class . To this end, it follows from (B.13) that

Here since is of class , is bounded uniformly in . Therefore the previous inequality holds. On the other hand, using the expression of in (2.14),

Then and the previous two equations combined yield that the second term on the right hand side of (B.14) is bounded from above by an integrable random variable, hence is of class . Meanwhile, using the class property of again, the first term on the right of (B.14) is also of class . This confirms the class property of . ∎

Appendix C Proofs in Section 3

To prove Proposition 3.2, let us recall the following result on the Laplace transform of integrated square root process; cf. [36, Equation (2.k)] or [8, Equation (3.2)].

Lemma C.1.

Consider with dynamics

where is a dimensional Brownian motion. When

the Laplace transform

is well-defined for any .

Proof of Proposition 3.2.

Assumption 2.7: Note . Consider the martingale problem associated to on . Since , Feller’s test of explosion implies that the previous martingale problem is well-posed. Then [10, Remark 2.6] implies that the stochastic exponential in Assumption 2.7 i) is a martingale, hence is well defined. For Assumption 2.7 ii), . Since has the following dynamics under :

where is a Brownian motion. Then follows from the fact that is bounded uniformly for .

Assumption 2.10: The operator in (2.16) reads

where . Consider , for two positive constants and determined later. It is clear that when or . On the other hand, calculation shows

where is a constant. Since , the coefficient of is negative for sufficiently small . When or , since , the coefficient of is negative for sufficiently small . Therefore, these choices of and imply that when or , hence is bounded from above on , verifying Assumption 2.10.

Assumption 2.11: Consider the martingale problem associated to on . Since , Feller’s test of explosion implies that this martingale problem is well-posed and its solution, denoted by , satisfies . Define via

Here, due to the independence between and , proof similar to (B.9) implies that both stochastic exponentials on the right are martingales; hence is well defined, and in Assumption 2.11 can be chosen as .

To verify (2.17), note

| (C.1) |

where is a Brownian motion. Following the construction of , one can similarly show is a martingale. Hence can be defined via

Combining the previous two change of measures, the dynamics of can be rewritten as

where is a dimensional Brownian motion. On the other hand, calculation using (C.1) shows

Then Lemma C.1 implies that the expectation on the right hand side is finite when

This is exactly the assumption in Proposition 3.2 ii). ∎

Proof of Proposition 3.4.

Assumptions 2.7, 2.10, and 2.11 are verified. Then statements of Theorems 2.14 and 2.16 follow. We denote throughout the proof to simplify notation.

Assumption 2.7: Note . Consider the martingale problem associated to on . This martingale problem is well-posed since all coefficients of have at most linear growth. Then [10, Remark 2.6] implies that the stochastic exponential in Assumption 2.7 is a martingale, hence is well defined. For Assumption 2.7 ii), is bounded from below when either or . Since is another Ornstein-Uhlenbeck process, with modified linear drift, under , then has all finite moments, cf. [22, Chapter 5, Equation (3.17)], then Assumption 2.7 ii) is satisfied.

Assumption 2.10: The operator in (2.16) reads

where . Consider , for a positive constant determined later. It is clear that as . On the other hand, calculation shows

When , since , , we can choose sufficiently small such that as . When , then , we can also choose sufficiently small such that has the same asymptotic behavior. In both cases, is bounded from above on , hence Assumption 2.10 is verified.

Assumption 2.11: Consider the martingale problem associated to on . Since all coefficients have at most linear growth, this martingale problem is well-posed and its solution, denoted by , satisfies . Define via

Argument similar to (B.9) implies that is well defined. Therefore in Assumption 2.11 can be chosen as .

To verify (2.17), note

| (C.2) |

where is a Brownian motion. Following the construction of , similar argument shows that is a martingale. Hence can be defined via

Combining the previous two change of measures, the dynamics of can be rewritten as

where is a dimensional Brownian motion. On the other hand, calculation shows, for any ,

| (C.3) |

where is a constant and is a constant depending on .

In order to appeal Lemma C.1 to calculate the expectation on the right hand side of (C.3), let us introduce another measure via . Under this measure, has dynamics

where is a Brownian motion. Let . It then has dynamics

which is of the same type of in Lemma C.1.

Come back to (C.3), Hölder’s inequality implies, for any ,

Observe that the first expectation on the right hand side is finite, since has all finite moments. For the second expectation, we can choose sufficiently small and such that, according to Lemma C.1, when

| (C.4) |

the second expectation is finite. Now combining the previous estimates and (C.3), we confirm (2.17). Finally, note that (C.4) is exactly the assumption in Proposition 3.4 ii). ∎

References

- [1] R. Bansal, Long-run risks and financial markets, Fed. Reserve Bank St. Louis Rev., 89 (2007), pp. 1–17.

- [2] R. Bansal and A. Yaron, Risks for the long run: a potential resolution of asset pricing puzzles, J. Finance, 59 (2004), pp. 1481–1509.

- [3] N. Barberis, Investing for the long run when returns are predictable, J. Finance, 55 (2000), pp. 225–264.

- [4] L. Benzoni, P. Collin-Dufresne, and R. Goldstein, Explaining asset pricing puzzles associated with the 1987 market crash, J. Financ. Econ., 101 (2011), pp. 552–573.

- [5] H. Bhamra, L. Kuehn, and I. Strebulaev, The levered equity risk premium and credit spreads: A unified framework, Rev. Financ. Stud., 23 (2010), pp. 645–703.

- [6] P. Briand and Y. Hu, BSDE with quadratic growth and unbounded terminal value, Probab. Theory and Relat. Fields, 136 (2006), pp. 604–618.

- [7] J. Campbell and L. Viceira, Consumption and portfolio decisions when expected returns are time varying, Q. J. Econ., 114 (1999), pp. 433–495.

- [8] P. Carr, H. Geman, D. Madan, and M. Yor, Stochastic volatility for Lévy processes, Math. Finance, 13 (2003), pp. 345–382.

- [9] G. Chacko and L. Viceira, Dynamic consumption and portfolio choice with stochastic volatility in incomplete markets, Rev. Financ. Stud., 18 (2005), pp. 1369–1402.

- [10] P. Cheridito, D. Filipović, and M. Yor, Equivalent and absolutely continuous measure changes for jump-diffusion processes, Ann. Appl. Probab., 15 (2005), pp. 1713–1732.

- [11] P. Cheridito and Y. Hu, Optimal consumption and investment in incomplete markets with general constraints, Stoch. Dyn., 11 (2011), pp. 283–299.

- [12] D. Duffie and L. Epstein, Asset pricing with stochastic differential utility, Rev. Financ. Stud., 5 (1992), pp. 411–436.

- [13] , Stochastic differential utility, Econometrica, 60 (1992), pp. 353–394.

- [14] D. Duffie and P.-L. Lions, PDE solutions of stochastic differential utility, J. Math. Econ., 21 (1992), pp. 577–606.

- [15] D. Duffie and C. Skiadas, Continuous-time security pricing: A utility gradient approach, J. Math. Econ., 23 (1994), pp. 107–131.

- [16] N. El Karoui, S. Peng, and M. C. Quenez, A dynamic maximum principle for the optimization of recursive utilities under constraints, Ann. Appl. Probab., 11 (2001), pp. 664–693.

- [17] H. Föllmer and M. Schweizer, Hedging of contingent claims under incomplete information, in Applied Stochastic Analysis, M. Davis and R. Elliott, eds., vol. 5 of Stochastics Monographs, Gordon and Breach, London, 1991, pp. 389–414.

- [18] P. Guasoni and S. Robertson, Portfolios and risk premia for the long run, Ann. Appl. Probab., 22 (2012), pp. 239–284.

- [19] D. Heath and M. Schweizer, Martingales versus PDEs in finance: an equivalence result with examples, J. Appl. Probab., 37 (2000), pp. 947–957.

- [20] Y. Hu, P. Imkeller, and M. Müller, Utility maximization in incomplete markets, Ann. Appl. Probab., 15 (2005), pp. 1691–1712.

- [21] I. Karatzas and C. Kardaras, The numéaire portfolio in semimartingale financial models, Finance Stoch., 11 (2007), pp. 447–493.

- [22] I. Karatzas and S. Shreve, Brownian Motion and Stochastic Calculus, Springer, New York, 1988.

- [23] N. Kazamaki, Continuous exponential martingales and BMO, vol. 1579 of Lecture Notes in Mathematics, Springer-Verlag, Berlin, 1994.

- [24] T. Kim and E. Omberg, Dynamic nonmyopic portfolio behavior, Rev. Financ. Stud., 9 (1996), pp. 141–161.

- [25] M. Kobylanski, Backward stochastic differential equations and partial differential equations with quadratic growth, Ann. Probab., 28 (2000), pp. 558–602.

- [26] H. Kraft, Optimal portfolios and Heston’s stochastic volatility model: an explicit solution for power utility, Quant. Financ., 5 (2005), pp. 303–313.

- [27] H. Kraft, T. Seiferling, and F.-T. Seifried, Asset pricing and consumption-portfolio choice with recursive utility and unspanned risk. Working paper, March 2014.

- [28] H. Kraft and F.-T. Seifried, Stochastic differential utility as the continuous-time limit of recursive utility, J. Econ. Theory, 151 (2014), pp. 528–550.

- [29] H. Kraft, F.-T. Seifried, and M. Steffensen, Consumption-portfolio optimization with recursive utility in incomplete markets, Finance Stoch., 17 (2013), pp. 161–196.

- [30] D. Kreps and E. Porteus, Temporal resolution of uncertainty and dynamic choice theory, Econometrica, 46 (1978), pp. 185–200.

- [31] J. Liu, Portfolio selection in stochastic environments, Rev. Financ. Stud., 20 (2007), pp. 1–39.

- [32] J. Liu and J. Pan, Dynamic derivative strategies, J. Financ. Econ., 69 (2003), pp. 401–430.

- [33] M.-A. Morlais, Quadratic BSDEs driven by a continuous martingale and applications to the utility maximization problem, Finance Stoch., 13 (2009), pp. 121–150.

- [34] É. Pardoux, BSDEs, weak convergence and homogenization of semilinear PDEs, in Nonlinear analysis, differential equations and control (Montreal, QC, 1998), vol. 528 of NATO Sci. Ser. C Math. Phys. Sci., Kluwer Acad. Publ., Dordrecht, 1999, pp. 503–549.

- [35] H. Pham, Smooth solutions to optimal investment models with stochastic volatilities and portfolio constraints, Appl. Math. Optim., 46 (2002), pp. 55–78.

- [36] J. Pitman and M. Yor, A decomposition of bessel bridges, Probab. Theory Relat. Fields, 59 (1982), pp. 425–457.

- [37] S. Robertson and H. Xing, Long term optimal investment in matrix valued factor models. Working paper, 2014.

- [38] M. Schroder and C. Skiadas, Optimal consumption and portfolio selection with stochastic differential utility, J. Econ. Theory, 89 (1999), pp. 68–126.

- [39] M. Schroder and C. Skiadas, Optimal lifetime consumption-portfolio strategies under trading constraints and generalized recursive preferences, Stoch. Process. Appl., 108 (2003), pp. 155–202.

- [40] T. Seiferling and F.-T. Seifried, Stochastic differential utility with preference for information: existence, uniqueness, concavity, and utility gradients. Working paper, July 2015.

- [41] C. Skiadas, Recursive utility and preferences for information, Econ. Theory, 12 (1998), pp. 293–312.

- [42] D. W. Stroock and S. R. S. Varadhan, Multidimensional diffusion processes, Classics in Mathematics, Springer-Verlag, Berlin, 2006. Reprint of the 1997 edition.

- [43] J. Wachter, Portfolio and consumption decisions under mean-reverting returns: An exact solution for complete markets, J. Financial Quant. Anal., 37 (2002), pp. 63–91.