A bivariate risk model with mutual deficit coverage

Abstract

We consider a bivariate Cramér-Lundberg-type risk reserve process with the special feature that each insurance company agrees to cover the deficit of the other. It is assumed that the capital transfers between the companies are instantaneous and incur a certain proportional cost, and that ruin occurs when neither company can cover the deficit of the other. We study the survival probability as a function of initial capitals and express its bivariate transform through two univariate boundary transforms, where one of the initial capitals is fixed at 0. We identify these boundary transforms in the case when claims arriving at each company form two independent processes. The expressions are in terms of Wiener-Hopf factors associated to two auxiliary compound Poisson processes. The case of non-mutual agreement is also considered. The proposed model shares some features of a contingent surplus note instrument and may be of interest in the context of crisis management.

keywords:

Two-dimensional risk model, survival probability, coupled processor model, Wiener-Hopf factorization, surplus note , mutual insurance1 Introduction

Insurance companies cannot operate in isolation from financial markets or from other insurance and reinsurance companies. Hence it is important to understand the effect of interaction on the main characteristics of an insurance company. Multivariate risk models, however, present a serious mathematical challenge with few explicit results up to date, see [1, Ch. XIII.9]. This paper focuses on a nonstandard, but rather general bivariate risk model and provides an exact analytic study of the corresponding survival probability, borrowing some ideas from the analysis of a somewhat related queueing problem in [7]. The proposed model may be of interest in the context of crisis management due to its relation to contingent surplus notes and mutual insurance. Moreover, it allows for an explicit structural result without imposing overly strict assumptions such as proportional or dominating claims, see Section 1.1.

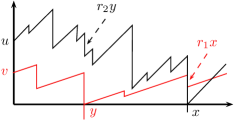

We consider a bivariate Cramér-Lundberg risk process as a model of surplus of two insurance companies (or two lines of one insurance business). The special feature of our model is that the companies have a mutual agreement to cover the deficit of each other. More precisely, if company gets ruined, with its capital decreasing to a value , then company compensates this deficit, bringing the capital of company back to . However, this comes at a price; a unit of capital received by company requires from company (cf. Figure 1). If this would cause the capital of company to go below , then both companies are said to be ruined. Similarly, if company gets a deficit , company compensates this deficit, but its capital reduces by ; and if this would cause the capital of company to go below , then again both companies are said to be ruined. Finally, ruin may also be caused by a single event bringing the surplus processes of both companies below 0. It may be more realistic to assume that if one company can not save the other from ruin then it does not transfer any capital at that instant and continues to operate. Note, however, that survival of both companies in this set-up corresponds to our previous notion of survival.

Our main goal in this study is to provide an exact analysis of the (Laplace transform of the) probability of survival (i.e., ruin never occurs) , as a function of the vector of initial capitals. We do this by (i) expressing the two-dimensional Laplace transform of in terms of the transforms of and , and (ii) determining the latter two transforms by solving a Wiener-Hopf boundary value problem in the case of independent claim streams. In the latter step, a key role is played by the Wiener-Hopf factorization of two auxiliary compound Poisson processes.

In our terminology, if one company cannot save the other then both are declared ruined, whereas in practice it is more likely that the company with a positive capital pays out all it has, but then continues its operation. Hence it may be more appropriate to call the probability of survival of both companies, or the probability that external help is never needed, see Remark 3. One may also notice that it is clearly better (with respect to survival) to merge the two lines eliminating transaction costs. There may be cases, however, where a merger is not possible due to legal, regulatory or other issues. Outside of an insurance context, the two lines may be two separate physical entities such as water reservoirs or energy sources. Furthermore, one may consider the case where for at least one company, see Remark 2, so that merging may not be optimal. This may correspond to the case where part of the deficit is written off or is covered by some other fund.

Our model resembles two insurance companies with a mutual insurance fund, which is used to cover the deficit of each of them. In our case, however, there is no separate fund - it is the other company which provides the capital to cover the deficit. Another related notion is that of a contingent surplus note which is a form of a CoCo bond issued by an insurance company. This bond pays a higher coupon, because of the risk that it is converted into surplus if a trigger event (e.g. deficit) occurs. Finally, we may consider an insurance company and a governmental fund which is used to save companies from default. In this case capital transfers are only possible from the fund to the company; this particular scenario is discussed in Section 7.

The above-sketched risk model bears some resemblance to a two-dimensional queueing model of two coupled processors. This model features two queues, each of which, in isolation, is known to be the dual of a Cramér-Lundberg insurance risk model, cf. [1, Ch. I.4a]. Just like in our risk model, the two processors are coupled by the agreement to help each other. When one of the two queues becomes empty, the service speed of the other server – say, server – increases from to , i.e. server is being helped by the idle server. It should be stressed that this similarity is rather loose and that there is no clear duality relation between these bivariate risk and queueing models. Strikingly, the crucial ideas of the analysis of the coupled processor model in [7] apply to our present setup as well. Moreover, solutions to both problems are based on the same Wiener-Hopf factors, which hints that there might be a certain duality relation between the two.

1.1 Related literature

Despite their obvious relevance, exact analytic studies of multidimensional risk reserve processes are scarce in the insurance literature. A special, important case is the setting of proportional reinsurance, which was studied in Avram et al. [3]. There it is assumed that there is a single arrival process, and the claims are proportionally split among two reserves. In this case, the two-dimensional exit (ruin) problem becomes a one-dimensional first-passage problem above a piece-wise linear barrier. Badescu et al. [4] have extended this model by allowing a dedicated arrival stream of claims into only one of the insurance lines. They show that the transform of the time to ruin of at least one of the reserve processes can be derived using similar ideas as in [3].

An early attempt to assess multivariate risk measures can be found in Sundt [22], where multivariate Panjer recursions are developed which are then used to compute the distribution of the aggregate claim process, assuming simultaneous claim events and discrete claim sizes. Other approaches are deriving integro-differential equations for the various measures of risk and then iterating these equations to find numerical approximations [10, 16], or computing bounds for the different types of ruin probabilities that can occur in a setting where more than one insurance line is considered, see [8, 9]. In an attempt to solve the integro-differential equations that arise from such models, Chan et al. [10] derive a Riemann-Hilbert boundary value problem for the bivariate Laplace transform of the joint survival function (see [5] for details about such problems arising in the context of risk and queueing theory and the book [11] for an extended analysis of similar models in queueing). However, this functional equation for the Laplace transform is not solved in [10]. In [5] a similar functional equation is taken as a departure point, and it is explained how one can find transforms of ruin related performance measures via solutions of the above mentioned boundary value problems. It is also shown that the boundary value problem has an explicit solution in terms of transforms, if the claim sizes are ordered. In [6] this is generalized to the case in which the claim amounts are also correlated with the time elapsed since the previous claim arrival.

Bivariate models where one company can transfer its capital to the other have already been considered in the literature. Recently, Avram and Pistorius [2] proposed a model of an insurance company which splits its premiums between a reinsurance/investement fund and a reserves fund necessary for paying claims. In their setting only the second fund receives claims, and hence all capital transfers are one way: from the first fund to the second. Another example is a capital-exchange agreement from [20, Ch. 4], where two insurers pay dividends according to a barrier strategy and the dividends of one insurer are transferred to the other unless the other is also fully capitalized. This work resulted in systems of integro-differential equations for the expected time of ruin and expected discounted dividends, which are hard to solve even in the case of exponential claims.

Finally, we briefly list related contributions in the queueing context. The joint queue length distribution of the coupled processor model has been derived by Fayolle and Iasnogorodski [15], in the case that the service time distributions at both queues are exponential. In their pioneering paper, they showed how the generating function of the joint steady-state queue length distribution can be obtained by solving a Riemann-Hilbert boundary value problem. Cohen and Boxma [11] generalized this queueing model by allowing general service time distributions. They obtained the Laplace-Stieltjes transform of the joint steady-state workload distribution by solving a Wiener-Hopf boundary value problem. In [7] the model of [11] was extended by considering a pair of coupled queues driven by independent spectrally positive Lévy processes and a compact solution was obtained. There the model was also linked to a two-server fluid network.

1.2 Organization of the paper

In Section 2 we describe the model in detail. In Section 3 we derive an integral equation for the survival probability , as a function of the vector of initial amounts of capital. Section 4 is devoted to the derivation of a so-called kernel equation for the two-dimensional Laplace transform of , see Proposition 1. After a brief discussion of the net profit condition, in Section 5, we solve the kernel equation in the case of independent claim streams in Section 6. The main result is given in Theorem 1, which is then illustrated by two simple examples. In Section 7 we specialize to a model of non-mutual insurance, where help is provided by only one company (or government). Some open problems are discussed in Section 8.

2 The model

Consider a bivariate Cramér-Lundberg risk process with initial capitals , premium rates , claim arrival rate and a joint claim size distribution . In other words,

where are iid distributed according to , and is an independent Poisson process of rate . Without loss of generality we can assume that does not have mass at . Next, we define the corresponding bivariate Laplace exponent by

| (1) | ||||

Remark 1.

Note that this model incorporates the case of two independent risk processes with claim arrival rates and claim size distributions with the relation

where denotes the Dirac point mass at 0. This yields with

Throughout this work we assume that the companies have a mutual agreement of deficit coverage: when a claim brings the surplus of a company below 0 then the other company transfers just enough capital to bring it to 0 so that company can continue its operation. If company has not enough capital then ruin occurs. We also assume that a capital transfer incurs some proportional cost: a unit of capital received by requires capital from . It is noted that in the case of no transaction costs our risk problem reduces to a classical one-dimensional problem obtained by considering the total surplus, see Section 6.2.

Remark 2.

All of the results below hold for any such that . Even the latter condition can be removed, except that then the second statement in Proposition 2 may no longer be true.

It is convenient to consider a more general model defined for all times , where ruin is avoided using capital from external sources. More precisely, if company has insufficient funds to save then it transfers to all its capital and the rest of the required capital is taken from the shareholders of company (or some other external source). Mathematically, we can describe the bivariate surplus process in the following way:

| (2) |

where and are the cumulative amounts of capital received by the -th company from the other company and from an external source respectively; . Note that the time of ruin in the original model is given by

| (3) |

In this work we only address the probability of survival . Note that in our setup the concepts of ruin and survival have unambiguous meaning, which should be compared to various possible ruin concepts in standard bivariate risk models, see [10]. In the following we provide two mathematical definitions of the processes involved in (2): A recursive definition and a definition as a modified Skorokhod problem.

Remark 3.

We note that the external sources are introduced only for modeling convenience. Throughout this work survival means survival in the original model which corresponds to never using external capital in the extended model. Hence never appear in the following apart from the discussion of the net profit condition in Section 5 and direct calculations in Section 6.2. Nevertheless, we believe that it is important to have an explicit model definition as given by (2) and (3), see also Section 8.

2.1 Recursive definition

Let us remark that the processes are piece-wise constant and non-decreasing, and can have jumps at claim arrival times only. One may define these processes recursively by considering their jumps at time for More precisely, with we have the following cases:

-

1.

: have no jumps (at ),

-

2.

: has a jump (and no other jumps at ),

-

3.

: has a jump ,

-

4.

: has a jump and has a jump ,

-

5.

: has a jump and has a jump ,

-

6.

: has a jump for .

2.2 Modified Skorokhod problem definition

The following equivalent specification of our model closely resembles a multidimensional Skorokhod problem, see [17, 18] building upon Skorokhod’s one dimensional construction [21]. It is noted that for the classical bivariate Skorokhod problem one must assume that which is clearly violated in our setup.

We consider the equations in (2) with the following additional requirements:

-

1.

and are piece-wise constant and non-decreasing,

-

2.

the jump times of are contained in ,

-

3.

the jump times of are contained in ,

-

4.

out of the only pairs which can jump simultaneously are and .

It is easy to check that these requirements are satisfied by the recursive construction from Section 2.1, and that no other choices of and thus satisfy these conditions.

A few words about the above requirements. The second states that a company receives capital when in need, and the third states that external capital can be used only when both companies are in need (or one is at 0 after trying to save the other). The final condition is necessary to prevent redundant capital transfers.

3 The survival probability

As stated in Remark 3, we now ignore the possibility of funding by external sources. Consider , the probability of survival for the initial capitals , and put for convenience if or . It is immediate from sample path comparison that is non-decreasing in both . Furthermore, is a (Lipschitz) continuous function on , which follows from as implying

| (4) |

where does not depend on . Moreover, our model definition implies the following equation

| (5) | ||||

In fact, this equation requires some careful considerations, and so its proof is given in the Appendix.

Remark 4.

If the partial derivatives and exist and are continuous at then . This can not hold in general when has an atom at , as can be seen from (5).

4 The kernel equation

Equation (5) can be equivalently formulated in terms of Laplace transforms. This results in a very simple identity given by the following Proposition.

Proposition 1.

Let and

Then for all it holds that

| (6) |

This result identifies the transform of up to the unknown functions . Equation (6) resembles the so-called basic adjoint relation in the semimartingale reflected Brownian motion (SRBM) literature, see e.g. [23, Eq. (3.2)], with the class of functions . In the queueing literature this type of functional equation is sometimes called ‘kernel equation’, see e.g. [11, Ch. III.3] and [7, Prop. 1].

Proof of Proposition 1.

We simply take the transform of (5) and let . Let us first consider the transform of :

By dominated convergence and continuity of we have

Similarly, we have

and . Combining these we obtain

| (7) |

It is left to consider the transforms of the integrals in (5). Using Fubini’s theorem we get

where .

The following Corollary for two independent driving processes is immediate.

Corollary 1.

5 The net profit condition

Let be the average drift of the driving process . In the following we assume that the net profit condition holds

| (9) |

The importance of this condition is explained by the following result.

Proposition 2.

The following dichotomy is true for with :

-

1.

if (9) holds then ,

-

2.

otherwise for all .

Proof.

Equation (2) implies that

Thus if then necessarily implying that . Note that if (9) does not hold then at least one of the Cramér-Lundberg processes and is certain to get ruined, which shows that .

In the following assume that (9) holds, which guarantees that at least one of is positive. Without loss of generality we assume that . By considering the case that the first company does not need any help we arrive at the bound

Here is the running infimum of the process . It is well known in the queueing literature that a.s. and as . Now we see from that a.s. and hence the infimum of this process is finite. This yields .

For any choose so large that , and consider the first passage time of the reflected process above level . In order to guarantee that we need to choose so large that , i.e. the second company has enough capital for the first to reach high capital. This is clearly possible, because a.s. ∎

5.1 From survival function to measure

Since is continuous and non-decreasing in both it defines a finite (probability) measure on , where . By Fubini we have for the following relation

Similarly,

for . We will refer to and as boundary measures. Note that one can easily rewrite the results of Proposition 1 and Corollary 1 in terms of measure transforms . Finally, observe that

and hence given we can easily find and .

6 Independent driving processes

Throughout this section we assume that the claim streams are independent, and thus we can focus on the kernel equation in Corollary 1. For this case we provide an explicit solution for the bivariate Laplace transform of the survival probability .

Even though the kernel equation is quite different from the kernel equation of a coupled processor model, the method of analysis from [7], building upon [11], can still be used. In the following we present a self-contained (apart from a few technical properties which can be found in [7]) application of this method to our risk problem.

We assume that and are two independent Cramér-Lundberg processes with exponents and , and so , see Remark 1. It is well known that for has a unique positive solution, call it . Moreover, is a solution of , which is positive when and when .

It turns out that there exists a unique non-decreasing Lévy process (descending ladder time process [19, p. 170] corresponding to ) such that

| (10) |

(here and in the sequel, the positive and negative parts of some entity are denoted by and ). In our case is a compound Poisson process (CPP) with no deterministic drift and jumps distributed as , see also [7]. Define two two-sided CPP processes and and two constants and as follows:

where we assume that and are independent. Note that according to the net profit condition (9). Observe that the corresponding Laplace exponents are given by

| (12) | ||||

| (13) |

where .

Finally, we introduce the Wiener-Hopf factors for :

where denotes an independent exponential random variable of rate and are the running supremum and infimum of respectively. It is well known that

| (14) |

see e.g. [19, Thm. 6.16]. In a similar way we define the Wiener-Hopf factors for . We are now ready to formulate our main result.

Theorem 1.

We note that the cases and should be understood in the limiting sense. Importantly, numerical evaluation of the survival probability function using Theorem 1 is feasible. We refer an interested reader to [13, 14] for a discussion of an efficient and accurate numerical inversion of a two-dimensional Laplace transform and computation of the Wiener-Hopf factors, respectively.

Proof of Theorem 1.

We rewrite (8) using measure transforms from Section 5.1:

By analytic continuation and continuity on the imaginary axis we see that this equation holds for all with . It is shown in [7] that can be analytically continued to . Moreover, in this domain for , for , and the identity is preserved. Thus we can plug in the above equation for to obtain the following:

Assume for a moment that and multiply both sides by which using (12) leads to

Using Wiener-Hopf factorization we arrive at

| (15) | ||||

Consider (15) and note that the lhs is analytic in , the rhs is analytic in , and both are continuous and coincide on the imaginary axis; for this is checked by taking the limit in the respective half plane, see also (16) below. Hence this equation defines an entire function. Let us show that it is bounded and hence is a constant, call it , by Liouville’s theorem. According to [7] the ratios of W-H factors are bounded in their respective half planes. The transforms of boundary measures are bounded by 1. Finally we consider for ; the corresponding term on the rhs can be analyzed in the same way. Boundedness follows from the following simple observations: as .

Both sides of (15) are equal to some constant , which can be identified by taking the limit . Suppose then and hence we have

| (16) |

This results in

and for we similarly have

Recall that under the net profit condition (9), we have and at least one of should be positive. Now it is not hard to check that .

Corollary 2.

For independent and satisfying (9) it holds that

Proof.

First observe that and similar observations hold true for the other W-H factors. From Theorem 1 we see that

To get the first statement, let and then . The second is obtained by reversing the order of limit operations. ∎

6.1 Example: contingent surplus note

Let us provide a check for a simple particular case, which admits a direct analysis. Suppose that , i.e. the second company is, in fact, a surplus note, which earns a constant premium and provides a cover for the first company. We also assume that the net profit condition (9) holds.

Note that our system survives if and only if the one dimensional Cramér-Lundberg process survives when started at . Hence, with the survival probability for the process when started at ,

| (17) |

where is the Laplace exponent of .

6.2 Example:

Assume that which in particular holds when there are no transaction costs, i.e. . The net profit condition reduces to a single inequality . From (2) it follows that

Observe that the ruin time is the first jump of . Hence we have and for all . Therefore, is the ruin time of the classical Cramér-Lundberg process started in . Similar to (17) we get

| (18) |

6.3 Numerical experiments

In this section we provide a simple numerical illustration of our main result, Theorem 1, by computing

i.e. the survival probability for initial capitals , which are two independent exponential random variables of rates and respectively. The main difficulty lies in evaluating the Wiener-Hopf factors. This task can be accomplished using various approaches, see e.g. [14] presenting an algorithm based on the Spitzer identity and Laplace inversion technique. In this study, however, we use a Monte Carlo simulation algorithm to obtain Wiener-Hopf factors, which is relatively straightforward to implement since the processes and are CPPs. These two processes are constructed from the inverse local time processes and , which we discuss in the following.

Consider any of and for the moment drop the index to simplify notation. From the general theory of local times, see [19, Ch. 6.2], we know that is a CPP with jump distribution , where . Let us determine the jump rate of assuming that :

where we used the exit identity [19, (8.6)] and the fact that in that formula. Comparing to (10) we see that . This allows to simulate the process by drawing from , which in turn requires to simulate the original process and to reject the paths with ‘long survival’.

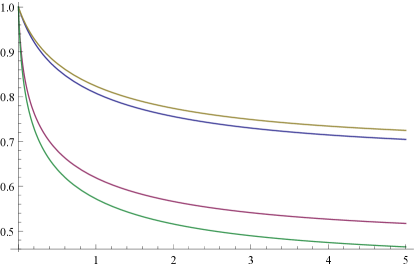

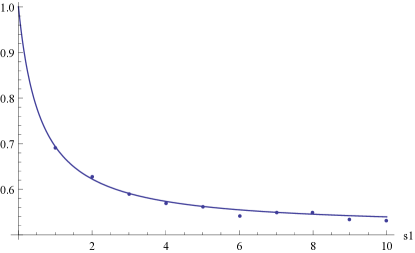

In our experiment we take deterministic claim sizes , and put and , which ensures that and yields . First we simulate realizations of and then assign values to the Wiener-Hopf factors in an obvious way, e.g. , see Figure 2.

Now we can use Theorem 1 to plot , see Figure 3 where we fix and let . Note that the survival probability is a decreasing function of and thus it is increasing as a function of the mean initial capital .

Finally, we report , the survival probability from zero initial capitals. Corollary 2 yields and using positive and negative Wiener-Hopf factors respectively; the direct simulation gives .

7 Making some capital transfers impossible

One can modify our risk model so that only the second company is allowed to help the first one, but not the opposite way. In other words, we regard the second company as an insurer of the first (against deficit) with its own stream of claims. Note that this new model is governed by the equations

In the following we specialize our results to this case by taking limits as . The survival probability we thus obtain corresponds to survival of both insurer and reinsurer.

Firstly, the kernel equation becomes

which is immediate from Proposition 1 and (1). Secondly, the net profit condition now reads

| (19) |

which is seen by repeating the steps of the proof of Proposition 2. Assuming independence of claim streams, we obtain the following corollary of Theorem 1.

Corollary 3.

Assume that and are independent and satisfy (19). Then for it holds that

Proof.

Let us examine the limiting quantities (as ) from the statement of Theorem 1. Firstly, stay the same, but

To see this notice that and so a.s., which yields the first limit. The second is then obtained from (14) (written for ‘R’) and (13). Finally, observe that and take the limit in the equation of Theorem 1. ∎

Finally, let us assume that neither company can help the other, i.e. . Thus we retrieve the standard bivariate ‘or’ problem, where the ruin means ruin in at least one line, see [8, Eq. (1.5)]. The kernel equation becomes

Now assume that and that are independent, and take the limit as in Corollary 3. Noticing that

we obtain

This yields the correct product formula

providing yet another check.

8 Open problems

Various interesting directions for future work exist with respect to the present model. Firstly, one may try to extend the model to allow for more general driving processes, that is for Lévy processes with negative jumps. This seems to be a hard problem contrary to many other settings, where such generalizations require little additional effort. In fact, there are essential difficulties in each step leading to Theorem 1:

- 1.

-

2.

The kernel equation. We believe that Proposition 1 holds for a general bivariate Lévy process with negative jumps. One may try to employ the generator of the underlying Markov process instead of an reasoning. There are various problems on this way including the required smoothness of the survival function. Alternatively, one may try to use a martingale approach, but the choice of an appropriate martingale is far from trivial.

- 3.

Secondly, it is important to understand if the kernel equation in Proposition 1 characterizes the survival probability in some sense. In the case of a reflected Brownian motion in a quadrant the basic adjoint relation characterizes the stationary distribution together with the boundary measures, see [23, Thm. 3.4]. This property allowed Dai and Harrison [12] to construct an algorithm computing the stationary distribution based on the basic adjoint relation.

Finally, one may try to interpret Theorem 1 (and the quite similar Theorem 1 in [7]) to provide a probabilistic approach. Moreover, one may consider some alternative risk measures of the model in (2) such as discounted external injections of capital. One may also try to extend the model to a setting with multiple companies. It seems that a probabilistic approach could be very helpful in this respect.

Acknowledgment

The authors are indebted to Hansjörg Albrecher (Univ. Lausanne), Esther Frostig and David Perry (Univ. Haifa) for stimulating discussions.

The research of Onno Boxma was supported by the TOP-I grant Two-dimensional Models in Queues and Risk of the Netherlands Organisation for Scientific Research (NWO),

and Jevgenijs Ivanovs was supported by the Swiss National Science Foundation Project 200020_143889.

Appendix

References

- Asmussen and Albrecher [2010] Asmussen, S., Albrecher, H., 2010. Ruin probabilities. World Scientific.

- Avram nad Pistorius [?] Avram, F., Pistorius, M. A capital management problem for a central branch with several subsidiaries (work in progress).

- Avram et al. [2008] Avram, F., Palmowski, Z., Pistorius, M., 2008. A two-dimensional ruin problem on the positive quadrant. Insurance: Mathematics and Economics 42 (1), 227–234.

- Badescu et al. [2011] Badescu, A., Cheung, E., Rabehasaina, L., 2011. A two-dimensional risk model with proportional reinsurance. Journal of Applied Probability 48 (3), 749–765.

- Badila et al. [2014] Badila, E., Boxma, O., Resing, J., 2014. Queues and risk models with simultaneous arrivals. Advances in Applied Probability 46 (3), 812–831.

- Badila et al. [2015] Badila, E., Boxma, O., Resing, J., 2015. Two parallel insurance lines with simultaneous arrivals and risks correlated with inter-arrival times. Insurance: Mathematics and Economics 61, 48–61.

- Boxma and Ivanovs [2013] Boxma, O., Ivanovs, J., 2013. Two coupled Lévy queues with independent input. Stochastic Systems 3 (2), 574–590.

- Cai and Li [2005] Cai, J., Li, H., 2005. Multivariate risk model of phase type. Insurance: Mathematics and Economics 36 (2), 137–152.

- Cai and Li [2007] Cai, J., Li, H., 2007. Dependence properties and bounds for ruin probabilities in multivariate compound risk models. Journal of Multivariate Analysis 98 (4), 757–773.

- Chan et al. [2003] Chan, W., Yang, H., Zhang, L., 2003. Some results on ruin probabilities in a two-dimensional risk model. Insurance: Mathematics and Economics 32 (3), 345–358.

- Cohen and Boxma [1983] Cohen, J. W., Boxma, O. J., 1983. Boundary Value Problems in Queueing System Analysis. Vol. 79 of North-Holland Mathematics Studies. North-Holland Publishing Co., Amsterdam.

- Dai and Harrison [1992] Dai, J., Harrison, J., 1992. Reflected Brownian motion in an orthant: numerical methods for steady-state analysis. The Annals of Applied Probability, 65–86.

- Den Iseger [2006] den Iseger, P., 2006. Numerical transform inversion using Gaussian quadrature. Probability in the Engineering and Informational Sciences 20 (1), 1–44.

- Den Iseger et al. [2013] den Iseger, P., Gruntjes, P., Mandjes, M., 2013. A Wiener–Hopf based approach to numerical computations in fluctuation theory for Lévy processes. Mathematical Methods of Operations Research 78 (1), 101–118.

- Fayolle and Iasnogorodski [1979] Fayolle, G., Iasnogorodski, R., 1979. Two coupled processors: the reduction to a Riemann-Hilbert problem. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete 47 (3), 325–351.

- Gong et al. [2012] Gong, L., Badescu, A., Cheung, E., 2012. Recursive methods for a multi-dimensional risk process with common shocks. Insurance: Mathematics and Economics 50 (1), 109–120.

- Harrison and Reiman [1981] Harrison, J., Reiman, M., 1981. Reflected Brownian motion on an orthant. The Annals of Probability, 302–308.

- Kella [2006] Kella, O., 2006. Reflecting thoughts. Statistics & Probability Letters 76 (16), 1808–1811.

- Kyprianou [2006] Kyprianou, A., 2006. Introductory Lectures on Fluctuations of Lévy Processes with Applications. Universitext. Springer-Verlag, Berlin.

- Lautscham [2013] Lautscham, V., 2013. Solvency modelling in insurance : Quantitative aspects and simulation techniques. Ph.D. thesis, University of Lausanne.

- Skorokhod [1961] Skorokhod, A., 1961. Stochastic equations for diffusion processes in a bounded region. Theory of Probability & Its Applications 6 (3), 264–274.

- Sundt [1999] Sundt, B., 1999. On multivariate Panjer recursions. Astin Bulletin 29 (1), 29–45.

- Williams [1995] Williams, R., 1995. Semimartingale reflecting Brownian motions in the orthant. IMA Volumes in Mathematics and its Applications 71, 125–137.