Optimal Selling Time of a Stock under Capital Gains Taxes

Abstract

We investigate the impact of capital gains taxes on optimal investment decisions in a quite simple model. Namely, we consider a risk neutral investor who owns one risky stock from which she assumes that it has a lower expected return than the riskless bank account and determine the optimal stopping time at which she sells the stock to invest the proceeds in the bank account up to the maturity date. In the case of linear taxes and a positive riskless interest rate, the problem is nontrivial because at the selling time the investor has to realize book profits which triggers tax payments. We derive a boundary that is continuous and increasing in time and decreasing in the volatility of the stock such that the investor sells the stock at the first time its price is smaller or equal to this boundary.

Keywords: Capital gains taxes, tax-timing option, optimal stopping, free-boundary problem

JEL classification: C61, G11, H20

1 Introduction

In practice, capital gains taxes are undoubtedly one of the most relevant market frictions. In most countries, an important feature of capital gains taxes is the rule that profits are taxed when the asset is liquidated, i.e., the gain is realized, and not when gains actually occur. Thus, even in the simplest case of a linear taxing rule (that we consider in the current paper), there is a nontrivial interrelation between creating trading gains and tax liabilities by dynamic investment strategies. The investor can influence the timing of the tax payments, i.e., she holds a deferral option. In the case of a positive riskless interest rate, there is some incentive to realize profits as late as possible, but this can be at odds with portfolio regroupings in order to earn higher returns before taxes.

Solving a portfolio optimization problem with taxes allowing for arbitrary continuous time trading strategies is a rather daunting task, especially for the so-called exact tax basis and the first-in-first-out priority rule. Namely, shares having the same price but being purchased at different times possess, in general, different book profits, and hence, their liquidation triggers different tax payments. Allowing the investor to choose which of the shares is relevant for taxation is called exact tax basis. The book profits of the shares in the portfolio become an infinite-dimensional state variable (cf. Jouini, Koehl, and Touzi [13, 14] for the first-in-first-out priority rule and [15] for the exact tax basis).

Dybvig and Koo [11] and DeMiguel and Uppal [9] model the exact tax basis in discrete time and relate the portfolio optimization problem to nonlinear programming. Jouini, Koehl, and Touzi [14, 13] consider the first-in-first-out priority rule with one nondecreasing asset price, but with a quite general tax code, and derive first-order conditions for the optimal consumption problem. The problem consists of injecting cash from the income stream into the single asset and withdrawing it for consumption. Ben Tahar, Soner, and Touzi [4, 3] solve the Merton problem with proportional transaction costs and a tax based on the average of past purchasing prices. This approach has the advantage that the optimization problem is Markovian with the only one-dimensional tax basis as additional state variable. Cadenillas and Pliska [6] and Buescu, Cadenillas, and Pliska [5] maximize the long-run growth rate of investor’s wealth in a model with taxes and transaction costs. Here, after each portfolio regrouping, the investor has to pay capital gains taxes for her total portfolio.

In practise, an investor is usually interested in much simpler optimization problems. Therefore, we want to analyze a typical and analytically quite tractable investment decision problem to determine exemplarily the impact of capital gains taxes and to see how model parameters, as the volatility of the stock, enter into the solution. Often, the investor wants to maximize her trading profits within a certain finite period of time by exchanging one asset for another one only once. This means that she has to solve an optimal stopping problem. In this simple setting, different tax basises, as, e.g., the exact tax basis, the average tax basis, or the first-in-first-out priority rule, coincide. To investigate the impact of taxes on investment decisions, we look at an investor owning an asset which she would sell immediately to buy another one if she was not subject to taxation. Under risk neutrality, this just means that the asset the investor holds at the beginning has a lower expected return than the alternative asset. Then, we investigate to what extent she is prevented from this transaction by the obligation to pay taxes at the time she liquidates the first asset. The price of the first asset is modeled as stochastic process in the Black-Scholes market to see the influence of the volatility on the deferral option the tax payer holds. We prove the plausible supposition that the possibility to time the tax payments is more worthwhile for holders of more volatile assets and, consequently, the risky asset is sold later (see Proposition 2.4). We assume that the second asset is then kept in the portfolio up to maturity. Thus, it is no essential restriction to model it as a riskless bank account.

In contrast to the classic model of Constantinides [7], we do not assume that the investor can both defer the tax payments and divest the stock from her portfolio at the same time by trading in a market for short sell contracts (see Subsection 4.1 of [7]). To our mind, it is mainly an interesting gedankenexperiment to shorten the stock, instead of selling it, in order to defer tax payments, but under real-world tax legislation, it is no option for private investors. By assuming the existence of such a market for short sell contracts, Constantinides can price the timing option in the Black-Scholes model by no-arbitrage arguments and without solving a free-boundary problem. Another essential difference to [7] is that we have a deterministic finite time horizon, whereas in [7] liquidation is forced at independent Poisson times. Thus, as in problems with infinite time horizon, in the latter article, one gets rid of ‘time’ as a state variable.

In this paper, some standard techniques from the theory of optimal stopping are used, especially an approach that turns the problem with a terminal payoff to one with a running payoff, see Peskir and Shiryaev [16]. The objective function is much simpler than in other recent papers on the optimal selling time of a stock without taxes, as Shiryaev, Xu, and Zhou [18], where the stock is sold at the stopping time which maximizes the expected ratio between the stock price and its maximum over the entire horizon. Du Toit and Peskir [10] complement this by determining a stopping time that minimizes the expected ratio of the ultimate maximum and the current stock price. Dai and Zhong [8] consider a similar problem in which the average stock price is used as reference. In addition to the above selling problems, in their recent work, Baurdoux et al. [2] discuss a ‘buy low and sell high’ problem as sequential optimal stopping of a Brownian bridge modeling stock pinning. This is a phenomenon where a stock price tends to end up in the vicinity of the strike of its option near its expiry, see [1] for a detailed explanation.

The paper is organized as follows. In Section 2, we formulate the optimal stopping problem and present its solution (Theorem 2.2), which is, accompanied by Proposition 2.4, the main result of the paper. Afterwards, the results are related to other contributions in the literature, and the tax-timing option is valued (Remark 2.5). Section 3 introduces the applied method to solve the problem and prepares the proofs which are given in Section 4.

2 Formulation of the Stopping Problem and Main Results

Consider a filtered probability space , , generated by a one-dimensional standard Brownian motion . The investment oppurtunities consist of a bank account with continuously compounded fixed interest rate and a stock whose price process solves the SDE

| (2.1) |

with , and . At time , the investor holds one risky stock. It was purchased sometime in the past at price . This means that already at time , the stock possesses the book profit . The economically interesting case is , but this need not be assumed. The investor can sell the stock at any time up to the end of the time horizon . At the selling time , the investor has to pay the capital gains taxes , where is the given tax rate, i.e., if , the investor gets a tax credit. Then, the remaining wealth is invested in the riskless bank account. At maturity , the portfolio is liquidated anyway. As the bank account pays a continuous compounded interest rate, we assume that taxes also charge the account continuously. This corresponds to the taxation of a continuous dividend flow and leads to the after-tax interest rate . Thus, the investor’s wealth at maturity when selling the stock at time at price is

| (2.2) |

Maximizing investor’s expected wealth at maturity leads to the optimal stopping problem

| (2.3) |

where , and by we denote the set of stopping times taking values in . The assumption that the second investment opportunity is a riskless bank account rather than another risky asset makes the payoff function a bit more tractable and is, given that the investor is risk neutral and cannot change her position again before , not very restrictive.

Because of the strong Markov property of , we define the value function associated with problem (2.3) by

| (2.4) |

where is the unique solution of (2.1) with initial condition and denotes the set of stopping times taking values in . Note that as with . By setting in (2.4), it is clear that

| (2.5) |

In addition, we have that

| (2.6) |

The continuation region is defined by

and the stopping region by

Proposition 2.1

Of course, the proof follows more or less directly from the standard theory. Thus, it is only briefly sketched in Section 4. The following theorem states the main results of this paper and is also proved in Section 4.

Theorem 2.2

Consider problem (2.4) with stopping region . Let and . Then,

-

(a)

there exists a continuous, increasing boundary such that the stopping region is given by

(2.8) where for all , the equivalence holds.

The boundary satisfies the terminal condition -

(b)

if and , the value function satisfies the smooth fit condition at the boundary, i.e.,

(2.9)

Remark 2.3

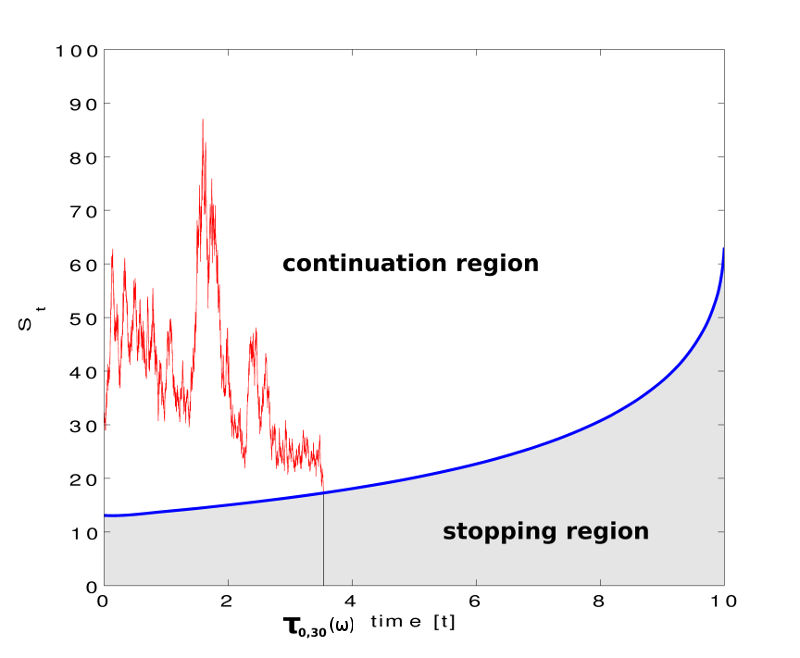

We are primarily interested in the case that , i.e., an investor who is not subject to taxation would immediatelly sell the stock. Then, Theorem 2.2 tells us that the solution is nontrivial if . Choosing the midpoint of the interval for and reasonable values for , , and , numerical calculations show that the boundary is far above the purchasing price , see Figure 1. This means that the investor always sells the stock with positive book profits. Then, it is evident that there is no incentive to buy the stock back at any later time and to repeat the game (namely, a renewed investment starts with zero book profit). This justifies the modeling of the decision problem as a simple optimal stopping problem.

On the other hand, if the stock is sold with negative book profits, the modeling is justified when wash-sales are forbidden, as, e.g., to some extent in the U.S. This means that the investor may sell the stock to realize the trading loss, but then she is not allowed to buy back the stock and has to take the other investment opportunity. Under the ban on wash sales, the investor may switch to the bank account even in the case , just in order to realize losses prematurely, which leads to a nontrivial solution of the stopping problem (see Theorem 2.2).

Proposition 2.4

(i) The value function is increasing in the volatility of the stock, i.e., for all , , and .

Consequently, for all .

Proposition 2.4 that is proved in Section 4 makes sense from an economic point of view. For a more volatile asset, the option to time the tax payments has a higher value for investors. This means that capital gains taxes can even motivate investors to take more risk. Of course, the extent of this effect depends on the riskless interest rate and vanishes for .

Seifried [17] solves the utility maximization problem for terminal wealth with (i.e., it can be assumed that taxes are paid at maturity), but there are no tax credits. In the model of [17], there can appear two opposite effects. Roughly speaking, if the drift of the stock is low, the tax may prevent the investor to buy the risky stock at all because, without negative taxes on losses, the expected after-tax gain becomes negative (literally, this only holds for buy-and-hold strategies in the stock). On the other hand, if the expected return is high enough, the investor may buy even more risky stocks than in the same situation without taxes. To make the latter plausible, consider a one-period binary model for the stock and a utility function that is linear around the initial wealth and satiable at some higher level of wealth. For the optimal stock position, the investor’s terminal wealth coincides with the saturation point if the stock price goes up. This means that, in the case of taxes, the investor buys even more risky stocks to offset the part of the gains that she has to pay to the government. [17] derives that for the Black-Scholes model with CRRA investors and realistic tax rates, the overall strategy effect of taxes is negligible (see Figure 8 therein).

Remark 2.5 (Value of the tax-timing option)

Assume that in our model, the book profit is taxed at time , and later gains on the stock are taxed immediately when they occur. Thereby, we assume that tax payments are financed by reducing the stock position, and tax rebates are reinvested in stocks. Then, the wealth in stocks satisfies the SDE

and thus . The optimal stopping problem degenerates: for , it is optimal to sell the stock at time , and for , it is optimal to sell at time .

Thus, one may interpret

as the time value of the timing option of the stock holder, i.e., the value of the right of the investor to influence the timing of the tax payments. By Proposition 2.4, this value is increasing in the volatility of the stock. This is in line with the results in Constantinides [7], where in a complete market model, including a market for short sell contracts, the price of the timing option, of course differently defined (see Equation (21) therein), is also increasing in the volatility of the stock (see Table III).

3 Method of solution

To solve problem (2.4), we make use of a standard method in the optimal stopping theory, see, e.g., Peskir and Shiryaev [16], where the terminal payoff is turned into a running payoff. Namely, thanks to the smoothness property of the payoff function , we can apply Itô’s formula to obtain the following decomposition of the payoff process :

| (3.1) |

where is a square integrable martingale with zero expectation, and is given by

| (3.2) |

By (3.1), from (2.4) can be written as

| (3.3) |

We have that

| (3.4) |

with

| (3.5) |

This means that the sign of does not depend on .

Remark 3.1

For with , the stopping time is strictly positive, and we conclude from (3.3) that and thus .

We have and

| (3.6) |

for all . Furthermore,

| (3.7) |

for , and

| (3.8) |

4 Proofs

4.1 Proof of Proposition 2.1

For all , one has

| (4.1) | |||||

for some constant that does not depend on . Thus, to establish joint continuity in , it remains to show that is continuous. Let . One has

where for the first inequality, we use that the processes and coincide in distribution.

To obtain an estimation in the other direction, one also has to find an upper bound for the increments of the payoff process between and because the remaining time to maturity is smaller for the problem started in . By the monotonicity of , one has

The first term can be estimated by

and the second term by

for some constants . Altogether, it follows that is continuous for any fixed .

4.2 Proof of Theorem 2.2

We distinguish three cases. The first two cases are trivial, whereas the third case is the interesting one, where we show the existence of a continuous, increasing, positive

boundary such that the stock is sold at the first time its price is smaller or equal to this boundary.

Case 1:

¿From (3.2), we see that . Then,

from (3.3), it follows that for all , i.e., the investor sells the stock immediately and

invests the proceeds in the bank account.

Case 2: and

One has for all . Then, again from (3.3), it follows that

for all ,

i.e., the investor never sells the stock prematurely and thus .

Case 3: and

Step 1: Let us show that for every with , the implication

| (4.2) |

holds. Together with the closedness of the stopping region, (4.2) implies that is of the form given in (2.8) with boundary .

By (3.3), for any and , one has

| (4.3) | ||||

where the last inequality holds by (3.6). By , this implies (4.2).

Step 2: Let us now show that in increasing. For and , one has

| (4.4) | ||||

where the second supremum is taken over all –stopping times taking values in . Since , (4.2) yields the implication

| (4.5) |

which induces that is increasing.

Step 3: Let us show that for all . At first, suppose there exists such that (i.e., ). As is increasing, one has that for all . As cannot reach , we have for all , which yields

For the first inequality, we use that for . For the second one, we use that is increasing in and for , increasing in .

We have that . In addition, and for . This yields that

which is a contradiction to the optimality of . Thus for all . follows analogously by extending problem (2.4)

to the interval .

Thus, the theorem is now proven, besides the smooth-fit condition, the continuity of the exercise boundary and its terminal condition. These assertions need some more preparation provided by the following lemmas.

4.2.1 Continuity of the optimal stopping times

The following two lemmas show that the optimal stopping times are close together for stock price processes started in a neighborhood of state and time.

Lemma 4.1

Let be defined as in (2.7). Fix . Then, for all , there exists such that for all .

Proof.

For all , one has

To compare the optimal stopping times for different state variables, we use that for all . Let be a standard Brownian motion. One gets

| (4.6) |

where the first inequality holds because is increasing, the second one holds by , and the third one follows by the strong Markov property of . For fixed, the right-hand side of (4.2.1) converges to for . ∎

Lemma 4.2

Let be defined as in (2.7). Fix with . Then, for all , there exists such that for all with and .

Proof.

Similarly to the proof of Lemma 4.1, for all , , and , one has

To compare the optimal stopping times, we write in terms of the process . Namely, by construction, one has

| (4.7) |

where . In addition, the following argument uses the fact that for small. Consequently, at the first time hits the boundary, the process is not far away, and one can argue as in Lemma 4.1. Let be a standard Brownian motion. Then, for and , one gets

| (4.8) |

where the first inequality holds because is increasing, the second one holds by (4.7) and , and for the fourth one, we use the strong Markov property of .

As in Lemma 4.1, one can choose small enough such that

| (4.9) |

Because converges stochastically to for , there exists such that

| (4.10) |

for all with . So, it remains to show

| (4.11) |

To estimate this probability, we renew at , where it is sufficient to consider the set . Then, we estimate from below and not from above as in (4.2.1). But, the calculations are completely analog to the estimation of , and we are done. ∎

4.2.2 Smooth-fit condition

Next, we show (2.9), i.e., the value function joints the payoff function smoothly at the boundary. For and , one has

4.2.3 Continuity of the boundary

Proposition 4.3

The boundary is right-continuous on .

Proof.

Fix and consider a sequence for . As is increasing, exists. Since for all , and and are continuous (Proposition 2.1), one gets that , i.e., . This results . As is increasing on , the claim is proved. ∎

Proposition 4.4

The boundary is left-continuous on .

Firstly, note that by monotonicity, the limit exists and . The proof of the proposition is divided into three steps. Under the assumption that a jump of the boundary occurs at some time , in the first two steps, we find an upper bound for the -derivative and the -derivative of for points in time in a left neighborhood of and prices between and . Then, we use these upper bounds to argue with the PDE which is satisfied by in to see that is bounded away from . Roughly speaking, the contribution of to the PDE is bounded away from zero by minus the drift rate of the payoff function (cf. Step 3 of the proof). In a neighborhood of the stopping region, this drift rate is strictly negative. Since is part of the stopping region, where , this turns out to be a contradiction to the linearity of in if .

This line of argument has already been applied to quite diverse payoff functions, see [16].

Proof.

Suppose that the stopping boundary has a jump at , i.e., .

Step 1 (upper bound for the derivative): Let , , and . Define the stopping time

| (4.14) |

which applies the optimal stopping rule for the problem started in to the problem started in . By construction, possesses the same distribution as . Because is in general sub-optimal for the problem started in , one gets

| (4.15) |

By the classic theory for parabolic equations, see, e.g., Friedman [12] (Chapter 3) or Shiryaev [19] (Theorem 15 in Chapter 3), one knows that in the continuation region. Therefore, exists for all and

Together with (4.2.3), this implies

On the other hand, lies in the stopping region for all and thus . Since , one can apply Lemma 4.2, and in probability for , where the convergence holds uniformly in . By uniform integrability, one gets

| (4.16) |

Step 2 (upper bound for the derivative): Let , , and . The arguments are similar to Step 1, but more convenient to write down because is already an admissible stopping time for the problem started in and need not be transformed as in (4.14). One gets

| (4.17) |

Again, by in the continuation region, one gets that exists for all and for . Together with (4.2.3), one gets

Again, by and , an application of Lemma 4.2 yields

| (4.18) |

The RHS is that does not depend on .

Step 3 (Conclusion of the left-continuity): Now, we want to lead the assumption to a contradiction.

Let . By Remark 3.1, one has and thus, by (3.4), it follows that . By Step 1 and Step 2, there exists such that for all and , one has that

where the second inequality holds by the continuity of and its monotonicity in . Again, by Theorem 15 in Chapter 3 of [19], we know that the value function solves the PDE

in the continuation region . Thus, we have

By , (smooth-fit condition), , and the Newton-Leibniz formula, it follows that

| (4.19) |

As this holds for all and is continuous, one concludes that

which is a contradiction to the fact that lies in the stopping region. So, it can be concluded that , and the continuity of the boundary is established. ∎

Terminal Condition of the boundary

By Remark 3.1, cannot exceed the boundary , above which the drift rate of the payoff process is positive. It remains to exclude that . But, this is done with the same arguments as in the proof of the left-continuity of the boundary, using the fact that for all

4.3 Proof of Proposition 2.4

(i) Let and w.l.o.g. . For two independent standard Brownian motions and , the process

possesses the same law as the stock price from (2.1) with . In addition, is Markovian w.r.t. the filtration which is generated by and . This implies that from (2.3) with standard deviation coincides with the value of the problem

| (4.20) |

where the supremum is taken over all –stopping times . Now consider the artificial optimal stopping problem where the second Brownian motion that enters into the stock price is not observable to the maximizer. This corresponds to the restriction to –stopping times. Of course, the latter supremum is at least as high as the previous one. On the other hand, for any –stopping time , we have

where the conditional expectation is because is –measurable whereas is independent of .

It follows that the value of problem (4.20) restricted to all –stopping times coincides with from (2.3)

with smaller standard deviation . Thus, one has . Note that the only property of the payoff function we use is its affine linearity

in .

(ii) For , the optimal stopping problem (2.4) reads

By simple algebra, one calculates that . So, we conclude that for fixed , the maximum of is either attained at or . For given by (2.10), one has , i.e., the investor is indifferent between stopping at and . It implies that lies in the stopping region. On the other hand, by for all , one has that lies in the continuation region for all . This implies that is indeed the optimal exercise boundary from (2.8).

It remains to show that for all . As is not attained at any , cannot hit the boundary before if it starts above it.

References

- [1] Avellaneda, M. and Lipkin, M. D. (2003) A market-induced mechanism for stock pinning. Quantitative Finance, 3(6), 417–425.

- [2] Baurdoux, E. J., Chen, N, Surya, B. A. and Yamazaki, K. (2014). Double optimal stopping of a Brownian bridge. Submitted for publication, http://arxiv.org/abs/1409.2226.

- [3] Ben Tahar, I., Soner, M., and Touzi, N. (2007) The dynamic programming equation for the problem of optimal investment under capital gains taxes, SIAM Journal on Control and Optimization, 46(5), 1779-1801.

- [4] Ben Tahar, I. B., Soner, H. M., and Touzi, N. (2010) Merton Problem with taxes: characterisation, computation and approximation, SIAM Journal on Financial Mathematics, 1(1), 366-395.

- [5] Buescu, C., Cadenillas, A., and Pliska, S. R. (2007). A note on the effects of taxes on optimal investment, Mathematical Finance, 17(4), 477-485.

- [6] Cadenillas, A. and Pliska, S. R. (1999). Optimal trading of a security when there are taxes and transaction costs, Finance and Stochastics, 3(2), 137–165.

- [7] Constantinides, G. M. (1983). Capital market equilibrium with personal taxes, Econometrica, 51(3), 611-636.

- [8] Dai, M. and Zhong, Y.F. (2012). Optimal stock selling/buying strategy with reference to the ultimate average, Mathematical Finance, 22(1), 165-184.

- [9] DeMiguel, V. and Uppal, R. (2005). Portfolio investment with the exact tax basis via nonlinear programming, Management Science, 51(2), 277-290.

- [10] Du Toit, J. and Peskir, G. (2009). Selling a stock at the ultimate maximum. Annals of Applied Probability, 19(3), 983–1014.

- [11] Dybvig, P. and Koo, H. (1996) Investment with Taxes. Washington University, St. Louis, MO, Working Paper.

- [12] Friedman, A. (1964). Partial Differential Equations of Parabolic Type, Prentice-Hall, Florida.

- [13] Jouini, E., Koehl, P.-F., and Touzi, N. (2000). Optimal investment with taxes: an existence result. Journal of Mathematical Economics, 33(4), 373-388.

- [14] Jouini, E., Koehl, P.-F., and Touzi, N. (1999). Optimal investment with taxes: an optimal control problem with endogenous delay. Nonlinear Analysis, 37, 31–56.

- [15] Kühn, C. and Ulbricht, B. (2014), Modeling capital gains taxes for trading strategies of infinite variation. Submitted for publication. http://arxiv.org/abs/1309.7368

- [16] Peskir, G. and Shiryaev, A.N. (2006). Optimal Stopping and Free Boundary Problems, Birkhäuser.

- [17] Seifried, F. (2010) Optimal Investment with Deferred Capital Gains Taxes, Mathematical Methods of Operations Research, 71(1), 181-199.

- [18] Shiryaev, A.N., Xu, Z.Q., and Zhou, X.Y. (2008). Thou shalt buy and hold. Quantitative Finance, 8(8), 765–776.

- [19] Shiryaev, A. N. (2008). Optimal stopping rules (Vol. 8). Springer.