The impact of a Hausman pretest, applied to panel data, on the coverage probability of confidence intervals

PAUL KABAILA∗, RHEANNA MAINZER AND DAVIDE FARCHIONE

Department of Mathematics and Statistics, La Trobe University, Australia

Summary In the analysis of panel data that includes a time-varying covariate, a Hausman pretest is commonly used to decide

whether subsequent inference is made using the random effects model or the fixed effects model. We consider the effect of this

pretest on the coverage probability of a confidence interval for the slope parameter.

We prove three new finite sample theorems that

make it easy to assess, for a wide variety of circumstances, the effect of the

Hausman pretest on the minimum coverage probability of this confidence interval.

Our results show that for the small levels of significance of the Hausman pretest commonly used in applications,

the minimum coverage probability of the confidence interval for the slope parameter can

be far below nominal.

* Corresponding author. Department of Mathematics and Statistics,

La Trobe University, Victoria 3086, Australia. Tel.: +61 3 9479 2594; fax +61 3 9479 2466.

E-mail address: P.Kabaila@latrobe.edu.au.

1. INTRODUCTION

In the analysis of panel data that includes a time-varying covariate, a preliminary Hausman (1978) test is commonly used to decide

whether subsequent inference is made using the random effects model or the fixed effects model. If the Hausman pretest rejects the null hypothesis of no correlation between

the random effect and time-varying covariate then the fixed effects model is chosen for subsequent inference, otherwise the

random effects model is chosen. This preliminary model selection procedure has been widely used in econometrics (see e.g. Wooldridge, 2002 and Baltagi, 2005).

As noted by Guggenberger (2010), examples of the practical application of this procedure are provided by Bloningen (1997) and Hastings (2004).

This preliminary model selection procedure has also been adopted in other areas such as medical statistics,

see e.g. Gardiner et al. (2009) and Mann et al. (2004), and has been implemented in popular statistical computer programmes including SAS, Stata, eViews and R, see

Ajmani (2009, Chapter 7.5.3), Rabe-Hesketh and Skrondal (2012, Chapter 3.7.6), Griffiths et al. (2012, Chapter 10.4) and Croissant and Millo (2008), respectively.

So, what is widely used in the analysis of panel data that includes a time-varying covariate, is the following two-stage procedure.

In the first stage, the Hausman pretest is used to decide

whether subsequent inference is made using the random effects model or the fixed effects model (see e.g. Ebbes et al., 2004 and Jackowicz et al., 2013). The second stage is that the inference

of interest is carried out assuming that the model chosen in the first stage had been given to us a priori, as the true model.

Guggenberger (2010) considers this two-stage procedure when the inference of interest is a hypothesis test about the slope

parameter.

He provides both a local asymptotic analysis of the size of this test and a finite sample analysis (via simulations) of the probability of Type I error.

In the present paper, we consider the case

that the inference of interest is a confidence interval for the slope parameter.

We prove three new theorems on the finite sample properties of the coverage probability

function of this confidence interval. By the duality between hypothesis tests and confidence intervals,

these new theorems imply corresponding new results when the inference of interest is a hypothesis test (see Remark 1 in Section 5).

Theorem 1 states that the finite sample coverage probability of the confidence interval resulting from the two-stage procedure depends on relatively few parameters. We use Theorem 3 to provide variance reduction by control variates, leading to more efficient simulation-based estimates of

coverage probability. Also, we use Theorem 2 to reduce the time required to compute the minimum coverage probability by a half.

These theorems make it easy to assess, for a wide variety of circumstances, the finite sample effect of the

Hausman pretest on the minimum coverage probability of this confidence interval (or, when the inference of interest is a hypothesis test, the size of this test).

We find that the Hausman pretest, with the usual small nominal level of significance, can lead to this confidence interval having minimum coverage probability far below nominal. We also find that if the nominal level of significance is increased to 50% then the minimum coverage probability is much closer to the nominal coverage

(as shown in Figures 1, 3 and 4).

The results presented in this paper were

computed using programs written in the R programming language, which will be made available in a convenient R package.

In Section 2, we consider the practical situation that the

random error and random effect variances

are estimated from

the data. We consider three estimators of these variances: the usual unbiased estimators, the maximum likelihood estimators of Hsiao (1986) and the estimators of Wooldridge (2002).

The coverage probability of the confidence interval resulting from the two-stage procedure is determined by 4 known quantities and 5 unknown

parameters. The known quantities are the number of individuals, the number of time points, the nominal significance level of the Hausman pretest and the nominal coverage probability of this confidence interval. The unknown parameters are the random error variance, the random effect variance, the variance of the time-varying covariate, a scalar parameter that determines the correlation matrix of the time-varying covariates and a non-exogeneity

parameter.

If, for given values of the 4 known quantities, we wish to assess the dependence of the coverage probability of the confidence interval resulting from the two-stage procedure on the 5 unknown parameters then we might consider, say, five values for each of these unknown parameters, leading to 3125 parameter combinations. Apart from the daunting task of summarizing so many results,

it is possible that one might miss important values of the unknown parameters, such as values for which the

coverage probability is particularly low.

Theorem 1 states that, apart from the known quantities, this coverage probability

is actually determined by only 3 unknown

parameters, including the non-exogeneity parameter. If we compute the minimum coverage probability with respect to the non-exogeneity parameter then

we have only 2 unknown parameters and our assessment of the coverage properties of the confidence interval resulting from the two-stage procedure is

greatly simplified. Theorem 2 states that this coverage probability is an even function of the non-exogeneity parameter, so that

the time required to compute this minimum coverage is halved. We also propose a scaling of the non-exogeneity parameter that takes account of the sample size. In effect, this scaling reduces the number of known quantities that determine this coverage probability

from 4 to 3.

In Section 3, we consider the coverage probability of the confidence interval

resulting from the two-stage procedure when the random error and random effect variances are assumed to be known.

Theorem 3 states that this coverage probability, conditional on the time-varying covariates, can be found exactly by the evaluation of

the bivariate normal cumulative distribution function. This theorem is important because it is used to reduce the variance of the simulation based estimators of the coverage probability

of the confidence interval resulting from the two-stage procedure (when random error and random effect variances are estimated). As we show in Section 4 this variance reduction is achieved by using control variates.

2. THE MODEL AND THE PRACTICAL TWO-STAGE PROCEDURE

(RANDOM ERROR AND RANDOM EFFECT VARIANCES ARE ESTIMATED)

Let and denote the response variable and the time-varying covariate, respectively, for the individual () at time (). Suppose that

(1)

where the ’s and the ’s are independent, the ’s are i.i.d. and the ’s are i.i.d. . We call the slope parameter, the error variance

and the random effect variance. Note that the ’s and the

’s are unobserved.

Suppose that the parameter of interest is and that the inference of interest is a confidence interval for .

Let .

Also suppose that the ’s are

i.i.d. multivariate normally distributed with zero mean and covariance matrix

(2)

where is a vector of 1’s, is a matrix with ’s on the diagonal and is a parameter that measures the dependence between and . We consider two models for : (a) the off-diagonal elements of are all (compound symmetry) and (b) the ’th element of is

(first order autoregression). We define the “non-exogeneity parameter” as follows. For the case of compound symmetry,

and, for first order autoregression,

.

As we show in Appendix A, in both cases is a correlation, so that it lies in the interval .

If then and are independent, so that the

’s are exogenous variables.

Also, as shown in Appendix A, for the compound symmetry case, our definition of the parameter coincides with the definition

given by Guggenberger (2010, p.339) of his parameter , which “measures the degree of failure of the pretest hypothesis”.

When , a confidence interval

for may be found as follows. Assume, initially, that

is known.

Condition on and use the GLS estimator

of . Let , where denotes the standard normal cdf.

The

confidence interval for based on this estimator is

where denotes the variance of , conditional on when . When the confidence interval

has coverage probability , conditional on .

Therefore, it has coverage probability unconditionally.

Of course, in practice is unknown and needs to be estimated.

So, in practice, we would use ,

where is an estimator of , as a confidence interval

with nominal coverage probability .

This model is called the between effects model.

When , an alternative estimator of

is , the OLS estimator based on the model (3), when we condition on . This estimator does not require a knowledge of .

Irrespective of whether or not, we may find a confidence interval for with coverage probability as follows. Subtracting

(3) from (1), we obtain

(4)

This model is called the fixed effects model. We estimate

by , the OLS estimator based on this model.

The

confidence interval for based on this estimator is

where denotes

the variance of , conditional on .

The confidence interval

has coverage probability , conditional on .

Therefore, it has coverage probability unconditionally.

Of course, in practice is unknown and needs to be estimated.

So, in practice, we would use ,

where is an estimator of , as a confidence interval

with nominal coverage probability .

In practice, we do not know whether or not . As noted in the introduction, the usual procedure is to use a Hausman pretest to test the null hypothesis against the alternative hypothesis . Assume, for the moment, that and are known. We consider this pretest, based on the test statistic

(5)

where denotes the variance of

conditional on and assuming that .

This test statistic has a distribution under the null hypothesis , conditional on . Therefore, this test statistic has this distribution under this null hypothesis, unconditionally. Suppose that we accept the null hypothesis if

; otherwise we reject this null hypothesis.

Note that is the level of significance of this test, conditional on ,

assuming that and are known.

We now describe the two-stage procedure assuming, for the moment, that and are known.

If the null hypothesis is accepted then we use the confidence interval ; otherwise we use the confidence interval . Let denote the confidence interval, with nominal coverage

, that results from this two-stage procedure. Of course, in practice, and are not known and need to be estimated. So, in practice, the two-stage procedure results in the confidence interval where and denote estimators of and , respectively. We consider the usual unbiased estimators, maximum likelihood estimators and Wooldridge’s estimators (described in Appendix B). The unconditional coverage probability of the confidence interval constructed from this two-stage procedure is denoted .

As stated in the introduction,

is determined by the 4 known quantities , , and and the 5 unknown parameters

, , , and . As explained in the introduction,

the assessment of the dependence of this probability on these 4 known quantities and 5 unknown parameters is a daunting task that could

easily miss important parameter values. However,

the following theorem shows that, for given values of the known quantities, this probability depends on the 5 unknown

parameters only through the 3 unknown parameters , and .

Thus, for fixed , , and , we only need to consider what happens as , and are varied

instead of what happens as , , , and are varied.

If we compute the minimum over of

then we are left with only 2 unknown parameters and .

Theorem 1.

For any of the

pairs of estimators listed in Appendix B, the unconditional coverage probability is determined by (the number of individuals), (the number of time points), (the nominal significance level of the Hausman pretest), (the nominal coverage probability), (the ratio ), (the parameter that determines ) and (the non-exogeneity parameter). Given these quantities, the coverage probability does not depend on either (the variance of the random error) or (the variance of the random effect) or (the variance of the time-varying covariate ).

The proof of Theorem 1 is provided in Appendix C.

We use simulations to compute , employing

variance reduction by control variates, as described in Section 4. When we compute this coverage probability, we also make use of the following theorem.

Theorem 2.

Suppose that , , , , and are fixed.

When and are replaced by any of the pairs of estimators listed in Appendix B,

the unconditional coverage probability

is an even function of .

The proof of Theorem 2 is provided in Appendix C.

A remarkable feature of the proofs of both Theorems 1 and 2 is that they are carried out without relying on a simple expression for the

coverage probability .

Using Theorem 2, we only need to consider in the interval , which means that we have reduced the number of simulations needed to estimate the coverage probability function (or its minimum) by half.

By Remark 2 of Section 5,

we expect this coverage probability, considered as a function of ,

to have a stable shape when is varied over a wide range of medium to large values.

We therefore plot this coverage probability as a function of , instead of .

Of course,

the set of possible values of changes with , since . In other words,

.

We now examine the influence that the nominal level of significance of the Hausman pretest has on the coverage probability function .

Suppose that

and

are the usual unbiased estimators of and , respectively (described in Appendix B).

Consider the case that the matrix has off-diagonal

elements (compound symmetry), where , , , and the

nominal coverage probability .

In practice, it is common to use a small value of , such as 0.05 or 0.01.

As noted by Guggenberger (2010), examples of practical applications that have used a small for the Hausman pretest are provided by Gaynor et al. (2005, p.245) and Bedard and Deschenes (2006, p.189).

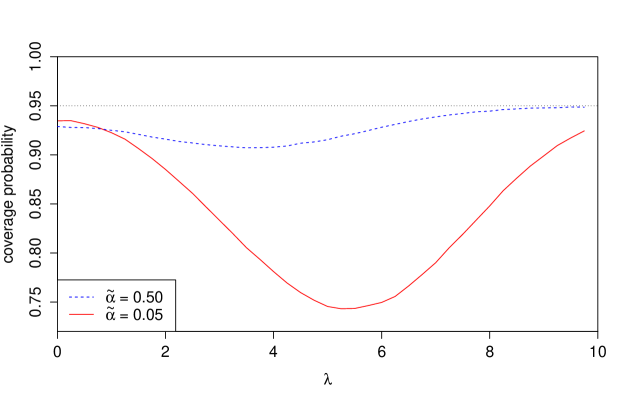

Figure 1 presents graphs of the coverage probability

,

considered as a function of .

Each graph is computed using the variance reduction method and the common random numbers (to produce smoother graphs)

described in Section 4.

The number of simulation runs used to compute each graph is .

The bottom (solid line) graph is for nominal significance level of the Hausman pretest.

This graph falls well below the nominal

coverage for a wide interval of values of , with the minimum of the coverage probability approximately equal to 0.75.

Suppose that we choose the significance level of the Hausman pretest to be quite large, say . Now the Hausman pretest is more likely to reject the null hypothesis that and therefore more likely to choose the fixed effects model for the construction of the

confidence interval.

The middle (dashed line) graph is for nominal significance level of the Hausman pretest.

Although this graph is still below the nominal coverage, there has been a large improvement.

Similar graphs, for and , are obtained when has ’th element (first order autoregression) and .

Figure 1 near here

As noted earlier, for given values of , , , and , we expect the graph of the coverage probability , expressed as a function of , to have a stable shape when is varied over a wide range of medium to large values.

Suppose that

and

are the usual unbiased estimators of and , respectively.

Consider the case that the matrix has off-diagonal

elements (compound symmetry), where , , and the

nominal coverage probability .

Figure 2 presents graphs of the coverage probability

,

considered as a function of , for and 1000.

Each graph is computed using the variance reduction method and the common random numbers

described in Section 4.

The number of simulation runs used to compute each graph is .

The value of for given must be less than . So when , must be less than 5 and when , must be less than . This is why the graphs of the coverage probability for these values of end before .

These graphs do, indeed, have the expected stable shape for and 1000.

Figure 2 near here

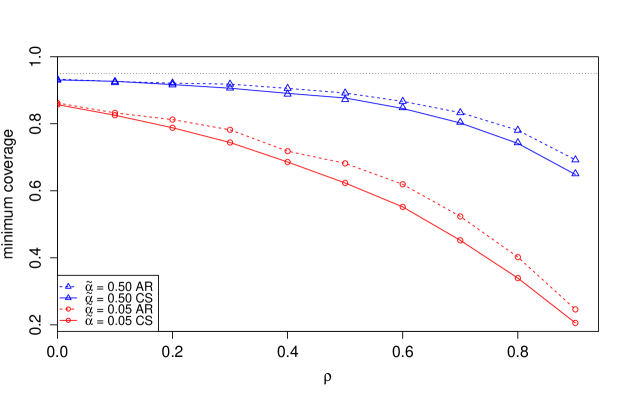

As noted in the Introduction and in Section 2, if we compute the minimum over of the coverage probability

then we are left with only two unknown parameters, and .

If we fix then the minimum coverage depends only on , where , as it is a correlation.

Suppose that

and

are the usual unbiased estimators of and , respectively.

Consider the cases that the matrix has (a) off-diagonal

elements (compound symmetry) and (b) ’th element (first order autoregression).

Suppose that , , and the

nominal coverage probability .

Figure 3 presents graphs of the coverage probability

, minimized over ,

considered as a function of .

Each estimate of the minimum coverage is found using the common random numbers and, for compound symmetry,

the variance reduction method described in Section 4.

Similarly to Figure 1, we see a vast improvement in the minimum coverage by letting rather than choosing to be the commonly used, smaller value 0.05.

Figure 3 near here

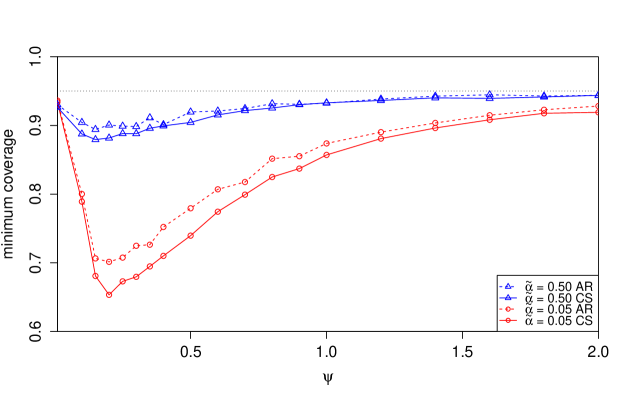

In practice, is not known and must be estimated from the data. However, one is likely to have some background knowledge about . This suggests that we fix and plot the graph of the coverage probability

, minimized over , as a function of .

Suppose that

and

are the usual unbiased estimators of and , respectively.

Consider the cases that the matrix has (a) off-diagonal

elements (compound symmetry) and (b) ’th element (first order autoregression),

where .

Suppose that , , and the nominal

coverage probability .

Figure 4 presents graphs of the coverage probability

, minimized over ,

considered as a function of .

For nominal significance level of the Hausman pretest, this minimized coverage probability

is far below the nominal coverage

for approximately equal to 0.2. However, for nominal significance level of the Hausman pretest, we see

(once more) a dramatic

improvement in the minimum coverage probability.

Figure 4 near here

3. THE TWO-STAGE PROCEDURE WHEN RANDOM ERROR AND RANDOM EFFECT VARIANCES ARE ASSUMED KNOWN

In this section we suppose that and are known.

In this case, the confidence interval resulting from the two-stage procedure is denoted by .

We also suppose that the matrix , which appears in the expression (2)

for the covariance matrix of ,

has 1’s on the diagonal and elsewhere (compound symmetry). We show that the coverage probability of this confidence interval, conditional on , can be computed exactly using the bivariate normal distribution. We employ this computed value in Section 4 to

find a control variate that is used for variance reduction for the estimation by simulation of

, when and are unknown.

Let denote the coverage probability of

, conditional on .

Observe that is equal to

(6)

where

,

and

.

By the law of total probability, (S0.Ex4)

is equal to the sum of and

(7)

The first and second terms in this expression are determined by the conditional

distributions of the random vectors and ,

respectively. Theorem 3 gives these distributions, whose description requires the introduction of

the following notation.

Let , (“sum of squares between”) and (“sum of squares within”).

We define to be , where is given in Appendix A.

Also let and .

The following theorem is proved in Appendix C.

Theorem 3.

Conditional on , and have bivariate normal distributions, where ,

,

Thus, when and are known,

can be found easily by evaluation of the bivariate normal cumulative distribution function

in the expression (7).

Similarly to Theorem 1,

this probability

is determined by (the number of individuals), (the number of time points), (the vector of time-varying covariates), (the nominal significance level of the Hausman pretest), (the nominal coverage probability), (the ratio ), (the parameter that determines ) and (the non-exogeneity parameter).

Note that the dependence on is through .

Also, similarly to Theorem 2, is an even function of . These results may be proved using similar, but much simpler, arguments to those used in the proofs of Theorems 1 and 2.

4. SIMULATION METHODS, INCLUDING THE USE OF VARIANCE REDUCTION, WHEN THE RANDOM ERROR AND RANDOM EFFECT VARIANCES ARE UNKNOWN

In Section 3 we described how to find the coverage probability of the confidence interval resulting from the two-stage procedure,

conditional on when and are known, using the bivariate normal distribution. In the practically important case that and are replaced by estimators, we can no longer use the bivariate normal distribution to find this coverage probability. Instead we estimate the coverage probability using a simulation consisting of independent simulation runs. We consider the model (1) and choose the intercept , the parameter of interest and the

values for (the number of individuals), (the number of time points), (the nominal significance level of the Hausman pretest), (the nominal coverage probability), (the variance of the random error), (the variance of the random effect) and (the variance of the covariate ). Of course, by Theorem 1, the coverage probability

does not depend on either , or and depends on and only through

. The simulation methods described in this section apply to any of the pairs of estimators and listed in Appendix B.

On the ’th simulation run, we generate observations of the ’s and ’s using the assumptions made in Section 2, i.e. the ’s are i.i.d. and the ’s are i.i.d. with a multivariate normal distribution with mean and covariance matrix (2).

Let denote the observed value of for this run.

For the observed values in this simulation run,

we compute the following three quantities.

The confidence interval resulting from the two-stage procedure, when and are assumed known, is denoted by .

The confidence interval resulting from the two-stage procedure,

when and are estimated by and ,

respectively, is denoted by .

The coverage probability of , conditional on , when and are assumed known, is

. Note that this conditional coverage probability is computed exactly using the bivariate normal distributions given in Theorem 3.

Let , the coverage probability of .

We use the notation

where is an arbitrary statement.

Now define the unbiased estimator

of CP. This is the usual “brute-force” simulation estimator of CP.

We estimate the variance of this estimator by noting that it is a binomial proportion.

Let , the coverage probability of , when and are assumed known. Now define the unbiased estimator

of CPK.

By the double expectation theorem, .

Thus another unbiased estimator of is

which is a much more accurate estimator of CPK than .

Define the control variate , which has expected value zero. The simulation-based unbiased estimator of

that employs variance reduction using this control variate,

is

We expect that the correlation between and will be close to 1.

Since is a much more accurate estimator of CPK than ,

we expect that the correlation between and the control variate

will also be close to 1. Note that

We estimate the variance of this estimator by noting that it is an average of i.i.d. random variables.

We evaluate the efficiency gain of using to estimate the coverage probability CP over ,

as follows. Let and denote the times taken to carry out simulation runs when we estimate CP by

and , respectively.

The efficiency

of the control variate estimator relative to the “brute-force” estimator is

The larger this relative efficiency, the greater the gain in using the control variate estimator , by comparison with using the “brute-force” estimator .

To give an example of the efficiency gained by using compared to , when estimating CP, we set (the identity matrix), , , , , and number of simulation runs . We obtain seconds, seconds, and . The time ratio is and the variance ratio is , so the efficiency of relative to is approximately 4.17. In other words, it would take approximately 4.17 times as long to compute the “brute-force” estimator with the same accuracy as the control variate estimator.

We also use common random numbers to create smoother plots of the estimated coverage probability, as a function of .

The estimates of the coverage probability are computed for an equally-spaced grid of values of .

On the ’th simulation run we generate an observation of by linearly transforming observations of independent

random numbers.

So, on the ’th simulation run, for each value of in the grid, we use the same random numbers that are used to generate the observations of the ’s and

the ’s. These observations are then used to construct our simulation-based estimate of CP. Therefore on the ’th simulation run, for each value of , we have an estimate of the coverage probability using the same random numbers.

5. REMARKS

Remark 1: As one would expect from the duality between hypothesis tests and confidence intervals, our results have important implications for the actual size of a hypothesis test for the slope parameter,

with nominal significance level , following a Hausman pretest,

when the random error and random effect variances are estimated by one of the pairs of estimators described in Appendix B. Consider the following two-stage

procedure. As previously, in the first stage we test the null hypothesis against the alternative hypothesis

as follows.

We accept this null hypothesis if

; otherwise we reject this null hypothesis.

In the second stage, we test the null hypothesis against the alternative hypothesis as follows.

If the null hypothesis has been accepted then we test against at the nominal significance level , using the test statistic , which has a nominal

distribution under . If, on the other hand, the null hypothesis has been rejected then we test

against at the nominal significance level , using the test statistic , which has a nominal distribution under .

It may be shown that the probability of rejecting

the null hypothesis , when it is true, is

. By Theorem 1, this probability of rejection is determined

by , , , , , and .

In other words, this probability of rejection does not depend on and depends on and only through . Since does not depend on either or , we may (without loss of

generality) suppose that and . Also, by Theorem 2, this probability of rejection is an even function of for fixed

, , , , and . Hence,

for fixed

, , , , and , the size of the hypothesis test of

against

is equal to

which can be computed efficiently using our methods.

Remark 2: Crossover trials are widely used in medicine and pharmaceutics. For many years, the following two-stage procedure was the standard

method for the analysis of data from a two-treatment two-period (AB/BA) crossover trial. In the first stage, a test of the null hypothesis of

zero differential carryover is used to decide whether subsequent inference is made using all of the data or only the data from the

first period (which is unaffected by carryover). In the second stage, we carry out the inference of interest assuming that the model

chosen in the first stage had been given to us a priori, as the true model. In a landmark paper, Freeman (1989) considers the case

that the inference of interest is a confidence interval for the difference of the effects of the two treatments. For simplicity,

he assumes that the error and subject variances are known and derives a formula for the coverage probability that

has some similarity to the formula (S0.Ex4) of Section 3, in that both of these formulas are evaluated using the bivariate normal distribution. Freeman’s

conclusion is that the two-stage procedure for crossover trials “is too potentially misleading to be of practical use”.

Our choice of the scaling is motivated by Freeman’s (1989) scaling of the differential carryover by the square root of the sample size. We expect that the coverage probability, considered as a function of , for given will be reflective of the coverage probability function as . This expectation is verified by Figure 2.

Remark 3: The Hausman pretest is an example of preliminary statistical (i.e. data based) model selection. Other examples include model selection by minimizing a criterion such as the Akaike Information Criterion or the Bayesian Information Criterion. The effects of preliminary statistical model selection on confidence intervals can range from the benign to the very harmful, depending on the class of models under consideration, the known aspects of the model, the parameter of interest and the model selection procedure employed (Kabaila, 1995, 2009 and Kabaila and Leeb, 2006). In other words, each case needs to be considered individually on its merits.

6. CONCLUSION

Our results show that for the small levels of significance (such as 5% or 1%) of the Hausman pretest commonly used in applications,

the minimum coverage probability of the confidence interval for the slope parameter with nominal coverage probability can

be far below nominal. The methodology that we have described makes it easy to assess, for a wide variety of circumstances, the effect of the

Hausman pretest on the minimum coverage probability of this confidence interval. An interesting finding is that if we increase the significance

level of the Hausman pretest to, say, 50% then this minimum coverage probability is much closer to the nominal coverage

for a wide range of parameters. This suggests that the Hausman pretest might continue to be used in practice to good effect, provided

that one uses such a relatively high level of significance for this pretest.

APPENDIX A. DEFINITION OF THE NON-EXOGENEITY PARAMETER

For the compound symmetry case, it may be shown that the distribution of conditional on

is normal with mean

where , and variance

This suggests that is a reasonable measure of the dependence between

and i.e. that it is reasonable to designate as the non-exogeneity parameter.

It may be shown that and

.

Thus

For the first order autoregression case, it may be shown that the distribution of conditional on

is normal with mean

where , and variance

This suggests that is a reasonable measure of the dependence between

and i.e. that it is reasonable to designate as the non-exogeneity parameter.

It may be shown that

and

Thus

APPENDIX B. DESCRIPTION OF THE ESTIMATORS OF THE RANDOM ERROR AND RANDOM EFFECT VARIANCES CONSIDERED

It has been suggested in the literature (see e.g. Hsiao, 1986 and Baltagi, 2005) that if a negative estimate of variance is observed then

one should do as Maddala and Mount (1973) suggest and replace this negative estimate by 0. We use this kind of approach to ensure

that is always positive and is always nonnegative. This ensures that

the proofs of Theorems 1 and 2 carry through for each of the three pairs of estimators that we consider in this paper. We

consider the following pairs of estimators of and :

(1) The usual unbiased estimators. Define

and

where

The ’s are the OLS residuals from model (4) and the ’s are the OLS residuals from model (3).

Note that is an unbiased estimator of only for .

(2) Hsiao’s (1986) maximum likelihood estimators and

. We assume, of course, that the maximum likelihood estimator is obtained by maximizing the log-likelihood

function subject to the parameter constraints and .

(3) Wooldridge’s (2002) estimators. Define

where is a very small positive number and

Also define

where

Here, the ’s are the residuals from pooled OLS estimation for the model (1)

and (no d.o.f. correction) or (d.o.f. correction).

APPENDIX C. PROOFS OF THEOREMS 1, 2 AND 3

The proofs in this section make use of the Hausman test statistic considered in this paper and the unbiased estimators of and

described in Appendix B. It is important to note that there are three different test statistics that can be used to carry out the Hausman test in the panel data context. Theorems 1, 2 and 3 hold for the three Hausman test statistics given by Hausman and Taylor (1981) and the three pairs of estimators described in Appendix B. Proofs of these theorems using these other test statistics or estimators are omitted for the sake of brevity, but follow similar arguments to the proofs that we present.

We present the proof of this result for the case that and are replaced by the unbiased estimators

described in Appendix B.

Suppose that , , the level of significance of the Hausman pretest, the nominal coverage , , and are given. Let

and

.

Recall the random variables defined in Section 3,

,

and

.

Note that , and are determined by , and . Let , and denote the statistics , and when and are replaced by the

unbiased estimators and described in Appendix B. We express , and in terms of and we emphasize this by using the notation , and , respectively.

Since is defined to be the OLS estimator of based on the model (3),

(8)

where , ,

,

and .

Also, since is the OLS estimator of based on the model (4),

(9)

where .

In our context, Maddala’s (1971) equation (1.3) is

,

where .

Thus ,

where . Observe that , where .

It follows from this and (8) and (9) that

We now introduce the following notation. Let , , , , , , , , , and . Thus and .

Note that the ’s and the ’s are independent, the

’s are

i.i.d., the ’s are i.i.d.

and the ’s are i.i.d. . Also note that

the distribution of is

multivariate normal with mean and covariance matrix

where is a -vector of 1’s, and is described in Appendix A for both the compound symmetry

and the first order autoregression cases. Thus the joint distribution of the

’s and the ’s

is determined by and (and does not depend on either or or ).

We now show that , and can be written in terms of the ’s, ’s, ’s and . This has the consequence that both the distribution of and the distribution of are functions of the quantities

, , and and the unknown parameters , and . The theorem follows from this.

The ’th OLS residual at time from model (4), which appears in the

expressions for the

usual unbiased estimators of and is

Obviously,

Dividing by gives

Hence

is a function of the ’s and the

’s. In a similar manner, it can be shown that and are functions of the ’s, ’s, ’s and , where is defined in Appendix B. Hence is a function of the ’s, ’s, ’s and . Thus is also a function of the ’s, ’s, ’s and . Now

Therefore, is a function of

the ’s, ’s, ’s and .

Dividing the numerator and denominator of the expression for

by , we obtain

Multiplying the numerator and denominator

by , we obtain

Therefore, is a function of

the ’s, ’s, ’s and .

In a similar manner, it can be shown that

and that

Thus and are also functions of

the ’s, ’s, ’s and .

Suppose that , , the nominal level of significance of the Hausman pretest, the nominal coverage , ,

and are fixed.

We assume that has a multivariate normal distribution

with mean and the covariance matrix (2) where and (the identity matrix).

The proof when has either a compound symmetry or first order autoregression structure and

follows in a similar manner using the definitions of given in Appendix A.

By Theorem 1 the coverage probability of the confidence interval constructed after a Hausman pretest is a function of .

So, in this section denotes the probability of the event conditional on , evaluated at . The set of possible values of is .

Our aim is to show that the coverage probability is an even function of , i.e. our aim is to show that

for every .

By the law of total probability, is equal to

Using the definitions of , and stated in the proof of Theorem 1,

is equal to

and by the law of total probability, is equal to

.

Therefore, to prove that the coverage probability is an even function of , when and are unknown, it is sufficient to prove the following:

(a)

(b)

(c)

First we consider (a). We have that

Similarly,

Therefore, to show that (a) holds, it is sufficient to show that

We introduce the following notation.

Let for , and . Let , , , and . Note that , and .

For , has a multivariate normal distribution

with mean and covariance matrix (2),

where

and .

Observe that,

for , has a multivariate normal distribution

with mean and covariance matrix (2),

where

and . Hence, for , has a multivariate normal distribution

with mean and covariance matrix (2),

where and .

From this point onwards we write as and as (as in the proof of Theorem 1) to emphasize the dependence on . Recall, from the proof of Theorem 1, that

It follows that

The usual unbiased estimator of is

Note that

Thus

We define to be , but with

replaced by for and . It can be shown that . Hence for the usual unbiased (for ) estimator , .

We then define and note that .

Hence

By a similar argument,

We see that and are the same functions of the ’s, ’s and ’s as and , respectively, are functions of the ’s, ’s and ’s.

Hence (a) is true. In a similar manner, it can be shown that (b) and (c) are also true. Therefore the coverage probability is an even function of .

Proof of Theorem 3

Suppose that the matrix has 1’s on the diagonal and elsewhere (compound symmetry).

As shown in Appendix A, and so

where

(a convenient formula for is given in Appendix A).

Therefore, conditional on , ,

where the ’s and ’s are independent and the ’s are i.i.d. .

It follows from this that, conditional on ,

(10)

Consider the expression (8) for . It follows from (10)

that, conditional on ,

Obviously, . It can be shown, after lengthy algebraic manipulations,

that

where and .

Now consider the expression (9) for .

Obviously, . It can be shown, after some algebraic manipulation, that

. It can also be shown, after lengthy algebraic manipulations,

that . We conclude that, conditional on , and

are independent normally distributed random variables with the stated conditional means and variances.

The distributions of the random vectors and are determined by the bivariate normal distributions of and . In our context, Maddala’s (1971) equation (1.3) is , where .

It follows from this equation that the distributions of and , conditional on , are bivariate normal, where

Theorem 3 follows from these distributional properties.

REFERENCES

Ajmani, V.B., 2009. Applied Econometrics Using the SAS system. John Wiley, Hoboken, N.J.

Baltagi, B.H., 2005. Econometric Analysis of Panel Data, 3rd edition. John Wiley & Sons, Ltd.

Bedard, K., Deschenes, O., 2006. The long-term impact of military service on health: Evidence from work war II and Korean war veterans. American Economic Review 96, 176-194.

Bloningen, B.A., 1997. Firm-specific assets and the link between exchange rates and foreign direct investment.

American Economic Review 87, 447–465.

Croissant, Y., Millo, G., 2008. Panel data econometrics in R: The plm package. Journal of Statistical Software, 27(2), 1-43.

Ebbes, P., Bockenholt, U., Wedel, M., 2004. Regressor and random-effects dependencies in multilevel models. Statistica Neerlandica 58, 161–178.

Freeman, P.R., 1989. The performance of the two-stage analysis of two-treatment, two-period crossover trials.

Statistics in Medicine 8, 1421–1432.

Gardiner, J.C., Luo, Z., Roman, L.A., 2009. Fixed effects, random effects and GEE: What are the differences? Statistics in Medicine 28, 221–239.

Gaynor, M., Seider, H., Vogt, W.B., 2005. The volume-outcome effect, scale economies, and learning-by-doing. American Economic Review 95, 243-247.

Griffiths, W. E., Hill, R. C., Lim, G., 2012. Using EViews for Principles of Econometrics. Danvers, MA: John Wiley & Sons.

Guggenberger, P., 2010. The impact of a Hausman pretest on the size of a hypothesis test: The panel data case.

Journal of Econometrics 156, 337–343.

Hastings, J.S., 2004. Vertical relationships and competition in retail gasoline markets: Empirical evidence from contract changes in Southern

California. American Economic Review 94, 317–328.

Hsiao, C., 1986. Analysis of Panel Data. Cambridge University Press, Cambridge.

Hausman, J.A., 1978. Specification tests in econometrics. Econometrica 46, 1251–1271.

Hausman, J.A., Taylor, W.E., 1981. Panel data and unobservable individual effects. Econometrica 49, 1377–1398.

Jackowicz, K., Kowalewski, O., Kozlowski, L., 2013. The influence of political factors on commercial banks in Central European countries. Journal of Financial Stability 9, 759–777.

Kabaila, P., 1995. The effect of model selection on confidence regions and prediction regions. Econometric Theory 11, 537–549.

Kabaila, P., 2009. The coverage properties of confidence regions after model

selection. International Statistical Review 77, 405–414.

Kabaila, P., Leeb, H., 2006. On the large-sample minimal coverage probability of confidence intervals after model selection. Journal of the American Statistical Association 101, 619–629.

Maddala, G.S., 1971. The use of variance components models in pooling cross section and time series data. Econometrica 39, 341–358.

Maddala, G.S., Mount, T.D., 1973. A comparative study of alternative estimators for variance component models used in econometric applications. Journal of the American Statistical Association 68, 324–328.

Mann, V., De Stavola, B.L., Leon, D.A., 2004. Separating within and between effects in family studies: an application to the study of blood pressure in children. Statistics in Medicine 23, 2745–2756.

Rabe-Hesketh, S., Skrondal, A., 2012. Multilevel and Longitudinal Modeling Using Stata, 3rd edition. Stata Press, Texas.

Wooldridge, J. M., 2002. Econometric Analysis of Cross Section and Panel Data. MIT Press, Cambridge.

Figure 1: Graphs of the coverage probability functions of the confidence interval resulting from the two-stage procedure, when the

usual unbiased estimators of the random error and random effect variances are used.

Here , where is the non-exogeneity parameter.

The bottom and middle graphs are for nominal levels of significance, and , respectively of the Hausman pretest. The matrix has off-diagonal

elements ,

(compound symmetry)

where . The number of individuals , the number of time points , and the nominal coverage probability .Figure 2:

Graphs of the coverage probability functions of the confidence interval resulting from the two-stage procedure, when the

usual unbiased estimators of the random error and random effect variances are used. Here, , where is the non-exogeneity parameter,

and and 1000.

The matrix has off-diagonal

elements , (compound symmetry) where . The number of time points , and the nominal

nominal coverage probability .

Figure 3: Graphs of the coverage probability functions, minimized over the non-exogeneity parameter , of the confidence interval resulting from the two-stage procedure. This minimum coverage is considered as a function of , for both compound symmetry (CS) and first order autoregression (AR) structures of the matrix .

The

usual unbiased estimators of the random error and random effect variances are used.

Two nominal levels of significance, and , of the Hausman pretest are considered.

The number of individuals , the number of time points , and the nominal coverage probability .Figure 4:

Graphs of the coverage probability functions, minimized over the non-exogeneity parameter , of the confidence interval resulting from the two-stage procedure. This minimum coverage is considered as a function of , for both compound symmetry (CS) and first order autoregression (AR) structures of the matrix , where .

The usual unbiased estimators of the random error and random effect variances are used.

Two nominal levels of significance, and , of the Hausman pretest are considered. The number of individuals , the number of time points and the nominal coverage probability .