Randomization Inference for Treatment Effect Variation

Abstract

Applied researchers are increasingly interested in whether and how treatment effects vary in randomized evaluations, especially variation not explained by observed covariates. We propose a model-free approach for testing for the presence of such unexplained variation. To use this randomization-based approach, we must address the fact that the average treatment effect, generally the object of interest in randomized experiments, actually acts as a nuisance parameter in this setting. We explore potential solutions and advocate for a method that guarantees valid tests in finite samples despite this nuisance. We also show how this method readily extends to testing for heterogeneity beyond a given model, which can be useful for assessing the sufficiency of a given scientific theory. We finally apply our method to the National Head Start Impact Study, a large-scale randomized evaluation of a Federal preschool program, finding that there is indeed significant unexplained treatment effect variation.

keywords:

causal inference, randomization test, Head Start, heterogeneous treatment effect1 Introduction

Researchers and practitioners are increasingly interested in whether and how treatment effects vary in randomized evaluations. For example, economic theory predicts that changes in welfare policy will lead to heterogeneous responses beyond those explained by observable characteristics. Given this, how can we use experimental data to assess whether there is in fact unexplained treatment variation (Bitler et al., 2010)? Similarly, we might be interested in assessing the effect of scaling up a promising intervention evaluated on a limited subpopulation (O’Muircheartaigh and Hedges, 2014). If we only use observed characteristics to predict the program’s effectiveness on the new population, we might wonder if we are missing critical unexplained variation, which could undermine our generalization. The goal of this paper is to build a framework to assess treatment effect variation not explained by observed covariates, also known as idiosyncratic variation (e.g., Heckman et al., 1997; Djebbari and Smith, 2008).

Unfortunately, assessing such variation is difficult—to paraphrase Anna Karenina: “constant treatment effects are all alike; every varying treatment effect varies in its own way.” In general, researchers investigating specific types of idiosyncratic variation must therefore rely on strong modeling assumptions to draw meaningful conclusions from the data (Cox, 1984; Heckman et al., 1997; Gelman, 2004). The key contribution of our paper is an approach that tests for the presence of unexplained treatment effect variation without requiring any such modeling assumptions. In the simplest case, the proposed method is a test of the null hypothesis that the treatment effect is constant across all units. More generally, the approach tests whether there is significant unexplained variation beyond a specified model of treatment effect.

Of course, all treatment effects vary in practice, especially in the social sciences, which is our area of application. The key question is whether the unexplained variation is sufficiently large to be of substantive importance. As with all omnibus-type testing procedures, rejecting this null hypothesis does not provide any indication of the source of the unexplained variation. Rather, we view this procedure as a non-parametric first step in characterizing the results of a randomized experiment.

In the simplest no-covariate case, the goal of this approach is to test whether the treatment outcome distribution is the same as the control outcome distribution shifted by the Average Treatment Effect (ATE), a constant. Such testing would be straightforward if this shift were known—we could simply apply standard Kolmogorov-Smirnov-type (KS) tests. However, since the shift is not known, it is a nuisance parameter that we must estimate. In this case, otherwise sensible methods, such as “plug-in” approaches, can fail, even asymptotically (e.g., Babu and Rao, 2004). Incorporating covariates only compounds this problem.

Testing features of distributions in the presence of nuisance parameters has a long history in statistics and econometrics, where in the latter it is known as the Durbin Problem (Durbin, 1973). Several papers tackle this issue in the context of comparing treatment and control outcome distributions, appealing to various asymptotic justifications to bypass the nuisance parameter problem. These include a martingale transformation (Koenker and Xiao, 2002) and subsampling (Chernozhukov and Fernández-Val, 2005).

We take a different approach, exploiting the act of randomization as the “reasoned basis for inference” (Fisher, 1935). The corresponding Fisher Randomization Test (FRT) does not rely on further model assumptions, asymptotics, or regularity conditions (for a review, see Rosenbaum, 2002b). For the constant treatment effect case, when the ATE is assumed known, the FRT procedure yields an exact -value for the sharp null hypothesis of a constant treatment effect (for one generalization, see Abadie, 2002). When the ATE is unknown, the null hypothesis is no longer sharp. To correct for this, we first construct a confidence interval for the ATE, repeat the FRT procedure pointwise over that interval, and then take the maximum -value. As Berger and Boos (1994) show, this procedure guarantees a valid test, despite the presence of the nuisance parameter. This process readily generalizes for testing treatment effects beyond a hypothesized model.

Our FRT-based approach has several key advantages. First, since the FRT approach is justified by the physical randomization alone, it yields valid inference in finite samples without relying on asymptotics or requiring absolutely continuous outcomes. Second, the FRT automatically accounts for complex experimental designs, such as stratified and matched-pair randomizations or even re-randomization (Morgan and Rubin, 2012). Third, this procedure is valid for any test statistic, though some statistics will be more powerful in certain settings. With this flexibility, researchers can easily extend the FRT approach, tailoring the specific test statistic to their particular problem of interest.

Using this framework, we assess treatment effect variation in the National Head Start Impact Study, a large-scale randomized evaluation of Head Start, a Federal preschool program (Puma et al., 2010). After evaluating a range of null models, we find that there is substantial unexplained treatment effect variation, even when considering heterogeneity across age of student, dual-language learner status, and baseline academic skill level, suggesting that policymakers should not base key decisions on the topline results alone.

The paper proceeds as follows. Section 2 describes treatment effect variation using the potential outcomes framework as well as how variation depends on the chosen outcome scale. Section 3 gives an overview of various measures of treatment effect variation. Section 4 outlines the FRT method we propose, and Section 5 generalizes this approach to incorporate covariates. Sections 6 through 8 provide some simulation studies, apply this approach to Head Start, and discuss next steps. The on-line supplementary material contains all proofs as well as additional details.

2 Defining Treatment Effect Variation

Following the causal inference literature, we describe our approach using the potential outcomes framework (Neyman, 1990; Rubin, 1974). We focus on the case of a randomized experiment with a binary treatment, , and continuous outcome, . Let be the number of subjects in the study, with of them randomly assigned to treatment and of them assigned to control. As usual, we invoke the Stable Unit Treatment Value Assumption, which states that there is only one version of the potential outcomes and that there is no interference between subjects (Rubin, 1980).

With this setup, the potential outcomes for subject under treatment and control are and . The science table is the table containing the potential outcomes for all units (Rubin, 2005). Each individual’s observed outcome is a function of the treatment assignment and the potential outcomes,

where the randomness comes only from the random treatment assignment. Let and denote the treatment assignment and observed outcome vectors, respectively. We define the individual treatment effect in the usual way as , but note that other contrasts are also possible. Finally, we define the finite sample average treatment effect as:

This is a statement about the units we observe. In other words, we condition on the sample at hand.

The treatment effect is constant if for all . Otherwise, we say that the treatment effect varies across experimental units. In the language of hypothesis testing, we can define the constant treatment effect null as:

| (1) |

If were known to be , this hypothesis becomes sharp.

2.1 Constant shift

We can not, however, directly observe any individual-level treatment effects, , since we only ever observe one potential outcome for each unit. Instead, we observe the marginal distributions of the treatment and control groups. Because of this, much of the literature (see, e.g., Cox, 1984) defines a “constant treatment effect” as a statement that the marginal CDFs of the potential outcomes of the experimental and control unit distributions and are a constant shift apart:

| (2) |

Rejecting implies rejecting the more restrictive null that for all , but rejecting does not necessarily imply rejecting . That said, it is difficult to imagine the practical situation in which there is a substantial, varying treatment effect that nonetheless yields parallel CDFs. Even more interestingly, the two nulls appear to be indistinguishable given observed data. Therefore, while not formally correct, we generally view tests for as tests for . Simulation studies, not shown, suggest that this practice generally leads to valid, if somewhat conservative, tests. Understanding this relationship is an important area of future work, and is closely related to the interplay between Neyman- and Fisher-style tests. See, for example, Ding (2014).

2.2 Treatment effect variation and scaling

Whether a given treatment effect is constant critically depends on the scale of the outcomes. For example, a job training program that has a constant effect in earnings does not have a constant effect in log-earnings. This scaling issue is a particularly salient issue if the outcome is, say, test scores in an educational context where scale is not necessarily well defined.

Cox (1984) demonstrates the importance of scaling in a special case first explored by G.E.H. Reuter: if the marginal CDFs of and do not cross, there exists a monotone transformation such that the distributions of the transformed treatment and control outcomes are a constant shift apart. Unfortunately, G.E.H. Reuter has since passed away and his proof is lost to the literature; we provide a proof of this theorem in the supplementary material.

Theorem 1.

Assume and are both continuous and strictly increasing CDFs of the marginal distributions of and , respectively, with strict stochastic dominance for all on . There exists an increasing monotone transformation such that the CDFs of and are parallel.

While the applicability of this result is limited to non-crossing CDFs, it nonetheless emphasizes the importance of scale and of understanding the problem at hand. In general, whether a given transformation is substantively reasonable depends on the context: a cube-root transformation might be very sensible if the outcome is in , but not if the outcome is in dollars (Berrington de González and Cox, 2007).

3 Measures of Treatment Effect Variation

There are many approaches to measuring treatment effect variation, dating back to early work on non-additivity in randomized experiments (see Berrington de González and Cox, 2007). We briefly highlight three basic measures: comparing marginal variances, comparing marginal CDFs, and comparing marginal quantiles. The usual testing procedures with the measures discussed here typically yield reasonable inference only when particular conditions, such as Normality or asymptotic regularity, are met. In the next section, we show how the Fisher Randomization Test can yield exact -values with any of these test statistics, regardless of whether these conditions are met.

To fix notation, assume that the potential outcome for treatment is drawn from the distribution of , with marginal PDF , CDF , quantile function , mean , and variance . Sample analogues are denoted with hats.

3.1 Comparing variances

Following Cox (1984), we can assess treatment effect heterogeneity by examining the marginal variances of the treatment and control outcomes. In particular, if the treatment effect is constant, and . Therefore, unequal sample variances imply treatment effect heterogeneity, although the converse is not necessarily true. This makes the variance ratio,

an attractive statistic, especially if the researcher believes that the treatment plausibly induces greater variance (e.g., Gelman, 2004).

Furthermore, if the marginal distributions of potential outcomes are Normal, then follows an distribution and the corresponding test is the Uniformly Most Powerful test of equal variance. However, as we show in the supplementary material, the test is highly sensitive to departures from Normality, even asymptotically. We also provide a test that uses higher-order moments, such as kurtosis, to improve inference in this case.

3.2 Comparing CDFs

In general, second-order moments might not capture some important features of heterogeneity, especially when varies with . For example, a classroom intervention might have the largest effect on the lowest performing students. An alternative approach compares marginal CDFs rather than higher-order moments, suggesting the use of a KS-like test to compare the treatment and control groups. The classic KS statistic, which measures the maximum point-wise distance between two curves, is . This test, however, could reject if the treatment effect is constant but non-zero, since it is an omnibus test for any difference in distribution.

To focus on heterogeneous treatment effects, we want to shift one of the CDFs by the ATE, and then compare the resulting distributions. In particular, if were known, we could calculate:

Under the null, the two aligned CDFs should be the same and we can directly compare the observed test statistic to the null distribution for the classic, non-parametric distribution-free KS test.

In practice, is unknown and is therefore a nuisance parameter. One natural approach is to plug in the difference-in-means estimate, , yielding the “shifted” KS (SKS) statistic:

As we prove in the supplementary material, however, comparing this test statistic to the usual null KS distribution yields invalid -values. In particular, converges to an asymptotic distribution that depends on the underlying distributions of the outcomes.

3.3 Comparing quantiles

A third approach focuses on quantiles rather than on CDFs. In this formulation,

where is the quantile process for the treatment effect. If the effect is constant, then is constant across . Based on this, Chernozhukov and Fernández-Val (2005) propose a class of test statistics based on the estimated quantile process,

where is an estimate of the treatment effect at the th quantile, and is some norm, such as sup.

As in the CDF case, remains a nuisance parameter, so the Durbin problem remains. Chernozhukov and Fernández-Val (2005) solve this via subsampling. Their main argument is that, under some regularity conditions, a particular form of re-centered subsampling can yield asymptotically valid tests for whether is constant, despite dependence on . Chernozhukov and Fernández-Val (2005) and Linton et al. (2005) also propose a bootstrap variant of the subsampling procedure, though the bootstrap does not have the same general, theoretical guarantees as subsampling. For other approaches for inference on quantiles, see Doksum and Sievers (1976), Rosenbaum (1999), and Koenker and Xiao (2002).

4 A Randomization Test for Treatment Effect Variation

Our analytic approach is based on the FRT. To perform an FRT, a researcher needs three main ingredients: a randomized treatment assignment mechanism, a sharp null hypothesis, and a test statistic, , such as those in the previous section. Under the sharp null, all missing potential outcomes can be imputed and are thus known. Given all the potential outcomes, a researcher can then enumerate the possible values of a specified test statistic under all possible randomizations. This enumeration forms the exact null distribution, called the reference distribution, of that statistic.

4.1 FRT with known

First consider a sharp null hypothesis of no heterogeneity for a known :

Given this null, we can immediately impute all missing potential outcomes from the observed data. For a unit with , the potential outcome under treatment is and the potential outcome under control is . For a unit with , the potential outcome under treatment is and the potential outcome under control is .

The steps of the FRT are then:

-

1.

Calculate the test statistic for the observed data, .

-

2.

Given the observed outcomes, , the treatment assignment, , and the sharp null, , generate the corresponding science table.

-

3.

Enumerate all possible treatment assignments, , under the given treatment assignment mechanism. These are all possible treatment assignments that we could have observed for a given experiment. Typically, there are too many possible enumerations so we instead take a random sample from the set of all possible assignment vectors.

-

4.

For each possible assignment, , compute: (1) the observed outcomes, given and the science table; and (2) the test statistic . The resulting distribution of across all randomizations is the exact distribution of the test statistic given the units in the sample and the null hypothesis.

-

5.

Compare the observed statistic to its null distribution and obtain the -value

This procedure yields an exact test for any test statistic assuming is known. For instance, we can use as test statistics any of the measures of treatment effect heterogeneity discussed in the previous section, such as and .

4.2 FRT with unknown

When is unknown, the null hypothesis is no longer “sharp” in the sense that we can no longer impute all the missing potential outcomes. We provide two options.

4.2.1 FRT plug-in method (FRT-PI)

One option is to impute the science table with the estimated instead of , and run the FRT to obtain the distribution of for that table. Ideally, if is close to , the resulting science tables will be close in that the exact reference distribution for the imputed science table should look similar to the true reference distribution for our sample. If this is the case, then inference from this plug-in procedure should be close to the case where is known, i.e., . Nonetheless, as Berger and Boos (1994) discuss, there are no general theoretical guarantees from such a procedure. In fact, as we show in the simulation studies, this approach can lead to invalid results when is highly variable, such as for skewed distributions, though it does appear to have sensible size for approximately Normal outcomes.

Nevertheless, this approach is distinct from appealing to the asymptotic distribution of a given test statistic. Instead, this attempts to generate a reference distribution based on the data at hand, which may make the Durbin problem far less severe. Even so, as we show next, we can guarantee validity with a mild extension of this approach.

4.2.2 FRT confidence interval method (FRT-CI)

An alternative approach is to find the maximum -value across all values of the nuisance parameter, :

where is obtained by performing an FRT under the sharp null . Although is conservative, it is still valid since . This approach, however, leads to two complications in practice: (1) maximizing a quantity over the entire real line is computationally intractable; and (2) doing so can lead to a dramatic loss in statistical power.

Berger and Boos (1994) propose a convenient fix to these issues—rather than maximize over the entire real line, they instead maximize over a -level confidence interval for , :

Following Rosenbaum (2002b), we could obtain an exact (under ) confidence interval, , by inverting FRTs for a sequence of sharp null hypotheses, . In practice, we approximate this confidence interval based on the Neyman variance estimator (Neyman, 1990). The following proposition guarantees the validity of the resulting -value.

Proposition 2.

Given that is a -level confidence interval for , is a valid -value, in the sense that under the null.

As Berger and Boos (1994) note, the behavior of the -values at the tails of the nuisance parameter interval can be complex and, unsurprisingly, depends on both the specific test statistic and the value of the nuisance parameter. For example, they might climb or be driven to zero. While we cannot provide theoretical guarantees, in our experience, the -values for our chosen test statistics, , tend toward 0 or remain flat for values of moderately far from , which suggests our method does not sacrifice much in terms of power.

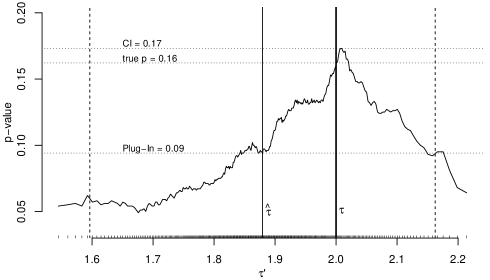

To illustrate this procedure, we simulate a balanced randomized experiment with a constant treatment effect, , , and . Figure 1 shows -values from FRTs for a fixed data set under for in a 99.9% confidence interval, following the procedure described above using as the test statistic. If the true were known, we could obtain the exact -value of . The -value at the observed value of is too low, around , demonstrating why a simple plug-in approach may yield incorrect size. Finally, taking the maximum -value over the Confidence Interval yields a -value of , only slightly larger than the true value of 0.16. This figure, with the “mountain” shape, is typical for this test statistic under many data generation processes.

5 Incorporating Covariates

In practice, we typically observe a vector of individual-level pre-treatment covariates, , that are possibly related to the outcome. This can help increase the power of our test and also enable exploration of variation beyond that which can be explained by .

5.1 Using covariates to improve power

To improve power we allow the chosen test statistic to account for the relationship between the covariates and outcome, such as via a linear regression of outcome on covariates and treatment with no interaction. In the linear regression case, for example, we can generate a “regression adjusted KS statistic.” This statistic compares the CDFs of the residuals of a regression of on and (with no interaction of and ). Let be the residuals of a pre-specified regression, with being the associated predicted values. Then define our test statistic as

| (3) |

where and are the empirical CDFs of the residuals for the treatment and control groups, respectively.

To motivate this, consider the simple regression of on . The residuals of this regression are for the treated units and for the control units. Since and , the regression-adjusted KS statistic for the simple regression of on is equivalent to the Shifted KS statistic: without covariates, .

Now, by including covariates we hope to remove variation due to covariates, making variation in treatment effect more readily apparent. As long as is predictive of , regression adjustment reduces residual variation in the marginal outcomes, but cannot directly reduce variation in the treatment effect. In general, covariate adjustment will therefore yield more powerful test statistics. Importantly, since the validity of the approach is justified by randomization alone, this adjustment does not require any underlying model assumptions. This approach is analogous to the classical, model-assisted covariate adjustment in randomized experiments (Rosenbaum, 2002a; Lin, 2013).

We can easily repeat this approach with , re-defining the test statistic via the residual variance after a regression of on . However, accounting for covariates with quantile-based statistics is more complicated, with two basic approaches in the literature. In the conditional approach, we re-define via the estimate of in a quantile regression of on both and , as in Koenker and Xiao (2002). In the unconditional approach, we re-define via the estimate of in a weighted quantile regression of on , with weights defined as a given function of , as in Firpo (2007) or Firpo et al. (2009).

5.2 Treatment effect variation beyond covariates

In many applications, the constant treatment effect null may be of limited scientific interest. Instead, we wish to investigate whether there is significant treatment effect variation beyond a particular model for the treatment. For example, Bitler et al. (2010) propose the Constant Treatment Effect Within Subgroups model, which assumes that the average treatment effect differs across observable subgroups (e.g., by education or age group) but is otherwise constant within those subgroups.

To make this more precise, let be an matrix of the unit vector and pre-treatment covariates. The unit vector corresponds to the overall average treatment effect and the covariates allow for modeled treatment effect heterogeneity. We then replace the null hypothesis of a constant treatment effect with the assumption that the individual-level treatment effects are a particular function of :

| (4) |

where is some (unknown) vector of coefficients for . Under the null, there is some such that the set of yields the same CDF as the set of .

We can easily test this hypothesis using the regression-adjusted KS statistic, , constructed via the residuals of a regression of on , , and . This regression yields point estimates with a corresponding -dimensional confidence region. To obtain the FRT-PI -value, we simply use the science table based on . To obtain the FRT-CI -value, we must repeat the FRT procedure for each point in a potentially high-dimensional grid. We defer a detailed discussion of the estimation issues in this setting to our companion paper.

We can also extend this regression approach to account for covariates that are not assumed to interact with the treatment (i.e., those in but not ). Furthermore, we can allow the treatment effect model to be arbitrarily flexible, including series expansions on the covariates, such as splines or higher-order polynomials. See Crump et al. (2008) for a discussion of non-parametric estimation in this context.

5.3 Subgroup variation

We briefly turn to the special case in which the treatment effect is assumed to vary across discrete groups. Let be the observed outcome of unit in group , for and , with the number of treated units in group .

For example, consider a stratified experiment, where both and are fixed. Of course, we can always analyze a stratified experiment as if it were separate, completely randomized experiments. However, we can also test whether variation across strata explains the full variation in treatment effects. This corresponds to the following joint null hypothesis of stratum-specific treatment effects, :

Under this null, the pooled CDF of the recentered-by-stratum outcomes of all the units under treatment (i.e., the residuals from outcome regressed on strata) would be the same as for control.

To test the null, we then need a measure of discrepancy between the estimates of the two CDFs as our test statistic. Several choices are possible. First, we can use , the regression-based test statistic above, letting be a matrix of indicators for stratum membership and be (with no intercept). However, if the proportions of treated units differ across strata or if homoskedasticity is implausible, pooling may not be appropriate. Instead, we can post-stratify by weighting each group-by-stratum empirical CDF with weight proportional to the stratum size. The revised is then

where is the empirical CDFs of the for those units in stratum with .

Similarly, we might instead take a weighted average of individual stratum-level test statistics as

Figure 2 demonstrates this last approach by extending the results from Figure 1 into two dimensions. Here we have two distinct subgroups, one of 75 units and one of 375 units, and simulate a balanced randomized experiment with a treatment effect that is constant within each subgroup, but not constant overall. The baseline distributions are exponential. We then test for treatment effect heterogeneity beyond these discrete subgroups. To do this we search over a confidence set, depicted in the figure, for a maximum -value. We again see the “mountain shape” and end up with a final -value of 0.46, versus for known and for the plug-in . As in the one-dimensional case, the plug-in -value is lower than the true -value. Moreover, the maximum -value is only modestly higher than the truth, as the -values fall away at moderate distances from the true . This plot is typical over several simulation settings. Finally, as expected, if we do an omnibus test for heterogeneity beyond a single average treatment effect, we reject with . Our model of constant treatment effect within groups is thus significantly better than a single average, and we have no evidence for needing a more complex model.

The Constant Treatment Effect Within Subgroups model of Bitler et al. (2010) is equivalent to except that the number of treated units in each group, , is possibly random rather than fixed. Here simply conditioning on the observed for each group (i.e., only considering randomizations that maintain the ) and performing the analysis as above yields valid inference. This is a conditional randomization test, the analogue of post-stratification for testing rather than estimation (see, e.g., Holt and Smith, 1979; Miratrix et al., 2013).

6 Simulation Studies

We now turn to a series of simulation studies that confirm the validity of the FRT approach and assess power under a range of plausible scenarios.

6.1 Validity results

First, we examine the different methods under the null hypothesis of a constant treatment effect. To assess validity, we repeat the following times each for a given test statistic and underlying distribution:

-

1.

generate a sample from the underlying distribution, assuming a constant treatment effect;

-

2.

randomly assign treatment and obtain observed outcomes;

-

3.

calculate our test statistic ; and finally

-

4.

calculate a -value using each of several different approaches described below.

We assess five methods:

-

•

Naive Plug-In: This method calculates the usual KS -value, assuming that the estimated treatment effect is in fact the true treatment effect.

-

•

FRT-PI and FRT-CI: These methods are the two FRT-based approaches discussed above. For this simulation, we use a 99.9% confidence interval for (i.e., ).

-

•

Subsampling: This method is the subsampling approach of Chernozhukov and Fernández-Val (2005), with the authors’ recommended subsampling size of .

-

•

Bootstrap: This method is based on the bootstrap proposed by Chernozhukov and Fernández-Val (2005) and Linton et al. (2005), using the test statistics. To generate the bootstrap distribution, we de-mean the treatment and control groups and sample with replacement from the pooled vector of residuals, keeping the number of treatment and control units fixed.

We assess these five methods for the following distributions: standard Normal, , standard Exponential, and Log-Normal, each with a constant treatment effect of unit.

Table 1 shows the rejection rates for a test of size for each method and Data Generating Process (DGP). As expected, the naive plug-in approach fails dramatically, either yielding hyper-conservative or highly invalid size. The FRT-PI approach appears to work well for the symmetric Normal and distributions, but leads to invalid size for the skewed Exponential and Log-Normal distributions. The FRT-CI approach corrects for this, yielding exact or conservative size for all DGPs assessed here, where conservative indicates lower than nominal rejection rates. It is encouraging that, even when the FRT-CI is conservative, it is not dramatically so, suggesting we are not giving up too much power due to the maximization procedure. Subsampling yields correct, if slightly conservative, rejection rates overall. Finally, the bootstrap approach is invalid for the Normal, , and Exponential distributions.

The bootstrap approach we used seemed the most promising choice. Other alternatives to the bootstrap exist, but they seem to perform even more poorly. For example, one seemingly obvious bootstrap is to repeatedly sample, with replacement, treatment cases and control cases from their respective original samples, calculating the resulting test statistic. Ideally, this would capture the variability of the entire process, giving a valid -value for the actual observed test statistic. Unfortunately, even if the null were true, the bootstrap null would generally not be in this context, and so we would end up simulating our distribution under a “near alternative” which gives poor size. We confirmed this intuition with simulations, not shown in this paper, that indeed show this approach can fail catastrophically.

| Normal | Expo | Log-Normal | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 1,000 | 100 | 1,000 | 100 | 1,000 | 100 | 1,000 | ||||

| FRT-PI | 4.5 | 5.1 | 5.4 | 5.2 | 11.3 | 7.7 | 15.1 | 7.0 | |||

| FRT-CI | 1.9 | 3.8 | 2.1 | 3.7 | 4.1 | 4.9 | 4.5 | 5.0 | |||

| Subsampling | 2.3 | 4.6 | 1.5 | 1.6 | 2.1 | 2.3 | 1.1 | 0.7 | |||

| Bootstrap | 9.3 | 8.8 | 7.4 | 8.3 | 6.3 | 6.1 | 5.0 | 6.5 | |||

| Naive Plug-In | 0.0 | 0.0 | 0.0 | 0.0 | 12.3 | 21.4 | 36.2 | 44.7 | |||

6.2 General power simulations

To assess the power of these methods under select alternatives we mirror a set of simulation studies conducted by both Koenker and Xiao (2002) and Chernozhukov and Fernández-Val (2005). For these simulations, we repeatedly generate data with different levels of treatment effect heterogeneity, denoted by , and estimate the probability that a method would reject the null of constant treatment effect (at ) given draws of data and random treatment assignment. Since the bootstrap, FRT-PI, and naive plug-in are invalid tests, we do not include them here.

We use a binary version of the DGP from Chernozhukov and Fernández-Val (2005):

with . This model can also be expressed as the classic additive treatment effect model under Normality, , where ; on the margin, and corresponds to a constant treatment effect. Note that, as Cox (1984) observes, the -test is the Uniformly Most Powerful Test in this setting.

We then extend the simulations from Chernozhukov and Fernández-Val (2005) by imposing Log-Normality rather than Normality. In particular, we assume a treatment effect of the following form:

Then marginally . In either case, for , the treatment effect increases with , which is non-negative. Rosenbaum (1999) calls this kind of treatment effect variation a dilated effect.

Table 2 shows the main power results. For Normal outcomes, both the FRT-CI and subsampling methods have correct size when . However, subsampling appears to be more powerful for , perhaps because the the asymptotics to “kick in” quickly under Normality. For Log-Normal outcomes, however, the situation is reversed, with much greater rejection rates under FRT-CI than under subsampling.

| FRT-CI | Subsampling | ||||||

|---|---|---|---|---|---|---|---|

| A. NORMAL OUTCOMES | |||||||

| 2.3 | 5.5 | 23.1 | 2.4 | 8.4 | 39.2 | ||

| 3.5 | 24.8 | 93.0 | 4.0 | 40.1 | 98.4 | ||

| 3.5 | 52.3 | 100.0 | 4.6 | 72.9 | 100.0 | ||

| B. LOG-NORMAL OUTCOMES | |||||||

| 4.7 | 7.3 | 19.3 | 1.2 | 2.2 | 5.9 | ||

| 4.7 | 19.8 | 70.5 | 0.6 | 3.4 | 32.9 | ||

| 4.6 | 35.1 | 94.1 | 0.8 | 9.1 | 70.7 | ||

7 Application to the Head Start Impact Study

Initially launched in 1965, Head Start is the largest Federal preschool program today, serving around 900,000 children each year at a cost of roughly $8 billion. The National Head Start Impact Study (HSIS) is the first major randomized evaluation of the program (Puma et al., 2010). The published report found that, on average, providing children and their families with the opportunity to enroll in Head Start improved children’s key cognitive and social-emotional outcomes. The report also included average treatment effect estimates for a variety of subgroups of interest, though there is only significant impact variation across a small number of the reported, pre-treatment covariates.

After these findings were released, many researchers argued that the reported topline results masked critical variation in program impacts. For example, Bitler et al. (2013) show that the treatment is differentially effective across quantiles of the test score distribution; Bloom and Weiland (2014) explore variation in program impacts across select subgroups and across the 351 Head Start centers in the study; and Feller et al. (2014) investigate differential effects based on the setting of care each child would have received in the alternative treatment condition.

All of these approaches, however, estimate treatment effect variation by relying on a specific set of models, such as quantile or hierarchical regression. Given the breadth of research in this area, a natural question is whether the topline and subgroup average treatment effects for HSIS are indeed sufficient summaries of the program’s effect. We investigate this question by focusing on the Peabody Picture Vocabulary Test (PPVT), a widely used measure of cognitive ability in early childhood. We also utilize a rich set of pre-treatment covariates, including pre-test score, child’s age, child’s race, mother’s education level, and mother’s marital status. In addition, we follow the experimental design and ensure that the randomizations used in the FRT procedure are stratified by Head Start center. For the sake of exposition, we restrict our analysis to a complete-case subset of HSIS, with 2,238 in the treatment group and 1,348 in the control group. Note that this restriction could lead to a range of inferential issues which we do not explore here; see Feller et al. (2014) for a detailed discussion.

As shown in Table 3, we apply the FRT procedure to a set of increasingly flexible null hypotheses. The least flexible models, Model 1 and 2, assesses the null hypothesis of constant treatment effect across all units without and with covariate adjustment, using the statistic and the statistic respectively. Model 3 adjusts for pre-treatment covariates and allows the treatment effect to vary by child’s age (three vs. four years old). The most flexible model, Model 4, allows the treatment effect to vary by child’s age, child’s Dual-Language Learner (DLL) status, and an indicator for whether the child was in the bottom quartile on an assessment of pre-academic skills prior to the study. The resulting -values are roughly for the model without covariates and across all three models that adjust for covariates, clearly demonstrating significant unexplained variation regardless of the exact specification. This provides evidence that there is indeed substantial treatment effect variation beyond that explained by these subgroups.

| (1) | (2) | (3) | (4) | ||

|---|---|---|---|---|---|

| -value: | 0.033 | 0.005 | 0.005 | 0.003 | |

| Treatment effect varies by: | — | — | age | age | |

| DLL status | |||||

| acad. skills | |||||

| Control for covariates: | — |

8 Discussion

Researchers are increasingly interested in assessing treatment effect heterogeneity. We propose a framework to unify and generalize some existing statistical procedures for inference about such variation, using randomization as the “reasoned basis for inference” for the testing procedure. As a result, the method does not rely on any further model assumptions, asymptotics, or regularity conditions. We use simulation studies to confirm that this approach yields valid results in finite samples and that its power is competitive with some existing approaches, especially subsampling. Finally, we apply this method to the National Head Start Impact Study, a large-scale randomized evaluation, and find that there is indeed significant unexplained treatment variation.

Other randomization-based approaches to heterogeneity also exist. These methods typically specify a model for heterogeneity and test based on that model. For example Rosenbaum (2011) provides randomization tests for rare but substantial effects. Rosenbaum (1999) proposes a randomization-based procedure for non-negative and non-decreasing quantile treatment effects under the assumption of rank preservation. See section 2.4.4 of Rosenbaum (2010) for discussion of testing general null hypotheses of non-zero treatment effects. By contrast, we attempt to test for heterogeneity in an unstructured way, though the choice of test statistic is motivated by the problem at hand. As additional assumptions on the structure of the heterogeneity will increase statistical power, using these approaches may be more appropriate than our omnibus method when such assumptions are met.

There is one important complication that we do not directly address here: the case of discrete outcomes. Even though the FRT procedure still yields valid inference in this setting, the constant treatment effect hypothesis may no longer be of scientific interest. This is a fundamental issue and is not specific to any particular testing procedure. For example, consider a semi-continuous outcome distribution, with a large point mass at zero. For example, in the Connecticut Jobs First evaluation, roughly half the sample has no earnings (Bitler et al., 2006). Here, the constant effect null hypothesis implies that welfare reform has the same dollar impact regardless of whether the individual starts with zero earnings, which is nonsensical. In future work, we hope to explore different approaches for this setting, including latent variable formulations.

In the end, our approach offers a flexible framework for assessing treatment effect variation in randomized experiments, allowing researchers to incorporate a broad range of test statistics and accommodate complex experimental designs. Most of all, our goal is to give applied researchers a set of tools so that inference about treatment effect variation can becomes standard step in the analysis of randomized experiments. Next steps are to explore the role of covariates in treatment effect variation and, in particular, the interplay between systematic and idiosyncratic treatment effect variation.

Acknowledgements

The authors would like to thank Alberto Abadie, Marianne Bitler, Paul Rosenbaum, Don Rubin, Tyler VanderWeele, and participants at the Atlantic Causal Inference Conference, the Joint Statistical Meetings, and the Harvard–MIT Econometrics Workshop for helpful comments. We especially want to thank Sir David Cox for his insights and for bringing G. E. H. Reuter’s lost proof to our attention. We also thank the editor and two anonymous reviewers for their very helpful feedback. The research reported here was partially funded under cooperative agreement #90YR0049/02 with the Agency for Children and Families (ACF) of the U.S. Department of Health and Human Services. The opinions expressed are those of the authors and do not represent these institutions.

References

- Abadie (2002) Abadie, A. (2002). Bootstrap tests for distributional treatment effects in instrumental variable models. J. Am. Statist. Ass. 97, 284–292.

- Babu and Rao (2004) Babu, J. G. and C. R. Rao (2004). Goodness-of-fit tests when parameters are estimated. Sankhyā 66, 63–74.

- Berger and Boos (1994) Berger, R. L. and D. D. Boos (1994). P values maximized over a confidence set for the nuisance parameter. J. Am. Statist. Ass. 89, 1012–1016.

- Berrington de González and Cox (2007) Berrington de González, A. and D. R. Cox (2007). Interpretation of interaction: A review. Ann. Appl. Statist. 1, 371–385.

- Bitler et al. (2013) Bitler, M. P., T. Domina, and H. W. Hoynes (2013). Experimental evidence on distributional effects of Head Start. http://www.socsci.uci.edu/~mbitler/papers/bdh-hsis-paper.pdf. Working Paper.

- Bitler et al. (2006) Bitler, M. P., J. B. Gelbach, and H. W. Hoynes (2006). What mean impacts miss: Distributional effects of welfare reform experiments. Am. Econ. Rev. 96, 988–1012.

- Bitler et al. (2010) Bitler, M. P., J. B. Gelbach, and H. W. Hoynes (2010). Can variation in subgroups’ average treatment effects explain treatment effect heterogeneity? Evidence from a social experiment. http://www.socsci.uci.edu/~mbitler/papers/bgh-subgroups-paper.pdf. Working Paper.

- Bloom and Weiland (2014) Bloom, H. and C. Weiland (2014). To what extent to the effects of head start vary by site?

- Box and Andersen (1955) Box, G. E. and S. L. Andersen (1955). Permutation theory in the derivation of robust criteria and the study of departures from assumption. J. Roy. Statist. Soc. B 17, 1–34.

- Chernozhukov and Fernández-Val (2005) Chernozhukov, V. and I. Fernández-Val (2005). Subsampling inference on quantile regression processes. Sankhyā 67, 253–276.

- Cox (1984) Cox, D. R. (1984). Interaction. International Statistical Review 52, 1–24.

- Crump et al. (2008) Crump, R. K., V. J. Hotz, G. W. Imbens, and O. A. Mitnik (2008). Nonparametric tests for treatment effect heterogeneity. Rev. Econ. Statist. 90, 389–405.

- Ding (2014) Ding, P. (2014). A paradox from randomization-based causal inference. http://arxiv.org/abs/1402.0142. Working Paper.

- Djebbari and Smith (2008) Djebbari, H. and J. Smith (2008). Heterogeneous impacts in PROGRESA. J. Econometrics 145, 64–80.

- Doksum and Sievers (1976) Doksum, K. A. and G. L. Sievers (1976). Plotting with confidence: graphical comparisons of two populations. Biometrika 63, 421–434.

- Durbin (1973) Durbin, J. (1973). Distribution Theory for Tests Based on the Sample Distribution Function. Philadelphia: SIAM.

- Feller et al. (2014) Feller, A., T. Grindal, L. Miratrix, and L. Page (2014). Compared to what? Variations in the impacts of Head Start by alternative care-type settings. Working paper available at http://scholar.harvard.edu/files/feller/files/feller_grindal_miratrix_p%age_12_6_14.pdf.

- Firpo (2007) Firpo, S. (2007). Efficient semiparametric estimation of quantile treatment effects. Econometrica 75, 259–276.

- Firpo et al. (2009) Firpo, S., N. M. Fortin, and T. Lemieux (2009). Unconditional quantile regressions. Econometrica 77, 953–973.

- Fisher (1935) Fisher, R. A. (1935). The Design of Experiments (First Edition). Edinburgh: Oliver and Boyd.

- Gelman (2004) Gelman, A. (2004). Treatment effects in before-after data. Applied Bayesian Modeling and Causal Inference from an Incomplete Data Perspective. London: Wiley, 195–202.

- Heckman et al. (1997) Heckman, J. J., J. Smith, and N. Clements (1997). Making the most out of programme evaluations and social experiments: Accounting for heterogeneity in programme impacts. Rev. Econ. Stud. 64, 487–535.

- Holt and Smith (1979) Holt, D. and T. M. F. Smith (1979). Post stratification. J. Roy. Statist. Soc. A 142, 33–46.

- Koenker and Xiao (2002) Koenker, R. and Z. Xiao (2002). Inference on the quantile regression process. Econometrica 70, 1583–1612.

- Lehmann (1999) Lehmann, E. L. (1999). Elements of Large-Sample Theory. New York: Springer Verlag.

- Lin (2013) Lin, W. (2013). Agnostic notes on regression adjustments to experimental data: Reexamining Freedman’s critique. Ann. Appl. Statist 7, 295–318.

- Linton et al. (2005) Linton, O., E. Maasoumi, and Y.-J. Whang (2005). Consistent testing for stochastic dominance under general sampling schemes. Rev. Econ. Stud. 72, 735–765.

- Miratrix et al. (2013) Miratrix, L. W., J. S. Sekhon, and B. Yu (2013). Adjusting treatment effect estimates by post-stratification in randomized experiments. J. Roy. Statisti. Soc. B 75, 369–396.

- Morgan and Rubin (2012) Morgan, K. L. and D. B. Rubin (2012). Rerandomization to improve covariate balance in experiments. Ann. Statist. 40, 1263–1282.

- Neyman (1990) Neyman, J. (1923 [1990]). On the application of probability theory to agricultural experiments. Statist. Sci. 5, 465–472.

- O’Muircheartaigh and Hedges (2014) O’Muircheartaigh, C. and L. V. Hedges (2014). Generalizing from unrepresentative experiments: a stratified propensity score approach. J. Roy. Statisti. Soc. C 63, 195–210.

- Puma et al. (2010) Puma, M., S. H. Bell, R. Cook, C. Heid, and G. Shapiro (2010). Head Start Impact Study. Final Report. Washington, DC: Department of Health and Human Services, Administration for Children and Families.

- Rosenbaum (1999) Rosenbaum, P. R. (1999). Reduced sensitivity to hidden bias at upper quantiles in observational studies with dilated treatment effects. Biometrics 55, 560–564.

- Rosenbaum (2002a) Rosenbaum, P. R. (2002a). Covariance adjustment in randomized experiments and observational studies. Statist. Sci. 17, 286–327.

- Rosenbaum (2002b) Rosenbaum, P. R. (2002b). Observational Studies. New York: Springer.

- Rosenbaum (2010) Rosenbaum, P. R. (2010). Design of Observational Studies. New York: Springer.

- Rosenbaum (2011) Rosenbaum, P. R. (2011). A new u-statistic with superior design sensitivity in matched observational studies. Biometrics 67, 1017–1027.

- Rubin (1974) Rubin, D. B. (1974). Estimating causal effects of treatments in randomized and nonrandomized studies. J. Educational Psychology 66, 688–701.

- Rubin (1980) Rubin, D. B. (1980). Comment on “Randomization analysis of experimental data: The Fisher Randomization Test”. J. Am. Statist. Ass. 75, 591–593.

- Rubin (2005) Rubin, D. B. (2005). Causal inference using potential outcomes: Design, modeling, decisions. J. Am. Statist. Ass. 100, 322–331.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic Statistics. Cambridge: Cambridge University Press.

Supplementary Materials for

“Randomization Inference for Treatment Effect Variation”

The supplementary materials contain four sections and a few additional notes. Section A.1 discusses the importance of scaling in treatment effect variation, and provides a “lost proof” of Reuter’s Theorem (Cox, 1984). Section A.2 discusses the asymptotic distribution of the variance ratio statistic for non-Normal outcomes and provides a distribution-free test. Section A.3 explains why the simple plug-in approach using the KS test fails, even asymptotically. Section A.4 gives a proof for Proposition 1 in the main text.

A.1 Reuter’s Theorem

As mentioned in Section 2 of the main text, whether a given treatment effect is constant depends on the scale of the outcomes. In particular, if the marginal CDFs of and do not cross, there exists a monotone transformation such that distributions of the transformed treatment and control outcomes are a constant shift apart as defined by (i.e., we can make the CDFs of the treatment outcomes and control outcomes parallel). This was first observed by Cox (1984), citing a theorem due to G. E. H. Reuter. Unfortunately, Reuter has since passed away and his proof has been lost to the literature. We therefore provide a proof of this theorem here. For convenience we restate the theorem:

Theorem 3.

Assume and are both continuous and strictly increasing CDFs of the marginal distributions of and , respectively, with strict stochastic dominance for all on . There exists an increasing monotone transformation such that the CDFs of and are parallel.

First, note that stochastic dominance occurs if and only if the CDFs do not cross, hence the statement of the theorem above. Next, assuming no ties, the finite sample analogue, or the analog conditioning on the realized sample, is immediate. To prove the theorem we first need a few lemmas.

Lemma A.1.1.

Assume that is a strictly increasing and continuous function defined on , which satisfies for all . Then there exists a monotone increasing transformation such that is a constant for all .

Proof of Lemma A.1.1. Define and for ; furthermore, define and for

For the trivial case with , we can easily rescale the range of to make it parallel to because the range is entirely below . To do so, define as follows:

Therefore, we have for all Note that for all our so only impacts the term in the difference.

For the case with , we first need to show that there exist an , such that for all and . We use a proof by contradiction, and assume for all A quick induction shows that, since and , the sequence is strictly decreasing. Furthermore, because the sequence is bounded below by , it must have a limit, , on . Taking on both sides of , we have , which is impossible. Therefore, such an indeed exists. We also have from taking on both sides of , and we can therefore partition the real line as follows:

We will define on each piece of the partition above, from the right to the left.

First define within , and within . This way of construction guarantees that, for any ,

Next define within giving, for all ,

Analogously, we can sequentially define within all intervals for which guarantees that

for all .

We finally define for , which guarantees that

for all .

This constructed satisfies for all .

Lemma A.1.2.

Take random variables and with invertible CDFs and . Then

is equivalent to

Proof of Lemma A.1.2. The conclusion follows if we couple and through a common Uniform random variable : and .

Proof of Theorem 3. Define

which is strictly monotonic and continuous. Furthermore, everywhere. If is then drop the second piece from the definition. Now, define two new random variables and . Then Uniform, and the quantile function of , is strictly increasing. Now, because for all

we can Lemma 1 to obtain such that

for some . We can instead can show that is our transform. Define and . Then ,, and

which implies that the CDFs of and are parallel according to Lemma 2.

A.2 Testing for Idiosyncratic Variation with Variance Ratios

If and are Normally distributed as and , then under the null and the variance ratio , the ratio of sample variances in the two groups, follows an distribution. While this conclusion is not generally true for non-Normal distributions, even asymptotically, we can use higher-order moments to correct this test statistic for non-Normal outcomes.

Theorem 4.

Assume that has finite kurtosis . Under the null of equal variance,

as .

Proof. From the classic result (Lehmann, 1999), we have

and therefore using delta-method we have that

Under the null, , and has the following asymptotic distribution

| (A.1) |

Due to the fact that in probability and Slutsky’s Theorem, we have

Equation A.1 shows that the statistic does not necessarily have an distribution—the distribution depends on and . However, by plugging estimates of these fourth moments in, we do recover an asymptotically distribution free reference distribution for our statistic. The test statistic essentially replaces the Normality assumption with an assumption of finite fourth moments, which is often more plausible. This theorem closely follows Box and Andersen (1955), who use randomization theory to demonstrate that the distribution of the variance ratio depends on the kurtosis of the underlying outcomes.

A.3 Why the Plug-In for the CDF Approach Fails

As stated in the paper, under the null the CDFs of each group aligned by should be the same. If were known, therefore, we could shift the treatment group and compare the resulting distributions via a Kolmogorov-Smirnov test:

Under the null, we can directly compare this observed test statistic to the null distribution from the classic, non-parametric KS test. This would be exact.

Unfortunately is unknown in practice and is therefore a nuisance parameter. One natural-seeming approach is to plug in the difference-in-means estimate, , yielding the “shifted” KS (SKS) statistic:

Comparing this test statistic to the usual null KS distribution, however, yields invalid -values. As Babu and Rao (2004) note, for such tests “the asymptotic null distribution of the test statistic may depend in a complex way on the unknown parameters.” See also (Van der Vaart, 2000, Theorem 19.23), and the relevant discussion in Koenker and Xiao (2002). We show this more formally in Theorem 5.

Theorem 5.

Let , be a standard Brownian Bridge, and be a Gaussian Process with mean function and covariance function The limiting distribution of the SKS statistic is

where and are independent realizations of the shifted Brownian Bridge processes: with covariance structure

The correlation between and is the “complex dependence” referred to above. Since the processes depend on , also depends on and is therefore not distribution free.

In other words, Theorem 5 demonstrates that “naively” plugging in for yields a test statistic with a null distribution that is not the null distribution of the classic KS statistic. Intuitively, if is known, the asymptotic distribution of depends on the sum of two standard Brownian Bridges, which do not depend on . The uncertainty in changes these from standard Brownian Bridges to shifted Brownian Bridges, which do depend on :

As we show in the simulation studies in Section 6 of the main text, the -value of this naive approach can either be inflated or deflated depending on the underlying distribution, . From our experience from simulation studies, the naive plug-in approach is conservative for symmetric distributions such as Normal and distributions, but it does not yield correct type one error for skewed distributions such as Exponential and Log-Normal distributions. Table 1 in the main text illustrates this point.

Proof of Theorem 5. Under the null, the means of the outcomes under treated and control satisfy , the variances are the same , and corresponding PDFs then satisfy . First, we have

The difference between the shifted empirical CDFs is

where the last equality is due to the stochastic equicontinuity of the indicator function. By definition of the empirical CDFs, we have

Since both

and

have the same asymptotic distribution as defined in Theorem 5, we have

The final conclusion follows from the symmetry of the shifted Brownian Bridge.

A.4 Proposition 1 for the FRT-CI Method

Proposition 6.

Given that is a -level confidence interval for , is a valid -value, in the sense that under the null.

Proof of Proposition 1. The validity of the FRT-CI -value is fairly immediate according to Berger and Boos (1994). First, the valid confidence interval guarantees . Second, given the true value of , randomization test yields a valid -value, which implies . Third, given the fact that , the supremum of -values over , , is greater than or equal to . These ingredients give us