neumaier,wecancompute^Relaxedi=(ViR12⊤R11(R11⊤R11)-1)⊤,=(ViR12⊤R11R11-1(R11⊤)-1)⊤,=(ViR12⊤(R11⊤)-1)⊤,=(Vi(R11-1R12)⊤)⊤,whichcanbeevaluatedwithatriangularsolver,hencedoesnotrequireexplicitmatrixinversion.IntheeventthatKispoorlyconditioned,toimprovenumericalstability,weaddasmallridgepenalty.ItissuggestedbyneumaiertoaddapenaltycorrespondingtoscalingadiagonalmatrixDconsistingoftheEuclideannormsofthecolumnsofKby(ri2+ri+1)ϵmachine,inwhichϵmachinedenotesmachineprecision.ThefullrefittingalgorithmisdetailedinAlgorithm3.

Appendix D StockandWatsonApplication

| Group | Brief description | Examples of series | Number |

|---|---|---|---|

| of series | |||

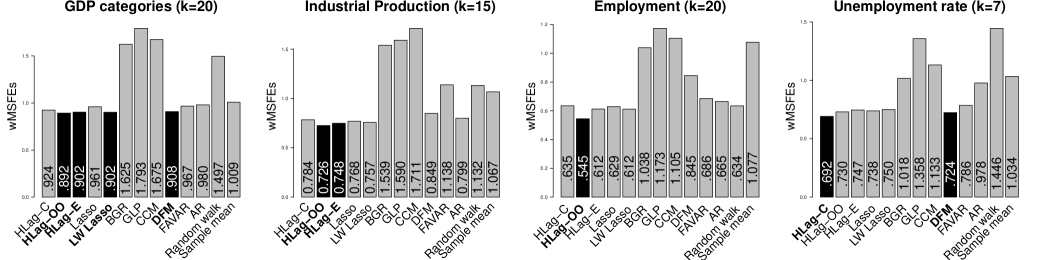

| 1 | GDP components | GDP, consumption, investment | 20 |

| 2 | IP | IP, capacity utilization | 15 |

| 3 | Employment | Sectoral and total employment and hours | 20 |

| 4 | Unemployment rate | Unemployment rate, total and by duration | 7 |

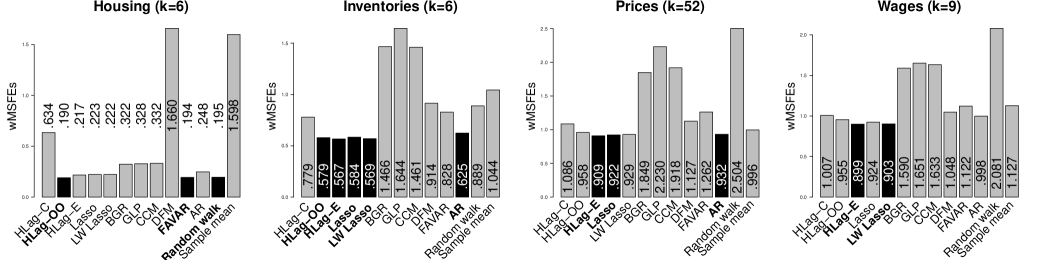

| 5 | Housing | Housing starts, total and by region | 6 |

| 6 | Inventories | NAPM inventories, new orders | 6 |

| 7 | Prices | Price indexes, aggregate and disaggregate; commodity prices | 52 |

| 8 | Wages | Average hourly earnings, unit labor cost | 9 |

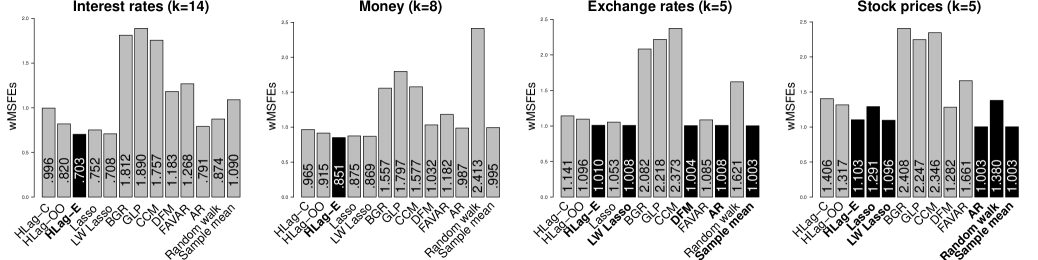

| 9 | Interest rates | Treasuries, corporate, term spreads, public-private spreads | 14 |

| 10 | Money | M1, M2, business loans, consumer credit | 8 |

| 11 | Exchange rates | Average and selected trading partners | 5 |

| 12 | Stock prices | Various stock price indexes | 5 |

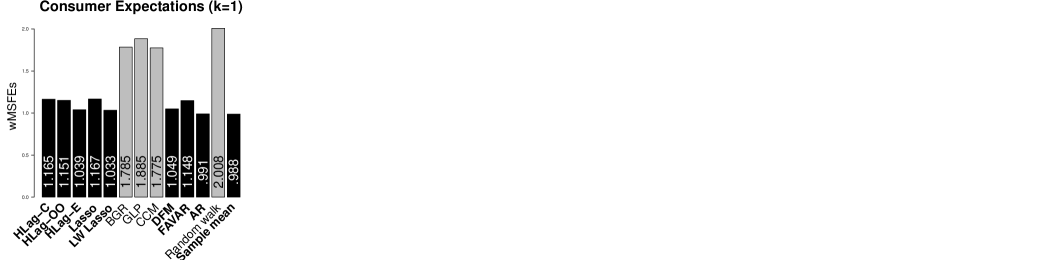

| 13 | Consumer expectations | Michigan consumer expectations | 1 |

stockdataset.Abriefdescriptionofeachvariable,alongwiththetransformationcodetomakethemapproximatelystationarycanbefoundintheDataAppendixofkoop.

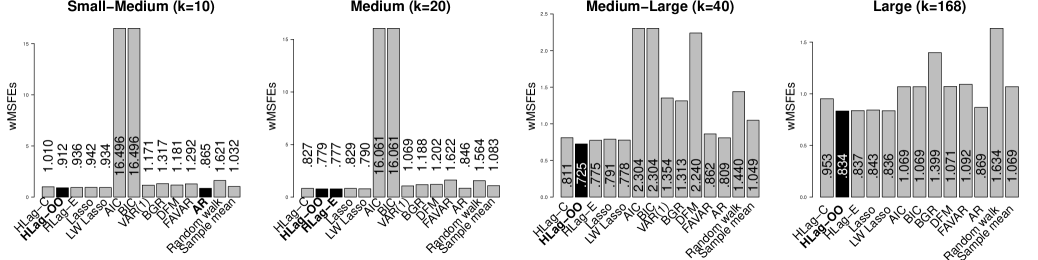

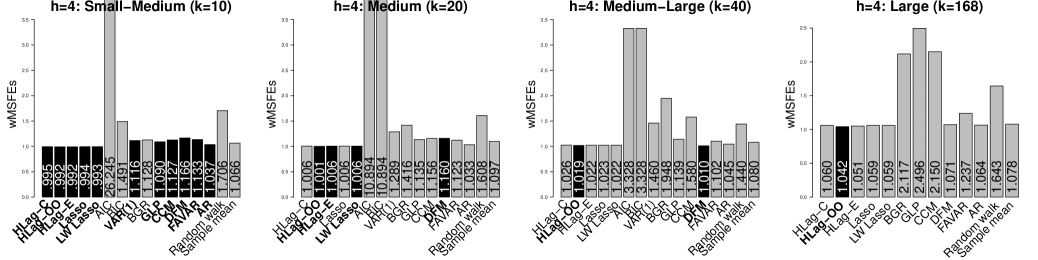

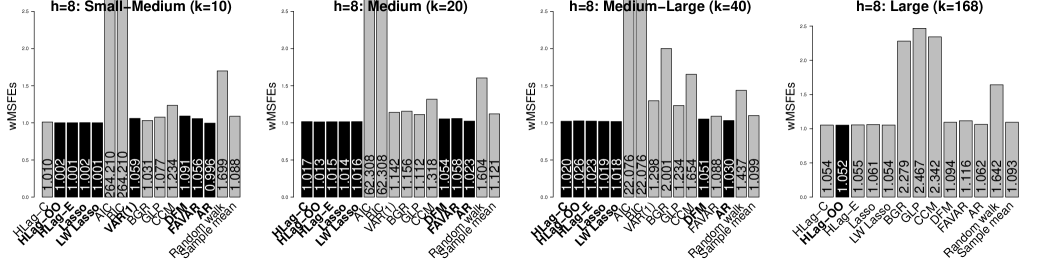

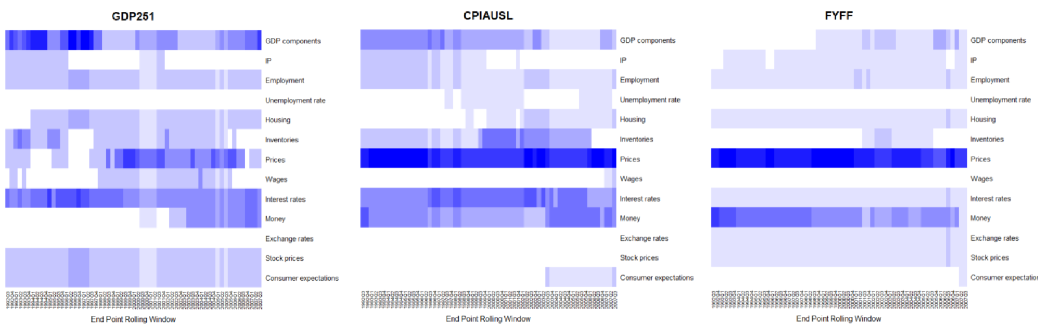

6.ThegoodperformanceoftheHLagmethodsacrossallvariablesisconfirmedbyasub-analysisonthe13macroeconomiccategories.Figure18breaksdowntheresultsoftheLargeVARbythe13macroeconomiccategories.Generallyspeaking,theflexibleelementwiseHLagisthebestperformingforecastingmethod;for10outof13categories,itisincludedintheMCS.Thesecondbestperformingmethodsareown-otherHLagandthelag-weightedlasso(bothfor6outof13categoriesintheMCS).

stock12,wefindmultivariateforecastmethodstoprovidenomeaningfulreductionsoversimpleunivariatemethods(ARorsamplemean).

McCracken2016.WehaveperformedthesameempiricalanalysisontheFRED-QDcontainingk=210variablesfromQuarter3,1959toQuarter4,2018(T=238).Similarfindingsareobtained:(i)Own-otherandelementwiseHLagperformcomparabletothelassomethodsandARforsmallVARsizes,butoutperformallothersfortheLargeVARandashortforecasthorizon.(ii)Own-otherHLagisthepreferredforecastmethodforseveralmajormacroeconomicindicatorssuchasnationalincomeandproductaccountsandindustrialproduction.Fordifficulttopredictindicators,suchasexchangerates,gainsovertheARmodelaredifficulttoattain.

Appendix E FinancialApplication

Thefinancialdatasetcontainsinformationontherealizedvariancesofk=16stockmarketindiceslistedinTable7.Alltimeseriesarelog-transformedtomakethemstationary.

| Variable | Description | |

|---|---|---|

| AEX | Amsterdam Exchange Index | |

| AORD | All Ordinaries Index | |

| BFX | Belgium Bell 20 Index | |

| BVSP | BOVESPA Index | |

| DJI | Dow Jones Industrial Average | |

| FCHI | Cotation Assistée en Continu Index | |

| FTSE | Financial Times Stock Exchange Index 100 | |

| GDAXI | Deutscher Aktienindex | |

| HSI | HANG SENG Index | |

| IXIC | Nasdaq stock index | |

| KS11 | Korea Composite Stock Price Index | |

| MXX | IPC Mexico | |

| RUT | Russel 2000 | |

| SPX | Standard & Poor’s 500 market index | |

| SSMI | Swiss market index | |

| STOXX50E | EURO STOXX 50 |