Extended -Gaussian and -exponential distributions from Gamma random variables

Abstract

The family of -Gaussian and -exponential probability densities fit the statistical behavior of diverse complex self-similar non-equilibrium systems. These distributions, independently of the underlying dynamics, can rigorously be obtained by maximizing Tsallis “non-extensive” entropy under appropriate constraints, as well as from superstatistical models. In this paper we provide an alternative and complementary scheme for deriving these objects. We show that -Gaussian and -exponential random variables can always be expressed as function of two statistically independent Gamma random variables with the same scale parameter. Their shape index determine the complexity -parameter. This result also allows to define an extended family of asymmetric -Gaussian and modified -exponential densities, which reduce to the previous ones when the shape parameters are the same. Furthermore, we demonstrate that simple change of variables always allow to relate any of these distributions with a Beta stochastic variable. The extended distributions are applied in the statistical description of different complex dynamics such as log-return signals in financial markets and motion of point defects in fluid flows.

pacs:

02.50.-r, 89.75.Da, 89.65.Gh, 47.27.-iI Introduction

Long-range interparticle interaction, long-term microscopic or mesoscopy memory, fractal or multifractal occupation in phase space, cascade transfer of energy or information, and intrinsic fluctuations of some dynamical system parameters are some of the properties that nowadays are related with complexity. One of the emergent properties related with these phenomena is the power-law statistics of the corresponding nonequilibrium states. While there exits different underlying formalism for tackling these issues, maximization of Tsallis “non-extensive” entropy tsallis ; TsallisBook ; Qlectures ; qConstraints provides an alternative basis over which complexity can be analyzed and studied in a broad class of systems. Introducing a generalized second moment constraint TsallisBook ; qConstraints , the formalism lead to a generalization of standard normal probability densities, named as -Gaussian distributions. In terms of a generalized exponential function, they can be written as where the parameter defines different complexity classes. Explicitly, these statistical objects read

| (1) |

where the variable of interest is restricted to the domain On the other hand,

| (2) |

where now is allowed to runs over the real line. The restriction follows from the normalization condition which is guaranteed by the dimensionless constant The parameter measures the width of the distributions. As is well known TsallisBook , in the limit both expressions reduce to the standard Gaussian distribution. These generalizations allow to describe variables restricted to a finite domain [Eq. (1)] as well as power-law statistics [Eq. (2)].

-Gaussian distributions also arise as solution of non-linear Focker-Planck equations QFokker ; LevyAsQ as well as in the formulation of central limit theorems with highly correlated random variables QCentralLimit . Furthermore they fulfill a generalized fluctuation relation symmetry budini . A wide and diverse class of systems obey their statistics TsallisBook , such as in fluids flows superstatistics ; lewis ; beck , optical lattices lutz , trapped ions interacting with a classical gas voe , in granular mixtures puglisi , anomalous diffusion in dusty plasma liu or cellular aggregates sawada , avalanches sizes in earthquakes latora , in astrophysical variables voros , as well as in econophysics osorio ; borland ; ausloos ; rosenfeld ; fuentes .

When introducing a first moment constraint, Tsallis entropy leads to a -exponential distribution [Eqs. (1) and (2) under the replacement with and respectively], which in the limit recovers the standard exponential probability density of a positive random variable. These objects, for example, allow to fit high energy collisions wloda , quark matter statistics biro , solar flares stella and momentum distributions of charged hadrons khacha . -exponential functions also fit anomalous power-law dipolar relaxation brouers as well as spin-glass relaxation pappas . More recently, a kind of generalized -Gamma probability density was introduced for describing stock trading volume flow in financial markets queiros ; souza ; cortines .

It is remarkable that all quoted probability densities can also be obtained from a superstatistical modeling superstatistics , where a parameter of an underlying probability measure becomes a (positive) random variable characterized by a Gamma distribution feller ; johnson ; kleiber ; vanKampen . This is the case of -Gaussian densities, where the underlying distribution is a normal one superstatistics , while for -exponential it is an exponential function wloda . For generalized -Gamma variables the underlying distribution is a Gamma density while the random parameter is distributed according to an inverse Gamma distribution queiros .

The main goal of this paper is to present a complementary and alternative scheme to those provided by entropy extremization and superstatistics. We show that random variables described by any of the quoted families of -distributions can be written as a function of two independent (positive) random Gamma variables feller ; johnson ; kleiber ; vanKampen . Their scale parameter is assumed the same, while their shape indexes determine the complexity -parameter. When the shape indexes are different, a class of extended asymmetric -Gaussian and modified -exponential distributions are obtained. Generation of -distributed random numbers is straightforward from these results IEEE ; levyNum . We also show that simple transformation of variables allow relating any of the obtained densities with a Beta distribution. Interestingly, this statistical function has been applied to model a wide variety of problems arising in different disciplines feller ; johnson ; kleiber . On the other hand, a -triplet constantino ; burlaga for the probabilities densities is obtained. The usefulness of the extended distributions in the context of financial signals ausloos and motion of point defects in fluid flows beck is demonstrated. These systems are characterized by highly asymmetric distributions. This feature is absent in previous approaches, being recovered by the present one.

The paper is organized as follows. In Sec. II we review the properties of Gamma random variables and introduce the main assumption over which the present scheme relies. In Sec. III asymmetric -Gaussian distributions are obtained, while Sec. IV is devoted to modified -exponential densities. In Sec. V the properties of the proposed scheme as well as its applications are discussed. In Sec. VI the Conclusions are provided.

II Model

A stochastic random variable is Gamma distributed feller ; johnson ; kleiber ; vanKampen if its probability density is

| (3) |

where is the Gamma function. This distribution is characterized by the scale parameter and its shape parameter In terms of these parameters its mean value reads with variance The underlying stochastic process that leads to this statistic involves a cascade-like mechanism feller ; johnson ; kleiber ; vanKampen . In fact, this property is evident from the Laplace transform where Hence, when is natural it reduces to a convolution of exponential functions, which can be read as a cascade of consecutive random steps.

The present approach relies on two independent Gamma random variables Their joint probability density then read

| (4) |

Here, we assumed that both scale parameters are the same, while and are the shape parameters of and respectively. The main ingredient of the present scheme is the ansatz

| (5) |

where the new random variable depending of the function develops different statistics. We will show that a wide class of -distributions arise from non-linear functions, which in turn are asymmetric in their arguments (see Sec. III and IV). Nevertheless, in all cases they fulfill a very simple symmetry (see Sec. V).

The probability distribution of is completely determined by the joint probability (4) and the function In fact, it follows from a elementary change of variables vanKampen . For closing the problem, we introduce an extra random variable defined by the addition

| (6) |

Therefore, the joint probability of and is given by

| (7) |

where is the Jacobian matrix

| (8) |

The probability of each variable follows by partial integration

| (9) |

As is defined by the addition of two independent Gamma variables with the same scale factor, it follows

| (10) |

Hence, is also a Gamma variable [ see Eq. (3)] where its shape index is feller ; johnson ; kleiber ; vanKampen .

III Asymmetric -Gaussian distributions

In order to motivate the election of the function that lead to -Gaussian statistics we may think (in a roughly way) in a Brownian particle that interact with a complex reservoir. and are the (positive and negative) impulse moments induced by the bath fluctuations. In addition, the complexity of the system-environment interaction is taken into account by a system response function that depends on both and Therefore, this contribution can be read as a random-dissipative-like mechanism. The particle fluctuation is finally written as One may also think in a economical agent that, from the available information, predict that a future price may increases or decrease a quantity or respectively. The weight of the available information is then measured by leading to the same kind of dependence.

In order to close the model, we assume that is given by a kind of average or mean value between the two random values and Specifically we take

| (11) |

where Therefore, we write the random variable [Eq. (5)] as

| (12) |

By convenience we introduced a factor one half. On the other hand, the additional parameter scales and gives the right units of In fact, notice that the remaining contribution in Eq. (12) is dimensionless. Taking different values of the real parameter a wide class of probability distributions arise, which in turn may also depends on the parameters and that determine the joint probability density (4).

III.1 Arithmetic mean

The arithmetic mean value corresponds to implying that

| (13) |

Notice that, for any possible value of and the random variable assume bounded values in the domain Taking into account the variable [Eq. (6)], we obtain the following inverted relations

| (14) |

which in turn implies that Eqs. (4) and (7) lead to where is given by Eq. (10). Therefore, the random variables and are statistically independent. Furthermore, obeys the statistics given by the probability density

| (15) |

where the normalization constant reads Notice that does not depends on the scale parameter [see Eq. (4)]. It only depends on the shape indexes and the scale parameter

The distribution (15) develop a maximum located at

| (16) |

when or at in any other case. Its average value read

| (17) |

while the variance is given by

| (18) |

-Gaussian distributions

Eq. (15) can be rewritten as

| (19) |

Hence, we name this function as an asymmetric Poissonian -Gaussian distribution with index and asymmetry parameter

| (20) |

From the positivity of and the asymmetry index must to satisfy In the symmetric case, we get

| (21) |

where Therefore, under the association with we recover Eq. (1). Over the domain the non-extensive parameter runs in the interval

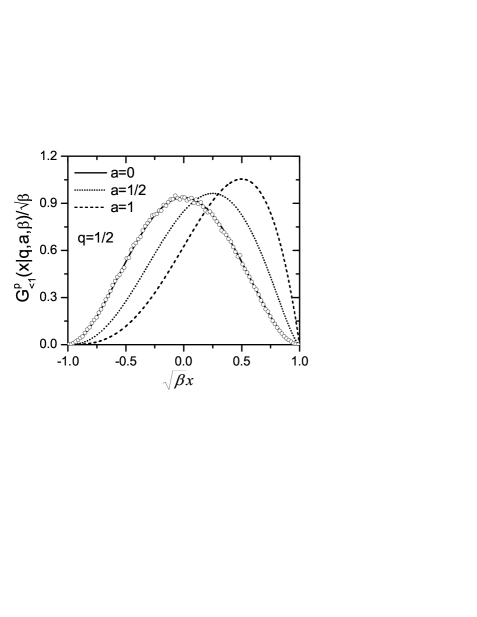

In Fig. 1 we plot the function (19) for different values of the asymmetric factor Eq. (20). For increasing the distribution accumulates around For a reflected accumulation around is developed. The distribution with corresponds to Tsallis non-extensive thermodynamics.

III.2 Geometric mean

In Eq. (11) the geometric mean correspond to which satisfies Therefore, we get the random variable [Eq. (12)]

| (22) |

Notice that assumes values over the entire real number line, In this case, the inverted relations are

| (23) |

implying that which in turn also lead to but here

| (24) | |||||

As in the previous case, this distribution is independent of the rate parameter The normalization constant is the same,

Eq. (24) develops a maximum, which occurs at

| (25) |

In the limit a power-law behavior arise

| (26) |

while for we obtain

| (27) |

Due to the previous asymptotic behaviors the moments are not defined for any value of the characteristic shape parameters. When and the average value reads

| (28) |

while the second moment, for and is

| (29) |

Outside the previous intervals the first two moments are not defined.

-Gaussian distributions

Eq. (24) can be rewritten as

| (30) |

As is the previous case, we name this function as an asymmetric Poissonian -Gaussian distribution with index and asymmetry parameter

| (31) |

Hence, and the asymmetry factor satisfy the restriction In the symmetric case, reduces to

| (32) |

where Under the association we recover Eq. (2). In the interval the non-extensive parameter runs in the interval

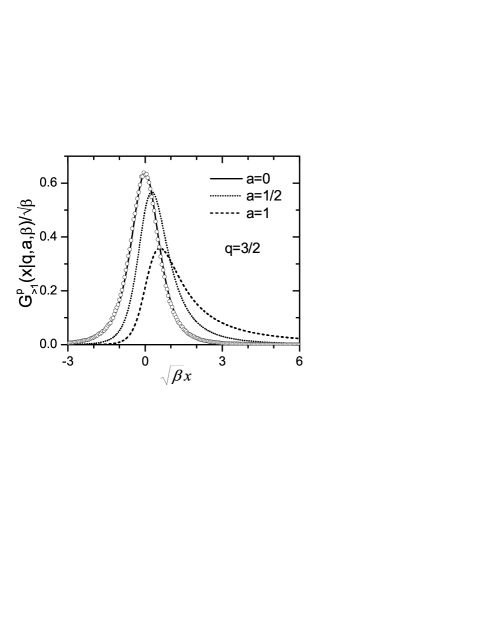

In Fig. 2 we plot the function (30) for different values of the asymmetric factor Eq. (31). For increasing the maximum of the distribution is shifted to higher values. For the extremum develops for negative values. The symmetric case corresponds to the -Gaussian distribution arising from Tsallis entropy.

III.3 Relation between both cases

Given determinate by relation (13), the random variable defined as

| (33) |

recover Eq. (22). This simple relation demonstrate that there exist a one to one mapping between -Gaussian variables in the different domains of the complexity parameter In fact, if we define for hence where has associated the index

Alternatively, if is given by Eq. (22), the inverse transformation

| (34) |

lead to Eq. (13). While these relations are known for symmetric -Gaussian distributions TsallisBook , here we showed that they are also valid for the asymmetric densities introduced previously.

IV Modified -exponential distributions

Variables distributed according to a -exponential density are positive. Therefore, the previous scheme does not apply, but a similar one can be implemented. We name the emerging distributions as modified -exponential densities. Taking into account the notation of Refs. queiros ; souza ; cortines they can also be called as generalized -Gamma densities. Nevertheless, it seems that they do not satisfy the same entropic properties than standard Gamma distributions stolongo . On the other hand, we remark that some properties of the following distributions are known and can be found under different denominations johnson ; kleiber .

IV.1 Bounded domain

For getting a positive variable, we introduce the following functional dependence

| (35) |

Notice that this assumption is very similar to Eq. (13), but here is a bounded positive stochastic variable, Using the approach defined in Sec. II, here we obtain the inverse relations

| (36) |

while leading again to a statistical independence of and that is The density of interest here is

| (37) |

where When and reaches a maximal value located at

| (38) |

Its first moment reads

| (39) |

while the variance is given by

| (40) |

-exponential densities

The distribution (37) may be named as a modified Poissonian -exponential distribution with index and “distortion parameter”

| (41) |

Therefore, and When that is Eq. (37) becomes

| (42) |

where Therefore, under the extra association we obtain a standard -exponential density. For it follows

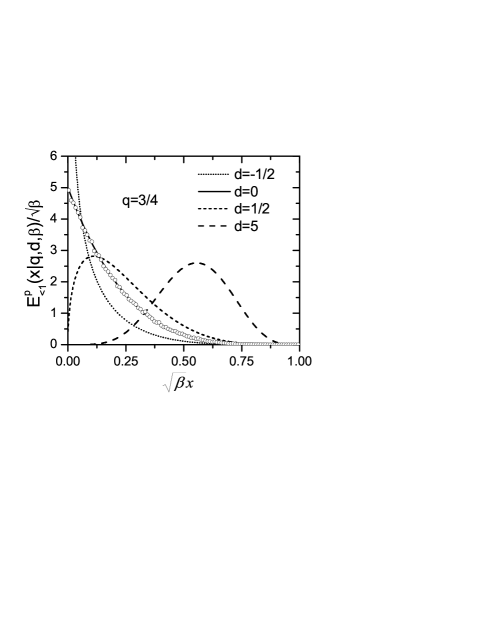

In Fig. 3 we plotted the function (37) for different values of the distortion parameter Eq. (41). For the density diverges around the origin. This property is inherited from the Gamma distribution Eq. (4). On the other hand, for the density vanishes at the origin and for increasing it accumulates around The plot for is the -exponential distribution arising from Tsallis entropy.

IV.2 Unbounded domain

An unbounded positive variable is obtained from the relation

| (43) |

where as in the previous cases scales the random variable Here, the inverse relations are

| (44) |

while leading to where

| (45) |

with This distribution develops a maximum that is located at

| (46) |

For it follows the asymptotic power-law behavior

| (47) |

In consequence, the moments are not defined for any value of the shape parameter For the mean value reads

| (48) |

while the second moment is only defined for

| (49) |

-exponential densities

The distribution (37) may also be named as a modified Poissonian -exponential distribution with index and distortion parameter

| (50) |

In consequence, and the distortion parameter satisfy When the distortion is null, Eq. (45) becomes

| (51) |

where Thus, under the extra association we get a -exponential probability density. In this case, for it follows

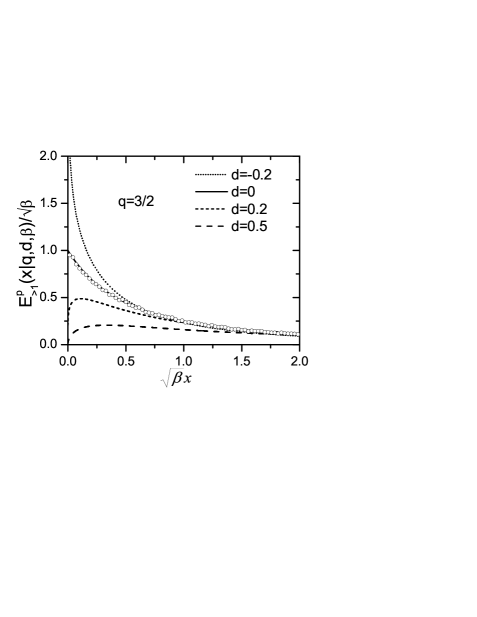

The function (45) is plotted in Fig. 4 for different values of the distortion parameter Eq. (50). For the density diverges around the origin. On the other hand, for the density vanishes at the origin. In all cases a power-law behavior is obtained for The plot for is the -exponential distribution arising from Tsallis entropy.

IV.3 Relation between both cases

IV.4 Stretched -exponential densities

Introducing the change of variables

| (54) |

defined by the extra parameter if is distributed according to Eq. (37), it follows

| (55) |

On other hand, if is distributed according to Eq. (45), we get

| (56) |

In both cases, imposing the condition the previous two expressions becomes stretched -exponential densities, Hence, these distributions can also be covered with the present approach [Eqs. (35) and (43) under the change of variables (54)].

V Properties and applications

In the previous two sections we demonstrated that the assumption (5) allow us to recover and to define an extend family of -Gaussian and -exponential densities. Here, we discuss some general properties of the approach as well as some applications of the extended distributions.

V.1 -distributed random numbers

Numerical generation of random numbers obeying -Gaussian statistics was explored previously by introducing a generalized Box-Muller method IEEE . Generation of Levy distributed numbers was also established levyNum . On the other hand, numerical generation of Gamma random numbers is also well established johnson ; kleiber . Therefore, the present scheme defines an alternative and solid basis for obtaining -distributed random numbers by generating two independent Gamma random numbers. Using this method, in Fig. (1) to (4) we explicitly show (circles) the recovering of the symmetric and unmodified distributions, all of then corresponding to Tsallis entropy formalism.

V.2 Symmetries

While the underlying joint statistics of the Gamma variables depends on the scale parameter Eq. (4), the distributions of do not depend on it. This is not the only symmetry of the proposed scheme. In fact, it is simple to check that the symmetry

| (57) |

is fulfilled, where define the random variable, Eq. (5). In fact, this property is valid for the -Gaussian case [Eq. (12) for any ] as well as for the -exponential variables [Eqs. (35) and (43)]. We notice that for arbitrary functions always satisfies the relation (57). Extra structures can be established by introducing arbitrary change of variables.

V.3 Relation with Beta distributions

As all functions fulfill the condition (57), it is clear that any of the corresponding variables are always related by a change of variables between them. Therefore, it does not make sense to affirm that one of them generates or is more fundamental than the others. Nevertheless, here we want to emphasize that any of the probability densities obtained previously can be related with the well known Beta distribution feller ; johnson ; kleiber . It reads

| (59) |

where the domain of its variable is Furthermore, its shape parameters and are positive.

Defining the change of variables all obtained -distributions becomes equal to Eq. (59). Alternatively, defining a new variable from the Beta distribution it is possible to obtain the -densities. Explicitly, for the asymmetric distribution Eq. (15) [or Eq. (19)], the change of variables read

| (60) |

Therefore, all (asymmetric and symmetric) -Gaussian distribution with are related to a Beta variable by a shifting of their arguments.

For Eq. (37), the relations are

| (62) |

that is, the modified (and standard) -exponential densities in the interval arise from an axe inversion of a Beta distribution. Finally, in the interval Eq. (45), the transformations are

| (63) |

The previous relations can be enlighten by using that a variable obeying the Beta statistics (59) can also be written in terms of two independent Gamma variables and feller ; johnson ; kleiber [Eq. (4)]

| (64) |

where the additional variable is also Beta distributed. In fact, After a straightforward manipulation, the random variables associated to the -Gaussian distributions, Eqs. (13) and (22), can respectively be rewritten as

| (65) |

while for the -exponentials densities, Eqs. (35) and (43), respectively it follows

| (66) |

Both Eq. (65) and Eq. (66) show the stretched relation between all the generalized -distributions and Beta random variables. In fact, any stochastic variable defined by a function satisfying the symmetry (57) can be related by a transformation of variables with a Beta distribution, Eq. (59).

One may also take the inverse point of view and to explore if the previous densities can be obtained from Tsallis entropy under a more general constraint. In fact, any of the extended distributions can be rewritten as This structure emerges from Tsallis entropy by using a constraint based on a generalized mean value of TsallisBook . Nevertheless, here the resulting functions depend on the parameter and also on the asymmetry and distortion factors. Therefore, a relation between Tsallis entropy and the asymmetric and modified distributions cannot be established in this way.

V.4 q-triplet for probability densities

In the context of non-extensive thermodynamics three different values of the complexity parameter, named as -triplet, are associated to different physical properties such as the statistics of metastable or quasi-stationary states, sensitivity to initial conditions, and time-decay of observable correlations constantino ; burlaga . Here, we show that three different values of allow to indexing the symmetric and unmodified probability densities. We remark that not any direct relation can be postulated between both triplets, because here it is established for normalizable objects,

We denote by and the complexity indexes of the -Gaussian distributions Eqs. (20) and (31) respectively. Furthermore, and denote the indexes of the -exponentials, Eqs. (41) and (50) respectively. The four indexes are given by

| (67a) | |||||

| (67b) | |||||

| We notice that [see Eqs. (20) and (41)]. This equality is expectable because -Gaussian and -exponential distributions for are related by a linear change of variables [see Eqs. (60) and (62)] with a Beta distribution. Therefore, the complete family of analyzed distributions can be indexed with only three -parameters: The previous expressions are equivalent to | |||||

| (68a) | |||||

| (68b) | |||||

| From here we realize that there exist simple relations between any of the -triplet parameters. | |||||

V.5 Applications of the extended distributions

The assumption (5) lead us with a broad class of probability densities, which in turn cover the most used probabilities densities arising from Tsallis entropy maximization. Hence, besides it theoretical interest, we ask about the possible applications of the asymmetric and modified distributions.

From the previous analysis, we arrived to the conclusion that asymmetric -Gaussian and modified -exponential distributions in the interval [Eqs. (19) and (37)] are related by a linear change of variables with a Beta distribution. Therefore, these functions fall in the wide range of applicability of this distribution feller ; johnson ; kleiber . For example, (unnormalized) Beta distributions emerge in the statistical description of quark matter (see Eq. (102) in Ref. biro ).

The modified -exponential function Eq. (45) was used in the description of stock trading volume flow in financial markets queiros ; souza ; cortines (named as generalized -Gamma probability density). This distribution is also known as a Pearson Type VI distribution or alternatively Beta-prime distribution johnson (see also kleiber ).

To our knowledge, asymmetric -Gaussian distributions Eq. (30) were not used previously. In the present approach, the asymmetry of these probability densities has a clear dynamical origin. In fact, associating a cascade process to each Gamma variable, asymmetries arise whenever the cascades have a different shape index and Below we discuss the application of these kind of distributions as a fitting tool in the context of financial signals ausloos and movement of defects in fluid flows beck .

V.5.1 Log-returns signals on large time windows

From the price signal in a financial market it is possible to define the stochastic process where is a constant time interval. This signal gives a simple way of representing returns in the market. Usually it is studied the normalized log-returns where is the average and gives the standard derivation of for a given Daily closing price values of the S&P index for a period of twenty years were analyzed by Ausloos and Ivanova in Ref. ausloos . Assuming a stationary signal, for large time windows day), the authors fitted the experimental data with a -Gaussian like distribution

| (69) |

where and depends on the parameters and (see Eqs. (4) and (5) in ausloos ). This distribution can be obtained from a superstatistical model assuming, for example, that Brownian particles diffuse in a potential superstatistics . On the other hand, Eq. (69) can also be recovered from the present approach based on random Poisson variables. In fact, it follows by extending symmetrically the stretched -exponential distribution (56), with and the following replacements and Random numbers generation is achieved by introducing an extra stochastic variable that with probability one half defines their sign (positive or negative).

Eq. (69) develops an asymptotic power-law behavior. Nevertheless, the authors also find that the experimental data are not consistent with the symmetry In particular, the power-law behaviors have different exponents for positive and negative values. Similar asymmetries were found previously in Ref. stanley .

Here, we may associate the observed asymmetry of the data to two cascades mechanisms, each one being represented by a Gamma random variable. In a roughly way, the difference between both variables can be associated to different networks properties related to the propagation of information that support an increased or decreased future value. The complete system response is defined by Eq. (22), that is a geometric mean value of the driving fluctuations. Hence, instead of using Eq. (69), we propose to fit the probability density of the log-returns with the asymmetric -Gaussian distribution (30) under the shifting where is given by Eq. (28).

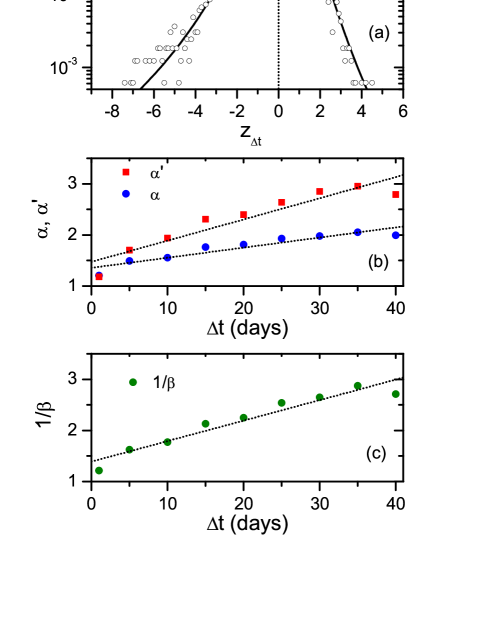

In order to check this proposal, here we analyze the daily closing price values of the S&P index yahoo for the period between Jan. 3, 1950 and Dec. 3, 2014, which provides a 16336 data base. In Fig. 5(a) we show the “experimental” probability distribution (circles) for days. The data are clearly asymmetric, which in fact are fitted by Eq. (30) (full line). Its characteristic parameters and were determinate by minimizing the global error. Based on the quadratic global error we checked that for a wide range of the asymmetric distribution provides a better fitting than Eq. (69).

In Fig. 5(b) we plot and as function of In the limit the asymmetry vanishes Furthermore, in the plotted interval, both shape parameters increase linearly with For higher values of an irregular-logarithmic-like grow behavior is observed (not shown). For the distributions approaches normal Gaussian ones. This limit is consistent with the grow of and [see Eq. (31)]. On the other hand, we find that also increases linearly with Fig. 5(c). This (diffusive) behavior is also found for intervals minor than a day fuentes .

Extra analysis and ingredients are necessary for explaining the linear behaviors shown in Figs. 5(b) and (c). On the other hand, Fig. 5(a) shows that the proposed probability density provides a reasonable and alternative fitting to that based on Eq. (69), which in turn is able to capture the observed asymmetries.

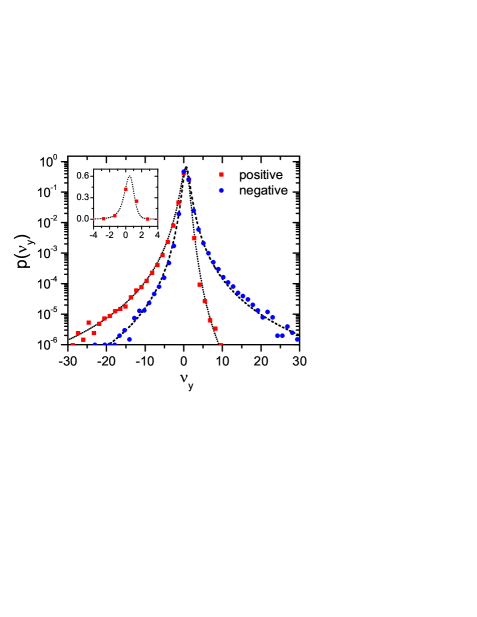

V.5.2 Defect velocities in inclined layer convection

In Ref. beck Daniels, Beck, and Bodenshatz studied the motion of point defects in thermal convection patterns in an inclined fluid layer (heated from below and cooled from above), a variant of Rayleigh-Bénard convection. Due to the inclination the system is anisotropic. The (experimental) probability distribution of the (positive and negative) defect velocities is different in the transverse ( across rolls) and longitudinal ( along rolls, uphill-downhill) directions. In the transverse direction the velocity can be fit with a symmetric -Gaussian distribution Nevertheless, in the longitudinal direction the distribution, depending on a dimensionless temperature (see details in beck ), develops strong asymmetries. In that situation, Tsallis distributions, even defined with a cubic potential, are unable to fit the experimental data (see Fig. 4(a) in beck ). As shown in the next figure, these asymmetries can be fitted with the probability densities introduced previously.

In Fig. 6 we show a set of experimental data karen , corresponding to the probability density of the dimensionless velocity of positive and negative defects (see also Fig. 4(a) in beck ). We find that these data can be very well fitted with the distribution Eq. (30) under the associations Hence, where follows from Eqs. (28) and (29). Furthermore, we introduced an extra dimensionless parameter that only shifts the complete distribution. Due to the previous rescaling, does not depend on the parameter The parameters and were determinate such that the global error is minimized. Even when the asymmetry is appreciable, the maximum of the distribution [Eq. (25)] is around the origin. In fact, the influence of the shift introduced by is only appreciable around the origin (note that in both cases For both positive and negative defects a very well fitting is obtained. We also checked that a similar fitting is obtained for higher values of the dimensionless temperature, where the distribution asymmetry is smaller than that shown in Fig. 6 (see Fig. 4(b) in beck ). Hence, we conclude that dynamics of the defects velocity may be though as being governed by two cascade mechanisms with different statistical properties, such as that defined by Eq. (22). While a rigorous derivation of this interpretation is not developed here, the quality of the fitting gives a consistent support to the proposed theoretical frame.

VI Conclusions

The present approach relies on expressing the variable of interest, associated to a given complex system, as a function of two independent Gamma random variables. These variables represent intrinsic fluctuations that drive the system. In addition, the complexity of the dynamics is represented by a random-system-response that also depends, in a non-linear way, on the fluctuations. Writing the system response in terms of a generalized mean value, Eq. (12), we showed that the arithmetic and geometric cases allow us to introduce a class of asymmetric -Gaussian distributions. In the symmetric case, for any value of the complexity parameter they recover densities that follow from Tsallis entropy maximization. A similar approach applies for -exponential distributions, which become defined in terms of a distortion parameter. We also showed that the complete family of obtained distributions can be related via a change of variables with a Beta distribution. A -triplet was derived for the symmetric and unmodified distributions.

On one side, these results define an alternative numerical tool for random number generation obeying the previous statistical behaviors. On the other hand, the present approach may provide an alternative and very simple basis for understanding statistical behaviors in complex dynamics. Of special interest is the possibility of relating any asymmetry in the probability distributions with different underlying cascade mechanisms. We have shown that in fact asymmetric Poissonian -Gaussian densities provide a very well fitting to the statistical distribution of log-return signals in financial markets (Fig. 5) as well as the probability distribution of the velocity of moving defects in inclined layer convection beck (Fig. 6). Therefore, the derivation of the present approach from deeper microscopic or mesoscopic descriptions is an issue that with certainty deserves extra analysis. The possibility of recovering asymmetric distributions or the Beta statistics from non-extensive thermodynamics also remains as an open problem.

Acknowledgment

I am indebted to K. E. Daniels for fruitful discussions and for sending the experimental data of defect turbulence. This work was supported by CONICET, Argentina.

References

- (1) C. Tsallis, J. Stat. Phys. 52, 479 (1988).

- (2) M. Sugiyama, ed., Nonadditive Entropy and Nonextensive Statistical Mechanics, Continuum Mechanics and Thermodynamics 16 (Springer-Verlag, Heidelberg, 2004); P. Grigolini, C. Tsallis, and B. J. West, eds., Classical and Quantum Complexity and Nonextensive Thermodynamics, Chaos, Solitons and Fractals 13, Issue 3 (2002); S. Abe and Y. Okamoto, eds., Nonextensive Statistical Mechanics and its Applications, Series Lecture Notes in Physics 560 (Springer, Berlin, 2001).

- (3) C. Tsallis, Introduction to Nonextensive Statistical Mechanics, (Springer, 2009).

- (4) C. Tsallis, R.S. Mendes, and A. R. Plastino, Phys. A 261, 534 (1998).

- (5) C. Tsallis and D. J. Bukman, Phys. Rev. E 54, R2197 (1996); M. Bologna, C. Tsallis, and P. Grigolini, Phys. Rev. E 62, 2213 (2000).

- (6) D. Prato and C. Tsallis, Phys. Rev. E 60, 2398 (1999); C. Tsallis, S. V. F. Levy, A. M. C. Souza, and R. Maynard, Phys. Rev. Lett. 75, 3589 (1995).

- (7) S. Umarov, C. Tsallis, and S. Steinberg, Milan J. Math. 76, 307 (2008); A. Rodriguez, V. Schwämmle, and C. Tsallis, J. Stat. Mech.: Theory Exp. (2008), P09006; R. Hanel, S. Thurner, and C. Tsallis, Eur. Phys. J. B 72, 263 (2009).

- (8) A. A. Budini, Phys. Rev. E 86, 011109 (2012).

- (9) C. Beck, Phys. Rev. Lett. 87, 180601 (2001); EuroPhy. Lett. 57, 329 (2002); C. Beck and E. G. D. Cohen, Phys. A 322, 267 (2003); H. Touchette and C. Beck, Phys. Rev. E 71, 016131 (2005); S. Abe, C. Beck, and E. G. D. Cohen, Phys. Rev. E 76, 031102 (2007).

- (10) C. Beck, G. S. Lewis, and H. L. Swinney, Phy. Rev. E 63, 035303(R) (2001).

- (11) K. E. Daniels, C. Beck, and E. Bodenschatz, Phys. D 193, 208 (2004); K. E. Daniels, O. Brausch, W. Pesch, and E. Bodenschatz, J. Fluid Mech. 597, 261 (2008); K. E. Daniels and E. Bodenschatz, Phys. Rev. Lett. 88, 034501 (2002).

- (12) E. Lutz, Phys. Rev. A 67, 051402(R) (2003) (optical lattice); P. Douglas, S. Bergamini, and F. Renzoni, Phys. Rev. Lett. 96, 110601 (2006).

- (13) R. G. De Voe, Phys. Rev. Lett. 102, 063001 (2009).

- (14) U. M. B. Marconi and A. Puglisi, Phys. Rev. E 65, 051305 (2002); A. Baldassarri, U. M. B. Marconi, and A. Puglisi, EuroPhys. Lett. 58, 14 (2002).

- (15) B. Liu and J. Goree, Phys. Rev. Lett. 100, 055003 (2008).

- (16) A. Upadhyaya, J-P. Rieu. J. A. Glazier, and Y. Sawada, Phys. A 293, 549 (2001).

- (17) F. Caruso, A. Pluchino, V. Latora, S. Vinciguerra, and A. Rapisarda, Phys. Rev. E 75, 055101(R) (2007).

- (18) M. P. Leubner and Z. Vöros, The Astrophys. J. 618, 547 (2005); A. Esquivel and A. Lazarian, The Astrophys. J. 710, 125 (2010); A. Bernui, C. Tsallis, and T. Villela, Europhys. Lett. 78, 19001 (2007).

- (19) C. Tsallis, C. Anteneodo, L. Borland, and R. Osorio, Phys. A 324, 89 (2003).

- (20) L. Borland, Phys. Rev. Lett. 89, 098701 (2002); L. Borland and J.-P. Bouchaud, Q. Finance 4, 499 (2004).

- (21) M. Ausloos and K. Ivanova, Phys. Rev. E 68, 046122 (2003).

- (22) T. S. Biró and R. Rosenfeld, Phys. A 387, 1603 (2008).

- (23) A. Gerig, J. Vicente, and M. A. Fuentes, Phys. Rev. E 80, 065102(R) (2009).

- (24) C. Wilk and Z. Wlodarczyk, Phys. Rev. Lett. 84, 2770 (2000); C. Wilk and Z. Wlodarczyk, Phys. Lett. A 290, 55 (2001).

- (25) T. S. Biró, G. Purcsel, and K. Ürmössy, Eur. Phys. J. A 40, 325 (2009).

- (26) M. Baiesi, M. Paczuski, and A. L. Stella, Phys. Rev. Lett. 96, 051103 (2006).

- (27) V. Khachatryan et al., Phys. Rev. Lett. 105, 022002 (2010).

- (28) F. Brouers and O. Stolongo-Costa, Europhys. Lett. 62, 808 (2003);

- (29) R. M. Pickup, R. Cywinski, C. Pappas, B. Farago, and P. Fouquet, Phys. Rev. Lett. 102, 097202 (2009).

- (30) S. M. Duarte Queirós, Europhys. Lett. 71, 339 (2005).

- (31) S. M. Duarte Queirós, L. G. Moyano, J. de Souza, and C. Tsallis, Eur. Phys. J. B 55, 161 (2007).

- (32) A. A. G. Cortines, R. Riera, and C. Anteneodo, EuroPhys. Lett. 83, 30003 (2008).

- (33) W. Feller, An introduction to probability theory and applications, Vol. I & II, (John Wiley & Sons, 1967).

- (34) N. L. Johnson, S. Kotz, and N. Balakrishnan, Continuous Univariate Distributions, Vol. I & II, (John Wiley & Sons, 1995).

- (35) C. Kleiber and S. Kotz, Statistical Size Distributions in Economics and Actuarial Sciences, (John Wiley & Sons, 2003).

- (36) N. G. van Kampen, Stochastic Processes in Physics and Chemistry, (Sec. Ed., North-Holland, Amsterdam, 1992).

- (37) W. J. Thistleton, J. A. Marsh, K. Nelson, and C. Tsallis, IEEE Transaction on Information Theory 53, 4805 (2007).

- (38) R. H. Rimmer and J. P. Nolan, Math. J. 9, 776 (2005).

- (39) C. Tsallis, Phys. A 340, 1 (2004).

- (40) L.F. Burlaga and A. F. -Viñas, Phys. A 356, 375 (2005).

- (41) O. Stolongo-Costa, A. González González, and F. Brouers, arXiv: cond-mat/0505525

- (42) P. Gopikrishnan, V. Plerou, L. A. Nunes Amaral, M. Meyer, and H. E. Stanley, Phys. Rev. E 60, 5305 (1999); V. Plerou, P. Gopikrishnan, L. A. Nunes Amaral, M. Meyer, and H. E. Stanley, Phys. Rev. E 60, 6519 (1999).

- (43) See http://finance.yahoo.com

- (44) K. E. Daniels, personal communication.