Forecasting day ahead electricity spot prices:

The impact of the EXAA to other European electricity markets

Abstract

In our paper we analyze the relationship between the day-ahead electricity price of the Energy Exchange Austria (EXAA) and other day-ahead electricity prices in Europe. We focus on markets, which settle their prices after the EXAA, which enables traders to include the EXAA price into their calculations. For each market we employ econometric models to incorporate the EXAA price and compare them with their counterparts without the price of the Austrian exchange. By employing a forecasting study, we find that electricity price models can be improved when EXAA prices are considered.

keywords:

Electricity price , EXAA, AR-Model , Forecasting , European electricity markets1 Introduction

Electricity is a standardized cross-border traded commodity. Especially in Europe, where an ongoing market integration between countries proceeds rapidly, national markets cannot be considered as one isolated trading place.

Several authors have studied the relation of European electricity markets empirically within the past years. For instance, using price data of forward markets Bunn and Gianfreda, (2010) showed by analyzing cross-market interactions of some of the major European electricity markets that they are integrated. Moreover, they provide evidence for an increase in this integration over time. The German electricity market turned out to be the most integrated market. According to their study the integration is not necessarily reliant on sharing a geographical border: The Spanish and German market, for instance, seemed to transmit shocks as well. The important role of the German electricity market for other European markets was also pointed out by Bollino et al., (2013). Using cointegration techniques they find that the German electricity price embodies a price signal for the other investigated European markets, e.g. France and Italy.

Even though the hypothesis of market integration for some of the major markets seems to be satisfied (see also Bosco et al., (2010), Kalantzis and Milonas, (2010) or Houllier and de Menezes, (2012)), it is debatable if this holds true for every European market. Zachmann, (2008) as well as Huisman and Kiliç, (2013) argued that especially some of the Scandinavian electricity prices are behaving differently. This issue was also analyzed in detail by Ferkingstad et al., (2011). They were able to show that at least for the weekly time series of Nordic and German electricity prices a connection through gas prices is present.

In our paper we exploit those findings by combining them with the different specifications of the European exchanges. As the price results for the day-ahead auction of each of these markets are revealed at different points in time, even though the same trading period is considered, we use the relationship of those markets to improve common modeling approaches. As basic electricity exchange we focus on the Energy Exchange Austria (EXAA) for two reasons. First, the EXAA discloses day-ahead prices prior to most of the other European exchanges which are connected with Germany and Austria. Second, the EXAA contains a special case of price relations, where not only the same time period is traded prior to other markets but also the same market region. This holds true for the European Power Exchange (EPEX) and the EXAA, as both cover Germany and Austria. The EXAA reveals their prices approximately at 10:20 pm, whereas offers to the EPEX can be submitted until 12:00 pm. These EXAA prices are the prices for all days ahead up to the next working day, which can be e.g. three days at once for weekends. If there is a systematic relation between both markets present, traders could use the price information of the EXAA to adjust their bidding structure. This approach is applied to many European exchanges. As the EXAA covers Germany and Austria, we focus only on these European markets, which are directly connected with Germany and Austria.

The existent literature concerning the usage of the early price disclosure of the EXAA is very scarce. It was only discussed in the framework of forward risk premiums, for instance in Ronn and Wimschulte, (2009) or Erni, (2012). In these studies the EXAA price is usually regarded as an early price signal for electricity of the EPEX or European Energy Exchange (EEX) respectively. Viehmann, (2011) for instance considers the EXAA prices as a snapshot for the German and Austrian electricity price traded via over-the-counter (OTC) business. However, a direct application of the EXAA price into modeling the electricity price of other European markets has, to our knowledge, not been done so far.

Our paper closes this gap by considering the time series of EXAA electricity prices as an external regressor. Because, in an econometric modeling framework, autoregressive models turn out to be of superior model performance, we will estimate the most common basic approaches and compare them with their counterparts when the EXAA electricity price is used as influencing variable.

Therefore we organized our paper as follows. In section 2 we will describe the different data sets and exchange specifications. Moreover, we will provide information about the necessary data arrangement for using the EXAA price as a regressor. The subsequent section will then introduce the econometric models which are applied to our data set. In section 4 we will employ a comprehensive forecasting study for every examined market place. Section 5 discusses our findings and analyses the temporal structure of the relationship. We will focus on short term forecasting of one day ahead. The last section summarizes our results and grants insights for future research.

Throughout the whole paper we will use bold symbols for multivariate expressions and normal symbols for univariate objects.

2 The considered electricity markets

In order to measure the impacts of the EXAA day-ahead price on other electricity exchanges, it is mandatory to determine a feasible set of these exchanges. In our case we decided to use exchanges, which are directly connected with Germany and Austria, as the EXAA covers both countries. According to the transparency platform of the European Network of Transmission System Operators for Electricity (ENTSOE) there are 10 different countries with a cross border physical flow to either Germany or Austria. These are Switzerland, Czech Republic, Denmark, France, Hungary, Italy, Netherlands, Poland, Slovenia and Sweden. Denmark operates two different interconnectors with such a cross-border physical flow to the investigated region. This specifically means that we ignore countries like Belgium or Slovakia that are geographically connected to Germany and Austria, but have no cross border physical flow. To each country and interconnector there can be a specific spot market price of electricity assigned. As the German electricity price is traded at two different exchanges, there are 12 different possible electricity price time series in consideration.

However, it is arguable that also indirectly connected markets may be affected by the EXAA. This would also coincide with the findings of Bunn and Gianfreda, (2010). But analyzing every indirectly related market would lead in a tremendously big study. One could even think of the Russian electricity market being affected by the EXAA – there would simply be almost no end to markets in focus. Therefore we decided to employ a criterion which, in our opinion, is intuitive and comprehensible and also grants a manageable size of markets to consider. Using the direct connection in terms of an interconnector fulfills these goals very well. Despite that fact we also analyzed the electricity price data of Spain, Norway and Belgium exemplarily, but the effects were not significant. We also avoided specifically the Nordpool spot price as it is only a reference price that is computed from several Scandinavian prices, like Danish, Swedish and Norway etc. and therefore not traded directly.

In order to use the information of the EXAA price disclosure as a snapshot for the market, it is mandatory to filter out those electricity markets, which allow for order submission post to the EXAA price results.

The set of investigated countries is shown in Table 1. It presents an overview about the name of the exchange, the used abbreviation within this paper, the latest submission time point, the time point of price results and the data source for the information gathered on these exchanges, including the time series of prices. Information in brackets corresponds to the name of a specific price zone of the region. Except for Poland they are chosen to represent the special zone which is directly connected with Germany and Austria. The two exchanges beneath the double horizontal line represent those markets, which are connected to Germany and Austria but did not meet our second criterion, as they did not allow for order submission post to the price disclosure of the EXAA.

Figure 1 illustrates those markets and provides additional information on the connection between the regions. Such a connection is depicted as a link between two bubbles. Any colored bubble represents a region which was finally included after the filtering described above. Hence, our dataset contains 10 different time series, for which we will utilize a possible relationship with the EXAA.

| Exchange | Region | Abbreviation | Sub. | Res. | Data source |

| EXAA | Germany&Austria | EXAA.DE&AT | 10:12 | 10:20 | exaa.at |

| EPEX | Germany&Austria | EPEX.DE&AT | 12:00 | 12:42 | epexspot.com |

| EPEX | Switzerland | EPEX.CHE | 11:00 | 11:10 | epexspot.com |

| EPEX | France | EPEX.FR | 12:00 | 12:42 | epexspot.com |

| APX | Netherlands | APX.NL | 12:00 | 12:55 | apxgroup.com |

| Nordpool | Denmark (West) | NP.DK.West | 12:00 | 12:42 | nordpoolspot.com |

| Nordpool | Denmark (East) | NP.DK.East | 12:00 | 12:42 | nordpoolspot.com |

| Nordpool | Sweden (4) | NP.SW4 | 12:00 | 12:42 | nordpoolspot.com |

| POLPX | Poland (Auction I) | POLPX.PL | 10:30 | 10:35 | tge.pl |

| OTE | Czech Republic | OTE.CZ | 11:00 | 11:30 | ote-cr.cz |

| HUPX | Hungary | HUPX.HU | 11:00 | 11:30 | hupx.hu |

| GME | Italy (Nord) | GME.ITN | 9:15 | 10:45 | mercatoelettrico.org |

| BSP | Slovenia | BSP.SL | 9:40 | 10:30 | bsp-southpool.com |

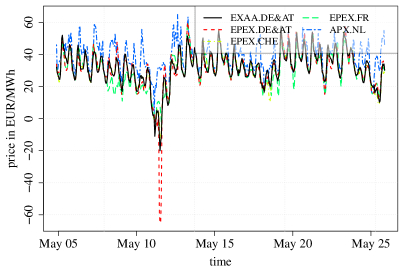

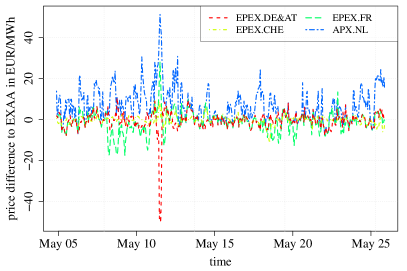

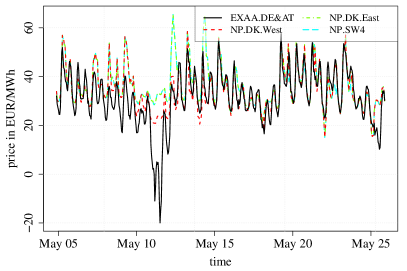

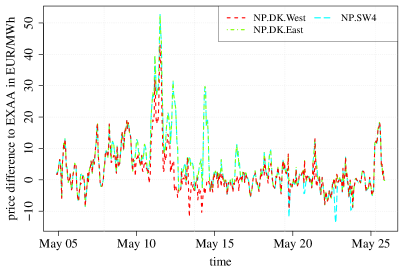

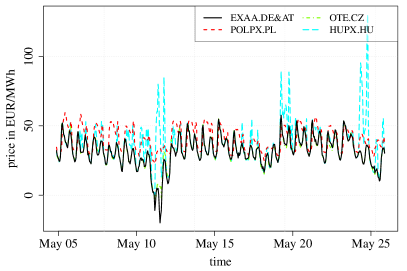

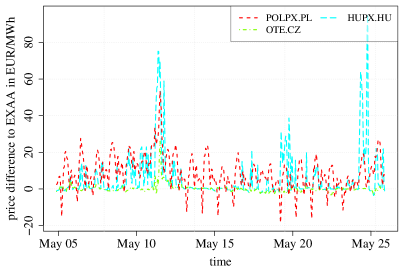

The time series of the investigated electricity prices for an exemplary time horizon in May 2014 can be obtained from Figure 2. As a first impression of the behavior of the time series, it shows that some of the prices exhibit similar patterns and price levels, e.g. EPEX (France) and EXAA, whereas others seem not to have a visible relationship, e.g. POLPX and EXAA. The right-hand side of the figure displays explicitly the differences between the EXAA and the other time series. It can be seen that they often follow a recurring structure, which seems to be most dominant for the EXAA and POLPX difference. Our whole dataset contains the hourly day-ahead electricity spot prices, which were downloaded from the websites of the different exchanges for the time period of the 15.08.2007-12.08.2014. In order to guarantee comparability some minor adjustments had to be done.

In case of the EXAA, data for the 13.11.2012 is not available, as one day before the data processing center suffered from a blackout and therefore no trading took place. To prevent excluding this day from our other time series, we decided to replace the prices of the 13.11.2012 with the prices of the previous week.

Moreover, for the HUPX and the Nordpool region Sweden (4) prices were not available for every day of the whole time period. Hence, we were only able to apply our methodology to their individual available time horizons, which is the 01.01.2012-12.08.2014 for the HUPX and the 01.11.2011-12.08.2014 for Nordpool Sweden (4).

Polish electricity was mainly traded at three different auctions throughout the day during our chosen time period. As most of the trading, measured in trading volume, takes place at the first auction, we chose to use only the prices of auction I for our modeling approach. Nevertheless, some days are missing within the time series. Those are the 18.03.2011 and the 02.03.2014. The hour values of the 08.01.2008 00:00, 15.02.2008 07:00, 01.04.2008 03:00 and 29.03.2009 01:00 were also missing. Analogous to the missing values of the EXAA, we replaced them with their counterparts 168 hours ago.

Finally all electricity markets except the POLPX trade in EUR or publish the reference price in EUR. We use the end-of-day Euro-Złoty (EUR/PLN) exchange rate of the trading days to make the Polish data comparable to EUR based data.

Besides the classical approach which uses historical data, we utilize the data of the EXAA for the next day that is available at 10:25 (CET), prior to the submission time point of the other electricity markets. As the EXAA has hourly data this corresponds usually to 24 observations, but when there is a time shift due to the daylight saving time we have once a year 23 observations in March and 25 observations in October. We denote other electricity markets as . represents the electricity price of market at time . Moreover, we assume that the hourly price is observable. In addition we define that is the day that corresponds to the time . So is the first observed day, the last one and that one which we want to predict. Given a day we can denote as the number of hours that are traded on the corresponding day. As mentioned above, is usually 24 and sometimes 23 or 25. For every market at day the observable set of prices of the EXAA market is , as there are additional observations available. Further, we denote as a two-dimensional process. Our focus of interest is now the series of , especially the values which we will forecast using the EXAA prices.

3 Models for electricity prices

In the following we present several models for . These models are easily structured and based on two very common modeling approaches. They are the persistent or naïve model and the autoregressive process of order - AR(). Especially the AR() modeling approach is considered as fundamental for an econometric analysis of electricity prices. The process itself or slightly modified versions of it are very often used in the literature, for instance in Weron and Misiorek, (2008), Ferkingstad et al., (2011) or Kristiansen, (2012). The persistent and the AR() also serve as benchmark models, for instance in Serinaldi, (2011) and Ziel et al., (2015). Furthermore, every stationary and invertible ARMA(, ) process can be well approximated as an high order AR process, as we can rewrite ARMA(, ) as AR() with exponential fast decaying memory, see e.g. Hamilton, (1994). ARMA type models are very popular for electricity price modeling, see e.g. Hickey et al., (2012) or Liu and Shi, (2013). The relationship holds true also for seasonal ARMA processes, as every seasonal ARMA process is a special ARMA(, ) process, this includes double and triple seasonal ARMA models as used in Taylor, (2010). However, the mentioned seasonal ARMA models are different to those ARMA models with a seperate modelling of seasonal trends as e.g. used by Koopman et al., (2007) or Keles et al., (2013). Such ARMA type models can not necessarily be well approximated by an AR().

Below we denote by the univariate and by the multivariate error term of the considered univariate or multivariate model. We assume that the error terms have zero mean with constant and finite variance resp. covariance matrix. Of course, the assumption of homoscedasticity is not satisfied, as there is a seasonal structure in the data that also effects the (conditional) variance of the error term. However, for simplicity reasons we assume homoscedasticity.

To point out the effect of the EXAA towards the other electricity markets, we estimate both models in their standard fashion and extend them afterwards by considering the EXAA price in various ways. By providing a comprehensive forecasting study we can test, whether the basic model is significantly outperformed by its counterpart with the EXAA.

3.1 Persistent model

The first basic model we introduce is the very simple and fast to estimate persistent, or naïve model, where the electricity price is estimated to be the same as 168 hours ago, which represents usually one week. It is given by and can be estimated by for .

3.2 Univariate AR()

The second basic model is the well-known autoregressive process of order (AR()), which usually provides a high goodness-of-fit and is also estimated in a very short time.

It is given by

| (1) |

with as mean of the time series and coefficients for . For the estimation procedure there are several options available, like the estimation by solving the Yule-Walker equations, (conditional) least squares estimation, or (conditional) likelihood estimation. We estimate the AR() process by solving the Yule-Walker equations which guarantees a stationary solution, for more details see e.g. Hamilton, (1994). The mean is estimated by the sample mean in advance.

The order of the model is selected via an information criterion. This is also a very common approach in the literature, see for instance Karakatsani and Bunn, (2008) or Liebl, (2013). We perform the selection of by minimizing the Akaike information criterion (AIC) which is given by with as estimated mean square error. Other criteria like the Bayesian information criterion (BIC) could be a reasonable choice, too. To carry out the selection procedure we decide on a maximal possible model order . Starting with , we estimate the model, calculate the AIC, increase by 1 and repeat this procedure until is reached. The model with the minimal AIC is then declared as the final model. The upper bound is chosen to be 1400. This is large enough so that all chosen values for are at least one week, e.g. 168 hours, smaller than . Note, that the estimated order is usually larger than .

Forecasting can be done iteratively by for where for .

3.3 Persistent EXAA based model

This model is the EXAA type equivalent of the persistent model. Here we simply assume that the electricity price on market is the same as the EXAA price. Because the EXAA price is settled at an earlier point in time, the price for the corresponding hour is observable. Hence, the persistent EXAA based model is given by and can be estimated by for .

3.4 2-dimensional AR()

Similarly to the univariate AR approach discussed above we can model the two dimensional , which contains both, the EXAA price and the time series of the investigated exchange.

We estimate the AR() process by solving the multivariate Yule-Walker equations and determine using the AIC strategy as described above, where .

For the forecasting we can now exploit the fact that is already observed for . Thus the forecast is given by where for with as second row of and for . Henceforth only the second autoregressive equation that models is required to be estimated, as we want to forecast only one day.

3.5 Modified 2-dimensional AR()

In the multivariate AR() model above the observed EXAA values for were only considered in the forecasting in order to replace the estimates by its true value . Hence, we can adjust the model so that this information is also directly used in the model estimation procedure. We denote by the two dimensional process that contains the price for at time in the second component and the price for EXAA one day ahead in the first component. Then the bivariate autoregressive model for is given by

In this case the forecasting is as simple as in the univariate case. It is iteratively done with for where for .

We want to highlight that both modelling two-dimensional approaches are different, as the additional information is used in another way. In the first approach the forecast is independent of the observed EXAA information for future hours, whereas for the second approach it substantially matters. There can depend on , but also on observed information for . For the forecasting, the maximum amount of considered deterministic future EXAA hour values for the first forecasted hour is 23, for the second 22 and so on.

3.6 Difference based AR()

The last two models are based on the difference of the target price to the EXAA electricity price . Hence we define . If would be an i.i.d. noise then the persistent EXAA based estimator would be a reasonable choice and modeling the difference would not lead to any improvement in the price prediction. However, if there is some correlation structure left, the assumption that follows an AR() seems to be reasonable. Therefore, we assume that

| (2) |

holds true for some lags , where represents the mean of the differences. As in the univariate case we use the Yule-Walker equations with the AIC for estimation, where we choose .

Indeed, (2) can be rewritten as

which shows that this is in fact a special case of an error correction model. So this is basically a special case of the 2-dimensional AR() on considered above.

The forecast of (2) is done iteratively by for where for , for , and for . Forecasts further than one day-ahead can not be covered directly by this model, as we have to specify a model for to plug-in the corresponding estimates.

3.7 Model summary

A summary table of all considered models with the most relevant information is given in Table 2. In the following sections we will refer to the models as presented in the abbreviation column of this table.

| Model | Abbreviation | Uses EXAA information | |

|---|---|---|---|

| persistent model | naïve | no | - |

| univariate AR() | AR() | no | 1400 |

| persistent EXAA based model | naïve-EXAA | yes | - |

| 2-dimensional AR() on | 2d-AR() | yes | 700 |

| 2-dimensional AR() on | 2d-() | yes | 700 |

| univariate AR() on differences | -AR() | yes | 1400 |

4 Setup of the forecasting study

For evaluating the forecasting performance and the desired impact of the EXAA price we carry out a forecasting study. We face the situation that we sometimes have to forecast 23 or 25 prices instead of 24, which complicates the notation and forecasting. Nevertheless, the occurence of such specific days is considered within the analysis. As mentioned previously the available data covers days which is about 7 years.

In the forecasting study we use a rolling window of hourly data of length with as rolling index shift. The length of the considered sample is days which corresponds to an in-sample period of usually 2 years. Hence, for the amount of used observations we have with and for . This expression is usually about . Given the 2 years of data we do the estimation procedure on the given window. As introduced above we shift the window by for with 111The forecasting range contains one leap year (2012) days. Therefore covers the remaining years of observations minus one day. In detail we have and for . In the latter formula we usually have .

After the estimation on a given window we do the forecast of the next day traded values of the electricity time series of interest. Remember that is the amount of traded hours of the proceeding day, it is in general 24, but sometimes 23 or 25. In order to compare our forecasts we compute the mean absolute error (MAE) and the root mean square error (RMSE) of all forecasted values. They are given by

5 Results and Discussion

All results are based on out-of-sample data. The estimated MAE and RMSE are given in Table 3. Every bold print number corresponds to the best model in terms of MAE or RMSE. An underlined value represents a model, which produced a MAE or RMSE which was at least in the confidence interval of the best model. The number in brackets shows the standard deviation, which was estimated via bootstrapping with a sample size of . First of all we can observe that the standard deviations of the MAE values are smaller in comparison to the RMSE ones. Thus, their results seem to be more reliable. The reason is likely that most of the electricity prices are heavy tailed which also affects the model residuals. Hence, squaring the residuals as done in the calculation of the RMSE halves the corresponding tail index. This automatically leads to more unreliable results. Considering the MAE values we see that for all neighboring price regions there is at least one model which involves the EXAA information and is superior to the naïve and AR() model without EXAA information. Taking into account the 2-sigma range we can obtain that the performances are significantly better, except for the case of Sweden. Hence based on the the MAE we can improve the forecasting results taking into account the EXAA information. An interesting feature is that for the EPEX.DE&AT price the naïve-EXAA model seems to be significantly better than the other complex AR type models that involve EXAA information. As both, the EPEX.DE&AT price such as the EXAA.DE&AT price, consider the same region this result may give an indication that the market efficiently prices the information observed at the EXAA. The relationship between both prices seem not to exhibit recognizable autoregressive patterns, and therefore could not be exploited for an investment strategy. However, this holds only true for our investigated type of AR model. The naïve-EXAA model is also superior for the OTE.CZ price, which covers the delivery region of Czech. This indicates that the markets seem to have a strong relationship.

The results considering the RMSE are basically similar. Nevertheless, the higher confidence regions due to high standard deviations make an interpretation more unstable.

In addition we define hourly versions of the MAE and RMSE to compare the forecasting performance at a specific hour of a day. The and are given by

with for . Note that the expression is the number of forecasts that correspond to hour . For this is simply , whereas for it is a lower amount due to the clock change in March. For this value is not really of interest as it contains only a very few October observations, also due to clock change. The and are visualized for all markets and models and hours in Figures 4 and 5 in the Appendix. The figures show clearly, that the evening to night hours from approximately 20:00 to 06:00 face a smaller forecasting error than, for instance, the hours around midday. Comparing both figures the before mentioned issue with the RMSE becomes visible. Due to heavy outliers especially during the midday hours the RMSE is often 10 times higher than at the other hours of the day. This complicates the interpretation of RMSE types of errors, which analyze the 24 hour forecast as a whole. Moreover, it can be obtained, that at least one of the EXAA related models seem to outperform all basic models for each time series in terms of hourly MAE.

| MAE | ||||||

|---|---|---|---|---|---|---|

| naïve | AR() | naïve-EXAA | 2d-AR() | 2d-() | -AR() | |

| EPEX.DE&AT | 8.273(0.056) | 5.980(0.037) | 3.835(0.029) | 4.597(0.032) | 4.021(0.030) | 3.899(0.028) |

| EPEX.CHE | 7.839(0.046) | 5.232(0.030) | 6.990(0.046) | 4.676(0.026) | 4.166(0.025) | 4.209(0.025) |

| EPEX.FR | 9.738(0.230) | 8.915(0.157) | 6.887(0.155) | 8.054(0.152) | 7.908(0.156) | 6.178(0.148) |

| APX.NL | 6.498(0.033) | 4.801(0.023) | 6.809(0.039) | 4.266(0.020) | 3.935(0.020) | 4.540(0.023) |

| NP.DK.West | 8.076(0.141) | 6.281(0.101) | 7.140(0.103) | 5.624(0.099) | 5.358(0.099) | 5.850(0.101) |

| NP.DK.East | 9.669(0.160) | 8.120(0.121) | 8.652(0.124) | 7.267(0.118) | 7.158(0.115) | 7.526(0.124) |

| NP.SW4 | 6.974(0.139) | 5.226(0.101) | 11.562(0.110) | 5.151(0.103) | 5.147(0.102) | 6.822(0.102) |

| POLPX.PL | 3.421(0.026) | 2.459(0.016) | 8.157(0.039) | 2.223(0.015) | 2.246(0.016) | 4.348(0.021) |

| OTE.CZ | 7.554(0.042) | 5.338(0.027) | 2.707(0.022) | 4.135(0.022) | 2.852(0.019) | 2.738(0.018) |

| HUPX.HU | 10.159(0.160) | 8.030(0.119) | 7.012(0.146) | 7.174(0.109) | 6.717(0.111) | 6.579(0.115) |

| RMSE | ||||||

|---|---|---|---|---|---|---|

| naïve | AR() | naïve-EXAA | 2d-AR() | 2d-() | -AR() | |

| EPEX.DE&AT | 14.221(0.395) | 9.659(0.340) | 7.299(0.452) | 7.965(0.418) | 7.323(0.445) | 7.090(0.436) |

| EPEX.CHE | 12.607(0.157) | 8.125(0.132) | 11.644(0.102) | 7.279(0.131) | 6.693(0.125) | 6.788(0.108) |

| EPEX.FR | 46.848(6.662) | 34.051(6.092) | 33.107(6.258) | 33.187(6.106) | 33.144(6.153) | 32.377(6.196) |

| APX.NL | 9.516(0.101) | 6.878(0.086) | 10.768(0.073) | 6.100(0.087) | 5.724(0.090) | 6.701(0.080) |

| NP.DK.West | 31.342(4.111) | 22.357(3.948) | 22.875(4.135) | 21.799(4.190) | 21.688(4.232) | 21.889(4.285) |

| NP.DK.East | 36.254(2.779) | 27.378(2.825) | 27.667(2.828) | 26.136(2.935) | 25.992(2.841) | 26.633(2.864) |

| NP.SW4 | 30.167(2.397) | 22.467(2.223) | 26.005(2.018) | 21.731(2.408) | 21.657(2.400) | 22.763(2.191) |

| POLPX.PL | 6.522(0.110) | 4.286(0.075) | 11.377(0.082) | 3.934(0.085) | 3.969(0.084) | 6.293(0.051) |

| OTE.CZ | 11.526(0.131) | 7.745(0.077) | 5.197(0.127) | 6.221(0.087) | 4.832(0.104) | 4.736(0.102) |

| HUPX.HU | 15.624(0.346) | 11.830(0.256) | 13.018(0.320) | 10.837(0.267) | 10.462(0.289) | 10.467(0.299) |

Additionally we conduct the popular Diebold-Mariano (DM) test to compare the forecasting performance, as done for instance in Hong and Wu, (2012), Bordignon et al., (2013) and Nan et al., (2014). For a recent discussion to the use and abuse of the test see Diebold, (2012).

The DM-test is based on evaluating loss differences of the forecasting errors of two different models. Given the forecasting errors this loss differential for two models and is commonly given by . Often this test is carried out by using squared residuals with . In our situation it turned out to provide unreliable results, as the residuals seem to be to heavy tailed. Instead we consider the case of absolute residuals with which corresponds to the MAE case.

One crucial assumption on the DM-test is that exhibits a homoscedastic and covariance-stationary process. If we would perform the DM-test on all loss differences for the assumptions of the test must be violated if the underlying process has some linear autoregressive structure that is non-zero. The reason is that two consecutive forecast errors, e.g. and , have different variances as the estimate for is based on the estimate for . The variance for increases with the forecasting horizon.

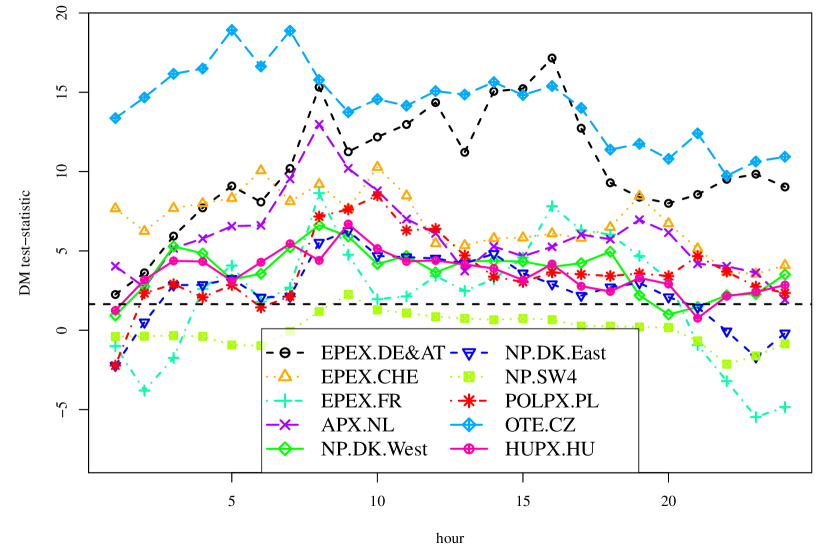

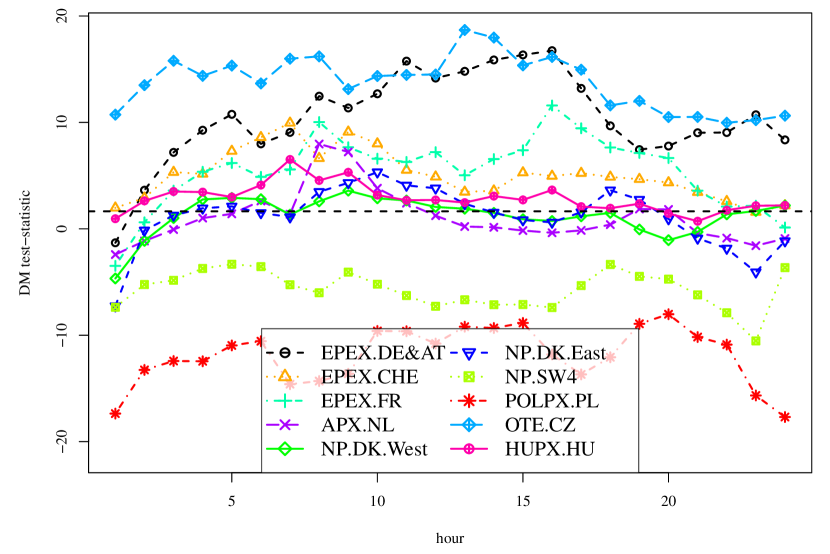

However, if we compare only forecasts that correspond to a specific hour the Diebold-Mariano assumption might be satisfied. Hence, we conduct the DM-test for all prices and hours (except the 25th) to compare all four proposed models that contain EXAA information against the AR() process which does not include the information. We consider only the AR() as the MAE and RMSE values suggested that it is the best model considered that does not use the EXAA information. As mentioned above must be a covariance-stationary process. To estimate the order of covariance-stationary we estimate an AR() process for the differential loss series as well and select the order of the best model concerning the AIC. In our application the optimal order is often chosen to be 7 or 14 which corresponds to weekly cycles.

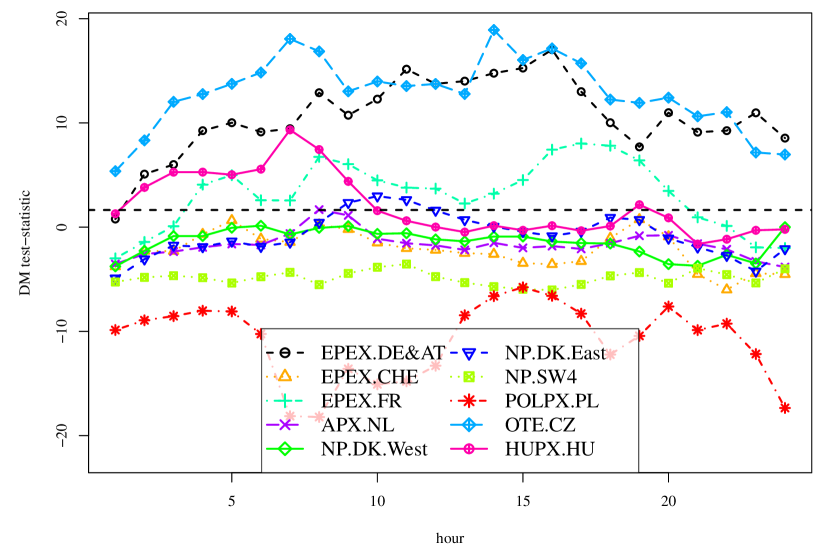

The resulting test statistics for the conducted tests are given in Figure 3. A higher DM test-statistic corresponds to a higher model error of the AR() in comparison to the EXAA-based model. All values above the dashed 95% confidence line indicate that the EXAA-based model provides significantly better forecasts for this specific hour than the AR(). Interestingly the DM-test results are in strong accordance with the conclusions drawn from the analysis of the MAE. So except for Sweden there is at least one model that contains the EXAA information that is significantly superior to the AR() in the majority of hours. The significance turns out to be very high especially for the German-Austrian EPEX price and the Czech OTE.CZ price. In accordance to our MAE study there is no model which dominates every other model for every hour. Regarding the hourly test statistics over the day it is difficult to establish any clear pattern. But In general we observe that the significance of the first hours, especially the first one is relatively small. The reason is that for this hour the AR() performs relatively well, as can be obtained from Figure 4 in the Appendix. Moreover, we can see that for the EPEX prices of Germany and Austria, Switzerland and France it seems that the significants is clearer during the hours from about 5am to 8pm.

5.1 Temporal Structure Analysis

Moreover, we want to analyze the temporal structure of the impact of the EXAA. In detail we want to discuss the daily, monthly and annual seasonal dependence of the impact. The latter might give hints for the progress of the European electricity market integration. However, a temporal structure analysis has to be interpreted carefully, as all of our assumed models have constant dependence structure over time, especially no seasonal variation in the parameters. Hence we restrict ourselves only on evaluating point estimates to get indication for the direction of the behavior. We omit uncertainty measures like confidence intervals as they might not be valid.

As the previous study showed, the MAE provides more robust results. Therefore, we perform the temporal structure evaluation only for the absolute residuals

where is the set of time partitions, is the set of all time points of partition and gives the number of elements of . For the monthly partition we use the twelve months of a year, for the daily we use the 7 weekdays and for the annual partition we divide our 5 year out-of-sample range into 5 equidistant time groups, each about a year. All computed -values are given in Figures 6, 7 and 8 in the appendix. Please keep in mind that for the HUPX we did not have the same data period as for the other markets.

Regarding the curves of the of the monthly seasonality which are presented in Figure 6, we can observe that in general the absolute forecasting error is less over the summer than over the winter. This is a commonly observed phenomenon, which can be mainly explained by the usually higher amount of holidays during winter time and the increasing uncertainty over the renewable energy, especially wind energy, due to more intense weather conditions. Both events tend to create price movements which are more difficult to forecast.

Concerning the impact of EXAA to the other markets it is hard to make general statements. In most cases the superiority of an EXAA-related model over a univariate model seems to maintain over the months. However, for the EPEX Switzerland price we observe that from October to March there is almost no difference between the univariate AR process that required no EXAA information to the processes that require EXAA information. Only in the winter months, where forecasting performance in general lacks accuracy, the EXAA inclusion leads to better results. As we have shown above, the EXAA based models for the Swiss price were significantly better than the models without EXAA information. So we can conclude that this significance is mainly driven by a better performance over the summer. We also observe tremendously high peaks, e.g. in France or Denmark West. But a closer look into the data showed, that they are all due to heavy outliers within a specific month.

For the daily behavior as presented in Figure 7 we observe no clear behavior that seems to hold true for every country. In some countries the weekend are easier to predict or benefit more from the impact of the EXAA than working days from Monday to Friday, but in some countries this does not hold. In most cases the superiority of an EXAA based model towards univariate model seem to maintain over the days. Only for Sweden 4 it seems that the univariate model sometimes leads to better results for some of the days, but the difference is typically very small. This uncertainty about whether the EXAA inclusion does provide better forecasting results for this market goes along with our previous findings. For the German and Austrian EPEX price we see that the absolute forecasting error is the largest on Sunday and Monday. The improvement from the naïve EXXA-model to the univariate AR() seem to be quite stable through the days. This is remarkable if we have the fact in mind, that at EXAA there are auctions only on working days, whereas the EPEX day-ahead market auction is every day.

The last temporal structure concerns the variation of the process over the years, as can be seen in figure 8. If the markets become more and more integrated we would expect that the difference of absolute forecasting error of the univariate model in comparison to an EXAA-based model becomes relatively larger over time. Also, on average, the forecasting performance of EXAA-based model should increase, leading to lower MAE over time. In fact we observe for some countries that the absolute forecasting error decreases as expected. This seems most clear for France, Denmark East, Sweden and Czech Republic. Interestingly for the Netherlands and Denmark West this seems to be the inverse. It seems as if they are become less integrated with respect to the EXAA. We only have supposition for this observation. For the APX Netherlands the reason might be that the Netherlands integrates more towards the APX UK market, which results in a lower coupling to the EXAA price.

Furthermore, we can observe that for some countries, most clearly for the Netherlands the difference between the MAE of the AR() and the best model with EXAA-impact is decreasing. So in general it seems that the impact of the EXAA is reduced over time. In contrast for the German and Austrian EPEX price and the Czech price we observe the opposite. Interestingly, these are the both markets where the naïve EXXA-model performed best. So on markets that behave very similar to the EXAA the impact of the EXAA seems to be increased over the years of our study.

5.2 Implication for Market Participants

Our results provide implications for several decision makers in the field of electricity trading. First and foremost every active participant of an exchange can consider the market results of connected exchanges as early price information of their own exchange. If their trading strategy is at least partly based on an econometric approach, including these prices will yield a decreased uncertainty about upcoming day-ahead prices. In the special case of Germany and Austria, where the EXAA and the EPEX cover the same regions, investors seem to get a very accurate early snapshot of the market and can therefore conduct valuable adjustments of their investment strategy. As using the early price settlement of exchanges is often accompanied by becoming an active member of this exchange, exchange companies could also utilize our results. If they decide to set their price settlement time point before the price submission of relevant connected exchanges, they may encourage participants of these exchanges to become a member, simply to get access to this early price information. Lastly, our findings provide also implications for portfolio managers of electricity companies mainly in Germany and Austria. Analyzing the price patterns of both, the EXAA and EPEX exchange, may lead to an optimal distribution of trading among these two exchanges. Orders, which were not settled at the EXAA, can be placed again at the EPEX – adjusted by the updated price information coming from the EXAA settlement.

6 Conclusion

We investigated several models to show the impact of the EXAA day-ahead price on electricity day-ahead spot prices of regions, which are directly connected to Germany and Austria. To conduct our study we introduced a unique investigation setting, where traders can utilize different price settlement time points of exchanges to get a snapshot of other markets. By analyzing different error metrics and test setups we were also able to provide insights in the relatedness of those markets. It turned out that including the EXAA information in standard and robust time series approaches increased the performance of those models for every examined market. In some cases, e.g. APX Netherlands or EPEX France, considering the early EXAA information resulted in a vast improvement.

Interestingly, the naïve EXAA model, which simply uses the price of the EXAA as predictor, turned out to be the best model for the EPEX Germany and Austria as well as the OTE Czech Republic. This in turn means that common and robust autoregression techniques for this relationship were not able to filter out additional information in the price relation of the EXAA and those exchanges. Especially in the case of the EXAA and the EPEX, which both trade for the same region, this may provide evidence for the reasoning of (Viehmann,, 2011), who considered the EXAA price as an approximation for the OTC prices for Germany and Austria.

Our findings provide important implications for traders and decision makers of electricity exchanges. Utilizing the EXAA price disclosure as an early price information for the upcoming prices of the EPEX will lead to a vast improvement of forecasting accuracy. Electricity companies which are also engaged in trading should therefore always incorporate the EXAA price, if they decide to make predictions for the EPEX price. If properly implemented, the EXAA price can also be exploited by market participants of other exchanges, even though they may not trade for the same region. Meeting the requirement of connected markets is enough to improve the trading strategy by using the EXAA price.

An analysis of the temporal structure of the relationship revealed that the impact of the EXAA towards other markets develops over the years. For some markets, e.g. the Czech Republic, it seems that the relationship becomes stronger, whereas e.g. for the APX Netherlands it becomes weaker. We also observe that for some markets, like Switzerland, the improvement in forecasting accuracy is only very high at some months of the year. An analysis of the daily structure revealed that the improvement by using EXAA-related models is relatively stable across all weekdays and for most of the markets.

Nevertheless, this paper still may function as an early introduction in a new perspective on the investigation of related markets. For our analysis we used very basic but robust modeling approaches for every time series. As explained in detail in section 3, our autoregressive modeling setup nests many models frequently used in the literature. However, we explicitly avoided higher tier models like seasonal ARIMA models, models with heteroscedasticity or models with regressors in general. This helped us to focus on the analysis of the relationship of the market prices but may also have biased our results, as those extended model may negate the improvement of forecasting we have found using EXAA-based approaches.

Therefore we still leave several issues for future research.

One feature that was not taken into account are the trading days of the spot markets. All considers electricity spot markets trade every day except the EXAA. The EXAA trades only on working days and not on weekends and Austrian public holidays. Therefore on a Friday of a common week there will be traded three days, Saturday, Sunday and Monday. Having this fact in mind it is even more remarkable that the EXAA results are that impressive. Hence, further modeling approaches could also investigate the trading days, so that the flow of information can be captured better.

Our analysis of the temporal structure of the relationship also gives clear indication for the usage of change points within the time series. Estimating and modeling those change points will very likely result in an overall better forecasting performance, as the markets have obviously changed over the past years. Such change points may also account for the fact that the performance of all models typically suffers during the winter months. The detection of such change points could be driven by real events like milestones in the ongoing coupling of electricity markets in Europe or statistical techniques.

Further research could also go into the direction of constructing a cascade model. As the Table 1 suggests we can push forward the idea of using certain available information. So we could e.g. incorporate the EXAA information to estimate the POLPX price, then using the POLPX and EXAA price to forecast the Czech, Hungary and Swiss electricity price. All these prices could be used to forecast all the other ones that trade later on. This cascade type model can be extend to a complex net of electricity prices for even greater regions.

Obviously, another room for improvement lays in the types of models we used. We could therefore extend the models to more complex ones. One way in this sense could be to take into account non-linearities, interactions or other regressors such as load, renewable energy feed-in, etc. Another way to improve the models could be the relaxation of some of our assumptions, e.g. allowing the variance to vary periodically over time.

7 References

References

- Bollino et al., (2013) Bollino, C. A., Ciferri, D., and Polinori, P. (2013). Integration and convergence in european electricity markets. Available at SSRN 2227541.

- Bordignon et al., (2013) Bordignon, S., Bunn, D. W., Lisi, F., and Nan, F. (2013). Combining day-ahead forecasts for British electricity prices. Energy Economics, 35(0):88–103.

- Bosco et al., (2010) Bosco, B., Parisio, L., Pelagatti, M., and Baldi, F. (2010). Long-run relations in european electricity prices. Journal of applied econometrics, 25(5):805–832.

- Bunn and Gianfreda, (2010) Bunn, D. W. and Gianfreda, A. (2010). Integration and shock transmissions across european electricity forward markets. Energy Economics, 32(2):278–291.

- Diebold, (2012) Diebold, F. X. (2012). Comparing predictive accuracy, twenty years later: A personal perspective on the use and abuse of diebold-mariano tests. Technical report, National Bureau of Economic Research.

- Erni, (2012) Erni, D. (2012). Day-Ahead Electricity Spot Prices-Fundamental Modelling and the Role of Expected Wind Electricity Infeed at the European Energy Exchange. PhD thesis, University of St. Gallen.

- Ferkingstad et al., (2011) Ferkingstad, E., Løland, A., and Wilhelmsen, M. (2011). Causal modeling and inference for electricity markets. Energy Economics, 33(3):404–412.

- Hamilton, (1994) Hamilton, J. D. (1994). Time series analysis, volume 2. Princeton university press Princeton.

- Hickey et al., (2012) Hickey, E., Loomis, D. G., and Mohammadi, H. (2012). Forecasting hourly electricity prices using armax–garch models: An application to miso hubs. Energy Economics, 34(1):307–315.

- Hong and Wu, (2012) Hong, Y.-Y. and Wu, C.-P. (2012). Day-ahead electricity price forecasting using a hybrid principal component analysis network. Energies, 5(11):4711–4725.

- Houllier and de Menezes, (2012) Houllier, M. A. and de Menezes, L. M. (2012). A fractional cointegration analysis of european electricity spot prices. In European Energy Market (EEM), 2012 9th International Conference on the European Energy Market, pages 1–6. IEEE.

- Huisman and Kiliç, (2013) Huisman, R. and Kiliç, M. (2013). A history of european electricity day-ahead prices. Applied Economics, 45(18):2683–2693.

- Kalantzis and Milonas, (2010) Kalantzis, F. and Milonas, N. T. (2010). Market integration and price dispersion in the european electricity market. In European Energy Market (EEM), 2010 7th International Conference on the European Energy Market, pages 1–6. IEEE.

- Karakatsani and Bunn, (2008) Karakatsani, N. V. and Bunn, D. W. (2008). Forecasting electricity prices: The impact of fundamentals and time-varying coefficients. International Journal of Forecasting, 24(4):764–785.

- Keles et al., (2013) Keles, D., Genoese, M., Möst, D., Ortlieb, S., and Fichtner, W. (2013). A combined modeling approach for wind power feed-in and electricity spot prices. Energy Policy, 59(0):213–225.

- Koopman et al., (2007) Koopman, S. J., Ooms, M., and Carnero, M. A. (2007). Periodic seasonal Reg-ARFIMA–GARCH models for daily electricity spot prices. Journal of the American Statistical Association, 102(477):16–27.

- Kristiansen, (2012) Kristiansen, T. (2012). Forecasting Nord Pool day-ahead prices with an autoregressive model. Energy Policy, 49(0):328–332.

- Liebl, (2013) Liebl, D. (2013). Modeling and forecasting electricity spot prices: A functional data perspective. The Annals of Applied Statistics, 7(3):1562–1592.

- Liu and Shi, (2013) Liu, H. and Shi, J. (2013). Applying ARMA–GARCH approaches to forecasting short-term electricity prices. Energy Economics, 37(0):152–166.

- Nan et al., (2014) Nan, F., Bordignon, S., Bunn, D. W., and Lisi, F. (2014). The forecasting accuracy of electricity price formation models. International Journal of Energy and Statistics, 2(01):1–26.

- Ronn and Wimschulte, (2009) Ronn, E. I. and Wimschulte, J. (2009). Intra-day risk premia in european electricity forward markets. Journal of Energy Markets, 2(4):71–98.

- Serinaldi, (2011) Serinaldi, F. (2011). Distributional modeling and short-term forecasting of electricity prices by generalized additive models for location, scale and shape. Energy Economics, 33(6):1216–1226.

- Taylor, (2010) Taylor, J. W. (2010). Triple seasonal methods for short-term electricity demand forecasting. European Journal of Operational Research, 204(1):139–152.

- Viehmann, (2011) Viehmann, J. (2011). Risk premiums in the german day-ahead electricity market. Energy policy, 39(1):386–394.

- Weron and Misiorek, (2008) Weron, R. and Misiorek, A. (2008). Forecasting spot electricity prices: A comparison of parametric and semiparametric time series models. International Journal of Forecasting, 24(4):744–763.

- Zachmann, (2008) Zachmann, G. (2008). Electricity wholesale market prices in europe: Convergence? Energy Economics, 30(4):1659–1671.

- Ziel et al., (2015) Ziel, F., Steinert, R., and Husmann, S. (2015). Efficient modeling and forecasting of electricity spot prices. Energy Economics, 47:98–111.

8 Appendix