1 Introduction

We are interested in a randomly biased walk ( X n ) n ≥ 0 subscript subscript 𝑋 𝑛 𝑛 0 (X_{n})_{n\geq 0} 𝕋 𝕋 {\mathbb{T}} ∅ \varnothing x ∈ 𝕋 \ { ∅ } 𝑥 \ 𝕋 x\in{\mathbb{T}}\backslash\{\varnothing\} x ← superscript 𝑥 ← {\buildrel\leftarrow\over{x}} ω := ( ω ( x , ⋅ ) , x ∈ 𝕋 ) assign 𝜔 𝜔 𝑥 ⋅ 𝑥

𝕋 \omega:=(\omega(x,\cdot),\,x\in{\mathbb{T}}) x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}} ω ( x , y ) ≥ 0 𝜔 𝑥 𝑦 0 \omega(x,\,y)\geq 0 y ∈ 𝕋 𝑦 𝕋 y\in{\mathbb{T}} ∑ y ∈ 𝕋 ω ( x , y ) = 1 subscript 𝑦 𝕋 𝜔 𝑥 𝑦 1 \sum_{y\in{\mathbb{T}}}\omega(x,\,y)=1 ω ( x , y ) > 0 𝜔 𝑥 𝑦 0 \omega(x,\,y)>0 x ← = y {\buildrel\leftarrow\over{x}}=y y ← = x {\buildrel\leftarrow\over{y}}=x

For the sake of presentation, we add a specific vertex ∅ ← superscript ← {\buildrel\leftarrow\over{\varnothing}} ∅ \varnothing ∅ ← ∉ 𝕋 {\buildrel\leftarrow\over{\varnothing}}\not\in{\mathbb{T}} ω ( ∅ ← , ∅ ) := 1 assign 𝜔 superscript ← 1 \omega({\buildrel\leftarrow\over{\varnothing}},\varnothing):=1 ω ( ∅ , ⋅ ) 𝜔 ⋅ \omega(\varnothing,\cdot) ω ( ∅ , ∅ ← ) > 0 𝜔 superscript ← 0 \omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})>0 ω ( ∅ , ∅ ← ) + ∑ x : x ← = ∅ ω ( ∅ , x ) = 1 𝜔 superscript ← subscript 𝑥 : superscript 𝑥 ← absent

𝜔 𝑥 1 \omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})+\sum_{x:{\buildrel\leftarrow\over{x}}=\varnothing}\omega(\varnothing,x)=1

For given ω 𝜔 \omega ( X n , n ≥ 0 ) subscript 𝑋 𝑛 𝑛

0 (X_{n},\,n\geq 0) 𝕋 ∪ { ∅ ← } 𝕋 superscript ← {\mathbb{T}}\cup\{{\buildrel\leftarrow\over{\varnothing}}\} ω 𝜔 \omega ∅ \varnothing X 0 = ∅ subscript 𝑋 0 X_{0}=\varnothing

P ω ( X n + 1 = y | X n = x ) = ω ( x , y ) . subscript 𝑃 𝜔 subscript 𝑋 𝑛 1 conditional 𝑦 subscript 𝑋 𝑛 𝑥 𝜔 𝑥 𝑦 P_{\omega}\big{(}X_{n+1}=y\,|\,X_{n}=x\big{)}=\omega(x,\,y).

For any vertex x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}} ( x ( 1 ) , ⋯ , x ( ν x ) ) superscript 𝑥 1 ⋯ superscript 𝑥 subscript 𝜈 𝑥 (x^{(1)},\cdots,x^{(\nu_{x})}) ν x ≥ 0 subscript 𝜈 𝑥 0 \nu_{x}\geq 0 x 𝑥 x 𝐀 ( x ) := ( A ( x ( i ) ) , 1 ≤ i ≤ ν x ) assign 𝐀 𝑥 𝐴 superscript 𝑥 𝑖 1

𝑖 subscript 𝜈 𝑥 {\bf A}(x):=(A(x^{(i)}),\,1\leq i\leq\nu_{x})

A ( x ( i ) ) := ω ( x , x ( i ) ) ω ( x , x ← ) , 1 ≤ i ≤ ν x . formulae-sequence assign 𝐴 superscript 𝑥 𝑖 𝜔 𝑥 superscript 𝑥 𝑖 𝜔 𝑥 superscript 𝑥 ← 1 𝑖 subscript 𝜈 𝑥 A(x^{(i)}):=\frac{\omega(x,\,x^{(i)})}{\omega(x,\,{\buildrel\leftarrow\over{x}})},\qquad 1\leq i\leq\nu_{x}\,.

When all A ( x ( i ) ) = λ 𝐴 superscript 𝑥 𝑖 𝜆 A(x^{(i)})=\lambda λ 𝜆 \lambda λ 𝜆 \lambda [19 , 20 ] . We mention that several conjectures in [20 ] still remain open and we refer to Aidekon [3 ] for an explicit formula on the speed of the λ 𝜆 \lambda

When A ( x ( i ) ) 𝐴 superscript 𝑥 𝑖 A(x^{(i)}) ( 𝕋 , ω ) 𝕋 𝜔 ({\mathbb{T}},\omega) [22 ] , and the biased walk X 𝑋 X

Let us assume that 𝐀 ( x ) , x ∈ 𝕋 𝐀 𝑥 𝑥

𝕋 {\bf A}(x),x\in{\mathbb{T}} x = ∅ 𝑥 x=\varnothing 𝐀 ( ∅ ) 𝐀 {\bf A}(\varnothing) ( A 1 , … , A ν ) subscript 𝐴 1 … subscript 𝐴 𝜈 (A_{1},...,A_{\nu}) ν ≡ ν ∅ 𝜈 subscript 𝜈 \nu\equiv\nu_{\varnothing} ∅ \varnothing 𝐏 𝐏 {\bf P} ω 𝜔 \omega ℙ ( ⋅ ) := ∫ P ω ( ⋅ ) 𝐏 ( d ω ) assign ℙ ⋅ subscript 𝑃 𝜔 ⋅ 𝐏 𝑑 𝜔 {\mathbb{P}}(\cdot):=\int P_{\omega}(\cdot){\bf P}(d\omega) P ω subscript 𝑃 𝜔 P_{\omega} ℙ ℙ {\mathbb{P}}

Define

ψ ( t ) := log 𝐄 ( ∑ i = 1 ν A i t ) ∈ ( − ∞ , ∞ ] , ∀ t ∈ ℝ . formulae-sequence assign 𝜓 𝑡 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 𝑡 for-all 𝑡 ℝ \psi(t):=\log{\bf E}\Big{(}\sum_{i=1}^{\nu}\,A_{i}^{t}\Big{)}\in(-\infty,\infty],\qquad\forall t\in{\mathbb{R}}.

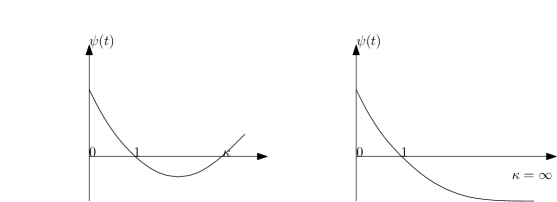

In particular, ψ ( 0 ) = log 𝐄 ( ν ) > 0 𝜓 0 𝐄 𝜈 0 \psi(0)=\log{\bf E}(\nu)>0 𝕋 𝕋 {\mathbb{T}}

sup { t > 0 : ψ ( t ) < ∞ } > 1 . supremum conditional-set 𝑡 0 𝜓 𝑡 1 \sup\{t>0:\psi(t)<\infty\}>1.

We shall consider the case when ( X n ) subscript 𝑋 𝑛 (X_{n}) [18 ] gave a precise recurrence/transience criterion for randomly biased walks on an arbitrary infinite tree. Their results, together with Menshikov and Petritis [21 ] and Faraud [10 ] , imply that ( X n ) subscript 𝑋 𝑛 (X_{n}) inf 0 ≤ t ≤ 1 ψ ( t ) = 0 subscript infimum 0 𝑡 1 𝜓 𝑡 0 \inf_{0\leq t\leq 1}\psi(t)=0 ψ ′ ( 1 ) ≤ 0 superscript 𝜓 ′ 1 0 \psi^{\prime}(1)\leq 0 ψ ′ ( 1 ) = 0 superscript 𝜓 ′ 1 0 \psi^{\prime}(1)=0 ( X n ) subscript 𝑋 𝑛 (X_{n}) | X n | subscript 𝑋 𝑛 |X_{n}| [11 ] for the maximal displacement of X 𝑋 X [16 ] for the localization of X n subscript 𝑋 𝑛 X_{n} ψ ′ ( 1 ) < 0 superscript 𝜓 ′ 1 0 \psi^{\prime}(1)<0 ( X n ) subscript 𝑋 𝑛 (X_{n}) 1.3 [15 ] ). We assume throughout this paper

(1.1) inf 0 ≤ t ≤ 1 ψ ( t ) = 0 and ψ ′ ( 1 ) < 0 . formulae-sequence subscript infimum 0 𝑡 1 𝜓 𝑡 0 and

superscript 𝜓 ′ 1 0 \inf_{0\leq t\leq 1}\psi(t)=0\qquad\hbox{and}\qquad\psi^{\prime}(1)<0.

Let us introduce a parameter

κ := inf { t > 1 : ψ ( t ) = 0 } ∈ ( 1 , ∞ ] , assign 𝜅 infimum conditional-set 𝑡 1 𝜓 𝑡 0 1 \kappa:=\inf\{t>1:\psi(t)=0\}\,\in(1,\infty],

with inf ∅ := ∞ assign infimum \inf\emptyset:=\infty

(1.2) { 𝐄 ( ∑ i = 1 ν A i ) κ + 𝐄 ( ∑ i = 1 ν A i κ log + A i ) < ∞ , if 1 < κ ≤ 2 , 𝐄 ( ∑ i = 1 ν A i ) 2 < ∞ , if κ ∈ ( 2 , ∞ ] , cases 𝐄 superscript superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 𝜅 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 𝜅 subscript subscript 𝐴 𝑖 if 1 < κ ≤ 2 𝐄 superscript superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 2 if κ ∈ ( 2 , ∞ ] \begin{cases}{\bf E}\Big{(}\sum_{i=1}^{\nu}\,A_{i}\Big{)}^{\kappa}+{\bf E}\Big{(}\sum_{i=1}^{\nu}A_{i}^{\kappa}\log_{+}A_{i}\Big{)}<\infty,\qquad&\hbox{\rm if $1<\kappa\leq 2$}\,,\\

{\bf E}\Big{(}\sum_{i=1}^{\nu}\,A_{i}\Big{)}^{2}<\infty,\qquad&\hbox{\rm if $\kappa\in(2,\infty]$}\,,\end{cases}

with log + x := max ( 0 , log x ) assign subscript 𝑥 0 𝑥 \log_{+}x:=\max(0,\log x) x > 0 𝑥 0 x>0

Figure 1: Case inf 0 ≤ t ≤ 1 ψ ( t ) = 0 subscript infimum 0 𝑡 1 𝜓 𝑡 0 \inf_{0\leq t\leq 1}\psi(t)=0 ψ ′ ( 1 ) < 0 superscript 𝜓 ′ 1 0 \psi^{\prime}(1)<0 κ ∈ ( 1 , ∞ ) 𝜅 1 \kappa\in(1,\infty) κ = ∞ 𝜅 \kappa=\infty

It was shown in [15 ] that if 𝕋 𝕋 {\mathbb{T}} ν 𝜈 \nu

(1.3) lim n → ∞ 1 log n log max 0 ≤ i ≤ n | X i | = 1 − max ( 1 2 , 1 κ ) , ℙ -a.s. . subscript → 𝑛 1 𝑛 subscript 0 𝑖 𝑛 subscript 𝑋 𝑖 1 1 2 1 𝜅 ℙ -a.s.

\lim_{n\to\infty}\frac{1}{\log n}\log\max_{0\leq i\leq n}|X_{i}|=1-\max({1\over 2},{1\over\kappa}),\qquad\hbox{${\mathbb{P}}$-a.s.}.

When κ 𝜅 \kappa κ ∈ ( 5 , ∞ ] 𝜅 5 \kappa\in(5,\infty] [10 ] proved an invariance principle for the biased walk X 𝑋 X [25 ] ; some recent developments cover the whole region κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] [4 ] for the convergence to Brownian tree).

The biased walk on a Galton-Watson tree has also attracted many attentions from other directions: In the transient case, Aïdékon [1 , 2 ] dealt with a leafless Galton-Watson tree, whereas Hammond [14 ] established stable limit laws for the walk on a supercritical Galton-Watson tree with leaves, which can be considered as a counterpart of Ben Arous, Gantert, Fribergh and Hammond [8 ] . When the tree is sub-critical, Ben Arous and Hammond [9 ] obtained power laws for the tails of E ω ( T ∅ + ) subscript 𝐸 𝜔 subscript superscript 𝑇 E_{\omega}(T^{+}_{\varnothing}) T ∅ + subscript superscript 𝑇 T^{+}_{\varnothing} T ∅ + subscript superscript 𝑇 T^{+}_{\varnothing} ∅ \varnothing

(1.4) T ∅ + := inf { n ≥ 1 : X n = ∅ } . assign subscript superscript 𝑇 infimum conditional-set 𝑛 1 subscript 𝑋 𝑛 T^{+}_{\varnothing}:=\inf\{n\geq 1:X_{n}=\varnothing\}.

In the above-mentioned works [14 , 8 , 9 ] , the authors explored the link between the biased walk ( X n ) subscript 𝑋 𝑛 (X_{n}) trap models (cf. Ben Arous and Cerny [7 ] ) to get various scaling limits, and an important step is the estimate on the return time to the trap entrance in their models.

We investigate here the return time T ∅ + subscript superscript 𝑇 T^{+}_{\varnothing} ( X n ) subscript 𝑋 𝑛 (X_{n}) κ 𝜅 \kappa ( M n ) subscript 𝑀 𝑛 (M_{n})

(1.5) M n := ∑ | x | = n ∏ ∅ < y ≤ x A ( y ) , n ≥ 1 , formulae-sequence assign subscript 𝑀 𝑛 subscript 𝑥 𝑛 subscript product 𝑦 𝑥 𝐴 𝑦 𝑛 1 M_{n}:=\sum_{|x|=n}\prod_{\varnothing<y\leq x}A(y),\qquad n\geq 1,

where here and in the sequel, | x | 𝑥 |x| x 𝑥 x 𝕋 𝕋 {\mathbb{T}} y < x 𝑦 𝑥 y<x y 𝑦 y x 𝑥 x y ≤ x 𝑦 𝑥 y\leq x y < x 𝑦 𝑥 y<x y = x 𝑦 𝑥 y=x ψ ( 1 ) = 0 𝜓 1 0 \psi(1)=0 ( M n ) subscript 𝑀 𝑛 (M_{n}) [28 ] further properties on ( M n ) subscript 𝑀 𝑛 (M_{n})

𝐏 ∗ ( ∙ ) := 𝐏 ( ∙ | 𝕋 = ∞ ) , {\bf P}^{*}(\bullet):={\bf P}\Big{(}\bullet\,|\,{\mathbb{T}}=\infty\Big{)},

where { 𝕋 = ∞ } 𝕋 \{{\mathbb{T}}=\infty\} M ∞ := lim n → ∞ M n assign subscript 𝑀 subscript → 𝑛 subscript 𝑀 𝑛 M_{\infty}:=\lim_{n\to\infty}M_{n} ( M n ) subscript 𝑀 𝑛 (M_{n}) 1.1 1.2 1.2 M ∞ subscript 𝑀 M_{\infty} 𝐏 ∗ superscript 𝐏 {\bf P}^{*} M ∞ > 0 subscript 𝑀 0 M_{\infty}>0 [17 ] Theorems 2.0 and 2.2, when κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2]

(1.6) 𝐏 ( M ∞ > x ) ≍ x − κ , x → ∞ , formulae-sequence asymptotically-equals 𝐏 subscript 𝑀 𝑥 superscript 𝑥 𝜅 → 𝑥 {\bf P}\Big{(}M_{\infty}>x\Big{)}\,\asymp\,x^{-\kappa},\qquad x\to\infty,

where here and in the sequel, we denote by f ( x ) ≍ g ( x ) asymptotically-equals 𝑓 𝑥 𝑔 𝑥 f(x)\asymp g(x) f ( x ) ∼ g ( x ) similar-to 𝑓 𝑥 𝑔 𝑥 f(x)\sim g(x) x → x 0 → 𝑥 subscript 𝑥 0 x\to x_{0} 0 < lim inf x → x 0 f ( x ) / g ( x ) ≤ lim sup x → x 0 f ( x ) / g ( x ) < ∞ 0 subscript limit-infimum → 𝑥 subscript 𝑥 0 𝑓 𝑥 𝑔 𝑥 subscript limit-supremum → 𝑥 subscript 𝑥 0 𝑓 𝑥 𝑔 𝑥 0<\liminf_{x\to x_{0}}f(x)/g(x)\leq\limsup_{x\to x_{0}}f(x)/g(x)<\infty lim x → x 0 f ( x ) / g ( x ) = 1 subscript → 𝑥 subscript 𝑥 0 𝑓 𝑥 𝑔 𝑥 1 \lim_{x\to x_{0}}f(x)/g(x)=1 1.6 κ ∈ ( 1 , ∞ ) 𝜅 1 \kappa\in(1,\infty) κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2]

The main estimate on the return time reads as follows.

Theorem 1.1

Assume (1.1 1.2 𝐏 ∗ ( d ω ) superscript 𝐏 𝑑 𝜔 {\bf P}^{*}(d\omega)

(i) if 1 < κ < 2 1 𝜅 2 1<\kappa<2

P ω ( T ∅ + > n ) ≍ n − 1 / κ ; asymptotically-equals subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 superscript 𝑛 1 𝜅 P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}\,\asymp\,n^{-1/\kappa};

(ii) if κ = 2 𝜅 2 \kappa=2

P ω ( T ∅ + > n ) ≍ ( n log n ) − 1 / 2 ; asymptotically-equals subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 superscript 𝑛 𝑛 1 2 P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}\,\asymp\,(n\log n)^{-1/2};

(iii) if 2 < κ ≤ ∞ 2 𝜅 2<\kappa\leq\infty

1 ω ( ∅ , ∅ ← ) M ∞ P ω ( T ∅ + > n ) ∼ c 1 n − 1 / 2 , similar-to 1 𝜔 superscript ← subscript 𝑀 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 subscript 𝑐 1 superscript 𝑛 1 2 \frac{1}{\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})\,M_{\infty}}\,P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}\sim c_{1}\,n^{-1/2},

with

c 1 := ( 2 π 1 − 𝐄 ( ∑ i = 1 ν A i 2 ) 𝐄 ( ∑ 1 ≤ i ≠ j ≤ ν A i A j ) ) 1 / 2 , assign subscript 𝑐 1 superscript 2 𝜋 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 2 𝐄 subscript 1 𝑖 𝑗 𝜈 subscript 𝐴 𝑖 subscript 𝐴 𝑗 1 2 c_{1}:=\Big{(}\frac{2}{\pi}\,\frac{1-{\bf E}(\sum_{i=1}^{\nu}A_{i}^{2})}{{\bf E}(\sum_{1\leq i\not=j\leq\nu}A_{i}A_{j})}\Big{)}^{1/2},

where 𝔹 𝔹 {\mathbb{B}} denotes the Beta function.

As a consequence, we get the asymptotic behaviors of the local times process:

L n x := ∑ i = 1 n 1 ( X i = x ) , n ≥ 1 , x ∈ 𝕋 . formulae-sequence assign superscript subscript 𝐿 𝑛 𝑥 superscript subscript 𝑖 1 𝑛 subscript 1 subscript 𝑋 𝑖 𝑥 formulae-sequence 𝑛 1 𝑥 𝕋 L_{n}^{x}:=\sum_{i=1}^{n}1_{(X_{i}=x)},\qquad n\geq 1,x\in{\mathbb{T}}.

We shall restrict our attentions to the local times at the root. It was implicitly contained in [15 , 6 ] that for any κ ∈ ( 1 , ∞ ] 𝜅 1 \kappa\in(1,\infty] ℙ ℙ {\mathbb{P}} { 𝕋 = ∞ } 𝕋 \{{\mathbb{T}}=\infty\}

L n ∅ = n max ( 1 / κ , 1 / 2 ) + o ( 1 ) . superscript subscript 𝐿 𝑛 superscript 𝑛 1 𝜅 1 2 𝑜 1 L_{n}^{\varnothing}=n^{\max(1/\kappa,1/2)+o(1)}.

Based on Theorem 1.1 L n ∅ superscript subscript 𝐿 𝑛 L_{n}^{\varnothing}

Corollary 1.2

Under the same assumptions as in Theorem 1.1 𝐏 ∗ ( d ω ) superscript 𝐏 𝑑 𝜔 {\bf P}^{*}(d\omega) P ω subscript 𝑃 𝜔 P_{\omega} n → ∞ → 𝑛 n\to\infty

(i) if 1 < κ < 2 1 𝜅 2 1<\kappa<2 L n ∅ n 1 / κ superscript subscript 𝐿 𝑛 superscript 𝑛 1 𝜅 \frac{L_{n}^{\varnothing}}{n^{1/\kappa}} ( 0 , ∞ ) 0 (0,\infty)

(ii) if κ = 2 𝜅 2 \kappa=2 L n ∅ n log n superscript subscript 𝐿 𝑛 𝑛 𝑛 \frac{L_{n}^{\varnothing}}{\sqrt{n\log n}} ( 0 , ∞ ) 0 (0,\infty)

(iii) if 2 < κ ≤ ∞ 2 𝜅 2<\kappa\leq\infty

L n ∅ n ⟶ (law) 1 ω ( ∅ , ∅ ← ) M ∞ 2 1 / 2 c 1 π 1 / 2 | 𝒩 | , superscript ⟶ (law) superscript subscript 𝐿 𝑛 𝑛 1 𝜔 superscript ← subscript 𝑀 superscript 2 1 2 subscript 𝑐 1 superscript 𝜋 1 2 𝒩 \frac{L_{n}^{\varnothing}}{\sqrt{n}}\,{\buildrel\mbox{\small\rm(law)}\over{\longrightarrow}}\,\frac{1}{\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})M_{\infty}}\,\frac{2^{1/2}}{c_{1}\,\pi^{1/2}}\,|{\cal N}|,

where 𝒩 𝒩 {\cal N} denotes a standard gaussian random variable, centered and with variance 1 1 1 .

By the classical fluctuation theory on the random walk in the domain of attraction, it is straightforward to deduce from Theorem 1.1 L n ∅ superscript subscript 𝐿 𝑛 L_{n}^{\varnothing}

Corollary 1.3

Under the same assumptions as in Theorem 1.1 κ ∈ ( 1 , ∞ ] 𝜅 1 \kappa\in(1,\infty] 𝐏 ∗ ( d ω ) superscript 𝐏 𝑑 𝜔 {\bf P}^{*}(d\omega) P ω subscript 𝑃 𝜔 P_{\omega}

lim sup n → ∞ L n ∅ f κ ( n ) ∈ ( 0 , ∞ ) , subscript limit-supremum → 𝑛 superscript subscript 𝐿 𝑛 subscript 𝑓 𝜅 𝑛 0 \limsup_{n\to\infty}\frac{L_{n}^{\varnothing}}{f_{\kappa}(n)}\in(0,\infty),

where

f κ ( n ) := { n 1 / κ ( log log n ) 1 − 1 / κ , if 1 < κ < 2 , n 1 / 2 ( log n ) 1 / 2 ( log log n ) 1 / 2 , if κ = 2 , n 1 / 2 ( log log n ) 1 / 2 , if κ ∈ ( 2 , ∞ ] . assign subscript 𝑓 𝜅 𝑛 cases superscript 𝑛 1 𝜅 superscript 𝑛 1 1 𝜅 if 1 < κ < 2 superscript 𝑛 1 2 superscript 𝑛 1 2 superscript 𝑛 1 2 if κ = 2 superscript 𝑛 1 2 superscript 𝑛 1 2 if κ ∈ ( 2 , ∞ ] f_{\kappa}(n):=\begin{cases}n^{1/\kappa}(\log\log n)^{1-1/\kappa},\qquad&\hbox{\rm if $1<\kappa<2$}\,,\\

n^{1/2}(\log n)^{1/2}(\log\log n)^{1/2},\qquad&\hbox{\rm if $\kappa=2$}\,,\\

n^{1/2}(\log\log n)^{1/2},\qquad&\hbox{\rm if $\kappa\in(2,\infty]$}\,.\end{cases}

Combining the estimates on the local times and the reversibility of the biased walk, we obtain the following estimates on the local probability.

Corollary 1.4

Under the same assumptions as in Theorem 1.1 𝐏 ∗ ( d ω ) superscript 𝐏 𝑑 𝜔 {\bf P}^{*}(d\omega) n → ∞ → 𝑛 n\to\infty

(i) if 1 < κ < 2 1 𝜅 2 1<\kappa<2

P ω ( X n = ∅ ) ≍ n − 1 + 1 / κ ; asymptotically-equals subscript 𝑃 𝜔 subscript 𝑋 𝑛 superscript 𝑛 1 1 𝜅 P_{\omega}\Big{(}X_{n}=\varnothing\Big{)}\,\asymp\,n^{-1+1/\kappa};

(ii) if κ = 2 𝜅 2 \kappa=2

P ω ( X n = ∅ ) ≍ n − 1 / 2 ( log n ) 1 / 2 ; asymptotically-equals subscript 𝑃 𝜔 subscript 𝑋 𝑛 superscript 𝑛 1 2 superscript 𝑛 1 2 P_{\omega}\Big{(}X_{n}=\varnothing\Big{)}\,\asymp\,n^{-1/2}\,(\log n)^{1/2};

(iii) if 2 < κ ≤ ∞ 2 𝜅 2<\kappa\leq\infty

P ω ( X n = ∅ ) ∼ 1 ω ( ∅ , ∅ ← ) M ∞ 2 π c 1 n − 1 / 2 . similar-to subscript 𝑃 𝜔 subscript 𝑋 𝑛 1 𝜔 superscript ← subscript 𝑀 2 𝜋 subscript 𝑐 1 superscript 𝑛 1 2 P_{\omega}\Big{(}X_{n}=\varnothing\Big{)}\sim\frac{1}{\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})M_{\infty}}\,\frac{2}{\pi c_{1}}\,n^{-1/2}.

2 Outline of the proof

For any x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}} P x , ω subscript 𝑃 𝑥 𝜔

P_{x,\omega} X 𝑋 X X 0 := x assign subscript 𝑋 0 𝑥 X_{0}:=x E x , ω subscript 𝐸 𝑥 𝜔

E_{x,\omega} P x , ω subscript 𝑃 𝑥 𝜔

P_{x,\omega} P ∅ , ω ≡ P ω subscript 𝑃 𝜔

subscript 𝑃 𝜔 P_{\varnothing,\omega}\equiv P_{\omega} E ∅ , ω ≡ E ω subscript 𝐸 𝜔

subscript 𝐸 𝜔 E_{\varnothing,\omega}\equiv E_{\omega}

T x := inf { n ≥ 0 : X n = x } , x ∈ 𝕋 , formulae-sequence assign subscript 𝑇 𝑥 infimum conditional-set 𝑛 0 subscript 𝑋 𝑛 𝑥 𝑥 𝕋 T_{x}:=\inf\{n\geq 0:X_{n}=x\},\qquad x\in{\mathbb{T}},

be the first hitting time of x 𝑥 x n > 2 𝑛 2 n>2

(2.1) P ω ( T ∅ + > n ) subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 \displaystyle P_{\omega}\Big{(}T^{+}_{\varnothing}>n\Big{)} = \displaystyle= ∑ | u | = 1 ω ( ∅ , u ) P u , ω ( T ∅ > n − 1 ) subscript 𝑢 1 𝜔 𝑢 subscript 𝑃 𝑢 𝜔

subscript 𝑇 𝑛 1 \displaystyle\sum_{|u|=1}\omega(\varnothing,u)P_{u,\omega}\Big{(}T_{\varnothing}>n-1\Big{)}

= \displaystyle= ω ( ∅ , ∅ ← ) ∑ | u | = 1 A ( u ) P u , ω ( T ∅ > n − 1 ) . 𝜔 superscript ← subscript 𝑢 1 𝐴 𝑢 subscript 𝑃 𝑢 𝜔

subscript 𝑇 𝑛 1 \displaystyle\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})\sum_{|u|=1}A(u)P_{u,\omega}\Big{(}T_{\varnothing}>n-1\Big{)}.

By Tauberian theorems, the asymptotic behaviors of P u , ω ( T ∅ > n − 1 ) subscript 𝑃 𝑢 𝜔

subscript 𝑇 𝑛 1 P_{u,\omega}(T_{\varnothing}>n-1) E u , ω ( e − λ T ∅ ) subscript 𝐸 𝑢 𝜔

superscript e 𝜆 subscript 𝑇 E_{u,\omega}\big{(}\mathrm{e}^{-\lambda T_{\varnothing}}\big{)} λ → 0 → 𝜆 0 \lambda\to 0 λ > 0 𝜆 0 \lambda>0 x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}}

(2.2) β λ ( x ) : = 1 − E x , ω ( e − λ ( 1 + T x ← ) ) , x ∈ 𝕋 , \beta_{\lambda}(x):=1-E_{x,\omega}\Big{(}\mathrm{e}^{-\lambda(1+T_{{\buildrel\leftarrow\over{x}}})}\Big{)},\qquad x\in{\mathbb{T}},

where as before, x ← superscript 𝑥 ← {\buildrel\leftarrow\over{x}} x 𝑥 x β λ ( ⋅ ) subscript 𝛽 𝜆 ⋅ \beta_{\lambda}(\cdot)

Fact 2.1

For any x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}} λ > 0 𝜆 0 \lambda>0

β λ ( x ) = ( 1 − e − 2 λ ) + ∑ i = 1 ν x A ( x ( i ) ) β λ ( x ( i ) ) 1 + ∑ i = 1 ν x A ( x ( i ) ) β λ ( x ( i ) ) . subscript 𝛽 𝜆 𝑥 1 superscript e 2 𝜆 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 subscript 𝛽 𝜆 superscript 𝑥 𝑖 1 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 subscript 𝛽 𝜆 superscript 𝑥 𝑖 \beta_{\lambda}(x)=\frac{(1-\mathrm{e}^{-2\lambda})+\sum_{i=1}^{\nu_{x}}A(x^{(i)})\beta_{\lambda}(x^{(i)})}{1+\sum_{i=1}^{\nu_{x}}A(x^{(i)})\beta_{\lambda}(x^{(i)})}.

We mention that conditioned on ( ( A ( x ( i ) ) ) 1 ≤ i ≤ ν x , ν x ) subscript 𝐴 superscript 𝑥 𝑖 1 𝑖 subscript 𝜈 𝑥 subscript 𝜈 𝑥 \big{(}(A(x^{(i)}))_{1\leq i\leq\nu_{x}},\nu_{x}\big{)} ( β λ ( x ( i ) ) , 1 ≤ i ≤ ν x ) subscript 𝛽 𝜆 superscript 𝑥 𝑖 1

𝑖 subscript 𝜈 𝑥 (\beta_{\lambda}(x^{(i)}),1\leq i\leq\nu_{x}) β λ ( ∅ ) subscript 𝛽 𝜆 \beta_{\lambda}(\varnothing)

Proof of Fact 2.1 This fact is an easy application of Markov property. We give the proof for the sake of completeness. For use later, we define for any n ≥ 1 , λ > 0 formulae-sequence 𝑛 1 𝜆 0 n\geq 1,\lambda>0 x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}} | x | ≤ n 𝑥 𝑛 |x|\leq n

(2.3) β n , λ ( x ) := 1 − E x , ω ( e − λ ( 1 + T x ← ) 1 ( τ n > T x ← ) ) , assign subscript 𝛽 𝑛 𝜆

𝑥 1 subscript 𝐸 𝑥 𝜔

superscript e 𝜆 1 subscript 𝑇 superscript 𝑥 ← subscript 1 subscript 𝜏 𝑛 subscript 𝑇 superscript 𝑥 ← \beta_{n,\lambda}(x):=1-E_{x,\omega}\Big{(}\mathrm{e}^{-\lambda(1+T_{{\buildrel\leftarrow\over{x}}})}1_{(\tau_{n}>T_{{\buildrel\leftarrow\over{x}}})}\Big{)},

where

τ n := inf { k ≥ 0 : | X k | = n } , assign subscript 𝜏 𝑛 infimum conditional-set 𝑘 0 subscript 𝑋 𝑘 𝑛 \tau_{n}:=\inf\{k\geq 0:|X_{k}|=n\},

denotes the first time when X 𝑋 X n 𝑛 n 𝕋 𝕋 {\mathbb{T}}

Clearly β n , λ ( x ) = 1 subscript 𝛽 𝑛 𝜆

𝑥 1 \beta_{n,\lambda}(x)=1 | x | = n 𝑥 𝑛 |x|=n | x | < n 𝑥 𝑛 |x|<n

β n , λ ( x ) subscript 𝛽 𝑛 𝜆

𝑥 \displaystyle\beta_{n,\lambda}(x) = \displaystyle= 1 − ( ∑ i = 1 ν x ω ( x , x ( i ) ) e − λ E ω , x ( i ) e − λ ( 1 + T x ← ) 1 ( T x ← < τ n ) + ω ( x , x ← ) e − 2 λ ) 1 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝜔 𝑥 superscript 𝑥 𝑖 superscript e 𝜆 subscript 𝐸 𝜔 superscript 𝑥 𝑖

superscript e 𝜆 1 subscript 𝑇 superscript 𝑥 ← subscript 1 subscript 𝑇 superscript 𝑥 ← subscript 𝜏 𝑛 𝜔 𝑥 superscript 𝑥 ← superscript e 2 𝜆 \displaystyle 1-\Big{(}\sum_{i=1}^{\nu_{x}}\omega(x,x^{(i)})\mathrm{e}^{-\lambda}\,E_{\omega,x^{(i)}}\mathrm{e}^{-\lambda(1+T_{{\buildrel\leftarrow\over{x}}})}1_{(T_{{\buildrel\leftarrow\over{x}}}<\tau_{n})}+\omega(x,{\buildrel\leftarrow\over{x}})\mathrm{e}^{-2\lambda}\Big{)}

= \displaystyle= 1 − ( ∑ i = 1 ν x ω ( x , x ( i ) ) ( 1 − β n , λ ( x ( i ) ) ( 1 − β n , λ ( x ) ) + ω ( x , x ← ) e − 2 λ ) . \displaystyle 1-\Big{(}\sum_{i=1}^{\nu_{x}}\omega(x,x^{(i)})(1-\beta_{n,\lambda}(x^{(i)})(1-\beta_{n,\lambda}(x))+\omega(x,{\buildrel\leftarrow\over{x}})\mathrm{e}^{-2\lambda}\Big{)}.

After simplifications, we get that

(2.4) β n , λ ( x ) = ( 1 − e − 2 λ ) + ∑ i = 1 ν x A ( x ( i ) ) β n , λ ( x ( i ) ) 1 + ∑ i = 1 ν x A ( x ( i ) ) β n , λ ( x ( i ) ) , | x | < n . formulae-sequence subscript 𝛽 𝑛 𝜆

𝑥 1 superscript e 2 𝜆 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 subscript 𝛽 𝑛 𝜆

superscript 𝑥 𝑖 1 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 subscript 𝛽 𝑛 𝜆

superscript 𝑥 𝑖 𝑥 𝑛 \beta_{n,\lambda}(x)=\frac{(1-\mathrm{e}^{-2\lambda})+\sum_{i=1}^{\nu_{x}}A(x^{(i)})\beta_{n,\lambda}(x^{(i)})}{1+\sum_{i=1}^{\nu_{x}}A(x^{(i)})\beta_{n,\lambda}(x^{(i)})},\qquad|x|<n.

Letting n → ∞ → 𝑛 n\to\infty β λ ( x ) = lim n → ∞ β n , λ ( x ) subscript 𝛽 𝜆 𝑥 subscript → 𝑛 subscript 𝛽 𝑛 𝜆

𝑥 \beta_{\lambda}(x)=\lim_{n\to\infty}\beta_{n,\lambda}(x) 2.1 □ □ \Box

For brevity, we make a change of variable ε = 1 − e − 2 λ , 𝜀 1 superscript e 2 𝜆 \varepsilon=1-\mathrm{e}^{-2\lambda},

(2.5) B ε ( x ) := ∑ i = 1 ν x A ( x ( i ) ) β 1 2 log 1 / ( 1 − ε ) ( x ( i ) ) , x ∈ 𝕋 , 0 < ε < 1 , formulae-sequence assign subscript 𝐵 𝜀 𝑥 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 subscript 𝛽 1 2 1 1 𝜀 superscript 𝑥 𝑖 formulae-sequence 𝑥 𝕋 0 𝜀 1 B_{\varepsilon}(x):=\sum_{i=1}^{\nu_{x}}A(x^{(i)})\beta_{\frac{1}{2}\log 1/(1-\varepsilon)}(x^{(i)}),\qquad x\in{\mathbb{T}},\qquad 0<\varepsilon<1,

then

(2.6) B ε ( x ) = ∑ i = 1 ν x A ( x ( i ) ) ε + B ε ( x ( i ) ) 1 + B ε ( x ( i ) ) , subscript 𝐵 𝜀 𝑥 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 𝜀 subscript 𝐵 𝜀 superscript 𝑥 𝑖 1 subscript 𝐵 𝜀 superscript 𝑥 𝑖 B_{\varepsilon}(x)=\sum_{i=1}^{\nu_{x}}\,A(x^{(i)})\,\frac{\varepsilon+B_{\varepsilon}(x^{(i)})}{1+B_{\varepsilon}(x^{(i)})},

where as for β λ ( x ) subscript 𝛽 𝜆 𝑥 \beta_{\lambda}(x) ( ( A ( x ( i ) ) ) 1 ≤ i ≤ ν x , ν x ) subscript 𝐴 superscript 𝑥 𝑖 1 𝑖 subscript 𝜈 𝑥 subscript 𝜈 𝑥 \big{(}(A(x^{(i)}))_{1\leq i\leq\nu_{x}},\nu_{x}\big{)} ( B ε ( x ( i ) ) , 1 ≤ i ≤ ν x ) subscript 𝐵 𝜀 superscript 𝑥 𝑖 1

𝑖 subscript 𝜈 𝑥 (B_{\varepsilon}(x^{(i)}),1\leq i\leq\nu_{x}) B ε ( ∅ ) subscript 𝐵 𝜀 B_{\varepsilon}(\varnothing) 2.2

(2.7) B ε ( ∅ ) = ∑ | u | = 1 A ( u ) ( 1 − E u , ω ( ( 1 − ε ) 1 + T ∅ 2 ) ) . subscript 𝐵 𝜀 subscript 𝑢 1 𝐴 𝑢 1 subscript 𝐸 𝑢 𝜔

superscript 1 𝜀 1 subscript 𝑇 2 B_{\varepsilon}(\varnothing)=\sum_{|u|=1}A(u)\,\Big{(}1-E_{u,\omega}\big{(}(1-\varepsilon)^{\frac{1+T_{\varnothing}}{2}}\big{)}\Big{)}.

The main estimate in the proof of Theorem 1.1

Proposition 2.2

Assume (1.1 1.2 ε → 0 → 𝜀 0 \varepsilon\to 0 𝐏 𝐏 {\bf P} L p ( 𝐏 ) superscript 𝐿 𝑝 𝐏 L^{p}({\bf P}) 1 < p < min ( κ , 2 ) 1 𝑝 𝜅 2 1<p<\min(\kappa,2)

B ε ( ∅ ) 𝐄 ( B ε ( ∅ ) ) → M ∞ . → subscript 𝐵 𝜀 𝐄 subscript 𝐵 𝜀 subscript 𝑀 \frac{B_{\varepsilon}(\varnothing)}{{\bf E}(B_{\varepsilon}(\varnothing))}\,\to\,M_{\infty}.

Moreover, as ε → 0 → 𝜀 0 \varepsilon\to 0 ,

(i) if 1 < κ < 2 1 𝜅 2 1<\kappa<2

𝐄 ( B ε ( ∅ ) ) ≍ ε 1 / κ ; asymptotically-equals 𝐄 subscript 𝐵 𝜀 superscript 𝜀 1 𝜅 {\bf E}(B_{\varepsilon}(\varnothing))\,\asymp\,\varepsilon^{1/\kappa};

(ii) if κ = 2 𝜅 2 \kappa=2

𝐄 ( B ε ( ∅ ) ) ≍ ( ε log 1 ε ) 1 / 2 ; asymptotically-equals 𝐄 subscript 𝐵 𝜀 superscript 𝜀 1 𝜀 1 2 {\bf E}(B_{\varepsilon}(\varnothing))\,\asymp\,\Big{(}\frac{\varepsilon}{\log\frac{1}{\varepsilon}}\Big{)}^{1/2};

(iii) if 2 < κ ≤ ∞ 2 𝜅 2<\kappa\leq\infty

𝐄 ( B ε ( ∅ ) ) ∼ c 2 ε 1 / 2 , similar-to 𝐄 subscript 𝐵 𝜀 subscript 𝑐 2 superscript 𝜀 1 2 {\bf E}(B_{\varepsilon}(\varnothing))\,\sim\,c_{2}\,\varepsilon^{1/2},

where c 2 := ( 1 − 𝐄 ( ∑ i = 1 ν A i 2 ) 𝐄 ( ∑ 1 ≤ i ≠ j ≤ ν A i A j ) ) 1 / 2 assign subscript 𝑐 2 superscript 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 2 𝐄 subscript 1 𝑖 𝑗 𝜈 subscript 𝐴 𝑖 subscript 𝐴 𝑗 1 2 c_{2}:=\Big{(}\frac{1-{\bf E}(\sum_{i=1}^{\nu}A_{i}^{2})}{{\bf E}(\sum_{1\leq i\not=j\leq\nu}A_{i}A_{j})}\Big{)}^{1/2} .

Recall that 𝐏 𝐏 {\bf P} { M ∞ > 0 } = { 𝕋 = ∞ } subscript 𝑀 0 𝕋 \{M_{\infty}>0\}=\{{\mathbb{T}}=\infty\} { T = ∞ } c superscript 𝑇 𝑐 \{T=\infty\}^{c} X 𝑋 X B ε ( ∅ ) = O ( ε ) subscript 𝐵 𝜀 𝑂 𝜀 B_{\varepsilon}(\varnothing)=O(\varepsilon) ε → 0 → 𝜀 0 \varepsilon\to 0

Let us give the proofs of Theorem 1.1 1.2 1.3 1.4 2.2

Proof of Theorem 1.1

By (2.2 2.5 λ > 0 𝜆 0 \lambda>0 ε = 1 − e − 2 λ 𝜀 1 superscript e 2 𝜆 \varepsilon=1-\mathrm{e}^{-2\lambda}

B ε ( ∅ ) = ( 1 − e − λ ) ∑ | u | = 1 A ( u ) ∑ k = 0 ∞ e − λ k P u , ω ( T ∅ ≥ k ) . subscript 𝐵 𝜀 1 superscript e 𝜆 subscript 𝑢 1 𝐴 𝑢 superscript subscript 𝑘 0 superscript e 𝜆 𝑘 subscript 𝑃 𝑢 𝜔

subscript 𝑇 𝑘 B_{\varepsilon}(\varnothing)=(1-\mathrm{e}^{-\lambda})\,\sum_{|u|=1}A(u)\sum_{k=0}^{\infty}\,\mathrm{e}^{-\lambda k}\,P_{u,\omega}\big{(}T_{\varnothing}\geq k\big{)}.

In view of (2.1 ∑ | u | = 1 A ( u ) P u , ω ( T ∅ ≥ k ) = P ω ( T ∅ + > k ) / ω ( ∅ , ∅ ← ) subscript 𝑢 1 𝐴 𝑢 subscript 𝑃 𝑢 𝜔

subscript 𝑇 𝑘 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑘 𝜔 superscript ← \sum_{|u|=1}A(u)P_{u,\omega}(T_{\varnothing}\geq k)=P_{\omega}(T^{+}_{\varnothing}>k)/\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})

(2.8) ∑ k = 0 ∞ e − λ k P ω ( T ∅ + > k ) = ω ( ∅ , ∅ ← ) B ε ( ∅ ) 1 − e − λ , superscript subscript 𝑘 0 superscript e 𝜆 𝑘 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑘 𝜔 superscript ← subscript 𝐵 𝜀 1 superscript e 𝜆 \sum_{k=0}^{\infty}\,\mathrm{e}^{-\lambda k}\,P_{\omega}\big{(}T^{+}_{\varnothing}>k\big{)}=\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})\,\frac{B_{\varepsilon}(\varnothing)}{1-\mathrm{e}^{-\lambda}},

with ε = 1 − e − 2 λ 𝜀 1 superscript e 2 𝜆 \varepsilon=1-\mathrm{e}^{-2\lambda}

When 2 < κ ≤ ∞ 2 𝜅 2<\kappa\leq\infty 2.2 𝐏 ∗ ( d ω ) superscript 𝐏 𝑑 𝜔 {\bf P}^{*}(d\omega) B ε ( ∅ ) ∼ c 2 M ∞ ε 1 / 2 similar-to subscript 𝐵 𝜀 subscript 𝑐 2 subscript 𝑀 superscript 𝜀 1 2 B_{\varepsilon}(\varnothing)\sim c_{2}M_{\infty}\varepsilon^{1/2} [12 ] , pp. 447, Theorem 5), yields Theorem 1.1

It remains to deal with the cases κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2] 0 < ε ≤ 1 0 𝜀 1 0<\varepsilon\leq 1

(2.9) r ( ε ) := { ε 1 / κ , if κ ∈ ( 1 , 2 ) , ε / log ( e / ε ) , if κ = 2 . assign 𝑟 𝜀 cases superscript 𝜀 1 𝜅 if κ ∈ ( 1 , 2 ) 𝜀 e 𝜀 if κ = 2 r(\varepsilon):=\begin{cases}\varepsilon^{1/\kappa},\qquad&\mbox{if $\kappa\in(1,2)$},\\

\sqrt{\varepsilon/\log(\mathrm{e}/\varepsilon)},\qquad&\mbox{if $\kappa=2$}.\end{cases}

For any n ≥ 1 𝑛 1 n\geq 1 2.8 ε = 1 − e − 2 λ 𝜀 1 superscript e 2 𝜆 \varepsilon=1-\mathrm{e}^{-2\lambda}

B ε ( ∅ ) ≥ ( 1 − e − λ ) ∑ k = 0 n e − λ k P ω ( T ∅ + > n ) = ( 1 − e − λ ( n + 1 ) ) P ω ( T ∅ + > n ) . subscript 𝐵 𝜀 1 superscript e 𝜆 superscript subscript 𝑘 0 𝑛 superscript e 𝜆 𝑘 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 1 superscript e 𝜆 𝑛 1 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 B_{\varepsilon}(\varnothing)\geq(1-\mathrm{e}^{-\lambda})\,\sum_{k=0}^{n}\,\mathrm{e}^{-\lambda k}\,P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}=(1-\mathrm{e}^{-\lambda(n+1)})\,P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}.

Taking λ = 1 / ( n + 1 ) 𝜆 1 𝑛 1 \lambda=1/(n+1) ε = 1 − e − 2 / ( n + 1 ) 𝜀 1 superscript e 2 𝑛 1 \varepsilon=1-\mathrm{e}^{-2/(n+1)} 2.2

(2.10) P ω ( T ∅ + > n ) ≤ 1 1 − e − 1 B ε ( ∅ ) ≤ c 3 r ( 1 / n ) , ∀ n ≥ 1 , formulae-sequence subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 1 1 superscript e 1 subscript 𝐵 𝜀 subscript 𝑐 3 𝑟 1 𝑛 for-all 𝑛 1 P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}\leq\frac{1}{1-\mathrm{e}^{-1}}\,B_{\varepsilon}(\varnothing)\leq c_{3}\,r(1/n),\qquad\forall\,n\geq 1,

where c 3 ≡ c 3 ( ω ) ∈ ( 0 , ∞ ) subscript 𝑐 3 subscript 𝑐 3 𝜔 0 c_{3}\equiv c_{3}(\omega)\in(0,\infty) ω 𝜔 \omega

To get the lower bound for P ω ( T ∅ + > n ) subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)} 2.10 2.8 n ≥ 1 𝑛 1 n\geq 1

∑ k = 0 ∞ e − λ k P ω ( T ∅ + > k ) superscript subscript 𝑘 0 superscript e 𝜆 𝑘 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑘 \displaystyle\sum_{k=0}^{\infty}\,\mathrm{e}^{-\lambda k}\,P_{\omega}\big{(}T^{+}_{\varnothing}>k\big{)} ≤ \displaystyle\leq 1 + ∑ k = 1 n e − λ k c 3 r ( 1 / k ) + ∑ k = n + 1 ∞ e − λ k P ω ( T ∅ + > n ) 1 superscript subscript 𝑘 1 𝑛 superscript e 𝜆 𝑘 subscript 𝑐 3 𝑟 1 𝑘 superscript subscript 𝑘 𝑛 1 superscript e 𝜆 𝑘 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 \displaystyle 1+\sum_{k=1}^{n}\,\mathrm{e}^{-\lambda k}\,c_{3}\,r(1/k)+\sum_{k=n+1}^{\infty}\,\mathrm{e}^{-\lambda k}\,P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}

≤ \displaystyle\leq 1 + ∑ k = 1 n e − λ k c 3 r ( 1 / k ) + 1 1 − e − λ P ω ( T ∅ + > n ) . 1 superscript subscript 𝑘 1 𝑛 superscript e 𝜆 𝑘 subscript 𝑐 3 𝑟 1 𝑘 1 1 superscript e 𝜆 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 \displaystyle 1+\sum_{k=1}^{n}\,\mathrm{e}^{-\lambda k}\,c_{3}\,r(1/k)+\frac{1}{1-\mathrm{e}^{-\lambda}}P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}.

Take λ = δ / n 𝜆 𝛿 𝑛 \lambda=\delta/n δ > 0 𝛿 0 \delta>0 δ 𝛿 \delta c 4 ( δ ) subscript 𝑐 4 𝛿 c_{4}(\delta) c 4 ( δ ) → 0 → subscript 𝑐 4 𝛿 0 c_{4}(\delta)\to 0 δ → 0 → 𝛿 0 \delta\to 0 n ≥ 1 𝑛 1 n\geq 1 λ = δ / n 𝜆 𝛿 𝑛 \lambda=\delta/n

1 + ∑ k = 1 n e − λ k r ( 1 / k ) ≤ c 4 ( δ ) r ( λ ) / λ . 1 superscript subscript 𝑘 1 𝑛 superscript e 𝜆 𝑘 𝑟 1 𝑘 subscript 𝑐 4 𝛿 𝑟 𝜆 𝜆 1+\sum_{k=1}^{n}\,\mathrm{e}^{-\lambda k}\,r(1/k)\leq c_{4}(\delta)\,r(\lambda)/\lambda.

By (2.8 2.2 𝐏 ∗ ( d ω ) superscript 𝐏 𝑑 𝜔 {\bf P}^{*}(d\omega) c 5 ≡ c 5 ( ω ) ∈ ( 0 , ∞ ) subscript 𝑐 5 subscript 𝑐 5 𝜔 0 c_{5}\equiv c_{5}(\omega)\in(0,\infty) 0 < λ < 1 0 𝜆 1 0<\lambda<1 ∑ k = 0 ∞ e − λ k P ω ( T ∅ + > k ) ≥ c 5 r ( λ ) / λ superscript subscript 𝑘 0 superscript e 𝜆 𝑘 subscript 𝑃 𝜔 subscript superscript 𝑇 𝑘 subscript 𝑐 5 𝑟 𝜆 𝜆 \sum_{k=0}^{\infty}\,\mathrm{e}^{-\lambda k}\,P_{\omega}\big{(}T^{+}_{\varnothing}>k\big{)}\geq c_{5}\,r(\lambda)/\lambda

Choose (and then fix) δ 𝛿 \delta c 4 ( δ ) ≤ 1 2 c 5 / c 3 subscript 𝑐 4 𝛿 1 2 subscript 𝑐 5 subscript 𝑐 3 c_{4}(\delta)\leq\frac{1}{2}\,c_{5}/c_{3} n ≥ 1 𝑛 1 n\geq 1 λ = δ / n 𝜆 𝛿 𝑛 \lambda=\delta/n

(2.11) P ω ( T ∅ + > n ) ≥ 1 2 c 5 r ( λ ) 1 − e − λ λ ≥ c 6 r ( 1 / n ) , subscript 𝑃 𝜔 subscript superscript 𝑇 𝑛 1 2 subscript 𝑐 5 𝑟 𝜆 1 superscript e 𝜆 𝜆 subscript 𝑐 6 𝑟 1 𝑛 P_{\omega}\big{(}T^{+}_{\varnothing}>n\big{)}\geq\frac{1}{2}c_{5}\,r(\lambda)\frac{1-\mathrm{e}^{-\lambda}}{\lambda}\geq c_{6}\,r(1/n),

for some c 6 ≡ c 6 ( ω , δ ) ∈ ( 0 , ∞ ) subscript 𝑐 6 subscript 𝑐 6 𝜔 𝛿 0 c_{6}\equiv c_{6}(\omega,\delta)\in(0,\infty) 2.11 2.10 1.1 □ □ \Box

Proofs of Corollaries 1.2 1.3 Fix a realization of environment ω 𝜔 \omega 2.10 2.11 1.1

Define for k ≥ 1 𝑘 1 k\geq 1

T ∅ ( k ) := inf { n > T ∅ ( k − 1 ) : X n = ∅ } , assign subscript superscript 𝑇 𝑘 infimum conditional-set 𝑛 subscript superscript 𝑇 𝑘 1 subscript 𝑋 𝑛 T^{(k)}_{\varnothing}:=\inf\{n>T^{(k-1)}_{\varnothing}:X_{n}=\varnothing\},

the k 𝑘 k ∅ \varnothing T ∅ ( 0 ) := 0 assign subscript superscript 𝑇 0 0 T^{(0)}_{\varnothing}:=0 n ≥ 1 𝑛 1 n\geq 1 L n ∅ = inf { k ≥ 1 : T ∅ ( k ) ≥ n } superscript subscript 𝐿 𝑛 infimum conditional-set 𝑘 1 subscript superscript 𝑇 𝑘 𝑛 L_{n}^{\varnothing}=\inf\{k\geq 1:T^{(k)}_{\varnothing}\geq n\}

Under P ω subscript 𝑃 𝜔 P_{\omega} T ∅ ( k ) subscript superscript 𝑇 𝑘 T^{(k)}_{\varnothing} k 𝑘 k T ∅ + subscript superscript 𝑇 T^{+}_{\varnothing} 2 < κ ≤ ∞ 2 𝜅 2<\kappa\leq\infty κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2] T ∅ + subscript superscript 𝑇 T^{+}_{\varnothing} max ( 1 / κ , 1 / 2 ) 1 𝜅 1 2 \max(1/\kappa,1/2) η 𝜂 \eta η ^ ^ 𝜂 \widehat{\eta} n ≥ 1 𝑛 1 n\geq 1

P ω ( η > n ) = min ( 1 , c 3 r ( 1 / n ) ) , P ω ( η ^ > n ) = c 6 r ( 1 / n ) , formulae-sequence subscript 𝑃 𝜔 𝜂 𝑛 1 subscript 𝑐 3 𝑟 1 𝑛 subscript 𝑃 𝜔 ^ 𝜂 𝑛 subscript 𝑐 6 𝑟 1 𝑛 P_{\omega}\big{(}\eta>n)=\min(1,c_{3}r(1/n)),\qquad P_{\omega}\big{(}\widehat{\eta}>n)=c_{6}r(1/n),

where r ( ⋅ ) 𝑟 ⋅ r(\cdot) c 3 subscript 𝑐 3 c_{3} c 6 subscript 𝑐 6 c_{6} 2.9 2.10 2.11 2.11 c 6 r ( 1 / n ) ≤ 1 subscript 𝑐 6 𝑟 1 𝑛 1 c_{6}r(1/n)\leq 1 η 𝜂 \eta η ^ ^ 𝜂 \widehat{\eta} max ( 1 / κ , 1 / 2 ) 1 𝜅 1 2 \max(1/\kappa,1/2) 2.10 2.11 η 𝜂 \eta η ^ ^ 𝜂 \widehat{\eta} T ∅ + subscript superscript 𝑇 T^{+}_{\varnothing} P ω subscript 𝑃 𝜔 P_{\omega} η ≥ T ∅ + ≥ η ^ 𝜂 subscript superscript 𝑇 ^ 𝜂 \eta\geq T^{+}_{\varnothing}\geq\widehat{\eta}

Then for the cases κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2] ( Ξ k ) k ≥ 1 subscript subscript Ξ 𝑘 𝑘 1 (\Xi_{k})_{k\geq 1} ( Ξ ^ k ) k ≥ 1 subscript subscript ^ Ξ 𝑘 𝑘 1 (\widehat{\Xi}_{k})_{k\geq 1} k ≥ 1 𝑘 1 k\geq 1 Ξ k subscript Ξ 𝑘 \Xi_{k} Ξ ^ k subscript ^ Ξ 𝑘 \widehat{\Xi}_{k} k 𝑘 k η 𝜂 \eta η ^ ^ 𝜂 \widehat{\eta} P ω subscript 𝑃 𝜔 P_{\omega} Ξ k ≥ T ∅ ( k ) ≥ Ξ ^ k . subscript Ξ 𝑘 subscript superscript 𝑇 𝑘 subscript ^ Ξ 𝑘 \Xi_{k}\geq T^{(k)}_{\varnothing}\geq\widehat{\Xi}_{k}. P ω subscript 𝑃 𝜔 P_{\omega}

Ξ n − 1 ≤ L n ∅ ≤ Ξ ^ n − 1 , ∀ n ≥ 1 , formulae-sequence subscript superscript Ξ 1 𝑛 superscript subscript 𝐿 𝑛 subscript superscript ^ Ξ 1 𝑛 for-all 𝑛 1 \Xi^{-1}_{n}\leq L_{n}^{\varnothing}\leq\widehat{\Xi}^{-1}_{n},\qquad\forall n\geq 1,

with Ξ n − 1 := inf { k ≥ 1 : η k ≥ n } assign subscript superscript Ξ 1 𝑛 infimum conditional-set 𝑘 1 subscript 𝜂 𝑘 𝑛 \Xi^{-1}_{n}:=\inf\{k\geq 1:\eta_{k}\geq n\} Ξ ^ n − 1 subscript superscript ^ Ξ 1 𝑛 \widehat{\Xi}^{-1}_{n}

When κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] Ξ k = T ∅ ( k ) subscript Ξ 𝑘 subscript superscript 𝑇 𝑘 \Xi_{k}=T^{(k)}_{\varnothing} Ξ n − 1 = L n ∅ superscript subscript Ξ 𝑛 1 superscript subscript 𝐿 𝑛 \Xi_{n}^{-1}=L_{n}^{\varnothing} k ≥ 1 𝑘 1 k\geq 1 κ ∈ ( 1 , ∞ ] 𝜅 1 \kappa\in(1,\infty] 1.2 1.3 ( Ξ n − 1 ) n ≥ 1 subscript subscript superscript Ξ 1 𝑛 𝑛 1 (\Xi^{-1}_{n})_{n\geq 1} ( L n ∅ ) n ≥ 1 subscript superscript subscript 𝐿 𝑛 𝑛 1 (L_{n}^{\varnothing})_{n\geq 1} 0 < α < 1 0 𝛼 1 0<\alpha<1 ℓ ( n ) ℓ 𝑛 \ell(n)

(2.12) P ω ( Ξ 1 > n ) ∼ 1 Γ ( 1 − α ) n − α ℓ ( n ) . similar-to subscript 𝑃 𝜔 subscript Ξ 1 𝑛 1 Γ 1 𝛼 superscript 𝑛 𝛼 ℓ 𝑛 P_{\omega}(\Xi_{1}>n)\sim\frac{1}{\Gamma(1-\alpha)}\,n^{-\alpha}\ell(n).

By [12 ] (Theorem 2, pp.448), we have that under P ω subscript 𝑃 𝜔 P_{\omega}

Ξ k ( k ℓ ( k 1 / α ) ) 1 / α ⟶ (law) 𝒮 α , superscript ⟶ (law) subscript Ξ 𝑘 superscript 𝑘 ℓ superscript 𝑘 1 𝛼 1 𝛼 subscript 𝒮 𝛼 \frac{\Xi_{k}}{\big{(}k\,\ell(k^{1/\alpha})\big{)}^{1/\alpha}}\,{\buildrel\mbox{\small\rm(law)}\over{\longrightarrow}}\,{\cal S_{\alpha}},

with 𝒮 α subscript 𝒮 𝛼 {\cal S}_{\alpha} α 𝛼 \alpha 𝔼 e − λ 𝒮 α = e − λ α 𝔼 superscript e 𝜆 subscript 𝒮 𝛼 superscript e superscript 𝜆 𝛼 {\mathbb{E}}\mathrm{e}^{-\lambda{\cal S}_{\alpha}}=\mathrm{e}^{-\lambda^{\alpha}} λ > 0 𝜆 0 \lambda>0 𝒮 1 / 2 = (law) 1 2 𝒩 2 superscript (law) subscript 𝒮 1 2 1 2 superscript 𝒩 2 {\cal S}_{1/2}{\buildrel\mbox{\small\rm(law)}\over{=}}\frac{1}{2{\cal N}^{2}}

Applying Fristed and Pruitt ([13 ] , Theorem 5) to the random walk ( Ξ k ) k ≥ 1 subscript subscript Ξ 𝑘 𝑘 1 (\Xi_{k})_{k\geq 1} P ω subscript 𝑃 𝜔 P_{\omega}

lim sup n → ∞ Ξ n − 1 f α ( n ) ∈ ( 0 , ∞ ) , subscript limit-supremum → 𝑛 subscript superscript Ξ 1 𝑛 subscript 𝑓 𝛼 𝑛 0 \limsup_{n\to\infty}\frac{\Xi^{-1}_{n}}{f_{\alpha}(n)}\in(0,\infty),

where f α ( ⋅ ) subscript 𝑓 𝛼 ⋅ f_{\alpha}(\cdot) 1.3 1.3

Now using the fact that P ω ( Ξ n − 1 ≥ k ) = P ω ( Ξ k ≤ n ) subscript 𝑃 𝜔 subscript superscript Ξ 1 𝑛 𝑘 subscript 𝑃 𝜔 subscript Ξ 𝑘 𝑛 P_{\omega}(\Xi^{-1}_{n}\geq k)=P_{\omega}(\Xi_{k}\leq n) k ≥ 1 , n ≥ 1 formulae-sequence 𝑘 1 𝑛 1 k\geq 1,n\geq 1 z > 0 𝑧 0 z>0

P ω ( Ξ n − 1 n α / ℓ ( n ) ≥ z ) → ℙ ( 𝒮 α ≤ z − 1 / α ) . → subscript 𝑃 𝜔 subscript superscript Ξ 1 𝑛 superscript 𝑛 𝛼 ℓ 𝑛 𝑧 ℙ subscript 𝒮 𝛼 superscript 𝑧 1 𝛼 P_{\omega}\Big{(}\frac{\Xi^{-1}_{n}}{n^{\alpha}/\ell(n)}\geq z\Big{)}\to{\mathbb{P}}\Big{(}{\cal S}_{\alpha}\leq z^{-1/\alpha}\Big{)}.

It follows that under P ω subscript 𝑃 𝜔 P_{\omega}

(2.13) n − α ℓ ( n ) Ξ n − 1 ⟶ (law) ( 𝒮 α ) − α , superscript ⟶ (law) superscript 𝑛 𝛼 ℓ 𝑛 subscript superscript Ξ 1 𝑛 superscript subscript 𝒮 𝛼 𝛼 n^{-\alpha}\ell(n)\,\Xi^{-1}_{n}{\buildrel\mbox{\small\rm(law)}\over{\longrightarrow}}({\cal S}_{\alpha})^{-\alpha},

which implies Corollary 1.2 □ □ \Box

Proof of Corollary 1.4 Under the framework (2.12 n − α ℓ ( n ) Ξ n − 1 superscript 𝑛 𝛼 ℓ 𝑛 subscript superscript Ξ 1 𝑛 n^{-\alpha}\ell(n)\,\Xi^{-1}_{n} L p ( P ω ) superscript 𝐿 𝑝 subscript 𝑃 𝜔 L^{p}(P_{\omega}) p > 0 𝑝 0 p>0

E ω ( Ξ n − 1 ) p ≤ ∑ k = 0 ∞ p k p − 1 P ω ( Ξ n − 1 ≥ k ) = ∑ k = 0 ∞ p k p − 1 P ω ( Ξ k ≤ n ) . subscript 𝐸 𝜔 superscript subscript superscript Ξ 1 𝑛 𝑝 superscript subscript 𝑘 0 𝑝 superscript 𝑘 𝑝 1 subscript 𝑃 𝜔 subscript superscript Ξ 1 𝑛 𝑘 superscript subscript 𝑘 0 𝑝 superscript 𝑘 𝑝 1 subscript 𝑃 𝜔 subscript Ξ 𝑘 𝑛 E_{\omega}\Big{(}\Xi^{-1}_{n}\Big{)}^{p}\leq\sum_{k=0}^{\infty}p\,\,k^{p-1}\,P_{\omega}\Big{(}\Xi^{-1}_{n}\geq k\Big{)}=\sum_{k=0}^{\infty}p\,k^{p-1}\,P_{\omega}\Big{(}\Xi_{k}\leq n\Big{)}.

Observe that P ω ( Ξ k ≤ n ) ≤ P ω ( Ξ 1 ≤ n ) k ≤ e − k P ω ( Ξ 1 > n ) subscript 𝑃 𝜔 subscript Ξ 𝑘 𝑛 subscript 𝑃 𝜔 superscript subscript Ξ 1 𝑛 𝑘 superscript e 𝑘 subscript 𝑃 𝜔 subscript Ξ 1 𝑛 P_{\omega}\big{(}\Xi_{k}\leq n\big{)}\leq P_{\omega}\big{(}\Xi_{1}\leq n\big{)}^{k}\leq\mathrm{e}^{-k\,P_{\omega}(\Xi_{1}>n)}

E ω ( Ξ n − 1 ) p ≤ ∑ k = 0 ∞ p k p − 1 e − k P ω ( Ξ 1 > n ) . subscript 𝐸 𝜔 superscript subscript superscript Ξ 1 𝑛 𝑝 superscript subscript 𝑘 0 𝑝 superscript 𝑘 𝑝 1 superscript e 𝑘 subscript 𝑃 𝜔 subscript Ξ 1 𝑛 E_{\omega}\Big{(}\Xi^{-1}_{n}\Big{)}^{p}\leq\sum_{k=0}^{\infty}p\,k^{p-1}\,\mathrm{e}^{-k\,P_{\omega}(\Xi_{1}>n)}.

Since ∑ k = 0 ∞ p k p − 1 e − k x ≤ c 7 x − p superscript subscript 𝑘 0 𝑝 superscript 𝑘 𝑝 1 superscript e 𝑘 𝑥 subscript 𝑐 7 superscript 𝑥 𝑝 \sum_{k=0}^{\infty}p\,k^{p-1}\,\mathrm{e}^{-kx}\leq c_{7}\,x^{-p} 0 < x ≤ 1 0 𝑥 1 0<x\leq 1 c 7 = c 7 ( p ) > 0 subscript 𝑐 7 subscript 𝑐 7 𝑝 0 c_{7}=c_{7}(p)>0 P ω ( Ξ 1 > n ) × Ξ n − 1 subscript 𝑃 𝜔 subscript Ξ 1 𝑛 subscript superscript Ξ 1 𝑛 P_{\omega}\big{(}\Xi_{1}>n\big{)}\times\Xi^{-1}_{n} L p superscript 𝐿 𝑝 L^{p} p > 0 𝑝 0 p>0 2.13

(2.14) E ω ( Ξ n − 1 ) ∼ 𝔼 ( ( 𝒮 α ) − α ) n α ℓ ( n ) , n → ∞ . formulae-sequence similar-to subscript 𝐸 𝜔 subscript superscript Ξ 1 𝑛 𝔼 superscript subscript 𝒮 𝛼 𝛼 superscript 𝑛 𝛼 ℓ 𝑛 → 𝑛 E_{\omega}(\Xi^{-1}_{n})\,\sim\,{\mathbb{E}}\big{(}({\cal S}_{\alpha})^{-\alpha}\big{)}\,\frac{n^{\alpha}}{\ell(n)},\qquad n\to\infty.

Under P ω subscript 𝑃 𝜔 P_{\omega} X 𝑋 X [27 ] , Lemma 1.3.3 (1), page 323)) that k → P ω ( X 2 k = ∅ ) → 𝑘 subscript 𝑃 𝜔 subscript 𝑋 2 𝑘 k\to P_{\omega}(X_{2k}=\varnothing)

When κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] Ξ n − 1 = L n ∅ subscript superscript Ξ 1 𝑛 superscript subscript 𝐿 𝑛 \Xi^{-1}_{n}=L_{n}^{\varnothing} 2.14

E ω ( L 2 n ∅ ) ∼ 1 ω ( ∅ , ∅ ← ) M ∞ 2 π c 1 ( 2 n ) 1 / 2 , n → ∞ . formulae-sequence similar-to subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝑛 1 𝜔 superscript ← subscript 𝑀 2 𝜋 subscript 𝑐 1 superscript 2 𝑛 1 2 → 𝑛 E_{\omega}(L_{2n}^{\varnothing})\,\sim\,\frac{1}{\omega(\varnothing,{\buildrel\leftarrow\over{\varnothing}})M_{\infty}}\,\frac{2}{\pi c_{1}}\,(2n)^{1/2},\qquad n\to\infty.

Since E ω ( L 2 n ∅ ) = ∑ k = 1 n P ω ( X 2 k = ∅ ) subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝑛 superscript subscript 𝑘 1 𝑛 subscript 𝑃 𝜔 subscript 𝑋 2 𝑘 E_{\omega}(L_{2n}^{\varnothing})=\sum_{k=1}^{n}P_{\omega}(X_{2k}=\varnothing) [12 ] , formula (5.26), pp.447) yields Corollary 1.4

It remains to treat the cases κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2] P ω subscript 𝑃 𝜔 P_{\omega} Ξ n − 1 ≤ L n ∅ ≤ Ξ ^ n − 1 , ∀ n ≥ 1 formulae-sequence subscript superscript Ξ 1 𝑛 superscript subscript 𝐿 𝑛 subscript superscript ^ Ξ 1 𝑛 for-all 𝑛 1 \Xi^{-1}_{n}\leq L_{n}^{\varnothing}\leq\widehat{\Xi}^{-1}_{n},\forall n\geq 1 2.14 Ξ ^ n − 1 superscript subscript ^ Ξ 𝑛 1 \widehat{\Xi}_{n}^{-1} c 8 ≡ c 8 ( ω ) ∈ ( 0 , ∞ ) subscript 𝑐 8 subscript 𝑐 8 𝜔 0 c_{8}\equiv c_{8}(\omega)\in(0,\infty) c 9 ≡ c 9 ( ω ) ∈ ( 0 , ∞ ) subscript 𝑐 9 subscript 𝑐 9 𝜔 0 c_{9}\equiv c_{9}(\omega)\in(0,\infty) n ≥ 1 𝑛 1 n\geq 1

c 8 r ( 1 / n ) ≤ E ω ( L 2 n ∅ ) ≤ c 9 r ( 1 / n ) . subscript 𝑐 8 𝑟 1 𝑛 subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝑛 subscript 𝑐 9 𝑟 1 𝑛 \frac{c_{8}}{r(1/n)}\leq E_{\omega}(L_{2n}^{\varnothing})\leq\frac{c_{9}}{r(1/n)}.

Note that E ω ( L 2 n ∅ ) = ∑ k = 1 n P ω ( X 2 k = ∅ ) ≥ n P ω ( X 2 n = ∅ ) subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝑛 superscript subscript 𝑘 1 𝑛 subscript 𝑃 𝜔 subscript 𝑋 2 𝑘 𝑛 subscript 𝑃 𝜔 subscript 𝑋 2 𝑛 E_{\omega}(L_{2n}^{\varnothing})=\sum_{k=1}^{n}P_{\omega}(X_{2k}=\varnothing)\geq nP_{\omega}(X_{2n}=\varnothing)

(2.15) P ω ( X 2 n = ∅ ) ≤ c 9 n r ( 1 / n ) . subscript 𝑃 𝜔 subscript 𝑋 2 𝑛 subscript 𝑐 9 𝑛 𝑟 1 𝑛 P_{\omega}(X_{2n}=\varnothing)\leq\frac{c_{9}}{n\,r(1/n)}.

For the lower bound, we choose and fix a sufficiently small δ ≡ δ ( ω ) > 0 𝛿 𝛿 𝜔 0 \delta\equiv\delta(\omega)>0 n ≥ 1 𝑛 1 n\geq 1 r ( 1 / ( δ n ) ) ≥ 2 c 9 c 8 r ( 1 / n ) 𝑟 1 𝛿 𝑛 2 subscript 𝑐 9 subscript 𝑐 8 𝑟 1 𝑛 r(1/(\delta n))\geq\frac{2c_{9}}{c_{8}}r(1/n) n ≥ 1 𝑛 1 n\geq 1 E ω ( L 2 n ∅ ) − E ω ( L 2 δ n ω ) ≥ c 8 r ( 1 / n ) − c 9 r ( 1 / ( δ n ) ) ≥ c 8 2 r ( 1 / n ) subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝑛 subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝛿 𝑛 𝜔 subscript 𝑐 8 𝑟 1 𝑛 subscript 𝑐 9 𝑟 1 𝛿 𝑛 subscript 𝑐 8 2 𝑟 1 𝑛 E_{\omega}(L_{2n}^{\varnothing})-E_{\omega}(L_{2\delta n}^{\omega})\geq\frac{c_{8}}{r(1/n)}-\frac{c_{9}}{r(1/(\delta n))}\geq\frac{c_{8}}{2r(1/n)} E ω ( L 2 n ∅ ) − E ω ( L 2 δ n ω ) = ∑ k = δ n + 1 n P ω ( X 2 k = ∅ ) ≤ n ( 1 − δ ) P ω ( X 2 δ n = ∅ ) subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝑛 subscript 𝐸 𝜔 superscript subscript 𝐿 2 𝛿 𝑛 𝜔 superscript subscript 𝑘 𝛿 𝑛 1 𝑛 subscript 𝑃 𝜔 subscript 𝑋 2 𝑘 𝑛 1 𝛿 subscript 𝑃 𝜔 subscript 𝑋 2 𝛿 𝑛 E_{\omega}(L_{2n}^{\varnothing})-E_{\omega}(L_{2\delta n}^{\omega})=\sum_{k=\delta n+1}^{n}P_{\omega}(X_{2k}=\varnothing)\leq n(1-\delta)P_{\omega}(X_{2\delta n}=\varnothing) n ≥ 1 𝑛 1 n\geq 1 P ω ( X 2 δ n = ∅ ) ≥ c 8 2 n r ( 1 / n ) subscript 𝑃 𝜔 subscript 𝑋 2 𝛿 𝑛 subscript 𝑐 8 2 𝑛 𝑟 1 𝑛 P_{\omega}(X_{2\delta n}=\varnothing)\geq\frac{c_{8}}{2\,n\,r(1/n)} 2.15 1.4 □ □ \Box

The rest of this paper is devoted to the proof of Proposition 2.2 2.6 [5 ] pointed out the variety of contexts where the recursive equations have arisen in various models on tree, see also Peres and Pemantle [24 ] for the studies of a family of concave recursive iterations using the potential theory. We analyze here the equations (2.6 [15 ] by establishing some comparison inequalities on the concave iteration.

The key point in the proof of Proposition 2.2 𝐄 ( B ε ( ∅ ) ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon}(\varnothing)) 3 𝐄 ( B ε ( ∅ ) ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon}(\varnothing)) κ ∈ ( 1 , ∞ ] 𝜅 1 \kappa\in(1,\infty] ε − 1 / 2 B ε ( ∅ ) superscript 𝜀 1 2 subscript 𝐵 𝜀 \varepsilon^{-1/2}B_{\varepsilon}(\varnothing) κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] 𝐄 ( B ε ( ∅ ) ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon}(\varnothing)) 4 2.2 B ε ( ∅ ) 𝐄 ( B ε ( ∅ ) ) subscript 𝐵 𝜀 𝐄 subscript 𝐵 𝜀 \frac{B_{\varepsilon}(\varnothing)}{{\bf E}(B_{\varepsilon}(\varnothing))} M ∞ subscript 𝑀 M_{\infty}

Throughout the rest of this paper, ( c i ) 10 ≤ i ≤ 23 subscript subscript 𝑐 𝑖 10 𝑖 23 (c_{i})_{10\leq i\leq 23} κ 𝜅 \kappa p ∈ ( 1 , κ ) 𝑝 1 𝜅 p\in(1,\kappa)

3 Concave recursions on trees

Let 0 < ε < 1 0 𝜀 1 0<\varepsilon<1 2.6 B ε ( ∅ ) subscript 𝐵 𝜀 B_{\varepsilon}(\varnothing)

(3.1) B ε = (law) ∑ i = 1 ν A i ε + B ε ( i ) 1 + B ε ( i ) , superscript (law) subscript 𝐵 𝜀 superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 𝜀 subscript 𝐵 𝜀 𝑖 1 subscript 𝐵 𝜀 𝑖 B_{\varepsilon}{\buildrel\mbox{\small\rm(law)}\over{=}}\sum_{i=1}^{\nu}A_{i}{\varepsilon+B_{\varepsilon}(i)\over 1+B_{\varepsilon}(i)},

where as before, ( A i , 1 ≤ i ≤ ν ) ≡ ( A ( x ) , | x | = 1 ) subscript 𝐴 𝑖 1

𝑖 𝜈 𝐴 𝑥 𝑥

1 (A_{i},1\leq i\leq\nu)\equiv(A(x),|x|=1) ( A i , 1 ≤ i ≤ ν ) subscript 𝐴 𝑖 1

𝑖 𝜈 (A_{i},1\leq i\leq\nu) B ε ( i ) subscript 𝐵 𝜀 𝑖 B_{\varepsilon}(i) B ε subscript 𝐵 𝜀 B_{\varepsilon} 𝐄 ( ∑ i = 1 ν A i ) = 1 𝐄 superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 1 {\bf E}\big{(}\sum_{i=1}^{\nu}A_{i}\big{)}=1 𝐄 ( ∑ i = 1 ν A i κ ) = 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 𝜅 1 {\bf E}\big{(}\sum_{i=1}^{\nu}A_{i}^{\kappa}\big{)}=1 κ < ∞ 𝜅 \kappa<\infty

It is easy to get the uniqueness among the nonnegative solutions. Indeed, If B ε subscript 𝐵 𝜀 B_{\varepsilon} B ~ ε subscript ~ 𝐵 𝜀 \widetilde{B}_{\varepsilon} ( A i , 1 ≤ i ≤ ν ) subscript 𝐴 𝑖 1

𝑖 𝜈 (A_{i},1\leq i\leq\nu) ( B ε , B ε ( i ) , 1 ≤ i ≤ ν ) subscript 𝐵 𝜀 subscript 𝐵 𝜀 𝑖 1

𝑖 𝜈 (B_{\varepsilon},B_{\varepsilon}(i),1\leq i\leq\nu) ( B ~ ε , B ~ ε ( i ) , 1 ≤ i ≤ ν ) subscript ~ 𝐵 𝜀 subscript ~ 𝐵 𝜀 𝑖 1

𝑖 𝜈 (\widetilde{B}_{\varepsilon},\widetilde{B}_{\varepsilon}(i),1\leq i\leq\nu) 3.1 B ε subscript 𝐵 𝜀 B_{\varepsilon} B ~ ε subscript ~ 𝐵 𝜀 \widetilde{B}_{\varepsilon} B ε subscript 𝐵 𝜀 B_{\varepsilon} ∑ i = 1 ν A i superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 \sum_{i=1}^{\nu}A_{i} 𝐄 | B ε − B ~ ε | ≤ 𝐄 | ε + B ε 1 + B ε − ε + B ~ ε 1 + B ~ ε | ≤ ( 1 − ε ) 𝐄 | B ε − B ~ ε | 𝐄 subscript 𝐵 𝜀 subscript ~ 𝐵 𝜀 𝐄 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝜀 subscript ~ 𝐵 𝜀 1 subscript ~ 𝐵 𝜀 1 𝜀 𝐄 subscript 𝐵 𝜀 subscript ~ 𝐵 𝜀 {\bf E}|B_{\varepsilon}-\widetilde{B}_{\varepsilon}|\leq{\bf E}|\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}}-\frac{\varepsilon+\widetilde{B}_{\varepsilon}}{1+\widetilde{B}_{\varepsilon}}|\leq(1-\varepsilon){\bf E}|B_{\varepsilon}-\widetilde{B}_{\varepsilon}| B ε = B ~ ε subscript 𝐵 𝜀 subscript ~ 𝐵 𝜀 B_{\varepsilon}=\widetilde{B}_{\varepsilon} B ε ≡ B ε ( ∅ ) subscript 𝐵 𝜀 subscript 𝐵 𝜀 B_{\varepsilon}\equiv B_{\varepsilon}(\varnothing)

This section is devoted to the asymptotic behaviors of 𝐄 ( B ε ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon}) ε → 0 → 𝜀 0 \varepsilon\to 0 κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] 𝐄 ( B ε ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon}) ε → 0 → 𝜀 0 \varepsilon\to 0 κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2] 4

First we check that B ε → 0 → subscript 𝐵 𝜀 0 B_{\varepsilon}\to 0 L 1 ( 𝐏 ) superscript 𝐿 1 𝐏 L^{1}({\bf P}) 𝐄 ( B ε ) = 𝐄 ε + B ε 1 + B ε 𝐄 subscript 𝐵 𝜀 𝐄 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon})={\bf E}\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}} 𝐄 ( ∑ i = 1 ν A i ) = 1 𝐄 superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 1 {\bf E}\big{(}\sum_{i=1}^{\nu}A_{i}\big{)}=1

(3.2) 𝐄 ( B ε 2 1 + B ε ) = ε 𝐄 ( 1 1 + B ε ) . 𝐄 superscript subscript 𝐵 𝜀 2 1 subscript 𝐵 𝜀 𝜀 𝐄 1 1 subscript 𝐵 𝜀 {\bf E}\Big{(}\frac{B_{\varepsilon}^{2}}{1+B_{\varepsilon}}\Big{)}=\varepsilon\,{\bf E}\Big{(}\frac{1}{1+B_{\varepsilon}}\Big{)}.

Therefore

𝐄 ( B ε ) = 𝐄 ε + B ε 1 + B ε ≤ ε + 𝐄 B ε 1 + B ε ≤ ε + ( 𝐄 B ε 2 ( 1 + B ε ) 2 ) 1 / 2 , 𝐄 subscript 𝐵 𝜀 𝐄 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝜀 𝐄 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝜀 superscript 𝐄 superscript subscript 𝐵 𝜀 2 superscript 1 subscript 𝐵 𝜀 2 1 2 {\bf E}(B_{\varepsilon})={\bf E}\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}}\leq\varepsilon+{\bf E}\frac{B_{\varepsilon}}{1+B_{\varepsilon}}\leq\varepsilon+\Big{(}{\bf E}\frac{B_{\varepsilon}^{2}}{(1+B_{\varepsilon})^{2}}\Big{)}^{1/2},

which in view of (3.2 κ ∈ ( 1 , ∞ ] 𝜅 1 \kappa\in(1,\infty]

(3.3) 𝐄 ( B ε ) ≤ 2 ε 1 / 2 , 0 < ε ≤ 1 . formulae-sequence 𝐄 subscript 𝐵 𝜀 2 superscript 𝜀 1 2 0 𝜀 1 {\bf E}(B_{\varepsilon})\leq 2\varepsilon^{1/2},\qquad 0<\varepsilon\leq 1.

The above upper bound is sharp (up to a constant) only in the case κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] 𝐄 ( B ε ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon})

⟨ ξ ⟩ := ξ 𝐄 ( ξ ) , assign delimited-⟨⟩ 𝜉 𝜉 𝐄 𝜉 \langle\xi\rangle:=\frac{\xi}{{\bf E}(\xi)},

for any nonnegative random variable ξ 𝜉 \xi 𝐄 ⟨ ξ ⟩ p = 𝐄 ( ξ p ) ( 𝐄 ξ ) p 𝐄 superscript delimited-⟨⟩ 𝜉 𝑝 𝐄 superscript 𝜉 𝑝 superscript 𝐄 𝜉 𝑝 {\bf E}\langle\xi\rangle^{p}=\frac{{\bf E}(\xi^{p})}{({\bf E}\xi)^{p}}

Lemma 3.1

Let ϕ : ℝ + → ℝ + : italic-ϕ → subscript ℝ subscript ℝ \phi:{\mathbb{R}}_{+}\to{\mathbb{R}}_{+} C 1 superscript 𝐶 1 C^{1} ξ 𝜉 \xi ξ 𝜉 \xi δ > 0 𝛿 0 \delta>0 𝐄 ϕ ( ( 1 + δ ) ⟨ ξ ⟩ ) < ∞ 𝐄 italic-ϕ 1 𝛿 delimited-⟨⟩ 𝜉 {\bf E}\phi((1+\delta)\langle\xi\rangle)<\infty 0 ≤ ε < 1 0 𝜀 1 0\leq\varepsilon<1

𝐄 ϕ ( ⟨ ε + ξ 1 + ξ ⟩ ) ≤ 𝐄 ϕ ( ⟨ ξ ⟩ ) . 𝐄 italic-ϕ delimited-⟨⟩ 𝜀 𝜉 1 𝜉 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 {\bf E}\phi\Big{(}\Big{\langle}\frac{\varepsilon+\xi}{1+\xi}\Big{\rangle}\Big{)}\leq{\bf E}\phi\big{(}\langle\xi\rangle\big{)}.

Proof: We shall use several times the following inequality in [15 ] , formula (3.3): Let x 0 ∈ ℝ + subscript 𝑥 0 subscript ℝ x_{0}\in{\mathbb{R}}_{+} I ⊂ ℝ + 𝐼 subscript ℝ I\subset{\mathbb{R}}_{+} x 0 subscript 𝑥 0 x_{0} h : I × ℝ + → ( 0 , ∞ ) : ℎ → 𝐼 subscript ℝ 0 h:I\times{\mathbb{R}}_{+}\to(0,\infty) ∂ h ∂ x ℎ 𝑥 {\partial h\over\partial x}

•

𝐄 [ h ( x 0 , ξ ) ] < ∞ 𝐄 delimited-[] ℎ subscript 𝑥 0 𝜉 {\bf E}[h(x_{0},\xi)]<\infty 𝐄 [ ϕ ( ⟨ h ( x 0 , ξ ) ⟩ ) ] < ∞ 𝐄 delimited-[] italic-ϕ delimited-⟨⟩ ℎ subscript 𝑥 0 𝜉 {\bf E}\big{[}\phi\big{(}\big{\langle}h(x_{0},\xi)\big{\rangle}\big{)}\big{]}<\infty

•

𝐄 [ sup x ∈ I ( | ∂ h ∂ x ( x , ξ ) | + | ϕ ′ ( ⟨ h ( x , ξ ) ⟩ ) | ( | ∂ h ∂ x ( x , ξ ) | 𝐄 ( h ( x , ξ ) ) + h ( x , ξ ) [ 𝐄 ⟨ h ( x , ξ ) ⟩ ] 2 | 𝐄 ( ∂ h ∂ x ( x , ξ ) ) | ) ) ] < ∞ 𝐄 delimited-[] subscript supremum 𝑥 𝐼 ℎ 𝑥 𝑥 𝜉 superscript italic-ϕ ′ delimited-⟨⟩ ℎ 𝑥 𝜉 ℎ 𝑥 𝑥 𝜉 𝐄 ℎ 𝑥 𝜉 ℎ 𝑥 𝜉 superscript delimited-[] 𝐄 delimited-⟨⟩ ℎ 𝑥 𝜉 2 𝐄 ℎ 𝑥 𝑥 𝜉 {\bf E}[\sup_{x\in I}\big{(}|{\partial h\over\partial x}(x,\xi)|+|\phi^{\prime}\big{(}\big{\langle}h(x,\xi)\big{\rangle}\big{)}|\,({|{\partial h\over\partial x}(x,\xi)|\over{\bf E}(h(x,\xi))}+{h(x,\xi)\over[{\bf E}\langle h(x,\xi)\rangle]^{2}}|{\bf E}({\partial h\over\partial x}(x,\xi))|)\big{)}]<\infty

•

both y → h ( x 0 , y ) → 𝑦 ℎ subscript 𝑥 0 𝑦 y\to h(x_{0},y) y → ∂ ∂ x log h ( x , y ) | x = x 0 → 𝑦 evaluated-at 𝑥 ℎ 𝑥 𝑦 𝑥 subscript 𝑥 0 y\to{\partial\over\partial x}\log h(x,y)|_{x=x_{0}} ℝ + subscript ℝ {\mathbb{R}}_{+}

Then depending on whether h ( x 0 , ⋅ ) ℎ subscript 𝑥 0 ⋅ h(x_{0},\cdot) ∂ ∂ x log h ( x 0 , ⋅ ) 𝑥 ℎ subscript 𝑥 0 ⋅ {\partial\over\partial x}\log h(x_{0},\cdot)

(3.4) d d x 𝐄 ϕ ( ⟨ h ( x , ξ ) ⟩ ) | x = x 0 ≥ 0 , or ≤ 0 . \frac{d}{dx}\,{\bf E}\phi\left(\big{\langle}h(x,\xi)\big{\rangle}\right)\big{|}_{x=x_{0}}\geq 0,\qquad\hbox{\rm or}\qquad\leq 0.

Applying (3.4 h ( x , y ) := x + y 1 + y assign ℎ 𝑥 𝑦 𝑥 𝑦 1 𝑦 h(x,y):=\frac{x+y}{1+y} 0 < x < 1 0 𝑥 1 0<x<1 y ≥ 0 𝑦 0 y\geq 0 x 0 ∈ ( 0 , 1 ) subscript 𝑥 0 0 1 x_{0}\in(0,1) h ( x 0 , ⋅ ) ℎ subscript 𝑥 0 ⋅ h(x_{0},\cdot) ∂ ∂ x log h ( x 0 , ⋅ ) = 1 x 0 + ⋅ \frac{\partial}{\partial x}\log h(x_{0},\cdot)=\frac{1}{x_{0}+\cdot} x 0 ∈ ( 0 , 1 ) ↦ 𝐄 ϕ ( ⟨ h ( x 0 , X ) ⟩ ) subscript 𝑥 0 0 1 maps-to 𝐄 italic-ϕ delimited-⟨⟩ ℎ subscript 𝑥 0 𝑋 x_{0}\in(0,1)\mapsto{\bf E}\phi\big{(}\big{\langle}h(x_{0},X)\big{\rangle}\big{)} 0 < ε < 1 0 𝜀 1 0<\varepsilon<1

𝐄 ϕ ( ⟨ ε + ξ 1 + ξ ⟩ ) ≤ 𝐄 ϕ ( ⟨ ξ 1 + ξ ⟩ ) . 𝐄 italic-ϕ delimited-⟨⟩ 𝜀 𝜉 1 𝜉 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 1 𝜉 {\bf E}\phi\Big{(}\Big{\langle}\frac{\varepsilon+\xi}{1+\xi}\Big{\rangle}\Big{)}\leq{\bf E}\phi\Big{(}\Big{\langle}\frac{\xi}{1+\xi}\Big{\rangle}\Big{)}.

Now we take h ( x , y ) := y 1 + x y assign ℎ 𝑥 𝑦 𝑦 1 𝑥 𝑦 h(x,y):=\frac{y}{1+xy} x ∈ ( 0 , 1 ) 𝑥 0 1 x\in(0,1) y ≥ 0 𝑦 0 y\geq 0 3.4 x ∈ ( 0 , 1 ) ↦ 𝐄 ϕ ( ⟨ ξ 1 + x ξ ⟩ ) 𝑥 0 1 maps-to 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 1 𝑥 𝜉 x\in(0,1)\mapsto{\bf E}\phi\big{(}\big{\langle}\frac{\xi}{1+x\,\xi}\big{\rangle}\big{)} 𝐄 ϕ ( ⟨ ξ 1 + ξ ⟩ ) ≤ lim x → 0 𝐄 ϕ ( ⟨ ξ 1 + x ξ ⟩ ) 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 1 𝜉 subscript → 𝑥 0 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 1 𝑥 𝜉 {\bf E}\phi\big{(}\big{\langle}\frac{\xi}{1+\xi}\big{\rangle}\big{)}\leq\lim_{x\to 0}{\bf E}\phi\big{(}\big{\langle}\frac{\xi}{1+x\,\xi}\big{\rangle}\big{)} x > 0 𝑥 0 x>0 𝐄 ( ξ 1 + x ξ ) > 𝐄 ( ξ ) / ( 1 + δ ) 𝐄 𝜉 1 𝑥 𝜉 𝐄 𝜉 1 𝛿 {\bf E}(\frac{\xi}{1+x\,\xi})>{\bf E}(\xi)/(1+\delta) ⟨ ξ 1 + x ξ ⟩ ≤ ( 1 + δ ) ⟨ ξ ⟩ delimited-⟨⟩ 𝜉 1 𝑥 𝜉 1 𝛿 delimited-⟨⟩ 𝜉 \big{\langle}\frac{\xi}{1+x\,\xi}\big{\rangle}\leq(1+\delta)\big{\langle}\xi\big{\rangle} ϕ italic-ϕ \phi ϕ ( ⟨ ξ 1 + x ξ ⟩ ) ≤ max ( ϕ ( 0 ) , ϕ ( ( 1 + δ ) ⟨ ξ ⟩ ) ) italic-ϕ delimited-⟨⟩ 𝜉 1 𝑥 𝜉 italic-ϕ 0 italic-ϕ 1 𝛿 delimited-⟨⟩ 𝜉 \phi(\big{\langle}\frac{\xi}{1+x\,\xi}\big{\rangle})\leq\max(\phi(0),\phi((1+\delta)\big{\langle}\xi\big{\rangle})) lim x → 0 𝐄 ϕ ( ⟨ ξ 1 + x ξ ⟩ ) = 𝐄 ϕ ( ⟨ ξ ⟩ ) subscript → 𝑥 0 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 1 𝑥 𝜉 𝐄 italic-ϕ delimited-⟨⟩ 𝜉 \lim_{x\to 0}{\bf E}\phi\big{(}\big{\langle}\frac{\xi}{1+x\,\xi}\big{\rangle}\big{)}={\bf E}\phi\big{(}\big{\langle}\xi\big{\rangle}\big{)} □ □ \Box

Lemma 3.2

Assume (1.1 1.2 p ∈ ( 1 , 2 ] ∩ ( 1 , κ ) 𝑝 1 2 1 𝜅 p\in(1,2]\cap(1,\kappa) c 10 = c 10 ( p , κ ) subscript 𝑐 10 subscript 𝑐 10 𝑝 𝜅 c_{10}=c_{10}(p,\kappa) 0 < ε < 1 0 𝜀 1 0<\varepsilon<1

(3.5) 𝐄 ( ⟨ B ε ⟩ p ) 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 𝑝 \displaystyle{\bf E}\Big{(}\big{\langle}B_{\varepsilon}\big{\rangle}^{p}\Big{)} ≤ \displaystyle\leq c 10 . subscript 𝑐 10 \displaystyle c_{10}.\,

Proof: The proof of (3.5 [15 ] , Proposition 5.1) in the case that ν 𝜈 \nu 2 2 2 ν 𝜈 \nu 𝐄 ( ∑ i = 1 ν A i ) = 1 𝐄 superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 1 {\bf E}\big{(}\sum_{i=1}^{\nu}A_{i}\big{)}=1 ( B ε ( i ) ) subscript 𝐵 𝜀 𝑖 (B_{\varepsilon}(i)) ( A i ) subscript 𝐴 𝑖 (A_{i})

𝐄 ( B ε ) = 𝐄 ( ε + B ε 1 + B ε ) , 𝐄 subscript 𝐵 𝜀 𝐄 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon})={\bf E}\Big{(}\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}}\Big{)},

which yields that

⟨ B ε ⟩ p = ( ∑ i = 1 ν A i ⟨ ε + B ε ( i ) 1 + B ε ( i ) ⟩ ) p . superscript delimited-⟨⟩ subscript 𝐵 𝜀 𝑝 superscript superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 𝑖 1 subscript 𝐵 𝜀 𝑖 𝑝 \langle B_{\varepsilon}\rangle^{p}=\Big{(}\sum_{i=1}^{\nu}A_{i}\Big{\langle}\frac{\varepsilon+B_{\varepsilon}(i)}{1+B_{\varepsilon}(i)}\Big{\rangle}\Big{)}^{p}.

We recall the following inequality due to Neveu [23 ] : Let k ≥ 1 𝑘 1 k\geq 1 ξ 1 subscript 𝜉 1 \xi_{1} ⋯ ⋯ \cdots ξ k subscript 𝜉 𝑘 \xi_{k} 𝐄 ( ξ i p ) < ∞ 𝐄 superscript subscript 𝜉 𝑖 𝑝 {\bf E}(\xi_{i}^{p})<\infty ( 1 ≤ i ≤ k ) 1 𝑖 𝑘 (1\leq i\leq k)

𝐄 ( ξ 1 + ⋯ + ξ k ) p ≤ ∑ i = 1 k 𝐄 ( ξ i p ) + ( ∑ i = 1 k 𝐄 ξ i ) p . 𝐄 superscript subscript 𝜉 1 ⋯ subscript 𝜉 𝑘 𝑝 superscript subscript 𝑖 1 𝑘 𝐄 superscript subscript 𝜉 𝑖 𝑝 superscript superscript subscript 𝑖 1 𝑘 𝐄 subscript 𝜉 𝑖 𝑝 {\bf E}\left(\xi_{1}+\cdots+\xi_{k}\right)^{p}\leq\sum_{i=1}^{k}{\bf E}(\xi_{i}^{p})+\left(\sum_{i=1}^{k}{\bf E}\xi_{i}\right)^{p}.

It follows that

𝐄 [ ⟨ B ε ⟩ p ] 𝐄 delimited-[] superscript delimited-⟨⟩ subscript 𝐵 𝜀 𝑝 \displaystyle{\bf E}~\Big{[}\langle B_{\varepsilon}\rangle^{p}\Big{]} ≤ \displaystyle\leq 𝐄 ∑ i = 1 ν A i p ⟨ ε + B ε 1 + B ε ⟩ p + 𝐄 ( ∑ i = 1 ν A i ) p 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 𝑝 superscript delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝑝 𝐄 superscript superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 𝑝 \displaystyle{\bf E}\sum_{i=1}^{\nu}A_{i}^{p}\,\Big{\langle}\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}}\Big{\rangle}^{p}+{\bf E}\Big{(}\sum_{i=1}^{\nu}A_{i}\Big{)}^{p}

= \displaystyle= a p 𝐄 [ ⟨ ε + B ε 1 + B ε ⟩ p ] + c 11 , subscript 𝑎 𝑝 𝐄 delimited-[] superscript delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝑝 subscript 𝑐 11 \displaystyle a_{p}\,{\bf E}\Big{[}\Big{\langle}\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}}\Big{\rangle}^{p}\Big{]}+c_{11},

where c 11 := 𝐄 ( ∑ i = 1 ν A i ) p < ∞ assign subscript 𝑐 11 𝐄 superscript superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 𝑝 c_{11}:={\bf E}\big{(}\sum_{i=1}^{\nu}A_{i}\big{)}^{p}<\infty 1.2

(3.6) a p := 𝐄 ∑ i = 1 ν A i p < 1 , assign subscript 𝑎 𝑝 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 𝑝 1 a_{p}:={\bf E}\sum_{i=1}^{\nu}A_{i}^{p}<1,

by the definition of κ 𝜅 \kappa 3.1 ϕ ( x ) := x p assign italic-ϕ 𝑥 superscript 𝑥 𝑝 \phi(x):=x^{p} 𝐄 ⟨ ε + B ε 1 + B ε ⟩ p ≤ 𝐄 ⟨ B ε ⟩ p 𝐄 superscript delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝑝 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 𝑝 {\bf E}\Big{\langle}\frac{\varepsilon+B_{\varepsilon}}{1+B_{\varepsilon}}\Big{\rangle}^{p}\leq{\bf E}\langle B_{\varepsilon}\rangle^{p} 𝐄 ⟨ B ε ⟩ p ≤ c 11 1 − a p 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 𝑝 subscript 𝑐 11 1 subscript 𝑎 𝑝 {\bf E}\langle B_{\varepsilon}\rangle^{p}\leq\frac{c_{11}}{1-a_{p}} 3.5 □ □ \Box

To get a lower bound of 𝐄 ( B ε ) 𝐄 subscript 𝐵 𝜀 {\bf E}(B_{\varepsilon})

Lemma 3.3

Assume (1.1 1.2 p ∈ [ 1 , κ ) ∩ ( 1 , 2 ] 𝑝 1 𝜅 1 2 p\in[1,\kappa)\cap(1,2] a > 0 𝑎 0 a>0 ϕ a ( x ) := ( x 2 a + x ) p assign subscript italic-ϕ 𝑎 𝑥 superscript superscript 𝑥 2 𝑎 𝑥 𝑝 \phi_{a}(x):=\big{(}\frac{x^{2}}{a+x}\big{)}^{p} x ≥ 0 𝑥 0 x\geq 0

𝐄 ϕ a ( ⟨ B ε ⟩ ) ≤ 𝐄 ϕ a ( M ∞ ) . 𝐄 subscript italic-ϕ 𝑎 delimited-⟨⟩ subscript 𝐵 𝜀 𝐄 subscript italic-ϕ 𝑎 subscript 𝑀 {\bf E}\phi_{a}\Big{(}\big{\langle}B_{\varepsilon}\big{\rangle}\Big{)}\leq{\bf E}\phi_{a}(M_{\infty}).

Proof: It is elementary to check that the function ϕ a subscript italic-ϕ 𝑎 \phi_{a} b ≥ 0 𝑏 0 b\geq 0 t > 0 𝑡 0 t>0 x ↦ ϕ a ( b + t x ) maps-to 𝑥 subscript italic-ϕ 𝑎 𝑏 𝑡 𝑥 x\mapsto\phi_{a}(b+tx) 3.1 b ≥ 0 𝑏 0 b\geq 0 t > 0 𝑡 0 t>0

(3.7) 𝐄 ϕ a ( b + t ⟨ ε + ξ 1 + ξ ⟩ ) ≤ 𝐄 ϕ a ( b + t ⟨ ξ ⟩ ) . 𝐄 subscript italic-ϕ 𝑎 𝑏 𝑡 delimited-⟨⟩ 𝜀 𝜉 1 𝜉 𝐄 subscript italic-ϕ 𝑎 𝑏 𝑡 delimited-⟨⟩ 𝜉 {\bf E}\phi_{a}\left(b+t\,\Big{\langle}\frac{\varepsilon+\xi}{1+\xi}\Big{\rangle}\right)\leq{\bf E}\phi_{a}(b+t\,\langle\xi\rangle).

Recall (2.3 λ 𝜆 \lambda 1 − e − 2 λ = ε 1 superscript e 2 𝜆 𝜀 1-\mathrm{e}^{-2\lambda}=\varepsilon

B ε , n ( x ) := ∑ i = 1 ν x A ( x ( i ) ) β n , λ ( x ( i ) ) , ∀ | x | ≤ n . formulae-sequence assign subscript 𝐵 𝜀 𝑛

𝑥 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 subscript 𝛽 𝑛 𝜆

superscript 𝑥 𝑖 for-all 𝑥 𝑛 B_{\varepsilon,n}(x):=\sum_{i=1}^{\nu_{x}}A(x^{(i)})\beta_{n,\lambda}(x^{(i)}),\qquad\forall\,|x|\leq n.

Then B ε = B ε ( ∅ ) = lim n → ∞ B ε , n ( ∅ ) subscript 𝐵 𝜀 subscript 𝐵 𝜀 subscript → 𝑛 subscript 𝐵 𝜀 𝑛

B_{\varepsilon}=B_{\varepsilon}(\varnothing)=\lim_{n\to\infty}B_{\varepsilon,n}(\varnothing) 𝐏 𝐏 {\bf P} | x | < n 𝑥 𝑛 |x|<n 2.4

B ε , n ( x ) = ∑ i = 1 ν x A ( x ( i ) ) ε + B ε , n ( x ( i ) ) 1 + B ε , n ( x ( i ) ) . subscript 𝐵 𝜀 𝑛

𝑥 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 𝜀 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 1 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 B_{\varepsilon,n}(x)=\sum_{i=1}^{\nu_{x}}A(x^{(i)})\frac{\varepsilon+B_{\varepsilon,n}(x^{(i)})}{1+B_{\varepsilon,n}(x^{(i)})}.

Since 𝐄 ( ∑ i = 1 ν x A ( x ( i ) ) ) = 1 𝐄 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 1 {\bf E}(\sum_{i=1}^{\nu_{x}}A(x^{(i)}))=1

⟨ B ε , n ( x ) ⟩ = ∑ i = 1 ν x A ( x ( i ) ) ⟨ ε + B ε , n ( x ( i ) ) 1 + B ε , n ( x ( i ) ) ⟩ . delimited-⟨⟩ subscript 𝐵 𝜀 𝑛

𝑥 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 1 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 \langle B_{\varepsilon,n}(x)\rangle=\sum_{i=1}^{\nu_{x}}A(x^{(i)})\Big{\langle}\frac{\varepsilon+B_{\varepsilon,n}(x^{(i)})}{1+B_{\varepsilon,n}(x^{(i)})}\Big{\rangle}.

Applying (3.7 ξ = B ε , n ( x ( 1 ) ) 𝜉 subscript 𝐵 𝜀 𝑛

superscript 𝑥 1 \xi=B_{\varepsilon,n}(x^{(1)}) t = A ( x ( 1 ) ) 𝑡 𝐴 superscript 𝑥 1 t=A(x^{(1)}) b := 1 ( ν x ≥ 2 ) ∑ i = 2 ν x A ( x ( i ) ) ⟨ ε + B ε , n ( x ( i ) ) 1 + B ε , n ( ∅ ( i ) ) ⟩ assign 𝑏 subscript 1 subscript 𝜈 𝑥 2 superscript subscript 𝑖 2 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 1 subscript 𝐵 𝜀 𝑛

superscript 𝑖 b:=1_{(\nu_{x}\geq 2)}\,\sum_{i=2}^{\nu_{x}}A(x^{(i)})\Big{\langle}\frac{\varepsilon+B_{\varepsilon,n}(x^{(i)})}{1+B_{\varepsilon,n}(\varnothing^{(i)})}\Big{\rangle} ( t , b ) 𝑡 𝑏 (t,b)

𝐄 ϕ a ( ⟨ B ε , n ( x ) ⟩ ) ≤ 𝐄 ϕ a ( 1 ( ν x ≥ 2 ) ∑ i = 2 ν x A ( x ( i ) ) ⟨ ε + B ε , n ( x ( i ) ) 1 + B ε , n ( x ( i ) ) ⟩ + A ( x ( 1 ) ) ⟨ B ε , n ( x ( 1 ) ) ⟩ ) . 𝐄 subscript italic-ϕ 𝑎 delimited-⟨⟩ subscript 𝐵 𝜀 𝑛

𝑥 𝐄 subscript italic-ϕ 𝑎 subscript 1 subscript 𝜈 𝑥 2 superscript subscript 𝑖 2 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 delimited-⟨⟩ 𝜀 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 1 subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 𝐴 superscript 𝑥 1 delimited-⟨⟩ subscript 𝐵 𝜀 𝑛

superscript 𝑥 1 {\bf E}\phi_{a}(\langle B_{\varepsilon,n}(x)\rangle)\leq{\bf E}\phi_{a}\Big{(}1_{(\nu_{x}\geq 2)}\,\sum_{i=2}^{\nu_{x}}A(x^{(i)})\Big{\langle}\frac{\varepsilon+B_{\varepsilon,n}(x^{(i)})}{1+B_{\varepsilon,n}(x^{(i)})}\Big{\rangle}+A(x^{(1)})\langle B_{\varepsilon,n}(x^{(1)})\rangle\Big{)}.

In the right-hand-side of the above inequality, applying (3.7 B ε , n ( x ( 2 ) ) , … , B ε , n ( x ( ν x ) ) subscript 𝐵 𝜀 𝑛

superscript 𝑥 2 … subscript 𝐵 𝜀 𝑛

superscript 𝑥 subscript 𝜈 𝑥

B_{\varepsilon,n}(x^{(2)}),...,B_{\varepsilon,n}(x^{(\nu_{x})}) t 𝑡 t b 𝑏 b | x | < n 𝑥 𝑛 |x|<n

𝐄 ϕ a ( ⟨ B ε , n ( x ) ⟩ ) ≤ 𝐄 ϕ a ( ∑ i = 1 ν x A ( x ( i ) ) ⟨ B ε , n ( x ( i ) ) ⟩ ) . 𝐄 subscript italic-ϕ 𝑎 delimited-⟨⟩ subscript 𝐵 𝜀 𝑛

𝑥 𝐄 subscript italic-ϕ 𝑎 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 delimited-⟨⟩ subscript 𝐵 𝜀 𝑛

superscript 𝑥 𝑖 {\bf E}\phi_{a}\Big{(}\langle B_{\varepsilon,n}(x)\rangle\Big{)}\leq{\bf E}\phi_{a}\Big{(}\sum_{i=1}^{\nu_{x}}A(x^{(i)})\langle B_{\varepsilon,n}(x^{(i)})\rangle\Big{)}.

Notice by definition B ε , n ( x ) = ∑ i = 1 ν x A ( x ( i ) ) subscript 𝐵 𝜀 𝑛

𝑥 superscript subscript 𝑖 1 subscript 𝜈 𝑥 𝐴 superscript 𝑥 𝑖 B_{\varepsilon,n}(x)=\sum_{i=1}^{\nu_{x}}A(x^{(i)}) | x | = n − 1 𝑥 𝑛 1 |x|=n-1

𝐄 ϕ a ( ⟨ B ε , n ( ∅ ) ⟩ ) ≤ 𝐄 ϕ a ( ∑ | x | = n ∏ ∅ < y ≤ x A ( y ) ) = 𝐄 ϕ a ( M n ) . 𝐄 subscript italic-ϕ 𝑎 delimited-⟨⟩ subscript 𝐵 𝜀 𝑛

𝐄 subscript italic-ϕ 𝑎 subscript 𝑥 𝑛 subscript product 𝑦 𝑥 𝐴 𝑦 𝐄 subscript italic-ϕ 𝑎 subscript 𝑀 𝑛 {\bf E}\phi_{a}\Big{(}\langle B_{\varepsilon,n}(\varnothing)\rangle\Big{)}\leq{\bf E}\phi_{a}\Big{(}\sum_{|x|=n}\prod_{\varnothing<y\leq x}A(y)\Big{)}={\bf E}\phi_{a}(M_{n}).

Lemma 3.3 n → ∞ → 𝑛 n\to\infty □ □ \Box

Lemma 3.4

Assume (1.1 1.2

(3.8) lim inf ε → 0 ε − 1 / κ 𝐄 ( B ε ) subscript limit-infimum → 𝜀 0 superscript 𝜀 1 𝜅 𝐄 subscript 𝐵 𝜀 \displaystyle\liminf_{\varepsilon\to 0}\,\varepsilon^{-1/\kappa}\,{\bf E}(B_{\varepsilon})\, > \displaystyle> 0 , if 1 < κ < 2 , 0 if 1

𝜅 2 \displaystyle\,0,\qquad\hbox{if }1<\kappa<2,

(3.9) lim inf ε → 0 ( log 1 / ε ε ) 1 / 2 𝐄 ( B ε ) subscript limit-infimum → 𝜀 0 superscript 1 𝜀 𝜀 1 2 𝐄 subscript 𝐵 𝜀 \displaystyle\liminf_{\varepsilon\to 0}\,\Big{(}\frac{\log 1/\varepsilon}{\varepsilon}\Big{)}^{1/2}\,{\bf E}(B_{\varepsilon})\, > \displaystyle> 0 , if κ = 2 , 0 if 𝜅

2 \displaystyle\,0,\qquad\hbox{if }\kappa=2,

(3.10) lim inf ε → 0 ε − 1 / 2 𝐄 ( B ε ) subscript limit-infimum → 𝜀 0 superscript 𝜀 1 2 𝐄 subscript 𝐵 𝜀 \displaystyle\liminf_{\varepsilon\to 0}\,\varepsilon^{-1/2}\,{\bf E}(B_{\varepsilon})\, ≥ \displaystyle\geq c 2 , if κ > 2 , subscript 𝑐 2 if 𝜅

2 \displaystyle\,c_{2},\qquad\hbox{if }\kappa>2,

where c 2 := ( 1 − 𝐄 ( ∑ i = 1 ν A i 2 ) 𝐄 ( ∑ 1 ≤ i ≠ j ≤ ν A i A j ) ) 1 / 2 assign subscript 𝑐 2 superscript 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 2 𝐄 subscript 1 𝑖 𝑗 𝜈 subscript 𝐴 𝑖 subscript 𝐴 𝑗 1 2 c_{2}:=\big{(}\frac{1-{\bf E}(\sum_{i=1}^{\nu}A_{i}^{2})}{{\bf E}(\sum_{1\leq i\not=j\leq\nu}A_{i}A_{j})}\big{)}^{1/2} 2.2

Proof: If κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] 𝐄 ( ∑ i = 1 ν A i 2 ) < 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 2 1 {\bf E}(\sum_{i=1}^{\nu}A_{i}^{2})<1 𝐄 ( M ∞ 2 ) = 𝐄 ( ∑ 1 ≤ i ≠ j ≤ ν A i A j ) 1 − 𝐄 ( ∑ i = 1 ν A i 2 ) . 𝐄 superscript subscript 𝑀 2 𝐄 subscript 1 𝑖 𝑗 𝜈 subscript 𝐴 𝑖 subscript 𝐴 𝑗 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 2 {\bf E}(M_{\infty}^{2})=\frac{{\bf E}(\sum_{1\leq i\not=j\leq\nu}A_{i}A_{j})}{1-{\bf E}(\sum_{i=1}^{\nu}A_{i}^{2})}. κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty]

(3.11) 𝐄 M ∞ 2 a + M ∞ ∼ 1 a 𝐄 ( M ∞ 2 ) , a → ∞ . formulae-sequence similar-to 𝐄 superscript subscript 𝑀 2 𝑎 subscript 𝑀 1 𝑎 𝐄 superscript subscript 𝑀 2 → 𝑎 {\bf E}\frac{M_{\infty}^{2}}{a+M_{\infty}}\sim\frac{1}{a}\,{\bf E}(M_{\infty}^{2}),\qquad a\to\infty.

When κ ∈ ( 1 , 2 ] 𝜅 1 2 \kappa\in(1,2] 1.6 a → ∞ → 𝑎 a\to\infty

(3.12) 𝐄 M ∞ 2 a + M ∞ ≍ { a 1 − κ , if 1 < κ < 2 , log a a , if κ = 2 . asymptotically-equals 𝐄 superscript subscript 𝑀 2 𝑎 subscript 𝑀 cases superscript 𝑎 1 𝜅 if 1 < κ < 2 𝑎 𝑎 if κ = 2 {\bf E}\frac{M_{\infty}^{2}}{a+M_{\infty}}\,\asymp\,\begin{cases}a^{1-\kappa},&\hbox{\rm if $1<\kappa<2$}\,,\\

\frac{\log a}{a},&\hbox{\rm if $\kappa=2$}.\end{cases}

Recall from (3.2 𝐄 ( B ε 2 1 + B ε ) = ε 𝐄 ( 1 1 + B ε ) 𝐄 superscript subscript 𝐵 𝜀 2 1 subscript 𝐵 𝜀 𝜀 𝐄 1 1 subscript 𝐵 𝜀 {\bf E}\big{(}\frac{B_{\varepsilon}^{2}}{1+B_{\varepsilon}}\big{)}=\varepsilon\,{\bf E}\big{(}\frac{1}{1+B_{\varepsilon}}\big{)}

(3.13) 𝐄 ⟨ B ε ⟩ 2 a + ⟨ B ε ⟩ = a ε 𝐄 ( 1 1 + B ε ) ∼ a ε , ε → 0 , formulae-sequence 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 2 𝑎 delimited-⟨⟩ subscript 𝐵 𝜀 𝑎 𝜀 𝐄 1 1 subscript 𝐵 𝜀 similar-to 𝑎 𝜀 → 𝜀 0 {\bf E}\frac{\langle B_{\varepsilon}\rangle^{2}}{a+\langle B_{\varepsilon}\rangle}=a\,\varepsilon\,{\bf E}\Big{(}\frac{1}{1+B_{\varepsilon}}\Big{)}\sim a\,\varepsilon,\qquad\varepsilon\to 0,

where a ≡ a ( ε ) := 1 / 𝐄 ( B ε ) → ∞ 𝑎 𝑎 𝜀 assign 1 𝐄 subscript 𝐵 𝜀 → a\equiv a(\varepsilon):=1/{\bf E}(B_{\varepsilon})\to\infty 3.3 3.3 p = 1 𝑝 1 p=1

𝐄 ⟨ B ε ⟩ 2 a + ⟨ B ε ⟩ ≤ 𝐄 M ∞ 2 a + M ∞ . 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 2 𝑎 delimited-⟨⟩ subscript 𝐵 𝜀 𝐄 superscript subscript 𝑀 2 𝑎 subscript 𝑀 {\bf E}\frac{\langle B_{\varepsilon}\rangle^{2}}{a+\langle B_{\varepsilon}\rangle}\leq{\bf E}\frac{M_{\infty}^{2}}{a+M_{\infty}}.

Hence for a = 1 / 𝐄 ( B ε ) 𝑎 1 𝐄 subscript 𝐵 𝜀 a=1/{\bf E}(B_{\varepsilon})

lim inf ε → 0 1 a ε 𝐄 M ∞ 2 a + M ∞ ≥ 1 , subscript limit-infimum → 𝜀 0 1 𝑎 𝜀 𝐄 superscript subscript 𝑀 2 𝑎 subscript 𝑀 1 \liminf_{\varepsilon\to 0}\frac{1}{a\,\varepsilon}\,{\bf E}\frac{M_{\infty}^{2}}{a+M_{\infty}}\geq 1,

which in view of (3.12 3.11 □ □ \Box

We are ready to give the asymptotic behaviors of B ε subscript 𝐵 𝜀 B_{\varepsilon} κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty]

Proposition 3.5

Assume (1.1 1.2 κ ∈ ( 2 , ∞ ] 𝜅 2 \kappa\in(2,\infty] 𝐏 𝐏 {\bf P} ε → 0 → 𝜀 0 \varepsilon\to 0

ε − 1 / 2 B ε ⟶ (law) c 2 M ∞ , superscript ⟶ (law) superscript 𝜀 1 2 subscript 𝐵 𝜀 subscript 𝑐 2 subscript 𝑀 \varepsilon^{-1/2}\,B_{\varepsilon}\,{\buildrel\mbox{\small\rm(law)}\over{\longrightarrow}}\,c_{2}\,M_{\infty},

with c 2 := ( 1 − 𝐄 ( ∑ i = 1 ν A i 2 ) 𝐄 ( ∑ 1 ≤ i ≠ j ≤ ν A i A j ) ) 1 / 2 assign subscript 𝑐 2 superscript 1 𝐄 superscript subscript 𝑖 1 𝜈 superscript subscript 𝐴 𝑖 2 𝐄 subscript 1 𝑖 𝑗 𝜈 subscript 𝐴 𝑖 subscript 𝐴 𝑗 1 2 c_{2}:=\big{(}\frac{1-{\bf E}(\sum_{i=1}^{\nu}A_{i}^{2})}{{\bf E}(\sum_{1\leq i\not=j\leq\nu}A_{i}A_{j})}\big{)}^{1/2} 2.2

lim ε → 0 ε − 1 / 2 𝐄 ( B ε ) = c 2 . subscript → 𝜀 0 superscript 𝜀 1 2 𝐄 subscript 𝐵 𝜀 subscript 𝑐 2 \lim_{\varepsilon\to 0}\varepsilon^{-1/2}\,{\bf E}(B_{\varepsilon})=c_{2}.

Proof: Based on the boundedness in L 2 superscript 𝐿 2 L^{2} ε − 1 / 2 B ε superscript 𝜀 1 2 subscript 𝐵 𝜀 \varepsilon^{-1/2}B_{\varepsilon} 3.5 B ε ε subscript 𝐵 𝜀 𝜀 \frac{B_{\varepsilon}}{\sqrt{\varepsilon}} ε → 0 → 𝜀 0 \varepsilon\to 0 3.3 3.10

(3.14) c 2 ≤ lim inf ε → 0 𝐄 ( B ε ) ε 1 / 2 ≤ lim sup ε → 0 𝐄 ( B ε ) ε 1 / 2 ≤ 2 . subscript 𝑐 2 subscript limit-infimum → 𝜀 0 𝐄 subscript 𝐵 𝜀 superscript 𝜀 1 2 subscript limit-supremum → 𝜀 0 𝐄 subscript 𝐵 𝜀 superscript 𝜀 1 2 2 c_{2}\leq\liminf_{\varepsilon\to 0}\frac{{\bf E}(B_{\varepsilon})}{\varepsilon^{1/2}}\leq\limsup_{\varepsilon\to 0}\frac{{\bf E}(B_{\varepsilon})}{\varepsilon^{1/2}}\leq 2.

In particular, under 𝐏 𝐏 {\bf P} ( B ε ε , ε → 0 ) → subscript 𝐵 𝜀 𝜀 𝜀

0 (\frac{B_{\varepsilon}}{\sqrt{\varepsilon}},\varepsilon\to 0) ε n → 0 → subscript 𝜀 𝑛 0 \varepsilon_{n}\to 0 B ε n ε n ⟶ (law) ξ superscript ⟶ (law) subscript 𝐵 subscript 𝜀 𝑛 subscript 𝜀 𝑛 𝜉 \frac{B_{\varepsilon_{n}}}{\sqrt{\varepsilon}_{n}}\,{\buildrel\mbox{\small\rm(law)}\over{\longrightarrow}}\xi ξ 𝜉 \xi 3.14 ξ 𝜉 \xi 3.1 ξ 𝜉 \xi

ξ = (law) ∑ i = 1 ν A i ξ i , superscript (law) 𝜉 superscript subscript 𝑖 1 𝜈 subscript 𝐴 𝑖 subscript 𝜉 𝑖 \xi\,{\buildrel\mbox{\small\rm(law)}\over{=}}\,\sum_{i=1}^{\nu}A_{i}\,\xi_{i},

where conditioned on ( A i ) subscript 𝐴 𝑖 (A_{i}) ξ i subscript 𝜉 𝑖 \xi_{i} ξ 𝜉 \xi [17 ] ), ξ = c M ∞ 𝜉 𝑐 subscript 𝑀 \xi=c\,M_{\infty} c 𝑐 c 3.2

𝐄 ( ( B ε ε ) 2 1 + B ε ) = 𝐄 ( 1 1 + B ε ) , 𝐄 superscript subscript 𝐵 𝜀 𝜀 2 1 subscript 𝐵 𝜀 𝐄 1 1 subscript 𝐵 𝜀 {\bf E}\Big{(}\frac{(\frac{B_{\varepsilon}}{\sqrt{\varepsilon}})^{2}}{1+B_{\varepsilon}}\Big{)}={\bf E}\Big{(}\frac{1}{1+B_{\varepsilon}}\Big{)},

which by Fatou’s lemma along the subsequence ε n → 0 → subscript 𝜀 𝑛 0 \varepsilon_{n}\to 0 c 2 𝐄 ( M ∞ 2 ) ≤ 1 superscript 𝑐 2 𝐄 superscript subscript 𝑀 2 1 c^{2}\,{\bf E}(M_{\infty}^{2})\leq 1 c ≤ ( 𝐄 ( M ∞ 2 ) ) − 1 / 2 = c 2 𝑐 superscript 𝐄 superscript subscript 𝑀 2 1 2 subscript 𝑐 2 c\leq({\bf E}(M_{\infty}^{2}))^{-1/2}=c_{2} 3.14 c = c 2 𝑐 subscript 𝑐 2 c=c_{2} B ε ε subscript 𝐵 𝜀 𝜀 \frac{B_{\varepsilon}}{\sqrt{\varepsilon}} c 2 M ∞ subscript 𝑐 2 subscript 𝑀 c_{2}M_{\infty} □ □ \Box

4 Proof of Proposition 2.2

In view of Proposition 3.5 2.2 ε → 0 → 𝜀 0 \varepsilon\to 0

(4.1) 𝐄 ( B ε ( ∅ ) ) 𝐄 subscript 𝐵 𝜀 \displaystyle{\bf E}(B_{\varepsilon}(\varnothing)) ≍ asymptotically-equals \displaystyle\asymp { ε 1 / κ , if 1 < κ < 2 , ( ε log 1 / ε ) 1 / 2 , if κ = 2 . cases superscript 𝜀 1 𝜅 if 1 < κ < 2 superscript 𝜀 1 𝜀 1 2 if κ = 2 \displaystyle\begin{cases}\varepsilon^{1/\kappa},&\hbox{\rm if $1<\kappa<2$}\,,\\

\big{(}\frac{\varepsilon}{\log 1/\varepsilon}\big{)}^{1/2},&\hbox{\rm if $\kappa=2$}\,.\end{cases}

(4.2) ⟨ B ε ( ∅ ) ⟩ delimited-⟨⟩ subscript 𝐵 𝜀 \displaystyle\langle B_{\varepsilon}(\varnothing)\rangle\, → → \displaystyle\to M ∞ , for all κ ∈ ( 1 , ∞ ] , 𝐏 -a.s. subscript 𝑀 for all κ ∈ ( 1 , ∞ ] , 𝐏 -a.s.

\displaystyle\,M_{\infty},\qquad\hbox{for all $\kappa\in(1,\infty]$, \, ${\bf P}$-a.s.}

We remark that the L p superscript 𝐿 𝑝 L^{p} L p superscript 𝐿 𝑝 L^{p} ⟨ B ε ( ∅ ) ⟩ delimited-⟨⟩ subscript 𝐵 𝜀 \langle B_{\varepsilon}(\varnothing)\rangle 3.5

Let us start with a preliminary lemma which compares ⟨ B ε ( ∅ ) ⟩ delimited-⟨⟩ subscript 𝐵 𝜀 \langle B_{\varepsilon}(\varnothing)\rangle M ∞ subscript 𝑀 M_{\infty} B ε ≡ B ε ( ∅ ) subscript 𝐵 𝜀 subscript 𝐵 𝜀 B_{\varepsilon}\equiv B_{\varepsilon}(\varnothing) ∥ ⋅ ∥ p := 𝐄 ( | ⋅ | ) 1 / p \|\cdot\|_{p}:={\bf E}(|\cdot|)^{1/p} L p superscript 𝐿 𝑝 L^{p}

Lemma 4.1

Assume (1.1 1.2 p ∈ ( 1 , κ ) ∩ ( 1 , 2 ] 𝑝 1 𝜅 1 2 p\in(1,\kappa)\cap(1,2] c 12 subscript 𝑐 12 c_{12} ε ∈ ( 0 , 1 ) 𝜀 0 1 \varepsilon\in(0,1)

(4.3) ‖ ⟨ B ε ⟩ − M ∞ ‖ p ≤ c 12 × { ( 𝐄 ( B ε ) ) κ p − 1 , if 1 < κ ≤ 2 , ε 1 / 2 , if κ ∈ ( 2 , ∞ ] . subscript norm delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 𝑝 subscript 𝑐 12 cases superscript 𝐄 subscript 𝐵 𝜀 𝜅 𝑝 1 if 1 < κ ≤ 2 superscript 𝜀 1 2 if κ ∈ ( 2 , ∞ ] \|\langle B_{\varepsilon}\rangle-M_{\infty}\|_{p}\leq c_{12}\,\times\begin{cases}({\bf E}(B_{\varepsilon}))^{\frac{\kappa}{p}-1},&\qquad\mbox{if $1<\kappa\leq 2$},\\

\varepsilon^{1/2},&\qquad\mbox{if $\kappa\in(2,\infty]$}.\end{cases}

Proof: It follows from (2.6 x ∈ 𝕋 𝑥 𝕋 x\in{\mathbb{T}}

(4.4) ⟨ B ε ( x ) ⟩ delimited-⟨⟩ subscript 𝐵 𝜀 𝑥 \displaystyle\langle B_{\varepsilon}(x)\rangle = \displaystyle= ∑ y : y ← = x A ( y ) 1 𝐄 ( B ε ) ε + B ε ( y ) 1 + B ε ( y ) subscript 𝑦 : superscript 𝑦 ← absent 𝑥

𝐴 𝑦 1 𝐄 subscript 𝐵 𝜀 𝜀 subscript 𝐵 𝜀 𝑦 1 subscript 𝐵 𝜀 𝑦 \displaystyle\sum_{y:{\buildrel\leftarrow\over{y}}=x}A(y)\,\frac{1}{{\bf E}(B_{\varepsilon})}\,\frac{\varepsilon+B_{\varepsilon}(y)}{1+B_{\varepsilon}(y)}

= \displaystyle= ∑ y : y ← = x A ( y ) ⟨ B ε ( y ) ⟩ + ∑ y : y ← = x A ( y ) Δ ( y ) , subscript 𝑦 : superscript 𝑦 ← absent 𝑥

𝐴 𝑦 delimited-⟨⟩ subscript 𝐵 𝜀 𝑦 subscript 𝑦 : superscript 𝑦 ← absent 𝑥

𝐴 𝑦 Δ 𝑦 \displaystyle\sum_{y:{\buildrel\leftarrow\over{y}}=x}A(y)\,\langle B_{\varepsilon}(y)\rangle+\sum_{y:{\buildrel\leftarrow\over{y}}=x}A(y)\,\Delta(y),

with

Δ ( y ) := ε 𝐄 ( B ε ) ( 1 + B ε ( y ) ) − 1 𝐄 ( B ε ) B ε ( y ) 2 1 + B ε ( y ) , assign Δ 𝑦 𝜀 𝐄 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 𝑦 1 𝐄 subscript 𝐵 𝜀 subscript 𝐵 𝜀 superscript 𝑦 2 1 subscript 𝐵 𝜀 𝑦 \Delta(y):=\frac{\varepsilon}{{\bf E}(B_{\varepsilon})(1+B_{\varepsilon}(y))}-\frac{1}{{\bf E}(B_{\varepsilon})}\,\frac{B_{\varepsilon}(y)^{2}}{1+B_{\varepsilon}(y)},

where conditioned on ( A ( y ) , y ← = x , ν x ) (A(y),{\buildrel\leftarrow\over{y}}=x,\nu_{x}) Δ ( y ) Δ 𝑦 \Delta(y)

(4.5) Δ := ε 𝐄 ( B ε ) ( 1 + B ε ) − 1 𝐄 ( B ε ) B ε 2 1 + B ε . assign Δ 𝜀 𝐄 subscript 𝐵 𝜀 1 subscript 𝐵 𝜀 1 𝐄 subscript 𝐵 𝜀 superscript subscript 𝐵 𝜀 2 1 subscript 𝐵 𝜀 \Delta:=\frac{\varepsilon}{{\bf E}(B_{\varepsilon})(1+B_{\varepsilon})}-\frac{1}{{\bf E}(B_{\varepsilon})}\,\frac{B_{\varepsilon}^{2}}{1+B_{\varepsilon}}.

We note from (3.2 𝐄 ( Δ ) = 0 𝐄 Δ 0 {\bf E}(\Delta)=0

By iterating (4.4 m ≥ 1 𝑚 1 m\geq 1

(4.6) ⟨ B ε ⟩ ≡ ⟨ B ε ( ∅ ) ⟩ = ∑ | x | = m ∏ ∅ < y ≤ x A ( y ) ⟨ B ε ( x ) ⟩ + Θ m , delimited-⟨⟩ subscript 𝐵 𝜀 delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑥 𝑚 subscript product 𝑦 𝑥 𝐴 𝑦 delimited-⟨⟩ subscript 𝐵 𝜀 𝑥 subscript Θ 𝑚 \langle B_{\varepsilon}\rangle\equiv\langle B_{\varepsilon}(\varnothing)\rangle=\sum_{|x|=m}\,\prod_{\varnothing<y\leq x}A(y)\,\langle B_{\varepsilon}(x)\rangle+\Theta_{m},

with

Θ m := ∑ k = 1 m ∑ | x | = k ∏ ∅ < y ≤ x A ( y ) Δ ( x ) , assign subscript Θ 𝑚 superscript subscript 𝑘 1 𝑚 subscript 𝑥 𝑘 subscript product 𝑦 𝑥 𝐴 𝑦 Δ 𝑥 \Theta_{m}:=\sum_{k=1}^{m}\sum_{|x|=k}\prod_{\varnothing<y\leq x}A(y)\Delta(x),

where conditioned on ( V ( x ) , | x | ≤ m ) 𝑉 𝑥 𝑥

𝑚 (V(x),|x|\leq m) ( B ε ( x ) , Δ ( x ) ) subscript 𝐵 𝜀 𝑥 Δ 𝑥 (B_{\varepsilon}(x),\Delta(x)) ( B ε , Δ ) subscript 𝐵 𝜀 Δ (B_{\varepsilon},\Delta)

Observe that for any m ≥ 1 𝑚 1 m\geq 1 M ∞ = ∑ | x | = m ∏ ∅ < y ≤ x A ( y ) M ∞ ( x ) subscript 𝑀 subscript 𝑥 𝑚 subscript product 𝑦 𝑥 𝐴 𝑦 superscript subscript 𝑀 𝑥 M_{\infty}=\sum_{|x|=m}\prod_{\varnothing<y\leq x}A(y)\,M_{\infty}^{(x)} ( A ( x ) , | x | ≤ m ) 𝐴 𝑥 𝑥

𝑚 (A(x),|x|\leq m) M ∞ ( x ) superscript subscript 𝑀 𝑥 M_{\infty}^{(x)} M ∞ subscript 𝑀 M_{\infty}

Y m := ∑ | x | = m ∏ ∅ < y ≤ x A ( y ) ( ⟨ B ε ( x ) ⟩ − M ∞ ( x ) ) . assign subscript 𝑌 𝑚 subscript 𝑥 𝑚 subscript product 𝑦 𝑥 𝐴 𝑦 delimited-⟨⟩ subscript 𝐵 𝜀 𝑥 superscript subscript 𝑀 𝑥 Y_{m}:=\sum_{|x|=m}\prod_{\varnothing<y\leq x}A(y)\big{(}\langle B_{\varepsilon}(x)\rangle-M_{\infty}^{(x)}\big{)}.

Then we have

(4.7) ⟨ B ε ⟩ = M ∞ + Y m + Θ m . delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 subscript 𝑌 𝑚 subscript Θ 𝑚 \langle B_{\varepsilon}\rangle=M_{\infty}+Y_{m}+\Theta_{m}.

To control Y m subscript 𝑌 𝑚 Y_{m} [26 ] , pp. 82, (2.6.20)): Let k ≥ 1 𝑘 1 k\geq 1 1 ≤ p ≤ 2 1 𝑝 2 1\leq p\leq 2 ξ 1 subscript 𝜉 1 \xi_{1} ⋯ ⋯ \cdots ξ k subscript 𝜉 𝑘 \xi_{k} 𝐄 ( | ξ i | p ) < ∞ 𝐄 superscript subscript 𝜉 𝑖 𝑝 {\bf E}(|\xi_{i}|^{p})<\infty 𝐄 ( ξ i ) = 0 𝐄 subscript 𝜉 𝑖 0 {\bf E}(\xi_{i})=0 1 ≤ i ≤ k 1 𝑖 𝑘 1\leq i\leq k

(4.8) 𝐄 | ξ 1 + ⋯ + ξ k | p ≤ 2 ∑ i = 1 k 𝐄 ( | ξ i | p ) . 𝐄 superscript subscript 𝜉 1 ⋯ subscript 𝜉 𝑘 𝑝 2 superscript subscript 𝑖 1 𝑘 𝐄 superscript subscript 𝜉 𝑖 𝑝 {\bf E}\left|\xi_{1}+\cdots+\xi_{k}\right|^{p}\leq 2\sum_{i=1}^{k}{\bf E}(|\xi_{i}|^{p}).

Applying (4.8 Y m subscript 𝑌 𝑚 Y_{m} p ∈ ( 1 , κ ) ∩ ( 1 , 2 ] 𝑝 1 𝜅 1 2 p\in(1,\kappa)\cap(1,2]

𝐄 ( | Y m | p ) ≤ 2 𝐄 ( ∑ | x | = m ∏ ∅ < y ≤ x ( A ( y ) ) p ) 𝐄 ( | ⟨ B ε ⟩ − M ∞ | p ) = 2 a p m 𝐄 ( | ⟨ B ε ⟩ − M ∞ | p ) , 𝐄 superscript subscript 𝑌 𝑚 𝑝 2 𝐄 subscript 𝑥 𝑚 subscript product 𝑦 𝑥 superscript 𝐴 𝑦 𝑝 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 𝑝 2 superscript subscript 𝑎 𝑝 𝑚 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 𝑝 {\bf E}\Big{(}|Y_{m}|^{p}\Big{)}\leq 2\,{\bf E}\Big{(}\sum_{|x|=m}\prod_{\varnothing<y\leq x}(A(y))^{p}\Big{)}\,{\bf E}\Big{(}|\langle B_{\varepsilon}\rangle-M_{\infty}|^{p}\Big{)}=2\,a_{p}^{m}\,{\bf E}\Big{(}|\langle B_{\varepsilon}\rangle-M_{\infty}|^{p}\Big{)},

by using the constant a p ∈ ( 0 , 1 ) subscript 𝑎 𝑝 0 1 a_{p}\in(0,1) 3.6 𝐄 ( | ⟨ B ε ⟩ − M ∞ | p ) ≤ 2 p 𝐄 ( ⟨ B ε ⟩ p ) + 2 p 𝐄 ( M ∞ p ) 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 𝑝 superscript 2 𝑝 𝐄 superscript delimited-⟨⟩ subscript 𝐵 𝜀 𝑝 superscript 2 𝑝 𝐄 superscript subscript 𝑀 𝑝 {\bf E}(|\langle B_{\varepsilon}\rangle-M_{\infty}|^{p})\leq 2^{p}{\bf E}(\langle B_{\varepsilon}\rangle^{p})+2^{p}{\bf E}(M_{\infty}^{p}) c 13 subscript 𝑐 13 c_{13} ε ∈ ( 0 , 1 ) 𝜀 0 1 \varepsilon\in(0,1) 3.5 1.6

(4.9) 𝐄 ( | Y m | p ) ≤ 2 c 13 a p m , ∀ m ≥ 1 . formulae-sequence 𝐄 superscript subscript 𝑌 𝑚 𝑝 2 subscript 𝑐 13 superscript subscript 𝑎 𝑝 𝑚 for-all 𝑚 1 {\bf E}\Big{(}|Y_{m}|^{p}\Big{)}\leq 2c_{13}\,a_{p}^{m},\qquad\forall m\geq 1.

By the triangular inequality,

‖ Θ m ‖ p ≤ ∑ k = 1 m 𝐄 ( | ∑ | x | = k ∏ ∅ < y ≤ x A ( y ) Δ ( x ) | p ) 1 / p . subscript norm subscript Θ 𝑚 𝑝 superscript subscript 𝑘 1 𝑚 𝐄 superscript superscript subscript 𝑥 𝑘 subscript product 𝑦 𝑥 𝐴 𝑦 Δ 𝑥 𝑝 1 𝑝 \|\Theta_{m}\|_{p}\leq\sum_{k=1}^{m}\,{\bf E}\Big{(}\big{|}\sum_{|x|=k}\prod_{\varnothing<y\leq x}A(y)\Delta(x)\big{|}^{p}\Big{)}^{1/p}.

For the above expectation term, we apply (4.8

(4.10) 𝐄 ( | ∑ | x | = k ∏ ∅ < y ≤ x A ( y ) Δ ( x ) | p ) ≤ 2 𝐄 ( ∑ | x | = k ∏ ∅ < y ≤ x ( A ( y ) ) p ) 𝐄 ( | Δ | p ) = 2 a p k 𝐄 ( | Δ | p ) . 𝐄 superscript subscript 𝑥 𝑘 subscript product 𝑦 𝑥 𝐴 𝑦 Δ 𝑥 𝑝 2 𝐄 subscript 𝑥 𝑘 subscript product 𝑦 𝑥 superscript 𝐴 𝑦 𝑝 𝐄 superscript Δ 𝑝 2 superscript subscript 𝑎 𝑝 𝑘 𝐄 superscript Δ 𝑝 {\bf E}\Big{(}\big{|}\sum_{|x|=k}\prod_{\varnothing<y\leq x}A(y)\Delta(x)\big{|}^{p}\Big{)}\leq 2\,{\bf E}\Big{(}\sum_{|x|=k}\prod_{\varnothing<y\leq x}(A(y))^{p}\Big{)}\,{\bf E}\Big{(}|\Delta|^{p}\Big{)}=2\,a_{p}^{k}\,{\bf E}\Big{(}|\Delta|^{p}\Big{)}.

Consequently, for any m ≥ 1 𝑚 1 m\geq 1

‖ ⟨ B ε ⟩ − M ∞ ‖ p ≤ ‖ Y m ‖ p + ‖ Θ m ‖ p ≤ ( 2 c 13 ) 1 / p a p m / p + 2 1 / p ∑ k = 1 m a p k / p ‖ Δ ‖ p . subscript norm delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 𝑝 subscript norm subscript 𝑌 𝑚 𝑝 subscript norm subscript Θ 𝑚 𝑝 superscript 2 subscript 𝑐 13 1 𝑝 superscript subscript 𝑎 𝑝 𝑚 𝑝 superscript 2 1 𝑝 superscript subscript 𝑘 1 𝑚 superscript subscript 𝑎 𝑝 𝑘 𝑝 subscript norm Δ 𝑝 \|\langle B_{\varepsilon}\rangle-M_{\infty}\|_{p}\leq\|Y_{m}\|_{p}+\|\Theta_{m}\|_{p}\leq(2c_{13})^{1/p}\,a_{p}^{m/p}+2^{1/p}\sum_{k=1}^{m}a_{p}^{k/p}\,\|\Delta\|_{p}.

Recall that 0 < a p < 1 0 subscript 𝑎 𝑝 1 0<a_{p}<1 p ∈ ( 1 , κ ) ∩ ( 1 , 2 ] 𝑝 1 𝜅 1 2 p\in(1,\kappa)\cap(1,2] m → ∞ → 𝑚 m\to\infty

(4.11) ‖ ⟨ B ε ⟩ − M ∞ ‖ p ≤ 2 1 / p 1 − a p 1 / p ‖ Δ ‖ p , ∀ ε ∈ ( 0 , 1 ) . formulae-sequence subscript norm delimited-⟨⟩ subscript 𝐵 𝜀 subscript 𝑀 𝑝 superscript 2 1 𝑝 1 superscript subscript 𝑎 𝑝 1 𝑝 subscript norm Δ 𝑝 for-all 𝜀 0 1 \|\langle B_{\varepsilon}\rangle-M_{\infty}\|_{p}\leq\frac{2^{1/p}}{1-a_{p}^{1/p}}\,\|\Delta\|_{p},\qquad\forall\,\varepsilon\in(0,1).

By (4.5