The random matrix regime of Maronna’s M-estimator for observations corrupted by elliptical noises

Abstract.

This article studies the behavior of the Maronna robust scatter estimator of a sequence of observations which is composed of a dimensional signal drown in a heavy tailed noise, i.e where and is drawn from elliptical distribution. In particular, we prove that as the population dimension , the number of observations and the rank of grow to infinity at the same pace and under some mild assumptions, the robust scatter matrix can be characterized by a random matrix that follows a standard random model. Our analysis can be very useful for many applications of the fields of statistical inference and signal processing.

1. Introduction

Estimation of covariance matrices is at the heart of the theory of multivariate statistical analysis [12]. Its importance can be seen from its broad range of applications including financial data analysis, statistical signal processing, and wireless communication. A natural way to estimate covariance matrices is represented by the sample covariance matrix. Given observations , of size , independent, and identically distributed, (i.i.d) then the sample covariance matrix is given by . The popularity of the sample covariance matrix essentially comes from its low-complexity and the existence of a good understanding of its behaviour in two asymptotic regimes: goes to infinty while is fixed when and go to infinity with the same pace. Recent advances in the theory of large random matrices have made it clear that in the second asymptotic regime, the sample covariance matrix is no longer consistent. Conventional estimation methods that are based on the use of the sample covariance matrix are thus inefficient when the number of observations and their dimension become commensurate and large. Such scenario naturally arises in current array processing applications where the trend is to employ large antenna arrays. Based on a deep understanding of the behaviour of the sample covariance matrix, a new wave of detection methods [4, 3, 13] and subspace estimation techniques [11, 14, 18] has recently emerged. Although consistent, these methods are bound by the fact that they still fundamentally rely on the sample covariance matrix, their consistency being obtained by resorting to a deep analysis of its asymptotic behaviour. Nevertheless, the use of the sample covariance matrix can lead to poor performances, especially when observations are drawn from heavy tailed distributions or contain outliers. In such situations, the use of robust covariance estimators has been aknowledged as an efficient solution to combat the presence of outliers. Although references to robust techniques are traced back to the eighties with the works of Huber [9] and Maronna [10], the study of their performance has been often restricted to the conventional regime where the number of observations is too large as compared to their dimensions. It was only recenlty that new tools have been developed in [6, 7, 8] which allow to analyse the behaviour of robust Maronna’s scatter estimators. The main contributors are Couillet et al. who established that the robust scatter estimator can be well-approximated in the asymptotic regime by a random matrix that follows a standard random model. One of the key advantages of this result, is that it allows to bring back the asymptotic analysis of robust-scatters to that of an other random object for which an important load of results already exist.

Despite their high value, these works have been derived only for the case of pure noise observations. While the case of a low rank signal observations can be dealt with by resorting to easy adaptations of the approach of [8], handling high-rank signal observations is much more challenging. Building on the tools developed in [8], we propose in this work to analyse this difficult scenario. We show that in this case the adaption of the method in [8] is not immediate and necessitates the development of additional appropriate tools. Some of the required results that were of independent interest were submitted in an other work which can be found in [1].

Notations: In the remainder of this work, we shall denote the real eigenvalues of Hermitian matrix . The notation will refer to the spectral norm of matrices and Euclidean norm for vectors, while ∗ sill stand for the complex conjugate operator. The derivative of a differentiable function will be denoted by .

2. Assumptions and Main results

We start by introducing the data model under study. We consider sample vectors satisfying:

where is a deterministic matrix and are random vectors defined as:

with the scalars . Let . We denote by and considers the following assumptions:

Assumption A- 1.

For each , , , and

with .

This paper studies the asymptotic behaviour of the Maronna’s M-robust scatter estimator in the regime of Assumption 1. We recall that the Maronna’s M-robust estimator which we denote by is given by the unique solution in of the following equation:

| (2.1) |

where function satisfies the following properties:

Assumption A- 2.

-

i)

Function is non-negative continuous and non-increasing,

-

ii)

The function is increasing, bounded and continuously differentiable with and .

-

iii)

.

and the scalars are such that:

Assumption A- 3.

-

i)

The random empirical measure converges weakly to which satisfies ,

-

ii)

There exists and such that for all large a.s., .

The conditions in Assumption 2 are the same as those considered in [8]. It is worth observing that Assumption 2- is different from the one considered by Maronna in [10], in that is not allowed to be constant on any open interval. However, Assumption 2:- is much more adapted to the high-dimensional regime than Assumption p.53 of [10], which requires that .

Assumption 3 is different from the original assumption in [8] as we assume here the weak convergence of the empirical measure . However, one can easily see by the Portmanteau lemma that Assumption 3 will bring about the same useful requirements, namely the a.s. tightness of , i.e., for each , there exists such that with probability one, , along with the absence of a heavy mass concentrating close to zero ( for large enough a.s.).

The statistical hypothesis on is detailed below:

Assumption A- 4.

-

i)

are independent invariant complex zero-mean vectors with for each , and are independent of ,

-

ii)

are independent standard Gaussian distributed vectors.

-

iii)

Define , then and .

In addition to the above assumptions, the following hypothesis might be required:

Assumption A- 5.

For each , a.s.,

Theorem 2.1 (Uniqueness).

Theorem 2.2.

Corollary 2.3.

Proof.

Let be the solution of the system of equations (2.2). Let be given by:

Let and . Then,

Noticing that and satisfy:

| (2.3) | ||||

| (2.4) |

it is not difficult to see that solving the system of the equations in (2.2) can be reduced to determining the solutions of a two equations system, whose solutions are and . The control of in Lemma 4.6 allow us to ensure that and are uniformly bounded for enough large a.s. Hence, there exists a subsequence over which and converge to and . Taking the limits of both sides of (2.3) and (2.4), we obtain

| (2.5) | ||||

| (2.6) |

Such limits are unique since the solutions of the systems of equations (2.5) and (2.6) are unique in case they exist. The existence and unicity of the solutions of (2.5) and (2.6) essentially relies on showing that the following function

is a standard interference function [20], i.e it satisfies the three conditions of positivity, monotonicity and scalability that have been used in the proof of Theorem 2.1. ∎

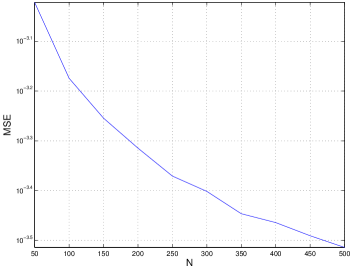

3. Numerical analysis

In order to assess the accuracy of our results, we represent in Fig. 1, the empirical estimate of the mean squared error (MSE) between the robust scatter estimate and with respect to

when and with is having independent standard Gaussian entries with zero mean and variance . We set , and . We note that the MSE decreases with , thereby supporting the convergence of to .

4. Proofs

4.1. Heuristic Analysis

The study of the asymptotic behaviour of robust scatter matrices requires careful attention. The difficulty essentially lies in the rank-1 matrices present in the sum of (2.1) being dependent through . At first sight, this observation might make us think that the asymptotic analysis of is out of the framework of the standard random matrix theory. However, a careful investigation of the expression of can lead us to replace by a random object, whose analysis using the theory of random matrices is quite standard.

Hereafter, we develop some heuristics that will lead to determine the asymptotic random equivalent of . We believe that beyond their interest to the considered scenario, these heuristics can facilitate the understanding of the asymptotic behaviour of robust estimation techniques in the regime where the number of observations is of the same of order of the size of the population covariance matrix.

Building on the ideas of [8], we will first start by deriving a new rewriting of that will also be extensively used in section 4.2 devoted to the exposition of the rigorous proofs. Let be the matrix where we remove , i.e.,

Applying the identity:

for any invertible , vector and scalar such that is invertible, we obtain:

where As is increasing and , function is positive increasing and maps to . It is therefore invertible with inverse denoted by . We have thus:

We can therefore express as:

with positive and non-increasing.

This new rewriting of is of fundamental importance. It has two major advantages. First, it reveals that is uniquely determined by . This can be seen by noticing that a solution to (2.1) exists and is unique if and only if the following system of equations in :

admits a unique positive solution . The estimation of the robust scatter matrix is then reduced to determining the solutions of a system of equations. The second advantage of this new rewriting is that it can provide, based on some heuristics, interesting insights about the asymptotic behaviour of . In effect, it is not difficult to understand that is weakly dependent on , since depends on only through the terms . Standard results from random matrix theory will thus lead to , which tends to imply that scales with . Assume that can be approximated by where does not depend on the random vector . Then, because of rank-1 perturbation arguments leading to replace with , we have:

On the other hand, from the asymptotic equivalence between and , we expect to be asymptotically equivalent to . As we will see later, without inducing a major error, one can assume that are Gaussian. The asymptotic behaviour of can be thus studied using results from [19]. If Theorem 1 in [19] is applicable, then should satisfy:

| (4.1) | ||||

where are the fixed point solutions to the following system of equations:

Multiplying both sides of (4.1), we thus get:

Plugging the above equations into (4.1), we obtain that are solutions to the following system of equations:

4.2. Rigorous Proofs

The main differences of our work with respect to the one in [8] lies in the considered data model. While [8] assumes purely noise observations drawn from elliptical distributions, we consider in the present work, sequence of time observations that are given by the sum of a heavy-tailed noise and a Gaussian distributed vector modeling the ”signal” part of the observations. In practice, the estimation of the covariance matrix of the available observations can help infer precious information on the signal of interest. From a theoretical standpoint, if the useful data live in a low-dimensional space, the same approach considered in [8] can be pursued with only minor changes. Although less popular, high rank data models, occurring when scales with , are more attractive for several applications of array processing concerning distributed source localization [17]. They are also more difficult to handle, since the use of the approach of [8] poses many technical difficulties, when is allowed to be of high rank . This can be easily seen by noticing that our heuristic computations involve solving a system of equations while those of [8] requires only solving the fixed point of a single equation. One can easily convince oneself that in the context of interest, it is much more difficult to get insights into the behaviour of the solutions of the underlying system. Before delving into the core of the proof, we need first to introduce in the sequel some preliminary results that will help adapt the techniques of [8] to our particular context.

4.2.1. Preliminary Results

Function and Related Functions

The robust-scatter estimator is parametrized by function , which significantly impacts its performance. This intuition is further confirmed by theoretical analysis, showing that a number of sequence of functions in relation with naturally arise. This section aims at presenting the list of these functions along with some of their most important properties. We first summarize in the following table some of the results that has been established in [8].

| Functions | Properties |

|---|---|

| Non-increasing | |

| Positive | |

| Continuous | |

| Increasing | |

| Positive | |

| Continuous | |

| Bounded with . |

| Sequence of Functions | Properties |

|---|---|

| Increasing | |

| Positive | |

| Continuous | |

| Unbounded | |

| Non-Increasing | |

| Positive | |

| Continuous | |

| Increasing | |

| Positive | |

| Continuous | |

| Bounded with |

In addition to the aforementioned properties, we need to prove the following results, which will be used in our proofs.

Lemma 4.1.

Let and be two functions satisfying assumption 2. Then, we have, for all ,

In other words, is Lipschitz with Lipschitz constant .

Proof.

We have:

Since is non-increasing:

Therefore,

∎

Lemma 4.2.

Proof.

The first statement follows from the previous lemma by setting . To prove the second, notice that when , , thereby showing that whenever . ∎

Remark 4.1.

As it has been proven in [8], functions and share respectively the same properties as and . As a consequence, we can prove that is Lipschitz with constant lipschitz . The constant Lipschitz being independent on , we conclude that form an equicontinuous family of functions and as such converge uniformly on . Moreover,

and whenever .

Lemma 4.3.

Let . Denote by the inverse function corresponding to . Then, for all , we have:

In particular, is lipschitz on with constant lipschitz . Besides, functions are Lipschitz and converge uniformly on .

Proof.

Let . From the relation , we have:

Since is increasing, . Hence,

Finally, after simple calculations, we can prove that:

Therefore, is Lipschitz with constant lipschitz equal to . This constant being independent on , the sequence of functions converge uniformly on . ∎

Useful results

As previously stated, the difficulty of studying the robust-scatter estimator lies in the control of the asymptotic behaviour of and . The proof of Theorem 2.1 and Theorem 2.2 will require us to show that and scale with and to control quadratic forms involving matrix where is a certain functional. To this end, we develop in this section two key results that will underlie the proof of the main theorems.

Proposition 4.4.

Let be a sequence of hermitian positive matrices satisfying Assumption 4-iii). In addition, let be positive random variables satisfying assumption 4-ii). Consider a sequence of piece-wise continuous positive bounded functions defined on that has at least one subsequence converging uniformly. We assume that functions satisfy the following additional properties:

-

•

Function grows at most linearly, i.e there exists such that:

-

•

-

•

.

Then the following equation in :

| (4.2) |

admits a unique positive solution which we denote by . Then, there exists a sequence with such that:

Moreover, we have:

| (4.3) |

where converges almost surely to zero.

Proof.

We start by showing that (4.2) admits a unique solution . It is clear that function is increasing and continuous on with the limit at less than , while the limit when is . Therefore, there exists a unique that satisfies (4.2). It is easy to check that is less than the maximum eigenvalue of . Therefore, we can restrict the domain of to the set . Since is convex, applying the Jensen inequality, we obtain:

Setting , the above inequality becomes:

| (4.4) |

Therefore, because otherwise, (4.4) would not hold.

The proof of the lower-bound inequality is more delicate. Let be as in Assumption 3-ii) and denote by the following map:

Functions and are both increasing, while . Furthermore, we can easily check that:

Therefore, there exists solution in to the equation . Moreover, we have , and thus . On the other hand, is differentiable with derivative given by:

Let . Hence, if ,

The mean value theorem implies that:

| (4.5) |

where

As a consequence,

| (4.6) |

Combining (4.5) and (4.6), we therefore get:

Note that it is easy to prove that , since and . Moreover, as and .

We will now proceed proving the inequalities in (4.3). Let be the eigenvalues of . We have:

| (4.7) |

where

| (4.8) | ||||

| (4.9) |

As is the unique solution of (4.2), can be further simplified as:

| (4.10) |

where follows due to the fact that . Substituting (4.10) into (4.7), we get:

Therefore, the result immediately follows once we prove that and converge almost surely to zero. We will only control . The control of can be obtained using the same arguments. We have:

Since and , sequences and are bounded. One can extract a subsequence such that: and converge. Over this subsequence, converge uniformly to and as such:

Moreover, since , . The sequence of functions converge also uniformly to , thereby yielding:

It remains thus to check that is almost surely bounded. For that, first note that since , we have:

As and , is almost surely bounded away from zero, thereby implying the desired result. The control of could be done using the same arguments. ∎

The second ingredient that will be of extensive use in the proof of the theorem is provided by the following key-lemma.

Lemma 4.5.

Let Assumption 1-4 hold true. Let be a sequence functions satisfying the conditions of proposition 4.4. Denote by the unique solution in to the following equation:

Consider the unique solutions to the following system of equations:

| (4.11) |

Then, the following statements hold true:

-

i)

-

ii)

If . Then, we have:

(4.12) -

iii)

If , then, there exists such that for large enough, a.s.

Proof.

The proof of the first two items is based on Lemma .15 and Lemma .16 in Appendix Appendix: Technical Lemmas. For these Lemmas to be applicable, we need to check that . To this end, first note that:

The right-hand side of the above equality is almost surely bounded above zero since and is almost surely bounded by proposition 4.4. We conclude thus by resorting to Lemma .14 in Appendix Appendix: Technical Lemmas.

In order to prove the last statement, let be the index of the maximum element in . We therefore have:

where follows from proposition 4.4. Besides, scalars being the limits of almost surely bounded random quantities are bounded. Therefore,

where . ∎

4.2.2. Proof of the Main Theorems

With the above preliminary results at hand, we are now in position to provide the proofs of Theorem 2.1 and Theorem 2.2.

Proof of Theorem 2.1: Asymptotic Existence of the Robust Scatter Estimator

Theorem 2.1 establishes the existence of the robust scatter estimate for large and . In particular, it implies that for each realization, there exists and large such that for all and greater than and , equation (2.1) admits a unique solution. Although we believe that a stronger result showing the existence of the robust scatter estimate for well-behaved set of samples can be established using probably the same kind of techniques as in [5], we have chosen in this paper to show Theorem 2.1 under the setting of the asymptotic regime. The reason is that the techniques used in that proof will be key to understanding some aspects of the asymptotic behaviour of the robust scatter estimate, thereby paving the way towards the proof of Theorem 2.2.

The proof of Theorem 2.1 follows the same lines as in [8]. Define with:

As it has been already mentioned, in order to prove that is uniquely defined for large enough a.s., it suffices to show that the system of equations in

admits a unique solution a.s. for large enough. To this end, we will show that is a standard interference function, i.e, it satisfies the following three conditions:

-

a)

Positivity: For each , and each , ,

-

b)

Monotonicity: For each and each , ,

-

c)

Scalability: For all , and , .

Item can be easily shown by noticing that matrix is invertible almost surely and is positive definite, while the monotonicity follows immediately from the fact that is non-decreasing of each . As for the scalability, we can assume without loss of generality that there exists as the results holds trivially when . With this assumption at hand, we rewrite as:

As is increasing, for and . Hence,

If there exists at least , we therefore get:

We have thus established that is a standard interference function. Referring to the results of [20], it remains to show that there exists vector such that for all , a.s. for large enough, a statement which is known as the feasibility condition.

In order to establish the feasibility condition, let be chosen so that:

for some sufficiently small satisfying:

This is possible since,

We will prove that is a bounded sequence. To this end, we will proceed by contradiction. Assume that there exists a sequence such that . Since the sequence of functions converge uniformly, one can extract a subsequence from such that: and converge uniformly to . Therefore, the sequence of functions converge uniformly to . Hence,

which is in contradiction with the fact that:

Now, consider the unique solution of:

Such exists and is unique by Proposition 4.4. Set . We will prove that this choice of guarantees:

a.s. for large enough. We have:

where . From item of Lemma 4.5, we have:

where with are the unique solutions to the following system of equations:

Let be the index of the maximum element in . Then, there exists such that for all

| (4.13) |

As , we obtain from item of Lemma 4.5,

| (4.14) |

where refers to some sequences converging almost surely to zero as grow to infinity. Plugging (4.14) into (4.13), and using the fact that:

we finally get:

thereby establishing that:

a.s. for large enough.

Proof of Theorem 2.2: Asymptotic Convergence of the Robust-Scatter Estimator

The proof of Theorem 2.2 heavily relies on the new rewriting of the robust-scatter estimate as:

| (4.15) |

where are the unique solutions of the following system of equations:

their existence and uniqueness in the asymptotic regime being established in the proof of Theorem 2.1. From the rewriting of in (4.15), it appears that an in-depth study of the asymptotic behaviour of can be a good starting point. As mentioned in our heuristic analysis, one intuitively expects the to approach in the asymptotic regime , the solutions of the following system of equations:

This intuition underlies the proof of Theorem 2.2. In particular, we will prove that:

satisfy:

| (4.16) |

This in particular will allow us to state that can be approximated by . The importance of this finding lies in the fact that unlike , follows a classical random matrix model, thereby opening up possibilities of exploiting an important load of available results. Prior to proceeding into the proof of the convergence stated in (4.16), we first need to introduce the following key lemmas that allow to identify the intervals within which lie almost surely quantities and . We start by handling terms . We have in particular the following Lemma:

Lemma 4.6.

Let:

Then, for all large , there exists a unique vector such that:

| (4.17) |

Besides, vector is given by:

with chosen arbitrarily in and:

Moreover, there exists and with and and such that, almost surely for large enough, we have:

Moreover, and satisfy:

Proof.

Similar to the proof of Theorem 2.1, we can show along the same lines that is a standard interference function. It remains to prove the existence of such that . To this end, take , where is the unique solution to the following equation:

Such exists according to proposition 4.4. Then:

| (4.18) |

Again, the limit in the above equation (4.18) can be controlled using proposition 4.4, thereby yielding:

where almost surely. As , one can conclude that there exists , such that for enough large ,

We are now in position to prove the uniform boundedness of . For that, consider such that . Let be chosen such that and is greater than the limit support of . Set and so that the following conditions are fulfilled:

| (4.19) | |||

| (4.20) |

Such choices are possible since

-

•

,

-

•

,

Moreover, we can check that one can choose and such that and . As a matter of fact, building on the same reasoning used to show that in the proof of Theorem 2.1, we take and the positive reals that verify:

where satisfies . Assume that . There exists a sequence such that . Since the sequence of functions converge uniformly, one can extract a subsequence from such that and converge uniformly to . Therefore, the sequence of functions converge uniformly to . Hence:

which is in contradiction with the fact that . The same method can be used to prove that . Consider now the function in the domain . Define the unique solution to the following equation:

Similarly, define on the function . Let be the unique solution to the following equation:

| (4.21) |

Note that from proposition 4.4, and are well-defined and satisfy:

Set for all , . Define recursively the sequences:

From the previous analysis, . To prove the uniform boundedness of , one can proceed by induction on . For , the result is true. Let and assume that holds true for any and . We propose to prove it for . We have

From the induction assumption along with the fact that is non-increasing, we obtain:

Hence,

From Remark 4.1 along with Lemma 4.3, function satisfies the assumptions of proposition 4.4. We have therefore,

where converges to zero almost surely. Equation (4.19) guarantees that , thereby showing, that almost surely for large enough:

We will now prove the lower-bound inequality. Similarly, consider for all , . The sequence:

converges to as . In the same way as for the upper-bound inequality, we will show the result by induction on . For , the result is true. Let and assume that holds true for any and . We propose to prove the result for . Similar to above, using the fact that is non-increasing, we have:

where follows from the fact that . Again, from remark 4.1 and Lemma 4.3, function satisfies the assumptions of proposition 4.4. We have therefore,

where converges to zero almost surely. On the other hand,

and hence, almost surely, for enough large ,

∎

The following refinement of Lemma 4.6 will be required in the proof of the asymptotic convergence of the robust-scatter estimator.

Lemma 4.7.

Let be couples indexed by with and such that . Then, for sufficiently small the following system of equations:

| (4.22) |

has a unique vector solution for all large a.s, and there exists with and and , such that for all small:

for all large a.s. Moreover, and satisfies:

Proof.

The same proof as that of Lemma 4.7 holds by taking smaller than and choosing so that it satisfies:

while is set in the same way as before. ∎

We will now provide similar results for the random quantities . In particular, we have the following Lemma:

Lemma 4.8.

Let . There exists with and such that, for all large a.s.,

| (4.23) |

Proof.

The proof is based on the same tools as those used to show Lemma 4.6. The single difference is that the random quantities involve quadratic forms which will be treated by resorting to Lemma 4.5. First recall that are given by:

with chosen arbitrarily in and:

Similar to the proof of Theorem 2.1, consider so that and . Let be the unique solution of:

Set . We will prove by induction on that . For , the result holds true. Assume now that for all :

and let us show that . We have:

Let . From item in Lemma 4.5, we have:

| (4.24) |

where with the unique solutions to the following system of equations:

The limit of the convergence in (4.24) can be bounded as:

where converges to zero almost surely (inequality (a) being a by-product of (4.3) in proposition 4.4). Finally. from item of Lemma 4.5. we get:

with converging to zero almost surely. Since satisfies:

we obtain that:

for large enough a.s. In order to prove the lower bound in (4.23), the same reasoning as the one used in the previous lemma applies. In particular, it suffices to set and such that , and . Taking such that:

and setting to the unique solution of the following equation:

with , we can establish by induction on and using the same steps as in the control of the lower bound of that:

∎

The determination of an interval in which lies all quantities is of utmost important in that it allows us to control the quadratic forms: and , where and are solutions of equations (4.22) and (4.17). In particular, we have the following two lemmas which easily follows from item- of Lemma 4.5.

Lemma 4.10.

Let be couples indexed by with , and such that . Then, for all , we have:

where are defined the solutions of (4.22).

With these results at hand, we are now in position to prove satisfies:

As in [8], we will distinguish two cases: the case where all s are bounded and that of unbounded . The proof is merely based on the same techniques with only some modifications and will be detailed for sake of completeness.

All -s are Bounded

Assume that there exists a constant such that for all . Define . Without loss of generality, we assume that . We have:

| (4.25) | ||||

| (4.26) |

In a similar way, we also have:

From Lemma 4.9, let with such that for all alrge , a.s. and for all :

| (4.27) |

In particular, since is non-increasing, taking in (4.26) and applying the left-hand inequality in (4.27), we obtain:

| (4.28) |

Assume now that for some , infinitely often. Therefore, there exists a sequence over which for large enough. We distinguish two cases. First, assume that . There exists a sequence obtained from a subsequence of over which .

From (4.28), we have:

which is in contradiction with . Therefore, for (4.28) to hold, we must have . Since all -s are bounded, is also a bounded sequence. One can thus extract a subsequence extracted from over which and . Let and write (4.28) in the following equivalent form:

| (4.29) |

We therefore have:

which is in contradiction with (4.29). Symmetrically, we obtain that for and for large a.s.,

which is equivalent to:

We conclude using the same reasoning as above that for each small for all large . a.s. so that finally, we have:

The uniform boundedness of implies that of and , thereby ensuring that:

Hence, for any , arbitrarily small, we have for all large ,

Since the spectral norm of is almost surely bounded and is arbitrary, we conclude that:

Unbounded

We now relax the boundedness assumption on the support of the distribution of . We will follow the same technique used in [8]. Similarly to [8], let be couples indexed by such that for all large , we have , for small enough, and . Denote by with cardinality . Then,

In the sequel, we will differentiate the indexes in from those in . Define as:

where are the solutions of the system of equations (4.22) given in Lemma 4.7. Let and denote by and . We have:

where we used in the first inequality the fact that . Since , we obtain:

The above inequalities imply that is almost surely bounded irrespective of small enough. To see that, note that if , the left inequality ensures that while if , the second inequality ensures that . As a consequence, we can assume that for all large and for all small enough. From this observation, for all large , a.s. we have:

| (4.30) |

where we defined similarly to [8] as:

with

Using the resolvent identity (for any invertible matrices and ) along with Cauchy-Schwartz inequality, we obtain:

Note that for small enough, matrix is invertible. Besides, from assumption 3, for small enough and for enough large , . Using Lemma .14 in Appendix Appendix: Technical Lemmas, we conclude that there exists such that . Since matrix has a bounded spectral norm, Theorem .15 in Appendix Appendix: Technical Lemmas along with the rank-1 perturbation Lemma [15, Lemma 2.6] yields:

where . From for positive definite , we have:

where

Since for all and for all large a.s., we have:

where is a constant that does not depend on . In the same way, we can control the term . Finally, we conclude that:

| (4.31) |

for some constant independent of . Quantities being controlled for , we can now proceed in a similar way as in the case of the bounded case. Lemma LABEL:lemma:quadratic_form_total_kappe implies that for any fixed there exists a sequence such that a.s. for large enough,

| (4.32) |

Combining (4.30), (4.31) and (4.32), we then have for all large a.s. and for all ,

which for becomes:

| (4.33) |

Assume that for some . Let us restrict the sequence to those indexes for which . Similar to the case of bounded , we can see that (4.33) implies that , a bound which can be chosen independent of . In effect, from (4.33). we have:

which is equivalent to:

or also:

Using the definition of , (4.33) reads for sufficiently small:

or also for large enough:

Hence,

or equivalently:

Since , . Therefore, for chosen sufficiently small so that: , we have:

| (4.34) |

Since belongs to the interval for large enough, taking the limit of (4.34) over some subsequences over which , and converges, we obtain:

| (4.35) |

where . We now operate on . If , the left-hand side of (4.35) goes to as so that starting from sufficiently small and taking the limit over on the considered subsequence raises a contradiction. If instead , then since , we have:

Let with . Recall that . Then,

Since as , from Assumption 5, the right-hand side must go to as . Therefore, taking sufficiently small and then consider the limist over on the subsequence under consideration raises a contradiction. Consequently, we must have a.s. A similar reasoning allows to show that a.s. for any given . We conclude thus:

We will now deal with for . Recall that is given by:

where

with:

Using the same reasnoning as with we can show that for sufficiently small and large enough,

with independent of . On the other hand, since , we have:

As a consequence, for sufficiently small and large enough:

where . Now, write as:

Then, one can easily note that:

Combining the results for and , we conclude that for each , there exists small enough such that a.s.,

It remains thus to show that for each , there exists such that for any and all large ,

Recall that are given by:

with are arbitrary and:

where we used the relation . Set for , . We will prove by induction on that for all , thereby showing that . Obviously, the desired result holds for . Assume now that for all , , and let us show that . Since is non-increasing and , we have:

Hence,

We are now in position to control the convergence of as . In particular, we recall that we need to prove that for each , there exists such that:

To this end, define the maps , as:

and

From Lemma 4.7 and 4.6, it is easy to see that the spectral norms of and are uniformly bounded. Note that:

and

for any . Setting large enough so that , we get:

Therefore, one can fix sufficiently large in such a way that:

| (4.36) |

and

| (4.37) |

With this value of at hand, we will now prove that:

To this end, we will work out the differences . We have:

Note that can be bounded as:

Let be the index of the maximum element of . Therefore:

or equivalently,

Hence,

The right-hand side in the above inequality converges to zero as . This is possible if and only if:

| (4.38) |

Function is continuously differentiable. Therefore, by the mean value theorem,

where denotes the derivative of and . Now, since for large enough, and , we obtain:

Since by Assumption 2-, we get:

| (4.39) |

Using the convergences (4.38) and (4.39), we can prove that:

This can be easily seen by noting that:

One can thus choose in such a way that for all

From (4.36) and (4.37), we therefore get for all

In an equivalent way, we therefore have, for each , there exists such that for any and all large ,

Using this result, we will show that for each , there exist small enough, such that a.s.,

To this end, it suffices to show that for each and small enough:

If this was not true, then one can find a sequence over which:

| (4.40) |

for any small . Since the sequence function converge uniformly, one can extract a subsequence from such that and converge uniformly to . On the other hand, we know that for any arbitrairly small there exists such that for any and for all large ,

or also, for all ,

Let be such that . Since is increasing and bounded at infinity by , we have, for any ,

Consider the indices such that , and thus . Take large enough such that:

Then, for those indices, one can prove that:

Consider now the indices such that . For those indices, we have:

Taking , we will get:

which is in contradiction with (4.40). We therefore have for each ,

which therefore implies that . This completes the proof.

Appendix: Technical Lemmas

This appendix gathers some technical Lemmas that will help control quadratic forms of the type:

where are independent random vectors with size and are matrices of size independent of and whose eigenvalues are bounded above and below by constants independent of and . The control of this quadratic form can be performed using the most well-known trace Lemma of Silverstein etal [2, Lemma 2.7], provided that we can guarantee that the infimum of the set of smallest eigenvalues of matrices is above zero uniformly in and or more formally,

for some a.s. for large enough. This is however a challenging task since the question of the smallest eigenvalue of matrices of the form being above zero almost surely was implicitly raised in [19] where this fact was assumed because no immediate answer can be provided in general. It was only recently that we have provided a rigorous proof thereof under the Gaussian setting [1]. In this appendix, we extend this result to the random vector model of the present work, i.e. with and zero-mean unitarily invariant satisfying . The control of the infimum of the set will be shown along the same lines of the proof of Lemma 1 in [7].

In the sequel, we will start by bounding the maximum eigenvalue of when are Gaussian random vectors. To this end, we will start by introducing the following concentration inequality, the proof of which is provided for sake of completeness.

Lemma .11.

Let be independent random variables having an exponential distribution with rate parameter , and , be positive scalars. Then, there exists such that for any :

Proof.

With this Lemma at hand, we will now control the maximum eigenvalue of . We have in particular, the following result:

Lemma .12.

Let be independent standard Gaussian vectors. Consider a family of matrices with uniformly bounded spectral norm, i.e,

Let be given by:

Then, there exists a constant such that a.s. for large enough,

Proof.

The proof relies on the observation that:

Based on the result of Lemma .11, a concentration inequality involving the term can be established. Define and expand as:

Since is unitary, the random quantity is a Gaussian random variable with zero mean and variance . Hence, is a sequence of independent exponential distributed random variables with rate parameter . Applying Lemma .11, we get:

where is some constant independent of and . For , we therefore have:

| (.43) |

With the above inequality at hand, we are now in position to control the behaviour of the spectral norm of . For that, we will resort to the well-known net argument. Let be an net of the unit sphere of . Using Lemma 2.3.2 of [16], we have:

Using (.43), we obtain that each of the probabilities of is bounded by for and large enough with some constant independent of . On the other hand, the cardinality of is of order . By taking large enough, this term can be absorbed into the exponential gain of . For some large enough the event holds with overwhelming probability. Setting . We have thus a.s. for large enough,

∎

All the above results are derived under the assumption of a Gaussian setting. Before going further into the proofs of the main lemmas of this appendix, we will show that the considered random model of the paper is equivalent to a Gaussian model. In particular, we have the following result:

Lemma .13.

Let be independent and identically distributed vectors such that where and are independent and distributed as:

-

•

-

•

is unitarily invariant zero-mean vector such that .

Write as with , and denote by the matrix given by:

where , and are some deterministic matrices with uniformly bounded norm. Let , and be given by:

Then, in the asymptotic regime,

Proof.

Notice that can be written as:

where

Then,

In the sequel, we will prove that the spectral norms of converge to zero almost surely. We will treat only the term since the treatment of and relies on the same arguments. Expanding using , we get:

Let us control .

Using the facts that converges almost surely to zero and and are almost surely bounded as a result of Lemma .12, we have:

Similarly, we can also prove that:

thereby implying that:

∎

Using the same notations of Lemma .13, consider and the matrices given by:

Arguing along the same lines as in the proof of Lemma .13, we can show that:

| (.44) |

This observation is essential to facilitate the proof of the first main result of this Appendix which is about showing that:

In fact, from the convergence inequality in (.44), we can see that the proof can be reduced to showing this result when is replaced with . The proof of the following Lemma will rely on this observation:

Lemma .14.

Let be independent and identically distributed vectors such that where and are independent and distributed as:

-

•

-

•

is unitarily invariant zero-mean vector such that .

Define matrices and as:

where are matrices satisfying:

and

Consider the asymptotic regime of Assumption 1. Therefore, there exists such that for all large a.s.,

Proof.

It is clear from the discussion before the statement of the above lemma that we can assume to be standard Gaussian vectors. Under the Gaussian setting, the fact that the smallest eigenvalue of is almost surely bounded above zero can be deduced from corollary 5 of our work in [1]. It remains thus to treat that of . To this end, we will resort to the same kind of the arguments as those used in the proof of [7, Lemma 1]. Notice first that we can assume without loss of generality that , for all . By definition, the eigenvalues of are solutions in of the following equation:

Developing the above equation, we obtain:

where . If is an eigenvalue of different from that of , then necessarily:

Building on the ideas of [7], we propose to study the behaviour of function:

in a neighborhood of zero. The result of the lemma follows if we prove that there exists such that for all and a.s. for large enough. From our recent result in [1], we know that there exists such that a.s. for large enough, . Functions being increasing in the interval , it suffices thus to show that there exists in such that a.s. for large enough.

Let us start by analyzing the behaviour of for . Define as . Using the matrix inversion relation: for and any invertible matrix, we obtain:

Now, for , using the trace lemma of Silverstein etal [2, Lemma 2.7] in conjunction with the rank-one perturbation Lemma [15, Lemma 2.6], we can prove that:

and thus:

Therefore, for and , we have for large enough a.s.,

| (.45) |

On the other hand, since the smallest eigenvalue of is greater than , we have for large enough, a.s.

| (.46) |

Plugging (.46) into (.45), we obtain that for each we have for large enough, a.s.

| (.47) |

Now, we will consider the analysis of functions on the open interval . Note that on this interval, functions are well-defined and continuously differentiable. Moreover, for each , we have:

Moreover, we have:

The above convergence along with the fact that for large enough a.s. yields:

By bounding the derivatives of functions over , we have by the mean value theorem:

Set . Then, we know from (.47) that:

Combining this inequality with the fact that , yields:

thereby finishing the proof. ∎

We are now in position to state the following key results of this appendix:

Lemma .15.

Let be independent and identically distributed vectors such that where and are independent and distributed as:

-

•

-

•

is unitarily invariant zero-mean vector such that .

Let be random matrices independent of and be a positive constant. Then,

Proof.

Write with . Let be the diagonal matrix given by:

Let . Then:

| (.48) |

Since ,

Therefore, it is easy to see that the maximum over of the first three terms in (.51) converge to zero almost surely. The problem unfolds thus to the control of . Let denote the expectation with respect to . From the trace Lemma of Silverstein etal [2, Lemma 2.7] applied for , we obtain:

where is any upper-bound on and a constant dependent only in . Since , we have:

This bound being independent of , we can take the expectation with respect to to obtain:

Therefore,

∎

Lemma .16.

Let be independent and identically distributed vectors such that where and are independent and distributed as:

-

•

-

•

is unitarily invariant zero-mean vector such that where .

Denote by a family of deterministic matrix that satisfy

Consider the asymptotic regime of Assumption 1. Let be given as:

Assume that there exists such that for all large a.s.,

Then, for any with bounded spectral norm,

| (.49) |

where are the unique solutions to the following system of equations:

Proof.

To prove lemma .16, we show first that:

From the resolvent identity, we have:

Since there exists such that for all large a.s.

and is almost surely bounded, we have:

| (.50) |

Similarly to the previous Lemma, write , and let . Denote by . Then from Lemma .13,

Therefore,

| (.51) |

Hence, plugging (.51) into (.50), we get:

The asymptotic convergence of has been studed in [19] for . Since the smallest eigenvalue of is almost surely away from zero, we can extend the convergence results for by using the same arguments as those presented in [8, footnote in page 20]. ∎

References

- [1] S. Alouini A. Kammoun. On the Smallest Eigenvalue of General Gaussian Matrices. Submitted to IEEE Transactions on Information Theory, 2014.

- [2] Z. D. Bai and J. W. Silverstein. No eigenvalues outside the support of the limiting spectral distribution of large-dimensional sample covariance matrices. Ann. Probab., 26(1):316–345, 1998.

- [3] P. Bianchi, J. Najim, M. Maida, and M. Debbah. Performance analysis of some eigen-based hypothesis tests for collaborative sensing. In IEEE 15th Workshop on Statistical Signal Processing (SSP’09), pages 5–8, Cardiff, Wales, September 2009.

- [4] L. S. Cardoso, M. Debbah, P. Bianchi, and J. Najim. Cooperative spectrum sensing using random matrix theory. In International Symposium on Wireless Pervasive Computing (ISWPC’08), pages 334–338, Santorini, Greece, May 2008.

- [5] Y. Chitour, R. Couillet, and F. Pascal. On the Convergence of Maronna’s M-Estimators of Scatter. IEEE Signal Processing Letters, 2014.

- [6] R. Couillet and M. McKay. Large Dimensional Analysis and Optimization of Robust Shrinkage Covariance Matrix Estimators. To appear in Joint of Multivariate Analysis, 2013.

- [7] R. Couillet, F. Pascal, and J. W. Silverstein. Robust M-Estimation for Array Processing: A Random Matrix Approach. IEEE Transactions on Information Theory, 61(16):4141–4148, 2013.

- [8] R. Couillet, F. Pascal, and J. W. Silverstein. The Random Matrix Regime of Maronna’s M-Estimator With Elliptically Distributed Samples. submitted, 2013.

- [9] P. J. Huber. Robust Statistics. Wiley Series in Probability and Statistics John Wiley & Sons, 1981.

- [10] R. A. Maronna. Robust M-Estimators of Multivariate Location and Scatter. The Annals of Statistics, pages 51–67, 1976.

- [11] X. Mestre. Improved Estimation of Eigenvalues of Covariance Matrices and their Associated Subspaces using their Sample Estimates. IEEE Transactions on Information Theory, 54(11):5113–5129, 2008.

- [12] R. J. Murihead. Aspects of Multivariate Statistical Analysis. John Wiley &Sons, Inc., 1982.

- [13] B. Nadler. Nonparametric Detection of Signals by Information Theoretic Criteria: Performance Analyis and Improved Estimator. IEEE Transactions on Signal Processing, 58(5):2764–2756, 2010.

- [14] P. Vallet and P. Loubaton and X. Mestre. Improved Subspace Estimation for Multivariate Observations of High Dimension: The Deterministic Signals Case. IEEE Transactions on Information Theory, 58(2), February 2012.

- [15] J. W. Silverstein and Z. D. Bai. On the empirical distribution of eigenvalues of a class of large-dimensional random matrices. J. Multivariate Anal., 54(2):175–192, 1995.

- [16] T. Tao. Topics in Random Matrix Theory, volume 132. American Mathematical Society, Graduate Studies in Mathematics, 2012.

- [17] S. Valaee, B. Champagne, and P. Kabal. Parametric Localization of Distributed Sources. IEEE Transactions on Signal Processing, 43(9), September 1995.

- [18] W. Hachem and P. Loubaton and X. Mestre and J. Najim and P. Vallet. A Subspace Estimator for Fixed Rank Perturbations of Large Random Matrices. Journal of Multivariate Analysis, 114:427–447, February 2013.

- [19] S. Wagner, R. Couillet, M. Debbah, and D. T. M. Slock. Large System Analysis of Linear Precoding in Correlated MISO Broadcast Channels Under Limited Feedback. IEEE Transactions on Information Theory, 58(7), July 2012.

- [20] R. D. Yates. A Framework for Uplink Power Control in Cellular Radio Systems. IEEE Journal on Selected Areas in Communications, 13(7):1341–1347, 1995.