BayesDccGarch - An Implementation of Multivariate GARCH DCC Models

Abstract

Multivariate GARCH models are important tools to describe the dynamics

of multivariate times series of financial returns.

Nevertheless, these models have been much less used in practice due to

the lack of reliable software.

This paper describes the R package BayesDccGarch which was

developed to implement recently proposed inference procedures to

estimate and compare multivariate GARCH models allowing for asymmetric

and heavy tailed distributions.

Key words: GARCH, dynamic conditional correlations, MCMC.

1 Introduction

Modelling the dynamics of financial returns has been object of much attention and extensively researched for decades since the introduction of the Autoregressive Conditional Heteroskedasticity (ARCH) model in the seminal work of \citeNengle82 and its generalization, the GARCH model of \citeNboll86. However, when dealing with multivariate returns, one must take into account the mutual dependence between them. For example, the dependence between assets tends to increase in periods of market turbulence which in turn might have implications for portfolio and risk management. Analyzing asset return covariances is crucial to portfolio selection, asset management and risk assessment.

It is therefore natural to extend to multivariate GARCH (MGARCH) models and this is the main focus of this paper. For recent reviews on multivariate GARCH models see for example \shortciteNbaulr06, \citeNsil-tera09 and \citeNtsay10. It is important that the model is flexible enough to be able to capture the dynamics in the conditional variances and covariances and yet parsimonious enough so that parameter estimation does not come at a high computational cost. In this paper, we focus on the so called conditional correlation models which allow to specify separately the individual conditional variances and the conditional correlation matrix. In this specification it is straightforward to impose positive definiteness in the conditional variance covariance matrix using some simple constraints.

The fact that the distribution of financial returns are typically characterized by fat tails and frequently show some degree of asymmetry should be taken into consideration too. To introduce some degree of asymmetry, \shortciteNcappuccio04 adopted a Bayesian approach to estimate stochastic volatility models with a skewed power exponential distribution while \citeNpipien06 and \citeNehl2012 compared GARCH models with different skewed distributions for the error terms. \citeNbaul05 proposed a new class of skew multivariate Student distributions and parameter estimation was based on (quasi-) maximum likelihood methods. \shortciteNehl2014 adopted a similar modelling approach from a Bayesian perspective and included a skew multivariate GED distribution. \shortciteNausin14a proposed a Bayesian non-parametric approach with applications to portfolio selection.

We give an overview of multivariate GARCH models in Section 2 using both symmetric and skewed multivariate distributions. An overview of the package implementation and usage including illustration with real data is provided in Section 3. Finally Section 4 offers some conclusions and possible future steps in improving the implementation.

2 A Multivariate GARCH Model

Consider a multivariate time series of returns such that . The model assumes that is conditionally heteroskedastic,

| (1) |

where is any positive definite matrix such that the conditional variance of is and which depends on a finite vector of parameters . The error vectors are assumed independent and identically distributed with and , where is the identity matrix of order .

There are different possible specifications for . In this paper, we focus on the so called conditional correlation models which allow to specify separately the individual conditional variances and the conditional correlation matrix. \citeNboll90 proposed a parsimonious approach in which the conditional covariances are proportional to the product of the corresponding conditional standard deviations. The constant conditional correlation model is defined as, , where , is a symmetric positive definite matrix which elements are the conditional correlations , . Each conditional covariance is then given by . Besides, each conditional variance in is specified as a univariate GARCH model. Here we specify a GARCH(1,1) model for each conditional variance, i.e.

| (2) |

with , , and , . Note that this model contains parameters. It is clear that is positive definite if and only if and is positive definite.

engle02, \citeNchris02 and \citeNtse02 independently proposed generalizations by allowing the conditional correlation matrix to be time dependent. The resulting model is then called a dynamic conditional correlation (DCC) MGARCH model. We adopted the same approach in \citeNengle02 by setting the following parsimonious formulation for the correlation matrix,

| (3) |

where are symmetric positive-definite matrices given by,

| (4) |

are the standardized returns and is the unconditional covariance matrix of . Also, , and . After some algebra it is not difficult to see that the conditional covariances are given by . So, from (3) and (4) we can see that is written as a GARCH(1,1)-type equation and then transformed to give the correlation matrix .

2.1 Skewed Distributions

baul05 proposed to construct a multivariate skew distribution from a symmetric one by changing the scale on each side of the mode for each coordinate of the multivariate density. This is a multivariate extension of what \citeNfsteel98 had proposed as a skewing mechanism for univariate distributions. The density is given by,

| (5) |

where is a symmetric multivariate density, such that if and if , . The parameters control the degree of skewness on each margin, right (left) marginal skewness corresponding to (). Also, the existence of the moments of Equation (5) depends only on the existence of the marginal moments in the original symmetric distribution. The interpretation of each is the same as in \citeNfsteel98, i.e. which helps with the specification of a prior distribution. Besides the multivariate skew normal distribution we allow the error term to follow a multivariate skew or a multivariate skew GED as well. In all cases, setting , recovers the original symmetric density.

2.2 Prior Distributions

The model specification is completed specifying prior distributions of all parameters of interest. These are assumed to be a priori independent and normally distributed truncated to the intervals that define each one (\shortciteNPehl2014). For the GARCH(1,1) coefficients in (2), these prior distributions are the same as proposed in \citeNardia06, , and , . The tail parameter is assigned a truncated normal distribution as or when using the multivariate Student or GED respectively. Finally, a similar approach is adopted for the parameters and in equation (4), i.e. and . As for the skewness parameters, we use truncated normal distributions on positive values, i.e. , .

3 Package Implementation

The major function in package bayesDccGarch is bayesDccGarch forBayesian estimation of the DCC-GARCH(1,1) model. The function performs simulations from the posterior distribution via Metropolis-Hastings algorithm. The synopsis of the function is,

bayesDccGarch(mY, nSim = 10000, tail_ini = 8, omega_ini = rep(0.03,

ncol(mY)), alpha_ini = rep(0.03, ncol(mY)), beta_ini = rep(0.8,

ncol(mY)), a_ini = 0.03, b_ini = 0.8, gamma_ini = rep(1,

ncol(mY)), errorDist = 2, control = list())

where the arguments are,

-

•

mY: a matrix of the data ().

-

•

nSim: length of Markov chain. Default: 10000.

-

•

tail_ini: initial value of parameter if errorDist = 2 or initial value of parameter if errorDist = 3. If errorDist = 1 this arguments is not used.

-

•

omega_ini: a numeric vector () with the initial values of parameters. Default: rep(0.03, ncol(mY)).

-

•

alpha_ini: a numeric vector () with the initial values of parameters. Default: rep(0.03, ncol(mY)).

-

•

beta_ini: a numeric vector () with the initial values of parameters. Default: rep(0.8, ncol(mY)).

-

•

a_ini: a numeric value of the initial values of parameter . Default: 0.03.

-

•

b_ini: a numeric value of the initial values of parameter . Default: 0.8.

-

•

gamma_ini: a numeric vector () with the initial values of parameters. Default: rep(1.0, ncol(mY)).

-

•

errorDist: a probability distribution for errors. Use errorDist=1 for SSNorm, errorDist=2 for SST or errorDist=3 for SSGED. Default: 2.

-

•

control: list of control arguments (See Details).

-

•

outList: an output element of bayesDccGarch function.

The control argument can be used to specify the prior hyper-parameters and the simulation algorithm parameters. This is a list where the user can supply any of the following components,

-

•

$mu_tail the value of hyper-parameter if errorDist=2 or the hyper-parameter if errorDist=3. Default: 8

-

•

$mu_gamma a vector with the hyper-parameters . Default: rep(0,ncol(mY)

-

•

$mu_omega a vector with the hyper-parameters . Default: rep(0,ncol(mY)

-

•

$mu_alpha a vector with the hyper-parameters . Default: rep(0,ncol(mY)

-

•

$mu_beta a vector with the hyper-parameters . Default: rep(0,ncol(mY)

-

•

$mu_a the value of the hyper-parameter . Default: 0

-

•

$mu_b the value of the hyper-parameter . Default: 0

-

•

$sigma_tail the value of hyper-parameter if errorDist=2 or the hyper-parameter if errorDist=3. Default: 10

-

•

$sigma_gamma a vector with the hyper-parameters . Default: rep(1.25,ncol(mY)

-

•

$sigma_omega a vector with the hyper-parameters . Default: rep(10,ncol(mY)

-

•

$sigma_alpha a vector with the hyper-parameters . Default: rep(10,ncol(mY)

-

•

$sigma_beta a vector with the hyper-parameters . Default: rep(10,ncol(mY)

-

•

$sigma_a the value of the hyper-parameter . Default: 10

-

•

$sigma_b the value of the hyper-parameter . Default: 10

-

•

$simAlg the random walk Metropolis-Hasting algorithm update. Use “1” for updating all parameters as one block, use “2” for updating one parameter at a time and use “3” for an automatic choice.

-

•

$cholCov the Cholesky decomposition matrix of the covariance matrix for simulation by one-block Metropolis-Hasting. It must be passed if control$simAlg=1.

-

•

$sdSim a vector with the standard deviations for simulation by one-dimensional Metropolis-Hasting. It must be passed if control$simAlg=2.

-

•

$print a logical variable for if the function should report the number of iterations every 100 iterations or not. Default: TRUE

After completing the simulations, bayesDccGarch() returns an object of class bayesDccGarch which is a list containing the following components,

-

•

$control : a list with the used control argument.

-

•

$MC : an element of class mcmc from package coda with the Markov chain simulations of all parameters.

-

•

$elapsedTime : an object of class proc_time which is a numeric vector of length 5, containing the user, system, and total elapsed times of the process.

We note that the package coda is loaded automatically with a call to bayesDccGarch. This package contains functions which provide tools for MCMC output analysis and diagnostics (\shortciteNPplummer-etal06).

3.1 Run MCMC

The sampler that is currently implemented in bayesDccGarch is a random-walk Metropolis algorithm in which the parameters are sampled in one block from a multivariate normal proposal distribution centered about the current value. By default, the variance-covariance matrix is specified as the negative inverse Hessian matrix evaluated at the posterior mode which is obtained numerically. This is accomplished with a call to the R function optim().

If the optimizer fails to find the mode or the Hessian matrix at the mode is not positive definite a random-walk Metropolis is run on each individual parameter sampling from a univariate normal proposal centered about the current value with a variance that tunes the acceptance rates to be between 0.20 and 0.50. A sample variance-covariance matrix is then calculated from the output of this algorithm which is in turn multiplied by a scale factor and taken as the variance-covariance matrix of the multivariate normal proposal distribution in the one-block random-walk Metropolis. We next provide some illustrations on the use of the package.

3.2 Illustrations

In this section we illustrate the package usage with the DaxCacNik dataset included in the package. First load the bayesDccGarch package into R,

> library(bayesDccGarch)

and the dataset provided,

> data(DaxCacNik)

The DaxCacNik dataset contains daily observations of the log-returns of daily indices of stock markets in Frankfurt (DAX), Paris (CAC40) and Tokyo (NIKKEI), from 10 October 1991 until 30 December 1997 (a total of 1627 observations). These data are also freely available from the website http://robjhyndman.com/tsdldata/data/FVD1.dat.

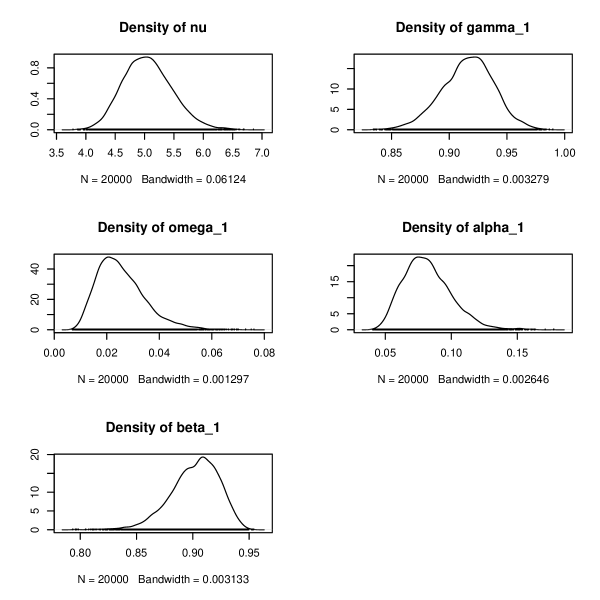

We begin by running a univariate analysis on the DAX index with a skew Student distribution for the errors.

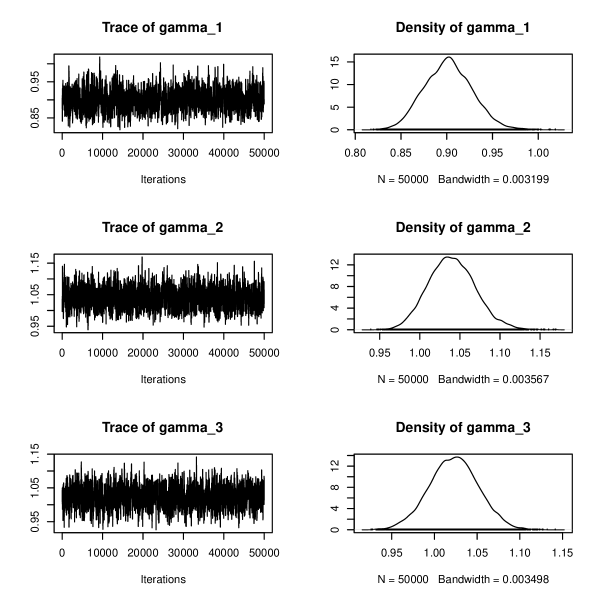

We now perform a multivariate analysis using the three daily indices, DAX, CAC and NIKEEI. Figure 4 shows the estimated posterior densities of the skewness parameters . They clearly indicate skewness in the marginal distributions for the DAX and CAC40 indices while symmetry is more likely for the NIKKEI index.

4 Conclusion

The current version of bayesDccGarch uses R and C and is available for the R system for statistical computing (\citeNPR06) from the Comprehensive R Archive Network at http://CRAN.R-project.org/.

Acknowledgements

The work of the first author was funded by CAPES - Brazil. The work of the second author was supported by FAPESP - Brazil, under grant number 2011/22317-0.

References

- [\citeauthoryearArdiaArdia2006] Ardia, D. (2006). Bayesian estimation of the GARCH(1,1) model with normal innovations. Student 5(3–4), 283–298.

- [\citeauthoryearBauwens and LaurentBauwens and Laurent2005] Bauwens, L. and S. Laurent (2005). A new class of multivariate skew densities, with application to generalized autoregressive conditional heteroscedasticity models. Journal of Business & Economic Statistics 23, 346–354.

- [\citeauthoryearBauwens, Laurent, and RomboutsBauwens et al.2006] Bauwens, L., S. Laurent, and J. V. K. Rombouts (2006). Multivariate GARCH models: a survey. Journal of Applied Econometrics 21(1), 79–109.

- [\citeauthoryearBollerslevBollerslev1986] Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31, 307–327.

- [\citeauthoryearBollerslevBollerslev1990] Bollerslev, T. (1990). Modeling the coherence in short-run nominal exchange rates: A multivariate generalized ARCH model. Review of Economics and Statistics 72, 498–505.

- [\citeauthoryearCappuccio, Lubian, and RaggiCappuccio et al.2004] Cappuccio, N., D. Lubian, and R. Raggi (2004). MCMC Bayesian estimation of a skew-GED stochastic volatility model. Studies in Nonlinear Dynamics & Econometrics 8(2).

- [\citeauthoryearChristodoulakis and SatchellChristodoulakis and Satchell2002] Christodoulakis, G. A. and S. E. Satchell (2002). Correlated ARCH: Modelling the time-varying correlation between financial asset returns. European Journal of Operations Research 139, 351–370.

- [\citeauthoryearEhlersEhlers2012] Ehlers, R. S. (2012). Computational tools for comparing asymmetric GARCH models via Bayes factors. Mathematics and Computers in Simulation 82, 858–867.

- [\citeauthoryearEngleEngle1982] Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50, 987–1007.

- [\citeauthoryearEngleEngle2002] Engle, R. F. (2002). Dynamic conditional correlation - a simple class of multivariate GARCH models. Journal of Business and Economic Statistics 20, 339–350.

- [\citeauthoryearFernandez and SteelFernandez and Steel1998] Fernandez, C. and M. Steel (1998). On Bayesian modelling of fat tails and skewness. Journal of the American Statistical Association 93, 359–371.

- [\citeauthoryearFioruci, Ehlers, and AndradeFioruci et al.2014] Fioruci, J. A., R. S. Ehlers, and M. G. Andrade (2014). Bayesian multivariate GARCH models with dynamic correlations and asymmetric error distributions. Journal of Applied Statistics 41(2), 320–331.

- [\citeauthoryearPipieńPipień2006] Pipień, M. (2006). Bayesian comparison of GARCH processes with skewness mechanism in conditional distributions. Acta Physica Polonica 37(11), 3105–3121.

- [\citeauthoryearPlummer, Best, Cowles, and VinesPlummer et al.2006] Plummer, M., N. Best, K. Cowles, and K. Vines (2006). CODA: Convergence diagnosis and output analysis for MCMC. R News 6(1), 7–11.

- [\citeauthoryearR Development Core TeamR Development Core Team2006] R Development Core Team (2006). R: A language and environment for statistical computing. Vienna, Austria: R Foundation for Statistical Computing. ISBN 3-900051-07-0.

- [\citeauthoryearSilvennoinen and TeräsvirtaSilvennoinen and Teräsvirta2009] Silvennoinen, A. and T. Teräsvirta (2009). Multivariate GARCH models. In T. Mikosch, J. Kreiss, D. R.A., & T. Andersen (Eds.), Handbook of Financial Time Series. Mikosch, T., Kreiss, J.P., Davis. R.A. and Andersen, T.G. (eds). Springer Berlin Heidelberg: Berlin, Heidelberg.

- [\citeauthoryearTsayTsay2010] Tsay, R. S. (2010). Analysis of Financial Time Series (Third ed.). John Wiley & Sons.

- [\citeauthoryearTse and TsuiTse and Tsui2002] Tse, Y. K. and A. K. C. Tsui (2002). A multivariate GARCH model with time-varying correlations. Journal of Business and Economic Statistics 20, 351–362.

- [\citeauthoryearVirbickaite, Ausin, and GaleanoVirbickaite et al.2014] Virbickaite, A., M. C. Ausin, and P. Galeano (2014). A Bayesian non-parametric approach to asymmetric dynamic conditional correlation model with application to portfolio selection. Technical report, Statistics and Econometrics Series 09, Universidad Carlos III de Madrid.