Nonparametric tests for detecting breaks in the jump behaviour of a time-continuous process

Abstract

This paper is concerned with tests for changes in the jump behaviour of a time-continuous process. Based on results on weak convergence of a sequential empirical tail integral process, asymptotics of certain tests statistics for breaks in the jump measure of an Itō semimartingale are constructed. Whenever limiting distributions depend in a complicated way on the unknown jump measure, empirical quantiles are obtained using a multiplier bootstrap scheme. An extensive simulation study shows a good performance of our tests in finite samples.

Keywords and Phrases: Change points; Lévy measure; multiplier bootstrap; sequential empirical processes; weak convergence.

AMS Subject Classification: 60F17, 60G51, 62G10.

1 Introduction

Recent years have witnessed a growing interest in statistical tools for high-frequency observations of time-continuous processes. With a view on finance, the seminal paper by Delbaen and Schachermayer (1994) suggests to model such a process using Itō semimartingales, say , which is why most research has focused on the estimation of (or on tests concerned with) its characteristics. Particular interest has been paid to integrated volatility or the entire quadratic variation, mostly adapting parametric procedures based on normal distributions, as the continuous martingale part of an Itô semimartingale is nothing but a time-changed Brownian motion. For an overview on methods in this field see the recent monographs by Jacod and Protter (2012) and Aït-Sahalia and Jacod (2014).

Still less popular is inference on the jump behaviour only, even though empirical research shows a strong evidence supporting the presence of a jump component within ; see e.g. Aït-Sahalia and Jacod (2009b) or Aït-Sahalia and Jacod (2009a). In this work, we will address the question whether the jump behaviour of is time-invariant. Corresponding tests, commonly referred to as change point tests, are well known in the framework of discrete time series, but have recently also been extended to time-continuous processes; see e.g. Lee et al. (2006) on changes in the drift or Iacus and Yoshida (2012) on changes in the volatility function of . However, to the best of our knowledge, no procedures are available for detecting breaks in the jump component.

Suppose that we observe an Itō semimartingale which admits a decomposition of the form

| (1.1) |

where is a standard Brownian motion, is a Poisson random measure on , and the predictable compensator satisfies . As a fairly general structural assumption, we allow the characteristics of , i.e. and to depend deterministically on time. Recall that can be interpreted as a local Lévy measure, such that

for each and denotes the average number of jumps that fall into the set over a unit time interval.

Now, we assume that we have data from the process in a high-frequency setup. Precisely, at stage , we are able to observe realizations of the process at the equidistant times for , where the mesh , while . In this situation we want to test the null hypothesis that the jump behaviour of the process is the same for all observations, i.e. there exists some measure such that for all , against alternatives involving the non-constancy of . For instance, one might consider an alternative consisting of one break point, i.e. there exists some and two Lévy measures , such that the process behind the first observations has Lévy measure and the remaining observations are taken from a process with Lévy measure . The restriction to a deterministic drift and volatility in (1.1) is merely technical here, as it allows to use empirical process theory for independent observations later. An argument similar to that in Section 5.3 in Bücher and Vetter (2013) proves that one might as well work with random coefficients and .

Throughout the work, we will restrict ourselves to positive jumps only. Thus, for , let denote the tail integral (or spectral measure; see Rüschendorf and Woerner, 2002) associated with , which determines the jump measure uniquely. For such that , define

with , which serves as an empirical tail integral based on the increments . If is a Lévy process with a Lévy measure not changing in time, Figueroa-Lopez (2008) illustrated that is a suitable estimator for the tail integral in the sense that, under regularity conditions, is -consistent for . Following the approach in Inoue (2001), it is therefore likely that we can base tests for on suitable functionals of the process

where and . Under the null hypothesis, this expression can be expected to converge to for all and , whereas under alternatives, for instance those involving a change at as described before, should converge to an expression which is non-zero.

More precisely, we will consider the following standardized version of , namely

| (1.2) |

for and , where . An appropriate functional allowing to test the hypothesis of a constant Lévy measure is for instance given by a Kolmogorov-Smirnov statistic of the form

| (1.3) |

The null hypothesis of no change in the Lévy measure is rejected for large values of . The restriction to jumps larger than is important, since there might be infinitely many of arbitrary small size.

The limiting distribution of the previously mentioned test statistic will turn out to depend in a complicated way on the unknown Lévy measure . Therefore, corresponding quantiles are not easily accessible and must be obtained by suitable bootstrap approximations. Following related ideas for detecting breaks within multivariate empirical distribution functions (Inoue, 2001), we opt for using empirical counterparts based on a multiplier bootstrap scheme, frequently also referred to as wild or weighted bootstrap. The approach essentially consists of multiplying each indicator within the respective empirical tail integrals with an additional, independent and standardized multiplier. The underlying empirical process theory is for instance summarized in the monograph Kosorok (2008).

The remaining part of this paper is organized as follows: the derivation of a functional weak convergence result for the process under the null hypothesis is the content of Section 2. The asymptotic properties of can then easily be derived from the continuous mapping theorem. Section 3 is concerned with the approximation of the limiting distribution using the previously described multiplier bootstrap scheme. In Section 4, we discuss the formal derivation of several tests for a time-homogeneous jump behaviour, whereas an extensive simulation study is presented in Section 5. All proofs are deferred to the Appendix, which is Section 6.

2 Functional weak convergence of the sequential empirical tail integral

In this section, we derive a functional weak convergence result for the process defined in (1.2). For that purpose, we have to introduce an appropriate function space. We set and let denote the space of all functions which are bounded on every set for which the projection onto the second coordinate, , is bounded away from . Moreover, for , we define , and, for , we set

where Note that defines a metric on which induces the topology of uniform convergence on all sets such that its projection is bounded away from , i.e. a sequence of functions converges with respect to if and only if it converges uniformly on each (Van der Vaart and Wellner, 1996, Chapter 1.6).

Furthermore to establish our results on weak convergence under the null hypothesis, we impose the following conditions.

Condition 2.1.

is an Itō semimartingale with the representation in (1.1) such that

-

(a)

The drift and the volatility are càglàd, bounded and deterministic.

-

(b)

There exists some Lévy measure such that for all .

-

(c)

has only positive jumps, that is, the jump measure is supported on .

-

(d)

is absolutely continuous with respect to the Lebesgue measure on . Its density , called Lévy density, is differentiable with derivative and satisfies

for all with . ∎

The next lemma is essential for the weak convergence results. Similar statements can be found in Figueroa-Lopez and Houdre (2009), with slightly stronger assumptions on , and in Bücher and Vetter (2013) in the bivariate case.

Lemma 2.2.

Remark 2.3.

The limiting behaviour of the process can be deduced from the next theorem, which is a result for weak convergence of a sequential empirical tail integral process. For and set

| (2.1) |

where and denote its standardized version by

| (2.2) |

Obviously, the sample paths of are elements of .

Theorem 2.4.

Let be an Itō semimartingale that satisfies Condition 2.1. Furthermore, assume that the observation scheme has the properties:

Then, in , where is a tight mean zero Gaussian process with covariance

for . The sample paths of are almost surely uniformly continuous on each ) with respect to the semimetric

with

Note that we have centered around its expectation in (2.2). In most applications, however, we are interested in estimating functionals of the jump measure, and according to Lemma 2.2 we need stronger conditions then. Precisely, we consider the process

and get, as an immediate consequence of the previous two results, the following sequential generalization of Theorem 4.2 of Bücher and Vetter (2013).

Corollary 2.5.

A further consequence of Theorem 2.4 is the desired weak convergence of the process , which was defined in (1.2), under the null hypothesis.

Theorem 2.6.

Using the continuous mapping theorem, we are now able to derive the weak convergence of various statistics allowing for the detection of breaks in the jump behaviour. The following corollary treats the statistic defined in (1.3).

Corollary 2.7.

The covariance function of the limit process in Theorem 2.6 depends on the Lévy measure of the underlying process, which is usually unknown in applications. If one only wants to detect changes in the tail integral of the Lévy measure at a fixed point , the following proposition deals with the simple transformation

of which yields a pivotal limiting distribution.

Proposition 2.8.

Let be an Itō semimartingale that satisfies Condition 2.1. Moreover, let be a real number with and suppose that the underlying observation scheme meets the assumptions from Corollary 2.5. Then, in , where denotes a standard Brownian bridge. As a consequence,

the limiting distribution being also known as the Kolmogorov-Smirnov distribution.

Remark 2.9.

We have derived the previous results under somewhat simplified assumptions on the observation scheme in order to keep the presentation rather simple. A more realistic setting could involve additional microstructure noise effects or might rely on non-equidistant data. In both cases, standard techniques still yield similar results.

For example, in case of noisy observations, Vetter (2014) has shown that a particular de-noising technique allows for virtually the same results on weak convergence as for the plain in the case without noise. For non-equidistant data, the limiting covariance functions and in general depend on the sampling scheme. The latter effect is well-known from high-frequency statistics in the case of volatility estimation; see e.g. Mykland and Zhang (2012). ∎

3 Bootstrap approximations for the sequential empirical tail integral

We have seen in Corollary 2.7 that the distribution of the limit of the process depends in a complicated way on the unknown Lévy measure of the underlying process. However, we need the quantiles of or at least good approximations for them to obtain a feasible test procedure. Typically, one uses resampling methods to solve this problem.

Probably the most natural way to do so is to use in order to obtain an estimator for the Lévy measure first, and to draw a large number of independent samples of an Itō semimartingale with Lévy measure then, possibly with estimates for drift and volatility as well. Based on each sample, one might then compute the test statistic , and by doing so one obtains empirical quantiles for .

However, from a computational side, such a method is computationally expensive since one has to generate independent Itō semimartingales for each stage within the bootstrap algorithm. Therefore we have decided to work with an alternative bootstrap method based on multipliers, where one only needs to generate i.i.d. random variables with mean zero and variance one (see also Inoue, 2001, who used a similar approach in the context of empirical processes).

Precisely, the situation now is as follows: The bootstrapped processes, say , will depend on some random variables and on some random weights . The , that we consider as collected data, are defined on a probability space . The random weights are defined on a distinct probability space . Thus, the bootstrapped processes live on the product space . The following notion of conditional weak convergence will be essential. It can be found in Kosorok (2008) on pp. 19–20.

Definition 3.1.

Let be a (bootstrapped) element in some metric space depending on some random variables and some random weights . Moreover, let be a tight, Borel measurable map into . Then converges weakly to conditional on the data in probability, notationally , if and only if

-

(a)

-

(b)

for all

Here, denotes the conditional expectation over the weights given the data , whereas is the space of all real-valued Lipschitz continuous functions on with sup-norm and Lipschitz constant . Moreover, and denote a minimal measurable majorant and a maximal measurable minorant with respect to the joint data (including the weights ), respectively. ∎

Remark 3.2.

-

(i)

Note that we do not use a measurable majorant or minorant in item (a) of the definition. This is justified through the fact that, in this work, all expressions , with a bootstrapped statistic and a Lipschitz continuous function , are measurable functions of the random weights.

-

(ii)

Note that the implication “(ii) (i)” in the proof of Theorem 2.9.6 in Van der Vaart and Wellner (1996) shows that, in general, conditional weak convergence implies unconditional weak convergence with respect to the product measure . ∎

Throughout this paper we denote by

the bootstrap approximation which is defined by

where . The following theorem establishes conditional weak convergence of this bootstrap approximation for the sequential empirical tail integral process .

Theorem 3.3.

Let be an Itō semimartingale that satisfies Condition 2.1 and assume that the observation scheme meets the conditions from Theorem 2.4. Furthermore, let be independent and identically distributed random variables with mean and variance , defined on a distinct probability space as described above. Then,

in , where denotes the limiting process of Theorem 2.4.

Theorem 3.3 suggests to define the following bootstrapped counterparts of the process defined in equation (1.2):

The following result establishes consistency of in the sense of Definition 3.1.

Theorem 3.4.

The distribution of the Kolmogorov-Smirnov-type test statistic defined in (1.3) can be approximated with the bootstrap statistics investigated in the following corollary. It can be proved by a simple application of Proposition 10.7 in Kosorok (2008) on an appropriate .

Corollary 3.5.

Under the assumptions of Theorem 3.3 we have, for each ,

4 The testing procedures

4.1 Hypotheses

In order to derive a test procedure which utilizes the results on weak convergence from the previous two sections, we have to formulate our hypotheses first. Under the null hypothesis the jump behaviour of the process is constant. More precisely, this means the following:

- :

We want to test this hypothesis versus the alternative that there is exactly one change in the jump behaviour. This means in detail:

- :

The corresponding alternative for a fixed is then given through:

-

:

We have the situation from , but with and .

4.2 The tests and their asymptotic properties

In the sequel, let be some large number and let denote independent vectors of i.i.d. random variables, , with mean zero and variance one. As before, we assume that these random variables are generated independently from the original data. We denote by or the particular statistics calculated with respect to the data and the -th bootstrap multipliers . For a given level , we consider the following test procedures:

-

KSCP-Test1.

Reject in favor of , if , where is defined in Proposition 2.8 and where denotes the quantile of the Kolmogorov-Smirnov-(KS-)distribution, that is the distribution of with a standard Brownian bridge .

-

KSCP-Test2.

Reject in favor of , if

where denotes the -sample quantile of , and where

-

CP-Test.

Choose an appropriate small and reject in favor of , if

where denotes the -sample quantile of .

Since has to be chosen prior to an application of the CP-Test, we can only detect changes in the jumps larger than . From a theoretical point of view this is not entirely satisfactory, since one is interested in distinguishing arbitrary changes in the jump behaviour. On the other hand, in most applications only the larger jumps are of particular interest, and at least the size of provides a natural bound to disentangle jumps from volatility. Thus, a practitioner can choose a minimum jump size first, and use the CP-Test to decide whether there is a change in the jumps larger than .

The following proposition shows that three aforementioned tests keep the asymptotic level under the null hypothesis.

Proposition 4.1.

Suppose the sampling scheme meets the conditions of Corollary 2.5. Then, KSCP-Test1, KSCP-Test2 and CP-Test are asymptotic level tests for in the sense that, under , for all ,

and

for all such that .

The next proposition shows that the preceding tests are consistent under the fixed alternatives defined in Section 4.1. For simplicity, we only consider alternatives involving one change point, even though the results may be extended to alternatives involving multiple breaks or even continuous changes.

Proposition 4.2.

Suppose the sampling scheme meets the conditions of Corollary 2.5. Then, KSCP-Test1, KSCP-Test2 and CP-Test are consistent in the following sense: under , for all and all , we have

Under , there exists an such that, for all and all ,

4.3 Locating the change point

Let us finally discuss how to construct suitable estimators for the location of the change point. We begin with a useful proposition.

Proposition 4.3.

Suppose the sampling scheme meets the conditions of Corollary 2.5. Then, under , converges in to the function

in outer probability, with and .

Since attains its maximum in , natural estimators for the position of the change point are therefore given by

for the test problem versus and

in the setup versus . The next proposition states that these estimators are consistent.

Proposition 4.4.

Suppose the sampling scheme meets the conditions of Corollary 2.5. If is true, there exists an such that as . In the special case of , we have

5 Finite-sample performance

In this section, we present results of a large scale Monte Carlo simulation study, assessing the finite-sample performance of the proposed test statistics for detecting breaks in the Lévy measure. Moreover, under the alternative of one single break, we show results on the performance of the estimator for the break point from Section 4.3.

The experimental design of the study is as follows.

-

•

We consider five different choices for the number of trading days, namely , and corresponding frequencies . Note that for any of these choices.

-

•

We consider two different models for the drift and the volatility: either, we set or , resulting in a pure jump process and a process including a continuous component, respectively.

-

•

We consider one parametric model for the tail integral, namely

(5.1) (which yields a -stable subordinator in the case of ). For the parameter , we consider different choices, that is , with , ranging from to .

-

•

We consider models with one single break in the tail integral at different break points, ranging form to (note that corresponds to the null hypothesis). The tail integrals before and after the break point are chosen from the previous parametric model.

The target values of our study are, on the one hand, the empirical rejection level of the tests and, on the other hand, the empirical distribution of the estimators for the change point . To assess these target values, any combination of the previously described settings was run times, with the bootstrap tests being based on bootstrap replications. The Itō semimartingales were simulated by a straight-forward modification of Algorithm 6.13 in Cont and Tankov (2004), where, under alternatives involving one break point, we simply merged two paths of independent semimartingales together.

The simulation results under these settings are partially reported in Table 1 and 2 (for the null hypothesis) and in Figures 1–4 (for various alternatives). More precisely, Table 1 and 2 contain simulated rejection rates under the null hypothesis for various values of and in the KSCP-tests, for the pure jump subordinator (Table 1) and for the process involving a continuous component (Table 2). For the CP-tests, the suprema over were approximated by taking a maximum over a finite grid : we used the grids in the pure jump case, resulting in , and in the case , resulting in . In the latter case, we chose depending on since jumps of smaller size may be dominated by the Brownian component resulting in a loss of efficiency of the CP-test (see also the results in Figure 3 below). The results in the two tables reveal a rather precise approximation of the nominal level of the tests () in all scenarios. In general, KSCP-Test 1 turns out to be slightly more conservative than KSCP-Test 2.

| CP-Test | Pointwise Tests | ||||||

|---|---|---|---|---|---|---|---|

| 0.06 | KSCP-Test 1 | ||||||

| KSCP-Test 2 | |||||||

| 75 | 0.054 | KSCP-Test 1 | |||||

| KSCP-Test 2 | |||||||

| 100 | 0.06 | KSCP-Test 1 | |||||

| KSCP-Test 2 | |||||||

| 150 | 0.06 | KSCP-Test 1 | |||||

| KSCP-Test 2 | |||||||

| 250 | 0.07 | KSCP-Test 1 | |||||

| KSCP-Test 2 |

| CP-Test | Pointwise Tests | |||||

|---|---|---|---|---|---|---|

| 0.049 | KSCP-Test 1 | |||||

| KSCP-Test 2 | ||||||

| 75 | 0.050 | KSCP-Test 1 | ||||

| KSCP-Test 2 | ||||||

| 100 | 0.051 | KSCP-Test 1 | ||||

| KSCP-Test 2 | ||||||

| 150 | 0.057 | KSCP-Test 1 | ||||

| KSCP-Test 2 | ||||||

| 250 | 0.049 | KSCP-Test 1 | ||||

| KSCP-Test 2 |

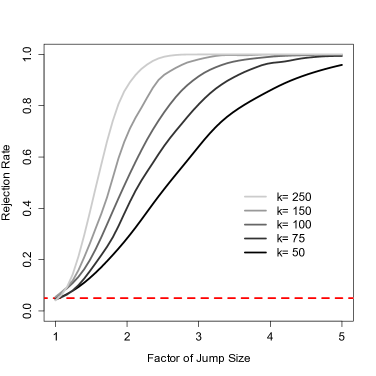

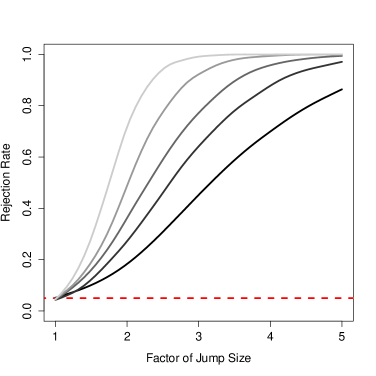

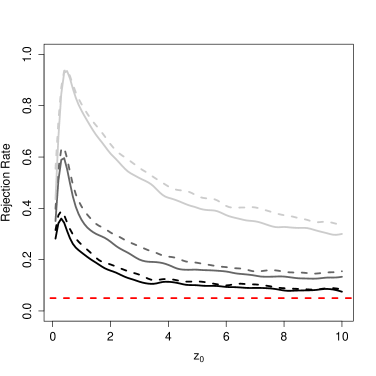

The results presented in Figure 1 consider the CP-test for alternatives involving one fixed break point at and a varying height of the jump size, as measured through the value of in (5.1). In contrast to the results in Tables 1 and 2, due to computational reasons, we subsequently used smaller grids for the case , resulting in , and for the case , resulting in . The left plot is based on the pure jump process (), whereas the right one is based on . The dashed red line indicates the nominal level of . We observe that the rejection rate of the test is increasing in (as to be expected) and in . The latter can be explained by the fact that represents the effective sample size (interpretable as the number of trading days). Finally, the rejection rates turn out to be higher when no continuous component is involved in the underlying semimartingale.

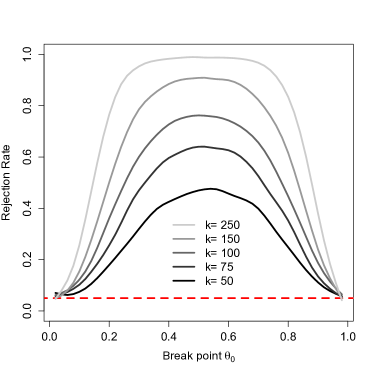

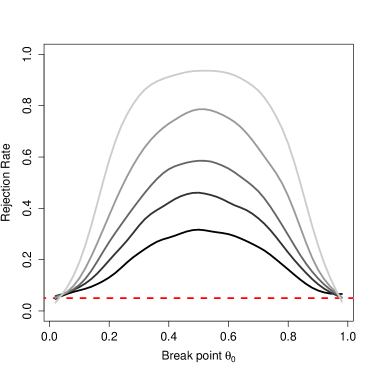

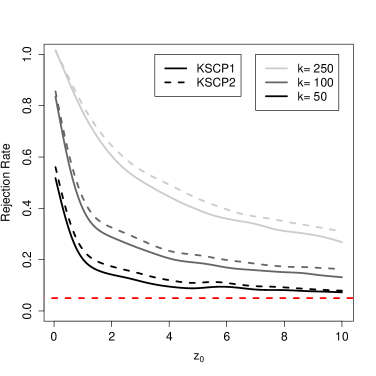

The next two graphics in Figure 2 show the rate of rejection of the CP-Test under alternatives involving one break point from to within the model in (5.1) for varying locations of the change point . Again, the left and right plots correspond to and , respectively. Additionally to the general conclusions drawn from the results in Figure 1, we observe that break points can be detected best if , and that the rejection rates are symmetric around that point.

Figure 3 shows the rejection rates of the KSCP-Test 1 and 2, evaluated at different points , for one fixed alternative model involving a single change from to at the point . The curves in the left plot are based on a pure jump process. We can see that the rejection rates are decreasing in , explainable by the fact that there are only very few large jumps both for and for . In the right plot, involving drift and volatility (), we observe a maximal value of the rejection rates that is increasing in the number of trading days, . For values of smaller than this maximum, the contribution of the Brownian component (an independent normally distributed term with variance within each increment ) predominates the jumps of that size and results in a decrease of the rejection rate.

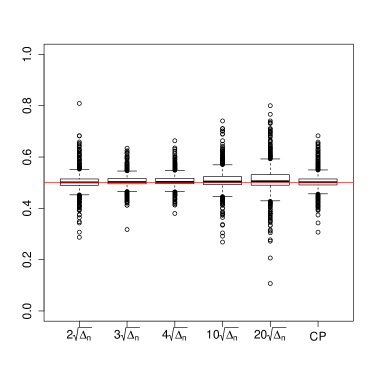

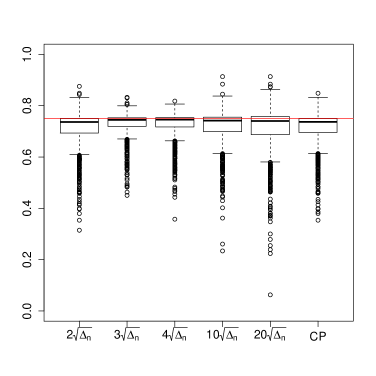

Finally, in Figure 4, we depict box plots for the estimators and of the change point for certain values of and for as specified in the case of Tables 1 and 2. The results are based on two models, involving a change in from to at time point (left panel) and (right panel) for and , and with . We observe a reasonable approximation of the true value (indicated by the red line) with more accurate approximations for . For , the distribution of the estimator is skewed, giving more weight to the left tail directing to . This might be explained by the fact that the distribution of the argmax absolute value of a tight-down stochastic process indexed by gives very small weight to the boundaries of the unit interval. Moreover, as for the results presented in the right plot of Figure 3, the plots in Figure 4 reveal that the estimator behaves best for an intermediate choice of . Results for are not depicted for the sake of brevity, since they do not transfer any additional insight.

6 Appendix

6.1 Proof of Lemma 2.2

Let and pick a smooth cut-off function satisfying

We also define the function via . We use to define the “large” jumps of the process, that means, there exist independent processes and such that where is a compound Poisson process with intensity and jump distribution . See e.g. Figueroa-Lopez and Houdre (2009). Accordingly, is an Itō semimartingale with characteristics , where we set .

Since our result is a distributional one only, it is possible to work with this particular representation of in the following. Call the number of jumps of up to time . Define . Using the law of total expectation we have

| (6.1) |

where the random variables are i.i.d. with distribution .

For the first summand on the right of the last display, i.e. the case of no large jumps, we discuss drift, volatility and small jumps separately. For that purpose, we write where , and where is a pure jump Lévy martingale with jump measure . By the triangle inequality

Let us show that the right-hand side of this display can be bounded by for all , with constants and . Regarding the summand , we can use equation (3.3) in Figueroa-Lopez and Houdre (2009) applied to a pure jump Lévy process. Following their result, ensures the existence of and , both depending on only, such that

| (6.2) |

for all . Since and are bounded, we further have and for an arbitrary integer and with depending on again. Markov’s inequality then yields bounds similar to (6.2) when applied to the processes involving drift, , and volatility, .

Also, for the sum over on the right-hand side of (6.1), we have

It therefore remains to focus on . As a consequence of Condition 2.1(d), and observing that the distribution of is with the Lévy density , it follows that

is twice continuously differentiable with bounded derivatives. Using independence of and , it is sufficient to discuss , for which we can use Itô formula now: for arbitrary we have

| (6.3) |

where denotes the quadratic variation and is the jump size at time . Plugging in for we discuss each of the four summands in (6.3) separately: first, implies by definition of . Thus, with

Second, two of the three summands in are martingales. Therefore

due to boundedness of the first derivatives of . We may proceed similarly for the third term in (6.3). Finally, conditioning on and using the definition of a compensator gives

for the final quantity. The Taylor formula proves that the inner integrand above may be bounded in absolute value by . Since is a Lévy measure, we obtain

From for the conclusion follows. ∎

6.2 Proof of Theorem 2.4

Due to Theorem 1.6.1 in Van der Vaart and Wellner (1996), it suffices to prove weak convergence in for any fixed .

To this end, we use Theorem 11.16 of Kosorok (2008). Note that can be written as

with the triangular array consisting of the processes

which are independent within rows since we assume a deterministic drift and volatility. By Theorem 11.16 in Kosorok (2008), the proof is complete if the following six conditions for can be established:

-

(1)

is almost measurable Suslin (AMS);

-

(2)

the are manageable with envelopes given through , which are also independent within rows;

-

(3)

for all ;

-

(4)

;

-

(5)

for all ;

-

(6)

for every , where

Moreover, for all sequences and such that .

Proof of (1). By Lemma 11.15 in Kosorok (2008), the triangular array is AMS provided it is separable, i.e., provided for every , there exists a countable subset , such that

Define for all . Then, for every element of the underlying probability space and for every , there exists an such that

Proof of (2). The are independent within rows since we assume deterministic characteristics of the underlying process. Therefore, according to Theorem 11.17 in Kosorok (2008), it suffices to prove that the triangular arrays

and

are manageable with envelopes and , respectively.

Concerning the first triangular array define, for and ,

For any , the projection of onto the -th and the -th coordinate is an element of the set

Hence, for every , no proper coordinate projection of can surround in the sense of Definition 4.2 of Pollard (1990). Thus, is a subset of of pseudodimension at most (Definition 4.3 in Pollard, 1990). Additionally, is a bounded set, whence Corollary 4.10 in Pollard (1990) yields the existence of constants and , depending only on the pseudodimension, such that

for all , for every rescaling vector with non-negative entries and for all and . Therein, denotes the Euclidean distance, denotes the packing number with respect to the Euclidean distance and is the vector of envelopes. Since , the triangular array is indeed manageable with envelopes .

Concerning the triangular array , we proceed similar and consider the set

Then, for any , the projection of onto the -th and the -th coordinate is either or . Therefore, the same reasoning as above shows that is a set of pseudodimension at most one, whence the triangular array is manageable with envelopes .

Proof of (3). For any , by independence of within rows, we can write

| (6.4) |

By Remark 2.3 and the choice and , we have

| (6.5) |

for all and all , whence the right-hand side of equation (6.2) can be written as

Proof of (5). For define . Choose and as in Lemma 2.2. Then, for any sufficiently large such that , we have

Proof of (6). For , we can write

as , where the -terms are uniform in for the same reason as in equation (6.5). Thus converges even uniformly on each to . Consequently, for any sequences such that , it follows .

Finally, is a semimetric: applying first the triangle inequality in and then the Minkowski inequality, one sees that each satisfies the triangle inequality. Thus the triangle inequality also holds for . ∎

6.3 Proof of Corollary 2.5

6.4 Proof of Theorem 2.6

We are going to use the extended continuous mapping theorem (Theorem 1.11.1 in Van der Vaart and Wellner, 1996). For , define through

| and | ||||

Note that is Lipschitz continuous for any .

Obviously, for each and . We have

and the proof of Corollary 2.5 shows that converges to in . Thus, by Slutsky’s theorem (Van der Vaart and Wellner, 1996, Example 1.4.7), it suffices to verify .

Due to Theorem 1.11.1 in Van der Vaart and Wellner (1996) (note that is separable as it is tight; see Lemma 1.3.2 in the last-named reference) this weak convergence is valid, if we can show that, for any sequence with for some , we have

Let be such a sequence with limit point . Convergence in is equivalent to uniform convergence on each with . The latter is true since

Obviously, is a tight, mean-zero Gaussian process. Moreover, from Theorem 2.4,

for any . ∎

6.5 Proof of Proposition 2.8

Because of Corollary 2.5 (and the continuous mapping theorem) converges to in probability. Therefore, it follows easily that the random variable converges to in probability. Hence, by Slutsky’s theorem (Van der Vaart and Wellner, 1996, Example 1.4.7) we obtain

By Theorem 2.6 the process on the right-hand side of this display is a tight mean zero Gaussian with covariance function . Thus, the law of that process is the law of a standard Brownian bridge on . ∎

6.6 Proof of Theorem 3.3

Due to Lemma 6.2 below it suffices to prove conditional weak convergence on for any fixed . Recall the triangular array consisting of the processes

Set and let

be an estimator for . Then, can be written as

Due to Theorem 3 in Kosorok (2003) the proof is complete, if we show the following properties for the triangular array :

-

(i)

is almost measurable Suslin.

-

(ii)

-

(iii)

The triangular array is manageable with envelopes given through .

-

(iv)

There exists a constant such that .

Proof of (i). As in the proof of (1) in Theorem 2.4, it suffices to verify that the triangular array is separable. This can be seen by taking again.

Proof of (ii). We have

where the final approximation error is a consequence of equation (6.5) in the proof of Theorem 2.4. The last quantity in the above display converges to in probability by Theorem 2.4.

Proof of (iii). In the proof of Theorem 2.4 we have already shown that the triangular array

is manageable with envelopes . Therefore, due to Theorem 11.17 in Kosorok (2008), it suffices to prove that the triangular array

is manageable with envelopes . But does not depend on at all, such that every projection of onto two coordinates lies in the straight line . Consequently, the set has a pseudodimension of at most (Definition 4.3 in Pollard, 1990) and is bounded. Hence, the same arguments as in the proof of Theorem 2.4 show the desired manageability.

6.7 Proof of Theorem 3.4

Again by Lemma 6.2 it suffices to prove the convergence in the spaces . Let therefore be fixed for the rest of the proof.

By definition, in , with defined in the proof of Theorem 2.6. Now, is a Banach space and the mapping defined in the proof of Theorem 2.6 is Lipschitz continuous. Hence, Proposition 10.7(i) in Kosorok (2008) yields the convergence

in . Furthermore, due to the definition of the mappings and the definition of the process we obtain that

By Theorem 3.3, the right-hand side converges to in probability. Another application of Lemma 6.1 shows that as asserted. ∎

6.8 Proof of Proposition 4.1

The assertion that under is a simple consequence of Proposition 2.8 and the fact that the KS-distribution has a continuous cumulative distribution function.

With respect to the assertion regarding note that, under , Proposition 6.3 and the continuous mapping theorem imply that, for any fixed ,

in , where with the limit process of Theorem 2.6 and where are independent copies of . According to the corollary to Proposition 3 in Lifshits (1984), has a continuous c.d.f. under . Thus, Proposition F.1 in the supplement to Bücher and Kojadinovic (2014) implies that

for all , as asserted. Observing that, under and for with , the distribution of has a continuous c.d.f., essentially the same reasoning also implies that

for all . ∎

6.9 Proof of Proposition 4.2

In order to prove consistency of the CP-Test, choose as in Proposition 6.4 such that for any . By Proposition 6.5, for given and fixed , we may choose such that

For this , we can now take such that

holds for all . Then, for any ,

This proves the assertion for the CP-Test, and the claim for KSCP-Test2 follows along the same lines. The assertion for KSCP-Test1 is a direct consequence of Proposition 6.4. ∎

6.10 Proof of Proposition 4.3

Let and denote two independent Itō semimartingales with characteristics and , respectively. For and , set and . Let and denote the quantity defined in (2.1), based on the observations and , respectively, instead on . Moreover, define a random element with values in through

for with , whereas for with ,

According to Theorem II.4.15 in Jacod and Shiryaev (2002), we have the distributional equality

Hence, for any and , we also have that

By Theorem 1.6.1 in Van der Vaart and Wellner (1996), we have to show uniform convergence of to on any with , in probability. Now, from the previous display, and from the fact that the function is continuous in and that the functions depend only through on and are left-continuous in , we immediately get that

This expression is in fact as a consequence of Corollary 2.5 and the continuous mapping theorem. Note that the proofs of Lemma 2.2, Theorem 2.4 and Corollary 2.5 show that Corollary 2.5 is in fact applicable in this setup, because the characteristics and have a uniform bound in and the resulting constants of Lemma 2.2 depend only on the bound of the characteristics and on . ∎

6.11 Proof of Proposition 4.4

Under , choose such that there exists a with . Then, according to Proposition 4.3 and the continuous mapping theorem, the random functions converge weakly in to the continuous function , which has a unique maximum at .

Similarly, under , the random functions converge weakly in to the continuous function , which also has a unique maximum in .

Thus, the asserted convergences follow from the argmax-continuous mapping theorem (Theorem 2.7 in Kim and Pollard, 1990). ∎

6.12 Additional auxiliary results

The following two auxiliary results are needed for validating the bootstrap procedures defined in Section 3. The first lemma is proved in Bücher (2011), Lemma A.1.

Lemma 6.1.

Consider two bootstrapped statistics and in a metric space with . Then, for a tight Borel measurable process in , we have if and only if .

For the second auxiliary lemma, let be arbitrary sets and set . Let be defined as the complete metric space of all real-valued functions on that are bounded on each , equipped with the metric

where denotes the sup-norm on (Van der Vaart and Wellner, 1996, Chapter 1.6). Bootstrap variables on such spaces converge weakly conditionally in probability if and only if the same holds true in for all .

Lemma 6.2.

Let be a bootstrapped statistic with values in and let be a tight Borel measurable process taking values in . Then, in if and only if in for all .

The proof of this lemma can be found in Bücher (2011), Lemma A.5, for a special choice of the . The proof, however, is independent of this choice.

The proof of Proposition 4.1 is based on the following auxiliary result, establishing unconditional weak convergence of the vector of processes .

Proposition 6.3.

Suppose the conditions from Theorem 3.3 are met. Then, under , for all , we have

in , where denotes (unconditional) weak convergence (with respect to the probability measure ), and where are independent copies of .

Proof. We are going to apply Corollary 1.4.5 in Van der Vaart and Wellner (1996). Therefore, let . Since are independent conditional on the data, we have

By Definition 3.1 and Theorem 3.4, converges in outer probability to for each . Therefore,

by using the continuous mapping theorem, Slutsky’s Lemma and Lemma 1.10.2 in Van der Vaart and Wellner (1996) several times.

Choose an with for all , and let be a bounded and continuous function with on . Then

| (6.6) |

Note that uses the fact that a coordinate projection on a product probability space is perfect (Lemma 1.2.5 in Van der Vaart and Wellner, 1996). Moreover, holds because the limit processes are independent.

By Theorem 2.6, Remark 3.2(ii), Theorem 3.4 and Lemma 1.3.8 and Lemma 1.4.4 in Van der Vaart and Wellner (1996) the vector of processes is (jointly) asymptotically measurable. Consequently, Equation (6.12), Fubini’s theorem (Lemma 1.2.6 in Van der Vaart and Wellner, 1996) and Corollary 1.4.5 in Van der Vaart and Wellner (1996) yield the desired weak convergence. Note that the limit process is separable because it is tight (Lemma 1.3.2 in the previously mentioned reference). ∎

Proposition 6.4.

Suppose the sampling scheme meets the conditions from Corollary 2.5. Then, under , there exists an such that, for all ,

If is true, the same assertion holds for and .

Proof. Choose such that there exists a with . Then , with the function defined in Proposition 4.3. But Proposition 4.3 and the continuous mapping theorem show that and this yields the assertion for .

The same argument implies the claim for , using the fact that and consequently under .

Finally, let us prove the claim for . As in the proof of Proposition 4.3, let and be independent Itō semimartingales with characteristics and , respectively. For and , set and . Let and denote the quantity defined in (2.1), based on the observations and , respectively, instead on .

Then the quantities and differ only by a factor , with being equal in distribution to (Theorem II.4.15 in Jacod and Shiryaev, 2002)

This expression converges to , in probability, which in turn implies the assertion regarding . ∎

Proposition 6.5.

Suppose the sampling scheme meets the conditions from Corollary 2.5. Then, under , for all and all ,

Moreover, under , for all ,

Proof. Since the results are independent of , we omit this index throughout the proof. Also note that, for both assertions, it suffices to show that, for any , under .

For and , let and be defined as in the proof of Proposition 4.3. Let , and , denote the corresponding quantities, based on the observations and , respectively, instead on .

Then, for , we can write as

The first term of this display is , uniformly in and , by Theorem 3.3 and Remark 3.2 (ii). By the classical Donsker theorem, the first term in curly brackets on the right-hand side is also uniformly in . The quantity is by Corollary 2.5. Finally, the same argument as in the proof of Proposition 4.3 yields

To conclude,

The supremum over and can be treated similarly. ∎

Acknowledgements. This work has been supported by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823, Teilprojekt A1, A7, C1) of the German Research Foundation (DFG) which is gratefully acknowledged.

References

- Aït-Sahalia and Jacod (2009a) Aït-Sahalia, Y. and J. Jacod (2009a). Estimating the degree of activity of jumps in high frequency data. The Annals of Statistics 37(5), 2202–2244.

- Aït-Sahalia and Jacod (2009b) Aït-Sahalia, Y. and J. Jacod (2009b). Testing for jumps in a discretely observed process. The Annals of Statistics 37(1), 184–222.

- Aït-Sahalia and Jacod (2014) Aït-Sahalia, Y. and J. Jacod (2014). High-Frequency Financial Econometrics. Princeton University Press.

- Bücher (2011) Bücher, A. (2011). Statistical Inference for Copulas and Extremes. Ph. D. thesis, Ruhr-Universität Bochum.

- Bücher and Kojadinovic (2014) Bücher, A. and I. Kojadinovic (2014). A dependent multiplier bootstrap for the sequential empirical copula process under strong mixing. Bernoulli (to appear), arXiv:1306.3930v2.

- Bücher and Vetter (2013) Bücher, A. and M. Vetter (2013). Nonparametric inference on Lévy measures and copulas. The Annals of Statistics 41(3), 1485–1515.

- Cont and Tankov (2004) Cont, R. and P. Tankov (2004). Financial Modelling with Jump Processes. Chapman and Hall/CRC.

- Delbaen and Schachermayer (1994) Delbaen, F. and W. Schachermayer (1994). A general version of the fundamental theorem of asset pricing. Mathematische Annalen 300, 463–520.

- Figueroa-Lopez (2008) Figueroa-Lopez, J. (2008). Small-time moment asymptotics for Lévy processes. Statist. Probab. Lett. 78, 3355–3365.

- Figueroa-Lopez and Houdre (2009) Figueroa-Lopez, J. E. and C. Houdre (2009). Small-time expansions for the transition distributions of Lévy processes. Stochastic Process. Appl. 119, 3862–3889.

- Iacus and Yoshida (2012) Iacus, S. M. and N. Yoshida (2012). Estimation for the change point of volatility in a stochastic differential equation. Stochastic Processes and their Applications 122(3), 1068–1092.

- Inoue (2001) Inoue, A. (2001). Testing for distributional change in time series. Econometric Theory/Cambridge University Press 17(1), 156–187.

- Jacod and Protter (2012) Jacod, J. and P. Protter (2012). Discretization of Processes. Springer.

- Jacod and Shiryaev (2002) Jacod, J. and A. Shiryaev (2002). Limit Theorems for Stochastic Processes (2 ed.). Springer.

- Kim and Pollard (1990) Kim, J. and D. Pollard (1990). Cube root asymptotics. The Annals of Statistics 18(1), 191–219.

- Kosorok (2003) Kosorok, M. (2003). Bootstraps of sums of independent but not identically distributed stochastic processes. Journal of Multivariate Analysis 84, 299–318.

- Kosorok (2008) Kosorok, M. (2008). Introduction to Empirical Processes and Semiparametric Inference. Springer.

- Lee et al. (2006) Lee, S., Y. Nishiyama, and N. Yoshida (2006). Test for parameter change in diffusion processes by cusum statistics based on one-step estimators. Annals of the Institute of Statistical Mathematics 58(2), 211–222.

- Lifshits (1984) Lifshits, M. A. (1984). Absolute continuity of functionals of ”supremum” type for Gaussian processes. Plenum Publishing Corporation 119, 154–166.

- Mykland and Zhang (2012) Mykland, P. and L. Zhang (2012). The econometrics of high frequency data. Proceedings of the 7th Séminaire Européen de Statistique, La Manga, 2007: Statistical methods for stochastic differential equations, edited by M. Kessler, A. Lindner and M. Sørensen.

- Pollard (1990) Pollard, D. (1990). Empirical Processes: Theory and Applications (2 ed.). Institute of Mathematical Statistics and the American Statistical Association.

- Rüschendorf and Woerner (2002) Rüschendorf, L. and J. H. C. Woerner (2002). Expansion of transition distributions of Lévy processes in small time. Bernoulli 8(1), 81–96.

- Van der Vaart and Wellner (1996) Van der Vaart, A. and J. Wellner (1996). Weak Convergence and Empirical Processes. Springer.

- Vetter (2014) Vetter, M. (2014). Inference on the Lévy measure in case of noisy observations. Statistics and Probability Letters 87, 125–133.