Nonparametric Stochastic Discount Factor Decomposition††thanks: This paper is based on my job market paper, which was titled “Estimating the Long-Run Implications of Dynamic Asset Pricing Models” and dated November 8, 2013. I am very grateful to my advisors Xiaohong Chen and Peter Phillips for their advice and support. I would like to thank the co-editor Lars Peter Hansen and three anonymous referees for insightful and helpful comments. I have benefited from feedback from Caio Almeida (discussant), Jarda Borovička, Tim Cogley, Jean-Pierre Florens (discussant), Nour Meddahi, Keith O’Hara, Eric Renault, Guillaume Roussellet, Tom Sargent and participants of seminars at Chicago Booth, Columbia, Cornell, Duke, Indiana, Monash, Montréal, Northwestern, NYU, Penn, Princeton, Rutgers, Sydney, UCL, UNSW, Vanderbilt, Wisconsin, and several conferences. All errors are my own.

Abstract

Stochastic discount factor (SDF) processes in dynamic economies admit a permanent-transitory decomposition in which the permanent component characterizes pricing over long investment horizons. This paper introduces an empirical framework to analyze the permanent-transitory decomposition of SDF processes. Specifically, we show how to estimate nonparametrically the solution to the Perron-Frobenius eigenfunction problem of HS2009. Our empirical framework allows researchers to (i) recover the time series of the estimated permanent and transitory components and (ii) estimate the yield and the change of measure which characterize pricing over long investment horizons. We also introduce nonparametric estimators of the continuation value function in a class of models with recursive preferences by reinterpreting the value function recursion as a nonlinear Perron-Frobenius problem. We establish consistency and convergence rates of the eigenfunction estimators and asymptotic normality of the eigenvalue estimator and estimators of related functionals. As an application, we study an economy where the representative agent is endowed with recursive preferences, allowing for general (nonlinear) consumption and earnings growth dynamics.

Keywords: Nonparametric estimation, sieve estimation, stochastic discount factor, permanent-transitory decomposition, nonparametric value function estimation.

1 Introduction

In dynamic asset pricing models, stochastic discount factors (SDF) are stochastic processes that are used to infer equilibrium asset prices. AJ, HS2009 and Hansen2012 show that SDF processes may be decomposed into permanent and transitory components. The permanent component is a martingale that induces an alternative probability measure which is used to characterize pricing over long investment horizons. The transitory component is related to the return on a discount bond of (asymptotically) long maturity. AJ and BakshiChabiYo have found that SDFs must have nontrivial permanent and transitory components in order to explain several salient features of historical returns data. QL show that the permanent-transitory decomposition obtains even in very general semimartingale environments, suggesting that the decomposition is a fundamental feature of arbitrage-free asset pricing models.

The pathbreaking work of HS2009 links SDF decomposition in Markovian environments to a Perron-Frobenius eigenfunction problem. Specifically, HS2009 show that the permanent and transitory components are constructed from the SDF process, the Perron-Frobenius eigenfunction, and its eigenvalue. The eigenvalue determines the average yield on long-horizon payoffs and the eigenfunction characterizes dependence of the price of long-horizon payoffs on the Markov state. The probability measure that is relevant for pricing over long investment horizons may be expressed in terms of the eigenfunction and another eigenfunction that is obtained from a time-reversed Perron-Frobenius problem. See HS2012; HS2014, BackusChernovZin, BHS, and QL; QL:or for related theoretical developments.

This paper complements the existing theoretical literature by providing an empirical framework for extracting the permanent and transitory components of SDF processes. We show how to estimate the solution to the Perron-Frobenius eigenfunction problem of HS2009 from time-series data on state variables and a SDF process. By estimating directly the eigenvalue and eigenfunction, one can reconstruct the time series of the estimated permanent and transitory components and investigate their properties. The methodology also allows one to estimate both the yield and the change of measure which characterize pricing over long investment horizons. This approach is fundamentally different from existing empirical methods for studying the permanent-transitory decomposition, which produce bounds on various moments of the permanent and transitory components as functions of asset returns (AJ; BakshiChabiYo; BC-YG; BC-YG:rec).111Recently, QLN used a complementary parametric approach to recover the permanent component in a parametric term structure model. Although presented in the context of SDF decomposition, the methodology can be applied to more general processes such as the valuation and stochastic growth processes in HansenHeatonLi, HS2009, and Hansen2012.

The empirical framework is nonparametric, i.e., it does not place any tight parametric restrictions on the law of motion of state variables or the joint distribution of the state variables and the SDF process. This approach is coherent with the existing literature in which bounds on moments of the permanent and transitory components are derived without placing any parametric restrictions on the joint distribution of the SDF, state variables, and asset returns. This approach is also in line with conventional moment-based estimation methods for asset pricing models, such as GMM (Hansen1982) and its various extensions.222Examples include conditional moment based estimation methodology of AiChen2003 which has been applied to estimate asset pricing models featuring habits (ChenLudvigson) and recursive preferences (ChenFavilukisLudvigson) and the extended method of moments methodology of GGR2011 which is particularly relevant for derivative pricing.

In structural macro-finance models, SDF processes (and their permanent and transitory components) are determined by both the preferences of economic agents and the dynamics of state variables. Several works have shown that standard preference and state-process specifications struggle to explain salient features of historical returns data. For instance, BackusChernovZin find that certain specifications appear unable to generate a SDF whose permanent component is large enough to explain historical return premia without also generating unrealistically large spreads between long- and short-term yields. BakshiChabiYo find that historical returns data support positive covariance between the permanent and transitory components, but that positive association cannot be replicated by workhorse models such as the long-run risks model of BansalYaron. Our nonparametric methodology may be used in conjunction with parametric methods to better understand the roles of dynamics and preferences in building models whose permanent and transitory components have empirically realistic properties.

Of course, if state dynamics are treated nonparametrically then certain forward-looking components, such as the continuation value function under recursive preferences, are not available analytically. We therefore introduce nonparametric estimators of the continuation value function in models with EpsteinZin1989 recursive preferences with elasticity of intertemporal substitution (EIS) equal to unity. This class of preferences is used in prominent empirical work, such as HansenHeatonLi, and may also be interpreted as risk-sensitive preferences as formulated by HansenSargent1995 (see Tallarini2000). We reinterpret the fixed-point problem solved by the value function as a nonlinear Perron-Frobenius problem. In so doing, we draw connections with the literature on nonlinear Perron-Frobenius theory following SolowSamuelson.

As an application, we study an environment similar to that studied by HansenHeatonLi. We assume a representative agent with EpsteinZin1989 preferences with unit elasticity of intertemporal substitution. However, instead of modeling consumption and earnings using a homoskedastic Gaussian VAR as in HansenHeatonLi, we model consumption growth and earnings growth as a general (nonlinear) Markov process. We recover the time series of the SDF process and its permanent and transitory components without assuming any parametric law of motion for the state. The permanent component is large enough to explain historical returns on equities relative to long-term bonds, strongly countercyclical, and highly correlated with the SDF. We also show that the permanent component induces a probability measure that tilts the historical distribution of consumption and earnings growth towards regions of low earnings and consumption growth. To understand better the role of dynamics, we compare properties of the permanent and transitory components extracted nonparametrically with permanent and transitory components implied by two benchmark parametric models for state dynamics, namely a Gaussian VAR and an AR process with stochastic volatility. We find that for certain values of preference parameters, the nonparametric permanent and transitory components can be positively correlated whereas the permanent and transitory components corresponding to the two parametric models are strongly negatively correlated. Overall, our findings suggest that nonlinear dynamics may have a useful role to play in explaining the long end of the term structure.

The sieve (or projection) estimators of the Perron-Frobenius eigenfunction and eigenvalue that we propose draw heavily on earlier work on nonparametric estimation of Markov diffusions by CHS2000 and Gobetetal and are very simple to implement.333See DFR, DFG, and CFR2007 for kernel-based estimation of conditional expectation operators and LintonLewbelSrisuma2011 and EHLLS for kernel-based estimation of marginal utility in nonparametric Euler equation models via eigenfunction methods. We also propose sieve estimators of the continuation value function in a class of models with recursive preferences. Implementing the sieve value function estimators requires solving a low-dimensional fixed-point problem for which we propose a computationally simple iterative scheme. Both estimation procedures sidestep nonparametric estimation of the state transition distribution.

The main theoretical contributions of the paper are as follows. First, we establish consistency and convergence rates of the Perron-Frobenius eigenfunction estimators and establish asymptotic normality of the eigenvalue estimator and estimators of related functionals. The large-sample properties are established in sufficient generality that they can accommodate SDF process of either of a known functional form or containing components that have been first estimated from data (such as preference parameters and continuation value functions). Second, semiparametric efficiency bounds for the eigenvalue and related functionals are derived for the case in which the SDF is of a known functional form and the estimators are shown to attain their bounds. Third, this paper is the first to establish consistency and convergence rates for sieve estimators of the continuation value function for a class of models with recursive preferences. Although the analysis is confined to models in which the state vector is observable, the main theoretical results on eigenfunction and continuation value function estimation apply equally to models in which components of the state are latent.

The remainder of the paper is as follows. Section 2 briefly reviews the theoretical framework in HS2009 and related literature and discusses the scope of the analysis and identification issues. Section 3 introduces the estimators of the Perron-Frobenius eigenvalue, eigenfunctions, and related functionals and establishes their large-sample properties. Nonparametric continuation value function estimation is studied in Section 4. Section 5 presents a simulation exercise, Section 6 presents the empirical application and Section 7 concludes. Additional results on estimation and inference are deferred to the Appendix. The Supplemental Material contains proofs of all results in the main text and sufficient conditions for some assumptions appearing in the main text. An Online Appendix contains additional results on identification, further simulation results, and additional proofs.

2 Setup

2.1 Theoretical framework

This subsection summarizes the theoretical framework in AJ, HS2009 (HS hereafter), Hansen2012, and BHS (BHS hereafter). We work in discrete time with denoting the set of non-negative integers.

In arbitrage-free environments, there is a positive stochastic discount factor process that satisfies:

| (1) |

where is the (gross) return on a traded asset over the period from to , denotes the information available to all investors at date , and denotes expectation with respect to investors’ beliefs (see, e.g., HansenRenault). Throughout this paper, we impose rational expectations by assuming that investors’ beliefs agree with the data-generating probability measure.

AJ introduce the permanent-transitory decomposition:

| (2) |

The permanent component is a martingale: (almost surely). HS show that the martingale induces an alternative probability measure which is used to characterize pricing over long investment horizons. The transitory component is the reciprocal of the return to holding a discount bond of (asymptotically) long maturity from date to date . AJ provide conditions under which the permanent and transitory components exist. QL show that the decomposition obtains in very general semimartingale environments.

To formally introduce the framework in HS and BHS, consider a probability space on which there is a time homogeneous, strictly stationary and ergodic Markov process taking values in . Let denote the stationary distribution of . Let be the filtration generated by the histories of . It is assumed that summarizes all information relevant for asset pricing at date . When we consider payoffs depending only on future values of the state and allow trading at intermediate dates, we may assume the SDF process is a positive multiplicative functional of . That is, is adapted to , for each (almost surely) and:

with the time-shift operator given by for each (see Section 2 of HS). Thus, is a function of and is the same function applied to . In particular, we have:

| (3) |

for some positive function . For convenience, we occasionally refer to as the SDF.

Given the Markovianity of , we may define a one-period pricing operator which assigns date- prices to state-dependent payoffs at date . That is, if is a payoff at date , then its date- price is given by:

| (4) |

Pricing operators may be defined analogously for payoff horizons . The operator assigning date- prices to date- payoffs is given by:

| (5) |

It follows by Markovianity of the state and the multiplicative functional property of the SDF process that (i.e. applied times) for each . Therefore, it suffices to study the one-period operator .

HS introduce and study the Perron-Frobenius eigenfunction problem:

| (6) |

where the eigenvalue is a positive scalar and the eigenfunction is positive.444We say a function is positive (non-negative) if it is positive (non-negative) -almost everywhere. Classical, finite-dimensional Perron-Frobenius theory says that a positive matrix has positive right and left eigenvectors corresponding to its spectral radius.555See, e.g., Theorem 8.2.2 in HornJohnson. The KreinRutman theorem and its well-known extensions generalize finite-dimensional Perron-Frobenius theory to infinite-dimensional Banach spaces. To introduce formally the left eigenfunction of corresponding to , we use a time-reversed version of the Perron-Frobenius problem (6). Recall that a first-order Markov process seen in reverse time is also a first-order Markov process (Rosenblatt1971, p. 4). Define the time-reversed operator

In what follows, we will assume that is a bounded linear operator on the Hilbert space such that in which case is defined formally as the adjoint of . The time-reversed Perron-Frobenius problem is:

| (7) |

where is the eigenvalue from (6) and the eigenfunction is positive.

Given and which solve the Perron-Frobenius problem (6), HS define:

| (8) |

It follows from (6) that (almost surely) for each . HS show that although there may exist multiple solutions to the Perron-Frobenius problem, only one solution leads to processes and that may be interpreted correctly as permanent and transitory components. Such a solution has a martingale term that induces a change of measure under which is stochastically stable; see Condition 4.1 in BHS for sufficient conditions. Loosely speaking, stochastic stability requires that conditional expectations under the distorted probability measure converge (as the horizon increases) to an unconditional expectation . The expectation will typically be different from the expectation associated with the stationary distribution of . Under stochastic stability, the one-factor representation:

| (9) |

holds for each for which is finite (see, e.g., Proposition 7.1 in HS). When a long-run approximation like (9) holds, we may interpret and from (8) as the permanent and transitory components of the SDF process. Moreover, the scalar may be interpreted as the long-run yield. The long-run approximation (9) also shows that captures state dependence of long-horizon asset prices. The function is itself of interest as it will play a role in characterizing the expectation and will also appear in the asymptotic variance of estimators of .

The theoretical framework of HS may be used to characterize properties of the permanent and transitory components analytically by solving the Perron-Frobenius eigenfunction problem. Below, we describe an empirical framework to estimate the eigenvalue and eigenfunctions and from time series data on and a SDF process.

2.2 Scope of the analysis

The Markov state vector is assumed throughout to be observable to the econometrician. However, we do not constrain the transition law of to be of any parametric form. This approach is similar to that taken by GGR2011, who also presume the existence of a stationary, time-homogeneous Markov state process that is observable to the econometrician but do not constrain its transition law to be of any parametric form.

We assume the SDF function is either observable or known up to some parameter which is first estimated from data on (and possibly asset returns).

Case 1: SDF is observable

Here the functional form of is known ex ante. For example, consider the CCAPM with time discount parameter and risk aversion parameter both pre-specified by the researcher. Here we would simply take provided consumption growth is of the form for some known function . Other structural examples include models with external habits and models with durables with pre-specified preference parameters.

Case 2: SDF is estimated

In this case we assume that where the functional form of is known up to a parameter , which could be of several forms:

-

•

A finite-dimensional vector of preference parameters in structural models (e.g. HansenSingleton1982 and HHY) or risk-premium parameters in reduced-form models (e.g. GGR2011).

-

•

A vector of parameters together with a function , so . One example is models with EpsteinZin1989 recursive preferences, where the continuation value function is not known when the transition law of the Markov state is modeled nonparametrically (see ChenFavilukisLudvigson and the application in Section 6). For such models, would consist of discount, risk aversion, and intertemporal substitution parameters and would be the continuation value function. Another example is ChenLudvigson in which consists of time discount and homogeneity parameters and is a nonparametric internal or external habit formation component.

-

•

We could also take to be itself, in which case would be a nonparametric estimate of the SDF. Prominent examples include BansalViswanathan, AitSahaliaLo, and RosenbergEngle.

In Case 2 we consider a two-step approach to SDF decomposition. In the first step is estimated from time-series data on the state and possibly also asset returns. In the second step we plug the first-stage estimator into the nonparametric procedure to recover , , , and related quantities.

2.3 Identification

In this section we present some sufficient conditions that ensure there is a unique solution to the Perron-Frobenius problems (6) and (7). The conditions also ensure that a long-run approximation of the form (9) holds. Therefore, the resulting and constructed from and as in (8) may be interpreted correctly as the permanent and transitory components. For estimation, all that we require is for the conclusions of Proposition 2.1 below hold. Therefore, the following conditions could be replaced by other sets of sufficient conditions.

HS and BHS established very general identification, existence and long-run approximation results using Markov process theory. The operator-theoretic conditions that we use are more restrictive than the conditions in HS and BHS but they are convenient for deriving the large-sample theory that follows. In particular, the conditions ensure certain continuity properties of , and with respect to perturbations of the operator . Our results are derived for the specific parameter (function) space that is relevant for estimation, whereas the results in HS and BHS apply to a larger class of functions. Connections between our conditions and the conditions in HS and BHS are discussed in detail in the Online Appendix, which also treats separately the issues of identification, existence, and long-run approximation.

We take the cone of all positive functions in as the parameter space for . Let and denote the norm and inner product. We say that is bounded if and compact if maps bounded sets into relatively compact sets. Finally, let denote the product measure on .

Assumption 2.1

Discussion of assumptions: Part (a) are mild boundedness and positivity conditions. If the unconditional density and the transition density of exist, then is of the form:

Part (b) is weaker than requiring to be compact. A sufficient condition for compactness of is the Hilbert-Schmidt condition .

To introduce the identification result, let denote the spectrum of .666See, e.g., DunfordSchwartz, Chapter VII.3 for definitions. We say that is simple if it has a unique eigenfunction (up to scale) and isolated if there exists a neighborhood of such that . As and are defined up to scale, we say that and are unique if they are unique up to scale. Normalizing and so that , we may define a probability measure that is absolutely continuous with respect to by the change of measure:

| (10) |

Finally, let denote expectation under , i.e. for any indicator function we have

| (11) |

where the expectation on the right-hand side is taken under the stationary distribution .

Proposition 2.1

Let Assumption 2.1 hold. Then:

- (a)

- (b)

-

(c)

The eigenvalue is simple and isolated and it is the largest eigenvalue of .

- (d)

Parts (a) and (b) are existence and identification results, respectively. This is a well-known extension of the classical Krein-Rutman theorem (Schaefer1974, Theorems V.5.2 and V.6.6). Recently, similar operator-theoretic results have been applied to study identification in semi/nonparametric Euler equation models (see EscancianoHoderlein, LintonLewbelSrisuma2011, Chenetal2012, and EHLLS). Identification under slightly weaker but related conditions is studied in Christensen-idpev.

Part (c) guarantees that is isolated and simple, which is used extensively in the derivation of the large sample theory. Part (d) says that and are the relevant eigenvalue-eigenfunction pair for constructing the permanent and transitory components and links the expectation to . Note, in particular, that . Estimating and directly allows one to estimate the Radon-Nikodym derivative of with respect to .

3 Estimation

This section introduces the estimators of the Perron-Frobenius eigenvalue and eigenfunctions and and presents the large-sample properties of the estimators.

3.1 Sieve estimation

We follow CHS2000 and Gobetetal in using a sieve approach in which the infinite-dimensional eigenfunction problem is approximated by a low-dimensional matrix eigenvector problem. Let be a dictionary of linearly independent basis functions (e.g. polynomials, splines, wavelets, or a Fourier basis) and let denote the linear subspace spanned by . The sieve dimension is a smoothing parameter chosen by the econometrician and should increase with the sample size.

To describe the approximation, let denote the orthogonal projection onto . Consider the projected eigenfunction problem:

| (12) |

where is the largest real eigenvalue of and is its eigenfunction. Under regularity conditions, the problem (12) has a unique solution for all large enough (see Lemma A.1). As the function belongs to the space , we have that for a vector , where . The eigenfunction problem (12) may be written in matrix form as:

where the matrices and are given by:

| (13) | |||||

| (14) |

and where is the largest real eigenvalue of and is its eigenvector (we assume throughout that is nonsingular). We refer to as the approximate solution for . The approximate solution for is where is the eigenvector of corresponding to . Together, solve the generalized eigenvector problem:

| (15) |

where is the largest real generalized eigenvalue of the pair . We suppress dependence of and on hereafter to simplify notation.

To estimate , and , we solve the sample analogue of (15), namely:

| (16) |

where and are defined below and where is the maximum real generalized eigenvalue of the matrix pair . The estimators , and may be computed simultaneously using, for example, the eig routine in Matlab. The estimators of and are:

Under the regularity conditions below, the eigenvalue and its right- and left-eigenvectors and will be unique with probability approaching one (see Lemma A.3).

Given a time series of data , a natural estimator of is:

| (17) |

We consider two possibilities for estimating .

Case 1: SDF is observable

First, consider the case in which the function is specified by the researcher. In this case:

| (18) |

Case 2: SDF is estimated

Now suppose that the SDF is of the form where the functional form of is known up to the parameter which is to be estimated first from the data on and possibly also asset returns. Let denote this first-stage estimator. In this case:

| (19) |

3.1.1 Other functionals

Recall that the long-run yield is . We may estimate using:

| (20) |

Another functional of interest is the entropy of the permanent component, namely , which is bounded from below by the expected excess return of any traded asset relative to a discount bond of (asymptotically) long maturity (AJ, Proposition 2). Previous empirical work has estimated this bound from data on equity returns and proxies for holding period returns on long-maturity discount bonds (see, e.g., AJ and BakshiChabiYo). Here we take a complementary approach by assuming the SDF process is identifiable and estimate the entropy of its permanent component directly.

In Markovian environments, the entropy has the simple form (see Hansen2012 and BackusChernovZin). Given , a natural estimator of is:

| (21) |

in Case 1; in Case 2 we replace by in (21). The size of the permanent component may also be measured by other types of statistical discrepancies besides entropy (e.g. Cressie-Read divergences) which may be computed from the time series of the permanent component recovered empirically using and . We confine our attention to entropy because the theoretical literature has typically used entropy to measure the size of SDFs and their permanent components over different horizons (see, e.g., Hansen2012 and BackusChernovZin) and for sake of comparison with the empirical literature on bounds.

3.2 Consistency and convergence rates

Here we establish consistency of the estimators and derive the convergence rates of the eigenfunction estimators under mild regularity conditions.

Assumption 3.1

is bounded and conclusions (a)–(d) of Proposition 2.1 hold.

Assumption 3.2

.

Let denote the inverse of the positive definite square root of and let denote the identity matrix. Define the “orthogonalized” matrices , , and . Let also denote the Euclidean norm when applied to vectors and the operator norm (largest singular value) when applied to matrices. Note that and are a proof device and do not need to be calculated in practice.

Assumption 3.3

and .

Discussion of assumptions: Assumption 3.2 requires that the space be chosen such that it approximates well the range of (as ). This assumption also implicitly requires that is compact, as has been assumed previously in the literature on sieve estimation of eigenfunctions (see, e.g., Gobetetal).777If is not compact but is compact for some , then one can apply the estimators to in place of and estimate the solution to and similarly for . Large-sample properties of the estimators of , and would then follow directly from Theorems 3.1–3.5. Assumption 3.3 ensures that the sampling error in estimating vanishes asymptotically. This condition implicitly restricts the maximum rate at which can grow with . Appendix C.1 in the Supplementary Material presents some sufficient conditions for Assumption 3.3.

Before presenting the main result on convergence rates, we first we introduce sequences of constants that bound the approximation bias and sampling error. As eigenfunctions are only normalized up to scale, impose the normalizations and . Define:

| (22) |

Here and measure the bias incurred by approximating and by elements of . Bounds for and are available for commonly used bases when and belong a Hölder, Sobolev or Besov class (see, e.g., Chen2007). Let and and normalize and so that (this is equivalent to ). Under Assumption 3.3, we may choose positive sequences and which are both , so that:

| (23) |

Appendix C.1 presents bounds on and .

Theorem 3.1

It is worth noting that Theorem 3.1 holds for , and calculated from any estimators and that satisfy Assumption 3.3. Indeed, Theorem 3.1 is sufficiently general that it applies to models with latent state vectors without modification: all that is required is that one can construct estimators of and that satisfy Assumption 3.3.

Theorem 3.1 displays the usual bias-variance tradeoff encountered in nonparametric estimation. The bias terms and will be decreasing in (since and are approximated over increasingly rich subspaces as increases). On the other hand, the variance terms and will typically be increasing in (larger matrices) and decreasing in (more data). Choosing to balance the bias and variance terms will yield the best convergence rate. As an illustration, we now establish the convergence rates of and in Case 1, where and are as in (17) and (18), under standard conditions from the statistics literature on optimal convergence rates. Although the following conditions are not necessarily appropriate in an asset pricing context, the result is informative about the convergence properties of and . Let with and denote a Sobolev space of smoothness equipped with the norm .

Corollary 3.1

Let Assumption 3.1 and the following conditions hold: (i) is compact and rectangular; (ii) has a continuous density bounded away from zero; (iii) and is a bounded linear operator from into for some ; (iv) is spanned by tensor-product B-splines of order with equally spaced interior knots; (v) for some ; (vi) ; (vii) is exponentially rho-mixing. Then: Assumptions 3.2 and 3.3 hold and we may take , and . Choosing yields:

If is bounded, the rates become which is the optimal -norm rate for nonparametric regression estimators when the regression function belongs to .

Sieve methods may also be used to numerically compute , , and in models for which analytical solutions are unavailable. For such models, the matrices and may be computed directly (e.g. via simulation or numerical integration) and , and can be obtained by solving (15). Lemma A.2 gives the rates , , and .

We close this subsection with a remark relating and under an additional condition on the sieve basis . Assumption 3.2 implies that is compact. Therefore, has a singular value decomposition where are the nonzero singular values of arranged in non-increasing order (i.e. ) and and are orthonormal bases for with and for each (see, for example, Chapter 15.4 in Kress).

Remark 3.1

Let Assumption 3.2 hold and let span the linear subspaces generated by and . Then: and are both .

For example, if is a scalar Gaussian AR(1), is exponentially affine in , and the basis functions are Hermite polynomials then and are for some . Similar spanning assumptions are often made in the literature on sieve estimation of nonparametric instrumental variables models (see, e.g., BCK).

3.3 Asymptotic normality

In this section we establish the asymptotic normality of . The semiparametric efficiency bound in Case 1 is also derived and is shown to be efficient in this case. Related results on asymptotic normality and semiparametric efficiency of the estimator of the entropy of the permanent component are presented in Appendix B.

3.3.1 Asymptotic normality in Case 1

To establish asymptotic normality of , we derive the representation:

| (24) |

where the influence function is given by:

| (25) |

with and normalized so that and . The process is a martingale difference sequence (relative to the filtration ). Therefore, the asymptotic distribution of follows from (24) by a central limit theorem for martingale differences. To formalize this argument, we make the following assumption.

Assumption 3.4

Let the following hold:

-

(a)

and

-

(b)

and

-

(c)

.

Discussion of assumptions: Assumption 3.4(a) is an under-smoothing condition which ensures that the leading bias terms and higher-order bias terms involving , , and are asymptotically negligible. Assumption 3.4(b) ensures that and converge fast enough that may be written in an asymptotically linear form similar to (24)-(25) but with , , and in place of , , and . This result, in view of the asymptotic negligibility of the leading and higher-order bias terms under Assumption 3.4(a), leads to the representation (24). Sufficient conditions for Assumption 3.4(b) are presented in Appendix C.1. Assumption 3.4(c) allows a CLT for square-integrable martingale differences to be applied to the martingale difference sequence . Let .

It follows directly from Theorem 3.2 that .

We conclude by deriving the semiparametric efficiency bounds for Case 1. We require a further technical condition to characterize the tangent space (see Appendix B).

3.3.2 Asymptotic normality in Case 2

For Case 2, we obtain the following expansion (under regularity conditions):

| (26) |

where is from display (25) with and where:

| (27) |

The expansion (26) shows that the asymptotic distribution of and related functionals will depend on the properties of the first stage estimator . The following regularity conditions are deliberately general so as to accommodate a wide class of estimators.

We first suppose that is a finite-dimensional parameter and the plug-in estimator is root- consistent and asymptotically normal. Let .

Assumption 3.5

Let the following hold:

-

(a)

for some -valued random process

-

(b)

for some finite matrix

-

(c)

is continuously differentiable in on a neighborhood of for all and there exists some function with for some such that:

-

(d)

.

Let and define .

We now suppose that is an infinite-dimensional parameter. The parameter space is (a Banach space) equipped with some norm . This includes the case in which (1) is a function, i.e. with a function space, and (2) consists of both finite-dimensional and function parts, i.e. with with . For example, under recursive preferences the vector could consist of discount, risk-aversion and EIS parameters and could be the continuation value function.

Inference in this case involves the (typically nonlinear) functional , given by:

We focus on the case in which is root- estimable. We say the functional is pathwise differentiable at if exists for every fixed . If so, we denote the derivative by . Define where . Let denote the centered empirical process on . We say is Donsker if is absolutely convergent over to a non-negative quadratic form and there exists a sequence of Gaussian processes indexed by with covariance function and a.s. uniformly continuous sample paths such that as (see DoukhanMassartRio). Finally, let denote the norm for any (note that in our earlier notation).

Assumption 3.6

Let the following hold:

-

(a)

is Donsker

-

(b)

is pathwise differentiable at and

-

(c)

for some -valued random process , , and

-

(d)

for some finite matrix

-

(e)

and either and or and holds for some .

Discussion of assumptions: Sufficient conditions for the class to be Donsker are well known (see, e.g., DoukhanMassartRio). Parts (b) and (c) are standard conditions for inference in nonlinear semiparametric models (see, e.g., Theorem 4.3 in Chen2007). Part (d) is a mild CLT condition and part (e) is a mild higher-than-second-moments condition.

For the following theorem, let and define .

4 Value function recursion as a nonlinear Perron-Fro-benius problem

This section describes how to estimate nonparametrically the continuation value function and SDF in a class of models with recursive preferences by solving a nonlinear Perron-Frobenius eigenfunction problem. We focus on models in which a representative agent has EpsteinZin1989 recursive preferences with unit elasticity of intertemporal substitution (EIS). This class of preferences may also be interpreted as risk-sensitive preferences as formulated by HansenSargent1995 (see Tallarini2000). After describing the setup, we present some regularity conditions for local identification. We then introduce the estimators and derive their large-sample properties.

4.1 Setup

Under Epstein-Zin preferences, the date- utility of the representative agent is defined via the recursion:

where is date- consumption, is the EIS, is the time discount parameter, and is the relative risk aversion parameter. We maintain the assumption of a Markov state process . Let consumption growth, namely , be a measurable function of . HansenHeatonLi show that the scaled continuation value may be written as where:

| (28) |

With unit EIS (i.e. ) the fixed point equation (28) reduces to:

| (29) |

with . Analytical solutions for are typically only available when the conditional moment generating function of the Markov state is exponentially affine and is affine in . Assuming frictionless markets, the SDF is:

| (30) |

The dynamics of determine both the value function and the conditional expectation in the denominator of the SDF. The value function and conditional expectation are therefore unknown when the dynamics of are treated nonparametrically.

Consider the following reformulation of the fixed-point problem in display (29) as a nonlinear Perron-Frobenius problem. Setting and rearranging, we obtain the fixed-point equation , where:

As we seek a positive solution, taking an absolute value inside the conditional expectation in the preceding display does not change the fixed point. Dividing by and using the fact that is positive homogeneous of degree , we obtain the nonlinear Perron-Frobenius problem:

| (31) |

where is a positive eigenfunction of and is its eigenvalue. Throughout this section we normalize the eigenfunction to have unit norm. Unlike with linear operators, here changing the scaling of changes the corresponding eigenvalue: is a positive eigenfunction of with eigenvalue for any .

Reformulation of the recursion as a nonlinear Perron-Frobenius problem also leads to a convenient representation of the SDF. Rewriting the SDF from display (30) in terms of , we obtain:

Rescaling by and using (31) yields:

| (32) |

In what follows, we show how to estimate and from time-series data on . The estimates and can be plugged into (32) to obtain nonparametric estimates of the SDF process (i.e. without assuming a parametric law of motion for ).

4.2 Local identification

In this section we provide sufficient conditions for local identification of the fixed point and its corresponding eigenfunction . We establish the results for the parameter (function) space because it is convenient for sieve estimation. One cannot establish (global) identification using contraction mapping arguments because is not a contraction on .888Suppose that has a positive fixed point . The function is also a fixed point. Therefore, is not a contraction on (else the Banach contraction mapping theorem would yield a unique fixed point). Some of the regularity conditions we require for estimation are sufficient for to satisfy a local ergodicity property which, in turn, is sufficient for local identification.

To describe the local ergodicity property, first choose some (nonzero) function and set . Then consider the sequence defined iteratively by:

for . Proposition 4.1 below shows that the sequence converges to for any starting value in a suitably defined region. This is similar to various “stability” results in the literature on balanced growth following SolowSamuelson.999The literature on infinite-dimensional Perron-Frobenius theory has typically dealt with function spaces for which cone of non-negative functions has nonempty interior (see Krause for a recent overview). The non-negative cone in has empty interior. If is bounded then these previous results may be used to derive (global) identification conditions in the space . However, bounded support seems inappropriate for common choices of state variable, such as consumption growth and dividend growth. There, is a homogeneous input-output system, lists the proportions of commodities in the economy in period , and is normalized by its norm so that lists the proportions in period . “Stability” concerns convergence of the sequence to a positive eigenvector of (representing balanced growth proportions).

Write where is the nonlinear operator and is the linear operator:

The operator is bounded (respectively, compact) on whenever is bounded (compact) on (see Chapter 5 of KZPS). We say that is positive if is positive for any non-negative that is not identically zero. Positivity of ensures that the sequence is well defined and that any nonzero fixed point of is positive. We say that is Fréchet differentiable at if there exists a bounded linear operator such that:

If it exists, the Fréchet derivative of is given by:

Let denote the spectral radius of .

Proposition 4.1

Let be positive and bounded and let be Fréchet differentiable at with . Then: there exists finite positive constants and a neighborhood of such that:

for any initial point in the cone .

We say that is locally identified if there exists a neighborhood of such that is the unique eigenfunction of belonging to where denotes the unit sphere in (recall we normalize eigenfunctions of to have unit norm). Similarly, we say that is locally identified if is the unique fixed point of belonging to some neighborhood of . To see why local identification follows from Proposition 4.1, suppose is a positive eigenfunction of belonging to . Proposition 4.1 implies that for each , hence . Local identification of follows similarly.

Corollary 4.1

and are locally identified under the conditions of Proposition 4.1.

In fact, local identification of and positive homogeneity of imply that is the unique fixed point of in the cone .

Existence and (global) identification of value functions in models with recursive preferences has been studied previously (see MarinacciMontrucchio, HS2012, and references therein). The most closely related work to ours is HS2012, who study existence and uniqueness of value functions for Markovian environments in spaces (whose cones of non-negative functions also have empty interior). HS2012 provide conditions under which a fixed point may exist when the EIS is equal to unity but do not establish its uniqueness. Their existence conditions are based, in part, on existence of a positive eigenfunction of the operator .

There is also a connection between Corollary 4.1 and the literature on local identification of nonlinear, nonparametric econometric models. We can write as the conditional moment restriction:

(almost surely). The conditions of Proposition 4.1 ensure that the above moment restriction is Fréchet differentiable at with derivative . The condition implies that is invertible on . The conditions in Proposition 4.1 are therefore similar to the differentiability and rank conditions that Chenetal2012 use to study local identification in nonlinear conditional moment restriction models.

4.3 Estimation

We again use a sieve approach to reduce the infinite-dimensional problem to a low-dimensional (nonlinear) eigenvector problem. Consider the projected fixed-point problem:

| (33) |

where is the orthogonal projection onto the sieve space defined in Section 3. Lemma A.5 in the Appendix guarantees existence of a solution to (33) on a neighborhood of for all sufficiently large. As , we have for some vector which solves:

| (34) |

where . To simplify notation we drop dependence of and on hereafter. For estimation, we solve a sample analogue of (34), namely:

| (35) |

where is defined in display (17) and is given by:

Under the regularity conditions below, a solution on a neighborhood of necessarily exists wpa1 (see Lemma A.7 in the Appendix). The estimators of , and are:

| (36) |

The estimators and can then be plugged into display (32) to obtain an estimate of the SDF consistent with preference parameters and the observed law of motion of the state.

Assumption 4.1

Let the following hold:

-

(a)

has a unique positive fixed point

-

(b)

is positive and compact

-

(c)

is Fréchet differentiable at with .

Assumption 4.2

Let the following hold:

-

(a)

-

(b)

for each .

Let be as in Assumption 3.3. Let and . Note that and are a proof device and do not need to be calculated in practice.

Assumption 4.3

and for each .

Discussion of assumptions: Assumption 4.1(a) is a global identification assumption, parts (b) and (c) imposes some mild structure on which ensures that fixed points of are continuous under perturbations. Assumption 4.2(a)(b) are analogous to Assumption 3.2. Assumption 4.3 is similar to Assumption 3.3 and restricts the rate at which the sieve dimension can grow with ; sufficient conditions are presented in Appendix C.2.

Let denote the bias in approximating by an element of the sieve space. Assumption 4.2(b) implies that . To control the sampling error, fix any small . By Assumption 4.3 we may choose a sequence of positive constants with such that:

| (37) |

Appendix C.2 presents bounds on .

The convergence rates obtained in Theorem 4.1 again exhibit a bias-variance tradeoff. The bias terms are decreasing in , whereas the variance term is typically increasing in but decreasing in . Choosing to balance the terms will lead to the best convergence rate.

For implementation, we propose the following iterative scheme based on Proposition 4.1. Set , then calculate:

for . If the sequence converges to (say), we then set:

This iterative scheme proved to be a computationally efficient procedure for solving the sample fixed-point problem (35) in the simulations and empirical application.

5 Simulation evidence

The following Monte Carlo experiment illustrates the performance of the estimators in consumption-based models with power utility and recursive preferences. The state variable is log consumption growth, i.e. , which evolves as a Gaussian AR(1) process:

The parameters for the simulation are , , and . The data are constructed to be somewhat representative of quarterly growth in U.S. real per capita consumption of nondurables and services (for which and ). However, we make the consumption growth process twice as persistent to produce more nonlinear eigenfunctions and twice as volatile to produce a more challenging estimation problem.

We consider a power utility design in which and a design with recursive preferences with unit EIS, whose SDF is presented in display (32). For both designs we set and . The parameterization and is typically used in calibrations of long-run risks models; here we take so that the eigenfunctions and continuation value function are more nonlinear. For each design we generate 50000 samples of length 400, 800, 1600, and 3200. Results reported in this section use a Hermite polynomial basis of dimension . Further experimentation with other sieve dimensions showed that the results were reasonably insensitive to the dimension of the sieve space. Similar results were obtained using B-splines (see Appendix E in the Online Appendix).

We estimate , , , , and for both designs and and for the recursive preference design. We use the estimator in (17) for both preference specifications. For power utility we use the estimator in (18). For recursive preferences we first estimate using the method described in the previous section, then construct the estimator as in display (19), using:

based on the first-stage estimators of . We impose the scale normalizations , , and .

The bias and RMSE of the estimators are presented in Tables 1 and 2.101010To calculate the RMSE of , , and , for each replication we calculate the distance between the estimators and their population counterparts, then take the average over the MC replications. To calculate the bias we take the average of the estimators across the simulations to produce , , and (say), then compute the distance between , and and the true , and . The use of the “bias” here is not to be confused with the bias term in the convergence rate calculations: here “bias” of an estimator refers to the distance between the parameter and the average of its estimates across the simulations. Bias for , , , and is the average of the estimates across simulations minus the true parameter values. Table 1 shows that , and may be estimated with small bias and RMSE using a reasonably low-dimensional sieve. Table 2 presents similar results for , , and . The RMSEs for and under recursive preferences are typically smaller than the RMSEs for and under power utility, even though with recursive preferences the continuation value must be first estimated nonparametrically. In contrast, the RMSE for is larger under recursive preferences, which is likely due to the fact that is much more curved for that design (as evident from comparing the vertical scales Figures 1(b) and 1(d)). The results in Table 1 also show that may be estimated with a reasonably small degree of bias and RMSE in moderate samples.

Figures 1(a)–1(e) also present (pointwise) confidence intervals for , and computed across simulations of different sample sizes. For each figure, the true function lies approximately in the center of the pointwise confidence intervals, and the widths of the intervals shrink noticeably as the sample size increases. Corresponding plots using a B-spline basis are presented in the Online Appendix and are very similar to Figures 1(a)–1(e).

| Power Utility | Recursive Preferences | |||||

|---|---|---|---|---|---|---|

| Bias | 400 | 0.0144 | 0.0129 | 0.0027 | 0.0247 | 0.0119 |

| 800 | 0.0115 | 0.0129 | 0.0020 | 0.0187 | 0.0090 | |

| 1600 | 0.0084 | 0.0104 | 0.0016 | 0.0128 | 0.0062 | |

| 3200 | 0.0058 | 0.0077 | 0.0014 | 0.0095 | 0.0040 | |

| RMSE | 400 | 0.1136 | 0.1683 | 0.0458 | 0.4068 | 0.1034 |

| 800 | 0.0872 | 0.1060 | 0.0413 | 0.3513 | 0.0760 | |

| 1600 | 0.0681 | 0.0837 | 0.0361 | 0.1763 | 0.0577 | |

| 3200 | 0.0552 | 0.0677 | 0.0317 | 0.1591 | 0.0455 | |

| Power Utility | Recursive Preferences | |||||||

|---|---|---|---|---|---|---|---|---|

| Bias | 400 | 0.0035 | -0.0029 | 0.0029 | 0.0010 | -0.0008 | 0.0034 | 0.0040 |

| 800 | 0.0027 | -0.0024 | 0.0024 | 0.0011 | -0.0010 | 0.0027 | 0.0022 | |

| 1600 | 0.0020 | -0.0018 | 0.0018 | 0.0010 | -0.0008 | 0.0020 | 0.0014 | |

| 3200 | 0.0014 | -0.0013 | 0.0012 | 0.0010 | -0.0009 | 0.0016 | 0.0009 | |

| RMSE | 400 | 0.0358 | 0.0338 | 0.0282 | 0.0216 | 0.0179 | 0.0420 | 0.1005 |

| 800 | 0.0264 | 0.0251 | 0.0214 | 0.0217 | 0.0172 | 0.0299 | 0.0318 | |

| 1600 | 0.0204 | 0.0192 | 0.0168 | 0.0190 | 0.0151 | 0.0227 | 0.0179 | |

| 3200 | 0.0159 | 0.0149 | 0.0133 | 0.0192 | 0.0155 | 0.0204 | 0.0123 | |

6 Empirical application

In this section we study an economy similar to that in HansenHeatonLi. We assume a representative agent with EpsteinZin1989 recursive preferences with unit EIS and specify a two-dimensional state process in consumption and earnings growth. Our analysis may be summarized as follows. First, with discount and risk aversion parameters estimated from asset returns data ( and ), we show that this bivariate specification is able to generate a permanent component which implies a long-run equity premium (i.e. return on assets relative to long-term discount bonds) of approximately 2% per quarter. Second, we document the business cycle properties of the permanent and transitory components. Third, we describe the wedge required to tilt the distribution of the state to that which is relevant for long-run pricing. Finally, we show that, unlike the linear-Gaussian case, allowing for flexible treatment of the state process can lead to different behavior of long-run yields and different signs of correlation between the permanent and transitory components for different preference parameters. This suggests that nonlinearities in dynamics can be important in explaining the long end of the yield curve.

All data are quarterly and span the period 1947:Q1 to 2016:Q1 (277 observations). Data on consumption, dividends, inflation, and population are sourced from the National Income and Product Accounts (NIPA) tables. Real per capita consumption and dividend growth series are formed by taking seasonally adjusted consumption of nondurables and services (Table 2.3.5, lines 8 plus 13) and dividends (Table 1.12, line 16), deflating by the personal consumption implicit price deflator (Table 2.3.4, line 1), then converting to per capita growth rates using population data (Table 2.1, line 40). The resulting state variable is where and are real per capita consumption and dividend growth in quarter , respectively. Similar results are obtained replacing with real per capita growth in corporate earnings (using after-tax profits from line 15 of Table 1.12) and with real per capita growth in a four-quarter geometric moving average of dividends, as in HansenHeatonLi.

We also use data on seven asset returns, namely the returns on the six value-weighted portfolios sorted on size and book-to-market values (sourced from Kenneth French’s website) and the 90-day Treasury bill rate. All asset returns series are converted to real returns using the implicit price deflator for personal consumption expenditures.

We estimate the preference parameters and the pair using the data on and the time series of seven asset returns. This falls into the setup of “Case 2” with . We estimate the parameters using a series conditional moment estimation procedure (AiChen2003). This methodology was used recently in a similar context by ChenFavilukisLudvigson.111111The differences between our estimator and that of ChenFavilukisLudvigson are as follows. First, we focus on the EIS case whereas ChenFavilukisLudvigson treat the EIS as a free parameter. Second, we exploit the eigenfunction representation of the continuation value recursion. Third, we “profile out” continuation value function estimation by solving for separately from estimating the preference parameters. Therefore, our criterion function depends only on . In contrast, ChenFavilukisLudvigson jointly estimate the preference parameters and the continuation value function. Fourth, the continuation value is a function of the Markov state in our analysis whereas the continuation value function in ChenFavilukisLudvigson depends on contemporaneous consumption growth and the lagged continuation value. For each , we estimate the solution to the nonlinear eigenfunction problem, namely , using the procedure introduced in Section 4. Here we make explicit the dependence of on and , since different preference parameters will correspond to different continuation value functions. We then form:

Let denote a vector of (gross) asset returns from time to and and denote conformable vectors of ones and zeros. As the Euler equation holds conditionally, we instrument the generalized residuals, namely:

by basis functions of to form a criterion function which exploits the conditional nature of the Euler equation. This leads to the criterion function:

where

We minimize to obtain and we set . We then estimate , , and related quantities using the estimator in display (19) for this choice of .

To implement the procedure, we use the same basis functions for estimation of , , and . We form fifth-order univariate Hermite polynomial bases for the and series. We then construct a tensor product basis from the univariate bases, discarding any tensor-product polynomials whose total degree is order six or higher. The resulting sparse basis has dimension 15 whereas a tensor product basis would have dimension 25. We sometimes compare with the univariate state process for which we use an eighth-order Hermite polynomial basis. We instrument the generalized residuals with a lower-dimensional vector of basis functions to form the criterion function (dimension 6 in the univariate case and 10 in the bivariate case). Similar results are obtained with different dimensional bases.

| 0.99 | 0.99 | 0.99 | |||

| 20 | 25 | 30 | |||

Table 3 presents the estimates and bootstrapped 90% confidence intervals.121212We resample the data 1000 times using the stationary bootstrap with an expected block length of six quarters. In the left panel we re-estimate , , , , , , and for each bootstrap replication. We discard the tiny fraction of replications in which the estimator of failed to converge. In the right panel we fix and and re-estimate , , , , and for each bootstrap replication. There are several notable aspects. First, both state specifications generate a permanent component whose entropy is consistent with a return premium of around 2% per quarter relative to the long bond, which is in the ballpark of empirically reasonable estimates. Second, the estimated long-run yield of around 1.9% per quarter is too large, which is explained by the low value of . Third, the estimated entropy of the SDF, namely is for the bivariate specification and for the univariate specification. Therefore, the estimated horizon dependence (the difference between the entropy of the permanent component and the entropy of the SDF) is within the bound of 0.1% per month that BackusChernovZin argue is required to match the spread in average yields between short- and long-term bonds. Finally, the estimates of are quite imprecise, in agreement with previous studies (e.g., ChenFavilukisLudvigson). The confidence intervals for , and in the left panel of Table 3 are rather wide which reflects, in large part, the uncertainty in estimating and . Experimentation with different sieve dimensions resulted in estimates of between and .131313ChenFavilukisLudvigson obtain using aggregate consumption data and using stockholder consumption data. Further, with stockholder data their estimated EIS is not significantly different from zero. This suggests that our estimates of and maintained assumption of a unit EIS are empirically plausible. The right panel of Table 3 presents estimates of , and fixing and , , and ( and are still estimated nonparametrically). It is clear that the resulting confidence intervals are much narrower once the uncertainty from estimating and is shut down.

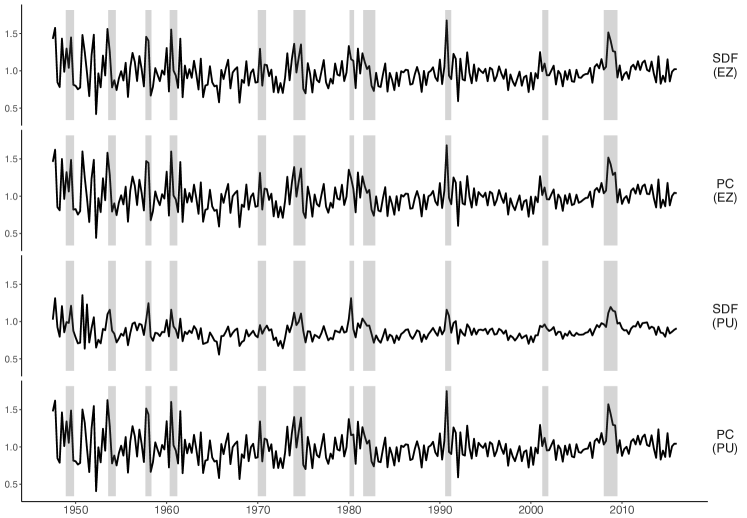

We now turn to analyzing the time-series properties of the permanent and transitory components. The upper two panels of Figure 2 display time-series plots for the bivariate state specification of the SDF and its permanent component, constructed as:

As can be seen, the SDF and its permanent component evolve closely over time and exhibit strong counter-cyclicality. The transitory component (not plotted) is small, consistent with the literature on bounds which finds that the transitory component should be substantially smaller than the permanent component. The correlation of the permanent component series and GDP growth is approximately whereas the correlation of the transitory component series and GDP growth is approximately . The lower panels of Figure 2 display time-series plots of the SDF and permanent component obtained under power utility using the same as in the recursive preference specification. This panel shows that the permanent component, which is similar to that obtained under recursive preferences, is much more volatile than the SDF series. The large difference between the SDF and permanent component series under power utility is due to a very volatile transitory component, which implies a counterfactually large spread in average yields between short- and long-term bonds (BackusChernovZin).

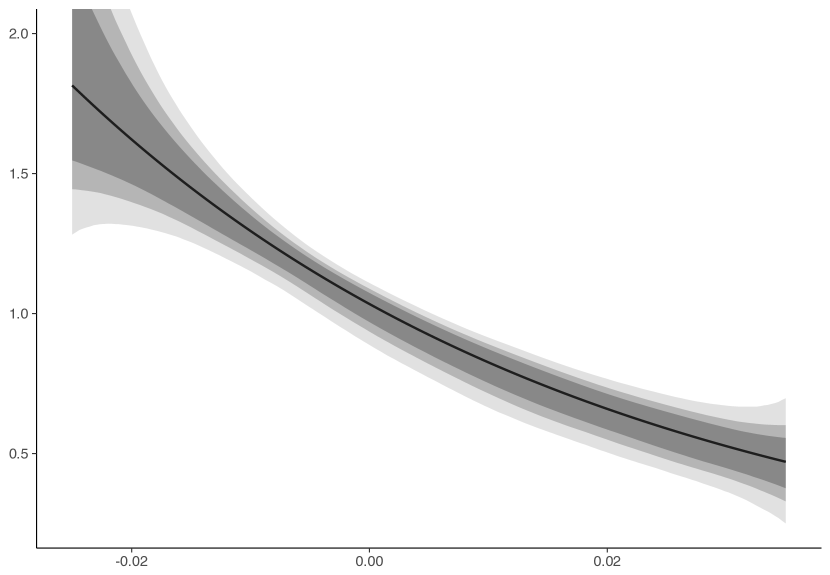

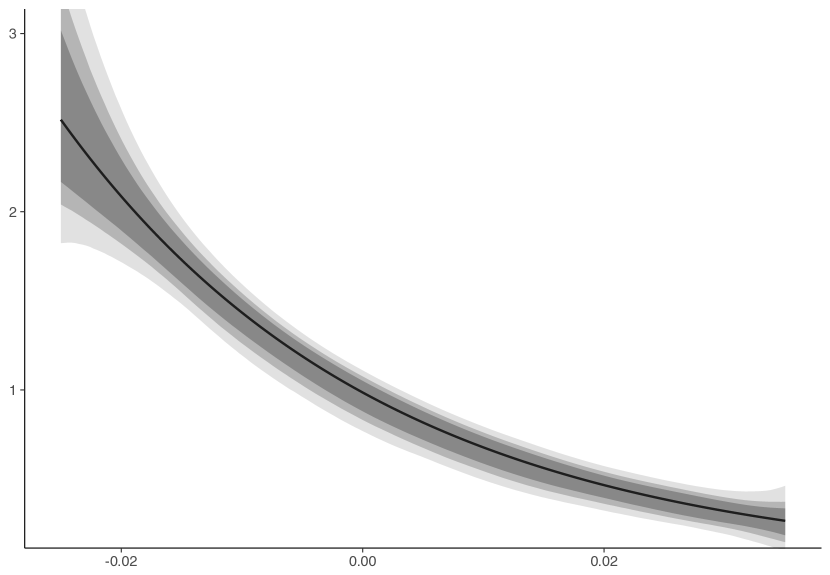

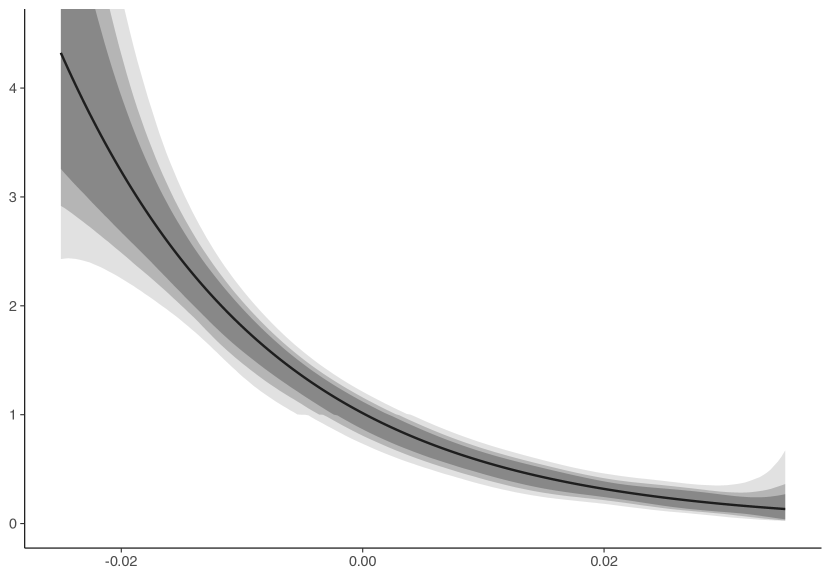

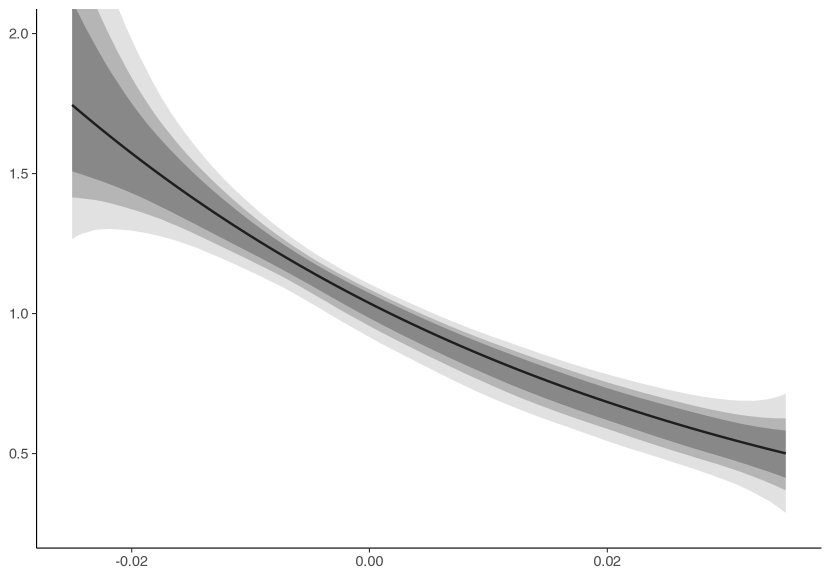

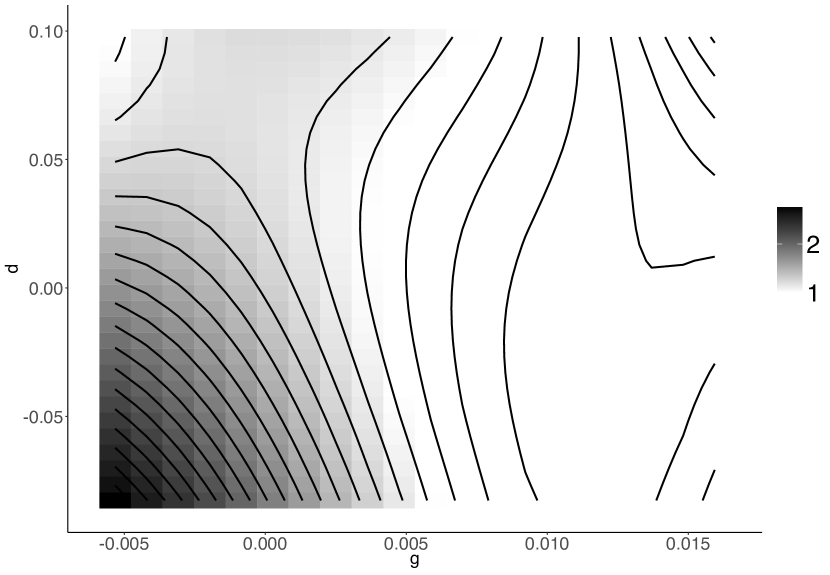

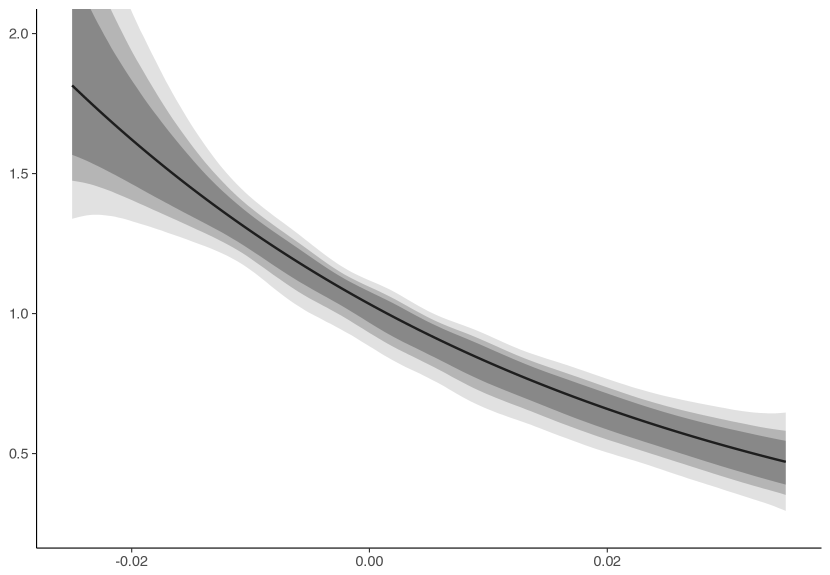

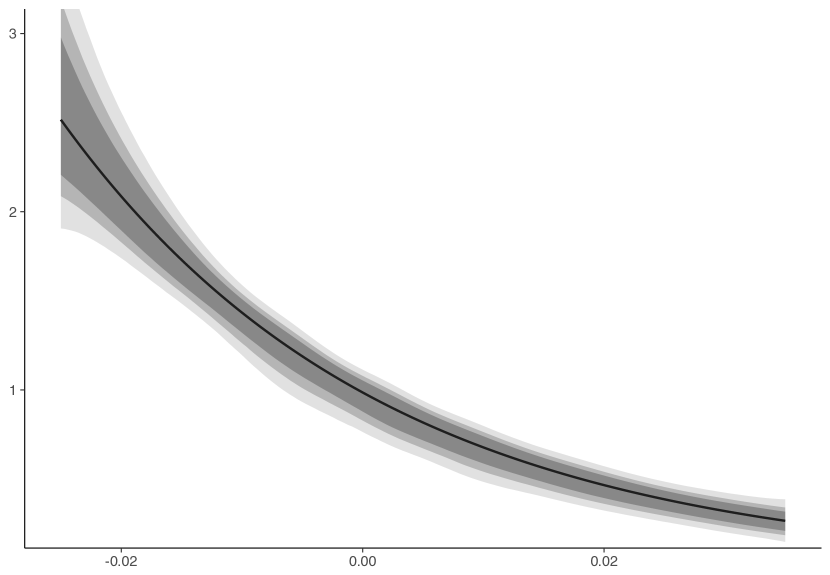

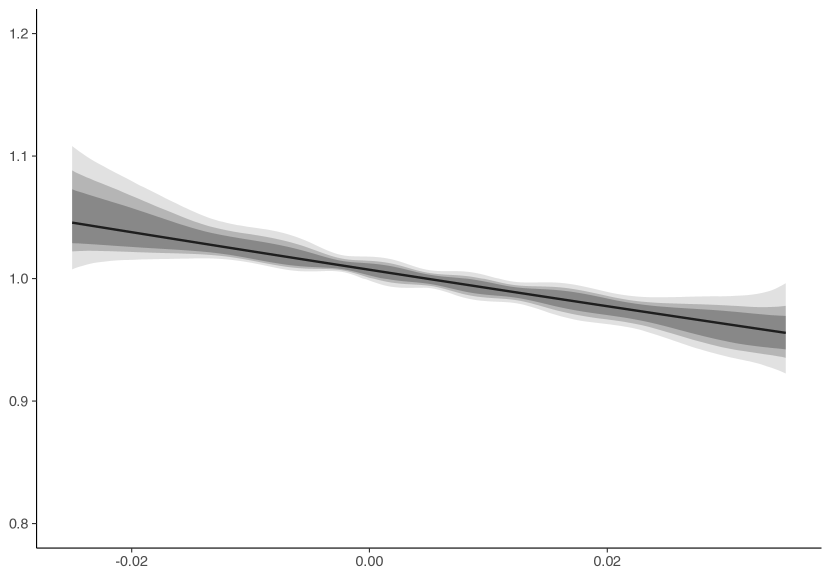

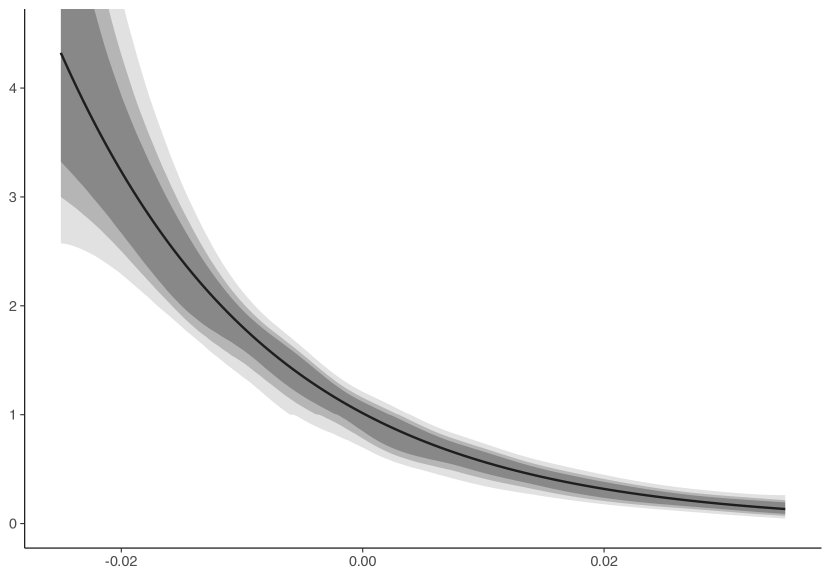

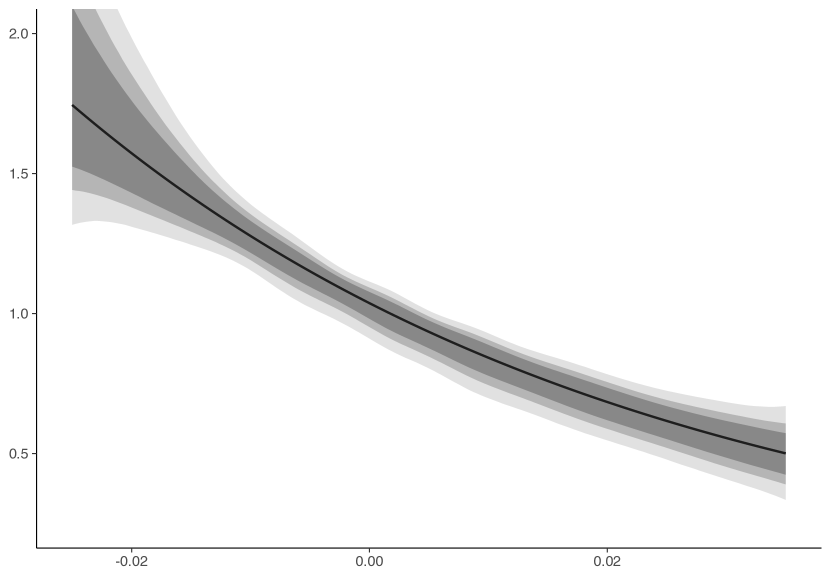

To understand further the long-run pricing implications of the estimates of , and , Figures 3(a)–3(d) plot the estimated and under recursive preferences for both the bivariate and univariate state specifications. It is evident from the vertical scales in Figures 3(a) and 3(b) that both estimates of are relatively flat, which explains the small transitory component obtained with recursive preferences. However, the estimated has a pronounced downward slope in . The estimated in the bivariate specification is also downward-sloping in at low levels of consumption growth. Recall that Proposition 2.1 shows that is the Radon-Nikodym derivative of with respect to . Figures 3(e)–3(f) plot the estimated change of measure for the two specifications of the state process. As the estimate of is relatively flat, the estimated change of measure is characterized largely by . In the bivariate case, the distribution assigns relatively more mass to regions of the state space in which there is low dividend and consumption growth than the stationary distribution , and relatively less mass to regions with high consumption growth.

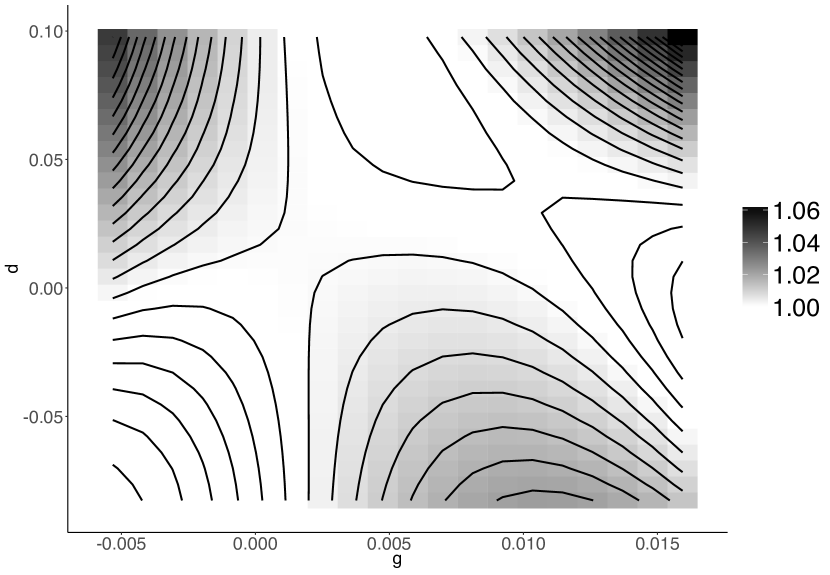

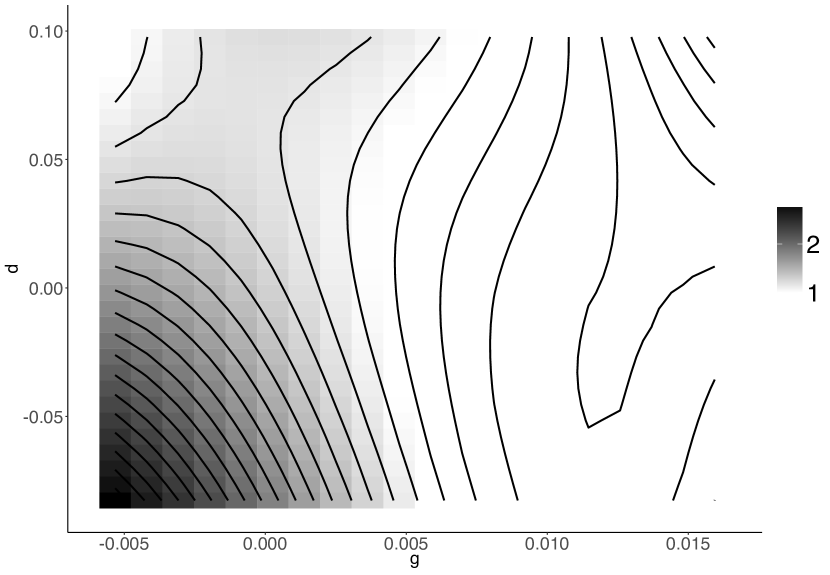

Finally, we investigate the role of nonlinearities and non-Gaussianity in explaining certain features of the long-end of the term structure. Figure 4 presents nonparametric estimates of (a) the (quarterly) long-run yield and (b) the correlation between the logarithm of the permanent and transitory components, namely and , recovered from the data on with and increased from to . The nonparametric estimates are presented alongside estimates for two parametric specifications of the state process. The first assumes is a Gaussian VAR(1), i.e. where the are i.i.d. . The second is a Gaussian AR(1) for log consumption growth with stochastic volatility:

where is a first-order autoregressive gamma process (a discrete-time version of the Feller square-root process; see GourierouxJasiak2006) so the state vector is . We refer to the second specification as SV-AR(1). The long-run yield and the correlation between and were obtained analytically as functions of , , and the estimates of the VAR(1) and SV-AR(1) parameters.141414The VAR(1) parameters are estimated by OLS. The SV-AR(1) parameters are estimated via indirect inference using an AR(1) with GARCH(1,1) errors as an auxiliary model. Derivations and further details on estimation are in the supplementary material.

Figure 4(a) shows that the nonparametric estimates of the long-run yield are non-monotontic, whereas the parametric estimates are monotonically decreasing. This non-monotonicity is not apparent in the nonparametric estimates using . It is also clear that the nonparametric estimates of the long-run yield are much larger for high than the SV-AR(1) model.

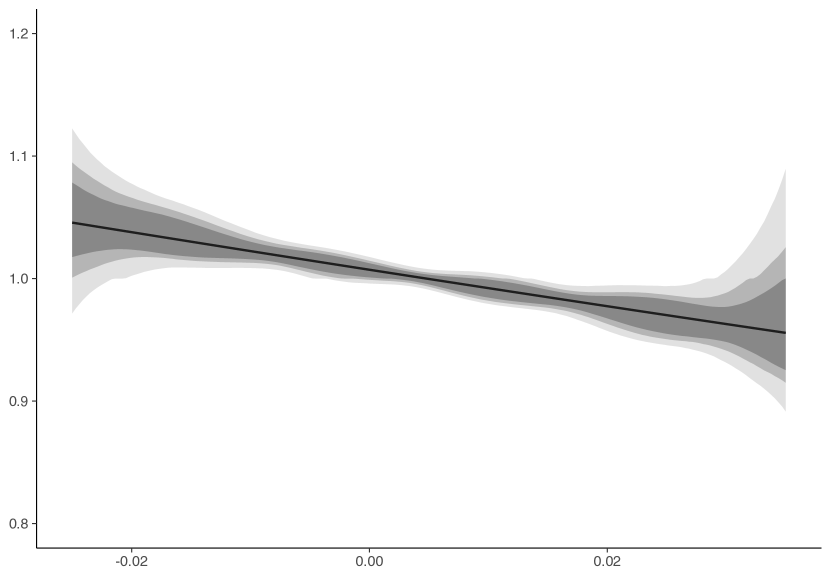

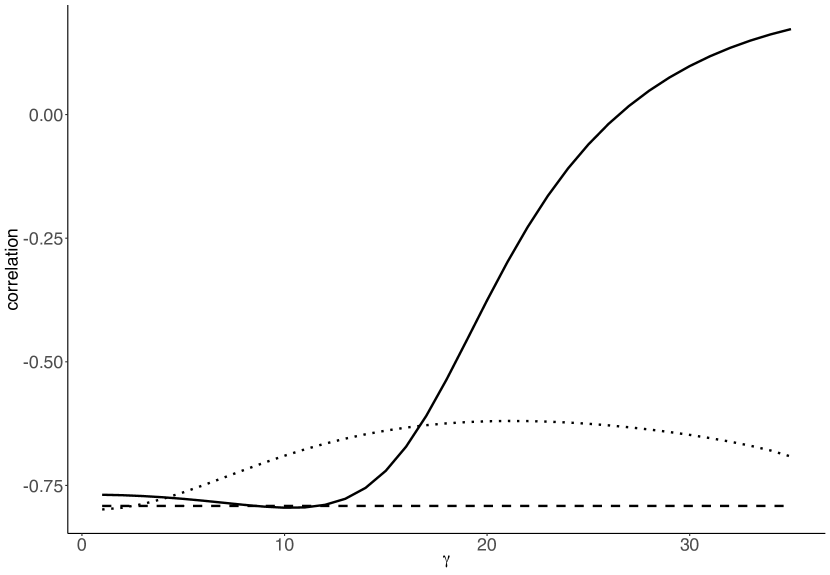

Figure 4(b) displays the sample correlation of the nonparametric estimates and of the log permanent and transitory component series for different values of . This is compared with the correlation of the log permanent and transitory components and for the two parametric state process specifications. The estimated correlation of the nonparametric estimates is negative for low to moderate values of , but becomes positive for larger values of . Similar results are obtained using lower- and higher-dimensional bases. In contrast, the correlations for the parametric state process specifications are around the same level as the nonparametric estimates for low values of but remain negative for larger values of . A recent literature has emphasized the role of positive dependence between the permanent and transitory components in explaining excess returns of long-term bonds (BakshiChabiYo; BC-YG; BC-YG:rec). Positive dependence also features in models in which the term structure of risk prices is downward sloping (see the example presented in section 7.2 in BorovickaHansen). However, positive dependence is known to be difficult to generate via conventional preference specifications in workhorse models with exponentially-affine dynamics. Although the correlation is estimated imprecisely for large values of , this finding at least suggests that nonlinearities in state dynamics may have a role to play in explaining salient features of the long end of the yield curve.

7 Conclusion

This paper introduces an empirical framework to analyze the permanent and transitory components of SDF processes in the long-run factorization of AJ, HS2009, and Hansen2012. We show how to estimate nonparametrically the solution to the Perron-Frobenius eigenfunction problem of HS2009 from time-series data on state variables and a SDF process. Our empirical framework allows researchers to (i) recover the time series of the estimated permanent and transitory components and investigate their properties and (ii) estimate the yield and the change of measure which characterize pricing over long investment horizons. This represents a useful contribution relative to existing empirical works which have established bounds on various moments of the permanent and transitory components as functions of asset returns, but have not extracted the components directly from data. The methodology is nonparametric in that it does not impose tight parametric restrictions on the dynamics of the state variables or the joint distribution of the state variables and the SDF process.

The main theoretical contributions of the paper are as follows. First, we establish consistency and convergence rates of the Perron-Frobenius eigenfunction estimators. Second, we establish asymptotic normality and some efficiency properties of the eigenvalue estimator and estimators of related functionals. Third, we introduce nonparametric estimators of the continuation value function in a class of models with recursive preferences by reinterpreting the value function recursion as a nonlinear Perron-Frobenius problem and we establish consistency and convergence rates of the value function estimators.

The econometric methodology may be extended and applied in several different ways. First, the methodology can be applied to study more general multiplicative functional processes such as the valuation and stochastic growth processes in HansenHeatonLi, HS2009, and Hansen2012. Second, the methodology can be applied to models with latent state variables. The main consistency and convergence rate results (Theorems 3.1 and 4.1) are sufficiently general that they apply equally to such cases. Finally, our analysis was conducted within the context of structural models in which the SDF process was linked tightly to preferences. A further extension would be to apply the methodology to SDF processes which are extracted flexibly from panels of asset returns data.

Appendix A Additional results on estimation

A.1 Bias and variance calculations for Theorem 3.1

The results in this subsection draw heavily on arguments from Gobetetal. The first result shows that the approximate solutions , and from the eigenvector problem (15) are well defined and unique (i.e. up to sign and scale normalization) for all sufficiently large.

Lemma A.1

Lemma A.2

The following result shows that the solutions , and to the sample eigenvector problem (16) are well defined and unique with probability approaching one (wpa1).

Lemma A.3

A.2 Bias and variance calculations for Theorem 4.1

The following two Lemmas apply known results from the literature on the solution of nonlinear equations by projection methods (see, e.g., Chapter 19 of Kras). The first result shows that is well defined for all sufficiently large.

Lemma A.5

Remark A.1

Remark A.2

In view of Remark A.1, in what follows we let be any one of the solutions to (33) in (or the unique solution under the additional assumption of continuous Fréchet differentiability of at ). Let and .

We now show that, wpa1, the sample fixed-point problem has a solution for which belongs to . We then derive convergence rates of the estimators formed using (see display (36)). The following two results are new.

Lemma A.7

Remark A.3

Although there may exist multiple fixed points of for which belongs to , under the conditions of Lemma A.7 we have that where denotes the set of all such belonging to .

Appendix B Additional results on inference

B.1 Asymptotic normality of long-run entropy estimators

Here we consider the asymptotic distribution of the estimator of the entropy of the permanent component of the SDF. In Case 1, the estimator of the long-run entropy is:

Recall that where the influence function is defined in (25). Define:

set . Let .

Proposition B.1

In the preceding proposition, will be the long-run variance:

where . Theorem B.1 below shows that is the semiparametric efficiency bound for .

In Case 2, the estimator of the long-run entropy is:

As with asymptotic normality of , the asymptotic distribution of will depend on the manner in which was estimated. For brevity, we just consider the parametric case studied in Theorem 3.4. Let and be as previously defined with . Recall from Assumption 3.5 and define:

Proposition B.2

Let the assumptions of Theorem 3.4 hold. Also let (a) there exist a neighborhood of upon which the function is continuously differentiable in for all with:

and (b) for some finite matrix . Then:

where .

B.2 Semiparametric efficiency bounds in Case 1

Let denote the -step transition probability of for any Borel set . We say that is uniformly ergodic if:

where denotes total variation norm and denotes the stationary distribution of .

Assumption B.1

is uniformly ergodic.

B.3 Sieve perturbation expansion

The following result shows that behaves as a linear functional of and is used to derive the asymptotic distribution of in Theorem 3.2. It follows from Assumption 3.3 that we can choose sequences of positive constants and such that:

with and as . Let and be normalized so that and (equivalent to and ).

References

Supplement to “Nonparametric Stochastic Discount Factor Decomposition”

Timothy M. Christensen

This supplementary material contains sufficient conditions for several assumptions in Sections 3 and 4 and proofs of all results in the main text.

Appendix C Some sufficient conditions

This appendix presents sufficient conditions for Assumptions 3.3, 3.4(b) and 4.3 and bounds for the terms and in display (23) and in display (37). Proofs of results in this appendix are contained in the Online Appendix.

C.1 Sufficient conditions for Assumptions 3.3 and 3.4(b)

We assume that the state process is either beta-mixing or rho-mixing. The beta-mixing coefficient between two -algebras and is:

with the supremum taken over all -measurable finite partitions and -measurable finite partitions . The beta-mixing coefficients of are defined as:

We say that is exponentially beta-mixing if for some . The rho-mixing coefficients of are defined as:

We say that is exponentially rho-mixing if for some .

We use the sequence to bound convergence rates. When has bounded rectangular support and has a density that is bounded away from and , is known to be for (tensor-product) spline, cosine, and certain wavelet bases and for (tensor-product) polynomial series (Newey1997; ChenChristensen-reg). It is also possible to derive alternative sufficient conditions in terms of higher moments of (instead of ) by extending arguments in Hansen2015WP to accommodate weakly-dependent data and asymmetric matrices.

C.1.1 Sufficient conditions in Case 1

The first result below uses an exponential inequality for weakly-dependent random matrices from ChenChristensen-reg. The second extends arguments from Gobetetal.

Lemma C.1

C.1.2 Sufficient conditions in Case 2 with parametric first-stage

The following lemma presents one set of sufficient conditions for Assumption 3.3 and 3.4(b) when is a finite-dimensional parameter.

Lemma C.3

The conditions on and bounds for and are the same as Lemma C.1. Therefore, here first-stage estimation of does not reduce the convergence rates of and relative to Case 1.

C.1.3 Sufficient conditions in Case 2 with semi/nonparametric first-stage

We now present one set of sufficient conditions for Assumptions 3.3 and 3.4(b) when is an infinite-dimensional parameter and the parameter space is (a Banach space) equipped with a norm . This includes the case in which is a function, i.e. with a function space, and the case in which consists of both finite-dimensional and function parts, i.e. with where .

For each we define as the operator with the understanding that . Let . We say has an envelope function if there exists some measurable such that for every and . Let . The functions in are clearly bounded by . Let denote the entropy with bracketing of with respect to the norm . Finally, let and observe that .

Lemma C.4

Note that the condition is trivially satisfied when .

C.2 Sufficient conditions for Assumption 4.3

The following is one set of sufficient conditions for Assumption 4.3 assuming beta-mixing. Recall that .

Appendix D Proofs of results in the main text

Notation: For , define:

or equivalently . For any matrix we define:

We also define the inner product weighted by , namely . The inner product and its norm are germane for studying convergence of the matrix estimators, as is isometrically isomorphic to . The notation for two positive sequences and means that there exists a finite positive constant such that for all sufficiently large; means and .

D.1 Proofs of results in Sections 2, 3 and 4

Proof of Proposition 2.1. Theorem V.6.6 of Schaefer1974 implies, in view of Assumption 2.1, that and that has a unique positive eigenfunction corresponding to . Applying the result to in place of guarantees existence of . This proves part (a). Theorem V.6.6 of Schaefer1974 also implies that is isolated and the largest eigenvalue of . Theorem V.5.2(iii) of Schaefer1974, in turn, implies that is simple, completing the proof of part (c). Theorem V.5.2(iv) of Schaefer1974 implies that is the unique positive solution to (6). The same result applied to in place of guarantees uniqueness of , proving part (b). Part (d) follows from Proposition F.3.

Proof of Corollary 3.1. We first verify Assumption 3.2. By Theorem 12.8 of Schumaker2007 and (ii)–(iv), for each there exists a such that:

Therefore,

and so as required.

Similar arguments yield and .

By Lemma C.2, conditions (iv)–(vii) are sufficient for Assumption 3.3 and we may take . Choosing balances bias and variance terms and we obtain the convergence rates as stated.

Proof of Remark 3.1. First observe that . Taking the inner product of both sides of with , we obtain for each . By Parseval’s identity, . Similarly, . Note that and if .

As spans the linear subspace in generated by , we have . Therefore, assuming (else the result is trivially true):

It follows that:

A similar argument gives .

Before proving Theorem 3.2 we first present a lemma that controls higher-order bias terms involving and . Define:

with and normalized so that and , and:

where is from display (25).

To simplify notation, let , , and .

Proof of Lemma D.1. First write

By iterated expectations:

using Cauchy-Schwarz, boundedness of (Assumption 3.1) and Lemma A.2 (note that the normalization and instead of and do not affect the conclusions of Lemma A.2). Markov’s inequality then implies . Similarly,

and so .

Since by Lemma A.2(a) and follows from Lemma A.2(b)(c), we obtain . Finally,

again by Cauchy-Schwarz and Lemma A.2. Therefore, .

Proof of Theorem 3.2. First note that:

| (S.1) |

where the second line is by Assumption 3.4(a) and the third line is by Lemma B.1 and Assumption 3.4(b) (under the normalizations and ). By identity, we may write the first term on the right-hand side of display (S.1) as:

| (S.2) |

where the second line is by Lemma D.1 and Assumption 3.4(a). The result follows by substituting (S.2) into (S.1) and applying a CLT for stationary and ergodic martingale differences (e.g. Billingsley1961), which is valid in view of Assumption 3.4(c).

Proof of Theorem 3.4. Let . By Assumption 3.4(a), Lemma B.1 and Assumption 3.4(b):

| (S.3) |

where the second equality is by Lemma D.1.

We decompose the second term on the right-hand side of (S.3) as:

| (S.4) |