Upper expectation parametric regression111 The research was supported by NNSF projects (11171188, 11071145, 11221061 and 11231005) and the 111 project (B12023) of China, NSF and SRRF projects (ZR2010AZ001 and BS2011SF006) of Shandong Province of China, and a grant from the University Grants Council of Hong Kong.

Abstract

Every observation may follow a distribution that is randomly selected in a class of distributions. It is called the distribution uncertainty. This is a fact acknowledged in some research fields such as financial risk measure. Thus, the classical expectation is not identifiable in general. In this paper, a distribution uncertainty is defined, and then an upper expectation regression is proposed, which can describe the relationship between extreme events and relevant covariates under the framework of distribution uncertainty. As there are no classical methods available to estimate the parameters in the upper expectation regression, a two-step penalized maximum least squares procedure is proposed to estimate the mean function and the upper expectation of the error. The resulting estimators are consistent and asymptotically normal in a certain sense. Simulation studies and a real data example are conducted to show that the classical least squares estimation does not work and the penalized maximum least squares performs well.

Key words: Distribution uncertainty, nonlinear expectation, penalized least squares, regression, upper expectation.

Running head: Upper expectation regression.

1 Introduction

Suppose that a sample is available in which the observations are independent. Consider the parametric regression model:

| (1.1) |

where ’s are the scalar response variables, ’s are the associated -dimensional covariate with a probability density . The parameters of interest are and the variances of the error. Under the independent identically distributed case (IID), the observations follow a common distribution, the errors ’s then follow a common distribution as well. The estimation and inference about and related parameters have been maturely studied, and the estimation consistency and asymptotic normality have been derived in the literature.

However, there are some more complicated scenarios. The IID property may be violated. Heteroscedasticity is one of the scenarios. A more serious problem is that several factors affect the observations we are obtaining and some of them are often latent, unobservable or at least unobserved. We call them the latent factors throughout this paper. Very often, we can not determine exactly how these uncontrolled impacts make the distributions of the observations different. Thus, the resulting model structure would be more complicated than the classical heteroscedasticity. In this paper, we investigate a more general problem: the distribution of involved random variable is an element that is randomly selected from a class of distributions, say . In this sense, all of the elements in can be seen as possible scenarios in the presence of uncertainty. More specifically, every element can be regarded as a “conditional” distribution when latent affecting factor is given, where is a set of latent factors. This is called the distribution uncertainty that has been acknowledged in some scientific fields. We will give a formal definition of distribution uncertainty in the next section. Another relevant methodology is Bayesian statistics, under which the parameter in the distribution is also regarded as a random variable following a prior distribution. However, observations are all with the same parameter value, that is, when the parameter is given, observations are IID. Whereas in distribution uncertainty case, every observation is related to a value of the parameter randomly selected from , the IID property is usually impossible. A well-known example in mathematical finance and risk measure was raised by a University of Chicago economist Frank Knight (1921). He distinguished between economic risk and uncertainty through that example. The Knightian uncertainty named after him has then become a well-known notion. Other examples are as follows. People have a limited ability to determine their own subjective probabilities and might find that they can only provide an interval in which any element can be regarded as a possible probability measure; as an interval is compatible with a range of opinions, the analysis ought to be more convincing to a range of different people. Some other relevant researches include Nutz and Soner (2012) who discussed risk measures under volatility uncertainty, and the references therein. In probability theory field, Soner et al (2011b) studied quasi-sure stochastic analysis and Peng (2006) discussed nonlinear expectations and nonlinear Markov chains.

Thus, in this setting, each individual expectation is difficult to estimate from the sample because we do not know which the distribution every observation comes from, even this class of distributions only has finite elements. Under the distribution uncertainty, people often concern the upper expectation of that will be defined in (1.2). This upper expectation can describe some realistic situations. For instance, if is a measure of the risk of a financial product, the upper expectation regression can describe the relationship between the maximum risk and relevant factors in the sense of averaging. A further discussion on the practical application of this model is included in Section 5 via a real data analysis. We in this paper investigate estimation problems where the distributions of ’s belong to . At the population level, we consider the following upper expectation regression. Assume that follows a distribution randomly selected from in a certain sense that will be specified in Section 2. When is independent of , we have

| (1.2) |

where is the upper expectation of defined as

| (1.3) |

is the classical expectation with a distribution . This upper expectation model is educed from the model (1.1).

It is worth pointing out that the notion of upper expectation is in effect not new in different settings. It may be at least traced back to, if not earlier, Huber (1981, Chapter 10) in which the relevant topics are related to robust statistics. A non-IID scenario is caused by data contamination and thus every observation still has a fixed distribution, not randomly selected from a class. Thus, the scenario is different from the one we are investigating. In this paper, the primary target is consistently estimating the parameters and by the observations from the model (1.1) under the distribution uncertainty. The following problems have to be solved in any estimation procedure:

-

1)

Upper expectation estimability: The definition of upper expectation implies the basic feature of nonlinearity, or more precisely, the sub-additivity:

for any random variables and . Consequently, the sample mean when a sample is available cannot be guaranteed to converge to a fixed value such as the classical expectation in IID cases. For example, if the regression function in the model (1.1), then we want to consistently estimate the upper expectation of . By Law of Large Numbers (LLN) under sublinear expectation (Marinacci 2005, Peng 2008 and 2009), the sample mean of would only satisfy that with large probability,

where and are respectively the lower and upper expectation. It presents an obvious evidence that even under very simple models, existing methods have difficulty to consistently estimate the upper expectation . Thus, the estimation consistency is a very challenging issue under distribution uncertainty.

-

2)

Data availability: From problem 1) above, we need to explore the conditions and then select the data that can be used to estimate the parameters of interest. This raises the issue of data availability. First, intuitively, for any if holds or at least approximately holds in a certain sense, the corresponding observation could then be used for estimation purpose. Thus, we have to, under certain conditions, identify those observations. Second, a more embedded issue in point estimation is about data availability for different parameters of interest. For instance, the observations that can be used for estimating the mean function may not be feasible for estimating .

These problems have not yet been explored in the literature. The essential difficulties involved in these issues are all rooted in distribution uncertainty. The classical statistical methodologies such as the least squires and the maximum likelihood are no longer applicable and thus new method is highly demanded.

As a useful tool to describe distribution uncertainty, nonlinear expectation has been developed in the research field of probability theory. A relevant reference is Peng (1997) who introduced -expectation (small ) via backward stochastic differential equations. As its extension, -expectation (big ) and its related versions were proposed by Peng (2006) with -normal distribution as its special case. Related results about LLN and Central Limit Theorem (CLT, Peng, 2008 and 2009) were acquired. Other references include Denis and Martini (2006), Denis et al. (2011), Coquet et al. (2002), Peng (1999, 2004, 2005), Nutz (2013), Nutz and Handel(2013). These works offer us a useful foundation in upper expectation research.

In this paper, we consider the class contains finite members. A penalized maximum least squares (PMLS) is introduced and then a two-step estimation procedure is suggested. The key feature of this method is that for different parameters and in the model (1.2), this method can identify available data for estimation. The resulting estimators are consistent and asymptotically normal in a certain sense. Moreover, the PMLS offers a general estimation approach under the nonlinear expectation framework.

The rest parts of the paper are organized in the following way. In Section 2, the definition of distribution uncertainty is given, the upper expectation regression is reexamined and the motivation for an estimation procedure is discussed. Section 3 contains the methodology development, the asymptotic properties of the estimators, the tuning parameter selection and a related algorithm. The method is further extended in Section 4 to the case where the upper expectation can be attained by several distributions. As a special case, the estimator for the upper expectation is constructed in Section 4. Simulation studies and a real data example are presented in Section 5. The proofs of the theorems are given in Appendix.

2 Definition of distribution uncertainty and motivation

2.1 Definition of distribution uncertainty

For ease of exposition, we mainly consider the linear case; a brief discussion on the extension of the results to the nonlinear model (1.1) will be given at the end of Section 4. In the linear case, the regression function reduces to

| (2.1) |

with being a -dimensional vector of unknown parameters. What we know is that the distribution of belongs to a class so that every follows a distribution randomly selected from .

To recognize this distribution uncertainty, we give the following definition. Suppose that is a distribution class with a factor set such that On the sample space of , there is a probability measure such that is the distribution with respect to . The factor variable defined on follows the distribution .

Definition 2.1.

Let be a random variable whose distribution satisfies the following property. For any fixed , the distribution of is and is a latent variable following the distribution . We call the random variable having the distribution uncertainty in the class . Two random variables are called independent identically distributed under the above distribution uncertainty if they are independent and satisfy the above property.

This definition can be explained as follows. There is a latent (at least not observed), random factor(s) that has impact on the distribution of the random variable . is a stochastic process/random variable sequence. Consider the pair of random variables . The corresponding joint distribution is , where can be regarded as a conditional distribution of when is given. Because the rendomness of , is different from the random variable defined in the classical stochastic process. In the case above, the distribution of is uncertain within the class because of the randomness of . If were observable, the problem would reduce to the classical functional data framework where all observations were functional data. However, under the distribution uncertainty framework, this is not the case, what we can observe is just in which is latent (or not observed). Therefore, any element within the class could be the distribution of in the above random manner. Without notional confusion, we then simply write as throughout the rest of the paper. Thus, for a random variable function , the expectation is actually the conditional expectation with conditional density given above.

In the following, we mainly consider distribution uncertainty of the error term in model (1.1). In this case, the error is of distribution uncertainty as we have defined above. By (1.2) and (2.1), the upper expectation linear regression is defined as:

| (2.2) |

where . That is to say, the upper expectation is the maximum of conditional expectations over all . If we use the conditional expectation notation, we may regard the expectation as a conditional expectation if is regarded as the conditional distribution of when is given. Note that under the distribution uncertainty, the original model (1.1) has no a constant intercept term and every expectation of is not assumed to be zero. Distribution uncertainty causes the expectation is a function of the random factor of and is not always zero. Thus, we need to handle the upper expectation . On the other hand, there is no need to consider a constant intercept term as it is not identifiable. In model (2.2), the intercept is absorbed in .

To estimate and , we first suggest an estimation procedure at the population level. A natural objective function is the squared upper expectation loss:

| (2.3) |

We first analyze what is the minimizer of this loss over . Because and are independent and follows a certain distribution , it is easy to see that the true is the minimizer over all . For all , we check what can be the minimizer. When is the true value, it is easy to see that the above squared upper expectation loss is equal to

| (2.4) |

Suppose that there is a distribution or equivalently a factor such that the above supremum can be attained over all . That is to say, there exists a member such that

| (2.5) |

This is a commonly used assumption for identification, in spirit the same as that in Peng (2008 and 2009). Then, by the projection theory, it is easy to see that the minimizer of the loss over is , rather than . Therefore, we need a two-step procedure to estimate and consistently. First, use the above criterion to get and . As described above, the estimator of can be consistent, while the one of cannot. After being obtained, we then re-estimate to get the estimation consistency. In the following, for ease of presentation, let for a positive integer . Under this situation, follows a distribution with unknown probability mass for .

2.2 Motivation for estimating and

Recall that are independent observations from the model:

Because of distribution uncertainty, every realization has a distribution with the latent factor having the distribution . For given ’s, we have the linear expectations and variances . The expectations and variances are in effect the conditional ones when the latent random factor are given. We consider the following treatment to get the initial estimates of and .

For any given and , let be the ordered quantities of in descending order:

| (2.6) |

To construct an empirical version of , instead of using all ’s to get an overall average, only using those larger ’s would make it possible to achieve estimation consistency. The intuition is as follows. Note that is the upper expectation being achieved at the distribution . Although we do not know what is, we can understand that the relatively larger quantities should be close to this upper expectation. More particularly, it can be expected that there should exist a positive number such that most of , come from the distribution . For illustration, we consider a simple example:

Example. Suppose that , in which the density functions and , two uniform distribution densities. It can be seen that Let and be the samples of and , respectively. Denote the largest order statistic and the random event

Let for a constant number , and , where stands for the integer part of . Then

| (2.7) |

The proof for (2.7) will be given in Appendix. This example shows that in the mixing sample , most of the data that have larger values should come from when is large enough. It gives a clear evidence to ensure that there exists a number such that most of , come from the distribution . Based on the above observation, for constructing an empirical version of , the following partial sum seems to work:

| (2.8) |

By this intuition, an estimate of would be defined as the minimizer of the partial sum:

| (2.9) |

where and are respectively the parameter spaces of and .

However, the problem described here is rather more complicated. First, in the probability sense, there are data points that come from the distribution for some . As we do not know the value of , the integer is unknown in practice. Thus, we cannot have prior information on what elements in the set can be included in (2.8). How to identify such elements is the key for selecting available data such that the estimation consistency can be achieved. Second, more seriously, the consistency of to cannot automatically result in the consistency of to . This is because is to make the loss function possible to achieve the maximum, but the linear expectation may not be equal to the upper expectation of . This shows the complexity of the problem: for estimating different parameters, the corresponding available data sets may be different. In the next section, we will give the detail of a two-step estimation procedure.

3 Methodology and theoretical properties

3.1 First-step estimation of and

In the previous section, we have discussed the issue of sample size determination because we cannot use all of the data for estimating and . We now suggest a general method for data selection and parameter estimation simultaneously. To this end, we need to assume that the distribution exists.

According to the correspondence between the indices and via for , we decompose the index set into two subsets as and satisfying . More precisely,

| (3.1) |

Denote

Since the sums in are based on the original indices, instead of the ordered quantities , it can be showed that if most of , come from the distribution , then should be small enough. Moreover, we need the following condition:

-

C0.

The scatter plots of , are asymmetric.

Under this condition, we have that if most of , do not come from the distribution . Combining the observations above, we choose a tuning parameter and consider a constraint as , where depends on . If is given, the estimator of can be defined as

| (3.2) |

Because the expectation of is a decreasing function of , the ideal choice of is

The relation between and implies that the optimization problem (3.2) contains two tuning parameters and . By the Lagrange multiplier, the optimization problem (3.2) can be rewritten as

| (3.3) |

where is a tuning parameter, and the related tuning parameter is related to . Since is a decreasing function of , and is not small when the value of exceeds a certain amount, the above objective function is an approximate convex function of in a certain region. Also it can be directly verified that the above objective function is a convex function of and . As a result, the resulting estimator is a unique global solution of the above optimization problem.

However, depends on unknown expectations for . We need a consistent estimator to replace it. Let be the ordinary least squares estimator of based on all of the data . Denote

We then have the following conclusion.

Lemma 3.1.

Assume that ’s are independent of ’s and the variances of with distribution exist for all , then

where .

This lemma leads to that the optimization problem (3.3) is asymptotically equivalent to

| (3.4) |

Here replaces . For any given and , a choice of is

The above estimation method is called the penalized maximum least squares (PMLS). Under -normal distribution (see Peng 2006), it is a penalized maximum-maximum likelihood. The penalty used here is to control the difference between the second-order moments of the random variables and then to identify the available data set.

We now investigate the theoretical properties of the estimators of and in (3.1). Denote and suppose that there are only elements , in the set such that , do not come from . Let be the smallest set of that contains all the elements from the distribution . Suppose without loss of generality that when , only the last elements in the set do not come from . To get the asymptotic properties of the estimators defined above, we introduce the following conditions.

-

C1.

The intercept of the model (2.1) is zero, is independent of , is a positive definite matrix, and the variances of with distribution exist for all .

-

C2.

The distribution satisfying (2.5) is unique and the size of the sample from tends to infinity as .

-

C3.

for a constant .

-

C4.

In the case of , , for a constant , and , where .

For the above four conditions, we have the following explanations. The first two conditions in C1 are standard. Condition C2 is based on (2.4) and (2.5). This condition implies that the second-order moment condition for all . Based on this condition, we can judge whether the corresponding errors come from the same distribution . The use of the uniqueness assumption on in C2 is to get a simple estimation procedure. However, this uniqueness assumption may not be always true. Thus, it will be removed when an adjusted method is introduced in the next section. We need condition C3 to constrain the convergence rate at which tends to zero. The first two conditions in C4 are based on the fact that most of , come from the distribution (see Subsection 2.1). The two conditions give the range of when the penalized estimation is used. The third condition in C4 is also standard.

Denote , and We have the following theroem.

Theorem 3.1.

The proof of the theorem is given in Appendix. The key of the proof is to show that most of the elements in come from via the penalty in (3.1). The proof implies that the uniqueness assumption on is unnecessary. In the next section, the assumption can be removed via an additional penalty.

The theorem guarantees that the PMLS estimator is consistent and normally distributed asymptotically. However, the PMLS estimator is not always consistent because it tends to , rather than the true parameter . On the other hand, compared with the properties of parameter estimation in the case of classical nonlinear regression, here the variance is enlarged and the convergence rate is reduced to . This is mainly because of the variability of the error terms, which comes from distribution uncertainty.

3.2 Second-step estimator of

We now go to the second-step of the estimation to refine the estimator of to achieve the consistency. Similar to (2.4) and (2.5), suppose the following holds:

| (3.5) |

Let be the order statistics of in descending order Similar to the decomposition in (3.1), the index set is decomposed as . Then, by the same argument as used in the first-step estimation, the second-step estimator of is defined by

| (3.6) |

where

Here the tuning parameter may be different from that in (3.1), but also satisfies condition C3. As argued above, the objective function in (3.6) is a convex function of . The estimator of (3.6) is a PMLS estimator as well. Comparing with the estimation procedure in (3.1), the data set used here should be different from the data set used in (3.1).

Let be the size of the sample from . The following conditions are required to establish the estimation consistency for the second-step estimator of .

-

C5.

and as .

-

C6.

Condition C4 holds when the notations are replaced by the above accordingly.

Unlike C2, here the uniqueness assumption on is not required. It is because the penalty for in (3.6) can make sure that most of , have the common mean .

Theorem 3.2.

Under the conditions in Theorem 3.1, conditions C5 and C6, when satisfies the same condition of as given in condition C3, and and are not overlapped, then the second-step estimator in (3.6) satisfies

where and

with

The proof of the theorem is presented in Appendix. Here we need the constraint of non-overlapping between and only for the simplicity of proof and representation. This condition can be replaced by and can be further reduced to that the number of overlapping elements in these two sets and satisfies . After and being determined, the condition can be checked by the methods of testing distributions to be equal; the details are omitted here. By the theorem, the second-step PMLS estimator is consistent and normally distributed asymptotically.

3.3 A summary of the algorithm

The above estimation procedures involves four tuning parameters: , , and . These parameters can be chosen by the cross-validation that is similar to those used in variable selection for high-dimensional models (see, e.g., Fan and Li (2001)). Since the set of the tuning parameters contains and , the numbers of data used for constructing the estimators, the cross-validation used here should be somewhat different from that given in Fan and Li (2001). If the discrete function is approximated by a continuously differentiable one, and a prior distribution for is assumed, then, by the Bayesian information criterion (see Schwarz (1978)), the Bayesian cross-validations for and can be defined respectively as

where is the cross-validation criterion defined by Fan and Li (2001). The above Bayesian cross-validations do not depend on the prior distribution, and they are in fact the large-sample criteria beyond the Bayesian context. Combining the above estimation procedure with the cross-validation for tuning parameter selection, the whole algorithm can be summarized into the following steps:

Step 1. Initial estimator of . Let be an initial selection of , and be the order quantities of the original squared quantities in descending order. For each pair of the tuning parameters , the full data set is first divided at random into cross-validation training sets and test sets , , and then the initial estimator is obtained by the training set via (3.1).

Step 2. Selection of . Write and let be the order statistic of in the descending order. Define a Baysian cross-validation criterion as

We then get an estimator by minimizing .

Step 3. Final estimator of . With the selected estimator , we estimate as the first component of the following vector:

| (3.7) |

Step 4. Initial estimator of . With the estimator obtained above, and for each pair of the tuning parameters and the training set , we find the estimator by (3.6).

Step 5. Selection of . Write and let

be the order statistic of , satisfying . Define the Bayesian cross-validation criterion as

We then get an estimator by minimizing .

Step 6. Final estimator of . With the selected estimator , we estimate by

| (3.8) |

Alternatively, we can use instead of as the tuning parameter and together with the others to design the algorithm. As the method is similar to the above and thus the details are omitted.

4 Extension and discussion

It is known that there may be more than one distribution in that can attain the upper expectation. In this section we first recommend an extended method to remove the uniqueness assumption on in C2. It can be seen from the proof of Theorem 3.1 that the uniqueness assumption is only to guarantee that most of , have the same mean . Then the uniqueness assumption on the distributions can be removed. All we need to do in the data selection procedure is to identify the data that satisfy the first two order moment conditions: , have the same mean and the variance .

Let be the order statistics of , satisfying Similar to (3.1), for the index set , the decomposition is designed as . Write

The proof of Lemma 3.1 given in Appendix shows

Thus, we can use to measure the difference among the means , and then use

to control the difference among the means for all . Consequently, an improved estimator of is defined as the first component of the following solution:

| (4.1) | |||

where and are two tuning parameters. We now use two penalties and to make sure that the selected data satisfy the first and second order moment conditions. Here a possible choice of is

Without the uniqueness assumption on , the condition C2 is replaced by

-

C7.

The number of the errors satisfying the first two order moment conditions tends to infinity as .

Now we do not need the uniqueness assumption on the distribution, however, the size of the data set used here is usually smaller than that in the previous section. We have the following theorem.

Theorem 4.1.

The proof of the theorem is given in Appendix. As stated above, the uniqueness assumption on is removed from the estimation procedure at the cost that the convergence rate of the improved estimator can be slower than that of , but the asymptotic normality still holds.

Also we can use the second-step estimation procedure as given in the previous section to construct the consistent estimator for . Let be the order statistic of , satisfying Denoted by the decomposition of the index set as in (3.1). Then, by the same argument as used above, the second-step estimator of is defined by

| (4.2) |

where

Then, this second-step estimator is consistent. The following theorem states the result.

Theorem 4.2.

Under the conditions of Theorem 4.1, conditions C5 and C6, when satisfies condition C3 and and are not overlapped, then the second-step estimator in (4.2) satisfies

where , and are defined in the previous section.

The difficulty we are facing now is the computational complexity because there are five tuning parameters: , , , and . The computational steps are similar to those in the previous section. Because of the complexity, if we have the prior information on the uniqueness of the distribution , we prefer to use the method given in the previous section to construct the estimators.

We now discuss the special case of . In this case, the model is simplified as

| (4.3) |

We can see how the upper expectation is estimated consistently whereas existing result only derives as we mentioned in Section 1. Although the methods proposed above can be used, for this simple model, estimation can be much simpler. Let be the order statistics of with descending order . For the index set , we define the decomposition as as (3.1). Write

Then, the estimator for is defined by

| (4.4) |

where is a tuning parameter as well.

Let be the sample size from given in (3.5). We need the following simpler conditions than before:

-

C8.

The variances of exist for all .

-

C9.

as .

-

C10.

Condition C4 holds when the notations are replaced by the above accordingly.

Theorem 4.3.

Suppose that conditions C8-C10 hold. Then the PMLS estimator defined in (4.4) satisfies

Before ending this section, we briefly discuss how to extend the methods proposed above to the nonlinear regression function as the estimation procedure is almost the same. We thus omit the detail. But, as the least squares estimation requires the derivative of with respect to the parameter , we need to assume that

are the non-constant functions of . This condition is to guarantee the identifiability of the regression function . For example, in the regression model:

the parameter is unidentifiable as it cannot be separated out from .

5 Numerical studies

5.1 Simulation studies

In this subsection we examine the finite sample behaviors of the newly proposed estimators by simulation studies. To obtain thorough comparisons, in addition to the new PMLS estimator, we comprehensively consider several competitors such as the OLS estimators that ignore the distribution uncertainty. Mean squared error (MSE), prediction error (PE) and boxplots are used to evaluate the performances of the involved estimators and models. Also the simulation results for estimation bias are reported to emphasize the influence from distribution uncertainty, especially from expectation uncertainty. In the following, we design 4 experiments. The first experiment is to compare the PMLS with the overall average for estimating the upper expectation of , the second and third experiments are designed for examining the performances of PMLS and OLS when estimating the parameter and in simple linear and multiple linear models. The fourth experiment is used to investigate the usefulness of PMLS for prediction.

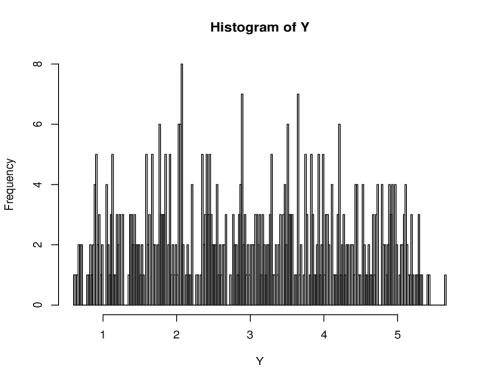

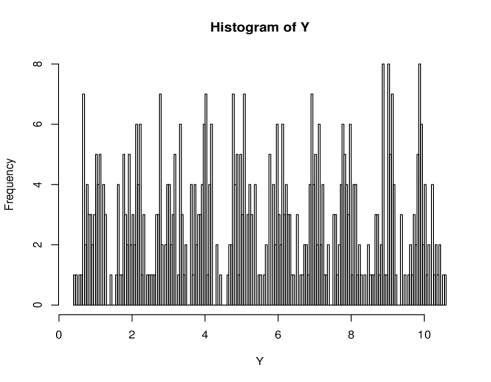

Experiment 1. Consider the simplest case with :

where are independent and follow the distributions in the class . In the following, we respectively consider two cases of distribution uncertainty:

-

Case 1. and is uniformly distributed on .

-

Case 2. and is uniformly distributed on .

For each , the size of the sample from is designed as .

Before performing the simulation, we first use the histograms of in the two cases to observe what pattern of the data appears to show distribution uncertainty. It is very clear from Figures 1 and 2 that the distributions in the two cases are multimodal although every distribution is unimodal. It shows that when we have a data set showing multimodal pattern, we may not simply believe the multimodality of an underlying distribution, distribution uncertainty would also be a possibility. Under this situation, the classical statistical inferences such as the estimation of population expectation, have less accuracy. Instead, our goal is to consistently estimate the upper expectation .

Figure 1 about here

Figure 2 about here

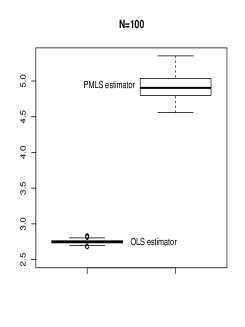

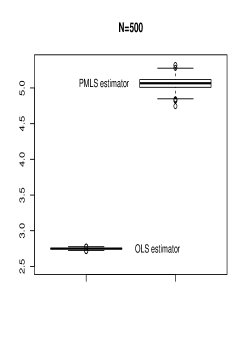

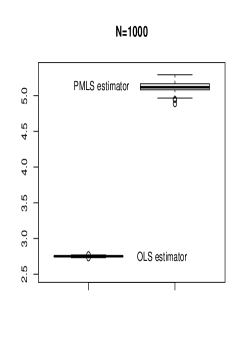

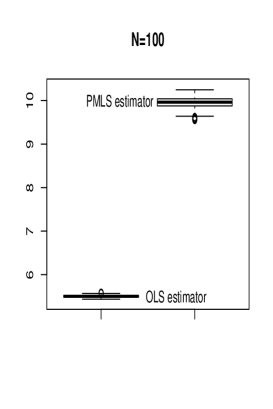

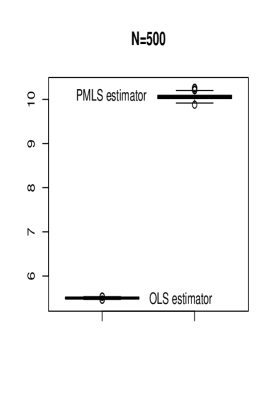

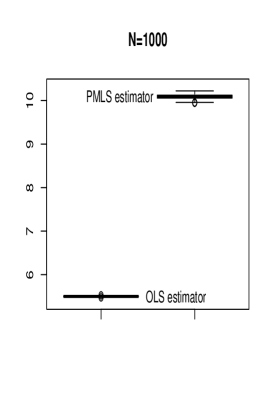

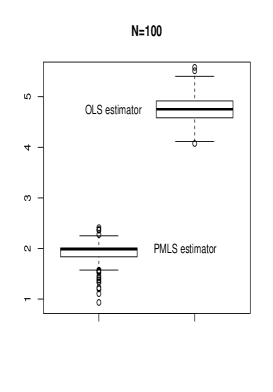

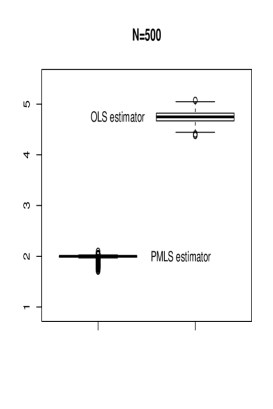

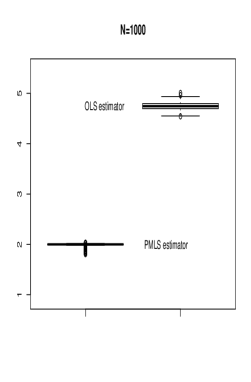

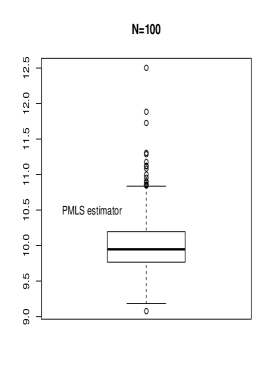

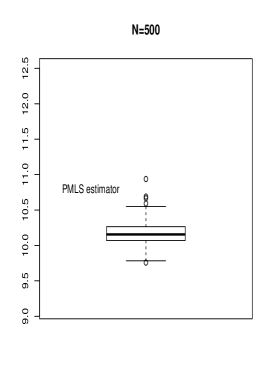

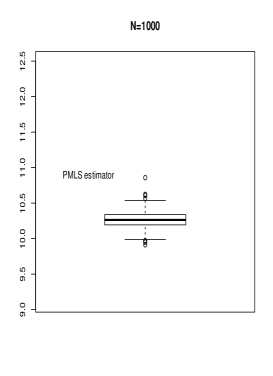

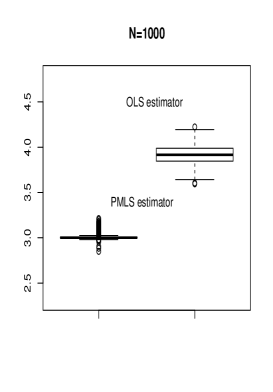

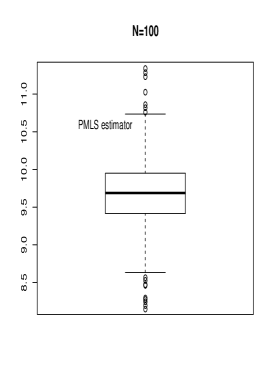

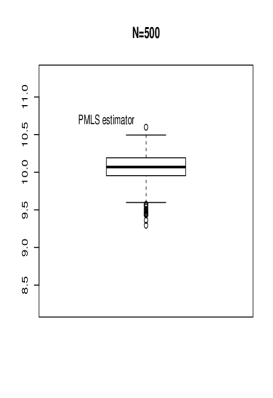

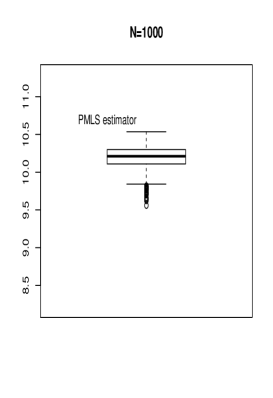

To examine the consequence of ignoring distribution uncertainty in estimation, we compare the PMLS estimator with the OLS estimator that is the overall average of all of observations in this experiment. In the simulation procedure, for each , the size of the sample from is designed as . For the total sample sizes and , the empirical bias and MSE, and the boxplots of the estimators with 500 replications are reported respectively in Tables 1 and 2, and Figures 3 and 4. Note that for this very simple model, we cannot have a constant intercept term because of distribution uncertainty. Therefore, theoretically, the intercept term for every observation is not identifiable, which is absorbed in the error term in the upper expectation of error term. The OLS estimator estimates nothing as its limit is in between, from the description in Section 1, the upper and lower expectation: with a probability going to one. The simulation results can verify that our PMLS estimator is clearly superior to the OLS estimator. More precisely, we have the following findings:

-

(1) From Tables 1 and 2, distribution uncertainty mainly results in the estimation bias of the OLS estimator, and the estimation bias almost obliterates the effect of variance in the MSE of the estimator. However, the uncertainty has no significant impact for the PMLS estimator for the upper expectation . The estimation bias of the PMLS estimator are very obviously smaller than those of the OLS estimator in both cases. The centerlines of the boxplots of the PMLS estimator are just located respectively at the true values 5 and 10 of the upper expectations. But the centerlines of the boxplots of the OLS estimator are far below the true values.

-

(2) From Figures 3 and 4, we can see that although the boxplots of the PMLS estimator are nearly centralized around the centerlines, the values have more dispersion than those of the OLS estimator, implying the new estimator has larger variance and a slow convergence rate. It is because the new method only uses a part of the data. However, this enlarged variance is negligible compared with the significant estimation bias of which the OLS estimator suffers.

Table 1 about here

Figure 3 about here

Table 2 about here

Figure 4 about here

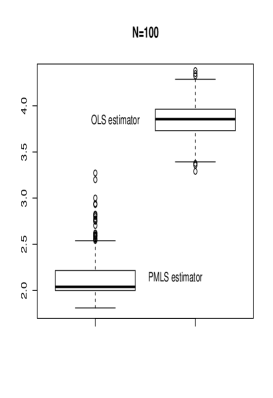

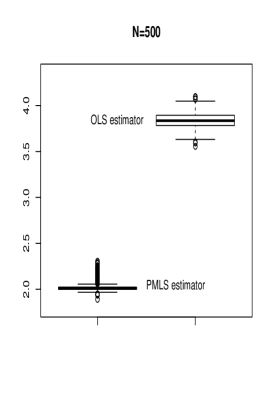

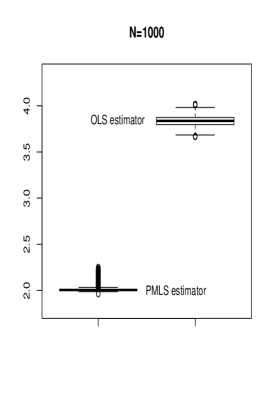

Experiment 2. Consider the following univariate linear regression:

where , are independent and identically distributed as . Suppose that are independent and follow the distributions in the class with . As we commented in Section 2, the model cannot contain a nonzero constant intercept term because even an intercept term is imposed, it is impossible to be identified and consistently estimated. The histograms of and the residuals derived from the OLS are multimodal to present distribution uncertainty (the histograms are not reported herewith for saving space).

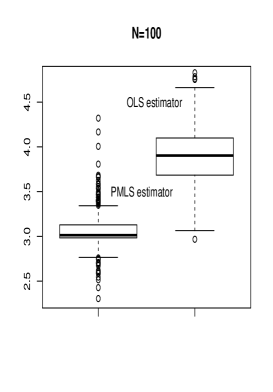

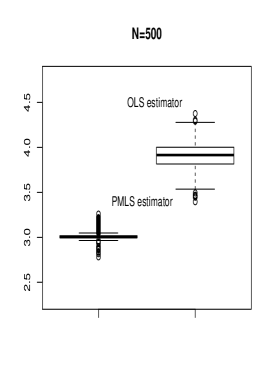

In the simulation, we set and let be uniformly distributed on . For each , the size of the sample from is designed as . For total sample sizes and , the empirical bias and MSE, and the boxplots of the estimators over 500 replications are reported respectively in Table 3, and Figures 5 and 6. Although the model used here is totally different from that in Experiment 1, a conclusion from the simulation results is similar to the finding (1) obtained in Experiment 1. That is to say, PMLS can accurately estimate the regression coefficient and the upper expectation of the error, while OLS gets the estimators that are far away from the true values. Unlike that in the finding (2) in Experiment 1, the variance of the OLS estimator is larger than that of the PMLS estimator in this experiment. The PMLS estimator of performs better than the PMLS estimator of with smaller bias and MSE particularly when the sample size is large. Perhaps it is because the two-step estimation procedure for introduces more estimation error.

We note that the OLS estimator has a significant bias. One may expect to centralize data to reduce the bias. As we explained before, for every observation, the center is a conditional expectation when is given, and such a center is actually a random variable because of the distribution uncertainty defined in Section 2. Thus, in theory, using the overall average of ’s as the center of every is not meaningful and it is also not estimable. On the other hand, in practice, when we use it as if distribution uncertainty did not exist, its practical performance can be promoted because is not centered. We now pretend that the observations do not have distribution uncertainty. If only ’s in the above regression are centered, it can be easily verified that, in this example,

which is also biased. If both ’ and ’ are centered, it can be seen that

The simulation result in Table 4 shows that when we blindly use OLS with centered data, the estimation efficiency does be promoted. However, even for the latter, the estimation bias is slightly larger than that of the PMLS estimator, and the MSE of the centered LS estimator is about 5 times of that of the the PMLS estimator although in the case without distribution uncertainty, the bias-reduction LS estimator should have a variance achieving Fisher information bound.

Table 3 about here

Figure 5 about here

Figure 6 about here

Table 4 about here

Experiment 3. Consider the multiple linear regression:

where , , and , the other settings are designed as those in Experiment 2. The simulation results are reported in Table 5 and Figures 7-9 and further indicate that the PMLS estimator is consistently superior to the OLS estimator in estimation bias, MSE and variance. Again we can see that OLS overestimates regression coefficients because the distribution uncertainty makes it impossible to remove the bias which is absorbed in the error terms. The effect of the overestimated regression coefficients by OLS is to compensate the loss of ignoring the positive error. Then, a new problem emerges naturally: Is OLS able to give a proper prediction? We discuss this issue in the following experiment.

Table 5 about here

Figure 7 about here

Figure 8 about here

Figure 9 about here

Experiment 4. The model and experiment conditions are completely identical to those in Experiment 3, but the purpose is to examine the prediction behavior. Before comparing the predictions derived by OLS and PMLS, we define the meaning of prediction under the situation with distribution uncertainty. Because the classical methods ignore distribution uncertainty, a natural prediction of based on OLS is given as

for a given predictor . However, the main goal of the upper expectation regression is to predict maximum values of conditional on predictor . Thus, under the framework of upper expectation regression, the prediction is defined by

where both and are the MPLS estimators proposed in the previous sections. On the other hand, if our goal is to predict all the values , not merely the maximum values, based on PMLS, a reasonable prediction is defined as

where is a suitable value in the interval . Here the estimator of the lower expectation of can be obtained by the similar argument proposed in the previous sections. If without additional information about expectation uncertainty of , we simply choose the middle point . It is worth pointing out that although the overall average of can also be between and , it does not converge to a fixed value under distribution uncertainty and thus, its use makes no theoretical ground.

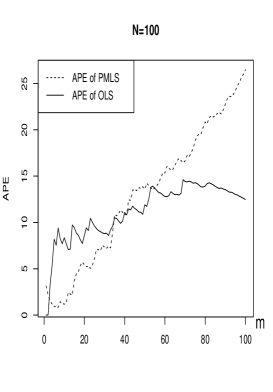

We first consider the performances of the predictions for some larger values of . For values , we rearrange them in descending order as

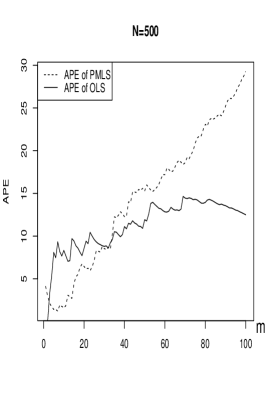

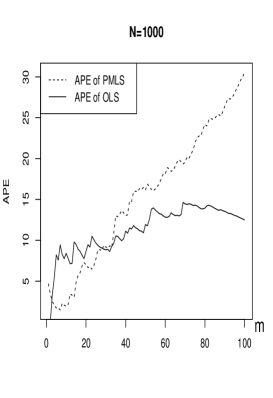

In this case, the average prediction error (APE) of predicting the first largest values of is defined by

where is a prediction value of . The simulation results are presented in Figure 10, in which the curves are the medians of APEs of 500 replications. It clearly shows that the upper expectation regression can relatively accurately predict the larger values of . More precisely, for 100 values of , the upper expectation regression gives relatively successful prediction for the first largest values of . However, if ignoring distribution uncertainty, the OLS-based prediction behaves poorly for predicting the larger values of .

Figure 10 about here

Finally, we investigate the behaviors of the predictions and for all the values of . The APEs of the two predictions are reported in Table 6. It is clear that the APE of is significantly smaller than that of . Because of distribution uncertainty, however, both the two predictions have relatively large APE even for large sample size. It shows that it is impossible to improve the predictions if without further information about the distribution of , in other words, we can not completely characterize the regression under the situation with distribution uncertainty.

Table 6 about here

5.2 Real data analysis

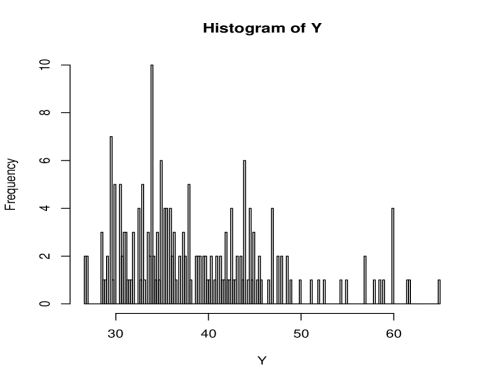

In this subsection we use a real data example to show how the upper expectation regression works under the setting with distribution uncertainty. We consider the data set of the Fifth National Bank of Springfield based on data from 1995 (see examples 11.3 and 11.4 in Albright et al., 1999). This data set has been analyzed such as Fan and Peng (2004) and Cui et al. (2013). The bank, whose name has since changed, was charged in court with paying its female employees substantially lower salaries than its male employees. For each of its 208 employees, the data set includes the following variables:

-

•

EduLev: education level, a categorical variable with categories 1 (finished high school), 2 (finished some college courses), 3 (obtained a bachelor s degree), 4 (took some graduate courses), 5 (obtained a graduate degree).

-

•

JobGrade: a categorical variable indicating the current job level, the possible levels being 1-6 (6 highest).

-

•

YrHired: year that an employee was hired.

-

•

YrBorn: year that an employee was born.

-

•

Gender: a categorical variable with values “Female” and “Male”.

-

•

YrsPrior: number of years of work experience at another bank prior to working at the Fifth National Bank.

-

•

PCJob: a dummy variable with value 1 if the empolyee’s current job is computer related and value 0 otherwise.

-

•

Salary: current (1995) annual salary in thousands of dollars.

Fan and Peng (2004) employed the linear model as

| (5.1) |

We first use histogram of salary to examine data distribution. We can see from Figure 11 that the histogram of Salary exhibits multimodality. We do not simply consider the error to have a multimodal distribution. This is because other factors, such as the years of working experience and the age of an employee, may affect the salary. Therefore, we regard these potential factors as latent factors in an upper expectation regression with distribution uncertainty. Consider the upper expectation linear model to fit the data:

| (5.2) |

It is worth pointing out that the differences from the model (5.1) are that the error in (5.2) is supposed to be of distribution uncertainty, and the model (5.2) does not have the intercept term, which is included in the upper expectation of .

Figure 11 about here

We use 170 data to estimate the model parameters and then use the obtained models to fit the rest of the data (to predict 38 values of “Salary”). The predictions and prediction errors are defined in Experiment 4. The results of parameter estimation and the APE are listed in Table 7. Compared with the OLS regression (5.1), the upper expectation regression (5.2) has the following interesting features:

-

(1)

The absolute values of the estimators of the coefficients of JobGrdi are significantly reduced, but the others, especially the coefficients of Gender and Edu2, are largened. We may explain these as follows. As JobGrdi may be related to the years of working experience and the age of the employee, when these factors are not included in model (5.1), the model requires larger coefficients of JobGrdi to draw the information of these factors. On the other hand, the effect of JobGrdi is absorbed into the error of model (5.2).

-

(2)

The difference of the APEs between the two models is not significant.

Table 7 about here

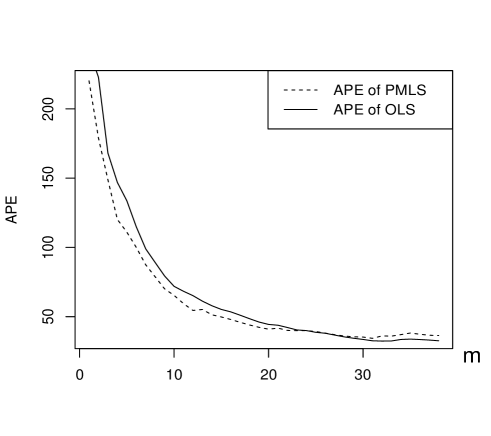

On the other hand, as shown in Experiment 4, the upper expectation regression is more concerned about the maximum information. Figure 13 presents the medians of the APEs for the largest values of “Salary” via 100 replications. From this figure, we can get the following finding:

-

(3)

The upper expectation regression can relatively accurately predict the larger values of “Salary”. For example, for the first 15 largest values of “Salary”, the APE of the upper expectation regression is 10.6892 smaller than that of the OLS regression; and for the first 24 largest values of of “Salary”, the APE of the upper expectation regression is 6.5338 smaller than that of the OLS regression.

Finally, we examine the values of the two models, which is defined by

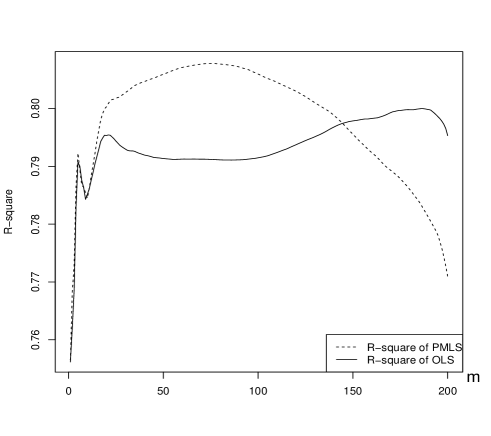

where with given in Experiment 4. We use the values of of the first largest values of “Salary” to check if the upper expectation regression can capture the maximum risk information. The result is reported in Figure 14. It indicates the following conclusion:

-

(4)

For the two models, most values of are larger than 0.79, while the upper expectation regression has a relatively high for the larger values of “Salary”.

All the numerical results aforementioned are coincident with the theoretical conclusions.

Figure 12 about here

Figure 13 about here

6 Appendix: Proofs

Proof of (2.7). It is clear that

By the definition of and a simple integral operation, we can get

It followings from this result and the stirling’s formula that

It can be verified that is a decreasing function of when is large enough. Then

Note that for . Then

implying the result of (2.7).

Proof of Lemma 3.1. For simplicity we only consider the case of and .

It can be easily proved that, under the assumption C1,

The result leads to

implying

Then, under model (2.1), if is independent of , then

where and

The relation above leads to the conclusion of the lemma.

Proof of Theorem 3.1. It can be see from Lemma 3.1 and (6.4) given below that for the asymptotic property of parameter estimation, the objective functions in (3.3) and (3.1) respectively have the following equivalent forms:

where is a parameter vector, is a positive definite matrix, is stochastically bounded and goes to zero in probability for each . Thus, by the basic corollary of Hjørt and Pollard (1993), we have that the objective functions in (3.3) and (3.1) are equivalent for parameter estimation with respect to asymptotic property. We thus only investigate the asymptotic properties of the estimator defined by (3.3).

For simplicity, here we only consider the case when is a even number: . Note that and are respectively decreasing and increasing functions of when exceeds . This leads to that the selected should satisfy . In this case, it can be verified that . Suppose without loss of generality that, for , only the last elements in the set do not come from , with being an even number: . Then,

By the treatments above, we have

By the above result and the condition C4, it is clear that if , then . If is diverging, then , implying . Note that is bounded and

Thus resulting in and . In this case, is diverging as well and, consequently, the minimum value of the objective function does not exist. We then need only to consider the objective function with for the asymptotic properties of the estimation.

Furthermore, because , the objective function can be further expressed as

| (6.1) |

Denoted by and the true values of and , respectively, and let and satisfy and . Because , we can assume , without loss of generality. Then, the objective function (6.1) can be replaced by

| (6.2) |

Because is free of and , the objective function in (6) is equivalent to

| (6.3) |

By the basic corollary of Hjørt and Pollard (1993), the term of order can be ignored for the asymptotic property of the estimation. We then rewrite the above objective function as

| (6.4) |

The objective function is obviously convex and is minimized at

Note that , are identically distributed with the common mean by the condition C2. It follows from the Lindeberg-Feller central limit theorem that

where . The convexity of the limiting objective function, , assures the uniqueness of the minimizer and consequently, that

(See, e.g., Pollard 1991, Hjørt and Pollard 1993, Knight 1998). Finally, we see and . Then the result follows.

Proof of Theorem 3.2. By the same argument as used in the proof of Theorem 3.1, can be replaced by the sample size . Let be the order statistic of , satisfying . Write the corresponding index decomposition as and let

It follows from Theorem 3.1 that . Denoted by and the true values of and , respectively, and let and satisfy and . Thus, the objective function in (3.6) can be expressed as

Note that and are independent, and depends only on . By the conclusion of Theorem 3.1 and the same argument as used in the proof of Theorem 3.1, we can prove the theorem.

Proofs of Theorem 4.1 - 4.3. The proofs are similar to that of Theorem 3.1.

References

- [1] Albright, S. C., Winston, W. L. & Zappe, C. J. (1999). Data analysis and decision making with Microsoft Excel. Duxbury, Pacific Grove, CA.

- [2] Coquet, F., Hu, Y., MT̂emin J. and Peng, S. (2002). Filtration-consistent nonlinear expectations and related -expectations. Probab. Theory Relat. Fields, 123, 1-27.

- [3] Cui, X., Peng, H., Wen, S. Q. and Zhu, L. X. (2013). Component selection in the additive regression model. Scand. J. Statist., 40, 491-509.

- [4] Denis, L. and Martini, C. (2006). A theoretical framework for the pricing of contingent claims in the presence of model uncertainty. The Ann. of Appl. Probability, 16(2), 827-852.

- [5] Denis, L., Hu, M. and Peng S. (2011). Function spaces and capacity related to a sublinear expectation: application to -Brownian motion pathes. Potential Anal., 34, 139-161.

- [6] Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. J Amer Statist Assoc, 96, 1348-1360.

- [7] Fan, J. and Peng, H. (2004). Nonconcave penalized likelihood with a diverging number of parameters. Ann. Statist., 32, 928-961.

- [8] Huber,P. J. (1981). Robust Statistics, John Wiley & Sons.

- [9] Hjørt, N. and D. Pollard (1993), Asymptotics for minimizers of convex processes. Statistical Research Report. http://www.stat.rutgers.edu/home/ztan/material/hjort-pollard-convex.pdf.

- [10] Knight, P. H. (1921). Risk, uncertainty and profit. Sentry Press, Kelly, Bookseller.

- [11] Knight, K. (1989). Limit theory for autoregressive-parameter estimates in an infinite-variance random walk. Canadian Journal of Statistics, 17, 261-278.

- [12] Lam, C. & Fan, J. (2008). Profile-kernel likelihood inference with diverging number of parameters. Ann. Statist., 36, 2232-2260.

- [13] Marinacci, M. (2005). A strong law of large number for capacities. Ann. Proba., 33, 1171-1178.

- [14] Nutz, M. and Soner, HM. (2012). Superhedging and dynamic risk measures under volatility uncertainty. SIAM Journal on Control and Optimization, 50, 2065-2089 .

- [15] Nutz, M. (2013). Random -expectations. Ann. Appl. Probab. 23, 1755-1777.

- [16] Nutz, M. and van Handel, R. (2013). Constructing sublinear expectations on path space. Stochastic processes and their applications, 123, 3100-3121.

- [17] Peng, S. (1997). Backward SDE and related -expectations, in Backward Stochastic Differential Equations, Pitman Research Notes in Math. Series, No.364, El Karoui Mazliak edit. 141-159.

- [18] Peng, S. (1999). Monotonic limit theorem of BSDE and nonlinear decomposition theorem of Doob-Meyer s type. Prob. Theory Rel. Fields, 113(4), 473-499.

- [19] Peng, S. (2004). Filtration consistent nonlinear expectations and evaluations of contingent claims. Acta Mathematicae Applicatae Sinica. English Series 20(2), 1-24.

- [20] Peng, S. (2005). Nonlinear expectations and nonlinear Markov chains, Chin. Ann. Math., 26B(2), 159-184.

- [21] Peng, S. (2006). -Expectation, -Brownian Motion and Related Stochastic Calculus of Itô s type, The Abel Symposium 2005, Abel Symposia 2, Edit. Benth et. al., 541-567, Springer-Verlag, 2006.

- [22] Peng, S. (2008). Multi-dimensional -Brownian motion and related stochastic calculus under G-expectation. Stochastic Processes and their Applications, 118(12), 2223-2253.

- [23] Peng, S. (2009). Survey on normal distributions, central limit theorem, Brownian motion and the related stochastic calculus under sublinear expectations. Science in China Series A: Mathematics, 52, 7, 1391-1411.

- [24] Pollard, D. (1991). Asymptotics for least absolute deviation regression Estimators. Econometric Theory, 7, 186-199.

- [25] Schwarz, G. (1978). Estimating the dimension of a model. Ann. Statist., 6, 461-464.

- [26] Soner M. Touzi N, Zhang J. (2011). Quasi-sure stochastic analysis through aggregation. Electronic Journal of Probability, 16, 1844-1879.

- [27] Zhang, C. M. (2008). Prediction error estimation under bregman divergence for non-parametric regression and classification. Scand. J. Statist., 35, 496-523.

|

|

| 100 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|

| criterions | Bias | MSE | Bias | MSE | Bias | MSE |

| PMLS | 0.0319 | 0.0113 | 0.1210 | 0.0187 | ||

| OLS | 5.0707 | 5.0631 | 5.0595 |

|

|

|

| 100 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|

| criterions | Bias | MSE | Bias | MSE | Bias | MSE |

| PMLS | 0.0157 | 0.0062 | 0.0920 | 0.0108 | ||

| OLS | 20.2330 | 20.2497 | 20.2509 |

|

|

|

| parameters | 100 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|

| criterions | Bias | MSE | Bias | MSE | Bias | MSE | |

| PMLS | 0.03101 | 0.00341 | 0.00063 | ||||

| OLS | 7.66282 | 7.55041 | 7.56090 | ||||

| PMLS | 0.13711 | 0.05203 | 0.26512 | 0.08386 |

| only ’s centralized | both ’ and ’s centralized | |||

| Bias | MSE | Bias | MSE | |

| 0.01568506 |

|

|

|

|

|

|

| parameters | 100 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|

| criterions | Bias | MSE | Bias | MSE | Bias | MSE | |

| PMLS | 0.03646 | 0.00362 | 0.00169 | ||||

| OLS | 0.92334 | 0.85260 | 0.84461 | ||||

| PMLS | 0.05200 | 0.00495 | 0.00282 | ||||

| OLS | 3.45390 | 3.38013 | 3.37050 | ||||

| PMLS | 0.34478 | 0.04601 | 0.18741 | 0.06053 |

|

|

|

|

|

|

|

|

|

|

|

|

| 100 | 500 | 1000 | |

|---|---|---|---|

| PMLS | 8.498254 | 8.489735 | 8.495854 |

| OLS | 12.47704 | 12.49915 | 12.49017 |

|

| parameters | OLS | PMLS |

|---|---|---|

| (Gender) | ||

| (PCJob) | 4.532 | 5.0824 |

| (Edu1) | 1.523 | 1.969 |

| (Edu2) | 0.086 | 0.474 |

| (Edu3) | 0.387 | |

| (Edu4) | ||

| (JobGrd1) | ||

| (JobGrd2) | ||

| (JobGrd3) | ||

| (JobGrd4) | ||

| (JobGrd5) | ||

| – | 68.832 | |

| – | 63.628 | |

| (Intercept) | 68.814 | – |

| APE | 32.615 | 32.544 |

|

|